Late to the QT game, it’s even selling its equity holdings outright. Nothing on its balance sheet is sacred.

By Wolf Richter for WOLF STREET.

The Bank of Japan started quantitative tightening late in the game, and only reluctantly, after the yen had plunged against other currencies and couldn’t find a bottom. But since the BOJ started QT in late 2024, it has proceeded at a solid pace that accelerated as it went.

The plunge of the yen – 53% against the US dollar since the beginning of 2012 – finally triggered the wrong kind of inflation, driven by price spikes of imported energy products, and sharp price increases of imported consumer goods, and of all kinds of components and materials for manufacturers. But the BOJ was aiming for the “virtuous” kind of inflation, associated with strong growth in domestic demand and supported by rising salaries.

The plunge of the yen was getting in the way and was going too far. So the BOJ has been trying to put a floor under the collapse of the yen, and instead of jacking up its short-term policy rates, it started QT in late 2024, and then accelerated the pace, including now selling its equity ETFs outright. Nothing on its balance sheet is now sacred.

That pace of QT allowed yields of long-term Japanese Government Bonds (JGBs) to soar further: the 30-year JGB yield hit 4.0%, up from near 0% in 2020; and the 10-year JGB yield hit 2.7%, up from negative in 2021. At the same time, it only raised its policy rates to a ridiculously timid 1.0%.

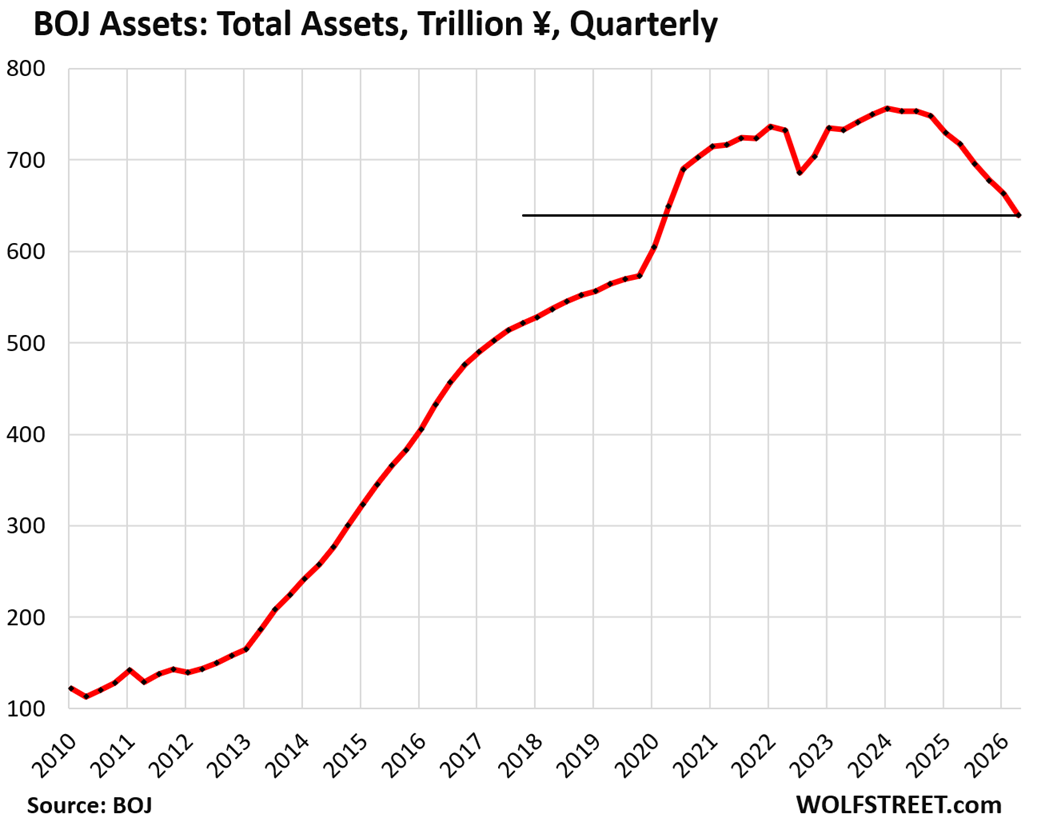

So, total assets on the BOJ’s balance sheet fell by ¥23.5 trillion (-$146 billion) in the quarter ended June 30, the largest quarter-to-quarter decline so far in this QT cycle.

Since the peak of its holdings in Q1 2024, the BOJ has shed ¥116.9 trillion (-$726 billion), or 15.6% of its total assets. This is a substantial amount of QT in a relatively short time.

Its holdings are now down to ¥639.6 trillion ($3.97 trillion), the lowest level since Q1 2020, according to the BOJ’s balance sheet data on Thursday.

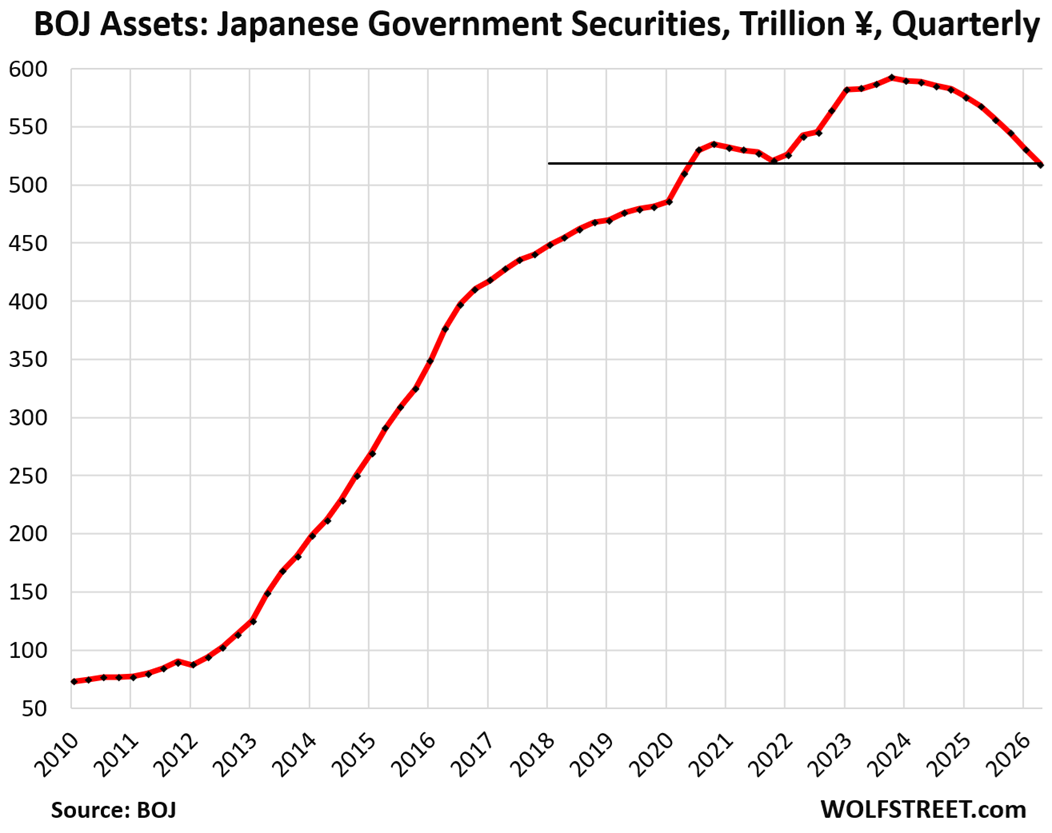

Its holdings of JGBs declined by ¥12.5 trillion in Q2 (-$78 billion), to ¥518.3 trillion ($3.22 trillion), where they’d first been in Q3 2020.

The BOJ no longer holds any short-term Treasury bills. It shed the last one of them in Q4 2025.

Since the peak in 2023, holdings of Japanese government securities have dropped by ¥73.9 trillion (-$459 billion), or by 12.5%.

They now account for 81% of the BOJ’s total assets.

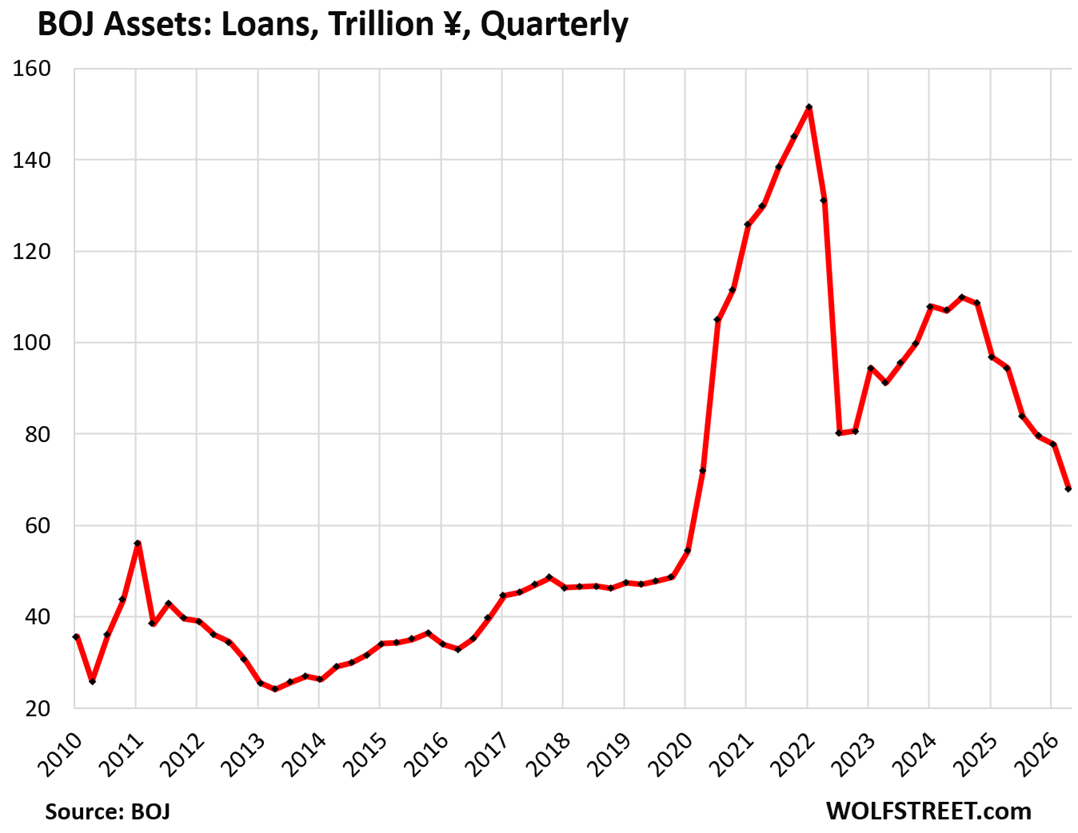

Loans declined by ¥9.7 trillion (-$60 billion) in the quarter, to ¥68.0 trillion ($423 billion), the lowest since Q1 2020.

Since the peak in Q1 2022, the outstanding loan balance has fallen by ¥83.5 trillion, or by 55%.

These loans now account for 10.6% of the BOJ’s total assets. The BOJ provided loans to banks and other entities under several programs, including the pandemic-era loans that had caused the total amount of loans outstanding to more than triple in two years:

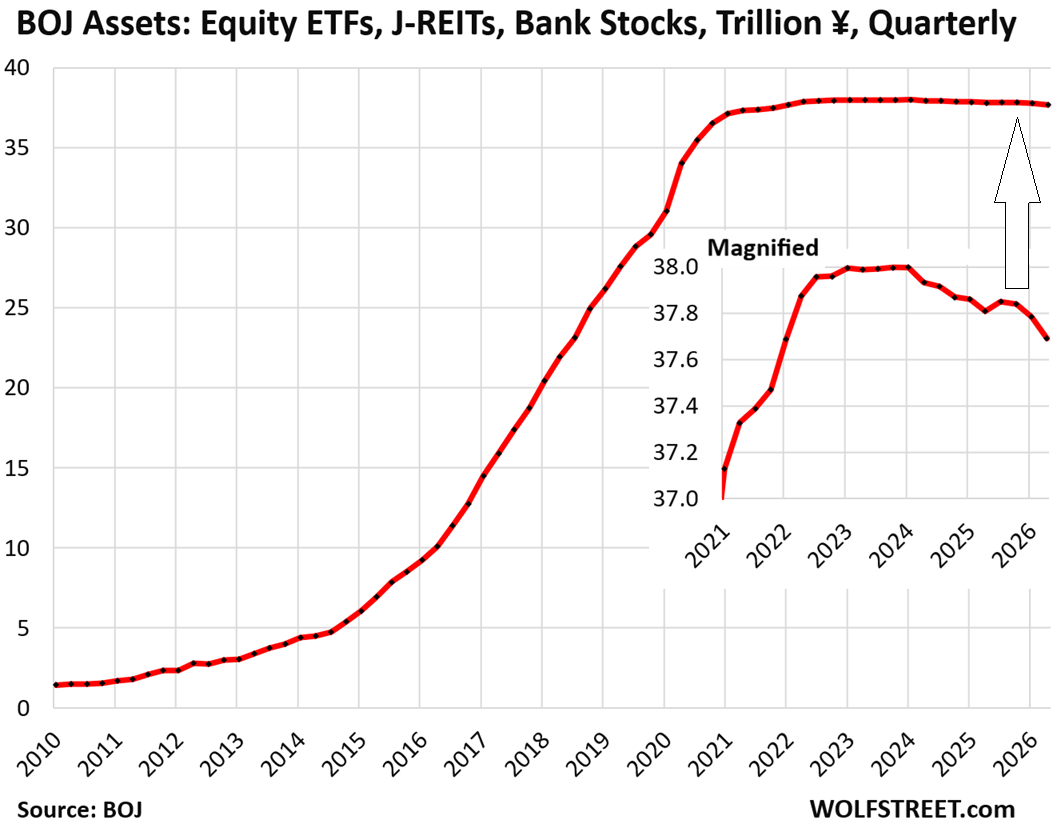

The BOJ is selling outright its equity ETFs and J-REITS, following its announcement last September. The initial pace is minuscule at ¥330 billion ($2.1 billion) in ETFs per year and ¥5 billion ($31 million) in J-REITs per year. It started selling them in Q1.

But that pace of sales is faster than it seems: The BOJ has carried its ETFs and J-REITs at acquisition cost ever since it started buying them in 2011, and has not marked them up to market, while the Nikkei 225 has soared by 500%.

And the pace of sales is also at acquisition cost. But measured in current market prices, these sales are by multiples higher.

The BOJ sold off its last bank stocks in the September quarter. It had purchased them in the early 2000s and again in 2009-2010, and started selling them in 2016.

In Q2, the BOJ sold ¥120 billion (-$74 million) at acquisition cost of equity ETFs and J-REITs – by multiples more at current market prices. Since the peak, it sold ¥390 billion ($2.4 billion) at acquisition cost, bringing its balance down by 1.0% at acquisition cost, to ¥37.6 trillion ($234 billion).

The decline of 1.0% from the peak has been so slow that it looks like a flat line on the 16-year chart. Hence the magnified insert.

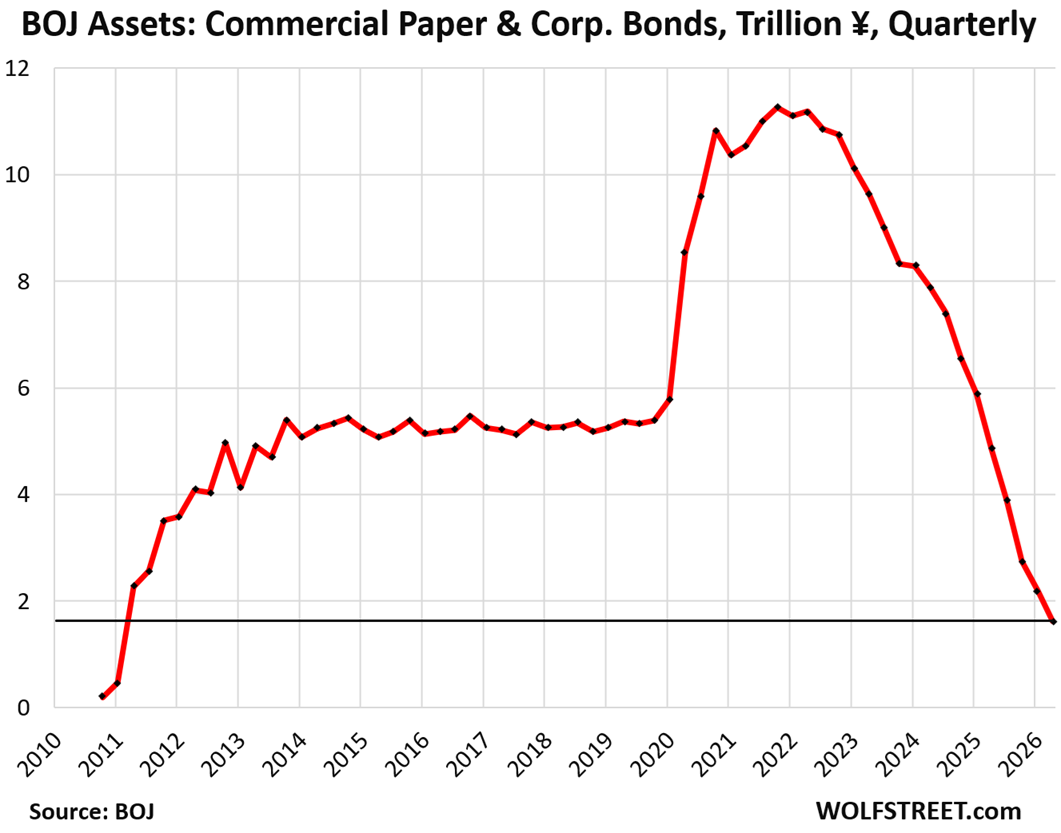

Corporate bonds fell by ¥563 billion ($3.5 billion) in the quarter to just ¥1.63 trillion ($10 billion). The BOJ already shed its last commercial paper in Q1, and they’re down to zero.

They’re now essentially gone and were always just a tiny part of the BOJ’s QE operations, at their peak accounting for only 2.2% of the BOJ’s total assets.

QT instead of bigger rate hikes. With this substantial quantitative tightening, instead of with steeper rate hikes, the BOJ is attempting to put a floor under the yen, which has been plunging for years, and is down by 56% against the US dollar since 2012.

And it is also trying to deal with the wrong kind of inflation that is percolating through the economy via import prices.

But it has only minimally hiked its policy rates, in tiny steps spread far apart, to only 1.0%. Instead of jacking up its policy rates, the BOJ has been assertive with its QT, which allowed long-term yields to soar. A late start, but catching up. With short-term yields near 1% and 30-year yields near 4%, it makes for a steep yield curve.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf – what are your thoughts on the US using this QT playbook, assuming inflation continues to heat up? The Fed similarly seems unlikely to raise rates in time. Thanks!

Warsh made comments to that effect before his nomination. Smaller balance sheet would allow for overnight policy rates to be lower… that’s kind of what he said back then. Now there’s a lot more inflation, so that changes the rate outlook. Plus he’s got 11 voting FOMC members to deal with, some of whom might support his views, and others might not.

The ECB has also been following that track, lower rates and smaller balance sheet, and QT continues to move forward at the accelerated pace. But it hiked by 25 basis points at its last meeting.

I think more aggressive “balance sheet reduction” is a near certainty in the US, starting this fall.

I also think inflation will fall immediately with the QT. It did so last time.

That will give the FOMC license to only hike rates only 25 or maybe 50bp, instead of exceeding the peak of inflation (lesson learned from the 1970s).

The Federal Funds Rate futures market seems to now expect just one 25bp hike in the next 12 months. I can get behind that.

Abenomics was huge failure

Japan is always too late to act like last war

From tokyo japan

The BOJ allowed transaction deposits to have unlimited deposit insurance. That froze a lot of savings held in their banks.

We can’t do this evidently.

🤔

So the JCB has sold its winners and is holding its losers (long term Japanese government bonds at extremely low interest rates). The long term government holdings have a huge unrecognized loss if sold today. Possibly the JCB is smart enough to sell some long term Japanese government bonds to use the losses against any gains on its other QT sales. In any case, the JCB is holding the bag on LT Japanese government bonds. They will roll off when they mature over the next few decades.

I suspect that a JCB policy of buying no new government securities and very slowly rolling off the old low interest rate bonds is likely to pressure the long term Japanese debt market as the Japanese government tries to peddle more long term debt without the JCB as the willing buyer. I suspect also that the carry trade is likely to wind down as the Yen continues to decline against the USD, while Japanese interest rates slowly rise. JMO

The only thing the BOJ sold were its stock-market-traded equity ETFs and J-REITs (very profitable).

The JGBs come off the balance sheet when they mature, which is when the BOJ gets paid face value for them. There are no losses at all involved. These JGBs mature at a faster rate than the pace at which the BOJ allows them to roll off. So it buys some JGBs to fill in the holes left behind by the excess.

What is the plan going forward? Is the plan to continue the decrease of balance sheet in same pace?

I think Matt the balance sheet is now resuming an increase month to month as a result of an end to QT and the rate of borrowing exceeding MBS rolloff.

When Wolf gets back from walkabout Im sure we’ll get an update.

Happy 250th America!

God bless us all.

You’re making up stuff.

1. Before 2008 before QE, the Fed’s balance sheet always increased roughly in line with economic growth, as it would have to given the Fed’s liabilities that grow automatically with the economy. And that is NOT QE, you goofball. I have posted this chart many times:

1. The increase this time was temporary to prepare for tax day (Apr 15), was tapered in May and June, and is ending now and will be over by mid-July. I discussed this many times. But reality is not as sexy as this constant braindead internet BS about the Fed having re-started QE.

Excellent report, thanks Wolf, Donald

Lower (market) rates and a smaller balance sheet don’t go together. QT signals that the CB’s don’t want the risk to be on their books any longer, but want the market to take it. With higher risks the market demands higher (market) rates, not lower. The CB’s can offer a lower base-rate while in the free market (commercial) rates are higher. Which again, signals that the CB’s see risk in collateral that they don’t want on their books.

When did the FED start shedding MBS’s? And what direction is that market going in now? They see things long before we get aware of them. And they only come out to tell us when they are save themselves. But the signals are out there.

And inflation. They don’t really care. How long have we been above the ancient 2% ceiling, morphed into being a bottom target now? It’s the sentiment around it that they care about. Sentiment can be managed to some extent. “Putin”, “Iran”, “The weather” are popular explanations. And when that fails it could be “extra terrestrial” of any kind.

. This has zero to do with “risk.”

2. “Lower (market) rates and a smaller balance sheet don’t go together.”

You’re talking about longer-term rates — and agreed. Smaller balance sheets mean higher long-term rates. Central banks impact long-term rates via their balance sheets, such as QE (bring down long-term rates) or QT (allow long-term rates to rise).

But the central banks don’t set longer-term rates with their policy rates. Their policy rates impact overnight rates. So a central bank can set 1% for its policy rates, and overnight rates, such as repo rates, will be close to 1%. But the 30-year yield can be 4%. That’s what the BOJ has been doing.

3. This comment is BS: “When did the FED start shedding MBS’s? And what direction is that market going in now? They see things long before we get aware of them. And they only come out to tell us when they are save themselves. But the signals are out there.”

It’s BS because those MBS that the Fed holds are guaranteed by the Federal Government and have the same credit risk (near zero) as Treasury securities. There is no risk for the Fed.

The Fed started shedding MBS in July 2022 and has continued to shed them and will continue to shed them for the reasons I explained here many times (they’re a hassle to manage because of their constant and uneven passthrough principal payments, they came off the balance sheet at an unpredictable rate depending on mortgage payoffs, and they indicate a Fed preference for type of private-sector debt). The Fed has said many times since 2022 that it wants a balance sheet primarily composed of Treasury securities and repos and shed all of the MBS for those reasons.

Maybe “late” to QT

But they were the first (circa 2000) to go to ZIRP

I remember Paul Krugman was their “advisor” that steered them to this policy and the massive buying of their own debt.

The demand for money is a paradox (see: Cambridge economist Alfred Marshall). All motives which induce larger holding’s, will tend to increase the demand for money, & reduce its velocity.

The Japanese save more and keep more of their savings in their banks.

“Japanese households have 52% of their money in currency & deposits, vs 35% for people in the Eurozone and 14% for the US.”

“The paradox of thrift (or paradox of saving) is a paradox of economics. The paradox states that an increase in autonomous saving leads to a decrease in aggregate demand and thus a decrease in gross output which will in turn lower total saving.”

So … Japan is the first country walking across a frozen lake and everyone else (incl. our Federal Reserve) is watching to see whether the ice holds?

They have been walking on that ice for 36 years.

The weak yen and their lower interest rates help their “ cary trade”

And everybody likes that treasury interest.

“ Reuters recently noted that Japan’s roughly $1.2 trillion in Treasuries generates more than $40 billion annually in income. “

The people of the U S gift to the world.

Maybe they bought Treasuries because the yen was collapsing, and buying USD assets would protect their wealth from the collapse of the yen?

Or maybe the Japan QE ended up in the US markets and Treasuries.

Thank you heavily indebted US citizens.

Everybody loves free money.

@Wolf

Maybe they knew the yen was going to collapse some more?

If this was driven by Japanese Housewives, then I would say that they were just looking at the coupon yield. If it was driven by Major Banks, then anything is possible.

So what do we buy when the USD starts collapsing? :)

Last year the lowest debt/GDP currencies went on a tear against the most indebted currencies, but so far this year the high-debt currencies are making a minor comeback.

I’m looking forward to the Fed also announcing a real QT program. Maybe whatever MBS naturally roll off + $30B a month of Treasuries? Somewhere in the neighborhood of $500B a year?

Happy Independence Day everyone.

For years and years we’ve heard stories about how either raising rates more substantially or selling assets into the market would eventually result in the yen crashing. Has this changed? Are they ‘saved’ now? JGB yields *must* be soaring.

JGB yields have soared from zero, but apparently not enough yet to protect the yen. The yen has crashed but apparently not enough yet.