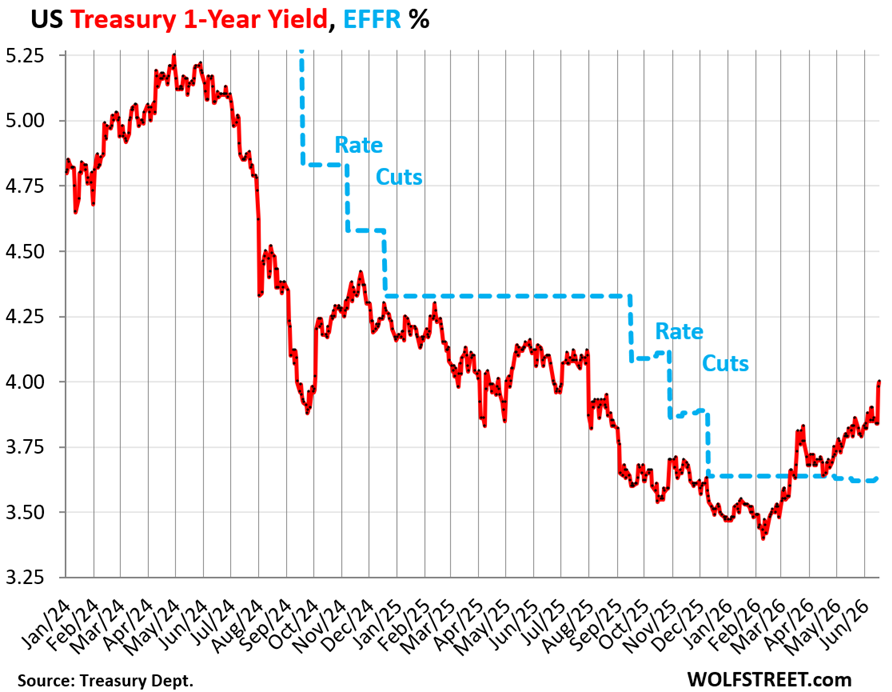

The 1-year Treasury yield spiked by 16 basis points, to 4.0%, highest since July, three rate cuts ago, as the bond market now expects multiple rate hikes.

By Wolf Richter for WOLF STREET.

The US government sold $518 billion of Treasury securities during the week: $477 billion of Treasury bills, spread over six auctions, with maturities from 4 weeks to 26 weeks, most or all of them to replace maturing T-bills; and $41 billion of Treasury notes and bonds spread over two auctions (5-year Treasury Inflation Protected Securities and 20-year Treasury bonds).

This was also the week of the first FOMC meeting under Fed Chair Kevin Warsh, when the extent of the “regime change” at the Fed became apparent in the FOMC statement, in the FOMC Implementation Notes – which opened the path for the Fed to end its Reserve Management Purchases of T-bills – and in the press conference, where he laid out the focus of his five “taskforces.” In response, 6-month to 2-year Treasury yields spiked.

The 1-year Treasury yield spiked by 16 basis points on Wednesday and Thursday to 4.0%, the highest since July last year, three rate cuts ago. Since early February, it has surged by 60 basis points and is now 37 basis points above the Effective Federal Funds Rate (EFFR, blue line) which the Fed targets with its policy rates.

Treasury yields of 1 year and shorter are boxed in by the Fed’s policy rates and by market expectations of those policy rates within their remaining maturity window. By pushing the 1-year yield up like this, the bond market has begun to price in a second rate hike within the window of the 1-year Treasury yield.

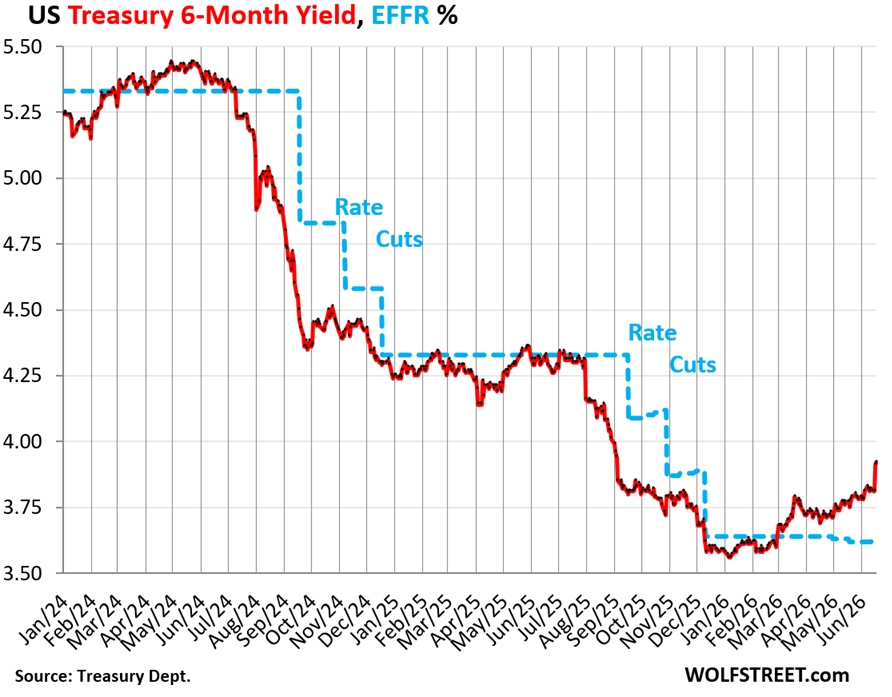

The 6-month Treasury yield spiked by 10 basis points on Wednesday and Thursday to 3.90%, the highest since September 2, three rate cuts ago.

It is 27 basis points above the EFFR, a sign the bond market has more than fully priced in one rate hike by yearend.

But the auction of the 6-month (26-week) Treasury bill took place on Monday, two days before the drama of the FOMC meeting when Warsh detailed his regime change, and therefore two days before the spike of the yield in the secondary market, and so the auction yield was actually a hair lower than at the auction a week earlier.

| Type | Auction date | Billion $ | High Rate | Investment Rate |

| Bills 4-week | Jun-18 | 74 | 3.58% | 3.64% |

| Bills 6-week | Jun-16 | 70 | 3.60% | 3.67% |

| Bills 8-week | Jun-18 | 80 | 3.64% | 3.71% |

| Bills 13-week | Jun-15 | 96 | 3.64% | 3.73% |

| Bills 17-week | Jun-17 | 73 | 3.67% | 3.77% |

| Bills 26-week | Jun-15 | 83 | 3.68% | 3.80% |

| Bills | 478 |

“High rate” and “Investment Rate” are the two different calculations of the yield that the Treasury Department provides with its T-bill auction results. T-bills are sold at a discount, and at maturity, the holder gets paid face value; the difference is the interest. There are no coupon interest payments. The “high rate” reflects the yield calculation of that process.

To make this discount yield comparable to the yields of coupon securities (2-year to 30-year), the Treasury Department re-calculates it as “investment rate,” which is higher than the “high rate.” And around the time of the auction, the “investment rate” is close to the “constant maturity yield” published by index providers to reflect trades in the secondary market for that type of remaining maturity.

But these T-bill yields are still negative in real terms, despite the spike – all of them are still below the rate of CPI inflation which has accelerated to 4.25%. But as rate hikes are being priced into these yields, they’re chasing after inflation from below.

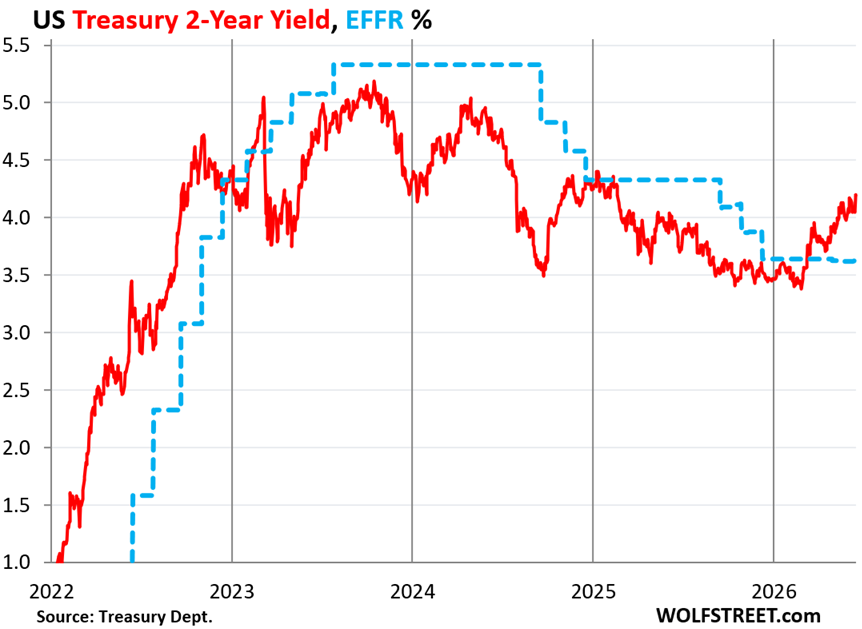

The yield of the 2-year Treasury notes spiked by 14 basis points on Wednesday and Thursday to 4.19%, the highest since February last year.

This longer-term view of the 2-year yield shows just how significant the directional change of short-term interest rates has been, going from two years of rate-cut mode into full-blown rate-hike mode, and the Fed has made no attempt to fight the bond market on it, but has been going along with it.

The US government also sold $41 billion of Treasury notes and bonds this week, spread over two auctions: 5-Year TIPS and 20-year Treasury bonds.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| TIPS 5-year | Jun-18 | 28 | *1.955% |

| Bonds 20-year | Jun-16 | 13 | 4.93% |

| Notes & bonds | 41 |

*TIPS yield is paid on top of the inflation protection that TIPS holders receive. This inflation protection is based on CPI and is added to the principal, and so the principal of the TIPS grows over time with CPI. The coupon interest rate is fixed for the term of the TIPS, and is applied to the entire principal, including the inflation protection. As the principal grows over time with CPI, the coupon interest payments increase, though the interest rate of the coupon remains fixed.

The 5-year TIPS sale was marked by a big difference between the coupon interest rate of 1.25% and the yield established at the auction of 1.995%, which caused the TIPS to be sold at a substantial discount: The unadjusted price was $96.79 per $100 of face value.

This difference between coupon interest rate and yield occurred because this was a “reopening” auction of a TIPS issue that was originally sold in April. Both auctions sold the same issue of TIPS with the same CUSIP number (91282CQP9), the same maturity date (April 15, 2031), and the same coupon interest (1.25%). At the time, the 5-year TIPS went through the auction at a yield of 1.367%. But yields have shot up since then. And the same issue of TIPS went through the auction this week at a yield of 1.955%. To get there, the price was established at the auction at a substantial haircut, and the investors who’d bought two months earlier got a worse deal. But those are the adventures in bondland.

Reopening auctions are routine, including for 10-year notes; each 10-year note issue has one original auction and two reopening auctions. So there are only four 10-year note issues per year (four CUSIP numbers), spread over 12 auctions. There are only two 5-year TIPS issues per year (two CUSIP numbers) spread over four auctions. This system increases the size of each issue of securities and thereby the liquidity in the secondary market of each issue.

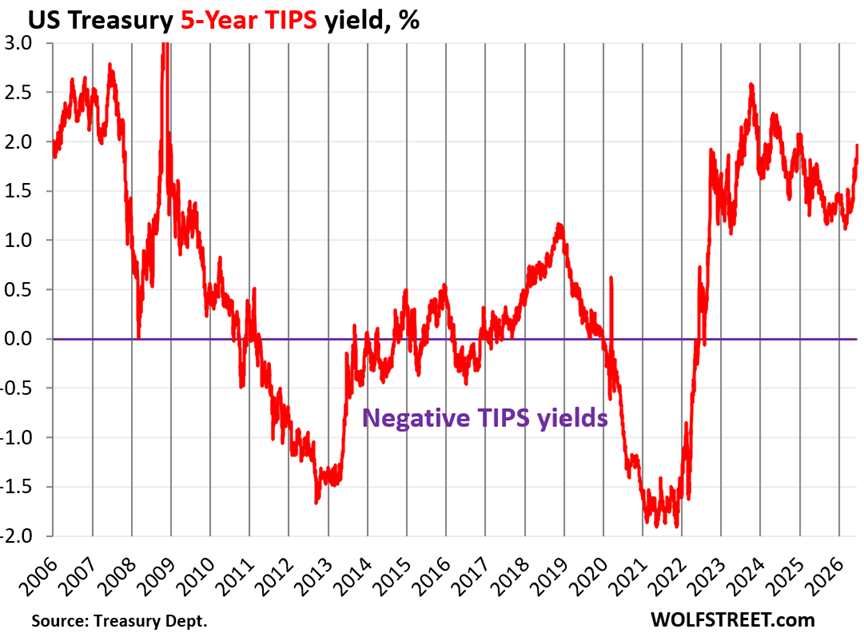

The 5-year TIPS yield had gone massively negative during the time of the interest-rate repression by the Fed through its QE programs. For example, the 5-year TIPS issue that matured on April 15, 2026, was sold at auction in April 2021 with a coupon interest of 0.125%, but the price was bid up during the auction to $109.11 per $100 of face value, which caused the yield to be negative -1.631%. These TIPS holders paid $109.11 for each $100 in face value but then received the inflation protection during those five years, plus the $100 in face value, plus the coupon interest payments of 0.125% on the face value plus inflation protection.

QE had driven the 5-year TIPS yield deeply into the negative, starting in August 2010. With the beginning of QT in late 2017, the TIPS yield emerged from the negative in a significant way. Then in March 2020, under mega-QE, it re-plunged into the negative. In June 2022, after QE had ended and on the cusp of QT, it re-emerged from the negative.

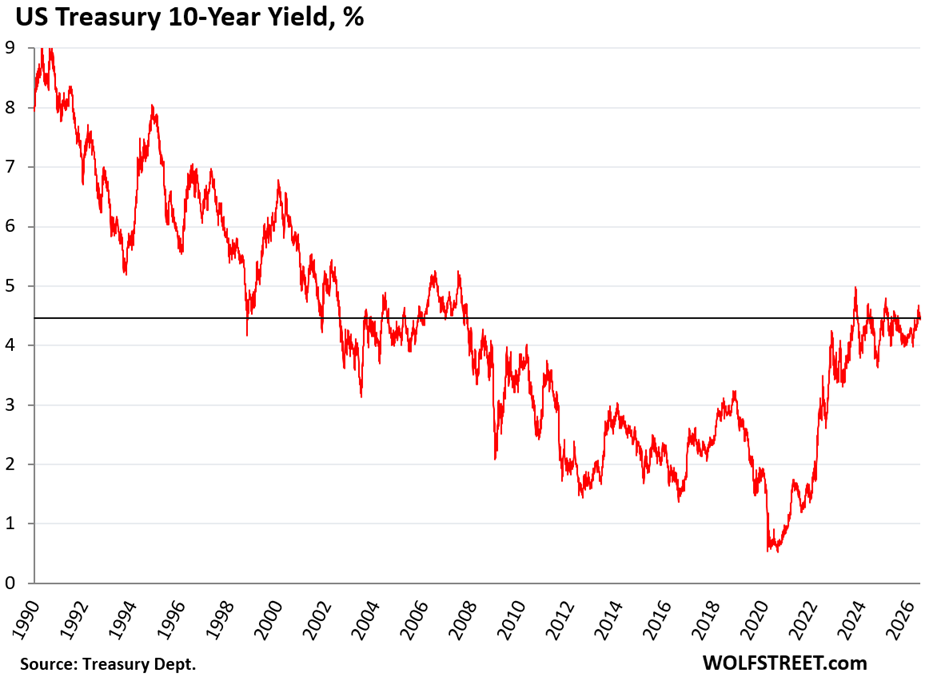

The 10-year Treasury yield declined 7 basis points during the week to 4.46% as falling oil prices have eased off pressure on fears of inflation blowing out. All the hoopla this week about a deal with Iran played into that. That longer end of the bond market dances to fears and hopes about the imagined path of inflation and the oncoming supply of Treasuries to fund the ballooning deficits that the market has to absorb and that may require higher yields to attract ever more investors.

Compared to the years before QE, before 2009, the 10-year yield at this level is still relatively low. And compared to 4.25% CPI inflation, the 10-year yield at 4.46% is very low. Clearly at this point the bond market still thinks inflation will go back somewhere near 2%.

If the Fed raises its inflation target from 2%, the bond market would then have to finally give up its hopes for a return to 2% inflation, and yields would likely adjust to it. Raising the official inflation target to 3% could push the 10-year yield to 5.5%.

Higher bond yields in the market mean lower bond prices for existing holders, and vice-versa.

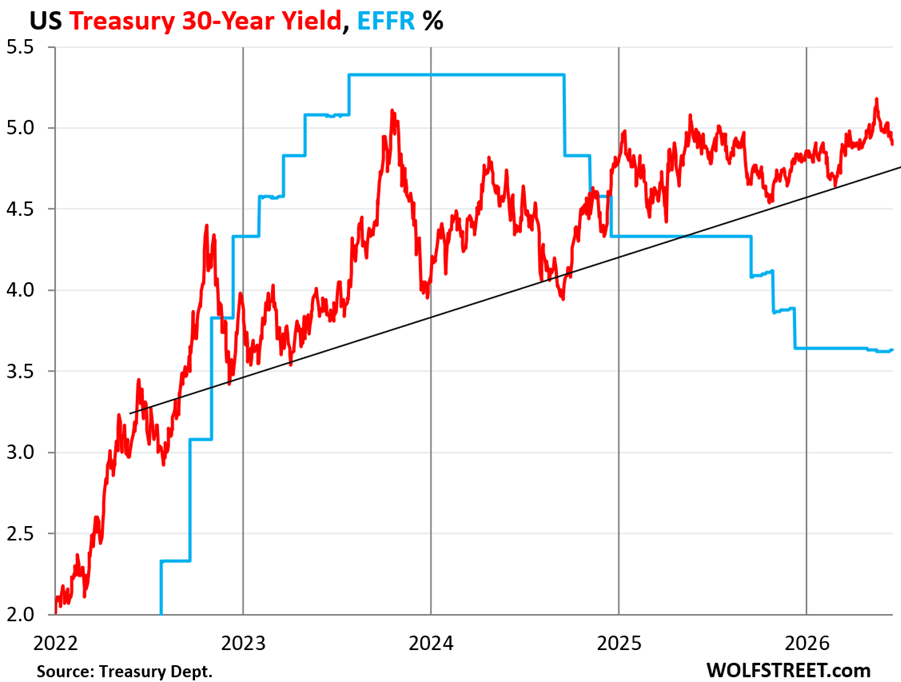

The 30-year Treasury yield declined by 7 basis points during the week to 4.91% on Thursday, on all the hoopla about the Iran deal.

The long-term Treasury yields completely blew off the Fed’s rate cuts. But the end of QE in early 2022 and the start of QT in the second half of 2022 allowed those long-term yields to rise. My imaginary trend line connecting some of the lows of the past three years still holds:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Great analysis on the Treasury market! It’s way too early to go long in this market.

The time to go long long bonds is when one is comfortably content to hold a 30-year Treasury to maturity.

The long bond continues to be the worst investment decision. An irony, where the risk free security becomes the most risky security.

The hallmark of monetarism where price is not a function of value but price is a function of the quantity of Federal Reserve notes issued by the USA.

re: “too early”

Why do you think gold is falling?

Too early is better than too late.

How will you know which is which?

Hehe

“The 10-year Treasury yield declined 7 basis points during the week to 4.46% as falling oil prices have eased off pressure on fears of inflation blowing out. ”

The markets are synthetic. I think the obese Fed balance sheet is at the root of a substantial number of financial capers that ……

I finally went longer on Bills and bought some 6 month. Nice yield.

Way to go out on a limb. 😀 I bought a week too early and will have to wait till next batch matures.

You risk taker you!

😉 🏴☠️

Watching Hormuz insanity leads me to believe 6 months is a reach.

-ng-

1 dissent out of 12 is hardly enough to call a “regime change”. He doesn’t have the votes to move rates. He said it himself

RTGDFA

Off topic buy my hysa raised interest rate from 3.25 to 3.5%.

Morgan Stanley Private Bank? That’s mine. Whoopie, their generosity is still negative, so we are forced to gamble at the table to hopefully gain more.

With the Middle East conflict behind us it is only days or weeks before everything is back to normal.

That made me chuckle! Good one.

Touché!

I can’t help but to agree with the grim humor of your feigned exuberance !

Long end lower with 0-2 years below inflation rate difficult time for bond holders especially if inflation drops and yields drop significantly. No signs of lower inflation with economy humming from massive aI and the need for long term electric demand

Wolf, how much short term Treasuries is the Fed buying on net? To keep their policy rates, don’t they have to do “short term QE”?

The Fed is currently replacing all MBS that come off the balance sheet with T-bills (ca. $15 billion a month). So that’s a reverse “operation twist”. QE is buying long-term securities. Rolling off the MBS and replacing them with T-bills is the opposite of what Bernanke did. Separately, the Fed currently adds $10 billion a month in T-bills. And the FOMC meeting indicated that that’s over starting July 15.

July 15th! I can’t wait to see what happens after that.

The planned purchases are announced for periods from mid-month to mid-month. The last announcement ($10 billion in purchases in one month) was for mid-June through mid-July. So they will conclude the announced purchases by mid-July. That kind of sets the date for the change. We’ll see if they make an announcement about no purchases, or whether they just don’t purchase without announcement.

Also, the next meeting is end of July, and they may provide more details on the balance sheet.

Wolf – what’s the exact mechanism by which the FED maintains the short term rates that they set ? If lots of selling appeared and drove the yield on the 3 month bill to say 4%, would the FED simply go into the market and buy those bills until the rate moved back down to their target range?

The Fed relies on banks. They get paid 3.65% for the cash on deposit at the Fed (reserves). When short-term T-bills yield substantially more for long enough, it makes sense for banks to shift some cash from their reserves at the Fed to T-bills to make some extra profit. Same with repo rates. They can also borrow from the Fed at 3.75% at the Discount Window or at the SRF and engage in the repo market when yields rise too far. Repo market yields and short-term Treasury yields are linked through arbitrage. Generally that keeps it within range.

If short-term yields rise because the market expects rate hikes, then that’s a signal and information that the Fed welcomes; for example, if investors are pretty sure that the Fed will hike in two months, the 3-month yield should be near 4%. That’s a market signal that the market got the message from the Fed about a rate hike. The Fed doesn’t need to do anything. The Fed doesn’t want surprises. It will prepare markets long in advance for rate hikes. And you can see that in short-term yields.

Are people buying less securities overall? From your last article on the subject, you stated that there were 504 billion securities sold.

Every single dollar of securities that the government sells, someone buys. Yield is the mechanism that makes sure that there is always demand. If there is no demand at 4.5%, the yield rises automatically until there’s demand for the sale, and it may be at 4.6% or at 5% or 6% or whatever. Yield is the key. At what yield does this demand take place?

Why are those buyers not holding out for HIGHER yields, especially with the inflation spike? Why are they satisfied with 4%?

Why do some investors think it’s time to dump shares of SpaceX while others think it’s the best time to buy those shares? Disagreement makes a trade.

Perhaps there’s a signal there that the obvious expectation — raging inflation — could be dead-wrong.

I suggest that higher yields. while the obvious path. The obese Fed balance sheet retards the competitive market hypothesis which Adam Smith laid out succinctly in his notes:

never elect a business man to the chief executive office. They would sell their own mother …..

All 5 tasks force and no forward guidance sounds great. Warsh still only has one vote. Those task force can help Warsh to build support for his policy changes. Few governors wanted to reduce balance sheet or tighten monetary policy. So may be Warsh can start with them.

Stopping RMP is at welcome change ( hoping that’s what happens). Amount was small but it shows intent backed with actions.

After getting burnt by FED in last 5 years on 2% promise, I will not take any FED chair on his/her face value. They all talk about it. I heard Powell also talked about 2% but didn’t back it with hard actions.

Warsh should start with balance sheet reduction quickly. Rate hike is more political and soon with Mid-terms that decision will be more difficult. Start reducing the balance sheet and financial conditions will tighten immediately. FED is not at all restrictive at this time; specially with T-bills purchases from MBS rollovers and rolling over existing securities into same type/term.

Start with simple and small step like “Stop MBS investment into T-Bills.” That’s very slow move. 15-20 B a month. If you can not manage that much amount, then FED will never have courage to reduce balance sheet.

Some men just want to watch the world burn.

The appointment of task forces assigned to advise the FOMC what to do six months from now is not a sign that immediate action is about to be taken. It’s a sign that inflation has at least another six months to run – during which time policy has switched to stimulative because the FFR is lower than the rate of inflation.

It’s all about NOT taking action before the midterm elections, no matter how fast inflation rises in that time. The task forces offer cover for a repeat of 2021: We’ll watch inflation rise and rise and finally get the first FOMC reaction in March of next year.

So, if you could go back to June/July 2021, how would you invest?

I agree and share your skepticism. What FED can do , should do and will do are different things. After 5 years of missing inflation target, cant say I trust any FED chair what they say unless backed up with an action.

“So, if you could go back to June/July 2021, how would you invest?”

You tell me. SP500 has more than doubled and many tech stocks stocks have gone multi-folds. What you would do?

“Money for Nothing: Inside the Federal Reserve”

Facts are facts

“SP500 has more than doubled and many tech stocks stocks have gone multi-folds. What you would do?”

Waited until 2022 when stocks were down 20%?

Actually the better bet would have been to short long duration bond ETFs like TLT, EDV, and ZROZ. Could have doubled your money a couple of times between late 2021 and mid 2022. Then maybe consider stocks.

Today that bond shorting opportunity isn’t there to the same extent. Convexity is different starting at 4.8% instead of <1%.

The Hawkish Front: The Fed is maintaining a strict public stance, holding interest rates steady at 3.5% to 3.75% under a rigid “higher-for-longer” policy.

The Behind-the-Scenes Reality: However, a sharp disconnect emerges when looking at actual operations. The Fed’s balance sheet has quietly expanded at a 10% annualized rate, climbing back above $6.7 trillion.

Words vs. Actions: While officials publicly preach restraint and voice ongoing concerns over inflation, their backroom reserve management operations are actively injecting liquidity into the financial system.

The Bottom Line: It is time for the market to stop listening to the Fed’s “restrictive rhetoric” and start paying attention to its “expansive actions.”

“…has quietly expanded at a 10% annualized rate” – that’s a sordid manipulative misstatement. The Fed increased its balance sheet at that rate ($40 billion a month) for short burst from mid-December through Tax Day (April 15). And that pace has since then been reduced by 75% to just $10 billion a month through July 15 and will likely be cut to zero after July 15.

And it wasn’t “quietly,” but loudly announced multiple times, and there are a bunch of articles here starting last November about it. And every month, the Fed preannounced the purchases for the next month. Periods go from mid-month to mid-month. That “quietly” was another load of gratuitous BS.

Here is the Fed’s balance sheet including the “Reserve Management Purchases” (RMPs).

So, how does The Fed “Fight Inflation” while expanding the balance sheet?

Interesting times, although it definitely has that 1930s feel…

Interest rate will continue to climb as RISK continues to be repriced globally.

Hedge accordingly.

Reserve balances (the correct interpretation)

From the grounded H.4.1 data:

Reserve balances July 2025: ≈ $2.93 trillion

(from the July 2025 H.4.1 tables)

Reserve balances June 2026: ≈ $3.56 trillion

(from the June 17, 2026 H.4.1 release)

Increase in reserve balances

≈ $625 billion increase in total reserves (reserve balances) since July 2025

Treasury securities are being monetized.