Several subprime-specialized dealer-lender chains collapsed, and shares of America’s Auto Mart imploded. Subprime lending is not for the squeamish. But it’s only a small part of auto finance.

By Wolf Richter for WOLF STREET.

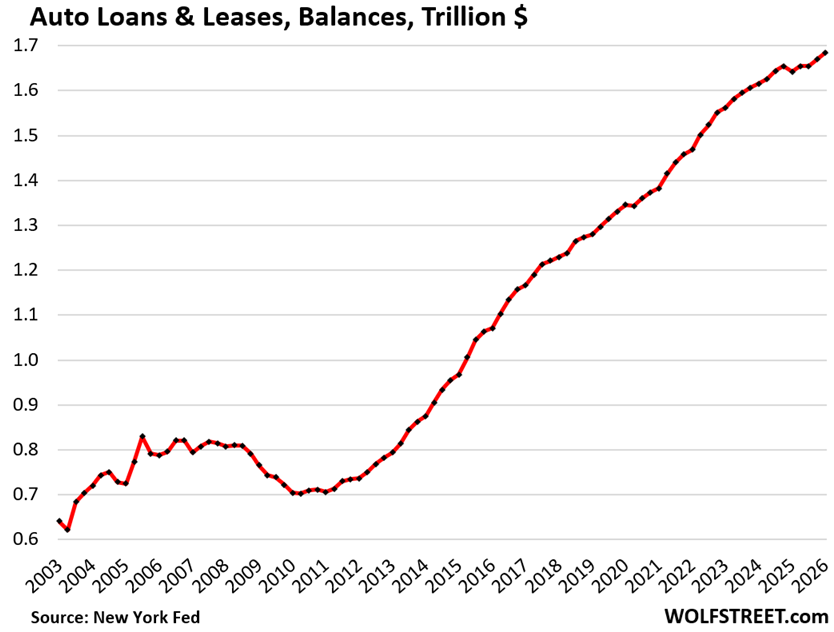

Total balances of auto loans and leases outstanding for new and used vehicles rose by $15 billion in Q1 from Q4 and by $43 billion (+2.6%) year-over-year, to $1.68 trillion, according to the New York Fed’s report on consumer credit, based on Equifax data.

But in the five years from 2020-2024, auto loan balances had surged by 23%, despite much lower vehicle sales, driven by the price explosion of new and used vehicles in 2021 and 2022.

How bad is it?

First, we look at the debt-to-income ratio across all households, then we’ll look at delinquency rates by borrowers with prime credit ratings, by borrowers with subprime credit ratings, and overall.

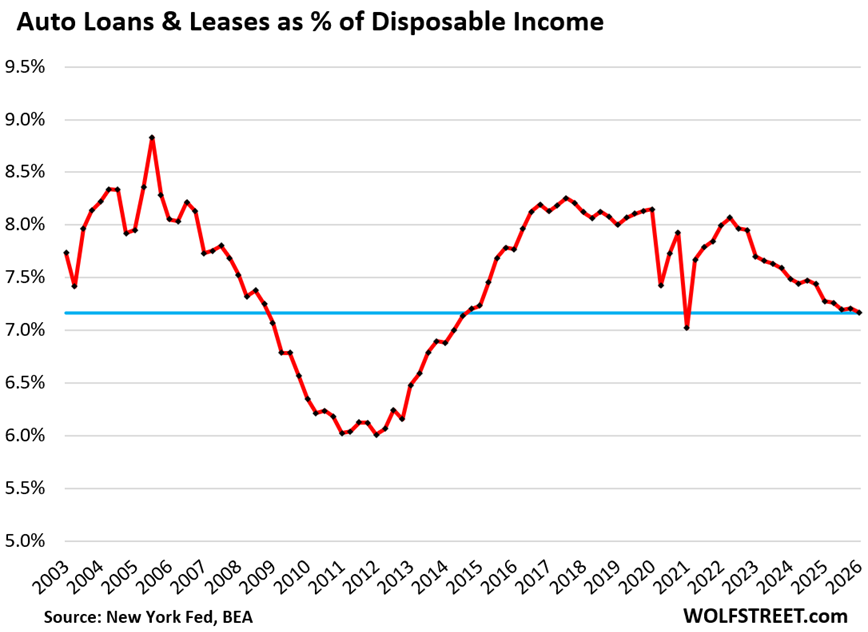

The debt-to-income ratio is a standard metric to evaluate credit risk. For household income, we use “disposable income,” released by the Bureau of Economic Analysis.

Disposable income consists of after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

But it excludes capital gains, which is where the wealthy make most of their money. Excluded are thereby income from stock-based compensation plans and capital appreciation where billionaires make their billions. And this upper crust of income is excluded.

The auto-loan-to-disposable income ratio in Q1 dipped a hair to 7.17%, the lowest since 2014, except for Q1 2021, when various government payments directly to consumers (stimulus, PPP loans, etc.) distorted disposable income into absurdity.

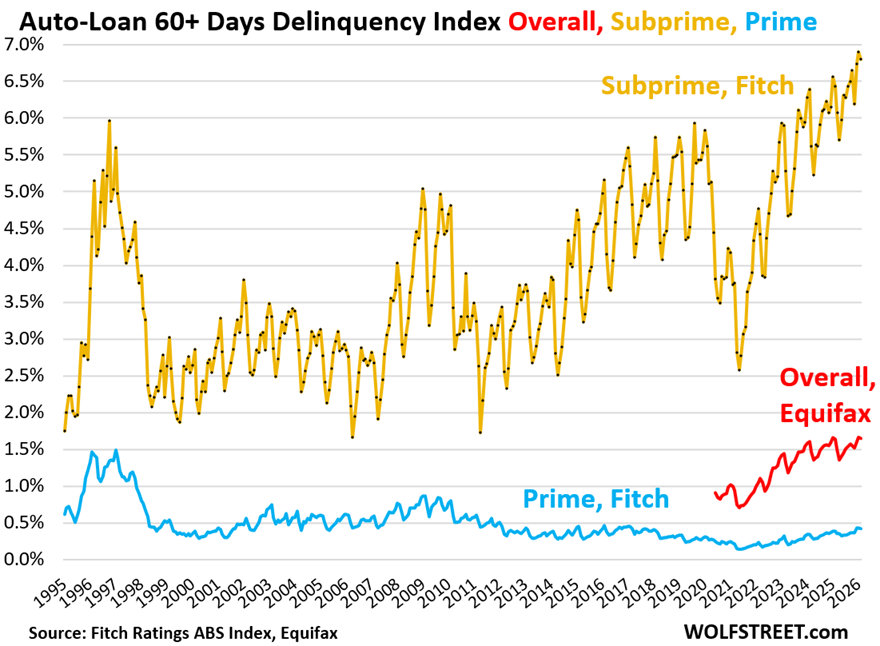

Delinquency rates of subprime & prime auto loans.

Subprime means “bad credit” and a low credit score. It does not mean “low income.” It means a history of having defaulted on loans, rent, utility bills, etc. The young dentist that got into it over his head and fell behind is a classic example of a high-income borrower with a subprime credit rating. They’ll get it worked out eventually. Subprime is not permanent.

Selling and lending to customers with a history of having stiffed their creditors is a high-risk small subsector of auto retailing, largely handled by subprime-specialized dealer-lenders and specialized lenders.

To make this business work despite the expected losses, dealer-lenders sell the vehicles at fat profit margins and then finance them at high interest rates through their finance subsidiaries, making massive paper profits on both. Periodically, they securitize large batches of their subprime auto loans through the Wall Street machinery, which then sells the resulting Asset-Backed Securities (ABS) to institutional investors. And that worked until it didn’t.

The 60-day-plus delinquency rate of subprime auto loans that have been packaged into ABS has been running at record highs, starting in 2023. The delinquency rate is seasonal, and January is the high of the year. In January 2026, the delinquency rate was a record 6.90%, up by 34 basis points from January a year ago.

The delinquency rate edged down to 6.80% in February, squeaking past February a year ago by 7 basis points, according to Fitch Ratings, which rates these ABS. Fitch has not yet released the March data (yellow in the chart below).

“Prime” auto loans are nearly always in good shape, with a low delinquency rate. The 60-plus-day delinquency rate of prime auto loans that were packaged into prime ABS tracked by Fitch inched up to 0.42%.

Even during the Great Recession, the prime delinquency rate maxed out at only 0.9%. There was a bigger problem in the mid-1990s, when securitizing auto loans was in its infancy and everyone was climbing up a learning curve (blue in the chart).

The 60-plus-day delinquency rate for all auto loans and leases declined to 1.49% in March, according to Equifax (red in the chart).

Unfortunately, the monthly Equifax data only goes back to 2020, the free-money era when delinquency rates dropped to ultra-low levels, and the increase since then is from those ultra-low levels during the free-money era. As monthly data for the years before the pandemic is not available, we lack the comparison to the pre-pandemic normal years.

Subprime is only a small part of auto finance. Of all $1.68 trillion in auto loans and leases outstanding, only about 15% were rated subprime and deep-subprime at the time of origination (Experian data).

The subprime business is very unforgiving when these dealers-lenders take reckless risks – the results of which we’re now seeing.

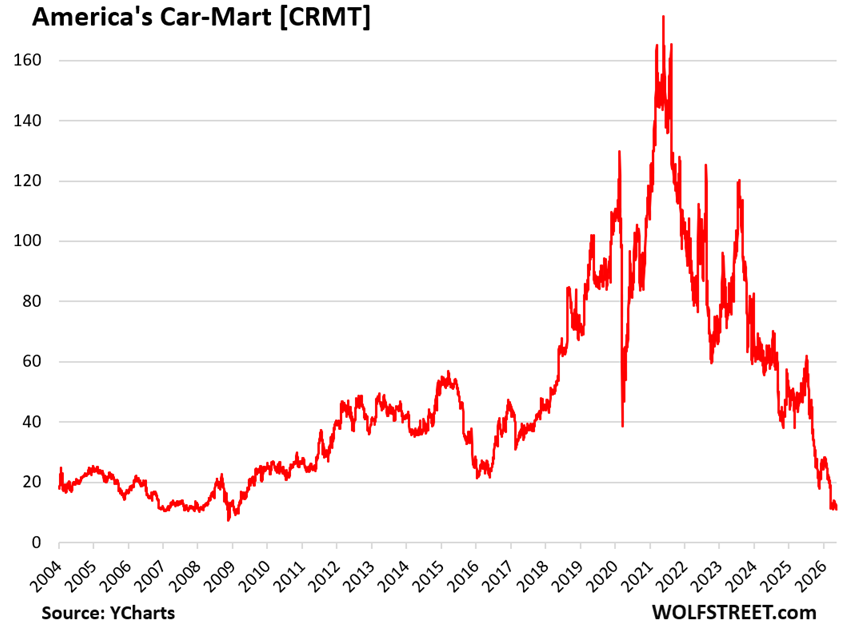

Last year, a couple of bigger companies involved in this business imploded, most spectacularly Tricolor amid a mushroom cloud of fraud allegations. PE firms got into the subprime dealer-lender business, and some of those chains collapsed.

America’s Car Mart [CRMT], the largest publicly traded subprime-specialized auto-dealer chain, also ran into severe problems, and has been in our pantheon of Imploded Stocks for a while. I featured it here in December 2023 when it began confessing to its issues, and when its stock plunged by over 20% that day to $63 a share, down by 61% from its high in May 2021. And it continued to plunge, as the company has been trying to restructure its operations and get its finances in order.

Today, share of America’s Car Mart traded at around $11 a share, a new low since the depth of the stock market crash in 2008-2009, down by 93% from its high. Taking big risks to lend to subprime-rated buyers that had previously stiffed their creditors is not for the squeamish (data via YCharts):

And in case you missed them: Here Come the HELOCs: Mortgages, Housing-Debt-to-Income-Ratio, Serious Delinquencies, and Foreclosures in Q1 2026

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I know repo guys cannot keep up, they are extremely business.

you know I bought truck couple months ago

I made 1 payment

and now

I’m recovering as those 1 payment loans are killers

tRump is a classic example of a high-income borrower with a subprime credit rating.

Most likely not. Like all ultra high net worth investors, they invest and borrow through LLCs or Corporations, and the lenders don’t require personal guarantees on those loans. This is no different from when companies like GM or pets.com go bankrupt. The lenders didn’t sue the shareholders for payment or report the shareholders for nonpayment of debt.

As I drive my 15 year old shite box with chunks missing from the hubcaps, scratches, and dents, I will remember the fools who make it possible that I am surrounded by $50,000 Shopping Utility Vehicles and Pretty Trucks.

Approximately 100% of these represent a poor decision being made by someone who has crippled their financial life for the sake of looking like everyone else. Their insurance alone is more than my depreciation, maintenance, fuel, & insurance combined. On the days when I “make” $10,000 in the stock market, I feel sorry for them, driving the shiniest handcuffs other people’s money can buy. It’s automotive serfdom.

It’s also weird to hear people talk about the stock market and how nervous they are for their $10,000 portfolio / life savings when they are driving a vehicle that burns up $5,000-$10,000 each year. Even weirder to hear them talk about gasoline, which accounts for 0.7% of my annual spending – maybe 1% now.

They feel like they get value from these things they buy, and yet they’re so financially weak $5 gasoline hurts them? I can’t understand it.

Hat tip for coining the phrase “Shopping Utility Vehicle”

Have a relative who got a promotion couple years ago, first time moving into six figures. New car bought within two months.

Everybody values stuff and not financial freedom. Math is hard I guess.

I didn’t even get into the Mall Crawlers made by Jeep.

I paid $16K cash (+TTT) last summer for a used 2025 Nissan Versa SV. It had 4,300 miles and was involved in a very minor accident. It was only titled with Hertz 14 days.

Extremely pleased so far. I’ve read where Nissan has moved up to about #7 in reliability, ahead of GM, Ford, Kia & Hyundai.

I’m a GenX’er, and I paid off our house Feb 2025. I’m convinced that when my home insurance company got the letter stating there was no mortgage that it’s standard practice to ask for extra.

Ah yes! Nothing like carefree driving a 28-year-old Honda Accord with dents, scratches and primer-paint highlights. It’s especially satisfying when a Tesla driver tries to pass me on the right in a merging lane. It’s simple economics: My cost of a fender-bender runs a few hundred dollars. Tesla driver’s cost of a fender bender runs tens of thousands of dollars.

Chis:

Agreed.

I am not the smartest financially, but it also perplexes me when someone complains to me that they can’t buy eggs because they are too expensive, as they are holding the newest $1,200 smart phone, and wearing $200 shoes.

Or the people that will drive 10 miles out of their way to save $.03 per gallon on gas maybe $.50 on a tank, and probably spent $5 or more to do it.

Spend a quarter, to save a nickel, to lose a dollar.

Perplexing to me….. but to each their own

“Shopping Utility Vehicles”

Nice.

“crippled their financial life for the sake of looking like everyone else”

See also, housing – McMansions for McMorons.

Pure Envy and there Self Esteem comes from what they Drive. Sad

That 401k may be funded mostly from safe harbor deposits.

People can, and many will, spend every dollar they make and go into debt too. Income just means nicer stuff. It’s why for many Americans, home ownership is a good financial decision because it forces them to save…until they discover the joys of HELOCs. Nothing new.

Folks hated eggs and hate gas because it’s a weekly inflation reminder/anxiety trigger, and there is not an easy substitute. Weirdly enough, my feelings towards my EV grow because electrons as not as volatile in price. I suspected it would be nice to have one during the inevitable gas gouging…and it was.

I bought 60 eggs for $5.50 in Chinatown SF last week. Took a gamble thinking maybe those are 1000-year eggs. Nope, pretty fresh.

It’s quite the hubris to claim knowledge that 100% of people spending $50k new (or $25k used in my case) on an SUV are “financially crippled”. You have no idea what strangers’ situations are.

Lots of people have high paying jobs. Lots of ordinary earners can budget savings for non-‘shite’ pleasures; whether it be food, vacations, electronics, or cars.

Is it some kind of flex to say you spend 1% of your income on gasoline? I spend 0.3% of my income on gasoline. Which of us would you consider “weirder” in that comparison?

Or just maybe: neither having an expensive car nor living an extra austere life doesn’t make ANYONE superior or weirder than the other? Perhaps unique people simply have unique preferences & priorities in life.

I think everyone can agree that some people find joy spending money on things like a vehicle if they have the means and can ay with whatever structure they want to use. I have a question though. I served in the military until 2008. It was when the military was transitioning from almost zero veteran benefits to everyone qualifying for really good benefits if they so much as wore a uniform by the late twenty teens. Obviously we should take care of our veterans in some form of another when they re-enter civilian life depending on need and service, but I have to say that I am wealthy now. I am shocked at the number of people living in my neighborhood that otherwise would never afford it if they did not receive those benefits. A lot of those people also drive absurd vehicles. I never sought out more benefits like maxing a higher disability. But I see that frequently from vets that I meet. Mind that even discussing this can bring on angry comment that veterans deserve even more, but I would love to know if any form of benefits like veterans receive now have ballooned over the years since 2008, and if those benefits have benefitted a significant portion of those still of prime working age.

@Grant

No one would give two craps what they spent their money on if we weren’t on the hook for the bailouts they’ll scream for when it all goes south.

Maybe there are several CEOs fighting their way through Monday morning traffic and risking their lives to get to jobs they absolutely love. IDK. But if they are 1 in 1,000 then “approximately 100%” is accurate rounding.

The rest of the people I see on my commute with anger / disappointment / sadness on their face are whittling their lives away working (and consuming) for the benefit of other people.

They might never get to retire, but for a few years they sat in traffic in something shiny that depreciated at a rate that, if invested each year would have made them millionaires in their 50s. Coulda shoulda woulda… people certainly do “have unique preferences & priorities in life.” For some, it is smelling the outgassing chemicals from a new car interior.

Howdy Chris B. Some folks could be small business owners, writing off the shiny new truck. Some folks may not look well driving up to a work site or place in a POS vehicle. Asking someone to trust you spending thousands of dollars sometimes requires that you look the part.

1) Tax write offs are not free money. Even if the jacked up pretty truck with custom rims, lights, and bumpers earns a small business owner a 20% reduction in their tax bill, the remaining 80% of the extra cost is still wasted if the vehicle has unneeded capabilities or vanity customization. There’s no way I trust the financial management of a large risky project to someone who broadcasts that they can’t make good choices even getting here. And the moral trustworthiness of a narcissist who abuses the tax system to put $2,000 rims on a pickup truck should be questionable.

2) In terms of “looking the part” I have received many quotes for construction services and noticed it is a waste of time to deal with the contractor in a brand new jacked-up crew cab with low profile tires that has never seen a day of use as a real truck. He’ll throw me a highball estimate, because he’s a salesman, not a worker. He throws highball estimates for a living, and lives off of fishing for the people who don’t know any better. The guys who deliver the best quotes and do the best work roll up in battered two wheel drive trucks that are 10-20 years old with a headache rack and the bed full of tools and materials. When I see them, I know they’ve cut out their middleman and have their own reputation to uphold.

I think you worry too much about what others do with their money and what they drive.

Some enjoy cars. Some don’t want a 15 yo vehicle. Some need something newer for a variety of reasons. Some just like it and prioritize their income to that…it is after all one of the reason why they work.

Because why don’t you drive a 20 yo car? Or 25yo…late 90’s early 00’s are super reliable.

Yep. My car is 25 years old now. It still looks like new because it well garaged and well maintained. I upgraded some of tech so its on par with most modern cars. I also do all my own maintenance.

Someone at a party last weekend asked why I have a fast SUV when I have fast sporty car? I laughed and said because money isn’t a factor in owning either I enjoy cars.

I only have 3 vices, cars, IT gear and maybe wine.

What’s crazy spending $15k on services for an old Italian or $15k on a stove for our upcoming remodel? My wife would argue I eat more than I drive…..

And the person riding a bicycle who doesn’t own a car is laughing at you. But life is relative

YES! Preach!!! I have 246K miles on my 4Runner but love those 10k days too! Need more people like Chris B!

I have been hearing about auto loans and credit card loans defaulting at exorbitant rates since 2022 but I cannot identify any real fallout for the economy. So, why does it matter?

Because what you were hearing was BS. Delinquencies are low on everything except student loans.

A few years back, I did a due diligence review of two different dealers for possible acquisition. Neither operation made money selling vehicles. Their goal was to “break-even” on the vehicle sales. For break-even, the cost calculation included both cost of vehicle plus direct overhead, e.g., commission, paperwork, flooring, etc. Direct overhead excluded facilities rent and utilities. Both dealers stated their profit was in loan origination, insurance sale, extended warranty, and accessories sold. From an examination of their financial records, this appeared to be true. I don’t know if this was normal industry business practice or if these two dealers were outliers.

To really understand this relationship… There are some very big publicly traded franchised dealers with lots of stores, such as AutoNation. You can look at their income statements. They split out gross profits on new and used vehicles (total and per unit, retail and wholesale), and F&I gross. They provide quite a bit of detail. All franchised dealerships are similar in that respect. F&I is huge in part because there are hardly any expenses against it, just commissions.

But our service department (so this was back in the day) was a huge money machine. We had nearly 100 techs, organized in teams, working in two shifts six days a week. It was a massive operation and hugely profitable.

My 2002 Silverado truck runs fantastically.

I had one of those Gms and loved it, but needed a newer 4X4 as my wife requires distance transportation for medical appointments (specialist eye stuff). Needed it yesterday when I bought. Because of potential snow, I bought a new Nissan Frontier and paid cash for it because I drove junk and saved money my entire working life. Never had an auto loan and never will, but it is quite an experience driving new. First two medical runs saw heavy snow needing 4 wheel drive. And yes, I crunch numbers as good as anyone but would still buy new next time around and this is why. Living rural, we just have one vehicle. It has to be reliable. Got rid of an old Yaris, a Westphalia, and pocketed insurance savings on all of them. No maintenance issues, and no more wrenching on the carport concrete. With no fault BC Govt insurance we pay under $1000 per year for collision, comprehensive, and liability coverage….using a 40% safe driving discount record. You get lawyers out of the insurance litigation racket and for profit insurance out of the coverage….. rates are cut in half, just sayin’.

I have one of that year as well, and if I have anything to say about it, I’ll own it until I die. My “newer” vehicle is a 2004.

@209er I hope you dn’t have the 8.1L V8 that my inlaws have in the Silverado 2500HD truck that they use to pull a horse trailer. Every time I have borrowed the truck the mpg has been in the high single digits. At current Bay Area gas prices it would cost over $200 to fill the (34 gallon) tank.

Mine has the 8.1, keep it at 65mph, empty, and it can squeeze out 14mpg. But you don’t buy it for mpg. You buy the 8.1L because it can do the work of the diesel with certain advantages — cheaper fuel, cheaper maintenance/repairs, simpler diagnostics. Pulling my 5th wheel RV (15k lbs) it delivers about 6.5 mpg.

A little over a year from closing the business and retiring.

I’ll keep the diesel work truck for the occasional heavy hauls.

But I will be buying an older gas truck for my day 2 day. Much cheaper to maintain,

And work on.

Besides baseball and apple pie, I think the average American purchasing way more car than they really need has become a national pastime. People driving pickup trucks without using the bed; big SUVs without ever putting down the rear seats, etc. Of course, I know that there are some who really need the additional room, but from what I observe for most it’s totally unnecessary, and a financial disaster.

Prime and Subprime are based on credit scores. But consumer (and lender!) behavior varies over the years – in some periods people are more financially cautious, and sometimes they’re more risky. Some of that is reflected in the loan balance vs. disposable income graph.

Given the trends in behavior, one would think that the relative proportion of Prime vs. Subprime borrowers would change over time. If so, can that data be graphed?

For instance, the article says around 15% of auto loans outstanding today went to borrowers who were Subprime at the time of origination. It’d be interesting to know how that 15% level has changed over time.

Overall credit scores have increased (improved) over the years. So the ratio of subprime to prime auto loans has declined (improved). Before the pandemic, I was writing about 20% of auto loan balances outstanding being subprime. Now it’s about 15%. I get this from Experian on a quarterly basis, but they have refused to give me the time series data on that.

A different metric is the credit score of loans originated in the quarter. The NY Fed publishes this data, which it gets from Equifax. And I track it, see chart below, and the ratio also declined over the years. Both ratios are pretty close, but prime auto loans tend to be longer term (new vehicles and recent-model new vehicles with 6-7 year loans) than subprime (mostly older used vehicles), and subprime loans get paid off on average soon, either through repossession or through refinance into a less onerous loan, so the subprime ratio of the outstanding balance is a little lower than the subprime ratio of loans originated by quarter.

Here is subprime as % of total auto loans originated per quarter:

Do you think this is due to financial literacy gains in newer generations, better controls by financial institutions, or maybe even ease of personal financial automation via technology? It’s hard to miss a payment on auto draft unless you routinely run you bank account to empty.

I don’t know why. But like you said, modern payment methods, and being able to instantly look up your bank balance, likely make a difference. People used to have to manually balance their checkbooks to see if they have enough money in it for a check to clear. I haven’t balanced a checkbook in over 35 years, every since I had an online bank account.

Excellent data, thank you!

Over the past 20 years, dare I say … Subprime has finally been “contained”.

At least for autos, and for now.

Subprime mortgages are now guaranteed by the government through the FHA, which insures low-down payment mortgages to subprime-rated borrowers. So mortgage subprime is “contained” to the taxpayer 🤣

Mortgages won’t blow up the financial system, but I’m starting to think that AI investments, if they keep ballooning like this, might.

If you go read the threads on Reddit or X they’re all proclaiming doom because of rising delinquencies.

As usual, thank you, Wolf, for the sober reality check.

Ha! True. The first comment on this was about repo’s being busy. Like they believe that vs this data.

Repo men probably ARE super busy!

It probably says more about the crummy nature of the work than the overall auto sector.

AI is not replacing them anytime soon.

You can’t draw a line for 330million people and say everything is good, the valuable data is always hidden or backward latent.

Good lordie, read the article. It has a whole gigantic portion on subprime, and how subprime-specialized dealer-lenders collapsed because of the problems in subprime, but that it’s only 15% of auto lending, and much less than that of vehicle sales since over half of used vehicle sales and about 20% of new vehicle sales are cash deals and don’t involve loans. I’ve been writing about the issues in auto subprime for many years. It’s always a problem, which is why it’s “subprime.”

@Chris B. The fancy new cars and trucks are only a “poor decision” for about 80% of the people in the US (Do you think Jeff Bezos someone worth 100x less than him should buy a 2012 Honda Civic?). I have never bought a “new” car in the 50 years I have been driving, but that only works for me since I own a half dozen cars and trucks so I don’t put a lot of miles on each one and if I have a problem with one I can drive another until I can either fix the broken one myself or have it flat bedded to someone who can fix it. For most people who just own a single daily driver the best tradeoff for cost, hassle, safety and dependability is to buy certified preowned every few years if you driver around 20K/year or every six years if you drive around 10K/year. Everyone will put a higher value on cost, hassle, safety and dependability. Driving a 1966 VW Beetle will not cost much if you can do your own maintenance (since they have been going “up” in value for the last 20 years like my 1995 Land Rover Defender) but there will be a lot of “hassle” keeping it on the road and it is not as safe as a new Volvo that you can lease for a lot more money and a lot less hassle.

Maybe some billionaires are out there in rush hour traffic on Monday morning. Who knows? Aside from them all the working stiffs upside down in $50k luxury Shopping Utility Vehicles and Pretty Trucks made a poor decision about their way to get from point A to point B. They certainly won’t make it to their destination if point B is financial security and early retirement.

Wolf – is it your job (or mission) to be the attendant in the movie theater to say ‘stay calm, stay in your seats. It’s just a little fire’? Or to say over the bullhorn ‘Everyone stay in your homes, it’s just a little tsunami’? Sometimes I wonder. Interestingly, you DO calm and convince SOME people, as evidenced by some of the responses in the comment section.

Is there a point where, if the data were bad enough, you would come out and say ‘The

U.S. economy is in big trouble. Abandon ship!’?

I’m genuinely curious. I’m also one of your most avid readers who reads every *%#@ article.

I’m one of the biggest bears out there. But I do look at the facts, and consumers are fine. The problems are elsewhere — and my articles show that. The next recession won’t be caused by consumers, but by the AI investment bubble when it implodes, just like the Financial Crisis and Great Recession wasn’t caused by consumers but by housing imploding. Those were the triggers. As consumers lose their jobs and get scared after the triggers cause something to implode, then you’ll see a tiny dip in consumer spending, as a result, not a cause.

Inflation is a big problem that it now bleeding into the bond market. The government’s fiscal situation is a fiasco that is now also threatening the bond market. There are plenty of big issues.

I don’t know why people are so hung up about consumers, who are doing fine, and close their eyes to the real issues all around them.

Is there a ranking of which banks are most exposed to the AI loans. I ask because I’ve been buying brokered CDs and I’m staying far away from the big name banks even though they pay .15% more interest. That’s .0015. big whoop, don’t want a personal relationship with FDIC. How about US bank? I have a money market account with them. Most of the $ is in a conservative local bank and a credit union.

If you stay within the FDIC limits for your brokered CDs, you do not need to worry about the soundness of the bank. That’s what CDs and FDIC deposit insurance are for.

If you don’t want brokered CDs and don’t want the risk of having to deal with the FDIC, you can buy Treasuries through your broker instead. There is no credit risk, and you don’t have to deal with the FDIC. Yields are similar to CDs for the same maturity. You can buy them at auction or in the secondary market. If you buy T-bills at auction, you can set them up T-bills on auto-rollover.

If you want to take some credit risk and possibly lose some or all of your principal – in return for a little higher yield – you can buy some corporate bonds. That also avoids the risk of having to deal with the FDIC.

Take a look at iBonds. You can only invest $10k per year, but it’s a competitive, inflation-adjusted yield. They are a better deal than open markets offer because of their restrictions.

Their yield is worse than TIPS yields. The I-bonds you can buy today only pay a .9% base rate, plus CPI compensation. The 10-year TIPS yield today at auction was 2.17%, plus CPI.

But I-bonds have huge tax advantages over TIPS. TIPS are a tax nightmare. In addition, if you want to, you can sell I-bonds back to the government after five years without penalty at face value plus accumulated inflation compensation. You’re not subject to market fluctuations.

Seems as though Americans are safeguarding their mortgages, but losing ground on credit cards, vehicles and student debt.

Is it wrong for me to think this? How much higher everything inflation can consumers take before housing is affected? The Bend housing market is humming along, no pain here.

They’re not losing ground. Delinquencies are low except for student loans, which people stopped making payments on for five years during the forbearance period. In about a day, I’ll post my analysis on credit card delinquencies, which have been dropping for two years and are about where they’d been just before the pandemic, and far lower than during stress periods of the Great Recession and prior recessions.

Until recently, wage growth exceeded the rate of inflation.

Paychecks rise, spending rises, and debt rises, yet all the proportions can stay roughly the same. The nominal debt chart in that situation would look like a disaster was happening though.

Seems the invisible hand of Adam Smith’s free market works even with autos. For the most part people buy what is rational to themselves and their needs, wants and finances. A few don’t make good decisions, but this is true in every area of life.

So how does an article confirming this works since the subprime market is not worse than before and not a big deal anyway result in all these comments telling other people what they are doing and what they should be doing?

In America there is no alternative to private car ownership or living in unwalkable car dependent neighborhoods.

This is largely because everyone is conditioned to believe only people too poor to own a car would humble themselves by riding public transit to work with their neighbors.

Retirement crisis is looming since everyone is paying 10K or more just for transportation each year. For many, it’s far more than 10K.

So says a guy, from his couch….

I don’t get the joke. Explain?

Just sold a house to a relative who struggled to make the 700 monthly rent payment. Somehow they qualified for the one time good VA deal & bought it ( kind of like a “liar loan”) @ 5.875%. Payment will now be 1450 plus the 2 Carvana car loans. Had to pay their delinquent way past due water/sewer bill for them so they could “qualify”. Not hard to see how this will end. Our tax dollars at work. Dazed & confused on how the “system” enables this type of subprime lending.

Well, they’d almost certainly vote against any politician who threatened to “take away” their “opportunity” to get themselves into a personal debt crisis.

So would the real estate broker, the closing company agent, the car dealer, and more.

For some people, the struggle is built into their behavioral patterns. If a person spends 100% or more of every paycheck and holds minimal savings, they will always “struggle” regardless of what they spend the money on.

I know nothing about the used car business but what caught my eye when looking at an Americas Car Mart website is that they werent posting the price of the vehicle. They say they have financing options, which most customers would use, so thats fine but not posting the price doesnt seem right to me as it is not giving them important information. Maybe they will give the price if asked, but have courtesy and respect for your customers.

Subprime-rated buyers have been turned down by other dealers because they could not get financing due to their bad credit history. Subprime-specialized dealers, such as Car Mart, don’t compete on price; they charge a lot more for their vehicles than regular dealers, and customers are getting ripped off. But these customers don’t have a choice, and price is essentially irrelevant to them. The key is getting financed so that they can buy the car, and subprime-specialized dealers will provide a loan at a very high rate, and will sell the car at a very high price, and these people take the deal because that’s the only option they have. That’s the punishment for being reckless with your credit and having ripped off lenders before.