Ugly trifecta that spooks the bond market. To soothe bond yields and mortgage rates, the Fed needs to hike, not “look through” inflation.

By Wolf Richter for WOLF STREET.

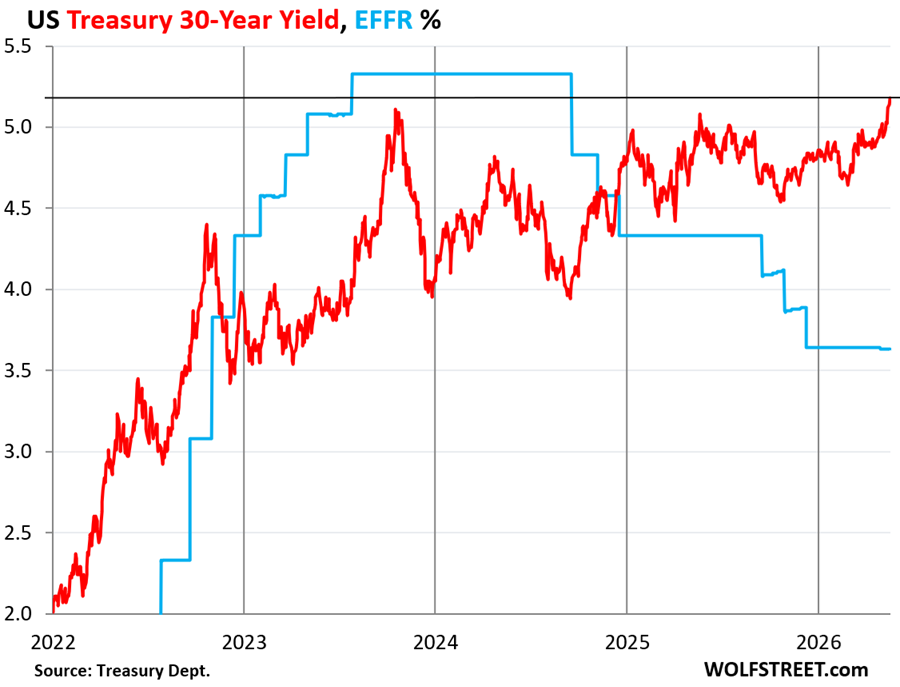

The 30-year Treasury yield rose by 5 basis points on Tuesday, and by 23 basis points over the past seven trading days, to 5.19%, the highest since June 2007. When yields rise, prices of those bonds fall, and existing bondholders take losses. It’s been a bloodbath – an orderly methodical bloodbath – in bond land.

The long-term bond market has completely blown off the Fed’s rate cuts. The more the Fed cut, the higher the 30-year yield rose: There is now a spread of 156 basis points between the 30-year Treasury yield and the Effective Federal Funds Rate (EFFR, 3.63%, blue line), which the Fed targets with its policy rates. Before the Fed started cutting rates in 2024, the 30-year yield was below the EFFR.

At the auction on Wednesday last week, the Treasury Department sold $31 billion of 30-year bonds at a yield of 5.046%, and those hapless buyers are now already substantially underwater.

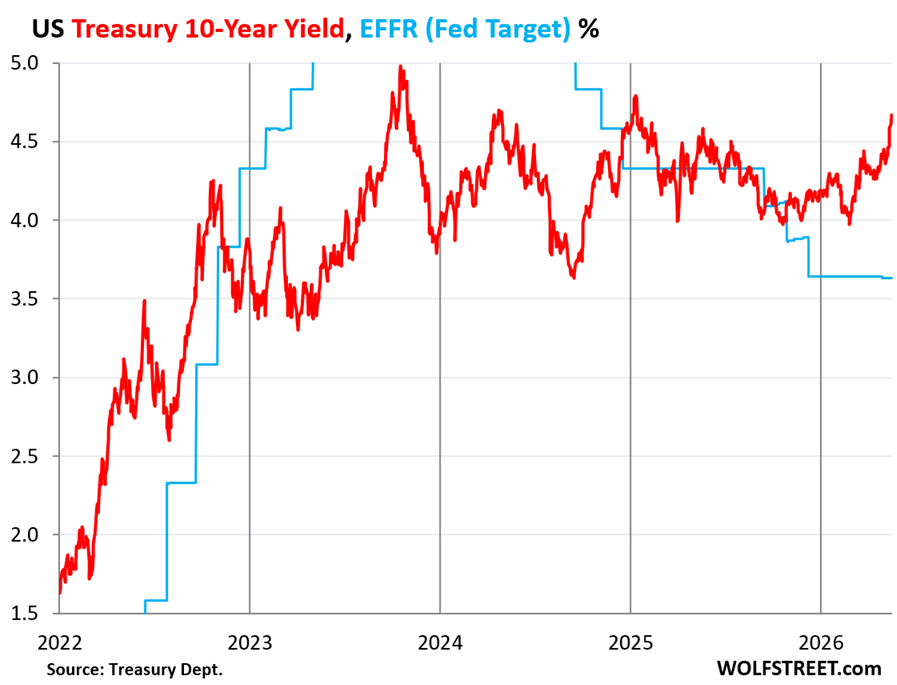

The 10-year Treasury yield rose by 6 basis points to 4.67% on Tuesday and by 29 basis points over the past seven trading days. At the end of February, it had dipped to 3.97%, and since then has risen by 70 basis points.

At the auction last week, the Treasury Department sold $52 billion of 10-year notes at a yield of 4.468%, and those buyers are now also substantially underwater.

The long-term bond market has been spooked by a trifecta of very ugly problems:

Surging inflation, with consumer-facing inflation spreading beyond gasoline into services, electricity (AI), and food, and with business-facing inflation that is now raging at 6.0%, driven by services inflation.

A lax Fed that has threatened to “look through” the surge of inflation and that is still recklessly talking about delaying rate cuts, instead of pounding home the message of multiple rate hikes. So, that raises the question: How many more mentions of rate cuts amid surging inflation can the bond market handle before the 30-year yield hits 6%?

The tsunami of new debt that the bond market has to absorb by enticing new buyers to step in with higher yields as there are no efforts underway in Congress and the White House to deal with the ballooning deficits that need to be funded with new debt. The recklessness in Washington is beyond the graspable. But the thinking is that it won’t blow up before the next election, and so no problem.

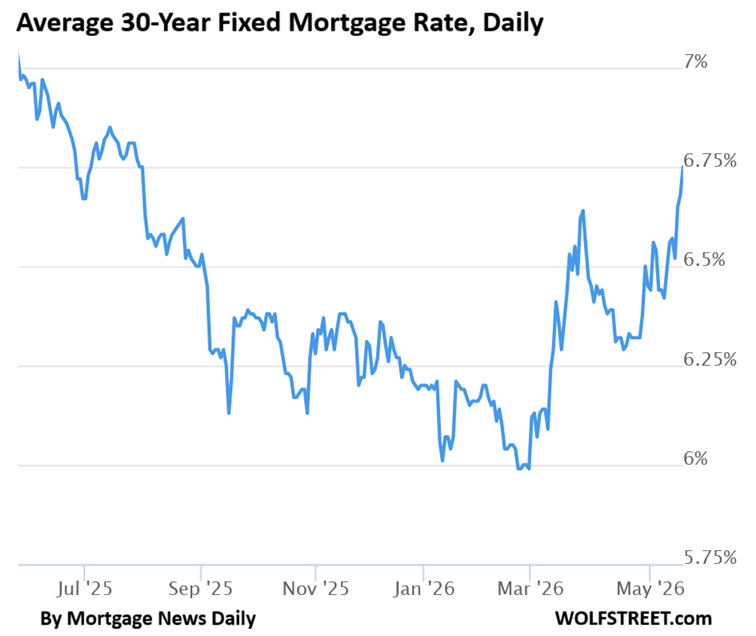

Mortgage rates, oh dear.

The 30-year fixed mortgage rate tracks the 10-year Treasury yield but is higher, and that spread varies.

The government has been trying to reduce that spread, and therefore hopefully reduce mortgage rates, by having Fannie Mae and Freddie Mac buying back their own MBS that they issued and guarantee. The idea is that the additional demand for MBS – the second-largest bond market behind the Treasury market – would reduce the yields of MBS, and therefore reduce mortgage rates.

But, but, but… To fund those purchases of MBS, Fannie and Freddie invest their cash flow from operations into MBS, instead of Treasuries, and they sell down their substantial Treasury holdings to raise the cash to buy MBS.

While the buybacks have reduced the spread between mortgage rates and the 10-year Treasury yield, the 10-year Treasury yield has shot up due to the reasons above, and… the fact that Fannie Mae and Freddie Mac, big holders of Treasuries, have now become net-sellers of Treasuries, two big institutional investors that are dumping Treasuries and are exiting the Treasury market! So the purchases may have narrowed the spread a little but pushed up the 10-year Treasury yield in the process?

And the net effect is that the average 30-year fixed mortgage rate on Tuesday rose to 6.75%, according to the daily measure of Mortgage News Daily, demolishing dreams in the real-estate industry of below-5% mortgages.

To soothe the bond market, the Fed needs to get hawkish on inflation. It needs to talk about multiple rate hikes for a couple of months, and then it needs to start hiking, and it needs to hike at every meeting, and it needs to fear inflation, not “look through” inflation. Warsh, Trump’s trusted man at the Fed, needs to get Trump on board. Voters hate, hate, hate inflation, and they have a history of throwing Presidents out over inflation. That shouldn’t be so hard to explain.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

At what point does this become the new normal

Never.

40 year bull market in bonds ended in 2020. It’s already the new normal.

Agreed.

This post coul have have mentioned the massive slaughter of bondholders that *already* occurred in 2022/2023 with unZIRP.

So you know, large part of the slaughter was taken by banks.. easy to get the stats on Unrealized Losses on bank balance sheets. More importantly, bank regulators, though tracking the numbers, fretting about the reduced real capital, did not require banks to actually reduce bank asset duration. There has been a period of reprieve for a couple years of lower term interest rates. The unrealized losses decreased significantly. There was time for banks to sell long duration bonds, reinvest in short duration, yes take losses, put correct the mismatch going forward. Few bankers bit the bullet, the regulators did not require it, and now with a 75 bp run up in intermediate term Treasury rates of 3-10 maturity, the unrealized losses are increasing again. Wait to see 2 nd quarter call report data..will be ugly.

True story:

During NIRP-ZIRP in 2022 the 30 yr was had been Bouncing around at 1.3 for years. It suddenly found itself at 1.8%

I bought $500 of the 30 yr just for bragging rights that I caught it at 1.8% because I knew it was going to zero. Then the bond bull died.

I’m so ashamed. No one should ever take financial advice from me. Not even a 10 year old.😢

It’s a good thing I’m poor. It would be a shame if I had a billion dollars. But… I have fun investing like gamblers love casinos. We both leave broke.

It already did.

It is the new normal.

Covid and spikes in inflation kicked off 6 years ago. Over half a decade of increased cost of living and everyone just shrugs. The fed even started cutting rates when it was crystal clear that inflation was trending the wrong way.

25 years ago…

This is already a new normal for the last 5 or so years where inflation si consistently much above FEDs target rate

Bond market will match the fed rate on the recession big!

2023?

I think the problem is neither FED and nor any govt (dem or rep) can face even a slight risk of recession. When there is a scent of slow down, they hose the market with money. Not just FED. Remember how the treasury bailed out SVB. For the markets, there is no significant downside risk (Yes, some individual stocks may go zero, but the index trend is always up. Same for most assets). This causes upside pressure on everything and ends with inflation.

I observe that middle class have started to changed their attitude. People are slowly tending towards stocking some items, not because they will be unavailable in the future, but because they believe they will be more expensive each day – which even causes more inflation.

“Remember how the treasury bailed out SVB.”

No, SVB did not get bailed out. It got shut down and dismembered. Stockholders lost everything. Bondholders lost everything. Executives were sued. What got bailed out were uninsured depositors, they were made 100% whole instead of having to take a 15% or so haircut on their deposits.

I will send cash after being strip searched trying to donate via my credit card because I would be honored to monetarily support your one of kind site

I need to figure out how to contribute incognito because I don’t want the security state tracking my habit of calling out the incongruities between my understanding of the social contract that lends legitimacy to any sitting government and what said government is actually doing.

First-class mail without return address works for cash.

Also, wear gloves. Let your dog lick the envelope glue.

Isn’t inflation self-limiting unless governments do helicopter drops? At some point people just don’t have the cash (or credit) to buy stuff. Real wages are falling at this point. $5 gas has to reduce other purchases or be offset with borrowing or savings drawdown.

wages are slow to catch up, and people fall behind, but then wage growth surpasses inflation rates, and people catch back up… that’s how it happened in 2021-2025. Now we’re in a new cycle, and the cycle starts out with people falling behind, as wages lag inflation, both as inflation rises and as inflation cools.

Wolf, does the old adage that the stock market falls as bond yields rise still hold true? There seems to be a view that stock market is a hedge against inflation. What is historical true and how have things changed?

One thing we know: A lot of the dynamics that held up in the past have fallen apart in this new era of craziness.

I agree, BUT, here’s the problem with the hypothesis that bond yields are going to impart any sort of fiscal discipline on our corporate puppets in D.C.;

In 1980 the DEBT/GDP was 35% (and people thought this was a “crisis”), the DEBT/GDP now is over 120%. As your own analysis has shown, there are limit’s to how low the Fed’s balance sheet can go and how high the interest on the ten year bond can go. The math tells us that we are left with some combination of Japan and Argentina. Hopefully, not 1990 Soviet Union…

This is historically true, but has indeed been exactly the opposite for the last year or so: when stocks rise, bonds rise (yields fall) and vice versa. It seems right now the buying action is either all or nothing (buy bonds or stocks or sell them both)

480 stocks in the S&P500 declined so far this year, but the S&P500 is up 12.5%.

It’s a two-track market. Tech mega-cap stocks are priced based on hope. The rest are priced based on deteriorating fundamentals, such as a rising discount rate.

So the relationship holds true, just not (yet) for the biggest tech stocks.

K shaped market for a K shaped economy

Maybe this is a possible scenario. When the yield curve re-inverts as it is now, that is an indication of a looming recession. During the 2008’s, oil prices skyrocket up, then dropped substantial. If we are going into a recession, the logical direction the Fed should go is to reduce the long end of the yield curve by buying long end bonds (yield curve control). It will reduce the interest the Fed has to pay as well as stimulate the economy. The Fed will have to reduce rates anyway during the recession. The Treasury will probably have to increase fiscal stimulus as well to counter the slowing economy.

“When the yield curve re-inverts as it is now…”

No, it un-inverted about two years ago, and there’s still no recession, and it is steeping now (the opposite of “re-inverting”)

The Fed has essentially almost continued the stimulus from COVID – which is the reason for the continued huge deficits and the reason why so much debt is being issued. Increasing stimulus would only make the problem worse.

The ONLY reason for $2+ trillion annual deficits is CONGRESS AUTHORIZING MASSIVE EXCESSIVE SPENDING OVER REVENUES and absolutely nothing else at all. The Federal Reserve hasn’t provided a single drop of ‘stimulus’ for many years.

Yes, haven’t the Japanese been doing the same thing for several years with yield curve control? Maybe the United Stated is “Turning Japanese” as the the old 80’s song goes.

The BOJ ended YCC in 2023 and started QT in 2024 and has been doing QT ever since, because it now has an inflation problem on its hands, the yen has plunged, and it has to put a floor under the yen. You cannot do YCC when inflation takes off and the currency collapses.

https://wolfstreet.com/2026/04/07/bank-of-japan-accelerated-qt-further-started-selling-equity-etfs-j-reits-shed-12-6-of-its-assets-since-the-peak/

“You cannot do YCC when inflation takes off”

So you predict interest rates will discipline the corporate puppets in D.C.?

I do not share your optimism.

To do YCC, they’d have to issue more short term debt (raising the yield of short term debt) to buy or issue less long term debt (lowering the yield of long term debt). It would be like doing QT at the short end and QE at the long end. But eventually the whole exercise evens out, on net, because it is just shuffling debt and cash from one place to another, not creating new cash or destroying it. I think that’s what Wolf means when they say they can’t do both YCC and QT.

The Federal Reserve will just do an “operation twist” again.

No, it will do a reserve operation twist to get rid of its long-term securities. It is already doing a reverse operation twist with its MBS, replacing long-term MBS with T-bills at a rate of about $14 billion a month.

So the fed is replacing MBS with T-Bills, and Fanny and Freddy Mac are replacing T-Bills with MBS.

Yes. What could go wrong?

In seriousness, this is rearranging the deck chairs in an attempt to get mortgage rates back down closer to the levels of 30 year treasuries. It doesn’t change the amount of debts or the amount of money in circulation.

The Fed is walking a tight rope given that the dollar is currently the world’s reserve currency.

I think they are likely to move at their hallmark snail pace

Great article. I am so tired of hearing about the K-shaped economy and how the “average” consumer is hurting. Nonsense. All actual data I’ve seen indicates the consumer base is resilient and healthy.

Meanwhile, every possible factor that can break the bond market seems to be happening. The Fed is already losing control of the narrative, as you so aptly point out with the gulf between the Fed Funds Rate and long-dated debt yields.

There does not seem to be any governmental interest in bringing any of the reckless (irresponsible is not a strong enough word) fiscal policy under control. It feels like we are on a plane in a nosedive with a drunk at the controls.

What would happen if the annual fiscal deficit were $0 ? Still a party?

Recession party at my house!

Just need somebody else to buy the beer and food.

Well, at a Congressional level I would agree, but the Anti-Fraud Task Force that Vance is heading up is a great start. The more we uncover in fraud should put pressure on Congress to show some level of fiscal restraint. One can hope at least. But overall, I do agree with your points.

Fraud task force, that’s funny. Sounds a lot like DOGE. We all know how effective that was.

IRS just absolved Trump and family and affiliates for any audits of several years of taxes, “forever.” In 3 of those years Donald/Melania paid less than $750.00 federal income taxes. Trump got settlement for taxing authorities’ alleged interference, $1.8 billion to a fund dispersible for his friends. OK then!

If anyone in this administration wants to find fraud, they should start by looking in a mirror.

Take, for example, the $1.776 billion taxpayer-funded settlement that Trump is making against his own DOJ, without any review by a judge.

You should read the whole of the fund. It applies to everyone, not just Trump. Hunter Biden could avail this fund. Go beyond simple twisted media headlines. That’s why we come here, to get the truth, not ideological bs.

@Candyman – Trump appoints everyone who’s in charge of dispersing the funds. Nobody believes he’s going to compensate anyone on the left, not the least because he’s been the one harassing them in the first place.

In theory, Congress would intervene here to ensure this is all fair and legal since they’re the ones who authorized that fund in the first place. But they’re completely captured; anyone who goes against the president gets primaried – just look at what happened to Massie. Trump just wants to get the money out before he loses the midterms.

To be clear, I was disappointed in Congress during the last admin as well. They’ve just been surrendering all of their power and any pretense of actually working for the public. It’s possible even that if they had asserted any kind of authority or concern about the law (say, international law in Gaza or federal law at the border), then they could have saved Biden from himself, and none of this would have happened.

I witnessed a new anti fraud measure recently. The IRS set up a special phone line to verify the identification of filers who claim a refund on their 2025 tax return. I had to call in and verify various items on a prior year tax return to get my refund. It took longer than I expected, but I’m glad they are doing it.

When they catch one of these scammers I hope they skin them alive on national TV.

Funny, I read the article and didn’t read anything about a K shaped economy.

I read that people hate inflation, and that inflation is getting worse, and that interest rates are heading up.

I’m 67. I’m trying to reconsile the “affordablity crisis” with the multitude of ways that people waste money that barely or didn’t exist in my youth.

I grew up in under 1000 square feet, carpeting and linomium flooring and counters. Today that would be unacceptible. Pickups were low cost alternatives to sedans, not a pumped up mega-car. Dogs were mutts, gotten from a shelter or a neighbor whose near feral dog got knocked up. Mine did and we kept a puppy.

Body art, casinos, lattes, non-existant in most localities. I can go on and on. I see it ll around me. My question is, which branch of the K am I looking at? I’m on the upper and I partake in much less of it than my resources would indicate.

I think much of it is rose colored glasses and your own youthful ignorance to what adults were wasting money on when you were young.

Pick-ups in their single can design are an incredible waste of money, they are single use vehicles if you have a family. AKC papered dogs have been a thing for a long time.

Body art? People have been getting tattoos for ages, maybe since humans existed. It was more hidden but I don’t think body is a major economic category. Lattes? It’s milk and coffee. Maybe they gave up the cheapo 6-pack habit older generations had.

@Gaston I’m just a little younger than Ron and I have always been more observant than most people. I think it would be hard to find even a single person that will say with a straight face that people “wasted” (or even spent frivolously) more money (as a percentage of take home pay to adjust for inflation) in the 70’s when the pickup was a “family” car since you could not only take your kids but legally as many kids who would fit in the back, AKC doge out there were about as rare as Porsche 911 or a coffee shop what had a milk steamer (when we asked for a dog my Dad told us we could play with the neighbor’s dogs for free) and most people would go years without seeing a person with a tattoo (unless they has a grandfather in the Navy or and uncle that was in a biker gang).

@Ron and @Appartment Investor – I’m 63 and I agree with you guys 100%. @Gaston – You got it wrong.

Yea, maybe my rose colored glasses missed the extra rooms and the granite counters in the house and that I actually had a show dog. Maybe my town had a Starbucks decades before it went public and all my female classmates had body art. Well I could’ve missed that.

Gaston:

Can you spell clueless?

Because that describes you too a tee.

I mean I guess I’m clueless but we keep

talking “wasting money” and yet the consumer is doing great. So is it wasting money?

Do you actually see people “all around you” complaining about the “affordability” of lattes, purebred dogs, luxury pickups, and tattoos?

Of course you don’t. You’re just feeling smug that you don’t personally spend money on those things and therefore anyone complaining about anything must be one of those tattooed, cybertruck-riding, latte-guzzling, terrier-toting whiners who doesn’t budget for austerity the way you do.

Out in the real world: people are complaining about the cost of gasoline, grocery staples, and health care. i.e. the same things you & your parents were consuming back in the good’ol’days.

The last latte I had was from a friend who made it, out camping, with his machine connected to his hybrid.

I don’t think any of that was a thing, in the 70s.

It’s like someone observing the money spent on a family TV in the 60s-70s, that also wasn’t available a generation before.

I had a friend comment on this phenomenon a decade ago: “rich people stuff is cheap tjese days.”

The price of electricity has doubled in recent years for some US markets, and someone just bought a private jet.

Clay they are hurting, it’s called inflation.

The dollars melt before the employees even get them!

Cmon

Looks like housing might have to take a bigger drop, but with higher mortgage interest rates, that won’t help affordability.

Most people pay more for interest than principal for their mortgage loans.

This is shaping up to become the worst of all worlds.

People are tired of being pawns for the Fed.

I believe an apt quote from Patrick Harker, former President FRB -Philly to you last point-

“The Fed can do many things, but it cannot manufacture a chip, unload a ship, or build a factory. When the supply side breaks, monetary policy gets handed a problem it was not designed to solve and is judged on the result anyway………..”

“……and the Fed will be asked what it plans to do about it. The answer is: not much that addresses the actual problem. Monetary policy can lean against second-round effects and keep expectations anchored but it cannot reopen a strait or replace eight million barrels a day.”

Inflation is in services.

Raising interest rates tamps down speculation, and speculation is what drives prices higher. There is plenty the Fed can do. The Fed also has regulatory powers that it rarely ever uses effectively anymore.

Yes it’s suppose to work that way, but we have just entered our 4th year in a roll, of over double digit gains on the stockmarket. Which has only happened one other time in the entire history of the market from 1995 to 1999. 😱

“higher mortgage interest rates, that won’t help affordability”

Bullshit. We have double-digit interest rates in the 80’s and homes were MORE affordable. It will depend on how precipitous the price drop is and whether or not your banking/finance overlords will actually allow that kind of deflation.

THIS is the problem with a centrally-planned “managed economy”. Moral hazard can be a real bitch.

WB

“We have double-digit interest rates in the 80’s and homes were MORE affordable.”

With a $1,000,000 purchase @ 3% 30 yr fixed rate the payment is

$4,216.04(Total Interest paid is $517,774.69)

With a $635,000 purchase @ 7% 30 yr fixed rate the payment is

$4,224.67(Total interest paid is $885,882.10)

Which would you choose?

LOL!!!! You completely miss the point. Try a $140,000 at 7%, because that’s where it needs to be. THAT’s the kind of deflation we will eventually get.

I’d pick the second option. There is greater potential for rates to fall (refinance) and greater chance of future home price appreciation.

Buying at lower prices at higher rate is always better than buying at higher price at lower rates

You can always refi but cant bring price afterwards

Home prices need to fall at least 50 percent and yes I am a land lord

The second for OBVIOUS reasons

Eh. It’s the problem with capitalism.

Capitalism only works well with a permanent, expanding slave class. It finally hit globalism, and then the slave class stopped expanding.

People hope that capitalism can provide deflation via greedy people competing with each other, but you only get that deflation once. Afterward, the greedy people, who are now rich, are free to fight _against_ capitalism. It’s what you get when you empower the greedy — why wouldn’t they take the logical next step? Why would they ever try to go back to the struggle that leads to the desired deflation?

The only way to save the local people from this greed is to turn the greedy’s attention elsewhere. To a new, enslaveable population who can bear the burden in place of the capitalist’s countrymen. But we did that with the Chinese, and it only worked once. It wasn’t going to happen a second time. And so the march toward capitalism’s inflation resumed.

Maybe it’s even inevitable. To make more money, more work has to be done; to get more work done, more money has to move faster, more private debt has to be issued, and in the end, that just means the _actual_ money supply increases.

So now, the final option: war.

Great comment.

We don’t have *free market* capitalism. We have crony capitalism which is just socialism for the wealthy. And we have a choice on the ballot for free market capitalism, which is Libertarian, but only one percent of voters choose it.

I think a rate hike would finally kill the hold out for a rate cut crowd and we’ll sellers finally accept their new reality.

Inflation is in services, commodities and energy. People will survive just fine without many of their service costs (i.e. years ago I self insured on several properties). However, energy and commodities are a different animal.

No, they will not survive just fine. Services means housing, utilities such as water and sewer, healthcare, insurance…

So services and energy are the same thing now? Insurance is THE largest scam that is bankrupting this country. Sorry but that which cannot be sustained WON’T BE.

Are you really suggesting that interest rates are going to discipline the corporate puppets in D.C.?

You really are an optimist.

Anyone going to the dentist lately? I was shocked by the costs for a routine cleaning not to mention to have a crown replaced.

Was your being shocked an appropriate response or just one of defective thinking ?

Answer these questions to find out:

What did you THINK it should cost ?

What DID it cost ?

What is your income ?

A little self reflection will provide insight.

I got a crown back in March. I have dental insurance. It paid for half the cost of the crown. I had to pay $652

Re “Voters hate, hate, hate inflation, and they have a history of throwing Presidents out over inflation. That shouldn’t be so hard to explain.”

Alas, Trump has no personal worries about voters “throwing Presidents out”, because he’s not running in 2026 nor eligible for re-election in 2028.

I suppose it still matters a lot for Trump who ends up in control of Congress after the November 2026 election.

But it’s not yet clear whether voters will actually make inflation the top priority for Congress. Or, if they did, whether Congress would actually do anything helpful.

Voters didn’t throw Biden out either. They threw out Harris. The name doesn’t matter. The party does.

We live in a one-party state. No way the Dems take either house of Congress this year. The ruling Republican Party has in it’s favor:

-Control of the media / social media (Fox, Meta, YT, TikTok)

-Gerrymandering advantages

-Electoral college advantages

-Senate advantages, because R’s control most states

-Far superior organization at every level

-More tribally loyal voters

-Support from Russia

-Support from Israel

-Support from the demographic most likely to vote: the elderly

-Support from the oil & gas industry, which is about to donate hundreds of millions as a small percentage of their profit from the Iran war

-A wider set of growing leaders to choose from in various state and local elections

-Institutions such as the Federalist Society, religious activists and colleges, Chambers of Commerce, and youth groups such as Turning Point

Meanwhile the DNC just released an autopsy of their 2024 collapse. It was incomplete a year and a half later, and they immediately started bickering amongst themselves about it. There is no reckoning or recognition that anything is wrong. They still believe in the old “demographic destiny” myth 20 years of losses later. They’ve been relegated to a regional party that is only competitive in coastal urban enclaves. In one sentence: They are not competent or motivated enough to win.

We had a Democratic Party trifecta President, Senate, and House just 5 years ago. These things always go back and forth. I have no idea what will happen in this fall’s elections, but since Reagan, the country has been between 60 and 40 for each side for a long time.

Us peons cannot self-insure if we have a mortgage. Lenders don’t like that.

So yes, insurance inflation matters.

it is becoming increasingly clear , by the evidence of policy and outcomes that economics is theory ,not gravity

inherent in the acceptance of any system is support of it and the weakness of legacy is that change is an affront to its veracity

economic theory has a great deal in common with the justice system in that legality and economic theory is a creation subject to review , modification and the behaviour of convenience

Correct and “laws” that are blatantly unenforceable simply reveal the banana republic for what it is.

I spent time in Russia in the early 90’s. There were all kinds of laws, rules, and “prices” in the “official” economy. None of them mattered. That is where we are headed.

The 10 year bonds have been at this level 3 times in the past 3 years. Seems to be trading in a ranged. Why do we think this time is special?

The 30-year tells us it’s special. It broke out.

Indeed. Yet I’m of the opinion now is the time to “begin” nibbling at LT bonds, and accumulating as they drop. If 30 yr hits 6%+ I’ll be accumulating with both hands!

The 10-year is also breaking out of this range (technically), based on the ‘23, and ‘25 highs.

That is, if the breakout is “confirmed” by a weekly close (which is questionable at the moment, on a pullback).

The bond bull is definitely dead. The bear is on the prowl.

Inflation is higher now than in those previous rate surges.

The bond market has a ways to go from here, just to catch up.

And the AI hyperscalers are now borrowers scrounging for cash to spend, instead of piling it up. That’s even more fuel for rates to go up.

You know what would be funny? If China decided to make the DeepSeek AI technology an open source project, to make all US AI investments worth about 10% of the loan values. That would be funny.

If bond market has any sense left then 10y would be at above 5 percent

I am waiting..

This time is special because Trump cannot TACO the Strait of Hormuz open, and Iran has an interest in hurting the US economy to get revenge on Trump.

The Straits of Hormuz aren’t critical to our economic survival. We can live indefinitely with 5$ gas.

If the US blockade of Iran continues a few more weeks, Iran won’t be able to feed its people. If the US got really serious and started bombing Iranian oil fields, refineries, and railroads, Iran would totally collapse.

Remarkable that there are STILL talking heads on the Financial shows calling for ….just one more cut this year. Huh?

Fed Funds at or under the inflation rates….and certainly well below the YOY PPI.

Does the SRF look like real cheap money at the moment?

Oh for a hard railed monetary policy where short rates are tied to perhaps a rolling average of inflation readings.

Slow to raise, quick to cut Fed that is “data dependent” but “sees through the data” when it is uncomfortable to do the right thing.

The problem is that people actually pay attention to these talking head financial and news shows. People think they are being informed and they are not. They are being entertained and being fed stuff that is designed to provoke an emotional reaction so that people will continue to watch.

TDLR, too many people cannot tell the difference between entertainment and actual news.

If people stopped watching and used better sources of information, these shows would die. Unfortunately people like being entertained, not informed.

Jim.

I knew a fellow who often was an “expert” on one of these shows.

I saw him one afternoon after I had seen him tout a company that was trading at $80 a share and just reported earnings for the quarter of 25cents per share. He said every portfolio should have some of this stock.

I engaged him……..noted that that was a PE of 80! He defended, but finally admitted…

“I am paid to be BULLISH on these shows.”

and there you have it. These shows are like infomercials for the stock market.

Fedwatch says the odds of a rate hike by December have increased to 60%.

Odds of a rate cut are showing at 0%.

That’s what the futures market thinks. The talking heads are way behind.

Maybe we are looking at it wrong. Maybe inflation is the goal and they intend to cut rates. The benefits are that you pay less interest on debt and you do so in cheaper dollars. Secondly, it will increase the wealth of existing asset owners relative to non asset holders. Everything this administration has done from tariffs , to tax cuts, to the war in Iran has been inflationary. It is not a coincidence. Expect more of the same.

Inflation is the goal to a certain extent. Inflation just under 3%, while pretending the target is 2%, is manageable. When inflation is above 3%, the credibility of the 2% target goes out the window and rates will explode.

No its not. There is a pressure building that is not going to end well, politically.

No matter who the US citizen votes for, the Fed remains the same. Name an election that changed Fed policy.

@Kurtis

We are heading for a very different animal politically.

Just because we haven’t voted in a full on hard left socialist government before doesn’t mean it isn’t going to happen.

@grimp

Lol full on left socialist government in the US? Oh my that made me almost spit out my coffee this morning.

The entire US system is designed around the primacy of capital. The powers that be don’t allow anyone who isn’t a threat to them near any levers of power.

Kurtis,

The us is going down the same path as Venezuela.

Go ahead and spit your coffee out and be a smart guy.

Your firmly in the “it can’t happen here” camp.

It has only happened everywhere else in the world.

Good luck with that.

“looking at it the wrong way”…..EXACTLY!

Ask someone to look at a chart of the CPI or PCE , the index and the accumulated price increases….and ask them

1. Is that a victory over inflation?

2. Is that a victory FOR inflation?

Once …inflation at 4% created suggestions of Wage and Price controls. I am not suggesting such, but look at how the inflation rate now is ACCEPTED as normal!

The Fed has failed to fight inflation, and as you mention, were they ever really trying???

Question the Fed….and hopefully someday we will get a Congressman to do so at one of these hearings.

I cannot rebut this.

It would be easier for a nation to stay solvent with >$40T in debt if you could lop off 25% or 40% of the real purchasing power through a few years of high inflation, even if that increased rates, than it would be to try to manage the debt by keeping rates low, like a household would do.

Wolf, you are only going to get your blood pressure up trying to apply logic to this crazy world we now live in.

By Fannie Mae and Freddie Mac tilting its portfolio towards more MBS and fewer treasuries, am I correct to assume that they’re taking on more risk? I.e., by concentrating more MBS instead of “risk-free” treasuries, they’re taking on more risk. So, what are they at risk of most such that F. Mae and F. Mac implode? Is it MBS yields spiking and causing prices to collapse?

My spidey senses are tingling. Saddle these two with riskier assets, let them implode, then allow the market to pick at the scraps? Personally, I’m ok with the latter outcome. Wolf, I’m ready for you to tear me a new one. This is, admittedly, speculative.

They did this before on a massive scale, and when MBS got into trouble in 2008, Fannie and Freddie collapsed and were taken over by the government. The issue is that they guarantee these MBS to third parties, but the MBS they hold on their own balance sheets are guaranteed by them, in other words, not guaranteed at all.

So if the value of the MBS held on their balance sheet drop precipitously, then does that mean taxpayers are on the hook? That’s my understanding from following your work very closely.

I mean what does that look like if the values drop as far as the mechanism for triggering something? If that happens does that mean the FED needs to print $ proportional to the drop in MBS value? Pardon my cluelessness.

Fox business this morning said mortgages were averaging 6.35%. Who’s right? Wolf or these shills?

That’s was the weekly average through Wednesday a week ago, released on Thursday last week. It’s ancient history. I gave you the daily figure as of Tuesday afternoon (yesterday).

Long-term moving averages pointed to higher yields this year. But what concerns me is the huge injections of liquidity that have prevented any recession have now ended. I.e., the FED is going to have to monetize more debt.

No, the Fed has to do the opposite. The bond market is the only discipline there is for Washington.

Howdy Lone Wolf Almost 40 trillion reasons Govern ment does not care what the Bond Market thinks.

The US Treasury cares ENORMOUSLY what the bond market thinks as the way the bond market PRICES US TREASURIES determines what the US Treasury has to pay in interest. How else do you think yields (interest rates) are priced on US Treasuries?

You have that 100% backwards. Debtors fear bond markets, not the other way round.

The U.S. government has 40 trillion “official” reasons to fear the bond market.

If rates rise 1% across the board, those bonds extract an extra $400B in interest “rents” from the taxpayers. The interest goes to those who own or benefit from the bonds, primarily wealthy retirees, but also our beloved overseas creditors such as China and Japan.

Globally, since 2020, we are in the inflationary growth period where debtors are rewarded and savers are punished (considering real rate/inflation). 2020s will be the decade of global inflation. Don’t know about the next decade.

Howdy Folks. To Invert or not Invert is the question??? When ” CASH is King “, you will not care… Those of US at Squirrels anonymous are loving this…Sailors bragging about all their purchases and future purchases…

20% percent off new cars with manufactures low interest rates loans.

FUN Times for some of US….

This is good, it will kill the housing market this summer. Sellers need to recognize they’re not getting a better price and are likely getting a worse one in the future….a rate hike would do that.

It would also kill all the NAR marketing BS. The posts and articles I still see from realtors are ridiculous.

Howdy MM1. Govern ment killed the housing market long ago… Its what Govern ment does. Picks winners and losers all the time.

DFB,

Markets killed the housing market. That’s what markets do. Markets pick winners and losers.

Technically, yes. But what if they are essentially government manipulated markets, all things considered, rather than free markets?

Many of the issues driving up the bond market are beyond Fed control;

1- The price of gasoline due to the Iran war

2- Food prices (services) as people are not buying more food and eating out more because interest rates are where they are at the moment.

3- Rent and housing as those are part of a dynamic mostly unrelated to the Fed interest rate as Wolf has so well documented here.

4- And the biggie which is unrestrained deficit spending by the Federal Government which is mostly blind to any effort by Fed rate policy.

So how is raising rates going to positively affect prices in these areas to bring down inflation?

IF and that’s a big if, Iran and the US were to come to some sort of terms that corrected the oil market, I would bet bond prices would be down at least 50 to 75 basis points in days. Most of the inflation related to that would be gone in 6 months.

AmericaisforAmericans:

“Most of the inflation related to that would be gone in 6 months.”

Dream on! There are a number of credible news sources that track and report on how much energy production has been taken off line in a very short period of time. Russian output, for example, is in a downword spiral…Moscow was just bombed for the first time since WWII. Damage done thus far to MidEast energy infrastructure is very significant. I could go on and on with more facts but you probably get the point. Inflation is going to blow out in the next few months, I believe.

Then inverse 3x short bonds and make some money if you think that will be the case. As for me, I’m a buyer at this point. One does their analysis and makes their trade. Good luck.

Thanks for the recommendation but I don’t gamble in the market. US treasuries only.

Raising rates tamps down speculation, and hence prices. That’s why Volcker has to “go nuclear” in a quick hit, pushing rates to 20%. It takes more than a circus tent over a house to kill these cockroaches.

Extract liquidity

Resume QT

100% agree. Restoring purchasing power to the dollar would help all the issues at the root cause.

This article was a masterpiece. I thoroughly enjoyed it.

More than ever I think the US and by extension, the global markets, are facing a new reality. There really isn’t a playbook for this not unlike drones have changed the battlefield. At this point it isn’t about pulling out the old playbook and tools but doing a paradigm shift, which honestly old established entities don’t excel at.

There absolutely is a playbook, we first learned it in the 1970s.

To control inflation:

Price controls … fail.

Supply constraints … make it worse.

Deficit spending … makes it worse.

Curtailment of credit availability … works.

Raising interest rates … unclear.

(High interest rates without credit curtailment wasn’t tried in 1970s. The Fed didn’t decouple rates from money supply until the 2000s. High rates alone doesn’t seem to have stopped the inflation that began in 2020.)

In the 1970s, the Fed’s mechanism for raising rates was to curtail overall credit supply. They could not do one without the other. There are beautiful historical graphs showing the relationship between the two. But nowadays, with the Volcker legend, people think it was the “increasing rates” that worked to break inflation. And no one wants to curtail credit because that means instant recession. So we’re gonna try just raising rates. I don’t think that’s gonna work.

If the total amount of credit stays the same, increasing interest rates just drives more churn: borrowers pay more in interest to lenders. Then lenders spend the money instead of borrowers. I think the result is wealth inequality and today’s K-shaped economy, with many borrow-and-spend folks struggling more than usual, and wealthy lenders living large. This is not a win.

“High rates didn’t curtail the 2020 inflation”

Huh?

Inflation hit 9% or somewhere thereabouts. After raising rates tp5.5%, which isn’t even really a “high” fed funds rate, inflation came down to 3ish, and then cuts began. The cutting at that point is only making the problem worse.

Raising rates did curtail the inflation.

right…the rates NEVER went high enough.

and now we have Fed Funds UNDER YOY inflation…and YOY PPI is 3 Xs the alleged and manufactured “2% target”.

The Fed is slow playing what is going on…….you dont have to wait for the scheduled meeting to raise rates….but it is a good excuse which they use.

We are in an economy that resembles the Jimmy Carter era of the late 70s’. I lived through that era. Today is very similar.

1. New Fed Chief Walsh replacing incompetent Powell.

(remember golf card manager Fed chief Miller, replaced by Volcker)

2. Easy money

3. Rising interest rates (especially on the long end)

4. Gas prices exploding, (gas $6/gallon)

( “Gas station from hell” had 3 hour wait in lines, I was in one of them)

5. Exploding energy prices

6. Endless War in IRAN

( Carter Hostage crisis)

7. Services inflation exploding

8. Cost of home ownership exploding, unaffordable

9 . commodity prices going through the roof

If you liked Jimmy Carter’s economy, you’ll love this one.

Crazy world indeed.

Oil and natural gas are down today.

Tomorrow???

3 HOURS? My man, go to another station and pay the extra $0.20 / gallon. Or get a used EV. It’s nice to not have to take weekly pilgrimages to those polluted shitholes with overpriced garbage food and drinks.

With EVs what happens when the grid inevitably fails? I thought the outdated electrical grid was one of the US’s biggest security risks. We can’t support sir conditioning in parts of this country without causing blackouts…

Not to mention what do most tyrannical 3rd world country governments do when their people act up? They turn off the electricity

When the grid fails, you cannot use your credit card or get gas at the gas station either. You cannot come to this site to complain about the grid failing because this site and your device will be offline and dead. When the grid fails, everything fails. EVs will be the least of all problems.

Are you aware that gas stations pumps will also not work without electricity?

If someone wants to protect against catastrophic infrastucture outages, the past 2 months should be a simple reminder that the vast petroleum refinement & distribution system is a lot more fragile than even the “inevitably going to fail” electrical grid in the USA.

At least EVs can be charged at home by people with solar panels installed. Not many people can manage to put cornfields & a biofuel refinery on their roof.

1979 they didn’t have EV’s. Read my post.

I was in a 3 hour gas line back in 1979. By the time I got up to the pump my car was nearly out of gas. So the next time I got up at 3 AM in the morning, parked my car in the front before the 3 hour line formed, went back home and slept till 7AM when the station opened. Then I went back to my car and got my gas topped off without the long wait. This station was only 2 blocks from my home. It was the same station (Exxon) that I named today as the “Gas Station from Hell” which is charging $6/gallon for gas (regular) and $6.99 for premium.

I remember those days, and the breathless reporting of peak oil.

“We are in an economy that resembles the Jimmy Carter era of the late 70s’. I lived through that era. Today is very similar.”

LOL!!!! Not even close. What was the DEBT:GDP then compared to now? Go ahead, raise the FFR to 15% I triple dog dare you!!!!

I forgot to add the one difference between the Jimmy Carter era and today. Volcker didn’t have to contend with over 2 trillion in annual budget deficits as far as the eye can see, and nearly 40 trillion in National Debt like we have now. Walsh has 500 left leaning PHd’s on his staff that have led us into this mess. They all need to be fired. He won’t be able to do that without major political fallout. Walsh has a much more difficult task if not impossible task ahead than Volcker did. I wish him luck.

Correct me if I’m wrong but wasn’t the litmus test for the fed chair to be substantially cutting rates. Got no kids. So I got my popcorn out.

Swamp Creature,

The absolute last thing the Fed should do is fire all its existing PhDs for political reasons and replace them with Trump’s favored sycophants. Then we’ll have a fed that’s even more ineffective.

Just like how our DoD is now being led by an alcoholic former Fox News host instead of someone actually qualified. And that’s not to mention the firing of generals who were not on board with the Iran war. The Iran war would have never happened if Trump had someone qualified who wasn’t a yes man running the DoD. Jim Mattis(from his first term) would have never been on board with that boondoggle.

Other examples include DOGE, which failed to improve efficiency or save any money.

RFK Jr., an antivaxxer nutjob with no medical training running the HHS.

The oil industry lobbyist running the EPA.

Pam Bondi and now Trump’s former personal lawyer(who negotiated Ghislane Maxwell’s move to minimum security prison) failing to release the Epstein Files.

When you have a government full of sycophants who are beholden to political ideology, you get results even worse than DEI.

@Mirage, that’s a big fancy straw man you just knocked down.

Swamp Creature never said “replace the useless Ph.D.s with Trump sycophants”, you made that up. And boy did you go off on that!

Might consider … do the Ph.D.’s even need to be replaced at all?

Could an AI do the job just as well?

How about something simpler, like the Taylor Rule?

Or even … like it was prior to the Fed … nothing at all?

Bagehot’s Ghost,

“Walsh has 500 left leaning PHd’s on his staff that have led us into this mess. They all need to be fired.”

No strawman, if Swamp Creature is only worried about firing left leaning PhDs and the Trump administration has any say over who they are replaced with it will be sycophants.

Thats how his whole administration has worked. Warsh is his man at the Fed and Trump would put pressure on the Fed to hire yes men replacements who are politically MAGA, the same way he has been pressuring Powell for the past year and a half to do his bidding and cut rates more and more. Trump seems incapable of letting the Fed be independent.

Cool,do I get me 70 GTO back and good concerts again?!

Why would you want a clunker like that instead of a BMW 2002tii?

Maybe. Boomer estates are selling them off as the boomers die.

And I’ve found the less I pay for a concert lately, the better it seems to be.

“That shouldn’t be so hard to explain.” To this audience no. To the president? I’m curious to know who has ever successfully changed his mind and how.

Lots of people have changed his mind. Just give him some money, make up a silly award and give it to him, flatter him, and it will change his mind.

Use fact or extensive experience to try and change his mind and you will fail.

Did Bernanke deserve a Nobel Prize or a dunce cap?

Results are in.

Bernanke lied to congress, he needs to go to prison.

How did Bernanke in any way ‘lie’ to the US Congress?

He monetized the debt after flatly telling congress he would never monetize the debt. Everyone knows you are a MMT troll, crawl back under your trust-fund rock.

WB:

By “monetized the debt” do you mean increasing money supply at what would turn out to be the bottom of the worst financial crisis since the Great Depression?

Oh Wolf, I know we’re not supposed to talk politics, but I fear you are overestimating Warsh’s capability to sell Trump on anything.

Yes, voters hate, hate, hate inflation. They also hate, hate, hate taxes (which tariffs are – they’re the taxes we overthrew the British empire in our history). And they, above all, hate, hate, hate high gas prices – even though they don’t make up a huge portion of our spend and we’ve diversified our energy production.

What I think will happen is Warsh will have the language be slightly more hawkish (or follow his proposed policy of the Fed should say less because uncertainty – that’s what the market needs!). Trumps guys will vote for cuts, the old guard will vote for neutral or raises. Trump will complain about a lack of rate cuts, and we’ll get nothing from the Fed before the elections unless the bond market freaks the fuck out if inflation continues exploding.

After the Fed’s credibility is reduced (its independence reputation is already very shaky), we’ll see what Warsh does with a lame duck, potentially impeachable President if (likely when) the House flips and maybe the Senate.

All in all, a short-term TIPS fund seems like the way to go with a bond allocation, unless you already got in on a normal TIPS fund or purchased TIPS before the market started pricing in this nonsense. Housing remains frozen. Don’t fight the Fed but maybe bet against it with this inflationary outlook and political situation?

You forgot that voters also hate rich people and pedophiles but yet here we are.

Also you underestimate the ability of marketing. It’s all smoke and mirrors and I’m sure trump will put on a good show to continue convincing the average American he’s helping them while inherently making their life worse and continuing to make the rich rich.

A side note, did anyone see the new proposed SEC rules to make it easier to go public and reduced filing requirements? No auditing of internal controls? This bring marketed as helping the public get access to things only PE and VC firms could? Lol. Wtf. It’s so PE and VC funds can unload their shares on the general public and leave them as the bag holders because the PE and VC firms are having trouble cashing out. Smoke and mirrors.

By further reducing investor protections — the SEC’s job — the stock market is going to become like the prediction market and wipe out most retail speculators for the benefit of a few. Retail speculators playing in the prediction market and losing their shirts are not be felt sorry for. The punishment for gambling is losing your money. People have a choice. I think the same about crypto. Don’t attempt to protect the gamblers. Let it burn.

Are all us long term conservative dca into sp 500 funds the speculators you speak of. It certainly looks like it.

Agree…don’t protect the gamblers…

BUT…

they did in 2009 with the bailouts

they did in the SVB debacle when Yellen unilaterally did away with the 250K limit on FDIC coverage

and who ended up losing any money in the FTX Sam Bankman Fried case?

If the right people get hurt, it all goes away…it seems.

My prediction is that Warsh will try his hardest to reduce liquidity without raising rates. He will restart QT, he will abandon the ample reserves policy.

He knows rates need to rise, but he will be afraid to raise them.

As a result, there are going to be all sorts of dislocation and emergencies in various markets and inflation is going to go crazy.

I’m not so sure Warsh is the kind of person to get scared. He has been very vocal about reducing the Fed’s balance sheet for over a decade, which is an “unpopular” position. Psychophants don’t do “unpopular”.

Warsh’s plan as of a couple of months ago was to combine rate cuts (inflationary, stimulative) with something similar to Quantitative Tightening (disinflationary, inhibitive) by letting the Fed’s assets whittle down over time.

Thus, he wants to reduce money supply and also lower the cost of money. It might work to reduce inflation, or it might hit the same hard constraint related to the supply-demand curve that price controls hit.

The market apparently loves higher yields and and inflation. In fact, the market seems to be embracing the possibility that the FED will raise rates. Just have to keep pilling into the 0DTEs and all will continue to go up.

Is the bond market being manipulated by the U.S. government? The UAE (a rich country that holds $114 billion in U.S. Treasuries) has requested a loan (currency swap line) from the U.S. Is this to prevent the forced selling of U.S. Treasuries?

If it isn’t being manipulated now, it may be in the future adding to investors caution with bonds.

Another bond investor concern may come from a perceived opening of the corruption gates.

Just added to the list of recent suspicious head scratching government transactions is this so called slush fund of 1.8 billion. And throwing out any past Trump tax audits and liabilities.

Another chink In investor confidence?

Is this a rhetorical questions “Is the bond market being manipulated by the U.S. government?”

The answer is YES.

The US Treasuries market is the largest bond market in the world and there is no way for the US government to ‘manipulate’ it. It a nearly $40 trillion free market.

Let me introduce a few terms for googling:

Operation Twist

Yield Curve Control

Quantitative Easing

Quantitative Tighening

Open Market Operations

Federal Funds Rate

There are many more, but each of these terms refers to a way that governments tweak interest rates on their own debt.

What would Treasury bond yields have been like 2008-2022 without the Fed buying almost 40% of them? Hint- they would have been much higher.

So would a short term rate hike by the Fed maybe have the effect of moderating long term rates and thereby stimulate the economy?

One lonesome rate hike would not do much. But a Fed that is hawkish on principle, stays hawkish, pushes its policy rates higher, stops talking about cuts, etc. may keep the long-term bond market from blowing out like it did in the late 1970s and early 1980s, when long-term Treasury yields were heading to 15%. This is not about lowering long-term rates but about keeping them from blowing out.

The 1970s experience was that inflation would come right back as soon as the Fed cut rates again. Only in the 1980s did rates exceed inflation by enough of a margin and for long enough that inflationary expectations were demolished.

Apply that lesson to today, and the FFR would need to be above 5%, and maybe 2% above inflation for a year or more.

I don’t see that kind of discipline. We’re still in the bargaining stage of grief, as Warsh’s testimony makes clear. Sent $20k to STIP and $10k to iBonds.

MW: The Federal Reserve minutes show increased chances of interest-rate hike ahead…

The Fed is so behind the curve……it can only be determined as INTENTIONAL.

How many months above the 2% “target”?

And now F F under the inflation rate……WAY UNDER.

And all we get is hand wringing and crickets.

MSN: USA national debt officially hits $39 trillion — adding $5 billion a day…

Should be “re-hit” because it hit the $39 trillion mark the first time on March 19, but then a flood of tax receipts ahead of Tax Day caused the debt to drop again and stay below $39 trillion for a couple of months.

https://wolfstreet.com/2026/03/19/bond-market-gets-edgy-as-us-treasury-debt-hits-39-trillion-spiking-by-2-trillion-in-7-5-months-and-not-slowing-down/

This is not just the Fed’s problem. This is a massive failure of the house to budget the national economy in a responsible manner. And until Congress gets it’s act together and actually puts a realistic budget in place (something we have not had in 4 administrations) inflation is going to hang around. This is the reality nobody in office wants to face.

The Fed increasing the interest rate will slow inflation, but to kill it you have to pay off the debt, and anyone who’s every had a credit card knows that’s the hardest thing to do.

Voters are not asking for fiscal responsibility.

They just repeat the mantra that they want “jobs” even during a period of historically low unemployment. They also want asset prices to zoom up so they can be rich.

The politicians are obliging in the same way Hugo Chavez did. Trump is taking equity stakes all over the semiconductor industry like a true comrade.

Most voters dont realize or understand the fiscal mess we’re in because of the illusion of normalcy of 2 trillion in deficit spending, but that cant last. “Jobs” is a term used by uniparty operatives and politicians to try and quell lower income people but the K shaped jobs like delivering food fueled by deficit spending arent helping long term prosperity of ordinary people.

Risk is being repriced globally. Simple as that. Do debts and deficits matter now Mr. “We would never monetize the debt” Bernanke?

“They did this before on a massive scale, and when MBS got into trouble in 2008, Fannie and Freddie collapsed and were taken over by the government. The issue is that they guarantee these MBS to third parties, but the MBS they hold on their own balance sheets are guaranteed by them, in other words, not guaranteed at all.”

Fannie & Freddie should have been eliminated or completely privatized long ago. They are completely corrupt and incompetent and no longer serve any useful service. Trump had some of the heads fired but the same personnel that lead to the 2007/2008 disaster are still in place and screwing things up worse than ever. Their MBS portfolio is already way under water and is heading south, and they should not be buying more of these securities. Worse yet, they have introduced new burdensome regulations which will freeze up the entire Real Estate market, and crash the housing market worse than 2007/2008. This goes against everything the administration has been promising about lifting the burden of Federal Regulations. These Agencies need to be abolished before it is too late.

And just what do you propose would take the place of these agencies for mortgage origination? Certainly NOT THE BANKS as they do not want to be part of that business and take on any risk by doing so.

The banks absolutely will originate mortgages to hold on their own books, just at less attractive rates and less attractive terms and durations. Which means lower prices. Which is a good thing.

The banks will not provide long-term funding for those mortgages. It may ‘originate’ some but that will drop to nearly nothing if the loans can’t be packaged into MBS instruments and passed on to MBS markets with other parties at risk of loss. As to prices of houses that’s always dependent on supply and demand.

SocalBeachDude

The banks will 100% originate. Houses need to sell when they need to sell. If they originate at 100k over a 20 year term vs a 600k over a 30 year term then so be it. You are delusional to think the market will not correct itself, even though it would likely be the most painful correction in economics.

As I clearly stated, banks are absolutely not going to go back into funding residential mortgages and retaining that risky stuff on their books. If those loans cannot be packaged into MBS instruments, then folks should start considering simply paying CASH if they want to ‘buy’ residential properties.

Fannie and Freddie have been subsidizing mortgages for people who are not really qualified to get a conventional mortgage. Those people should have to keep renting until they can properly qualify. It should be difficult to get a mortgage and require a substantial down payment. Bank’s underwriting departments would actually have to scrutinize applicants. Rates would be higher to properly access risk. This would drive down home prices which is what we really need. Government intervention always drives the price up of anything it touches. Same thing with student loans!

Fannie and Freddy are serving an important function for this government.

All the risky MBS debt once held by the Treasury is going to them. When they fail, the politicians will bail out the bondholders and blame the management. We’re dumb enough to believe it.

One thing is for certain: Privatization is off the table. The GSE’s are too valuable to the political class as a tool for manipulating long-term bond prices lower.

Socialize the inevitable losses to come and privatize the gains. Hardly anyone will sell at these highs to secure their profits. Most will watch their portfolio’s deflate. Some will panic and sell it all on the way down. Not enough room for all to hit the exits. At the bottom the masses will be cursing and hoping the prices come back again. Their retirements deferred again to sometime in the future………if at all.

Well, Cathy Wood is selling at these highs. I doubt she’s the only one right now. Maybe we’re finally there…

Fool me once fool on you, fool me twice fool on me, fool me thrice, I don’t learn from my lessons.

– USD debt buyers for the last 15 years and rising.

You’ve got long term debt buyers living in fairy land, if 2022 wasn’t a big fat red flag I don’t know what would be… and stock buyers buying on the stimulus and rate cut after a crash front-running, and then the inflation trade hypothesis… as if businesses will do well in a deep recession with hot inflation?

Only if everyone stays calm and follows that mantra, and no one thinks to sell.

What could possibly go wrong?

at the first sign of trouble I bet we start hearing about “tax rebate” stimulus checks like we received in early 2008.

like they say they ain’t buying what you’re selling and USA debt will not be selling very well

The US Treasury can sell 100% of its debt in perpetuity with the only issue ever being the yields (interest rates) for buyers to buy that debt.

Do you have any concept what you just stated would actually look like?

“only issue ever being the yields”

A 10% ten year bond would blow through everything in sight.

Can you imagine the burden placed on towns, cities, states, corporations, etc. Not to mention the blowout in US debt financing costs. Property taxes would skyrocket.

Either that or inflation could skyrocket. Maybe it will be something in between both scenarios. One way or the other it seems we’re going to need to learn to get by with less.

Why the Government Must Honor Debt Constitutional Obligation:

The Public Debt Clause of the 14th Amendment dictates that the validity of the public debt of the United States shall not be questioned.

Economic Consequences: Refusing to pay Treasury bonds would trigger a sovereign default, resulting in an immediate collapse of the U.S. credit rating, a plummeting dollar, and soaring borrowing costs for citizens and businesses.

Are We There Yet? Not Likely to Happen on our 250th anniversary celebration. We are the GOAT, Too Big Too Fail. We still many Alexander Hamilton Patriots among us. I’m ready to see a movement of $10K, $100K, $1M pledges to those citizens of the USA who want to pay down the deficit and be done with soap opera on the world stage. Congress should make the first mandatory contributions. I never really actually knew and understood the severe hatred, socialist tendencies and ideologies, the extreme Left Wing had for my country.

The inflation we’re living through is being driven far more by structural, supply‑side, and geopolitical forces than by consumer demand. The Fed is a spectator with a broken lever. We are in a physical‑economy inflation regime, and the Fed only has a financial‑economy tool. The kind of inflation that interest rates cannot fix, because it originates in physical bottlenecks, not excess demand.

Core inflation is in services — they’re 65% of consumer spending.

Wolf needs do do some charts on Freddie and Fannie Mae ‘s history of mismanagement and recent developments, including their massive purchases of MBS’s. They are the elephant in the room. If they go down like I think they will, look for them to take a lot of people with them. No one is talking about them. Where was Musk and DOGE when we needed him?

As long as they’re under government conservatorship, they won’t go down. They’ll just swallow up a lot of taxpayer money again.

Just checked my local bank webpage, they are offering loans that appear to be kept in house, never heard of Fanny Mae buying a 20 yr loan. They have arms fixed at 5% for the first 5 yrs, best deal IMO is an arm that is fixed at 5.5 for 15 yrs. I usually got refis from them with no hassle & low closing cost. Seemed I was going the 2nd mortgage department. Not sure I could tolerate the hoops for a sold loan.

My credit union offers in-house loans as well. I got a home purchase loan from them once. I have a commercial loan on a rental house but it has to get renewed every 5 yrs.

Small potatoes in the greater scheme of things but it’s a niche. Aren’t HELOCs kept in house?

You do not know in advance if the bank will keep your loan on the balance sheet, or sell it to Fannie, securitize it into a private label MBS and sell it to investors. If it is a non-conforming loan (too large), Fannie will not buy it, but it can still be securitized and sold to investors, and you would not know. All you know upfront is that your bank or credit union will originate that loan. What they do afterwards with it may never become known to you if your bank/credit union remains the servicer of the loan, after having sold it; you will continue to make your mortgage payment to your bank, and it then passes on the payment minus its fees to the servicer of the MBS (such as Fannie), which passes it on, minus fees, to the MBS holders.

Fannie will buy conforming fixed-rate loans (max size) of 10-30 years, no problem. But 20-year mortgages are not common. The two standard terms are 30-year and 15-year.

Do Fannie and Freddie buy second mortgages? Besides I kinda doubt they would have taken on some of my houses. They also might have been more diligent about my income, not assuming my hourly wage was multiplied by 40 hrs a week, for example. Besides, my debt to income levels were way out of whack for a sold loan, because they treated investment mortgages like a personal loan. In their view a loan on a duplex was the same as a loan on a boat.

Now I might have had a loan sold once. I refinanced my home at the same time as a rental property at a mid size bank. That involved some hoops. Near the end they balked at the rental property location and suggested another. I cried redlining and that put an end to that. Later my renters got a letter indicating I lived in the rental, I’m guessing the bank said it was my home and sold that loan. Meanwhile, when I got around to selling my former home the bank said it was assumable. Is that allowed on sold loans?

I have a basic economics 101 question for Wolf, or any of the informed readers.

So, Fed trimmed it’s asset size by ~2.5T in 3 years (Q4 22 to Q4 25). Globally it may have been ~4T. On top of that govt issued ~6T of debt. Globally may be 10T.

Usually in such a scenario, private investment should have been crowded out. As per basic economics when Govt borrows recklessly and it is not monetized by Central Bank, it should result in money being directed from private investment to public coffers. QE is usually done to prevent this, govt may continue to borrow while private sector is not bothered.

But if private sector had to cough up 8.5T to finance US govt (6 – (-2.5)) and globally may be 14T, how did it still have spare to finance such massive AI investments? What am I missing? Is there a substantial lag effect in this transmission mechanism?

That “crowding out” theory, if simplified like this, is somewhat nonsensical. What happens is that an economy with profitable growing businesses creates money by definition, and this money gets invested (often in expansion projects, machinery, etc.) to produce more growing profitable economic activity. And some of it gets invested in government bonds, but the government then plows that money back into the economy. It’s not like the government removes that money from circulation – it just redistributes it, and it keeps circulating.

What also happens is that Treasury yields rise until there is enough demand to absorb all the Treasuries, and if there is a lot of supply of Treasuries (new issuance), then more buyers need to be pulled in, and it may take higher yields to do that.

The IRS did a great job with my paper tax return that I did myself. They got it on March 6th and I received my $3000 refund on May 14. Paper returns are still alive and well. I’ve used them for many decades and never had a problem. Saved over $10,000 in fees to Junkyard dog accountants.

You can file electronically directly with the IRS, and it’s free. Or you can use tax preparation software, which makes doing taxes a breeze, and it will let you file the return electronically. A week later, you have your refund. So in your case, you might have had your refund by March 14. And it’s a lot lot lot safer than mailing paper returns.

I heard that paper returns have less chance of being audited. I report every penny, so that is not a concern to me. Last year I overpaid by $500 because I forgot to include an estimated payment of $500. They caught it and sent me the $500 a few months after I submitted my return with interest. The IRS gets a bad rap, but I’ve never had any problem with them.