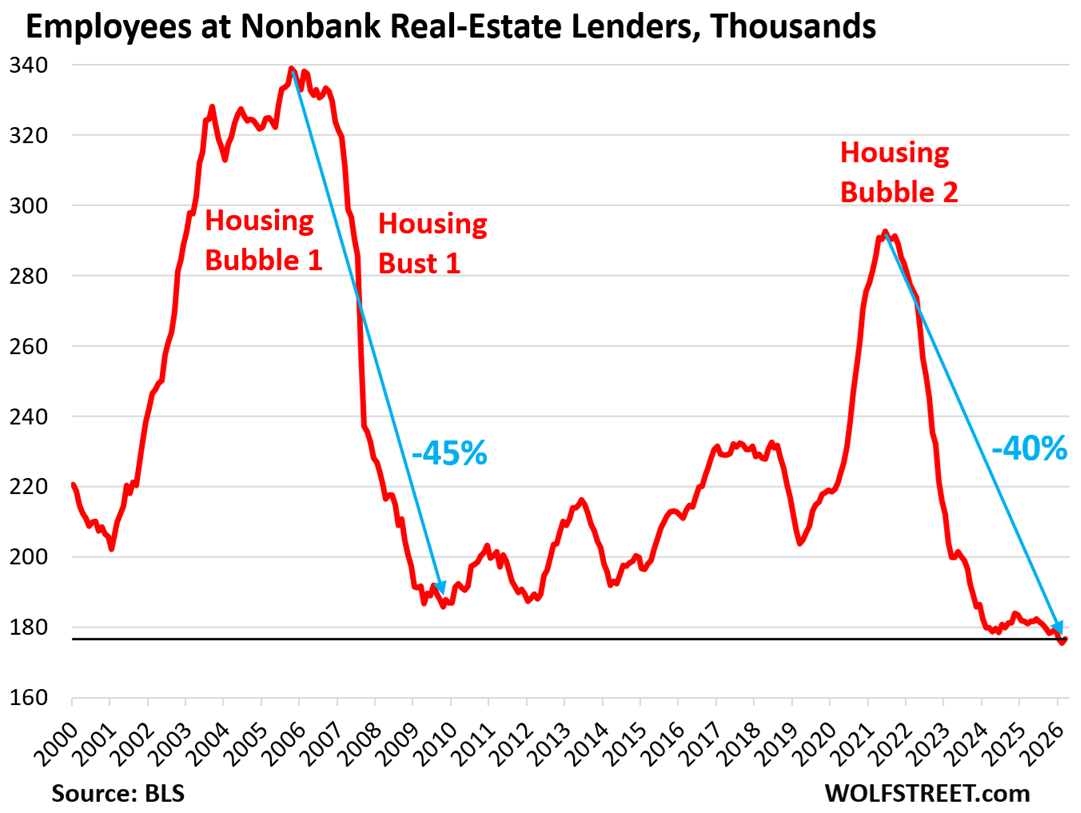

Nonbank mortgage lenders shed 40% of their jobs this time, and loan brokers 38%. They react to demand, which collapsed.

By Wolf Richter for WOLF STREET.

Housing bubbles entail employment bubbles at mortgage lenders and mortgage brokers. And housing busts then dramatically unwind those employment bubbles as mortgage lenders and brokers react to plunging demand in the housing market.

Employment at nonbank mortgage lenders – which dominate mortgage lending in the US, see list below – has plunged by 40% from the cycle peak in mid-2021 to 176,700 workers in March, according to the Bureau of Labor Statistics. Employment in February and March at these companies was the lowest since 1997.

The employment bubble of Housing Bubble 1 had been even bigger than the employment bubble in Housing Bubble 2. Since Housing Bubble 1, a lot of work in mortgage lending has been automated, digitized, and moved online, now requiring less human work and a relatively smaller workforce than 20 years ago.

These jobs are at nonbank mortgage lenders only. The jobs at the mortgage-lending divisions of banks, credit unions, and thrifts are not included here.

But mortgage-related employment at banks traced a similar line, documented by announcements of mass layoffs in 2021-2023 at the mortgage divisions of Wells Fargo, JPMorgan Chase, Bank of America, Citi, and other banks.

Housing Bubble 2 was characterized by a home-price explosion from mid-2020 through mid-2022, in many markets reaching 50% and more in just two years, fueled by the Fed’s reckless monetary policies, including purchases of trillions of dollars of securities, including mortgage-backed securities (MBS) that repressed mortgage rates below 3%, despite surging inflation which at the time was heading toward 9%.

Mortgage lenders reacted with largescale layoffs, starting in the second half of 2021, even as home prices were still exploding through mid-2022. They saw it coming.

By now, home-sales volume has been in the deep freeze for four years, along with mortgage originations. Home prices have dropped in many cities, including by 25% in Oakland and Austin, with condo prices falling faster in more cities – here are 31 major cities where condo prices dropped by 12% to 31%.

The nonbank mortgage lenders dominate mortgage lenders.

The employment data in the chart above is about jobs at nonbank mortgage lenders. The largest four mortgage lenders by the number of mortgage originations were nonbanks in 2025, according to data from Bankrate. Combined, those four nonbank mortgage lenders wrote 1.08 million mortgages in 2025, of about 5.4 million total mortgages.

Thousands of smaller nonbank lenders, banks, credit unions, and thrifts carve up amongst each other the remining mortgage originations.

| Mortgage lender rank in 2025 | # of Mortgages | Billion $ originated | |

| 1 | Rocket Mortgage | 429,322 | 116 |

| 2 | United Wholesale Mortgage | 422,120 | 164 |

| 3 | CrossCountry Mortgage | 125,099 | 49 |

| 4 | Pennymac | 100,816 | 35 |

| 5 | Chase | 94,234 | 66 |

| 6 | LoanDepot | 91,730 | 26 |

| 7 | Bank of America | 88,530 | 37 |

| 8 | Guild Mortgage | 86,111 | 27 |

| 9 | Veterans United Home Loans | 82,764 | 28 |

| 10 | Navy Federal Credit Union | 80,547 | 19 |

| Total | 1,601,273 | 567 | |

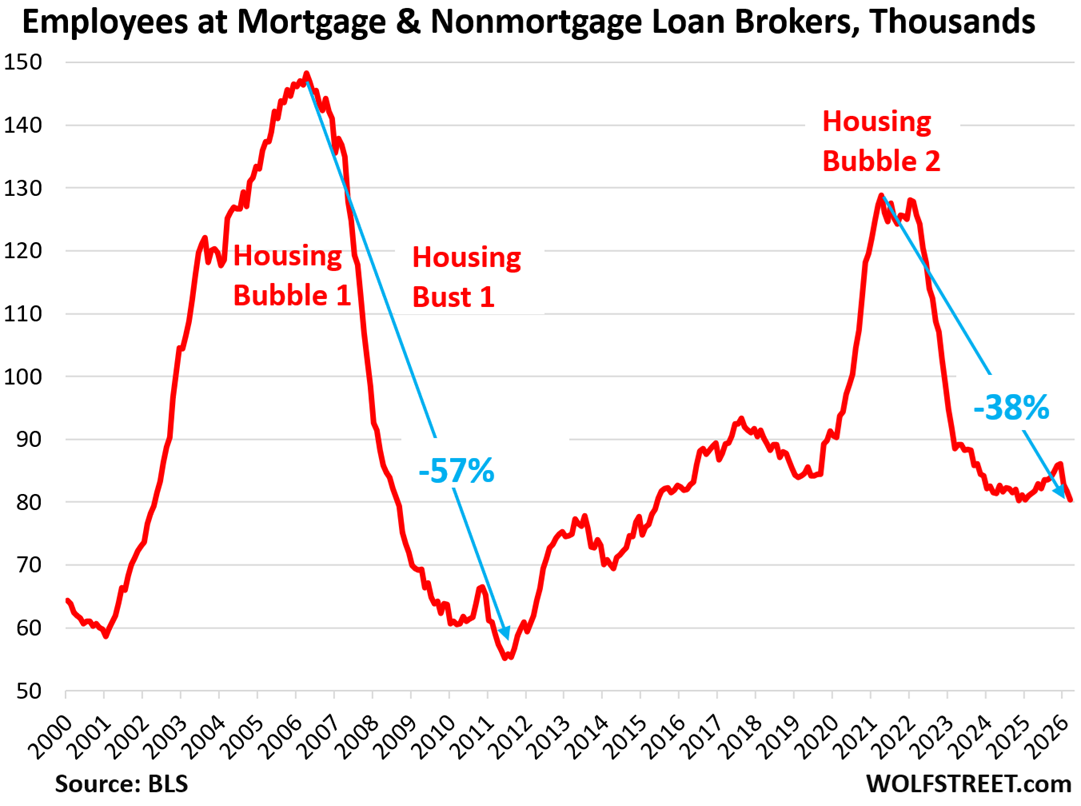

Employment at loan brokers has also formed the double-hump of Housing Bubble 1 and Housing Bubble 2.

Mortgage brokers have shed 38% of their employees since the cycle peak in April 2021. The level of employment of 80,400 workers in March along with about the same level in November 2024 were the lowest since 2015.

Note the ramp-up through December 2025, that then fell apart as the crucial spring selling season has turned into a dud.

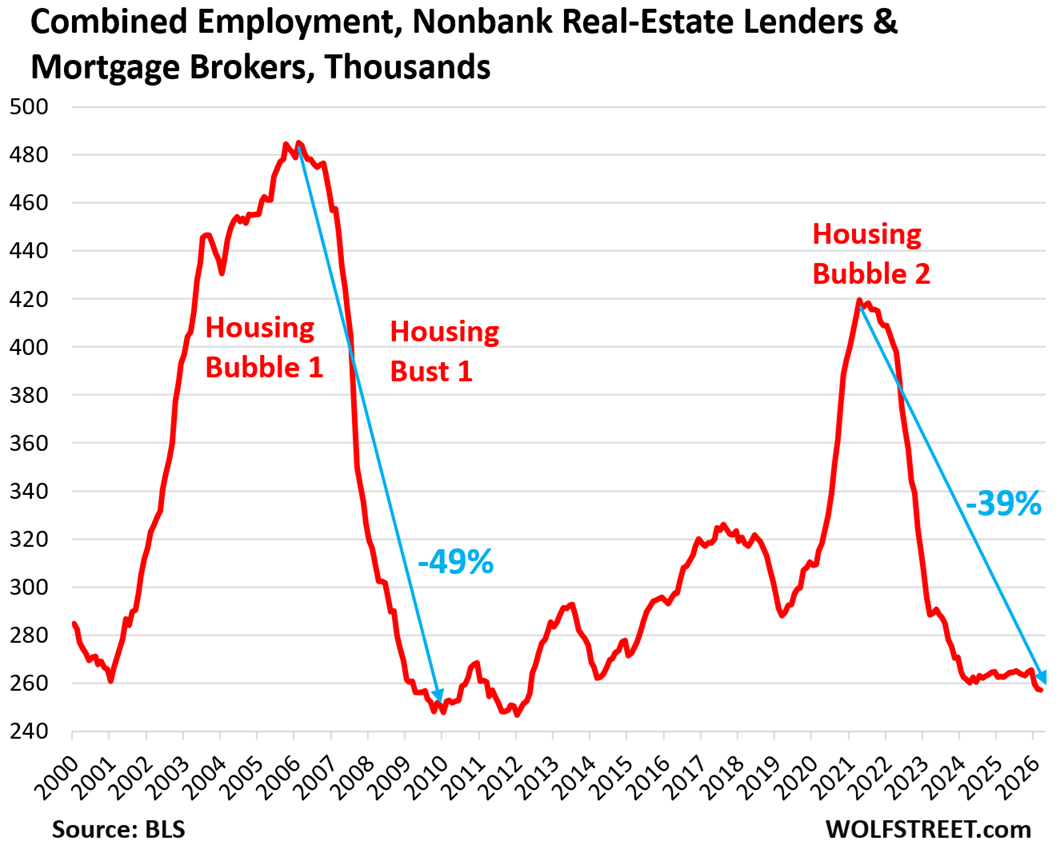

Combined, at nonbank mortgage lenders and at loan brokers, employment plunged by 39%, or by 163,000 jobs, to the lowest level since May 2012, coming out of Housing Bust 1.

Because demand plunged…

Employment in mortgage lending plunged because home sales plunged, and so mortgage originations plunged, and refinancings collapsed because mortgage rates had risen, and there wasn’t enough work to do.

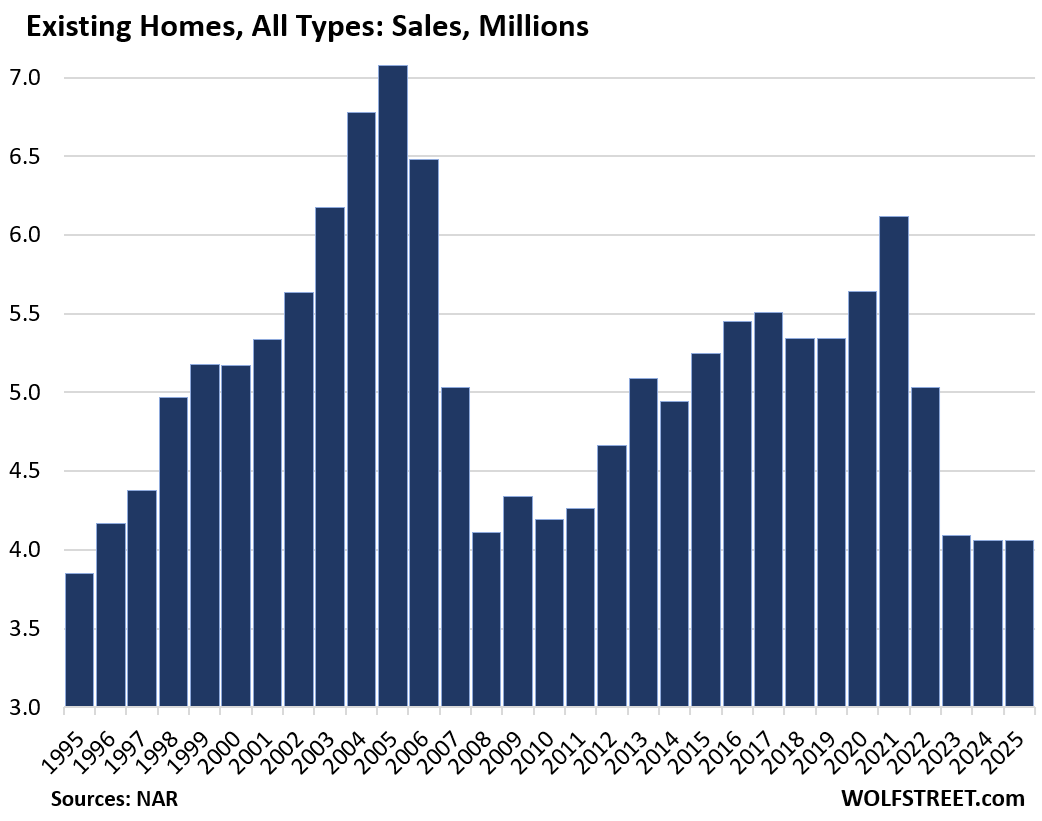

Sales of existing homes plunged by 24% from 2019 for the third year in a row, to 4.06 million homes of all types, the lowest since 1995, below even the worst years during the Housing Bust.

Compared to the pandemic high of 2021, home sales were down by 34%; compared to the all-time high in 2005, they were down by 43%. And so far this year, it hasn’t been any better.

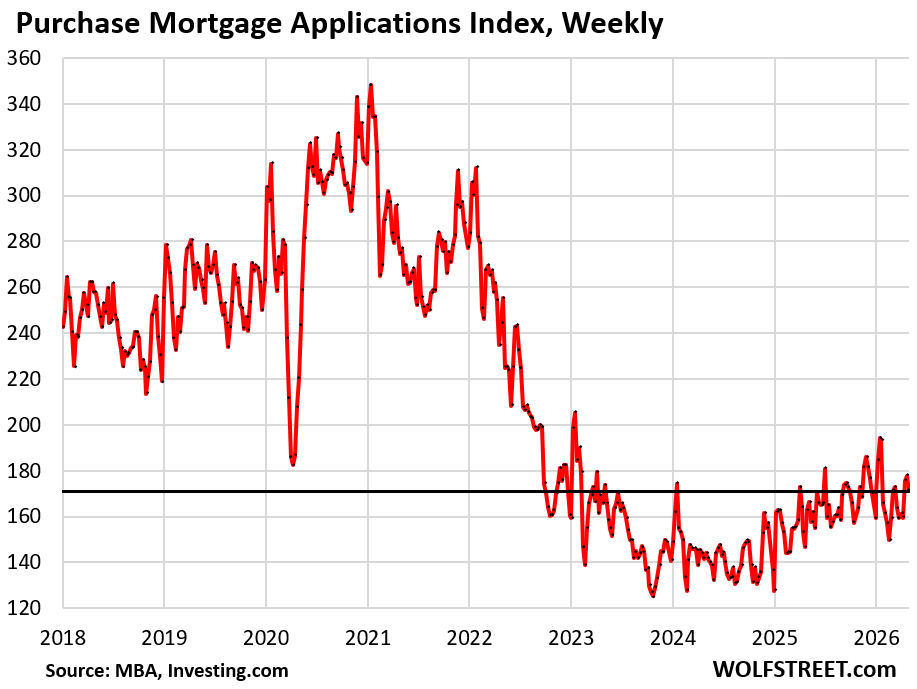

Mortgage applications plunged even more than home sales.

For the mortgage lenders and mortgage brokers, the number of mortgage applications is the metric that ultimately matters the most. That’s their business.

Applications for mortgages to purchase a home were still down by 34% in the latest week compared to the same week in 2019, and by 38% compared to the same week in 2021, according to data from the Mortgage Bankers Association.

The beginning of 2021 was the peak of mortgage applications to purchase a home, followed by a second but lower peak in late 2021 and early 2022, as mortgage rates had begun to rise and a renewed frenzy ensued as people wanted to lock in the low mortgage rates while they were still available.

Applications for mortgages to refinance a home in the latest week plunged by 71% compared to the same week in 2021, when mortgage industry employment was peaking, as everyone and their dog refinanced their mortgage with these 3% mortgages that resulted from the Fed’s interest-rate repression.

For mortgage lenders and brokers, this refinance tsunami in 2020 through was a huge business that vanished very quickly when interest rates began to rise.

In case you missed it: Housing Unit Growth Far Outruns Population Growth: Vacant Units on the Market and the “Accidental Landlords”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks very much.

I told Marty that if they rehire him and he’s busy again, to let me know.

💡 📈