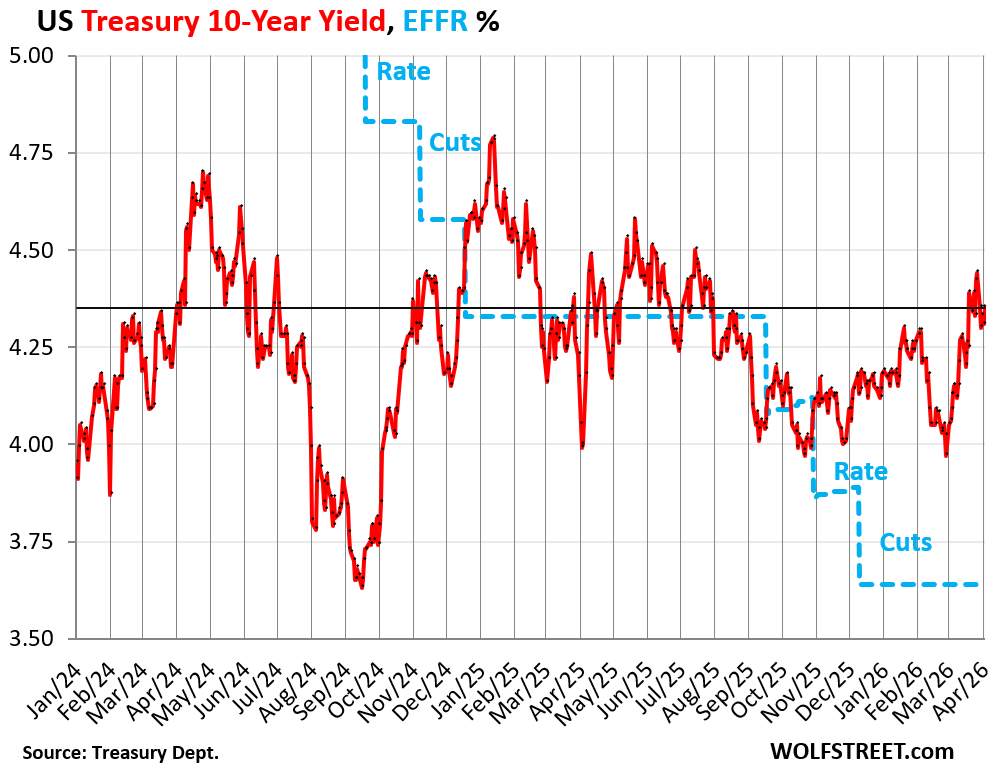

10-Year Treasury yield bounced to 4.35% on Friday, after dipping earlier in the week. 30-year Treasury near 5%. Entire Yield Curve above EFFR.

By Wolf Richter for WOLF STREET.

The 10-year Treasury yield rose 5 basis points in shortened trading on Friday on the release of the jobs report and closed at 4.35%. It had spent the first four days of the week backpedaling 14 basis points, after spiking by 47 basis points from 3.97% on February 27 to 4.44% on Friday March 27.

At 4.35% on Friday, the 10-year yield is where it had been in July 2025. And there were three rate cuts in between, as depicted by the Effective Federal Funds Rate (EFFR, blue line), which the Fed targets with its policy rates, and which the 10-year yield has been blowing off.

The bond market is now very edgy, with inflation fears front and center, followed by supply fears as it is facing Trump’s new budget, formally released on Friday, in which he asked for a 44% increase of the military budget to $1.5 trillion, which added to the concerns about the Treasury debt that has already been increasing at a rate of about $2.2 trillion a year that the bond market has to absorb, with new investors needing to be enticed in, and that may take higher yields (and lower prices for existing bond holders).

There has been a lot wailing and gnashing of teeth about the 10-year Treasury yield rising again, and dragging up economically important interest rates.

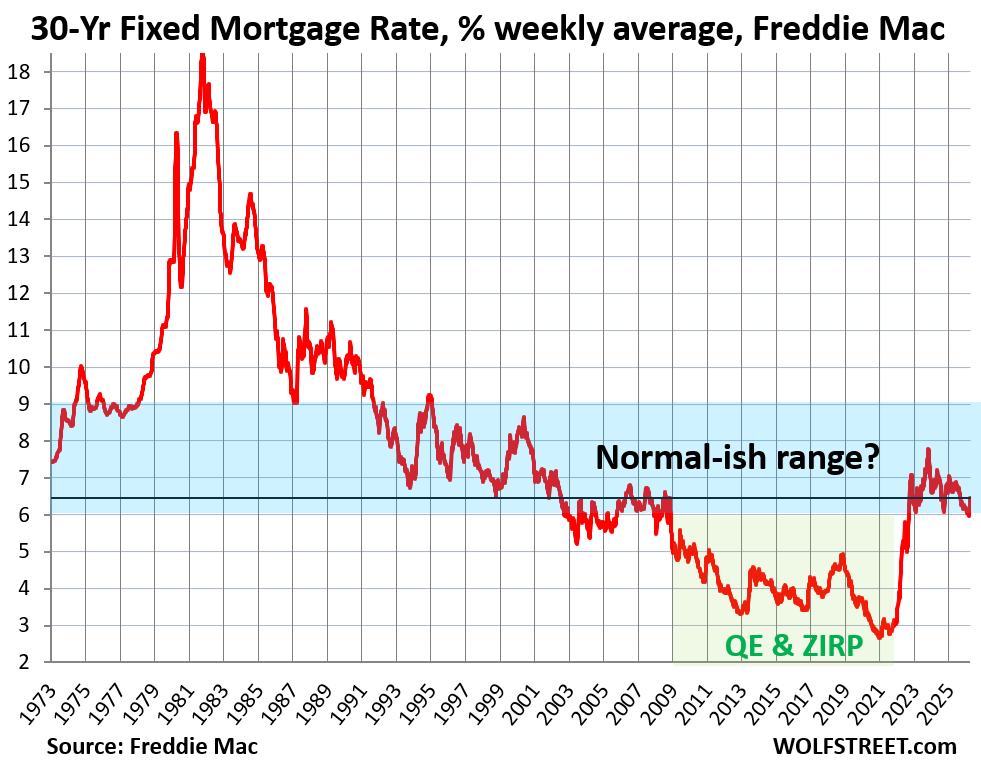

For example, and crucially, the average 30-year fixed mortgage rate, per Freddie Mac, has jumped by nearly 50 basis points since late February, to 6.46%.

Yields of corporate bond have jumped. The average yield of BBB-rated bonds, the low end of investment grade, jumped by 40 basis points since late February. Yields of BB-rated bonds, the high end of junk bonds, jumped by 60 basis points. Yields of B-rated junk bonds jumped by 80 basis points since late February (my cheat sheet for corporate credit ratings by ratings agency).

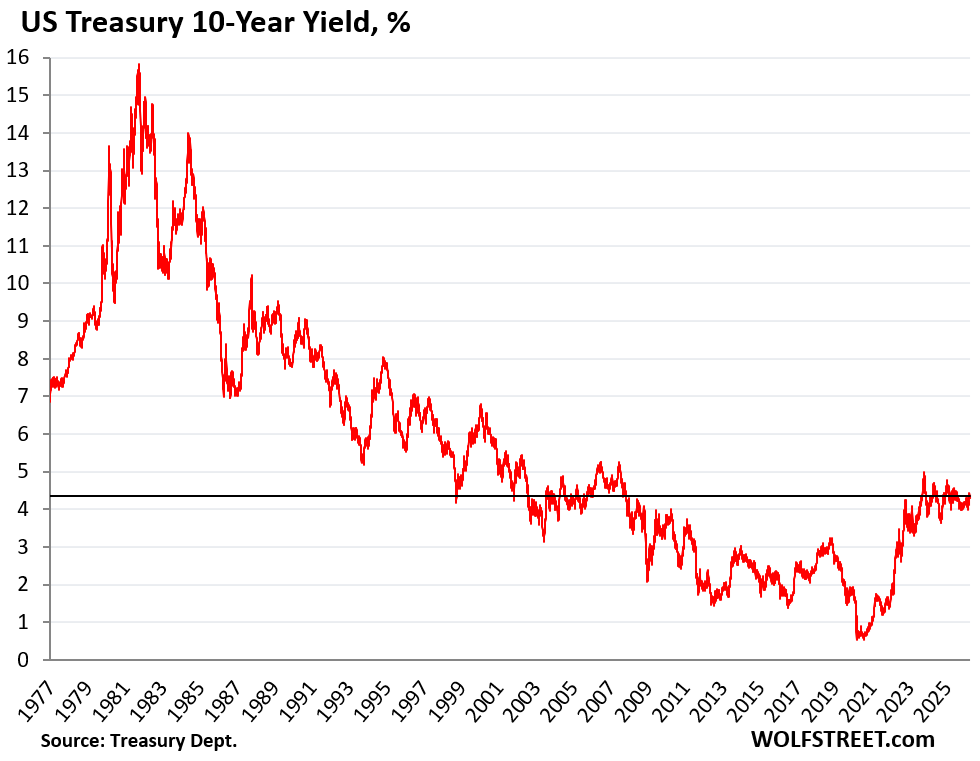

But Treasury yields are still relatively low in a historical context. It’s just that the years of QE and interest-rate repression by the Fed have distorted everything. And now there’s inflation, quite a bit of it, well above the Fed’s target, and once again accelerating. So for the Fed to be buying long-term Treasury securities to push down long-term yields is off the table.

The current 10-year Treasury yield is only about where it had been in 2007, before QE started, and it is much lower than in the decades before 2002.

The Dotcom Bubble and the accompanying big economic growth and very tight labor market occurred in the 1990s when the 10-year Treasury yield was mostly between 5% and 8%.

Bond prices rise when yields fall, and there was this magnificent 40-year bond bull market from 1981 through mid-2020, during which the 10-year yield zigzagged down from nearly 16% to 0.5%. But now there are inflationary pressures everywhere, and it’s a different ballgame than in 2008-2020.

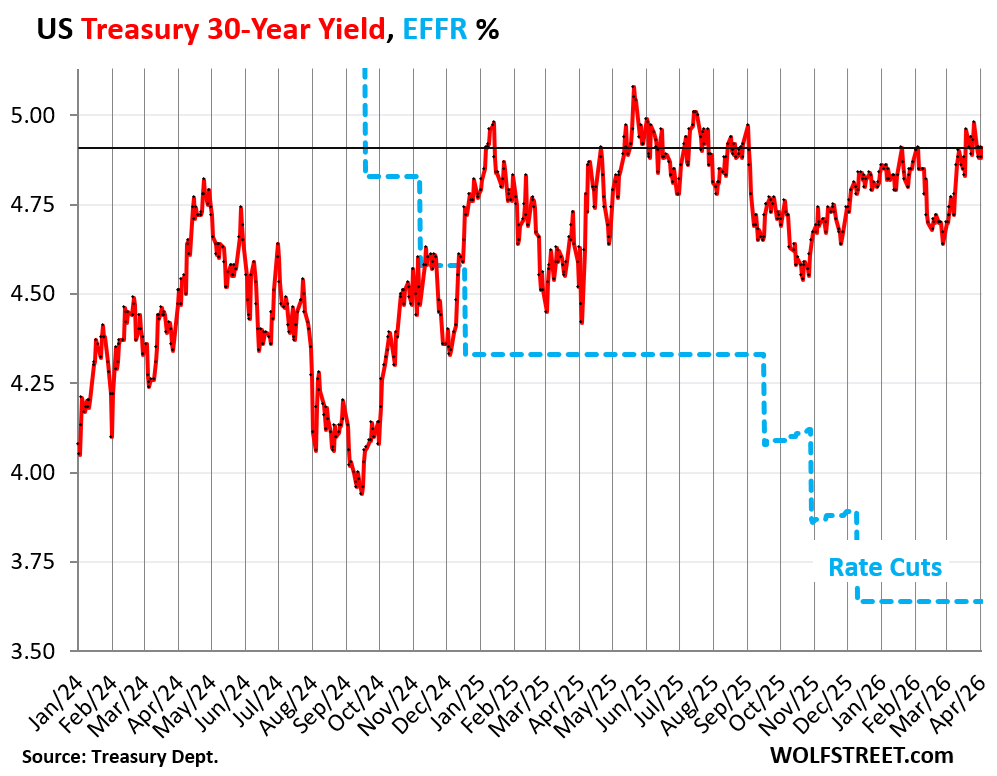

The 30-year Treasury yield rose by 3 basis points on Friday to 4.91%. It has been within a spitting distance of 5% since mid-March.

And it is higher now than it had been before the rate cuts even started in September 2024. The long-term bond market doesn’t care about rate cuts; in fact it worries about rate cuts if inflation still traipses around the economy, and the Fed is lax about it, or ignores it, or “sees through it.”

For holders of long-term paper, that’s a dreadful thought. They want a hawkish Fed that keeps inflation down with an iron fist. Reliably low inflation begets low long-term bond yields.

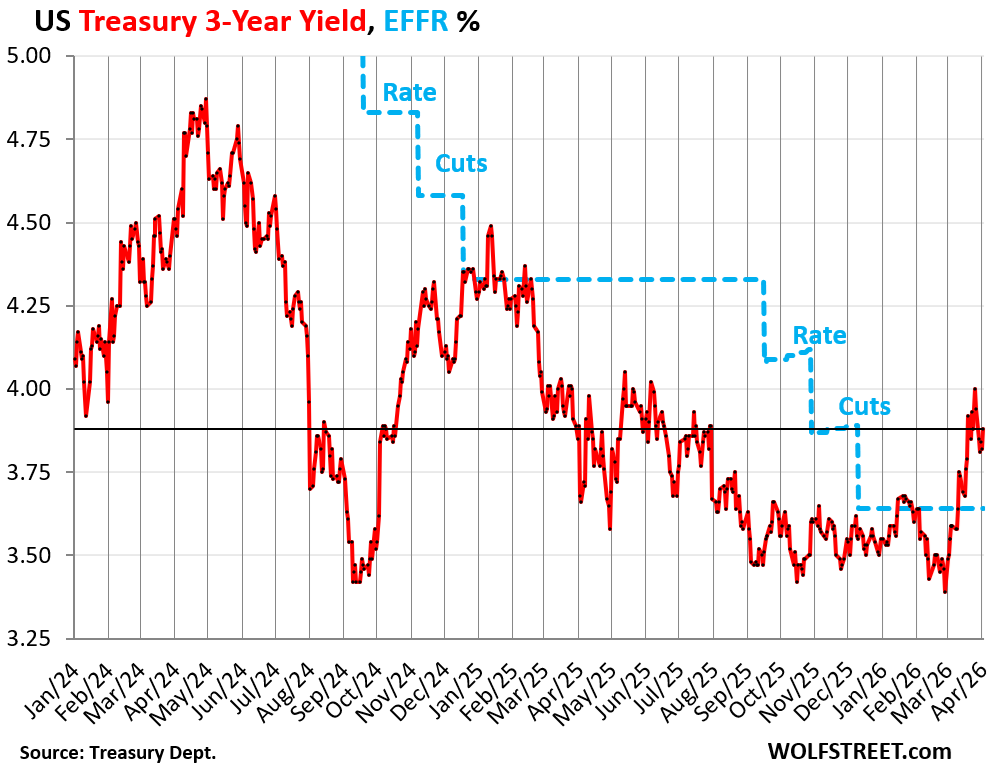

Yields from 1 year to 3 years had spiked in March as rate cuts were swept off the table, and a rate hike as the next move was put on the table.

The 3-year Treasury yield had spiked by 60 basis points in March through Friday last week, from 3.39%, when it was pricing in a rate cut, to 4.0% by Friday March 27, when it was pricing in a rate hike as the next move.

Over the first four days this week, it backpedaled 18 basis points. But on Friday April 3, it rose by 6 basis points and closed at 3.88%, so 20 basis points above the EFFR, and right where the EFFR had been before the last rate cut.

That end of the bond market is counting on a rate hike as the next move. And Friday’s jobs report on Friday gave it more confidence, after wobbling earlier in the week.

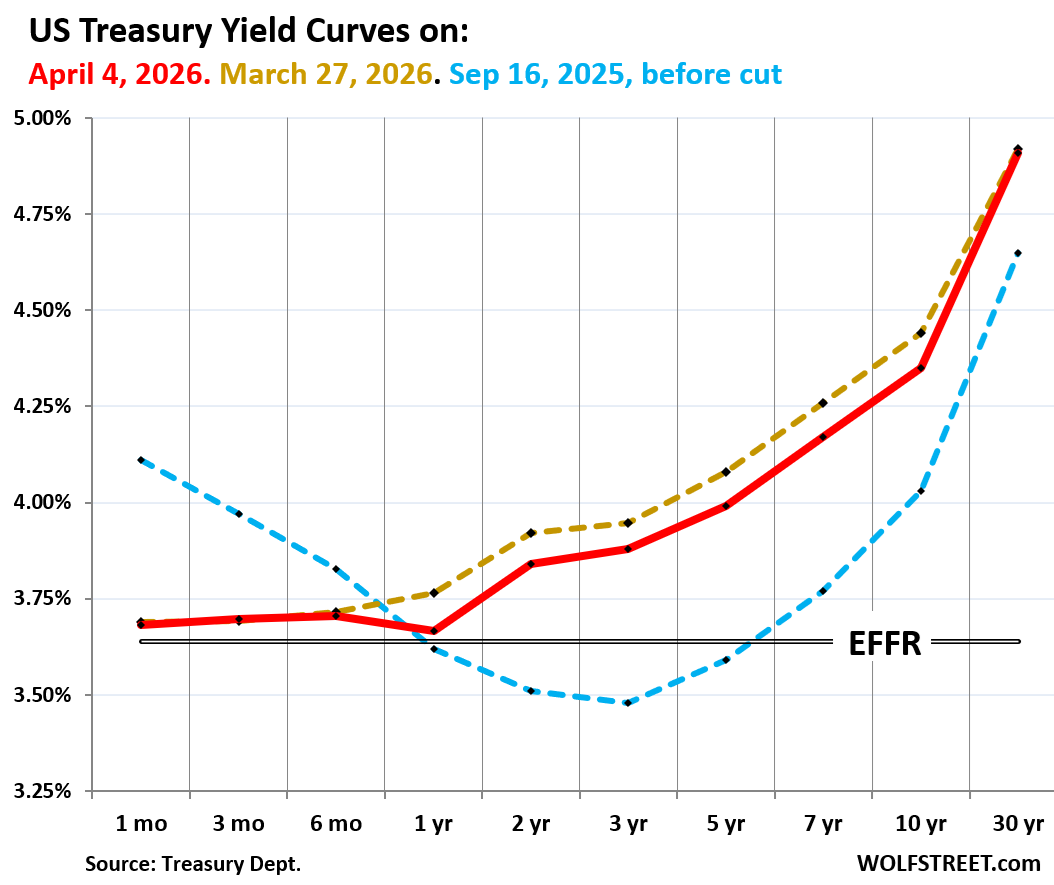

The Treasury yield curve.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates in 2025 and 2026:

- Red: Friday, Apri 3, 2026.

- Gold: March 27, 2026, near the recent high in yields.

- Blue: September 16, 2025, before the Fed’s first of three rate cuts in 2025.

In terms of the 1-year to 10-year yields, after the drop over the first four days, and the partial rebound on Friday, they ended the week a little lower than they had been a week earlier, on March 27. But all were higher than they’d been before the last three rate cuts, which started in September 2025.

The 30-year yield closed on Friday essentially unchanged from March 27.

And the 1-month through 6-month yields were roughly unchanged from March 27. They had been pushed down by the Fed’s rate cuts, and they don’t really move unless the Fed is expected to move in their window, which for the 6-month yields is up to about four to five months out. So that end of the bond market expects no move by the Fed over the next four to five months.

And since about mid-March, the entire yield curve has been above the EFFR (black double line), as the bond market gave up any rate-cut ambitions.

Mortgage rates follow. The real estate industry, which always wants low mortgage rates, needs to understand this: Instead of agitating for rate cuts, it needs to agitate for a hawkish Fed that cracks down on inflation. Low inflation and a hawkish Fed beget lower long-term Treasury yields, which beget lower mortgage rates. Rate cuts in face of accelerating inflation can be toxic for mortgage rates.

Since late February, the weekly measure by Freddie Mac of the average 30-year fixed mortgage rate has jumped by 48 basis points to 6.46%.

Outside of the period of QE and interest rate repression, mortgage rates are now roughly in the normal-ish range that prevailed before 2008, except for the period of very high inflation from the late 1970s through the late 1980s, when CPI topped out at just over 15%, and when mortgage rates topped out over 18%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I assume municipal bond yields track in a manner similar to that of the 10-year bond?

Why isn’t anyone discussing the derivatives market and how a 5 to 6 percent 10 year will light the fuse?

March CPI release is April 10th and the PPI is April 14th. Those reports are not going to be well received IMO.

Something like 40% of cpi is estimated. It’ll be fine.

U.S. 30‑year mortgage rates moving to around 7% is a real risk if upcoming CPI/PPI prints keep surprising to the upside, forcing the market to price stickier inflation on top of a swelling deficit driven by a much larger defense budget and Iran‑war outlays; that combination lifts term premia and pushes the 10‑year yield higher up toward 4.7–5.0%, while continued Fed MBS runoff and only modest relief from slower Treasury QT and April tax‑month flows leave private investors to digest heavy Treasury and agency supply, skewing mortgage risk upward rather than back toward the low‑6s.

How long will the Fed call the war inflation effects “transitory”?

Once again they will be slow to raise (but always quick to cut)

We need a hard rail monetary policy devoid of convenient subjectivities

(Taylor Rule for example)

I wouldn’t expect the Fed to tighten because of the war and ensuing inflation. What good would it do? Likely just slow the economy down (which isn’t exactly flying anyway, despite the claims of a certain administration), handing us stagflation. This upcoming inflation is not from an overheated economy/easy money, it’s simply from an elevated price of some important goods.

The danger is that it will once again unleash the inflationary mindset, as we saw in 2021; and when that happens, prices take off because companies are confident their customers will pay higher prices, and those customers pay them because they’re confident consumers will pay them, and consumers pay them because everyone is talking about higher prices, and then they ask their employers for bigger wage increases, and their employers will do that because they’re confident they can pass on those higher costs plus some to their customers…

Automation of monetary policy would prevent us from being in situations like where we are now, with a 2% jawboning target, >3% actual inflation, and a board full of dovish FOMC members talking about how uncertain it is what they should do.

Given how angry the mouth breathing public already is with the FOMC, imagine how mad they’d be if a computer raised the FFR to 5%, where it probably should be.

Wasn’t ‘Everybody’ hoping mortgage rates would go back down to 2 – 3%? Maybe it’ll happen when hell freezes over? High rates are what the housing market needs.

Because of prior manipulation every market in the U.S. needs higher rates.

Because of prior tax cuts, we’ll get higher rates.

I agree with your logical conclusion which happens to coincide with both religious and popular secular myth that Jesus needs to appear pronto

Wolf,

Are we not going to have Balance sheet articles on every First Thursday?

We cant say FED started QE after Dec 2025. But stopping QE and FED doing additional 40B Bills purchases have added more liquidity to Market. I understand they are doing it to manage the Reserves for Tax day prep.

But end result is FED Balance sheet has gone back to Jun-July 2025 level. So effectively FED has unwound 6 months of QT.

Only time will tell if FED and Powell has courage to wind down those reserves purchases for Tax Day OR as usual he will come up with some excuse to keep them on balance sheet.

Powell has stood up to Trump’s pressure. But his insistence of Abundant Reserves is one of the root cause of today’s problems (Higher inflation, All Asset Bubbles).

The banks don’t need an extra 40b of reserves every month to make loans to or buy securities from the nonbank public. Both increases in the Treasury General Fund Account and increases in currency won’t curb bank credit creation provided there are credit worthy borrowers.

The FEDs purchases are to stabilize interest rates. That being said the current situation paints a dire picture of future economic outcomes.

Banks don’t need all those reserves. But the repo market needs the banks to use their reserves to lend to the repo market during a period of liquidity drain (such as around quarterly tax days), and if the banks are tight on reserves, they don’t lend to the repo market, and it blows out, as it did in the fall of 2019. That’s the reason the Fed wants “ample reserves.”

Obviously, banks could get used to borrowing at the SRF to lend to the repo market, but there was no SRF in the fall of 2019. Then the Fed re-established the SRF in July 2021, but banks didn’t get set up to use it — they have to set it up with the Fed — and they had gotten out of the habit of using it, so it was rough in September 2025.

Reserves could shrink a lot more, but banks must relearn how to manage their liquidity and lend to the repo market with smaller reserves. The Fed’s Logan had a good piece on that last year. So that will take some time.

Powell is the architect of the ample reserves regime, and it will not change while he is there. Warsh will likely give it a second look when he takes over. But any change to a smaller balance sheet is going to be very slow – everyone agrees on that.

I am sure that tax cuts for Billionaires will be put forward as the cure for everything (sarcasm).

Here in the Retirement Village we have scheduled April 15th as a holiday in the rec room. Sure to be a boozy event. Hope it goes better than the last one (I went with 2 bottles of wine, and came home with four). How does that happen in the real world ?

Cue the Boomer jokes.

Somebody please poison the viagra. These guys are the worst.

Those T-bill purchases will slow in April and slow further in May to near nothing. The Fed already said that last week. This spurt into April was to get ready for Tax Day, which is a huge liquidity drain (running down reserves).

MBS are declining by about $14 billion a month, and are replaced by T-bills.

There is essentially nothing else happening on the balance sheet, and it’s not worth a monthly article. I last covered the balance sheet a month ago on Thursday March 5, and few people read it:

https://wolfstreet.com/2026/03/05/update-on-the-feds-balance-sheet-and-its-reserve-management-purchases/

Powell will eventually be replaced by Warsh, and all those things will be up for review when Warsh takes over. Miran has already come out for a smaller balance sheet recently. Last year before this started, others have come out for a smaller (“more efficient”) balance sheet as well, including Logan and Williams. So there is no telling what will happen in the second half of 2026.

If there is escalation and the war drags on we may see first, higher inflation then stagflation and later, recession.

I think any effort to super pump liquidity will probably backfire, this time.

I think the hawks/doves chart tells a very clear story of what happens in 2026 and beyond.

https://www.itcmarkets.com/hawk-dove-cheat-sheet-2/

A dovishly-biased FOMC keeps finding reasons not to raise rates. The latest is a transitory blip in oil prices that has to move through the system before they’ll trust the next inflation reading. Then maybe they add AI services to the CPI calculation just as the price of those services starts to follow the historical curve for televisions.

You’re talking about policy rates. I was talking about the balance sheet. Miran for example is a “dove” on your scale, but he wants a smaller balance sheet AND lower rates. Waller (dove on your scale) is open to a smaller balance sheet AND lower rates. Williams (dove on your scale) won’t move on rates for now, but may be comfortable with a smaller balance sheet. Etc.

Warsh has mentioned his wish for a lower balance sheet..

I propose that the current market structure while appearing stable is hardly that.

A repeat of the financial industry failing because of a fraudulent business model that relied on duplicity and avarice to thrive,

I’ll preface this with saying I consider myself a Doomer (even though I’m still maxing out the 401k) but it seems like we are almost in the perfect storm territory here:

The private credit (shadow banks) are cracking, no one knows how much exposure they have to the rest of the economy (afaik). There’s a chance this is the first domino that goes.

If the strait stays closed for the foreseeable future then we’ll see inflation kick off just about everywhere. Energy prices go up, food goes up, wallets start hurting. Layoffs start creeping up..

At this point the fed can’t lower rates both because inflation is raging and the cost of borrowing keeps going up. And we are stuck in a war we can’t win.

If gas prices stay up, and I think they will, some of the world is going to go into a recession, if not an outright depression. The bombing of Iraq is going to get a lot more painful, and inflation is going to be the leading indicator.

I can see scenarios where 30 years bonds head to 8-9%. Congress has to do it’s job and get a realistic budget.

Raising the federal funds rate to 5.0% by the Federal Reserve acts as a tightening monetary policy intended to curb high inflation by increasing borrowing costs for banks, consumers, and businesses. This action generally slows economic activity, cools hiring and spending, decreases demand, and can stabilize prices.

Kicking the can down the road has its consequences, I blame Powell and the rest of the team. Oil will complete the 3 legged stool experiment as it inflates its way to the moon. The fuel surge charge has already started with Amazon and other online giants. Never waste a good crisis. start looking for used EV prices to skyrocket.

Maybe The Bond Vigilantes are awakening after a long and extended sleep.

Only time will tell.

I think there’s a sense the US is still the cleanest dirty sheet in the laundry. I’m amazed the 10-year hasn’t gone up even higher.

In a world such as this one where the Fed balance sheet is morbidly obese would explain the boyant proclivity of a market that one would think would be collapsing under the weight of its own excess 0

There are many overseas holders of Treasury securities, such as sovereign wealth funds. I would particularly point to bond holders in the Middle East. If they need money because of the war, they may have to sell Treasury securities, as well as stocks, to raise cash to pay their bills. How long can the Gulf emirates go without revenue from oil? We will soon find out.

The amount of Treasuries held by Middle East countries is not big. The largest one, Saudi Arabia, holds only $134 billion, less than South Korea, and only 1.4% of all foreign-held Treasuries ($9 trillion).

Growing massive supply of unsold houses, get back to the office in effect, actual population decreases from deporting the line jumpers, tight borders, crackdowns on systemic government welfare frauds, increasing mortgage rates…

The suspense of a true housing bubble implosion is getting to me… :-)

“For example, and crucially, the average 30-year fixed mortgage rate, per Freddie Mac, has jumped by nearly 50 basis points since late February, to 6.46%.”

“

Be careful what you wish for. 1983 was a financial nightmare for many.

A non-naive view of the world would suggest, that just like the US stock market, the US bond market is manipulated “around the edges” by the US. Caymen Island accounts most likely.

However, just like the stock market, bond market manipulation can only go so far. A major sell off in either could not be stopped by the government.

Iran war may well be the final straw, as I do not believe the US will come out a clear victor.

I agree that the Iran war is a game changer and what I call a black swan event of epic proportions. Picking an unnecessary fight with the largest drone producer in the world was a spectacular blunder that will cost the american taxpayers dearly.

The US abandoned over 13 bases in the middle east in a matter of days becase they cannot be defended!!! Buckle up…

The interest rate structure of bond market I think is synthetic. The interest rate structure of the bond market leaves me earning less in interest while inflation that exceeds the official number which ravages the people

Net private saving: Households and institutions divided by the 2025 Federal Deficit has fallen to 2.392 from 2.629 in 2024.

With the supply of loanable funds decreasing while the demand for loanable funds has increased (e.g., Feb 2026 deficit: -307,501.43343) there is only one way for interest rates to go – up.

There is a strange connection to this news and it’s the manipulation and incompetence of Congress – the Fed – and the two corrupt political parties.

“with new investors needing to be enticed in, and that may take higher yields (and lower prices for existing bond holders).”

THANK YOU WOLF!!! Here I am, 70 years old…..and never understood the phrase “higher bond yields, mean lower bond prices”. That made absolutely no sense to me!!!! But now I get it!!!!

Higher yields on “new” bonds, makes the lower yields on “old” bonds less attractive…..and viola, less demand (lower prices) for old bonds!!!

Again, thank you!!!

It is absolutely amazing to me that investors are not ALREADY demanding higher yields on new debt considering the sorry state of US gov’t finances….and our nation’s inability to even come close to living within its means.

Fortunately, for us many other countries are financially in worse shape than we are. So these countries are willing to invest here. Thus rates here are not on the.moon yet. But the full story has not been told yet, either.

Long term averages for long interest rates tend to be in the 4-5% range. This is also in line with typical discount rates, implying that having $1 now is worth roughly twice as much as having $1 in 15-20 years.

So this about the neutral point. Obviously those rates can go significantly higher in times of high inflation or other uncertainty (having that $1 now becomes worth much more).

The Bond Market is getting “Yippy” ….. again.

It’s still a great time to sell a house. Prices are still high before the downswing.

Worst case scenario: Recession hits. Unemployment rises. Current homeowners stay locked in low rate mortgage and ride out a significant value decline. Owners not only suffer price drop but lack liquidity to capitalize on lower asset prices.

Markets get back in balance, but the owners’ advantage has been lost.

Wealth continually shifts.

The banks don’t need RMPs.

Charles Hugh Smith Blog | Bank Reserves And Loans: The Fed Is Pushing On A String | Talkmarkets

Banks don’t need all those reserves. But the repo market needs the banks to use their reserves to lend to the repo market during a period of liquidity drain (such as around quarterly tax days), and if the banks are tight on reserves, they don’t lend to the repo market, and it blows out, as it did in the fall of 2019. That’s the reason the Fed wants “ample reserves.”

Obviously, banks could get used to borrowing at the SRF to lend to the repo market, but there was no SRF in the fall of 2019. Then the Fed re-established the SRF in July 2021, but banks didn’t get set up to use it — they have to set it up with the Fed — and they had gotten out of the habit of using it, so it was rough in September 2025.

Reserves could shrink a lot more, but banks must relearn how to manage their liquidity and lend to the repo market with smaller reserves. The Fed’s Logan had a good piece on that last year. So that will take some time.

Powell is the architect of the ample reserves regime, and it will not change while he is there. Warsh will likely give it a second look when he takes over. But any change is going to be very slow – everyone agrees on that.

Wolf

Why cant the repo market (hedge funds and money markets i’m assuming) borrow from the SRF or discount window. ? It seems too complicated for repo to have to go through the banks like jumping through an extra hoop.

Only approved banks are allowed to borrow at the SRF. The Fed deals with banks, not with hedge funds, thankfully.

Isnt it true that the SRF is there to tamp down free market forces that on ocassion drive rates higher than desired?

IMO, the need for a mechanism like that is indication real rates are too low and the Fed policy is askew.

That’s nonsense. There is no free market for overnight interest rates, and there is not supposed to be. It’s the Fed’s job by definition to control overnight interest rates, and provide liquidity to the banks, and it has been ever since the Fed was established 113 years ago. When there was a free market for stuff like that, there was one financial panic after another. The Financial Panic of 1907 was why the Fed was created.

The liquidity drains are due to fund transfers from nonbank ownership to bank ownership which reduces the supply of loanable funds. Strains ease with the reverse of these operations.

But the 2019 repo spike was largely caused by raising the remuneration rate on interbank demand deposits. This Romulan cloaking device, the payment of interest on IBDDs, vastly exceeded the level of short-term interest rates which is still illegal per the FSRRA of 2006. I.e., the banks are able to outbid the nonbanks for loan funds – but not the other way around.

Remember Reg. Q Ceilings that gave nonbanks a 3/4 point interest rate differential in 1966 (the first “credit crunch”)?

30 year Treasury going over 5% tomorrow.

4.889%.

Close but not a winner.

In December I predicted the S&P would fall below 6000 again, mainly due to high tech valuations and the concentration of the index weightings. That was before the war of course, which I had not factored in. I thought 5500 was very possible, but I thought that 6000 was a lock at some point.

Now that energy costs are skyrocketing again and with the real possibility that the Fed may have to RAISE interest rates, I don’t see how stocks will NOT have a more severe downturn.

So in other words you were wrong… the S&P 500 averaged around 6850 for most of December 2025… and spent most of 2026 ABOVE that price level. Only the start of the conflict with Iran has managed to bring it down to Friday’s close of 6,583… nowhere even close to 6000… much less 5500.

I am curious… what do you do when you are wrong like that? Your last sentence seems to show that you double down on your previous wrong estimate of the future. Do you ever re-examine your assumptions? Try to figure out why they were wrong?

The reason that I am curious is that as I enter my 60s I have come to the conclusion that I have always been a Negative Nelly when it comes to the American economy. I am resolved to do better in the last 20 years of my life.

QUICK STORY…In my senior year in college (1988) one of my classmates was telling us that his father (a stock broker) was advising him to invest in some new company none of us had heard of call “Microsoft.” He wanted to listen to his father and invest his initial bonus check in it (we were all getting $10,000 signing checks from the military) but he was suspicious because “this company has already doubled in price since its IPO in 1986… how much further can it go up?” That $10k investment would be worth $35 million today.

I’m really tired of seeing posts like this throughout the internet. What he wrote had nothing to do with “being a negative nelly when it comes to the American economy.” The stock market has long ceased to have anything to do with the real economy. It’s become more of a barometer of whether rich people think the government is going to bail someone out.

You picked. Exactly the wrong time to turn positive. So it seems your track record of being wrong will continue into perpetuity

“That $10k investment would be worth $35 million today.”

Not for me. I would have sold it any an infinite number of points along the way! Such is the curse of being happy hitting singles.

Read my comment, I did not specify precisely WHEN the S&P would fall below 6000, only that I thought it was a “lock” to happen again.

The market began to roll over months before the Iran invasion and high gas prices.

I am not bearish, like many people (including Buffett) I am just waiting for a richly valued stock market to drop to a much more reasonable level.

From bottom to top:

1) ACE: I am afraid that is a bit of a dodge. We are trying to invest in the here and now… not listen to Nostradamus-like predictions that might eventually come true in the fullness of our civilization’s time on this Earth. After all, in contrast to your so-called “lock” there is another more normal way that the stock market can adjust to being overpriced… simply flatline for six months to a year. Happens all the time… far more often than a 20% price drop.

2) Gattaparado… good point. Wolf makes that same point from time to time about Bitcoin as well… he wouldn’t have made the magical returns we all know exist with hindsight because he would have sold out far before they were achieved. But the opposite is also true… for the next five years I could have watched Microsoft go up and up and up and still jumped on the gravy train with my $10,000 and been a millionaire by now… but my friend’s statement kept ringing in my ears… “how much further can it go up?”

3) JJ Stred: Literally nobody on this planet knows whether I have picked the wrong time to turn positive. Perhaps you are correct and perhaps I am. My point is that after 40 years of listening to the naysayers of the American economy perhaps I should look at it from a different angle. In the late 1980s all the talk was about how the Japanese were going to dominate the global economy… for over the past decade (some of those same) naysayers have been claiming it is the Chinese economy which will dethrone American dominance. They have been DEMONSTRABLY wrong for 35 years…

What might the different angle be… well American managers are the best in the world… not held back from course corrections by multi-year plans imposed by government policies or cultural concerns… operating in a low-tax environment with secure borders provided by massive oceans and friendly neighbors. Due to how they themselves are compensated they tend to manage companies for stock price growth rather than dividend growth, market share growth, or any other metric. Based on THAT angle, how rational is the belief that the stock market is always one day away from a massive plunge?

4) TSonder305: NEITHER of Mr. Ace’s comments takes the viewpoint that you do (I realize that he wrote his second one after your post). The idea that the stock market is little more than “a barometer of whether rich people think the government is going to bail someone out” is a pony that YOU want to ride… not him and not me. FEEL FREE to do so!!! I don’t mind how you invest your own money (or what assumptions you make while doing so).

I will give you this advice though… if it doesn’t work out the way you think it will… don’t be like me and wait 30 years to re-examine your assumptions. After all, how often are rich people wrong about the stock market… or bailouts for that matter!!!

To some extent, the blowout federal deficit creates the currency needed to buy the massive amounts of treasuries that need to be issued to cover it. This is the MMT-adjacent explanation for why interest rates haven’t already gone to the moon. The more money the government prints, the more money somebody has that must find a home.

One snag would be if people decided some of the money they received from government contracts and tax cuts should go into something else than treasuries, such as other currencies.

I know this is OT but following up on previous Medicare discussion…

April 6 (Reuters) – The U.S. has finalized an average rate increase of 2.48% in payments next year, compared with the near flat proposal in January, to private insurers for the Medicare Advantage plans they manage for older adults, the government website said on Monday.

Considering how much healthcare costs have jumped, it’s a small increase.

Wolf, wondering if you believe that a more hawkish fed can have a significant reducing effect on inflation these days, given where deficit and debt are.

As I said in the article, and as other mentioned here in the comments, the Fed is not really trying to get inflation down to 2% because the debt is ballooning so fast and is so big. That’s the job of Congress, but Congress is just handing out more money and making the debt worse. So “Let it run hot” seems to be the mantra. The Fed talks 2% but is obviously comfortable with core PCE at 3% (where it is right now), and won’t hike if core PCE inflation stays around 3%. If core PCE inflation heads to 4%, the Fed might get nervous and start hiking again so that it doesn’t go over 5%. Or maybe it’ll wait too long again. Obviously, the Fed can never admit that, it’ll be talking about getting back to 2% while feeling comfortable at 3%-plus. But with core PCE at or above 3%, it won’t cut rates either. That’s what I mean by “comfortable” – not hiking, not cutting.