Quantitative Tightening so far has removed 41% of Treasury securities and 29% of MBS that pandemic QE had added.

By Wolf Richter for WOLF STREET.

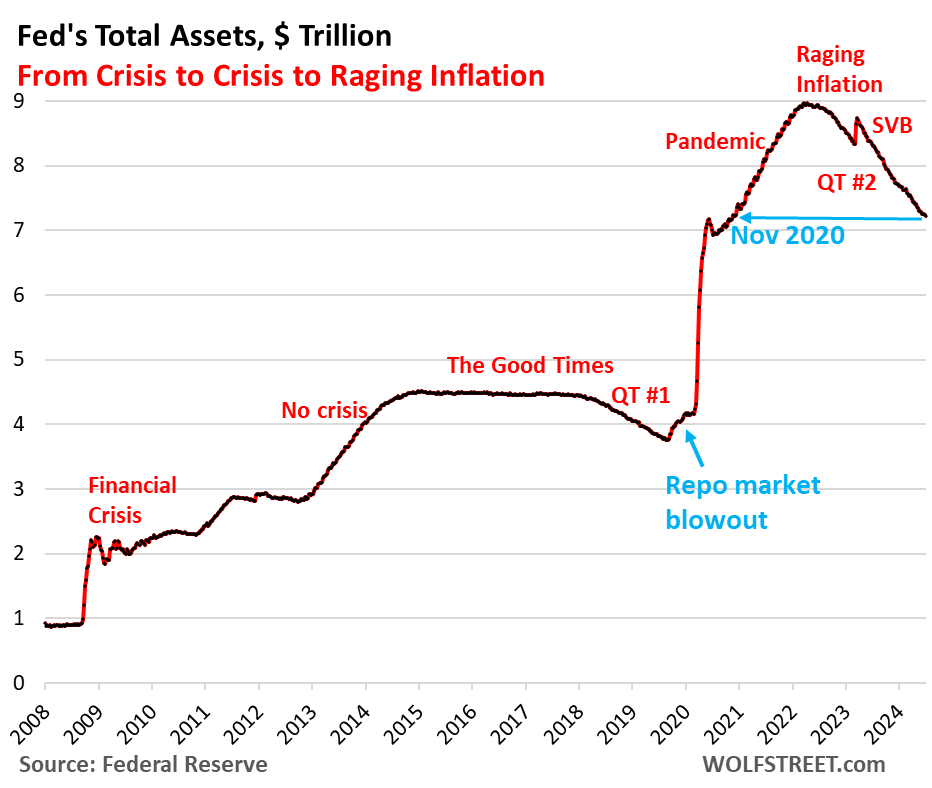

Total assets on the Fed’s balance sheet dropped by $34 billion in June, to $7.22 trillion, the lowest since November 2020, according to the Fed’s weekly balance sheet today. Since the end of QE in April 2022, the Fed has shed $1.74 trillion.

At its FOMC meeting in May, the Fed outlined how it will slow QT in order to get the balance sheet down as far as possible without blowing anything up, by slowly approaching the unknown level below which liquidity is too low, to avoid another debacle, such as the repo market blowout in September 2019 that caused the Fed to undo a big part of QT-1 (blue in the chart above).

June was the first month at the new pace of QT that reduces the cap for the Treasury runoff to $25 billion a month, but removes the cap for the MBS runoff, and whatever MBS come off, will just come off; any amount over $35 billion will be reinvested in Treasury securities, in line with the plan to get rid of MBS entirely over the “longer term.”

QT by category.

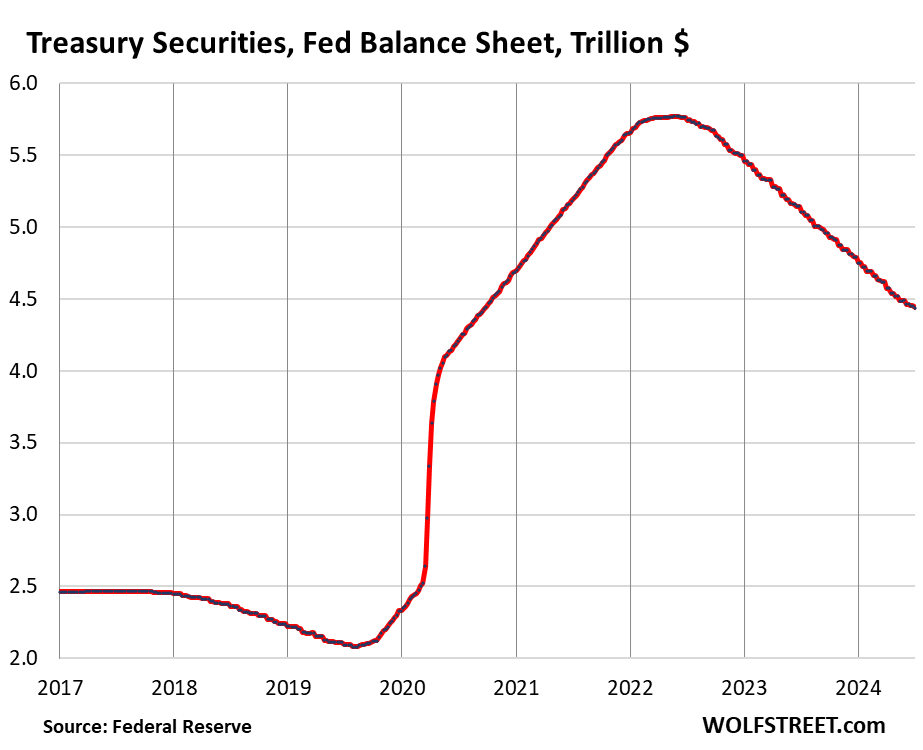

Treasury securities: -$23 billion in June, -$1.33 trillion from peak in June 2022, to $4.38 trillion, the lowest since September 2020.

The Fed has now shed 41% of the $3.27 trillion in Treasury securities that it had added during pandemic QE.

Treasury notes (2- to 10-year) and Treasury bonds (20- & 30-year) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. The roll-off is now capped at $25 billion per month, and about that much rolled off in June, minus the inflation protection the Fed earns on Treasury Inflation Protected Securities (TIPS) which is added to the principal of the TIPS.

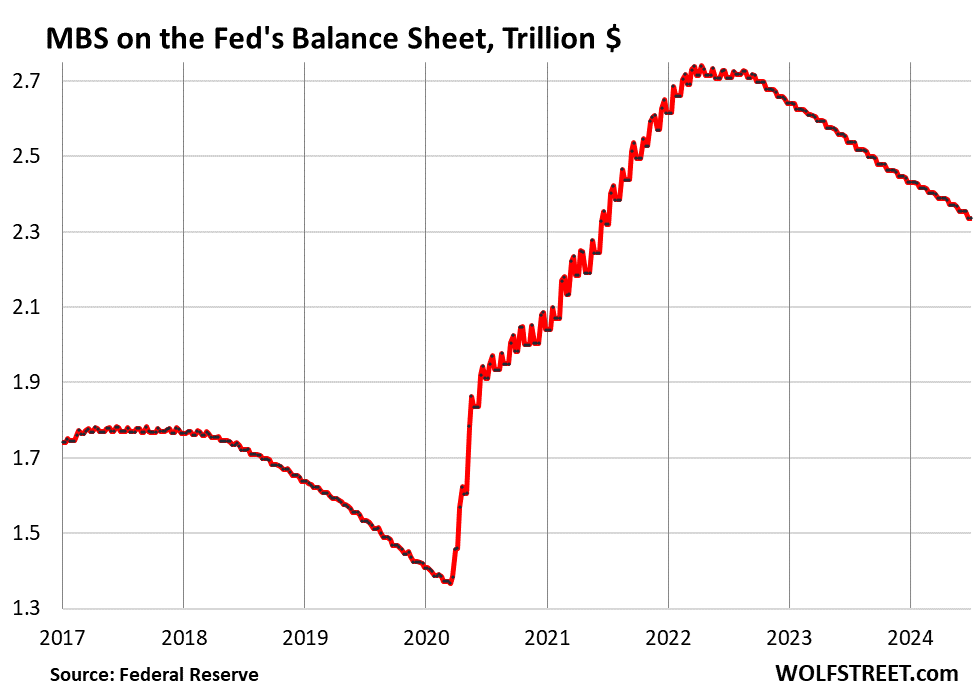

Mortgage-Backed Securities (MBS): -$19 billion in June, -$404 billion from the peak, to $2.34 trillion, the lowest since July 2021. The Fed has shed 29% of the MBS it had added during pandemic QE.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made. But sales of existing homes have plunged, and mortgage refinancing has collapsed, and so fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have been reduced to a trickle. As a result, MBS have come off the balance sheet at a pace that has been below $20 billion in most months.

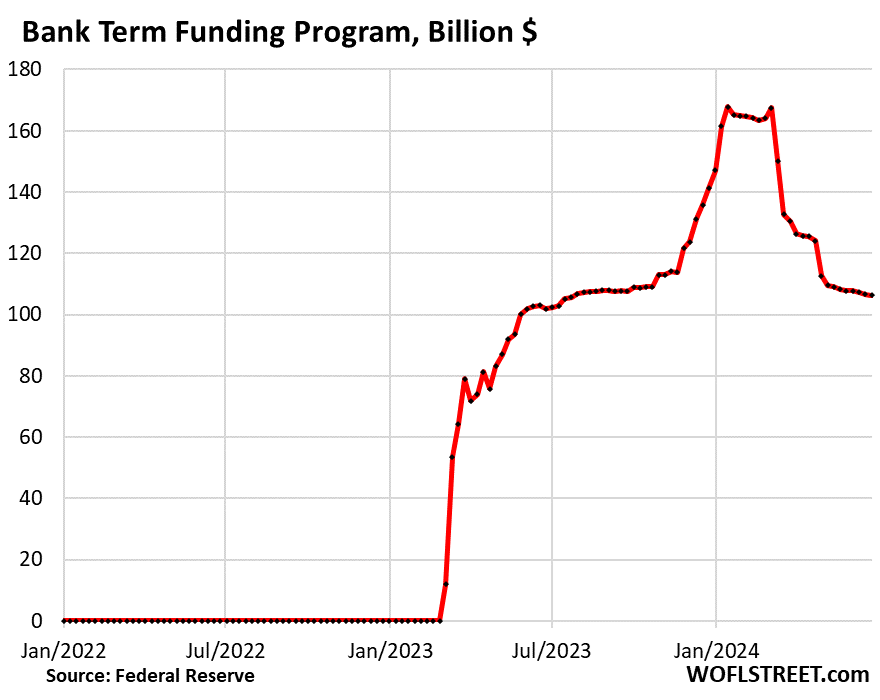

Bank liquidity facilities.

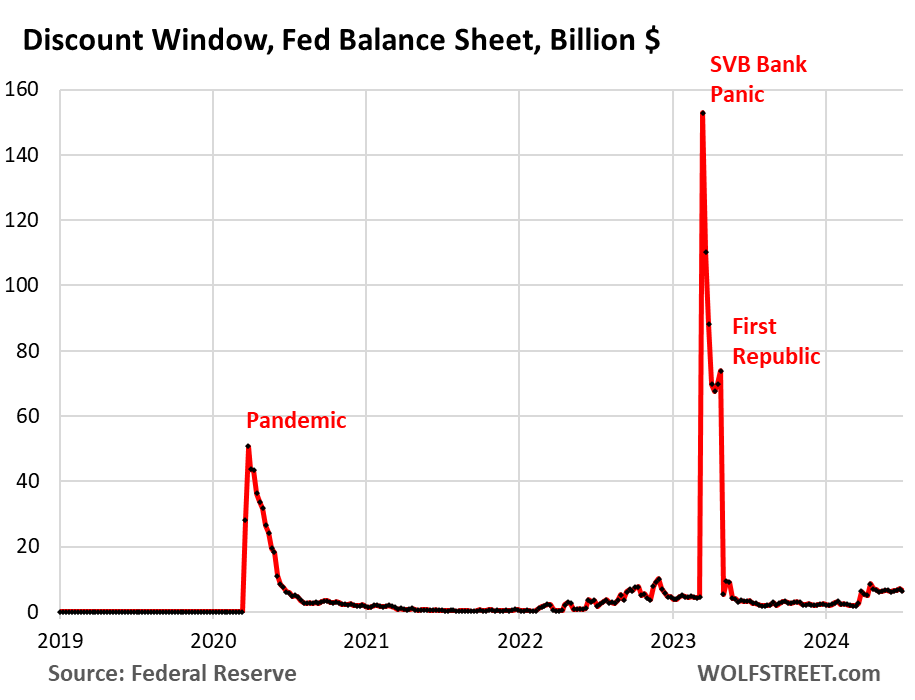

Only two bank liquidity facilities currently show a balance: The Discount Window and the Bank Term Funding Program (BTFP). The other bank liquidity facilities — Central Bank Liquidity Swaps, Repos, and Loans to the FDIC — are either at zero or near zero.

Discount Window: +$200 million in June, to $6.4 billion. During the bank panic in March 2023, loans had spiked to $153 billion.

The Discount Window is the Fed’s classic liquidity supply to banks. The Fed currently charges banks 5.5% in interest on these loans – one of its five policy rates – and demands collateral at market value, which is expensive money for banks. In addition, there’s a stigma attached to borrowing at the Discount Window. So banks don’t use this facility unless they need to, though the Fed has been exhorting them to make more regular use of it.

Bank Term Funding Program (BTFP): -$1.6 billion in June, to $106 billion.

The BTFP had a fatal flaw when it was cobbled together over a panicky weekend in March 2023 after SVB had failed: Its rate was based on a market rate. When Rate-Cut Mania kicked off in November 2023, market rates plunged even as the Fed held its policy rates steady, including the 5.4% it pays banks on reserves. Some banks then used the BTFP for arbitrage profits, borrowing at the BTFP at a lower market rate and then leaving the cash in their reserve account at the Fed to earn 5.4%. This arbitrage caused the BTFP balances to spike to $168 billion. The Fed shut down the arbitrage in January by changing the rate. It also let the BTFP expire on March 11, 2024. Loans that were taken out before that date can still be carried for a year from when they were taken out. By March 11, 2025, the BTFP will be zero.

So over the next 8 months, the BTFP will remove another $106 billion from the balance sheet, on top of regular QT.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Very interesting as always. The MBS rolloff has picked up a bit of speed – was at $15-17B monthly, now at $19B. Could be the beginnings of more home sales as the UE rate has started to tick up. When the MBS balance is dropping $35B or more a month that will be an indicator that the worm has turned and houses are being sold for today’s prices and today’s reasons. Job loss or change has always been a big reason to sell a house.

I’d love to see the MBS roll off with 1.5% of all homes in foreclosure.

The real question, though, is when do RRPs go to zero? Supposedly, the Treasury plans borrow $700B before the end of FY 2024. As of 7/5, $390B was remaining. Let’s see how quickly that gets gobbled up.

I for one want to see RRPs gone, so we can see what happens without that liquidity in the market to buy treasuries.

If the Federal Reserve sold all of its assets and ceased to exist completely, would that make even the slightest bit of difference?

It wouldn’t if you live in the jungle and don’t see anything else. Just a guess though.

My guess is it wouldn’t matter if no one knew. But since they do, it would result in chaos.

Have the “it wouldn’t matter” crowd read ANY history of banking and central banking? Seems not. All kinds of things have been tried, and have crashed in various ways. That doesn’t mean, in a world emerging new every day, things aren’t “being tried.” But a system this vast and complex doesn’t run itself agreeably across large populations. But I know it seems smart and powerful to sound snarky. Any 6-year-old can do that.

phleep: in the words of Charlie Munger: “I have nothing to add”.

I will jump in hear.

The teeter totter or seesaw has a spring mechanism in the center that helps control the motion.

The teeter totter, like our economy goes up and down, that’s what they do… but It doesn’t spit out money

But the feds teeter totter also spits out money.

The feds seesaw is broken, it has one side stuck in the air, and the other side lying on the ground in a pile of money… the mechanism has been tampered with…it’s quite sad.

The feds mandate, don’t screw up the mechanism.

Yes, the simple act of seeking bids for the securities would tank the UST market and lead to a melt down. So, that is not a real scenario — ever.

But the graphs here highlighted how pathetically small the Fed’s QT action has been when put in perspective of total Fed assets, as opposed to only Govt Securities. And the MBS run off looks to be a 10 year glide path? To paraphrase Jerry Seinfeld: “they know how to take the bonds, just not how to unload the bonds. . .”

It probably wouldn’t matter for a short while, until some random bank somewhere ran into some liquidity issues and experienced a bank run. The bank may or not survive, but it would cause a panic at other banks causing liquidity crises throughout the system.

The only question would be how many of those banks could survive their liquidity issues. If most could it probably would sick but not be too big of a deal. If many couldn’t, there would be a massive recession as lots of banks go under.

As the lender of last resort, the FED isn’t important until it is. It is like insurance. It’s value is not realized until it is desperately needed.

Just let the bad banks go bust and be done with them, especially those who bought 30 year US government Treasuries.

That’s what they did in 1930. Worked out great for the American people.

“especially those who bought 30 year US government Treasuries”

The problem with this view is the Fed *wants* banks to buy 30 year treasuries – they shouldn’t be discouraging it.

With the Fed’s upcoming changes to the PCF, they’ll be encouraging banks to pledge more collateral (treasuries and other AAA debt) to borrow against at the DW. Ergo, banks will need to own more treasuries.

banks owning a lot of long-term treasuries caused some of those banks to fail in 2023. Why would the fed “want” that?

That’s what the entire world needs to do not just America. We don’t need to promote socialism or communism.

Grant,

Because the Fed wants banks to have sufficient collateral on hand to use for a loan at the discount window.

Bank runs are bad.

Supply and demand principles would apply. Higher interest rates and lower prices.

When you say “sold all of its assets” you realize you’re talking about $7 TRILLION, right? And all of those funds right now are providing a combination of liquidity and stability to our financial institutions?

Now I’ll be the first to argue that the Fed’s actions in 2020-2023 were too heavy-handed, and they moved too slowly to try to address the inflationary bubble they caused by excessive QE. But saying they did “too much” or “too little” is a completely different thing than saying the Fed doesn’t play an important role in helping buffer shocks to our financial system.

Comments down below 👇:

😏 🏆

Wall Street analysts are widely expecting QT to end by mid-2025, under the base case scenario (no/soft landing, no serious downturn.)

That would take the balance sheet down to $6.6-6.7 trillion, including treasury & MBS rolloff at the current pace, plus the scheduled end of the Bank Term Funding Program.

Wolf said under the current balance sheet regime, the absolute floor is between $5 to 6 trillion. Of course, there will be a buffer of at least a few hundred billion to prevent something breaking.

Wall Street is salivating for the day when QT ends.

There are lots of Wall Street analysts. They all do not share the same opinion.

FRED’s data for Fed MBS holdings (symbol: WMBSEC) reports that the Fed’s pre-Covid MBS holdings on 3/18/20 was 1,370,430 millions.

The Fed’s MBS inventory then surged and peaked on 3/23/22 at 2,737,626 millions — a 100% percent increase, a compound annual growth rate of 41%.

In the 2.3 years since 3/23/22, the Fed’s MBS holdings have decreased from 2,737,626 to 2,335,997 (as of 7/3/24) — a shrink rate of only -6.72% per annum, a percent decline by my calculation of only -14.7%, not 29%, as you report.

What numbers & dates are you using to arrive at your statement that “The Fed has shed 29% of the MBS it had added during pandemic QE” ?

What’s the FRED symbol for the data you’re referencing?

1. I download the data from federalreserve.gov, not FRED. But the data is the same because FRED gets it from federalreserve.gov.

2. Pandemic QE with MBS was $1,373 billion.

From Mar 18, 2020, balance: $1,367 billion

To April 13, 2022, balance: $2,740 billion

$2,740 – $1,367 = $1,373 billion = pandemic QE with MBS

MBS QT = $404 billion = 29.4% of $1,373 billion.

IMHO, tracking MBS run off is pointless. What matters is will the Fed keep mucking with mortgage rates by investing in MBS? As layman, if I could list my top 3 things that have caused everything to get out of whack, these would be them:

1. Rent & mortgage relief

2. The Fed purchasing MBS, starting back in 2008.

3. The Fed purchasing treasuries with maturities longer than 7 years.

4. QE

The CDC knew by April 2020 that the general population COVID IFR was .5%, so there was this massive overreaction, including rent & mortgage relief, shutting down the economy, etc, and the Fed’s near zero ZIRP that was held in place WAY TOO LONG. The FFR should not have dipped below 1% and should have started to rise within 3-4 months of being cut based on significant rebounding economic activity by summer 2020.

In addition, the Fed has no business manipulating the longer end of the yield curve, 10Y+. They should be statuary barred from doing so. It’s downright criminal that they’re allowed to create these enormous asset bubbles that are causing ever increased wealth disparities.

QE needs to have limits placed on it. At some point, the Fed, as the bank of the USA, has to look down the barrel and just start to say NO to Congress in terms of lending so profusely. With structural deficits approaching $2T for the foreseeable future in a GROWING economy, the credit agencies need to step in and start downgrading our debt.

Just like nuclear fusion has gotten over the hump of always being 30 years out, our exploding debt isn’t a 2050 issue. Exploding interest expense & entitlements are going to be an issue by 2030, when the SSTF will move forward from its current 2033 red date. And we will most certainly have a recession in the next six years, ensuing more debt it dumped onto the pile. Steps need to be taken to limit the Fed’s ability to pump trillions of inflation producing dollars into the system.

GW – mebbe they’re anticipating the offsets provided by fusion’s effect on energy markets and think that will cover them? (/s).

may we all find a better day.

I agree. From a quick search, the Fed board of governors are nominated by the President and confirmed by the Senate. I believe as others that the President and Senate to some extent act in the interests of their campaign donors by installing Fed leadership that will effect monetary policy they believe is beneficial to their donors and lobbies but maybe not for the aggregate prosperity and stability of the country. So it seems that campaign finance and lobbying reform would be a good place to start. Also, education for all about the workings of the system, the risks of the debt and how it is and has been dealt with might lead more to support candidates and reps committed to prudent responsible policy through the challenges of achieving it.

Presidents tend to (rightfully) lose their jobs when inflation gets out of hand. Americans HATE HATE HATE inflation, even though economists are telling them that inflation is good for them, LOL. The ravages of inflation, once inflation takes off, and then the fear of inflation returning, are what keeps central banks in check. But the US (and other economies as well) had stopped fearing inflation by 2008 because there hadn’t been much inflation in decades. And so they went haywire. But now inflation is a thing. So we have 5.5% and QT instead of 0% and QE. And lots of rich people have already gotten a lot less rich because their investments in CRE are getting wiped out and bonds got hit hard and a bunch of stocks have collapsed or are way down, etc. And the Fed has been looking on with a smile.

Tbv3

Luckily you gave some details of your calculations and of course easy to get things wrong with txts. You are quoting total MBS drop and Wolf clearly stated the percent drop is on the Covid portion . Different denominator values

Succinct and to the point; very easy to follow.

Removing the MBS cap of $35 billion when the actual flow is $20 billion makes one wonder what sort of mathematics is taught on the business side of the campus, because it is nothing like the engineering curriculum. Fixing the Federal Reserve’s balance sheet “over the longer term” may want to get some help from the Quantum Physics educated or maybe Theology for the meaning of eternity.

You’re being silly, I guess. The average mortgage gets paid off in seven years, at which point the Fed gets the pass-through principal payments, and the MBS come off the balance sheet. The Fed bought fewer MBS in early 2022 and stopped buying MBS in Sept. 2022. So all the MBS on its books are now at least 22 months old. Most of them are older. The Fed bought a huge amount in 2020 and 2021. Those are now 3-4 years old. With the average mortgage having a lifespan of about 7 years, that big QE bulge will start to come off in big numbers in 2027 and 2028. In addition, when the pool of mortgages in an MBS pool gets small enough, the MBS get called by the issuer, and the holder gets paid face value — and Fed’s MBS then come off the balance sheet — and the issuer repackages the remaining mortgages into new MBS and sells them to other investors. So most of the MBS will be off the balance sheet in seven years.

7 years may sound long. But the Fed started buying MBS in 2009.

Wolf, 7 years was fair before QT but it’s a dynamic, not stationary, value. I would look for 10 years or more for 2020/2010 vintage mortgages because refinance and upgrade will be less likely for that cohort.

@Cervantes – I agree. Too many lust or need to keep a 3% mortgage, so until rates drop (if they ever do) it is probably more like 10 to 12 years.

The capitalization of the largest 3 NASDAQ stocks alone is now more than $12 TRILLION and that’s leaving aside the ‘worth’ of all of the other 7,000 or so US stocks and the rest of the assets in the US including all real estate. So where’s the money supposed to come from if hardly anyone wants to see any of these assets and get paid actual money for them?

What’s a couple of trillions among friends! $10 trillion, $12 trillion, who cares, same thing, it’s all just trillions.

What are these trillions based on? Think air? Hype? Speculation? Wishful ‘thinking?’ Utter BS???

It’s based on what the marginal buyer is willing to pay, so those trillions could evaporate very quickly if momentum slows, even a small amount. Momentum can slow, even while prices are rising.

The greater fool theory?

See NASDAQ, March 27, 2000.

Unless the asset is crypto crap (which is not intrinsically worth Thin Air), they all have underlying sellable assets. Now the value of a lot of those assets could head south in stormy weather, which will eventually come.

Time to prepare…

Black Limo pulls up:

“Pardon me sir, could I trouble you for some grey pou Trillion?”

No chance that cap doesn’t come back.

1) If the Fed will cut rates wealthy people will park their capital in promising companies instead of the gov roach motel. Gov % cost will drop. The Dow might reach 42K, before 50K.

2) Demand for nurses is high. Within a few years new factories will be completed. Demand for highly skilled workers will rise. They will fill the gov coffer. If the gov size will not rise and it will cut taxes and regulations the budget deficit will turn green. With its surplus debt will fall.

3) For those who earn more in real terms tariffs don’t matter. This summer youth unemployment is rising bc the 16/19 and the 20/24 compete with new immigrants. For those who pay rent the CPI is higher than wages. Demand for mascara and women’s perfume is falling. If companies will earn more they will raise low end workers

salaries as well. All workers, the highly skilled and the low end workers, will earn more money. If saving will rise inflation will fall. The gov will cut its debt.

4) The risk : congress will vote for more spending on pet projects.

#4: p >.999999 ?

Plan accordingly..

I am missing something. You posted Treasury securities: -$23 billion, Mortgage-Backed Securities (MBS): -$19 billion, and Bank Term Funding Program (BTFP): -$1.6 billion but Total assets on the Fed’s balance sheet dropped by $34 billion in June. Shouldn’t the drop be $43 billion?

What you’re missing is the rest of the balance sheet that doesn’t have anything to do with QE/QT, and so I don’t get into these items. For example, in June, there was $6 billion in “accrued interest” added to assets. This is interest the Fed earned in June from its securities but that it will get paid later, which is when this accrued interest is deducted from assets (reduces assets). In May, the Fed got paid interest and it removed $10 billion in accrued interest, and asset fell by that much more. So in June, it went into the opposite direction, but less. When the Fed gets paid interest, it destroys the money (central banks create and destroy money as a matter of routine; they don’t have a cash account, like companies do).

Monetary policy objectives should be formulated in terms of desired rates-of-change, RoC’s, in monetary flows, M*Vt [volume X’s velocity], relative to RoC’s in R-gDp. There is evidence to prove that rates-of-change [roc’s] in nominal-gDp can serve as a proxy figure for [roc’s] in all transactions. But rates-of-change in real-gDp have to be used as the policy standard.

The FED should hold the line so as to cause disinflation. I doubt that they will. They will cut before the election.

It’s like 2007. If the FED cuts rates, then stocks will rise even given a deceleration in the economy. If the FED holds steady, then downward pressure is exerted.

Stocks plunged 50% from 2007 through March 2009.

Stocks rose conterminously in response to the FED cutting rates. Then they fell.

As I said: ) The rate-of-change in the proxy for real-gdp (monetary flows MVt) peaks in July. The rate change in the proxy for inflation (monetary flows MVt) peaks in July. Therefore it should be obvious: interest rates peak in July.

Because interest rates top in July, the exchange value of the dollar should resume it’s decline. A very good time to buy gold!

The “Holy Grail” has no disclaimer.

posted by flow5 at 7:50 AM on 06/29/07

I got the downswing and the bottom in March.

We knew the precise “Minskey Moment” of the GFC:

AS I POSTED: Dec 13 2007 06:55 PM |

The Commerce Department said retail sales in Oct 2007 increased by 1.2% over Oct 2006, & up a huge 6.3% from Nov 2006.

10/1/2007,,,,,,,-0.47 * temporary bottom

11/1/2007,,,,,,, 0.14

12/1/2007,,,,,,, 0.44

01/1/2008,,,,,,, 0.59

02/1/2008,,,,,,, 0.45

03/1/2008,,,,,,, 0.06

04/1/2008,,,,,,, 0.04

05/1/2008,,,,,,, 0.09

06/1/2008,,,,,,, 0.20

07/1/2008,,,,,,, 0.32 peak

08/1/2008,,,,,,, 0.15

09/1/2008,,,,,,, 0.00

10/1/2008,,,,,, -0.20 * possible recession

11/1/2008,,,,,, -0.10 * possible recession

12/1/2008,,,,,,, 0.10 * possible recession

RoC trajectory as predicted

You’re funny. The financial crisis was already in full swing in 2006 and smaller mortgage lenders were starting to fail. By 2007, hedge funds were imploding. The financial system was obviously going to hell for all to see, well before the Fed cut rates, and before the market peaked. The market was delusional and didn’t see it until Nov 2007.

Retail sales increases were in big part driven by the price of gasoline, which doubled from early 2007 till mid-2008, as WTI soared and ultimately hit $150. Then in July 2008, WTI began to collapse, and gasoline prices began to fall hard, ultimately plunged by 60%, and this is a big impact on retail sales. We constantly talk about gasoline retail sales and gasoline prices.

That was the only recession call I made in the 2000’s.

Rate cuts prophesized. Stocks up.

Stock prices tend to fall when the Fed cuts rates, because the Fed cuts rates in response to economic weakness.

The MBS on the Fed´s balance sheet are problem, and the strategy “hold until maturity” is the wrong way. In my view, the trading desk had sold the MBS shortly after they buy them, and the best time point was after the worst of the pandemic was over. The whole QE after the pandemic was far too much and far too long, and the Fed missed the exit.

For example, the Fed could transform the 35 billion cap into 35 billion sales per month. These would bring down the MBS holdings more quickly, and give the Fed the room to expand their treasury and bill holdings which is necessary to hold interest payments for the government on a “acceptable level.”

No one, not even the Fed, can hold MBS “till maturity” because they vanish bit by bit through passthrough principal payments long before they mature, which occurs when the underlying mortgages are paid off (sale or refi) and when mortgage payments are made, and each passthrough principal payment reduces the Fed’s balance of MBS, and when the underlying pool of mortgages gets down to a certain point, the MBS are called at face value and are gone entirely.

I don’t view this reduction as significant or meaningful. At this rate, it’d take us almost a decade to finish paying this back to 2010 levels, which we were told were only okay because of THAT crisis. And now they’re laying off less of their holdings every month. Comfort with this accepts we’ll own massive amounts of our own worst liabilities, without assets to cover them.

It’s so crazy that owning this much of our own debt is somehow now accepted as okay. Has this citizenry figured out what they’re trading of their own, to allow Congress’s absurd spending and borrowing spree? That we’re opting to be the lender to an operation that so clearly hasn’t the means to repay is insane. What are we doing. lol.

This number needs to go down faster, and more pressure needs to be applied to leadership to do so. Otherwise we’re just shrugging our shoulders as we risk the end to our current way of life. It shouldn’t be a radical position not play chicken with dollar hegemony and our position in the world. It’s all so absurd.

Adam Smith,

“At this rate, it’d take us almost a decade to finish paying this back to 2010 levels,”

People who say that the balance sheet should be at $800 billion to get us back to where we were don’t understand what the Fed’s “balance sheet” is and how it works. So let me help you with this.

In 1976, the balance sheet was about $100 billion. And it grew steadily to $900 billion by 2008, before QE started, so that’s an 800% increase.

In the five years between Jan 2003 through Aug 2008 (before QE), the Fed’s balance sheet grew by 27%, from $712 billion to $910 billion.

It increased dollar for dollar with currency in circulation (paper dollars), which are a liability for the Fed, and must be balanced by assets for the balance sheet to balance. During that time, relatively speaking, the balance sheet remained at about 6% of GDP. Currency in circulation is demand-based: Those $20-bills must be in the ATM and at the bank branch when you’re trying to withdraw them. The Fed provides currency to the banks and they must have it ready for their customers. Maybe half of USD currency is overseas, for various reasons, which is where a lot of demand for it comes from.

Since 2008, the balance sheet must grow not only with currency in circulation but also with the TGA. This is the government’s checking account that was moved from JPM and other banks to the New York Fed during the financial crisis and has therefore been on the balance sheet since then. Both currency in circulation and the TGA are a liability for the Fed, and assets MUST balance liabilities dollar for dollar when capital is fixed — which the Fed’s capital is — so that the balance sheet balances.

READ THIS – it discusses currency in circulation and the TGA, along with the other big liabilities on the Fed’s balance sheet:

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

Here’s GDP, not adjusted for inflation. The Fed’s balance sheet is also not adjusted for inflation:

The relative size of the balance sheet can be seen when total assets are figured as a percent of GDP:

If Reserves fall to the point that they are considered “ample” reserves. In which they can no longer fall or else 2019 will repeat, and the balance sheet as a whole can no longer fall. But inflation is still a problem. What option does the Fed have at that point to fight inflation? Only the Federal Funds Rate? Won’t that be 1980 all over again?

At the end of the day its dual Mandate is price stability and maximum employment. Not banking stability.

They’re way outside their mandate. I think buying our own debt is actually likely illegal, constitutionally. At the very least, it’s not an explicit power they were granted.

Basically, we ended up the the system William Jennings Bryan wanted, which was full government control over our central banks. Now we’ve got it, and they’ve crafted it into a credit card to finance infinite spending for reelections at the cost of American citizens’ savings and assets, and likely the dollar hegemony our society deserves and derives from its free(er) market principles and free society.

They could drop the rate paid on reserves to less than the 2yr etc. treasury rate. That’s a big enticing pot, that could do more than simply sit still while providing risk free liquidity to the financial system.

Wow. Thank you for that amazing response. I’m genuinely flattered. I just finished rereading your suggested link. Thanks for that as well.

1) I do not have an arbitrary level of holdings the Fed should be targeting. I only cited 2010, because it was at the time in itself historic, and unprecedented, and let’s be fair, generally considered a radical policy maneuver. I picked a point everyone remembers as unprecedented, massive, and historic as opposed to a more arguably “normal” figure over the last 80 years. The point is that even returning to a previously massive and historically high level rather than what many might feel as more “normal,” right now looks impossible. Too many in policy and the pundit class are not treating this current historic policy and condition with the seriousness it deserves. The Federal Reserve System was built to combat inflation, and it’s inarguable right now, it’s a central part of a massive inflationary policy.

2) My broader take is narrowly based on the last chart in your kind reply. In fact, my point is based on that same chart stretched back to WWI. These are wildly unprecedented times from a monetary policy standpoint and are not sustainable without great cost and also, acceptance of the contradiction in our Federal Reserve system systemically spurring inflation via its QE holdings while it’s mandate is to control inflation. The 10yrs on the Feds balance sheet are still massively depressing the 10yr yield, which is propping up massive asset classes in our economy artificially. More importantly, (and why it’s happening) is it’s wildly depressing the costs of our Federal debt, daylighting the loss of independence in our Federal Reserve system. The American electorate is not skilled enough in finance to know why the government is inflating our assets and currency, and that in the end they’ll be the ones holding the bag. I’m calling for an unwinding of the treasury holdings, a correction in asset values and the value of our currency, even if it hurts (and it will). Without it, there are massive structural problems our society will face, as they accept the Fed’s propping up of Congressional largesse and the translucent values our society has on major areas of our economy.

I think the medicine we’ll need to take for this policy’s correction is going to be pretty awful but shouldn’t deter us from taking it! These balance sheet holdings, whether nominal and AFI, or a percent of GDP are recklessly irresponsible and risk major structural components of our society, its position in the world and its citizens’ lifestyles at home.

Americans need to understand that financing our own debt is not sustainable and comes at a cost most of them wouldn’t accept if they understood it. In combination with endless reckless deficits, this policy will arouse the end of dollar hegemony in the world, and our ability to finance great things at home and abroad from our military to our social services. It’ll bring continued durable inflation which will sap American savings and retirements, bringing sectors of our population into poverty that smart policy now could have avoided. Until we tame the liquidity flushed into the marketplace by this administration’s balance sheet, that risk will sustain.

3) I remember reading the article you linked this past spring. Great read (I’m wildly interested in your and others’ analysis on this matter). But I don’t think this balance sheet’s negative condition is based in our national overnight repos or the general account, both which are returning to “normalcy” on good trends. As noted above, my concern is with the holdings of notes (and less so now, MBS). These are massively inflationary policies and fly in the face of the Fed’s mandate. Removing that liquidity from the market is important if we’re to tame inflation and restore balance to our capital markets. We’ve already seen massive valuation corrections in various asset categories. Eventually, more newsworthy sectors like the stock market are at risk of correction.

It’s time to remove the brakes from QT. End the caps and let all these assets roll off. Just because the 10yr will likely spike as relative demand weakens, shouldn’t be reason to continue to violate the mandate and sacrifice the well-being of Americans. The 10yr yield is the only way we’ll get congress to take responsible action on their policy. Let’s stop giving them these relief valves so they can delay doing their jobs, and let’s stop lighting American citizen wealth and savings on fire.

I read somewhere that the money supply (M2) is now rising. How is that possible if the Fed continues to roll off securities? Banks creating money through loans, or what?

Money supply (such as M-2) is a bad metric that doesn’t measure money supply. For example, M-2 includes CDs of less than $100k, but excludes CDs of over $100k. So if someone has a CD of $120k that matures, and the cash goes into a bank account, or into to two $60k CDs, then money supply increases. There are other problems with M-2, including how ON RRPs are handled. M-2 is meaningless, which is why I don’t cover it, and why the Fed no longer mentions it.

Cash in circulation, however, is still bouncing around at all time highs.

Wolf,

I wonder how much is currently sitting

in Treasury Direct as T-Bills. If the whole

world were like I, then M2 would have

cratered, if this is not included.

This is as accessible as CDs with a bank,

but I don’t even have a good guess as

to the magnitude of money involved.

Very small trillions, maybe?

J.

What have you done to all comments, I don.’t see mine any more. ? You only post the one’s you like. Ed Koller

I deleted your last comment, and only comment today, because it violated the Commenting Guidelines and was BS. Your old comments are still here somewhere.

Also have nominal gdp growth going on and regular inflation. That will help suck some of the liquidity out

My gut tells me mortgages roll off faster when they cut rates.

I am thinking late this year we see them stop the balance sheet run off.

This market looks more like 2000-2003. AI is overpromissed and will reset. The fed is still reactionary. Fed wait and see translates to “we have no clue and will react when it’s obvious”. Enjoying short term treasuries until the pivot where we’ll jump into interest rate sensitive dividend paying funds (which we’ve already started to dollar cost average into, 6%+). Good luck to all

Hello Wolf, is BTFP included in the Fred Total Assets chart?

🤣 RTGDFA

Yeah Wolfman, I remember you writing that the Federal Reserve likely will stop Quantitative Tightening when its balance sheet is between the range of $4 trillion to $5 trillion.

I hope that does not mean then they start another recession cycle of Quantitative Easing right after they reach that range.

The numbers are not quite right in terms of what I said: $5.8 trillion is the lowest possible level, and getting close to $6 billion is more realistic, according to my math. Here is my math, quoted from the linked article:

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

The “lowest possible level” of the Fed’s balance sheet in 2026?

No one knows, not even Fed, but here is our guess: $5.8 trillion, limited by the liabilities.

The minimum balance sheet level is determined by the liabilities. In the current setup at the Fed of “ample reserves,” it’s the reserve balances that the Fed will watch. If reserve balances drop too low, as they did in 2019, bad things can happen. Let’s say this theoretically lowest possible level of ample reserves is $2 trillion in two years. Add a little margin of safety, so maybe $2.2 trillion.

In this scenario, this lowest possible level of the balance sheet in this scenario would be $5.8 trillion, below which the balance sheet cannot decline without something blowing up:

Realistically speaking, getting the balance sheet close to $6 trillion by the end of 2026, so shedding another $1.5 trillion, after the $1.45 trillion that have already been shed, will be a big improvement, meaning that the Fed’s balance sheet will by then have shed about $3 trillion, assuming that nothing blows up along the way.

Technically, If the Fed has to balance assets with its liabilities and since they only want to keep Treasury Securities on their balance sheet. Then shouldn’t they outright sell MBS and not even let the Treasury securities roll off. Since7.22 trillion (total assets) minus 2.34 trillion (MBS) that would be 4.88 trillion. A trillion less than 5.8 trillion.

When QT stops in the future, MBS will continue to roll off and be replaced with Treasury securities.

Indeed Jose! If the Fed will meet their balance sheet composition in a faster way, it is impossible to avoid MBS outright sales. In my second commentary which was not published, i say the MBS holdings blocks balance sheet potential which they Fed need for treasury purchases.

Your prior comment was deleted because the first sentence contained a series of lies about the housing market and the MBS runoff. RTGDFA.

Excuse me Wolf, but where was the series of lies? Because i said no MBS roll off will happen when the housing market freezed when nearly no transactions will be settled? Or because i said the MBS holding blocks balance sheet potential the Fed needs for treasury purchases?

Marcus,

First sentence, 3 lies, do you see them? You said:

“but actually the housing market is in fact dead due the high mortgage rates, and this means no transactions and payments which resulted in a zero roll off.”

You cannot just make up stuff here to suit your narrative. It triggers a delete when you do.

What’s interesting is M2 is growing again. And is rising fast. While fed balance sheet is still declining slowly.

Banks are expanding lending and that drains reserves.

Yep, coupled with deficit spending, inflation is going to get much worse.

Wolf continues to document (what made public anyway) the operation of what may have been a noble idea, but now a criminal enterprise. The Fed NEVER should have been allowed to buy MBS and the people/corporations behind the creation of MBS, and all the derivative bets, should have been allowed to FAIL (go bankrupt and have their assets sold).

I’ll maintain my own prediction/bet that the Fed will not be able to get it’s balance sheet below 7 trillion. Especially now that other central banks in the western world have begun lowering their own rates. IN ADDITION, our CONgress is fully captured by global money interests/corporations and refuses to actually balance the fucking budget. Both of these last two facts make it impossible for Jerome to get inflation under control, and so, the DEBT will require hyperinflation to resolve.

Buckle up buttercup.

I’ll maintain my own prediction/bet that the Fed will not be able to get it’s balance sheet below 7 trillion.

That prediction seems almost bizarre at this point. The Fed is already 90% of the way to that goal since it started QT in 2022 and it just slowed QT for the express purpose of letting it run longer into the future. At the current pace the Fed’s Balance Sheet will be below $7 trillion in less than seven months… and HALF of that will come from eliminating the BTFP deposits that the Fed would be happy to dump in a heartbeat.

Being as this is the second half of an election year… the Fed’s normal M.O. in these situations is “steady as she goes”… there won’t be any more changes to the QT program (or even ANNOUNCEMENTS of changes) until 2025 (if then). By then the $7 trillion marker will be in the rear view mirror.

Sure, we are not there yet. Guess we will see. Place your bets, because this isn’t a real market. Hasn’t been for a long time.

Mbs in my opinion is not as inflationary as buying treasures.

I mean mbs is backed by actual assets housing.

The only thing backing treasury’s is the credibility of the us government. Which in my opinion is worth less

Gabriel,

You missed something: What keeps these MBS pristine is that they’re backed by the US government, same as Treasuries.

Well technically there backed by us Treasury and housing both.

At the end of the day. The fed owns housing indirectly. When it buys mbs. It basically owns equity in something physical. Tangible.

Us treasury’s on the other hand are not the same they are just paper at best and are not backed by anything at all. Mbs in my opinion are safer to own.

I said in Wolf’s report in May on the effects of QT that the BTFP program was what drove the FED to lower its regular QT efforts since they couldn’t control the rate of withdrawal from the banks in that program. This month shows why… ONLY $1.06 BILLION in withdrawals in June???

That drives the average that has to come out over the next eight months UP to almost $9 billion per month.

https://wolfstreet.com/2024/05/02/fed-balance-sheet-qt-1-60-trillion-from-peak-to-7-36-trillion-lowest-since-december-2020/

I suspect that funding market are hinting we are near the limits of how low the balance sheet can go. I think around September they cut rates and pause balance sheet reduction as part of it.

This article is brilliantly written and incredibly informative.