Stuck with a 6% or 7% mortgage that was supposed to be refinanced? The Fed is counting on them to help bring inflation down.

By Wolf Richter for WOLF STREET.

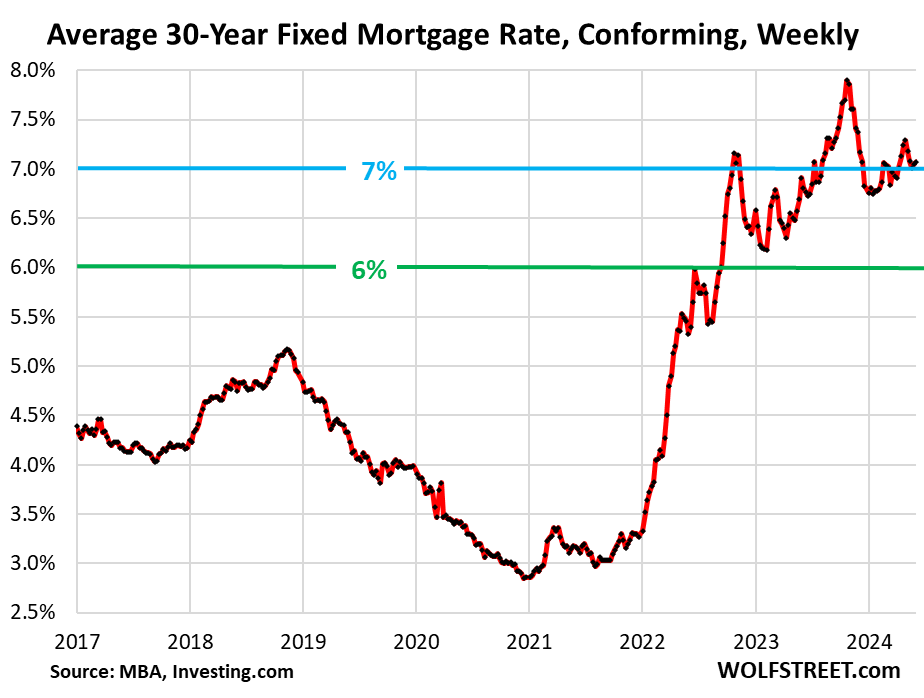

The over-7% mortgage rates seem to have become a fixture in the housing market. The average conforming 30-year fixed mortgage rate edged up to 7.07% in the latest week, and has now been above 7% since early April, according to the Mortgage Bankers Association today. During Rate-Cut-Mania, the average mortgage rate had dropped to 6.76% at the low point in early January.

These mortgage rates are not high compared to the pre-QE era. From 1970 through 2001, mortgage rates ranged from 7% to 18%. What was different then that allowed those rates to function were the lower home prices. When mortgage rates dropped below 7% in 2002 and eventually as low as 5.5% in 2005, they fueled Housing Bubble I, which led to the Housing Bust from 2006-2012. So these 7% rates are fairly healthy rates:

Stuck with a 6% or 7% mortgage that was supposed to be refinanced? Mortgage rates have been above 6% since September 2022. But no problem, the real-estate industry has been telling homebuyers that they should buy now even at these rates because they will be able to refinance at a much lower rate shortly, after the Fed starts slashing interest rates.

Meanwhile, there still haven’t been any slashed rates. Instead, recalcitrant inflation in the US has caused the Fed to backpedal on the three rate cuts in 2024 that it has seen as possible in December 2023. The economy is humming along, the labor market hasn’t yet collapsed or whatever, and there really isn’t anything “forcing” the Fed to cut rates.

These new homeowners may feel kind of stuck with their 6% and 7% mortgage rates, and their big mortgage payments that may force them to cut back spending on other stuff. But the Fed is counting on them. They’re one of the official transmission channels of Fed policy, via higher interest rates to lower demand in the economy, and thereby to lower inflation. So they’re carrying the Fed’s water in trying to get inflation down.

Home sales still frozen; prices are too high.

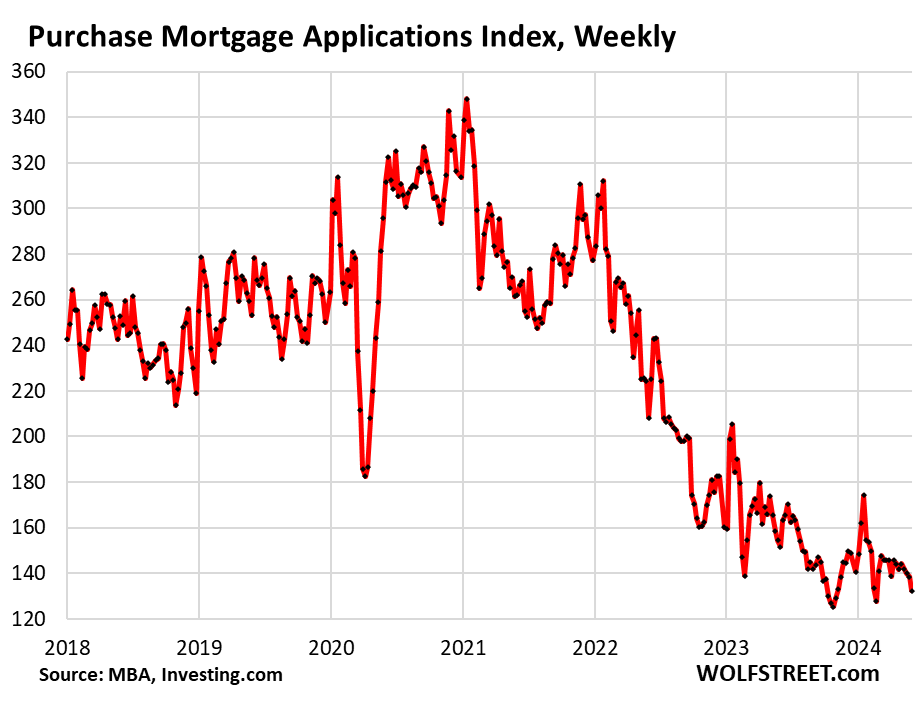

Mortgage applications to purchase a home dropped further in the latest reporting week and are just a hair above the record lows in the data going back to 1995. The records were set in November 2023 and February 2024. The mini-spike of Rate-Cut Mania has by now completely worn off.

How far mortgage applications to purchase a home have plunged from the same week in the prior years:

- From 2023: -13%

- From 2022: -36%

- From 2021: -46%

- From 2019: -48%

Volume of closed sales of existing homes in April had dropped by 26% from April 2022, by 30% from April 2021, and by 24% from April 2019.

Volume of pending sales in April, an indicator of closed sales in May and later, dropped 7.7% from the prior month and by 7.4% from the already beaten down levels a year ago, according to the National Association of Realtors last week.

“The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market,” NAR said, adding of course the rate-cut thingy that the industry has been hanging out there for two years: “But the Federal Reserve’s anticipated rate cut later this year should lead to better conditions, with improved affordability and more supply.”

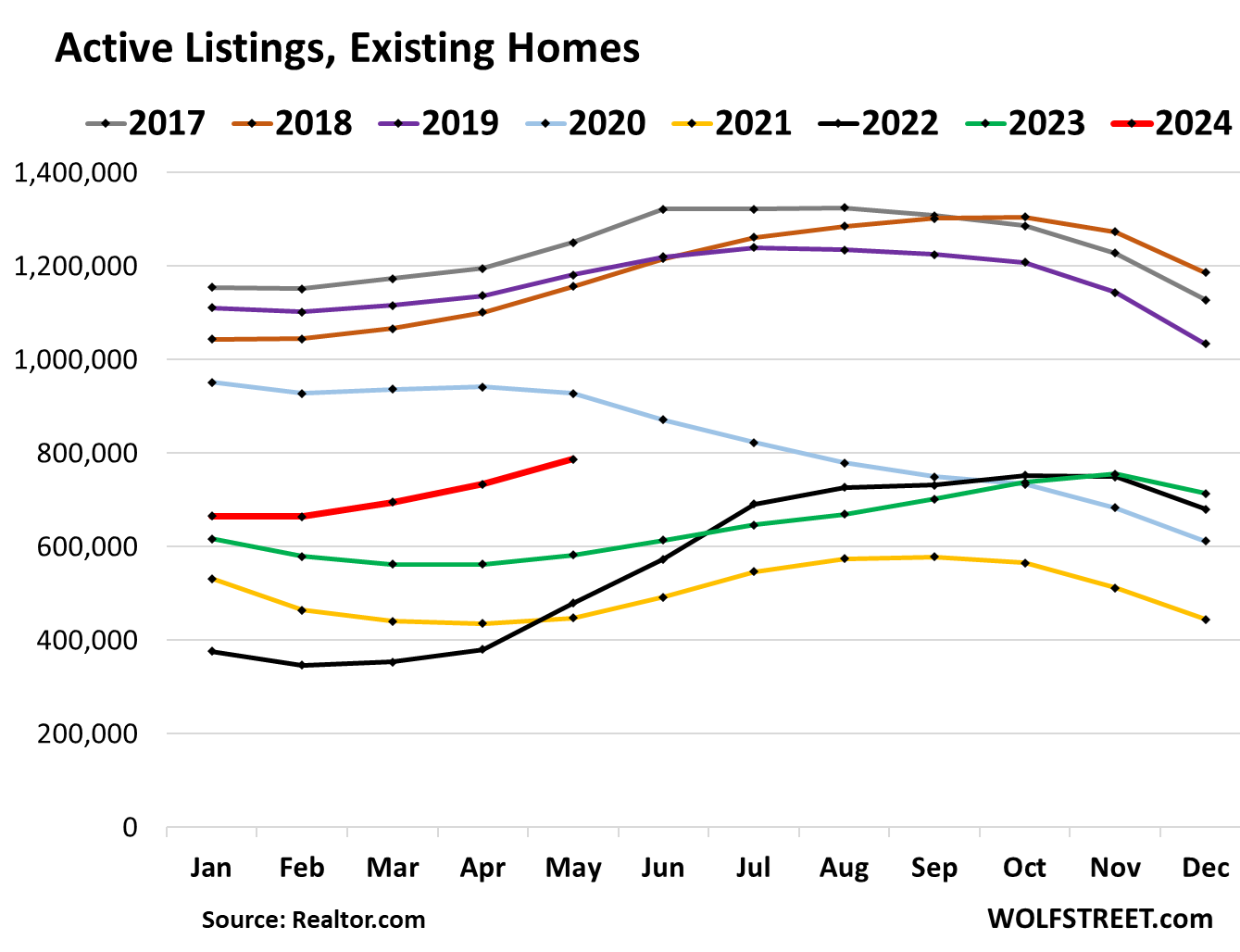

Supply is already increasing. Active listings in May rose to the highest for any may since 2020, according to Realtor.com:

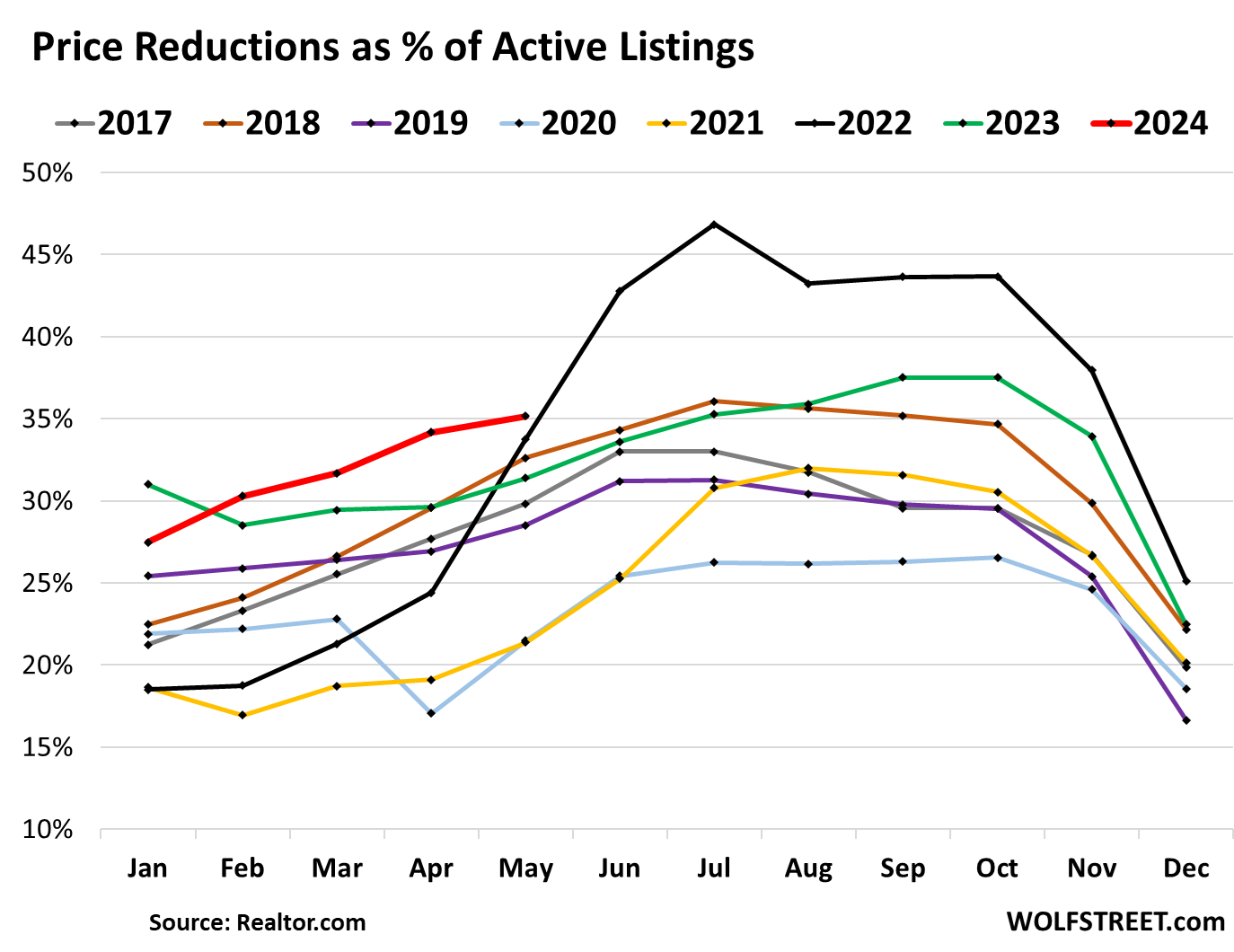

Price reduction rose to the highest for any May in the data by Realtor.com going back to 2017. Price cuts are a first sign that the housing market may be thawing out just a little, but it will take a lot more than cutting exaggerated asking prices a little bit.

And for now, the housing market remains frozen because prices are still too high, keeing many potential buyers on strike. And some of them have figured out that they can rent a nice house for a lot less on a monthly basis than buying at these sky-high prices:

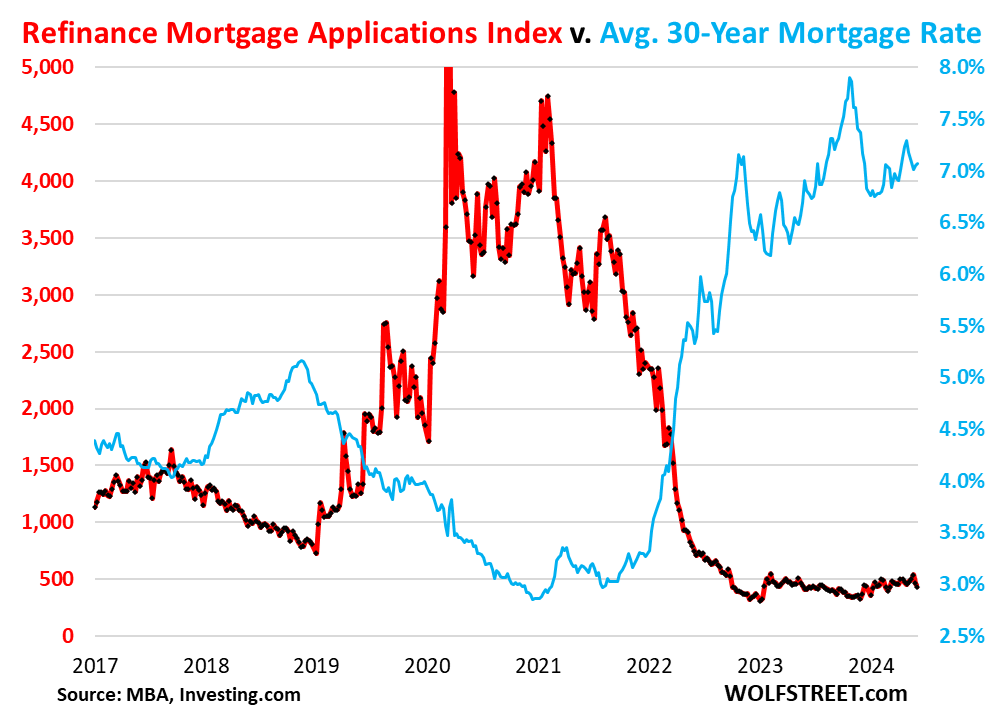

Mortgage applications to refinance a home without cash-out have nearly vanished. The refis that are still taking place are mostly cash-out refis.

In the latest reporting week, total refis dropped further and were down by 85% from the same week in 2021 and by 67% from the same week in 2019, having squiggled along historic lows since August 2022.

Refis are dependent on low and falling mortgage rates. They had seen a historic boom during the 2.5%-3.0% mortgage-rate era, and in the months as mortgage rates began to rise in the fall of 2021 and early 2022, after the Fed started talking about rate hikes, the end of QE, and eventually QT. And then refis died.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here’s the long view of mortgage rates for history buffs, and for those who can’t remember or weren’t around. 7% really isn’t a bad deal; what’s a bad deal are the prices, fueled by too-low-too-long mortgage rates since 2008 when QE started:

All that said, there’s just no catalyst for prices to come down either. Just a slow march as forced sales take place and wage gains eventually catch up to the new prices. Could take decades.

A REAL recession is the only cure for high home prices. The good news is that more inventory is coming online, which will create some downward pressures in over bought states like Florida. At least over the next 3-6 months, prices may start to rise in the new homes space, IMO. Unless the ADP figure was way off, Friday’s jobs report is probably going to push interest rates below 7% by next week. The slog to a recession will be more protracted than most expect, giving the housing market time for one last pushing higher. There’s the narrative building that the economy is slowing. That may be the case, but again it’s going to be slower than most expect. I could see there being a surprise rate cut in July. The Fed will lower rates well before the 2% target comes into view. The CRE crisis is a great example of needing lower rates to avert a crisis. The Fed has started to buyback small amounts of longer dated treasury bonds using short maturity treasuries at much higher rates. Are they doing this to get out ahead of the CRE crisis? What’s the goal?

Good points GuessWhat. Agreed a genuine recession is the only event that would break the RE pricing gridlock. Even here in flyover land, many sellers are retaining an attitude of high price entitlement. The unspoken sentiment seems to be “my neighbors got this high price in 2022, so why shouldn’t I?”

A friend of mine and I jokingly refer to some of the current residential RE prices as “fund my retirement prices.” The markup between what they are asking now and what they originally paid (easily checked on the County Auditor website) is ridiculous. Even after making an inflation adjustment to their current asking price.

Another obvious reason is the large population of people who received mortgage loans with low interest rates during the pandemic. With the interest rate differential as great as it is today, they WILL NOT move unless they absolutely must – and who can blame them? Even if that means tolerating a property that is larger or smaller than they now need.

What would cause some of that low-interest-rate-loan population to move would be a recession. Some of that group would get caught up in layoffs and would subsequently accept positions in new metros. A few might rent their current home instead of selling but others would not want that headache and would sell their property.

Further, some would rent for a period instead of purchasing in their new location. They would rent to A) see if their new position is working out and B) to determine if the new area is to their liking.

That scenario would break things loose to a degree. But this recession is very slow to arrive. I’ve given up on trying to guess when it will happen. This has been a counterintuitive economy for quite a while now.

You are missing the real cure for high home prices – wildly increasing insurance costs and more wildly increasing taxes. Not to mention maintenance. When your taxes are 1-2% annually, it’s approaching mortgage territory. In Florida I have heard a lot of scare stories on condo assessments and single family home rates due to insurers pulling out due to hurricanes and rising costs of deferred maintenance. I lived through a Florida hurricane rebuild on an investment property and it was not fun. I had to write a letter to the insurance commissioner documenting the damage costs and the insurer denial of claims before my lame insurer would pay out.

Same in California due to wildfires.

People have yet to feel the real squeeze of inflation. Rising ownership costs versus decreasing equity value when measured by the pool of qualified buyers.

// Another obvious reason is the large population of people who received mortgage loans with low interest rates during the pandemic. With the interest rate differential as great as it is today, they WILL NOT move unless they absolutely must – and who can blame them? //

What if there are massive unemployment, say, 10%? When people can’t afford their mortgage even at 3%, they either have to sell the house, or become delinquent.

I don’t want to see massive unemployment. However, I don’t see there are other ways to bring down housing prices.

“I could see there being a surprise rate cut in July. The Fed will lower rates well before the 2% target comes into view.”

Muh rate cuts!!

8_mile_road,

>>(…)When people can’t afford their mortgage even at 3%, they either have to sell the house, or become delinquent.(…)

Many people buying houses in our area in 2021-2022 got houses for $300-400k with sub-2k mortgage payments.

There is barely anything cheaper than $450k in the area now, even townhouses, besides, if they want to buy something smaller, they will likely not qualify for a new loan, and even if they do, their mortgage payment will be at least 2.5k.

There are very few rents in the area that are less than 1.5 – 2k and those that show up from time to time tend to scrutinize tenants.

That said, for example, if I, God forbid, ended up without a job, I would stay put and do whatever I can to keep the house – do all the odd jobs I can find, send my kid to work somewhere after school etc. – whatever it takes to stay afloat when my cushion is exhausted, up until I can get a stable employment again.

It’s a classic zugzwang. Unfortunately, for many people who locked themselves into more affordable houses in 2020-2022 at good rates, moving will almost always make things worse, not better, unless they move with relatives (i.e. don’t pay for their housing at all or pay very little).

“The CRE crisis is a great example of needing lower rates to avert a crisis.”

But the low rates caused the crisis so….?

“All that said, there’s just no catalyst for prices to come down either”

The catalyst is/ will be the increasing number of houses for sale relative to the number of houses being sold.

Yes.

I have to wonder about the emotional state of people who complain about high house prices then go out and buy a house. Are they thinking the system has forced them to buy an overpriced house? Government actions seem to be driving people crazy.

That said, if people choose to put their hand in the garbage disposal while government paid children play with the switch, it’s a decision THEY make.

Many people have been beaten to the point of desperation. They don’t believe anything normal, expected, or warranted can happen in the future. Deep down, many people have lost faith in government institutions. The average person with low or moderate wealth is not adequately represented.

There’s a difference between a 5-10% national drop and a 20% drop. FYI the median sales price of all home sold from the top to bottom of the Great Recession was only about 20%. Adding inventory to the market in the numbers we’re talking about outside a really big spike in foreclosures is only going to do so much and it will definitely have differing effects across different states. I’m talking about at least a 30% price reduction NATIONALLY. That’s going to require a pretty big recession. And even then, as I’ve said for two years now on WS.com & other sites, the MOST IMPORTANT QUESTIONS OF ALL IS THIS:

Will Congress redux rent & mortgage relief once we finally find ourselves in the middle of a REAL recession? IF they do, then they’ll stave off the much-needed drop in prices to truly make housing affordable again.

My guess is that Congress does something. The question is, of so, then how big do they go?

Again, the only meaningful way there’s a return to affordable housing is through a REAL recession. And currently, the MMT-based means of managing the economy since Sept. 2008 doesn’t bode well for that to happen.

Hopefully like Joe2 points out that insurance & property tax costs are going to combine with spiraling consumer debt to push us towards a recession. And, I’ve read where it’s possible that the backend of a recession could see businesses push hard with AI / robotics sooner rather than later. Something like this would exaggerate the problem.

The builders can’t afford to sit on inventory for years until they get a 2020 price. They’ll have to discount, and to the extent that new homes compete with used ones, eventually it will get to the point where the used homes have to come down in price. Or they’ll get no bid.

The builders are playing kick-the-can games like not cutting the list price but buying down mortgage rates, offering free upgrades, etc.

Hope you are right but the danger is that higher interest rates (which is correct move about 7 years too late…) will simply cause “modern” homebuilders (see below) to simply down tools and stop building houses/increasing supply (the only true long fix for high prices).

Until the Fed went ZIRP insane post 2000, “traditional” homebuilders somehow magically were able to build sub $200k houses that median families could afford with mortgage rates of 7%-9%.

Then, in a fit of persistent empirical atheism, the Fed went stark raving ZIRP.

(The initially understandable logic being that lower interest rates – engineered via money printing or related tools – promotes investment including homebuying/homebuilding. The crime came from the Fed ignoring the actual multi-year results – see below).

1) If homebuilders circa 2003 – 2022 had continued building $200k homes, demand/volume/housing employment would have exploded (since ZIRP would have halved monthly mtg payments).

2) But that **isn’t what happened** (for 10+ years). (F you, Fed, for being dead at the switch for 20 years)

3) Homebuilders saw ZIRP cutting interest rates in half…and simply worked so as to double the purchase price of homes (McMansions for McMorons).

So instead of $200k homes with halved payments due to ZIRP, we saw $400k homes (phony asset boom) with constant payments.

4) In the intervening 20 years, it is as though the ZIRP addicted homebuilders have lost will/knowledge/memory/etc. of how to build big wooden boxes at anything other than the maximum price level (despite 20 years of new technology and the internet’s ability to disseminate such knowledge essentially infinitely and almost costlessly).

So I am worried about “modern” homebuilders actually adapting/improving rather than downing tools and ratting off to some beach with their ill-gotten ZIRP gains.

No catalyst for price reductions? I beg to differ.

Look at the active listing graph above. Listings at the start of 2022 were 400,000. They are 800,000 now, so they’ve gone up 100% in 2.5 years. Meanwhile, demand has actually dropped due to high mortgage rates. A simple continuation of current trends could cause the the floor to fall out.

A second potentially huge catalyst is the stock market. Look at how the housing graphs above were impacted by the modest stock market drop in 2022. Look how active listings rose when the stock market started dropping.

Be patient. Rent a nice house or apartment and wait it out. Earn 5.3% guaranteed on the core of your funds, then put a smaller allocation to stocks and put options collars on the position. If you do it right, you are guaranteed not to lose, and you’ll most likely get investment gains in the 5-10% range with little to no risk.

In addition, people always have the option of moving to a different location where cost of living is less.

@Bobber “are they thinking the system has forced them to buy an overpriced house?”

Real estate is not simply driven by economics. People are forced to move for a number of reasons unrelated to the current market state.

I have seen an unbeliveable number of cash offers over the past 24 months. The majority of which have been made from recently retired individuals. Their decision to buy and where to buy, were made many years ago. Likewise, financed, non-contingent offers are high from non-retired people flocking to the midwest due to a historic change in the number of remote workers and simple job changes. The remote workers are looking for affordability and comparing these 2X 2020 midwest prices against their 3X 2020 price from Cali, Florida, Texas and every other big city Wolf reports on.

Lol! According to your theory, no one will be buying or selling for decades. Not going to happen.

Right. The rate-of-change in money flows, the volume and velocity of money, would have to decelerate.

Housing Bubble I was created by Bankrupt-u-Bernanke draining legal reserves for 29 contiguous months. Means-of-payment money didn’t increase for 4 years.

Here in California minimum wage for a pimple riddled teenager flipping fries at McDonalds has reached $20/hour. that means that a late high school student with no credentials, probably no car can make $42k/year.

If rule of thumb for SoCal room rentals used to be $1000/month and its pushing toward $1500 already as I type this reply. You can imagine that value getting close to $2000/month in the near future. That can easily put a bottom to real estate prices and rentals.

Home prices are high online on platforms like Zillow/Redfin but when you actually make offers and negotiate, prices can drop as low as 30% from the unrealistic bubble peaks.

I just bought a 3bed/2bed in Torrance for $525k, dropped it from an original asking prices of $600k and that was already priced to sell. A year ago the place would have easily gone for $750k. Its in need of repairs to bring it to my standards, probably will shell over $100k in renovations and it was a cash offer which helped overall. I’ve been busy not spending. But shows how the minds of the sellers after a really slow year and these high interest rates have already adjusted.

This 2023-2024 might be that deflationary period for home prices where the discounts can be found before they print again. And they will! Just looking at our deficit in the US, the weaponization of the SWIFT banking system. I was personally hoping that Austrian economics would prevail and we would see a real recession and price drops, but I’m more worried now about currency devaluation then I am about a real deflationary recession.

I could be wrong, time will tell if I should have held out a bit longer.

But anyway, now that I have made the jump from a millennial playing monopoly to taste real estate to an actual boomer. Howdy to my favorite boomer website. <3 your work Wolf.

The $42,000 / year kid is taking home $34,000 and waiting for his draft notice.

Thanks Nick,

Perfect example of recency bias as you recently bought a home and now thinking: How things can put a bottom to real estate prices and rentals…

@jon

I believe the bottom in real estate wont be as low as previous bottoms, that’s why I made the decision to buy, not the other way around. The government is creating a new normal for general pricing pushing inflation into different areas of the market so its not a huge shock and goes unnoticed.

When I tried to hire some “Amigos” from Home Depot to help with the demo, could not get anyone to bite unless I shelled out at least $200/day. It used to be ciento dolares to hire uncertified / undocumented migrant help before covid.

Inflation is here gentlemen, and its sticky. Its not just the food that’s doubled.

Unlike what @Jon might think, I’m not trying to rationalize my purchase. That was very simple. After cashing this 3bed/2bath 1550 sqft my expenses are $1000/month for the place. Rent in my area for a similar condo ranges in the $4k/month.

$525k + $100k in renovation = $625k. If I were to simply put that money in treasuries for 2-3 year duration @4.7%average I would get 30k/year.

Alternatively If i rent just two rooms for $1500/month each I would get 36k plus my own master bedroom and home ownership, inflation hedge etc etc. Now treasury investment has the issue of duration. For how long do i put it, what then? Is it inflation hedged?

Just like most of you I’m under the opinion that the low interest rates added too many people in the housing market that should have never been allowed to buy a home. That unfair competition hurts people who actually have saved their 20% or more down payment by increasing prices through artificial competition.

So when I say this 2-3 year period we are going through now with high interest rates might be the “deflationary period” we were sort of waiting for I don’t’ believe I’m that wrong. Its a frozen market, the amount of buyers is low, they’re on strike.

If you have cash, and you can manage to drop the price by 30% how can you lose?

Honestly, how much lower did you guys think prices would drop?

just curious? Do you all on this site believe we’ll see a 50% drop and, are you all so sophisticated in real estate that if prices drop by 50% you’ll be able to corner a great deal in a great location?

It might be easier to snatch a really nice place with an awesome location at -30% then wait for the real bottom even if we reach -50%. The amount of competition then might be smarter then you.

Anyway, my 2cents.

According to Zillow, the sold prices for both condos and single family homes are at alltime highs.

SocalJim

LOL, you failed to say that these condo prices in April were up by just $366 from the prior peak in July 2022. So they were essentially FLAT with July 2022, per Zillow. This manipulative trolling gets old:

“If i rent just two rooms for $1500/month each I would get 36k plus my own master bedroom and home ownership”

And then your two roommates are a package deal in order to make your finances work.

Whatever floats your boat – personally, I bought a house so I could have my own space and not need roommates.

I like the way Nick thinks and predict he will do well in life…

Those $20hr fast food jobs are drying up fast as restaurant’s close and even large chains like McDonalds and In & Out are thinking about abandoning CA all together.

Bottom line is you cannot support an economy on ever decreasing productivity. Burger and service jobs do not create anything of any real wealth building importance, and will not sustain an economy as we are now seeing in real time.

Thanks @ApartmentInvestor

@MM I am in my early 40s yet addicted to boomer websites and have become a perpetual pessimist and constantly plan for the worst case, so when I get surprised, its usually good news.

To give Wolf full credit, thanks to this site I invested heavily in oil stocks during the pandemic, was able to get Exxon @10% dividend, slightly lower returns on the other Standard Oil offshoots, so I doubt I’ll ever need to rent my two rooms since those investments alone completely cover my living expenses. Just mentioned renting as an alternative option to match the returns vs bonds.

I was trying to point out that what you see on Zillow might not be a true reflection on the ground. With these high rates, those ninja loans and no money down shenanigans have all but disappeared and really good deals can be found in my opinion.

Timing the bottom is a risky game. 7-8% mortgage rates have removed all those undesirable elements in the housing market we all don’t want. If rates go higher, then sure, mea culpa. You will have a smorgasbord of options but in case the government intervenes again and drops rates like the ECB and Bank of Canada just did, then my decision to by at -30% wont be so bad, maybe?

Just don’t believe all the price averages on Zillow/Redfin.

These online portals are bias toward higher prices. I closed 3 months ago. When I try to go on Zillow under sold page in my area, mine is nested with 3 other units while the overpriced 2bed/2bath sold 2 years ago for $100k higher then my 3bed are listed separately and more visible.

If you got anything from my real live example and are in the market for a home is to negotiate hard, you might get a really good deal now, before the economy “crashes”.

Amen^2

I’d be happy with 7% interest as long as prices drop 30-50% to sane levels.

Don’t listen to the naysayers about a house price crash necessarily plunging the economy into the next Great Depression.

Sure, real estate speculators get wiped out (who cares), asset holders get a haircut while making housing affordable for young families (a good thing for equality-sake and upward mobility), and after a brief shock to the economy capital gets reallocated towards productive uses (a wonderful thing).

A recession (ie. reduction in GDP) is also not a bad thing since its mainly the zombie investments that get cleansed. That is, unless the government prints $10T, up from $5T, to bailout the natural correction of the $50T asset bubble. If that occurs, then we have a super bubble on top of the super bubble.

I say bring on the falling knives!

Ratio between median income and median home price, highest ever!!!

The catalyst for the pop is never obvious until it’s happening.

It would be interesting to see those ratios geographically, to see how outrageous that ratio is in major metro areas in various states or even at the county levels.

The interesting thing in my neck of the woods in the far edge of Bay Area CA is houses go on sale and:

1) Price reductions within 10 days

2) Zillow has removed previous sales data- who would buy the home at that price when the same house went for 200k-500k less 3 years ago when no improvements have been made?

3) Sitting on market 30+ days because sellers refuse to believe that their house is worth less than what their realtor tells them. Then they incrementally lower the price by 10k, another 10k and then another.

It’s all a game. And the ones who end up buying are institutional investors in the end for rent. Or stupids thinking they are getting a deal. Madness.

It’s very often that the realtors are not the ones setting the prices. As a person who sold multiple homes (relocations, moving elderly parents, etc..) the listing price is established by the seller, not the realtor.

Realtors provide “comps” and then give you a range that they think the house will sell in. I don’t think I’ve ever taken their advice at 100%. Usually, I *underprice* the house to just get rid of it as we’ve always had sufficient equity to do so – even withstanding the commissions, fees, and other nonsense expenses.

I fell into the trap of shooting for the higher end of the estimated sale price when I sold my sister’s house. The exact same house sold across the street for $1.85M @ 18 months prior. I priced hers at $1.3M, thinking a 33% discount should be enough to move it. Then I listened to the feedback from buyers as presented in the weekly activity report. I dropped the price to $1.1M (which is what most buyers thought it would bring). Got an all cash 14 day close offer at $1.0M and I grabbed it. Because FL, insurance, maintenance, a pool that was eating $200 a month sitting there, the amenity fee going up yearly, the insurance cost, the fact that it was 10 years old and would need a roof in the near future to be insurable…..

One of the things that interests me is why certain people think some unrelated person should cheap sell an asset to help a complete stranger. If I sold my son a house below market value, the IRS would want them to pay tax on the differential if they found out about it. If the cost of something is X, then there should be no expectation that the seller should give it away “just because they were lucky”. Reminds me of an old saying: “People make their own luck.”

And to those harping about eliminating home interest/property tax deductions: It’s a proven fact that home ownership creates stability in communities and people become more invested in what goes on as a result. That’s why some areas are considered “safe” and others not. That’s why people want their children to go to the schools in such communities – “They have all the good schools” which has more to do with parental involvement than other factors. More stable communities come at a higher price. Hence, protecting the interest/property tax deduction is an important factor that encourages people to buy and invest their time and money in keeping some sense of social order.

Very good post, El Katz.

El Katz,

I’ll have express disagreement. Does home ownership outweigh other government priorities? Money for subsidies has to come from somewhere. Where’s the evidence that home ownership provides more societal benefit than other uses of government money?

Sure, home ownership is nice (for some people), but so is public education, social security/Medicare, national defense, aid to the poor, unemployed, etc. Shouldn’t we be expanding the safety net for those who are truly disadvantaged before providing continuing subsidies to home owners, many of whom are wealthy.

What’s the justification for forcing non home owners to subsidize home owners? It’s a reverse Robin-Hood concept that makes no sense from a fairness standpoint. It doesn’t make sense from a logical standpoint either, given subsidies provided to current home owners raises prices and make it more costly for people to buy homes in the future. It’s counterproductive.

Also, why should people be incentivized to invest money in home ownership, when they could be investing in other investment vehicles? Is it valid for government to say that a home is the worthiest investment? Is that true when home prices are in bubble territory? Is a home a good investment, all the time, regardless of a person’s personal circumstance or preferences?

I’m a believer in small government that provides essentials, not one that arbitrarily transfers wealth from one group to another, particularly when the wealth transfers move upstream.

The reason you don’t burn down your house to get rid of roaches, is the same reason you dont want this to happen. Its better to just handle it with higher for longer rates and tightening to see where the pain point is.

Not a good analogy. Crashing the housing market wouldn’t be burning the house down to clear the roaches; it would be a total fumigation to purge the roaches (real estate speculators qualify as roaches).

I can tell you that this is exactly what I and a large segment of the population want to happen. The only people who don’t want it to happen are the ones who tie their entire financial existence, and their hopes and dreams and identities, on houses remaining at inflated bubble prices.

Carlos,

The Fed has a tightrope to walk. Housing prices CANNOT drop below 20-30% or there will be a taxpayer/banking revolt and millions will foreclose causing mass chaos just like 2008-2012. With many homeowners holding 3% mortgages, a 25% drop in housing prices would start to worry them and possibly cause them to jump ship on their underwater houses causing much economic pain. We’ve seen this before in 2008.

I guess the question is: How much can housing drop before the majority is underwater. That is a danger point for a foreclosure crisis . I’m guessing 30-40% but I have no data to back it up. House sales volume has been historically low during this bubble period. Maybe everyone has at least 50% equity if they bought from 2012-2019 and they won’t walk away?

We don’t have capitalism anymore. If the Fed decides to crash the housing market with massive losses to taxpayers, they will. If the Fed decides to inflate the housing bubble, they will. I keep thinking of the intro the the famous “Outer Limits” show where the narrator controls the vertical, horizontal and everything.

Thank you for posting this. Clearly, the past 20 years have been an aberration.

Who knows what the future will bring, though. I’m afraid that the population has been conditioned to expect “help” so “help” will be provided, one way or the other. See the recent news about “zero down” mortgages.

Unless there’s a major disruption of some kind, such as a war, or a stock market crash, things may continue at the current pace for much longer than we think. Of course, absolutely no one today thinks such things can happen _to them_, but, sadly, they do. In addition, the situation is complicated by the fact that a lot of potential sellers + buyers are simply gone, for years, probably, as Wolf repeatedly described.

I have a mortgage amortization table book that doesn’t even go below 7%.

I appreciate your commentary. However, I exited the house flipping market because the overall costs have far exceeded the aggregate value of individual components. For instance, replacing windows in a 2,800-square-foot house now exceeds $30,000. The United States currently lacks the necessary inventory for housing prices to decrease. If you are unable to afford a house today without significant economic or demographic shifts, (massive deportation) it is unlikely that you will ever be able to do so.

Prices are set by the market, not the costs that go into it. It doesn’t matter what it is. Companies go out of business all the time because their costs are higher than the price for their product in the market.

Whenever I try to explain exactly this concept to people they look at me like I’m an idiot.

“costs are higher than the price for their product in the market”

Of course true in the long run.

But in the highest-dollar world of financed products (cars/housed/etc) Fed f*ckery-pokery vis a vis interest rates can fatally distort true price “affordability” in the interim.

I know you know this, but it can’t be repeated too much – the price mechanism works fine…but in the realm of financed products, distorting interest rates distorts (unsustainably) prices – derailing the whole market mechanism.

Prices are set by the FED.

The Fed’s not setting my prices, I wish, LOL, haven’t raised them in years.

Isnt the other side of your argument that if prices are not high enough to cover costs, production ceases until demand puts a new floor under prices.

We might want to argue that the cost of construction will follow prices down but that remains to be seen. For now, I’m not seeing it.

Long-term money flows fell by 80 percent from 1/2013 to 1/2016. Oil fell by 70 percent during the same period. Then Yellen raised policy rates.

spencer

Oil plunged because of US frackers ramped up production, as fracking technology matured, and supply exploded, but demand didn’t change, and the price collapsed. We covered this at the time. Basic economics.

A lot of the increase is due to so much money floating around from cash out refi’s. Sooner or later those prices will fall as demand continues to decrease.

“If you are unable to afford a house today without significant economic or demographic shifts, (massive deportation) it is unlikely that you will ever be able to do so.”

Yes, yes Jay, I am sure that you are right.

Love,

2006

Excellent! 🤣

And it was fueled by more and more women entering the workforce over the last say 50 years.

If you consider that more women entering the labor pool probably resulted in smaller families, fewer children per family, one could also argue the opposite.

Your point is that increasing numbers of adult workers causes inflation. If supply of goods and services increases at the same rate as demand, which could be the case, I don’t think that more adult workers is necessarily the cause of inflation.

I think what’s relevant here is the ratio of total labor hours to total demand. More kids increases both and so cancels out, but more women working where they didn’t before disproportionately increases labor supply, thus devaluing each labor hour in aggregate. It’s similar to increasing or decreasing the number of hours in a full time work week, for example.

Yes, those of us who are fortunate enough to have a good wife are wealthier in numerous ways.

I was actually just telling someone how this phenomenon means you have to be married or partner up (which may also be a catalyst for an increase in domestic partnership arrangements) to compete in the wealth game (stuff like housing is basically zero sum).

Women don’t need us anymore, per se. so best up your game and learn to deserve love, boys.

The mirage of upping your game is sweet and self-aggrandizing until the moment she utters the words “I’m not happy”

MussSyke:

For an in depth analysis of this phenomena, do a web search for hoe_math.

Yes, Carlos. Not something we want to hear. Better to find a woman who is permanently happy, like a cheerleader. When you find one, please let me know.

Advantageous marriages have long been a tool used by the wealthy and the wannabe wealthy.

Carlos – It’s no-one’s job to make anyone else happy; in fact, it’s an impossible charge.* Now, if you’re actively impeding someone’s pursuit of happiness, then that’s another story. Otherwise, someone’s probably just looking for a ‘newness’ fix, while you’re still playing Autumn Leaves & drinking gimlets.

(*getting really good at balloon sculpture or bringing home a kitten might could help.)

Change your jockeys regularly, try not to snore, don’t kick your dog & remember to laugh at shit. Everything after that is either gravy or purely ornamental.

Yup, in 1985 we had an 11% mortgage, but the house only cost 45 grand.

My future in-laws bought a $70k home in 1979 at 12%. They later refinanced when rates dropped. But that same house is now worth $450k, only because it is in a suburb of Portland, OR — the meth/crime/scuzzy capital of Oregon. People are fleeing Portland and moving to the suburbs, driving up prices there.

Parents house bought in 1983 in prime Bay Area for 153k is not worth 1.3 million. Insanity. This is why Newsom wants to reverse Prop 13. Watch this closely. It will decimate the housing market here.

“But that same house is now worth $450k, only because it is in a suburb of Portland, OR — the meth/crime/scuzzy capital of Oregon. People are fleeing Portland and moving to the suburbs, driving up prices there.”

You explained the phenomena of increasing home prices all by yourself. No one wants to live in a scuzzy high crime area. Your choices are few: Stand and fight within the system or cut and run to the ‘burbs. Increased competition for housing due to “flight”, which is exasperated by the Urban Growth Boundary limiting land that is available for development, drives prices. It’s not greed…. it’s people making a decision as to what is best for them and acting accordingly.

We lived in Lake O / West Linn area in the late 90’s / early 2000’s. Portions of the City of Portland were hell holes back then. We loved it there, but watched as it went off the cliff as a result of the choices the voters made. The suburbs have funded police forces….

Is it really that bad? Or is this another media assassination a la San Francisco? I was through there briefly in late ‘21 and it was a little sad, but nothing like the hellscape I often see depicted.

appreciation at the rate of inflation is 294k. so the real return is 156k over 43 years…. …S&P would have garnered a real return of $2.3 million.

The house isn’t really over priced at all.

> Is it really that bad? Or is this another media assassination a la San Francisco?

Portland is fine, lol. Home prices are almost at pace with Seattle in the city, so if people are “fleeing” they’re quickly being backfilled…

@Volpe,

Portland isn’t at all “fine”, there are 27,000 fewer Multnomah County residents than there were in 2020, more than 3% loss of population, in a place that was one of the most attractive places in the country just 20 years ago. The reasons are manifold, really stupid drug laws, associated street crime and homelessness, and income tax rates behind only NYC and CA, world capitols of finance and tech, with massive populations of very wealthy people, whereas Portland isn’t the epicenter of anything in business unless you count facial hair and maybe fancy coffee. I don’t see how anyone making more than about 300K would choose to live there. And these days, that’s a lot of dual income professional families, probably the kind of people you need for a reasonable tax base.

Thanks for the chart. It confirms my feelings, as now an old man, that 6% mortgage rate seems “normal.” I guess it all depends on how long your perspective is per your age.

Wolf – agreed. Bloated list price “cuts” are not really price cuts afterall. If the market comp is $500K, and a seller lists for a bloated wish price of $550K, but then “cuts” their price down to $525K and the house eventually sells for $515K, well it still sold higher than the comps. Home prices move UP. This is what we are seeing in my market. Minimal exisitng inventory, wish list price “cuts” are not the same as comp price cuts, homes sell in hours/days, etc. Outside of say maybe parts of FL, TX, etc., this market is staying quite firm on prices. Sales and refi transactions will come roaring back as the FED cuts rates (very soon IMO) and buyers & investors rush back into a still low inventory market.

“keeing many potential buyers on strike.”

you can erase this

keeping

Interestingly related post today on Marginal Revolution: “The Danish Mortgage System Avoids Lock-In”

Still feels like a mexicam standoff with housing bear losing the war…at least in certain metro..

Time will tell i guess

“…at least in certain metros.” If you’re in the Sahara Desert waiting for rain, it might make more sense to seek rain in Oregon.

Nothing wrong with living in any major city. Life is arguably better in the outskirts but whatever….

People see what they want to see or are hypnotized to see. City dwellers crave what others seek and think they’re positioning themselves higher on the status ladder. And they refuse to see what they’re compromising, putting up with the real, lower standard of living that they think they’re enjoying.

Love how so many people can only see the world “their” way. Some people like the peaceful, slow life of a town in nowhere USA. Some people like having all the dining, entertainment and culture a large city offers and will put up with the high prices, homelessness and crime that go with that. Neither are wrong. Yet the primate urge to be in a tribe blinds us to the truth that we are all right.

House prices come down only when sellers outnumber buyers, such as places that are losing population.

For most of the country, the housing market is going to be “locked up” for a long time before it returns to something normal (a balance between buyers and sellers).

Connecticut had a crazy housing market in 2020-2021 where bidding wars were common. When rates spiked in 2022, the bidding wars stopped. That was the crash. It lasted 2 months.

Prices in CT are up 20% since mortgage rates spiked in 2022 and the bidding wars are back and more crazy than before.

I don’t think anyone who bought there in 2022 is regretting it or lamenting not being able to refinance at a lower rate.

“such as places that are losing population”

Wish that was the case – the city and county I live in is losing population for the first time in our history, and high prices are a big reason for it. Shouldn’t that cause home prices (and rents) to come down for people who didn’t leave? NOPE! Peak prices, all cash offers left and right, starter homes become “vacation homes”, and full-blown vineyard estates become “second homes”. Sure, some people still live here to serve those investors/tourists, but also a lot of commuting is happening that didn’t happen before.

Once inequality reaches a certain point, housing demand is not necessarily coupled to population, and prices don’t need a relation to the supply/demand dynamic. “Markets can remain irrational longer than you can remain solvent” – things will swing back, but who knows how long that could take. (my guess is a really long time)

I’m thinking of places like Elmira, NY, one of the worst housing markets in the country right now with falling prices. Their problem is loss of jobs and population.

A place that is losing population (like Massachusetts) can still have a hot housing market because the buyers still outnumber the sellers even with population loss.

Massachusetts is really two economies, a declining rust belt economy, and Boston. In Boston population shrinks due to gentrification and decreasing household size. In Western Mass it shrinks due to slow economic death.

Mass is losing population because of us former massholes that moved over the NH border.

32 more months on my 3.99% 5-yr adjustable mortgages on my investment properties, which contain 1, 2 and 3 Br apartments. Thanks to this site I had the wisdom to re-fi them 28 months ago, right at the beginning of 2022. My tenants benefit, because their rents are still stuck at pre-2018 amounts, more or less. There’s a lot of anti-landlord commentary that goes on here so I’ll post the rents based on bedrooms for proof – all of which include heating & hot water in a very cold place (northern New England). All my tenants are working class.

1 Br – $825/mo

2 Br – $1000-1200/mo

3 Br – $1275-1560/mo

You are a great landlord Digger.

I live in a 1650ft2 ranch. Property taxes alone are $460/month.

Utilities, insurance, maintenance all up double digit.

My ranch is about 60% the size of yours, and I pay $540/mo in prop taxes.

Thank you for being a considerate landlord Digger.

I am sure, there are more out like you.

Is this near a city like Burlington or Portland, or father out?

Just curious. When I rented in Boston from 2013-2020, my leases ranged from $1900-$2500/mo for 3br units (usually one floor of a triple deckah). I always had roommates.

I’ve got lots of landlord friends. They are all good people looking for a reasonable financial return on a hands on investment that can go really wrong with just one bad tenant. The corporate landlords in the other hand, I’ve got no good will toward those sharks.

One item left out in housing price analysis is Covid and WFH and west coast house inflation spreading across the US.

Pre-Covid I could sell my house in CA for 1.5M and buy almost anywhere I’d want to retire for $750k, pocket half.

Today I can sell in CA for $2M but it will cost closer to $1M for a nice retirement place most outside the state. Net difference not too bad still, but taxes, etc means higher ongoing costs. Sure I can live off a noisy highway for less, but basically the CA property inflation followed the exodus, with cash-rich sellers on the West Coat taking their money and bidding up Boise, Phoenix, Vegas…I was shocked when I saw the burbs of Phoenix: why would I spend over a million for 105 degree summers viewing rocks when I pay that in coastal CA for 80 degree summers with some green?

A friend bought in Reno right before Covid. His modest new build there cost $750k in early 2020. He’s now selling for 1.5M, even with high interest rates, okay place nothing special. He’s taking the money and retiring to a burb of Tuscan, new build in the middle of nowhere for $750K (there are $1M plus homes in there as well). Sounds crazy to me but he’s pocketing $750k so doesn’t really care what he pays in nowhere AZ.

Staring at a bunch of rocks versus staring at manicured landscape. What aspirations!

Don’t knock it unless you’ve tried it.

I look at “rocks” and have done so for 7 years. Said “rocks” are beautiful mountains with a landscape that constantly changes with different flowering plants and more than abundant wildlife. The “heat” only requires minor adjustments to your lifestyle – mostly having to do with hydration, sun exposure, and being active in the early morning when it’s cool and dry. AKA common sense.

But, please, keep your conviction and convince your friends it’s horrible here. Don’t come. Go away. We refer to the seasonals as “locusts”. If rocks are so bad, why do they constantly return in December other than to chase a ball into a hole like a ground squirrel?

That’s like saying the ocean is just a buncha water.

…besides, there’s too often an inverse relationship in the neatness of a landscape and the level of dysfunction in its keepers.

Thanks for the lengthy humble brag.

Ever been to Moab? Or Jackson WY? Rocks can be spectacular.

I hope mortgage rates won’t start a massive fall. The Ten Year has fallen drastically in two days. BOC just cut rates with ECB and possibly the Fed to follow. Looks like some central banks have thrown in the towel on inflation.

With no end in US deficit spending and the stock market making new highs (Nvidia just surpassed Apple), only time will tell how this crazy bubble ends.

The ECB will follow. The Fed won’t anytime soon.

The ECB is already looking at inflation that started ticking up again yoy. That has happened in other countries now too, including Mexico. Everyone is leery of that. The BOC pointed at that risk.

Places like Canada, Australia/NZ are massively dependent on their housing bubbles. They simply do not have any other good avenues for investment, and after 20 years of house prices always going up, people consider things like starting a business far too risky and too much hard work (when I lived in one of those countries that is precisely what everyone kept telling me). If the masses cannot get easy gains from housing, then they will realise that their economies are hollowed out and their countries are basically broke.

I get the sense that in the US they still have a business culture, and people still aspire to starting a business that produces something.

IMHO if the bubbles pop in places like Canada they end up in a very bad place – you could imagine a flight of foreign investment causing a collapse of their currency and massive structural issues within their economy. They have boxed themselves in and do not have the options that the USA still has (yes, I know the USA has problems, but as someone outside the country, its ability to execute when it finally gets around to it is awe inspiring).

Some very good observations there, eg:

“If the masses cannot get easy gains from housing, then they will realise that their economies are hollowed out and their countries are basically broke.”

There are towns and even small cities in the Carolinas that had their industry (one of tobacco farming, textile related, or furniture related) get exported or consolidated and those towns are standing ghost towns. The success stories of the high growth major metros belies the fact that many, many small towns are hollowed out.

If you want cheap housing, these towns have an oversupply. You just have to put up with “country” culture. Not a surplus of critical thinking going on.

The masses don’t get easy gains from housing, most are barely getting by from what I can see. Plus, unless you have had the pleasure of living the high interest rate years and the nightmare inflation of the late 70s, many seem to think carrying debt is normal…..that excessive debt is normal.

If you have no debts, it is all just interesting to watch. My US nephew with massive debts for housing and ‘stuff’, who looked like he was on top of the World 3 years ago, is freaking out.

The historical chart shows the sweet spot of normal rates, what? 7%? Free money from 2008? Really? What could go wrong?

Here is a crazy example of greed and ignorance, just down the street from me. The couple arrived here on rural Vancouver Island with an inherited $85K. From Victoria. Both alcoholics with additional drug issues. They bought a 62 year old crapola double wide mobile on 1.3 acres for the 85K cash, and spent the next 6 years working once in a while, drinking too much, a few arrests including an impaired charge with loss of driving license for 1 year. He, a self employed flooring installer. She has worked at dozens of jobs. They last maybe 2 months? He was banned for life from the local pub for spitting on the floor when they wouldn’t let him play with the band. Seriously. They tried to hire me to ‘help’ redo their deck, I declined. Help replace their windows. Declined. For backhoe work. Declined. (Help means good luck getting paid, we all know that). They suddenly realised they did not fit in here and left to live with in laws in a basement suite. Overnight. One day he showed up with a Uhaul and some friends. Gone, junk and crap everywhere. They are in their fifties.

He says he is buying a house down Island. (where it is even more expensive!!!!) Tells people the in laws will help them do it.

The shack/place is now listed and the the listing is the butt of jokes around here. It has been circulating by email. Price? $469,000. Nothing is selling here. Nothing, and they expect a 400% profit for doing nothing the last 5 years. The RE agent must have listed it sight unseen because the ‘large deck’ is too dangerous to even step on, the ‘house’ does not have a mountain view, and no it is not on the river and never has been. And also a no, you cannot build your dream home and then keep the trailer as an income producer rental. Lot too small….need 2 acres to do that here. It will now sit, empty, for years. We have seen it all before.

The lawn won’t even get cut.

I wonder how extensive (or not) has been the use of ARMs and balloons in blowing up this bubble.

Good question. I can’t find a source for current data. The most recent report I can find is from consumerfinance.gov from Sept, 23 for data that covers calendar 2022. For 2022, adjustable-rate mortgages were a minority – like 10% of volume.

An interesting side-note is the number of cash-out refinances that occurred in 2020-2022. Lots of people who took advantage of lowered rates to pull equity out of their homes while keeping their monthly payments flat. It is one more factor keeping prices inflated.

Anecdotal, but we have a close friend in mortgage banking for a large bank working the Chicago area. She’s seeing a few more ARMs, but mostly for HNW clients. It looks like some of the mortgage lenders are loosening zero down, which probably isn’t good.

I’d be curious to see active listings for new construction – and then the combined total. In our area, they are building cluster homes on small lots as fast as they can bring in the truckloads of materials. The biggest builder is DR Horton – but there are several others. We’re talking housing developments with 500 – 1500 homes.

My area too. So much ugly sh!t everywhere.

Agreed They resemble barracks or assylums.

“I’d be curious to see active listings for new construction…”

Me too. A nearby lumber mill that only makes 2×4 studs for the big-box vendors, i.e. Home Depot and Lowes, recently shut down — permanently — for lack of orders.

It was running 10-hour shifts, balls to the wall, even up to a year or so ago and then orders vanished. It was a specialty mill: 2x4x8 studs only, using computerized equipment to mill smaller logs.

But the orders dried up and with no more pending on the horizon, they closed shop. Apparently the mother company can make more money selling its logs to other mills than milling studs for new home construction.

…only makes 2×4 studs…

That’s when you know you are @ peak insanity.

My other indicator is when all my neighbors decide to turn their hobby tractor and excavator into a business.

All the sellers holding out, should calculate what it is costing them every month to get their price.

They may be better positioned to sell and reinvest, than pray for a better day.

Your good at charts. Do one of the average home price adjusted for inflation. Then add another line adjusted for cost of upkeep.

I did similar math when I sold my sister’s house. It was munching on about $3K per month (utilities, taxes, amenity fees, pool, yard service, house watcher, etc.), with the wild card being insurance premiums in the near future and demand the roof be replaced within a year or so to not get canceled. Add to that the cost of my flying across country, renting a car, etc., so I could do minor maintenance and inspect for deterioration that would require professional repair – which would require me to extend my stay. Then I looked at taking the lesser proceeds and investing them on her behalf. Worked out that it would be about $110K per annum – all in – with the income from investing the proceeds and the reduction in expenses to keep it – and that would be assuming nothing happened to the “birdcage” around the pool or any storm damage from either a tornado or the backside of a hurricane. Plus the risk of falling prices (the market there is softening and price drops appear to be consistent flow and frequent).

Houses aren’t “investments”. They’re places to live.

Most people are not number driven like you.

People are made to think that holding homes would make you rich.

Insurance and maintenance cost have increased quite a lot in last 2 years.

I got rid of my rentals in So Cal for the similar reason and I don’t want to be in land lord biz anymore.

Not enough inventory in popular places, and what they are building (typically high end large SFHs) is not what is needed. More multi family dwellings rather than mini-mansions. Not the market driving this trend but local building codes.

What of the 3 bedroom Cape Cod cottage with attached garage on a 1/4 acre lot that went for $35,000 in the postwar 50’s? Cost to build now? Selling now for $375,000 and up.

These are hot in the suburbs commuting distance to NYC.

Zillow provides a sales history of most the houses for sale on their site. Here are some typicals for the corner of the Olympic Peninsula. A crapper with a view of the Straights offered at $625k….it last sold for $125k in 2014. Here is another pressed wood palace being offered at $729k…..sold in 2015 for $300k. Here is a run down rancher on an acre offered at $649k that last sold in 2013 for $216k. Another crapper offered at $620k that previously sold for $169k in 2012. Looks like you get a “double” every ten years but the money is only worth one third as much.

Maybe start turning all the charts upside down and denominate the rapidly depreciating fiat paper wipes in fixed units of house for a better glimpse of reality?

I guess buy one & hold for ten years & then walk away a millionaire…I mean, it’s a linear trajectory, right? Up up up

No ceiling in sight and no shortage of innumerate hyper-credulous buyers. What could go wrong?

Home value have not gotten up but this is a story about how purchasing power of USD is gong down. W.r.t Housing, USD has lost 50% in last 10 years or so.

This. Plus some highly desirable locales that are full of NIMBYs and restrict building.

My first mortgage was in 1974. 30 year fixed at a 10% rate. It was a 1,008 square foot 3 bedroom ranch on a small lot. Given the mortgage climate then, that was the small starter home we could afford (barely) at the time.

From what I see around my area, the same home would easily be over $250,000 to $300,000 in decent condition.

Theory has it that a rising (financial) ocean lifts all boats however, in today’s world, how many first time buyer candidates have $50k to plunk down on a $250k starter home?

Seems like housing prices have risen well above the affordability horizon for an increasing number of folks. Maybe the only thing keeping them in the hunt was the 3% rates.

How long until the panderers in D.C. enact “down payment assistance” or a 0%-down program to combat the lack of affordability??

The “panderers” in D.C. did that during the last RE meltdown. It was a “first time buyers credit” on your income tax. My daughter qualified for it.

Since “0 down” loans are back, how far behind can the liar loans be? Or you can simply steal the deed to the house (like Graceland) and attempt to sell it.

BTW, back in 1974, who had 20% of the money on hand for a down payment? We needed $8K+ for our first home (including fees and prepaid property taxes) but that was nearly a year’s gross income for me at the time. Back in those days, they wouldn’t count the wife’s income (female) because the banks thought she’d get pregnant and quit working – putting their loan at risk.

The best fix for all this is to get the government out of the mortgage business and let the banks eat their own cooking like it was back in the day. Housing prices would fall because the banks wouldn’t want to assume the risk of hocking an over priced asset to a person of limited means.

“Since “0 down” loans are back”

Some of those require balloon payments when the regular mortgage is paid off.

Hopefully folks are reading the fine print before signing.

VA Loans are 0% down. Should those go away?

As a recipient of one of those, I still had to pay a significant “Funding Fee” in order to take advantage of the benefit that I EARNED via my service. See the difference?

Yes! Why burden our heros with perpetual debt?

How about a better rate with financial education for as long as live in the home?

This can play out over a few years. Some markets might have bigger, faster adjustments than others. Overall, nominal prices can stay flat or go down a little (might even drop 5-10 percent or more in the overbought places or with a recession) while inflation stays at 3-5 percent, which cumulatively results in large changes in real prices.

Howdy Youngins. Is the perfect storm brewing AGAIN??? This Bubba Squirrel sure thinks so…..

Thick tail, frostbitten ears…….

Great historical chart. Not coincidentally, the FIRE sector of the economy has been booming since the rates have been declining. Cashout refis, mortgages, 2nd mortgages, home flipping bros, strs, mom and pop home investors, any kind of leveraged asset owner… everyone made a killing with the scales tilted in their favor (with some turbulence during the GFC). Pretty amazing that assets are still holding up with the rate increases. For how long who knows.

There are a lot of analysts & economists aligned with Wall Street & the RE industry who are making the questionable argument that the Federal Reserve should lower interest rates, “unfreeze” the housing market, and inflation would magically go down.

For a sneak preview of what would happen to housing prices if interest rates were reduced, just look at what’s happening in the stock, bond, gold, virtual funnymoney, etc. markets – and this is without any rate reductions having actually taken place yet, only expectations of future rate reductions.

“making the questionable argument that the Federal Reserve should lower interest rates”

Fed Pivoteers doing what they do best: crying for their rate cuts.

If anything, home buyers are impatient and will soon justify paying the higher rates as context shifts. The argument that rates were a lot lower a couple years ago will have just as much meaning as the old-timers saying that rates were double digits when they were younger. How long will people just give up waiting a few more years for rates to fall where they were and accept the new reality?

The buyers haven’t figured it out yet but as prices keep on rising eventually they’ll figure it out. Get in on the ground floor before home prices double again.

“Get in on the ground floor” 🤣❤️

have you looked at the home price charts? Get in on the top floor and take the elevator down?