Fascinating: “Prices that families pay” when they buy homes “can affect their overall well-being.”

By Wolf Richter for WOLF STREET.

The housing sector – rental market and purchase market – is one of the most interest rate-sensitive sectors of the economy and “an important channel of monetary policy transmission,” Fed Vice Chair Philip Jefferson said today at the Mortgage Bankers Association conference. In plaintext, as we’ll see in a moment: The Fed is counting on its higher policy rates to do their thing to the housing market (rental and purchase), with the ultimate goal of lowering demand by households in the broad economy.

It’s good for the Fed Vice Chair to spell that out because the housing industry with its incessant hype and hoopla wants everyone to believe otherwise.

The recalcitrant rents?

With its monetary policy of 5.25% to 5.5% rates and $1.6 trillion in QT so far, the Fed has been trying to push down demand to remove some fuel from inflation, and that has worked to some extent. Inflation has come down a lot, but then reversed course, with the hugely important measures of housing inflation – Rent and Owner’s Equivalent of Rent – having remained stubbornly high at 5%-plus in recent months. Against all expectations. And that has turned out to be a bummer.

Jefferson explained away the persistently high rent inflation by pointing at the theory of the “lag effects,” where asking rents take their goodly time before becoming actual rents (the inflation index Rent measures actual rents that current tenants pay, not asking rents which are advertised rents), a theory that we have had to listen to for about 14 months, without seeing a lot of results as rent inflation has remained persistently high.

7% mortgages slowly crimp consumer spending to bring down inflation?

“The current restrictive stance of monetary policy has weighed on the housing market” by bringing “supply and demand into better balance” – thereby ending the crazy price spike that had occurred during the pandemic – and putting “downward pressure on inflation,” Jefferson said in the speech, but it hasn’t been enough yet.

One reason why higher policy rates have not been fully transmitted into the economy is the very common 30-year fixed rate mortgage where neither the mortgage rate nor the payments change for the life of the mortgage. “It is often argued that this loan structure dampens the effect of monetary policy,” Jefferson said.

While the average current 30-year fixed-rate mortgage interest rate is at around 7%, the average rate on all mortgages outstanding is below 4% as households refinanced into lower mortgage rates during the pandemic, and are now slow to sell or refinance the home to get a more expensive mortgage.

There is a delay between when mortgage rates rise in response to higher policy rates, and when the total amount in mortgage payments in aggregate rises as more mortgages with 7% rates make it into the averages.

So “households in the U.S. borrowed over $1.5 trillion in new mortgage loans in 2023. These borrowers include first-time homebuyers, existing homeowners moving between homes, and homeowners obtaining cash-out refinances,” he said.

These households that got 7% mortgages recently will be spending a much larger share of their income on mortgage payments, than households with a 3% mortgage of yore. And as those households with the 7% mortgages will have less money left over to spend on other stuff, “their consumption may be correspondingly lower,” he said.

This is the way higher policy rates work their way into demand for consumer goods and services, by forcing households with 7% mortgages to cut back on buying other consumer goods and services, which reduces consumption, and thereby demand. But it’s a slow process.

“The cumulative effect of a higher interest rate on aggregate mortgage payments grows over time as more new loans are originated at the higher rate,” Jefferson said.

Home “prices” too high?

“The housing sector is where many households have made, or will make, their largest investment. Therefore, the prices that families pay for that housing can affect their overall well-being,” Jefferson said without elaborating further.

This is fascinating. The “prices that families pay” when they buy the home – not the prices they get when they sell the home – “can affect their overall well-being.” Purchase prices that are high can mess up a family’s “overall well-being?” Is it finally sinking in? After years of purposefully inflating said home prices?

The conclusion seems to confirm that: “The housing sector is also a key part of the transmission mechanism of monetary policy” – that is trying to bring inflation down. “That is one reason why policymakers will continue to pay close attention to this vital sector,” Jefferson said.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Howdy Folks. No money down loans, No income verification loans, No Red Lining, Community Reinvestment Act, and lets go ZIRPing too and see what happens……

Free beer and a housing crash tomorrow.

This article was neither about “free beer,” nor about a “housing crash.”

T’was about “inflation.”

“Transitory” according to some old goat.

But then, I guess, we’re transitory too.

Keynes/DC – “In the long run we – and by we, I mean I, – are all dead…so eff the debt and the future”.

Modest house in Lawrence KS I looked at today went from tax appraisal of $238K 2020 to $409K 2024…

Federal reserve destroyed the housing market in the short term with sub 3% 30yr mortgages and 2%+ 15 year notes…

Also an example of why people don’t trust inflation numbers, housing inflation has been ridiculous…

Houses are assets and are part of asset price inflation, not consumer price inflation. Consumer price inflation covers consumption items, goods and services that consumers consume. Asset prices go up and down, and they can go down a lot. Consumers prices in the US overall almost never go down. Big difference. That’s why they’re tracked separately.

Unfortunately when the one item you really want to purchase for yourself or your family is a house, which is not in the CPI basket (at least not directly), then the CPI figures have very little meaning to you.

I have a feeling that with the 30-yr mortgage lock-in effects, they’ll have to keep rates high (or even higher) for even longer than they’re thinking just to undo those effects to bring inflation down*. And that’s just the rate of increase, we’re all still screwed on the price levels.

*OR they’ll just switch up the inflation formulas, and… presto! Wow, now we’re magically at 2.0% inflation, would you look at that!

Bailouts4Billionaires

“Unfortunately when the one item you really want to purchase for yourself or your family is a house, which is not in the CPI basket (at least not directly), then the CPI figures have very little meaning to you.”

Jeeeeesus.

House price inflation is in other indexes that we cover here. Maybe you people never ready anything here so you don’t know it???

To find food inflation or used-car inflation, or services inflation, you go to our articles about CPI.

To find house prices inflation, you go to our many articles about house price inflation. AND READ THEM.

Wolf,

People don’t care if they are getting screwed by “consumer” or “asset” inflation (note, one person’s asset tends to be somebody *else’s* liability vis a vis housing rental) they just know that their total gross costs are going up…with zero improvement in value.

And, as you correctly point out, asset valuations are volatile (largely driven by erratic/incompetent gvt decision making, operationalized via interest rate changes) so even the putative “beneficiaries” of allegedly benign “asset inflation” are continually under threat of reversal/collapse (especially late buyers vs early buyers).

The only entity that really profits from this print-driven casino-fication of the macro economy is the Printer in Chief/Master Forger his-own-self, the G – who’s habitual deficit spending is financed by the Fed’s printed money (and the parallel, unvoted expropriation of dollar savers).

The government = taxpayers ultimately. So if the government is “the only entity that really profits from this print-driven casino-fication,” then it’s actually the taxpayer that benefits, is that what you’re trying to say?

Didn’t mean to rile you up, and I’m still not quite sure what the disconnect is. Cas127 captured my thoughts nicely. The larger point is that the fed doesn’t seem to care that millions of people have been priced out of buying a home and more and more people also become homeless (or “unhoused” whatever the term is) as a result. Yes there are other inflation indices and very well covered here (and appreciated!), but if the fed doesn’t care and lowers rates anyways (and slows down QT, per their dot plot and public statements, also seemingly taking rate hikes off the table), we’re stuck with the inflation and the asset holders get bailed out again and again.

I think when Cas127 refers to “government” he’s referring to the political class just looking to get themselves re-elected and take as much from the system as they can. Handing out tax breaks to their special interests like candy and running up the debt without a care for future generations. (Just my interpretation).

Let’s say wages go up 5%/year and housing prices go up 3%/year, on average, over the next 14 years. That would bring the inflation adjusted cost of housing down from 8x income, to a mere 6x income. So, that addresses the price side of shelter costs. Now, let’s talk mortgage interest expense, and the yearly inflation of taxes, insurance, and maintenance….

So lets say wages go up 4% a year and houses go down 4% a year. It doesn’t take that long. You’re hung up on house prices always going up. They’re not. Prices of existing homes stopped going up in June 2022 on a nationwide basis. And prices of new houses have dropped a bunch already.

To see what can happen with real estate, look at CRE which has been blowing up just fine for the past two years. And massively so. Investors and banks are taking huge losses. Developers are having the hardest time getting funding for anything. Refinancing many maturing loans is nearly impossible because lenders refuse to do it at the amounts needed to pay off existing loans. This is a HUGE mess, and we’ve been talking about it here for two years. But you can’t lose money in real estate?

The ideal scenario would be wages going up 0% per year and housing prices going down 10% per year for 4-5 years. That would fix a lot of problems in the US economy.

There’s something called “money illusion”. There should be a “real estate price illusion” added to the pantheon of human fixation. AKA: cognitive bias.

If inflation gets to 6% or 7%, the 3% house price inflation means prices are going down 3% or 4% a year. I think we are on the same page, but in an inflationary reference frame.

But I hear you though. Prices fell markedly for years in 2008 and it is likely to happen again.

@HowNow,

I assure you that over the 14 year time frame I outlined, home prices will go up averaged over that time frame, yes, even from current nosebleed levels.

The more relevant things are that:

1. While it is true that NOMINAL house prices have gone down maybe 4 years in the last hundred years, INFLATION-ADJUSTED house prices go down maybe four or five years in twenty. Think 2008-2012.

2. When you figure REAL interest rates, rather than nominal rates, you can see that there is a rather large affordability cycle.

I expect inflation to stay around 6% for the next 2-5 years, because I do not expect the federal deficit to drop much below $1T per year any time soon.

The Fed has an ugly choice: Juice the economy by holding nominal interest rates below inflation, or try to bring real inflation up to 2% while risking some ugly unemployment numbers.

Decisions . . . Decisions

Fat fingers:

I meant to say “bring real interest rates up to 2%”.

Free Bear was a San Francisco punk band.

Holy random references, yeah i remember that band. Tommy Guerrero played bass I think. Check out his solo stuff on guitar, pretty cool. Met him once back in the bones brigade days after he won a contest, guy exudes cool.

haha by this definition, I guess every household that bought in SoCal in the last 3 years must be insane or close to one layoff away from slaughtering each other. I know thinking about housing price and having to pay insane money for very little makes me depress everytime..

“Fascinating: “Prices that families pay” when they buy homes “can affect their overall well-being.”

Sorry for this comments but even my dog understand this:

“Fascinating: “Prices that families pay” when they buy homes “can affect their overall well-being.”

Yes, high prices mess up people’s well-being. The Fed finally gets it. Even my dog understands that.

Since 88% of all mortgages are agency backed, all the FHFA has to do is roll back the conforming loan limit to 2019 levels, and then let market forces bring down prices. There truly are easy fixes to this problem, but bottom line, those people holding appreciating assets aren’t willing to give up their gains. No one thinks out the long term consequences of their actions anymore. Showing egegious disrespect for the under 40 cohort won’t end well under any scenario.

“Showing egegious disrespect for the under 40 cohort won’t end well under any scenario.”

LOL, the BS and lies people are trying to post here and elsewhere about boomers is often outright bigotry. I now delete nearly all of it, just like I delete antisemitic posts. This BS has gone waaaay toooo far.

Typo — the under 40 age cohort, not 49. And I’m not talking about the upper 20%, but rather the lower 80%. You know… the overwhelming majority.

I bought a junkie rancher in Northridge, Ca for over $730,000 3 years ago and am trying to get over it, I understand how high prices can negatively affect your well being. It’s now worth $850,000. Go figure.

Why does this article bring out the silliest comments??? There are already a whole slew of them here, and we just got started. Also see below, LOL

Because your articles are controversial but interesting and most people are not finance and economics experts. So they write dumb comments to be funny or insulting. I see this on every financial article I read. Play stupid games, win stupid prices. Most readers are clueless to reality in financial markets. Linked in and SA authors get the same… let it go.

Most people only want to talk about their gains(wins)….not their losses(mistakes). Nature of the beast.

I have had a rental for 18 years. Low income rental neighborhood. Very little margin.

I bought it in 2002 for $58k. During the HB1 it rose to $78k. I should have sold. There were lots of subprime foreclosures in this neighborhood from 2010 to 2014 in this neighborhood. You could buy the houses for $40k but they would take $30k to renovate and still only be worth $50k. So price went nowhere for years. Wife wanted me to sell. I said….for what…$40k. I told her this was rock bottom. Luckily, rent never really dropped even though price dropped 30%. Afterall, where else could you rent a 3 bedroom, 1 car garage on a big log for $600 or less. But if you wanted to buy a house here on a 30 year loan, you were looking at $350/month house payment. LOL

Anyway, prices got back up to $60k by 2018. Thus, it took 16 years for $k of price appreciation. Thanks to the pandemic, it is probably worth $140k now. But I had a tenant trash it 4 years ago and it cost $40k to rehab. So after 22 years of owning this rental, I have a net operating loss of $20k because of crappy tenants.

Tenants over the years have paid off the mortgage so that is a plus. But from a cash flow perspective, this has been a negative asset and looking back….a waste of time. I will make a little profit when I sell but I am holding on as I still think this house goes to $180k which would put it at 3x local median income.

Needless to say, there are still some regional bargains. I get calls and letters weekly from investors to buy this house.

What it’s worth is an objective discussion. Sounds awful, I’ll give you 350.

An asset is only worth what a buyer agrees its worth with the seller. It is the buyer that brings money to the contract and Money buys a lot of options for the seller in how they will spend it.

You won’t believe this but the ask price for real-estate has the Agents fee built into to it. This knowledge is a pry bar when in negotiations, along with faults and defect of a building inspection.

In 992I brought a new, never occupied display home off the bank for the cost of the asking price of the block of land across the street. I was unconditional no finance.

“worth $850,000”

Actually, it ain’t worth 850k until you actually sell it…no matter what the Zillow Zoomcaster (or whatever it may be called) says.

Just ask those pyramided housing “millionaires” of 2007 who had 3 homes foreclosed on by 2011.

Good (important) point. Maybe this will keep Phoenix_Ikki’s and Lily Von Shtupp’s shirt on. If they weren’t paying attention when a few of the several housing busts took place, maybe they’ll trust your observation.

Another variable is wage growth vs a fixed rate loan.

One third of your revenue becomes 1/5 after 10 year if you get a 4% wage increase each year.

Applicable either to old or new loans, if sustained inflation is a boon to fixed rate indebted working homeowners.

Edit :

One third of your revenue as mortgage payment becomes 1/5 after 10 year if you get a 4% wage increase each year.

Let’s see – 46% of homeowners live in the same home for 6-10 years and 35% for 10-15 years. It’s going to be quite a while before high rates meaningfully impact the housing market.

The fed’s policy clearly forgot to look at some basics facts in the real estate industry. They also failed to engage their brains by thinking folks are dumb enough to trade a 3% mortgage for a 7% mortgage.

Because of low mortgage rates the payback from refinancing and moving will be much slower. I wouldn’t be surprised to see the average mortgage duration increase to over 15 years for those folks with 3% mortgages.

It is important to remember that about 4 in 10 owner occupied homes across the country don’t have a mortgage with about 6 in 10 homes owned by seniors owned free and clear. It will impact a few people but I don’t see many (e.g over 10% of homeowners) deciding on where to live based on the interest rate on their first mortgage. I don’t think that many “average” college educated families that bought a “median priced” home ten years ago for $200K in their early 30’s are going to focus in the ~$120K low rate debt they have on their home that is probably worth close to $450K today (couples in their 30’s tend to spend more than average to “keep up with the Jones’s” and a homes owned and improved by couples in their 30’s tend to appreciate above average (and WAY more than homes owned by people in their 70’s and 80’s since people in that age group rarely do a lot of improvements to their homes).

CCCB

Seems you forgot to read the article?

You said: “The fed’s policy clearly forgot to look at some basics facts in the real estate industry. They also failed to engage their brains by thinking folks are dumb enough to trade a 3% mortgage for a 7% mortgage.”

The Fed said in this article: So “households in the U.S. borrowed over $1.5 trillion in new mortgage loans in 2023. These borrowers include first-time homebuyers, existing homeowners moving between homes, and homeowners obtaining cash-out refinances,” Jefferson said.

Howdy CCCB YEP. Will the prisoners realize they are trapped? Hopefully some learn about HELOCs and uncuff themselves…..

“They also failed to engage their brains by thinking folks are dumb enough to trade a 3% mortgage for a 7% mortgage.”

Reading the article it seems they’re quite aware of that. It also seems they’re not aiming to convert 3% mortgages to 7%, not sure where you read that, they hope to raise the average with new mortgages from new buyers.

Seems like a very very slow process though and only new buyers doing all the lifting in bringing inflation down with reduced spending, I dunno how well that’s going to work out if 3% crowd keep spending as usual and maybe more if they’re getting raises and collecting interest on some investments as well.

I think you missed the point of the article. It wasn’t about how long it takes for high rates to impact the housing market (they already have), it was about how long it takes for these high rates to reduce aggregate demand and inflation (via the housing market).

The high rates have already had a huge impact on the housing market (see existing home sales and new home prices).

Are the higher rates included in the CPI statistics or simply mixed in with all the other ingredients. Like Prego Spaghetti sauce?

It’s kind of like the price of oil: If the price of oil goes up, then the price of everything goes up (in 3-4 months).

Same thing with the price of loans: If interest rates go up, then the price of everything goes up, after a few months.

“They also failed to engage their brains by thinking folks are dumb enough to trade a 3% mortgage for a 7% mortgage.”

Given the choice I agree that is a bad trade, but there’s lots of folks in the “must sell” category due to a variety of life circumstances.

It would seem so but I have known people, in need of cash, refinanced in the manner that assures their financial destruction, if they live long enough.

A bit lengthy: I was trying to remember what era it was when I heard of farmer/peasants who had to sell their children to pay their debts. I thought it was in the Middle Ages. But I was corrected by the AI system that Google is now employing to improve their searches. Here’s the reply:

“Neither was common. Sons and daughters of peasant farmers usually married sons and daughters of other peasant farmers. I assume you are asking about selling children into slavery to pay off one’s debts. That was more commonly the practice in the Ancient World, I.e. Mesopotamia, Greece, Rome.”

All this to say that creditors and debtors have been at it throughout our history.

You know you are getting a bad deal, because parents would only sell kids that are more trouble than they’re worth.

Germanic peoples sold their children to the Romans as slaves, because they were trapped outside the walls of Rome and starving to death. They were fleeing the horrors of the Huns. Unfortunately for the Romans, things did not work out so well. I guess they didn’t learn their lesson the last time they tried screwing the Germans. I think the story you might be thinking of started with Alaric and ended with the Vandal King, Gaiseric.

There are always some “involuntary” sales despite less than ideal interest rate conditions — the three D’s (death, divorce, diapers), plus factors like foreclosures or layoffs forcing relocation that increase in a slowing economy. Not everyone can choose to sit tight waiting for just the right combo of interest rates and prices.

What is today’s market value of the 3% Mortgage for the lender? If the same quantum Mortgage today demands 7% then someone has taken one H of a loss on the Net Present Value of the original loan.

The value of a “low coupon interest rate” mortgage depends on your assumptions about duration. If you think that the borrower will stay in the house for 7 years, then you would pay more for the mortgage than if you think they will stay in the house for 12 years.

I don’t have my HP12C handy :-( , but the lost interest would be $4000 per year on a $100k face value mortgage. So, you would ballpark it that a reduced propensity to refinance or move would turn a $28000 loss into a $48000 loss.

As always, your mileage may vary.

I should’ve never decided to pay off our degrees and cars. My thought was, it’s the responsible thing for my wife and I to do. But there went the down payment for the house. Now the market is so absurd I have no desire to even participate in it. I don’t want to over pay, deal with the taxes, insurance, and maintenance. Pretty sure we’ll be renting from here on out. This country is a mess. We make 250k a year and have been priced out of the market for years at this point, maybe permanently. Never thought I’d say this in my entire life. Depressing to say the least. Oh well.

Did the same thing, paid off loans after residency ended in 2020. I keep coming back to this website seeking news/ catharsis that I will have a place i own to put my family soon but nope. Wolf keeps telling it like it is. And it will be awhile or never that I will be able to. All my friends that I thought were frivolous and ignored the student loans and high price of housing made out like bandits and are laughing now. I spend a fair amount of time just reorienting myself and reminding myself that having a bunch of stuff doesn’t really make one happy. And that in the scheme of the universe… or humanity… or my life. Things are just fine. I gotta go do some living with my family instead of re-engaging my feeling of FOMO.

I feel ya, I watched the majority of my friends most of whom make about 50% less than me buy houses with 3% down at the max their lender would approve them for. They have student loans, car loans, credit card debt and don’t contribute much of anything to their 401Ks. It seemed so foolish at the time. Knowing what they make I’m not even totally sure how they afford their payments even at 3%. I paid off my student loan and have no car payment, contributed to my 401k a reasonable amount, waited until I had saved 20% down plus 3 months emergency savings, wanted to be at my new job for 6 months to ensure it was stable, etc all the “right choices”. I could buy right now, but it seems insane to buy something that run down and falling apart for $650K at 7%. So I may never own a home and I have to listen to everyone talking about how they made $100K and that they’re a real estate investing genius.

We now seem to be at a point where the markets reward financial illiteracy and/or excessive risk taking. My roommate who didn’t go to college, was pretty much permanently stoned, and supported himself by working part time for a grocery deliver service made a ton on meme stocks because he thought they were cool – no research, no financial analysis, he just bought whatever everyone else was buying because it was cool.

Yep. Momentum traders. Some get luckly. Most do not know when to stop.

Level 1 in trading is when you make some good/lucky trades and think your smart.

Level 2 is when you make a lot of money losing trades and you cannot believe just how good you are at losing money.

The trick is to not give up, learn from level 2 and try to move to level 3 if you still have any money left.

Level 2 is you make a lot of trades that lose money and you are amazed how good you are at losing money.

The government is bound and determined to turn the story of the Ant and the Grasshopper on it’s head. Financialization to the moon, baby!

correction: “made 100K on their house”

Your comments here reminds me we need a support group for people like us, the non-FOMOyers, then again maybe I am doing too much wishful thinking but in the back of my mind, I am always thinking of that analogy of when the tide goes out, you get to see who’s swimming naked, at least that won’t be us. If that time does come in another multi-verse perhaps..

There’s also another important point about lack of moral hazard in our current financial system and how that can wreak havoc to others that are prudent and trying to do the right thing…

“I am always thinking of that analogy of when the tide goes out, you get to see who’s swimming naked”

That happened in 2008 crisis. I pray it happens again. I too feel like a schmuck for having done the responsible things in life, paid off my student loans, paid off cars, etc. This country used to be about personal responsibility but has changed, and I’m not loking it one bit. The pendulum always swings to both extremes. I’m hoping it swings back to rewarding the responsible soon.

You are in a support group, PI.

Good lord, some of the comments on this site are just insufferable. Stop whining and move to a place where you can afford a better standard of living. If your residency is done and your loans are paid off, you can probably get a job anywhere you’d like. Either you live in an expensive city or you’re terrible at managing money (or both). But those conditions are correctable. Just move. I was hopelessly stuck in the L.A. area where I and my wife made decent money, but couldn’t comfortably afford a bombed out shack near terrible schools. So I got a job making the same money in Albuquerque. We live in a nice house on a 1/4 acre corner lot in a great neighborhood and we can comfortably afford it on just my one income. My wife is now free to focus on our son instead of working herself into insanity to pay daycareless workers to raise him. And his school is amazing. It’s leaps and bounds nicer than the dumps I went to as a kid. Moving was the best decision I’ve ever made for my family.

It’s been a little while since I’ve commented, but your pity party was just too much for me to resist. It’s that bad. Find a more affordable city that you like, pick up an abundant healthcare job in like 15 minutes, rent for a little while if you need to, and then buy a house that you like within your budget. Don’t get hung up on timing… As Mr. Munger once said, “The time to buy a house is when you need one.” Even if you overpay a little, don’t worry. The money printers never really stop, so whatever today’s price is won’t seem like a big deal 5-10 years down the road anyway. If the price goes up, great. If it doesn’t, then you still have an asset that you’ve paid down a bit. At least you won’t be waiting your life away. This ain’t rocket surgery. Geez.

Even Detroit is starting to get net in-migration (for the first time in 66 years or so) due to those dirt cheap houses. Houses too expensive where you live? Then look elsewhere.

Optionally, buy 2 houses in Oklahoma and rent them out while renting your place in LA or Brooklyn. The rent on the rentals can pay their mortgage while enjoying both the appreciation and a decent life in the big city.

“Good lord, some of the comments on this site are just insufferable. Stop whining and move to a place where you can afford a better standard of living.”

Took the words out of my mouth. If they can’t live in San Diego life is not worth living?

Heff,

Not only “in San Diego,” but it’s gotta be my “dream house in my dream neighborhood in San Diego.”

Lots of sour grapes in the comments.

I dunno – I sympathize with wanting a house, but I make 50k and managed to overpay for one in early 2021.

“I don’t want to over pay, deal with the taxes, insurance, and maintenance”

Ok: but you have to “deal” with those things no matter the price you pay. So do you really want to own? Renting sure is less work.

yes this is the way. worked for us also. a house is not an investment and prices going up are actually bad for the home owner as well. you have to live somewhere. All expensive housing does is raise taxes and insurance making a 100k on a house is the same as increasing your expenses so not actually a good thing.

I’ll take issue with: “Stop whining and move to a place where you can afford a better standard of living.”

For giggles, I looked at my hometown of BFE, Kansas versus the suburb I live in here in Texas. Price per square foot is identical and the lot sizes aren’t radically different; in fact, in many cases, they’re pretty much the same. My hometown, BFE, doesn’t have anything going for it in terms of high paying jobs and is mostly propped up by AG and service sector stuff that doesn’t pay much. (to wit: the median household income in ’22 was 55k)

But you mean to tell me that the house in town is 350k+? It seems scary to me when two places 500+ miles apart have the same housing prices and one has an actual reason for the pricing (demand, ostensibly) versus the other. It’s become unmoored from geographic location, amenities, taxes, and industry (in terms of jobs to support the pricing). I welcome the high interest rates and choose to sit it out while I watch the drunken sailors keep drinking. At this point it’s monkey see, monkey do in the markets and is purely cynical speculation.

AngryMilennial,

You might want to expand your search beyond two cities if you want affordable housing.

In fact, you might want to expand your search beyond cities in general. They’re usually overpriced – although the above commenter mentioned Detroit having cheap homes.

“Insufferable”, yes. Move. If being able to tell stories about celebrity sightings, tolerating insane levels of traffic, and paying for everything through your nostrils is worth indentured servitude for an “effin” house, then suffer.

There’s more to life than weather and living within ten miles of a celebrity or godforsaken influencer.

Appreciate the insight above. We have a great community of humans around us that would be difficult to replicate. So HCOL It is for us… for now. So yea truth in I wouldn’t feel the desire to process the new cost of things if I moved to a LCOL area. And whining accomplishes nothing so apologies to get ya worked up. I like my community and hope to make it better not just for me but the people we love in it that are having a difficult time making things work. Maybe we all just move to a commune together somewhere cheap and stop paying for clothes and run wild naked.

Howdy Forever Renter. WOW. 250 K a year? How long has that been going on? Save any of that or spend it all? SAVE SAVE SAVE or become Debt Free????

$250K and can’t afford a home? Seriously?

As a business acquaintance once said when we were discussing an expansion of his facility: “Man, you thinkin’ way too big”.

Most of us geezers played the property ladder game. First one wasn’t all that and a bag of donuts. Second one was a step up. Third one was the trophy…. and then the fourth one? In our case, it was smaller, fewer (but larger) rooms, and ambiance.

I doubt that many bought their dream “my homies are gonna be impressed” house right out of the box.

Howdy El Katz. YEP. Purchased my first POS house at age 20. Friends would not come by because it was a POS. No friends and 30 something houses later. Life is good. Did not move that many times but HELOCed my way to prosperity. Hear that 3% ers?????

$250k income is barely adequate to buy a home in many locations.

In Seattle suburbs, a plain home in a decent school district is at least $500-$600 per square foot. A 2000 sq/foot 3 bd/2 bth starter home goes for about $1.1M. If you want 3000 feet, it’ll cost around $1.6M or so.

That’s 4-9x gross income for something old and plain.

I think the best advice in these areas is to rent, not buy, otherwise you could lose several years’ pay if/when home prices decline. If you need or want to buy a house right now, I suggest moving to a more reasonably priced location to limit loss potential. The goal is to provide financial security for your family, not fund somebody else’s retirement.

Of course, opinions will vary on the direction of RE prices, particularly when the Fed insists on pursuing a soft landing via years and years of elevated inflation.

Decision-making has become difficult, if not arbitrary, as a result of monetary and fiscal policies that foster moral hazards.

Remember that the property ladder game is zero-sum. It’s like telling people that you beat everyone at Monopoly and so they should too.

“Monopoly”, the game, was invented by a socialist who wanted to show that as players became more greedy, they would ruin everyone else. Here’s an entry from Wikipedia:

Monopoly is derived from The Landlord’s Game, created in 1903 in the US by Lizzie Magie, as a way to demonstrate that an economy rewarding individuals is better than one where monopolies hold all the wealth.[1][5] It also served to promote the economic theories of Henry George.

I am a landlord and have helped many a resident buy their first home. Needless to say we don’t overcharge.

I always tell those who are looking for a first home to look at duplexes to four plexus because you can get conventional financing and let the resident pay some or all of the mortgage. Plus all the deductions you receive are really nice to reduce income taxes. Also, your first purchase is rarely your last and your rental property becomes part of your retirement. Think out side the box for crying out loud.

“That’s 4-9x gross income for something old and plain.”

@Bobber,

You’ve hit the nail on the head. Homes are 4x income for the top 10%, and 9x income for the lower 70%. Go back 50 years, and the housing situation wasn’t this bifurcated.

Most of the people here have never seen an environment with higher for longer interest rates. Every asset was a winner thanks to the Fed’s 40 years of declining interest rates. Almost anyone who bought or speculated was a genius. Now days you better take a good look at capital.

You have my sympathy and I am more or less in the same boat. Difference is, I am not priced out and have more than enough for down payment but simply doing this little thing call buyer strike (purely by choice) which apparently majority of people in SoCal can’t seem to wrap their head around as Wolf pointed out before and also as seen by many commenters here complaining about price and yet still try to outbid each other…

Plus part of me as depress as it can be at times, still can’t shutoff the logic part of my brain to accept the fact that you can do a half a mil down payment and still pay $8-9k a month (mortgage, property tax, insurance..etc) for 30 years for a run of the mill house, that’s a tough pill to swallow…call me stubborn.

That’s me as well. But it has gotten somewhat better now that I am at least collecting 5.5% risk free on that down payment. It has also made me less interested in buying a house.

Same here. I’d rather have my money earning 5.5% than to pay for some overpriced sht shack money pit.

The people who bought my 1300sqft home from me in 2019 are paying obout $1100/month right now in just property tax and HOA fees. Meanwhile, I’m paying $2300/month right now to rent 1000sqft, living 3 miles from the beach, in what is arguably the nicest place in the country. Who’s the sucker?

“Pretty sure we’ll be renting from here on out.”

I thought the same thing when I was in my 20s-30s. If you’re younger than 40, give it some time…as in a decade! A lot can and will happen. Too many young people wanting to buy homes RIGHT NOW sound like 25 year olds saying “I’ll never find a spouse!” Come on, check back in when you’re 35.

People I know aren’t impatient so much as nervous. We’ve been watching this bubble growing for like 15 years with no end in sight. The expectation that things will only trend upward is a lot more tenuous in our de-facto centrally managed economy.

I also know plenty of people who were afraid they’d never find a spouse in their 20s, and we’re now in our 30s and 40s without any luck. You see it in the birthrates. I don’t think the old rules apply anymore. There are all kinds of interesting theories as to why, and many whole books written about it. I think there are plenty of things that could be done about it but following the status quo isn’t one of them.

Don’t worry, you’ll be able to afford a 30 year mortgage just a few years before your income disappears?

Sounds like a sound decision. Debt becomes a master.

Why the doldrums? Quarter mil a year in income should position you quite handsomely in just about any market minus maybe Malibu, and it’s gross there anymore anyway.

$250k in a HCOL area is not that much when you consider taxes, sales taxes (like double taxation) retirement, savings and healthcare.

And rent prior to buying is high so savings isn’t much.

For those that don’t live in a HCOL area it can be hard to fathom.

And yeah, you can rent a dump in a dangerous area but why? For a chance for a house one day in a not so dumpy area.

OP should just rent something decent and not worry. Owning houses in HCOL areas often mean owning something with deferred maintenance as the original owner aged out.

I’ve moved/lived all over the US. HCOL to rustic little armpits in FOC. Living in Austin last 16 years — which is overpriced as hell but still…good. All to say, I think I have a pretty reasonable vantage.

$250K annually is solid remuneration for any jockey. Live beneath your means a few years & then gradually move into a more comfortable band. Money isn’t the problem here — it’s the markets that are the problem. Be patient and let the jackassery boil off a bit more. You’re doing damn’d well!

Don’t forget that you have to make that $250K for 30 years with zero lapse in employment

Exactly. I’ve been making that much for the last two years. My first thought was to pay the debt off while I knew 100 percent for sure it could be done, while stashing some cash on the side. So I did it. Three degrees and two cars between my wife and I cost a lot of money…. The cars are modest. I literally buy clothing from Walmart and Target.

Who wants that debt hanging over their head while maintaining an overpriced depreciating asset? Apparently a lot of people do from the sounds of it.

In regards to the move comments. No, I’m not going to move. Mainly due to the fact my skill set and occupation is heavily needed at my present location. Long term, this provides me with good employment opportunities should something unfortunate happen. Ask the WFH folks who moved away from Silicon Valley and bought homes how they feel after a layoff. Plus, lower cost of living just means lower pay. Home values are up across most of the country.

Yes, I will sound insufferable to some people. But at least I’m trying to be responsible, reasonable, hard working, and patient. So maybe the people (older folks in most cases?) who are griping about me complaining should be thankful some of us actually still try to behave responsibly for crying out loud. Btw, back to work. Thanks for the replies.

At age 25 I experienced 18% mortgage rates and also thought I would never own a home. 5 years later I bought my first home with a 10% mortgage, refinanced it twice and fully paid off the loan years before it’s maturity.

This has all happened before… An average person will experience 10 complete business cycles in their lifetime. Your frugality will be rewarded. You are doing the right thing

“Purchase prices that are high can mess up a family’s “overall well-being?””

(… fewer kids, having kids later in life, delayed household formation)

unless said family is in the FIRE sector.

“Purchase prices that are high can mess up a family’s “overall well-being?””

Most peeps are payment buyers. We never were. We might have “underbought” or bought an ugly ducking (as they call them “good bones”), but 100% of the time (good economy and bad) we came out at least financially alive.

High asset prices are the principle side effect of QE, the reality of MMT.

I think that Matt Taibbi described Stefany Kelton’s understanding of monetary authority as a chimera was insightful, not spiteful.

So…where was this ‘concern’ for the housing market during the decade plus the FED was unnecessarily (and illegally) loading up on MBS.

There have been more and more indications that the Fed is coming to grips with the issues caused by its prior monetary policies.

Tom Hoenig will have the last laugh.

Hoenig was seated at the Fed’s table for years. I heard him say the table discussions always focused on tackling immediate issues, with hope of tackling long-term issues later. It’s this continual procrastination that allowed moral hazards and financial instabilities to thrive. It’s no wonder stock and RE prices are at insane heights, relative to income/GDP, to the point where asset prices are stoking elevated consumer inflation.

They refused to accept a small recession earlier, so now they’ll have to deal with a bigger one at some point, unless they plan to inflate until the entire economic and political system buckles.

Wolf,

Other than more aggressive MBS QT, what options does the Fed have to force housing prices down?

The Fed cannot “force” anything. It can raise or lower its policy rates, and it can increase or decrease its balance sheet, and hope for market reactions.

@TulipMania I think that’s the wrong question. A better question would be “What options do the financial authorities have to stabilize the economy?”

The Biden people (Treasury Department) mainly want to have the voters stop noticing inflation long enough to get Joe re-elected. Congress is similar.

As Wolf points out, the Fed has control over short-term interest rates, and a modest amount of influence over 10-year rates. That’s it.

Right now, the fact that most major parameters in the financial and monetary system have a 3-18 month lag means that there is pretty much nothing they can do to fix this mess before November.

“The price you pay for your house is more important than the price you get for it when you sell.”

That is fascinating….I will be pondering that gem for awhile.

That’s not a quote from the article but from our own imagination.

Most wealthy person I know always says “you make money when you buy, not when you sell.”

And was always planning his exit in a buy even before buying. How long and difficult a safe may be for example.

I’ve heard the same “you make your money when you buy” tenet for decades. Both in real estate and the car biz. However, it’s the antithesis of the “what’smystrokes: mentality often displayed by the drunken sailors.

Read Hussman, this is his main thesis about any investment. The price you pay fixes your long term rate of return when you sell.

Search the phrase ”you make your money when you buy”… AKA “buy low sell high”.

A second verse

A home is different than a house. One cold and foreboding, the other warm in the glow of love.

My thoughts exactly!

I overheard just last night “I own 3 homes in that area.”

I questioned to myself: Are they homes or houses?

We have a LOT of “dark houses” in resort country.

Sometimes I wonder if getting an education means much. Either you have it or you don’t.

Decades ago a neighbors son who was an attorney told me that putting up a really nice looking fence around my backyard had reduced the value of my middle class home……..at the time I lived in an area where everybody had a fence.

This fed governor must have been drinking the same kool aid. By his numbers we just have to wait five to ten years for a good number of homes to be bought so folks will be paying 7% mortgages……. for monetary policy to work. Not much to do with the demand for housing…..and it’s price.

No wonder the governors seem to have a speech every day………there is no end to the crap they can create. Of course if I were getting paid 10 grand for a 30 minutes spiel I guess I’d come up with something too.

This is one factor why inflation will blow out in the coming years IMO.

Home prices aren’t going down anymore they’ve reversed losses in most markets and are now rising again

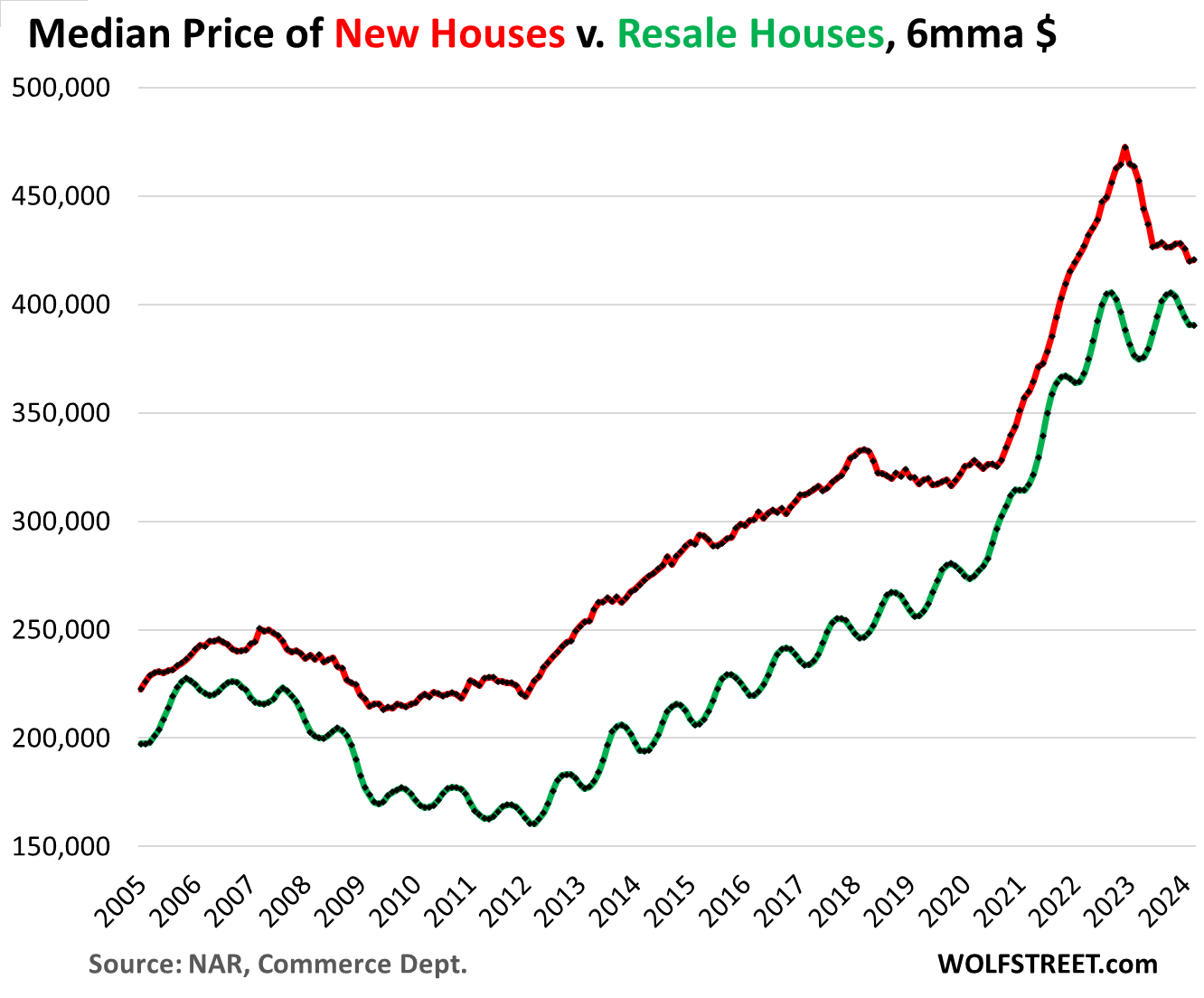

Wolfs chart above does show a double top but also shows a higher low setup.

Commodities are blowing out, bonds looking like they’ve bottomed or close to it, stocks blowing out (although with neg div)

Fed blew the soft landing last December with rate cut talks.

Throw in 33 trillion in debt, 3 terrible Presidential candidates, and a world on the brink of war

What could go wrong lol new ATHs baby🚀

As AI slowly takes hold over the coming decade or so, wealth will be further concentrated in fewer hands. Where is the money going to come from as the number of available high wage jobs drops year by year as home prices increase?

If no one makes any money, they cannot spend it, and so the wealthy will not get it. Simple as that.

A helicopter could crash?

“Fascinating: “Prices that families pay” when they buy homes “can affect their overall well-being.”

Indeed, but for the best, its the only way to keep up with inflation for most folks.

Zillow is showing that my home that I paid $770k in 2018 is now worth $1,355k that is $585k in my pocket, more money than I will ever save in my lifetime working as a forklift operator in this damned warehouse.

In lots of cities, home prices are down bigly already from the peak a couple of years ago, and in addition to the home losing purchasing power due to inflation, it then lost market value due to home price declines. Double whammy. People there said the same thing you just said. And then it happened. Home prices can sag and stagnate just fine for years and decades on a market by market basis.

Yes, a tiny sliver of metros are losing value, including the one you live in. So what? The fiscal dominance will drive housing prices higher almost everywhere. A $3+ Trillion/year forcing function cannot be overcome.

Look, do the math. Nationwide prices have been roughly down to unchanged since mid-2022. For prices to balance that way, the down-markets and the up-markets must be roughly in balance. Now Miami is starting to give. One by one.

Is it in your pocket?

Or just on a computer screen under net worth?

And if it is the only way you keep up with inflation how are the people that don’t own houses doing?

“$585k in my pocket, more money than I will ever save in my lifetime”

Try paying for gas or groceries with your theoretical dollars of home equity appreciation. Its not a gain until you sell.

The real investment of buying a home is that you don’t have to keep paying rent into retirement.

$770K house…gotta say, that is one helluva forklift gig.

If I had 585K in my pocket, I might have a touch of irrational exuberance and spend more like a drunken sailor.

In that case, the price I paid and the ethereal gain would affect my short term well-being.

Is it in your pocket? What about RE commissions and cap gains taxes?

Nevermore, there is NOTHING in your pocket until you sell.

Brilliant observation, if they make housing so expensive no one can afford eggs the price of eggs will drop and people will be happy again!

A simple law the Fed can lobby for to permanently end inflation: 99% of any income above current rent or mortgage payments must be delivered as a tip to one’s dedicated landlord or lender.

This should dramatically reduce consumer spending and finally get inflation into the 2% zone.

I see another nobel in economics coming their way.

You misunderstood. They’re NOT making housing more expensive. They’re making interest rates more expensive and houses cheaper.

Folks also manage their home purchases with smaller homes which is the trend we see. Also I imagine Gen Z are now buyers of homes as they form families as well just not as large as millenniums generation . Demand for homes is high in my opinion just not the larger homes . Builders are adjusting . The take I get from the Vice Chairman is higher for longer until housing too starts stabilizing. I think an area that could be influencing the trend for higher demand is the job creation from manufacturing, immigration , and migration of people from rural areas continues which increases demand for homes in the country where these populations are growing . Population growth is not even across the USA . Not even at a state level can one measure the demand . There are areas in Oklahoma that are in big demand yet the state probably is pretty flat on jobs creation .

“Folks also manage their home purchases with smaller homes which is the trend we see.”

Exactly why I bought a 960sqft ranch.

I grew up in a 900 square foot ranch…. 4 people and one bathroom, sadly with a tub only.

We survived. A house is a house. The people make it a home.

One bathroom can be tough at times. Fortunately the basement utility sink doubles as a urinal.

Urinals are in the eye of the beholder.

MM,

I actually put a urinal in a closet in my old house’s basement. It took a 3/4” plumbing line, but it was really sweet.

I intend to do that with my current house as well, but this one came with two utility sinks…

Wonder if more modest offerings and frugal strategies will be represented on the silly tv home shows before too long. No more granite countertops, 1.5 bathrooms, what a concept.

Population is growing in Florida but rent and house prices are dropping across the state.

There is a reference in the article about houses as an investment. They may be a speculation, they may even be a trading vehicle, but they are not an investment. they are a depreciating asset and they have the built in drag of mortgage costs, insurance costs, and tax cost as well as endless upkeep cost.

Even Warren Buffett has indicated he would have been money ahead had he rented all these years, and I would agree with him.

Do not agree. If you are a renter you are still paying for all of the above plus profit for the owner. The secret is to buy a home with a mortgage payment no higher than rent. That was my strategy 45 years ago and we have been mortgage free for the last 25 years. Plus, some extra property we own has a rental cottage that pays all taxes and insurance for that one, and also on our main home. Planning on buying another place as soon as it comes up for sale.

And the feeling of owning a home is quite wonderful in many many ways. It is a home, not just an asset.

At least someone here was smart enough to get a 20 year instead of a 30 year mortgage. Ten extra years of mainly interest payments stinks.

Get a 30 year, then pay extra principal to make it a 20. It gives you extra capital in the house you can HELOC if you need it, reduces the overall interest you pay over the years, and gives you the ability to drop your payment to contracted level if you have to.

Yes, it’s a home-and there is value to that.

It’s just not an investment. That’s all I am saying here. You are mortgage free, but your tax man has a superior position to you. Your insurance man and handyman are still lurking. Investments don’t have that kind of continuing burden.

Investments don’t keep the rain, wind, and cold out. Walls and a roof do that.

“ The secret is to buy a home with a mortgage payment no higher than rent”.

Great advice, but in May 2024, not possible.

Under normal markets the cost to rent vs buy are close.

At some point the market will adjust back toward long term averages. When??

“The secret is to buy a home with a mortgage payment no higher than rent.”

Keep watching Wolf’s awesome chart of OER vs house prices. They intersected from 2011-2012.

When it happens again, it is time to buy.

There’s still a 40% difference today. House prices need to fall 20% and rents need to increase 20%.

The crazy thing is this…in the grinding bottom from 2010/11/12/13 when it actually made sense to buy a SFR with 20% down and the rent would cover the payment …it was almost impossible to get a buyer to buy. First and only time I’ve seen that happen in Hawaii, that rent would cover the mortgage.

Blood in the streets and all that…

Yes. After 4 years of plummeting home prices from 2008-2012, Fear Of Jumping In (FOJI) dominated homebuyer thoughts and actions even though it made financial sense to buy. Who would want to buy a house when prior years dropped 10% per year and millions had foreclosed?

Housing Bubble Blogs predicted no end to the free-fall.

There’s still too much FOMO today.

Anecdotally, we bought a house in 2014 but I experienced severe fear.

What if I lost my job like 25% of my co-workers did at the time? Some of these co-workers were so underwater and over-extended that they had to foreclose after not being able to find a job for over a year. Some raided their 401Ks and took the tax hit to not lose their house. They couldn’t refi without finding enough cash to achieve the 80% LTV.

Even though house prices had fallen to 2002 levels(10 years of no gains), buying a house was very scary.

Read the book “Nomadland” to get a sense of the fear at the time.

I don’t agree. At all.

Property for property? My rent would have been close to parity with the mortgage…. and, presently, I’m living in a “free house” – paid for, in it’s entirety, by the last non-investment, consumable, depreciating asset we owned.

You just have to learn how to effectively manage your money…. and know how not to get fleeced when something goes haywire. Just about anything you buy is a depreciating asset. Even your spousal unit’s diamond ring. Yesterday’s lunch. Your shoes. The car in your driveway.

It’s just a matter of priorities. I like having a fixed *rent* on my dwelling. I can assure you that you can’t rent a home like this for what we pay (all in, including accruals for future broken stuff). Even if i invested the original price in 5% t-bills, I’m still ahead because this dump has appreciated in market value and the delta between what this would rent for and what I pay is a zero sum game.

Your mileage may vary…. but not everyone who buys a house vs. renting is a rube.

(PS: Buffett is a cheap azz…. lives in his original house, drove an old Caddy until the wheels fell of it, and had a flip phone up until the point he couldn’t replace it – or so the legend goes).

Primary residence is for sure an expense, not an investment, a rental property can be an investment.

You do realize that real estate is not housing, but land…

@Louie I don’t like to look at a primary residence or even a vacation home as an “investment” but that does not take away the fact that more often than not they go up in value over time more than people pay in mortgage interest greater than market rent, n taxes, insurance and maintenance cost resulting in a positive return on investment over time. P.S. Many people that bought Bay Area rental properties over the past 50 years have had a better return on their investments than if they bough Berkshire Hathaway…

Buffett is brilliant but some of his personal values… He had a lot of money, even early in his marriage, but kept his wife on a small weekly allowance and had her use a drawer in a dresser as the crib for Howard, their first son. He didn’t want to buy one.

Correction: I posted something I remember reading about in “Snowball”, Buffett’s biography. Slightly different: He used the drawer as a bassinet for the first child. He rented a crib for the second child.

Wrong. The tax code makes homes the most attractive investment on the planet at the moment. That’s the problem the tax code is FUBAR.

winnah winnah chciken dinnah!

“The tax code makes homes the most attractive investment on the planet at the moment”

I’ve dealt with many folks that are serial flippers and bank that $500k tax free every 2 years or as often as possible. it’s a very lucrative lifestyle.

By *slowly* lowering (or raising) the interest rate, mortgage rates are more likely to trigger transactions, leading to more effective policy and quicker overall outstanding mortgage rate adjustment. By increasing rates too fast the Fed messed up. They ended up locking in a bunch of homeowners who would have otherwise been fine to trade in a mort suitable home if the mortgage rate was only a point or two higher. Now what the fed has created is two groups of haves and have nots: low mortgage rate folks who are still spending like crazy, in homes that don’t fit them, and house poor folks without any money to spend. Or folks who lost the housing lottery by having to give up their low rate mortgage for one reason or another. I believe this rapid increase in rates was a policy error that backfired and led to a lot of housing market inefficiencies that will continue for the foreseeable future.

But wasn’t there this little problem called inflation? There is more to life than mortgage rates.

This is the best comment I’ve read in a long time ANYWHERE. You hit the nail on the head.

“There is a delay between when mortgage rates rise in response to higher policy rates, and when the total amount in mortgage payments in aggregate rises as more mortgages with 7% rates make it into the averages.”

to the fed, who could argue with that logic!!!!!! in the same token, a higher policy rate of say 6%-7% should accomplish that task even more effectively! No? 🤣❤️ :-)

6%-7% policy rates might crash the labor market and then lead to lower interest rates. Wall Street would love that. They’ve been praying for it. Easy does it. Keep the rates higher without crashing the labor market so that rates can stay higher for longer.

C’mon, Wolf, that sounds like something Barry Sternlicht would say right now as he’s begging for rate cuts. We need BIG rate hikes, and soon.

Depth Charge,

We all know that’s how you feel. We all know that you want the Fed to collapse everything and burn everything down so that somehow we can rise from the ashes. And you keep forgetting: if rates go too high, the labor market will tank at some point, and then rates will get cut a lot. That’s the last thing you, who wants higher rates, should want.

If the Fed crashes the market, won’t home prices fall because the unemployment rate will rise and there will be a flood of homes hitting the market?

wolf,

please do explain how 6-7% policy rates would/might:

‘crash the labor market’

and

‘lead to lower interest rates’.

seems to me, neither of these is a direct consequence BOUND to happen. the subject isnt about gravity’s effect, chemical reactions, or anything with a defined and predictable outcome.

easy does it?

no, easy ISNT doing it. that much is abundantly clear. ‘real life/costs’ is/are the only reference anybody needs to see that.

while i dont share quite the same level of Depth Charge’s sentiment.. it is correct in that NOT ENOUGH was done with regard to the purported ‘fight’ to really get inflation down..

the fed is a big joke.. they show their whole hand to everybody before hand, make nonsensical projections about cutting rates when there is NO REASON to, and generally come off as spineless when it comes to doing what they should be.

there NEEDS to be some kind of ‘shakeup’. not fully scripted theatre as their has been. the market(s) NEED TO feel fear once again. they are laughing and have been laughing for awhile now.

wall street needs a punch in the mouth. not a warm fuzzy hug from uncle fed..

i really struggle to understand how you can argue against this logic, considering your attention to the goings on out there and writing on this site nearly everyday.

n0b0dy,

I agree with you 100%.

The business cycle always has booms and busts, so maybe it’s not that bad of a thing if the Fed does shake up the economy.

so this ‘transmission mechanism of fed policy’ works real fast when the fed cuts rates but not so when they raise rates. hmmm … who could’ve known? certainly not all the PhD’s at the fed.

All this will accomplish is funnelling even more homes to the wealthy. The only thing that will fix the housing market at this point is phasing out investor tax breaks for single family residence home ownership over a multi-year period. The other thing that could help is reducing regulations and fees for home construction. The concentration of wealth is out of control.

“All this will accomplish is funnelling even more homes to the wealthy.”

What is “this”???? Higher mortgage rates for longer? Bringing rent inflation down? Bringing home prices down? What exactly do you mean by “this?”

There is a wage-rent spiral, and anyone under 35 doesn’t have a chance in this game. All cash buyers have gone from 10% of all purchases in 2003 to 32% now, and I promise you that the bulk of those all cash purchases are not by people under 35 years old.

1. NAR less than a month ago: “All-cash sales accounted for 28% of transactions in March, down from 33% in February but up from 27% one year ago.”

2. The year 2003 was after the Nasdaq had collapsed by 78% and the S&P 500 by 50% and a lot of the wealth and cash had vanished, and cash buyers with them. DUH.

3. What plunged over the past two years were mortgage applications and therefore the number of buyers having to finance. What dropped less but still dropped were cash buyers. Because they dropped less than mortgage-buyers, their share increased some. Basic math.

4. How would someone “under 35” come up with the cash to buy a home? What kinds silly nonsense is this? You accumulate wealth as you get older unless you’re born with silver spoon in your mouth. That’s how it has always been. You pay cash for a house when you’re older after you have worked, saved, and invested for decades.

5. Here is the NAR’s chart of all-cash buyers going back to 2008. The rate of last month (28%) is represented by the red line:

Jeff:

Both of my children could be “all cash buyers” on a home into the 7 figures The “cash” would come in the form of either a loan from me or an equity position in the property + their down money. It still is reported as an “all cash” sale, but they can refinance and get me out of the picture within a few months. “All cash” isn’t what most people think it is. Could be a hard money loan. HELOC. Drunk father in a moment of weakness. Spinster aunt with tons of money.

All cash is attractive to sellers. No appraisal hokey-pokey. No demands on repairs, etc., as with a VA or “get me done” mortgage. I sold my sister’s house for $100K less than it should have brought if I waited for a sheep to shear. Why? All cash. No contingency. Quick close (14 days). If I carried that turkey much longer, it might need a roof, the pool could throw ace-deuces, a tornado could have leveled it, a hurricane could have shredded it, plus the carrying costs (without any mortgage) were $3k+ a month. In month 6, I have $18K+ of that $100K back, the proceeds have earned $25K rusting in t-bills, with the added bonus that I can sleep at night. I can only imagine what the 2024-2025 insurance premium would have looked like (it was in FL).

All this cash buying sounds like desperate impulsive gambling. For the past 15 years prior to QT, people have been buying on credit. It was mostly free money, so why pay cash? Now, it’s not so free anymore, but the compulsion remains. So they put all their chips on the roulette table and bet on black. What could possibly go wrong?

When a Dad takes $500K out of 5% CDs so one of his kids can join the list of “all cash buyers” and pay him 5% on the money after buying a home it is not “gambling (especially if the Dad is on the title as a co-owner)”…

These types of family dynamics are toxic to personal character growth and unhealthy for all the parties involved, whether they realize it or not.

I’ll venture to say that people paying cash to buy RE in high-priced locations don’t understand or appreciate the concept of opportunity cost. Cap rates are currently in the 1-3% range, plus there is increased potential for loss. I can get better returns by holding a piece of treasury paper. What brought riches in the past isn’t likely to recur.

But I won’t blame flippers for buying with cash now, as long as they plan to get and out in a hurry. Even flipping is getting risky at these price levels.

Financially you might be better off buying a house with a 30-yr mortgage as an owner occupant. Then, when convenient, become a renter somewhere else, rent your house out and turn the house into income property, getting all the tax benefits that that involves.

You guys are hilarious. All you are doing is driving my point home. All of the sales are currently to those with wealth, not low level workers who desperately need a home they can afford from the fruit of their own labors. Look at the latest quarterly report from the california Association of Realtors, focusing on the “qualifying income” data they present (which assumes a 20% downpayment). These are the wealthiest 20% of the population that can hit those *household* income levels (assuming a 20% downpayment). What are the other 80% that don’t have a rich daddy supposed to do?

“With its monetary policy of 5.25% to 5.5% rates and $1.6 trillion in QT so far, the Fed has been trying to push down demand to remove some fuel from inflation, and that has worked to some extent.”

I am going to wholeheartedly disagree with this. The FED stopped well short of where rates should be, and that is why inflation is now rocketing higher and you see these massive speculative bubbles shooting the moon. All-time highs in all stock indices. All-time highs in many housing markets. Crypto going parabolic with all-time highs. Meme-stocks are back, etc.

It used to be said that the FED was there to take the punch bowl away just as the party was getting started. Now we have a raging mania everything bubble and they are just standing by watching rather than being proactive and raising rates. There is absolutely NO DANGER in raising another 100 basis points. But these cowardly, corrupt pr!cks won’t do it.

DC – but what about all the people that /make/ money from higher rates?

Its a double-edged sword.

I tend to agree with Depth Charge. I don’t think raising rates a little more will tank the labor market. Inflation is out of control, and the market rallied. Inflation is coming down, the market rallies. It’s to the moon for infinity. I see Wolf’s point about not wanting to crash things but I just don’t think we are even remotely close to that with all of the strong consumer indicators Wolf has shown us over the past week and all the newly originated corporate debt.

With current interest rates, someone I know has more than doubled their income in retirement over the past 18 months. That money will go somewhere…. buy their kid a house, send them a check for several grand for no other reason than they feel like it. Or they could keep it invested and let it compound out the wazoo. If it goes higher, it just continues to stack.

The same tale of the tortoise and the hare still applies. Punishing one class of people benefits another. Raise interest rates? Works for them. Depress interest rates and the equity markets go to the moon? Works for them (if they’re diversified). Home prices rise? Cool. Drop? Likely doesn’t matter if they have no intention of selling. No one person’s situation is identical to that of everyone else. Heck, one of my silly piles of depreciating junk has become a 6 figure car… and it’s original (paint chips and all) and bone stock…. it once was depreciated to the point that it became nearly worthless and trashed by the fart pipe generation.

Rant all you want…. most people are resilient and will figure out a way to thrive.

Government spending is the problem now. Like it or not, the Fed’s core rate policy lever will soon be impotent. Maybe they aren’t raising rates because they don’t want to let people see how little control their rate actions actually have, waning by the day.

People say financial conditions are tight but they are not. They have been loosening all year.

https://www.chicagofed.org/research/data/nfci/current-data

CRE has been blowing up just fine for the past two years. And massively so. Investors and banks are taking huge losses. Developers are having the hardest time getting funding for anything. Refinancing many maturing loans is nearly impossible because lenders refuse to do it at the amounts needed to pay off existing loans. This is a HUGE mess, and we’ve been talking about it here for two years. How many more industries do you want to see collapse like that before you’re happy?

While I’m not happy with industries “blowing up” I’m tired of taxpayers being on the hook for every failed industry that’s been mismanaged and for zombie companies that should have been held accountable and let fail years ago. Janet Yellen’s idea that everything that her friends have invested in is “too big to fail” is just another entitlement that is going to be very ugly when the cost comes home to rest.

Investors got wiped out just fine during the bank failures in 2023. Uninsured depositors got bailed out, but not by the taxpayers but ultimately by the bigger banks that have to pay the special assessment to the FDIC. This was very different than the bailouts in 2008/2009, where investors got bailed out.

I’ll guarantee you not one developer/banker has missed a day out on the course, missed a single payment for his kid’s private school, cut back on any vacations, etc.

Now pension funds and IRA’s have likely taken a hit. 2008 deja vu.

Wash, rinse, repeat.

The flip side to the current exuberance will be a forceful downturn eventually, leading to solvency challenges.

Forecasting lower interest rates, albeit with caveats, was not a great idea, unless it was in acknowledgment of the downturn to come.

When house prices are falling and becoming more affordable for the masses, they call it a “housing crisis.” When prices are shooting the moon and putting people out on the streets, they celebrate it. Bankers and their political toadies are a cancer upon society.

Love you DC!

They call it a housing crisis when prices fall because the “masses” usually hocked themselves up to their eyeballs and now they are upside down and can’t manage the HELOC, the second and the purchase payments. Those people also get destroyed. It’s a two edged sword.

We bought a house for my daughter out of foreclosure in 2010. The previous owner had it hocked for $550K…. we bought it for $350K from the bank. Cash. Only an inspection contingency. 30 day close. The *seller* (aka knucklehead) hocked the house to put in a fancy kitchen for his wife, sued his neighbor because the bamboo said neighbor planted took over their yard and he took the proceeds from that and over-improved the yard, then he bought a motor home and a boat plus a pickup to haul the boat….. and lost it all.

So, who was the victim? The bank? The prior owner? Both? We paid a fair price for the house (market plus a tad).

That was the fifth house I bought from a bank / distressed seller. In all cases, the other party was happy to get out and we were happy to get in. That’s how it’s supposed to work. But in order to participate, you have to either have big boy pants or brass ones. We’ve used both. Could have rolled 7’s but we didn’t.

Simplistic “solutions” don’t resonate with most of the world. Too many variables Blaming ‘da Fed or Banksters is naive. If someone showed me a muzzle print on their forehead that proved they were an unwilling participant, I’d have empathy for them. Without that proof of coercion, they’re just a player that lost a game they didn’t understand.

As my Daddy used to say, “If you’re looking for sympathy, you’ll find it in the dictionary between sh*t and syphilis.”

Sure…a player playing a negative sum game on a minefield with moving goal posts, lots of smoke-n-mirrors, ever-changing rules and liars/cheats for referees.

Not everyone starts life with a jetpack and a gold plated double safety net. The types of handsome endowments you humble brag about doling out to your kids are actually pretty rare. $350K cash for a house? Yeah — that’s not the norm. At least none of the kids I grew up with ever had it so soft. They were lucky to bum the gas card from their dads on a Saturday night (and usually felt low-lived for doing it).

For many Americans, the pursuit of happiness is a heart disease-inducing grind through the aforementioned playing field/hellscape. Why do you think there’s such a ‘wellness’ mania right now? Perhaps because people feel a bit sicker & tireder than in generations prior?

Trying to blanket delegitimize a generation’s grievances with a broken system by reframing it as poor game on their parts is myopic at best, and sneery nonsense at worst. You shouldn’t have to be a scheming cut-n-thrust psychopath to get a little ahead in this country — it shouldn’t be a disadvantage.

In the distant past, the Fed used to trigger recessions, which gave people many good entry points to invest in RE and stocks. People didn’t have to worry about the build-up of artificial stimulus, moral hazards, and system-ending financial instability.

The next time asset prices fall, they might not reflate for a LONG time. Politicians and monetary authorities have been kicking the can for 30 years. Things were good, albeit unsustainable, during those 30 years, but will it continue the next 30 years? The next year?

We’ve never seen the system pushed this far with artificial stimulus.

“Fed triggering recessions”. I guess you’re basing this on a Fed reaction to the inevitable excesses of ‘the business cycle’.

Ray Dalio has a good animation of these sequences called, “The Economic Machine”. It can be found on the web.

Depth Charge -Excellent comment

Don’t be intimidated –

Nothing is coming down with the stock market hitting all time highs. The only thing that is happening is increasing the wealth divide and screwing over gen Z. This wait and see approach is just draining the pockets of young non-homeowners and lower middle class. People who feel rich because the stock market is up and they have 50% in home equity are not going to stop spending. The only thing that fixes this is a mild but somewhat longer recession with unemployment in the 5%’s. It’s enough to kill speculation, see some of those vacation homes start to hit the market and cause a bit of a stock market correction but not enough to necessitate going all the way back to 0.

What I wonder is how can people who are supposed to be economic experts be this dumb? They sat and watched 2021’s housing market and thought what, yay I own a home, so I’m getting rich? They just screwed a whole generation.