So let’s extend and pretend, please? But industrial still in pristine condition, multifamily limping along.

By Wolf Richter for WOLF STREET.

The delinquency rates of commercial real estate mortgages that have been securitized into commercial mortgage-backed securities (CMBS) – investors on the hook here, not banks – keep getting worse, driven by the not yet fully blooming mayhem in the office sector, and also by the ongoing troubles in mall loans and lodging loans.

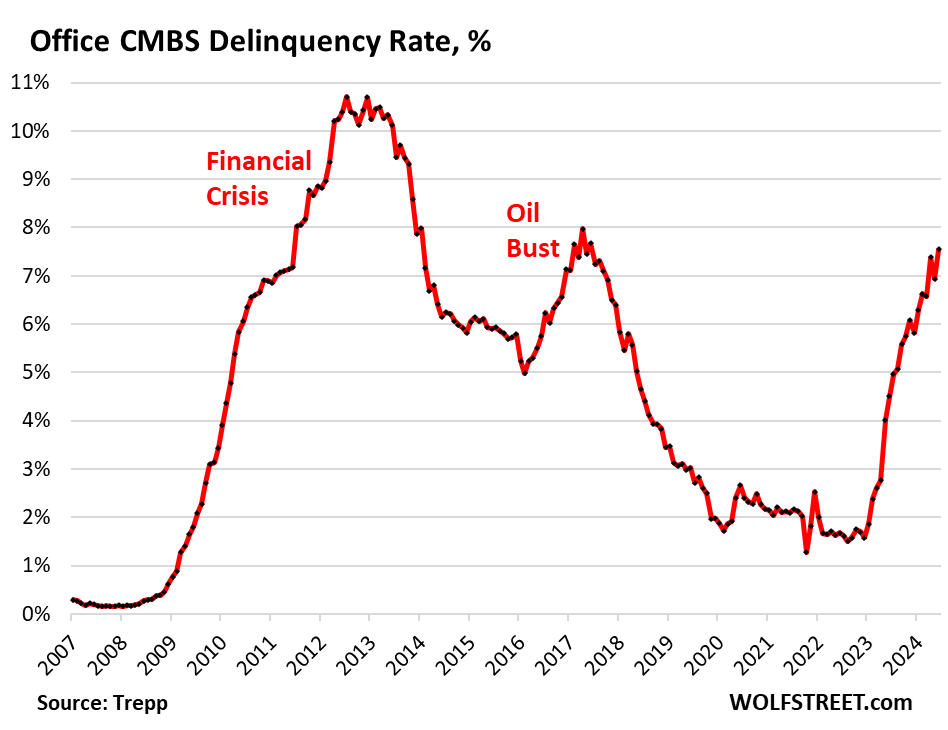

Office CMBS. Delinquency rates of office mortgages backing CMBS spiked to 7.6% in June, according to data by Trepp, which tracks and analyzes CMBS. This was the highest rate since the worst moments of the oil bust that had devastated the Houston office market in 2016. Mortgages are considered delinquent after the 30-day grace period has expired without interest payment.

About $1.87 billion in office loans became newly delinquent in June, but $900 million in formerly delinquent mortgages were no longer delinquent – see our extend-and-pretend section below – producing a net increase in delinquent loans of about $1 billion:

The culprits are three-fold: the structural collapse of demand in the office market, floating-rate mortgages, and loan maturities amid higher interest rates.

According to a prior report by Trepp, the delinquency rate for floating-rate office loans was 20%, while for fixed-rate loans it was 4.7%. In terms of loan maturities, when a 3.5% loan must be refinanced with a 7% loan, the rents, especially in a building with a high vacancy rate, may fall far short of covering the interest and other expenses, and the building no longer makes economic sense.

So, yes, let’s extend and pretend, please.

Loans are pulled off the delinquency list if the interest gets paid, or if the loan is resolved through a foreclosure sale with big losses for the CMBS holders, or if a deal gets worked out between landlord and the special servicer that represents the CMBS holders, such as the mortgage being restructured or modified and extended.

This extend-and-pretend is now all the rage because CMBS holders do not want to end up with a half-empty decades-old office tower, which is the gun the landlord holds to the lender’s head.

And many landlords have already pulled the trigger over the past two years by walking away from the loan and the property, losing whatever equity they had in the building, and letting the lender take the remaining loss.

Even the biggest landlords, such as PE firm Blackstone, have been doing just that, even with huge office towers in the middle of Manhattan, and in Blackstone’s case, even the top-rated tranches of the CMBS had to take losses, while the lower-rated tranches got wiped out. That’s the gun the landlord holds to the lender’s head.

And the lender is threatening the landlord with foreclosure and loss of the equity in the building, which is the gun they hold to the landlord’s head. But collateral values have plunged, and the landlord has the bigger gun.

So increasingly now, they both blink and make a deal, and the mortgage gets restructured or modified and extended past the maturity date. The landlord gets a loan that is economically a little more feasible, and the CMBS holders are just too happy to stick their heads deep into the sand and wait for the Fed to perform a miracle, or whatever. Everyone is now doing that, banks too.

But office properties have a massive structural problem – a huge glut of vacant office space for which there is no demand, and office property values have collapsed in many markets by 50% to 70%. This structural problem is on top of the interest rate problem. Whatever miracles the Fed is hoped to perform with interest rates, it won’t be able to fill that glut of half-empty office towers.

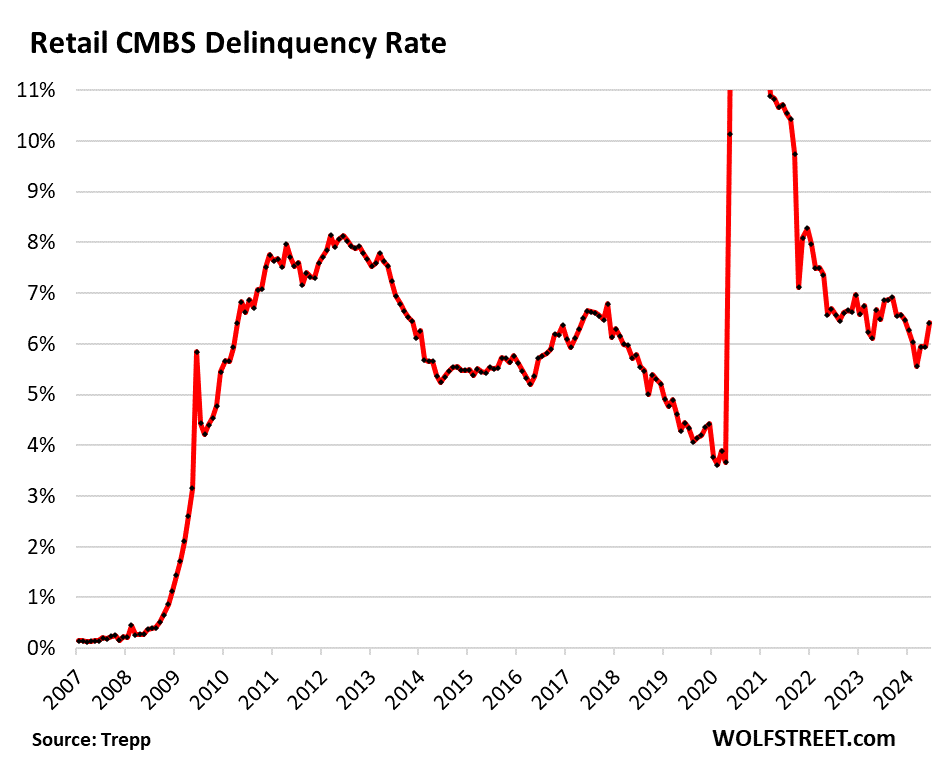

Retail CMBS.

The delinquency rate for mortgages backed by mall properties rose to 6.4%. Retail CMBS have been afflicted with high delinquency rates ever since the Great Recession. Since 2017, we’ve called this phenomenon the Brick-and-Mortar Meltdown. Countless retail chains, from Sears on down, filed for bankruptcy, and many were liquidated. Even the biggest mall landlord, Simon Property Group [SPG] walked away from malls across the US, and that started before the pandemic, such as Independence Center near Kansas City, Missouri, which in 2019 generated the largest loss ever by a retail CMBS loan. Since 2020, there has been a flood of bankruptcies. The more recent retailer bankruptcies include Express in April 2024 and Joann in March 2024. In December 2023, mall REIT PREIT filed for bankruptcy for the 2nd time. In April 2023, Bed, Bath & Beyond went bye-bye. Retailer bankruptcies and liquidations put enormous stress on retail properties.

This is the structural problem of brick-and-mortar malls, brought about by the relentless shift in shopping patterns to ecommerce. No one is going to stop that, not even the Fed. Exempt have been strip malls with big grocery stores as anchors, and service establishments and restaurants among the other tenants.

In June, retail CMBS delinquencies increased on net by $525 million, including four mall loans with balances of over $100 million each, according to Trepp.

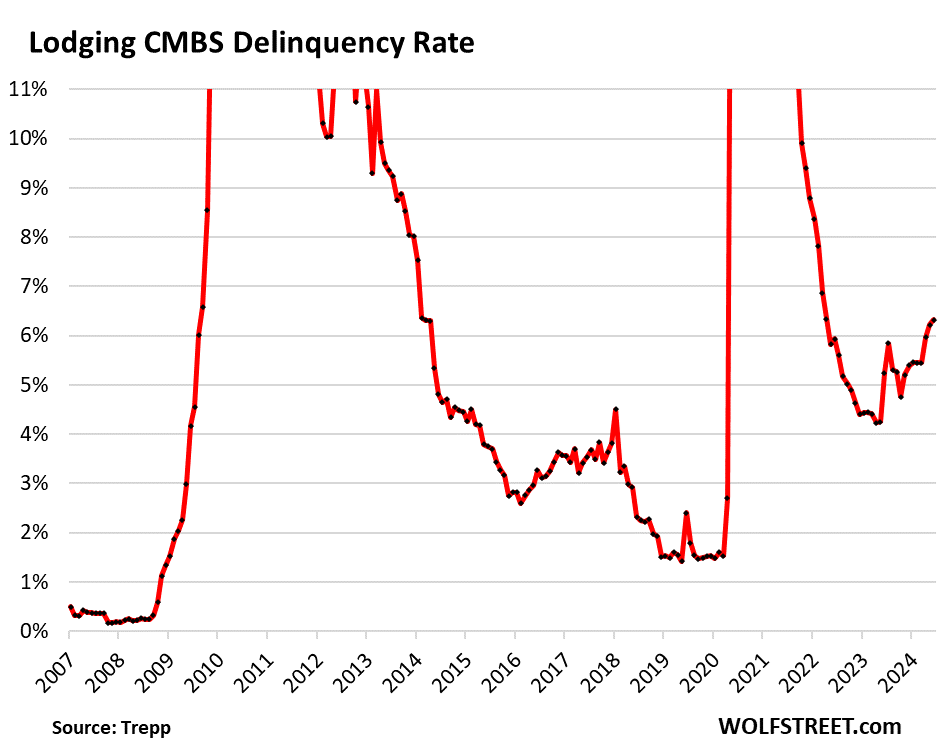

Lodging CMBS.

The delinquency rate for mortgages backed by hotel and resort properties rose to 6.3% in June:

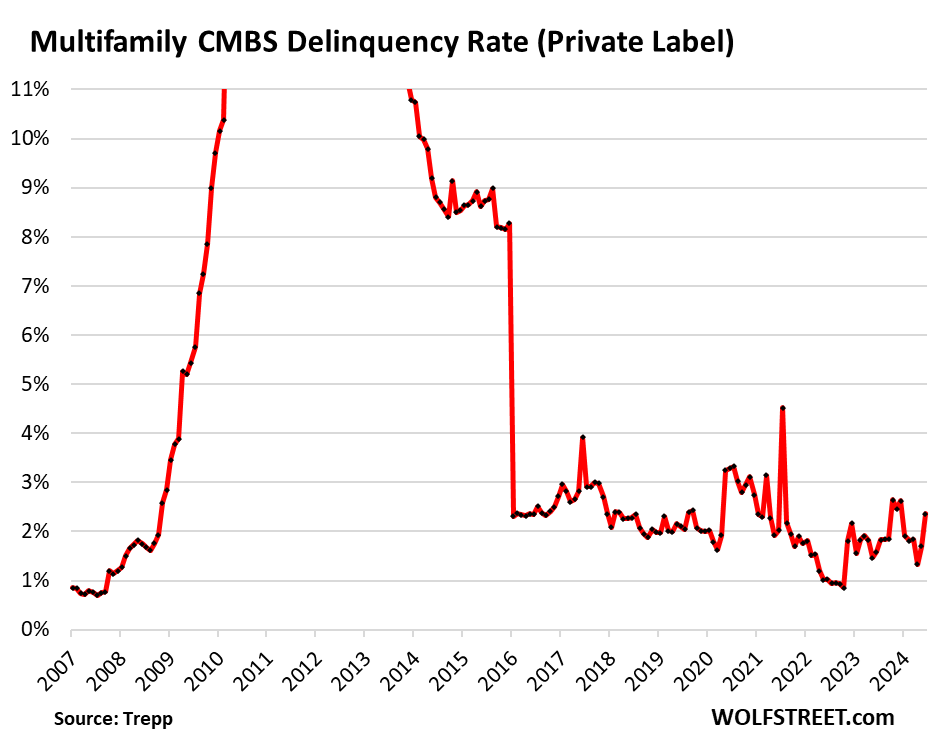

On the other hand…

Multifamily CMBS. The delinquencies for mortgages backed by multifamily buildings also rose in June, but at 2.4%, they’re limping along at manageable levels for now. There have been some big mortgages that defaulted over the past two years, but it’s also the biggest CRE sector, with a total of $2.1 trillion in loans spread across all lenders, globally, and only a small portion has been securitized by the private sector.

The US government is on the hook for $1.1 trillion, or 55%, of mortgages backed by multifamily buildings. The remainder is spread across private-sector lenders.

Private-sector CMBS, CDOs (collateralized debt obligations), and ABS (asset backed securities) combined hold only 3.2%, or just $67 billion, of the multifamily mortgages. CMBS alone represent an even smaller portion. Which is why each major delinquency moves the needle up a lot, and each major resolution moves it down a lot.

For example, the plunge of the delinquency rate in January 2016 was caused when one $3-billion delinquent loan was resolved when Blackstone and Ivanhoe Cambridge bought the Stuyvesant Town–Peter Cooper Village residential development in Manhattan (11,250 apartments in 110 buildings) and paid off the delinquent loan.

Industrial CMBS. The delinquencies for mortgages backed by industrial buildings – warehouses, fulfillment centers, etc. – ticked up in June to 0.6%, which is still historically low. The sector is driven by the expansion of the physical infrastructure needed to support the ecommerce boom.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Walkaway’s (or ‘Jingle mail’) on a grand scale.

sfchronicle.com/sf/article/s-f-hotels-lose-1-billion-in-value-19552250.php

Biz travel appears not to be coming back anytime soon.

Nonsense. Those are the hotel PROPERTIES that are owned by landlords. The hotels are operated by other companies. The properties are in trouble, not the operating company. Same with offices. It’s not Google that’s in trouble, or Meta, but the landlords that own the towers (and their lenders).

It’s clear that a lot of unused office space is not going to be filled for years because of changes in WFH for many employees. IMO, developers and policymakers should put their heads together and repurpose this unused space to un subsidized multifamily and subsidized multifamily for low income families. This will yield many benefits to workers, employers and create safer cities.

Large groups of subsidized low income housing projects are famous for creating safe cities…

Better than living in tents or on benches,

Yeah, it’s astonishing the extent to which neoliberals will go to make any amelioration of our dire socioeconomic situation impossible “because imperfection.” It’s a form of cultural suicide.

To sum up a personal story the flying doctor told.a couple articles back, “There are no ethics, it’s all just business”.

So obviously he merely decided he needs more private prisons in his portfolio for all the coming vagrancy laws. (it’s kinda my investment thesis, too).

He meant no harm to anyone…….after all he is a doctor.

Asking here because I don’t know this civil engineering at all, but is it doable to convert the commercial CRE office space, into residential? Most offices from what I see, the way plumbing and design set up, seems like it different from how they do the plumbing in apartments. And a lot of offices, with the cubicles and how the windows are, doesn’t seem to be designed the way a builder would do apartments. But would be interesting if there’s a way to arrange and build around that, without too much extra cost. A neat way to open up multi family housing if the builders can.

Maybe 5% of office buildings are excellent candidates for residential conversion. Maybe another 5% are good candidates. After that, it’s pretty bad.

Major factors include:

-Getting a good price when you buy the property.

-Having an honest and co-operative local government.

-Getting a good price when you buy the property.

-Getting good terms on the construction loan.

-Getting a good price when you buy the property.

-Having a building which is tall and skinny.

-Getting a good price when you buy the property.

-Having a building with plenty of parking.

-Getting a good price when you buy the property.

There are a few more parameters, but you get the idea.

I do not think that many shopping malls are good candidates for residential conversion, and I do not think that low-rise office buildings would be good, either.

There’s always pickle ball courts……..

But malls and low-rise office buildings are easy to knock down. Replace them with good mixed use communities with shopping amenities.

Malls have huge parking lots. They’re ideal for conversions, and that’s being done. But zoning issues, permitting, etc. can slow down the process a lot.

Incredibly cost ineffective. Actually more effective to level existing property and start from scratch.

Not too many takers in the near future however. Cause you know… They’d be subject to real interest rates when borrowing.

Government subsidies on deck

remember cities/counties like property taxes/permit fees

and make you tear down existing and start over

making most unprofitable – except for contractor

Residential and commercial codes have diverged massively over the past 60 years. Many office buildings are simply not convertible to living space. The irony is, the newer the office building, the more divergent the residential and commercial building codes were at time of construction, thus the harder & more expensive to convert to residential. I’ve heard it said that only 3% to 5% of current office towers are even feasible for conversion in the average North American city, and even that would require enormous capital investment. A seemingly great idea on the surface is actually fraught with problems and prohibitive costs.

A M nailed it. It would probably be far cheaper to just tear them down….which is what will happen, anyway. This is nothing new. There are whole areas of every country of the World that has abandoned buildings, factories, housing….places that don’t get repurposed. This is just another sector left behind….CRE speculation, like the rust belt fell to Chinese steel mills and ‘Globalization’.

Folks point at Covid, WFH, etc etc…for this situation, but what about AI effects down the pike? News flash, it’ll get worse going forward and guess what? The wealth will not be shared.

Be careful what you speculate in, I guess.

Maybe buy Nvidia stock instead of commercial real estate :)

GIVE IT UP AMC;

While there certainly are SOME currently ”commercial” properties that will NOT be candidates for conversion to residential,,,

MOST can be, with or without GUVMINT subsidy…

Retired now from years of analyzing and costing such conversions around USA; almost all made cost effective sense then, and based on what I read here and elsewhere, continue to make sense….

Gotta watch out for any “data” that begins with, “I have heard it said that…..”.

And people that mention no credentials at all to speak on the subject.

Who ARE these A-holes? What is their personal agenda?

We all know another guy who would have simply said, “More impossible than anything you have ever seen”…..thereby beating AMC’s comment flat….and be ready to move on, on any subject.

Only 3-5% are feasible under current residential codes and individual space expectations. Many more properties would facilitate dorm like conversions with communal bathrooms on each floor or within each block of 10 apartments.

Your idea will work just fine ONLY if “Put The Lid Down” is STRICTLY enforced…..that is a much bigger problem than ANY codes.

Who doesn’t want to live in a concrete box with no windows or plumbing!

I would love to live in an office building / flex type space. I dig those barndominium things as well.

Ever hear of a big screen TV and a choice of rotating (stoppable and with zoom) 1/2 sec time delayed cameras all over the building?

Get MUCH MORE viewing time than any stupid window ever will.

There are also things called light pipes that save on electricity….or wet walls? Make interior apts cheaper….or let the market determine that, considering camera feature mentioned.

I think all these “won’t work” types are just afraid of TAXES!…..and I doubt anyone here makes enough or has enough net wealth to seriously worry about them.

Again, look at that 1960 tax rate schedule (adjusted for today’s money)…it’s perfect.

Any similar jerk I missed feel free to consider these posts are for you, too.

Check out the Tower of David in Caracas Venezuela. And they didn’t even have to invest in repurposing!

I think it may have been cleared out by now though.

Maybe they can be repurposed to store old EV batteries.

Every time CRE is mentioned someone always says “just convert the excess to residential!”

It doesn’t work that way. Most office buildings are simply no good for residential and many others would cost so much to convert it is cheaper to demolish and rebuild.

Yeah Wolfman, I’ve been following Vanguard’s Real Estate ETF (ticker: VNQ) which has some exposure to commercial real estate and its loans.

Its down about 72% from its all time high set in 2021.

I suspect it may go down further if more commercial real estate goes bust.

Something has to give, and that may include virtually no new supply of commercial real estate for next 5 to 10 years to allow the existing supply to eventually be more utilized, which may include re-purpose it (i.e., residential, stores, restaurants, etc) if economically feasible.

Surely not! Low cost ETF tracker funds can only ever go up! It is the fifth force of the cosmos.

VNQ is NOT down 72% since the peak in 2021. It’s down 28% in price. Then add back in roughly 12% in dividends over that period, and its only down roughly 12%. Far cry from 72%. Personally I am surprised it is not down much more given where rates are and how bad office & retail CRE are doing.

It will be interesting at what time will be the time to buy a REIT index? Problem is the S&P is so overvalued. And if it ever crashes, REIT’s will crash with it. That’s what worries me. I also worry at some point these deliquencies will catch up to the CRE market as a whole. Private CRE has not been market to market like public REIT’s.

REITS are already in trouble. CVS & Walgreens are closing a significant number of stores.

Since you brought up VNQ, I’ll ask why is SRS not going up.

I apologize for the error as the ticker VNQ is down about 29% from its all time high set in 2021.

VNQ also has paid about a 4% dividend over that time since the 2021 peak. So that is roughly say 12%. So its really only down 17% from the peak. I think the overvalued S&P is likely propping the price up. Passive indexing from 401k’s, pension systems, etc… That buy everything on a monthly basis regardless of valuation.

I agree. The passive index investments from structured retirement plans are raising the water level. Secure Act 2.0 turned up the flow of these investments, which will contiue to increase over this decade.

Something big indeed will be needed to plug up these water works. Hope everyone has structured a way to enjoy this “growth” tax free!

Great investment! Only down 17%…before inflation. You should have bought more!

no one is claiming it was a great investment

imo if someone is not ok taking a 20%+ drawdown on their investment, then they shouldn’t be buying sector ETFs or equities in general

Howdy youngins! The Lone Wolf Strikes again. Squirrels love nuts.

As more of the CRE risk has gravitated to investors from banks ( and banks are a weak link to their importance to the economy and due to their Leveraged Debt/Equity position, magnifying any losses ) this has mitigated some of the CRE risk away from the economy.

One issue that investors now face is the lack of skill sets in managing the CRE losses coming down the pike.

Extend and pretend is probably easier for a bank to pursue than an investment group. The bank has an internal skill set of managing the process and one CEO to make the decision.

Investor groups hire a “Special Servicer “who they pay very high fees to

Manage the process, with different goals amongst a committee that manages the Special Servicer .

I just suspect that it will be a much slower and inefficient process to get to the point where investors are making the best decisions as banks would ( even though the threat to the economy is less pointed)

I totally agree: “I just suspect that it will be a much slower and inefficient process to get…”

We’re already seeing some of that. The special servicers have been incredibly slow in dealing with this, and they’re dragging their feet on everything. Same with some of the CRE funds.

Part of that is that the incentive is wrong: special servicers are paid fees, and the longer they drag this out, the more they make in fees, and the smaller the ultimate recovery for CMBS holders.

I recently moved a couple bookcases in my office and grabbed a couple old books to re-read, One was “Zeckendorf The autobiography of the man who played a real-life game of Monopoly” (published in 1970 that I first read ~1980) . I was just sitting on the deck at the cabin this morning with a cup of coffee and read him describing what happened to office buildings in the 1930’s:

“the worst thing that could befall such a receiver would be to make excellent profits that his property soon recovered and he was no longer needed. The best thing that could happen to him would be to receive just enough income to pay the minimum charges needed to keep his particular ship afloat, while maintaining his own and his lawyer’s fees”. P.S. the people that make fees from deep pockets keep getting better and better at it and just yesterday I read that after four YEARS and OVER $100K per campsite the Crane Flat campsite at Yosemite is open again (with new tables and fire rings)…

You do understand that there is a key difference between the 30’s and now, right? In the 30’s all assets were subject to the deflation caused by the great economic depression started in 1929. After the aggregate demand recovered, so did the different asset classes, during the 50’s and 60’s. Now the CRE are subject to significant technological disruption, which makes a huge difference with the 30’s.

P.s. All those that have tried to fight against technological innovation, have failed in the end.

Historical lessons needs to be adjusted to current conditions.

Hugely successful Zeckendorf said: “If I can’t walk to it, I don’t buy it.”

He didn’t follow his own advice and went broke.

If the investor is a large insurance company with an equity real estate department, the property can be taken back on the assumption that some or all of the loss will eventually be recouped. Banks and CMBS holders do not have this option. The only question for them is when to take the loss.

The big question is if, when, and how all this distress in commerical real estate hits the broader economy? How & when does it effect the broader stock market?

So far the average John Doe investor has not been affected much by all of this. As mentioned in a earlier post, the CRE index etf VNQ is only down about 17% from the 2021 peak (including dividends). And your average buy & hold stock market investor doesn’t even hold a lot of that etf.

“The big question is if, when, and how all this distress in commerical real estate hits the broader economy?”

Unless it turns into a tsunami, it’s not going to hit the economy in any great way, unless there’s a moderate recession with 6%+ unemployment. And if that happens, the downturn in jobs will be the primary driver of the length & depth of the recession, not CRE.

In addition, a lot of these bad loans are going to get worked out to better deals, especially in markets with the higher vacancy rates.

The thing is that, as the article states as well, at the current moment everyone is extending and pretending, while waiting for FED to cut. How much will the FED be able to cut, and how much of an impact those cuts will actually have, considering the huge vacancies as consequence of technological disruption, well that’s a discussion that noone wants to even think about. Human, when things get really messy, are ready to do everything just to take more time and meanwhile wishing that they will never have to deal with the problem that themselves caused. That’s the current state of the market, and not only related to CRE, let’s take time, waiting for FED to fix everything by cutting rates. Everything is fine, ignore the problems and smile.

If we’re lucky the losses in commercial real estate will be confined mostly to the already rich, leaving the bottom 3/4 (at least) of the income and wealth distributions unaffected.

The real question is who ultimately holds the loans, and is taking the losses. It’s not like the sophisticated investment world didn’t see this coming, it’s been obvious for the past four or five years. The normal approach of institutional money is to dump the assets at the first sign of trouble – that’s why everything is so volatile nowadays. But who did they sell these assets to? Vultures? Unsophisticated foreign banks? Retail investors?

“Vultures” are buying the defaulted loans for cents on the dollar so that they can foreclose on the building and get the building at a low cost. If a developer has a very low cost in the building, somewhere near land value, they then can do something with it, either tear it down, or convert it to residential at a huge cost, or upgrade it at a huge cost and try again.

I wonder what is driving the uptick in lodging delinquency? Travel seems to be as strong as ever, so is it just the rise in interest rates?

It’s NOT the hotel operators that are in trouble. They’re just leasing the property. It’s the landlord and their lender that are in trouble.

The hotels are operated by other companies (such as Hilton, or such as a Hilton franchisee), and they’re doing fine. But the landlords (hotel REITs, PE firms, etc.) who own the land and buildings are in trouble because their costs have doubled as rates have jumped, and the rents from the hotel operator no longer pay for the more-than doubled interest payments. The landlords of the older hotel properties are now in trouble because they cash-out refinanced them a few years ago (and securitized the loans) at very low interest rates and at hysterically high valuations.

Same in the office sector: it’s not Google or Meta (who lease the office) that are in trouble; it’s the landlords and their lenders that are in trouble.

Are the lanlords really in trouble? I’m guessing their personal bank accounts are bursting, while the loan is someone else’s problem. A corporation takes the finacial hit while the people who worked for the corporation keeps their winnings. At the end of the day, it’s all just numbers in a computer somewhere, right? Someone just reduces one of the numbers in a spreadsheet, then it’s business as usual like nothing happened. At least, that’s the way things have seemed to increasingly work each and every year since the 1980s.

For example, this is a big landlord with lots of financial resources: Park Hotels & Resorts, a publicly traded REIT [PK], is the real-estate spinoff from Hilton (Hilton was bought out by PE firm Blackstone in 2007 and split into different divisions, with the RE part getting spun off separately). Park Hotels owns the properties of many big hotels and resorts that were originally under the Hilton brands. They walked away from a bunch of hotels and resorts, including two run-down mega-properties in San Francisco, the 1,921-room Hilton San Francisco Union Square and the 1,024-room Parc 55 San Francisco (dating back to the 1960s-80s). Park Hotels cash-out-refinanced the properties in 2016, with an interest-only non-recourse 4.1% mortgage of $725 million, backed by fantasy valuations of these run-down properties of $1.02 billion and $540 million respectively. By 2023, the towers needed an estimated $200 million in upgrades and renovations that Park Hotels never performed.

The stock [PK] is down 50% since 2019, despite a recent rally, and despite the massive stock market rally over those five years. They have booked big losses on their equity stakes when they walked away from the hotel properties.

So yes, the lenders will likely take bigger losses, but PK also took big losses. And that’s how the losses are split up. Obviously, if you go all the way back many years, those properties were a good deal for the landlord, especially the cash-out refis, which is how they got cash out of the properties, but the exit from those properties was not a good deal – they lost a bunch of money doing that.

Thus the nationwide war against VRBO type rentals…

After all, why should travelers have a say in where they stay?

Vacation rentals have driven up housing costs for locals in big touristy cities; that is an insidious thing. That’s why there are efforts underway to rein them in at least somewhat in the most touristy cities, at least have hosts pay hotel taxes and register. NYC is cracking down harder, and it should. In terms of neighborhoods, a large number of vacation rentals — the constant come-and-go of tourists instead of neighbors — destroy the neighborhood. Converting residences, designed for families to live in and make their home in, to vacation rentals is the worst thing that happened to big touristy cities. We need a big travel recession to sort this out. Lodging for tourists in big cities should be purpose-built, and should be in the touristy parts of the city (zoning).

There have always been vacation rentals, and it was fine because it was just a small part of the housing units. Since Airbnb came along with billions of dollars of investor money, vacation rentals in big touristy cities have turned into a scorched-earth war on housing affordability.

Thanks for giving me a chance to say that.

You’ve nailed it, Wolf — AirBnB and VRBO pulled a fast one on municipalities and the social costs are redounding upon the citizenry whose neighborhoods are affected. The backlash is just beginning …

eg – second the sentiment and more kudos to Wolf. (Yet another facet of that gemstone of: “…privatize all profit, socialize all risk…”). Best.

may we all find a better day.

All of this information is fine & dandy. Maybe my memory doesn’t serve me well, but I don’t remember there being a major ordeal back in 2008 – 2010 with regards to CRE. As your graphs point out, they took a hit back in the day, but I don’t remember it being a “driver” of extending the recession.

You said six months ago that this would take 3 years to play out. If true, we still have a long way to go, but again I don’t see CRE as being something that pushes us into a recession. And, I’m not saying that’s your opinion either. Given that the demand for office space is SO MUCH less than housing, my GUESS is that there’s going to be a lot more dealing that will minimize a potential implosion.

And, the FDIC will step in to protect depositors in these 67 high risk regional banks. Finally, we’re easily a year into the doom & gloom over CRE and IMHO it continues to be a big nothingburger.

You’ve got to distinguish between something that causes a global financial crisis and something that is an industry-specific catastrophe. Just because something (CRE) doesn’t cause a global financial crisis, it doesn’t mean it’s a nothingburger.

There was a huge “ordeal” back then during the GFC in the CRE industry, but it was papered over by the much bigger ordeal of the residential mortgage crisis and the near-implosion of the financial system. The Fed’s 0% then resolved the interest-rate issue for CRE, but it didn’t resolve the demand issue — that took years, and retail never recovered.

It’s not a “nothingburger” for the industry. The CRE industry is in a depression. The losses (equity and debt investments) may have already reached $1 trillion spread across investors and banks globally, some of it “realized” and some of it not. But it’s not causing a financial crisis because banks in the US are not the majority holder of the debt; global investors, the US government, and global banks are the majority holders. And that’s a VERY GOOD THING!!!

Thanks for your reply. When I say nothingburger I’m talking about to-date, and I agree it could at some point get very ugly and make other convergences that may cause a recession even worse.

Honestly, I’m glad everyone is taking a much-needed haircut in CRE. The same thing needs to happen to the housing market here in the US. Home prices remain WAY TOO HIGH. Somehow, someway, @ sometime, home prices need to see sustained & lengthy drop.

Best regards

As soon as someone can figure out how to profitably ship straw bales and bulk hog or chicken feed via ecommerce, that will be one more thing that I don’t have to buy locally. :)

BillyBobsFeed&Seed.com?

Repurpose all defaulted CRE as MAGA prisons to house the flood of democrats and anti-Trump republicans.

Better yet, Trump can purchase these properties with his campaign cash and lease-back to the government.

That is a great idea! Do you think it will go public?

Spoken like a true fascist. I hope that’s a joke. The Rubber Stamp Court might approve too tho.

It’s obviously a joke.

Sorry I’m a little sensitive to comments like these. I hear them locally more than I care to and they’re quite serious.

The more I read about RealPage, the more certain I become that multifamily is going to self destruct if legislation passes to prevent use of such software by property owners. On a very basic level, 100 units at $900/month provides the same revenue as 90 units at $1000/month (essentially an 11% rent increase) , so substantial annual rent increases would negate the impact of higher vacancies.

There was an newspaper article in the Charlotte Observer from 2014 that described how apartment pricing algorithms were causing huge swings in prices. An example provided was rates of $982 to $1307 for the least costly one bedroom apartment within a 10 day period in a specific complex with a total of 267 units, and the assistant property manager was quoted as ‘Unfortunately, it can do that…’, prices were set daily, and each unit has it’s own rate.

The names popping up were the same as those currently under investigation. At the time in Charlotte (March 2014), there were 10000 units under construction and 11000 more proposed, and there were concerns that there may be an oversupply in the making.

Where there’s smoke, there’s fire.

@northern lights I have been renting apartments since the early 80’s and I have never personally used a pricing software, but it has “always” been a practice at medium size units to keep a unit available to show so the price of the “last unit of a floorplan” gets jacked up just like a car dealer does with the “last car of a specific model” on the lot (small apartments are typically leased to 100% and big apartments almost always have dedicated full time “model” units).

Office building CRE, is this becoming an issue with remote work or offshoring our service organizations negating the need for CRE? Could it also be less businesses in America as in the last century?

@Gabby Cat, it is crazy how much traditional office work has been sent overseas in recent years. It has been over 20 years since most big commercial and residential lenders started sending loan origination packages to India to enter all the data from the Borrower into a software and do market analysis of the subject property. Since the Indian work day is the opposite of the US West Coast work day you can scan 100 pages to pdf at 5:00pm on a Monday and have three years of operating statements from a Borrower along with a credit report and property market report waiting for you at 8:00am the next day. A friend that is a veterinarian now sends all his x-rays and MRIs overseas for analysis since it is inexpensive and since that is all the guys do all day they are better at it than he is.

Appreciate this update to my understanding of how much and who, etc., etc. Aptguy:

Had been one of the first to agree to help the ”beta folx” trying to bring forth the OST ( On Screen Takeoff ) software back in the day.

Never actually used it because it never came close to my speed or accuracy then.

Seems likely, and I, for one, hope it does take the place of the hours, days even, I spent ”taking off” plans and specs, sometimes hundreds of pages of plans and thousands of pages of specifications.

Still seeing challenges due to lack of both specificity and thouroughness of OST software, but I continue to hope, eh

ISM data show sharpest U.S. business contraction since scamdemic

Make sure you understand that the ISM services PMI is a sentiment survey of purchasing managers in non-manufacturing industries. It’s not hard data. The questions are such as:

New Orders:

a. higher than last month

b. same as last month

c. lower than last month.

Answers a=1, b=0, and c=-1. Then they’re totaled. In the final tally, 50% = no change from last month. The overall survey result (48.8%) more than reversed a jump in May (53.8%). There was a below-50% figure in April 2024 and in December 2022.

“The landlord gets a loan that is economically a little more feasible, and the CMBS holders are just too happy to stick their heads deep into the sand and wait for the Fed to perform a miracle, or whatever. Everyone is now doing that, banks too.”

I think this is the keypoint.

I was feeling sort of Charles Heston in Planet of the Apes (the real one) : “You Maniacs! You blew it up! Ah, damn you! God damn you all to hell!“, but now I am feeling more like Snake Plissken / Kurt Russell in Escape from New York. Just get out as fast as you can.

What did you expect when you checked onto this planet. I’ll call the mother ship and tell them to send you some uplifting movies…maybe the devil in Mrs jones.

Our markets.

Imagine you are standing in the basement of beautiful three-story house. Another person is in this basement wearing a hard hat, orange vest, and wielding a sledgehammer. They use this hammer to whack what you assume is the central support of this structure. Nothing happens. They whack it again and the post kicks out and falls to the floor.

They scratch their head and look around. You become intrigued as this person who you assumed was knowledgeable construction worker appears to be confused.

They walk to another post and with one solid whack, knock it to the floor. The structure groans and settles somewhere else.

They grunt and wander over to another post near the exterior wall. They whack, then whack again. The structure lets out a feint creak as dust falls from the ceiling, but otherwise nothing seems to happen.

They realign their grip on the hammer, taking a big breath as they lift it into a mighty swing and slam it into the center of the post. You hear a cracking sound from above and you can now see a slight bow in the abused post. The worker cocks their head, puts a hand on the post and gives it a wiggle. The top of the post slips out of place and there is a large crash as the structure settles again on the post which is now seemingly defying the laws of psychics in its cockeyed stance. The worker grabs the post again and begins kicking the base while pulling with their entire body.

Why are you still here?

Because the Fed will soon lower rates!

MW: Trump’s tariff plans could lead to five extra Fed rate hikes, Goldman Sachs chief economist says

What is the logic behind this Goldman Sachs claim?

The logic is this. These tariffs along with retaliatory tariffs by our trading partners would lead to MUCH higher inflation in the US. The Fed would have to go into overdrive to combat this inflation.

Yes, but you forget…last time around all were claiming that bad orange man tweeted Powell into rate cuts. He is back on X, so we can forget about the hikes.

That’s the part that makes me roll my eyes. Inflation will go nuts and the plebes will pay, yet they’re still trying to bring on their own doom without understanding the ramifications, not that I feel I have a great handle on the total picture there either. Predictibility is not Mr T’s strong suit…

Where’d my popcorn get to anyway?

DM: Popular nationwide pizza chain set to file for bankruptcy in days – sparking fears its 500 restaurants could close

A popular pizza chain is the latest to face money problems in the face of rising costs and falling customer numbers. Mod Pizza is preparing to file for bankruptcy as early as next week, sources told Bloomberg on Wednesday. The plans are not finalized and could still change, the person familiar with the matter said. ‘We’re working diligently to improve our capital structure and are exploring all options to do so,’ a Mod Pizza spokesperson said in an emailed statement.

Those little bite size pizzas cant compete with chains that offer large pies. The value was never there for people like me. Plus, who wants to stand there in line while waiting?