It’ll take years to get this mess cleaned up, at the expense of investors, landlords, and banks.

By Wolf Richter for WOLF STREET.

Availability rates in the office sector of Commercial Real Estate (CRE) are not getting any better, and in many markets, they’re getting still worse and are hitting new records, as landlords and lenders grapple with waves of massive repricing, with office tower values, those towers that have sold, plunging by 40%, 50%, 60%, 70% and more. Numerous landlords, from Blackstone on down, have let buildings go back to lenders to let them deal with the mess.

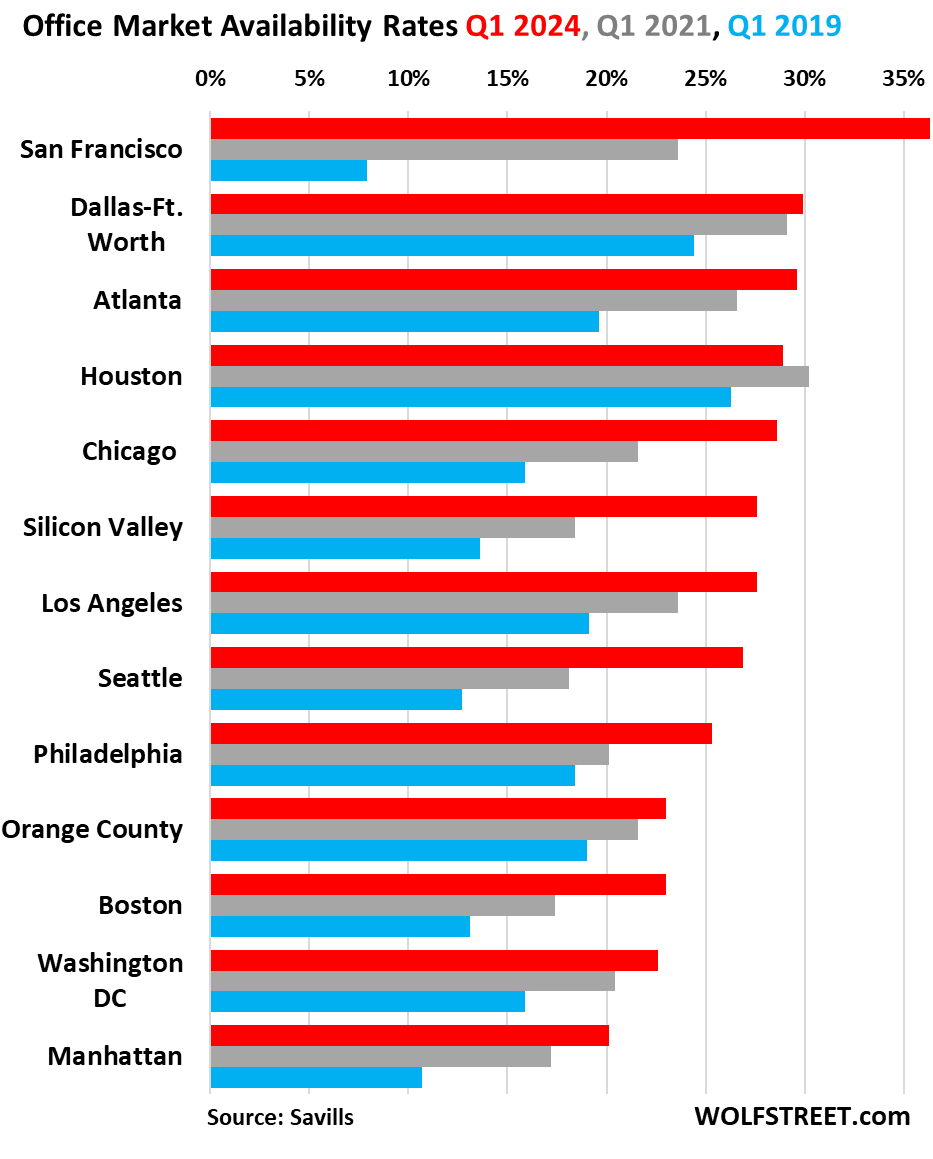

Here is a chart of the 13 markets for which Savills released the Q1 data today, showing the availability rates of office space, so that’s the space that has been put on the market for lease either by the landlord directly or by a tenant as a sublease. Red shows the availability rates for Q1 2024; gray for Q1 2021, and blue for Q1 2019, which were the Good Times.

While San Francisco’s availability rate edged down from a record 36.7% in Q4 2023, to 36.3% in Q1 2024, it remained the worst office market in the US, followed by Dallas-Fort Worth and Atlanta, both at or near 30%. Houston was for years the worst office market in the US, with availability rates of 30%-plus. With the oil boom over the past couple of years, it edged away from 30%.

New worsts. Availability rates in nine of the 13 office markets in the chart rose to new records:

- Atlanta: 29.6%

- Chicago Downtown: 28.6%

- Silicon Valley: 27.6%

- Los Angeles: 27.6%

- Seattle: 26.9%

- Philadelphia: 25.3%

- Boston: 23.0%

- Washington D.C.: 22.6%

- Manhattan: 20.1%

The Good Times for office CRE was 2019 (blue in the chart) and before. In 2019, for example, San Francisco was still the hottest office market in the US, with an availability rate of 7.9%, amid a super-hyped “office shortage” that caused every square foot of office space to be instantly “nabbed,” as the media liked to say at the time to promote the CRE promo-hype further, such as in, “Sony PlayStation nabs big chunk of S.F. building,” or infamously “Facebook nabs first urban office in downtown San Francisco,” 436,000 square feet of office space spread over 33 floors of a high-end tower, the “181 Freemont,” for up to 3,000 Facebook employees someday, God willing, the biggest office lease signed in three years at the time. A year ago, Meta put it on the market as sublease. Now TikTok is talking to Meta about leasing three of the 33 floors.

Obviously, asking rents are not coming down, or are coming down only slowly, or still going up in some markets (LOL?), because the last thing that landlords can afford to do right now, when they have to refinance a maturing mortgage, is to show that asking rents, if they can actually fill the space at those rents, will not support the new mortgage payments at the new interest rates.

Instead of lowering asking rents, landlords throw in massive concessions, from long periods of free rent, to fancy buildouts. And actual rents signed into the lease may also be lower than asking rents. And when landlords get tired of messing with it, they throw in the towel, give up on their investment, and walk away to let the lenders mess with it.

Massive repricing underway. So for example, the plot thickens in Los Angeles, where the availability rate rose to a record 27.6%. Last year, Canadian real-estate giant Brookfield defaulted on $1.1 billion in mortgages backed by office towers, and it is now getting rid of those towers.

In late March, it was reported that Brookfield made a deal to sell the 1-million-square-foot tower at 777 S. Figueroa for about $145 million to Consus Asset Management in South Korea. The debt on the building amounts to $319 million, composed of a $269-million mortgage and a $50-million mezzanine loan. The sale price would amount to less than half the value of the debt. We would assume that Consus Asset Management will make some kind of deal with the lenders.

Brookfield’s Gas Company Tower, which is collateral for a $350-million mortgage and a $65 million mezzanine loan, and its EY Plaza, which backs a $275-million loan, are in court-appointed receiverships and face foreclosure sales.

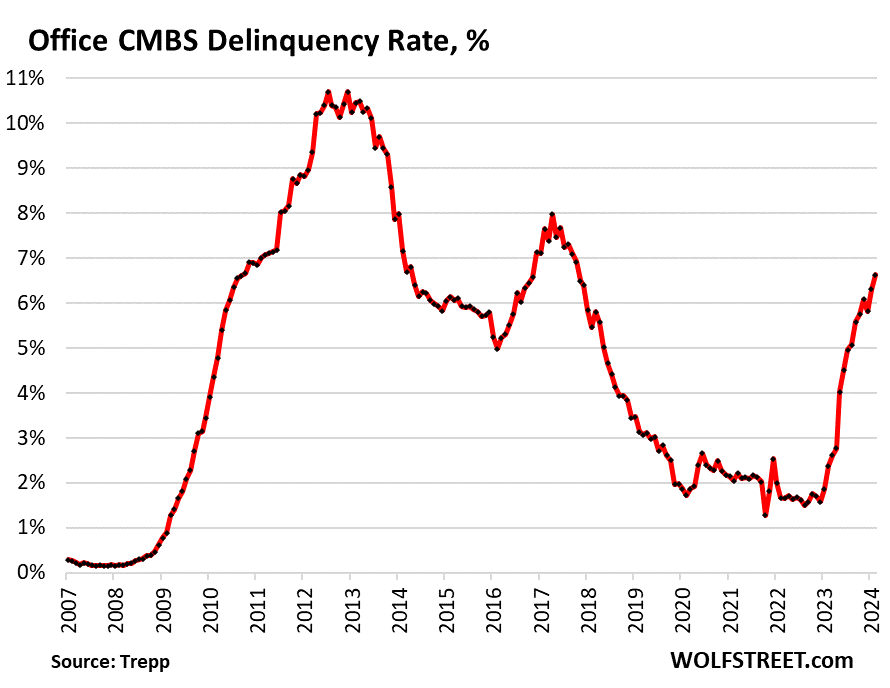

Who is on the hook? For some office mortgages, banks are on the hook, including foreign banks. But lots of the loans that have spectacularly blown up were held by investors not banks, by holders of commercial mortgage-backed securities (CMBS), mortgage REITs, PE firms, life insurers, holders of collateralized loan obligations (CLOs), etc.

So the delinquency rate of office mortgages that have been securitized into CMBS rose to 6.6% in February, according to Trepp, which tracks CMBS. And we’re just one year into it, so this is just the beginning because it will take years to get this mess cleaned up. And at this point, it’s still getting worse:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hi Wolf,

My small company is looking for office space in Phoenix.

You have answered one of my biggest mysteries while touring office space: “this building is half empty..why don’t they lower the rent?!”

You demystified it by explaining that lowering rent is the last thing they’ll ever do.

They’d rather lose the g*dd*mn building than lower rent!

So instead, I will ask for a few months free and plenty of TI, and see how that flies.

Will we get a full-on damn burst soon? Seems like these huge mortgage balances make it impossible to sell, lease, or demolish / rebuild. But the lenders aren’t in a hurry to collect, because they don’t want this problem either.

If you’re discussing a 10-year lease, ask for the first year free.

Good advice. At some point, though, doesn’t this become accounting fraud?

Not talking about the deal itself, but the fiction that a landlord can claim they’re charging $X in rent when they’re really only charging $X – $Y.

If they’re using the $X number to report in financials, or if they’re selling loans to a third party based on fictional rent numbers, that could be fraudulent. Sort of like lying about your income on a loan application.

I’m wondering if there is something weird about CRE that allows such shenanigans to go on.

Accounting rules require that the lease be recognized over the entire period, roughly on a straight line basis. The amount recognized is driven by the cash, but the timing is not.

How is what Trump did in NYC any worse than these deceptive contracts and financial “reports”?

Separately, Louis Rossman on Youtube had a whole series about how he wanted to lease (smallish) retail space in Manhattan and how the realtors routinely claimed the retail space was, say, 25% bigger than the actual area.

The whole CRE market seems like a cesspool of fraud.

If an applicant discloses everything honestly to the lender, then they are not being deceptive.

Most lenders require a copy of the leases, which they will examine during the underwriting phase.

Leases usually contain the full terms of the incentives given. Just like when you rent an apartment, if you get 8 weeks free, it’ll be right there in the lease.

On the other hand, submitting incomplete or inaccurate information would be bad.

Hope this helps!

This is similar to a well known New York case. Over stating value, and all parties agree….yet it is deemed fraud. What goes around, comes around!

Pavel,

My understanding is that while he did take out the loans, the banks agreed on the loans, and he paid them back in full, what raised flags (or, at least what ‘they’ claim raised flags) was he then used differing values for the same properties on the insurance paperwork.

At least that’s whats told to the average news viewer. So much in every industry from RE to Medicine is acceptable or suspect depending on perspectives and motivations. Lots of buildings in the NY area get built, inspected and occupied with greasy palms. Didn’t find the fuss particularly scandalous personally.

*didn’t find the matter particularly scandalous, I meant to say. The fuss, pretty damn silly.

Great answer. Also, commercial rent is usually broken into parts. CAM charges. May or may not include water, electric, security,etc. Real estate taxes. Sq. Footage rent. Not only ask for first year, but perhaps a percentage of revenue, plus cam and real estate., based on occupancy of building. The landlord is not losing money if cam and real estate taxes are paid by you. No out of pocket to them. The percentage is better than nothing toward their loan.

I own a small commercial building with four tenants ( one tenant is H&R Block).

I’m in Gross Lease at about 80% market rent value.

My tenants are happy and won’t go away.

The problem is not demand -but greedy careless landlords asking sky high rent with triple net.

Typical response from a commercial property owner. The problem is exactly demand, LOL, these are systemic changes that aren’t going away. It’s not as simple as greedy landlords.

TD,

Isn’t he saying that if you price at 80% of some mythical, essentially never achieved “market rate” (grossly inflated by those owner-landlords desperate/deluding themselves) there are plenty of tenants to be had.

The problem is that decades of ZIRP and pre-ZIRP caused building buyers to get sloppy…very very sloppy and badly overpay for buildings.

And since most buyers use heavy leverage to goose returns, once their ZIRP era floating loans reset upward (to something remotely resembling reality)…they get destroyed financially (rents can’t remotely cover loan service).

(Note how Fed’s endless, desperate interest rate manipulations (ie money printing) have moved from sector to sector, creating doomed bubbles and ruin in their wake).

You are right about structural change in demand…but ZIRP incentivized/made possible a lot of asinine deals that are now erasing owners’ mythical equity.

Hi Wolf,

I believe you left out pension funds when you described who is going to get stuck with this. The really stinky ones, the ones that need double bagging, will go to the unsuspecting pension funds for disbursement. Don’t you agree?

Maybe ask for free air conditioning for length of lease as well.

So will this powder keg just mess up individual investors or can we look forward to another regional bank blow up or even a foreign bank?

Are the usual suspects shorting the CMBS? Paulson mentioned by Trump for treas sec? Ridiculous?

At some point, 4-5 macro factors have to combine to push the US into a recession. In 2008, it was SkyHigh home combined with subprime mortgagees that did the trick. This time maybe we’ll see CRE, consumer credit & higher for MUCH longer inflation combine into just the right mix to cause a recession. For now, though, that synergy doesn’t appear to be strong enough to push us into a recession. In fact, it’s still far off as is any real implosion from CRE. It’s unlikley that we’ll see any meaningful bank failures this year that cause any great concern for the Fed or the economy.

In the grand scheme of things & as is usually the case, a recession is what really corrects things, so let’s not be overly concerned about comes out on the other side the slowly simmering CRE debacle.

Pants,

I work in CRE. To your question about lowering the rent. It’s two-fold. Once the landlord starts marking down the face rate, in the eyes of the market, the entire building will be marked to that lease rate – the landlord would much rather give concessions (free rent and TIs). The second piece is that the lender sometimes (debt funds often) have the right to approve a lease and if it’s not within the leasing guidelines. It will be denied by the lender.

I would recommend: first, make sure you are represented by a tenant rep (landlord pays the fee). Next, ask for as much free rent and tenant improvement dollars you can. There are likely a number of landlords competing for your lease. Sign a shorter term (5 years) lease with an option to extend for another 5 yrs at 3% above the last year of the initial term. Good luck!

Real Estate Guy,

Very Useful Info.

How do market pros peer through the misleading “market rates” and discover the “net rents” actually realized after unpublicized landlord concessions?

With these landlord tactics so common, I have to imagine that services have arisen to provide potential lessees with more accurate rent rate info, so they don’t have to rely entirely on the landlords’ cooked numbers.

As to lender approval of leases…that is very, very interesting also.

Considering that CRE frequently requires building owner equity of 35% to get the other 65% in loans…handing this sort of power (lease sign off) to lenders…is just asking for trouble (see floating rates too).

With that much owner equity in a deal, lenders can,

1) Help building prices get irrational through pseudo-loose lending at cycle bottoms (luring in naive equity),

2) Require high required equity to create big margins of error/collateral cushions for the lenders – even in eras of idiot overvaluation,

3) Watch as building prices soar thanks to naive, exposed building equity owners,

4) Lenders start to drool as inevitable interest rate hikes occur (years of ZIRP, really? Really?)

5) Building values start to crater as lenders *now* pull back, so deals evaporate and comps implode,

6) Desperate building equity owners (facing soaring debt service costs) then try to save themselves by cutting lease rates to fill building…only to be cut off at knees by calculating lenders, who block lowered lease rates.

7) Equity owners are forced to default, losing some/all of their equity, lenders get building back, with somewhere between 0% and 35% of the starting cost paid for by the forfeited equity, and tenants get put through a psycho-circus of absurdly inflated/volatile/misleading rent rates.

Basically, ignorant/paint-huffing building equity owners have walked themselves (and, temporarily, their tenants) into a calculated lender trap.

(Which doesn’t sound all *that* different from tactics employed by lenders pre-2008 in different sectors).

cas127,

It’s quite easy to see through landlord tactics like this because in the office market, most landlords are price takers, not makers. Keep in mind that a landlord with pricing power is one that has very low vacancy in a building that is well-located, high amenitized, and desirable physical attributes (large windows, high ceilings, etc).

So going back to the price taker landlords, it’s simple to know within a certain radius which buildings are giving what free rent and tenant improvements. As landlord with more vacancy become starved for cash flow, they will increase the amount of concessions or ultimately fold and lower the rent. From my seat, most office landlords are in the phase of holding on hope and giving large concession packages instead of lowering the rent.

Also, mathematically speaking, it’s easy to run a simple net effective rent analysis that will account for all of the levers and “tactics” being used. Also, it’s the tenant rep’s job to make sure their client is getting the best deal they can relative to other lease deals being signed in the market. They run availability surveys and do net effective rent calculations to help their clients understand the landlord tactics.

Real Estate Guy,

Thanks for the info.

I guess I was really asking about how more casual outside observers (like bloggers…) might divine true net rent rates (vs. Mythical building owner ask rates).

An actual potential tenant can invest the time and money to do detailed bird-dogging for a very localized one-off mkt.

But a blogger trying to get a read on market over-valuations for dozens/hundreds of metros…can’t go down this route.

And even for lessees who pay tenant reps…there is always the very real danger that these reps have been suborned by landlords (who those “tenant” reps are continuously doing business with – not like one-off tenants – and such landlords who are highly incentivized to pay kickbacks to get multi-million dollar leases.)

Landlords have to show their banks and insurers, I think, high rental figures. What they don’t show them is rental holidays, rather than lower rents. I.e. 6 months rent holiday per year rather than halving the rent. Not a problem

See my comment above about accounting fraud. How do they get away with this?

I’m told it’s a victimless crime to lie to lenders.

I do work in insurance, and your supposed to give an estimated value of amount. If you fall short of actual costings you get penalized by higher deductibles and they give you less for replacement value because well you didnt buy enough coverage. The insurance underwriter is going to bloat the replacement value of a property to charge you more. Same thing with banks, if they know you will pay them back they rather loan you more money so they make more off you. The underwriter will devalue what they can get off your property if they have to sell as collateral so that factors in interest payments due to risk. Then both parties negotiate based on what they agree is the true value, just like insurance. Do us a favor and stop politicizing BS. It’s considered victimless because its not really a crime. Its contract negotiations.

It might be, but there really is a victim – the notion of a free market.

Imagine if you went to rent an apartment, and the sites like apartments.com said the average rent in the neighborhood was $1000/mo. But everyone is secretly getting a special deal – with incentives, they’re only paying $500/mo.

You’re the sucker who pays full price. That’s called a market failure.

A commercial lease is a long legal document that spells out everything plus some. There are no verbal side-deals. It’s to protect both parties.

It is not victimless. Many borrowers overstate their property values but the punishment for lying is very selective. Those that are punished are the victims.

Owing a little is a problem for the borrower, owing a lot is a problem for the lender. Hence, lenders have an incentive to stick their head in the sand and hope the problem goes away. Many RE invest have used this as a tactic to make the best out of a sour deal (Trump)…. Incentives are reported to the bank, but the bank is hoping for the best as they are married to the borrower.

You’re asking about disclosure.

During the application process, most lenders demand a copy of all active leases, which will plainly show the rents and incentives to the lender’s underwriters.

Some leases also have a clawback for the incentives if the tenant breaks the lease early.

Pretty stupid bank or insurance company that doesn’t require actual financial statements and support to make their own estimate of value.

As a former CRE lender, I will tell you that the banks are FULLY aware of the free rent and TI concessions being offered by landlords to potential tenants. It is understood and underwritten into the credit approvals. Banks are in the business of lending $$, but more in the business of making sure those $$ eventually come home! These markets are cyclical by nature and subject to boom and bust. Now … if you can sell off some of that risk through syndication?? Or even better, through a commercial mortgage-backed securitization?? Buyer beware.

We’d love for you to get in on the ground floor… or Any floor! Please just lease something! I’m having to drink Aldi coffee I make myself. For the love of all things holy, lease this floor.

😉

Finally inflation seems to be going down, somewhere at least ?!

The good news is that while you cannot afford food, you are free to starve in some of the largest and cheapest office space on the face of the planet !

I remember during covid, building my 120 square foot chicken coop and buying used solar panels from decommissioned solar farms (two separate projects around my gentleman’s farm of mine) and at one point, being privy to the pricing of these materials, realizing to myself that I could build a shed the size of my chickens coop using fully functional solar panels as walls instead of weather rated plywood and it would be cheaper with the solar panels than the plywood.

From that day forward it has been ingrained in me that the things that ALL people NEED will be forever going up in price and nearly everything else will be blowing in the wind.

What a world our betters have created for us, huh ?

Fried Chicken. Yum

I suspect that a lot of these vacancies are tech related and all of the post-covid work-from-home-mandates. I know family members who are “tech” workers and who work from home (WFH). Their employer would all employees return to the office, but has not pushed the issue because specialized niche employees are tough to replace.

Granted, just like at the office, employees are qualitatively different. Although these guys work from home, they work a lot of hours.

I would think that some employers would see WFH as a way to reduce costs and skip the brick-and-mortar all together. Or at least downsize to a minimum.

I’m a software engineer and almost everyone at my company works from home. Most of us don’t ever live nowhere near an office. Personally, I live 500 kms away from the nearest company office.

Most of my co-workers are extremely intelligent and the most efficient people I’ve ever met. Despite not living even in the same country, we coordinate and provide value at a very fast pace. My manager is delighted with my productivity, so much that he raised my salary several times without me asking.

And yes, sometimes I’ve worked in my pijamas. That doesn’t matter.

* pajamas

(I’m Spanish, by the way)

“Pajamas” is transliterated from Hindi. With the way it’s pronounced in India, “pijamas” should really be just as correct. Buenos dias!

Many of the persons who increased the sizes of their homes with “offices” and the like during the pandemic with the expectation of WFH can now look forward to having no job and proportionately-higher HVAC bills.

Not clever.

Most people I know that were working remotely during 2020-2021 are still working from home, at least partly. Location: Spain

Some just put a cover on the 1960s billiards table in the basement.

Perhaps the accounting is collateralized similar to car financing with O% interest, or delayed payments for x months.

We’ve seen this American movie before with the “Mallpocalypse” right? Or are there ways in which this time it’s different?

Among other things I suppose it may end up having a material impact on municipalities’ tax revenues, depending upon the extent to which they are reliant upon corporate real estate taxation as opposed to residential.

When these towers sell for close to land value, the new owner can do all kinds of things with them, from renovating and cutting rents by a lot, to tearing down the building and building a condo or apartment tower. That’s what needs to happen, and it’s happening, but very slowly.

It disgusts me how much waste and misallocated capital happens due to the easy money policies. Many of those office towers should never have been built.

I agree with you, Misemeout.

I still see cranes around here in ATL; some of them may be for residential condos but the stupid was strong here in the South.

Meantime the 10 year breaks out on the up side thru 4.34 this morning. Trouble is brewing. I wonder if the fed will step in to save its donor class?

With inflation already stewing this does not sound good.

Of note…… if AI calls for employment to decline it will be so much easier to cut folks who work from home.

I only have a subjective opinion but I think AI will initially create jobs until products are brought to the market that eliminate jobs, and in some cases, AI will create additional jobs such as AI in conjunction with automation. This quote from 1958 still relevant today, with a twist. Can AI be utilized to improve the quality of life or will it simply create more profits for the few?

“No worker is against automation as such. He recognizes that automation creates the possibility of such a development of the productive forces that no one anywhere need ever live in want again… But at the same time automation is forcing every worker to re-examine the very manner of his life as a human being simply in order to answer the question of how he shall exist at all.”

Glen – that quote is THE existential question, if there ever was one, for the spacecraft’s large-and-varying crew since the Enlightenment and Industrial Revolution…

may we all find a better day.

The one thing AI can’t replace is being retired!

Not to mention oil exploding……

The fed is in a bad place……thanks to the dc morons.

Yes. Kicking the hornets nest in the middle east around the time that oil demand is finally recovering in China and the global south is…not clever.

Kong was killed climbing a skyscraper. The great ape fell 100 floors to his death. Fay Wray was unharmed.

Myself, I avoid any large city that harbors these tall bldgs, nothing good seem to come from them ( except wolf street). Also the clothes I wear would be out of place, I would need to dress like a transient or put on a suit and tie.

@fred flinstone: The Fed cannot escape its own culpability by pointing fingers at dc. They are part of the same cesspool. I remember the Oohs and Aahs emanating from the media and financial talking heads when they were fascinated by how Greenspan was indecipherable – this was during the years he kept interest rates down while he talked about the “wealth effect” and “irrational exuberance” from both sides of his mouth. I repeat, both the Fed and dc are part of the same cesspool promoting the interests of the American oligarchs while grinding the masses into the ground. “Greed is Good” is the ultimate statement for how we lost our way.

Btw, they also awarded the title of “Maestro” to Greenspan for his rich contributions in creating the dot com bubble smh.

And, of course, who could forget “Helicopter Ben Bernanke” and his follower Janet Yellen who continued to blow bubbles in the last 20 years.

Thinking about it a bit more, I would lay almost all of the blame on the Fed rather than on the dc morons – because the Fed is attributed to have more knowledge and responsibility than the wheeling-dealing dc crowd.

The oil me be ‘exploding’ in the next few months but look at the future contracts. Lower Oil prices are still in the future. So no, the FED know this and will still lower rates June/July.

Ciprian Gal, nothing fails so spectacularly as a futures market.

Remember last year, when the CME Fed Futures market said we’d have 7 rate cuts by now?

Good times!

Howdy Folks. More ZIRPed to Stupidity? Why not build, borrow, at 2 to 3 %???? You can possibly IPO it too….. Good Luck Youngins, watch and learn…………

My buddy who has since passed owned a higher end furniture store. He did well for years until he hit a big retail speed bump some years ago….well before this latest debacle in CRE. He could either move, or shut down, but instead asked his landlord to adjust his rent to a percentage of gross. In good months the landlord did great, in tough times he did not. Worked for both parties. Next months rent was based on last months receipts.

…but, but, I understood the idea/goal was to play with mostly ‘someone else’s’ skin in in the game?

may we all find a better day.

The waste water district my wife manages just purchased a building . 3 story Class A space with big parking lot. Landscaped grounds complete with a creek and Koi pond. Hottest part of the Suburbs of Portland within a stones throw of Nike’s Campus. Built in 1998 by a growing software company that eventually sold out to a big UK company including the building.

After much negotiation this 90,000 square foot building sold for only $169 per square foot.

The towers in downtown LA are now selling for $145 per square foot, including the 777 S. Figueroa mentioned in the article.

If the Boston market is any indication – those vacancy rates are misleading.

Let me explain:

At the end of 2020 I worked for a mass media holding company that had several operating subsidiaries in Boston with large work sites in downtown Boston or its surrounding cities. This, of course, was during the height of the pandemic and everybody was WFH and had been for months.

In early 2021 the holding company suddenly shuttered three of those subsidiaries. All 420 people who had formerly worked at the three corresponding work sites (which varied in size from ~80 – ~200 persons) were terminated. All ~400 people received 14 days of severance, instead of the 60 days that should have been allocated under the WARN act. (Note: I luckily took a buyout about 90 days before the cuts).

How did they skirt the WARN act? About 100 days prior to the job cuts the holding company’s lawyers sent out “surrender letters” to the two landlords indicating that they surrendered any claim on occupying the space. In effect, they declared in a legally-rigorous way that there was *no* worksite. In doing so, they successfully skirted the scope of the WARN act. The two lawsuits subsequently filed by terminated employees were quickly dismissed.

Yes, the holding company was still obligated to continue paying the lease – but they must saved at least $5 million on severance payouts.

This was not a unique occurrence. I don’t know how widespread the practice is/was, but I know of at least 70K additional sq ft in Boston that is technically “leased but vacant” due to similar actions.

I’m disappointed that this sort of sleight-of-hand hold legal water – but demonstrably it does. Plan accordingly.

Interesting point. However, it seems that those lawyers in MA got away with something that no longer works:

https://www.nortonrosefulbright.com/en-us/knowledge/publications/d4a250ec/warn-act-counting-for-remote-employees

While the regulations provided guidance on “outstationed” employees, until recently, it was not clear whether remote workers should be considered under this guidance or as separate employees working from their own personal site of employment. A recent case has added clarity on this issue.

In Re: Hoover v. Drivetrain LLC, the Court concluded that the text of the “outstationed” employees regulation undoubtedly covers remote employees.” No. AP 20-50966, 2022 WL 3581103, at *4 (Bankr. D. Del. Aug. 19, 2022) (emphasis added).

Accordingly, a remote or telecommuting worker’s “single site of employment” is determined by either (1) the single site of employment to which they are assigned as their home base, (2) from which their work is assigned or (3) to which they report. Id. (citing 20 C.F.R. §639.3(i)(6)). The US Department of Labor’s guidance also confirms this interpretation. Thus, for example, an employee living in Miami who receives work from or reports to a supervisor in the Houston office of a business would be considered an employee in the Houston site of employment for WARN.

You can thank WFH for much of this situation. According to Kastle Systems’ metrics, in person office attendance rose sharply, from about 15% of the pre-pandemic rate in April 2020 to almost 49% at the beginning of fall 2022 for its national index. But then it hit a brick wall and has only risen to about 52%. The very slow recovery (if you could even call it that) since the end of summer 2022 definitely does not portend well for office landlords.

Honestly, if Metro Boston is any indication – WFH isn’t much of a thing outside of Boston proper and it’s immediately-surrounding suburbs.

Curiously, I have noted that a couple recent startups shifted from “in office-only” models to WFH when they grew beyond a couple dozen employees. Both are presently wholly-owned by private equity. I wouldn’t be surprised if the shift isn’t being motivated by WARN Act skirting in the manner I describe in one of my comments.

WFH is killing business district in Boston. I’m one of five retailers, street level, left in my building. Boston avg. may be 23%….but I think the financial area is about 30% vacant. Add that to only 50% of workers back, basically Tues thru Thurs..we are dying a slow death. The landlord will not budge, as the mortgage holder will not allow reductions . last week a building near by sold for half of its purchase price in 2020. Change is coming, and it will be painful for some

I’ve also noticed Boston is on a Tues-Thurs schedule the last few months. Not much traffic on the expressway or 128 on Mondays & Fridays lately.

Our business (mid sized medical practice) has cut back office space size by 80% over the last 10 years, the back office personnel are fully WFH now with only occasional in person training meetings and enough physical space for IT equipment. I’ve said this many times in the comments here, but multiply our business by 10,000 other similar businesses, and it’s really hard to see CRE ever being the same as knowledge work just doesn’t require old school physical proximity.

Many of these contracts have clauses that prevent the owners from renting at a lower price to other tenants; otherwise, the lower price must be applied to the previous contracts.

Seems like some parallels exist to the shift many, many decades ago from manufacturing to service sector. Cities built around manufacturing would have significantly changed as well as the labor force and more importantly the factories and the land was likely repurposed. I would imagine this took a long time and admittedly just a loose parallel.

Its still happening across the US, especially in the upper Midwest. Plenty of old factories and steel mills rotting away. It will be interesting to see how long it takes for office towers to be demolished and replaced with something useful.

These loans typically migrate to the most naive investors – retail customers looking for high yields, hedge funds willing to take big risks, foreign banks who don’t know what’s going on over here. Most US banks, including the regionals, have pretty good books of loans because they know how value properties. They have the medical buildings, the apartments, the retail that is still good.

So if there are losses, they will probably not hit the banking system. There maybe be one or two dumb banks who missed the boat, but the overall regulated system should not see much of an impact.

Lots of weasely statements in this article… but it takes a different view from Wolf’s perspective.

The headline is ignorant bullshit, and I deleted the link. No, “banks” don’t hold ALL of the CRE debt, far from it; investors and the government hold the majority of CRE debt, and so banks don’t face the maturities of those loans they don’t hold. I’m so sick of this ignorant bullshit about banks and CRE. I have discussed this at length and in detail in numerous articles, who holds what CRE loans — including who holds the maturing debt. If you’re too lazy to read those articles and get informed, do not drag this ignorant bullshit (written by a moron reporter with a degree in journalism) into here just because it tickles your fanny.

And by “ignorant bullshit” I’m being merciful with that moron reporter. Because if the reporter actually knew that the government and investors are on the hook for the majority of CRE debt, the article headline would be an outrageous filthy effing lie. So assuming that the reporter is just a stupid moron who doesn’t know any better is the merciful thing to do.

These people need to replaced by AI. AI cannot possibly dish up more BS and lies, and it’s free and fast.

But you should have known better.

LOL because Gemini didn’t get historical imagery wrong at all…. We are beholden to what the AI programers “feed” us.

My apologies… I didn’t mean to do a drive-by four days ago and get your dander up. I am just circling back around to this now.

I get most of my news from either specialists like you (Wolf) or from the overseas media. In this case the article was in an Irish newspaper and was a reprint of a Financial Times (British) article. So I don’t know from the way it was written if they are talking about just US banks or global banks in general… obviously we are more interested in American banks’ exposure but I suppose that a London journalist might have a different focus. And clearly the journalist didn’t understand (or convey) that for the most part the problem doesn’t rest with the banking sector.

Moreover some of the lingo strikes me as weird … but that may just be something lost in translation. I honestly don’t know if the reporter is stupid (entirely possible), lying (also possible), or just confused. He is relying on analysis from financial analysts at a real estate consulting firm so it is also possible that they aren’t very good at THEIR jobs… or (more likely) there is some benefit to them to get the reporter to tell the story this way.

But what grabbed my attention was the article’s effort to quantify the problem. While I have enjoyed your articles about the CRE debacle (and totally agree with you about who is going to bear the burden) I have nonetheless never seen the size of the problem laid out. Their guess is that $2 trillion in CRE loans will need to be refinanced over the next three years and $670 billion of those can be considered “troubled.”

To me that seems like a reasonable guess.

SpencerG,

“While I have enjoyed your articles about the CRE debacle (and totally agree with you about who is going to bear the burden) I have nonetheless never seen the size of the problem laid out.”

Yes you have. Maybe you just didn’t read it? These articles are full of numbers, just not in the headline. You’re going to have to read the actual articles. Here are some examples:

https://wolfstreet.com/2024/03/18/whos-on-the-hook-for-multifamily-cre-mortgages-1-taxpayers-far-ahead-of-2-banks/

https://wolfstreet.com/2024/02/12/cre-loans-maturing-in-2024-balloon-by-41-to-929-billion-after-loans-that-matured-in-2023-werent-paid-off-but-extended/

https://wolfstreet.com/2024/02/19/49-small-banks-are-heavily-exposed-to-bad-multifamily-cre-loans-some-may-topple-but-their-small-size-limits-contagion-fitch/

https://wolfstreet.com/2023/04/10/banks-and-commercial-real-estate-debt-a-deep-dive-investors-and-the-government-on-the-hook-the-majority-of-cre-debt/

So we have a market (rental space) that is unable to respond to demand shocks with price adjustments because both the landowner and the bank have normalized lying to each other as being a normal business practice.

We will end up with empty buildings while new companies are also wanting space, but cant get it except by using gimmicks. I suppose the gimmicks do provide value but also reduce market place transparency and price discovery.

The response is by either renegotiating the mortgage or letting the building go back to the lender which then can sell it for land value, at a huge loss to the lender (mostly investors, but also some banks, including foreign banks) which allows a developer with a much lower cost base to do something with that building, from tearing it down and replacing it with an apartment or condo tower, to renovating the building and putting the space on the market at much lower rents. And this process will go tower by tower, and it will go on for years.

My real estate firm was just hired by a bank to prepare and sell a 58,000 sq ft light industrial building that is licensed for cannabis manufacturing. Two years ago the building appraised for $17.9m, the bank took it back for a little under $5m last month. There are approximately 260 buildings in LA that are some stage of default, and the list is growing each month.

FYI. Small regional banks, unlike their larger counterparts, are more likely to hold loans originated by the bank. The Fed put out a watch list that contained 540 small regional banks after SVB went tits up. A lot of investors are going to get hurt before this is over.

DD,

I can not imagine the amount of money fleeced out of investors in California. An indoor grow inside a building in southern California?

$.26-.30+ per kWh? Sorry, you couldn’t give it to me for free to grow.

California never addressed the cartels or the whacked out taxes.

From studies I have read, you need about 4000 acres of irrigated farmland to grow enough cannabis for the ENTIRE USA. So if you look on the map, you can see those green circles of farmland. Those are 125 acres out of 160 acres. So, roughly 500 acres per square mile (640 acres).

You need just 32 of those green circles. So, maybe 2-4 medium sized farmers at a retail price of about $.05 a gram which is generous. This is nothing, compared to regular ag. Nothing. This is what looks like if it was legalized as a farm ag. Look at those hemp production and harvesting videos.

Almost all of the cost is due to regulations, so better pray for the hold outs against total legalization. I am hoping for maybe 8 years of hold outs. I had a very good 8 years of this, but I doubt I will be doing this very much longer. Good luck.

Comment Section: “How could Office landlords HIDE these rent concessions, isn’t that fraud?!”

Multiple Responders: “They’re not hiding them, the rent concessions are written in the leases, which is given to lenders and buyers for underwriting.”

Comment Section: “LALALA cant hear you, fraud fraud fraud, office owners bad, prominent New York case!”

I’m not a fan of corporate greed either, but why do people ask questions yet refuse to acknowledge the responses? It’s almost like people will not look at the nuance of truth if it contradicts their assumptions.

I don’t see how its any different than the mortgage-rate buydowns & other incentives that builders offer to new residential buyers.

Good article, Wolf. Let me try to add a thought to it. The greatest pain of all this will befall debt investors/ lenders. Largely, they just don’t understand how bad this can get (and will get, IMO). Equity should be priced to lose some money. It’ll often lose all, but at least it’s not a big shock. Debt is another story. Lenders will get the keys on properties that are underwater. They kind of expect that from time to time, but not at the magnitude they will see. What they don’t expect is to get the keys on properties that are worth zero, or negative. How would you like to be a lender on Oceanwide Plaza in Los Angeles, a property that, optimistically, is worth negative $150mm?

Oceanwide had another $2 billion two-tower project, this on in San Francisco. Oceanwide — the Chinese property development firm — is now being liquidated, and that’s the equity part you mentioned. That project in SF was brought up to grade, before construction was halted. This is cattycorner from the Salesforce tower, which you can see in the background. Contractors haven’t been paid, everything is in bankruptcy, no one know what to do with this cancer in the middle of San Francisco, debt investors likely got wiped out too.

I took this photo on May 24, 2021… so that was nearly three years ago. It still looks that way, but the construction crane in the background is gone. This will remain a huge cancer in SF for years to come before it gets sorted out somehow.

I’m still waiting to see some homeless tents cropping up on the site.

There’s a big fence around it and 24/7 security inside.

MW: Inflation concerns reverberate for second day, putting a 5% 10-year Treasury yield on the map

Re: the cost of demo of an office tower in a dense urban setting, which is where most of them are: I knew explosives were out but didn’t think it would be as expensive as this guy says on Quora.

Profile photo for Ned Boff

Ned Boff

·

Follow

Retired Electrical & Controls Engineer

·

When the World Trade centers collapsed in 2001, a nearby building was damaged severely enough that it required complete demolition and removal… it did not collapse, it needed to be, essentially, dis-assembled floor by floor.

The 39 storey building cost about $130 million to build, and cost almost $240 million to demolish (including the costs of toxic materials removal and remediation)

Even adjusting for the fact that the tower was built in the past when it was cheaper, that is still pricey. As expensive as conversion to condos might be, it must be cheaper than this.

Before the Kushner building on Fifth Avenue was saved from foreclosure by a Qatari purchase, it was run by every investor in the US. One remarked: ‘it would be better if it was just dirt’,

Good thing McKinzie advised many corps on the ‘open office concept’, including with extra bathrooms. Easier to convert to dormitories and flop houses.

This was very informative Wolf. Thank you!

While it is possible that humanity (and technology) will evolve to a point where it will no longer be necessary to work together in a supervised setting, like an office, it is a uniquely Western/North American phenomenon that offices there are still much less inhabited than their counterparts in Asia and most of Europe. Location, customs and practices still matter in office investments.

Those localities enjoy a much higher rate of daily occupation in their office buildings/workplaces than in the US and Canada. Regardless of that singular distinction, in the US – we do have too much unoccupied office space. Office is now a four letter word for most investors and lenders. Employees do not want to work 5 days per week and employers are still having difficulty breaking the habits of WFH post covid. Compounding that problem are the long list of troubles that most major urban centers in the US are currently experiencing – all of which boil down to two factors – (a sense of) Personal Safety and Cost.

There will always be a few brave souls who will venture out and in contrarian fashion, buy when prices are low, however – the nuances and trends in office locations are many – it is essentially a fixed location commodity on the one hand, yet when properly capitalized and managed, a durable, income generating asset. Regardless of that – location ultimately matters more than all other factors combined. If you are invested in areas where businesses want to be, you will be rewarded for your perseverance.

In the 1970’s – the US business community led a rush out of the urban centers for ostensibly safer and less expensive suburban office accommodations. That trend reversed in the late 90’s and continued for years thereafter. The migration is reversing again today and will impact valuations of high rise urban office buildings for the foreseeable future. If the current news cycle of doom and bad news continues unabated for major urban centers in the US – I suspect (that reversal) will last for many more years.

A brief story – in the mid 90’s – this writer (a professional RE investor) went to look at a 1920’s vintage high rise office building located in the heart of Newark NJ. Many of the office suites were vacant. The building had not been modernized in any sort of substantial way, although it had been well maintained for many years. In one of the vacant suites, I noticed a calendar thumbtacked to the wall in a private office – it was from the year 1967 – approximately 3 decades prior to my visit. This long term vacancy had very little to do with the building’s capitalization, management or condition obviously. It was 100% about the desirability (or more precisely the lack thereof) of Downtown Newark as an office location over that long period of time.

I completely agree that it will take years to sort the current state of affairs out between Lenders, Investors and Borrowers. Some “out of downtown” localities will get sorted out and stabilized quicker, my guess is that the majority of distressed buildings in urban centers will not, by and large, lead that wave. Until such time that the mantra of the urban “Doom Loop” changes substantially, one should expect that the tide will remain out for this asset class.