That’s what “spread far and wide” means. During the US CRE bubble, yield-chasers not just in the US but globally gorged on invincible US CRE.

By Wolf Richter for WOLF STREET.

We talked a lot about how exposure to the massive losses in US commercial real estate has been spread far and wide, particularly exposure to the office sector of CRE that now faces a structural crisis that’s not just going to go away, but will have to be dealt with by demolishing older office towers and building something new, and by converting some older office towers at a high cost into residential buildings in cases where that’s even feasible.

But losses are spread far beyond US banks, as we have seen: CMBS holders, CLO holders, global investors, bond funds, pension funds, insurance companies, property REITs, mortgage REITs, PE firms, etc. And no one cares about them because they’re not banks; they’re just investors taking losses, and those investors got paid yield to take losses. It’s when banks take big losses that regulators and central banks sit up straight

US banks have taken losses on office CRE loans, and some US banks have disclosed some of those losses, and there will be more, and so their profits get hit, and their shares crash, and they slash dividends, and some smaller ones with heavy exposure to office CRE might be shut down, but that hasn’t happened yet.

And US CRE losses have spread to banks around the globe. Aozora Bank, a mid-sized Japanese bank, disclosed that it had nearly $2 billion in US office loans; and that it had booked heavy losses on these loans, and its shares plunged. The big Canadian banks have set aside capital to deal with the expected losses from their US CRE loans, and Canadian regulators have been talking about it. European banks too. Deutsche Bank AG got the ball rolling by more than quadrupling its loan loss provisions for US CRE.

So now there is Fitch Ratings discussing the losses on US CRE loans held by banks in the Asia-Pacific (APAC) region.

That’s what “spread far and wide” means. Because during the US CRE bubble, everyone chased yield and gorged on this debt backed by US office towers and other commercial properties in the invincible US CRE market.

Fitch Ratings released a report about US office CRE loans and other US property loans held by APAC banks that it rates, and it had some things to say about banks it doesn’t rate.

“The potential impact of exposure to troubled US CRE segments, particularly office and retail properties, was highlighted after Japan’s Aozora Bank reported a loss for 4Q23, due partly to bad loans associated with US real-estate lending,” Fitch Ratings said in its report.

But this stuff is spread so far and wide that “APAC banks’ exposure to US property, including CRE, is generally less than 2% of lending where publicly disclosed, though many banks do not break out the data.” OK, so we really don’t know and expect more surprises.

Shanghai Commercial Bank Limited: “Higher exposure to the US market accounted for 29% of loans (12% of assets) in June 2023, but the bank does not disclose what share of this is CRE-related,” Fitch said.

China CITIC Bank International Limited: “US exposures accounted for around 5% of loans (2.7% of assets) but similarly this is not all CRE,” Fitch said.

Macquarie Group Limited (Australia) “may have US exposure above the average for Fitch-rated banks in APAC, but this would be mostly in the less-troubled power and infrastructure segments through its asset management business,” Fitch said.

And then there’s this: “Some APAC financial institutions, including banks not rated by Fitch, potentially have US CRE exposure levels higher than the average for Fitch-rated APAC banks,” Fitch said.

And this: “For the small number of outliers in our APAC bank portfolio where US CRE exposures are significantly above average, the lending is generally to select clientele that have low loan-to-value (LTV) ratios, generally around (if not below) 50%. This ameliorates potential vulnerability to US CRE asset price declines. Moreover, banks may be lending against US CRE segments other than office properties – though Fitch also expects weakening across retail, hotel, multifamily and industrial properties through 2025,” it said

Among the banks in APAC that Fitch rates, exposure to US CRE “is generally low,” and it adds, “though there may be a small number of banks across the region where the risk of losses is greater.”

And this report by Fitch adds to the theme that US banks’ exposure to US office CRE and US CRE debt in general is not nearly as bad as initially feared because this debt that is now blowing up is held far and wide around the globe, with global investors and global banks on the hook, and the 4,000 US banks hold only a portion of it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So US entities sold high and, maybe, majority global investors bought high, and gotta eat the loss?

Also thanks for posting late at night Wolf. I always check the website before going to sleep, lol.

I was able to finish this after we got back from cross-country skiing (skate skiing) this afternoon. Skiing was absolutely gorgeous, lots of snow and sun all day. Too bad it was just for two days over the weekend.

Nice! I am glad you had a great weekend!

Talking about the devil, isnt it? (Sorry if i am breaking any rules by putting an external website link, just let me know and it won’t happent again)

I deleted the link. Summarize the article in two paragraphs instead of posting the link, or copy the relevant two paragraphs from the article and paste them into the comment, and add where this came from. You can add the link also, I don’t mind, and I may or may not delete the link. But I will 100% of the time delete the link or the whole comment if you write a one-sentence info-less tease to induce people to click on the link.

Commenting guideline #5

https://wolfstreet.com/2022/08/27/updated-guidelines-for-commenting-on-wolf-street/

Howdy Lone Wolf. Way to go you sailor you. Keep up the good work spending some of your hard earned $$ and enjoying life.

Yes, we splurged on services (lodging and trail passes) and made sure that the CPI for core services remains high.

XC skating rocks! This what I at least try to do few times a week. But here no snow these days.

Shades of 2008 home loan securitizations, spread out globally. But I never saw what percentages of foreign banks’ holdings those were — presumably more than these?

This also reminds me of Japanese purchases of US trophy assets heading into 1990, or US loans into Latin America in the 1980s.

Thank god for US banks — and for those who favor QT and hate QE. If US banks were sitting on all of the $4.5 trillion in US CRE loans, it might be Financial Crisis 2, and QE all over again.

I suppose, I agree, that living compromises ones morals.

Phleep-

I’m vaguely remembering a short TV documentary of Northern European public pension schemes that owned what they thought were secure American debt instruments – the notorious mortgage-based derivatives. A small town Norwegian school district was the case in point, I think.

Some of these were run by local citizen-boards who had no idea what they owned, and even if they did, the way those securities deflated had never occurred like that before. Baptism by fire for the naive investment committee members who bought because others were doing it, or who blindly trusted their 20-something buy-side advisors.

As Aman mentions below, it was the “small guys” (e.g. pension beneficiaries) who suffered from the investment misdeed of their “fiduciaries.”

The scale and contagion of that blowout led to systemic endangerment. Presumably the scale of CRE lending will prove to be less catastrophic…

Investment banks will push whatever product where they have an oversupply, not what is the best deal for the customer. And a lot of the time the customer is far less knowledgeable about the product than the bank.

Financiers must have salivated over these naive investment committees like wolves eyeing fat, complacent sheep.

Serves these guys right. The playbook of exporting to US (by taking US jobs), buying US debt from proceeds to avoid currency appreciation is coming back to haunt.

The Fed deprived yield on safer assets and yield chasing foreigners holding CMBS will now take losses.

But it is the small guys in these countries that will eventually pay the price. Their central bankers will jump in to recapitalize their banks and shadow banks :)

And the world will go round and round and round.

I’d say it’s also enabled by US politicians so they can hand out free stuff to those ironically impoverished by the outsourcing.

Don’t be too happy, other investors include insurance companies, pension funds, bond funds etc. Meaning you or one of your family members may be on the hook also.

Like guys who have, I dunno, some kind of insurance that they pay premiums for?

So… the Fed can cut rates to zero? (Lol!)

No, quite the opposite.

Because this burden is distributed globally, your banks and foreign banks are not on the hook.

So no central bank is going to cut interest rates to zero because of this problem.

The bag is in the hands of the investors

Why are you falsely claiming that credit card debt is low? It’s growing by hundreds of billions:

You posted an ignorant BS comment, linking an ignorant bullshit article on a goldbug site that ignores income growth and population growth, and you ignore the simple fact that most people use credit cards as payments method, not borrowing method, and pay off the card at due date. And the balances you see are statement balances, not interest bearing debt. I’m getting really tired of seeing this dumb BS on my site. Go post that crap on X.

Read this:

https://wolfstreet.com/2024/02/09/our-drunken-sailors-credit-cards-balances-burden-delinquencies-and-available-credit/

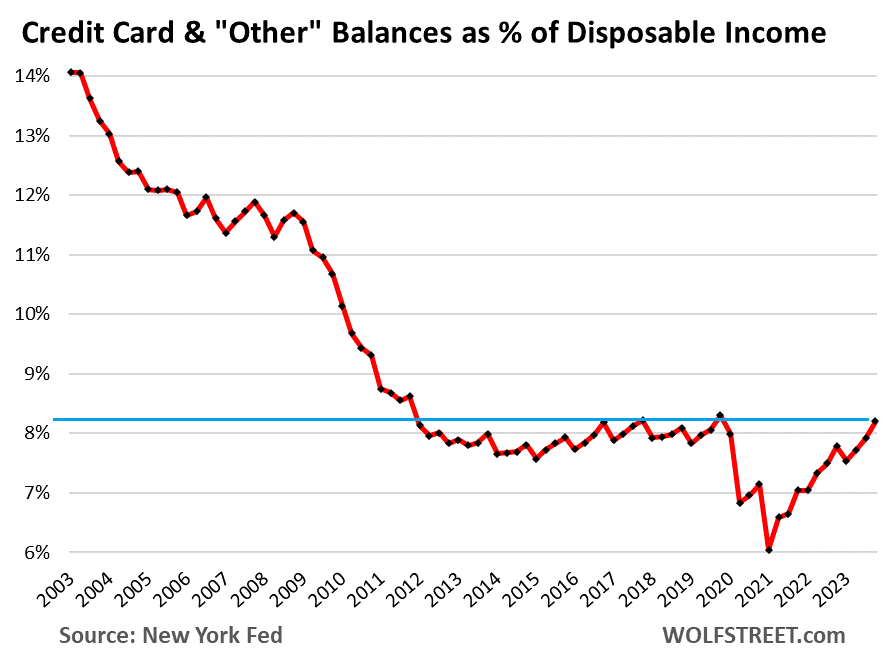

Here is credit card balances to disposable income:

Out of curiosity, why was it so high back in 2003 and kept falling (almost unimpeded) through the GFC? Are people just smarter about keeping balances on credit cards now?

Look at credit card balances – they’ve only increased by 57% since 2003, and “other consumer loans” such as personal loans, payday loans, BNPL loans, etc. have not increased AT ALL since 2003 — despite 20 years of population growth, income growth, and inflation

People are really not borrowing much on their credit cards, which makes sense since CC interest rates are so high; they’re using CCs as payment devices and they’re paying them off by due date, and they collect that 1% or 2% cash-back. The interest-bearing credit card debt is relatively small. Households overall are in good financial shape in term of their debts.

It’s the government and businesses that are overburdened with debt, not consumers.

Here’s a graph of credit card rates since 1995:

https://fred.stlouisfed.org/graph/?id=TERMCBCCALLNS

Although it shows the minimum as being 12%, I’m pretty sure I had a 10.49% rate at some point, and my rate might have been even lower. Margin loans from a broker were at a ridiculous 3% (or lower) at some point. Im actually glad CC rates are sky high now, since it moderates spending for the small remaining sane subcomponent of society.

Funny how everyone talks about US CRE but noone talks about the biggest (Evergrande) and second biggest (Country Garden) real estate developers in the world now being officially bust with 500 billion US$ gone just between these two. Fun fact: the biggest asset class in the world is -or, as of now, was – not the “US Stock market”. It was chinese real estate.

Then the question about the reciprocal of foreign bank exposed to US CRE come. To what degree are US banks exposed to risk overseas?

But how exposed to them is the rest of the world?

GFC 1 was a disaster because everyone had their hands in US real estate pie.

If their exposure is low then that doesn’t really affect us does it

You also forgot Germany me thinks the banking system is a worldwide spider web ,all intertwined. Going to bring the whole system down . Could be a whole new world no pension,ss Medicare. NASTY

Plenty of people talk about Evergrande and Country Garden — the Wall Street Journal does every week or two and Bloomberg almost every day. If you want somebody with Wolf levels of care and intelligence maybe Michael Pettis comes close, though he unfortunately posts on Twitter instead of having a blog with a great comment section.

The difficulty though is that China is *way* less transparent than other countries. You can tell that Wolf has a good idea of what’s happening in the US, Canada, Japan, Germany and a few other countries, but rarely talks about other ones, presumably because they don’t have data which is as public or accessible.

And China goes further than “not public/not accessible”. Half the stuff they do publish are lies. It is like trying to figure out what’s going on in North Korea or in the USSR. You can do it, maybe, but you need to know people inside the borders and you need to speculate a lot, and I guess that’s just not what happens on this site.

We here talked about Evergrande so long ago that people already forgot it? Namely TWO YEARS AGO, in 2021:

https://wolfstreet.com/2021/09/12/the-wolf-street-report-what-a-collapse-of-chinas-evergrande-would-mean/

https://wolfstreet.com/2021/09/15/what-a-collapse-of-chinas-evergrande-would-mean/

https://wolfstreet.com/2021/09/19/the-wolf-street-report-chinas-crackdown-on-debt-tech-evergrande-sends-frazzled-wall-street-titans-to-china/

And we’ve talked about some others too, including Oceanwide, which has some huge now defunct and bankrupt projects in the US.

What about this Top 40 bank, which is much closer to home for me in the USA.?

New York Community Bancorp (NYCB.N).

• Backstory: In late 2022, NYCB doubled its size by buying mortgage lender Flagstar Bancorp. A few months later, it bought some of the good parts of Signature Bank, which had just been seized by regulators during a bank run.

• Feb 8 (Reuters) – Embattled NYCB faced its third credit-rating cut on Thursday while default worries from exposure to the beleaguered U.S. commercial real estate (CRE) took its toll on lenders in Europe and Asia.[Its debt is effectively “junk.”]

• Feb 9 (Seeking Alpha) – New York Community Bancorp: Just The Tip Of The Upcoming Banking Crisis Iceberg:

(*) “NYCB is a top-40 U.S. bank by total assets, reported a loss of $252MM for 4Q due to a sharp spike in loan loss provisions, which were $552MM for 4Q. By comparison, these provisions were just $62MM in 3Q.”

(*) “…this huge reserve build-up was primarily due to just two loans: A co-op loan and an office loan. One can just imagine how bad risk management is at many U.S. banks if only two loans can lead to a large loss and a huge dividend cut.”

(*) “…NYCB has relatively low exposure to CRE loans, which accounts for 12% of its total lending. As such, U.S. banks with a higher exposure to CRE lending will very likely face much worse issues soon.” [Wells Fargo, Deutsche Bank, etc.]

(*) “The FDIC and FED have just changed its rhetoric: the FED removed the phrase ‘The U.S. banking system is sound and resilient’ from its latest FOMC statement. Moreover, Jerome Powell recently said that commercial real estate ‘feels like a problem we’ll be working on for years. It’s a sizable problem.’”

1. We’ve been mentioning it, including in this article.

2. Your last paragraph at least is twisted manipulative Zero Hedge BS, which shows me where you’re coming from. What the Fed actually deleted was this paragraph on the bank panic that is now gone — which they had started inserting in every statement after March 2023 bank panic:

“The U.S. banking system is sound and resilient. Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain.”

That’s the paragraph it deleted.

The Fed removed the paragraph because the bank panic is gone, and the “tighter financial and credit conditions” are gone and financial and credit conditions are now loosey-goosey. Removing this bank-panic paragraph was part of what made the statement hawkish.

Wolf-

You have a “Debtor Nation” link on the Home page (left side, blue), along with other well chosen and useful subjects.

Given the importance and interdependent nature of cross-border investment, especially in the credit markets and in crisis management, would you consider adding a new link that includes articles related to global debt levels. For example, commenters often express befuddlement over sky high Japanese government debt levels, and concern over bloated Chinese Local Government Debt.

Systemic debt analysis (government, corporate, household, financial, actuarial) from country to country would be fascinating. McKinsey Global Institute tried to do a series on this back in 2010, but seems to have given up — it was probably distasteful to their government and financial industry clients.

Thanks for your diligent reporting!

Agree with this idea!

on this topic public and private debt in japan is no different from the total in the uk!

More free stuff from donations not that hard to build your own links document yourself copy paste the links into a notes page on phone or computer and done.

Bs ini-

“… build your own links document yourself…”

True enough, but it’s Wolf’s interpretive abilities I keep coming back for.

Also, I wouldn’t trust myself to scratch and peck between all the data chaff to find the kernels of data wheat…

Very interesting. I wonder if the CRE vacancy/valuation problems buried in CRE backed securities are as much a part of this in other major cities globally. Paris, London, etc., or is this a more N American thing with so much work from home sticking around.

And the bank examiners are where? The banks shouldn’t even be in real estate. Bring back the Real Bills doctrine.

Howdy Folks. Bubba is looking into his crystal ball and sees the Govern ment subsidizing residential rehab of tall buildings in the sky.

@DFB I won’t be surprised if the government bails out the banks and the rich people that own empty office towers, but I don’t expect many to be converted to residential since it would cost a crazy amount of money to convert an older high rise office building into apartments.

Howdy ApartmentInvestor. Are you sure Govern ment would not spend a crazy amount of money on this????????? I think the cities with the overflowing new populis, legal and illegal is perfect for exactly what I saw. My crystal ball is crazy though, some of the things I have seen had me scratch all the hair off my head.

If it is needed, this would happen for sure: Convert to residential apartments.

Just wait and watch.

But we already have glut of multifamily homes coming to the market in the coming time.

Howdy jon. YEP. HUD has so many tools in its toolbox too….

Fed and State governments already are funding building conversion subsidies in all different ways . In my small town grants and other incentives to convert buildings ongoing

TYLER, Texas (KLTV) – A Tyler skyline staple will soon get a new life as an apartment building with space for new business. A New Orleans-based private developer is teaming up with Tyler architects to redevelop the old Carlton Hotel building into something Tyler and East Texas can be proud of.

A conceptual plan shows what the Carlton Hotel building could look like following its…

A conceptual plan shows what the Carlton Hotel building could look like following its transformation.(Fitzpatrick Architects)

“We are projecting that construction would begin next year,” said Brandy Ziegler with Fitzpatrick Architects.

Ziegler said for years Fitzpatrick Architects have focused on revitalizing downtown Tyler. It’s an effort that really started for them with the transformation of the People’s Petroleum Building, and now they’re tackling another skyline fixture: the old Carlton Hotel building.

The Carlton Hotel featured bright colors and a vibrant rooftop pool at one time.

The Carlton Hotel featured bright colors and a vibrant rooftop pool at one time.(File photo)

“Right now we’re studying it as apartments,” Ziegler said. “And we’re looking at over 100 apartments in the building, which would mean 100 new apartments for downtown Tyler.”

QE can take many forms with Fed government subsidies just not funded by the FRB but is inflationary

As a layman who knows nothing, it makes me wonder what would happen if the US government launched fixed-rate 10-, 20-, 30-year mortgages for commercial real estate.

The US appears to get away with it for residential real estate, yet other countries haven’t followed its example.

Howdy Borb. They ZIRPed US into craziness, doubt we will ever be surprised at Govern ment stupidity again…….

Are you sure about other counties not providing cheap mtgs for residential ? Canada and Scandinavian countries were some of the worst with super low interest loans on RE for 40-50 year terms but not fixed the rate floated

I’m trimming at what I consider to be a top and will probably wait for the natural correction. Commercial real estate is “deep tricky” and white swans can rapidly lose their brightness depending on where they swim. It looks like the usual malarkey and shenanigans are at work.

Job #1, preserve capital.

This is the problem with THE DOLLAR as international reserve ccy!

You trade and accept dollars, then deposit the dollar into US assets! In fact, i think credit suisse targeted “foreign”ers for their own AT1 bonds.

There are externalities.

I guess we’ll see whether there is any contagion effect.

I know this is about office space, but retail isn’t immune either.

There won’t be any contagion effect.

These things are so wide and thinly spread, I don’t see any thing out of ordinary here.

Even with a slightest of the problem, FED would come to rescue.

As long as they are interfering in the free market, they never have and never will rescue anything but indeed cause further damage. If we think this recent bout of inflation is bad, just wait and see if we let them continue “rescuing”. $15 Big mac meal bad? Well if you want a $30 big mac meal, keep voting for the Republican AND Democrat money printers.

Debt – CRE, National Debt, Personal Debt, and so on

all part of the “EVERYTHING BUBBLE.”

This has all happened before…….and has always ended badly.

The difficult part is the timing,

Today, tomorrow, or when?

No one knows, only educated guesses.

What blows up first?

Or will the Fed determine it is TOO BIG TO FAIL ?

Unfortunate Cookie saying:

‘Congratulations, your savings is in American CRE investments.’

The only way to figure out who is really in trouble here with these distressed properties is to see what the pricing on the credit default swaps are pricing in with the owners of the bonds within the underlying. If anyone can see the cds spreads on distressed properties then and only then can someone make a logical determination as what to do imo. In my view this is a big game of lets hide the schitt sandwich.

The problems exist but we can’t see who is getting thumped.

The rules are so opaque its almost best not to play.

“And US CRE losses have spread to banks around the globe.”

There seems to be no discernible perturbance in the relentless bid on asset prices that we have seen for the last 15 years of the reality of MMT, er, QE. A zombie economy, dependent on government spending to support repression of any idea of what the concept of a “free market” entails.

First and foremost would be the non-prosecution of the criminals to enforce, apparently toothless, draconian punishment for financial crimes.

The reality failed the first test.

Banks are immune from the disease the cause.

This is not surprising. The sharpies in the US always sell the worst stuff to suckers overseas. The Japanese, in particular, are famous for being able to swallow anything. They have lost their shirt every couple of years on US investments.

Thank you for that, the heads up about what the Japanese are famous for. Not the war in the Pacific rather than their incompetence as Wall Street investors.

An ancient, beautiful society.

Why are getting mad at someone framing something in a different time frame than you would?

For over 70 years the Japanese have been known more as investors than warriors.

Sorry you are hung up on something that happened 70+ years ago. The world has moved on.

Sometimes there is a “too big to fail” pig out there too.

My guess is that commercial real estate is not, currently, a good investment. CRE prices are not determined in a competitive market of everyday slogs bidding on a rocking chair built in the 1700’s.

Tying this back to a previous article, one of the things the U.S. is good at exporting is their bubbles. From movie studios in the 1980’s to CRE now, they U.S. is great at dumping their crap on foreign investors who have to to have the latest trend and alway catch the tail before it crashes.

None of this shows up in trade balances either.

With residential RE white hot, conversion to residential apartments with some investment won’t be a big problem and any government will provide convenience with a toll.

Except that many office buildings cannot be converted into apartments at a reasonable cost, such as those 1980s models with big square-ish floorplates. Apartments need windows. It’s cheaper to tear down those worthless old buildings and build something new.