All of these Treasury securities have been sold. So here are the holders.

By Wolf Richter for WOLF STREET.

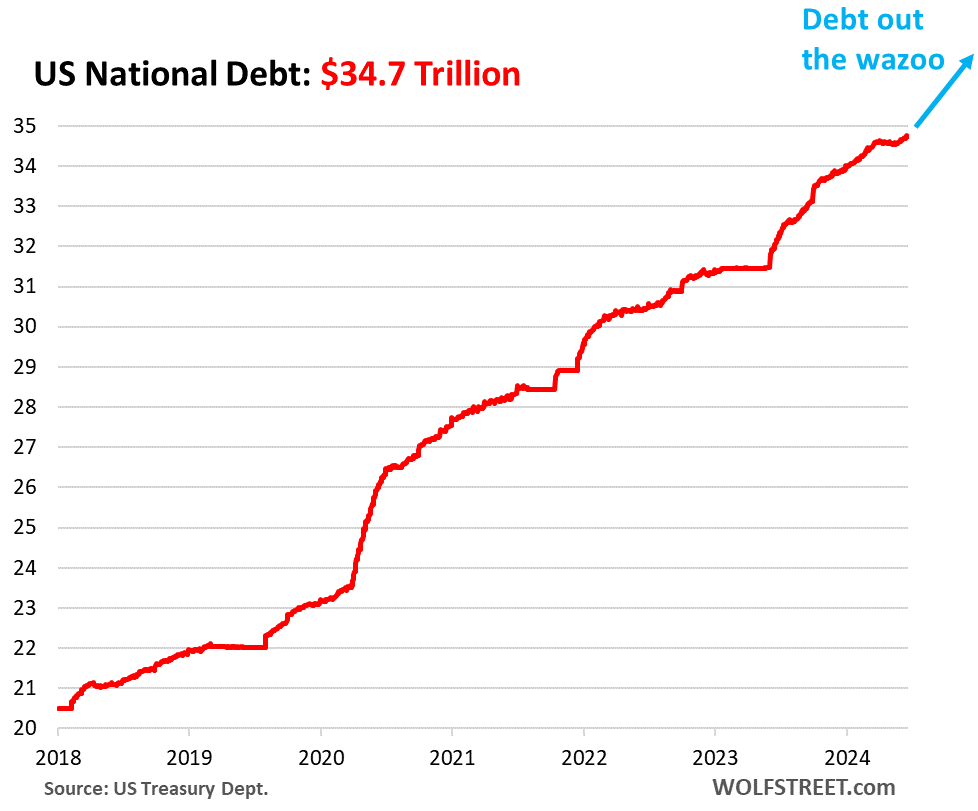

The US national debt – now $34.7 trillion, up from $23.3 trillion in January 2020, and from $27.6 trillion in January 2021 – has spiked so fast that it would make our eyes water with disbelief, if we didn’t know better. Over the four years and five months since January 2020, it has spiked by $11.4 trillion. Since the pandemic trough, the economy has been growing rapidly, yet trillions were flying by so fast it’s hard to see them. We don’t even want to imagine what this will look like during the next recession.

But every single one of the Treasury securities that the government issued was bought, and we’ll get to the holders in a moment:

Who holds this $34.7 trillion in debt?

Every single one of these Treasury securities is held by some entity or individual. So here they are.

US Government funds: $7.1 trillion. Held by various US government pension funds and by the Social Security Trust Fund (we discussed the SS Trust Fund holdings, income, and outgo here). These Treasury securities are not traded in the market, but are purchased directly by the funds from the Treasury Department, and at maturity are redeemed at face value. They’re called, “held internally,” and are not subject to the yield-whims of the markets.

The remainder amounts to $27.6 trillion currently, they’re the securities “held by the public.”

A small portion of these $27.6 trillion in securities cannot be traded, such as savings bonds (including the popular I bonds), and some other bond issues.

The remainder are Treasury bills, notes, and bonds, plus Treasury Inflation Protected Securities (TIPS), and Floating Rate Notes (FRN). These securities are traded (“marketable”). At the end of Q1 – that’s the timeframe we look at below), there were $26.9 trillion of these securities outstanding.

Foreign holders: $8.0 trillion. Includes private sector holdings, and official holdings, such as by central banks. China, Brazil and other countries have been reducing their holdings for years. European countries, the big financial centers, Canada, India and other countries have been loading up. In total, foreign holdings rose to an all-time high in March and dipped a little in April, which was still the second highest ever. While foreign holders in aggregate have increased their holdings in dollar terms over the years, their share of the total debt outstanding has plunged from 33% a decade ago, to 22.9% now because they have not kept up with the rapid increase of the US debt (we discussed the details of those foreign holders here).

The rest is in the hands of US Holders.

The Securities Industry and Financial Markets Association (SIFMA) just released its Quarterly Fixed Income Report for Q1. It doesn’t spell out the dollar amounts, but the percentage of Treasury bills, notes, bonds, TIPS, and FRNs outstanding. As of March, there were $26.9 trillion of these Treasury securities outstanding. And they were held by:

US mutual funds: 18.0% of Treasury securities outstanding (about $4.8 trillion). They include bond mutual funds that hold Treasury securities, and the T-bill holdings at money market mutual funds.

Federal Reserve: 16.9% of Treasury securities outstanding (about $4.6 trillion in March). Under its QT program, the Fed has already shed $1.31 trillion of its Treasury securities since the peak in June 2022 (our latest update on the Fed’s QT).

US Individuals: 9.8% of Treasury securities outstanding (about $2.6 trillion). These are people who hold them in their accounts in the US.

Banks: 8.1% of Treasury securities outstanding (about $2.2 trillion). We saw in March 2023, banks hold a lot of long-term Treasury securities and MBS that lost a lot of market value due to the rise in yields, and as depositors saw this and got scared and yanked their money out, some banks collapsed. According to FDIC data, the total amount of all types of securities held by banks – Treasury securities, MBS, and other securities – was $5.5 trillion at the end of Q1, with cumulative unrealized losses on all their securities rising to $517 billion. The $2.2 trillion are just Treasury securities.

State and local governments: 6.3% of Treasury securities outstanding (about $1.7 trillion).

Pension funds: 4.3% of Treasury securities outstanding (about $1.2 trillion).

Insurance companies: 1.9% of Treasury securities outstanding (about $510 billion). Warren Buffett’s insurance conglomerate, Berkshire Hathaway, has increased its holdings of T-bills to $153 billion.

Other: 1.5% of Treasury securities outstanding (about $400 billion).

This shows just how far and wide Treasury securities are spread. If these investors lose interest at current yields and demand at current yield vanishes, yields have to rise until sufficient demand materializes. And that can happen all of a sudden, which we saw happen when the 10-year yield briefly pierced 5% in October, unleashing a torrent of demand that bid up prices, and so the yield plunged again. Currently, amid blistering demand, the 10-year yield is back down to 4.25%, even though T-bill yields are close to 5.5%.

To what extent are interest payments eating up the national income, and how long can this continue? See… Spiking Interest Payments on the Ballooning US Government Debt v. Tax Receipts and Inflation: Q1 Update

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I have my little piece of this…T-Bills. First time I had a return on my $$$ in 15 years

You haven’t made any $ in 15 years??? How is that possible?

You have to remember for every 1 good choice there are 99 other bad choices.

For example crypto. Versus say a nice safe 5.5% return on your cash. One is guranteed, the other… well.

“You have to remember for every 1 good choice there are 99 other bad choices.”

100% correct.

During the phoney-upped “good times” of 2002-2024 it was all about paint huffing return on capital (“home prices never go down”, AI, etc).

But the underlying macroeconomic reality is so bad that everybody should have paid attention to return *of* capital.

(Just ask UBS, which is auctioning off a *1 million sq ft office building* in midtown *Manhattan” for a tiny $7.5 mil minimum bid

The past 20 years have been a DC directed enterprise of falsely strangling interest rates through loose monetary policy/outright money printing.

And once those Treasury interest rates were gutted (for year upon year) the moronic application of the discounted cash flow formula “mandated” that low/no return investments were “winners” no matter how risky or ill conceived from the outset.

But it was always a game of Russian roulette masquerading as musical chairs (music provided by the Fed).

The only way to sleep soundly was to embrace the ZIRP, accept zero interest “investments”, and await the inevitable slaughter of those self-proclaimed real estate/AI/etc geniuses.

Maybe ask Ben Bernanke how it could have happened.

Or the American (and global) public that took various benefits at the time. Some was shoring up asset values, some was bailouts. The US political process was stalemated all through the time (except when rushing off to two wars), and nobody would step into the breach but — Bernanke and company. I’m not saying they didn’t overdo it.

0.1% counts as nearly nothing

Me too Mike. Finally after being ripped off for fifteen years.

Ditto, and about damn time. Hopefully, this isn’t too little, too late.

Savers were being punished and con artists were being rewarded.

What is your rate of return after taking inflation into account?

Back of a napkin calculation shows .gov is borrowing $1K in the name of every citizen each month. Likely $2K/month borrowed for each taxpayer (on top of the taxes already paid).

Gen Z will probably see zimbabwe dollars in their lifetime.

That’s probably how it will be dealt with. Either way, it won’t be paid back, because it can’t. Ever.

Ever single Treasury security will be paid back, and always has been. Period. But the overall balance of the debt outstanding will not go to zero, if that’s what you mean.

For the entity which can print the money required to pay off its own bonds to simply refuse to print that money required to pay off its bonds would literally just be a slap in the face to all investors.

Under what legitimate scenario would they not print the money to pay off the bonds ?

That’s right, none. There is no legitimate reason to not do so.

So let’s not act like this is some big accomplishment or anything other than the exercise of raw power through legal tender laws, backed by the full force of the state, and the eventual threat of violence.

Debt gets paid back by borrowing new money to pay off old debt. That is standard practice in corporate America, and it’s standard practice in government — and has been since debt capital was invented. This has nothing to with “printing money.”

… and due to the fact that the “Treasury securities will be paid back” with deflated dollars — created via debt monetization and rate repression — the conversation, it seems, is back to Mike’s opening comment about interest rate manipulation.

Maybe calling it “credit money production” (rather than “money-printing”) would be a more descriptive word choice. Isn’t money production essentially the act of monetizing debt?

Monetizing debt has been the M.O. for decades now. The world’s dominant monetizer is the U.S. central bank. U.S. “debt out the wazoo” is an important and unsavory result, among others…

If and when this monetization/rate suppression/debt growth cycle ends, the economic breakage feared by Powell will begin in earnest, I fear. If it doesn’t end, it’s cantering or galloping inflation to eternity?

Every Treasury Security will be pain back with money borrowed by issuing even more Treasury Securities.

In the private sector they call that arrangement a ponzi scheme.

Lawrence Pusateri,

LOL, no they don’t call it a ponzi scheme. They call it “refinancing” of debt. It’s the most common issuance of debt. Look at the corporate debt, it does nothing but grow, because companies refinance old debt and add new debt.

There are two types of capital for companies: debt capital and equity capital. Both are crucial. This here is debt capital:

Correct, BUT, to quote Alan Greenspan; “The purchasing power of the dollar that you are paid back with, may decline”

Or some such bit of truth. Come on Wolf, CONgress needs to get the fiscal side under control. $50 bead WILL be a problem.

Bernie did nothing wrong.

Weimar republic, and , since I am Italian, in th 80′ inflation and high rates will act as an hidden taxation, taking out of the pocket of taxpayer. Problem is that 80% of the resources are outside the us , and those billionaires only option is to have an oligarchic state.

And collectively we’re paying them interest, at an amount that is more than military spending

“We’re” paying interest to a lot of “us here” who hold these securities, and the “us here” are paying income taxes on this interest income, and are spending some of this interest income on stuff we buy and thereby plow it back into the economy, which creates more economic activity and then more tax receipts for the government to pay for this interest.

On a more serious note, there are lot of other factors that go into this equation. So read this (I linked it at the end of the article):

https://wolfstreet.com/2024/06/01/spiking-interest-payments-on-the-ballooning-us-government-debt-v-tax-receipts-and-inflation-q1-update/

High intereste rate in the 70s to 90s is responsible for the high interest burden. The same thing will happen again if interest rate spike.

The reason is generation x and generation z are lazy and won’t work two jobs at the same time like the boomers did. That’s why everything fell apart because generation x and generation z had no initiative to work. Consequently GDP has been lower than it would have been ever since.

Tony,

I am lazy assssssss fuck. I mean, not in my private life, but for work, yes. You must be amazing.

Thank you for this. Lots of people seem to forget that one person’s debt is another person’s investment.

Hi Wolf, thanks for your knowledge.

Isn’t paying old by freshly printed debt something like Ponzi ;-)

Mighty USD lost about 98% its value since 1971, the time Nixon killed Dollar.

It is something like -2% annually.

It makes me wonder what sane person collects worthless paper/binary code in network.

There is one asset that survived 5000+ years, and still has same value.

In mighty Switzerland, we got screwed in last 3years by about 40%. Of course, everybody talks economic theory.

Well my bills, food stores payments tell the real story. Swiss still have lots of money, so nobody cares about 50% inflation yet.

1. “Mighty USD lost about 98% its value since 1971,”

Not quite that much, more like 87%.

2. “It makes me wonder what sane person collects worthless paper/binary code in network.”

Send me all your “worthless paper dollars,” I will dispose of them properly. You can find the the mailing address here: https://wolfstreet.com/how-to-donate-to-wolf-street/ Any “binary” dollars can also be gotten rid of via the instruction.

Your entire comment documents that you don’t understand what dollars are. They’re financial measure of a quantity: such as assets or liabilities or labor or goods or services that you measure in dollars. You can measure gold in dollars. Or RE, or stocks or oil or crypto and your wages of course. A currency makes trade possible, instead of bartering. Using dollars to account for everything from labor costs and stuff you sold, to the value of the factory allows you do to modern bookkeeping.

No one invests in “dollars.” They invest in assets measured in dollars, and they take on liabilities measured in dollars. Even the paper dollars are not “dollars” per se, but are “Federal Reserve Notes,” as it says on each one of them: an interest-free loan (“note”), denominated in dollars, from you to the Fed; an asset for you, and a liability for the Fed. There are only $2.35 trillion in paper dollars out there, much of it overseas, and for people who hold them, they’re assets.

If you want to compare gold, you have to compare it to other assets, such as RE, stocks, bonds, cryptos, etc. That’s a legit comparison. Gold did better than some and worse than others. But comparing gold to “dollars” (a measuring device) is goldbuggery silliness.

If it is any consolation to you, Hajes, the Canadian $ has done a lot worse than the US$ since 1971. Most household goods lose most of their resale value within a few years of their purchase even when their value is measured in US$. My own standard of living has gone up significantly since 1971 and I am now in my 20th year of retirement.

@RealTony,

Thanks for keeping it real and always pointing a finger at someone else.

As a Gen x who worked for 30 years climbing the it corporate ladder only to be left holding the bag do to mass retirement of baby boomers. It was clear most corporations didn’t read the writing on the wall or plan for such a large shift in the workforce. That led to many of us gen xers being burned out and choosing to retire early.

Blame whatever you like or whoever you like, it doesn’t change the situation we’re in. The booming market, the booming real estate, and growing consumerism of the newly retired boomers and growing younger generation facilitated my ability to retire early.

I like to say we get what we get or more clearly we get what we allow and that’s just exactly what we’re getting.

Tony sux!

You sound a little like a tool, too. But I guess Tony brings put the worst in everybody.

” at an amount that is more than military spending”

Since some of us would love to see military spending slashed by 75%, that’s a good thing! It’s just that we’d like to see the military number drop, not the interest number rise….

Ask Britain how it feels to be a former great global power. Gettng there is not a joyful path either. It feels pretty poor in everyday life, methinks, unless one is a scavenger atop what remains.

The national debt can’t stop spiking or it would crash the economy sooner. Everyone should thank Congress for this wisdom. Just watch for when Government members start piling into the lifeboats first, that’s your cue to bail.

Obviously, this fiscal madness of vast overborrowing and can will crash just as it need to do to reach a balance again.

“your cue to bail.”

To what assets? To where geographically? To what lifeboat?

Elysium was on last nite, maybe that, or the moon, or Mars, or whatever it really is Flannery Associates are up to over by Rio Vista, CA ? They even have a few % of your remaining filthy rich Brits and Irish “bailees” in on that one.

I’m just gonna go down with the ship where I lived most all my life….if I can.

Luther Burbank was right.

…the utter irony of ‘California Forever’ – a foreign outfit with the gold rush mental landscape hellbent on cashing in on yet another chunk of the beautiful, rapidly vanishing unpaved one…

may we all find a better day.

Seems natural that the political machine with attempt to control or reduce this but the side affects of that will clearly offset any progress if any. One could argue a less stable world keeps the US attractive for buying debt. More imperialism, trade wars and related likely coming for America as when you can’t fix your problems you look for deflection. Crazy what part of that debt is illegal and unnecessary wars and that is just looking at the front headline ones.

Historian Niall Fergusson recently invoked what he calls his own personal law of history: Any great power that spends more on debt service than on defense will not stay great for very long. True of Habsburg Spain, ancien regime France, Ottoman Empire and the British Empire.

I’m gonna have to read a bit more history to check that one out… I suppose the Other way to keep ahead of that is, as u mention, blow more on Military and Wars to keep the balance there ahead of the debt service. Seems like a debt spiral to me. :-(

The only thing that remains the same from these historic civilizations or societies and now, is human nature. Systems have continuously evolved and failed over time because of humans. No system has been developed that can withstand our ability to make it fail by simply being ourselves.

What if the proponents of MMT are correct and since most countries are in the same boat, or their finances aren’t well audited (China, etc). none of this matters does it?

Right. Look out for yourself.

The big tuna is ok, the small tuna is going to be left in the sun flapping it’s tail when the tide turns, a slow, miserable and desperate future awaits the small tuna.

On our way to the promised land… We have only managed the promissory note landing.

The shining city on the hill is now the run down casino on the hill with a debt of 34.7 trillion and counting.

Of course it matters, and matters now more so than ever.

Ha ha like there no such thing as history. “This time is different” LOL.

The proponents of MMT ARE NOT RIGHT. FYI, you do realize that the MMT method for managing inflation is to raise taxes. Now, I’d say they may have a point, if you could find politicians willing to raise taxes to the extent necessary to cure our current & future spikes in inflation. Otherwise, they’re a bunch of looney tunes characters. FYI, MMT was dreamed up as a basis to speed up wealth transfer and equity to lower income cohorts.

Pre-Great Recession, US debt to GDP averaged about ~60%.

Post-GR to COVID it ran around 100% for a decade.

In the post-COVID period, it is running around 120%.

Why is this time different?

Is it that we are arguably at full employment based on the unemployment and labor force participation rates?

Nice reply to put it in perspective. I just wish you would have gone back further in time.

The federal government just needs to hold spending at current levels for a couple of few years while inflation rages at 3%+ and things will look much better fiscally.

It’s not government’s job to inflate out of fiscal crisis. Views like yours are the reason many people do not trust government any more. Government and the monetary system should be transparent, fair, and honest.

Are you glued to news sources that promote a can-kicking mindset? You seem to be convinced inflation and money printing are normal and acceptable.

And I’m not referring to Wolf’s site, obviously. The charts don’t lie. The bias is in the interpretation.

This time is different because there is no leadership in government. How can there be, when leadership is punished by the masses, and griftership is rewarded. The USA is a B grade bond rated organization at this point, at best, and people don’t realize it because of the entrenched momentum governments have compared to stocks. Governments are supertankers, while individual companies are more like speedboats. The time it takes for the behavior of the vessel to change after engine failure is very different.

The public cannot or will not process the critical facts, and make the needed critical decisions collectively. Walter Lippman wrote about this in, like, the 1920s. One gets a feedback loop of fools or liars through the electoral and political process. Politicians promising free candy are voted in. This is the cardinal defect of self-rule by the people, as agonized over by the founders.

…”the tragedy of the median(s)”?

may we all find a better day.

Would be useful to know just how much collateral value those bonds have. If you are a retail investor who buys at auction your buy takes a real haircut in the secondary market. Treasury does stealth QE by rolling over mature bonds, when there is no real purpose than that, other than inflating the money supply. Expanding the money supply is inflationary. Asset inflation is inflation, period. All sources of cheap labor and cheap oil has been exhausted. (This is why tech is so alluring, it requires minimal input from either. Unless you consider all the energy needed to run those AI data banks). If you want to buy a bond don’t worry about the yield, ask yourself what my dollar will be worth when they are done with it. My thought is it that loss of purchasing power will reverse in correlation with DEFLATION in the money supply.

A comment to your great work Mr. Wolf. The Federal Reserve’s “purchase” of the debt on behalf of the government it is chartered under, is really a form of monetization of the debt.

This has been done for literally thousands of years in its more crude technology form of debasing precious metals with base metals, shaving off the edges of coins (direct inflation), different changes of coins’ replacements all starting for Rome in the 3rd century BC. The historical record of this debased inflation’s best surviving record is Emperor Diocletian’s decree carved in stone of 301 AD (a period of 600 years since the Roman start of debasement at least). The US Constitution originally stated that money was to be gold and silver written a mere 230 years ago by classically educated people.

Look at a Federal Reserve note (dollar brand); that states: “This note is legal tender for all debts public and private,” meaning that the note has to be accepted when it really has no intrinsic value.

This question of where the inflation is coming from has been going around in circles on a wild goose chase. Some is the essential monopoly of trade; i.e., “supply chains;” also historic as in President Theodore Roosevelt and the “Trust;” i.e., Antitrust legislation, enforcement of said legislation being questionable today. The second is this obvious debasement of the currency through quantitative easing exposed recently in the UK in a official report by the House of Lords entitled: “Quantitative Easing a Dangerous Addiction.”

Bottom Line: The Federal Reserve isn’t going to stop inflation because they need as much as the population will accept to cover the currency debasement they already funded the government with; i.e., Federal Reserve’s “holdings.”

The Federal Reserve, as the articles above clearly states, only owns / holds 16.9% of the US federal government debt and it has told the federal government repeatedly to stop its massive federal overspending or face severe consequences as has the IMF.

“it has told the federal government repeatedly to stop its massive federal overspending or face severe consequences”

I suggest a simple search

‘the revolving door and the Fed’

Because Wall St. has the public’s best interest in mind?

Is that them warning us all in the public interest, or them covering their arses so they don’t get the blame when the shit hits the wazoo?

In managing the deficit the only thing untouchable, not able to drop, is the interest expense.

Ellen Brown: “the government is borrowing at interest to pay the interest on its debt, compounding the debt”

One possible mid-term solution (can kick) could be an increase in the Social security tax rate from 6.2% currently to something more like 8%, on both the employer and employee side. Assuming no immediate increase in benefits this would put the SS system back into surplus, allowing it to buy Treasuries again instead of running them off. Coupled with a likely increase in the US population to something around 350 million by 2050 – all net immigration – you have more workers paying more SS taxes buying more bonds. Maybe as China and Japan and the Fed withdraw SS picks up the slack. The $2.8T pile could grow to many times that if paid benefits grow under the true rate of wage inflation (another can-kick).

Few people have any real money directly invested in US debt. Even knowing that Treasurydirect exists puts you in rare company. Forcing everyone to else to support the Treasury maker through payroll taxes would have little political resistance compared to some of the alternatives.

That works, but an even easier solution is eliminating the cap on earnings that are taxed.

I think Ol’B’s proposal and your proposal are kind of an overkill. Fiscal 2024 will have a very small deficit, or even a surplus — because interest income rose, payroll taxes (income) rose, and the COLA fell from 8.7% to 3.2% (which reduced the growth in the outgo). I will cover this in October when the SSA releases its income and outgo figures for September and the fiscal year. But a small surplus wouldn’t surprise me.

Removing the SS taxable earnings cap is a bad idea. The wealthy have a track record of changing tax laws that affect them directly. Removing the earnings cap could put the entire Social Security program at risk.

Great comment. The funding mechanism for SS was created specifically to make sure that the wealthy couldn’t coopt it. The wealthy hate SS because it allows people to retire, which reduces the labor force and drives up wages. SS has a cap to ensure that the wealthy don’t overpay and convince people that it is a welfare program, unfairly paid for by the rich. The way it is now, people consider it “their money”. It is probably the governments most successful program, next to the military of course.

“Great comment. The funding mechanism for SS was created specifically to make sure that the wealthy couldn’t coopt it. The wealthy hate SS because it allows people to retire, which reduces the labor force and drives up wages.”

Mao, not great comment, Kent. And your comment was ridiculous. GMAFB. Some of you people need to drop this whole wealthy vs not wealthy b.s.

JimL, you’re right. Very few people pay attention to this. But trying to get taxes raised on the upper echelon of America is a non-starter. Those are the people who contribute to and control Congress.

JD & HN

Spoken just like members of the wealthy elite.

I notice that the wealthy do in fact pay taxes.

Since you say they run the joint, why don’t they pay zero tax currently ?

I mean them being all powerful and all.

The rest of the country outnumbers them is why they pay taxes.

Pitchforks, eh ?

“Trying to get taxes raised on the upper echelon of America is a non-starter”.

I’d say your comment violates several core principles that made America what it is, including democracy, transparency, and equality of opportunity. Once you disregard these goals, it’s a different country. Think about it.

They’re also the people who pay more than 50% of their marginal income to taxes. Enough of this b.s.

G

You are absolutely right.

Those individuals should NOT be paying 50% marginal tax rates.

They should be paying 90% marginal tax rates.

You have to be kidding me! You want to hit me with an uncapped SS payment, on top of an uncapped Medicare payment? Plus 3.9% added to my dividend and cap gains tax?

Wolf – what kind of site is this , comrade?

C

We’re not kidding.

Relax, you will still have oodles of money left over

I don’t think we should tax future generations of workers to correct the fiscal excesses of older generations. The burden of balancing our fiscal affairs should be placed, as much as possible, on those folks who benefited from past excesses.

Taxes are fine where they are or reduce them by half. It’s the wasteful gov.

Reduce the gov by half and their waist full spending by half. Problem solved.

But not happening…

Yes, there is lots of wasteful spending, and I think we need to throw unnecessary and unfair tax subsidies into that category, such as RE tax benefits and the capital gain tax preference.

The entire federal budget should undergo a rationalization study every four years, at a minimum.

How about an honest review of PPP program and unemployment benefit fraud? Fraud is the worst kind of waste.

Bobber, that’s cool. Do it via estate taxes, not income taxes. Income taxes nail the younger people who are just now starting to earn legit income. This is something that seems to escape most people who scream about the rich not paying their fair share. If you just started earning $500k, after years of $100k, you aren’t even close to rich.

I never understood why some people think “death taxes” are so harmful. As far as I’m concerned, I’d rather pay tax when I’m dead than when I’m alive.

The estate tax is an incentive for me to spend my wealth and spur the economy before I pass.

F U, Dude. Let me invest my own money; I can do better than the Government. And I don’t need to subsidize all the losers who can’t bare to save some cash versus ordering out for trash.

Do you all remember a time when journalists presented the facts and just the facts? I really miss that. I love this blog! But, I would be thrilled to do without the snarky and well-broadcast opinions of the author.

Mind you, in this case, I agree with the author. But, it would be wonderful if I could draw my own conclusions without being “steered” to the “right” conclusion.

Sometimes I wonder if our hyper-polarized environment is the outcome of opinionated journalism.

“But, I would be thrilled to do without the snarky and well-broadcast opinions of the author.”

I would like to buy a Mercedes, but without the star? If you don’t like the star, buy a Ford, it comes with the Ford Oval. But don’t ask Mercedes to build cars without the star.

Ehh Wolf, I always took you for an Audi type more than a Mercedes type.

Ford sucks!

My favorite of your comments to date.

Wolfstreet is an awesome online University I have learned more her than anywhere else.

A person who lacks the discretion and subtlety to pause and be quiet here and there, while an opinion is displayed he does not specifically hold, and while reaping these huge benefits from this site, should look within, and not point fingers outwardly that way.

R

You talking about stenography.

Yeah, probably easier if thinking is a burden.

All that snark and opinion gives background and context. You know, the stuff that allows understanding. And aids bullshit detection.

R

You talking about stenography.

Yeah, probably easier if thinking is a burden.

All that snark and opinion gives background and context. You know, the stuff that allows understanding. And aids bullshit detection.

What would have happened if they didn’t print 10 trillion dollars after the pandemic stock market crash? Probably some struggling businesses would have failed but the economy would have recovered slowly. Now that they printed so much money during 2000/2008/2020 crashes, we are now at 35 trillion dollar debts and looking at 50 trillion in the next 10 years. One would hope governments and Fed would have learnt the lessons but they will keep printing money to prop up the stock market quickly during next recession.

Nobody ‘printed’ $10 trillion. Where do you come up with such nutty and totally incorrect notions? As to the Federal Reserve it has been SHRINKING its balance sheet which is now DOWN to around $7 trillion.

SoCal: In Adam’s defense, he’s basically citing unchecked money supply growth (Hanke’s golden number is 6% annually).

I’m not a global- macro guy, but the chart of USM2 is pretty frightening. In Jan. 2020 it was about $15.4 Trillion, and went near vertical in March/May. Topping out at about $21.7 trillion.

The global money supply was also following that trend, and added many trillions (seems to be a difficult number to gain consensus on), going from maybe around $80 Trillion to north of $100 trillion: a 25% increase (or conversely loss of purchasing power).

I see estimates that global debt is as much as 3X that ($300 trillion?). I don’t fully understand how the amortization table works out on that one?

Also, the many aspects of the “shadow banking system” of private credit creation is difficult to measure.

An economy that is fully reliant on debt (sorry “credit creation”) means that anyone with a promise and a pen can “print money.” (Maybe a mouse and a meme?)

APE coins anyone?

Don’t get me started on the derivatives markets.

In the quadrillions by some guesstimates? SRSLY?

Don’t go blaming the Federal Reserve for any of that as it is not participating in that process and has been consistently lowering its balance sheet down to around $7 trillion. As to the rest that is just bogus totally fake ‘money’ creation with no semblance of value whatsoever in any of those numbers.

USM1:

Mar. 31 2020 – $4.79 T

Apr. 30 2020 – $16.25 T (+ $12.47T)

Source: TradingView

Because savings accounts were reclassified from M2 -> M1 in that month.

Grant:

Thanks for the insight. I don’t really follow M1, and only recently started to learn about M2 (as contraction is hailed as a death knoll by some).

And now you see the damage Costco chickens have wrought.

Howdy Folks. 28 Day T Bills. Keep informed by the Lone Wolf and as the you know what hits the fan, YOU will be able to move the $$$$ where YOU decide…….Warren Buffet bought a bunch of T Bills or Bonds? Not sure myself…….

Why are foreigners buying all this American debt despite knowing that its almosy guaranteed that the govt & quasi governmental FED will print money & keep diluting them away forever. There simply cannot be an end to money printing.

Cleanest dirty shirt? One of the most stable currencies?

Yes. As badly as the US$ has performed in recentdecades, it has done better than the C$ and the pound.

Anyone who wonders why foreigners buy our debt should look at everyone else’s debt. Whose debt would you buy? Many Third World currencies have been obliterated by the mighty dollar in the last decade – we are talking down 40 or 50 per cent.

“Cleanest dirty shirt”!!!!!!! I am going to steal that one…

It sounds like you surely know a better option :)

Out of curiosity, what else do you propose foreigners buy?

Prada?

Common stock, including American Depository Receipts issued by foreign companies trading on the NYSE.

Russian!

Thank you for this article. Is it possible from the data to get a breakdown of % owners of t-bills vs. notes vs. bonds?

These investors currently hold $5.86 trillion in T-bills, $14.0 trillion in notes, and $4.5 trillion in bonds, plus $600 billion in FRNs, and $2.0 trillion in TIPS.

“Currently, amid blistering demand, the 10-year yield is back down to 4.25%, even though T-bill yields are close to 5.5%”

Guess that the inflation expectation reflects a return to 2%? The survey says a bit north of that (2.35 on the 5-year breakeven?).

Will the 10-year continue to fulfill Grant’s “return free risk”?

You hit upon one of the most puzzling things. The 10 year has almost continually been less than the risk free t-bill rate for the past couple of years.

I don’t understand it at all.

But I welcomed the opportunity. When I recently purchased a house, I did not need to take out a mortgage, but I did anyway. I like the idea of a cheap, low cost, uncallable source of funds.

The money is currently invested in t-bills used as collateral for selling some deep in the money puts on a couple of very select stocks.

Right now, it is pretty much a wash. The interest on the t-bills plus the premium from selling the puts just about covers the interst cost of the mortgage. I say pretty much only because the timing of money in and out is not perfect, but close enough.

What this gives me is a pool of liquidity that allows me to enter some great price points on stocks at reasonable prices if the puts ever hit (if Brk-b ever drops back into the mid to upper 300’s I will love getting the puts exercised). Or just have access to a large pool of money if some other great opportunity presents itself.

The downside is limited due to the uncallable nature of mortgages. If things get too crazy where I am uncomfortable, I can just close out the position and pay off the mortgage with minimal loss.

As long as the market is going to keep repressing the cost of the 10 year, it provides ample opportunity to take advantage of having a mortgage.

A few nice features of having a mortgage are: fixed mortgages are adjustable if you choose to refi (if rates decline) but are fixed and protect you from rising rates; they can be a tax deduction depending on income level, etc.; they allow you to use money that would otherwise be sunk into the property for gains elsewhere, if you can beat the mortgage rate.

Jim,

You admit you don’t understand it all (who does?), yet you are selling naked puts?

Do you like walking tightropes?

I think there is denial of tail risks today, particularly at the Fed. They probably figure they can just print money in times of crisis, despite the unfairness of it all. That’s why trust is gone and why the system is breaking down.

But will you be able to print money if crisis hits?

Jim,

If there is a downward spike in those assets, even if the federal plunge protection/bailout team shows up again, that takes time. Puts expire and register a potentially big loss before that can take effect. Can you ride out that bottoming-out moment? Sure, you might be right, and will cash in, in ways I never dared to. Or the opposite.

MW: Stocks are having their best election year since 1976. Here’s what the rally needs to continue.

It seems endless inflation or bankruptcy are the only ways out.

The US can never go bankrupt. No country that borrows in its own currency can ever go bankrupt. But they can destroy the currency through inflation.

Indeed, but its citizens can be bankrupted by the inflation.

Yes, but the offset to borrowing is either reductions in spending or increasing taxes. Both of which can also bankrupt citizens. Choose your poison.

They’re more likely to be impoverished by inflation than bankrupted.

If a German investor bought 50,000 marks worth of German government bonds in 1915 with a maturity date of 1925, was he repaid in old marks or new ones?

Would have been rentenmarks, not 1915 era reichsmarks in 1925

Sorry, you lose, bondholder

The easy way is the way the French did it in 1960. Simply say that beginning Jan 1 (or any other date), new dollars will be issued, and that each new dollar is worth 100 old dollars. Then follow that up with a largely state controlled economy.

In 1960, the French economist / mathematician Jacques Rueff, during Charles de Gaulle’s presidency, converted the old franc, to a nouveau franc, equal to 100 of the old franc. However, even with this substitution, inflation continued to erode the currency’s value, though at lower rates of change, in comparison to other countries. And this new franc equaled 20 cents to a U.S. dollar. The old rate was 5.00 to a dollar.

In 1960, the French franc, which was one of the weakest currencies, overnight, became one of the strongest. Correcting policies included plans to 1) balance the budget, 2) stabilize the currency, and 3) eliminate currency controls.

The gold content of the franc increased 100%, & 1) foreign exchange rates, and 2) France was on a managed paper standard; externally, on a modified gold bullion standard. With the new policies, France’s economy strengthened, and the franc became fully convertible @ approximately its gold par, into gold for foreign exchange and into foreign currencies.

With the introduction of the Euro, the franc in Jan. 1, 1999, was worth less than 1/8 of its Jan. 1, 1960 value

Didn’t work out so great for Mexicans 30 odd years ago when 1,000 old pesos equaled 1 new peso. That’s why there were so many immigrants to the USA from there since then, and ongoing.

Holding federal spending at current levels while inflation (and therefore GDP) rises at 3-4% per year for a few years makes everything look much more palatable.

It is a way out.

How so?

If you wanted the dollar to drop and continue its erosion of reserve status you would do exactly what DC is doing….

Is this yet another case of ‘money’ not being actual money, but just a series of black squiggles on a white piece of paper, or whatever colours you have on your screen? A new English word needs to be invented to describe it, although ‘Spawn’ I think would cover it. The number of squiggles is now growing very large, but so is the amount of actual money in Americans hands, more so by far than just about any other country in the world, and has been so for a long time now. Localised turbulence certainly occurs, but widespread bankruptcies with 40%+ stock market plunges have not been experied for quite some time. Something seems to be working, so enjoy it, keep saving, and let the future take care of itself, as it always does. The 5% inflation price being paid is so far manageable, but if it becomes a much bigger squiggle then all bets are off though.

This part of your comment, ” but so is the amount of actual money in Americans hands, more so by far than just about any other country in the world, and has been so for a long time now.” IS true old one like me;;; howsomeever, the problem is the long term and continuing degradation of the money in our hands so by the FRB and other tools of the fools that run and ruin us that the actual VALUE of that money in our hands is less and less and less and less…

Just referencing the official US GUVMINT inflation calculator at the BLS website should be enough to convince any sane person of this stone cold hard fact.

The clear fact of being ”the cleanest dirty shirt” or at least one of them, does not make this degradation any less true in terms of buying REAL stuff such as food, clothing, energy, etc.

END THE FED! And make an independent USA BANK!!

Spoken like a true Geriatric:

“Something seems to be working, so enjoy it, keep saving, and let the future take care of itself, as it always does.”

When the attitude becomes “as long as it is good during my lifetime,” it doesn’t bode well for the “future.”

I recently saw the John Stewart interview with a co-author pf a book called “white poverty.” The claim is that basically 40% of our nation’s population lives in poverty.

The “official” poverty line is a $15k/ year income… somewhere around the federal minimum wage (which shouldn’t be legal/ however it seems like few people are paid this little).

I see many articles about the cost of living in our country. Some propose that a family of four must make $175-$250k annual income for the minimum (seems high/ my family of 4 lives in under 1000sf. Tho).

One I saw today concluded the national median income for a single person has to be $25/hr ($50k/year) to live comfortably. That’s a $17.50/hour difference from the “official” and real numbers.

The point is that the “something” that IS working is the population and the destruction of a “middle class.” The numbers can easily lie. I don’t live in urban area: every one I visit is plagued by homelessness.

I see a tale of two economies.

50k a year is about what is needed to even qualify to rent and still be able to cover insurance and utilities with bunking up. Live in BFE and even a small one bed apartment is $1200/month plus utilities.

“…even a small one bed apartment is $1200/month plus utilities.”

Living by yourself is a luxury for those who can afford it.

When I first moved out and started working, I lived in squalor with several roommates – but that allowed me to save money. The first room I rented was $475/mo.

Struggler – believe it important to consider the psychological effects of the term ‘poverty’ and the self- and external- consideration/placement in a ‘class’. (…have always remembered Mike Todd’s utterance: “…I’ve been broke plenty of times, but i’ve never been poor…”). Best.

may we all find a better day.

The situation can chance very quickly. I mean the USA is an exceptional case but you can see the consequences and speed of the market turning against you in the case of the Liz Truss debacle in the UK, excessive tax cuts were announced and the market panicked about the debt. The Bank of England had to step in with quantative easing to steady the market, not to avoid deflation, but to prevent a mass sell-off. Liz Truss the Prime Minister then removed or pressured to resign. Many blame the BoE for continuing with QT while also passing the bill for renumerating the banking system to the government (something the Fed does not do).

We are now seeing this process begin to be enacted with France.

I wrote in a post maybe last or the one before that France has hit the limit, i.e. the debt interest has hit the deficit borrowing i.e. that they must cut and now the ECB has begun proceedings against France as well.

There is no supra-national body for the USA of course, but I think you can see the writing on the wall. Greece has blown up, France is too big really with their banking system saturated with Italian debt amongst others, and the situation in the USA is that those debts are not being repaid. 10 year USA treasuries at 4.27%, a very high yield for a supposed safe borrower. The foreign holdings at 8 trillion, which aren’t mandatory holders, are the big danger. Japan and China selling off. That section alone is 50K USD per worker assuming 150 million workers.

The reality is that if you willfully refuse to be responsible, like France, like the US, then its inevitable that your fingers get painfully slammed as the till closes. The UK is on the line we had a warning shot across the bows the consensus is now to raises taxes, how thats going to work when people already dropping out of work I don’t know.

Debt accumulation always leads to a crisis.

Not if the assets are growing simultaneously.

Exactly. But are they? Some govt expenditures (like airports) produce assets that are greater in value than the debt used to finance them. But I fear these are the exception…

The method seems nonsensical. You could very well avoid all this at this point and simply have the Treasury issue nothing but 3 month 0 bills forever because US bonds are now a commodity in and of themself.

I mean tbh the US Treasury technically doesn’t have to issue anything. The debt is irrelevant because US dollars are required to pay US taxes.

The interest literally props up social security and the entire insurance industry. Mosler has a lot of interesting takes on this because MMT is generally correct.

MMT is nothing other than bogus nonsensical stupidity. Debt is extremely relevant and very critical to proper economic policies.

The re-circulation of savings is important. Unless savings are expeditiously activated via debt, then a dampening economic impact is generated, aka, secular stagnation.

Nothing “modern” about MMT. Just good old-fashioned currency debasement…

Not saying there is any obvious similarity here, but I keep remembering the City of Detroit. They kept selling bonds to payoff bonds that paid off earlier bonds that paid off even earlier bonds. Corrupt spending on friends, family, and and political favors, paying ever higher interest until they ran out of bond buyers willing to ignore the looming certainty of default. Chapter 9 bankruptcy.

Had the city been able to print money, maybe they’d still be spending like drunken sailors.

All I know is that this kind of spending and debt wouldn’t last a year if people did what the Gov does.

I dunno, all this massive debt and spending just seems surreal.

Detroit didn’t issue debt in its own currency. Big difference. There is no Chap. 9 Bankruptcy for the federal government. There is only the combination of economic growth and inflation.

Ok, what about the Confederacy?

The Confederacy ceased to exist, and its currency was valued accordingly, i.e., worthless. Similar to a person dying with lots of debt and no assets, no need for bankruptcy at that point. The debt is worthless and the debt holders take the loss.

What about it?

You make it seem like we’re good for the $35 trillion debt, no biggie.

How so? You asked about the Confederacy and I didn’t say anything about the Federal government. Invoking the Confederacy is a pretty back-handed way to suggest the Federal government, which does exist, won’t pay its debt. If you were actually commenting about the Federal government’s debt, then Wolf answered your question already: economic growth and inflation.

MW: Stocks down 40% would pop this market bubble — but slow deflation is more likely than a quick crash

When has slow deflation occurred in the past?

I’d say it’s more likely that some greedy fools start selling, which triggers more greedy fools to start selling, etc., until another huge monetary response is triggered. Once people realize stonks and RE won’t keep rising, a tsunami will hit the shore.

In my own mind, I like penciling in another $2.5 trillion or so that the Fed holds in mortgage backed securities, because I see those purchases as kind of “in lieu” of buying treasuries. So, I see around $7 trillion owed the printing press.

Its murky who owns all the ballooning debt, but I’ll go with the Hindenburg.

There’s nothing ‘murky’ at all about who holds / owns the $34.7 trillion US federal debt and the ownership is very clearly and specifically detailed in the article above.

How about, it’s interesting that as the fed dumps their portion of treasury debt, the public debt portion continues rising at an unsustainable level.

I think that’s actually the entertaining thing here, with foreign buyers and the fed, mechanically and temporarily stepping back as debt buyers — which shines the light back on massive treasury issuance, apparently being sucked up by individuals that think they understand this casino.

Obviously the fed will be refilling their debt-based punch bowl as a recession hits, as they bail out somebody or something called Wall Street

No, the Federal Reserve is not going to be filling any imaginary punch bowls at all in the future.

Wolf,

Question for you (to the extent you know the answer):

Do you ever think about how intentional inflation to pay off sovereign debt played out in Ancient Rome, Babylon, etc.?

In Ancient Rome silver coins were intentionally mixed with tin in order to debase the currency (cause inflation), which happened slowly then got worse. Followed by periodic attempts to re-issue new currency, more debasement, etc.

Interestingly, there was a point where interest rates got to about 2%, then fluctuated wildly (hitting 20% and higher several times). Inflation ranged from zero into the hundreds. Interest rates were set by prominent merchants, but the Roman Senate (and later Emperor) had a lot of behind the scenes influence. Periodically, there were threats by the political structure to merchants to force them to cut rates, which then tended to make inflation worse.

The psychology of the period was fascinating, because people tended to have faith that the inflation was behind them with each new attempt to reform the currency (the optimism faded after a while, resulting in a new crisis, which then fueled more reform, etc.).

Assuming you believe that historical cycles repeat because human nature doesn’t change and humans put into a similar situation will react similarly, what are your thoughts about where we are now vs. what is coming down the pike?

If you care what Ray Dalio thinks, he believes that we are headed into one of these periods where the kinds of stuff that happened in Ancient Rome will start happening (not this week or year, but within the next 10 to 15 years).

Tin was not involved with the rather sudden debasement of Roman money, somebody had figured out how to silver-wash copper coins to give them the appearance of being silver, although they had no silver content at all. This happened in the mid 3rd century AD, and amazingly things kept going for a few hundred more years until the end came for the empire.

What parallels do you see to the present time and how do you see this playing out?

A rather sudden collapse that will mystify those who religiously regard official numbers given out regarding the economy, as if they are indeed the holy grail because you can make bitchin’ charts and graphs from said numbers.

And got news for you sunshine, every other country in the west is pretty much in the same leaky boat.

The amount of debt growth is insanely astounding.

@Wolf, Thank you for your insightful analysis. Wondering if there are firther insights into how the borrowed money was spent ? Did the entities that benefited from the borrowed money end up being investors in the additional debt ?

What has surprised me most are the parallels in psychology.

Back then, there was an almost religious faith that the currency value debasement was a temporary measure to fix [fill in the blank– war debts, spending due to the plague, necessary public works like the aqueduct repairs, etc.] and that everything would be fine again.

Then it wasn’t, crash, new policy, renewed optimism, rinse and repeat.

If you read some of the writings from the time, they even talked about pressure being applied by the political class to curb “predatory interest rates”. Now there are endless talks about rate cuts.

It feels like we are careening into the iceberg in the Titanic and no one cares.

MW: Nvidia’s stock set to enter correction territory as chip-sector selloff sustains

Thanks for sharing this insightful breakdown of Treasury securities holders. It’s interesting to see the distribution among various entities. This really helps in understanding the current financial landscape better.

The amount of debt growth is insanely astounding.

@Wolf, Thank you for your insightful analysis. Wondering if there are further insights into how the borrowed money was spent ? Did the entities that used the borrowed money end up being investors in the additional debt issued ?

From: https://wolfstreet.com/2024/06/19/the-foreign-holders-of-the-ballooning-us-debt/

it looks like foreign interest in treasuries is lukewarm; they might be seeing better yields or returns somewhere else.

As mentioned elsewhere https://wolfstreet.com/2024/06/01/spiking-interest-payments-on-the-ballooning-us-government-debt-v-tax-receipts-and-inflation-q1-update/ that the deficit is hanging around 34.6 t for a few months now, so it seems the Treasury does not need to put out supply at the moment, so there would be more demand than supply. was trying to get an idea of the total U.S. bond market including corporate, state and city bonds as compared to the treasuries (and US stock market)?

over the previous 20 years. to flow the money :)