Ugly inflation in services drives up the 3-month “core CPI” for 7th month, to 4.5% annualized, worst in a year, and the 3-month overall CPI to worst since Nov 2022.

By Wolf Richter for WOLF STREET.

So inflation behaved very badly again in March. January was terrible, but it was kind of written off as maybe one of those January blips. February was bad, and so the January-blip story began to fall apart. And the Consumer Price Index for March, released by the Bureau of Labor Statistics today, was just as bad as in February.

It was driven by ugly inflation in “core services” which dominate consumer spending – even as prices of durable goods continued to decline, and as food prices remained relatively stable at very high levels. That energy prices started rising again, after their vertiginous plunge, didn’t help either.

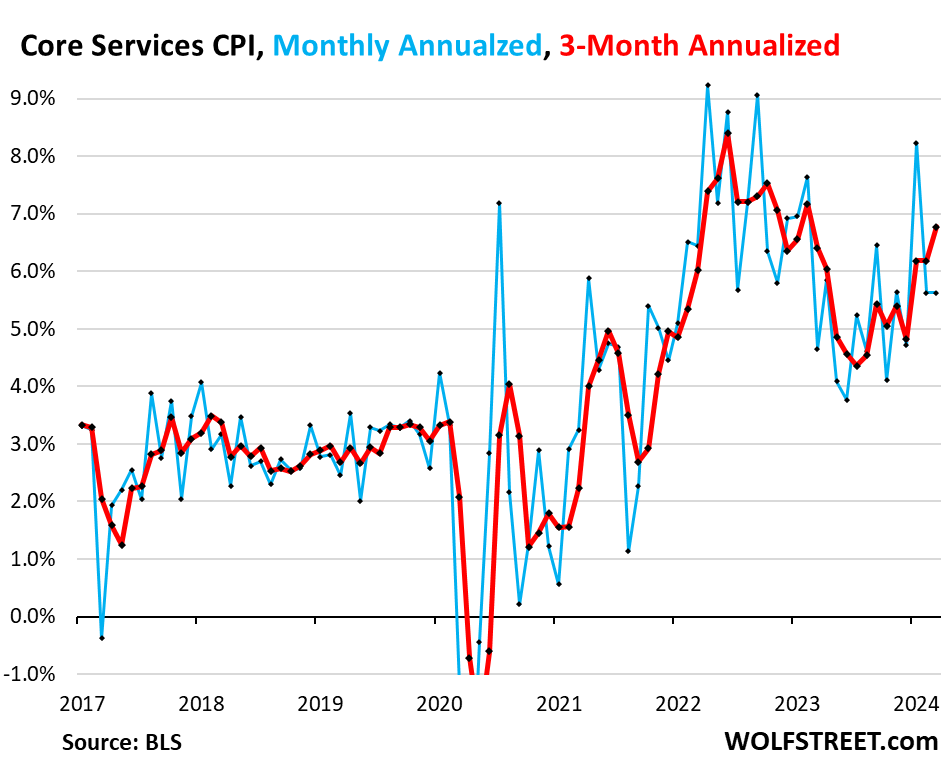

“Core services” CPI jumped by 5.6% annualized in March from February. On a three-month basis, core service CPI jumped by 6.8% annualized, the worst since February 2023. We here have been disconcerted since late last year about inflation in core services. After cooling a lot into mid-2023, it has been reheating. And we started suspecting that the cooling had been one of the head-fakes that inflation is infamous for.

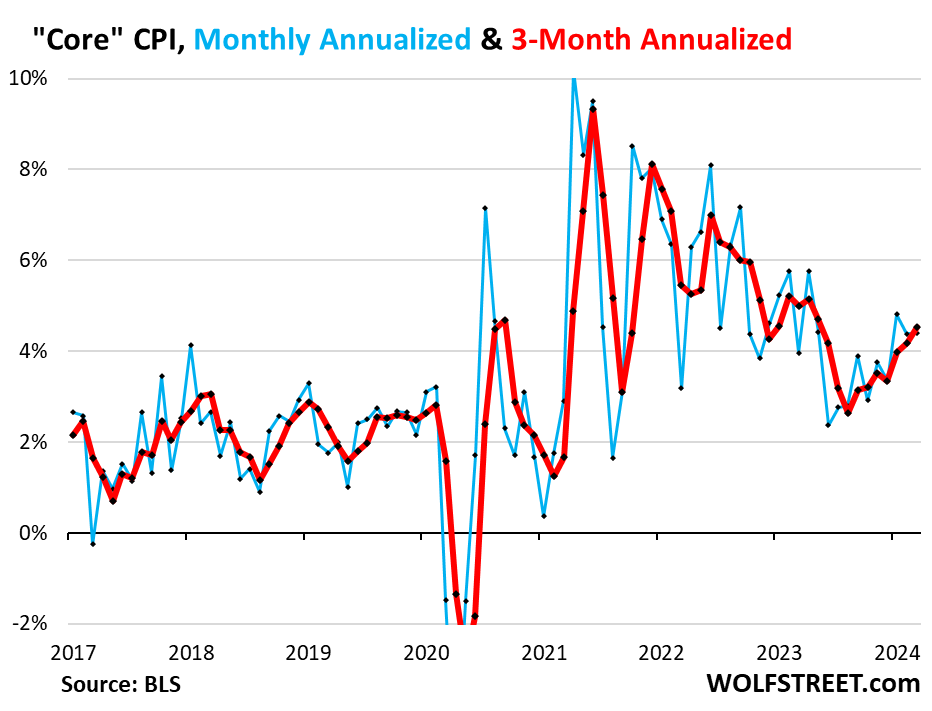

Core CPI, which excludes food and energy, rose by 4.4% annualized in March from February, same increase as in February.

The three-month core CPI rose by 4.5%, the worst increase since May 2023. The drop in prices of durable goods (dominated by motor vehicles) still softened the impact of hot services inflation, but not enough. Inflation in services is just behaving really badly.

The Fed has been in desperate search of “confidence” that inflation would continue to cool after the Amazing Cooling through mid-2023. But that search has gotten tangled up in a nasty turnaround. The cooling process had ended in August. It was hard to see in the fall of 2023. But over the past five months, it has become clear: Inflation, thought to have been vanquished, has raised its ugly head again.

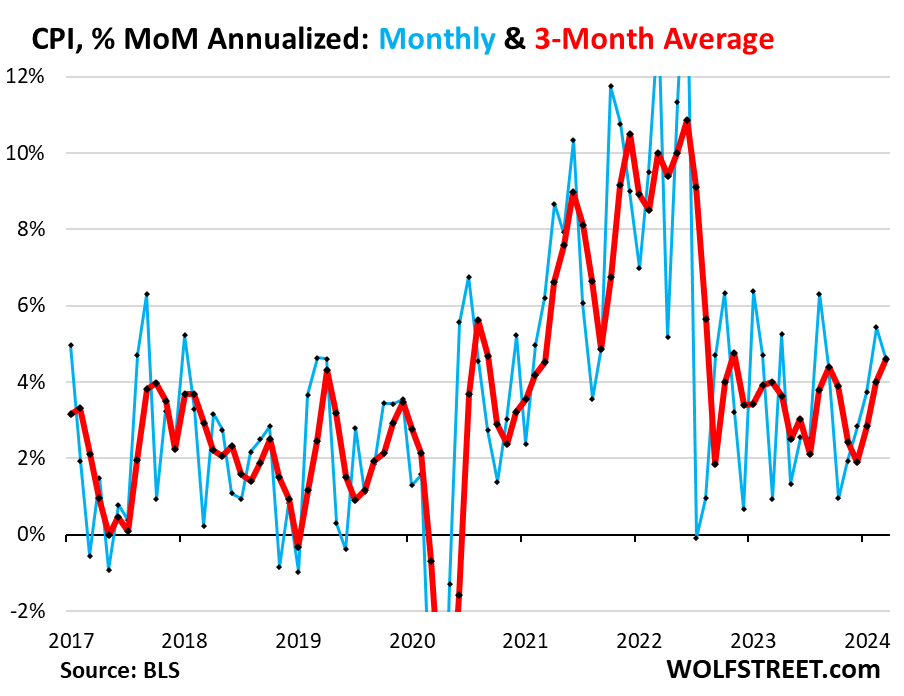

The overall CPI rose by 4.6% annualized in March from February (blue in the chart). The three-month reading, which irons out some of the month-to-month squiggles, also rose by 4.6% annualized, the worst increase since November 2022, and the third month of acceleration in a row (red).

Inflation in Services.

“Supercore CPI” is red hot. The “supercore services CPI — “core services” without housing — jumped by 7.5% annualized in March from February, same red-hot increase as in the prior month, on top of the 11.6% spike in January. So it’s not just housing that drives services inflation.

The six-month reading – six months to iron out the very volatile month-to-month readings – jumped by 6.4%, the highest since October 2022. This is really ugly. And we’ll get to some of the drivers in a moment:

The housing components of services CPI.

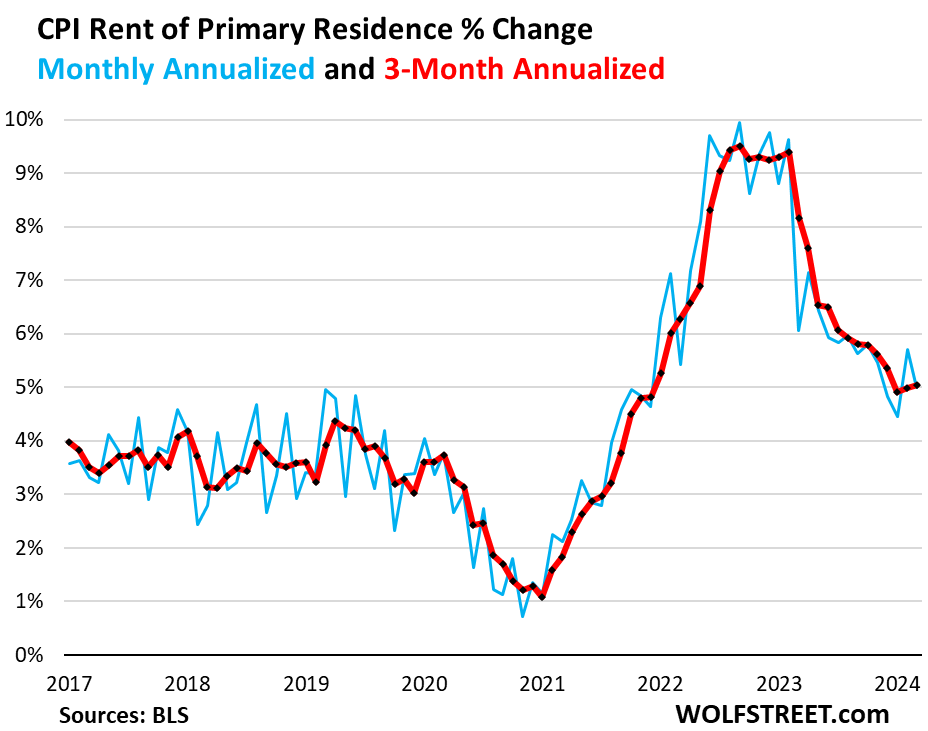

Rent of Primary Residence CPI jumped by 5.0% annualized in March from February after the 5.7% jump in February, and the 4.4% jump in January (blue).

The three-month reading edged up to 5.04%, from 4.99% in the prior month, and from 4.91% in January (red). This was the second month in a row that the three-month reading didn’t drop, something we haven’t seen since peak-rent-inflation in February 2022.

The Rent CPI accounts for 7.6% of overall CPI. It is based on rents that tenants actually paid, not on asking rents of advertised units for rent. The survey follows the same large group of rental houses and apartments over time and tracks the rents that the current tenants actually paid in these units.

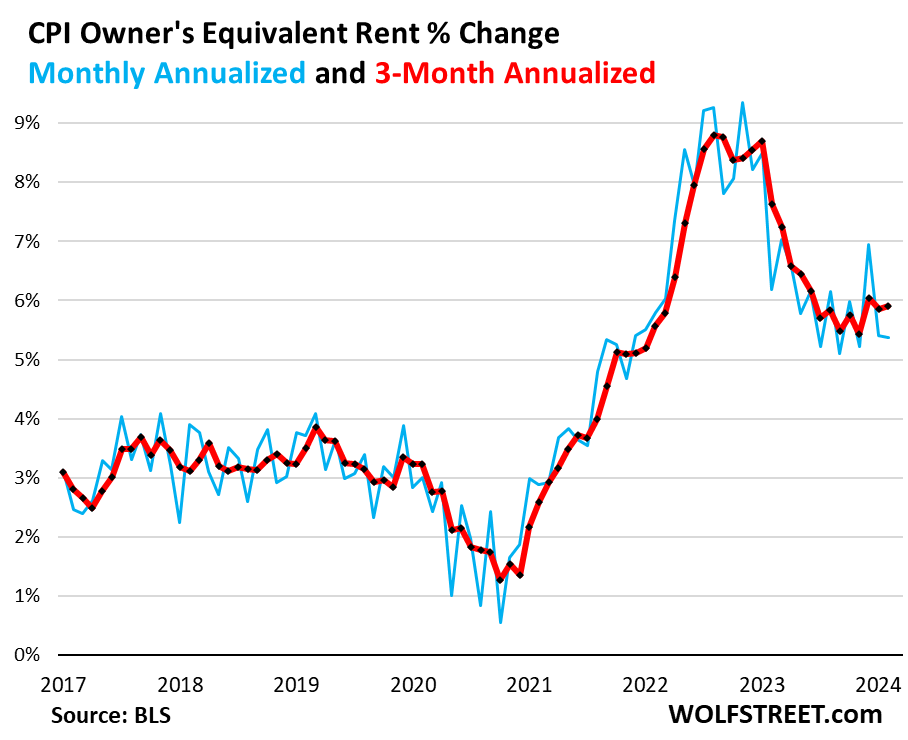

The Owners’ Equivalent of Rent CPI jumped by 5.4% annualized in March from February, roughly the same as in the prior month, after the 6.9% spike in January.

The three-month OER CPI jumped by 5.9% annualized in March from February, the third month in a row near 6%, and above the 5.5% range that had prevailed in the second half of last year. The long-awaited further cooling remains long-awaited.

The OER index accounts for 26.7% of overall CPI. It is designed to estimate inflation of “shelter” as a service for homeowners and is based on what a large group of homeowners estimates their home would rent for.

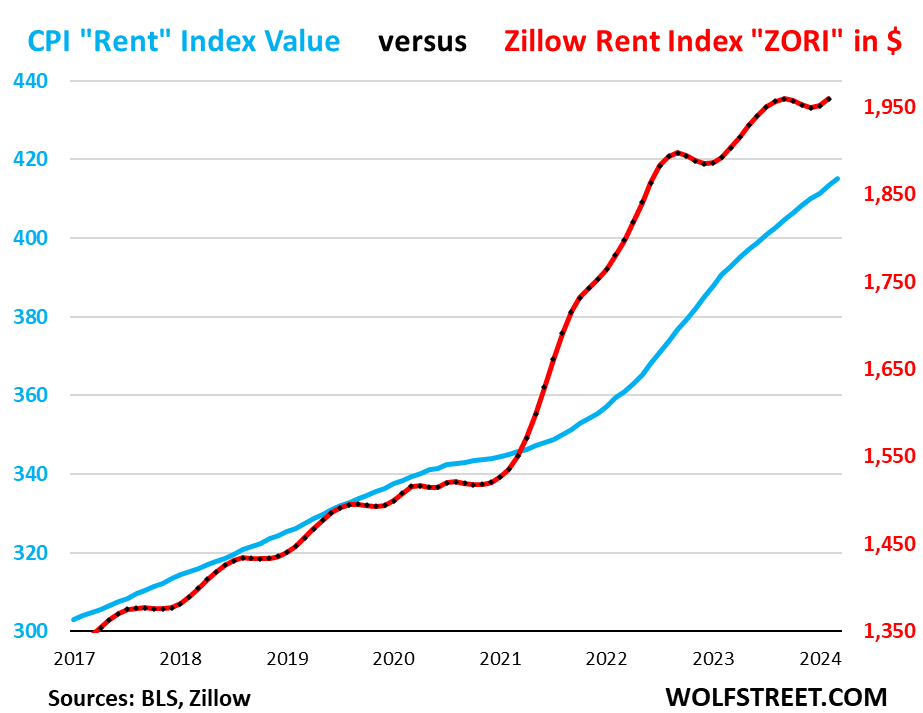

“Asking rents…” The Zillow Observed Rent Index (ZORI) and other private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market. Because rentals don’t turn over that much, the ZORI’s spike in 2021 through mid-2022 never fully translated into the CPI indices because not many people actually ended up paying those asking rents.

The chart shows the CPI Rent of Primary Residence (blue, left scale) as index value, not percentage change; and the ZORI in dollars (red, right scale). Zillow has not released the ZORI for March yet. The left and right axes are set so that they both increase each by 50% from January 2017, with the ZORI up by 48% and the CPI Rent up by 37% over the period.

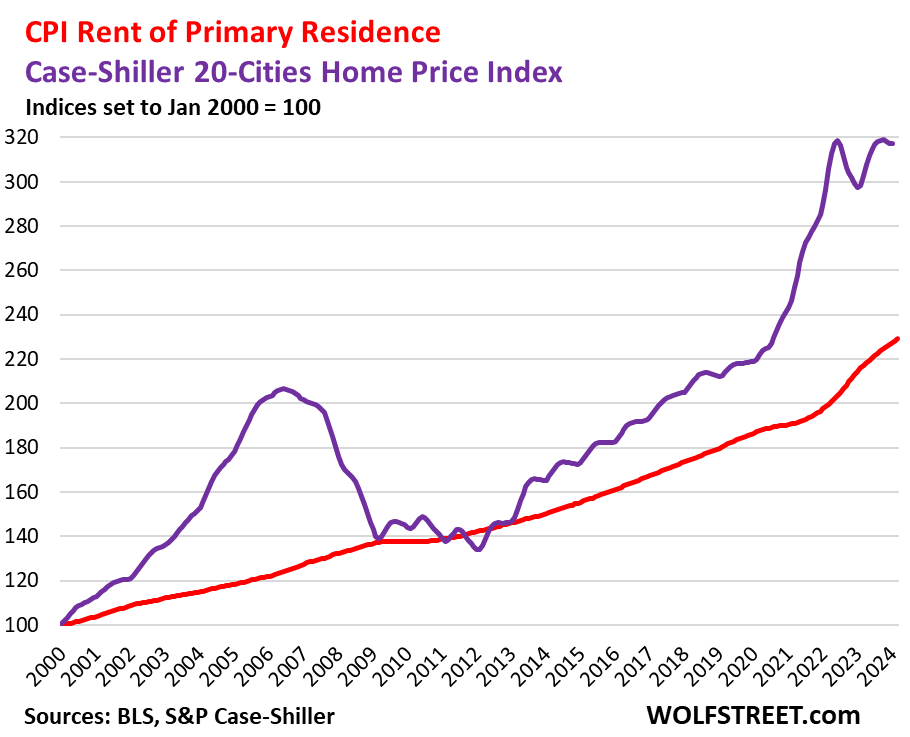

Rent inflation vs. home-price inflation: The red line in the chart below represents the CPI for Rent of Primary Residence (tracking actual rents) as index value, not percentage change. The purple line represents the Case-Shiller 20-Cities Home Price Index (see our “Most Splendid Housing Bubbles in America”). Both indexes are set to 100 for January 2000:

| Major Core Services ex. Energy Services | Weight in CPI | MoM | YoY |

| Major core services | 59% | 0.5% | 5.4% |

| Owner’s equivalent of rent | 26.7% | 0.4% | 5.9% |

| Rent of primary residence | 7.6% | 0.4% | 5.7% |

| Medical care services & insurance | 6.5% | 0.6% | 2.1% |

| Education and communication services | 5.0% | 0.2% | 1.4% |

| Motor vehicle insurance | 2.9% | 2.6% | 22.2% |

| Admission, movies, concerts, sports events, club memberships | 1.9% | -0.8% | 4.4% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.5% | 0.8% | 5.4% |

| Motor vehicle maintenance & repair | 1.2% | 1.7% | 8.2% |

| Water, sewer, trash collection services | 1.1% | 0.3% | 5.3% |

| Video and audio services, cable, streaming | 0.9% | 1.0% | 4.4% |

| Lodging away from home, incl Hotels, motels | 1.4% | 0.1% | -1.9% |

| Pet services, including veterinary | 0.4% | 1.9% | 7.3% |

| Public transportation (airline fares, etc.) | 1.1% | -1.0% | -5.6% |

| Tenants’ & Household insurance | 0.4% | 0.5% | 4.6% |

| Car and truck rental | 0.1% | -0.8% | -8.8% |

| Postage & delivery services | 0.1% | 0.4% | 3.5% |

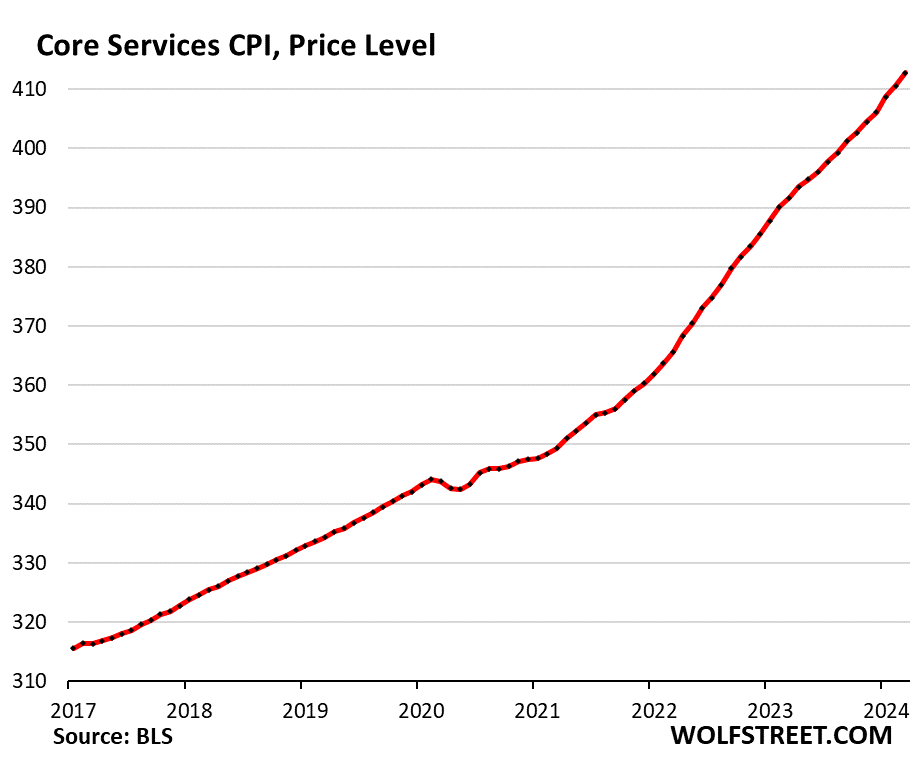

Core services price level. Since March 2020, the core services CPI has increased by 19.4%. This chart shows the core services CPI as index value, not as percentage-change of that index value. Note how the curve of price levels has become steeper in recent months.

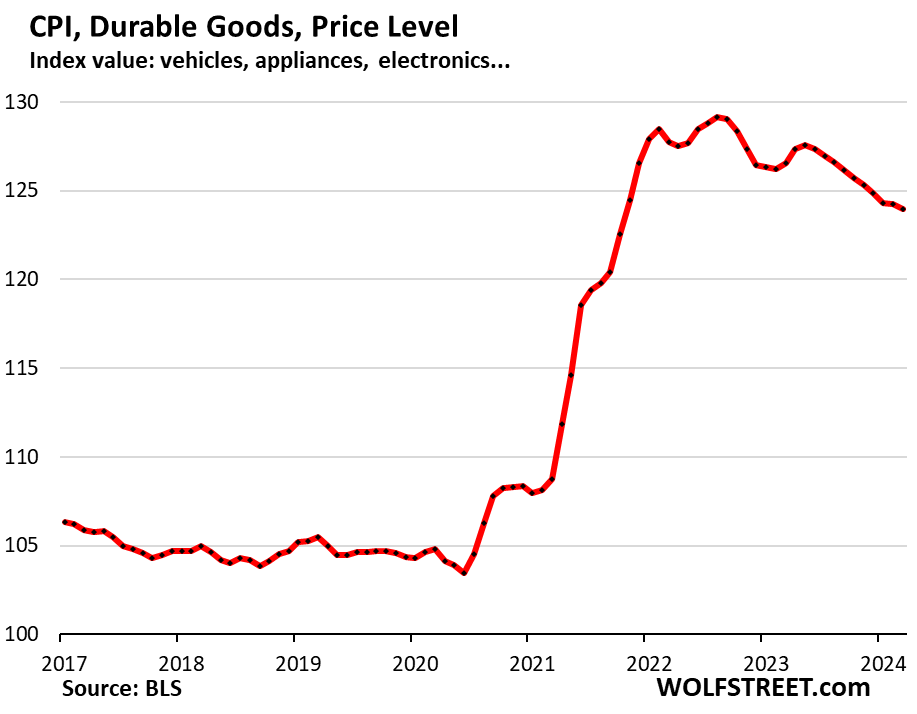

Durable goods CPI.

The durable goods CPI dipped 2.7% annualized in March from February and by 2.1% year-over-year.

New and used vehicles dominate this index, which also includes information technology products (computers, smartphones, home network equipment, etc.), appliances, furniture, fixtures, etc. And all categories experienced price declines, as durable goods prices are slowly coming down from their pandemic spike that had ended in August 2022.

From March 2020 to the peak in August 2022, durable goods prices spiked by 23.4%. Since then, they have dropped by 4.0%, having given up about 21% of the pandemic spike.

| Major durable goods categories | MoM | YoY |

| Durable goods overall | -0.2% | -2.1% |

| New vehicles | -0.2% | -0.1% |

| Used vehicles | -1.1% | -2.2% |

| Information technology (computers, smartphones, etc.) | -1.2% | -6.6% |

| Sporting goods (bicycles, equipment, etc.) | -1.0% | -2.2% |

| Household furnishings (furniture, appliances, floor coverings, tools) | -0.1% | -2.7% |

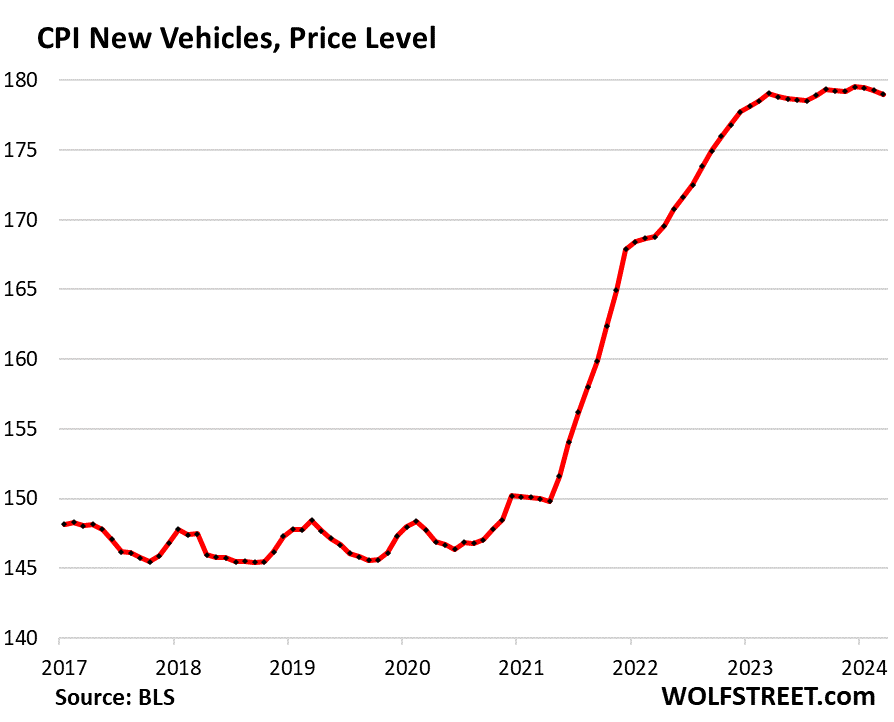

New vehicles CPI edged down for the third month in a row, after the 20% price spike in 2021 and 2022. But since March 2023, the index is essentially unchanged. New vehicle prices, unlike used vehicle prices, have turned out to be very sticky.

In the years before the pandemic, the new vehicle CPI was also meandering along a flat line, though vehicles were getting more expensive. This is the effect of “hedonic quality adjustments” applied to the CPIs for new and used vehicles and other products (detailed explanation of hedonic quality adjustments in the CPI).

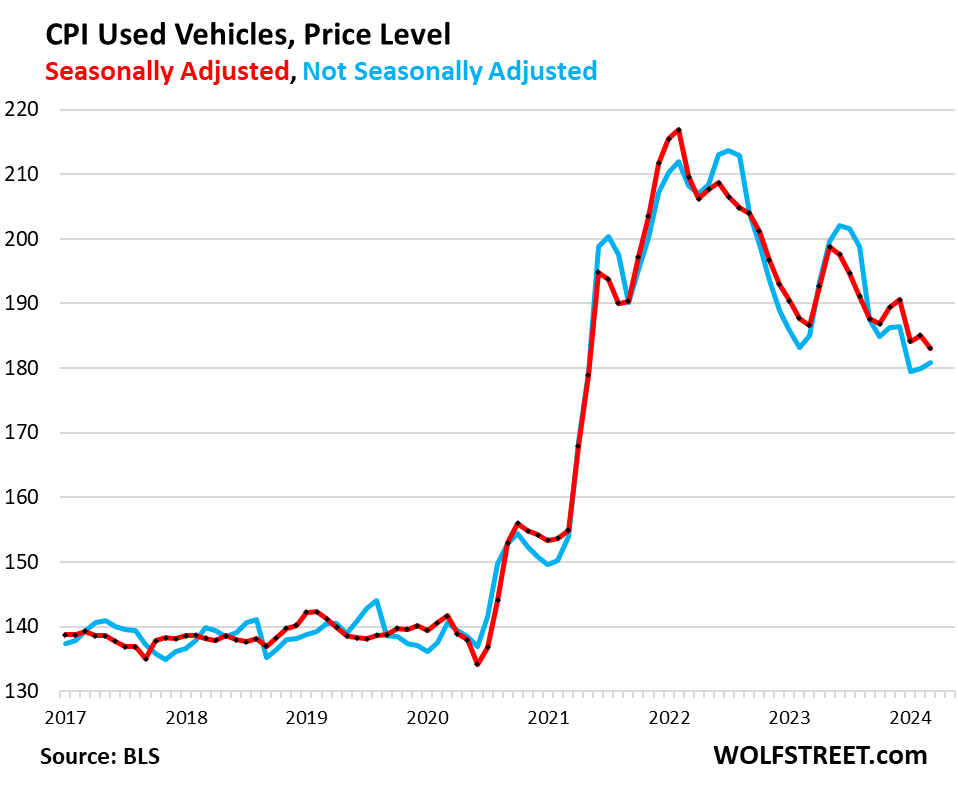

Used vehicle CPI fell by 1.1% seasonally adjusted in March from February (red); not seasonally adjusted, it rose by 0.5% (blue). March is tax refund season when people use their tax refunds for down-payments, and business perks up, and profits are easier, and prices nearly always rise in March from February. But this March, they rose less than normal.

Used vehicle CPI had spiked by 53% from February 2020 through January 2022. From that peak, it has dropped by 15.1% (seasonally adjusted), having given up 43% of its pandemic spike.

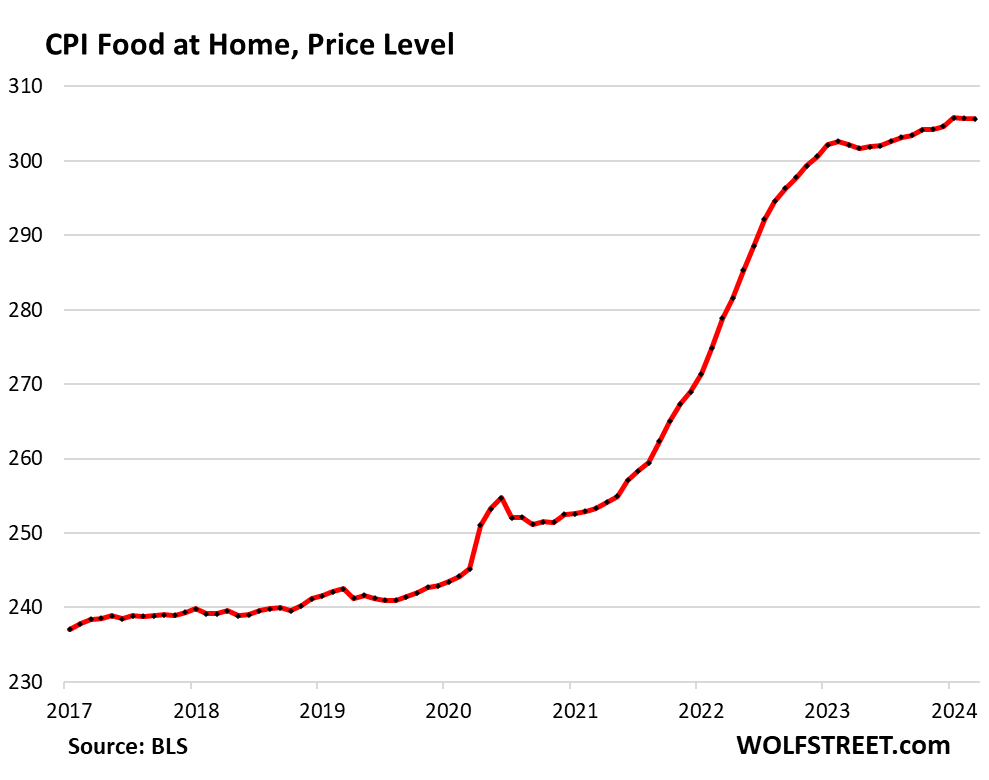

Food Inflation.

Food at home CPI – purchased at stores and markets and eaten off premises – was unchanged in March for the second month in a row, and was up 1.2% from a year ago. But after the pandemic spike, the index is still up 25% from February 2020.

| Food | MoM | YoY |

| Food at home | 0.0% | 1.2% |

| Cereals, breads, bakery products | -0.9% | 0.2% |

| Beef and veal | 0.2% | 7.6% |

| Pork | 1.1% | 0.3% |

| Poultry | 1.5% | 2.1% |

| Fish and seafood | 0.3% | -2.6% |

| Eggs | 4.6% | -6.8% |

| Dairy and related products | -0.1% | -1.9% |

| Fresh fruits | 0.3% | 1.5% |

| Fresh vegetables | -0.2% | 3.0% |

| Juices and nonalcoholic drinks | 0.6% | 3.6% |

| Coffee, tea, etc. | 0.3% | -2.2% |

| Fats and oils | -1.0% | 1.4% |

| Baby food & formula | 0.7% | 9.9% |

| Alcoholic beverages at home | -0.2% | 1.7% |

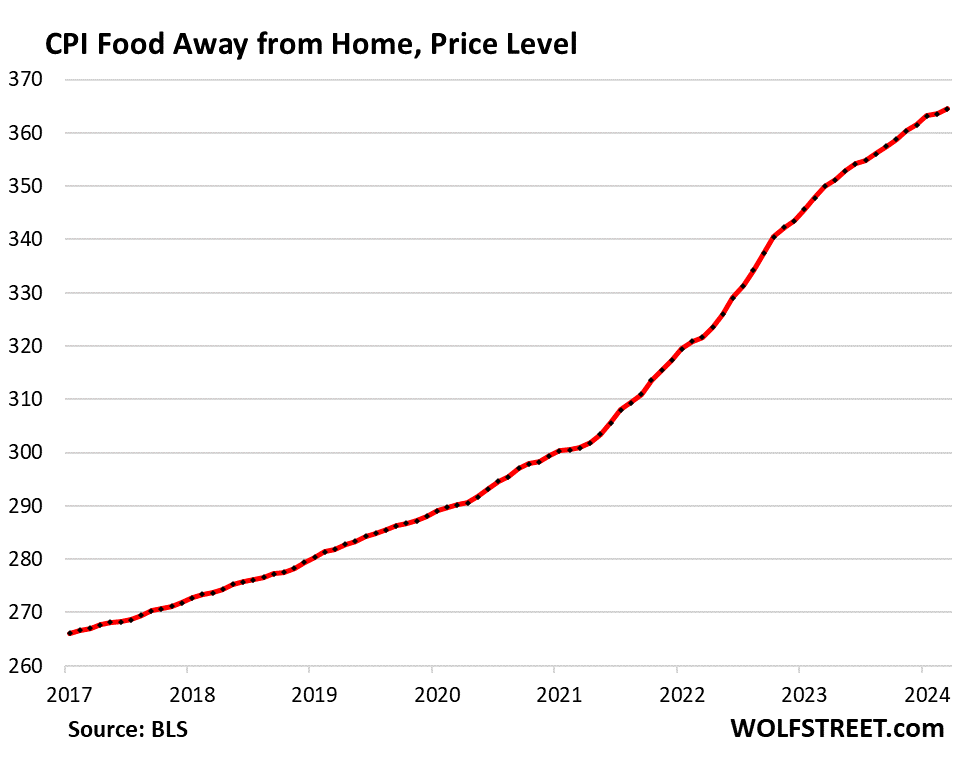

| Food away from home | 0.3% | 4.2% |

Food away from Home CPI rose by 3.2% annualized in March from February and year-over-year by 4.2%, after the massive price spikes in 2022 and 2023. Since February 2020, the index has soared by 26%.

The category includes full-service and limited-service meals and snacks served away from home, food at schools and work sites, food from vending machines and mobile vendors, etc.

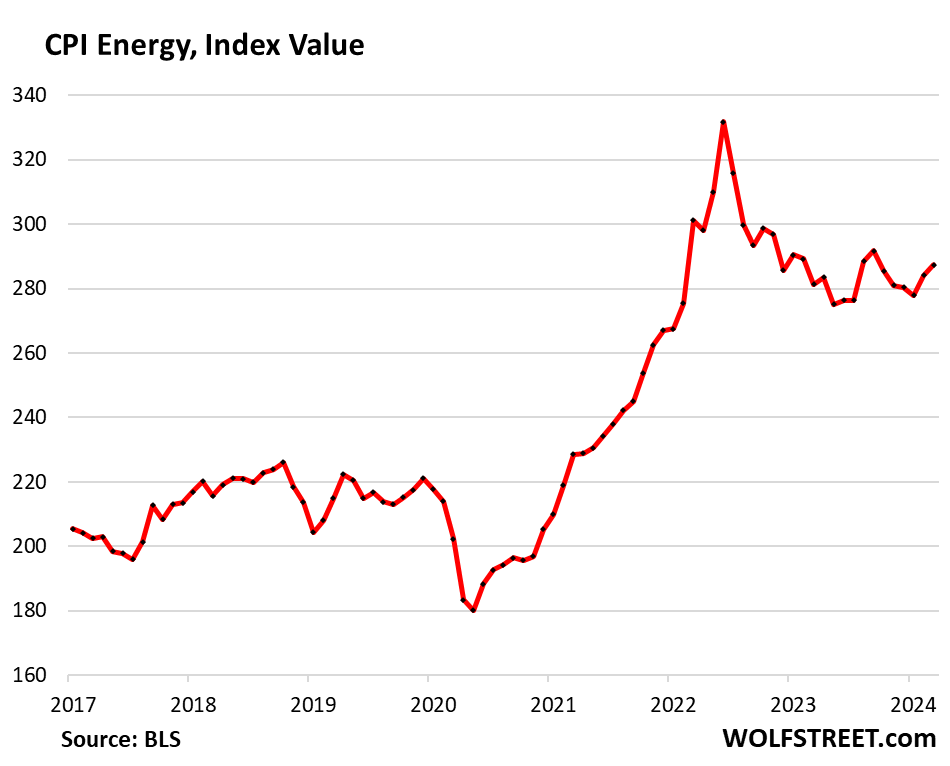

Energy.

The CPI for energy products and services that consumers buy directly rose for the second month in a row and was year-over-year for the first time since February 2023:

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | 1.1% | 2.1% |

| Gasoline | 1.7% | 1.3% |

| Electricity service | 0.9% | 5.0% |

| Utility natural gas to home | 0.0% | -3.2% |

| Heating oil, propane, kerosene, firewood | -1.1% | -3.1% |

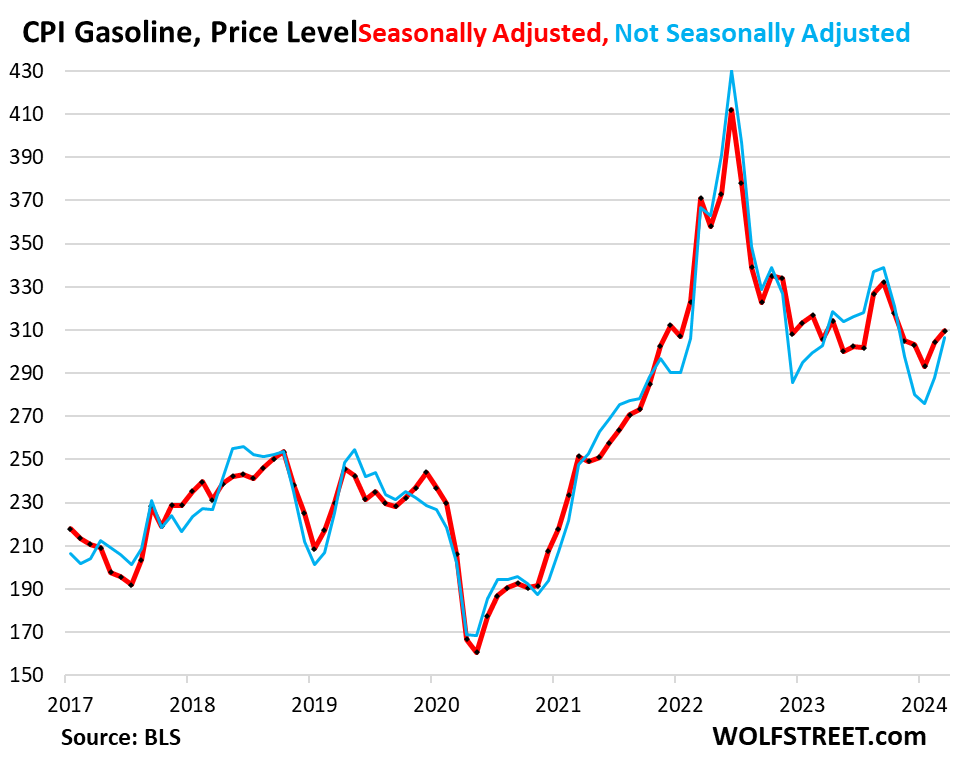

Gasoline, which accounts for about half of the energy price index, is very seasonal, with the lowest prices in December or January and the highest prices during driving-season in the summer. The chart shows the seasonally adjusted price levels (red) and the not seasonally adjusted price levels (blue), and both of them rose over the past two months:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

A dagger through the rate cut crowd who have been pumping hard for them. If anything hikes should be on the table.

Clearly the market felt this report today! It will be interesting to see how/if the rate cut crowd convinces themselves that 3 cuts are still likely this year.

CNBC is going to have to start having literal hypnotists on as guests soon…

“You are getting sleepy, very sleeeepy…there will be rate cuts soon, there will be rate cuts soooon…”

That’s because the market believed the narrative about imminent rate cuts. We have a saying in my language (Swedish):

“Believe, that’s what you do in church.”

If the market felt this then it was quite light.

Market is on fire for last few months and then this tiny bit drop of 1% or so.

Jon, Just a tiny crack true, but pressure is building, then larger cracks, then it happens “the come apart”.

But really nothing to see from a birds perspective,they live in the moment, eat or die. They build their nests every year, lay eggs, fly over our roads and houses, with their keen eye they check “wolf street” for morsels of edibles.

Exactly. The FED should be talking about rate hikes, not cuts. Once again they are in the bag for Wall St. speculators. Jerome Powell needs to be removed from his position immediately.

How nobody over the past several months has even questioned Powell as to why he was talking about rate cuts and not hikes in the face of worsening inflation just shows how rotten the entire system is.

I can see inflation surging past the previous high levels. Meanwhile, these clowns are out talking about slowing QT. There is absolutely NO REASON to slow down QT right now. They are doing the exact opposite of what they should be doing.

In Canada, financial bloggers are hoping for rate cuts in order to pump real estate. They cut welfare for the poor so that they can buy mortgage backed securities for the property owners.

The budget coming out April 16th certainly won’t be to push home prices lower. A thirty year mortgage amortization would add about 5 percent to home prices and if the CMHC insured celling is raised to 1.25 million from one million apartments and old townhouses will be bid up to 1.25 million instead of one million in some cities.

Indeed. Should have never talked about rate cut. The same as inflation is transitory. And when market became delusional, they never pushed back. They totally failed their job.

Oh they “pushed back,” but their heart wasn’t in it. They knew full well what they were doing.

The Fed members should be prohibited by statute from speaking. Period. No more jawboning, no more parading people out to talk about rates, nothing.

Amen!

Oh, sure. Then you can whine that the Fed is opaque and cronies instead of transparent and cronies.

We can throw in a Inflation Reduction Act II, that should do it

Unless you, along with the rest of the cognoscenti, have the relationship precisely backwards. What if the larger Federal deficit/debt means that higher interest rates actually INCREASE inflation via the interest income channel?

That would mean Wolf’s “drunken sailors” are getting even more hammered on higher rates …

Depth charge you see the problem, but Im not sure you understand the solution. In my mind, this debt based system we live in today is the problem, as its always borrow more, extend more credit etc etc. bail out the banks, bail out the monied elite, extend fdic, keep the party going at all cost; and the only solution is to change the system as its in systemic failure. Hey it was good while it lasted, now watch as the wheels come off the cart, and the drunken sailors slowly then quickly go without. either that, or get used to continued dollar erosion.

Now im no wolf, but to keep adding debt based liquidity in one form or another in an inflationary environment is not going to end well. I know what bernanke said about this matter, but I disagree with his answer. QT is one thing, but borrowing trillions in the national debt to shell out to many different programs that are unaffordable, while inflation runs hot is another. I hope all this turns into false drivel.

I believe precious metals see these current problems and to an extent so does cryptocurrency. Not yelling ‘wolf’ here, but the feces looks to hit the rotary oscillator shortly imo.

That huge step change on the 10 year chart this morning sure was something to behold. Don’t see a 15 bp change like that every day.

Related, the jump in yields/dxy also spiked USD/JPY over 152 (close to 153 at time of writing). Any possibility the BoJ will intervene in the next couple days, and drive rates even higher (assuming they sell off treasuries)?

The awful auction at 1pm just added to the losses

Any information about the auction?

Bad tail on the offer as well as bid to cover. Very weak. Almost a 4 basis point higher rate after it posted. Which is saying something considering how badly bonds were already at that point.

It was a big slap in the face too because the last couple 10 year auctions weren’t that bad. But yields blew right thru the when issued this time.

Good to see investors finally sticking their noses up at these absurdly low rates for duration. Next up corporate HY spreads should widen.

Minutes, MM…just wondering if this affected the auction any, since you seem to have such a good grasp of all the variables that do?

Earth added another remarkably warm month to the year so far, with March 2024 ranking as the warmest March in the planet’s climate record.

Last month also continued the world’s streak of record-breaking warm months — 10 in a row — according to scientists and data from NOAA’s National Centers for Environmental Information (NCEI).

Don’t mind me, I’m just one of those Econ-challenged fools who just doesn’t realize a massive comprehensive GREEN NEW DEAL just doesn’t “pencil out”.

Good luck getting wealthier.

“We here have been disconcerted here since late last year…”

I am not sure if you wanted two “heres” in here, even though they rhyme with year and remind us of Dr. Seuss of yesteryear.

Good, raise them rates. I like to see even better return on my T-bill. Will that happen? Unlikely and best we can hope for is no rate cut this year and magically somehow this inflation will go down and stay down on its own…sounds like a lot of wishful thinking of FED’s part but who knows, stranger things have happened a lot in the last 3 years…

and for those homeowners that bough at sky high price and rates because you listen to your genius RE agents telling you rates will go down soon and you can refinance…hope you all have plenty of funds to last until that rate cuts, might be a little bit longer than you think..

This environment of sky high home pricing can’t last forever. Sooner or later immigration rates will return to normal levels, construction will catch up to housing demand, and the pendulum will swing back toward sanity. Until then, we can only screw up our fists and damn our political “leaders” for bringing this mess upon our heads …

You wish…

Or everything else inflates and makes housing seem less high

Not going to happen. Dropping the price of assets would hurt the bank who have loans out to cover at the inflated (or now current) prices. They can’t write off the amounts a drop in housing costs would entail. It’s much more viable to devalue the dollar and pay the debt in those.

Just look at what pain the Commercial sector collapse is causing. Housing would be much worse and require to print even more to cover Fanny Mae and Fanny Mac.

This just in:

A.I. can’t solve our problems, your car driving you around is useless and anticipating the future just makes it worse.

Read history books and not Twitter. Bingo Bango

AI is the future we can talk to it until it what we want to make a picture I want to see Farrah fawcett in a pair of roller skates eating cheeseburger in 1971. It will then draw that picture and it will look something like Abraham Lincoln in a dress in 1991 when Nirvana was making never mind.

Understand they don’t want to blow up the credit market by going too high on rates then force to cut when things fall apart but by releasing those dot pot with rate cuts on the table however far in the future and based on below, sure sounds like they are in one of those situation “F around and find out moment…:

“The Fed has been in desperate search of “confidence” that inflation would continue to cool after the Amazing Cooling through mid-2023. But that search has gotten tangled up in a nasty turnaround. The cooling process had ended in August. It was hard to see in the fall of 2023. But over the past five months, it has become clear: Inflation, thought to have been vanquished, has raised its ugly head again”

If current interest rates aren’t slowing down inflation and it’s in fact increasing again, the solution is pretty simple.

Raise rates further until inflation starts dropping again.

5.5% FFR obviously isn’t high enough to get to 2.0% inflation. Besides, the whole point is to break inflation, which only happens when you BREAK THE ECONOMY and BREAK THE CONSUMER.

Or increase taxes or cut government spending…

Which is unlikely until 2025

“which is unlikely until 2025”

more like,

“which is unlikely [EVER]”

there. fixed it for ya..

The consumer isn’t the problem. It’s greedy corporations that “need” to increase profit margins, and they are doing it by raising prices instead of cutting costs. Free markets need rules to abide by, but those that only care about making as much money as possible would rather pay off politicians through PAC slush funds to get rid of those rules.

No one is forcing you to buy from these “greedy corporations”

I’ve been saying it for months – there will be no rate cuts in 2024. The Fed can’t come out and actually say this because the S&P would plummet to 3800 within a couple of weeks. So they have to keep smiling and sweating and pretending they plan to cut…”soon”.

A house nearby me just sold for 35% more than it did in 2019. And about a half mile past that the price of gas is back up to $4.49 from 3.49 in late February. Inflation is FAR from over.

Home in my neighborhood are selling more than 80%plus from 2019 price.

You are lucky in that respect!

Biden literally said inflation report ‘may delay’ expected interest rate cut by a month.

LOL. He didn’t say from which month to which month? From January 2029 to March 2029?

Thank you for making this content it’s approachable and informative

How about ‘ole blue bags’ when Powell took baby steps to raise rates six years ago. That was just after pushing through his tax cut for the rich. Ole blue bags called Powell ‘worse than Xi’.

‘old / ole’

nice to see agreement on something..

there should be an upper age limit on the presidency, all the top cabinet positions, the joint chiefs, the whole of congress, the supreme court, and all major agency heads AT MINIMUM.

Yes, it is coming out what Powell & Gang think of the mean tweeter & those who lean right.

in August of ’22 Jerome Powell: there will be “pain” fighting inflation

in Feb ’24, on 60 Minutes: “I was being honest in saying that we thought there would be pain,” Mr. Powell said in the interview aired Sunday. “And we thought that the pain would likely come, as it has in so many past cycles, in the form of higher unemployment. That hasn’t happened.”

No pain, huh? So we have painless inflation, right? It’s a miracle. Only in Washington DC.

I think when he said pain, he meant for himself and his elite class, 1%, .0001%…etc. For non asset/property owning middle to lower class, pain started long time ago and still there…

but gaslighting is free and they got plenty of that to go around, no inflation on gaslight for sure.

I was being honest in saying that we thought there would be pain…I just wasn’t being honest in saying that we would fight inflation.

Sigh. Our mandatory yearly rent increase letter is due any week now. Inflation is heating back up. Goodbye, pay raise.

Just bought ice cream – the half gallons are no more. Now 1.5 QT for $4.99 “on sale”. Bidenflation/shrinkflation.

How the hell you blaming that on Biden. They decreased in size during the Bush administration. Have you been living under a rock?

You both are living under a rock. Half gallons are readily available, at least in my area. I get them for $4.99 at BJs and its real ice cream made with actual cream, not the cheap stuff that’s just frozen milk.

But ice cream is unhealthy and I’m trying to cut back.

All three of you are living under a rock. You should NEVER buy ice cream, and especially not in these large quantities, that stuff is really bad for you, LOL

Always good to see non essentials like baby food and formula leading the YoY increases in food.

And shelter. Because you don’t need to eat or sleep indoors, right? This political era will forever be known as “The Money-Printers.” These people are absolutely horrible human beings.

Companies basically setting prices in very condensed market is the case with baby food, formula, and diapers is where I see this problem rather than money printing, although that was the way they got away with it.

It is literally soulless in my opinion.

Car insurance is at least going up because of rising cost of repairs.

Most things are avoidable like beef. Sure, eat more chicken or other proteins but in certain categories companies know they got you by the cahonnies.

Agree, but it is just part of our national sport, that we WERE in the process of making a little more fair….like having boundaries, rules, and referees that actually enforced the rules, like all other sports. But Reagan era changes pretty much ended that effort completely.

So now the ever increasing number of the worst players (aka “losers”) are homeless in the streets, in jail, enslaved to various “jobs”, independent “businessmen”/contractors, addicted to drugs, dead, or soon will be any of the above.

Being in an outlier country where 40-70% believes everything is controlled by some mystical diety and they will live forever does seem to cushion the blows and also pretty much eliminates any efforts to have a better game, though.

It’s also a very lucrative game figuring out what said diety wants at a given time, and it employs millions, many quite lucratively, and oddly, one of the very few rules to our game is that it is a TOTALLY tax free job.

One of these employees proved the diety enjoys a “just war” which allows wars amongst all his followers….so the losers in our sport be engaged one of these favorite pastimes of his soon, it seems. The winners usually never participate, as they seem to prefer money to glory.

Nothing left to do but cut rates. LOL

The Federal is now likely to raise their interest rates to match the soaring yields on US Treasuries.

While we were looking dumbfounded at the left hand of rate cuts, we were slapped across the face with the right hand of inflation.

The CPI data, reflected in Real 10 year yield, continues to bring back haunting memories of 80s and 90s inflation. As mentioned above, the auction wasn’t successful…

I continue to watch my 10y real minus 3m spread barometer and can’t help but think we’re in an evolving hurricane.

Seems like for now 4% is the new 2%. They’re going to have to take more aggressive action instead of sitting on their hands and waiting if they have any hope of driving inflation back to 2% anytime soon. I get they don’t want to rock the boat too much and cause a bad recession. It’s further complicated by it being an election year.

Yes a hurricane and the eye is and has been at the T bill location. Move very slowly towards longer duration.

Of course inflation remains high. Short-term interest rates never entered restrictive territory.

When Average Joe homeowner is locked into a 3% mortgage rate for 30 years and watches his RE and stock go up $50k to $400k every year, does anybody except Powell think these homeowners give a rat’s arse about a 5.3% short rate? As long as they have jobs, they’ll spend the perceived wealth, even if it reduces their current savings rate. Note that homeowners are 65% of family units.

A 5.3% ST rate might be restrictive in the long-term, but inflation needs to be fought in the short term, or it grows stronger. If your roof is on fire, should you treat it like an emergency and call in the fire department, or should you wait for the rain you know will eventually come?

Average Joe homeowner isn’t really that rate-sensitive /because/ they locked in a low fixed rate.

Higher rates can also be stimulative in the form of increased interest income.

Post. The. Cartoon.

“There may be the possibility of possibly thinking about reducing rates later than anticipated earlier, or if not then perhaps considering a possibility of thinking about not raising rates but depending on data sets maybe not pausing too fast or it could be advantageous to wait a bit longer rather than sooner to address inflationary pressures nearer the end of the year unless conditions warrant an earlier appraisal”

Powell could say something like this, and the markets will all have good reason to tilt in in their favor.

Powell is the worst public speaker the world has ever seen.

That’s another reason we’ve been trying to talk Wolf into taking the Fed chair job, but he’s been giving us a lot of pushback on this!

Without making any comment on smarts or policy, Yellen is in another league. A ghastly accent with a lisp.

oh come on.. biden has him beat.

powell may talk counter-intuitive gibberish in an opaque and ham-fisted way, but his sentences are complete and dont contain forgetful substitutions/mismatches of places/things/people..

MW: US Treasury yields jump by most since 2022-2023 after hotter-than-expected CPI inflation report

As mentioned yesterday, inflation can be a real beeeatch to stamp out once it becomes embedded in the system which you are seeing now, especially with services. I really don’t see how the Fed is going to get a handle on inflation without being more aggressive and ultimately pushing the US into a recession, driving up unemployment rates. Back in the 1980’s, Volcker battled through an ugly inflationary period, driving interest rates through the roof to 18+%, resulting in two recessionary periods I believe.

The Fed, like the markets, seem to think that inflation can be stamped out by simply driving interest rates higher. The problem with this thinking is that forces on the other side of the equation are offsetting their efforts including a solid jobs market, aggressive fiscal policy (with annual deficits over $2 trillion), and a boomer wealth effect that I’m not sure is being properly accounted for (i.e., either boomers retiring and spending money or dying and transferring wealth to new spenders). I’m sure other factors are present but the bottom line is a more coordinated effort between fiscal and monetary policy will be needed to get inflation under control.

BTW, what really needs to happen is that the yield curve needs to normalize, moving away from rate cut expectations into a normal upward sloping yield curve you would usually see in a growing economy. ST rates of 5.5% to 6.0% seem reasonable, but where the action needs to be is in the belly of the curve and at the long end as 2 to 5 year rates should be at least 1% above these (6.5% range) and long-term rates another 1% higher (7.5% range). Will these rates be painful for borrowers and businesses, absolutely but in the end, inflation is sending a very clear message to the Fed. You’re job isn’t even close to being completed as higher rates for longer will be needed to cool the economy and jolt the federal government into realizing they can’t continue to spend at these clips!

“BTW, what really needs to happen is that the yield curve needs to normalize,”

Yes. What really needs to happen is that the Fat Lady sings: Higher for Longer Inflation & Interest Rates Not Over Until the Fat Lady Sings? Waiting for the 2-Year Treasury Yield to Overshoot

Four decades of history say it’s not over until the 2-year yield overshoots the EFFR. It has undershot for a year, and inflation is taking off again.

And the 2 year won’t overshoot while the Federal Open Mouth Committee members keep talking up rate cuts

“BTW, what really needs to happen is that the yield curve needs to normalize”

I think this is on point. The long end of the curve suggests that investors believe that yield curve normalization will happen by lowering short term rates. Investors need to believe higher rates are here for longer and push the long end of the curve up. 5.5% short term rates are historically normal.

Hey Mr. Powell, are you still prognosing three cuts this year? You sounded very confident at the last meeting that you are on the right path for that. Let’s see who of those experts will realize this inflation won’t be brought under control without a recession.

Looks like QT will slow down.

“ FOMC says “majority of survey participants now expecting the [tapering of QT] to start around midyear.”

Why ?

We have for months discussed this here. All you have to do is read it:

https://wolfstreet.com/2024/03/02/fed-discusses-balance-sheet-normalization-on-rrps-mbs-to-go-to-zero-reserves-drop-a-lot-srf-to-prevent-accidents-future-qe-without-increasing-the-balance-shee/

https://wolfstreet.com/2024/02/22/the-fed-wants-to-drive-qt-as-far-as-possible-without-blowing-stuff-up-and-its-working-on-a-plan-fomc-minutes/

https://wolfstreet.com/2024/03/20/what-powell-said-about-slowing-the-pace-of-qt-by-going-slower-you-can-get-farther/

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

I don’t see the gold bugs here crowing about their precious rocks. It’s supposed to be an inflation hedge they said.

It’s an inert shiny rock that doesn’t pay dividends and has limited industrial use. It was purely speculation that drove the gold rally over the past 2 weeks, not fundamentals.

The central banks say it’s now a tier one asset and are accumulating the shiny rock for some reason.

So your household operates the same way as Central Banks and you should imitate them? That’s as stupid as imitating Kramer or Buffet or Dimon or one of the two “bond kings”.

Remember the what was probably the most honest thing Buffet ever said, “The first billion is the hardest”.

Just saying your agenda and actual future is likely different.

I’m not a gold bug but I own a broad collection of precious and industrial metals as well as energy stocks and if you dare to walk the walk, go ahead and short – you ain’t seen nothing yet. Commodities of all types are rallying hard and aren’t going to stop until the Fed grows a pair and hikes. And Congress will have to control spending ultimately.

Gold will easily hit 2500, beyond that who knows.

In 2001 the yearly low in AU price was $270. Closed today at $2350, about 10 times higher.

I won’t predict where its going but you better pray the dollar stays strong.

The Bitcoin guys say the same thing, LOL.

Id rather be a gold bug than a dollar bug rite now!

Goldman’s analysts better go back to the drawing board and reassess their grossly premature rate cut expectations 🤣😂

They won’t reassess anything because their job isn’t “to be right”.

It’s to look smart enough to fool us into doing what they want us to do.

Economists haven’t been right about anything important for decades, in fact they are famous for being horribly wrong when it matters the most to people (2007 “subprime is contained”, 2021 “inflation is transitory”…) and yet somehow they have a lot of authority. Don’t give them more than they earn.

4.5% inflation is going to feel like”the good old days.”

Wolf,

If we have a full scale war in the Middle East and oil prices blow out, what do you think the Fed will do?

Wait and see, or hike?

The U.S. is the world’s largest oil producer. The Middle East, which is always in perpetual conflict, shouldn’t impact oil prices to the extent it has. But American oil companies are more cautious about overexpanding than they were in previous oil bull cycles.

In 2022-23, Biden was able to lower oil prices by releasing supplies from the strategic oil reserve. But the reserve has now fallen a lot, and it seems like he’s not comfortable doing the same this year.

Bond Vigilante Wannabe,

No. But you’ve been violating commenting guideline #13, No Warmongering. And you keep doing it. And I keep deleting this BS.

https://wolfstreet.com/2022/08/27/updated-guidelines-for-commenting-on-wolf-street/

Americans love wars, they’re so fascinating and so entertaining, livestreamed into their living rooms and smartphones, with all these special effects. The more wars, the more entertainment. People have been warmongering here with gusto since the first day I opened the comments. And I throw them out when they do. Not here.

Thank you, Wolf. That sort of behaviour is disgraceful.

The only thing that I could add is a different interpretation to your observation that Americans love wars.

I suggest it is the majority of Americans who never fought a war that insist we go to war. Men that have been to war have told me it was bad, not the kind of thing that one wants too engage in as an outlet.

Oil is a global commodity. Shortages anywhere produces price increases everywhere except where the Govt owns and controls production and pricing. I’m pretty sure the Majors will get the best price possible for their shareholders and exec. bonus packages.

Well there is a type of oil the us produces and there is a type of oil other countries produce.

I would think the prices of certain types of oil would be affected. Maybe someone can color in some details though.

BVW,

I think that Powell will call and emergency press conference on a Saturday afternoon, walk in smoking a cigar in one hand with Paul Volcker’s book in the other, with a very serious face, and move up to the podium.

Then he will say “Inflation has entered dangerous territory, which requires us to take bold and decisive action– we are instituting an emergency 100 basis point hike, and will continue hiking and speeding up QT until inflation gets down to our 2% target. Nothing, and no one, will get in our way, because if inflation is allowed to burn hot, we will lose reserve currency status. If we fail in our inflation fight, all is lost.”

Then, everyone on this site will be very happy.

THE END

Volcker certainly made a lot of people rich with the spread between the Fed funds rate and the inflation rate.

Tulip: From your two lips to the Fed’s ear.

Meanwhile, calling all you bond vigilantes…your nation beckons!

When you say that every single person on this site will celebrate a specific event, conjured up in a mind incapable of incorporating the facts.

Actually I bet that most of the people are trapped in one side or the other low income versus high income. “And never the train shall meet.”

Would that this could be so!

A rate hike will not solve the war in the Middle East. A rate hike will not stop increased entitlement spending. The FED is doing the best they can with the tools that they have.

Bond Vigilante Wannabe,

No. But I just shortened your runway. You’ve been violating commenting guideline #13, No Warmongering. And you keep doing it. And I keep deleting this effing braindead shit.

https://wolfstreet.com/2022/08/27/updated-guidelines-for-commenting-on-wolf-street/

Americans love wars, they’re so fascinating and so entertaining, livestreamed into their living rooms and smartphones, with all these special effects. People have been warmongering here with gusto since the first day I opened the comments. And I throw them out when they do. Not here.

Thank you Wolf,

I participated in one of those of which you speak. Friends listed on the wall are a reminder what it was truly like and I can’t forget.

And no I don’t need any help. Time cures all ills!

It’s certainly possible all the late-2023 rate cut talk from Federal Reserve communications reignited some animal spirits in the economy.

This is why they shouldn’t have talked about it. When the time is right to ease, it’ll be obvious to everyone. The modern Federal Reserve has an overcommunication problem: it’s better to just STFU, stick to data-dependence, and stay humble & nimble.

It absolutely did! Look at the market reactions after the December meeting when they projected 3 rate cuts. They are either as dumb as they seem or they know exactly what they’re doing who knows🤷

Seems like oil will keep CPI hot next month also.

Markets hanging by a thread named nvidia (up 2 percent today lol and🤢)

Next comes ppi tomorrow and maybe we can get that June cut fully priced out.

Small caps ready to break Nasdaq might hold up this entire things the for one more 🥳

There is way too much liquidity in the system and until it is drained, the speculation will continue. The FED has concocted a speculative mania Everything Bubble which rages, unchecked, and they do not want to pop it. They REFUSE.

Yeah I’m thinking even if we do break tomorrow we’ll get another ramp up before it really tops out…. Unless these budget deficits actually turn into a mainstream issue

Another 300 billion in the hole from just last month lol

This. Economic cycles are driven by liquidity. Economists have been scratching their heads wondering why 5.5%, a federal funds rate that looks high on paper, isn’t doing much to slow the economy & inflation. The Federal Reserve’s balance sheet operations are ensuring there’s plenty of liquidity sloshing around in the financial system.

Yes. Pump Trillions into the economy and scratch your head about why there is inflation. Morons.

US CPI increased by 73% from 1913 – 1929; or 3.5% annually on the gold standard. In 1919 CPI inflation ran 23%. In 1920 – 21 everything crashed.

As originally designed, the Fed Res Dollar was given a half life of 21 yrs. – that is one human generation. This is a rate of 3.25% annually.

The Feds current 2% fantasy would represent a half life of 34 yrs.

We do live a bit longer now I suppose.

The dollar is a currency, not an asset. You don’t own dollars, you own assets denominated in a currency, such as the dollar.

yes a little like a measuring tape but the distances from inch to inch keep getting smaller and smaller so you never know how long your 2×4 is

Yes, that’s the problem, you nailed it, so to speak.

your 2×4 is now 1.5×3.5 for real but like you say the ruler shrank.

Dollars are cash, and cash is a liquid / tangible asset (under GAAP, IFRS and any other financial construct known to man).

BS. The bank notes in your pocket are “Federal Reserve Notes,” and an asset for you and a liability for the Fed, which is why the Fed calls them “notes.” The cash in your bank account is money that the bank owes you, it’s an asset for you and a liability for the bank. “Cash” is an asset of some form for the holder (such as deposits, T-bills, bank notes, etc.) that is a liability for the issuers (they borrowed this money from you). There are no “dollars” just like there are no “miles” or “gallons.” They’re measurements in which something is denominated. There are assets and liabilities denominated in dollars – or any other currency.

Silly and rather pointless semantics. Cash is an asset class, and the US Dollar is a type of cash. If you don’t believe me, pull out your wallet.

;)

READ what it says on the dollar in your wallet at the top right above the face: “Federal Reserve Note” — it means that you lent the Fed $1 interest free, and the Fed gave you this “note” in return. This piece of paper (the “note”) is an asset for you worth $1, and it’s a liability for the Fed of $1.

The concept of a currency and how it used to denominate assets and liabilities (but also labor and other economic factors) is not “semantics.” It’s THE single biggest most fundamental concept in finance and economics. And if you don’t understand it, you don’t understand shit.

Energy and housing are putting the spin on this. It is axiomatic that an overheated economy can flame out suddenly. All the wars and proxy wars guarantee we keep pushing growth. Biden said we will cut rates this year. Hey, he’s the boss.

When is Powell going to start bringing up the Federal spending and deficit of 1.2 trillion in the 1st 6 months of the FY, which is the root cause for the current inflation? That spending level negates anything the Fed tries to do to bring down inflation. Volcker and Greenspan did so in their day. Powell has been silent.

Probably because reducing that $2.4 trillion of deficit spending sends the US into an immediate and severe recession. A lot of cars are bought, hotel rooms booked, meals eaten, and clothing purchased with the $6.5 billion the Fed Gov borrows and spends every single day.

So since it can’t be reduced it won’t be, and instead inflation will run higher and higher until *something* else changes.

I told my neighbor to expect $5 gasoline by memorial day..and maybe $6 by labor day. Just like in 2008 oil and gas went wild right before the pop.

Howdy Folks. If we are headed to double digit interest rates? Slow is the way to go……. Some of US lived through this before. Takes a long time…

Fed is an utter failure.

Short of abolishing it, new leadership is desperately needed.

Jerome Burns will go down in infamy.

Biggest QT ever (even if they slow the Treasury roll-off by half, it’s still the biggest QT ever), and 5.5% rates. We can quibble over the margins. But two years ago, no one ever thought the Fed could or would go anywhere near that far.

And the market’s Rate Cut Mania starting November 2023 has assured us that this will continue. If everything had crashed, with 3 million more people out of work, and inflation getting forced down by a collapse in demand, well then, rates would have been cut to deal with unemployment and stimulate the economy.

So why don’t you just relax a little and enjoy the 5.5% rates and QT?

Yes, Powell did that.

That’s what I tell all the working homeless when they’re getting ready to sleep in their car. “Just relax a little and enjoy those 5.5% rates, and QT.”

I was surprised last month to see a lot of homeless tents in Spokane WA. Pretty darn cold there in the winter.

Lol, good one! I heard QT is gluten free but retains that same great taste you’ve grown to know and love.

His job is not assessed by how high or low he puts rates, but whether he delivers or not price stability to the public.

He has not.

His “transitory has become persistent transitory.

FYI, electricians and plumbers are charging close $500/hour on top of $120 truck fee in SoCal. Try to call one if you fine one to show up.

Powell’s real job is to ensure the world and its pet rabbit continue to buy treasuries. As long as they do, at reasonable rates, he has done his job corre tly.

Amen. Price stability was lost 3 years ago and no one cares how much they have raised rates or how far behind they are on QT (at least a year).

Yep, I’m enjoying my 5% CD return with no risk, and I would enjoy 6% even more. J Powell, keep up the good work.

Wolf, where’s the cartoon of Powell pulling his hair out?

I would like to see one of Powell having a COW

Meanwhile, here’s what paid liar Mark Zandi is saying about today’s CPI data on Twitter/X: “Inflation continues to moderate, and the only thing keeping it from the Fed’s target is shelter costs, which will recede . . .”

Oh, what I would give to see him show up in this comment section so Wolf could give him the firm spanking he deserves for this flagrant BS. RTGDFA, Zandi!!!

🤣❤️

Zandi must think today is opposite day.

We should have something Walk of Shame OR Hall of Shame where we give awards to worst liars of Paid Media and Wall st and even Ex-FED Governors too.

James Bullard. This guy was saying we need to go to 6-7% hike to bring down inflation when he was in FOMC. This week he gave interview saying 3 cuts as baseline. Come on. In Dec 2023 if he said, I can understand thats most optimistic case and his poor forecast. But even after Hot Jan and Feb data, he said 3 cuts. What a crook?

My lawyer has increased his rate from 750 per hour to 1000. Back 15 years ago it was 250. Same lawyer and same inefficiency. I am still paying for his lunch. Contingency rates are now like 50%. So you lose two legs and it is like the lawyer lost one and you lost one except you do not have a leg to stand on. And they tell me divorce money is way up since the Dow is so high. Wives are seeing the gains and deciding to cash out…..and so the normal half of the estate that the lawyers split before settling is much larger. Inflation in services really helps the legal profession. What’s not to like?

The goal is to never, ever need a lawyer.

A life without lawyer and doctor if you can do it , is the best life!!

Life without seeing a lawyer- agreed. Life without seeing a doctor – that’s a bit too dangerous for my blood.

Even if you can’t do it anyway. A shorter happy life beats a longer miserable one.

I hope up in Canada the Bank of Canada tells the truth this month on the CPI and inflation front. The bond market doesn’t even bat an eyelash anymore. It’s like the boy who cried wolf story its getting so ridiculous.

Maybe they’ll skip an inflation report and gaslight you guys some more with your immigration numbers.

Corporate bond yields on 3 year paper up 25 bps in past few days due to inflation report

I want to commend you for your outstanding reporting on inflation the past few years Wolf. You have called this correctly the entire way. While much of the establishment financial media was not only saying it was transitory in 2021, but also declaring “mission accomplished” back in fall 2023.

And many of the same establishment types were telling people to go long bonds back when the 10 yr was at 3%, but you never fell for that. Well done.

The 60 minutes Jerome Powell interview on Feb 4th belongs right there beside the “Mission Accomplished” declaration/ Bush photo op. Nail in the coffin.

Well……if this was a surprise……I’d be understanding.

For three years and more several folks on this site have been screaming for higher rates……while the congress continues to appropriate more and more and more money.

If the goofs on this site know it…..and I include myself in the goofs…….

How can highly educated, experienced folks with huge professional staffs not know it.

The only possible answer……incompetence, crooked, political and plain stupid inhabits the eccles building.

and they continue to give speeches every day

come on let’s not overreact here. 😊

Compare the inflation charts to FRED’s deposits, all commercial banks (DPSACBW027SBOG). Apply a 4-week moving average for greater clarity.

Look at how deposits peaked in April of 2022 and then declined until April of 2023.

Then, they basically moved sideways until November, when they began climbing again.

Compare the chart of commercial bank deposits to the story Wolf told in the paragraph below and see if you can tell any difference:

“…would continue to cool after the Amazing Cooling through mid-2023. But that search has gotten tangled up in a nasty turnaround. The cooling process had ended in August. It was hard to see in the fall of 2023. But over the past five months, it has become clear…”

Modern inflation is a monetary phenomenon. As the formerly sterilized cash moves out of the ONRR storage tank and into the economy to buy Treasuries (or whatever), they are converted into deposits.

And then they begin multiplying through the fractional reserve banking system, turning into more and more deposits.

It was the contraction of commercial banking deposits that cooled inflation. And now, they are growing again.

Buckle up.

Deposits track the reserves (cash that banks put on deposit at the Fed), and they’re both a function of QT (now $1.5 trillion). Reserves (and deposits) are also a function of ON RRPs as funds shift between bank deposits and money market funds. The last 12 months of QT came out of ON RRPs, rather than reserves (deposits), which actually rose since March 2023, as ON RRPs fell by nearly $2 trillion. When ON RRPs drop to near-zero in a few months as a result of QT, then reserves (and deposits) will begin to decline again.

Any similarity of the curves between reserves (and deposits) and inflation is coincidental. It’s really just a vague similarity and you have to do a lot of chart-doctoring, including offsetting the time lines to make them look similar.

Here are reserves and ON RRPs:

Re: “Note how the curve of price levels has become steeper in recent months.”

I just was looking at some random page, and it seems that you have to go back to early 90s to see a similar start to an inflationary period/level.

I don’t think there’s any reason to assume lightening will strike in exactly the same way today, but while a hurricane is cycling through a season, chances are extremely high that lightning will be part of a storm cell.

Our innovative pre-AI economy is still processing and adapting to the pandemic shock — and synthetic resilience. The pandemic shock has been mitigated, but in terms of big cyclical patterns, we’re still in a recovery mode, that’s being threatened by the dynamics of inflation.

I think sustained inflation forces will subdue GDP growth and impact non-AI reality.

I read today that the Russell 2000 has roughly 40 percent of its balance sheet debt in short term floating rate notes, versus the S&P with 9 percent.

It’s that type of bifurcated mismatch that’s going to separate our economy in this resurgence of inflation.

This storm will test many zombies and it looks like the horrid growing darker. Amen

To get through the last 15 years they had to print $8T, reduce interest rates from 8% to zero, increase equity p/e multiples from 15 to 25, imprison the poor with inflation, gut out the middle class, open the borders, and spark a class war.

What will they do to get through the next 15 years?

I don’t think a couple .25% interest rate decreases is going to work.

I agree. If it took all that it may be scary. I promise you tech unicorns will be more scarce. Their free cash flow comes from bloating their float not earnings. You want that or 5.5%?

If there was no election on the horizon and the bond market did not blindly follow whimsical BS dot plots, then the next rate move would not be a cut, but a hike. Tomorrow there will be some idiots who will buy 30 year bonds at artificially low rates. There is a price to be paid for stupidity.

It seems to me the last 15 (if not 60) years has been a concerted fiscal and monetary effort at the federal level to force the electorate to pay no price for stupidity: to write “free” insurance for the excesses of fools. It will be an amazing defiance of classical physics and finance if that self-levitating motion is perpetual, and not merely pooling risk for some new form of rainy day.

Wolf,

Read all the way through and didn’t see any question about

Motor vehicle insurance 2.9% 2.6% 22.2%

The 22.2% looks like a typo. 2.2%?

No resource or quotation just a sneaky suspicion as I’ve played with numbers for years and had a lot of fun.

What you think?

That’s the yoy increase. Sounds about right.

Mine was up 40% and thats after a lot of figuring.

Softtail Rider,

LOL, I wish. People here have complained for two years about their auto insurance. Lots of commenters have talked about their 20%-plus increases in their auto policies. We did too. This is real. 22% year-over-year for motor vehicle insurance CPI sounds about right. At any rate, I wish it were a typo. It’s not.

Mine hasn’t budged for 5 years, which probably means my 800 claims number has been disconnected or is no longer in service.

Staring at an M2 chart with bloodshot eyeballs after a couple of 24 ouncers. M2 increased 40% from 2020 to 2023. M2 has now decreased about 5% from its 2023 peak. Hanke (Quantity Theory of Money) is now predicting under 2% inflation by 2024 year end based on his QTM. Hmmmm…… Humble nsa doesn’t believe it either but Hanke did predict the recent 10% inflation peak. Just saying.

IMO money supply is really the whole thing. Hanke is probably right with some caveat on the timing.

We don’t have a good money supply measure. M-1 and M-2 include and exclude certain types of cash — though it might have made sense decades ago when the measures were designed. So when cash shifts from one category to another category of cash — such as cash going from several CDs of less than $100k to one CD of over 100K, then it changes M-2, though nothing really changed. Same with money market funds ON RRPs, etc. That’s why M-2 stopped falling when ON RRPs started getting drained, and part of that drain when into reserves. That’s why lots of people who understand this don’t look at M-2 anymore. It gives a faulty signal and needs to be fixed.

If inflation is a fire, Powell is using a squirt gun, while Congress pours 5 gallon cans of gas on it.

How can the economy not expand and prices not go up with $2 trillion of added fuel each year?

Wolf,

Does this count as a head fake? Do we need couple more months of these neanderthal mouth breathers saying, “Oh, it is only housing. Tame that, tame inflation.” ?

My head-fake chart is a year-over-year chart. And it takes a while for current inflation to turn around a year-over year line. Core services CPI has turned higher on a year-over-year basis, but it will take a while for it to be clear. So right now, “we’re suspecting,” as I said, that the decline in 2023 may turn out to have been a head-fake.

The narrative (the lie) must be that inflation is licked. Otherwise all hell breaks loose. If effective, real rates DO start to edge back up, it seems to me that the market is toast, and Hussman, Grantham, and value investing will be gloriously redeemed.

Standing by for over a year on this to happen🎉

Inflation is not all the FEDs fault. Almost every government in the world is printing debt. Mexico’s 2 year bond rates were 4.2 percent last now are 11.2 percent. We think a 5% increase is bad, they are getting hit with 7%.

I think they measure inflation more accurately and truthfully

Mexico inflation = 4.4%, similar to the US.

But the Bank of Mexico was trying — very successfully — to protect the peso from the Fed’s rate hikes, and it front-ran the Fed by a year with huge rate hikes eventually taking its policy rate to 11.25%. And is has now cut its rate to 11%. Brazil followed a similar strategy. And their currencies were among the few that didn’t crater when the Fed started hiking rates. Japan blew off the Fed’s rate hikes, and the yen plunged 30%. Japan can afford that, Mexico cannot.

Motor vehicle insurance 2.9% 2.6% 22.2% YOY

Thanks Warren Buffett with the mass holding of GEICO – keep the shareholders at BH happy riding the inflation train for all it’s worth.

Then why did the other insurance companies’ rates also go up?

MW: ‘Serious possibility’ that Fed’s next rate move is a hike, warns Larry Summers

He said it was maybe a 15-20% possibility, and even then things could abruptly change over the next few months, from what I heard him say.

I’ll take a synthetic market point of view that the monetarists have been given the task of how to limit inflation at a 1.96 std deviation on this monster they created.

Two percent inflation is the maximum with a meaningless mean which would include deflation. An important distinction, not as a remedy but a statistically likely hopeful event.

I was wondering how they determined the Owner’s Equivalent Rent data. I found this explanation in my search and I was surprised, to say the least; assuming this is correct.

Understanding Owners’ Equivalent Rent

Owners’ equivalent rent is a statistic that is followed by homeowners and tracked by the Bureau of Labor Statistics. The data used for calculating owners’ equivalent rent is obtained through surveys, which ask members of a household (called a consumer unit) the following question: “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished, and without utilities?”

Wolf, does it bother you that this number is determined by what homeowner’s say they would be willing to rent their home for? They are relying on responses from people without any data and most likely zero expertise to back up their responses?

Am I missing something?

Just looking at the numbers, it looks reasonable to me. OER has been one of the hottest elements of CPI for the past two years. And it tracks very closely the rent CPI, which validates it.

Homeowners have to figure their costs to determine what their house would rent for. so Interest, property taxes, insurance, maintenance, etc. It makes sense. You get enough people doing that (tens of thousands across the US), and you come up with a pretty good estimate. Homeowners are not stupid.

Wolf. Go ask 20 people who have owned their home for over a decade what it would rent for. And then ask some who have owned for over 20 years.

They have no idea what current rents are.

Lots of homeowners rent out their homes, and they can figure out just fine how much to rent it out for, it’s not that hard. It’s not rocket science. These are serious surveys, and you’re expected to spend some time with them. It’s not like you walk up to someone and ask what their house would rent for. That kind of thinking is just BS. I’ve gotten several government surveys of this type – I even wrote about one of those surveys in an article to let people know what they’re like. They’re time-consuming, you have to think about stuff and look up stuff. It’s like homework.

Monthly P/I + monthly water bill + monthly sewer bill + (annual prop tax / 12) + (annual home ins / 12).

That’s how I figure my monthly “rent” as a homeowner.

NB; in every apartment I’ve rented, water & sewer were paid by landlord, which is why I include them.

Wolf,

How come our hair-pulling dear Powell is not on the post? We sorely miss him.

If inflation continues like this, he might well be bald soon. so time to get another cartoon of Powell ready…

The likely outcome from the Fed policy has always seemed in a manner that favored the wealthy at the expense of the American family.

Pitting individual Americans against a mechanized stalker seeking to profit by claiming monetary rights to a victims identity and monetizing that claim by selling the rights for their persona too advertisers. My vision of big tech is that it sold it’s soul when it adopted civilian surveillance as their profit model.

Agreed, I’ve been in tech since the 90s and am embarrassed by what it’s become. If i had to do it over today I’d become a botanist or similar. Tech is just lame and soulless now. Nerds need to take it back.

I feel this vibe as an old tired website admin.

20 years ago I was designing and building my own computers from scratch, overclocking them, dual-booting Linux etc. etc.

2 months ago I ditched my smartphone for a flip phone, with the goal of living a more offline life.

The irony of sharing this in a comment on a website is not lost on me.

Wait until drones with sophisticated AI start stalking everyone. Raises all this an order of magnitude — to real time serfdom. Flattens out spontaneity and choices into an unhappy (and peak-times calibrated-inflated) meal menu.

Wolf,

Thank you. You have educated me so much in last few months. I am sure there are lot of people like me who never understood so many things which matter to us until we started reading your blog. My only regret, I didn’t know about long before. :)

Gratitude.

So the MSM’s “sticky inflation” story is coming unglued. Inflation has well and truly become unstuck and is accelerating higher.

Why do I feel that the Fed has put themselves in a box. I hope it is constructed of riot resistant materials. Powel put his shoe in his mouth with the whole notion of cuts, let alone three this year. There is no more lipstick for this pig. Call in the Piper for payment.

It’s no happenstance. Draining the O/N RRP injected new money and new reserves into the payment’s system.

Wolf, please break down what in the punch bowl is contributing to our “drunken sailors” inebriation and the approximate degree the each sector contributes, i.e. wage growth, (surely income growth of the bottom 20% has an outsized influence on the results of inebriation compared to a similar amount of income growth of the top 1%) interest income growth, wealth effect and so on. You have been elucidating quite precisely what our “drunken sailors” are doing but have been quite muted about what factors explain their behavior. Granted a similar degree of precision will be impossible to do with authority, nonetheless a pie chart of the punch bowel approximating it’s contents backed up with as much authoritative data as you can muster would be appreciated.

go back and look for other drunken sailor articles on the site and he explains it in great detail and several of those articles. Hope that helps!

I’m sure California’s increase of the minimum wage for fast-food workers (from $16 to $20) will have minimal effect on inflation (sarcasm).

Yesterday’s selloff sure lasted long!

Bond selloff continued today.

This has to be the roaring 20s 2.0

When .6’s, .5’s and .4s become twos and ones…

Not even Steve Liesman talks about the comps falling off. The stock market rallied on many CPI reports that were obvious “disinflationary” considering the massive prior year number rolling off. The April 2023 number is still high relative to historical, but that’s the last high monthly until August. So what happens folks when 0.1’s and 0.2’s are replaced by 0.4’s? That’s rhetorical.

The last 2% mile is going to be the hardest, the economy is strengthening and gasoline is rising. We are coming off a good year of utility rates as well… and the government deficit fuels the fire ever more.