A Bloodbath was had by all?

By Wolf Richter for WOLF STREET.

It was probably not the best timing ever for the 10-year Treasury auction to fall on the day that the CPI inflation data had given people the willies hours earlier, with its ugly core-services and supercore services CPI pushing up core CPI and overall CPI.

The $39 billion 10-year Treasury notes were sold at a yield of 4.56%. This yield was up by 21 basis points from where they traded minutes before the CPI report was released, and it was up by 50 basis points from the 10-year Treasury auction a month ago.

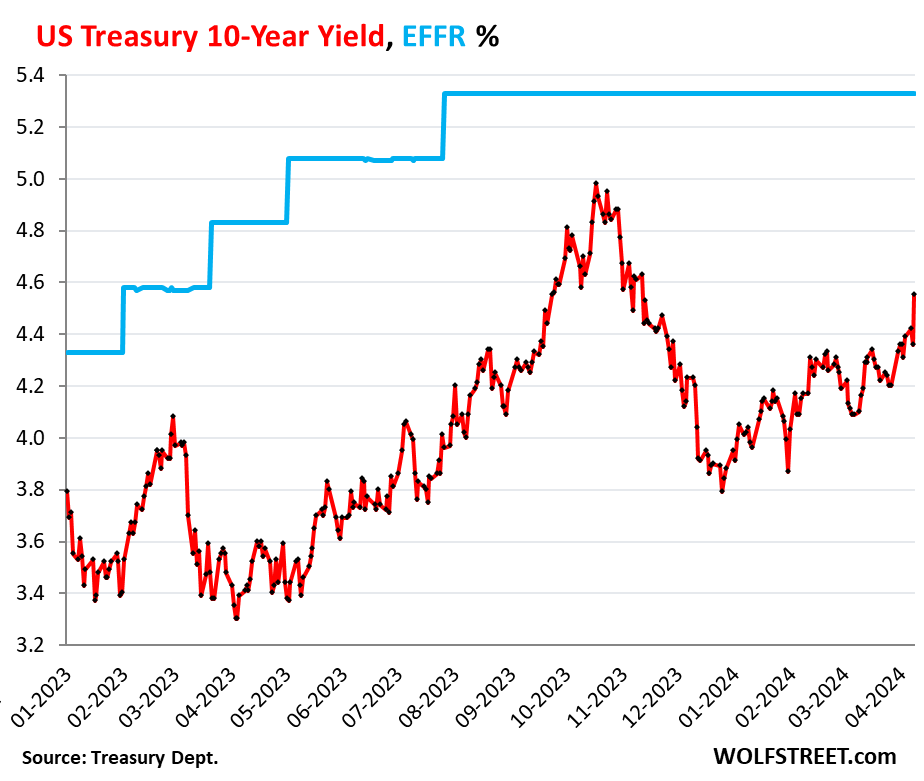

In the secondary market, the 10-year Treasury yield spiked by 19 basis points from the prior day, to 4.55%, the highest since mid-November. The blue line represents the Effective Federal Funds Rate (EFFR), currently at 5.33%, that the Fed brackets with its target range of 5.25% to 5.50%.

The difference between the 10-year yield (red) and the EFFR (blue) gives us an indication to what extent the bond market is still in denial, after it got whipped into hilarious frenzy during Rate Cut Mania late last year and into early this year.

But the 10-year yield has risen by 80 basis points since then, as folks were trying, apparently, to come to grips with reality. And it has a long way to go.

Who the heck would want a 10-year Treasury note yielding 4.56% if CPI inflation gets sticky around 5% for years to come? Apparently, lots of people — or else the yield would be a lot higher.

But they’re not seeing inflation sticky at 5% for years to come. They’re still seeing inflation in the below-3% range. So we disagree on where inflation is going. But today’s spike of the 10-year yield shows that longer-term inflation scenarios are getting tinkered with after today’s inflation data.

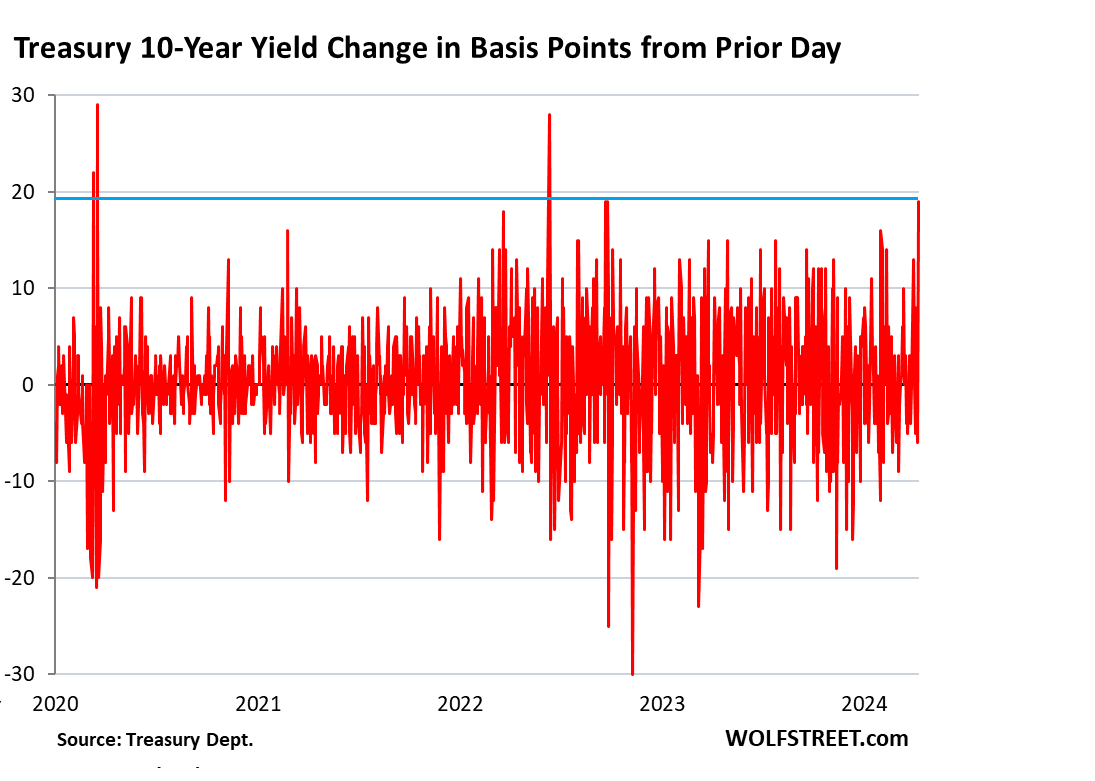

Today’s 19-basis-point jump for the 10-year yield was the biggest since September 22, 2022 (also 19 basis points), and both had been the biggest since June 2022:

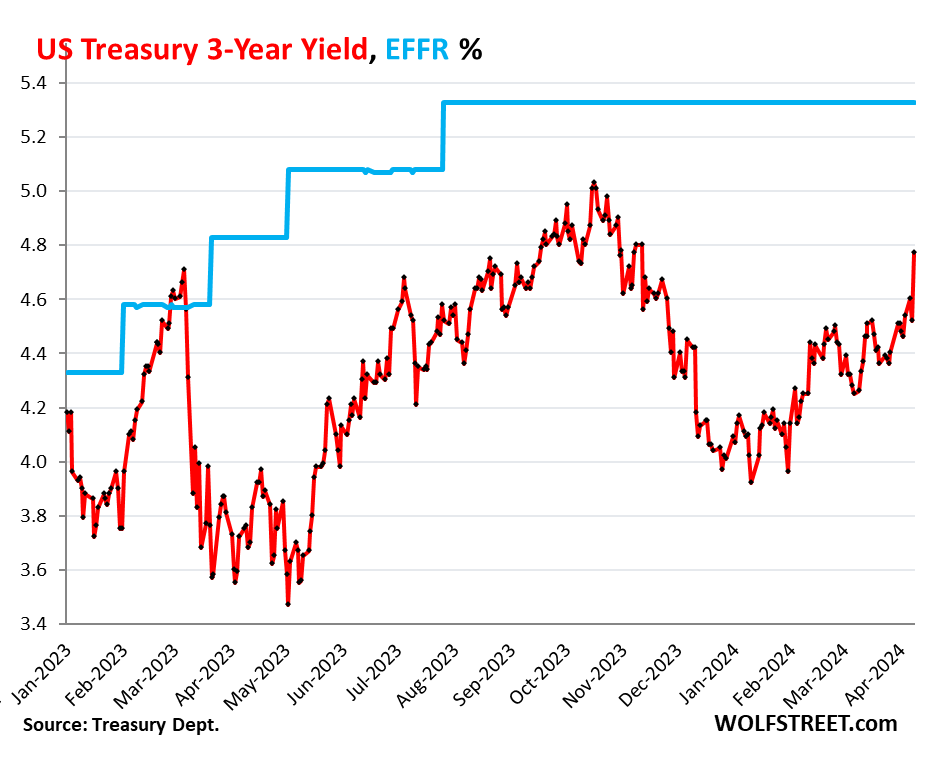

A bloodbath was had by all, but it was worse in the midrange, with the two-year yield jumping 23 basis points to nearly 5% and with the 3-year yield jumping 25 basis points to 4.77%.

- 6-month yield: +6 basis points to 5.40%

- 1-year yield: +16 basis points to 5.19%

- 2-year yield: +23 basis points to 4.97%

- 3-year yield: +25 basis points to 4.77%

- 5-year yield: +24 basis points to 4.61%

- 7-year yield: +21 basis points to 4.59%

At the auction yesterday, $57 billion of 3-year Treasury notes were sold at a yield of 4.55%.

In the secondary market today, the 3-year yield’s jump of 25 basis points was the biggest since June 2022. Today’s yield of 4.77% is just 26 basis points below the high in this cycle on October 18, 2023, of 5.03%, though inflation-denial is still driving this market, as we can see in this chart:

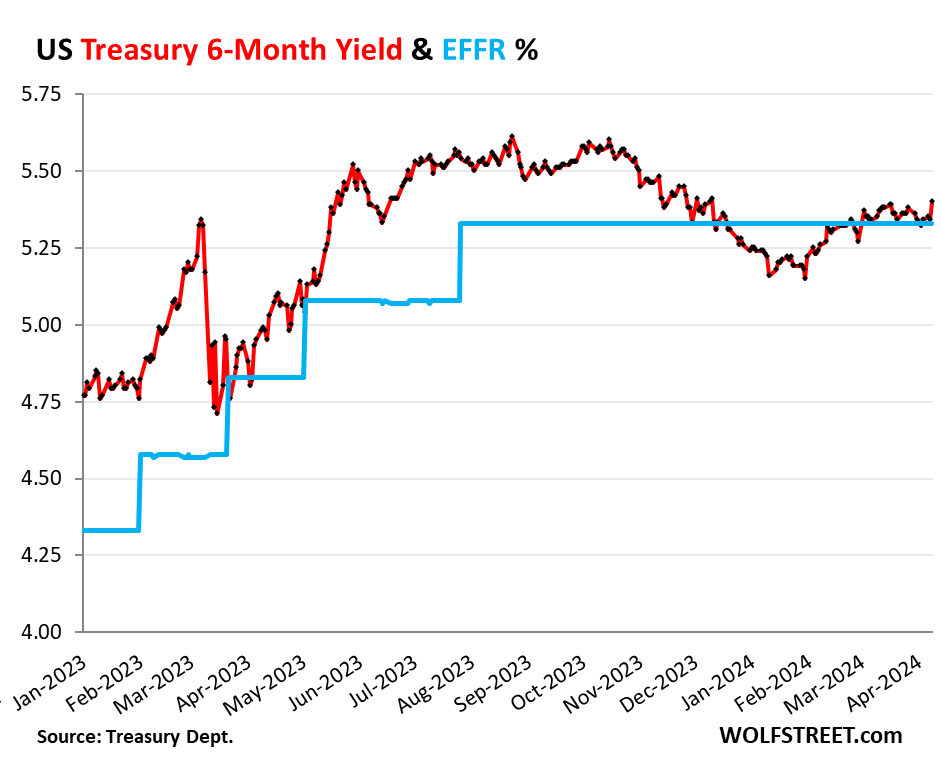

But Rate-Cut Mania is over, is what the six-month yield is telling us. The window of the six-month yield – bondholders don’t care what happens after their security matures in six months – now goes into October, and it shows that the market is in the process of walking back from rate cuts during the time frame, with the yield today rising 6 basis points to 5.40%, into the upper portion of the Fed’s target range.

Mortgage oh my. The average 30-year fixed mortgage rate spiked 28 basis points today, to 7.34%, the highest since November 20, according to the daily measure by Mortgage News Daily, which is going to cause a lot of potential buyers to turn on their heels and do more wait-and-see, while potential sellers get to reminisce about the good old times of 6% mortgage rates in 2022.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Didn’t make any sense that people were willing to buy 10-year Treasuries at 4% in January when 15-year mortgages were at 6.5%.

I think after the last 4 years it’s safe to say nothing make sense anymore..

7.34% mortgage rate doesn’t seem to curb price much after all in RE especially in SoCal, that should tell you something how insane things are and maybe stay this way forever.

In upside down world USA, JPMorgan said Fed should drop rates to reduce housing costs?!? US bankers seem desperate for rate cuts, no?

Maybe Fed will finally allow the $12 TRILLION in US market cap increase from October 2023 to deflate a few percent points versus go up another 5-10%, like seems to be the plan. Logically, would inflation be better at SP500 at 6,000 or SP500 at 4,000 due to animal spirits, no?

For the answer why bankers want rate cuts, ask yourself and try to answer the question: “when yields on new notes go up, what happens to the price of the already existing lower yielding notes? And who are holding them?”

Those lower yielding notes are now harder to sell. So if some entity must sell, it must do so at a loss.

Bankers are not concerned about mortgage holders or the prices of houses. They only care about themselves and their profit margins.

Historically banks have always wanted higher interest rates to maximize their profits on the spread between the yield on certificates of deposit and mortgages. When interest rates fall the spread narrows as does their profits.

BlackRock CEO is asking for 2 or more rate cuts for 2024 and expecting that FED would be fine with 3-4% inflation and call it a day with 3-4 % rates.

Damn these greedy Corp Execs!! These guys are out there to hollow out the working middle class at all cost.

That maybe on his wish list. But you don’t get 3-4% inflation with 3-4% rates. You’ll get 5%-plus inflation. The Fed will have to keep rates above inflation to prevent inflation from rising further.

@Phoenix_IkkiCancel,

It feels like there are two very different worlds in this country. There’s a large group of people who do what they can to cobble one or two incomes into just enough to get by. This group feels like a noose is slowly tightening around their necks.

But above that there are very high incomes decoupled from what people actually need to live. These people live the consumer-first lifestyle because they have enough income to support it and because it is part of their being and I would argue is the primary upper middle class culture in this country – which cars you drive, expensive hobbies & travel you pursue, town/schools/daycares you avail yourself of, etc.

You cannot restrict this group without serious harm to the economy as they have enough income to just keep chugging along. Their jobs would have to go away and their retirement/investments decimated with no indication that they’re coming back any time soon.

So inflation continues until there are large structural changes in the economy. When there are not shortages in key but relatively average jobs like nursing, police, teaching then we’ll know we are there. The demographics are much different but the early 70s were like this – you had to know someone or get lucky to get one of these jobs.

It’s looking like we don’t really want this to happen even if we think we want correcting in housing and affordability of every day needs. Because the top is now protected against downsides in economic slowdowns there is too much reward that has been built-in to the system with only small isolated risks. It would take a lot of contraction to revert to the historical mean and getting there could get real ugly, as in do you like your democracy? Because it may not survive that kind of depression.

LMAO, meanwhile Jim Cramer, the consummate Wall Street shill, says he believes there’s really not much inflation and stocks over reacted in the selloff.

BUY, BUY, BYE !!!!

Right, that’s the consequence of asset printing and offshoring good jobs such that the economy is bifurcated into a small number of haves and a much larger group of have nots.

So much of the spending comes from the “haves” that you can’t take from them without everything crashing down.

I think you might have the last backwards. The US might need a recession for democracy to survive.

I think you have an accurate picture of the way things are, but part of the reason for that upper income class is the enormous and still growing value of technical skills and analytical ability. The reward for people with those skills in the tech based economy is just far beyond what it was in the 50s.

INSANE indeed.

The ONLY cure for the current housing market is a recession that results in at least 6% unemployment. 7% would be better.

And, as I’ve said 25 times here on WS, my main concern is, does Congress trot out rent & mortgage relief? I’d say there’s a 90% chance they do so.

If so, it will be a long time before housing returns to the mean and becomes affordable again.

Phoenix,

“7.34% mortgage rate doesn’t seem to curb price much after all in RE especially in SoCal, that should tell you something how insane things are and maybe stay this way forever.”

Agree in general, but SFH sales *volumes* are *way* off in CA (by about 33%) and that is usually a prelude to a price collapse (at some point either investor-owners panic and try to exit first/best or natural turnover – due death/divorce/work relo – triggers the collapse).

(“First Tuesday” on the internet puts out monthly CA sales volume numbers.)

The old saying, “That which cannot go on…stops” is usually pretty true in economics.

You simply cannot have housing prices perpetually rise much, much faster than incomes because (obviously) there are fewer and fewer people who can come anywhere close to buying them.

All sorts of market distortions/transient factors (ZIRP, foreign buyers, mortgage buy-downs, gov subsidies, and on and on) can disguise this fact for a while…but incomes and home prices are the final fundamental facts.

Trust me, I hope to god you’re absolutely right on this and I am super wrong on this, looking at current environment, I just don’t have a lot of confidence….

“Agree in general, but SFH sales *volumes* are *way* off in CA (by about 33%) and that is usually a prelude to a price collapse (at some point either investor-owners panic and try to exit first/best or natural turnover – due death/divorce/work relo – triggers the collapse).”

If you believe this, check out, say, housing prices in Prague.

“An average Prague apartment will cost you 15 annual salaries, study shows”

No rule saying you have to be able to afford the housing. Just that it makes sense for somebody to pay it.

Volpe,

But who are those “somebodies” buying the homes 15 times an annual Czech salary?

Perhaps foreign capital (although why isn’t that foreign capital worried about all kinds of exposure – FX, political, etc?) and even if the “mystery buyers” are long-term sustainable (varies depending upon who and what they are) then Prague itself slowly but inevitably turns into a sort of “Disneyland in Decline” as the people who make a city actually function slowly abandon it due to the insane home prices (see California…)

I’m wondering with that thought in mind, if what does drop these ridiculous US housing bubble prices back into affordability–more than rates themselves, is the increasing downward pressure from homeowner’s insurance costs, or insurance companies pulling out all together, even more as weather gets worse and worse. Florida already has a massive homeowner’s insurance crisis and soon much of the state will be uninsurable.

This would make it insane to buy homes at such nose-bleed prices when there’s increasing likelihood of hurricanes, floods, tornadoes and other weather events taking out your house overnight. Not to mention that the outrageous housing costs are big part of why those homes are getting uninsurable–it costs the insurers a lot more to cover a more expensive home, so if housing prices come down and stabilize, insurers are under less stress and cut their losses, that becomes even more important as home wrecking storms get more common. I just don’t see any way Florida maintains these bonkers home prices when insurance no longer covers those homes, or surges so much in cost itself it’s like piling on a second monthly mortgage fee.

And, not just Florida anymore. California is having its own housing insurance crisis with all the wildfire risk, but now also increasing floods, mudslides and even blizzards wiping out large blocks of homes. All of this might of been manageable for insurers at say, half the current average housing cost, but they can’t realistically insure such high-valued homes at increasing risk of weather wipe-out. And then of course it’s now worsening in other states too. Those tornadoes, flooding and major storms just yesterday in Texas and Louisiana heavily damaged or wiped out hundreds of homes, that insurers would now have to pay out for.

I feel like this may turn out to of been the fatal flaw all along with using a housing bubble for (fake) wealth, certainly in the US. We’re uniquely vulnerable to terrible damaging weather at high frequency, especially hurricanes, tornadoes and wildfires but now also increased flooding, wind, snow and hail risk. My meteorologist friend said it’s like every season we get literally bombarded.

Insurance could handle this at more reasonable housing prices, but not at Everything Bubble prices. And only a fool would buy an uninsured home especially at these costs and weather damage risk–a hurricane or tornado means complete financial ruin for you then. So inevitably, housing prices have to come down to be insurable in more of the country.

You left out Texas. With a very high crime rate, expensive houses and climate disasters, homeowners insurance is extremely expensive. You will pay five times what you would pay in New England. Then you have the astronomical property taxes…

Yeah absolutely Texas is in there too with its own mounting insurance crisis. I’d imagine maybe Oregon, Colorado and Washington too with worsening forest fires and maybe flood and snowstorm risk, I know Oregon got hit hard recently. And the Gulf Coast in general. But more and more states are going to be facing this, ex. Tornado alley is a lot bigger now and the tornadoes more devastating. So maybe even a lot of the Plains states may start getting hard to insure.

I feel like this is maybe along those lines of what Wolf says about yield solving all problems with Treasuries. What makes housing in these regions of the US uninsurable isn’t simply the weather and risk of storms itself. It’s that risk for insuring housing at these prices. If the American housing bubble pops soon and home prices come back down to earth, then they become insurable again because the numbers finally start working again for the insurers. Banks won’t give a mortgage without an insurance policy leaving only cash buyers, so the insurance crisis is just another symptom of the US housing bubble, and housing costs have to come down.

So what makes US homes uninsurable isn’t really the worsening storms or climate change, it’s the fact that all this is happening amidst this outrageous housing bubble and houses across the United States costing so much to buy and, so to insure. It’s another reason that ZIRP and QE were such disastrous as policies, By inflating the housing bubble esp with MBS buying, the Fed basically created the home uninsurability crisis, in addition to record homelessness and affordability crisis. Rates still have to go higher and stay higher for longer, and even stronger QT to help correct this. And reducing the migration pressures (or more Americans leaving for an ancestral country or retiring to Costa Rica or Ecuador) might also help.

Much of the FL, TX insurance company flight is due, in part, to roof replacement fraud. Hail “damage”. I think it’s FL that makes it virtually impossible for an insurance company to deny a claim of roof damage, the gypsy roofers charge double what the job is worth, and then use puke materials to further screw the geezers.

@El Katz

Yeah that too, between Florida’s already outrageous housing bubble, storms getting worse and that massive roofing fraud, the whole state seems bent on doing whatever it can to make even the housing stock far from the ocean uninsurable. Insurers are just realizing best “solution” is leave the state. Ironically this may do more than anything to bring about the housing crash that should of happened anyway, though maybe in less dramatic fashion.

Soon it’ll be cash-buyers only and self-insurers in a big chunk of the state. And even many of them with cash to spare will hesitate to just throw money at a home with a high likelihood getting swallowed up in a hurricane, and total loss in value. The GFC started with a housing crash in Florida and in Vegas if I’m recall correctly, and soon (maybe by early 2025) history repeating. Another lesson to the Fed about why you don’t do ZIRP and inflate housing bubbles and asset bubbles in first place.

And not to mention, those soaring homeowner’s insurance costs for bubble-inflated houses also come on top the soaring property taxes, soaring repairs and maintenance costs too. It’s another reason a lot of us already doubted “the wisdom” that rising home prices are good thing for the economy, or even for most homeowners themselves. Sure, they’re maybe good for big real estate investors and house-flippers on HGTV, but for huge majority of Americans who just want shelter to go home to for years or decades in one place, with no immediate plans to sell, rising home prices hurt more than help. You can’t draw on your rising home value like a bank savings account and use it to pay expenses, so you just have spiraling high costs for the home without the extra income to pay for it. HELOC’s maybe but that’s minor in the scheme of things.

In fact about the only group in the USA soaring home prices are good for, are soon to be expats. I have seen this with a lot of people I know with this growing trend of Americans using their ancestors to get one of those passports to move into Europe (or the golden passports if they can afford a real estate investment), or with retirees going south of the border to central America or South America. They can obviously make bank selling their homes, but then they don’t have to buy right back into that same over-inflated housing bubble in the US (or renting at higher rents), they can instead take their profits and buy and move into overseas markets that haven’t seen a housing bubble like the US or Canada (or Australia, worse than our’s I guess). For almost every other American, housing bubbles make things worse and less affordable and their own expenses go up, without extra cash to cover. And insurance costs on these inflated home prices maybe straw that breaks the camel’s back.

It’s rather cut and dry. The FED’s done its best to confuse us. Actually, the FED’s confused. The FED’s gone downhill after the influx of Keynesian economists in their midst in the early 60’s. Anyone trying to decipher Gurley-Shaw’s thesis will become disoriented.

Not people. The retirement funds and banks are buying. Actually, banks are buying because Treasury department is asking them to buy. Retirement funds buy because they seek yield at all cost. Of course, it doesn’t make sense. The retirement funds are having a hard time right now holding 2% 30 year bonds they bought a few years ago. My own pension might take a hit because of the massive stupidity of the fund manager.

Treasuries and mortgages are correlated, but they’re not really comparable. Mortgages are callable; treasuries are not. Mortgages have administrative fees; treasuries do not.

The 30-day SEC yield of the MBS ETF $MBB is only 3.56% and effective duration only 5.76 yrs despite its average yield to maturity being 5.41% and average maturity being 7.96 yrs for these reasons.

Holders of 6.5% mortgages aren’t getting 6.5% returns.

A 2.5% delta between treasuries and mortgages is quite normal.

Wolf,

Thank you all the detailed update.

General question. How to know how the auction went?

One obvious thing is Yield outcome and Allotted at High %. That I can understand. How much

But I also see some articles and videos describing how bad it went, not much demand, Primary Dealer had to take a lot etc etc.

All those comments/articles are BS or some truth to them?

If truth, How to get this kind of information?

Auctions are done electronically, and you can’t even see them, I mean like watch them on TV or whatever, like an art auction or a classic car auction. There is nothing to see. They’re set up to be routine and boring.

Today, there were not enough bids at the lower yields, but there were lots of bids at higher yields, and the auction system went up the yield ladder and did what it took to sell the notes. This happens routinely, but today the system had to go up the yield ladder a little further to rope in more buyers.

So it’s hard to write gripping headlines about how the auction went. I just look at the auction results, and that’s good enough for me.

For example, for the 10-year today: The announcement on April 4 tells you the size of the auction ($39 billion). The results today tell you among other things that they got $91.8 billion in bids for $39 billion in notes, and they sold all $39 billion in notes, no problem. So there was plenty of demand, but the demand was at higher yields after the CPI report.

God bless America!

Wolf, since the yield curve has been inverted last year and this year, is that a lost recession indicator?

1. The yield curve is supposed to predict a business cycle recession.

2. The last time the yield curve un-inverted was in April 2019, and there was no recession.

3. Then a year later, in March 2020, we got a pandemic and lockdown, totally unrelated to the business cycle, and the yield curve cannot predict and is not supposed to predict pandemics and lockdowns. And it didn’t predict it because it came a year after the un-invert.

4. So, the last time the yield curve inverted and un-inverted it predicted a business cycle recession that didn’t come.

5. Since the era of QE started, the yield curve has become useless as a predictor. It reflects what the Fed is doing: pushing up the short rates and still weighing on the long end with its gigantic balance sheet. And that’s all.

Are you getting the results from TreasuryDirect or somewhere else?

After comments by MM and some others I’m dabbling in buying some directly and through a brokerage account.

Here are the auction results:

https://www.treasurydirect.gov/auctions/announcements-data-results/announcement-results-press-releases/auction-results/

The left sidebar also has links for the announcements of upcoming auctions, and other stuff.

Scroll down to where you can choose the year:

– click on the little arrows next to “TIPS” or “Bond” etc. which opens the box with the results per month.

– select a different year to get the old auction results.

you can probably get the same info from your broker, but for me this is easiest.

I think the Fed should increase the FFR for the following reasons

Inflation is now fully anchored, a condition that many on this site, predicted.

When even the treasury yield curve is irrational like now, I think too myself, what a wonderful world.

Louis Armstrong, satchemo.

Totally agreed. A FFR increase and much tougher QT, and get rid of those MBS a lot faster. Of course that might cause cracks elsewhere but this is the price for such stupid policy with ZIRP and QE to begin with. Once those bubbles over-inflate it’s hard to soft-landing despite how the term gets used.

My feelings, this year max of 2 cuts (simply as it is an election year), more likely 1 or no cuts, and a possible chance of one rate increase late in the year.

As the wolf says, “No one likes inflation.” So no layoffs in the US this year. Unfortunately, this cannot be said for Europe and Canada

Mass immigration has driven up the unemployment rate in Canada. Productivity has fallen sharply due to most coming in from the third world.

I don’t think they will cut …but I definitely don’t think they will raise. The Fed is stuck with a terminal rate that’s probably 2% lower than it should be, so all they can do now is wait. Like painting a wall with a paint brush that’s too small, it will just take longer.

Any talk of rate cuts was very much tied to the political calendar. Even JB mentioned cuts yesterday – he knows that inflation is killing him and high rates are also killing him. No way out. After the election, no matter which guy wins, the Fed will be able to back away and say “rates will change when they need to”. Which now might be well into 2025 or beyond. 5.25% rates fighting 3.5-4% inflation will be a long and bloody battle.

– I am still waiting for 2 things. I am waiting for the yield curve to go back to steepening and for the FED to cut rates (this or next month).

While you wait “for the FED to cut rates (this or next month),” I suggest re-reading Beckett’s play, “Waiting for Godot.”

haha you’re kidding me Wolf!

About 150 more points on the 10 year before sanity is setting in.

I agree that 6% feels right. I have no analysis to back that up…

I say set the engine at full power all the way to 7% or 8%.

What’s stoping us from reaching this setting is in the engine room. New engineer powell is fearful, says ship will explode.

Myself, sitting here next to the beautiful nyota uhura, death is nothing.

Real rates are crazy low because inflation is way higher than reported. Just ask Larry Summers.

This Summers stuff is BS. Economists say a lot of stupid stuff all the time, but now it fits into people’s narrative, and so suddenly he’s some kind of Jesus??

The paper he co-authored said: if mortgage interest rates were added back into the CPI basket, as they has been before 1982, then CPI would be much higher.

Here is the paper:

https://www.nber.org/system/files/working_papers/w30116/w30116.pdf

This is a stupid idea, and the only reason why THE HEADLINE of the paper went viral (no one read the actual paper) was because it fit into people’s narrative.

If you add mortgage rates into CPI, then you would have had mega DEFLATION from 2008-2018 and then again from 2020-2022.

If mortgage rates are included, then:

Every time the Fed starts a hiking-cycle, mortgage rates go up and CPI goes up even further due to the Fed-induced increase in mortgage rates, which falsifies the signal CPI is sending.

And every time the Fed cuts rates, the mortgage rates go down, and as a result, CPI goes does, which causes the Fed to cut rates even more, even though actual inflation may have taken off again.

INCLUDING MORTGAGE RATES IN CPI IS STUPID. And it was a good move in 1983 to remove them and replace them in the CPI basket.

And thank God they removed them because we would have had DEFLATION during the ZIRP years, which would have caused the Fed to go to negative interest rates and even bigger QE, which would have inflated home prices even more.

These economists are idiots sometimes.

Also life has changed. Lots of products and services that we have today that are in the CPI basket didn’t even exist back then. So CPI has to be adjusted to modern times. People who claim that the old method was better don’t have a brain. They need to look at how people today spend their money and how that differs from what they bought 40 years ago.

Summers is responsible for a lot of stupid shit, including helping repeal Glass-Stegall.

Here is a fun-to-read piece on Summers from 2013 when he was trying out for the Fed chairman job.

https://www.thenation.com/article/archive/return-lawrence-summers-mr-spectacular-failure/

This is how the article starts, to give you a flair:

“Tell me it’s a sick joke: Former US Treasury Secretary Lawrence Summers, the guy who tops the list of those responsible for sabotaging the world’s economy, is lobbying to be the next chairman of the Federal Reserve. But no, it makes perfect sense, since Summers has long succeeded spectacularly by failing.

“Why should his miserable record in the Clinton and Obama administrations hold him back from future disastrous adventures at our expense? With Ben Bernanke set to step down in January, and Obama still in deep denial over the pain and damage his former top economic adviser Summers brought to tens of millions of Americans, this darling of Wall Street has yet another shot to savage the economy.”

You’ve beat the bejezzus out of that Summers clickbait headline more than once. That horse should now be entirely dead. Many thanks for the detailed explanations.

This is one of those things that will show up here in the comments for years, I think. So I have my canned response on the shelf, LOL

The sign of a great website is when the comments section is as valuable as the articles itself. Your comment here was very valuable to me – we get tripple value, your content and your readers comments and your responses to their comments…

In fairness to Summers, he seemed to have had a pretty good call that Washington was overstimulating a supply constrained economy (post COVID) and that the result would be inflation. He was pretty early on that call if memory serves.

Sure. I’m not saying he was always wrong.

But that was an easy thing to be right about, if you weren’t being paid to be wrong about it. The evidence was overwhelming. The fact that so many “experts” failed to see it speaks (very, very, very) badly of them rather than speaking particularly well of Summers.

But Larry Summers resurrected the theory of secular stagnation in November 2013 !

Let’s say that the old methods were faulty, and I hear your arguments on that. Then we should take a look at the older inflation data with today’s methodology for actual comparability. It’s my understanding that most long-term inflation charts have old methodology in the 70’s mixed with current methodology today, and then everyone says inflation today is bad but nearly as bad as the 70’s. My guess is that they would be a lot more in line than people think, especially if comparing old and old methodologies were similar, as Summers suggested.

Then if that’s the case, compare Volcker FFR’s to the revised inflation to see the actual spread it took to properly defeat inflation, and compare that spread to today.

A lot of people, businesses and all government bodies are making wads of money from 5% interest deposits and do not wish to go back to 0.5%, or 0.05%, which was a historical abnormality. At this point buyers and consumers are managing well, thanks to past wage increases, but quite soon these will diminish, because costs always rise faster in longer term inflationary cycles. The last two decades or so of ZIRP and such peculiarities are now something for future text books. Or YouTubers.

A callable one year not getting called at 5.7%. Getting 3 months no roll over. Waiting for it! Super core inflation doesn’t help a 3% mortgage. Insurance, taxes, car insurance, car payments. Is it true Wolf hiking rates won’t do much with super core inflation?

I don’t care who is getting cooked by nukes as long as I’m getting a good return for my money each year.

I’ll be checking the federal funds rate all the way up to the hour that my family’s skin is melted off.

All hail the mighty dollar. Clutch a fistfull of those paper bills tight, clench your fist, squeeze hard, and watch it turn to sand flowing out between your fingers.

Until then, see everything through the green tinted lense of money.

Idiots massing piles of green paper are not the problem.

It’s the ones that use the paper to fund the political experiments that lead to the nukes that are the problem.

It’s not the financial greed, it’s the political narcissism that finance buys.

Indeed.

Well…as in ZIRP and the vast housing market stupidity (Take 2) it really takes two to tango.

Blind, idiot greed (apparently without any sense of history or proportion) funds – indispensably – a similar species in the political sphere.

It is getting harder and harder to see how exactly this country rose to greatness in the first place.

(Depressingly, it might amount to little more than other idiot former “Great Powers” offing themselves in endless wars – ahem – and the two oceans that formerly insulated the US from that sort of thing).

But the US seems insanely committed to making stupidity its only growth industry domestically and to seeking out trouble around the world (that the US is actually too incompetent to handle).

“A callable one year not getting called at 5.7%”

That’s interesting. Is that a CD? How many years?

One year cd. Since October.

Thanks. So it’s only got about 5 months left to run. May not be worth calling. But it’s a high rate for a 1-year CD even in October, which was the month when yields hit highs.

If they do call it, let us know.

Your bank would call it if they thought rates would go lower before maturity. Sounds like they think rates will be higher.

I have some callable Fed Farm bonds at 5.98% with a 2033 maturity. I don’t anticipate these will be called either.

Will do. Possibly because there are two other one year cds. 5.05 and 5.5%. at JPM. Brokered cds. I read somewhere that super core inflation wouldn’t really respond to a rate hike.i myself think everything would respond to a rate hike eventually. I’m sure housing prices are raising insurance costs like a poster mentioned.

Anybody besides me remember when US Treasury issued callable bonds (just some issues, I think — not all in a given year), and more specifically, what were the circumstances that spurred them to issue them?

Thanks.

I remember people getting really pissed off when the government started calling their 30-year bonds with a 15% coupon that had soared in value as yields had dropped. That uproar eventually caused the government to stop issuing callable Treasury securities.

Maybe so, maybe not. I don’t know if I agree or disagree with that dichotomy.

I’ve spent a while working in town in construction seeing residential neighborhoods that are currently occupied. It’s a weird strata to observe for sure.

Many of these 1200-1800 sqft old ranch homes that are 500k+ on postage stamp lots are owned by old folks who can barely stumble into the yard and give you the death stare for improving their amenities. Lots of houses with 1 person or an old couple bumbling around with 3 new cars parked in the yard. Many of them with retired: firefighter/law enforcement/military etc license plates.

The very few houses with younger people (as in under 60) in them are owned by obvious pencil pusher kind of guys that come and go wearing a suit and tie. The wife if applicable heads off to work as well. In a subdivision there may be 1 house with about 10 vehicles parked around it in bad shape with possibly a dozen people living in it. Family hotel with a 2 BD1 BR with a camper in the back yard.

Meanwhile over in the slums of run down old mill houses that are about to cave in to the time of 300k+ are all the working families. Almost all of them have a mother/father with the kids still living there up into their 30s.

Talking with the other guys in the company they have all but given up hope of being anything other than camper dwellers or maybe apartments. Most of them are between 21-35 and almost all live at home still with one or both parents. A lot of guys nearing 30 don’t have kids. And this company pays pretty decent. New hires get 30/hr with up to 10hr OT a week if they want. After a year and specializing with a CDL you could be at 45-50/hr.

These boys don’t have anything other than a dozen empty Redbull cans in the bed of a 100k dollar customized truck. A handful have custom sports cars or restored muscle cars. It’s something I see a lot of seems. Young people having insanely expensive toys and nothing that isn’t a depreciating asset. Paycheck to paycheck for nice clothes, jewelry, tattoos, cars, etc. Only to drive up to mom-n-dads place at 40 years old.

I think the poor class and the middle class are dumping money into the consumerism machine. It’s hard to get a job here paying less than 20/hr. You’d have to be trying to make abysmal wages that couldn’t allow you to eat. Even at 1500/mo rent. Assuming you had roommates or lived with family you can buy a lot of crap status symbols on today’s wages. But you’re not starting a family or buying a house anytime soon. The things that actually matter and can help you rise up in the class system are becoming more and more out of reach.

Then again, after the past month, I’m thinking the silver tsunami might have some credence. When half of the homes in a neighborhood have the occupants retired and spending their day falling and can’t get up; maybe the housing bust will come in the next 10 years.

Excellent article on the interest rate “head-fake!” Kudos to you, Wolf, for your sense of humor (“… the bond market is still in denial, after it got whipped into hilarious frenzy during Rate Cut Mania late last year…”)

Along those lines:

“At least half of all economic history is concerned with the tragi-comedy of governments getting into debt by extravagance and trying to get out by fraud. A good deal of the other half is concerned with individuals attempting to do the same thing.”

— Tilden Freeman, A World in Debt

Freeman’s “fraud,” of course, is currency devaluation…

That is a fantastic quote from a book that I never heard of.

Wow.

It *is* interesting how few saw ZIRP as essentially the same thing as an internal devaluation of the USD (by definition ZIRP meant you were making less on your savings).

And…how that outcome was operationalized by G money printing…which “coincidentally” engorged the G’s buying/buy-off power.

In effect, ZIRP simply transferred the economic returns that private citizens would have received on *their* savings to the G.

A huge tax.

A huge, unvoted tax.

cas127-

The Freeman book is fabulously well-written, perhaps, in part, because he was NOT an economist — he was an well-respected “heritage interpreter” for the National Park Service. The book was published in mid 1930’s.

Gets into the emotions and pathology of debt, from both the lender and borrower perspective. Also discusses what he called “the science manque” surrounding debt. The whole book is very thoughtful, and applicable to today’s debt problems.

Treat yourself — used copies are available. (Best enjoyed with a dark caramelly porter.)

John H.

Isn’t everything in life best enjoyed with a dark caramelly porter?

I just looked on Amazon and the cheapest copy of “A World in Debt” is $187 and many are listed for over $400 (I made a note to look at prices a year from now)

Apartment Investor-

Look at Internet Archives, if you’re willing to read a photocopied version.

Cheers

“A bloodbath was had by all”

Great day to be short housing and TLT

What are you using to short housing? I am using TBF to short TLT.

SRS, which is the Proshares inverse 2x RE. This fund holds various RE swaps and T-bills.

I also use TBF as my short TLT vehicle.

Reminder that these are meant for intra-day trends, but if you use limit orders and trade in & out of them, you can gradually lower your cost basis. This is the strategy I use to hang onto both of these for hedging purposes.

NB; not investment advice.

I believe this is a very important point, made by Torsten Sløk, last October.

“The bottom line is that the world only saves a limited amount of dollars every year, and the significant growth in the size of the Treasury market is at risk in 2024 of crowding out demand for other types of fixed income.”

After looking at historical recently, it seems we need to go back to 1992 for a year that started with this level of core CPI acceleration — and unfortunately, once sticky inflation is in the punchbowl, it tends to remain sticky and linger.

The recent shift by walk street zombies to trim back their narrative for seven rate cuts is profoundly absurd — and the strategy of hopefulness being hyped for one cut, is simply idiotic.

Additionally, the massive issuance by Treasury the rest of this year will be increasingly absurd and idiotic.

I really have no political agenda, but it’s worth recognizing that massive fiscal spending has more than likely fueled inflation growth, but that sugar coma high is going to be a noose in terms of Uncle Sam servicing the debt.

Thus, as the deficit continues to rocket parabolic with the Fed in the red, the Treasury in chaos, investors will be demanding higher rates for several years.

It’s actually funny that a few big banks recently reduced their savings yields, in anticipation of Fed cutting rates.

Who knows, maybe a surprise flash recession does suddenly shock rates lower … We saw that with the pandemic and the apparent 2 month recession, but, here we are again in a world that makes no sense.

I was pounding the table about new treasury auctions being a liquidity drain last year… but I was wrong.

At 4.5 to 5.5%, tsy yields are still wayyy below what you can get with a proper fixed income portfolio.

My father always said ” Our family does not pay for services “. To this day I still mow my own lawn and sparingly spend money on anything I can do my self. Granted not all services can be avoided but at some point the drunk sailors will pull back swiftly and that may be the sign our economy is finally correcting. This pull back can only come from services. The days of maxing out your credit with auto loans, credit cards, personal loans to a choking point then just wash it all away with a big fat Cash Out Re-fi are over so I can see trouble coming soon.

Now that you mention it, that’s how I roll! However, I do buy a lot of insurance which has inflationed bigly: car insurance, triple A membership for roadside assistance if needed, long-term care insurance (I do not want to be in a government-run nursing home, yikes) and more.

When I walk around my neighborhood I pass about a hundred houses. I see two homeowners who mow their own lawns. I stopped and shook their hands and congratulated them.

I’m sorry, I thought you were going to say something else!🙂

Escierto, so true, some look at a lawn mower or a car jack with a blank look, like they’ve never seen one before. I’m very good with my hands, a little behind on the brain thing.

There are only a few of us old farts in my neighborhood that do our own yard work and wash our own cars. I have a neighbor and his wife in their 40’s that pay to have their lawn moved even though they have 2 teenage sons.

MJ wrote: “My father always said ” Our family does not pay for services “

I grew up with a Dad like MJs and it was VERY rare when we would pay someone to come to the house and it would be only “after” we spent at least a half day trying to either clear the drain or fix the dishwasher ourselves. I now just do the things that like doing and I am good at and I pay others to do the things I don’t like to do that I’m not good at. I still do a lot of yard work but I pay a couple hundred a month for some guys to come once a week to do a basic mow, blow and go and I still do all my own oil changes and brake jobs but I did my last clutch 20 years ago. My son knows how to mow the lawn (and get a lawn mower or chainsaw that has been sitting for years to start) but he is more valuable to me using his free time helping me with apartment management and bookkeeping than pushing a lawn mower.

If you can do your own oil, you can also do your own transmission, power steering, and differential fluid flushes as well. Same principle, different drain & fill plugs.

Meanwhile the Producer Price Index came in at 0.2% instead of 0.3% this morning and bond yields are dropping again. At some point something is going to break.

It didn’t take long for the bond market to see through the headlines, and now yields are back up, and the 10-year is at 4.58%

Nice to see the bond markets had a great day for meaningful price discovery in US Treasuries and equities.

I have a 5.75% CD that’s being called today. I’m starting to wonder if it can be “un-called”…

Unemployment claims DROP 11 thousand and Williams comes out and says……I think we’ll still do a cut.

So….at this point…..We have to face reality……stupid……just stupid.

No wonder we’ve lost every war since Korea…..the wrong folks are at the top. We are being lead by a generation of morons.

Howdy fred. The FED speak is scripted. Follow the dots and eventually they should show double digit rates in the years to come.

DM: Billionaire In-N-Out heiress Lynsi Snyder speaks out about soaring fast food costs and future price hikes – and reveals fascinating reason why she REFUSES to allow mobile ordering

Lynsi Snyder, who became the president of In-N-Out Burger at just 27 years old, has spoken out against the price hikes affecting fast food outlets, following the minimum wage being raised in California.

It’s pure tragedy when these billionaire fast-food-chain owners and other billionaire business owners are getting squeezed a tiny little bit by higher minimum wages, isn’t it? My thoughts and prayers go out to them.

I owned a chain of McD for a while……..labor runs approximately 20 to 23 percent depending on the owner. I’am not in CA but I’d guess based on their up scale economics, wages for most fast food were running somewhere in the 18 per hour area……The increase to 20 is approximately 11 percent however based on hot inflation some of that would have happened anyway and a portion of compensation for some of the better chains in this hot market are things like health care etc. The increase does not affect management costs except indirectly because they make more. So take an abnormal 6 percent cost increase related to the bill. Six percent of 22 percent is approximately a 1.3 percent increase in overall costs. On a 2.5 million revenue unit with a normal net of $200k…….the owner is getting hit by a profit reduction of roughly $32,000.

So if an owner installs a kiosk to take orders for portion of his floor traffic and mobile orders continue to increase as they are doing…….and he/she lays off one or two counter help……he is ahead……way ahead.

Most chains are requiring operators to be multi location. The old days of running one store are long gone. So the multi owner with 3 stores is running a 650k profit and getting dinged 90k. If he is not modernizing……but he will because MCD HQ will require it. They always push new equipment of the operators to max profit.

So a modest increase in minimum wage results in a modest reduction in employee headcount. #Econ101

No it doesn’t. Econ 101 tells you that a productive workforce is key to success, and if your business can only thrive when paying slave wages, you shouldn’t be in business.

I expect some businesses in CA that you believe shouldn’t be in business will soon no longer be in business.

Fast food outlets have ~150% annual turnover. That should tell you something about wages and job security/advancement.

I wonder what the turnover rate and pay is like in slaughterhouses… probably better.

Aptly said WR.

I am in So Cal and looks like In N Out is pretty popular.

I never eat out so don’t know what’s the appeal.

There is one a few blocks from here right in the tourism center. Some years ago, I walked in with a buddy to have lunch, and the grease smell turned me off, and we walked right back out. Other people seemed to like them. So fine with me.

‘ You know what that means when someone pays you minimum wage? You know what your boss was trying to say?

“Hey if I could pay you less, I would, but it’s against the law ‘

Chris Rock

At least she will still get the 20% employee discount on a Double-Double Animal Style.

They don’t want to admit the real truth, which is that if the U.S. starts from unemployment around 3.5-4% and also wants to restart domestic manufacturing, low-end wages will come up and make fast food less competitive.

We can’t all have domestic servants if the bodies are needed at the factory.

There is an easy ways to lower your finance costs! They call them down payment and paying extra each month.

I bought my first home in 1967. It was a fixer upper for 15k and the banks snubbed me as I was 17.

A real estate guy sold it to me for a third down and 12 percent interest. I was earning less than five bucks an hour so it was harder than today. It was paid off in three years.

All todays whinning is bs. It is easier to get ahead today than anytime in my lifetime.

News Flash! If you can’t afford a down payment – you can’t afford a home, new car, etc., etc.

Howdy Bear Hunter. Youngins do not believe in Starter Homes, or how squirrels can save and borrow at the same time. They do not even realize they are prisoners in their own homes. HEE HEE.

Well, in the good old days too, older people who systematically took advantage of younger people by lying to them were frequently thought of as scumbags or pedophile-adjacent.

But that seems to have gone out the window too.

Read some of the recent articles on how baby boomers, flush with cash, are supporting their adult children. Many are getting help buying homes too.

These same “children” (many in their 30’s and 40’s) are still taking expensive vacations, sending kids to private schools, driving late model cars, going out to eat all the time, etc.

Why save if mommy and daddy will always bail you out.

The problem you describe, living beyond one’s means, goes both directions. Have you read any articles on the Sandwich Generation? Sometimes it’s mommy and daddy who need the bailout. Everyone’s circumstances are different and these broad brush generalizations about different generations often make no sense on an individual level.

Per my little understanding, this is the worst time to buy, even a starter home: High Home prices with High mortgage rates: A poison for common Joe to swallow.

Rent till things become clear.

I hope housing becomes affordable again. If it does not then we are looking at bigger problems in the coming future.

I agree buying fixer upper but now is absolutely the time.

5 dollars an hour was a lot of money in 1967. And 15k was your cost. The idea you are comparing it to today with affordability at the lowest ever as far as the government numbers goes back shows a lack of basic math on your part. There are 2 segments to this. Price and interest rates. Your pick yourself up by your bootstraps routine is tired.

Howdy minutes YEP, bootstraps has been replaced with brastraps. HEE HEE.

Agree. In Van BC new doctors can barely afford to rent, let alone buy.

This guy needs to look up ‘finalization of real estate’. When he bought this house it almost never occurred to mom and pop to buy another house as an investment. Now it’s a hobby, or was for last 10 yrs.

Did his house double in value in 3 yrs? No. Different era.

They used to tear houses down and build apartment buildings. Now we just price out the doctors.

The head of Fannie Mae has publicly addressed the 20% down payment issue. She thinks it is too much. A $400k home requires $80k down payment. She is proposing new programs of less like 10% or 5% or 3%.

How? She said the GSEs would take on the risk or the loan. If renters will allow the GSEs to monitor their rent payments and if they are always on pay their rent on time then she said these renters should be able to qualify for a home loan.

Such a program would possibly help with the down payment or if the loan is for less than 20% down, then Fannie would guarantee the loan and no losses to the lender if the borrower defaults.

Of course, this will not help make homes less affordable LOL but it would help more people qualify for a loan.

Everything these pieces of shit do to make housing, health care and college more “affordable” makes it less while putting more wealth in the hands of the top 1%.

What’s too much is the house PRICE, not the 20% for a down-payment. These morons need to get real. Housing needs to correct bigly for the sake of this country.

There have now been 12 boom/busts in real-estate in the U.S. since WWII. The busts have all been triggered by a flawed monetary policy, a correction for a loose monetary policy.

Powell hasn’t yet to drain money flows enough, the volume of money times its transactions rate of turnover. And he’s likely not to succeed in dropping housing prices.

Secular stagnation has been swapped for stagflation, or business stagnation accompanied by inflation.

If I’m not mistaken, reducing down-payments is part of what led to the first housing bubble/GFC. Weren’t we all just recently discussing about history not repeating, but possibly rhyming?

Let’s see… $5/hour translates to around $10,000/year, assuming 40 hour weeks working 52 weeks per year. The house you purchases cost $15,000. That’s 1.5x your salary.

It my area, homes are around $700k-1m and starter homes are around $500k (maybe less if you want crime next door or if you want to live 2 hours away from employment centers). The average household income in my area is $70k. That starter home is 7-8x the median salary.

And it’s easier to get ahead today than anytime in your life time? News Flash! It’s not.

LOL, yes

Thank you for putting these numbers which totally makes sense.

A lot of house humpers may not see this objectively as they are emotionally tied .

A realtor called me saying best time to buy is NOW as rates are high. When the rates go lower in coming future, home prices would spike up as competition increases.

At $5/hr you would earn $10,400/yr assuming 40 hours a week. Your mortgage was apparently $10,000. Even earning less than $5/hr your mortgage was a little more than 1X earnings. Those numbers are essentially non-existent today for prospective homebuyers in most parts of the country. You had a tremendous opportunity and good for you taking advantage of it. However, you apparently missed when the world changed and for decades home price growth exceeded wage growth for most people.

I have to laugh when you complain “todays whining is bs” and it’s easier to get ahead today than anytime in your lifetime. The facts and figures provided in your comment alone, if true, prove that to be false.

I mean, just looking at the numbers with inflation. 5 dollars an hour in 2024 dollars would be around 45 dollars an hour today, ie just shy of 100k. A house at 15k would be the equivalent of a 140-150k home today, a bit less than the median home price of around 400k. If I could find a property for 150k that’d be amazing but property in my state sells a third acre for that price with no home when it’s on sale. It is definitely not the same situation. Housing has gone up much faster than wages.

If you were making $5/hr in 1967 that was 3.85x the minimum wage and $10,400/year when you bought the $15,000 home. Today the CA minimum wage is $16/hr or $33,300 and 3.85x that is $128,205 but there are not many homes (even fixer uppers) for under $200K (~1.5x a decent income like you paid) in CA today. I don’t see many kids working as hard as I did today (and most to whine a lot more), but since the cost of college and homes have both gone up WAY more than inflation I would not say it is easier to get ahead today than in the early 80’s when the cost of a UC education and a Palo Alto home were both about10x less than than they cost today (and the minimum wage and most other wages are up less than 5x).

This has to be some sort of bait. But let’s run those numbers through the BLS inflation calculator. Being very conservative with “less than 5 bucks” we’ll use $4. $4 in 1967 was the equivalent of $37.97 today. 15,000 is 142,400. At fucking 17 years old. Yep, it was definitely harder than today. Sure

It’s amazing how far we’ve fallen as a country. This country used to be so strong that a whole generation of morons who can’t take 30 secs to google something could thrive and prosper.

“This has to be some sort of bait.”

I think it was. The guy is pulling your leg. I can see at least two giveaways:

1. In 1967, the minimum wage was $1.40. So if he made less than “5 bucks” so let’s say $4.20, he made 3x the minimum wage at 17. So that’s very doubtful. The purchasing power of the minimum wage peaked in the 1960s, it was a decent entry-level wage back then.

2. He bought a home at the age of 17? LOL. You cannot sign a contract at the age of 17. You cannot do a real estate transaction at the age of 17. I don’t know what kind of deal that was, if any, but he didn’t “buy a house.”

I tend to believe the guy since anyone with any kind of skill has always been able to make 3x the minimum wage. I was making $15/hour (almost 4.5x the $3.35/hr CA minimum wage) in college in the early 80’s toing apartment maintenance. The guy says he could not get a bank loan but got someone to sell him the home at 17. I bought a half dozen cars before I was 18 and could legally enter into a contract and there were a lot more “handshake” deals in the 60’s (in ’67 $15K bought a nice house and I recently saw an ad from 1967 where the Streng Brothers were selling “new” three bedroom homes in Sacramento for $20K).

A minor can sign a contract for the necessities of life, such as food, shelter, and clothing.

Sledgehammer,

Nope. So the minimum legal age to sign contracts is determined by state law, not federal law. In California, the legal age to enter into a contract – including a lease to rent an apartment or buying a house – is 18 years old. However, there are exceptions for emancipated minors and individuals who are married or in the military.

When a minor signs a contract, the contract is not valid, and the minor cannot be held to it.

In other states, it’s the same.

From the California Department of Real Estate:

“Contract specifics. The general rules regarding the creation of a lease (and contract), in addition to those governing whether or not there must be a writing, include:

…

3. legal capacity of each party to contract (which, in general, excludes minors, persons of unsound mind, and persons deprived of their civil rights);…”

https://www.dre.ca.gov/files/pdf/refbook/ref09.pdf

It’s based on the California Civil Code:

Civil Code – CIV

DIVISION 3. OBLIGATIONS [1427 – 3273.69] ( Heading of Division 3 amended by Stats. 1988, Ch. 160, Sec. 14. )

PART 2. CONTRACTS [1549 – 1701] ( Part 2 enacted 1872. )

TITLE 1. NATURE OF A CONTRACT [1549 – 1615] ( Title 1 enacted 1872. )

CHAPTER 2. Parties [1556 – 1559] ( Chapter 2 enacted 1872. )

1556. All persons are capable of contracting, except minors, persons of unsound mind, and persons deprived of civil rights.

(Enacted 1872.)

https://leginfo.legislature.ca.gov/faces/codes_displaySection.xhtml?sectionNum=1556.&lawCode=CIV

A minor can sign any contract, but it is not a contract, it’s not enforceable, it’s worthless. Did you fry your brain?

The Dow is doing well and is only down around 200 points.

Howdy Folks. How long did it take to get to double digit rates before? Could be headed there again is the old school bald headed bet. Youngins probably think double digit rates is an empty headed bet? We shall see.

Good Luck

As a 30-something who is apparently locked out of the housing market forever, I wasn’t aware that everything today is the same as it was in 1967. Every day I learn something new.

In 2019 I theoretically had enough cash to do what you said. Then, global pandemic, lockdown, interest rates tripled while ZIRP bubble prices remained, and my savings were devalued by at least 20% because the government has decided to get us into an unrecoverable debt spiral.

Meanwhile I have two roommates who are your age and neither of them have been able to keep their houses either. My mom is living with me because she lost her house in ’08. The other one just lost her job and a lot of my savings are tied up covering her portion of the rent until she can catch up.

Or maybe your post was just sarcasm.

Damn, meant as a reply to Bear Hunter.

He made his own boots from bear skins.

Yeah, that’s the stupidity of comparing 1967 to today’s world. $5/hour then is the equivalent of a wage of nearly $47/hour. Not a bad wage today. The house price though? A $15K house in 1967 is the equivalent of $140,000.

I’ve looked, and I’m sure you have too, but there sure aren’t any $140,000 houses any more. I earn a solid wage at my job, but there’s nothing remotely affordable like that. My landlord is willing to finance me, but he’s asking >$1M for his places (the going rate in my town). Even if I didn’t live here, finding anything south of <$300K is laughable.

So we'll keep hearing from these old folks who lived through those "great" times and they'll keep complaining about today's folks simply not trying enough, but they just don't understand rudimentary math or economics if that's what they're doing. It's sheer, laughable, stupidity to even compare the two eras.

Howdy Tom Still lots of ways, times, math are exactly the same. Housing Bubbles happened before, double digit interest rates happened before. Simple math worked well till Govern ment math took over every thing.

It’s not a matter of not understanding. It’s a matter of not caring.

Comparing era’s is still very useful, which is why Real rates are used when looking at impacts of inflation.

Obviously we live in a new era of tech driven excellence, and even though productivity has continually declined for decades — we still have the AI Crack pipe fantasy expanding — obviously very different from the mid 60s when any stock associated with the narrative of tonics was a path to exponential wealth — until reality blew apart that stupidity.

It’s hard to compare era’s, like today, when every Costco employee thinks they deserve to be a millionaire for pushing groceries around. The employees from decades ago, performing that exact job, had lower expectations, but who cares?

People had lower expectations, but people also could afford a house, wife, and two children with a blue collar job.

The world has changed. And not for the better.

“The world has changed. And not for the better.”

That BS never gets old, does it? You have no idea what it was like. Yes, houses were cheaper, and wages were lower, and cars were cheaper and shitty. But there was no internet, and no streaming, and no smartphones, and no websites where you spread silly comments around the world, you could maybe paper-mail them, or if you were into tech, you might have had a fax with a thermal printer that printed on rolls of paper, and you could have faxed these comments to your friends that had faxes. And you might have gotten drafted fresh out of high school to go to Vietnam and end up with your name on the granite wall in Constitution Gardens. And if you went to college instead and protested the war and the US invasion of Cambodia (so 1970), you might have gotten gunned down on campus by the National Guard.

And one more thing: It would have been illegal in many states back then for me to marry my wife.

“But there was no internet, and no streaming, and no smartphones, and no websites”

Gee Wolf, you kind of just proved his point lol.

DougP

“Gee Wolf, you kind of just proved his point lol.”

I dunno if I agree on those points being bad specifically lol, without the internet we’d be eating up whatever WSJ or the like want us to think.

In terms of the blue collar wage stuff I do believe labour has been getting devalued and the wealth gap has been increasing over the decades. However, it is kinda nice not to have to go die in Vietnam or whatever, and really my parents were living under a communist puppet regime at the time and by all accounts that sucked way worse than the “horror” of today’s economic reality. I’m too young to be nostalgic about those eras either way, I barely remember things from the 80s, I remember wanting bubble gum but the store rarely had any which was a bummer and some Stasi MFer at the border staring through the back window while I pretended to sleep as we crossed over for our forever vacation, so not so great even by my blurry account 😆

@DougP. Really, as a millennial you’d think I’d be all about tech and how much good it’s done. I’ve built computers, played all kinds of games, taught myself a variety of programming languages, I run Linux right now and like to do everything on the command line and in Vim, etc.

But, I’m having a really hard time convincing myself it’s been a net benefit to society, especially now with crypto and AI and state surveillance etc. Rationally I think it has been a benefit but apparently my gut doesn’t agree.

I’m reminded of “Bowling Alone”, where the author found that by far the most tightly correlated factor in the decline of social capital in the decades leading up to 2000 was the rollout of television.

With every new technology there are many benefits, but it is easy to overlook the negative aspects that always go along. No one will ever admit their strong addiction to their phones. Rather they tout the many reasons why they are so beneficial. And they are, but often the associated costs are not talked about.

Matt B, this might hit a little too close to home but a good read is,

“The Anxious Generation: How the Great Rewiring of Childhood Is Causing an Epidemic of Mental Illness” by Jonathan Haidt.

It tracks diagnosable mental illness in young people with the development of phones and social media.

Matt B,

I empathize very much with your feelings. 20 years ago I was building my own computers, overclocking them, and dual booting linux/windows. I also ran my own game servers out of my (parents’) house. Taught myself Basic and wrote programs on my TI‐84 graphing calculator to do all my math problems for me. Oh and a bit of Python too. Etc etc.

But I can’t stand modern tech. I quit all social media a couple years ago and recently switched (back) from a smartphone to a ‘dumb’ flip phone.

I can’t stand new cars either – feels like I’m flying the friggin space shuttle. I’ll drive my 2011 till the day I die.

I understand rudimentary math and economics quite well. I ran a department with a $2B+ annual operating budget.

Both my kids were taught the same basic things my parents taught me. In a conversation last evening with my daughter, she acknowledged the fiscal lessons she was taught as a young adult by this out of touch geezer and also recognizes the discipline that it takes to get what you want. She had to apply those lessons in order to personally pony up the $250K required to gain the training, licensing, certification, and on job experience to achieve her goal and vision for how she wanted her life to play out. During the years it took, (she left a job that was paying $200K plus stock options and bonuses because she couldn’t see herself spending the rest of her working life commuting to an office and the BS politics it required) she wasn’t even earning minimum wage when she netted it out. But she kept her eye on the prize with absolutely no guarantee she’d get there. Lots of couch surfing to make her dream come true. And she did it… the ultimate goal achieved in January 2023, with multiple stops along the way. Income restored with even high financial potential as well as an improvement in her quality of life.

The situation changes over time, but the basic tenets don’t. We run our household(s) like a business. Income. Expense. Liabilities. Make a plan, check it, do (execute), revisit the plan, act on the revision. If you have no idea of what you spend on things and where the leaks are, how can you ever move forward? No idea how to invest your money? Don’t realize that passive income isn’t evil, but a gift? Like other posters have said – there is no such thing as perpetual growth – in salary or otherwise.

Life is a tough teacher. First you get the experience and then it teaches you the lesson.

@Tom. By the way I know what you mean, 140k in CA would be a dream right now. If you want to double that figure and see what that gets you here, I just saw this fantastic “rebuild or remodel” show up in the local news. If anyone wants a laugh have a look at it on Zillow: 7765 Locher Way, Citrus Heights, CA

It’s a burned out husk. The firefighters cut a hole in the roof and rain has been pouring in for two years. The owners put up blue tarps and were living in it until recently. Is this what boomers mean when they say “be frugal and buy a fixer-upper”?

“a lot of my savings are tied up covering her portion of the rent”

One of the hidden costs of renting – sharing a lease with someone who isn’t solvent.

My old roommates still owe me over $4k from rent I covered for them, but there’s no chance I’ll see any of that money.

Which is why joint and several liability provisions should be outlawed. The risk should fall on the landlord, not the other tenants (assuming the landlord consented to all of the tenants being on the lease in the first place).

If that risk fell on the Landlord, no Landlord would ever rent to multiple tenants.

I find your terms to be quite satisfactory indeed!

Sure they would. They would just diligence all the roommates, and not just one.

Replying to DougP:

it is very common in CA to rent a single home to multiple tenants, separate lease for each, as it fetches more money

I don’t do it, but the hottest trend in renting today is “by the bed” or “by the room” leases since renters will pay a premium to not have to worry about a roommate not paying the rent (or coming home to a dark apartment because a roommate didn’t pay the power bill)

That was the other issue, the shared gas & electric bills.

Somehow I was the financially responsible one in all my former roommate groups, and always ended up collecting $ and writing the check.

I’ve seen those “by the room” rental arrangements, but then you’re living with a bunch of randos instead of your friends.

Look at the home price graph from 2007 to 2012 and be glad you didn’t buy in 2007. Perhaps it is 2007 again…

Wolf,

Thanks.

Bloody day for dollar bears as well with the USD$ index up 126 pips…and $USDJPY hitting a new three-decade plus high. Stick a fork in the yen, it’s done.

“:$USDJPY hitting a new three-decade plus high. ”

If BoJ starts selling US Treasuries to defend YEN then it’s gonna increase the yields on US Bonds!

Larry Summers is in the Jamie Dimon camp. Jamie thinks rates could go higher. Larry this week is saying the FED messed up in the past saying inflation was transitory and now Larry is saying they need to raise rates. 5%ish is to low when he thinks inflation is really at least 6%. I think he called it something like “supper core” inflation. LOL Which probably means what people really feel?

“You have to take seriously the possibility that the next rate move will be upwards rather than downwards,” Summers said on Bloomberg Television’s Wall Street Week with David Westin. He indicated that such a likelihood is somewhere in the 15% to 25% range.

He also noted that core inflation, which excludes food and energy costs, has been surging due to wage growth.

“It sure looks like super-core was explosive in January,” Summers said.

Dot plots are tea leaves for the incredibly naive; which most bond traders now seem to be. If Jamie Dimon says 8% or higher rates are a reasonable expectation, why would anyone buy 30 year bonds wishing for a rate cut that might not even come?

Starting to wonder if I’m making a mistake holding short term Canadian T-bills (saving for a home) instead of US, right now the % difference is small and I dont have to pay cap gains on Canadian ones but that might widen in the near future and then I think CAD is going to get crushed further. Any advice? Lol

All of this stupidity to avoid a recession.

If you never stop drinking you never get a hangover, right?

No, you just kill yourself, which is what politicians and bureaucrats are doing to this country.

DW

He’s just mad because his margins on kitchen cabinet installs have fallen.

It will be nice when US interest rates / yields move above 10%.

Fact: the purchasing power of fiat dollar buttwipes has been decreased by 25% since 2020.

Question: is this level of theft adequate to make the public and private debt burden manageable?

Humble nsa follows QTM (Quantity Theory of Money) by observing the squiggles in the M2 chart. M2 increased about 40% between 2020 and 2023, resulting in an inflation peak of 10%. M2 has since decreased about 5% since 2023. Does this portend under 2% inflation by the end of 2024? QTM doth doth say it’s so………….

We don’t have a good money supply measure. M-1 and M-2 include and exclude certain types of cash — though it might have made sense decades ago when the measures were designed. So when cash shifts from one category to another category of cash — such as cash going from several CDs of less than $100k to one CD of over 100K, then it changes M-2, though nothing really changed. Same with money market funds ON RRPs, etc. That’s why M-2 stopped falling when ON RRPs started getting drained, and part of that drain when into reserves. That’s why lots of people who understand this don’t look at M-2 anymore. It gives a faulty signal and needs to be fixed.

MW: Long-term Treasury yields end at nearly five-month highs after March producer-price data

MW: Nasdaq sweeps to record close as market sentiment buoyed by PPI inflation report

Two Things about the PPI Today: The March Seasonal Adjustments Were Huge, and the 3-Month Rates All Jumped

Including by 7.9% annualized for the not-seasonally adjusted PPI, worst since June 2022. So we’ll take a look.

Now all asset prices are just melting up because inflation expectations are firmly entrenched and the speculators are buying anything and everything. The FED has completely failed. There is an everything bubble mania going on, and even NFTs are making a comeback.

Look Depth Charge, some days I just want to sit down with you somewhere, get you some nice liquidity, and force you to take a deep breath and relax.

A popular Canadian financial blog discovered that Ottawa plans to assent 30-year mortgages. This worsens a housing bubble.

And I say again; housing appears too big to fail in Canada despite the economy is performing worse than the States with a 73 cent Loonie.

Can’t start a business if the feudalistic commercial landlord wants all of the revenue to pay rent for land that was obtained for Pennie’s on the dollar like the Greenbelt scandal.

This was part of the budget a year ago, and it has now been implemented. So your blogger is quite late with his “discovery.” The government is borrowing by issuing government of Canada bonds, and then it’s taking this money and buying government guaranteed mortgage-backed securities (CMBs). The whole thing is questionable for all kinds of reasons, but what it hasn’t done and won’t do is visibly lower mortgage rates. This blogger has written a lot of nonsense about it – apparently it’s getting him clicks. I’m on his email list and I see this stuff.

Borrowing money to prop up homeowners and corporate landlords while tent cities are popping up everywhere. And people thought Canada was like Norway.

All they’re doing is swapping bonds that they’re on the hook for anyway. But yes, it’s kind of a useless exercise.

Endless oddities, but just saw that copper was starting to test new highs, which is super curious because that implies commodity inflation— which is somewhat at odds with gold testing new highs — which is especially weird, because the ust10y is pressing over 4.5% — and that doesn’t compute.

I’m only looking back to 1999, but in general, inflation isn’t good for gold, but I’m not a goldbug. It’s also a bit weird that $us dollar is high and oil going higher and stocks.

As Wolf has stated probably 200x, why would anyone in the world hold a ust10y whilst it pays less than a bag of Cheetos?

I think that mismatch dynamic has a lot to do with mispriced long treasury bonds, but as Wolf also denotes, demand is super high and resilient — even though foreign demand is weaker.

I assume these undervalued bonds plug into various institutional portfolios, as hedges that produce enough income flow to be a useful offset, but, WHY would locking up a long bad rate be more beneficial than a short term money market?

That general idea is even more interesting in terms of sticky inflation eating away the performance/reward of a hedged portfolio. That seems like a guaranteed bad bet.

A stupid guess is that someone gets paid fees to churn accounts, which means a lot of people are not paying attention to risk, which might dovetail with the idea that term premiums are screwed up, implying that there’s too much discounted transactions— which may say something about weaker auctions, as Treasury dumps massive issuance.

Bottom line, long Treasury yields are too low and as yields go higher, overvalued equities and commodities reprice.

My two cents, worth nothing.

The second wave of inflation is coming. Higher, for longer! Has CONgress figured out how to balance a budget yet?

Hedge accordingly.

Here’s a valuation clue from Kansas Fed, giving a puzzle piece from 2020, about the G-spread. Unfortunately they don’t update this and gathering the data for this isn’t exactly easy, or made readily available by the Fed or Treasury.

The G-spread is a way to look at bond risk:

“The G-spread depicted is the average spread between on-the-run and off-the-run Treasury yields at maturities of two, five, and 10 years averaged over the previous 15 days.

Source: Wall Street Journal”

Good luck putting this together, because Fred seems less and less useful and more and more data seems suspicious.

You should have read a little further in the same article – or was this too hard? – where it also says this, which explains the issue: