Consumers got a break on prices of durable goods, and so they tripled down?

By Wolf Richter for WOLF STREET.

It’s not a surprise that our Drunken Sailors, as we’ve lovingly and facetiously called them all year, keep splurging on goods and services, despite endless expectations that they would run into whatever wall of the day. A record number are working, and they have gotten big pay raises, and they’re making record amounts of money, and retirees have received an 8.7% Social Security cost-of-living-adjustment for 2023, and yield investors have been receiving around 5% or more on their trillions of dollars in money market funds, CDs, high-yield savings accounts, and T-bills, and mom-and-pop landlords have pocketed nice rent increases this year, and it all adds up.

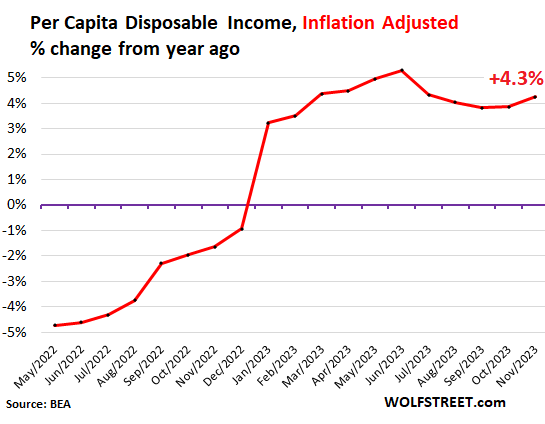

Per-capita disposable income, adjusted for inflation, jumped by 0.4% in November from October, the biggest increase since March 2023, and beyond that since peak-stimulus-March 2021, according to the Bureau of Economic Analysis today.

Year-over-year, per-capita disposable income, adjusted for inflation, jumped by 4.3%. That’s a huge relief, after having fallen woefully behind inflation in 2022. In other words, per-capita disposable income has been outrunning inflation by 3 to 5 percentage points all year. This is where the money came from to do all this spending:

Disposable income is income from all sources minus income taxes and social insurance payments. It includes income from wages and salaries, transfer payments from the government (mostly Social Security benefits), income from interest, dividends, rentals, farms, personal businesses, etc. But it excludes capital gains. This is what consumers had left to spend on goods and services and to save. And they spent a lot and saved some too.

The personal saving rate rose to 4.1% (from 3.8% in October) – somewhat lower than in the years after the Financial Crisis, but higher than in the years before the Financial Crisis. That’s the portion of disposable income that consumers didn’t spend but put aside in various ways, such as contributions to retirement accounts, paying down credit cards, or leaving a little extra in their checking accounts.

Personal income without transfer payments, adjusted for inflation, jumped by 0.6% in November from October, and was up by 2.9% year-over-year.

This is income from wages, interest, dividends, rental properties, farm income, small-business income, etc., but without Social Security benefits, unemployment insurance, VA benefits, etc.

This income growth is a function of record employment, rising wages, higher interest incomes and rental incomes, etc. It means our drunken sailors have out-earned inflation by a fairly wide margin in November – not including government transfer payments – and that’s where this spending growth comes from.

You can see the period in 2022, when inflation-adjusted income fell as inflation outran income growth.

![]()

And they went partying.

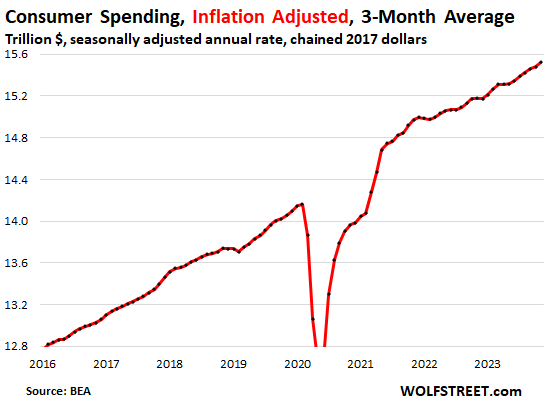

Consumer spending, adjusted for inflation, rose by 0.2% in November from October, as consumers were outspending inflation at a good clip.

Year-over-year, adjusted for inflation, spending rose by 2.7%, the most since March 2022.

The three-month moving average, which irons out the monthly squiggles and shows the trends better, rose by 0.3% for the month and by 2.3% year-over-year, the most since April 2022. The chart shows the three-month moving average. Note the slowdowns – the flat spots – late last year and in the spring this year.

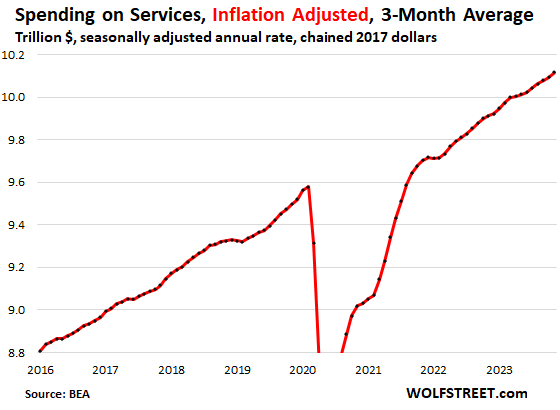

Spending on services, adjusted for inflation, rose by 0.2% for the month and by 2.2% year-over-year.

Services is of course where inflation is now entrenched. Services PCE inflation, also released today, rose by 4.1% year-over-year, on inflation in rents, accelerating to 6.2% annualized, and consumer spending outran that 4.3% services inflation by 2.2 percentage points!

Spending on services accounts for 65% of total consumer spending. It includes housing costs, utilities, insurance, streaming, broadband, cellphone services, entertainment, healthcare, airfares, lodging, rental cars, memberships, etc. The remaining 35% are spread among durable goods (cars, computers, furniture, appliances, etc.) and non-durable goods (food, gasoline, clothing, shoes, supplies, etc.).

The three-month moving average of spending on services, adjusted for inflation, rose 0.2% for the month and 2.1% year-over-year.

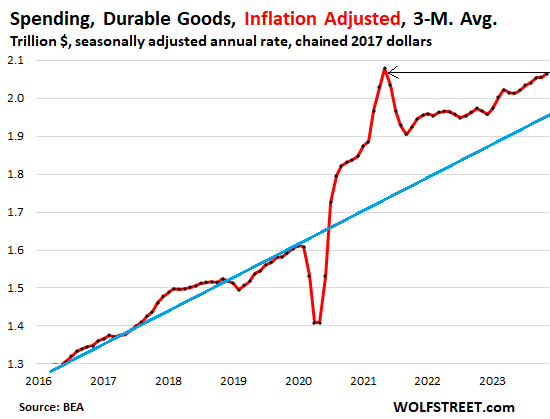

Spending on durable goods, adjusted for inflation, jumped by 0.9% for the month, by 6.7% year-over-year.

Durable goods prices have been dropping for a year – meaning negative inflation. In November, the PCE price index for durable goods, released today, fell by 0.4% for the month and by 2.1% year-over-year.

Not adjusted for inflation, spending on durable goods jumped by 0.5% for the month, and by 4.5% from a year ago. Consumers got a break on prices of durable goods, and so they tripled down?

The three-month moving average rose by 0.5% for the month and by 5.0% year-over-year.

It’s just mind-boggling, this continued spending on durable goods well above pre-pandemic trend, even after the huge spike during the pandemic. Homes, garages, storage lockers, and toolsheds full to the ceiling, no problem. On an inflation adjusted basis, spending is now almost where it had been during the very peak of the stimulus craze:

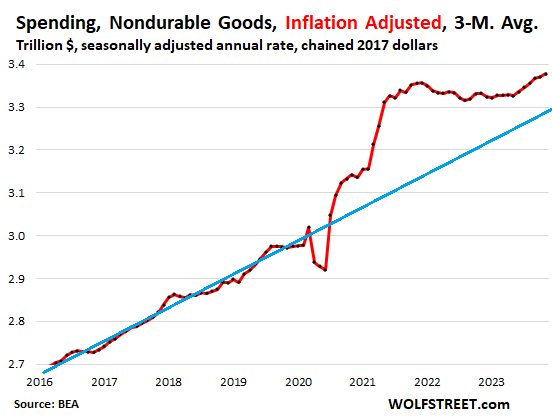

Spending on nondurable goods, adjusted for inflation, rose by 0.3% in November from October, and by 2.0% year-over-year.

The three-month moving average rose by 0.2% for the month and by 1.4% year-over-year. There had been a mild decline in spending after the huge pandemic spike, but it never reverted to pre-pandemic trend, and then started growing again in the second half of this year roughly in parallel to pre-pandemic trend, but well above it, and looks to be pulling gently away from it. These are just astounding charts:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Howdy Lone Wolf. YEP. This retiree is spending, saving more than ever before. Lots of Christmas $$$ to the children also. Rest in peace ZIRP.

So I boost 7 Big Tech stocks by 75% with my shenanigans, and all media thinks that economy is doing great!

No, Bro! You boosted interest income from 1% to 5% for like a hundred million people, created 10s of millions of jobs and big pay raises for everyone else!

I’m retiring in 3 months with more money than I know what to do with. In the market for a smaller live aboard sail boat for overnight excursions. Maybe a Catalina 28 or something. So keep doing what you’re doing!

Can you brag some more?

@Kent. That 5% interest is about to be rolled back to aid the banksters and the 1% pretty soon according to the Wall Street whizzes.

So the 100 million people (less the 1%-ers) are not going to be happy…in fact, they will be downright pissed that Powell bro is back to helping the tiny minority.

Hope you’re not banking on the 5% interest to buy your Catalina…if you are, then it might get repossessed pretty soon. Enjoy it while it lasts.

John:

People who have money don’t usually talk about it, so this one is definitely suspect. I’m doing fine but still think the economy sucks. That’s not bragging but pointing out that even people who are doing okay don’t always like what’s happened in the past three years. In fact, I’ve never been more miserable in my entire life and don’t much like my country anymore. It’s disgusting. Housing, insurance still outrageously high. Sick of the bragging on here and talking up the economy too. I’m not in the market for durable goods, so I don’t give two shts if the prices dropped when many other necessities are out of sight.

Catalina 28 is too tiny! I am selling my Leopard 48 in a few months in Florida! Enjoy all that money?

It looks like 2024 is going to be the year for small caps to do well. Or maybe we are in a new era that the economy will be dominated by a few companies that have monopolies on key industries.

Yes. That is exactly the problem. I think the monopolies are propping up the market with buybacks. I wonder if generational changes in money management skewed the market permanently. Could our drunken sailors, Generations Y and Z, be happy living in generational homes (aka. Mom’s Basement)? They are saving in 401K and other stock markets, purchasing lavish cars, and spending on services with friends? Our count over the holiday had 1 in 8 living the American Dream. The others, mind you working 40 hours with a very decent wage, are comfortable in their childhood bedrooms. Not wanting to move away from home. Kick in on monthly payments for utilities and help with renovating the homes. They are comfortable buying autos (new status symbol) with monthly payment over $1,000 for 48 months. They state with their 401K, Roth and other savings investments, they can retire easily at 50. None really care about owning a home, starting a family, or living in their own. These are both girls and guys between 22-31. The parents are okay due to house prices. Many just placed their kids on the deed. I am not sure the markets will ever turn back to traditional norms. This new generation is okay with owning nothing and being happy. The only thing that caught them was my 11 year old asking the elder kids, “Without kids, who is going to help you when you are old and have a medical emergency?” They answered each other. I guess these siblings really remind me of the stories from the Great Depression. It seems like their hope is strained and they are accepting this behavior. What does that say for our traditional market?

Americans sure love their stuff. The Sackler’s have nothing over Stuff!

Howdy Randall. Yep, and we have the Federal Govern ment playing Santa like never before ….. 34 trillion and then to the moon….

Basically, if you own a house or rental property, you’re doing great. If you rent, you’re hurting.

Nah, I know there’s plenty of well off folks who choose to rent. I think, below certain income levels though, you are correct.

I could have bought a home but choose to rent.I have medical issues so it’s too hard for me to take care of a house. Secondly, we have neighbours who actually own homes and use that money to pay for an apartment here. Don’t know what they are planning but buying isn’t for every single person.

Banks own it if you have a mortgage, and if you bought them before 2020 and refinanced. Renting and owning properties are not easy to manage it’s a part time job if you DIY.

Renters have been hurting since over a decade. Owners have been killing it. But it’s gonna crash soon! Next year…..never mind, the year after…..okay, but the year after for sure this time!!

We have a rental condo. It takes care of itself….but it’s not a huge moneymaker. And actually….it almost seems like a waste of time, when one considers if the money was instead invested in the stock market, it would easily return double. On the other hand, the value of the property continues increasing (as does the rent); but those gains are only realized at some unknown date in the future when it is sold.

If you have a job or income you are doing great, otherwise the house may not be such a great asset. Lots of unemployment in tech and white collar salaries are dropping.

More BS per usual.

Tech employment is still near all time highs.

Same with white collar salaries.

I work in tech and almost all of my friends work in tech

Techies made it like crazy in 2020 and 2021 but right now tech job market is really tough

I have friends who got laid off from faang last year and still have not found jobs

One of my friend was offer a job in distant location with 50 percent of his previous base salary.

I can’t speak about other white collar jobs but I follow tech job market very closely.

“Tech employment is still near all time highs.”

For citizens or imported workers?

Marc Heatherington,

“For citizens or imported workers?”

FYI: Imported workers can be citizens, including me, myself, and I, since the 1980s.

I work in tech, my company had layoffs at the start of the year. Hit 3 people on my team. Two I would consider largely useless and one who I felt was a great asset. The asset had a new job in less than 3 weeks, one of the other two had a job in two months, and the third appears to have stopped updating his linkedin. Its possibly he has left tech entirely, which would be the correct choice for him.

Ive seen lots of churn in jobs from old coworkers Im connected with, but notice almost no one who cant find something.

I rent with nearly $ 1 million in the bank. I’ll continue to do so until housing prices drop. I’m in no rush.

Which explains why you have a Mil.

It looks like they may never drop.

The Real Tony,

You’re in the Toronto area. This is what home price are doing there:

https://wolfstreet.com/2023/12/14/the-most-splendid-housing-bubbles-in-canada-toronto-19-from-peak-back-to-sept-2021-hamilton-area-25-back-to-feb-2021-new-high-in-calgary/

Not really true still have taxes,insurance and maintenance. There all increasing . It hurts us senior citizens

If it makes you feel any better, I’ll have like a hundred bucks in my checking account after paying my mortgage, prop tax, and insurance at the end of this month.

That is an existence that I have not lived for 50 years when I was 20.

That would terrify me to no end.

Homeowners won the lottery.

Renters did not.

Wolf,

Thank you for the update. In many ways, it looks like we have gone back to pre-pandemic trajectories (roughly speaking). I don’t know that our pre-pandemic trajectory was rational, but who am I to say something is wrong with the economy, it’s working so well for so many people. Perhaps someday things will be different, but for now it is what it is. Wishing everyone happy holidays and a wonderful 2024.

I see the trajectory on the charts, but my tenants, mostly truckers, are definitely showing some signs of pain. Local and over the road. Rates are down, load volume is down, and repair prices are bordering on criminal. I also believe repair skills are far from what they once were.

I can also say that my tenant waiting list is probably 10% of what it was 2 years ago.

Maybe it’s the doom and gloomer in me speaking but I can see this won’t end well for the drunken sailors down the road…party now and worry about the hang over later. Wonder how many of these drunk sailors (or I refer to as Ye-yo addicts) even looking out the corner of their eyes to spot if that 100 miles an hour curve ball is anywhere in sight…

Or not, maybe this is the new normal and prosperity for all forever, well all except for major asset owners like homeowners..etc. My work, one of the big pharma just laid off a bunch of people right after getting back from Thanksgiving, wonder if any of them will curtail their spending now, or bounce back with another job in a month?

It is Aesop’s old Ant and the Grasshopper fable playing out. The grasshoppers are having one whale of a time right now.

Instant gratification beats boring saving and planning any time, right? So don’t be a square! PARTY ON DUDES!

Best way to stave off a hangover is to start drinking again.

Works eve better if you just don’t stop drinking.

Well, obviously you know exactly who the culprits are, drunken sailors which, in this context, is a euphemism for us, the population.

I went to Costco this morning 30 minutes after it opened 1030 AM). I had to park in their site gas station area as the lot was full. Never, have I had to do that. Inside, it was like a Chinese fire drill in the store. It took me 20 minutes to check out with my two boxes of chocolates and I was in one of the three self checkout lines.

It took me 10 minutes to get out of the parking lot due to jam ups of people in the parking isles and coming in the three entrances.

This shopping madness I witnessed this morning reminded me of past Black Friday deals at Walmart where people would line up at 2:00 AM to get a cheap TV set.

Pure madness.

The Costco near me is like that too. I woudln’t read that much into it. First, Costco is a place where people go to save $. Second, it’s the last weekday before Christmas. People were stocking up on Christmas turkeys, mashed potatoes, hors d’oeuvres platters, etc.

1/2 the millionaire in the US shop at Costco.

Two months free Costco Instacart+ is a good way around all that.

Except Costco raises their prices when listing items on Instacart, sometimes by a lot. There is no way around it, Costco will make you suffer by crowds or higher prices. But it is worth dealing with the hordes to a lot of people to buy stuff cheap. However, not me.

I’m pretty anti Costco myself, mostly because I don’t have a family and don’t have space for 1.5yrs worth of TP and toothpaste otherwise I’d probably have to put up with it, but the lineup madness is one more good reason to avoid it. The one that gets me is the $3 you can save on gas or whatever but you gotta sit there and idle half the savings away because the entire town is lined up, I mean most regular gas stations have rewards programs that save you less yes but life is short and you can get in and out in a matter of minutes.

Seba-

My 1.5 yrs of TP from Sam’s Club served me well during the pandemic. There was a big promotion in November 2019 and I bought the minimum to take advantage of the sale–which saw me through the crisis!

The rich horde wealth; the wannabe-rich horde toilet paper.

(Hoard, dammit)

I’m with Seba, I just can’t find anything I need at Costco. You can see thru their business model pretty easily. And their cheap overhead lighting gives me headaches. I’ll keep their membership and just order the random need from them online.

Costco’s 4.99 chicken roast beats Kentucky, Churches, and Popeyes. And my dog gets the legs.

spencer,

Happy to hear that you give your dog the best parts (the drum sticks), and that you’re stuck with eating the boring chicken breasts.

Costco gas is always .80 to 1.00 cheaper per gallon for 93 for me. 30 gallon tank, 4 times a month, the membership more than pays for itself the first month of I never do anything else than get gas one time. Everything else is a good bit cheaper than elsewhere as well. I’ll fight the lines when I have to.

LOL…

1) The drumsticks ARE the best part. Ask any kid! For the life of me, with chicken wings in short supply I have never understood how there isn’t a sports bar chain named “Drumsticks”

2) Back in the pandemic I was watching an old cooking show with the famed Cajun chef Paul Prudhomme (inventor of blackening fish and other foods) on it and he said his father (a chicken farmer) would double over in laughter if he could see what chicken wings were priced at these days. He giggled a bit at the memory and said, “We used to feed them to the pigs because there was no market for them!”

It’s worth the money, time & hassle just for gas which is $0.40 cheaper at my local Costco than anywhere else.

My main gripe is that they check your stuff on the way out for stealing. Seems like a huge waste of time & labor expense.

IMHO … If you are hearing impaired Costco is a purchase hearing aids. You get a free checkup each year and their warranty – 2 years – is first rate. Your details are available nationwide at any Costco Hearing Aid center.

You DO have to be a member.

————

Shopping wise … you get whatever products they have on they shelves. If it’s not what you want … too bad :-( Some of their bulk prices, especially for popular OTC “medical supplies” are pretty good.

Their gasoline prices can be good but expect to wait in line.

And if you like junk food – we do – a hot dog and a slice of pizza with a soft drink for each of us is pretty cheap.

—————

All that said if I didn’t need Hearing Aids we probably wouldn’t bother being members. Other wharehouse clubs exist with better brand selection.

YMMV

I do around 90% of my shopping online. I’m almost nostalgic for physically shopping for stuff amongst the thronging holiday crowds….no scratch that, I don’t miss that at all. I’d rather chill at the local cafe and peoplewatch.

Nobody shops at Costco anymore. It’s too busy

(I couldn’t resist. Apologies to Yogi Berra…)

Exactly. I don’t shop there anymore due to the crowds, even at opening.

Going to a Costco shortly after it opens is always the worst time. Either go and get gas before it opens and then park right before it opens to be first one in (they open the doors before actual opening most places). I find the best time is late evening an hour before it closes on a weekday when everyone else is having dinner at home. Nice and laid back. Saturday mornings 1 hour after opening is the worst.

I think the gas pumps open an hour before the store.

The gas pumps are generally open until at least midnight I would think. I used too fuel there at 11 at night 20 years ago.

Inflation is kind of a funny thing. If you expect it, it gets worse and you start to expect more of it. So you buy in anticipation of of inflation. Then you buy the asset in anticipation of being able to resell it later at a “profit”. And do on,……. It is kind of like a merry-go-round until the music stops. And it will stop. The big question is when.

I think your description of inflation as a merry go round which ends when the music stops is worth considering as a potential likely outcome, assuming that that is in fact the policy of the Fed. Which I don’t think that the Fed is prepared to be so transparent about what they really think.

Obviously they see the asset bubbles that they blew which are now creating the inflation we are experiencing.

Where I live its like that everyday of the year all day long from open to close never a parking spot ever unless you get there about 20 minutes before they open.

With bear market over, investors are also flush with cash and are partying. Wall street bonuses are going to be epic and Ferrari’s and Porsche’s will zipping through Connecticut.

Actually, Wall Street bonuses are flat or lower. Wall Street makes money on volume, and deal volume (M&A, IPOs, etc.) is down substnatially.

They can’t do prop trading anymore, ever since Dodd-Frank and the associated reforms.

As a Pop-only micro-rentier, my net worth has not dived as much as expected because of rent increases and Social Security payments inflation increase. So currently not so inhibited in blowing cash. But that helps Thailand economy, not United States.

I honestly don’t see inflation in any real sense myself. When gas was $6 in CA I did. I own my house so fortunate there. Apps make a big difference as well as stores are competing for all the money that is being spent. That said, I am financially in a sound place, as I get how difficult this is for people living paycheck to paycheck as a lot of people can’t handle an unexpected expense of just a few hundred dollars and not easy to rack those up.

Good times, good times! Ain’t we lucky we got em!……good times!

As a retired person I would suggest that my income didn’t outrun inflation by any stretch. I’m too old to take giant risks in the market. I am thankful that I can park money in CD’s that seem to match or slightly exceed inflation.

I think that is half a wise strategy. The other half is addressing duration. Is a one year CD better than holding a three month T Bill. On a million dollar portfolio, the difference between the rates could cost as much as 70 dollars per day.

Where’s the recession?

In your pocket

According to financial indicators, the Fed tightening has failed to make any impact – assets are close to ATH, financial conditions looser than in March 2022. The real economy is just starting to get impacted, with employment still record high.

Inflation reduction to 3% had nothing to do with the Fed. Inflation was mostly caused by temporary shortages and monstrous money printing.

But the lag is just starting to hit the real economy – bank lending, business financing. 100 bps easing won’t make a difference.

The 2019 economy could not tolerate 2.5% interest rates, what is 5 or 4 going to cause?

It got lost in the woods.

Capitalist running dog lackeys: This hope of no recession is the dream of the capitalist’s running dog lackeys, dreaming of billions of dollars by acquiring an interest in a couple middle class rental properties, hoping there appreciation brings them millions.

Capitalist pig: However, the capitalist pig with real wealth wallowing in their own filthy nest of ill gotten cash needs to have a boom and bust cycle. Get the property cheap and sell it to any sucker. Then the capitalist needs a bust to get the property back cheap and start a new cycle.

@Gary,

Wow

Why research, work, or even invest in the future if the world is two sides of a stinking sty?

Did you come here hoping to find a better way? If you already know one, please enlighten us all.

“It got lost in the woods”

Not for long though.

I’m keeping an eye on:

-retail sales to fall

-credit cards debt to maximize

-auto loans falling behind

-home equity tapped

It might take a while but, eventually we’ll get there.

Only if rates go up and sadly it will mostly hurt the withouts even more.

The Fed really blew it over the past decade and there is no way in the world they will ever let it crash as the cost to bring it back is worse than the pain now.

I’ve told my daughter graduating law school..invest in just about anything..the Fed has your back. If by chance they don’t, don’t worry..things will be so bad you will be just hurting like everyone.

Party on!

60% of Americans live paycheck to paycheck…so there’s that. Of course, most people are just used to servitude.

I wonder what percentage of Americans have always lived paycheck to paycheck? I had a blue collar alcoholic uncle back in the ’80’s who paid his bar tab with his paycheck every Friday. The bar got paid first, then food for my cousins.

EXCELLENT answer!

How are they defining paycheck to paycheck? I only have like a few hundred dollars in my checking accounts at any given time. As soon as I get money deposited I pay bills regardless of when they are next due (including cc balances) and rest gets invested immediately. So I guess I live paycheck to paycheck then…

…always understood it was ‘how much month ’til the end of the money’…

may we all find a better day.

The recession …. if the rich are getting richer and the poor poorer, then the poor are in a recession…simples… What percentage of people are poor, that’s the question.

Malls are crowded again! Wow, who knew. Our local raleigh news station did a report, 45 minutes to find parking at most of the local malls! That’s a pretty 2015 problem right?

Also about got mugged for being in the wrong area of the city. Luckily my big city senses kicked in and I hopped in the car when I spotted the 2 thugs coming at yo boy. Lol

You have made good points delineating the high and stickiness of Inflation while consumer spending remains strong.

So I ask , why did Powell and the rest of the speakers at the Fed signal future easing in Monetary Policy in recent weeks?

Good question. The landing would appear to be super soft. $34 trillion debt no longer a problem. If government can spend so can we.

Core PCE has come down a lot. The six-month average core PCE is at 1.9% annualized, BELOW the Fed’s target. It’s nearly impossible to defend 5.5% policy rates with 6-month core PCE at that rate.

So we look at the details, and we know that there are inflationary pressures underneath and that some lucky things came together and that core PCE will likely not stay that low for long. But that’s where it is now and has been for the past 6 months. So the Fed is starting to talk about cutting rates, and if the expected bad things happen and core PCE jumps again, they can delay the rate cuts.

The Fed is talking 3 cuts in the second half. So that gives them 6+ months to see the results, and if core PCE is still at 2%, they should cut rates, but if core PCE is starting to surge again (which I think it will, and which I suspect they suspect it will), they can move the dot-plot cuts out further before they cut rates in the second half.

“if core PCE is still at 2%, they should cut rates”

Why? If PCE has proven stable for that long, a year by then, why mess with it?

I’ve been mostly on board with the pace of tightening, maybe wish they’d not paused earlier once or twice. To me, the Fed always has a dovish bias, and I never believed them when they said rates would stay at zero for years (was it 3 or 4 years they’d said?). Therefore, I expect the Fed to ease sooner than you do and even in higher inflationary conditions (e.g., PCE rises a few 10ths to mid 2s rather than falls/stays flat).

I agree with you Gatto. There is no reason to cut unless we are in a recession. Especially with the loss of purchasing power over the past three years that never should have happened in things like housing, insurance, etc. The obsession with consumerism and everything wall street in this country is sickening. It’s over the top. We never should have become a consumer based economy. It will eventually catch up with us.

So retirees and savers get to pay less income tax.

Sometime soon and i mean soon all this debt will come crashing down; CRE,CMBS,housing, CC debt and a global melt down from all this over spending. Forgot about the soft landing and recession BLAH,BLAH, BLAH we’re headed for much bigger issues. A global reset is more in order. Hard to believe I’m an optimist, but I am. Just watching ……….

You’re no optimist. You’re just one of hundreds of negative nabobs on this site who have predicted 35 of the last two recessions.

Funny part is that you’ll eventually be right when a recession inevitably comes and you’ll tell everyone that you called it.

Amen to that! So many bears on this blog. Wolf posts amazing content, but one of my favorite things to do is read the comments just for the fun of it/to check the sentiment. When people are super happy that the market is crashing like they were over the summer/throughout 2022, it’s my favorite time to buy stocks.

Matt,

So by your theory, now would be the best time to sell stocks?

Well you seem to have a handle on something JD, not sure what it opens, but Robert frank walker says were in debt, meaning we owe a lot of money and I agree it’s best to be cautious.

Hope that settles it.

He’s not talking about being cautious. He’s talking about a global reset and humans moving back into caves. This level of negativity and pessimism is bad for any person and inevitably leads to them being alone (as they alienate everyone around them). I’ve seen it many times.

Bidenomics in action. Consumers complain about rising prices, but when they are unhappy, they spend more, and the added income certainly helps.

The shift in the composition of the money stock, more transaction accounts relative to gated deposits, has propelled the economy so far.

Maybe the consumer/earner/saver should always have a fair return on their money to keep the economy growing.

Suppressed rates may actually have the opposite effect than the notions promoted by “economists”. Suppressed rates certainly contain negative impacts ……such as subsidizing debt creation and stealing wealth from savers and earners.

Those who pay the drunken sailors are struggling : the gov piled up

$34T debt, businesses which lead the corp profit are under attack and

tenants are struggling to pay the high rent. To cut cost both gov and

businesses might start laying off. The unemployed cannot pay rent, medical bills and debt.

If Corporate Profits are under attack, someone forgot to tell FRED:

https://fred.stlouisfed.org/series/A053RC1Q027SBEA

The data you linked includes the big losses of the Federal Reserve Banks. Here are corporate profits without the Federal Reserve Banks:

https://wolfstreet.com/2023/12/21/the-inflationary-aspects-of-corporate-profits-by-major-industry-with-charts-its-starting-all-over-again-good-lordy/

IMO going to the mall is going to end up like going to the movies.

Folks predicted the end of the movies when TV came in…..but they are still here.

Folks like to get out of the house and walk around…..and spend, spend spend. Costco yesterday was jammed.

As for the drunks……..an internet site Thursday proclaimed…..unemployment report jumps……so I looked at the report…….up from 207 to 209……continuing claims down. LOL.

Who writes this crap. Find something else to do for a living.

Someday they will write books about the roaring 2020’s……sort of like the roaring 20’s……and yes…..I do believe our debts will result in a 30’s……but that is a long time from now.

One has to wonder when AI is writing most of the articles and headlines whether it will be programmed to be clickbait. More than likely.

One has to wonder when the AIs will understand most people better than most people will understand themselves.

Never..

AI already understands what motivates people. People have long understood the same.

People are irrational which makes predictions difficult and will limit the usefulness of AI. Thankfully, it will allow us to overcome our future robot masters. ;)

Play a game with “great AI”, then play some people. You’ll quickly be bested by someone doing something you thought didn’t make sense.

Glen – one could wonder when listening to the existing analog reporting corps at a Fed presser if ‘artificial intelligence’ didn’t come ready-made…

…oh well, at some level, we’re ALL bozos on this bus, still giving it our all, aren’t we?

may we all find a better holiday season, New Year, and day…

fred flintstone

“IMO going to the mall is going to end up like going to the movies.

Folks predicted the end of the movies when TV came in…..but they are still here.”

You only see the surviving malls and surviving theaters. Countless malls have been closed, hundreds of retail chains from Sears on down were dismembered in bankruptcy court. Countless theaters have closed. AMC is losing a ton of money and is constantly issuing new shares to raise capital to pay for its losses, and it closed innumerable theaters to cut costs. And Regal’s owner, Cineworld, went bankrupt.

It’s naïve to assume that all malls and theaters would all vanish in one day; and that when they don’t all vanish in one day, but spread out over the years, to assume that there is no problem.

You can go straight to here and get the whole series of 7 years of the brick-and-mortar meltdown:

https://wolfstreet.com/tag/brick-and-mortar-meltdown/

Here are department store retail sales:

And here are ecommerce retail sales:

The pandemic accelerated many things related to the baby boomer demographic shift, from early retirements encouraging the eldest to become comfortable with online shopping. E-commerce has benefitted from new (old) customers they never expected. In the same way, brick and mortar has suffered.

Will we get enough new blood to create a soft landing when the next boomer shoe drops? Here’s hoping the Ponzi Scheme holds until Secure Act 2.0 adds millions more to 401K in Jan. 2025.

“…baby boomer demographic shift, from early retirements encouraging the eldest to become comfortable with online shopping.”

Boomers when they were young, invented ecommerce, back then with dialup, in the 1990s, maybe late 1980s. In 1990, a mid-boomer was 35, they were in the driver’s seat of the dotcom bubble, which created ecommerce as we know it today, with browsers and all, 🤣😍. Amazon’s founder Bezos is a boomer 😎. Yeah, those hated boomers did all that, and you just sat there as a toddler reaping the benefits?

You’re thinking about the prior generations that are in their late 70s to 100+ now.

…Sears’ mail-order catalog the prototype template existing pre-WWI. (…late-term management, like many, assumed their particular business model was the pinnacle of evolution, so didn’t consider, let alone see, that they had the future in their hands…).

may we all find a better day.

@Wolf

My comment wasn’t intended to minimize the baby boomers’ contribution. Quite the opposite, it was to remind anyone who had forgotten that a large demographic shift was expected and accelerated.

The baby boom is defined as those born between 1946 and 1964. That puts the median at 68 years in 2023.

As of 2021 67.6% of the population was over 60. That is expected to continue growing. More retirees pulling retirement funds from markets. More on social security. More on Medicare.

I’m looking for those smarter than me to figure out how that will play out and where Gen-X should shelter.

The tax man cometh.

Fred flintstone, Nope, not everybody likes to get out of the house and walk around and spend spend spend. Of course some movies and malls are still active, perhaps near where you live. However extrapolating that to the entire US is ridiculous. It is like saying, hey, my gall bladder is fine, so everybody’s gall bladder is fine, or hey, I am making a lot of money, so everybody is making a lot of money. It’s just stupid.

God Bless the Drunken sailors!

Mexico now projected by the IMF to have 12th largest economy in the world, up from 14th last year. Is this because we are bringing the factories back to North America and the free trade agreement(s)?

Canada not quite as drunken this year but still 10th and with a much smaller population.

We have quite an economic synergy in North America; labor, resources, and tech.

Took my tax selling shorts off. I think I learned that year end tax selling at most neutralizes bull markets. Works better in bear markets.

I still see angst about commercial debt but I doubt it will reach far into the drunken sailors this year.

Federal debt may be a problem eventually but not soon because the sailors are paying more than ever in taxes.

Be strong and long.

Thanks Wolf

Two letters might interrupt the dream.

QT

Hey Bobber,

QT and QE in addition to setting interest rates give the Fed enormous power over the economy. Add that to the fact that services make up 70% of the economy and are quite sticky and cyclical recessions (like the business cycle) become much easier to avoid (the longest bull market ever from the financial crisis to the pandemic) and another reason to be more confidently bullish most of the time.

Bears have fun roaring but they don’t make money.

I wish fed keeps the financial conditions as loose as possible as they have been doing for last 15 or so years.

I made a lot of money in last 15 not because I am smart but because of Fed.

I am sure wealth inequality would increase drastically over time like what we see for last 29 years but more.

Also working class would be suffering a lot because of loose fed policies.

I dream of a day when I can donate all my money and live like a pauper thus experiencing true liberation like I used to 25 years back.

But right now it game on and time to make money with feds blessings.

It took six years of ZIRP to sustain that bull run. The pre-pandemic economy was a dud on its own. If we are going back to that economy without ZIRP and much higher government debts, you need to be nimble in case Goldman Sachs flips the switch.

Jon

“I wish fed keeps the financial conditions as loose as possible as they have been doing for last 15 or so years.”

Well, I don’t. What exactly is your end game with your excessive greed? I’m serious. How much money do you need, especially fake wealth like that created over the past 15 plus years. We are spoiled little children in this country always demanding more. And the sad thing is most don’t deserve it. Like you admitted, much of your wealth has been created by the casino. Most of the permabears here are nothing but gamblers who brag about their wealth but really only attained it by the corruption on the part of our government and the Fed. It takes no talent to trade anymore. I pray the way this country operates with its excesses ends.

People are emigrating to Mexico because they get a huge rate of return on their money as interest rates are paying 11+ percent. Through the magic of compound interest everyone going there with money will be wealthy in no time flat.

But they don’t get 11% on USD or CAD in Mexico. They get 11% on pesos. Which is what has kept the peso strong against other currencies. The Bank of Mexico front-ran the Fed with rate hikes, and hiked big and fast to protect the peso. And it worked. Brazil did that too.

MJ – with all due respect, having had to evacuate our rural Sonoma County coastal neighborhood (a long way from I5) pre-’20 due to dry-lightning strike fires, and in other contemporary cases the result of decades of PG&E neglect of the rural electricity grid, your supposition may be correct in part, but not the whole. Your final sentence are words to do one’s best to live by. Best-

may we all find a better day.

Nice, interesting analysis. I am confused though. How can consumer spending be so high but the CPI/PCE is going down and PPI is near zero? Why aren’t manufacturers/sellers exerting their pricing power? Why is the only extremely elevated things are the asset prices?

Gasoline prices plunged from the spike because the US is the largest petroleum and petroleum products producer in the world and ramped up production when prices spiked, and because the US and many other countries released petroleum from their SPRs, and so supply overwhelmed the price spike and prices plunged, including of diesel, jet fuel, marine diesel, and bunker, which show up in the prices of all goods that get transported, which is all goods.

Durable goods prices spiked ridiculously during the pandemic due to shortages and transportation chaos. Used car prices for example spiked by about 60% in a little over a year, which is totally ridiculous. Now they’re coming off those ridiculous levels. Used car prices have dropped about 12% or so.

But services prices continue to surge.

You get all the dynamics here:

https://wolfstreet.com/2023/12/12/beneath-the-skin-of-cpi-inflation-november-core-services-inflation-accelerates-as-rent-cpi-glows-in-the-dark-insurance-spikes/

This chart of durable goods shows the price level of the index, not the percent change, and you can see the massive spike and the rather gentle decline:

So, a $30k used vehicle went up to $48k, which is totally insane, and now it’s down to $42,240 – still no bargain by any stretch of the imagination. Long way to go.

Correct. No one said prices are a bargain — they’re not — but they did fall. They gave up about 1/3 or the pandemic spike.

And there is no telling how much longer they will fall. There still isn’t a lot of used vehicle inventory out there, and I doubt they will give up another 1/3 of the pandemic spike. That just seems unlikely to me.

All the conclusions drawn from these charts assume CPI and PCE correctly estimate inflation. They don’t. They are intentionally rigged. Adjusted for real inflation, the charts merely show people are just continuing to spend as they always have.

Absolutely. I don’t give any credence to anything that comes out of the current administration.

People continue to spend because the job market is still tight, in spite of the rate hikes & QT that have happened so far.

I just had a thought. Ultimately, the 2% “inflation target” doesn’t mean much, because they’ll never aim to undershoot the target to make up for overshoots. So it’s really a 2% floor, with more for “emergencies,” however defined.

But that means, why are institutional investors jumping all over each other to buy 10 year treasuries at 3.8%? Sure, if inflation returns to 2%, that’s not a bad return, but it assumes no emergency over the next 10 years that necessitates absurd amounts of printing.

Institutions have to buy treasuries, no matter the yield. They receive a continuous stream of money that needs to be invested at current rates.

Why? They can always buy short term ones. Why do they have to buy 10 or 30 year treasuries?

They hold long-term liabilities, so they need to hold long-term assets for proper matching and risk mitigation. Think insurance liabilities and pension liabilities.

When the Fed monkeys with the long-end of the yield curve like it’s been doing, it creates havoc for these institutions that have to buy distorted paper. Long term financial instabilities result.

The thrill of victory vs the agony of defeat. It’s great to see the economic explanations in laymen’s terms, thank God for WolfStreet.com. Many are still standing on the seashore, avoiding taking the plunge in the new reality of change. Capital is made to be deployed, so many negative predictions in spite of massive ROI’s being recorded. Let the good times roll, it’s seems that there are those who are still wishing for the S&P to drop to 3500 levels, Jeremy Grantham cult followers hoping for USA economy meltdown for the future generations.

America corrupt you mean. Younger generations don’t want things the way they are. Many see through it and are repulsed by the excessiveness and greed and downright criminality in this country. Wall Street gets away with crimes no one else could.

You remind me of the people who flocked to the shore of California during the last tsunami warning.

Prior to the pandemic we had six years of ZIRP to keep the economy out of recession. During the pandemic we had $5T of money printing and 20% inflation to keep it going. What are we going to do now – keep the $2T deficits flowing? Maybe grow them to $3T? That will work only if the Fed buys the govt debt.

And this is exactly why so many of us are bleak about the economy and its future, even if we’re technically “making money” on our investments.

An economy that only works for the capital class is not sustainable.

” That will work only if the Fed buys the govt debt.”

That’s how the BOJ kicks the can.

If one looks at the M2 chart, the established trajectory of the money supply prior to the bulge would suggest there is still $4 Trillion too much in the system. And certainly, 5% short rates hasnt cooled the economy…….as noted ….. the consumer is on fire.

For now, it seems like there’s enough demand for treasuries in spite of the Fed no longer being a buyer.

But I can imagine future increased treasury issuance crowding out other investments. Every new bond issued is chasing the same $$ that stocks etc. are.

This is fundamentally my bearish thesis: I don’t think the economy is going to crash or anything – stocks/assets are just overvalued and not a great place to park one’s capital over the coming decade.

If the Fed kept QT going, stocks would drop 50% or more at some point. The question is – when does the Fed step in with QE to save the stock market? After a 0%, 20%, 40%, or 60% decline? The M2 money supply is 6x higher than it was prior to the Great Recession, and there is no reason for that except creation of an unfair illegitimate wealth effect.

It’s shameful that government has distorted asset markets for decades, such that stock investing now depends entirely on how much money is printed and when. Long-standing norms were discarded without discussion. Somewhere along the line, the societal framework tipped from capitalism (hard work, accountability, and sensible safety net) to monkey business and free money for all.

I’m all for a healthy safety net but not when it supports the entire economic spectrum including free-loading and overly speculative behaviors.

The 10 commandments of this economic system appear to be the following:

1. Thou shalt not have other Gods before the banking system.

2. Remember Cyber Monday. Keep it holy.

3. Honor speculation and indebtedness.

4. Thou shalt not save.

5. Thou shalt not bear false witness against the stock market.

6. Thou shalt not commit to hard work.

etc…….

Can anyone explain how and why gasoline prices plummeted?

Classic commodities spike that then unwinds, same with lumber, natural gas, lithium, and lots of others, some of which we have covered here. Commodities do that after a ridiculous spike. There was never any real reason for gasoline prices in the US to spike, there was never a shortage of any kind — the US is a huge producer and exporter of gasoline! Even California refineries are big exporters of gasoline, diesel, and jet fuel. It was all just hype and hoopla. So now the prices are returning back toward where they used to be. That’s what commodities prices do.

The narrative during the summer, here in AZ, is that gasoline in the Valley (PHX) is required to be the CA blend due to the poor air quality from the heat. Allegedly, the only place that does produce that blend are the CA refineries and one was – again, allegedly – down for maintenance. There is no “backup” source here as other refineries in TX and elsewhere don’t produce CA blends.

Remarkable with the turmoil in the Mideast, shipping routes threatened, and oi producers boasting of production cuts.

Will this administration refill the SPR? They should, IMO.

It is not widely reported, but the US is producing more oil than ever.

Unpopular opinion: the SPR is obsolete, and should be drained & abolished.

Its a holdout from before the USA was a net oil exporter, but is no longer relevant.

First the oilfields were NOT replenished to rig the price of oil lower. When they finally had to replenish them someone came up with the brilliant idea of buying oil from Venezuela to rig the price of oil lower. They also spread unfounded rumours of recession. This is an all out effort to push the inflation rate lower but in the real world it isn’t falling at all.

I am debt free except for a vehicle lease, on fixed income that includes SS that increases annually but is somewhat offset by medicare plan increases.

So far, able to enjoy life in the country but notice that my income is simply shrinking. Sure gas is down, but it’s not that big a factor for me. Insurance both home and auto is up, way up with zero claims made on either.

Then its daily stuff, first it was a pound of widgets went from weighing 16 ounces to 14 ounces at the same price, to now being 12 ounces at 30% higher price. Not all things, but enough so you begin to notice.

Guess I’m slipping into Curmudgeon Land here so will retire to the cave now.

I was just talking to a friend who retired at 62 and telling him that I thought he should go back to work while he still can since I think there is a good change he will run out of money due to inflation (he spends way more than he gets in Social Security every month). A (now only 12.0oz.) “pound” of Starbucks Coffee is $14.49 at most places today (but on sale for $6.19 at Safeway with the digital coupon). My sister texted this morning asked asked if we would bring a pie to Christmas dinner tomorrow and my wife told me she was going to go to Costco today to get a pie and I had to remind her that no sane person would ever try to go to the Redwood City Costco on Christmas Eve. P.S. I bought my first “new” car tires at the Redwood City Costco when it was a “Price Club” in the 80’s (after going years of getting free used tires behind the tire places and having friends in auto shop mount and balance them for me for free)…

Coffee has gone way up, but not as much as snack chips, soda, and ice cream. Interesting how companies have confidence to raise prices in these areas. They must believe demand is inelastic, and maybe it is, pitifully.

If you ever buy used tires, check the DOT date codes on the sidewall. A tire can *look* just fine but is toast due to age and heat. I tossed out a set of Michelin Pilot Sports that had 80% tread because they were 8 years old. Most legit tire stores won’t even touch a tire that is aged out – for repair, mounting or balancing.

ElK – very well-said, and goes double (even triple!) for moto tires…

may we all find a better day.

At every meeting Jerome Powell always states his concern for the needy, the poor, the have nots. His concern and awareness is noble, an award please.

I finally got to read Jan Hatzius’s Dec. 18th note, ‘The Great Disinflation’. Hatzius is Goldman’s chief economist and the first major economist (that I saw) to call that there would be no recession.

As far as investing goes Hatzius’s thesis sentence is: “The combination of solid growth, sharply declining inflation, easier monetary policy, and lower long-term rates is exceptionally friendly for risk asset markets, and both our equity and credit strategists have therefore upgraded their return forecasts materially.”

This is very much my view. I think the next decade for U.S. markets will be better than the one between the financial crisis and the pandemic and I don’t think the Fed will have any need to get anywhere near zirp.

Thomas Curtis-

Do you, or does Hatzius, prognosticate on the trajectory of systemic debt in the US (gov’t, corp., household, financial) over the next several years — say 3, 5, or 10 years?

I would think that projections on stock returns would be highly dependent on the progression of one’s guestimate of debt levels and issuance, and the resultant interest rates demanded by bond-buyers.

Thanks for your optimism.

John H, my view is that the current economy is unsustainable without multi-trillion government deficits, and that the sustainability of these government deficits depends on investors’ willingness to buy long-term paper at low rates.

I don’t think it’s a foregone conclusion either way that at some point, people (and especially foreigners) will stop wanting 10 year treasuries at 3-4% when we’re issuing $2 trillion new treasuries every year.

There is no organic “growth.” The “growth” is purely based on deficit spending, so that is the key factor.

Sentiment has turned decidedly bullish on bonds.

“Nearly 90% of respondents to Bank of America’s Global Fund Manager Survey anticipate lower short-term rates to come, with 62% believing that bond yields will fall further in the coming months, each representing record highs going back to the turn of the century. The share of money managers reporting an overweight position in fixed income now stands at its highest since 2008.” —from Almost Daily Grant’s, December 22, 2023.

The majority opinion of the crowd is looking for rates to come down in 2024. The crowd isn’t always wrong, except at market tops, when it is always wrong. (Admittedly, the top can only be confirmed from below!)

Gareth Soloway is one of the very best and he correctly said gold would go higher and the stock market will be sideways to down for the next decade non-inflation adjusted. See when the middle class has no money then the rich can only sell stocks to the other rich so there’s no bag holders. Therefore in a zero sum game the stock market can’t go higher only lower.

The sailors are drunk and partying hard, but with QT on autopilot the Fed threatens to reduce its pour at some point.

In my view, the Fed’s next move in the QE/QT area will reveal its true intentions. If QT is ended near current asset price levels, preservation of overly-inflated asset prices would take pole position, not long-term health of the real economy. In that case, expect mega-inflation in years ahead until the Fed loses complete control.

If past is prologue….

I don’t need to see anything else at this point to know that high asset prices – “the wealth effect” – is in pole position, and is the main goal. They have both shown us and told us.

As for rampant consumption, there is this notion that if people feel prices will continue to be going higher, it is smart to buy all the stuff they will need now, especially durable goods. It’s a third world mindset, but may apply to the US now.

“This time is different” are typically famous last words. An inverted yield curve and multiple asset bubbles I’m sure we’ll nail the soft landing. But then again maybe it will be different.

The last time the yield curve inverted, we didn’t get a business-cycle recession either. It inverted in March 2019 and uninverted in Oct 2019. And there was no recession. What we got in March 2020 was a pandemic and a lockdown, not a business cycle recession. The yield curve isn’t supposed to predict pandemics and lockdowns, but business cycle recessions. So it failed then. And it might fail now. So “this time may be the same” as in 2019, not “different.”

Isn’t there typically a lag between yield curve inversion and recession. I have to wonder if we would have gotten a business cycle recession in late 2020 if COVID hadn’t happened. I agree though economic numbers are not currently pointing to a recession and people still seem to be spending. However, there’s a lot of CRE maturities coming due in 2024, student loan payments will take a bit to hit the economy, construction has slowed significantly outside of government funded projects, continued QT – so I still feel 50/50 on the recession. Everytime I finally believe this time is different tends be when everything tanks and I get screwed.

Inverted yield curves have lost their predictive power because recessions are no longer a necessary condition for the Federal Reserve to cut interest rates.

DM: US economist makes chilling prediction for 2024 – warning of ‘biggest crash in our lifetimes’ as ‘everything bubble bursts’

Harry Dent claims the effects of his 2024 predicted market crash will ‘be obvious’ and will slow the

Hey SoCalBearchDue,.

Your 4:29pm post ended rather abruptly…you OK?

Wolf, I think I need a new username on this website. My thesis appears to have been disproven solidly, as evidenced in this article. I’m shocked and in disbelief, but facts are facts.

Wolf, it’d be a nice feature for your site if you tacked a “monthly % to annualized %” conversion chart onto the sidebar. And maybe one for quarterly %s.

I frequently find myself doing this in Excel while reading these articles. It’s a simple calculation but a little inconvenient to need to tab over to another program for it.

I understand what you mean in terms of the inconvenience of converting month-to-month changes into annualized rates. I do that for the inflation data and for some other things where I have raw index values, and you see those annualized rates mentioned in the articles.

But here, all the dollar-data in the consumer spending spectrum are already seasonally adjusted annual rates, and if adjusted for inflation, they’re expressed in 2017 dollars. So the percentage changes are based on these seasonally adjusted annual rates in 2017 dollars. So I don’t think it’s conceptually a good idea to annualize these percentage changes of already annualized data.

However, the levels in dollars, their three-month moving averages (shown in the charts), month-to-month changes and their three-month moving averages, and the year-over-year changes of this annualized data work out pretty well when they’re used in combination. That’s my compromise.

Annualized rates exaggerate volatile month-to-month movements, such as the sudden stimulus payments that happened in one month, but the annualized rates assumed that they would happen every month for 12 months, and so you see the huge spikes in annualized disposable income in early 2021 that in reality was only about 1/12th that size. And then a year later, in the year-over-year comparisons, you see that huge collapse in income (annualized) that didn’t take place either. Dollar amounts expressed in annualized rates are a very mixed blessing, and I have railed against them a few times. So I don’t really want to do charts of annualized percentage changes of already annualized dollar figures.

The formula for annualizing from one month is sort of simple:

((1 + R)^12)-1. If R is .22 percent then that is .22/100 which is .0022. Add 1 to get 1.0022. Take that number to the twelfth power. This is 1.02672. Subtract one to get .02672. Multiply by 100 to get percent, which is 2.672%. Maybe not so simple. You could also get an approximation by simply multiplying .22 times 12 which is 2.640%. Not much different.

Wolf, is it possible that consumer spending is being pulled forward by (hidden) expectations of inflation? As in, if this item is going to cost more tomorrow, I should buy it today?