Inflation is like so not defeated? Jacking up prices faster than costs are rising creates stunning profits. Strong demand sees to it that companies can do it.

By Wolf Richter for WOLF STREET.

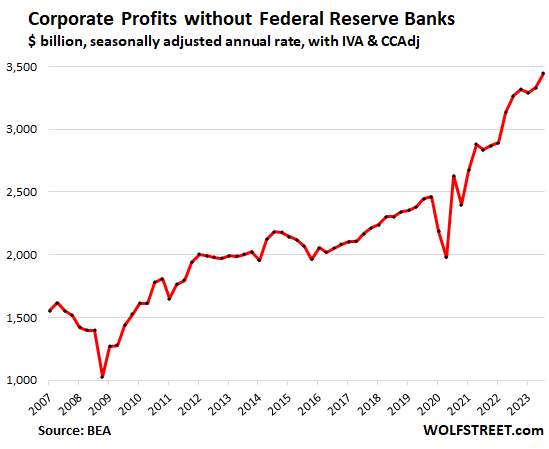

Overall corporate pre-tax profits (excluding the Federal Reserve Banks), jumped by 3.4% in Q3 from Q2, and by 5.5% year-over-year, to a record seasonally adjusted annual rate of $3.45 trillion, fueled by profit spikes in a number of industries whose figures the Bureau of Economic Analysis released today, and we’ll get to them in a moment.

The BEA’s measure of “corporate profits” broadly track profits from current production by all businesses that have to file corporate tax returns, including LLCs and S corporations, plus some organizations that do not file corporate tax returns. It’s based on income tax data from the IRS and on financial statement data filed with the SEC.

During the surge of inflation in 2021 and 2022, price increases were outstripping cost increases by extraordinary margins, hence the spike in profits. Then there was a lull in Q1 and Q2 this year, and now it’s starting all over again:

The inflation aspects.

Surging profitability during a period of big inflation is a sign that companies have leveraged inflation to their advantage, hiking prices much faster than their costs went up, and thereby doing their part in fueling inflationary momentum. And they’re able to do it because their customers are willing to pay those whatever-prices.

Interestingly, the surging labor costs have so far not made a dent into these profit spikes, and they might not if companies can continue to jack up their prices faster than their costs go up, including labor costs, which is precisely how inflation is nurtured and propagated.

First some definitions.

IVA: The “inventory valuation adjustment” removes “profits” derived from inventory cost changes. Profits from inventory are more like a capital-gain than profits from current production.

CCAdj: The “capital consumption adjustment” converts the tax-return measures of depreciation (based on historical-cost accounting) to measures of consumption of fixed capital, based on current cost with consistent service lives and with empirically based depreciation schedules.

Capital gains & dividends received are excluded to show business profits from current production, rather than financial gains.

Profits by industry.

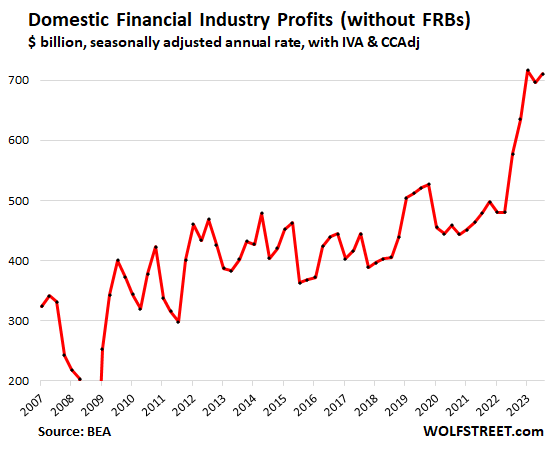

Profits by financial domestic Industries rose by 2.0% in Q3 from Q2, to a seasonally adjusted annual rate of $710 billion, the second highest behind the record in Q1, and was up by 23% year-over-year.

These are domestic profits by all financial companies except the Federal Reserve Banks (FRBs): banks and bank holding companies, other credit intermediation and related activities; securities, commodity contracts, and other financial investments and related activities; insurance carriers and related activities; and funds, trusts, and other financial vehicles.

Their customers are paying for those profits by paying higher prices, fees, insurance premiums, etc., which contribute to the still hot inflation in services.

Profits in durable-goods manufacturing spiked by 7.8% in Q3 from Q2, and by 18.5% year-over-year to a record seasonally adjusted annual rate of $400 billion. This amounts to a 100% spike in profits from just before the pandemic.

These industries produce computers, electronics, motor vehicles, trailers, machinery, fabricated metals, electrical equipment, appliances, components, and other durable goods.

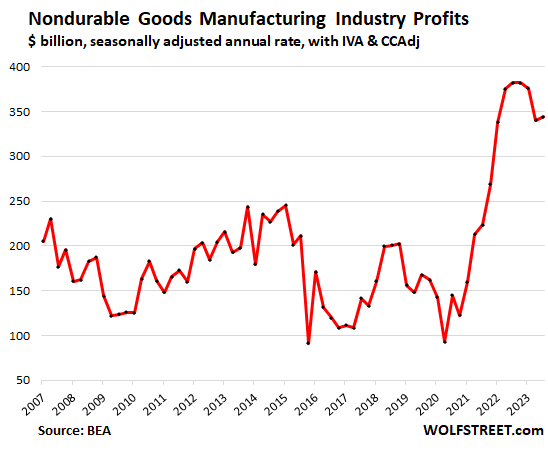

Profits in nondurable-goods manufacturing rose by 1.1% in Q3 from Q2, to a seasonally adjusted annual rate of $344 billion, after having dropped in the prior two quarters. Compared to a year ago, profits were down by 10%.

These industries produce food, beverages, and tobacco products; petroleum products (including gasoline and diesel), coal products; chemical products; and other nondurable goods.

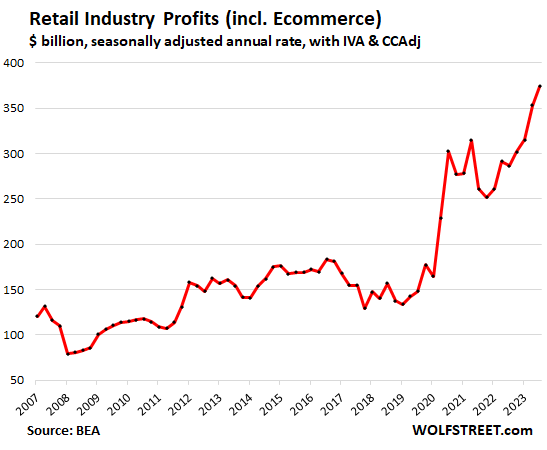

Profits in the retail trade, incl. Ecommerce, spiked by 5.9% in Q3 from Q2 and by 30.6% year over year, to a seasonally adjusted annual rate of $374 billion.

Inflation is a wonderful profit-generator when demand is so strong and customers so befuddled with the inflationary mindset that companies can raise their prices much faster than their costs go up.

And our drunken sailors, as we have called them facetiously and lovingly all year, are eagerly playing along, splurging and dropping money left and right, armed with per-capita disposable incomes that have outpaced inflation by a wide margin this year:

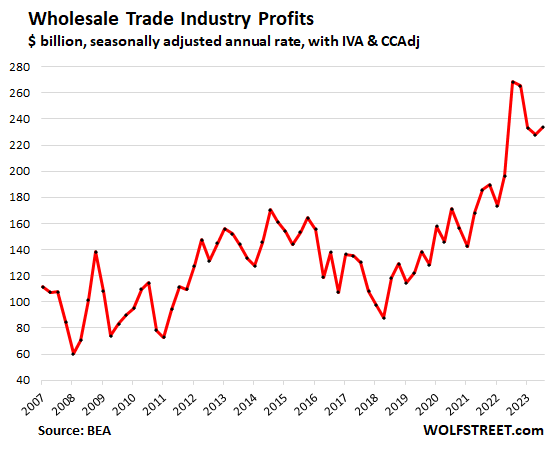

Profits in wholesale trade rose by 2.3% in Q3 from Q2, to a seasonally adjusted annual rate of $233 billion, the first increase after three quarters of declines. Compared to a year ago, profits were down by 13%:

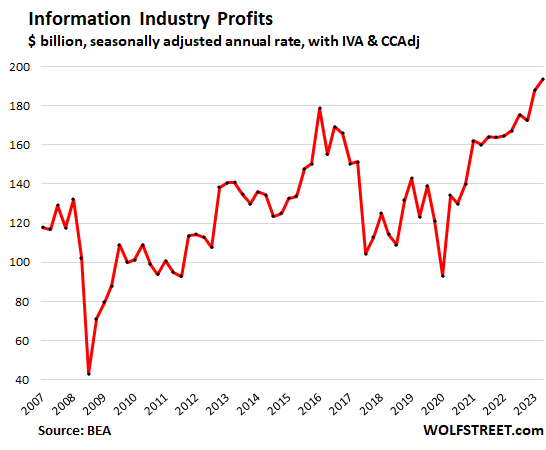

Profits in information spiked by 3.0% in Q3 from Q2, and by 15.7% year-over-year, to a record seasonally adjusted annual rate of $193 billion. The layoffs in this industry in 2022 and early 2023 likely helped bring costs down and boost profits.

Information is a relatively small sector with only about 3 million employees, so compared to its small size, it’s hugely profitable. It includes web search portals, data processing, data transmission, information services, software publishing, motion picture and sound recording, broadcasting including over the Internet, and telecommunications. Some of the tech and social media companies are in this sector.

Profits in transportation & warehousing plunged by 8.1% in Q3 from the record in Q2, to a seasonally adjusted annual rate of $117 billion. Year-over-year, profits were up by 3.6%.

![]()

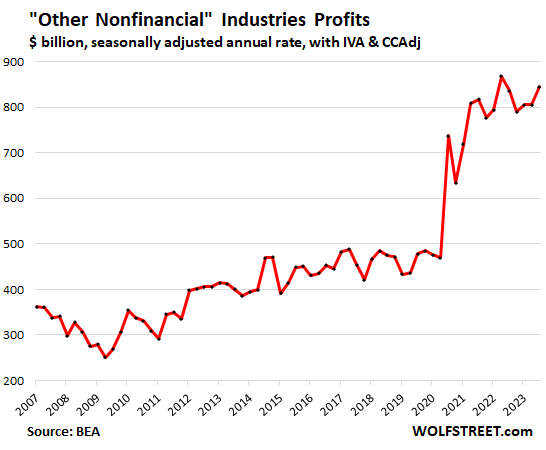

Profits in the huge category of “other nonfinancial” industries jumped by 4.8% in Q3 from Q2, to a seasonally adjusted annual rate of $845 billion. Year-over-year, profits were up by 1.0%. But they’re still below the record of Q2 2022.

Includes mining; construction; real estate and rental and leasing; professional, scientific, and technical services (where some of the tech and social media companies are); administrative and waste management services; educational services; health care and social assistance; arts, entertainment, and recreation; accommodation and food services; agriculture, forestry, fishing, and hunting; and other services, except government.

This category is responsible for inflation in healthcare, concert tickets and other entertainment, lodging, eating out, construction, etc. And after the lull, it’s starting all over again:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The consumer will not go on strike!

In a society which you are pretty bombarded non-stop with message of consumption, keeping up with the jones or shop like a billionaire as Temu’s favorite tagline…majority of consumers will only go on strike if they are absolutely force to and even then some will still live beyond their means to look fab on the gram….

the CONSUMER has no choice but to go on strike

when PAYCHECK doesn’t = enough to live on

Wait, don’t forget ‘Buy now pay later’.

Hey, there is always the savings account, and don’t forget that “available credit” on the CCs. Maybe get a few new ones just in case! There is always a HELOC, to “consolidate” the CCs, so plenty of “disposable” cash to spend!! Can’t wait to get a robot lawn mower, the neighbors will be so knocked out!! Yippee!!

Oh, wait….my CCs are maxed and the rates are impossible. My savings are gone, and my house has dropped in value so my first two mortgages put me underwater…can’t sell now…. what WILL I DO? The trinkets on Temu and Amazon are calling me!!!

Sorry, just my poor stab at sarcasm. I’ll go back to my corner.

Now that Wal-Mart has that buy now pay later option, why not trot by and pick up those impulse items? That would fit into the time preference model. :(

And how about Uncle Sam’s 35% deficit spending ($1.7T def/$4.7 rev)?

They’re the biggest drunken sailor of them all.

I just don’t see a recession in the cars with this type of spending.

I believe that CONgress/potus/spotus/fed all should be PERSONALLY responsible for all govt debt along with heirs

make sure to bankrupt them 1st

This is JPow:

I’d like to differ from you. We have already declared victory and have many rate cuts planned for 2024.

That wasn’t the message. The message was that some members see this diminishing and this making it acceptable to reduce rates.

The final decision will be based on the data that comes in between now and then.

Of course, that isn’t what the market heard.

I think these dot-plots are a bad idea. The market is so focused on getting ahead of the curve that they end up changing the very curve they’re trying to front-run.

If you look at the FED policies for last 15 or so years then you’d get the message loud and clear.

Some people even think that fEd has full control of economy and they’d never let recession happen and thus green light for stock to go full speed ahead.

Infact we didn’t have meaning ful recession in last 15 years gfc.

People think many things, the data Wolf puts out in his articles seems to suggest that at the very least cuts may be delayed past projected dates just as in 2023 when cuts not only didn’t happen but we got a higher rate than projected. If there is too much money in the system it might not be so bad for some of it’s holders to blow it on these bets. 2001 and 2008 were a very long time ago and maybe people think “this time it’s different” because central bankers have all the “tools” to just keep pumping markets.. we’ll see, if that’s the case who needs markets, just go all in and make bankers “ministers of industry” and give them the power to command entire economies. /S

The Fed policies prevented the GFC from becoming the Great Depression 2.0 and a major crash from the pandemic.

I’ve said several times that they could have done better but that’s only with the full benefit of hind-sight.

Outside of the FFR, the market is bigger than the Fed and the market controls interest rates.

$1 trillion of PPP (aka corporate welfare) forgiven, tax free, still working through the system.

Yep. This filthy shit is roaring through the system.

1% have been vacuuming it up

other 9% have plenty and trying to figure out were to put it

personally I don’t want cash/savings and will NOT put dime into anything wally street, stock market, insurance, bankster products

it’s

REAL ASSETS I can kick tires or ???

It’s been 3 1/2 years. That money is long gone.

No it’s not. PPP money give away, not the couple months of unemployment checks to stay at home money. Business owner buys property, assets go up, leverage, sell, bother other things with profits…………..it goes on. People got tens of thousands handed to them for free, many had millions handed to them for nothing. That money may have been shifted and spent in many ways but it holds more weight than people’s savings accounts. How can you increase the money supply that much and think your 2010 money is still worth much compared to 2020 PPP and Inflation Acceleration Act money?

Forgiveness is done by tranches. One construction company I know got $1.3 million, employs about 25 workers. Last tranche forgiven this summer. Owner put all the money on real estate.

If you win the lottery you have to pay taxes but government can raid public treasury and forgive it tax free to the wealthiest 1%, this is beyond obscene.

I personally know of similar scenarios to what you described. That’s just construction contractors. Imagine what white-collar criminals were able to pull off and look like geniuses for doing so.

The purpose of the lockdowns was to mitigate the velocity of that money at the peon level.

The application period runs through April ’24, I believe or there abouts. Danielle D Booth follows this stuff closely and said that this past summer is when the PPP really started to slow down. I know in the spring there were some months that close to $30B was doled out. Where it’s at nowadays is a little hard to track, but it’s not over put rather winding down slowly for 3-4 more quarters.

“The application period runs through April ’24”

Nonsense. PPP ended May 31, 2021. No applications accepted after that. Google it! This baby has been dead for nearly 3 years.

Applying for loan forgiveness — to have an existing loan forgiven — extends through the maturity of the loan.

Your number that is “working through the system” seems a bit low. if one includes all the helicopter money to consumers and direct cash injection to select corps, i.e., 50 billion to airlines alone, I’m pretty sure the aggregate number is 4 trillion that had/has to work through the system. Correct me if I’m wrong please.

And yet you thought all of the pauses were a good idea. Why again?

Yep. I’ve heard many people say “Ehh, yeah, it’s overpriced but prices have gone up everywhere.”

Truly means the inflation mindset has set in, and it won’t be broken without a recession.

The Fed’s refusal to tolerate one means that inflation is a permanent feature.

We get what we allow. I hear the sentiment frequently from people that it’s ok their service companies like cable, Software, auto, etc.. screw them because “they all do it”.

Sadly, it’s not enough for 1, 10, 50, or even 5000 people to say stop. There are too many people in the world now and the passive masses are making corporations ever more profitable and sleazy.

Expect less in the future.

@DC: My sense is that the people who think the pauses are a good idea are people who made some quick money over the last few years and are desperately seeking to hold on to it.

That’s not going to happen because inflation is going to rear up again and give some sharp slaps to Powell and the rest of the FOMC.

If we look at it at a 30k-foot level, the demand for everything got pulled into a very tight time-frame during Covid. Common sense dictates that all of this needs to be digested before the economy can perform at a sustainable level. You can’t have a party this size without a horrible hangover. And a doozy hangover is what we are going to have.

Whatever the media and wall street pundits are babbling all over the place is just plain noise.

This fed is a sneaky critter. It always seems to find a way to get more credit into this system. This system is beginning to figure this out and it’s pricing in the ‘closet surpluses’ in credit before Joe Schmo realizes what is even happening. All in my humble worthless opinion.

The FED does a lot of things backwards.

Let’s not forget the buy now, pay later crowd/trends. These alternative consumer finance credit companies are everywhere now (e.g., Affirm). In fact, I read an article recently that consumers can select this payment option now at thousands of self check out systems across the country (at the largest retailers), even for basic necessity items. Nothing like greasing the consumer with perceived easy/cheap credit to keep them spending.

Sure, but BNPL is included in our consumer credit data that we report here quarterly — it’s part of the green line in the first two charts below, which also includes personal loans, payday loans, etc. The actual BNPL amounts are relatively small because these loans typically have to be paid off in 4 or 5 weeks, and they’re interest-free, so they don’t really accumulate, unlike credit cards. And as soon as you default on one such a 4 or 5-week loan, you cannot get another one.

Note that credit cards are the universal payment method in the US, paying for about $6 trillion worth of goods and services in 2023, including by reimbursed expense accounts, for things like corporate travels. The balances are statement balances at month-end, and most are paid off by due date and never accrue interest.

And increase in credit card balances means an increase in spending, not an increase in interest-bearing debt. For more details, read this article:

https://wolfstreet.com/2023/11/09/credit-cards-the-big-payment-method-balances-burden-delinquencies-available-credit-how-are-our-drunken-sailors-holding-up/

My conjecture is that the FED is inevitably playing a game (especially in light of what happened after their December meeting) to make sure that your last graph (on credit) stabilizes at the green line. Inflation or not.

My apologies Wolf as I was actually trying to layer in some sarcasm involving consumers and their use of credit to maintain lifestyles. Your charts are very helpful and confirm two points. First, delinquency rates are back to normalized levels for the past 10+/- years. That I agree. However, the more interesting information is the direction of the charts which are all heading up/North, and rather quickly. Higher credit card balances, higher delinquency rates, and higher balances as a % of disposal income.

The question is, will these trends begin to decelerate and moderate or will the trends continue their upward climb at accelerated rates? Based on your charts, the last two years has seen a rapid return to what might be considered normal (at least since 2010) so I’m wondering if a leveling off should be expected as if not, and the trend lines continue at these rates, by 2025 it will be “Houston, we have a problem”.

BTW, your comment on there being no interest expense/charges to the consumer is correct, but only from the perspective of the consumer. If they paid $100 for an item and pay the purchase off in four equal installments of $25 (not uncommon terms for a BNPL credit company), the consumer is not hit with any interest charges (at least on paper). The merchant, on the other hand, will have to absorb added fees (similar to credit card fees that can easily range from 2 to 3% of every purchase) which are paid to the BNPL credit company. For the merchant, its an added and accepted cost of doing business as the benefit of driving the sale far outweighs paying an additional fee of let’s say $3 to $5 on a $100 purchase. But make no mistake, merchants will account for this fee and recoup it via pricing and promotional strategies which most consumers have no idea occur behind the scenes.

Down the road, it will be interesting to see how the BNPL credit companies fair when a reasonable level of defaults hit them (from consumers not being able to pay). As Wolf has previously pointed out, catering to the subprime market can be very profitable, until its not. I suspect the same logic will hold for the BNPL credit companies that push the limit on approving credit to marginal consumers.

Re: interest free for BNPL. I have a chase visa card and just received a mailing indicating their program, although interest free, it does carry a fee of 1.73%. A distinction without a difference. Has anyone else seen this?

I received the mailing. 1.73 percent per month. They don’t want to call it interest any more.

From my post above about PPP. My bad. I’m talking about the Employee Retention Credit. I think a lot of people get this confused. Sorry about that.

The IRS is now going after people for ERC fraud!!! It halted applications in Sept. It’s pretty easy to prove fraud in these cases, apparently.

The ERC applies to wages paid between March 13, 2020, through December 31, 2021. So the applications after that were after the fact, for amended tax returns with wages paid through Dec 2021. It does NOT apply to wages paid after Dec 2021.

On my little corner of the internet, we have Affirm at checkout. Very few customers use it – I’d guestimate 2-4% of orders are paid via Affirm. And its always small dollar orders. Most orders are paid with a CC.

We do get a signficant number of orders paid for via the “Pay with Paypal” button, which could have been paid for with Paypal’s “Pay in Four” financing. Paypal doesn’t tell the retailer how the customer paid (part of the point).

Affirm’s merchant fees aren’t that much higher than Paypal’s, both of which are significantly higher than CC fees (except Amex). And Affirm does the customer verification for us (also like Paypal) so we know its not fraud.

Is there much of a premium for Amex anymore? Back in the day we paid a 3.72% discount for Amex transactions. These days Stripe is charging 2.9% + 0.30 for all cards including Amex, and my experience is that other processors are moving in the same direction.

This will push back on rate cuts.

Rick Rieder of Black Rock on ‘Wall Street Week’ (found on YouTube) argued that recessions are now only caused by by exogenous events now, like the pandemic and the financial crisis. For one thing he said that services are very sticky and that about 70% of the U.S. economy is services and that in the last 100 years we have only had 13 quarters of negative services growth.

I take that to mean that the Fed now is able to pretty eell control the ‘business cycle’. That is huge to me if true!

I note that from the financial crisis to the pandemic there were no recessions for a very long period. I also note the Fed seems likely to bring us in for a soft landing even if inflation ratchets up and they raise rates a little.

Today’s corp profit numbers and Reiders thoughts, AI, employment, and a number of other factors continue to push the equity bull case though I think we will have a bit of correction into the new year.

In January, asset.managers begin to make new bets in the market which sectors they need to put in for the next 12.months; no recession and GDP growth has been high (yes, including this Q4 is projected at around 3%see Atlanta FED GDP tracker). The answer is cyclicals and small caps (away from Magnificent 7), which do well in such high growth environments (comared to the low growth environment of prepandemic erra, before 2020). The indices will go up not down the first two months of 2024. I have a good bet on it.

Better hedge

Thomas Curtis-

Can’t tell if your pressing the Sarcasm key when you made the following statement:

“I take that to mean that the Fed now is able to pretty eell control the ‘business cycle’. That is huge to me if true!”

That line of thinking strikes me as far-fetched, and reminiscent of a parallel line of thinking from a “reputable” (but dead-wrong) source when the Fed was created:

“ It [the Fed] supplies a circulating medium absolutely safe….under the operation of this law such financial and commercial crises, or ‘panics,’ as this country experienced in 1873 or 1893, and again in 1907, with their attendant misfortunes and prostrations, seem to be mathematically impossible.”

The latter quote was, at best, misguided, and at worst delusional.

Maybe you were pointing out the doubtful nature of perpetual prosperity, and I misunderstood your viewpoint. If not, I sincerely wish you luck at investing in the perpetual motion machine.

John H.,

Go listen to what Rieder said and then comment on what you heard. It was extraordinary what I think I heard and I don’t ignore evidence around me.

Reider is a sharp cookie, we are pulling off an almost unheard of soft landing and until the pandemic the fed led us through a 10 year plus expansion.

I have never seen a better set up for equity bulls long term.

I thank you for sincerely wishing me luck in investing.

Thomas Curtis-

I’m not finding the Wall Street Week clip, but Rieder’s viewpoint is not my issue with your post.

My comment simply questions your assertion that the Fed can “control the ‘business cycles.”

If that were true, The US would not have experienced recessions in 1948, ‘53, ‘57, ‘60, ‘69, ‘73, ‘79, ‘81, ‘90, ‘01, ‘08, ‘20, and, some would say 2022. Add the 1921 post WWI commodity-led depression, the Great Depression of the 1930’s, many bouts of unemployment, the inflation of the 1970’s, a century of purchasing power erosion, and today’s 35 trillion federal debt, and it sure doesn’t appear to be a Fed “in control of ‘business cycles.’ If it IS in control, it should be fired for malfeasance.

I am sincere about the well-wishes on your portfolio trading, though. You sound like you stay flexible and alert.

Cheers.

PS- might Rick Rieder be talking his significant bond ETF book, do you think? He’s entitled to market himself and company, but may have strong biases…about 3 trillion of them.

John H.

Tried to send the link but the filter would not pass it.

Search YouTube or Google videos for ‘Wall Street Week 12/15/2023’.

He and David discuss a number of things but at 32:00 the conversation about recessions and cycles begins.

Reider said, “I really think the U.S. economy doesn’t go into recession except for pandemic, financial crisis, unless there is some big exogenous shock…” and he keeps going explaining this in terms of services being so sticky. Later he says, “I just don’t think cycles are like they were…” and keeps elaborating.

Take a listen if you can find it. His thoughts seem reasonable and do explain a lot.

“Tried to send the link but the filter would not pass it.”

Your comment with the link is way down toward the bottom of the comments because you posted it as a new comment, not in reply to anyone. So scroll nearly all the way down, and you’ll see it.

Thomas Curtis-

If his “soft landing” prediction transpires, then for a period he could be on the mark. But it strikes me as a Goldilocks balance that will not endure.

I think its odd that he did not mention the huge corporate and government bond financings that will occur in the short and intermediate timeframes.

As I listened, I heard distinct echos of bond fund wholesaler presentations (from a period in the ‘80’s and ‘90’s when I lived in that world) describing “better research,” “bigger scale,” “superior macro analysis,” “more effective trading” as mostly unprovable reasons to park the 40% of one’s portfolio NOT dedicated to equities in their product.

These presentations became significantly more numerous (in hindsight) before bond market catastrophes. Similarly, Rieder is coming to market with a 3rd fund…

I know I’m not being very scientific, but neither was Rieder’s presentation, in my opinion. (I hear myself sounding pretty old and cynical, but bond funds made me that way!)

Thanks for getting this link to me.

^^

This is what delusion looks like.

Yes but it worked well for last 15 years or so

The wall street firmly believes the fed has their back.

Tc along with many believe that Fed controls the economy via money printing and cone what may ..may not let recession happen .

The only price to be paid by common people is inflation which can be easily manipulated.

Even wr latest article says overall core inflation is down

Einhal,

You are an economic idiot.

No, I am more an economic realist. There is no something for nothing. The Fed did not

I don’t know why it hit “post.”

The Fed did not lead us on a ten year expansion by creating wealth. All they did was stole money from 80 year old retirees with $200k in savings. They didn’t create new wealth, they just stole it from some parties to give to another.

They also didn’t lead us to a soft landing. A landing that means 40% cumulative inflation over 6 years is not a soft landing.

I can see you’re a kool-aid drinker, where you think the Fed is some magic entity that can make something out of nothing. It can’t (other than dollars of course).

All it can do is forcibly appropriate from one person to give to another.

“All it can do is forcibly appropriate from one person to give to another.”

Einhal, this sounds like the Treasury, not the Fed — fiscal policy rather than monetary.

I know you don’t consider aggregate credit card debt to be an accurate measure of consumer resilience. Credit card delinquency rate is up but only slightly (newly delinquent card holders in 2019 were 1.5%, 2% in 1st Qtr 2023 *)

Do you consider CC delinquency rate to be a good gauge of health of our

consumer economy, or perhaps another metric?

For credit card delinquency rates from the NY Fed, see my comment above, middle chart. They’re back to the good-times normal. It’s just not a factor. Nearly all the delinquencies are in subprime, and subprime is nearly always in trouble (except when people got the free money), which is why it’s subprime. But that’s a small part of consumer spending.

Print more money and this is what happens. Prices go up, profits go up, wages go up, stock markets go up, home prices go up. It all goes up as purchasing power goes down.

Money didn’t go up assets did money gets devalued. Common sense,they can print until no one buys bonds. Then will just go full digital in next crisis

Flea knows the formula

And the end result of all of this is we end up with a great deal more unhoused persons.

Up 12% in the last year if the braindead click bait is to be believed.

700k and counting nationwide give or take.

You are right. Currently, the Fed pays over $750 million in interest every day to banks, hedge funds and other large financial institutions that have parked $5.7 trillion in its vaults. A year ago, that daily interest payment was only $18 million. The interest payments are adding three-quarters of a billion dollars to the money supply daily, working at cross purposes to the Fed’s higher interest rates, meaning higher rates would be needed to stop inflation snowballing. Fed has no exit strategy. If it stops paying interest on reserves and running massive reverse repo operations, it will immediately add $5.7 trillion of liquidity to the market – about 25% of the entire money supply. The extra liquidity would unleash an inflationary tsunami

1. “…the Fed pays over $750 million in interest every day to banks, hedge funds and other large financial institutions that have parked $5.7 trillion in its vaults.”

Just to update your figures. The total has dropped due to QT: So $3.54 trillion in reserves plus $778 billion in RRPs = $4.32 trillion (not $5.7 trillion) at about 5.4% translates roughly into $640 million a day.

2. “If it stops paying interest on reserves and running massive reverse repo operations, it will immediately add

$5.7[$4.32] trillion of liquidity to the market…”That’s a BS hypothetical statement. The Fed has 5 policy rates, including 1 for reserves and 1 for RRPs. Why the hell would the Fed suddenly cut those two rates to 0%, and leave the others at 5.5%? The Fed moves them up and down together.

So.much free credit man, which be financed at higher rates than prepandemic (remember the 0% cheap credit the magnificent 7 used to get free money to fund their growth? Now these companies use their own money to do so, no more free or cheap loans. The game is on, let’s see the survival of the fitest, rates will go down but they will still be in the 4% in the next two years.

So $640 million per day of money printing?

kam,

LOL, No. This BS never dies, does it? Paying interest is not QE, and getting paid interest is not QT. The Fed has been getting paid interest on its securities forever, lots of interest, and still does to this day, and collecting interest is not QT. And paying interest is not QE.

But nowadays it collects less in interest than it pays. So it has losses instead of profits. the Fed was remitting its profits to the Treasury department, earned mostly from the interest on its securities. Now that it’s paying out more in interest than it’s earning, and losing money, it no longer remits anything to the Treasury, and thereby the deficits worsen.

To be fair though, Wolf,

The poster didn’t say “QE” rather “printing”. To be fair, this interest paid is money that’s being created when it’s in excess of interest earned on treasury securities. And the accounting for this is the negative entry on the Fed balance sheet – that line item is money that has been created and sent to holders of interest-bearing accounts at the Fed thereby entering the economy.

This new money will be destroyed when the Fed earns future interest and offsets this negative entry with it and “destroys” the money paid in interest.

John Hussman has written extensively about this, and is upset (understandably) that this constitutes an improper tax on Americans, as all of this money is money that cannot be remitted to the Treasury in the future.

It’s true though that this amount is being offset by QT, which is happening at a faster clip.

question tho

EVERY TIME the Fed pays the salaries for its thousands of employers, it creates money because it doesn’t have a cash account.

And EVERY TIME it collects interest (a huge amount) and fees (it collects lots of fees) it destroys money.

It is pure idiotic BS to isolate the interest the Fed pays and call that money printing, and not call it “money destruction” when the Fed receives interest and fees.

If you want call anything “money printing,” it’s the net of its revenues and costs – currently a loss. But that amount is much smaller: a cumulative loss of $129 billion since September 2022 (before then, it was profitable), so in 16 months = $8.1 billion per month, or 268 million per day.

But then by the SAME logic, you MUST call its profits before September 2022 “money destruction” and that’s a huge amount. Since QE started in 2008 through September 2022, the Fed has made a profit of $1.1 trillion, and has remitted all of it to the US Treasury. So do these morons call that $1.1 trillion “money destruction?” Did they ever? Nope.

People that traffic in this BS that paying interest is money-printing never mention that massive scale of money destruction, do they?

Here are the Fed’s profits that it remitted to the US Treasury – money destruction on a huge scale as you would have to call it, LOL:

https://wolfstreet.com/2023/01/13/despite-losses-since-september-the-fed-still-made-a-profit-for-the-whole-year-2022-remitted-76-billion-to-us-treasury-dept/

You are forgetting the ongoing BTFP, the master con job engineered by banks to buy long treasuries at a discount and sell them to Fed at par. Over $120billions so far, and you can be sure it will be extended in March.

Eastern Bunny,

“…con job engineered by banks to buy long treasuries at a discount and sell them to Fed at par.”

Jeeeeeeesus. Banks cannot post newly purchased securities as collateral. They can only post collateral that they purchased before March 12, 2023. Why does this BS keep getting spread? Who are the moron YouTubers out there that still spout off this crap? Tell them to go read the effing term sheet:

“Eligible collateral includes any collateral eligible for purchase by the Federal Reserve Banks in open market operations (see 12 CFR 201.108(b)), provided that such collateral was owned by the borrower as of March 12, 2023.

https://www.federalreserve.gov/newsevents/pressreleases/files/monetary20230312a1.pdf

“If it [the Fed] stops paying interest on reserves and running massive reverse repo operations, it will immediately add $5.7 trillion of liquidity to the market – about 25% of the entire money supply.” Which is why the Fed will never take these actions. There is already too much liquidity in the system which is why there is a good chance the Fed will have to raise interest rates [surprise!} in the first half of 2024 to cause a slow down, and maybe a recession. The economy is growing too fast (see 3rd quarter GDP final report) and will soon need to be slowed. You heard it here first.

So have real productive assets that protect you from this event; otherwise you are screwed.

I need to buy dairy sheep.

A distillery for me…

Is there a calculation that shows the share of GDP per industry above?

And then calculates the industry’s profits as a percent of its share of GDP?

Inflation is under reported. Government is propping up the economy. Politics rule everything anymore as opposed to doing what is right. Too bad.

LOL at dot plot 3 rate cuts next year and WS projected 6 rate cuts next year with this kind of inflation and corp profit…Not saying it’s utterly impossible in this insane world but that would truly be something to see and the whole back to 2% target would be about as real as the promise of Hyperloop…

Forget WS cut estimates. These are just wishes for Santa.

As for the fed estimate of 3 possible cuts, remember it only happens if their assumption that inflation drops to 2.0% holds true, in which case the funds rate remains 2.5% above inflation at 4.5% from our current 5.5%.

Powell and the governors continue to be very clear about this. If inflation doesn’t drop further, not only will there be NO rate cuts, there will be rate INCREASES.

Buy now before the price goes up.

Might as well live it up, the world is on fire?

Befuddled. 😂😂😂

Seems that those who said inflation was not caused just by supply bottlenecks and excessive PPP, but also corporations using these as a cover to raise prices beyond their increased costs were right. The business press of course said that was hogwash, but the consumers are the ones getting hosed.

Yup — Isabella Weber is no fool.

Isn’t what we’re seeing is the reverse process, prices holding firm while input costs ex labor are weakening, hence strong profits. Question is how long can consumption hold up?

steve,

Prices holding firm? No, you missed what’s going on with inflation though I have endlessly discussed it here.

– Gasoline/diesel prices plunged, which you can see in the lower profits of nondurable goods.

– Food prices (also nondurable goods) continue to rise from already very high levels.

– Durables goods prices for CONSUMERS fell, but these manufacturers don’t make as much for US consumers (outside of vehicles) as they do for other companies, such as transportation equipment, machinery, electrical equipment, oil and gas drilling equipment, generators, etc. Higher prices there take a while to filter into higher consumer prices.

— Services is where consumer price inflation is, and prices there are not steady AT ALL. From my last CPI article:

https://wolfstreet.com/2023/12/12/beneath-the-skin-of-cpi-inflation-november-core-services-inflation-accelerates-as-rent-cpi-glows-in-the-dark-insurance-spikes/

The CPI for core services (without energy services) on a month-to-month basis rose 0.47% in November from October, or by 5.8% annualized (blue line).

The three-month moving average rose by 0.46%, or 5.7% annualized, the sharpest increase since April (red line). The acceleration of the three-month moving average in September, October, and November is very disconcerting:

Wolf, I thought you made a compelling case a couple weeks ago regarding the stickiness of services inflation.

The surprise and puzzle to me was Jay Powell stating specifically that service inflation was also coming down , thereby hinting to everyone that the Fed was going to cut rates ( as inflation came down).

Why did he do that?

Inflation: too many dollars chasing too few goods and services. Somewhere over the rainbow, follow the yellow brick road.

Not anymore my friend, that problem got ‘fixed’ too.

Inflation: businesses increasing profits and consumers willing to lower their standard of living to help them.

Yup — inflation is always and everywhere a distributional conflict phenomenon.

Doesn’t economic theory say that high profits will attract new competitors who will undercut prices?

Of course, in a booming economy, the competition won’t show up right away, but they’ll be around sooner or later.

Don’t hold your breath. Any more industry consolidation and we’ll all be begging billionaires for crumbs on Shark Tank.

And of course Shark Tank is just entertainment and 90% of investments never make a profit. Selling the narrative that anyone can make it!

Glen – …sounds like opening a restaurant (one in six chance of success, as I recall) gives slightly better odds than that!

may we all find a better day.

anyone notice Apple and Microsoft have a monopoly (biopoly) on operating systems for PCs?

You nailed it, Bobber — mind the oligopolies and monopsonies.

“Doesn’t economic theory say that high profits will attract new competitors who will undercut prices?”

No it doesn’t say that because this is a very dynamic and complex process having to do with all kinds of variables, from barriers to entry and concentration via M&A to there being plenty of demand so that no one wants to cut prices, and everyone wants to maximize profits, and so they all raise prices. See my articles on the pickup truck oligopoly — only four companies make full-sized pickup trucks in the US. Pickups have become HUGELY profitable for automakers. Now we get a couple of new ones, Tesla and Rivian, but they don’t matter yet in the huge segment of pickups. What we had is decades of oligopolist pricing behavior for pickup trucks, with plenty of demand, and huge price increases, and this is the result:

https://wolfstreet.com/2023/12/15/the-shocking-price-increases-of-the-pickup-truck-oligopoly-ready-for-tesla-to-mess-up-their-party-f150-xlt-camry-le-price-index/

Early stage capitalism yes, late stage not so much. It is the nature of winners and losers. Winners keep getting bigger and bigger. They like to have a few ‘competitors’ so it doesn’t look like a monopoly but plenty of informal price fixing occurs.

Sorry, but it’s going to take a complete breakdown in the economy is stop this sh*t. The corporations and banks are in complete control and driving onward. Every aspect of our financial lives is being manipulated and attacked.

Nothing is going to change and only gets worse until these bastards are brought down.

I don’t want cheap-made products to fill the dump. But in many cases that’s all the selection we have from our darling retailers. It’s buy for $5 from China, sells for $50 here, cheap-made crap. Why doesn’t anyone wake up to this?

Planned obsolescence is how they continue to make money. It isn’t that China makes cheap goods as they can make goods at all price points. It is much more profitable to design and engineer a product to fail at a certain point. This does require some level of brand loyalty or dominance in the market. Apple lost a lawsuit around this although they claim they intended no wrongdoing.

This is kind of dumb. You believe engineers are conspiring to make a product fail at a certain point? Everyone always points to failed obsolescence as if people can just design in a failure point at will and know exactly what will happen over the life of a product. Nothing lasts forever, you realize that right? The same reason a semi goes 1M miles and your car goes 250k? Sure, i can design a car to go 1M miles, the price will go up, and people might not want to buy it. But i can do it. So is it failed obsolescence if i design it to work for 250K? .,…Or is it just designed to last for a certain lifecycle and duty cycle?

People dont understand planned obsolescence and how much its really not a thing in most cases. Poor engineering and poor quality is not planned obsolescence. Stuff doesnt last forever, and if you want it to, it has to be designed to last forever and it will be built and priced accordingly. Most people who complain about this are the ones who buy the harbor freight tools to save money and then complain ‘they dont make it like they used to’.

With the exception it is a well documented economic principle with plenty of examples. They come in all forms and in some countries are illegal. In the US it is easy to find examples and laws put in place as well.

There’s also many variables in product longevity. The 1M mile truck above won’t last 1M miles if you never change the oil or do other preventative maintenance. The average schmuck probably doesn’t remember the last time they checked their tires (“But, the light didn’t go on so I didn’t think there was a problem”), oil (“But the light didn’t go on so I didn’t think there was a problem), the condition of their coolant (“It’s not overheating so I didn’t think there was a problem”), brake fluid….. and so on.

That’s how two of the same vehicles have a different life expectancy. One goes 250K and the other is on the end of a hook at 15K miles.

Except when products are irreparable by design — hence the need for a “right to repair” movement.

When the government drops $5T of printed money on the table, the recipients will spend it and corporations will take their cut through increased prices. No surprise there.

They dropped $4T printed money after the 2008 recession, then 5T of printed money in 2020/2021. Markets are eagerly anticipating the next round, which will be necessary to avoid the defationary Boogieman which haunts the Fed.

Yep. I hope the next round creates the crack up boom and collapse we so desperately need and deserve.

R&T: How Toyota Was Able to Make Its $13,000 Future Pickup So Affordable

It turns out the $10,000 pickup truck is actually too good to be true. But only by a little bit. The production version of the Toyota IMV 0 concept, now known as the Hilux Champ in Thailand, starts at 459,000 Thai Baht, or just over $13,000 at the current exchange rate. On the one hand, that’s 30 percent higher than the price we heard from Toyota engineers during a brief test drive in Japan. On the other hand, it’s a brand new truck with a full bed capable of hauling 2,200 pounds that’s almost as cheap as a 22-year-old Ford Ranger on Bring a Trailer. As a further reminder, the 2024 Tacoma base price is $32,995. The Hilux Champ is still a deal, and to learn more about how Toyota pulled this off, we got some answers straight from Dr. Jurachart Jongusuk, chief engineer for Toyota’s IMV platform as well as regional chief engineer for Toyota Daihatsu Engineering and Manufacturing.

Americans feel they deserve ‘luxury’ and are willing to pay the higher price for that and status. If they want to throw their money away let them, Most consumers are willing to pay ridiculous prices for just about anything because they are not willing to wait for a better deal. The American consumer is their own worst enemy.

I hear Toyota work vans are very popular in my parts of the world, but it is not available in the US for some reason.

Brant – take brad’s comment, and that USDOT/NHTSA/DOC doesn’t have a supreme legislative presence (for good and/or ill) of the global market and you could find yourself on the way there…

may we all find a better day.

Wolf,

At the risk of getting yelled at (and “I read the damn post”), it isn’t clear if the figures on the chart are real or nominal, inflation adjusted or not.

If the G instantaneously doubled the entire money supply, everywhere (including all ledger entries of net wealth, debt, revenue, expense, etc.) then *everything* would double…including profits…in nominal terms.

Obviously, instantaneous and universal inflation isn’t how things actually work…but some grossing up of more-or-less everything (in nominal terms) is the very definition of inflation.

I’m not saying that corporations aren’t making out…but perhaps less than is implied…if the numbers you are using are *nominal*

(I’ve read the post and searched for “real” and “nominal” and “adjusted”…they don’t show up in the post in a clarifying way. Seasonal adjustment by itself doesn’t convert nominal figures to real ones).

1. If it isn’t clearly specified as “real” or “inflation adjusted” or “2017 dollars,” or similar, ALL figures everywhere all the time are nominal.

2. Financial statements, revenues, profits, tax returns, etc. are NEVER inflation adjusted.

3. Raising prices = inflation. That’s the definition of consumer price inflation. Higher prices for the same product.

4. Profits show the second part of inflation for companies, namely costs, which also go up with inflation. But companies have been raising their prices faster than their costs, including labor costs, have gone up.

10-4 BRANT….

It’s the opening scenes with Harrison Ford in “The Mosquito Coast” (1986) in the US of A hardware store (think Ace?)

James – our apocrypha has a rich and varied existence here in the comments, so I’ll redux one of mine dating back a decade or so…

There’s a small, independent hardware/auto shop I worked for (and still periodically help out at) in our local hamlet. The owner stocks US-made goods whenever possible, but fewer and fewer as normal exchanges went more like this (remembering the rate of brick ‘n mortar meltdown has seriously accelerated, exacerbating the always-fraught existence of small local business since then):

Customer: “Wow, i really love old-timey stores like this! I need a pipe wrench, but I want a GOOD one. Do you have anything made here (sic: US)?

Me: Yes, sir! We carry Rigid, best on the market, and replacement jaws are available should you ever manage to wear them out. What size?

Customer: uhh, 18”?

Me: Close enough (taking one from the display behind the counter). That’ll run about $75.

Customer: WHAT!?! Well, maybe not THAT good, it’s just for using around the weekend cabin here, anyway. Do you have something a bit cheaper?

Me: (replacing the Rigid and taking down a China mfd. Olympia in its place), we have these for $30.

Customer: ah, yeah, that’ll do…

may we all find a better day.

Similar to many other charts that Wolf has shared, it seems we’re detached from what was a fairly stable trendline in most economic metrics pre-pandemic. Has to be all the money printing that basically served as a step ladder towards a new, higher normal.

I’m not sure when/if we’ll see things descend the ladder back towards our pre-pandemic trendlines. Maybe the forces of gravity are no match for the epic spending spree we’ve seen the past few years. A moderate recession would probably do the trick, but it seems the fed may have dodged the bullet by permanently altering the fundamentals.

How are people not understanding by now that inflation is the differentiator here. What do recessions primarily do? Reverse the trends to shift them back in favor of employers and financiers. This lowers their major cost of operation and the balance of power. Where were wages at in 2017, 2018, 2019 relative to historical trends? What were all the propaganda news articles saying in 2018 about go ask your boss for a raise or it’s time to start browsing job listings for other companies.

The only way out of all that for companies was the long overdue and guaranteed recession right? Yeah, or wait, no…………inflation.

The government did the companies a big favor through inflation. It set people’s wages back the equivalent of a recession in terms of true wealth and purchasing power without the companies themselves having to be set back by a recession. The government inflated away a recession and the corporations want to thank you and the charts can vouch for their gratitude.

What year is this, almost 2024 right? Was anyone paying any attention in 2018, 2019, 2020, 2021, or did you ride that transitory line all the way to the persistent inflationary state of being that we are in? Our society received it’s official stamp of approval for complete transition to full on ‘F— you I got mine!” status by 2021 so if you didn’t get yours by then, well………

Energy is cheap at least. Oil is selling at the equivalent of $40 a barrel in inflation adjusted 2000 prices.

Nat Gas is selling at the equivalent of $1.7 in inflation adjusted 2000 prices. You can thank the US oil and gas producers for keeping the prices low even though we have had a lot of inflation and a devaluing dollar. I am pretty sure labor and materials cost more than in 2000.

Saudi is upset an not being able to rise prices as inflation rises. They are seeing their in the ground oil diminish in value.

Somehow the government is able to fine tune it’s management of supply and demand and economic driver pressures largely through the price of diesel fuel and to a similar but lesser extent through the price of gasoline and natural gas. This is another aspect that I can’t believe people don’t point out or simply see. I could elaborate in detail about this and why I am saying so but I’m not sure it’s worth it to anyone to try to do so other than to see you can actually see it in the graphs in the last financial cycle in the use prior to, during, and following the ‘great financial crisis’.

ru82-

Oil is cheap indeed.

I just saw in a Doomberg article that oil (WTI), priced in ounces of gold, has declined from a 40 year high in 2006 of 0.16 oz per barrel, to 0.04 oz. per barrel.

Technological advancement is miraculous!

1) During the zero rates Corp debt hiked from $6.4T in 2010 to $13.7T in 2023. That debt will have to be paid at higher interest rates.

2) To cut costs Corp might resort to layoffs. When income is cut people

will not be able to pay debt.

3) We need a recession badly, but the Fed will try to prevent a total

collapse. The Dow might decay in stepping stones.

4) The Dow reached a line coming from : 1929 to 2000 highs. It might

drop with several lower highs and lower lows.

5) Shortages of good collateral in the o/n markets will cause interest

rates spikes.

These obscene profits simply point to stop the Trump Era corporate tax cuts.

Taxation wise these graphs show the corporate cash register is ripe for the picking.

Bacon at 50 dollars a slice is coming. Couple that with 5 dollars for a bag of Cheetos XXX Spicy and you know that the American Dream is coming true.

Murica!!!

Windham ski resort (NY) became “ultra exclusive”. The locals and the middle class are deprived.

$299 discounted to $269 for a day pass at Park City. At these prices cross-country skiing will be taking market share from downhill again as it has done in the past. When I was a kid, Cortina d’Ampezzo, Val d’isere, St Moritz, St johann, and Kitzbühel were unaffordable, but the places down the road from those resorts usually weren’t nearly as expensive and the skiing was just as good. But even if you lived in Park City today three hundred bucks for a day’s skiing is beyond the means of many individuals and certainly a lot of families. Just read an article in the South German press, apparently the same thing is happening in the Alps. Kids in a German school recently voted to eliminate the ski week holiday and shift the week to summer break. Add the snow shortage in many ski areas, and the shortage of reasonably priced worker housing in same, soon only the wealthy will be able to use bespoke skilifts on manufactured snow in secure redoubts accessed by Netjet.

I looked into helicopter skiing once, but since I had to ask, I couldn’t afford it.

Cross-country trail passes are getting expensive too, but are still in the double digits. Royal Gorge is now at $50 a day, $45 for seniors. Super seniors (75+), which I aspire to become in the distant future, knock on wood, pay $15, sure worth it getting old, LOL.

I’m looking at getting into split-boarding. Ski up and snowboard down. Save money, avoid lines and great workout.

With inflation moving to services, most working class people and retirees are becoming broke just paying for services which they have to have, and some that they don’t even want. Most of these services are provided by monopolies and government entities. Cable, Insurance companies, property taxes, medical services, transportation, licensing, utilities, etc. The average retiree spends $60,000/yr just paying to keep a roof over their head. There is very little discretionary income left to buy luxury items and expensive durable goods. So, all these inflation numbers that I see every day on the financial news networks are not only under reported (service inflation is more like 10% or higher), but don’t relate to the average working class stiff or retiree on fixed income.

are you saying the average retiree spends 60k on housing or what exactly are you saying here? and where is this information coming from??

I wouldn’t be surprised if the average retiree spends $60k a year when you include housing costs, utilities, medical services (including Part B premiums), car payments, and so forth.

Sure, some spend more, and some spend less.

He said “to keep a roof over their heads”, not “total cost of living”.

Talk about twisting a post to your bias….

Blake

I meant 60K spent yearly on necessary items like Food clothing shelter, insurance, utilities, transportation, medical care, etc. These figures are well documented. Of course, it depends on where you live but I can say that I’m in the same boat. I’ve got the receipts to prove it. I’m not complaining but just presenting the facts. That’s why we’re still in the workforce, so we can have some discretionary spending.

John H,

Normally we don’t post links at Wolf but:

https://m.youtube.com/watch?v=dY5IOyCXecc

Or search for Wall Street Week 12-15.

Rieder and Weston have a long conversation but start listening at 32:00 where Weston asks a question about inflation.

Reider said, “I really think the U.S. economy doesn’t go into recession except for pandemic, financial crisis, unless there is some big exogenous shock…'” —meaning that the business cycle is gone because the cycle ended with a recession, boom and bust, a recession is part of the cycle. These words shocked me and he also alluded that he had talked about this before.

He wasn’t blowing or talking his book here (earlier in the conversation when he was talking about his new bond ETFs he might have been but not here).

TC – but you can have a decade of high rates, high inflation, and a stock market that trades sideways, all without a recession.

Recession isn’t the only reason to advocate for staying out of equities.

The odds that the Fed will actually hike rates in 2024 just went up (in my head if not dot plots and market expectations). Markets are going to react badly when the Fed next gives some brutally hawkish guidance. No cuts for you!

@pmbug: Not sure. CNBC and Bloomberg have started pushing today’s “cooling inflation” report as a reason why rate cuts will happen. Will wait for Wolf’s analysis of the same to learn about the actual status of inflation beyond these headlines.

The other day I mentioned in a post that the Fed may be buoying the stock market with Powell’s post-FOMC interview on Dec 13th. Then they trotted out other Fed FOMC members to say that they are not discussing rate cuts at all at this time.

It just struck me that the Fed is just putting its finger on each side of the scale so that it doesn’t swing too much in either direction. Put another way, they would rather see a slow leak rather than an implosion of the markets. The end result in either case would be the same but a slow leak would be easier to manage and provide better optics rather than an earth-shattering implosion.

I only see a more bubble inflating although but slowly than a slow leak.

The market is up evey day little bit and seldom down.

PCE report just came out today, and numbers from previous months were revised DOWN (as often happens when GDP is re-estimated)

From the October report, the 4 months from July to October were

Core M/M: +0.2, +0.1, +0.3, +0.2

Core Y/Y: +4.3, +3,8, +3,7, +3.5

In the November report, these July-October numbers were revised DOWN to

Core M/M: +0.1, +0.1, +0.3, +0.1

Core Y/Y: +4.2, +3.7, +3.6, +3.4

November had a core M/M of ZERO, bringing the annualized metric down to +3.2% Y/Y.

The difference between core CPI = +4.0% annualized and core PCE is now a whopping +0.8% annualized. It’s usually below 0.5% at these levels.

I just find the July-September numbers incredibly hard to believe, ESPECIALLY considering they came from the “outlier” +5% GDP quarter. All that growth and near-zero inflation? Seriously?!

In the coming months, thanks to favorable base effects CPI will likely fall to 3.x% annualized while PCE will fall to 2.x%, and Wall St-FOMC will declare mission accomplished.

1) France in recession. Germany might be next. Macron followed Sunak and Meloni foot steps.

2) Gravity between US10Y and the German 10Y pulls them together.

3) In France 6M minus 5Y = 3.68 – 2.16 = 1.5%. The spread between the

6M and the long duration is growing. The 6M decayed slowly. The 5Y

sinks deeper & faster. The 6M is hooked to madam ECB belly button. She will be forced to cut rates.

4) When the Fed hiked aggressively the banks parked their money in RRP for higher O/n rates, providing good collateral in the O/N market.

5) When the Fed stopped and the 10Y reached 4.999% the banks cut

RRP and moved in to US notes and bonds.

Wolf – is there any further breakdown of corp profits between brick & mortar retail vs ecommerce?

No, retail is retail.

Appreciate the compilation of empirical evidence, Wolf.

Wage-price spiral my ass — it’s always been anti-labour propaganda!

BEA release 12/21/2023 corporate profits 2023Q3 historical comparison table shows -0.6% change from quarter one year ago (with IVA and CCAdj). I’m not sure how to reconcile the huge difference. Link to BEA site: https://www.bea.gov/sites/default/files/2023-12/hist3q23_3rd.pdf

Thank you!

RTGDFA, or at least read the heading of the pictures!!!

The overall figures, which your link cites, include the huge losses from the Federal Reserve (the 12 regional Federal Reserve Banks are private corporations). The BEA also provides a figure without the FRBs, which is what I use here [WHICH I SPELL OUT CLEARLY 2x IN THE ARTICLE, INCLUDING IN THE FIRST LINE, PLUS ON THE CHART IN HUGE FONT], because the FRB’s losses have nothing to do with business but are a result of the Fed paying interest on reserves and on RRPs.

I normally delete this BS by people who didn’t RTGDFA. Commenting guideline #1.

I had read the article more than once. It’s just that I didn’t know that FRB’s losses were included in the BEA’s historical comparisons. Now I do thanks to you. I appreicate not only the accuracy but also the relevance of the data you painstakingly provide. One of very few unbiased and credible.