20-City index below 2022 high, 9 metros below 2022 highs, 10 metros set new highs. The unsavory “National” index cocktail in the headlines today gets shredded.

By Wolf Richter for WOLF STREET.

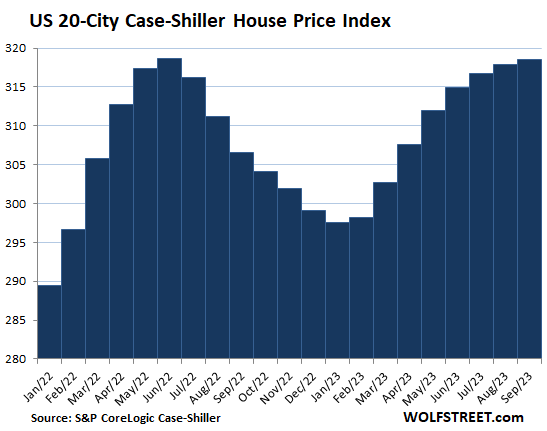

Home prices in the 20 metropolitan areas that today’s S&P CoreLogic Case-Shiller Home Price Index covers eked out the smallest month-to-month gain (+0.2%) since January, and remained a tad below its all-time peak of June last year. Here’s the close-up. We’ll get into the most splendid of the 20 metros in a moment in all their individual glory.

The S&P CoreLogic Case-Shiller Home Price Index uses the “sales-pairs method,” comparing the sales price of the same house over time, thereby eliminating the issues associated with median price indices (see “Methodology” toward the end of the article). But it lags: Today’s index for “September” is a three-month moving average of home prices whose sales were entered into public records in July, August, and September.

By contrast, the national median-price index by the National Association of Realtors fell for the fourth month in a row in October and was down 5.1% from the all-time high in June 2022, making 2023 the first year since the Housing Bust that the seasonal high of the current year was below the high in the prior year. And this is an actual national index.

By contrast, the “National” Case-Shiller index hit an all-time high, which is what the headlines today screamed about. But the Case-Shiller Index, which I think is the most reliable house price index out there, does not cover the entire US; it only covers the 20 metros discussed here.

So S&P CoreLogic, in its attempts to give the 20-City data the aura of a “National” index, combined the clean 20-City Case-Shiller data with data from the FHFA House Price Index. The FHFA data is based on mortgage data from Fannie Mae and Freddie Mac that systematically excludes all cash deals and all deals with mortgages that hadn’t been bought by Fannie and Freddie. This systematic selection and exclusion of home price data makes the FHFA index very weird and skews it.

Nevertheless, S&P CoreLogic mixed these two data sets into a cocktail it calls “National Home Price Index,” and the doofus reporters or bots at the media outlets to make clickbait out of it.

So today’s 20-City Case-Shiller housing numbers.

Prices are below their 2022 peaks in 9 of the 20 metros in the index (% from their respective peak):

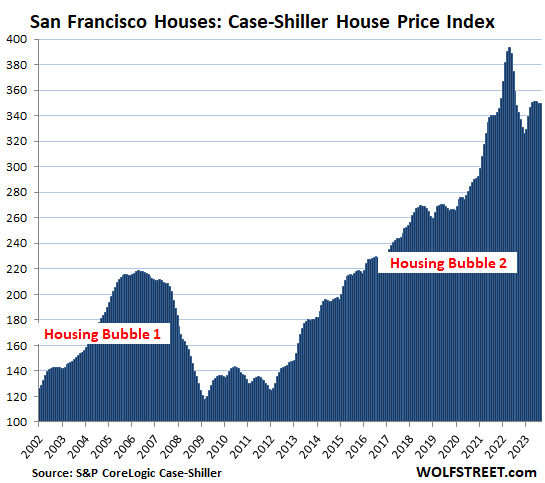

- San Francisco Bay Area: -11.2%

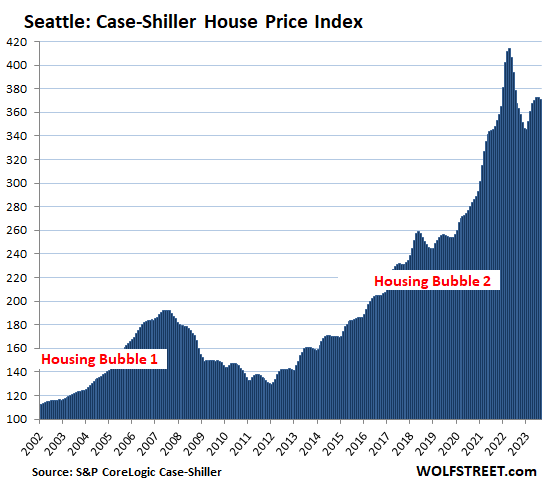

- Seattle: -10.4%

- Las Vegas: -5.6%

- Phoenix: -5.6%

- Portland: -5.0%

- Denver: -4.7%

- Dallas: -4.1%

- San Diego: -2.0%

- Los Angeles: -1.1%

Prices set new highs in 10 of the 20 metros in the index (% year-over-year):

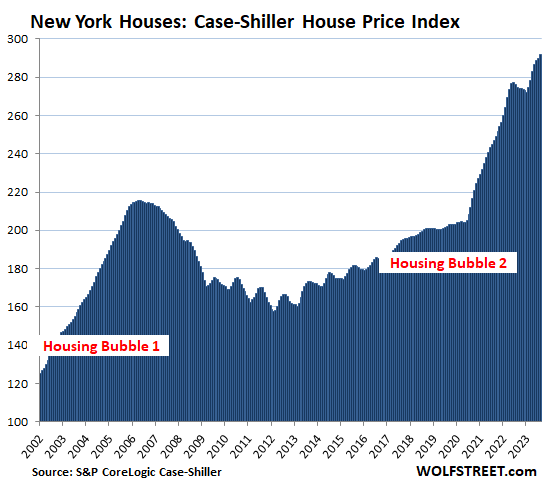

- New York: +6.3%

- Detroit: +6.7%

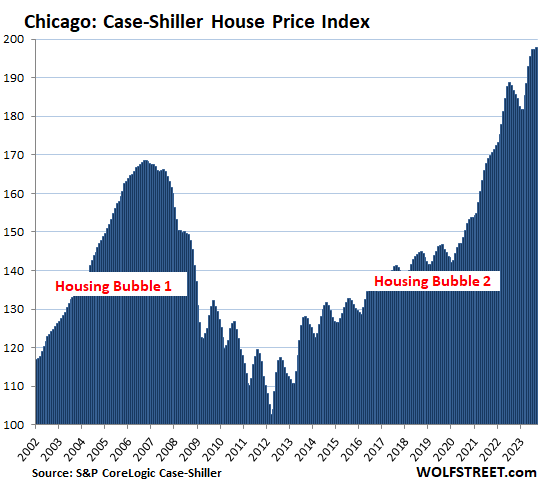

- Chicago: +6.0%

- Boston: +5.3%

- Cleveland: +5.0%

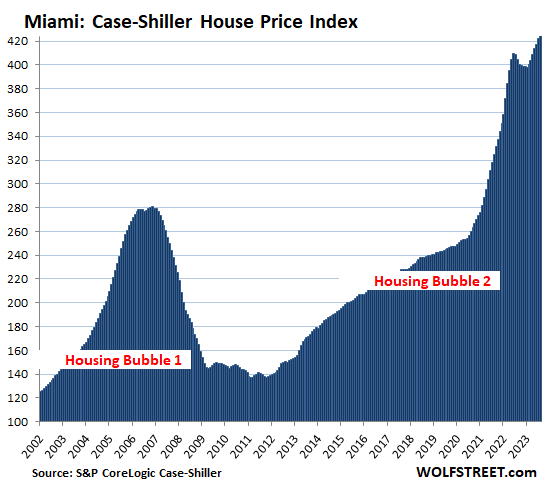

- Miami: +5.0%

- Charlotte: +4.7%

- Washington DC: +4.4%

- Atlanta: +4.3%

- Tampa: +1.5%

The most splendid housing bubbles by metro.

San Francisco Bay Area:

- Month to month: flat

- Year over year: +0.5%

- From the peak in May 2022: -11.2%.

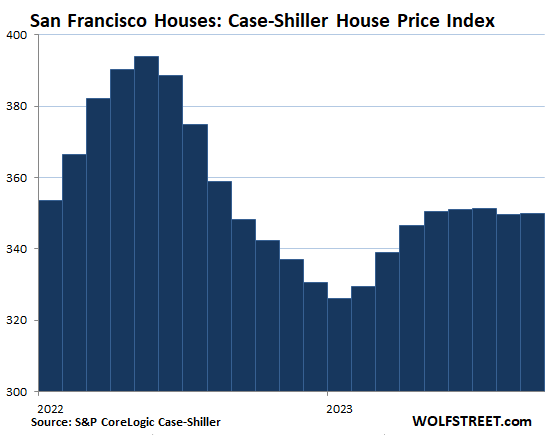

And here is the closeup of San Francisco:

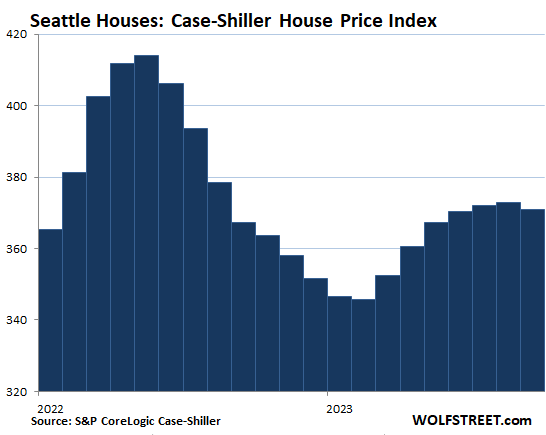

Seattle metro:

- Month to month: -0.5%.

- Year over year: +0.9%.

- From the peak in May 2022: -10.4%.

The closeup of Seattle:

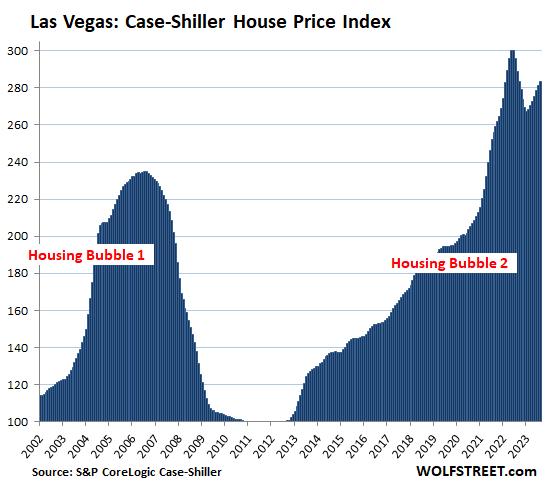

Las Vegas metro:

- Month to month: +0.6%.

- Year over year: -1.9%.

- From the peak in July 2022: -5.6%.

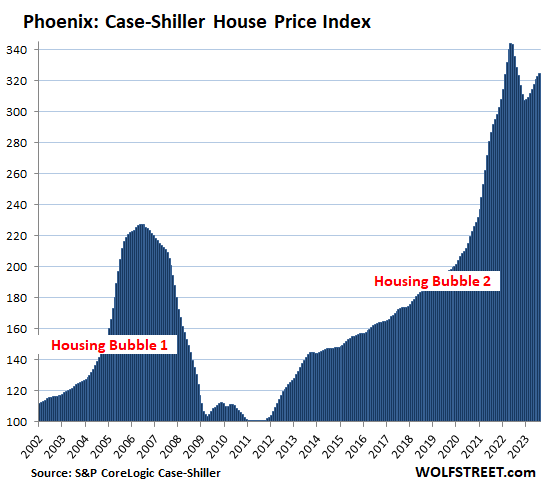

Phoenix metro:

- Month to month: +0.5%.

- Year over year: -1.2%.

- From the peak in June 2022: -5.6%.

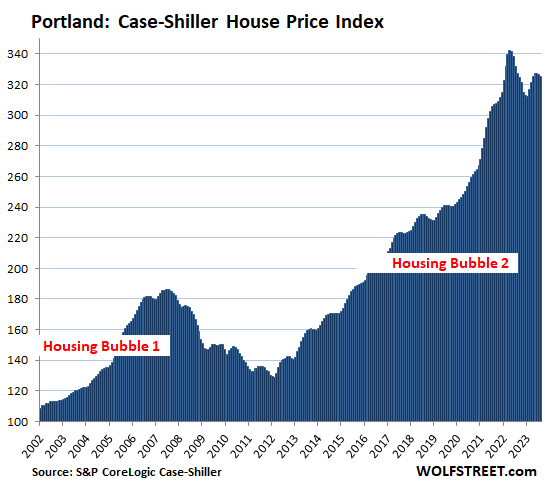

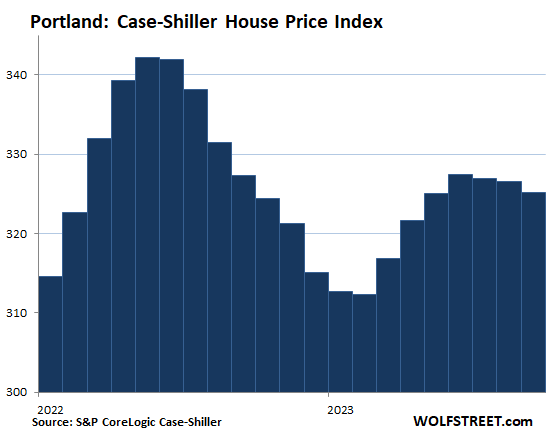

Portland metro:

- Month to month: -0.4%.

- Year over year: -0.7%.

- From the peak in May 2022: -5.0%.

The closeup of Portland:

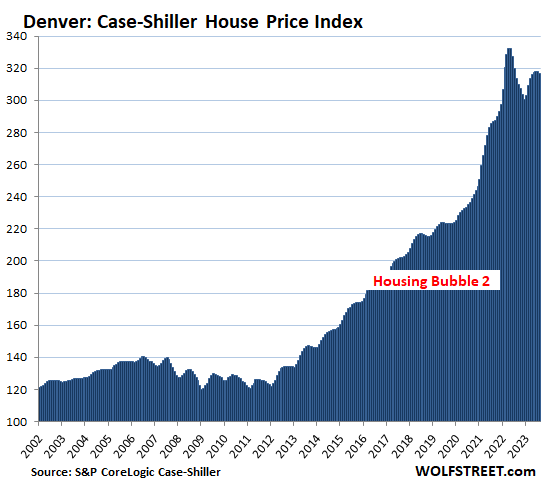

Denver metro:

- Month to month: -0.3%.

- Year over year: +1.0%.

- From the peak in May 2022: -4.7%.

Note: I will post closeups of Denver and a few other markets in the comments below as soon as I have a little extra time.

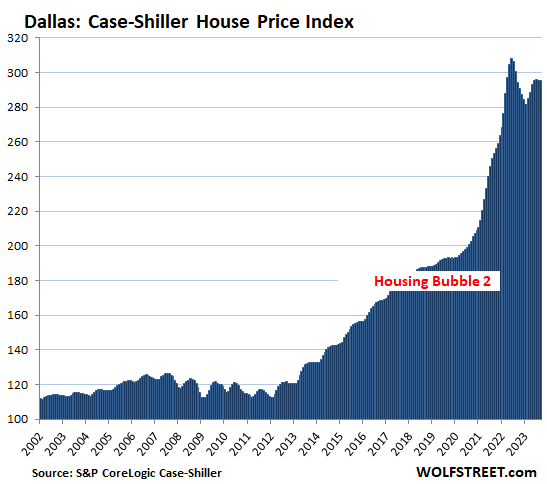

Dallas metro:

- Month to month: -0.1%.

- Year over year: +0.3%.

- From the peak in June 2022: -4.1%.

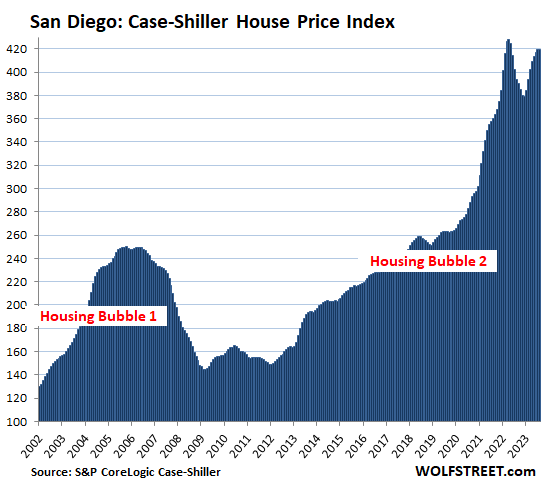

San Diego metro:

- Month to month: flat.

- Year over year: +6.5%.

- From the peak in May 2022: -2.0%.

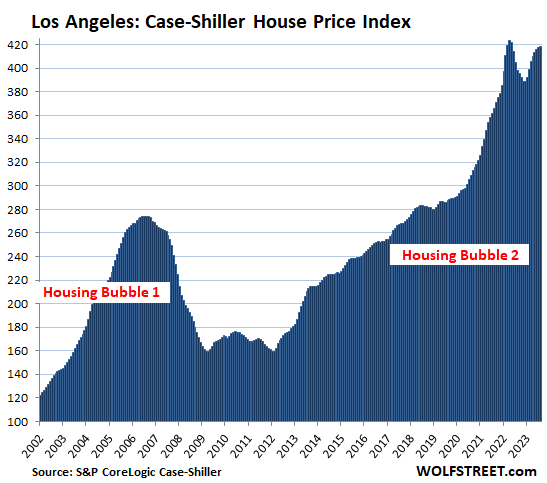

Los Angeles metro:

- Month to month: +0.2%.

- Year over year: +5.2%.

- From the peak in May 2022: -1.1%.

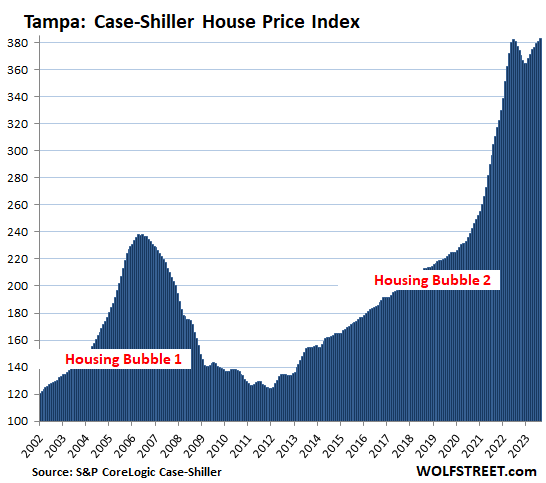

Tampa metro:

- Month to month: +0.5%.

- Year over year: +1.5%.

- Set new high by a hair, squeaking past the high of July 2022.

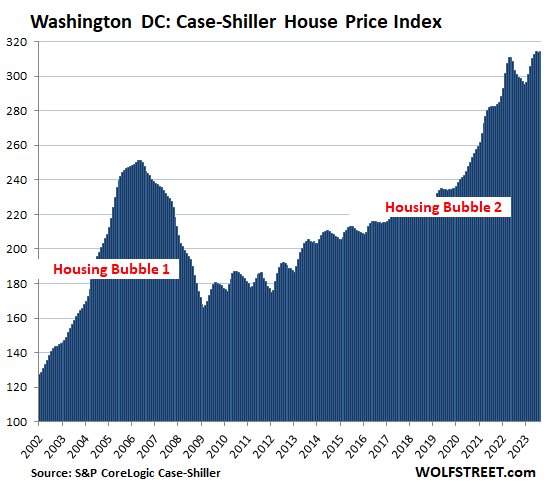

Washington D.C. metro:

- Month to month: 0.1%.

- Year over year: +4.4%.

- Set new high.

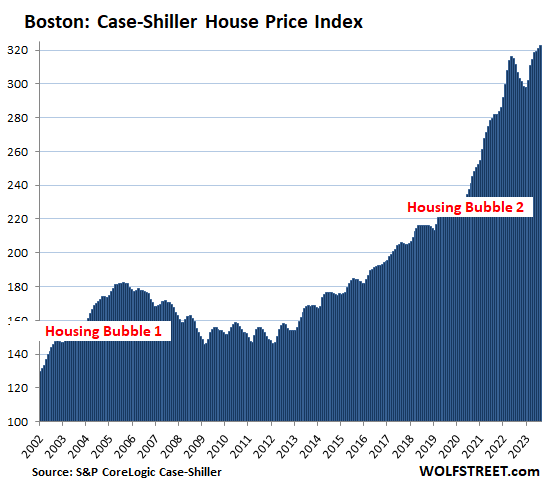

Boston metro:

- Month to month: +0.5%.

- Year over year: +5.3%.

- Set new high.

Miami metro:

- Month to month: +0.6%

- Year over year: +5.0%.

- Set new high.

New York metro:

- Month to month: +0.6%.

- Year over year: +6.3%.

- Set new high.

Methodology. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors. This “sales pairs” method makes the Case-Shiller index a more reliable indicator than median price indices, but it lags months behind (37-page methodology).

It’s Home-Price Inflation. By measuring how many dollars it takes to buy the same house over time, the Case-Shiller index is a measure of home price inflation. The indices were set at 100 for the year 2000. So today’s index values of 425 for Miami and 419 for San Diego and Los Angeles are up respectively by 325% and 319% since 2000. Miami is thereby the #1 Most Splendid Housing Bubble in terms of home price inflation since 2000, followed by San Diego and Los Angeles.

To be included in this list of the Most Splendid Housing Bubbles, the metro must have experienced a home price inflation since 2000 of at least 180%.

By comparison, Consumer-Price Inflation, which tracks price changes of goods and services that are consumed by consumers was 82% over the same period since January 2000, according to the Consumer Price index (my latest on CPI: Beneath the Skin of CPI Inflation).

The remaining 6 of the 20 markets in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) had far less home price inflation than 180% since 2000, and don’t qualify for this list of the Most Splendid Housing Bubbles. But in 2022 and 2023, these metros were the ones with the biggest home price increases in percentage terms.

Chicago is among the 6 metros that don’t qualify for this list, with an index value of 198, which is up by “only” 98% from 2000. But here it is anyway:

- Month to month: +0.3%

- Year over year: +6.0%.

- Set new high.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here is the closeup of Dallas:

10 year yield crashing. How can that be despite so much QT and rate hikes?

Leo,

It’s volatile, my friend. It’s volatile.

Lookie here. There have been much bigger retracements over the past two years, and before. It’s just a bunch of short-term bets, such as Ackman going out and promoting his latest bet, and the doofus reporters/bots at the WSJ, CNBC, Bloomberg, et al. are carrying his water, and after everyone jumped in, he cashes out. That’s what makes a market, and causes the volatility:

Wolf,

I was looking at the newest fed balance sheet, where i saw that almost all fed’s MBS will mature in over 10 years. Why does fed only hold MBS’s that have so long until maturity? Are they selling mostly the ones with shorter term to maturity during QT?

Goldenexchange,

Maturity dates are irrelevant for MBS for these reasons:

MBS are not like normal bonds where the holder gets paid face value on the maturity date. Instead, MBS holders get regular passthrough principal payments when mortgages are paid off (such as when the home is sold or when the mortgage is refinanced) and are paid down via regular monthly payments. The principal portion of those payments is forwarded to (“passed through to”) MBS holders, such as the Fed, and the balance of the MBS shrinks.

For the Fed, these passthrough principal payments amounted to about $80 billion a month before the increase in mortgage rates. Now, with these high mortgage rates, refis have collapsed and home sales have plunged, and so passthrough principal payments have slowed to about $20 billion a month, well below the $35 billion cap. So that drives the decline of MBS on the Fed’s balance sheet.

In addition, the ongoing mortgage payoffs cause the pool of mortgages backing the MBS to shrink to such a point that it’s not worth maintaining the MBS. The issuer (such as Fannie Mae) will then call the MBS, meaning pay holders for it and withdraw it, and repackage the remaining mortgages into new MBS and sell the new MBS.

If the Fed cuts interest rates enough, and mortgage rates drop below 5%, the roll-off of MBS will become a flood because there will be a tsunami of refis, which means mortgage payoffs, and the principal is passed through to MBS holders. And those MBS will vanish.

This is why 30-year MBS never live to be 30. They keep shrinking, and after some years, they’re called – sooner during a refi boom, and later when there are fewer refis.

So don’t worry, those MBS will come off a lot more quickly if mortgage rates drop some.

Thanks for explaining this so clearly, Wolf. Admit a lot of us have been confused about MBS passthrough and how it compares with other bonds. First rate finance education here

Good What caused the snake tongue at the end of the graft, I’ve been watching the housing market for a long time because I’m looking to buy but I don’t want to buy the peak I want to buy when blood’s running in the streets but I remember the housing market started going down when they started raising interest rates and I thought it was going to be like 2008 where they just kept going down but then they went right back up so I was always curious to why that happened.

Looking at your graft you’ll see 2008 it’s like a big hill it goes up and then it goes down but then this new super bowl 2.0 you see it goes straight up then it comes down a little bit at the top and then it goes back up, I find it fascinating but I can’t really find anybody who knows why that happened 😞.

And the closeup of Denver:

Thank you Wolf!

I’ll recommend that my son not buy yet in Denver. The HB 2 ramp up was enormous and the fall has been underwhelming.

We have seen a couple of flip houses that were purchased in early 2023 and were sold in November for a 5% loss from the purchase price.

Good things come to those who wait.

Thank you for all that you do!

Your reporting of the mundane facts is always refreshing. Always forces me too engage in the painful work of thinking.

My impression is that this is what a short term, in the historical sense, manufactured economy looks like. Almost as far away from the referential concept of a “free market”.

The obese Fed balance sheet, designed to prevent the free market from delivering it’s punishment to bad and criminal businesses, continues to dominate the market for credit, the mother’s milk of speculation.

100% agree, these types of currency debasements you would normally see in third world countries.

Except that the currency debasement in all of those countries is even worse. The $USD is the least dirty shirt.

I wonder how long this will take to play out?

Judging by the charts, it looks like HB1 took about 4 years to hit bottom and about 6ish to peak. We have hit the peak at about 12 years. Hopefully. If we are at the top right now, would we take twice as long to hit bottom or twice as fast!?

Exciting but also sobering.

Bleak that prices kept rising after June 2023 in the 20 city index. Afraid to think they could hold at these prices and these rates, and further explode in a year or two with eventual rate cuts pouring buyers back in.

A pessimist may view the current investment horizon as bleak while the opportunists, who are a lot more fun, see the potential.

Earthquakes are the energetic expression of the movement of the continental plates. The resolution of the obvious dislocation between the asking prices for assets and the affordability of that asset by the every man, who pays for it all and fights the national wars.

And the closeup of Washington DC:

And of course, San Diego:

So is what’s happening in San Diego and Los Angeles actually a bubble? When I think bubble I think of 2008+- and previous crashes. From the charts it looks to me like we’ve virtually corrected to the high of 2022 and are about to enter a holding pattern. Nobody who has actively been watching the market in San Diego is surprised by these numbers and several months ago a few of us even braved being flamed in the comments when we pointed out what we were seeing, and why, and as expected, we got flamed.

Personally, I think we’re going to see things continue an upward trajectory in San Diego, maybe not the spike type increases, but still up. That being said, don’t discount the possibility of small spikes through 2024 as interest rates lower some (election season coming up). Regardless of anything else, all of this is still extremely influenced by the fact that virtually nothing single family is being built here and everyone on 3 and 4% loans is holding tight.

A bubble is on the way up, a BUST is on the way down. Housing Bubble 1 and Housing Bust 1; Housing Bubble 2 and Housing Bust 2.

Your question should have been: “Is San Diego in Housing Bust 2 yet?”

Wolf, your point about “housing bust 2 yet?” is well taken, but I wonder if history will call that 6 month period from mid 2022 to January 2023 the bust, or micro bust. When looking at San Diego not in years but in decades wouldn’t one come to the conclusion that’s it’s just been one big bubble? The house my mom bought in the mid 60’s for 20,000 would sell for 1.5mil today. The house I bought in the early 90’s for 145k would sell for at least 1.2 today.

To “Not Sure”‘s point, which I think is spot on, isn’t the recent “bubble” very heavily influenced by the rampant money printing of the late? That money isn’t going away and asset values, while not worth any more than the given asset they are, simply cost more because there are more dollars pushing them up in price.

I would suggest that the commenteers with their pedestrian catch phrases come to San Diego, city and county, and see what’s happening with the single family market here. Multi family is a totally different bird and is setting itself up for a huge correction with all that’s being over built, but single family simply isn’t being built here like it was in previous cycles and folks are really holding on to what they have. The land to build 10,000 SFR tracts, let alone 1000 units, doesn’t exist anymore and hasn’t since the last crash of 2008.

The tech folks and old money that are moving in here from other locales is really working the market as well.

There’s nothing special about what’s happening, just market and political forces at play, which are driving costs up.

I agree not in my neighborhood 😕.

We in sd are special and home prices can never go down .

This is just a blip.

When rates drop then people won’t be as committed to holding the 3-4% loan they don’t actually want. It will work both ways.

I heard this exact same thing the last housing bust.

“San Diego is special and there’s no more land and etc…”

We all know how that one ended.

The last housing bust was driven by a credit bubble. But Wolf has shown, much to the astonishment of most of us, that the consumer’s credit is in amazingly good shape.

Today’s asset prices are driven by a glut of money printing. We know exactly how that ended last time around. Median house price tripled in the 70s. And instead of cooling back down, it doubled again through the 80s not really slowing much until the 90s. I’m not talking about value driven by demand, I’m talking about price driven by more abundant dollars floating around. This outcome isn’t very complex at its core.

Everyone on Bay Area said same thing, even in Atherton values absolutely tanked. No place is immune , if these places are so perfect then prices would be way higher RIGHT NOW. There is already a HUGE premium to live in San Diego and Bay Area .

A big difference between the 80s and now is assemble loans – you used to be able to transfer your low mortgage rate to a buyer, you can’t do that right now.

Nothing is ever the same so comparing apples to oranges is ridiculous.

I live in SD, yes it is special, but not that special. I know many high income earners that are completely priced out of the housing market. Not because they are eating too much avocado toast, but because housing payments are grossly unaffordable. In order to be able to afford the median priced home at $956k, and a 7.5% interest rate, 20% down, and at a 43% debt to income ratio (extremely high) someone needs to make $185k a year. That’s almost double the median income.

Sustainable? Probably not.

@SDEngineer

If anything, I think you’re understating the affordability problem. A $956k home at 7.5% with 20% down will result in a payment of ~$7500/mo.

If you’re making $185k, then it’s probably safe to assume takehome pay of about *max* $9500/mo. And that’s if you’re making very little retirement contributions, if any at all.

That leaves $2k per month for utilities, food, transportation, etc. it’s not feasible, unless you’re totally okay with stopping all other forms of saving, and skimping on consumption across the board. It’s called being house poor and a significant drop in quality of life compared with just 5 years ago.

Eroded purchasing power and the equivalent of monopoly money juice the numbers a bit. 2008 dollars are not 2021-23 dollars, that’s for sure.

The declines, possible troughs, then continuous rinse/repeats has me scratching my head. I don’t get how it’s not a more steep and straight decline.

We will get to a bottom, just at a slower and random pace that doesn’t seem to be attached to reality.

Are you sure about that?

Q3 GDP was just revised up to 5.2% from 4.9%. The stock market went up yesterday with two Fed officials providing competing voices over the direction of the FFR. One says more increases are needed and one says we’re at a rate that will bring core PCE inflation back to 2%.

From my vantage point, it doesn’t even look like the Fed really has a firm handle on what to say or to do. And this happens one day before GDP is revised above 5%. That’s flabbergasting.

The Fed seems prepared to finish the year with another FFR pause which is going to let the 10YT to continue to fall, bringing mortgage rates down with it. A January 25-basis points increase MAY not be enough to keep core PCE inflation from pushing higher as we move into next year.

We easily could be in the middle of a ’74 – ’76 head fake on inflation. The only thing that’s clear to me is the Fed desperately wants to avoid a REAL housing recession. To-date, we’ve just lopped off the froth. What happens over the next 12 months is what matters.

STom,

Your thoughts seem reasonable to me. My crystal ball is a bit cloudy but if PCE drops tomorrow stocks and bonds will rally (I think).

I think I heard Powell say the other day that now as opposed to the 70’s the Fed tries to pre-announce it’s direction and rate moves and get the markets to move before they do.

I don’t know what it means when the Fed calls it two different directions like they did yesterday. Since stocks went up and rates went down does that mean the Fed will hold or cut?

What happens when markets misinterpret the direction that ‘Fed Speak’ wants it to move in? That was your question wasn’t it?

“I don’t know what it means when the Fed calls it two different directions like they did yesterday.”

IMHO, it means the Fed is borderline clueless. Obviously, they have ALL the data, but we’re in such uncharted territory that they really don’t know what to do.

And IMHO, it’s only going to get worse as they backstop everything. Non-FDIC insured depositors in SVB & Signature should have taken haircuts. The magnitude of QE after QE is only going to get worse and worse.

I believe it all starts to fall apart in the next 5-7 years when Congress is forced to deal with the SSTF going broke. It will be a perfect storm: higher for longer inflation, lower tax receipts, increasing interest expense of the debt & what is starting to be exploding Medicare costs.

By 2030, we won’t be able to kick the can down the road anymore.

I agree that the GDP growth rate, assuming that it is real, adjusted for inflation, is remarkable, especially with record imports over exports.

Wolf, what is the vertical axis on this? I thought it was $1,000 but NY and Boston can’t be right…

Its the index value itself. With ‘100’ being prices in 2001 I believe. So 300 means 300% increase relative to price on the date the index started.

Yes, thanks. But an index value of 300 means a 200% increase since 2000, and an index value of 400 means a 300% increase since 2000.

Got it. Thanks.

Everyone in the thread seems to be calling San Diego and LA a bubble. 400% in 23 years is strong performance… essentially doubling every 11.5 years. Essentially, that’s strong returns on an investment. I don’t know if bubble fits… there are just a lot of people that covet SoCal real estate. I’m pretty versed on SFR real estate in both cities, and they have a lot going for them.

Both cities have diverse economies: this is newer for SD, as the economy has definitely diversified with tech (Apple bought hundreds of acres recently), biotech, pharma, etc since the last bust, in addition to defense, education, healthcare, and Qualcomm which the city has always been strong in. LA has a famously diverse economy. Tons of jobs being created, and both cities are basically land locked at this point. Building density is a MAJOR issue in terms of both cost and time for LA, SD is a little better, so new supply is stagnant.

Demand trends are still positive: migration from NorCal and other areas remains pretty consistent. There’s a good chunk of AirBnB operators buying and foreign buyers as well, though I’m not super happy about some of these activities as it takes homes out of the hands of American families, but it does keep prices high.

Climate predictions seem to show coastal SoCal should avoid a lot of the brunt of temp extremes (though we may actually get hurricanes, which is just nuts to think about).

I dunno. It’s hard to find holes in it other than just that the prices are so damn high so they must inevitably come down. Buyers have a ton of money and a ton of income… just depends on whether they want to spend on a house, which–so far–they seem fine doing at least for now. We’ll see how the prices hold when recession hits. I think prices will stay pretty flat assuming rates come down as well as in previous recessions.

J Bank,

It’s just set to have a value of 100

at the start of the series, if I recall

correctly. So there are no units.

J.

Buyers strike may have finally hit Seattle. You may remember me as the guy who said Seattle prices were rising last spring and the wolf bears all doubted it. Let’s hope things finally start decreasing.

All the Chinese money is pouring back into Vancouver, Canada real estate via foreign students from China.

Like the Japanese money that poured into Rockefeller Center about 3 decades ago? LOL!

Yup SD and LA are definitely the last tip of Titanic…or maybe they will end up being the life raft instead..stranger things have happened before…

Yes. Remember Sydney and Vancouver, or more broadly Canada and Australia, a little pause in 08, then Zoom!

You cannot compare Canada and the US for housing prices. Massively different dynamics. Canada is f’d when all the 2% mortgages come due in 2-3 years. The US 30 year holders can sit tight and be fine.

Well, I don’t think that’s quite right. Your assertion that the US holders of overpriced assets with an absurdly low mortgage for 30 years are insulated from the carnage that is likely to occur to the least deserving to be punished by life as they renegotiate their ARM mortgage just as the cold wind of recession, unemployment, and foreclosure inflict.

The US exemplars, can’t sell the shack they overpaid for, without going into debt. The cold winds of recession blow without preference.

It looks like real estate prices hit bottom in Canada last month and will go nowhere but up. The Chinese real estate ponzi just moved from China to Canada with the Chinese buying up everything they don’t already own. The Bank of Canada is hellbent on saving the banks/lowering interest rates but they won’t have to worry because the Chinese both local and foreign will save all the banks as home prices keep rising.

“It looks like real estate prices hit bottom in Canada last month and will go nowhere but up.”

No, it doesn’t look like that at all.

The Home Price Benchmark Index for single family houses in Canada dropped 1.6% in October from September, the fourth month in a row of month-to-month declines (CREA).

“The index is down by 15.6%, or by $148,400, from the frenzied FOMO-inspired peak in March 2022. But not all markets are getting hit equally: Some haven’t gotten the memo yet and carved out new highs, while others have gotten hit a lot harder than the national average.”

https://wolfstreet.com/2023/11/15/the-most-splendid-housing-bubbles-in-canada-prices-drop-to-where-theyd-been-2-years-ago-sales-swoon-supply-rises-further/

Greater Toronto Area (GTA): The MLS Home Price Benchmark Index for single-family houses fell by 2.1% in October from September, to $1.318 million, the fourth month in a row of declines after the FOMO mini-spike in the spring.

From the peak in February 2022, the index has plunged by 17.2% or by $273,200.

Thanks, Wolf — I have no idea what Tony is looking at.

Most of the charts look as though there was a spike, then dropped back to the trendline they were already on. There seems to be a floor of resistance.

Well the market thinks the Fed is gonna cut rates. The trend is down on home prices. I can thank Wolf for that, otherwise I would have thought they were up. I think another hike coming from the Fed, rates are volatile since last Fed meeting.

Think the Fed will surprise the market next meeting and raise while most think it will be held? I don’t think Fed will want to surprise so probably not a hike this time.

Florida prices still crazy, but more inventory is coming on and more price cuts from what I see. The good stuff still goes pending quickly and ends up selling 40-50% more than the same place sold in 2020 without renovations (this is the $1-3mm range, which is crazy imo). Average and below average places aren’t crazy like that thankfully. Lots of construction going on still…shopping centers, apartments, condos/townhomes, and SFH…

The Fed can’t raise rates before the Christmas buying season. Remember how the 10 year treasury bond magically fell half a point right before Black Friday sales?

So I’ll just repeat this here:

It’s volatile, my friend. It’s volatile.

Lookie here. There have been much bigger retracements over the past two years, and before. It’s just a bunch of short-term bets, such as Ackman going out and promoting his latest bet, and the doofus reporters/bots at the WSJ, CNBC, Bloomberg, et al. are carrying his water, and after everyone jumped in, he cashes out. That’s what makes a market, and causes the volatility:

My opinion is the drop then rise in 2023 correlates directly to when the Fed started to bail out banks in 2023.

The real estate market was decreasing with the rise in rates. As soon as buyers saw the feds would continue to bailout banks (and the economy) they jumped right back in.

While I think the Fed should get tough, raise the FFR by 25 bpt and let it be known that zero inflation is the current target.

They will perform a drama about their decision to hold the current rate. And reaffirm their commitment to stop being the cause of inflation. And promise, as soon as they can, they will apply the monetary tools that they possess too achieve 2 pct inflation.

All the while, allowing inflation too make overpriced assets less expensive for working families whose income has been increased by some measure of income. If they’re income increases less than the increase in prices, the people become poorer, over time.

Not a scenario the promotes the so called Democracy that we hold sacred.

Its all downhill from here on folks.

Lots of folks have been saying that for years now, but they’ve been very wrong. Just look at the charts.

Not to say we wont have a down cycle, but guessing when is a fool’s errand. It’s always just different enough to make a lot of smart and not so smart folks look really dumb.

I agree with your astute hypothetical possibility about all of our, frankly, ability to devine. Contorted by reality.

Got to keep values UP to support the Mortgage Backed Securities…..OR ELSE

Plebes

Case Shiller data is way too dated to pay attention to. I follow real time housing data in my markets in SW FL. The numbers aren’t good. My take is we have a 2001 style correction. No big deal unless you bought during the last 18 months.

I agree, it doesn’t track relatively new homes which are dropping like a rock. See Austin, TX.

I’d say more like 1987 when we were coming off high inflation.

Back then, stocks were the catalyst. Lets see what ignites things this time.

Will be interesting when the rate hikes really start to impact prices significantly. Rate hikes have clearly impacted volume but haven’t significantly moved price points. I live in a housing market that significantly benefitted from the pandemic so that is likely a factor.

There are very few places that didn’t significantly benefit from the scam.

I’m in Palm Beach County, Florida, an area that benefitted from the pandemic as well. It’s my theory that many of the 2020-2022 arrivals were “work from home” people where the jobs never really followed them. I see the trend reversing, with stuff sitting on the market. But it’s not going to happen immediately.

Back in the day, just after the GFC, asset prices had declined to a point that my FIA advised me to buy the stock market. I explained too him that I thought the Fed was going to reform the criminal financial oligarchy they had created. He looked at me with that GI look and said they’re not going to do that. I should have listened. maybe. no.

What’s going to happen first?

Airbnb ARMs reset or interest rates go down?

I don’t know, but “Spring Selling Season” opening day is like 4 weeks away. I remember last January and all the real estate “green shoots”. The plan is apparently to just keep kicking the can until rates go down.

As far as the Case-Shiller index is concerned, which lags a lot, it will start in half a year exactly. The CS will pick up the spring selling season with its release in May (three-month average of January, February, and March). So we still have Dec, Jan, Feb, Mar, and Apr in between then, and May will be the 6th month from now.

“The plan is apparently to just keep kicking the can until rates go down.”

My view is that the moment the Fed or any central bank cuts interest rates even a little bit, the mass of people will go back to buying. This will send inflation skyrocketing. So I’m betting that interest rates will stay at these levels for a very long time.

The only thing that would make banks raise interest rates without doing QE is a recession.

The only thing that would cause the banks to LOWER rates without doing QE is a recession.

Interest is the price of credit. The price of money is the reciprocal of the price level.

Bernanke held the means-of-payment money supply constant for 48 months, then remunerated interbank demand deposits thereby bankrupting half the home builders.

Powell has only been at it for 20 months.

The lag in interest rates is about 6 to 8 months. So subtract 6 to 8 months from the 2024 election date for the first Fed funds rate cut. In the March to June time frame.

The Real Tony

*So subtract 6 to 8 months from the 2024 election date for the first Fed funds rate cut. In the March to June time frame.*

After the election, add the increase in reduced rates to their current level and add another 1 could be 1.5 or even 2 percent.

Otherwise, your inflation will spiral out of control.

Firstly, a plan is not consistent with any accurate description of a free market. I’m guessing you have accepted the current level of a corrupt government as normal.

Great Tanta’s Ghost! I see a mortgage pig emerging from those charts. Second ear and round shoulder would complete the sacred real estate formation.

Time will fix it, LoL

These graphs are insane.

This isn’t a bubble, this is something else entirely.

I can’t escape the thought that everything is completely rotten, corrupt, fraudulent and that society is unravelling.

And I know I’m not the only one having these thoughts.

Of course, if you’re a homeowner you obviously look at the current state of things different to someone desperately looking for a house for the past 10 years.

Properties in my area/country have doubled in 5 years and there’s no sign of prices coming down or supply coming on the market.

And then there’s 150.000 immigrants a year on a 5 million population with a shortage of 500.000 houses.

Ireland will be a completely different society in 10 years time and I doubt I want to be a part of that.

If anyone is even reading this I can inform you that the current mood is quite rotten over here. You’re either completely supportive of tens of thousands young, fighting age men without families, wives, children coming here and given 3-star hotel-accomodation and holidayhomes plus an allowance….or you’re far right hateful undesirables.

There’s no inbetween apparently. Would you stay in a country like that?

If I was looking for a good independent home builder in Chicago metro area (I’m not, escaped a few years ago) I would check at Gaelic Park in Oak Forest in sw burbs. More real Irish contractors there than The Old Sod. All of the ‘national’ builders near where I’m at now build embarrassing crap, with ‘amenities’.

“Desperately looking for a home for the last 10 years”

Really???, H, You only missed the lowest interest rates in your lifetime and the history of the mortgage world as well as some of the the cheapest houses in this century. You could have locked in 30 years of the lowest house payments ever in 2013, 2014, 2015, 2016, 2017, 2018, 2019, 2020 and 2021.

What were you waiting for?????????

Not everyone is able to get a mortgage or even wants to.

The 10 years I mentioned included some life-changing events.

It’s quite easy to comment on ‘you should’ve done this or that’.

In real life, stuff happens.

But what did undeniably happen is another insane housingbubble in Ireland combined with a massive influx of approx 1 million people resulting in a current shortage of at least 500.000 homes.

And also, low interestrates don’t make any difference when you can’t qualify for any kind of mortgage with completely disconnected wages vs houseprices being out of touch with reality.

And that’s happened more than a few times in Ireland.

I guess you need to broaden your view outside of your own circumstances to find that a LOT of people are in the same exact position I find myself in.

Government legislation doesn’t help in most countries, I find. People can’t get mortgages that would have a payment at the same or lower level as they are forced to pay in rent. So these equity gains have ended up in the hands of investors who already had the money to buy.

Harry,

A local and unpopular couple just up and sold their property where I live ( mid Vancouver Island) in order to move to Ireland. He is German and she is English. Blow-in immigrants who will tell all who will listen what they should do and what they are always doing wrong. From what I understand bargain hunters are becoming intolerable for you folks, overwhelming. We get the same thing here but most new arrivals don’t last more than 3-5 years before they move on. Good luck as this goes forward.

Additional info: Know two folks with property who are planning to relocate. They are now going to purchase pre-fab modulars as opposed to having homes built for them by a contractor. My brother in law will be building their foundations and offering guidance. I no longer build for a living but keep my interest and hand in doing renos, etc. I recommend modulars all the time for efficiency and cost savings. These are not the trailer towns that tornadoes love to level. I believe it is the future, 1,000-1200 sq foot modulars with small amounts of customization to make them personal. They are to code and very energy efficient. After installation, which takes days….not months, buyer can jazz up decks etc to make the design personal.

It is one realistic way to save money and allow more people to own homes.

Thank you Paul.

At this stage, it’s either a scenario of finding something in 12 months or leaving the country.

Because the political and media-class here in Ireland are giving signals to a course of action I simply cannot agree with.

This isn’t going to be solved in 5 years or 10 years or possibly ever when they continue this destructive policy of bringing in 150.000 people a year to a country that already has a shortage of houses that can never be solved.

Ireland has been captured by EU conformists, the Green party with unrealistic ideals, NGO’s, large tax-evading corporations and a bankingcartel consisting of 3 banks that STILL pay savers 0,01% on deposits while receiving 4% from the ECB.

But the worst part has to be the media.

There’s simply not a word in existence to describe this level of collusion, gaslighting, lying and spinning.

So there’s anger and then there’s desperation. I can tell you, a LOT of people are way past desperation.

But you must understand, this is not a unique situation. Germany, Holland, France, Sweden, etc are ALL waking up to the reality of mass-immigration.

Up to 70% of German immigrants are on welfare. So the myth that mass-immigration is beneficial has long been busted.

When your own citizens can’t even access the basic right of housing, something went deeply wrong. And when healthcare is overwhelmed that’s another lifethreatening consequence of irresponsible and unsustainable levels of immigration.

Sorry for making this long and slightly off topic, but it’s not really off-topic. It’s THE number one reason for the housingcrisis in Ireland but we’re not allowed to talk about it.

If this hate-speech bill passes here, I might very well expect a knock on the door from the police-department because of being critical of immigration.

That’s Ireland in 2023.

Harry, well said.

In the U.S., when people voice concerns like this, the open borders crowd screams at us “We’re a nation of immigrants!” This is despite the fact that times have changed in terms of needed skills and needed population.

Ireland doesn’t have that excuse. There’s zero reason for mass third world immigration into Western nations. If the problem is one of population, incentivize young couples to have children.

Hi Harry

Don’t come to Canada. It’s exactly the same here!

2008

I had the audacity of being 20 years old, graduating with student loans with 9.8% rates, starting my career during a period of historically depressed wages and being laid off during covid when rates hit rock bottom. And every year from 2012 to 2020 median sale price of homes marched up 25k. Rent inflation averaged 5% for those years. Theres a reason the median age for first time home ownership has gone up 20 years since the 80s.

If I could do it all over again Id buy Apple when I was 3….

That’s happening throughout the West. Ordinary people in Western countries nearly universally opposed this, and it was foisted on them. This won’t end well.

Einhal,

Wow, this is happening everywhere in the world!

By design. They want nations of rentslaves who need to work their entire lives. Homeownership is a path to financial security and thats bad for the bottom line.

I read in the history books that 1/2 of Ireland moved to the US in the late 1800’s.

I had two grandparents come to the US from Ireland in the early 1900s.

In the 80’s on my first visit to Ireland (when I still had living great aunts and uncle’s living there) I didn’t see a single person that didn’t look “Irish” (and most bartenders had a thick Irish brogue looked like House Speaker Tip O’Neill)

In 2005 I went back to Ireland and it was a LOT more diverse (and it seemed like most of the bartenders in the West had eastern European accents and looked like they were related to Vladimir Putin)

“Would you stay in a country like that?”

Probably not. After 35 years living outside a major city, I moved my family 700 miles and have never been happier. That said immigrants are still flocking in because they see the promise of something better than what they left behind.

I had a co-worker from Uzbekistan who lived in NYC’s outer boroughs make a similar complaint one time and explained it to him like this. Capitalism won’t dictate where you can or can’t live but if a place is popular and overcrowded it will make life increasingly difficult until enough people quit/leave and balance is restored. You can look around at all the wonderful things your place has to offer and decide its worth the sacrifice and hustle, or you can find a less desirable place that offers other advantages to compromise around. The struggle you experience is the cities way of saying that it’s overcrowded, there is a competition going on, you’re not winning it, and you’re no longer welcome, but you can stay if you really want to.

Other places will offer less career, transportation, and entertainment options priced accordingly. I have friends who THRIVE in a city but personally have always preferred a quite place in the country but even then it took me a long time to get out. Giving up the rat race represents a huge shift in priorities, no wrong answers, competition exists everywhere, just find a place where the terms and pace best fit your priorities and you’ll be happier for it as long as you go in with the understanding that their is always a compromise somewhere…. Good luck.

Since I was born in the shadow of the WW2 armistice, I can’t escape the thought that everything is completely rotten, corrupt, fraudulent and that society is unravelling. I had similar ideas while I awaited my 18th birthday and the Vietnam draft lottery.

What I find interesting, is that the resistance that the common man has their elected officials in Congress.

Wokesterism, a philosophy of neo-Marxism, racism, and rabid collectivism, has totally captured governments everywhere. But especially in the cities, from which their corrupt and degraded ideas spread out to the general population.

No, Harry, but then again my family escaped that place almost 200 years ago now …

On the ground anecdote in my local market:

We’re looking to rent yet again because the interest rate hike has completely screwed up our house buying plans. 3 times now we’ve run into houses that were for sale, but were taken off the market because the owners “didn’t like the prices they were being offered” and aren’t under pressure to sell. We never came across these situations in prior searches, so it’s a recent development.

Rental yields are lower than you can get on risk free cash in my area, and that’s before property taxes and maintenance, so there’s chunky opportunity cost to their decision. I think these owners view the house as their nest egg, and they feel comfortable because prices in my area have held so far and, well, house prices never go down, do they? I wonder what will happen if/when they start losing equity? Has the potential to snowball.

Hmm. On reflection, I wonder if this is common enough to be distorting our local index? It’s one of the “new high” ones. If enough sellers are refusing to participate unless they get a crazy bid, then the index has a very heavy selection bias and could rise even though the “true” house values have declined. Would be accompanied by a collapse in volume in that case.

Interesting….

I found the home pair counts here:

https://fred.stlouisfed.org/series/SPCS20RPSNSA

The 20 city index is down around 23% yoy in count. Our local market is down over 30% and is at the same level as the great recession.

Yes, roughly in line with existing home sales across the nation in October: -27% from 2019, -39% from 2021

https://wolfstreet.com/2023/11/21/home-sales-collapse-prices-drop-further-supply-jumps-people-are-finally-on-buyers-strike/

You will see the same style of charts in new and used cars in 2021. Car makers were making and selling few high end vehicles which skewed the charts much higher then they would if they made more cars and sold a variety of models.

Been in the residential rental business for a while and I’ve never seen the buy vs. rent equation shift to such an extreme in favor of renting.

This economic misequilibrium will have to eventually resolve itself somehow. Either houses have to crash or rents have to rise materially, or some combination thereof. Unless you buy properties in the slums (with all the associated headaches that come with that to a landlord), then if you include financing costs, in many markets you simply cannot make a positive return on newly-purchased residential real estate at this time. This is a very unusual situation from a historical perspective.

“Either houses have to crash or rents have to rise materially, or some combination thereof.”

I have been pounding the table about this mismatch as well.

While I fear the outcome from an asset price crash, grateful that monetary policy is preventing the violent collapse of asset prices.

What I really feel is a moral sadness that our government has lost it’s integrity.

I’ll second that here. Where I am in South Florida, $500-$600k houses rent for $3,000-$4,000. The numbers don’t work out. Anyone buying today intending to rent it out is insane, in my opinion.

I think the reason that these owners are taking on chunky opportunity cost, as you state, is that there’s something emotional about selling for less than you could have gotten 18 months ago.

At some point, these people will have to sell (rentals are sitting empty too, more so than before), and then the “shortage of inventory” will become a “glut of inventory.”

I have been looking at 2 bedroom rentals (SFH, duplexes and townhomes) in Los Angeles. They are sitting longer and many that were asking $3k are now down to $2750 and some close to $2500.

In my condo complex in the best part of San Antonio, there are five units available for rent:

3 bed 2.5 bath $2100 down $400

2 bed 1 bath $1150 down $75

2 bed 1 bath $1195 down $25

1 bed 1 bath $1200 down $75

1 bed 1 bath $1200

All of them have been empty for months with almost zero traffic. I know because one of these units is directly across from me. I saw someone look at it a couple of weeks ago.

@Einhal,

“Anyone buying today intending to rent it out is insane, in my opinion.”

To me, too. I know many who have bought to rent and/or are looking to buy more. While initial yield is low, they expect that over time that yield will get much wider through rent growth and appreciation. History has shown that to be very lucrative, and they assume history will repeat itself.

I wonder how much longer the Boomer gens will find their lifestyle sustainable as younger gens are priced out and leave town.

This is a big issue in my area. Neighborhood is mostly fresh retiree Boomers who lament renters unless of course they decide to relocate and rent to them instead of trying to sell.

Neighbors down the road thought I bought in, and on their walk by smugly shared how the one bedroom small house no one likes is worth over $400k now and I should be happy. When I informed them I rent, work in healthcare, am hanging by a thread and many professional collegues are leaving the state to where they can afford, then wished them a very healthy retirement, the smile left their face.

But, NY is a different beast as the graph shows. An old school North East neighborhood won’t be so quaint and upscale when its rented out by absent landlords to people who can barely afford it. Say good bye to a sense of community, home upkeep, and the service industry. Its already happening around here.

Around here, too (central Austin), and I suspect it’s a going trend in most metros/urban communities. Sucks. I want to go live inside a Jonathan Richman song.

Once the younger gens are broke and fleeing, how valuable will these existing and newly flourishing communities be?

They put in low income ‘artist lofts’ into Peekskill to try to maintain some semblance of culture. Fat lot it does for young struggling families and frontline workers, etc., but the rich folks need their art to launder money through I guess.

There will always be stupid money here, but its gotten so much worse now there aren’t bus drivers to drive kids to school. How can property values hold up once the wealth inequality becomes massively unstable? Who’s gonna want to live where teachers, garbage men and healthcare workers aren’t? A genuine curiosity, not just idle griping.

@random50 when you wrote “aren’t under pressure to sell”. A wise (and rich) man told me once told me to focus on people that “need” to sell when buying and people that “need” to buy when selling…

‘We had a guy walk on pretty much a million dollar deposit on a condo in Vancouver Place last week’ according to a realtor with the Rennie brokerage.

There is an orgy of re-thinking among the ‘buy off plan’ crowd, who put deposits down as far back as 2017 to enjoy the inevitable appreciation. Lawyers are busy but after the GFC, contracts were made much tighter and harder to get out of.

Apart from the folks who want out of projects that are complete or likely to complete, there are folks who might wish to proceed but the projects are in foreclosure and work has halted. If they wanted out anyway, you might say this is a blessing. But what about their deposit?

One lawyer who has handled hundreds of cases involving condos to be built says: ‘this buying of stuff that doesn’t exist yet is not for the faint hearted’

PS: to read about some of the probs in Vancouver, enter ‘Coromandel’

The builder can stall seemingly forever and collect all the monthly condo fees and other fees from the unbuilt condos also seemingly forever. This is the main reason most walk away from their deposit hoping they don’t get sued for even more money from the builder. The Canadian government recently tried to kill off assignment sales in Canada and more recently AirBNB.

That would be called totally illiquid futures! You have to take physical delivery at expiry. Ballsy, and yet available to anyone with a checkbook thick enough.

I’m still amazed that Zillow Manchester NH price index is still up 8.5% YOY and here we see Boston hitting new highs. Seems there’s plenty of money to go around despite the very high prices and higher interest rates. I’m glad we bought 8 years ago; we would have a hard time paying the $5000/month mortgage (with escrows) if we bought our house today and we make decent money.

I commented on this in a few posts above (didn’t specify Boston, but that’s our market).

We’ve come across multiple sellers who are instead renting because they didn’t get the price they wanted. This potentially creates a bias in the index because the people who did get the price they wanted are included (they may have got lucky or there’s something especially nice about their property) while the true market price of the seller turned landlord’s property does not get included to balance.

I agree, and I think prices dropping is more likely, but many others, like a poster in the other thread, wrote that rents are too low.

I personally think rents are close to the top of what many people can pay, so I don’t see how they can go up substantially.

But you point out an interesting phenomenon. People aren’t willing to sell for below the March 2022 (or whatever it was) peak, so they rent it out. But eventually, they’ll realize they’re losing money, and sell.

Many things, like stock and house valuations today, only make sense if you assume a return to ZIRP in the next year.

Someone is going to be in for a world of hurt. Just not sure whom yet.

“I personally think rents are close to the top of what many people can pay”

The thing is, everyone has fat they can trim from their budget. Most Americans are not that poor.

I have poor friends – as in “hey can I borrow $20 for gas so I can get to work this week” poor, yet they still overspend on things like takeout.

If the rent goes up, they’ll figure it out because moving is likely still more expensive.

That isn’t a bias. That’s exactly how a supply curve works. Sellers at the margin either accept the price, or hold back from selling at the market price. If prices rise, the sellers at the margin start selling at the new market price.

Is it me or do a lot of these charts also look just like the S&P500 stock index since 2002.

Well, I guess they’re both sets of assets, right?

Spread on the 30-year mortgage over the 10-year has remained well in the high risk range for over a year, and it seems to be getting worse. No one is talking about this.

Why Charlotte, why?

Why do these idiots keep buying McMansions. It’s gotten to nearly two million dollar homes in my neck of the woods.

The traffic there is horrific

I’ve written off Charlotte. Hell, I hate crossing Raleigh nowadays.

I was coming into north Raleigh from Virginia, I was so lost. Took an hour to get thru the gummed up mess.

Well… the low cost of living and the dropping state income tax rate have something to do with it. :) When you have people from NYC moving to Charlotte, a $2 million house on the south side feels like a bargain to them. I can understand Charlotte – because it is growing and much of that growth is mid-high end. What I CAN’T understand is Boston and NYC, which are seeing record population out-flows, with a lot of those people being on the upper end of the socio-economic spectrum.

There’s a very clear East vs. West bifurcation in the US housing market. It’s like there are two different countries when it comes to housing.

Regardless of price, there are two different countries…one is west of the continental divide and the other is east of the continental divide…

Maybe some of the “poor” Chinese from China own real estate on the west coast of America. They got tapped out when the real estate market crashed in China. In Canada all the money coming into real estate in Vancouver and the province of British Columbia is coming in via foreign students mostly from China after the Canadian government barred foreign township. Prices are poised to move to all time highs out west.

It really is amazing – even as rates have gone up so much, the bubble – which started to deflate- has been re-inflated.

Put it down in part to Gulliver-scale salary gains in the past three years? With take-home rocketing up by 30-60% in some instances since the pandemic, the US seems stuck in a perpetual shopaholics unanimous meeting. What’s gonna stand between Mr & Mrs Big Stuff and their dreams? Certainly not an 8% jumbo mortgage on a house marked up by $150k in just 18 months since its prior sale.

Some of these charts give “higher for longer” an entirely new slant.

@bulfinch,

My co-worker just left the company where I work. He got a 48% pay increase! He was way under paid for his experience and education. He is a mechanical engineer with a masters degree in materials engineering. This is a game changer for him.

American Yale Professor Irving Fisher’s “price-level” is still rising. Rates-of-change in money flows, the volume and velocity of money, the proxy for inflation, is still accelerating.

Any downward shifting will come from a fall in the transaction’s velocity of money.

At some point in time the rent component in the CPI will level off. Soon after that the Fed will cut interest rates. June 2024 will probably be the latest date for the first Fed funds rate cut.

In Cleveland, Ohio I’ve notice softening of prices at the high end but not really anything under 350k.

Flippers are still making money hand over fist, rents are still reasonably high even with increasing vacancies due to new apartment builds.

I never thought I’d see $3700 2 bedroom apartments in Cleveland but they’re here in new buildings. I foresee a slow progression downwards over the next 6-7 years. No spectacular drop unless foreclosures rise sharply.

That will only happen if unemployment goes up above 5.5%-6%. This is when we see meaningful declines imo

Wish I could figure out many of the plausible variables. Seems like if we get higher unemployment that depends on where it hits but if just service businesses cutting back that may not really impact the housing market. Increasing unemployment might put pressure on the Fed to reduce rates which might entice more sellers and buyers to get back in the market but may not move the price down at all. Just seems like we will be stuck in this type of cycle given so many people want to hang into that low 30 year mortgage. Even in my case where my house is paid for I want to see how things evolve until mid 2025 at least as 2024 looks like a nothing burger. I wonder if the upcoming election will make rent affordability an issue although not clear what really could practically be done. Only positive seems to be if you want to sell you should be able to negotiate a low sales commission.

Compared with last month, more metros have new high, fewer have dropped from 2022 high.

Data from Oct, Nov, Dec are crucial. If it doesn’t drop too much, 2024 will push for new high.

In reading all the comments I think we are in a bear market rally in everything! I’m taking what they give me. Five percent plus! For now. Cash is no longer trash, it adds up for when it does come down more.

NYT’s had an article comparing corporate debt to homeowner mortgage debt.

While homeowners were locking in the low mortgage debt, Corps were locking in as well.

Basically everyone wants to ride out inflation so the high rates do not affect them. But if the fed lowers rates, inflation may just start up all over again. It’s like the game Green light Red light.

Inflation is a result of policy, not a banshee. QE is the cause of inflation.

The overproduction of cash, stimulated a price indiscriminate over expenditure by those holding the cash. The roots of inflation hasn’t been a mystery for thousands of years.

Fed rate is still around 5%. 5.25-5.50. Wolf mentioned prior articles just too much money for Fed to be restrictive enough. Market seems to be taunting the Fed or just making money out of thin air with these rallies. Time for action in my opinion to get the market and curve in order. Wait for it in my opinion.

I agree completely. Yesterday, Christopher Waller of the Fed made a couple of dovish comments about the possibility of rate cuts in Q1, 2024, if inflation “continues to fall”. It was enough to cause a minor bond rally and dip in mortgage rates. It’s like the entire economy is poised and waiting for any sign of a Fed “pivot” towards rate cuts – without first popping the asset bubbles caused last round.

Inflation isn’t falling, it’s decelerating.

No, he did not and there will be no Federal Reserve ‘pivot.’

Assume they will do the most corrupt thing to keep the rich richer and the poor poorer. And that means return to zirp as quickly as possible. So long as prices of cheap goods stabilize they will say the inflation battle is won and revert to policies that make the expensive necessities like housing march up 5%+ a year. I expect cuts Q1 of 2024. Tomorrow another pause. QE probably in 2025.

You’re forecasting, and OK, people forecast all kinds of stuff. But this line, “QE probably in 2025,” is nonsense and wishful thinking because the Fed is done with QE. It’s going back to the pre-2008 way of dealing with market chaos, namely short-term liquidity injections, as in March 2023. It now has revived its standing repo facility (again) like it did before Bernanke scuttled it in 2009, and that’s what it used during the 9/11 period when markets first shut down and then froze, and after a few weeks, when markets settled down, the liquidity was withdrawn.

The Fed has gone back to the future – as March 2023 showed, when people hyped this as the new QE, when in fact it was just short-term liquidity injections while QT continued.

I wouldnt call it “wishful thinking” more just doom posting. I pray your right, I honestly do. But I have to prepare for the worst, and QE would be the worst. We have no idea how the fed will respond to a recession. Will it simply be rate cuts? Will they already have cut rates so the housing and stock markets could double? Will they be forced to pull the QE card again? Who knows. But theres little sign of housing prices recovering substantially before any rate cuts, and rate cuts will pour buyers back, and these are millennial buyers, first time home buyers, so them buying wont also mean selling something. This is going nowhere fast. This bubble wont have the 5 year burndown it needs before cuts are on the table… and who knows what else.

Easy to label things good or bad but more reliable to adjust to what actually is likely to happen. Admittedly easier said than done but best to be positioned for a variety of scenarios and of course you own personal needs, income versus long term, etc. Our system creates an every person for themselves mentality and while I don’t like it I have no ability to change it but that is another topic altogether.

LOL! Not without losing dollar hegemony. Wolf has done a good analysis of this. The Fed can do QT all the way down to approximately 5.5 trillion before global monetary explosion. I doubt they will get that low, but you get the idea. They must remain higher for longer in order to preserve their power and control, period. I will maintain that The Fed, like myself, is wondering who is going to show up to buy all the new debt that has to be issued. Your move CONgress…

Either way, these Fed people need to STFU.

I would say the Fed has already cut by at least 50 bpt following Powell”s wink and nod performance, feigning concern about monetary policy being the cause of of the current inflation.

So for those of us living in the central and eastern US, prices more or less continue to rise at a decent clip, at least when comparing YoY statistics. Most of this “housing bust” narrative has been relegated to the frothiest of markets on the West Coast. This is in spite of mortgage rates spiking massively to 7-8%, which underscores just how resilient the market has been.

Homes definitely seem to be sitting on the market longer in my neck of the woods (Boston suburbs) but most well priced homes continue to sell in 1-2 weeks. If 10-year yields continue their downward trajectory into winter and spring and mortgage rates follow suit, one might prognosticate new all time highs coming summer 2024.

“If 10-year yields continue their downward trajectory into winter and spring and mortgage rates follow suit”

I’d like to think the market will eventually digest the Fed’s ‘higher for longer’ mantra and yields will react accordingly.

I too have been frustrated at how sticky Boston prices are, but what goes up must come down.

I think the market has fully digested the Fed’s intentions and have decided to call the Fed’s bluff. Should the bubbles begin to implode then the Fed will blink and bail the gamblers out, again.

Ignoring the disaster that is commercial real estate, single family housing in the southeastern part of the U.S. seems to be just fine. Then again, this is no real surprise as the southeastern part of the U.S. has been largely ignored for a long time and has the last remaining large swaths of inexpensive, arable, land. I am painting with a broad brush I know, but you get the idea.

There is still far too much liquidity, in many other forms. Look at bank reserves and all the “emergency” lending being done by the Fed, plus deficit spending by congress. Rates are going up, they have to.

Not necessarily. Government can simply take on more debt as part of GDP like Japan and even cap rates, although that would be most unlikely. There aren’t that many rules they have to follow and short term gain versus long term solutions always seems to win out. A new ‘normal’ will just be established as not a lot of games in town.

And with that “new normal” more faith will be lost as capital and talent will go were they are respected…

LOL! Japan is a homogeneous culture and vassal state of the U.S. The U.S. cannot follow Japan’s monetary path AND maintain dollar hegemony. Pick one because you can’t have both!

“Full FAITH and credit” and all that.

Well, yes, the government can continue QE to pay for the budget deficits without allowing the market rate of interest to increase which would change the outlook from hopeful too pensive.

Existing home prices continue to move higher after a slight dip in 2022. Incredible resiliency given 7% 30 year rates. Still no inventory, or forced sellers. Unemployment remains extremely low.

Redfin just launched their own home pricing index, meant to be a quicker moving repeat sales index than Case-Shiller: https://www.redfin.com/news/redfin-home-price-index/

The methodology looks promising, though I’m sure people who know more than I can certainly find flaws in it, but it certainly scratches that itch for getting numbers out quicker than CS. I’d love to hear your thoughts on it if you think it’s worth the time to investigate or use as an additional monthly article. Even if it’s just to have a good laugh at it if it proves useless and diverges from what’s actually happening.

Who cares what the price of housing is, at this point, it is overpriced and only a fool would buy a used home under the current circumstances unless they have a different agenda.

Calling people “fools” for buying is unfair. The psychological impact of not having your own place is intense for many people, especially if they have a young family. This isn’t (parts of) Europe where you can enter a rental expecting to stay a decade if that’s what you really want.

Readers should note that calculating inflation on a year-to-year basis minimizes, over time, the rate of inflation since the rate is being calculated from higher and higher price levels. A $ formally, using 1967 (a former base year), is equivalent to $9.35 of consumer purchasing power today.

In absolute terms, each year confronts all of us with a higher and higher level of prices with no end in sight.

Fed’s Waller signaled that they’re gonna pivot soon. Get ready for prices to shoot up again. Fed is not serious about the inflation.

Waller did exactly the opposite of what you falsely assert.

I’ll take the other side of that trade Ben. The Fed is not stupid, quite the contrary, and they know that there is still plenty of liquidity (i.e. unrecognized inflation) in the system. Rate will remain higher, for much, much longer. (Baring some “unexpected” tragedy like war of plandemic…)

The more immediate problem for CONgress is who will buy all the new issuance?!?!? THIS, in my humble opinion, is the ONLY thing the Fed is concerned about right now. They cannot legally buy without increasing their balance sheet. If they do that now, they will lose control on many other fronts…

“Full FAITH and Credit” and all that. Same as it ever was…

And you may ask yourself, “How do I work this?”

And you may ask yourself, “Where is that large automobile?”

And you may tell yourself, “This is not my beautiful house”

And you may tell yourself, “This is not my beautiful wife”

A classic from The Talking Heads.

Of course, you may ask yourself, how did I get so lucky.

1) The median price in PA is 215K. Every city in C/S top five is five times

higher.

2) C/S is a stand alone mountain high above the flyover country. It’s

positively biased.

3) Demand for C/S top ten is down, b/c prices are in bubble territory. There aren’t enough houses for sales in PA. That’s why transactions are down 40%.

4) Dec first is time to pay the mortgage and other monthly expenses. In recession C/S might drop lower, first slowly before plunging faster, when home owners cannot take it anymore.

5) QQQ [1M] flipped up on a low monthly vol. QQQ trend is up, until cancelled. Intel, MSFT, NVDA, IBM… are 20 miles south of Lebanon.

SPY and the Dow flipped lower in Oct. The trend is down until cancelled.

MW: Fed’s Barkin says he is not willing to take another rate hike off the table

Check me on this Wolf but the biggest problem with housing prices might be that average wages haven’t kept up for decades.

Housing prices don’t appear inflated compared to most hard commodities like copper nor do they appear largely inflated compared to the S&P.

They are inflated compared to oil but the West and the U.S. in particular have spent a lot of blood and treasure in the Middle East influencing the price of oil. The need for that appears to be moderating.

According to a recent IEA estimate the U.S. produced 19.8 million barrels/day in October (includes natural gas liquids) which is almost more than Saudi Arabia and Russia combined. Further, many OPEC members are not happy with Iran/Hamas and are putting pressure on Iran which should help keep oil down. Electric cars and higher fuel efficiency standards are hobbling oil prices. Finally, Chinese oil demand is weak.

Wages rising and staying higher for longer will help with the housing problem and perhaps help us avoid a recession.

Meantime, the stock market will continue climbing because most think rates have peaked and will likely continue falling at least into year end.

“Wages rising and staying higher for longer will help with the housing problem”

NO. It won’t help. Higher wages = the ability to pay more for rent or mortgage. Rising wages absolutely contribute to housing inflation. What you’re suggesting is the equal of the government creating all these “affordable” mortgage programs, which of course just allow more people to pay more.

For prices to moderate/fall, the demand for housing needs to weaken. Buyers have to stop being so WILLING to pay so much.

Your comment seems to me to be more of a litany of things that may be at risk of going wrong rather than the things that have already gone wrong. The last thing that is likely too happen is for the long term rates to decline, as a result of the FOMC declaration.

These are the most important charts to highlight the FED’s deranged and destructive money-printing. Turning shelter – a basic need for every human being – into an unaffordable speculative asset for gamblers is the worst policy in the history of the US.

The entire FED should be fired and replaced with new people. Clean house. Instead, nothing will happen, because they are beyond reproach and answer to nobody. In fact, nobody is even allowed to ask questions of them which aren’t first vetted.

No, they shouldn’t be fired. They should be convicted of treason and hanged. That’s what the West used to do with traitors.

Correct. Simply put, we, as a country have been rewarding bad behavior for some 50+ years at an exponentially increasing rate. Good behavior (saving, capital investment in productive capacity etc.) has been punished. Is it any real surprise that we see more bad behavior?

If you don’t understand, then perhaps I can interest you in a financial “product”… …like these mortgaged backed securities. Remind us, who went to prison for that massive fraud?

LOL!

Einhal,

You and Depth Charge are going to outdo each other? Good luck!

I’d like to have a beer with you and Depth Charge, and see who can outdo each other first!

You’re right. Bernanke was the first to censor his staff.

NQ, Nasdaq E mini [1M], at 11:58 : today close is July high @16,062.75.

Insane, that’s all I have to say, this is not a bubble, this is something worse, there is no way people can afford a house at this price with rates over 7% without being underwater once the economy goes down in a recession, Defaults!!! that’s what I see.

So they are all saying Fed has or will cut rates. The yield curve has not even normalized. Wtf?

As I lived through and watched the spectacular collapse of the real-estate market in the late 2007 through early 2009, I am reminded of Bernanke and other idiots like the NAR economist who kept saying it was only a temporary correction. What was left after the carnage of real-estate speculation and the flooding of the financial markets with subprime mortgages sliced and diced as equities was a decade of misery. I have an MBA and my morbid fascination with the bubble and meltdown, which then led to the “Great Recession” was unquenchable. I read all the articles and analysis as well as gathering my own first-hand data regarding the meltdown of real-estate and financial markets during that 2007-2009 era.

This, today, is not a bubble. This is a classic supply and demand scenario. Too few houses, used, on the market, because the people that bought homes, like me, over the past 10 years got loan rates in the low single digits. There is no incentive to sell our houses and then trade in our 3% loan on a 7% loan – it doesn’t make financial sense. So, everyone is holding on to their houses, leaving a very meager supply on the market with a lot of prospective buyers on the outside looking in. The only other competition is new homes, but inflation and rising cost of labor and materials is pricing those new homes out of the market for first-time buyers and those of modest means.

This is not a bubble. Everyone that owns a home and got it in the 2015-2022 timeframe is tied with their golden handcuffs of mortgage rates in the low single digits. Very few houses on the market and way too many buyers. Classic supply and demand. Current homeowners wanting to move up to bigger homes can’t and buyers can’t find homes in their price ranges, because short supply is driving up prices. Classic supply and demand. Not a bubble. Cheers.

You don’t get it. Someone who is not trading up is also not a BUYER in the market. So they’re out as a seller and as a buyer.

Non first time home buyers are about 3/4 of the market. So you’re telling us that this segment of home buyers disappearing is good for the market? Lol.

Bubble is when the monthly home payment rises much higher than wages.

This bubble may never pop , but it still remains a bubble.

BTW, there are absolutely no shortage of homes in USA.

If the FED is brave enough to hikes rates more aggressively ( I am sure they won’t ) then a lot of STRs holders and investors would come to senses that they can make easy money on CDs/Bonds/Bills risk-free than being a landlord.

I don’t think home prices would come down meaningfully in my hood ie san diego but we’d see.

Very well put vadertime, I can’t understand how informed readers of wolfstreet cannot see this. I stated at the beginning of this drop that this was not like the previous bubble and got pushback, then we got the small rebound we are experiencing and I started seeing more comments like yours but still too much pushback. Once the interest rates start moving down housing will start the next leg up and those that have been crying that they have waited for the housing crash will be waiting a lot longer.

@vadertime

I disagree with your argument about golden handcuffs.

Mortgage payments are a function of interest rates AND prices! Yes, if prices remain the same and interest rates skyrocket, existing owners will lack incentive to sell/buy into the new market.

In a healthy market, where affordability is roughly maintained in spite of interest rate changes, meaning that rising rates will lead to reduced prices, you’d be perfect fine exchanging your $3000 mortgage (500k price and 3% rates) for a $3000 mortgage (380k price and 7.5% rates.

Or if we allow for a moderate inflation of affordability, we could call it a $3500 mortgage (440k and 7.5%). In either case, the price drops from the level the golden handcuff people bought at. This is what would happen in an otherwise normal market.

If anything, this golden handcuff argument (which we’ve all heard many times at this point) is actually proof to me that current prices are astronomically unreasonable. They should have come down quickly in the face of rate hikes.

I personally can’t say whether it’s a bubble or not. But I’m leaning towards yes. The fact that few families could even afford their OWN houses at today’s prices and rates tells me that there’s a serious fundamental issue on the price side of the market, and that prices will HAVE to come down to simply meet people at what they can actually afford.