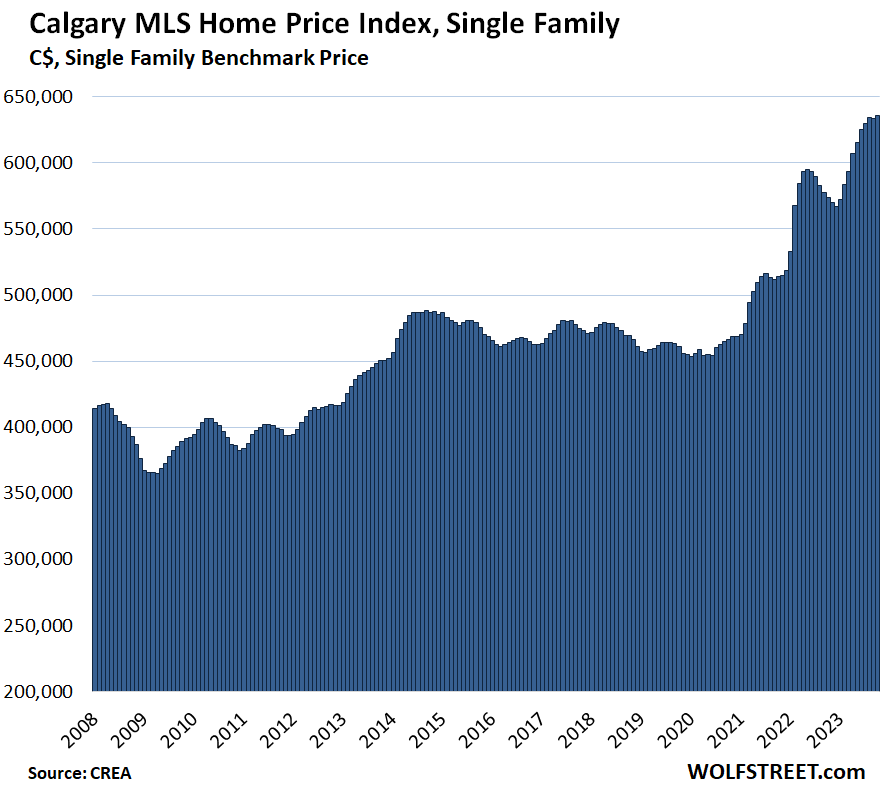

From peak in March 2022, prices fell 15.6%, in Toronto 17.2%. But Calgary reached a new high (still waiting for the memo?).

By Wolf Richter for WOLF STREET.

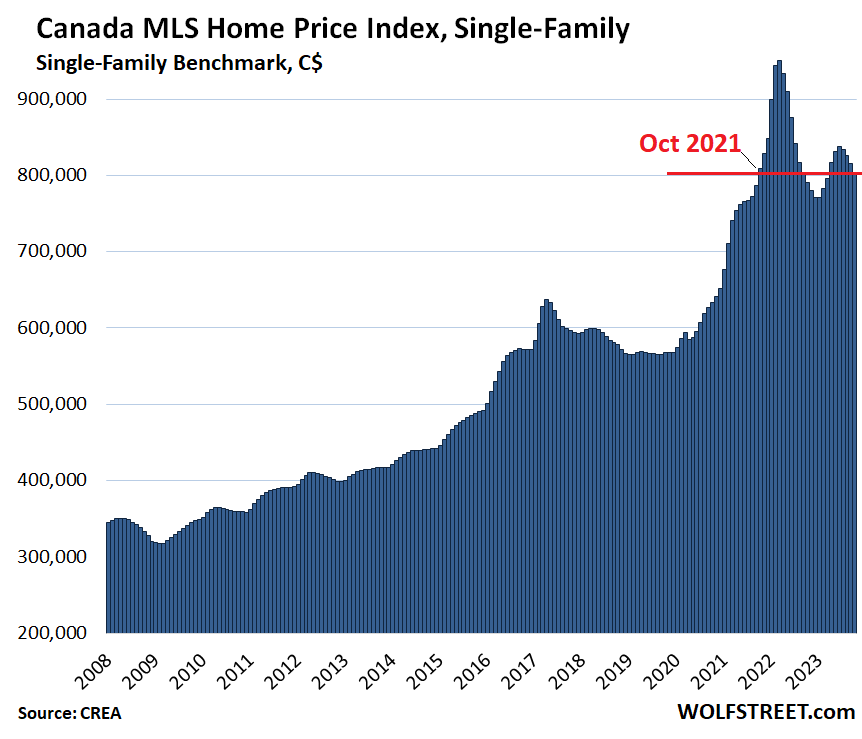

Home prices in Canada dropped 1.6% in October from September, the fourth month in a row of month-to-month declines, according to the Home Price Benchmark Index for single family houses by the Canadian Real Estate Association (CREA) today.

At $802,200, the benchmark house price is below where it had been two years ago, in October 2021 (all prices in Canadian dollars).

The index is down by 15.6%, or by $148,400, from the frenzied FOMO-inspired peak in March 2022. But not all markets are getting hit equally: Some haven’t gotten the memo yet and carved out new highs, while others have gotten hit a lot harder than the national average. And we’ll get to them in a moment.

Home sales swooned by 5.6% seasonally adjusted in October from September, the third month in a row of declines. “The sizable decline was the result of fewer sales in most of Canada’s largest markets,” CREA said. “We’re only in November, but it appears many would-be home buyers have already gone into hibernation.”

And with sales dropping faster than new listings, supply rose to 4.1 months, up from 3.1 months in May. So home sales being low isn’t a problem of there not being any supply, or whatever, but of prices being far too high for these kinds of mortgage rates, and with potential home-sellers clinging to these prices.

The effects of the rate hikes are now on display. The Bank of Canada hiked its overnight rate to 5.0% in July and has kept them there. It has been talking about the excesses in the housing market for two years, and it faces the worst rent inflation since 1983. Canadian mortgages are largely tied to shorter-term interest rates, causing the housing market to react faster to changing policy rates than the US market, where the 30-year fixed-rate mortgage is standard.

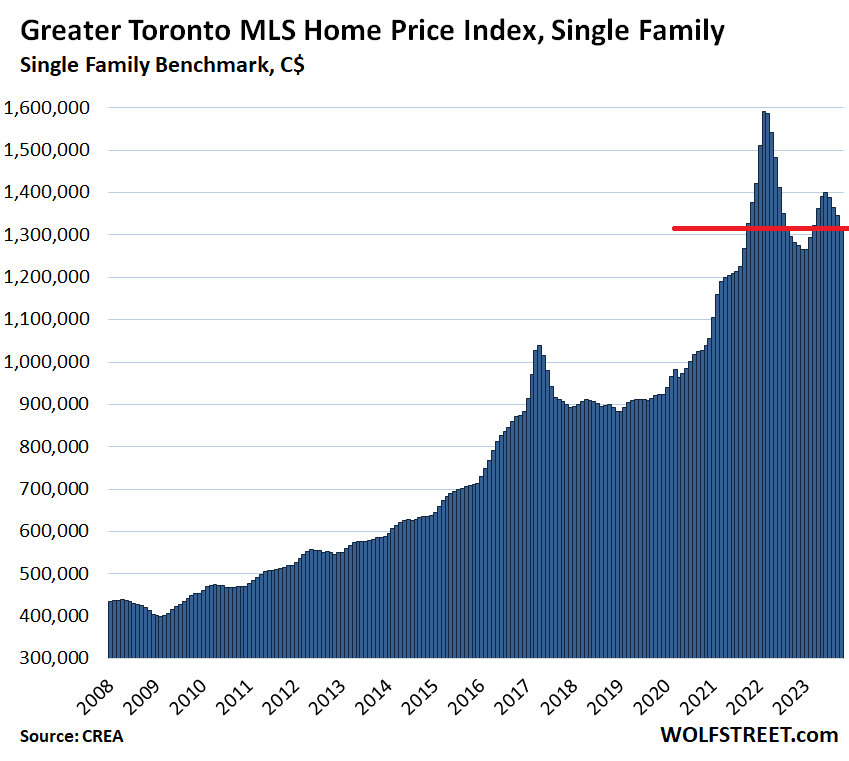

Greater Toronto Area (GTA): The MLS Home Price Benchmark Index for single-family houses fell by 2.1% in October from September, to $1.318 million, the fourth month in a row of declines after the FOMO mini-spike in the spring. The October drop whittled down the year-over-year gain to 2.8%.

From the peak in February 2022, the index has plunged by 17.2% or by $273,200.

These kinds of central-bank engineered easy-money spikes and the subsequent unwinding would be funny, if it didn’t have serious implications.

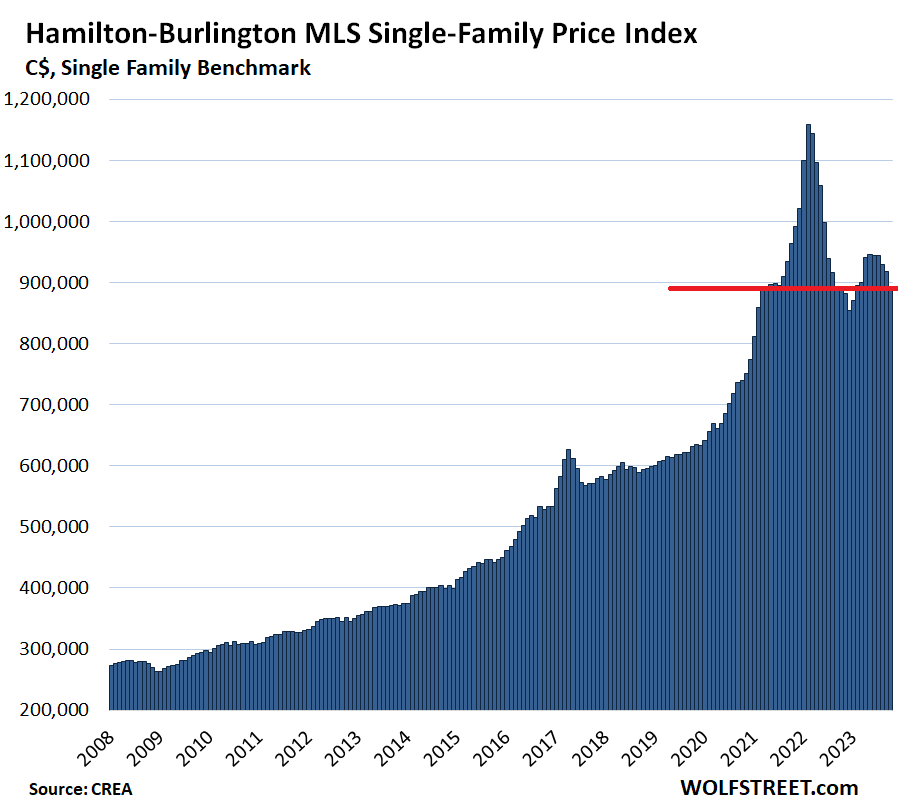

In the Hamilton-Burlington metro (part of the “Greater Toronto and Hamilton Area”), the single-family benchmark price fell by 2.9% in October from September, to $891,200. This whittled down the year-over-year gain to nearly nothing.

- From peak in February 2022: -23.1%, or -$267,700

- Year-over-year: +0.1%.

Another tragic-comic chart of easy-money policies gone awry.

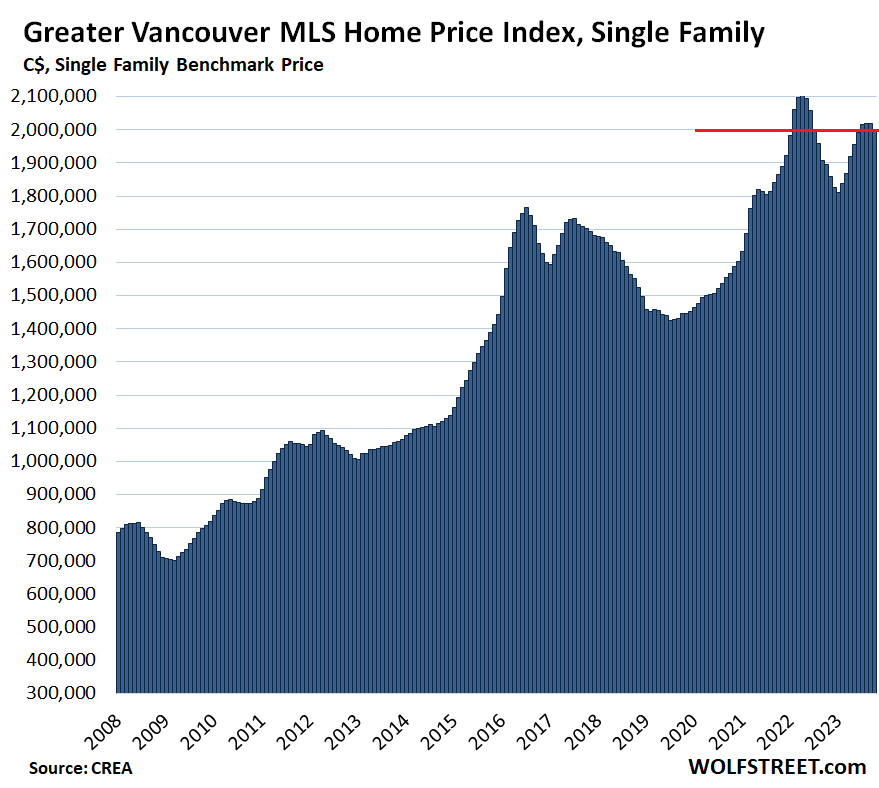

Greater Vancouver: The benchmark price for single-family houses fell 0.9% in for the month, to $2.0 million:

- From peak in April 2022: -4.8% or -$101,200

- Year-over-year: +5.6%

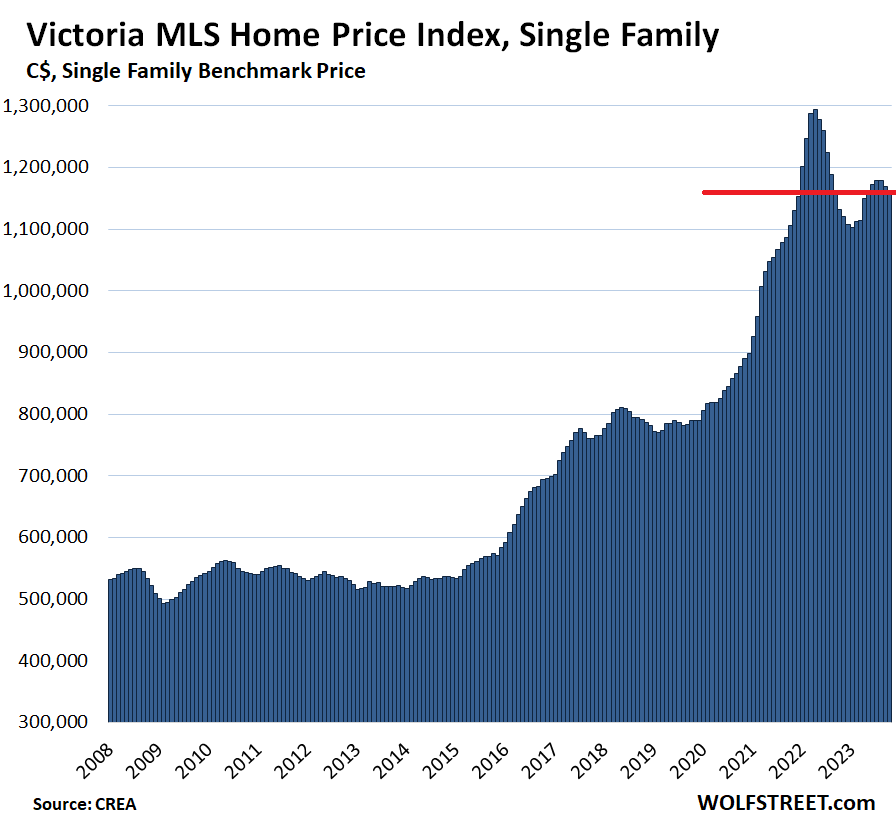

Victoria: The single-family benchmark price fell 0.6% for the month to $1.162 million:

- From peak in April 2022: -10.2% or -$132,300

- Year-over-year: +2.6%

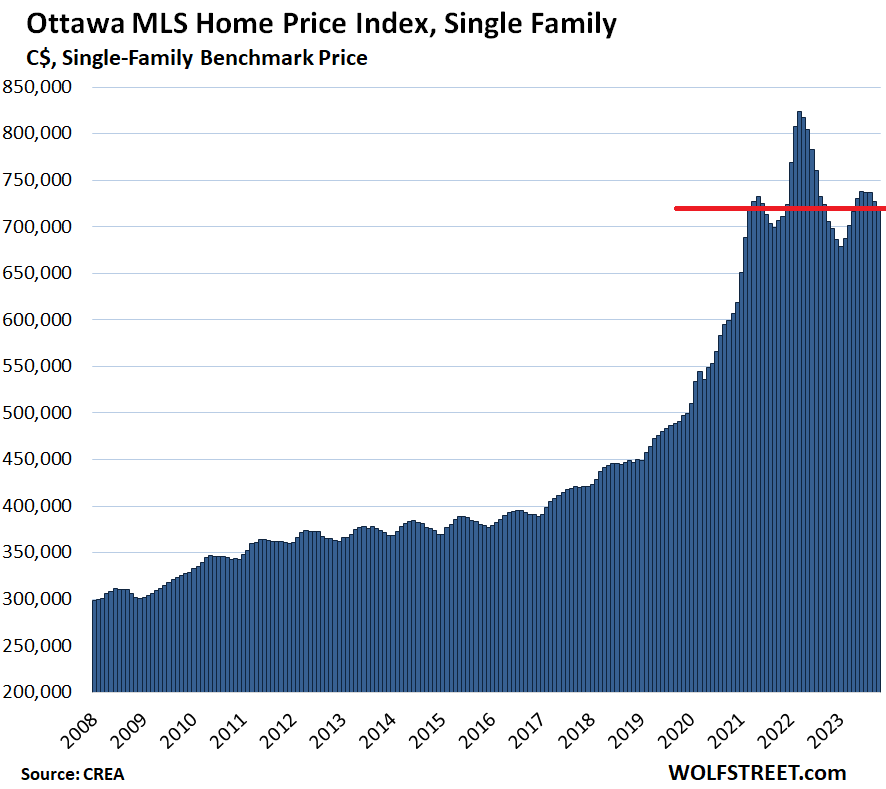

Ottawa: The benchmark price of single-family houses fell by 0.8% for the month, to $721,600:

- From peak in March 2022: -12.3% or -$101,600

- Year-over-year: +2.2%.

This is a funny-looking head-and-shoulders chart. I mean funny because until the pandemic, Ottawa’s housing market had been relatively sane, compared to some of the over-the-top Canadian markets.

Calgary: The single-family benchmark price rose 0.3% to a new record of $636,100, and was up by 10.9% year-over-year. People haven’t gotten the memo yet?

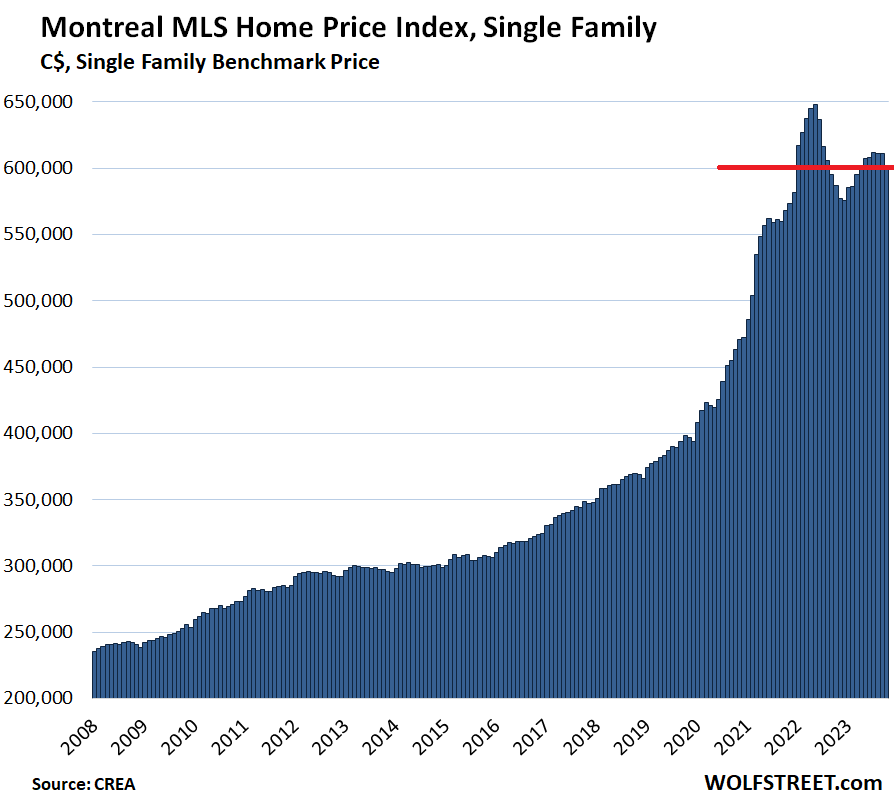

Montreal: The single-family benchmark price fell 1.4% for the month, to $602,300:

- From peak in May 2022: -7.0% or -$45,300

- Year-over-year: +2.6%

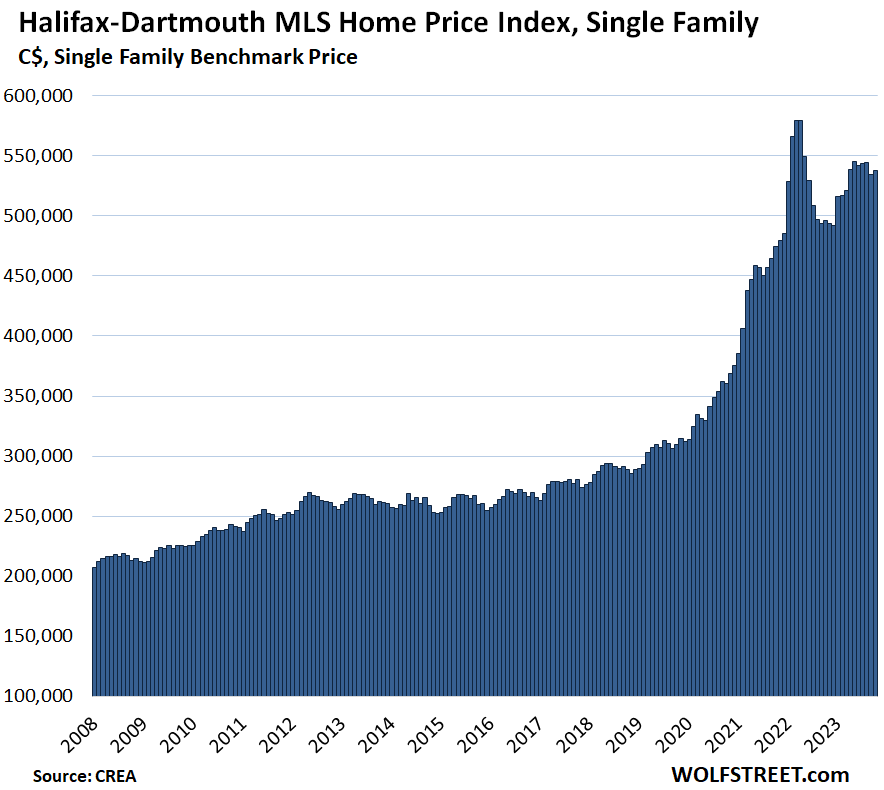

Halifax-Dartmouth: The single-family benchmark price rose by 0.7%, to $538,300:

- From peak in April 2022: -7.2% or -$41,500

- Year-over-year: +8.4%.

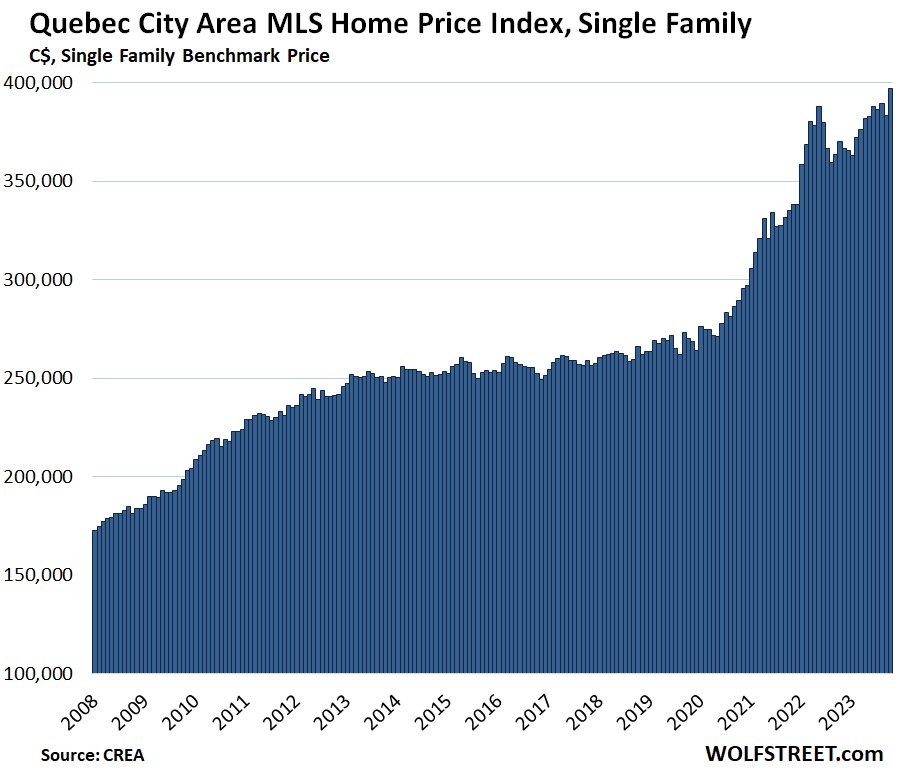

Quebec City Area: The single-family benchmark price jumped by 3.6% to a record of $397,000, and was up by 7.3% year-over-year:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wonder if Canada have the same 30 years fixed mortgage as we do, if this decline will look significantly different? If not, then perhaps there’s hope this is what to come for the US soon enough…

30 years mortgages in Canada are rare.

5 or 7 year adjustable are more common.

And the banks that write the mortgage tend to hold it. Way less selling of the mortgages into a secondary market. Might be why the somewhat risk averse banks prefer 5yr terms.

Peaks aka “bubble tops” are essentially blips on a chart. The more time goes by the more insignificant the blip becomes. Inflation and time cause asset prices to go up in price. We are not Japan. IF you can comfortably afford it, it’s the right time to buy. I sound like a realtor lol. In all seriousness, you save money when you rent but that is TODAYs snapshot. What happens if you rent for 15-20years? Your mortgage would have been the same but your rent will be x times higher…..just food for thought. I remember when I could rent a room for 500 in 2009 in San Diego. You could buy houses for 300k in SoCal. Lol. I’d love for houses to go down in price (meaningful) but maybe this little nothing burger correction is all we got. IMHO, it’s like this: ask yourself if you can afford to NOT buy. In 15-20 years your house will be double if not triple the price. Same with rents. If you have a long term horizon it’s a no brainer to buy. Again, we are not Japan. We are the freaking United States of America, baby!

*I sound like a realtor lol*

You rather sound like someone who bought at the top of the bubble, 2020 to 2022, lol

That long dated chart will show the most important correlation of all; rates go up home prices go down, rates go down prices go up.

Up in Canada it’s standard to start with a 25 year amortization and a 5 year term. A lot of folks slap a measly 5% down payment onto a place and have the government insure the mortgage, for a small fee of course.

Since COVID we’ve seen even shorter terms become popular because an increasing number of people are betting hard on that imminent rate pivot.

Wolf: I’d love an article on the differences between American and Canadian mortgages. I think that they imply a different future for their respective markets and I’m interested in your take.

I have always felt that more limited terms…as opposed to 30 year fixed etc, is better for everyone. How can a lender safely commit funds for 30 years? Then lenders need bailouts because…. Our first house was for 20 years, five year fixed. It was stable enough for planning and our budget. Nowadays there are so many payment options that go right on the principal in order to pay off the house quicker; term payment schedule fixed, but borrower pays bi-weekly, and/or pays an extra 10% outstanding on the mortgage anniversary every year, etc. My sister in law will pay her house off ten years early doing this. Plus, on renewal you can pay off even greater chunks of the principal.

“How can a lender safely commit funds for 30 years? ”

30RYFM rates should be much, much higher to reflect the duration risk.

I won’t touch 30 year paper until its yield is in the double digits.

Paul S-

“How can a lender safely commit funds for 30 years?”

Great Point: The 30-year mortgage is designed to help buyers buy more house, or in some cases to help low-income renters to buy a house in the first place.

This market is hugely subsidized through:

– agency backing of mortgages

– gigantic mortgage market supports (See agency or Fed balance sheets)

– federal hovering up paper when bond markets bust

– bailouts of SIFI cronies

Results include magnified booms and busts in building, bond price dislocations (referenced by MM above), house price instability, bloated government institutions (e.g., FHFA, Fed balance sheet), and sadly, individuals enabled to buy beyond their means, thus setting up for a life-altering jolt when foreclosure knocks.

Subsidization on this scale leads to bad economic decisions all around, and our economy is more brittle for it.

At the end of the day it doesnt matter the mechanism, the fed will intervene to raise prices when needed. We are probably 5 years away from the next round of MBS QE, and its likely going to make all the previous rounds combined look like a skimpy tip.

Similarly I’ve always felt if you have to go for more than 20 years you can’t afford the house. Also, the additional interest for the longer amortization can be in the hundreds of thousands. Even for a 500K mortgage it’s maybe 170,000 at 5%.

For faster amortization, in Canada at least, you can opt for accelerated payments by dividing the monthly payment by 4, giving an extra 8.33% off the principal in a year. Additionally, when renewing the mortgage after the initial term (say 5 years), just reduce the balance of the amortization period by increasing the payment to what you can afford, ex: 15 year balance of the am, reduce it to 12 years when you renew.

You can comfortably pay off the mortgage in about 13 years or less.

How can a lender safely back 30 year loans at ultra-low rates?

They can’t. They need them to be backed by the US government through Fannie, Freddie, FHA, VA. The US government backs over 80% of all 30 year fixed home loans.

Note that this is different than 2008 when the banks were on the hook.

If there is trouble, there’s always the taxpayer and deficit spending to bail out everyone. Except for the taxpayer.

Vote for me! A house for everyone!

The shorter terms was the only way they could obtain a mortgage. With the lower rate on the variable rate mortgage at the time they could buy something but not at the higher fixed rates for longer terms. With the loophole closed for lying about income to obtain a mortgage this was the only way they could qualify for a mortgage.

5% down payment has gone long time ago, now 10 % minimum requirements and now people who have put 10% down payment,some of them are walking away from closing the deal

Most mortgages are 5 years variable or 5 years or fewer fixed rates with 25+ year amortization. One big difference from the US is that Canadian mortgages can be ported to a new home so they’re not locked in like Americans.

Well, I’d imagine 30yr fixed rate mortgages would affect supply but I don’t know by how much, it would be all the people who could barely make things work at super low rates but not at current %, those people on a 30yr would be alright now and into the future, until next recession at least. Prices would still fall as they have fallen in various parts of the US because some homeowners still have to sell no matter what and prices are still high enough for a lot of people to be coming out ahead and the transactions taking place set the averages in those charts.

There’s probably some way to compare transaction volume as percentage of total home ownership between markets or something like that but I’m not a numbers guru so I can only speculate that at this time it’s probably not a huge difference yet. The real fun in Canada probably starts when slowdown in RE translates to significant layoffs in residential construction, it’s not really happened yet since condo towers and such take couple years to complete, same with subdivision developments, and ongoing projects are not stopping but some future projects will get tabled as buyers/investors dry up. Layoffs would have to be significant enough that commercial can’t soak up all of those workers though, currently there’s still shortages there and a lot of projects kicking off across Canada.

Any minute now, someone impatient will complain “sure, but prices are still up X% vs 2019….:

Phoenix_ikki, yes, things sure would be more interesting without government backing and 30 year fixed. “But but but then so many people wouldn’t be able to buy, and build equity, and would be left behind!!!”

Thanks for the fine data. It confirms our experiences. My son in law just sold his Dad’s very nice 2 bedroom/den patio home in Duncan, just 30 minutes west of Victoria. It sold for 50K less during the time it took probate to clear. There had been couples asking to buy with cash, no questions asked just 6 months ago, and now there are 3 other units for sale in the same 55+ complex by sellers willing to drop their price. They had to match. Offer should close next week. In my area nothing, repeat nada, is selling. Zip. Same old listings, no price drops, and no action. Now the weather is crappy and Christmas is looming so expect a further drop in activity. Our hope is that prices continue to drop so first time buyers can afford to purchase. We are presently renting a cottage to a young couple who are saving for a home. We are charging them less than trailer pad rental, just enough to pay our taxes. The cottage is only 5 years old and quite nice, but because I built it myself it was pretty inexpensive, about 25% of a modular of the same size. When we were young my wife and I could both buy our own homes with basic budgeting on blue collar wages. Our kids could buy homes just 15 years ago, both with regular jobs. Hopefully, it will reset again for the younger generation coming up.

Yesterday, had to a trip to town and I drove past several new subdivisions and projects. Many many new apartments going up in Campbell River, and many new town house developments on small small lots. These new row houses look just like our old family pictures of the Council Flat my wife’s grandparents lived in…..Manchester. Small footprint, wee backyard, parking on the street. That is where this is heading, smaller homes in more modest developments. The boomer MacMansions are going to become relics, imho.

regards

Except Canada is huge and given the choice, no one wants to park on the street. Small footprint is about maximizing developer profits. The idea that young people don’t want to maintain a yard is a myth that the elderly tell themselves so they can sleep at night. (Or maybe during the day, considering they’re greedy bloodsucking ghouls.)

Howdy Paulo,

You are back. I’ve missed you for quite some time.

–Geezer

Do you have the same chart for Edmonton? Would be interested to see the comparison between it and Calgary.

I don’t include Edmonton because it’s just not a “housing bubble.” Prices are relatively low, and now are just a tad higher than at the peak in 2007. They did have a housing bubble up to 2007 that then collapsed.

Thank you for sharing!

Calgary is still being floated on the price of oil. Edmonton, while the main center of oil field manufacturing, is still a Government town.

Also e everybody is moving to Alberta $200,000 in the last year net increase in population. There is all time record numbers for any province and population growth percentage wise since counting has started.

Thanks Wolf!

Resale condos and resale apartments today are still selling for what they sold for back in 2007. Country Club Estate today is selling for what it sold for back in 1990. The very bottom of the market has moved up somewhat no more apartments selling for under $35,000 like in 2021.

Edmonton always trails Calgary and is cheaper now but is tightening up. Rents rising rapidly as Canadians are flooding into Alberta in all time record numbers because of affordability and the low tax regime like no other in Canada. The whole central corridor from Calgary thru Edmonton if filling up with newcomers from all over. Real estate was beat down for about 15 yrs by the anti energy extremist movement and now the worm gas turned. My $249,000 townhouse I bought last year is similar and nicer than one sale featured in King city outside Toronto which sold a 5 1/2 times the price this month. In the Fraser Valley of BC it would cost me about $800,000 plus. I also buy gas for about $1.20 per litre, pay no sales tax except GST, get free medical without monthly premiums, enjoy Alberta Angus beef I buy directly from the ranchers and am located around 1 to 1 1/2 hrs from 2 international airports and the 4th and 5th largest cities in Canada.

Wolf,

I’m trying to donate. I don’t use Zelle, I avoid PayPal, and I’m outside the USA (post is a nightmare). Now trying to send by AcacH but can’t set u up since can’t locate phone number.

I’ll keep trying; but should be easy to make it easy for us. I love your work,

Thank you for trying.

I use PayPal as a payments platform so I don’t have to deal with credit cards. You don’t need a PayPal account. It’s just the place that handles the credit card.

Wolf, for what its worth:

Folks that don’t want to use Paypal, are likely doing so because of their objection to Paypal’s corporate policies, rather than the perceived hassle of creating an account.

I have many customers who refuse to pay via Paypal who have told me this is why. Admittedly these folks are a minority, but they are adamant about their opposition to Paypal policies.

Admittedly I don’t have an alternative – I wish Zelle worked with more banks. I’ll be mailing you a check.

Yes, I get the PayPal issue. It’s the same with all payment platforms.

Have you checked your bank about Zelle recently? Banks and credit unions are constantly being added to the system. Maybe it joined recently.

Bitcoin

I’d be really interested to hear your comments on the housing market in Australia. The rumors seem to be that prices are more-or-less flat, rents are taking off like a Saturn V and surprisingly construction is going hell-for-leather. Construction stocks seem to be booming.

I’ve seen reports that it’s being driven by immigration increasing demand — but all this in the face of dramatically increasing interest rates that seriously compromise the affordability of mortgages and the economics of borrowing money to rent properties out. My guestimate is that the rent return on residential property after expenses is around 1.5%, which is surely not enough to borrow the capital.

– Canadians also have socalled “Fixed payments and floating rate” mortgages. The mortgage holder pays a fixed amount every month for e.g. 25 years. This payment consists of paying interest and principal. The higher the rate then a larger portion goes for paying interest and less towards re-paying the loan.

I must elaborate a little more on this type of mortgage. So A LOT OF canadians have a “fixed payment” with a “variable interest rate” mortgage.

Let’s assume a household pays monthly $ 2,000 for the mortgage. Then e.g. $ 1,000 goes to paying interest and what remains ($ 1,000 ) goes towards the repayment of the mortgage.

When the interest rate goes down then this household pays e.g. $ 500 on interest and the remaining $ 1,500 goes towards repaying the mortgage debt.

When rates go up then e.g. $ 1,500 goes towards paying interest and the remaining $ 500 goes toward repaying the debt.

In the last 30 years rates went only down in Canada. This meant that this type of mortgage was very beneficial for homeowners.

The “interesting thing” about this type is when the interest payments are rising above (in this example) $ 2,000 to e.g. $ 2,300. Then a payment of $ 2,000 is no longer sufficient to cover the interest costs. In this one example one pays $ 2,000 and then the mortgage (debt) grows with $ 300. In this case the mortgage holder can/will be forced to increase its monthly payments to $ 2,300 or higher. Ouch & OMG.

The problem in the Canadian housing market is almost all the new buyers have to go to a third tier lender and pay higher mortgage rates that in theory they can’t really pay in the first place. They just believe prices have to start going up and never stop going up to save them from losing their homes. In the past mortgages were obtained through lying about your income. Laurentian Bank was the first bank to be called out for this and is now up for sale and most of their mortgages are based on falsified incomes. I’m talking about cities like Brampton, Milliken Mills and Mississauga.

The great Canadian reeducation begins.

So far this is still the thin end of the wedge.

New legislation tabled by NDP gov in BC would drastically alter densification (ie… something all cities in N. America should copy) basically, it would enforce the construction of buildings over a certain height near transit stations;

“The move is aimed at “speeding up” the creation of homes and encouraging communities to build housing closer to transit, services, and amenities. The legislation, if passed, would require municipal governments to identify “Transit Oriented Development Areas (TOD Areas)” within 800 metres of rapid transit stations, like SkyTrain, and within 400 metres of bus exchanges, like the Newton Bus Exchange.”

It’s happening in the US as well. I live near Tacoma and just read that our local US House rep – with bipartisan co-sponsors – introduced the “Build More Housing Near Transit Act”. Same general idea as what you outlined.

Calgary is the exception because it wasn’t as expensive as Vancouver or GTA in the first place and people desperate to find an “Affordable” house at higher interest rates have realized Calgary can still offer homes with relatively affordable payments. Particularly if you are selling in Fraser Valley or GTA cashing in on some of the equity and moving to Calgary. It won’t stay that way for too long but for now Calgary is the “it” place to be if you still subscribe to the “passive income” wealth strategy nonsense.

(Edmonton isn’t a bubble because it’s too cold a climate for most, even in Canada)

2 years ago, Calgary was the city with the highest unemployment of any major city in Canada.

Now the price of oil has risen and boosted the city’s economy.

But this is not a permanent state of the market there. And economically, this city depends exclusively on the oil industry. The moment the price of oil goes down, many people who came there will regret it.

You two guys obviously agree here: ‘It won’t stay that way for too long but for now Calgary is the “it” place’ and ‘But this is not a permanent state of the market there.’

I agree with both of you since as noted, Calgary RE is on oil boom-bust cycle, which is different from the rest of Canada; Post Covid money splurge madness notwithstanding.

Why does Montreal seem less expensive?

French language laws. It’s not an easy place for English speakers.

Lower wages, higher taxes.

There are also good wages, but the mass of people, mostly immigrants, work at or around the minimum wage.

However, in Montreal there are many people on the laufer who work illegally and bring in more money than other people who work at or around the average wage.

In addition, when you are at Laufer after the second year, you are entitled to a free dentist and a free eye examination.

People selling out in the Vancouver Rainforest move to Kelowna, Kamloops, or Vancouver Island. And that is what is pushing up prices in the Hinterlands.

Calgary is not a destination for the Left Coast.

It’s interesting that a large corporate landlord is saying it may be a good time to sell properties with 4% cap rates and put proceeds into a fixed income vehicle yielding 5%. It would be accretive to earnings.

I’ve been saying this for some time, even though it has antagonized some RE diehards on this board. The math of being a landlord doesn’t work for people who buy properties at these levels in many locations. For many investors, it’s better to sell at these levels and wait the market out, like this large corporate landlord is planning to do.

This is happening in the States. Not sure if Canada is also has large corporate landlords.

That will just make it worse for all the people on the sidelines as they are shut out. I believe in the last US housing bubble the banks were selling portfolios of properties wholesale to institutional buyers?

Probably need to outlaw corporate ownership of SFH.

I believe rent caps were recently removed in most of Canada.

Any rental unit built after Nov. 15, 2018, is not subject to provincial rent control in Ontario.

Earning 5% risk free for doing nothing is the best WFH job ever!

Interesting but US House builder stocks are close or hitting ATHs this week.

During HB1, builder stocks peaked mid 2005 and started rolling over while Case Shiller house prices started to roll over about a year later in mid 2006. Builders stocks started to crash spectacularly in 2007 but Case Shiller crash accelerated to the downside starting 2008.

Builder stocks bottomed in 2010…house price in 2012.

Builders stock prices tend to lead house prices.

In my opinion the leading indicator for housing is the stock market. Stocks crash, because they are liquid, then RE follows. 2007 is an example.

This makes sense because they are alternative asset classes for investors.

Well stocks are near all time highs…

It appears that housing bubbles are a global phenomenon. So many countries seem to be experiencing one. China is no exception. The housing bubble there was as bad as anywhere else. Real estate speculation was one of the national pastimes. There are stories of people whose apartments in the center of cities like Beijing or Shanghai inherited from the old communist system are worth more than a million dollars. This ended up creating a huge affordability crisis for the country’s youth.

Now that this bubble has imploded in spectacular fashion along with the real estate developers like Evergrande, the government is doing everything in their power to reflate it.

Constantly increasing real estate property prices are beneficial for governments. Increased property taxes for the municipalities and increased capital gains taxes for the national governments as properties are inevitably sold. Then you have the wealth effects so much promoted by Bernanke.

Because of all of this there is no incentive for governments to allow these bubbles to deflate. They may address affordability by promoting incentives like lower down payments, longer mortgages, lower mortgage rates, etc. but these in the end drive up prices even more.

If the real estate market downturn in Canada gets much worse, it would not surprise me to see some action from the government to address it.

What they gonna do?

They can’t fix the potholes.

They can’t get enough doctors.

They can’t get enough teachers.

Earning local wages while competing against Foreign money, of dubious sources, for a house/home is the dirtiest result of Globalization.

I always thought paying off your mortgage was the best way to save money. Please correct me if I’m wrong. If I have a 4% mortgage and my house is appreciating at 5% a year, am I not getting 9% interest on my prepayments to the principal?

Putting the prepayment in a MMF earning 5% would raise the return to 10%.

Actually I am not sure that I agree with the math. But putting the prepayments in a MMF earning 5% would still be better than prepaying a mortgage at 4%.

Nope, you have to pay taxes on the MMF, which reduce the actual return. With his example, paying off the principal is more constructive as you pay with after tax dollars unless your effective tax rate is very very low (<20%)

I agree. It depends on your tax bracket. If you are making 5% in a MMF and your tax bracket is 20% then you are breaking even. You are effectively making 20% less interest or 5% minus 0.2*5% = 4% after taxes. The higher your tax bracket over 20%, the better it is to pay off the mortgage.

TBills and MMF are short term. So if the short term rates go higher before your mortgage is paid off , the better it is to hold cash. If they go lower, take the cash and pay off the mortgage.

What gives you peace of mind? A paid off house or cash in the bank?

However if you pay a lot in interest (over 16K (married) including charity), and 10K in SALT taxes, you can itemize deductions and deduct the mortgage interest over that 26K amount.

Also, if you rent out a room in your house, you can deduct the portion of the mortgage directly from the rent received.

It is a hard question to answer without details.

On our first mortgage decades ago I put a “what-if” extra principal payment into my excel mortgage schedule. The results were astounding; the last payment date moved up a few months and the lifetime amount of interest paid plummeted. You may want to check that out and then decide how important that is to you vs 5% MM interest.

I am deliberately making the minimum payment on my mortgage, because I can earn a much higher yield with 6-month treasuries.

In this context, my treasuries are accruing interest faster than my mortgage. I’m borrowing long at low rates, loaning short at higher rates, and profiting from the spread – just like a bank!

In the (extremely unlikely) event that rates go below my mortgage rate, I’ll switch to paying down extra principal on my mortgage.

I am doing the same (for now while TBills are at 5.5%.)

Since I am in the 22% tax bracket, my actual interest rate on the TBills is 5.5 -.22*5.5 = 4.29% after taxes. My mortgage is 3%. it wouldn’t make sense to pay down the mortgage (Other than peace of mind with owning the house.)

If I get laid off or retire, I may drop into the 12% tax bracket though would be hard to live here with that income.

The after tax rate for the Tbills would be: 4.84%

If i retire, it may be tempting to pay off the house with IRA money but it may not be financially smart. The highest tax bracket is currently 37%. If I pulled a windfall out of the IRA and it pushed me into the highest bracket, I would owe a lot in taxes. It would be better to only take enough out of the IRA to stay in the lowest tax bracket possible and continue to pay the low mortgage.

Abstractly (ignoring considerations of tax and specific subsidies to housing costs) your math is wrong because the 5% appreciation isn’t connected to your prepayments. The 5% appreciation of the house value goes entirely to you and is unrelated to the loan, other than in the edge case where you default and the bank takes the house.

(Prepayments actually *reduce* your “yield”, measured by the increase in value of the house as a percentage of your total principal payments. Because they reduce the size of your mortgage without affecting the value of the house, reducing the amount of leverage you have on the 5%.)

The correct comparison is simply between the 4% loan and whatever rate you could alternately get with the money.

There are stories where international students are renting beds by the hour inside already cramped rooms. Paying at least C$500 to share a room with somebody.

News reporters discovered that slumlords were offering shared beds to rent, telling a female applicant that the guy she will be sleeping next to on the same bed is a good hardworking guy. Rent was about C$700 I think.

Canadian economy does not produce enough of GDP per capita to sustain these real estate valuations. It is all blown into the bubble territory simply because of the availability of the credit. Build more crowd is failing to understand that developers will never overbuild to the point where the availability of the units is so big that the prices will go down. They are in the business to make money and if needed be they will slow down release of the new inventory until market picks up (already happening in GTA).

Major point with this situation is Canadian banks and stability of the Canadian monetary system. Canadian bank stocks have been taking beating this year(for the right reasons) and they will lean heavily on the politicians to demand rate cuts so that the real estate wheels can start turning again. Otherwise there is a significant danger of significant negative events if people who own real estate are incapable or unwilling to continue paying mortgages. Canadian banks are already in uncharted territory where average mortgage duration has ballooned to over 35 years and many mortgages are in excess of 70 years. Last stat that I was able to see was telling that 5% of mortgages are not being paid off at all and actually not even interest was being paid and as a result they were growing.

Imagine situation where people are paying mortgage and the mortgage is becoming bigger. So needles to say Canadian banks are well capitalized and they are paying big dividends alas I don’t think they were ever in this kind of situation before and somehow investors are not paying enough of attention to this matter( at least I dont see enough of conversation about it).

Connected to the Canadian real estate market is the ongoing turnover in 5 year mortgages (very typical here) from those struck 4 years ago at very low rates (3% or so) to current rates at close to 8% — depending upon the outstanding principal, that’s a big increase in monthly payments which will no longer be available for discretionary monthly spending. This could be recessionary, and the drag will likely increase over the next 3 years — about 20% or so of homeowners have to renew every year.