Home buyers “seize a dip in rates” and rush back into the housing market, LOL?

By Wolf Richter for WOLF STREET.

For example, on CNBC this morning, we read: “Mortgage demand climbs to the highest level in five weeks after interest rates move lower. Or on MarketWatch, we read: “U.S. mortgage demand hits five-week high as buyers seize a dip in rates.”

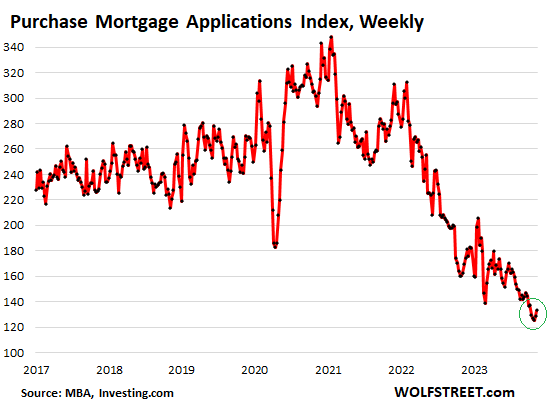

This was based on the weekly applications for mortgages to purchase a home, released this morning by the Mortgage Bankers Association. Mortgage applications ticked up a tiny little bit, but that uptick can barely be seen in this three-year plunge of mortgage applications to the lowest levels in the data going back to 1995.

And that uptick itself was tiny compared to prior increases in this very volatile data, and mortgage applications to purchase a home were still down by 47% from the same period in 2019, and by 61% from January 2021:

“Declining spending adds to signs the economy is cooling after hot summer,” the WSJ said hilariously as subtitle under the article, “U.S. Retail Sales Fall for First Time Since March as Holiday Season Approaches.”

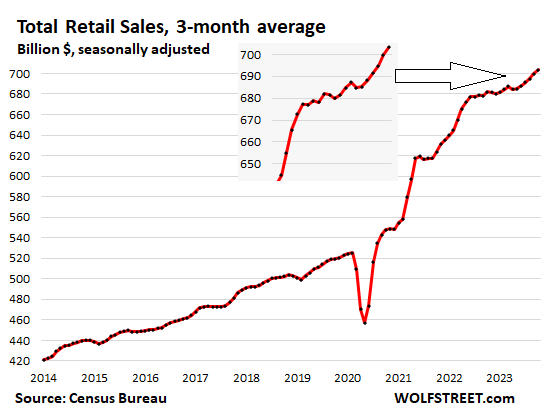

Total retail sales, after having jumped by an upwardly revised huge 0.9% (11.3% annualized) in September, and by 0.7% (8.7% annualized) in August, edged down 0.1% in October from September, in what is highly volatile data that gets heavily revised as more data is collected.

Retail sales dipped to $704.95 billion in October, from the record in September of $705.7 billion, seasonally adjusted.

Retail sales in October were higher than the unrevised September retail sales. That’s how it goes. The volatility in the data and the revisions are why we use a three-month moving average, which shows the trend.

The three-month moving average shows the actual slowdowns we briefly had last year:

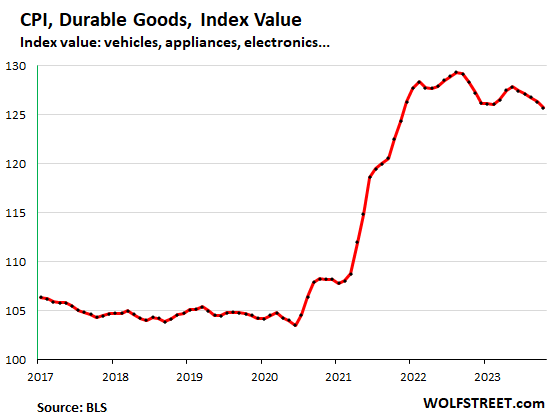

In addition, prices of goods dropped, showing that consumers bought more product.

Retail sales are sales of goods by retailers. And prices of many goods have been dropping as inflation has wandered off into services.

Prices of durable goods (autos, electronics, furniture, appliances, tools, etc.) dropped 0.4% in October from September – I discussed this at length yesterday in Beneath the Skin of CPI Inflation:

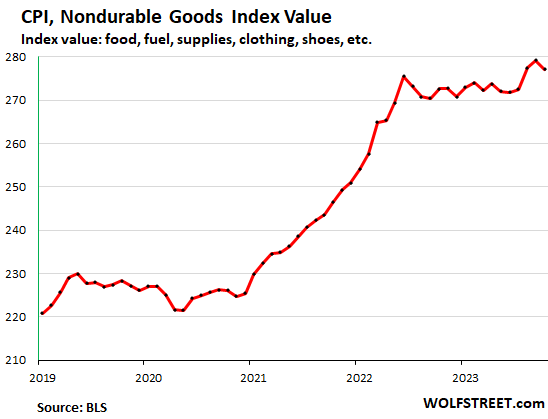

Prices of non-durable goods (gasoline, food, supplies, clothing, shoes, etc.) dropped by 0.7% in October from September, driven by a plunge in gasoline prices.

Because prices of goods dropped faster than retail sales of goods, consumers bought more product in October than in September.

This is why the dip of 0.1% in retail sales was smaller than expected; the consensus had pointed at a drop of 0.3% based on the price declines in goods we’ve been seeing which should have lowered the dollar sales. Inflation has long ago moved to services.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf it’s ok. Those clickbait headlines are just that … complete nonsense. All of the financial news streams are focused on traffic. They’ll do whatever it takes to generate views or clicks. Retail investors who use that to ‘inform’ their strategy are … well how do i put it nicely … they’re sheep.

Thank you for the outstanding work and i’m using this as an opportunity to make a contribution. You’re way better than any of the ‘experts’ touted by the financial media. Thx!

My wife and I got pre approved for a mortgage (more than we want to spend) and the realtor and mortgage lender have been calling us daily. It’s just a “gulley”.

Must not be in SoCal. Most RE agents are still pretty snotty around here and you have to go to them as if they are doing you a favor. Guess the resiliency of price and still some demand chasing so little out there is giving them that sense of confidence this market is bust proof.

friend said those not paying cash are asking for $5-10k to buydown mortgage rate

went by I wouldn’t want to live there sub-division along I-10

building with crane lifting trusses into place

another build-in(former school site – now low cost at $250k+)

around 15 units in various stages

A month ago I did a credit check with my credit union to get pre qualified for a mortgage as I was looking at a condo to purchase.

I was deluged with text messages and calls for two weeks from mortgage brokers. I would say up to 10 an hour. Easily 50 to 60 a day for two weeks. These calls dissipated after that. But even week 3 and week 4 I probably received at least 20 calls a day.

Very annoying.

Hopefully independent analysis and journalism all thrive in the coming years drawing “clicks” away from such “publications” increasing their desperation and poor decision making, hastening their slide down the death spiral to ever greater irrelevance.

Seems clear AI will clearly move us back in that direction.

When the war started in the Mideast, I noticed new pendings really slowed. But, in the last week, I witnessed a surge in new pendings, especially in the 5M to 7M price range. In fact, the 5M to 7M price range is doing better than the 3M to 4M price range, which is the lower end of single family prices. I have never seen this pattern before in Newport Beach, CA.

What’s up are new listings. They’re now coming out of the woodwork, out of nowhere, LOL, when they should normally drop this time of the year. The NAR just reported its latest weekly number for new listings. Redfin is showing similar numbers. That has been going on since August. This is going to get fun.

What happens in the $5-7 million range or the $3-4 million range is largely irrelevant for the broader housing market. San Francisco nearly always has a spurt in luxury sales after Labor Day, for example. Not sure why, but we almost always get it, and it’s well documented and talked about.

I can attest to that where I am. I have seen more new listings in the last two months than last two years. Just too bad (for me) that they are all absurdly priced. But that’ll change soon enough.

Define soon? New home prices are down 15% while existing prices are up 3-5%. There’s absolutely nothing about the current housing market that makes sense outside of the absurdly priced point.

So what you’re saying is…rate cuts by July?

The way financial conditions have loosened over the past 7 days, I’d say two more rate hikes by July?

@Wolf, I would loooove to see this but knowing PowPow best we can hope for is holding steady next year and he will likely tell us data dependent and lag effect..blah blah. Love to be proven wrong in this.. nothing better to see WS bust a nut too early celebrating victory only to get cold cock in the face later.

“the 3M to 4M price range, which is the lower end of single family prices”

That’s nuts – literally 10x higher than the lower end of the SFH range in my area (300k-400k, and even those are bubble prices in my mind)

You can have this 800 sqft gem for $5,565,000 in Newport Beach:

My wife and I walk by this place every other day, and I have my doubts that it is 800 sqft.

@Socaljim I just went to Zillow and it blew my mind that there were over 100 $5-7mm sales in Newport Beach just in the past year (including five on Balboa Island and even one in “East Bluff” where poor NB people lived in the 80’s).

It sucks that some people will read these headlines and rush out to secure a property/mortgage when the “surge” in applications is essentially a fiction.

Some accountability for media sensationalism would be awesome.

A fool and his money are soon parted…

Unfortunately the fools keeping prices high for everyone

Hmm. That would mean there is a shortage of stupid rich people …

Funny how in our capitalistic world, everything is measure by supply and demand and seems like everything is finite (housing, commodity…etc) Yet we seem to never run out of dumba$$ FOMO sheeps to keep the party going…perhaps bagholders are infinite in supply…

The “bag holders” will be the kids sent off to private school by their moms with a fresh packed lunch and fresh filters in their O2 generators.

This of course on applies ONLY to the top 5-10% (or higher) net worth families.

That’s if they let the lower 50% live at all. Methods and world political consequences already being tested as I write.

Am I spoiling everyone’s sleep number setting?

Sure hope so.

By being a negative nabob and a conspiracy theorist? Nah, people like that are a dime a dozen. I’ll sleep like a baby tonight.

Don’t forget to say your prayers first.

Sometimes (actually, most of the times) I feel like most of the main stream media and Wall Street traders are leaving in the Barbieland, where everything is great, every indicator is amazing. May be we are actually living in the Barbieland, but about people like me are “just Ken”s.

The media and Wall Street are in cahoots, run by the same elite.

It is intentional, trying to manipulate the markets. They know fully well what they are doing.

I scan Google Financial News article titles and click into maybe one in thirty and even then I seldom read for detail. Most of it is a waste.

What I mostly look for is video interviews of the really successful and straight forward (will tell you what they think) investing pros.

Wolf’s data/charts are wonderful and worth more than 95-99% of the financial news. They will keep you on track if you let them.

Thanks Wolf for putting out information we can rely on. Every time I see those MSM articles screaming about demand rushing back in, I want to rip my eyes out.

Both housing and stock market run on on premature ejaculations model on every possible positive or in our crazy time bad news and hype up the FOMO narrative to no end…disgusting and exhausting to even just ignore and sadly the less informed will fall victim to the FOMO…

Just like after last couple of days of with the market rally stemming from interpretation of CPI numbers, WS is once again busy busting out more organism…and jackA$$ like Tom Lee is running his mouth again with crap like this..

“”I have researched markets for over 30 years, and I am struck how investors’ ‘default’ stance on equities is bearish for stock ideas and for the market overall,” Lee said, later adding, “the bubble today remains ‘the bear bubble’ — the entrenched belief that equities need to fall 30% to 40% to properly reflect the doom out there.”

But bullish stock market investors have the persistent bears to thank for the recent rally in stocks, according to Lee, as he sees much of the S&P 500’s 7% gain over the past two weeks driven by overly bearish positioning among institutional investors that had to be reversed via buying stocks.

And going forward, Lee continues to recommend that investors “buy the dip” in stocks”

Yes. And crap is the correct word. That is one skill both RE agents and financial media commentators have in spades. Coming up with creative arguments why NOW is the time to buy. Even though a (very) strong case can be made that it isn’t.

FOMO investors seem to forget the inherent bias of people who make their living from generating financial transactions. The “buy it now” hype and hoopla continues regardless of economic conditions.

Realtor commissions and mortgage commissions/fees are in a depression – just look at the drop in sales volume – but the massive bubble in house prices is one of the main drivers of this grotesquely overheated economy right now.

As long as sheep can continue to pull up fantasy valuations on Zillow to enjoy their deluded thoughts about how wealthy they are from their shack, they will continue to borrow and spend as if they’re some Bezos baller. The roads and businesses are packed, as usual.

Perhaps a little off topic, but the realtors are in the process of losing pretty bigly in a couple of antitrust cases that allege that their commission structure is anticompetitive and some form of price fixing. As those cases wind toward conclusion, this could be a second reason why RE agents’ commissions may be going down shortly. It makes me wonder if the mortgage brokers could also become defendants in antitrust litigation related to the housing and property markets anytime soon?

As an outsider to the housing market looking at it from the sidelines, as I have no desire to buy or sell & have owned my home for 28 years, it appears that technology is making real estate brokers less important.

Wolf has commented that he sold his condo, back in the day, directly to a buyer without using a real estate agent, and that seems like a much better way of selling one’s house or condo. For example: My house is worth X amount of dollars. If I sold it, I would want X amount of dollars — not .97 times X amount.

Again, I’m just an outsider on real estate transactions, but on a house worth a million bucks, 3% is a lot of cash. Does a real estate broker bring that money back to the client if hired to sell a property?

DanRo – everbegging the oft-unasked question when dealing with ‘Murican advertising in all of its configurations: “…XX% OFF!!!…”.

…but off of what?…

may we all find a better day.

91B20 1stCav (AUS),

Funny you should ask that question, as today my gravel bike is at my local shop getting set up for another pair of wheels. This winter, I’ll have my studded winter tires on the current wheels, and I’ll run my three-season 32mm tires on the new ones.

Last winter was the third snowiest in the record books for the Twin Cities, so just studded tires were fine. This winter, we’ll be warmer and drier; El Niño. So, it’s time to get ready. But my options for another set were: inexpensive from Shimano, another set of DT Swiss, or a set of HED Emporia GA Pro wheels — made in the USA.

20% off! The HED wheels are on sale for $760 a pair instead of $950. My decision was helped by the discount.

My bike shop owner, and friend, bought his shop from Steve Hed decades ago. My two carbon road bikes have HED wheels. My gravel bike is a Minnesota product (carbon frame laid-up in Taiwan). So, now, the trilogy is complete with three carbon bikes rolling on HED wheels. With a twenty percent discount, eh?

The sale ends tomorrow.

The current rates (7.5) may be a “dip” when compared to on month ago (>8). When comparing two last 15 years, 7.5 is still crazy high.

For house prices, Wolf says “Buyers are laughing at those prices”. I am not sure whether they are saying that, but I think they know that they cannot afford those prices and these rates, which is why the housing market is essentially frozen.

At these rates, only the sellers have the discretion to revise their pricing, (most) buyers do not have the option to increase their purchasing limit as they won’t qualify for the mortgage if they try to go higher. But it seems like most sellers have an absolute faith that there is almost a divine rule (fed by the FED for a really long time) that house prices must always go up even if the mortgage rates go two digits.

“When comparing two last 15 years, 7.5 is still crazy high.”

And when comparing to* the last 50 years, 7.5% is perfectly normal for a 30YRFM.

The last 15 years of near-0 interest rates were abnormal, not current rates.

Yes, but the prices are not perfectly normal.

I agree. Still way too high.

I keep reminding myself (and so does Wolf) that housing moves slow and will take time to correct down.

But if 1 to 2 major economic hiccups happen then the fed is going to panic and push rates a lot lower. The “plateau” never lasts long.

I wish 5-7% money market, CDs, etc lasted forever. I think within 2 years we will be at 2% or less.

Then real estate will go even higher, which will put more folks out of homeownership territory.

“I wish 5-7% money market, CDs, etc lasted forever. I think within 2 years we will be at 2% or less.”

If you really think this, prove it and buy some TLT.

I’m taking the opposite side of that trade and shorting it… literally betting on rates going up.

I may be sticking my neck out into territory I know nothing about, but will the international investment environment allow our taxes to drop that low again? The dollar must be defended, after all, no?

I meant rates not taxes…maybe a Freudian slip…

My $0.02 is that the Fed will keep rates higher than other nations, because they want to defend the currency and ‘out-hawk’ other central banks.

Inflation will also put a floor under how low rates can go.

No, 7.5% is actually below the 50 YEAR average mortgage rate of 7.75%

All the whiners are just spoiled from 15 years of below market rates. Once everyone realizes 7.5% is normal, folks who can afford to buy will start buying again, regardless of whether home prices are higher, lower or the same.

Oh wow.

Great analysis.

As Wolf likes to say, what BS.

The problem isn’t the mortgage rates. They’re fine. The problem is the ridiculous prices. People need to wrap their brains around that.

*At these rates, only the sellers have the discretion to revise their pricing*

Remember, the price of anything is always determined by the buyer.

The price requested by the seller is solely his wish or dream.

Without a buyer willing to pay the asking price, there is no deal.

Actually, it’s the “meeting of the minds” that determines if there is a transaction, and therefore if there is an actual price. Both have to agree to it. if the seller doesn’t agree, there is no deal.

1. Consumer Debt is up and will continue to grow

2. If these folks are homeowners, they should at least get a HELOC

9% vs 18-29%….

3. Many that get a HELOC will like have to punt on their 3% 1st Mortgage or simply be forced to sell. it’s coming

Disagree with all of this:

1. Credit card spending is up, but this is a measure of spending but not debt.

2. No way in hell will I do a HELOC at 9%. I can borrow from myself at 5.5%.

3. See #2. They can pry my house and mortgage from my cold, dead fingers – never selling.

Wolf, I got an even more ridiculous article for you to tear to shreds. Yesterday The New York Times published a piece called “The Fed Has Put Our Housing Market In Jeopardy”. In it, the author begs the Fed to restart their MBS purchases. Amongst other things, he claims more affordable mortgages will lead to more inventory and lower home prices. Did I mention the author is an investment banker?If the New York Times is publishing this sort of nonsense I can only imagine what else is floating around out there. It makes me realize the unimaginable amount of pressure that will be applied in an effort to keep the housing market defying gravity and treading water in the coming years.

On that note, I’m off to see an overpriced home!

hmmm….maybe good ol Lawrence Yun has taken up a pseudonym and took out a second job as NY contributor…this type of shameless pandering is definitely within the scope of RE insiders…

I just read it. Reads like your typical older guy trying to make sure that he can sell his overpriced assets to younger generations.

I think anyone can buy space in any publication to push their own agenda. Perhaps you can even rent a journalist to write it.

I remember the “masks don’t work” articles during the pandemic. Hehe then why do all the car painters wear them? Hmmm hehe ;)

They just hire whomever to write whatever they need to point to. To get their rock rolling in the direction they want to roll it.

Most financial media should be lumped in with manufacturing these days… They run an endless supply of mole hills through their “journalism” machines so they can ship mountains to their customers.

One would expect mortgage applications to be down going into winter and sales to be up going into the holiday season. The WS graphs show us just how small the deviations are from expectations, but nobody is going to sell those little clicks without a little spin, eh?

Sales normally drop around 10% seasonally during the holidays. A lot of unmotivated sellers dont want buyers coming through their houses when theyre all decked out for Christmas, I suppose.

A lot of realtors also slow down or stop working altogether around Thanksgiving.

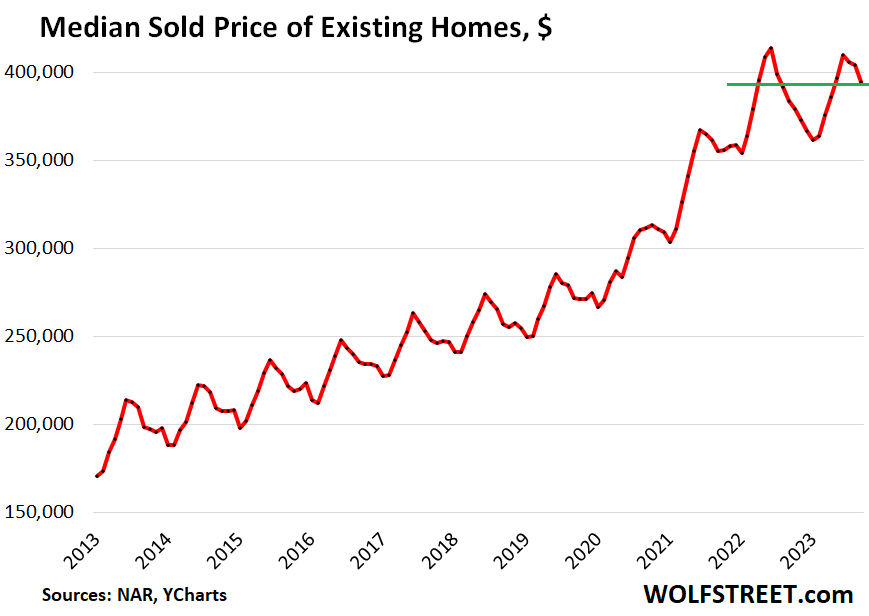

It’s pathetic as it is hilarious. The Real Estate Industrial Complex has tried time and again this year to co-opt the media into “manifesting” a different reality than currently exists in housing markets. Nobody is falling for it. Home prices and rents are falling in most markets and it’s snowballing.

Read some real stats. Sales are down. Sales prices are up in most markets. Rents are up in most markets… up less than before but still going up

Prices are DOWN overall, peak was June 2022, NAR data:

https://wolfstreet.com/2023/10/19/median-price-of-existing-homes-falls-further-peak-was-june-2022-demand-crashes-price-cuts-jump-supply-days-on-market-rise/

And sales have collapsed:

Wow! Look at that huge disconnect between the sales trend and the price trend.

Lot of pressure building up there.

No wonder the Mighty Wurlitzer is shouting “no better time to buy” and “need to restart the MBS purchases.

It’s all a con job, from the media up through the government.

I would like to buy a house, but with cash. I don’t care about mortgage (or insurance) rates. But the prices of homes seem way out of whack compared with the rest of consumables, and compared to normal historical increases. So I am on hold. I don’t know what is going to happen, but it is going to take a lot to get me interested. There are a lot of downsides to buying a house that need to be compensated for by a lot lower prices. Prices are being kept up by an historically small number of buyers (people who have to buy, or have so much money they don’t care about price, or are just crazy, or are just plain stupid), while the bulk of potential purchasers are on the sidelines (willingly or unwillingly).

If you were to look at building a house with cash right now, how much house could you build? My wife and I started building right before the pandemic hit. We saw inflation coming and bought everything we could get our hands on from appliances to tile as the supply chain issues started affecting our project. Thankfully we are almost finished and should be ready to move in on March 1st. If I were to spend the approximately 700K we have put into this place starting now I doubt I could build half the house I have. So perhaps prices will come down in certain way-overvalued markets, but from my perspective in rural Midwest I don’t see a lot on the market, and it is snapped up very fast unless it’s ridiculously overpriced, which is perhaps one out of a dozen listings.

You can see the fed “wave” (as I like to call it). It shows when RE prices have been low, high, low again and high again. And yes they are pretty darn high now. It looks like the tide is receding now. The waves will go lower but def not 2012-13 low. Then after they bottom, they will start gaining volume and head for a new peak, slowly.

When will the next 2012-13 be? Stay tuned to wolf!

The 2012-13 low adjusted for CPI 2013 to 2023 would be about time for me to jump in.

According to one of Wolf’s excellent charts, home prices dipped below the inflation line OER(extrapolated from the chart starting in 2000) in 2012.

I agree with you. If you adjust the home price up with CPI inflation from 2012, it will be an excellent time to buy.

Wolf’s other excellent charts unfortunately show that either inflation will have to rise 20-30% or house prices will have to fall comparably for that to happen again. Or a combination of both.

I’m waiting and watching Wolf’s charts.

House prices tracked inflation from the 1950s through the 1990’s. Housing tracked inflation even during the high inflation of the 1970s and 1980s They deviated immensely during the 2000s with 2 huge bubbles that caused house prices to deviate from tracking inflation. We are at the top of a bubble heading back down to the inflation line.

BobE, good information. That is substantively my view.

As a mortgage loan officer for a credit union, I can assure everyone that there is no “surge” in mortgage demand. It is still incredibly slow.

One of my clients works for a mortgage co that is laying off ppl every quarter. She said that they offer 40 yr loans and are approving “just about anyone”, even those who can’t afford it. She said it’s scary.I thought lending standards were tighter?

What???? Did I miss out again? A dip implies there will be rise again soon.

I fear my FOMO is kicking back into high gear. That is likely the intent of the headline.

It’s not FOMO anymore.

It’s GLDMOBCNREitFP

Glazed Look Definitely Missed Out Because Not Rich Enough in the First Place

sorry

/s ;)

sufferin’ – and here I thought it was my Parkinson’s when I looked in the mirror!…

may we all find a better day.

The financial media is just helping wall street pump up the market… and it probably works

1) Zori rent is 2K x 12 months = 24K/y. House prices = 500K.

2) In the next ten years, if the average rent increases will be : 5%/y

rent accumulation will be : 24K + 24Kx1.05 + 24Kx1.05×1.05 +

24Kx1.05×1.05×1.05…+ 24Kx1.05^8 + 24Kx1.05^9 = 302K

3) The value of the house should be : 500K + 302K = 800K.

4) If in ten years the price will be : 700K today prices are too high.

5) The intrinsic value of the house should be 425K ==> 425Kx1.05^10 =

392K.

Looking at rent to value (what old school Realtors used to call the Gross Rent Multiplier or GRM) is fun but does not tell you anything about “intrinsic value” since a newer high quality home with rent of $2K/month low taxes, low insurance, low utilities and no HOA will have a higher “intrinsic value” than an older low quality home with high taxes, high insurance, high utilities and a big monthly HOA.

The economy is being run in reverse. The FED should drain reserves and simultaneously lower their administered interest rates.

Draining reserves has an immediate effect on prices. Raising the administered rates has a delayed effect on prices.

Lending/investing by the DFIs expands both the volume and the velocity of new money. Lending by the NBFIs increases the turnover of existing deposits (a transfer of ownership within the payment’s system, and a matching of savers with borrowers within the NBFIs).

The American Bankers Association has flourished on its free lunch. There is no collateral shortage.

Michael, you need to recalibrate your slide rule. Average rent inflation since 1954 is 4.2%. Given the fact we had much higher rent increases in the last few years, its unlikely we’ll see continued oversized increases in upcoming years. More like < 3%

Not sure where you pulled up only $2,000 rent for a $500,000 house, but that number makes no sense. The monthly PITI cost of that house with 10% down at 8.5% would be about $4,500. I doubt anyone would rent a property out for a $2500/month loss

As a matter of fact, throw that slide rule away

I agree that landlords with a 8.5% mortgage will probably lose money renting a place out, but most landlords have mortgages at 3-5%, not 8.5%, or they have no mortgage at all. I’d venture to say less than 5% of landlords bought their properties the past year or two, when mortgage rates were high.

Once you factor that in, a $500k home renting for $2000/mo. can be profitable to most landlords, unless the home price drops.

@CCCB Knowing the average US rent increase since the 1950’s is like knowing the average current temp from Hawaii to Maine. In CA every fast food worker will be making $20/hr in 2024 (up more than 40% in a couple years) and few people moving to CA for jobs and afford to buy a home they want (putting more upward pressure on rents).

@Bobber Pretty much nobody is “paying”$500K for a home that rents for $2K/month, but lots of people “own” them. When my young cousin wanted to sell a home he bought in Folsom CA (for <$200K in 2012) when he was buying a bigger home in 2015 I convinced him to keep it as a rental and he ended up buying a couple more homes in the area a couple years later for ~$250K. All the homes are worth just over $500K today and rent for a little over $200K/month (with sub 4% mortgages).

Most of those workers are going to be automated away in the next 36 months down to a minimal staff.

And holding a property in todays environment at 500k but rents for $2000 a month is just losing money that’s why a lot of smart money sold out over 2021 , 2022 and holding paper gains is useless.

Wolf, it would be interesting to see a graph that combines “Purchase Mortgage Originations” (not just applications) and Refi’s to get an idea of just how much loan volume (and loan originators’ incomes) have plunged.

Ed Pinto over at AEI has a series based on rate locks, so further along than the MBA’s applications. It looks similar, but it lags applications a little. Applications is the most real-time as we can get.

Purchase volume was down 38% from the same week in 2019 and down 31% YTD compared to 2019.

Cash-out volume was down 72% from the same week in 2019 and down 67% YTD compared to 2019.

No cash-out volume was down 95% from the same week in 2019 due to refi burnout and down 93% YTD compared to 2019.

Wait…did Rupert buy the NYT on the sly to add to his American business media portfolio?

It gets tiring seeing these sensationalist headlines from the big news sites. I tend to just look at the headlines and then come to this site to see said headlines greatly diminished in impact or outright refuted with actual hard data.

All the bigs think that since things are trending down (even if it’s in the most minute of measurements) that the Fed will be forced into rate cuts by next year. There haven’t been any big movements I’ve read about that should trigger such a thing.

If anything, I’m curious to see how inflation is going to be impacted since that insurance adjustment thing is done and over with now.

Any housing articles on CNBC (e.g., the one you cite) are written by Diana Olick. She’s a moron.

When rates move from 7.80% to 7.60% she writes “Mortgage rates have plummeted!”

She’s also the climate and fitness correspondent…so that should tell you all you need to know.