Food is the exception and pricing levels “continue to be a concern”: Walmart CEO. Sky-high food prices rose further.

By Wolf Richter for WOLF STREET.

What we got today confirms what we’ve seen develop for over a year: Prices of many consumer goods are coming down from their crazy spike, and I mean prices are actually falling, rather than just rising more slowly, as inflation has moved from goods to services, such as insurance and housing. Falling prices are good for consumers, and they boost inflation-adjusted consumer spending and “real” GDP, but they’re not good for companies that sell these goods, though their own input costs are also declining.

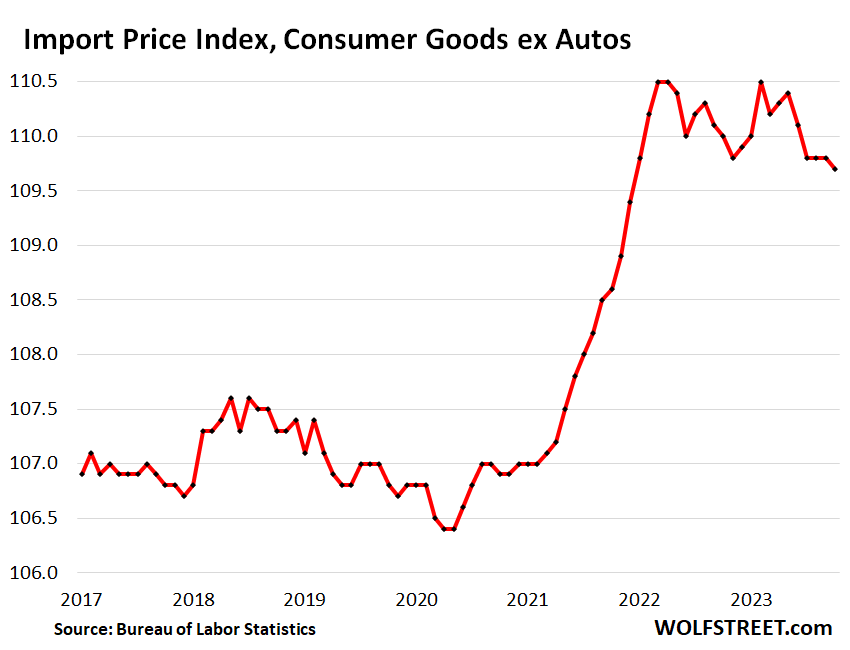

Import prices of consumer goods excluding autos – see Walmart, which we’ll get to in a moment – dipped again in October and are now down close to 1% from the peak in May 2022, after the surge, according to data from the Bureau of Labor Statistics today.

This is what we’re seeing elsewhere in consumer goods: Prices are easing off their sky-high levels, but they’re not plunging, as there is resistance by businesses to cutting their prices, but it’s happening. The drop in import prices of consumer goods reflects part of the input costs for retailers, such as Walmart and Amazon:

The pay-whatever craziness before.

Prices of many goods had spiked in 2020 through at least 2021, and for some goods deep into 2022, fueling the original inflation fire, with stupid inflation in used vehicles of 55% from 2020 through 2021; “stupid” because it was totally unnecessary. Many people – enough people to cause demand to collapse – could have just refused to buy and drive their trade-in for a while longer. But no. They were armed with stimulus checks, PPP money, extra unemployment benefits, spiking gains in their stock and crypto holdings, and what not, and they went out and gleefully paid whatever.

It gave rise to idiocies such as Tesla-flipping where people would buy a new Tesla and flip it for huge profits. It gave rise to a pandemic of addendum stickers at new car dealers that where ripping people off by charging $10,000 and more on top of MSRP while the ripping was still good, and people went for it and paid whatever instead of driving the still-good trade-in for a few more years.

This is “stupid” inflation: Consumers, armed with all kinds of cash, were willing to pay whatever, and inflation was off to the races. We started documenting this inflationary mindset in January 2021.

And now it’s over. Americans are back to their normal self, no longer willing to pay whatever when they go to the store or shop online, which largely ended those price increases. And goods prices are dropping.

But inflation moved to services, and 65% of consumer spending goes into services, and inflation is hot in services, such as insurance and housing, and that’s where inflation now is now entrenched.

Slight deflation in durable goods has been common for the past 20 years amid more efficient manufacturing, technical innovation, offshoring to cheap countries, etc.

Walmart: Consumers are no longer willing to pay whatever.

Walmart shed some light on this today when it reported earnings. Comparable sales at its Walmart U.S. unit – a huge ecommerce retailer and the largest grocery retailer in the US – rose 4.9% on the strength of groceries and ecommerce; and its ecommerce sales soared by 24%.

So there is plenty of consumer demand, even though more people buy this stuff online and avoid the stores, a structural change that has been going on for 20 years.

CEO Doug McMillon said on the earnings call (transcript via Seeking Alpha) that “the other good news is that general merchandise prices continue to come down.” They’re now “down low to mid-single digits versus last year.”

“That enables us to rollback pricing which will help our customers during this holiday season when general merchandise is so important for gift-giving,” he said.

“In the U.S., we may be managing through a period of deflation in the months to come. And while that would put more unit pressure on us, we welcome it because it’s better for our customers,” he said.

CFO John David Rainey told CNBC that consumers are “leaning heavily” into major promotions and search for deals. As customers hold out for lower prices, Walmart has seen a drop in purchases before and after a sales event, he said.

At the start of the holiday quarter — which began November 1 — sales of items including clothing picked up as holiday promotions gained momentum, he said.

But falling prices – though good for consumers and for inflation-adjusted consumer spending and for “real” GDP – are not good for stocks because they cause the opposite of rising prices: downward pressure on dollar revenues and profit margins.

So Walmart, which beat expectations today, gave disappointing earnings guidance. And worst of all, it slashed its share buybacks in the quarter to $111 million, from $3 billion in the same quarter a year ago, as it too is no longer willing to pay whatever for its shares. And the stock tanked 8% today.

Food is the exception.

Walmart, the largest grocery retailer in the US, pointed out today that food is the exception. “Pricing levels in many food categories continue to be a concern,” CEO McMillon said in the conference call.

“Overall, our [food] product costs are up versus last year, and they remain up even more on a two-year stack, which is putting pressure on our customers,” he said.

“Beef prices are high. But we’re happy to see lower pricing in dairy, on eggs, and with chicken and seafood. The pockets of disinflation we are seeing are helping, but we’d like to see more, faster, especially in the dry grocery and consumables categories,” he said.

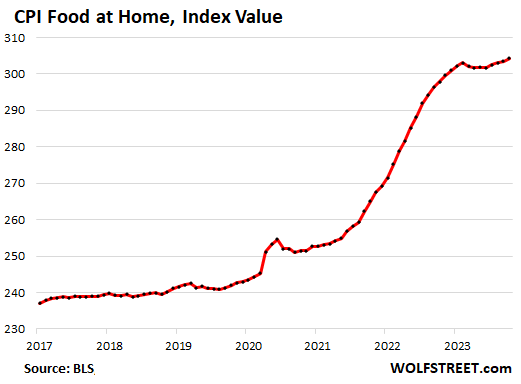

Overall, food prices have ticked up further from their already sky-high levels – after having surged by nearly 25% during the pandemic. We’ve discussed this in detail in “Beneath the Skin of CPI Inflation.” The CPI for food at home rose in October and was up 2.1% year-over-year:

But other goods prices dropped, consumers no longer willing to pay whatever:

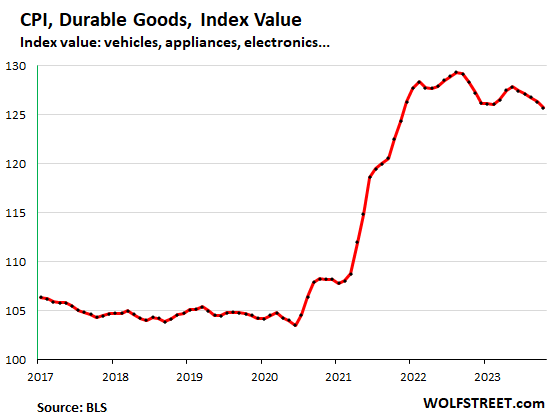

The CPI for durable goods (new and used vehicles, electronics, furniture, appliances, tools, etc.) dropped 0.4% in October from September and by 2.8% from the peak in August 2022, after the huge spike during the period when consumers were willing to just pay whatever.

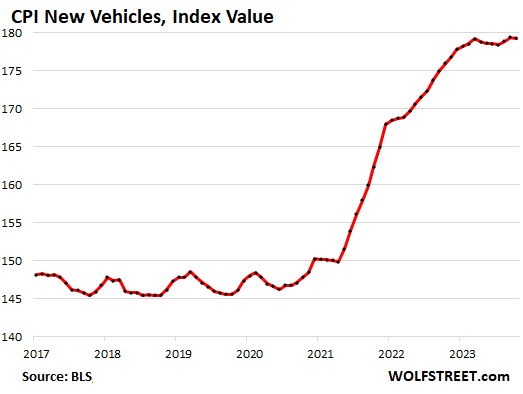

New vehicle prices have remained roughly flat for the past six months, after the 25% spike:

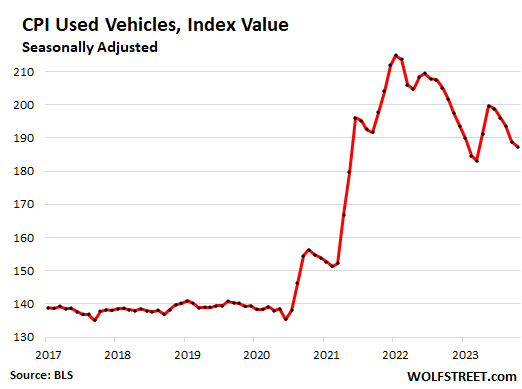

Used vehicle prices fell further in October and have dropped by nearly 13% from the peak of the spike at the end of 2021, after the stupid 55% spike during the pandemic. But it’s still up 34% from February 2020:

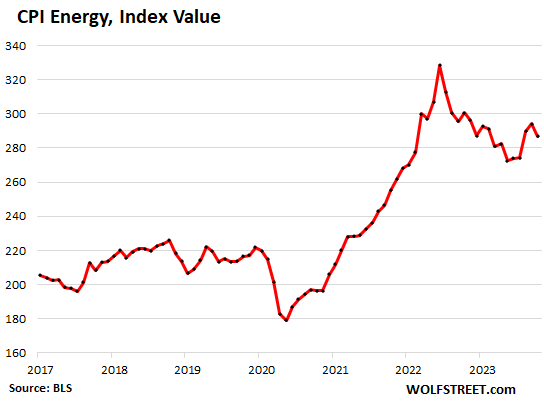

Energy prices have been zigzagging lower from the spike. The CPI for energy – half of which is gasoline, the rest is natural gas piped to the home, electricity, heating oil, propane, firewood, etc. – dropped by 4.5% and it’s down by 13% from the peak of the spike in June 2022.

But the energy CPI is near where it was in 2008, pushed down by gasoline and natural gas which are now both cheaper than they had been in 2008. Natural gas is trading for around $3 per million Btu currently, far below the $5-12 range in the six years between 2003 and 2008:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

There’s so much inflationary spending in the auto segment. They say the average new vehicle is $50k, but I can go buy a new Subaru Forester now for $32k. Are Subarus and Toyotas not cutting it any more for the average new buyer? If so, why?

The average transaction price is $47K. Lots of vehicles sell for less, a lot less, and lots sell for more, a lot more. Every major automaker has models that sell for less than the ATP.

My local Dodge dealer has the following listed.

2023 DODGE CHALLENGER SRT HELLCAT – Black Ghost Special Edition

MSRP: $100,865

Market Adjustment: +$125,000

Total: $225,865

Who would pay that kind of “Market Adjustment”? Or for that matter, who would pay that much for a Dodge?

Well, it IS the Black Ghost Special Edition, you know!

I believe they are ending production of those models, it could be the last. Can always negotiate the market adjustment part.

Remember we might have limited supply of everything else but when it comes to stupid a$$ infected with a case of FOMOism, we have infinite supply the Murica..

Honda dealer has a Civic on the showroom floor at 65k. Granted it has a bunch of crap on it I don’t know because I was too disgusted to look. 65k for a Civic?

Anthony,

Wait until you see the price of the Black Ghost Special Edition *Deluxe* (w/free cupholder).

Those adjectives don’t pay for themselves, you know.

FedUp – probably a Civic Type R. They are FAST tho – 300+ HP stock, and you can squeeze amother 100 HP out of that 4banger witu bolt-ons and a tune.

It would give that Challenger a run for its money in a 0-60 test.

MM

Interesting, although I would never pay that kind of money for one.

it sounds like the only consistent thing is that prices basically destabilized and are all over the place now

Funny how printing a ton of symbolic money doesn’t actually alter the supply of real assets…but does alter the ratio of symbolic money to real assets (formerly known as…”prices”).

Barter is looking better and better…

Heck of a job, Fed!

My daughter had 2015 expediation

owed like $10k

worth $16k

dealers $12k

she bought 2020 kia sportage(grad dec 2023 BS degree)

wanted better mileage now that mom/dad didn’t pay gas

she worked during college as we didn’t pay tuition/books

she got free rent and board(mom helped with gas)

—–

best lesson you can give kids – nothing is free

—–

she paid CASH FOR KIA sportage at 22

definitely knows VALUE OF $$$$

Here is another Tesla Model S with a new battery for $18,500 with lifetime free supercharging on Autotrader.

VIN 5YJSA1CN5DFP22476

You can get a model 3 Tesla for under $40k and the taxpayers will cover $3750 and in California they send you another check for $2k, so you are really barely paying over $30K

Available right now for my area (I just looked it up on Tesla’s website):

Model 3 price: $38,790

Destination fee: $1,390

Total: $40,180

eligible for the federal tax credit: -7,500

Cost: $32,680

Not including the California incentive

Amazing tesla builds those cars for such a low manufacturing price

And now you can even buy your new car on amazon! Not sure if they’ll deliver it by drone the next day though

I’m waiting for amazon to get in the real estate brokering business next

Plus $1,390 destination fee

Plus $12,000 for self driving package

Plus $475 for Wall charger

Plus $230 for mobile connector

Plus $250 order fee

Plus $250 registration fee

Plus $1200+ in sales taxes

WOW!! And all that for your very own Corolla sized electric car.

At least the total price went down a little. That is a TON of fees and extra costs though. Their real profit is on the software.

sufferinsucatash,

1. You’re comparing a Tesla Model 3 to a Corolla??? Your brain had a short-circuit, the CPU flamed out, and you need to get it repaired.

2. you added a bunch off stuff no one needs, including the self-driving package. And you added taxes and license fees.

3. Now add to a Corolla what no one needs. Start with the 2023 Corolla GR which has an MSRP of $52,640. And then add stuff to it that no one needs. And then add taxes and license fees.

4. Idiotic comment. The EV stupidities dumped into the comments here no longer astonish me. But they do get old.

Sure, but how much for the Tesla Black Ghost Special Edition?

And Elon is laughing all the way to the bank.

I have a friend (don’t we all, and doesn’t it make us a little green with envy) who got lucky, got rich, and got to retire at 44.

He has Ferraris and Porsches in his garage, but was once humble enough to tell me “If I wasn’t so lucky and wasn’t so rich, I would be driving a Toyota … well priced, low running costs, and reliable”.

So I can’t answer your question, but would add, in the last days of Rome, you could hear Lazius Arseius and his fellow Roman citizens shouting out: “F*&k it, just buy the expensive wine”

We clearly travel in different circles!

Perfect. Made me laugh out loud.

Lazius Arseius: “YOLO, bit*ches!! WooHoo!!…Does this wine, I don’t know…taste a little…lead-y…to you?”

That’s our finest Sherry!

Don’t be such a turd in the punchbowl!

Put my order in for my ‘22 wilderness outback in late ‘21 for 38k and some change. Traded n a 2015 Chevy Cruz for 9500. I could have sold it separately for about 13k. Today msrp on outback wilderness ‘24 is 39,900 and my old Cruz would be worth 3200. I did pretty ok for having been in the middle of raging inflation.

I just purchase a 2020 Mitsubishi Mirage with 60K miles for a delivered price of $11,600 from a reputable dealer. This will replace my 2000 Toyota Corolla historical vehicle which was totaled last week in a violent hit & run accident. Wolf is correct. Prices are coming down. There are now some good deals on used cars out there if you shop wisely.

daughter got(grad undergrad) kia 2020 sportage with 20k

$23k

had 2015 expedition – got $16k cash

paid off $10k loan

put in another $10k saved(as college student)

bank dad pooped rest

still provided excellent finanical moment

Would be interested to see what inventory carrying levels are for some of them like Best Buy. Their ‘deals’ either simply match Amazon or are the same products day after day after day. Hoping the stuff I am looking for goes on sale during the 10 day black Friday event.

“Black Friday” has been extended. It’s now Black Sunday through Saturday for the entire month of November and first two weeks of December. Hell, it’s every day of the year.

Soon enough…it will be Black October.

…when was it ‘Paint it Black’ was written? (1929 the ORIGINAL ‘Black Friday’?)…

may we all find a better day.

been commenting on how FULL of all vehicles(Used) dealer lots are

daughter bought 2020 Kia 2 weeks ago and paid cash($23k)

dealers woundn’t deal with 2023/24 on lots

she went with 20k used 2020

still has 2 years on 5 year warranty

my son made sure she didn’t get BS pushed by dealers

Deflation will be a new experience for us and I’m sure will bring pain in different ways. It will be interesting to “watch and learn”

But inflation moved to services, and 65% of consumer spending goes into services, and inflation is hot in services, such as insurance and housing, and that’s where inflation now is now entrenched.

Deflation in goods has been common for the past 20 years (more efficient manufacturing, technical innovation, offshoring to cheap countries, etc.)

Wolf,

(I know you are simply following convention but…)

Thanks for throwing the “housing” clarification in there.

But “Services” sounds so benign and optional (like a second massage at DisneyWorld…) and since HOUSING is 30% of all HH expenditures (and so maybe 50%+ of all “Services”)…maybe we all oughta swap HOUSING for Services in the nomenclature.

Only partially kidding.

“Services” lets the responsibility for horror become too diffuse…and therefore less amenable to solution.

Services = 65% of consumer spending. Inflation in services is NOT benign. I’ve been railing about it for 18 months.

believe me I close my eyes when I have to call on services

recently had to have 15′ of sewer line repaired from cast iron to abs

simple little 6 hour job(not nice)

$4k

material line was 1 unit $1k – no explanation

THANK YOU PLUMBERS FOR help

talk about having bad taste in mouth

I was musing yesterday about a theory related to this and admitted I wasn’t an economist, so not able to test this but…

I suspect prices consumers are willing to pay are anchored to online price histories, which have become increasingly transparent to the consumer in some categories. There are several that track Amazon and Walmart goods specifically. This may be further influenced by histories that reflect episodic price drops.

Other categories, such as services and groceries, have way less price history available to the consumer and thus experience less bargain behaviors.

I do think that greater price history transparency would help restrain acceptance of inflation.

I do think that even casual consumers get pissed when they find out last year’s Product X for $100 is now this year’s product X for $125. Ain’t all that much that’s really changed in the real world.

See also, $1.25 DollarTree…

no kidding, I was thru a store and wasn’t looking for anything I needed

when I spotted nice product(don’t remember) and price was $225

I was like REALLY

I rarely look at prices at checkout

just hand over cc and charge it

2023 – YEAR OF LIVING PAYCHECK TO PAYCHECK

RETIREMENT – no way TODAY

gonna have to wait til I can save again – thinking 2027 ????maybe

Interesting that prices of discretionary goods continue to go down but essentials remain elevated.

Exactly what monetary inflation should achieve in the long term

Yep,

Plenty of free bridges for people to be “housed” under…

willing as good christian to drop off plenty flour/canned goods for them

govt made them, and I won’t prevent them from being fed

gotta love our new found fascism

In other news, Hyundai announced that they would be selling vehicles on Amazon.

No, not The Onion. Per Automotive News.

I’d buy a Hyundai on amazon just so I don’t have to buy from a stealership.

LOL. You just read the headlines again, didn’t you?

You can shop for it on Amazon, but it’s the DEALERS that list their vehicles on Amazon, Amazon will allow DEALERS to list their vehicles on Amazon, and you get your price and pay for it online, and you’ll buy it from the dealer.

State franchise laws don’t allow automakers to sell behind the backs of their dealers directly to the consumer.

Tesla, when it was a nothing, got a bunch of states to exempt it because it was a nothing back then, and they figured it would never be anything, and the problem would vanish when its stupid EVs that will never work would vanish.

How is that different/better than cars dot com ?

Yes. Or the dealers’ own websites.

my daughter found this out couple weeks ago when she was looking for more fuel efficient(non-ev,over priced hybrid)

she got 2020 Kia Sportage(just graduating college)

better than her 2015 expedition(she used to haul church teens with)

I love my 2001 DIESEL – pulls greatly

Yeah you’re going to be double screwed there buddy.

You have to find the new dealers who sell at rock bottom prices just to move units. They are out there!

It’s a large 48 state country, just drive your savings back home! :)

sufferinsucatash (I’m lisping as I write this) your comment prompted me to ask my freebee version of Chat GPT which state has the lowest new car prices. New Hampshire, according to some article in Forbes.

Relying on ChatGPT is like relying on general information. Your mind is much more capable. Albeit lazy.

There used to be whole forums dedicated to finding the best car prices. Then Reddit came along and someone would post there “I know a better price!” And 18 people would down comment him/her.

The forums were the ticket.

I don’t need anything and they can go bankrupt

looking forward to mal-investment getting business lesson(ie bankrupt)

always on look out for GOOD investment opportunities

nothing in past 5 years

I have seen this Tesla Flipping first hand but with 2022 and 2023 new dirt bikes and side by sides. I watched as industrious individuals would get on the list for these new units. They became middle men and would flip them on craigslist and marketplace. Since they would buy every bike coming in that would leave the showrooms empty. It looked like they made a few thousand a flip from what I could see. Now I am seeing these same individuals stuck with more than one bike and keep slashing the price but no sale! One guy in Minden NV has been trying to sell four or five ” Brand New Never Ridden ” Honda Yamaha and Kawasaki Bikes for months. Now with the 2024s coming in these bikes are 1 and 2 year old new bikes. I would think this is happening in many more markets like autos RVs and even furniture.

Couldn’t happen to better people!

Cars, bikes, homes… there is always someone who makes money flipping, but never knows when to get out of the game and gives back all his profit in the end.

In my area news stories abound after the 2008 housing crash about flippers stuck with 5 to 10 houses they couldn’t unload.

Felt really bad for them…

Not just 2008. I knew two realtors who filed for bankruptcy back in 1983. Same issue.

At least the boat market is rational.

…ah, those never-plugged holes in the water…

may we all find a better day.

Deflation is a nightmare in my option for our economy and businesses. A low inflation much preferred however with the economic activity that was propped up by zirp and bond purchases by the fed generating less and less gpd can quickly unwind. Price stability is what we want deflation is not stable pricing .

But inflation moved to services, and 65% of consumer spending goes into services, and inflation is hot in services, such as insurance and housing, and that’s where inflation now is now entrenched.

Deflation in goods has been norm for the past 20 years (more efficient manufacturing, technical innovation, offshoring to cheap countries, etc.)

The FED is to maintain up to 2% inflation over time. Might require some deflation to get there.

Deflation a nightmare? Are you serious? Are you a FED-paid economist pretending to be someone on the internet?

Without central banks counterfeiting money (which is fraud, a form of theft, upon which the central institution of our economy, money, is now based), deflation would be normal in most things as improved efficiency lowered prices across the scale.

It would not be borrowers who benefited as they do now with inflation, which erodes the value of the remaining principal by defrauding the lenders who remain gracious enough to lend.

Deflation would increase the burden of the remaining principal over time, thereby encouraging shorter term loan durations. It would promote thrift and future orientation.

Did you get a BS degree in economics at a university?

I been hearing the deflation fear-mongering all my life. At this point people are so brainwashed to fear prices actually going down and savers actually coming out ahead of the speculators/borrowers, they just can’t fathom a different way of life.

Only someone who never lived with deflation could wish for it. There’s a reason states avoid it like the plague.

BS ini-

You’ve been reading Ben Bernanke.

“Price stability” is NOT what we want, at least if to get there we have to use price manipulations and subsidies.

What we really need is economic system sustainability, which in turn relies on prices determined by unhindered production and natural (non-subsidized) consumer demand.

Let prices fluctuate and do what they do: send accurate signals to producers about what consumers want them to produce next.

Great point. System stability is lacking at this time. Bernanke’s model relies on ever-increasing debt until the system erupts.

Dots, the box of candy, was a dollar a couple of years ago. It went to $1.29 a year ago, and then a few months ago to $1.49. Today it is back down to a dollar. But we all knew food inflation was over, and any deflation will just be back to “normal” prices a couple of years ago. The bottlenecks and gouging are pretty much over for food. But service prices, as in wage costs, you can be pretty sure will never go down, especially among union and government workers.

I hope so. I’m tired of over paying for groceries.

And, frankly, I’m tired of overpaying for Dots.

*But service prices, as in wage costs, you can be pretty sure will never go down, especially among union and government workers*

Agreed on the salary of the government workers

But in a deep recession, wages can not only decrease, but disappear overnight.

When someone loses their job, it will be harder to find a new one, and if you do find one, it will be at a lower salary.

This is how wages in the private sector can also decrease. A deep, all-out recession is simply needed.

Did you check the net weight on that box? Many items we buy did not necessarily increase in price overall, but the price per ounce sure did. “Shrinkflation” is worse than inflation sometimes.

Shrinkflation is fully accounted for in our inflation measures, which go by weight or volume (per ounce, gallon, pound, etc.) not by packaging (box, bag, bottle, etc.). So it measures the price of gasoline by the gallon, not by the “fill up”, and it measures OJ by the ounce, not by the carton or bottle, it measures cereal by the ounce, not by the box, it measures coffee beans by the ounce…

Shrinkflation is designed to deceive consumers (good luck!), but it’s fully accounted for in CPI.

My Suave hair shampoo got hit with massive shrinkflation this year. Same price $1.97 but 25% less shampoo. The size difference in the bottles is overt.

Who do they think they’re fooling? Just raise the dang price, J&J!

The one I don’t think I’ll ever get used to is the 6 pack box of granola bars that now only have 5 in the box.

Or the chip bags that are mostly air. You take them up to altitude and they inflate like a party balloon. We will know the end of the dollar is here when we see chip bags floating through the air.

I’m waiting for the day that my six-pack of IPAs only has five cans in it.

Phew! So relieved to hear our ever thoughtful government thought to include shinkflation into the CPI. Now i know I can used the CPI confidently as a financial guide for my life.

If CPI says prices only went up 3% or whatever, that’s all I need to increase my budget to keep the same lifestyle. I can count on this.

I did not mean to suggest otherwise, WR. I was referring to William’s box of Dots specifically. And I hate it because they’re trying to be sneaky and we know it and they know we know it. I hate playing “spot the difference” on every aisle of the grocery store.

They really get into that kind of minutia?

Where does one learn how many ounces of grape nuts Kellogg’s sold to bilo grocery in detroit?

sufferinsucatash,

Don’t be silly. Every package shows the quantity. Every computer file that tracks that package includes the quantity data. At some stores, it even shows up on your receipt.

For shoppers, price per ounce is basic math. I do it all the time because I don’t want to get ripped off by the different package sizes:

One granola box is 12 oz., the other is 15 oz. The first costs $4.95, and the second $5.95. Which is more expensive???*

I do this stuff in my head routinely and base decisions on this. If you don’t have your head with you, you can use a calculator.

*the first one.

…didn’t this happen to dimensional lumber a long time ago? (…for those unfamiliar, measure w&d of a ‘2×4’, ‘4×4’, etc. Now how to make that 5-pak the new standard?-gottit, make it a FOUR-pak with extra cardboard packaging… ).

may we all find a better day.

Mustbeaduck, same weight, 6.5 ounces. This was clearly a case of price gouging. I responded by not buying Dots at a ridiculous price, which is the correct response. Just like I won’t buy a house until the price gouging is reduced or eliminated.

Julian, when a worker is laid off, he no longer gets a wage. It’s not like all the unemployed who get zero wages are lumped together with wage-earners to calculate an average wage. So when a worker is laid off, it has no effect on the average wage (or wage inflation). It does increase the unemployment rate. I think that is how it works.

When I worked in high velocity consumer packaged goods (groceries primarily) we had access to incredibly detailed data down to the item/store/time level, plus all the product attributes you could imagine.

Amidst raging shrinkflation during the great recession I developed a simple measure that kept everything roughly constant, cost per calorie. Forget about ounces, units/package, etc. cost per calorie was the key to understanding price variation over time for edibles and led to some very actionable insights for my clients.

My employer ultimately shut down that avenue of research when the recommendations coming out of my group began to contradict those coming from the price elasticity team.

My earliest experience of shrinkflation was in the early ‘70s with a snack called Wagon Wheels — even a 10 year old could figure it out.

I want 2020 back. Look at all of the charts, they are all the same. Will we ever get back down to a lower trend like 2020 and looking back?

What a mess. Free money sounds great, until it isn’t free anymore. It came fast and easy but the payback will take years if even then.

The best chance for prices reverting to pre pandemic levels is via the deflationary forces associated with a recession or worse.

Would love to see insurance companies come to the same epiphany, but I’m not going to hold my breath though. You have to eat to live, but more & more people are dropping homeowner’s insurance. That’s a pretty good sign. Something tells me Allstate, State Farm et al aren’t listening.

Everyone loves the equity in their house until the insurance to cover it costs more than their original mortgage did.

And therein lies the problem with equity, for someone who buys a house to live in rather than speculate… equity actually becomes a burden in the form of tax & insurance increases.

wow! my sentiments exactly. I keep telling my circle I want my home price to be 50% underwater right up until the moment I need to sell it. :D

I can’t stand people complaining about loss of 10% equity in their homes etc.

Yea its a stupid system. If housing wasnt so expensive, people could just invest that money elsewhere and get equity other ways, but people LOVE their houses being expensive, because in the future it will be more expensive and they can somehow use this magic money by selling their current house and buying a cheaper one! But they forget all the houses rise in value so now that cheaper one is also similarly overpriced. And eventually you hit a point where the younger generations cant afford houses until theyre well in their 40s. Broken system, needs to collapse and never be rebuilt. No other solution.

This is why I’m moving onto a mat. Houses suck.

Most people have way more insurance than they need. Fear sells. Look at your personal history of claims and adjust coverage and deductables accordingly. And if the insurance provider is a household name and runs ads on TV, you are paying too much regardless.

My rates have increased also but I would bet I pay about half for better coverage on a higher-value home (SF bay area) than most do. It is a product like any other. Rather than cancel, trim the fat.

Pay only for the risk you are not willing to accept yourself.

A family with a newborn making 400K called into an Atlanta based finance call in show the other day…

They insure thru USAA, they said they have 1.5 million in assets (guess it’s mainly the house). Their mortgage is like 600 or 800.

They have an umbrella policy for a million.

Their life ins. was not ideal. The host told them to get 10x the life insurance on each spouse. Just to maintain the lifestyle if one earner should pass away.

So in that case they needed More insurance.

You insure for the assets you are protecting. A mortgage does reqiure insurance but not low deductables, earthquake, high limits etc.

People buy umbrella policies not understanding that they don’t even come into play until your main policy is exhausted, resulting in money wasted for nothing, in my opinion. I asked my agent how many times she saw one used, and she told me twice in 30 years. To each his own. For me, my strategy has been well suited for a very long time.

Doug P,

It just has to do with how many assets you have and your liability profile while interacting with the world. If someone could possibly sue you, to take your wealth , then they are nice to have.

Pretty cheap as well. A million dollar policy is like $99 annually.

Sucatash –

I bought into the umbrella policy mentality a few years ago when my daughter was in a car wreck that settled for the entire amount of her policy coverage.

I now carry an umbrella policy for an additional $1 million. That policy protects me up to that amount over my standard coverage. However, what prevents someone from just suing me for $2 million and I’m right back in the same situation. Can’t seem to find a clear answer and would appreciate your insight.

Russel, the more coverage you have, the more incentive of the insurance company to fight your claim vs settle.

A friend of mine was hit with ridiculous claims after he accidently bumped the car of a low life at 2 MPH. Because he had high liability limits, his insurer spent $150k on trial defense and prevailed in court.

So if you have a $1 mil policy, yes sure, the claimant will find out the limit in discovery and sue you for $2 mil+, but theoretically, your insurer will fight to protect their $1 mil, which will also theoretically protect you above that amount. So if the insurer can get out for less than $1m, which is likely unless you badly disabled someone, you would be fully covered.

Freewary –

Thanks. Clear, simple explanation.

Example: For me as a single guy, zero use for life insurance

Most homes are financed with mortgages where lenders require an amount of coverage. This limits most people from doing exactly what you are doing, which is smart.

do not do what doug suggested regarding adjusting your property coverage downward —

if you are not insured to at least 80% of value you will be in a situation called co insurance —

under co insurance,after the deductible is applied,the claim is adjusted so that the insurance company pays a certain %% and the property owner pays a % –you are in effect self insuring a portion of your risk —

here is a link that explains co insurance —

https://www.investopedia.com/terms/c/coinsurance-formula.asp

That’s garbage. With most insurers, you’re not allowed to tell them what you believe is the real replacement cost is. They, of course, want to say the replacement costs is skyhigh. You don’t get to tell them what percent to use for covering your interior contents. About all you get to do is adjust your deductible which has very limited effect on your premium.

Now, what most people DON’T do is to shop their rate every few years. But with the way premiums have been increasing, even that is getting to be a nothingburger.

Friend of a friend in Florida dropped the insurance on their house then Ian destroyed it, but they just sold another rental to pay for the repairs…

So if insurance is getting dropped then does cost go higher with fewer people to spread the risk over or does the risk and cost stay the same . I’m thinking same cost same risk same premiums

Harvard degree?

Bs – those newly uninsureds are no longer part of the risk pool and as far as the insurance co.s are concerned they don’t exist.

That risk now belongs to the homeowner in the case of a one off loss (fire for instance). Should a mass casualty event occur (hurricane/tornado) the loss would be FEMA’d up by the Feds in some morally hazardous manner.

Risk and cost stay (roughly) the same for insurers but total revenues decrease. Remaining risk is transferred to owners and taxpayers.

Meanwhile, the 10 year keeps on its downward trajectory. I’m so sick of this crap.

No. the “downward trajectory” stopped on Tuesday at 10 am after the 10-year yield plunged to 4.41%. It stayed near there all day Tuesday and on Wednesday and today. It’s now 4.45%. Actually up a little from Tuesday 10 am, LOL

That’s what I get for reading a CNBS article that came out today that says, `The yield on the 10-year Treasury was down by 9 basis points at 4.45%.” And that wasn’t the headline and was dated today. Been busy and didn’t look it up myself. That’s what I get.

Buy some TLT if you really think long rates are going down.

MM

I don’t think one way or the other as far as direction of rates. I was just quoting garbage from CNBS. I don’t know what to think jn this corrupt country anymore. I don’t want rates going down, but since all this country stands for is greed, consumerism, and wall street, I wouldn’t doubt rates go down.

FedUp – rates will continue to rise, in my opinion. I’m literlly betting on it.

Just not in a straight line, as Wolf frequently points out.

What is keeping the grocery food prices so high?

Cream Cheese is an item I notice fluctuates a lot. Without a sale it is $5. With a sale it is $2.50.

And just a passing thought: Walmart has sales? Wow! I never go into one unless I’m forced to.

The run on bagels has driven all topping up outside of plain butter.

I would think it’s because we the consumer can do a “buyers strike” with goods, but if we try that with food we will die

You should go sometime. They have just spent 100s of millions to spruce them up. Our local Walmart rearranged the shelves, painted the outside, slicked the shiny floors now it looks like a warehouse. Every isle has a push cart with big blue totes pushing there way around customers standing at a display trying to compare prices.

It’s fantastic!

I’m just waiting for the fork trucks to come down the new wide isles.

This is the place to feel valued especially when it’s self check out time.

Sufferin-

On cream cheese: remember last holiday season the Philadelphia company came out and sorta pre-announced a predicted shortage of their product. Very much like the “egg shortage”, I think it was a bald-faced lie to jack up prices and see who would still buy it. And how many would even stock up at the elevated price. I, for the record, never saw any change in available inventory at any of the stores I visited during that period. It seemed very plainly to me to be a fabricated excuse to jack up the price as much as possible.

Since then, even after the “shortage” ended, the prices remained high, but may be coming down now, along with lots of other jacked-up prices.

I suspect part of the lowering process will be having half-off sales like you’ve seen. And as the price restabilizes at fair market value, the list prices may drop back down from that $5 to maybe 3.99 or 3.79, with sales in the 2.50-3.00 range.

Inflation in everything you need. (Note: “Need” keep being redefined).

Deflation in everything you want.

That’s the world we’re in.

Mike R. -very well observed. (…what’s that old saying? ‘…to dine with the elite, cater to the masses…’).

may we all find a better day.

What is fascinating to me right now is the speed at which the reverse repo is being sucked dry. We are down to 912 billion now and in the past week the pace seems to be about 80 billion a week. Now I have to admit that when you look over a longer term, the pace might be only 40 billion a week.

My theory continues to be that after the reverse repo is dry, the shit is going to hit the fan. This reverse repo money is where money markets have been parking cash they have from investors earning 5% to just stash their cash. Right now, that money is being sucked from the reverse repo into short term Treasury issuance. Think of this a big pool of liquidity that is providing demand for short term Treasuries, but it is a pool that will eventually hit an end.

Depending upon the pace that the remaining 900 billion gets sucked out, it could hit zero anywhere between February and maybe April at the latest.

The problem is that once this piggie bank of liquidity is gone, what happens? The Treasury still needs to issue a ton of Treasuries, so where does that money come from? Seems to me that bank reserves are the next pile of money and we also might see money getting sucked from longer dated Treasuries into the short term Treasury market. But then that means that longer dated debt runs into supply-demand problems and where does that come from? It creates higher long term rates as the marginal buyer wants higher rates. I need to understand better how the bank reserve system works and what implications that has as a source for short dated Treasuries.

When Yellen decided to change the issuance from long to short dated Treasuries, it stopped long term rates from rising, but it didnt solve the problem.

I would also say that I have been wondering why QT was not causing equities to crash, the way it did the Fed was pulling money out. Now what I see is that they are just drawing out liquidity that is sitting there in the reverse repo. But this is a very short term situation. The cash is going to run out.

There are tons of very smart people on Wall Street that see this coming too. I’m sure there are some models built that look at exactly WHERE, OH WHERE, will all the money to fund Treasury issuance and QT come from? These people will take action ahead of when the reverse repo runs dry, so expect the market to anticipate this by weeks to months.

The ONLY way to prevent a crisis is to stop QT and leave the Fed with a massive balance sheet. But that is inflationary and it is risky. So my guess is that before consumers stop buying and before companies start laying people off, we are going to hit a financial crisis and the financial crisis will be the thing that brings on the layoffs and that triggers the recession.

The only question is whether the Fed will finally say enough is enough and force the politicians to cut spending and raise taxes to put the deficit on a more sustainable path, or will they cave and go back into money printing?

“My theory continues to be that after the reverse repo is dry, the shit is going to hit the fan.”

Quit this BS.

THE REVERSE OVERNIGHT REPO FACILITY WAS AT $0 before January 2021, and it will go back to $0, NO PROBLEM

It’s the reserves you’ve got to watch, but they’re rising, and hit $3.3 trillion. Long way to go. But that doesn’t fit your narrative, right?

It’s normal for RRPs to be at $0. It’s abnormal for RRPs to have had these huge balances. These huge balances occurred twice, both times as a result of huge QE. And now RRPs are on their way back to normal.

Wolf, question.

If RRPs are a way to take liquidity out of the system, then this is clear the Fed is sharply reducing that effort, right?

Any raising of rates off the table, but the QT can keep going and without concerns of smothering the economy, right?

Not exactly. It has to do with what other Fed products are paying in interest. This is from Wolf’s article on September 16th.

“This 5.3% is less than what the Fed pays banks on their reserve balances (5.4%), so banks don’t use RRPs much. For money market funds (MMFs), ON RRPs are a good risk-free deal, but they pay a little less interest than Treasury bills (around 5.5%). And MMFs have been yanking their cash out of these RRPs, to load up on T-bills.”

and…

“Rising/falling reserves & RRPs don’t negate effects of QE/QT. They’re part of those effects.”

https://wolfstreet.com/2023/09/16/feds-balance-sheet-liabilities-rrps-plunge-reserves-rise-after-bank-panic-currency-in-circulation-dips-after-pandemic-spike-tga-gets-refilled/

1. “If RRPs are a way to take liquidity out of the system,…”

The Fed makes RRPs available, and money market funds use this facility because they have too much cash that suddenly came in with QE. Back in early 2021, with all this QE liquidity sloshing around, as money market funds were trying to use this cash to buy T-bills, the new demand pushed T-bill yields below zero, which threatened money market funds because they might “break the buck,” which can cause all kinds of contagion. So the Fed stepped in and gave MMF an outlet where they can earn interest on their excess cash. Before April 2021, the Fed didn’t pay interest on RRPs. That’s all that changed.

2. QT will whack the same asset prices that QE inflated, which is why the manipulative Wall Street crybabies totally hate QT and come up with all kinds of reasons why the Fed MUST stop it.

For a long time, QE did nothing for the labor market or the broader economy. It just inflated asset prices. And then the dam broke, and QE inflated consumer prices, which did a job on the economy that is now to be dealt with.

Same with QT, it does nothing to the economy or the labor market, it will just deflate asset prices; and eventually, it will help get inflation under control.

Contrary to the FED, MMMFs are not banks. They are intermediary financial institutions, NBFIs. Their deposits should not be double counted in the money stock. I.e., the transfer of funds from O/N RRPs to the MMMFs is an increase in liquidity.

Spencer G

I Didnt say the banks were the only user of RRPs.

And someone is using the facility …. .it was over $2 Trillion at one point.

Perhaps I have a misconception. RRPs exchange securities for cash.

Money market funds use the RRP, not banks. Banks use the reserves facility at the Fed which pays more, and which only banks can use.

Don’t you ever read anything here????

For example:

https://wolfstreet.com/2023/09/16/feds-balance-sheet-liabilities-rrps-plunge-reserves-rise-after-bank-panic-currency-in-circulation-dips-after-pandemic-spike-tga-gets-refilled/

Dude, you received the red font lashing. I feel better now. ;) lol

Question though:

The real NIRP of 2020-21 did create monetary excess though did it not?

So if the Yield Curve uninverts healthily, and the Fed maintains these rates wouldn’t that mean that the long end goes up?

Because the only reason the Fed would cut the short end would be recession. They control that rate. Not the bond market.

So how does that play out? Because MMF’s are taking on more TBills to exceed returns on the overnight facility.

Do you see immaculate disinfection still being the most likely? Or do you see a reacceleration of inflation? Or a recession (which I admit, I see no indication of)?

This deflation reminds me of furniture sales. Save 50%, but you know they already jacked the price up more than that. I don’t call it deflation, when there was just a huge ramp up, and some of it backs off a bit.h

I understand that’s how you feel. But this website is not about how you feel. That’s what a kaffeeklatsch is for. What you need to say is something like this, for example: there was x% inflation in durable goods from this period to that period; and since then prices fell, and so since then there is y% deflation in durable goods. And then you can add that durable goods are still z% higher than they were three years ago.

Hi Wolf,

a short follow up question regarding rates.

We still see inflation in services which Fed cares a lot about. Fed also cares about labour market, still strong. And we also see a quite good health in loan segment (auto, mortgage, credit cards) from your summaries a week ago.

So we could exptect the Fed to keep rates up for a “while” until something breaks up? I assume that an easing in todays environment could trigger higher demand = higher core inflation.

Is that correct?

The last time something “broke” (bank panic in March), the Fed continued to raise rates and just dealt with the issue through short-term liquidity support.

This was the official confirmation that the Fed separated monetary policies (rates, QE/QT) from fixing temporary issues, such as a bank panic or a market freezing up.

So if core inflation goes down low enough for long enough for the Fed to be convinced that it’s finished, it will cut rates. If inflation is high, the Fed will not cut rates, and if something “breaks” it will deal with it in other ways.

It looks like the ability to dictate prices by producers is slipping, just as the unions are striking and the costs to businesses from these strikes havent fully been factored into their business costs. Not good for businesses going forward.

“Food is the exception and pricing levels “continue to be a concern”: Walmart CEO. Sky-high food prices rose further.”

Eating is so overrated anyway. /s

Fed Up,

Inflation is just trying to slim you guys down.

Put that $20 tub ice cream and the steak back hahahaha

Better buy eggs & rice and beans for protein (they’re delicious, don’t knock it).

“Inflation Diet” could be a new fad weight loss diet.

U can’t afford Weight Watchers & the Gym anyways cause, u know, Services Inflation.

I thought the spike in auto prices was the result of chip shortages during Covid. That lasted for a while didn’t it? Has manufacturing for autos recovered or is dealer supply (still) constrained? This isn’t my wheelhouse, so I’m just curious if auto pricing is just gouging or if there are real market forces at work.

There were permanent increases in labor costs over the pandemic that have raised the floor for new car prices. Also there has been a shift to more NA vehicle content as a result of USMCA and transportation costs, which is driving the increase as well.

That said, some of it is consumers are flush with cash paying whatever for that new truck/SUV.

pm – production capacity has recovered, more or less. It varies by OEM, but for the most part they (collectively) could make and sell 17MM units per year if they wanted to. Margins would fall, but it could be done.

In order to move that much plastic the transaction prices would need to come down quite a bit from $48k, and they’ve grown to like that $48k. It funds EV research and has kept stock prices manageable vs. pre-pandemic (F flat, GM -25%, STLA +30%).

More importantly, ask yourself why they would relent on price when the total dollars now are so much higher than they were pre-COVID. Rough numbers:

2019 – 17MM units sold at $38k/unit – $663B

2023 – 15.5MM units sold at $48k/unit – $744B

Overly simplistic, but directionally correct – 12% more $ for 10% less work, I’ll take that all day long. Granted, the 12% increase in dollars doesn’t cover inflation, but they’re keeping up better than I am.

And in order to really change the situation on the ground a big fraction of those 1.5MM incremental units would need to be Cars (vs. SUVs, and Trucks). None of the historically domestic OEMs can make money on Cars. That’s why they ceded that market to the historically Japanese (and Korean) OEMs prior to COVID. The current situation has been building for a long time, COVID just accelerated things by 5-7 years.

The good news, nobody needs a new car. Post 2010 product will last 20 years+ with proper maintenance. I’ve made a great living off new car sales and still I tell anyone who will listen – buy a 5 year old Toyota (or Honda, Mazda, Subaru, etc.), and think of it as a mobility device, not a status symbol. A depreciating asset, not an investment

I would say it’s recovered, but new car prices aren’t likely to outright deflate in any meaningful way. Used car CPI will keep chugging downward for another quarter or two

Here’s the chart of the Manheim wholesale prices, not seasonally adjusted (red) and seasonally adjusted (green). I took out your link to the Manheim general page. So these are wholesale prices. Retail CPI chart is in the article above. The both look similar, with retail prices lagging a little.

Housing starts and housing permits were up in todays economic report.

It’s a two tier economy, and the bottom tier is running out of money. Those in certain industries can lobby for wage increases to fight it but it won’t be enough. Watching personal savings rate closely.

Let’s all thank the Fed for goosing the labor market. Better to have people working and deal with elevated inflation than to have people without jobs has been the thought. Keeps GDP positive. The wealthy get to watch their assets appreciate, and the poor are too tired from working to complain. Well it’s going to decimate the middle class if it continues. There simply won’t be any upward mobility because prices are rising faster than wages can chase them. Real DPI has flatlined well below trend and won’t recover. The policy has been a disaster. Slow clap.

I read an amusing, although irrelevant article on the massive wealth inequality amongst only the top 1%. I don’t think the tiers are even as seems like top tier of those doing okay might be 70-80% while the bottom 20-30% are having a tough go of it. Admittedly generalizations but wage gains recently combined with free money helped quite a bit. It does seem many labor leaders are more aligned with businesses rather than labor but likely more complex than that.

“Let me tell you about the very rich. They are different from you and me.”

– F. Scott Fitzgerald.

I find it hilarious that Walmart is talking about consumers no longer “paying anything,” yet automakers are jacking prices by many thousands of dollars per year on all models.

If “consumers” can’t or won’t afford the price increases on cheap Walmart sh!t, how in the world are they able/willing to keep up with the nonsense in expensive things like autos?

This whole economy is broken. The pricing no longer makes sense. And the entity charged with maintaining stable pricing – the FED – is the one who broke it. Like the BLS, all the top brass at the FED should be fired and replaced. And the new replacements should be reminded of their mandates, and explicitly told that they will be replaced as well if they don’t adhere to them.

“yet automakers are jacking prices by many thousands of dollars per year on all models.”

Automakers DID jack up their prices. But that ended in 2022. You’re living in the past. Now there’s plenty of inventory and lots of competition, and price increases ended about a year ago. Lots of brands are CUTTING prices either directly or through rebates and incentives.

“If “consumers” can’t or won’t afford the price increases on cheap Walmart sh!t, how in …”

Look this is the stupid BS that drives me nuts. I can afford all kinds of things but I REFUSE to get ripped off, I shop for deals. That’s the normal American condition. But during the pandemic, that broke, and people paid whatever. Now they’re back to normal and REFUSE to get ripped off, though they could easily afford to get ripped off.

Refusing to get ripped off and shopping for deals is different from “can’t afford” to buy. This braindead BS has got to stop, dude. You’re so pissed off about everything that you cannot use your brain anymore?

“Automakers DID jack up their prices. But that ended in 2022. You’re living in the past.”

I beg your pardon, but every single model I have looked at has had a large msrp increase over last year.

And my brain is doing just fine, Wolf, but thanks for your concern. LOL. Didn’t mean to set you off.

I know you understand how the legacy automakers work, which is why I’m so surprised you’re giving me this BS. Legacy automakers don’t cut the MSRP. Instead, they’re using incentives, rebates, dealer cash, rate-buydowns, etc.

For example, here in the Bay Area, San Leandro Ram dealer, in inventory on their website:

New 2023 RAM 1500 Big Horn, stock #230710

$57,665 MSRP

-$5,020 Dealer discount

$52,645 “sales price”

-15% Off “sales price”

$43,995 “Net price”

The dealer has a bunch of trucks priced like this.

The first 2024 models have shown up, and they come with discounts that include a “dealer discount” which varies by truck, plus “National Retail Consumer Cash” of $4,500, so even on these 2024 models, you’ll get around $5,000 to $6,000 off MSRP.

So these are huge price cuts. That’s how they work. Tesla cuts its sticker price. But the legacy automakers hand out incentives to bring prices down without cutting MSRP. This has always been the case, and you know that too!!!

Go online, check the websites of the RAM dealers in your area, you’ll see!!! This has been going on all year.

I see inflation continuing higher as the Banks and Brokers attempt to dump US long bonds on the unsuspecting public. The US Gov Debt to GDP is at 129%. Lower Inflation is a Fake Out. This administration pumped out the SPR and refined the crude into petrol products and stored probably 90 days of product supply in storage tanks? But, now they must allocate funds to buy crude to refill SPR or stop filling the SPR? If I distill the Crude place in long term storage gasoline and Heating Oil did I actually change anything? Basically, they flooded the storage tanks with products to lower Crude Prices?

Food inflation is directly the result of Climate and currently climate change is causing shortages of food all over the world. The same population is chasing less available food? Food prices will go higher. Food and Energy are not part of core inflation. But, Higher food and energy slowly filter down to higher prices for everything else.

The problem with Walmart is their customer is a discount buyer and there are better deals out there in categories where Walmart wants to expand.

I never shop in Walmart, but I saw a big push in the summer of online influencers pushing Walmart fashions. What I saw wasn’t impressive. At the price points they offer I can get better stuff at other big box discounters. There is no reason for me to go to Walmart.

I am in Walmart quite a bit. I totally can see what the CEO is saying. Chicken thighs (and other chicken part too I would guess but I use a lot of thigh meat in my cooking so I notice those prices more) are three times what they were before COVID… not sure when they will start coming down.

Meanwhile tonight I bought some shipping straps (and ratchets) that were marked down by about 20% over what I normally pay at Walmart for them… from $16 and change to $13 and change.

This even in the USA, UK etc. used to be pretty common in some other weaker countries: the government would contrive a few years of high inflation to make wages more “competitive” in real terms. One it one of three ways of achieving that:

#1 “external devaluation”: a fall in the exchange rate and real wages become become “more competitive” in “strong currencies”.

#2 “internal deflation”: a recession with much unemployment results in wage cuts, especially for those hired from unemployment, who are desperate to get a job, and wages become “more competitive” in the local currency.

#3 “internal devaluation”: most prices, except wages, increase, and wages become “more competitive” in terms of purchasing power of the local currency.

There is one vital detail: in some countries inflation is zero or negative, for example Russia and China. Now the USA, UK etc. import a large percentage of goods from China, and buy raw materials and agricultural products from the same global markets from which China imports them. How is that consistent with negative or zero inflation in China and high inflation in the USA or UK?

“…in some countries inflation is zero or negative, for example Russia and China.”

Yes for China.

LOL for Russia. Russia’s inflation is now surging, the yoy inflation rate has doubled from June, to 5.5% in Oct. Just going straight up now.

Inflation is still rising on most everything.. Don’t believe the print. I live it and see it.

Wrongo. Check used cars, prices are falling; check new cars, HUGE incentives on many of them now. Check electronics, many hard goods, shoes, etc. Prices are falling…

Read the article: prices are falling in durable goods and gasoline. Not Food. And not in services.

Broadband is also down. We just upgraded service with the same company from 75 mbs to 200 mbs and the price also went down by $5/mth.

My wife and I are empty nesters and one of our two cars was totalled during Covid lockdown. We realized we didn’t need 2 cars and never bought a 2nd one. Maybe we will if the prices come down enough.