“If the markets don’t infer from this that it’ll be high for longer, we’ll have to use our rate instruments and hike to get where we want to go.”

By Wolf Richter for WOLF STREET.

Rate-cut bets have been piling up and getting moved closer, as everything that central bankers say – no matter what – is either being interpreted as “dovish” or is being brushed aside. The “Powell-was-dovish” mantra has been getting spread across the internet after every FOMC press conference since June 2022. In early 2022, just as the Fed had started hiking, rate cuts for later in 2022 were already being bet on. Then came the bets for rate cuts in 2023, and now there’s only one meeting left, and still no rate cuts. So the heavy breathing about rate cuts has shifted to 2024, and the cuts are getting bigger and closer.

Meanwhile, central bankers at the Federal Reserve, at the Bank of Canada, at the ECB, at the Bank of England, at the Reserve Bank of Australia, etc. have been flagellating their arms to tamp down on these rate-cut bets.

The Reserve Bank of Australia finally has had it and hiked by 25 basis points in November after a long pause.

There is a problem with markets betting against central banks. Central banks are “tightening” in order to tighten financial conditions in the markets – including higher long-term yields and wider spreads between government debt and risky debt, such as junk bonds, etc.

These tighter financial conditions make it more expensive and harder for companies and consumers to borrow which is then supposed to slow economic growth and take some of the froth off, thereby hopefully putting the kibosh on inflation. But it doesn’t work when financial conditions are loosening, with long-term interest rates falling and spreads narrowing, because markets are betting against central banks.

So ECB Governing Council member Pierre Wunsch came out and made it explicit – not that anyone in the markets listened: These rate-cut bets could actually trigger the opposite: a rate hike.

“Is it a problem if everybody believes we’re going to cut?” Wunsch said in an interview with Bloomberg. “Then we have a less restrictive monetary policy. And I’m not sure that then it’s going to be restrictive enough. So it increases the risk that you have to correct in the other direction.”

“I think markets are relatively optimistic today that they exclude the possibility that we have to do more or that we have to remain at 4% for longer,” said Wunsch.

“If we arrive at the conclusion that inflation is not going down fast enough, we’ll communicate it through our projection and through our communication,” he said.

“If the markets don’t infer from this that it’ll be high for longer, then we’ll have to use our rate instruments and hike to get where we want to go.”

Which is what the Reserve Bank of Australia did earlier in November when it hiked by 25 basis points.

Wunsch doesn’t see any rate hikes at the next two ECB policy meetings thanks to “recent marginal positive surprises on inflation.”

“That moves the question to the next uncertainty: Are we going to see some inflation resistance at some point at 3% or something like that because of wages?” he said. “That is something we’re not going to know by December or January.”

It’s almost funny how markets have been betting against central banks ever since they started tightening. But recently, those bets have turned into a raging party, and as a result financial conditions have loosened a lot, instead of tightening.

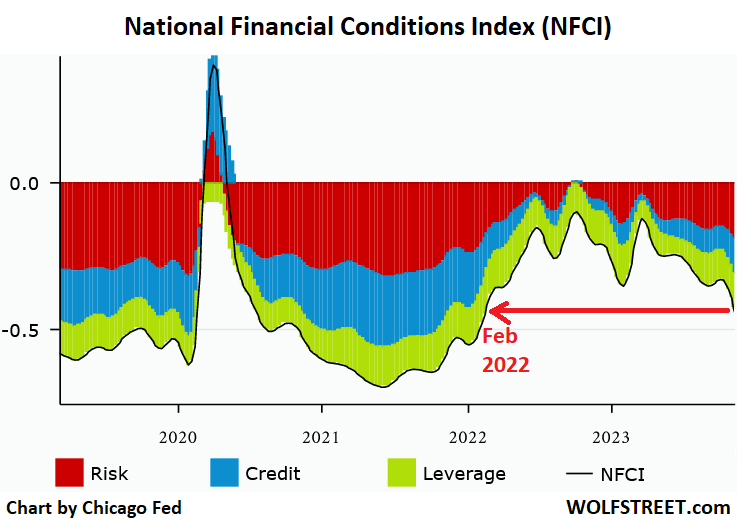

In the US, there are various measures that track financial conditions. For example, the Chicago Fed’s weekly National Financial Conditions Index (NFCI) is based on 105 measures of financial activity to track conditions in money markets, debt markets, equity markets, the banking system, and the “shadow” banking system (what goes into it is explained here). For the week ending November 17, the index showed further loosening, with the index value falling to -0.47, the lowest since February 2022, before the Fed even started hiking.

The Fed, the ECB, the BOC, the RBA, and the BOE have been facing the same issue: markets are not cooperating – markets are fighting them, financial conditions have gotten looser and thereby provide additional fuel for inflation, and the longer markets are doing this, the more they’re risking that rates will end up even higher for longer. The Chicago Fed’s NFCI:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The old ” the Fed decides when to hike rates and the bond market decides when to lower them” might be a little like the recession prediction models that have predicted 10 of the last 3 recessions

Time heals all wounds. Your dollars keep losing value permanently, it’s not reversible.

You will eventually get used to high inflation and I will keep talking about my intention to reduce inflation.

Precisely. Well said JP

1stTDinvestor,

I second your motion.

“If the markets don’t infer from this that it’ll be high for longer, we’ll have to use our rate instruments and hike to get where we want to go.”

Not if the “hikes” continue in the 1/4 to 1/2 percent range. They need to be hiking ONE to TWO percentage points at a time.

I said something similar many months ago.

I wrote the above comment even before I read the article. And then I read Wolf’s post and what did I see? Comments about 1/4 point…er excuse me…. 25 basis point hikes all over the place.

How did the financial system survive relatively rapid rate hikes all the way up to the 18 percent Money Market rates between 1979 and 1981 or 1982? I lived through that time as a Stockbroker.

And time wounds all heels.

Been waiting for the Q3 credit card loan delinquencies report from Fed St Louis. Updated November 20th. 2.98% in Q3. Up from 2.77% in Q2.

Also reading articles indicating that early withdrawals from and outstanding loan balances borrowed from 401k retirement accounts are on the rise. Also, unemployment creeping up slowly.

Is this an indicator, that the long awaited recession is finally coming soon? I guess only time will tell.

Both are only up compared to all-time record lows. Congrats on writing so much, saying so little, and then not making a strong stand on your point.

So “How did the financial system survive relatively rapid rate hikes all the way up to the 18 percent Money Market rates between 1979 and 1981 or 1982?” — If memory serves, in the late 1970’s the Fed lowered rates prematurely only to find inflation soaring again. Paul Volcker’s response was to raise interest rates above the inflation rate, and to leave rates higher for longer. It worked, although Volcker was hated and he received death threats as the rolling recession was severe. The Fed doesn’t want to repeat that easing mistake again. They’ve got to keep rates higher longer in order to kill inflation. Otherwise it’s going to flare up again, and it will be a decade long battle. Unfortunately the national debt is sky-high and rising, so interest costs are devouring the federal budget.

We’ll be at 6.5% within a year and 8% by 2027. The amount of guff I took here for saying several years ago that rates were not coming down. This is a mere retracement. Rates are going higher.

… and fr everyone discussing the Fed, you might recall that the Fed only controls the short end…the long end 10 year+ is set by the market. Rates are going higher and a liquidity crisis is right around the corner. Blackrock has stopped redemption from a REIT… anyone care to recall BNP Paribas’ failure/inability to asses fund values in 2007 which led to them shutting in money. It’s back. But this time its going to be bigger, ‘better’ and stronger.

With an extra $1.5-2T in annual Uncle Same deficit spending, there’s not going to be a recession. Clearly, the Fed has been in all hands-on deck, full backstop mode for any & all possibilities.

The only question now is how much further core inflation will fall before a “possible” rise next spring? My bet is 3.7-3.9%. With 4% core inflation in October, we’re still 2X the Fed’s target, yet CME Group says there’s a 91.2% chance rates hold steady. That’s optimism for ya!

But how much can we afford to pay on the debt? 6%? Or how much will the world demand to buy all of the debt later? 8%?

Perhaps the real reason the FED has no room to drop rates is for fear all the U.S. can’t be sold. Especially stacking on 2T yearly. It’s all a runaway train.

“Perhaps the real reason the FED has no room to drop rates is for fear all the U.S. can’t be sold.”

Bingo! We have a winner!!

And it IS a runaway train. (got dissed for saying that too…months ago.)

Fin de Siecle

If the Fed wanted to tame inflation, it could easily do so.

It also doesn’t want to crash the economy and blow up the financial system to where you cannot turn on the light in the morning, though it could easily do so.

Tightening is a compromise: getting inflation under control without blowing everything up.

The Fed has hiked to 5.5% from 0.25% and has shed $1.1 trillion from its balance sheet, which is a good start. This stuff takes time, unless you want to blow up everything, which you and some others here apparently want.

Inflation has already come down a lot, though it remains high because it’s alive and well in services, but it’s very hard to stamp out in services.

People have been posting this idiocy that the Fed does not want to “tame” inflation. It’s just pure BS in light of what it has already done so far. My patience for this BS has been used up and has reached the zero level.

I don’t think people mean that the Fed does not want to tame inflation, in a vacuum. I think nearly everyone thinks that the Fed would, if it could snap its fingers and cause something to happen without causing anything else to happen, reduce inflation to its target.

What I think people mean is that the Fed is not serious about taming inflation if a consequence means a drop in asset prices.

“What I think people mean is that the Fed is not serious about taming inflation if a consequence means a drop in asset prices.”

This is precisely the bullshit I no longer have any patience with.

Alternative possibilities…

1) Market players are pitching/paying for dovish rate bets in order to lure in more/bigger bagholders to ultimately dump their remaining adverse positions onto, and/or

2) They look at DC’s behaviour of the last 50+ years and the soaring Treasury interest payouts (thanks to 50+ years of cancerous national debt accumulation) and reasonably assume that DC will be utterly compelled to cut rates (or otherwise destroy the Federal budget for good…as opposed to dumping the consequences on the public via inflation.)

I know you have laid out why higher rates won’t necessarily destroy the Fed budget (more or less for good this time) but I don’t know if your understanding/point of view is shared by enough in NYC.

Wolf, the S&P is only about 5% below all time highs. You might believe (as I do) that the market is deluding itself regarding a Fed pivot, but the fact is, the Fed hasn’t been tested yet, because no one has seen their stock or housing prices drop by 30-40%.

We’ve basically traded sideways for two years. There are a lot of people who think that the Fed has been able to continue its rate hikes, higher for longer and QT precisely BECAUSE the asset markets are still very high, and that if they weren’t, the Fed would be pivoting in a heartbeat, inflation fighting be damned.

I get it that you disagree. But it’s not a completely unreasonable belief, based on the past 15 years.

A drop or a stabilisation in asset prices or disinflation is the goal as long as it is not catastrophic, the ‘soft landing’

all are hoping for

@Einhal

The S&P 500 dropped to 3,500 last year and there was no pivot. There was no doubt a Federal Reserve Put existed for some 30 years, but inflation had never really been a problem. And recent well-publicized controversies about FOMC officials trading their personal portfolios have made them more mindful of the optics.

“What I think people mean is that the Fed is not serious about taming inflation if a consequence means a drop in asset prices.”

Except this is precisely wrong.

Asset prices have been (very) gradually falling.

It is services that have been driving inflation.

You would be more correct to say that thr FED is not serious about taming inflation because they are not willing to tank the labor market. It is a misrepresentation, but more accurate than what you are saying.

The medicine for inflation is bitter, so US society is unwilling to take it at first. So they wait until inflation becomes intolerable. And by intolerable, I mean that politicians are voted out en masse. Volcker got his mandate by the 1980 election it seems to me (see the Senate re-election rate): https://www.opensecrets.org/elections-overview/reelection-rates

Everything is politically driven. Theoretically, the central bank itself could be abolished by Congress, for example.

What makes the Fed’s job harder is the addition of QE to its toolkit and the existence of the Greenspan Put (i.e. the willingness to aggressively cut interest rates in an economic slowdown), and a stated increased tolerance of inflation. Also, the existence of Bubblenomics – google “Larry Summers bubble” and ditto for Paul Krugman. All of these things make society’s financial elites wealthier, ditto for politicians and asset holders in general. There has been no negative consequence to politicians per the Open Secrets link, although I do think Obama and Trump were protest candidates who won due to economic hardship by the voters.

Retail knows about QE and interest rates strategy. Wall Street knows that retail knows and likes to goad them on. Inflation expectations regarding stocks and real estate have become “entrenched”. There’s still a lot of injected money sloshing around out there (e.g. the Fed has a huge balance sheet still which requires replenishment when debt matures, leading to more liquidity in the economy).

So these factors need to be considered to see where interest rate policy is going.

There’s a middle ground between approving of the Fed’s timidity and wanting everything to burn down, blow up, etc. Reasonable people can hold the opinion that the Fed could and should be more aggressive than they have been, and that they could do this without causing massive explosions, fires, or other cinematic special effects in the broader economy.

This is not to say that I agree with Bobber that the Fed doesn’t want to tame inflation. I believe that they genuinely want to, but are only meeting limited success because of a combination of 1) relying on flawed models and 2) an institutional bias toward excessive caution when tightening (but little or no caution, of course, when loosening).

I never said the Fed should “blow everything up”, whatever that means. The Fed can tame inflation very easily by accelerating QT and keeping interest rates above inflation. It may cause asset price reductions, but that wouldn’t cause long-term high unemployment. It might cause a recession, but so what. That is normal.

The Fed is obviously trying to fight inflation without tipping the economy into a recession, but that is not an inflation fight. That’s a timid bow to Wall Street and asset prices.

What is so controversial about this?

Bobber, I agree. They refuse to give up the fantasy of a soft landing, so they’re acting too slowly.

I however don’t believe rates are the problem. I think it’s the giant balance sheet.

While it remains to be seen whether inflation will successfully return to target (2%), it’s really not accurate to say only “limited progress” has been made.

Inflation peaked at 9% CPI & 7% PCE (annualized) last year, and since then, both metrics have declined to 3.5%. That’s a lot of progress in such a short time. It’s the reason FOMC members have been so remarkably united so far, and mainstream politicians have gotten out of the way.

Have we all forgotten that when inflation started to rise (as we all knew it would when government pumped money into the economy), the federal reserve called the inflation transient? And then initially slow walked the rate hikes?

If we look at the rate hikes only, then yes, the fed is trying to stop inflation. But only AFTER pretending it wasn’t real even though we all knew it was real. AFTER contorting itself, pretzels of truth to pretend they had reason to delay raising rates has damaged their authority and societal trust in them. Which is contributing to the sentiment the Fed don’t want to stop inflation….

IMO, the Fed do want to stop inflation, reluctantly. They are trying to achieve a soft landing, which most of us believe is impossible. If they wanted to avoid questions regarding their intentions, they should have started the rate hikes early before this inflation became entrenched.

Has everyone forgot the role of government spending?

I agree with you. When the COVID hit, FED along with all other major CBs pushed out enormous stimulation in a hurry. They did not use reasoning when determining the amount of liquidity to push out and the rate to drop, e.g. Surely the situation needs some relaxation in monetary policy, but does it necessarily to be such a huge amount and drop to 0% rate? Some central bank heads apologized later for this (e.g. Aussie and Canada and maybe British, but not FED).

Even worse, after the inflation situation manifested in early 2021 (Wolf and all people here knows that), FED denied it and called transitory BS for another year, unwilling to tightening. It is not unreasonable to infer that FED has a loosening bias, and recent market mania has a lot to do with this.

The Treasury giveth and the Fed taketh away.

Lest we forget!

Classic Economic Theory says deficit spending creates inflation.

Of course; “we don’t need no stinkin’ Classic Economic Theory” because everyone knows – this time is different.

I know that this comment will not generate any “at a boys” from the host, but I have to say it.

The only way to tame inflation is to do essentially what Paul Volcker did. He was the greatest Fed chief in the history of the country. He saved the country. We need someone in there like him who has the guts to do what is right. With Federal spending completely out of control, with NO END IN SIGHT, the Fed is the only game in town. I would say to them if I could, DO YOUR JOB!

These tiresome Volcker hagiographies reveal a simplistic understanding both of monetary policy effects and a lack of appreciation for how other policy changes played a significant role in inflation reduction during the early ‘80s — not to mention zero acknowledgement of structural changes in the world economy over the past 40 years which make direct comparisons moot.

“The only way to tame inflation is to do essentially what Paul Volcker did.”

Agree. Taking rates back to “historical norms” just isnt enough, IMO. But this is a different type of Fed since Bernanke, Yellen and Powell. They seem to all serve a different “master”.

If one assumes 2% is the correct rate of inflation (illegitimate IMO) then prices should only be 6% higher in the past 3 years.

Take whatever metric you like for price hikes the past 3 years and deduct 6%. What remains is the “overshoot” and logic would suggest that should be “rung out” of the system. Not likely. Would love to hear Powell address this.

longstreet,

Volcker didn’t “wring out the overshoot” either. That’s just silly nonsense. The inflation rate (CPI, yoy) came down but remained high for years. And no, prices didn’t drop to make up for prior increases under Volcker, they kept rising but just rose more slowly. Same as now.

When Volcker left office in Aug 1987, CPI was 4.2%, HIGHER THAN NOW. You people need to get your head on straight about inflation under Volcker.

eg,

It’s hard to sympathize with Fed policies that irresponsibly increased asset prices 200% to 300% in a decade, created a permanent 20% inflationary step up during the 2020-2023 period, is adding 3%+ inflation under a “higher for longer” regime, while ultimately “hoping” for additional 2% inflation every year after that. The results and actions speak for themselves. Ask anybody who lost 50% on government bonds in a couple years.

It’s even harder to sympathize with a Fed that throws its stated goals out the window under challenging conditions. The promise was 2% average inflation, but we’re obviously headed for 25% to 35% inflation for the 2020’s decade. Why does the Fed continue to tout an average 2% inflation goal if it has zero intention of reversing recent inflation overruns to meet the average inflation target?

The Fed has an opportunity right now to throw the economy into a recession, thereby creating some needed deflation to meet its 2% average inflation target this decade. It can NEVER fulfill that promise by seeking to tack on additional inflation.

Deflation has become intolerable to this Fed; hence, so have normal recessions.

If the real Fed policy is to allow non-reversing inflation overruns whenever “emergency” stimulus is needed, perhaps they should admit this, increase the 2% target accordingly, and define what an emergency is. At least the flaws in current monetary policy would be transparent, and people won’t be set up to lose another 50% on government bonds.

Mkts are NOT acting as if Fed is going to tighten, if one follow the mkt action these days. S&P even came out of ‘correction’ zone. The FAANGS Keep inching up after a initial blow off. Santa rally (real or NOT) is approaching.

Does Fed dare to rise before X-mas or even in a election year? These are the perplexing questions, the investor is facing. Contrary to my inner self, I followed the momentum approach but reduce exposure by trimming and profit taking. Yes Mkt remains overvalued but investors are in a FOMO mood. To each his own

“Mkts are NOT acting as if Fed is going to tighten, if one follow the mkt action these days.”

LOL. RTGDFA. Markets fighting the Fed is exactly the problem as spelled out in the article!!!

How are you going to get inflation to go down if the markets refuse to tighten financial conditions, and instead loosen the financial conditions? That’s the topic of the article.

Markets are not only NOT pricing in further tightening, there’s a widespread expectation the low-rate environment of 2008-2021 will return in the near future.

Some of the valuations are nonsensical relative to current rates.

The traditional measure of overall market value is not reflected in today’s market: the top 7 companies are richly valued (because of their rapid growth, monopolistic character, and extraordinary balance sheets) and skew the market’s P/E. This is not necessarily wrong. It’s the weighting of the entire S & P 500 that makes the CAPE so excessive.

Traditional valuations apply to industries that are more staid than the high-growth FAANGS. Using the same valuation measurements to value Google, Chevron, Nucor, etc. gives distorted outcomes.

Even the magnificent 7 have a limit to growth, especially as they rely on the greater economy to prop them up.

Thanks Wolf I’m fed up too with over tightening wishes. Blowing things up financially even though we still broke the inflation barrier does not mean we over react.

Just because inflation is back in the 3’s does not erase the spikes that are “baked in”. Do we just leave those “spikes” in and keep tacking on 3% and call it a victory?

longstreet,

That’s just silly nonsense. Even under Volcker, the inflation rate (CPI, yoy) came down but remained high for years. And no, prices didn’t drop and CPI turn negative to make up for prior increases under Volcker, they kept rising but just rose more slowly. Same as now.

When Volcker left office in Aug 1987, CPI was 4.2%, HIGHER THAN NOW.

Wolf, the CPI calculation was different in the 80s than today. 4.2% back then is more like 2% today due to hedonics and substitution and especially the move to OER.

DM,

EVERYTHING was different in the 1980s. Life was different. The goods and services we consumed were different. The basket of goods and services changed too. Cars in the 80s were a POS. We just drove home with our adaptive cruise control and automatic high beams in a big car that gets 50 mpg when I drive it (less when my wife drives it), and it comes with equipment that you couldn’t even dream of back in the 1980s. And there were no laptops, and today’s $800-laptops would have been super computers back then, and there were no smartphones, and there was no internet as we know it today, and no broadband, and no streaming, and HD TV, and no flat-panel TVs even, and you had to go to a travel agency to buy your plane tickets, and the news media that is free online today, including this site, weren’t available back then, and you had to pay for all the papers you wanted to read, and all those things are now in the CPI basket.

People who say, “4.2% back then is more like 2% today due to hedonics and substitution” don’t know what they’re talking about; including there isn’t even any substitution in CPI.

And people who say “especially the move to OER” are just circulating clueless BS. The CPI for OER = 6.8% in October So what’s your problem!

In addition, there is the CPI for Rent of primary residence, which is the best rental measure we have, and it was 7.2% in Oct.

CPI isn’t perfect, nothing is perfect, but it’s better today than it was back then. There is a lot of braindead BS being circulated about CPI. And I’m tired of it, and I normally just delete. People can dump this crap somewhere else.

The Federal Reserve, Jerome Powell wants people to believe they are seriously combating inflation; various officials and notably Jerome Powell give speeches and news conferences with that talking point.

It would seem that a way to make the Federal Reserve take more aggressive action would be to indicate a disbelief of the Federal Reserve inflation fighting narrative by such actions as the consumer expectation of inflation survey staying at high levels; that would require a general societal disbelief at the grass roots level.

Nice job censoring opinions you don’t like, Mish!

You’ll never change.

What you posted was uninformed BS, it was just wrong and nonsense, and you spread it like facts. I no longer have the time to straighten this stuff out line item by line item, and then you come back with more BS to argue about it, and I have to waste more time on it. Part of the problem is that you never read the articles, and are clueless, and just come here to dump your stuff into the comments. There is a whole internet out there where you can do that, but not here.

TomS – hey, YOU can always create (…wait for it…) A BLOG!!!.

…or, in the words of the immortal ‘Scoop’ Nisker: “…if you don’t like the news, go out and make some of your own…”.

may we all find a better day.

I absolutely agree with you, Wolf. I see the same idiocy around the internet (especially Reddit) where people are lamenting that the Fed and other central banks aren’t hiking fast enough.

This is like a symphony. The music doesn’t stop at the peak of the 3rd movement, but needs a whole 4th movement to come to the stop.

People simply don’t understand that if something goes up for years and years, it also takes years to come back down.

What is long forgotten is that Volcker was absolutely hated: he was attacked by all quarters for his hiking of rates and bringing on a massive recession. All industries were being hammered, especially construction.

Today the commenters are talking about him as though he was a savior who waved his magic wand and brought down inflation, as though it was widely believed to be necessary.

He tried his damnedest to remain calm when Congress was slamming him during and after testimony.

How – well observed. We now seem to rush to pronounce history’s judgement before the clock can tick even a minute further into the future (…to obviate the heavy labor of honestly analyzing of the past?).

may we all find a better day.

Volcker deserved to be hated by working people. He reputedly kept a note in his wallet reminding himself to crush labor.

This article is again pure wisdom dispensed daily. Elegant assemblage of facts clears the view into the crystal ball.

Always love your fuming replies Wolf, Stay sharp, stay angry. Dont become a pussy like the rest of em.

Last 2 months across all central banks there have been more rate cuts than hikes. It does seem that (globally at least) the tide has turned.

Since what central bank leaders say affect prices – there is a case to be made that they’re talking tough to hedge against overreaction from a hold or drop. Especially in the ECB’s case given their recent history pre-covid.

“Last 2 months across all central banks there have been more rate cuts than hikes.”

This is typical CNBC context-less headline BS.

For example, the central bank of Brazil has cut three times, but it cut from 13.75%, to 12.25% now.

This 12.25% is way restrictive still!! Inflation in Brazil is now 4.8%!!! It has come down from 12%.

Brazil started hiking a year before the Fed, and it hiked in huge mega leaps of 2 percentage points at a time, and got way high to (successfully) protect its currency ahead of Fed rate hikes.

Mexico’s inflation is now down to 4.3%, from about 8.5%. It hasn’t cut yet, and the rate is still at 11.25%!!! So it will cut eventually.

Unlike the euro and the yen, Brazil’s and Mexico’s currencies did well against the USD due to the huge and early rate hikes. And both of their rates are still in the double digits with inflation not much worse than in the US.

So when you talk about rate cuts in the headline, you need to say where from and to where and in which country!!! Obviously the morons or algos that write those articles don’t have a clue. So careful dragging this context-less BS into here.

I’ve been saying this for two years now. The fed has been very clear and up front about its intentions.

In November 2021 they told the world all about their impending rate increases and continued to tell everyone for the next two years, even the size of those increases

They’ve done EXACTLY what they said they were going to do. All the while, markets and individuals claim they’re lying and going to do the opposite. They didn’t.

The fed now says it’s going to continue restrictive policy until inflation is certain to stay below 2%. This will likely take years unless we have a bad recession.

Nonetheless, everyone is already predicting rate cuts in the spring. That’s just plain ignorant and a sure fure way to lose a lot of money.

“They’ve done EXACTLY…” In spite of your faith in the FED’s integrity, they have a long term credibility problem.

Take a look back at the Fed’s predictions about future rates and you will quickly see that what they are telling you now about future rates is completely meaningless.

“Unlike the euro and the yen, Brazil’s and Mexico’s currencies did well against the USD due to the huge and early rate hikes”

Do you think Federal Reserve had made a mistake of choosing a path of modest and gradual rate hikes ? Or is too early to tell ?

“modest and gradual rate hikes”

Are you nuts? What kind of manipulative BS is this??? Those were the fastest rate hikes in 40 years. And QT is running at a record pace.

The US isn’t an emerging economy, like Brazil and Mexico.

I looked at the graph of financial conditions that you included in your article, and I noticed that financial conditions tightened dramatically in the period of time when Federal Reserve was doing larger rate hikes, and then loosened again when Federal Reserve switched to 25 bps hikes.

The US sure looking like EM now, first high inflation, now insane fiscal spending. The only path forward is more currency devaluation. They just trying to make it soft, so you don’t notice your standard of living collapsing.

If FED wants to send a message to markets, I bet the 0.25 hikes will not work. It should be a single hike at 2% or more and with a stern message that more could be coming. Even if they remain optimistic, they know the FED will not do a 2% reverse swing in the next FOMC.

But then as you said, they are all worried about the blowback to the Ponzi financial system.

“…should be a single hike at 2% or more”

🤣 That’s just nuts. Inflation isn’t 15%. It’s in the 3%-5% range, below policy rates.

Yes. Why gradually press the brakes when instead you can hit a brick wall and stop so much quicker.

If course it might matter to the occupants of the vehicle……..

Would you say I am correct in my assessment that India at around 6% and massive double deficits is nowhere near safe from a run on capital. Might put options on certain emerging markets be a reasonable investment given low implied volatility.

India’s trade deficits have been sustained entirely by inflows.

Not really a surprise the markets can outplay the Fed. Pretty safe bet that the US will just decide increasing deficits are okay. If you are running a massive deficit during good times then imagine a downturn. Reality it seems as this game could be played out for decades will the occasional recession, printing of money, then rate hikes all while not addressing fundamentals. Next stop S&P to 5000 and beyond and Treasury yields at 4%. Markets struggle, no problem, increase the deficit and help them out! Just glad we have a functioning democracy of capable leaders who will sort this all out and take care of the people.

It would be interesting to see what the policy would be if we have a recession and no meaningful let down in commodity inflation and services inflation (which as Wolf points out is unlikely to be stamped soon or easily)

What policy would help us out of the woods then is anybody’s guess. That is the problem with debt fueled consumption….the end is ugly and solutions uglier (Perhaps a Japanese can add more color here)

Japans debt is 263% of GDP so we have a way to go to that. Seems like an apples to oranges comparison but not intelligent as to understand implications.

I wouldn’t pick Japan as a positive example, their stock market is still not back to 1989.

Powell has said in the event of stagflation, the committee will have to make hard decisions but it’ll be based on which of unemployment or inflation is further away from target

Honestly this FMOC has shown more spine than has come to be expected of Central Bankers of late. I think they should get credit for that even if it a correction to their fantasy policy for nearly 15 years.

I guess the market doesn’t seem to get that this new economy is all about the supply side. Therefore loose monetary policies will not work anymore. This is a very different economy than that after the dot-com bubble (drop in aggregate demand plus China based disinflation) and housing bubble (outright deflation from asset bubble popping)

The new economy has lots of demand and insufficient supply. Likely that China will also focus on domestic consumption to fix its economy…adding more fuel to inflation over the medium to long term.

“China will also focus on domestic consumption to fix its economy”

How is it doing? Chinese are saving now more seeing that their investments in RE is going south every month. Where is domestic consumption come from?

Probably the billion people not spending 50% of their income on housing.

The chance to teach the market players “not to fight the FED” was missed in March 2023, when FED instantly printed $400B with the early signs of panic. Now markets learned that FED is weak. Whatever stupid thing they do, they believe that the FED will be there to rescue. FED is like a father who repeatedly tells his son to be careful, but every time the son goes to jail, he pays the bail.

If your policy is to not allow anyone to fail, corporations will take all kinds of stupid risks and loosen the financial conditions, as they assume you are always ready to rescue with your finger on the money printer button.

This is such dumb manipulative bullshit. I cannot believe I have to keep reading it.

In March:

1. The banks FAILED and investors lost all their money.

2. The Fed helped bail out depositors to avert a broader bank panic due to the Fed’s high interest rates that had caused the unrealized losses that triggered the run on the bank.

3. Throughout, the Fed HIKED and continued with QT.

4. It was a short-term end-the-panic moment. And it was gone after two months.

I think his point is that it’s more psychological. It doesn’t matter what actually happened with the bank panic programs, it’s the message that was sent, that they won’t allow anything to happen in a disorderly manner.

But any recession, by definition, will cause some disorder. So the market inferred that they won’t really allow any strong pain with cascading consequences, and acted accordingly.

“So the market inferred that they won’t really allow any strong pain…”

The market may have inferred that, but it’s bullshit. There has been all kinds of pain already since late 2021 (outside of 10 giant stocks), and the Fed has kept at it, hiking o 5.5% and QT. All kinds of investments have already crashed, from CRE to crypto, and bond holders have taken huge losses, and most stocks are way down from their peaks, to where Wall Street is trying to force the Fed to end QT. But the Fed has just marched forward.

Yep, the bank bail-out was a classic case of moral hazard. “In economics, a moral hazard is a situation where an economic actor has an incentive to increase its exposure to risk because it does not bear the full costs of that risk. ” With the recent bank crisis, should the FDIC have guaranteed deposits only up to $250,000, instead of bailing out all depositors by letting Chase take over the failed banks (on pretty good terms and increasing concentration in the bank industry)? I say yes. All depositors with over $250,000 should have lost everything over $250,000. Because now every large depositor (>$250,000) knows he will be bailed out, so he can dump a ton of money into a bank in return for cushy incentives (easier loans, lower cost loans, whatever deals they make) and he no longer needs to care if the bank is engaged in highly risky activity or not. He will be backstopped by government action (tax-payers). The maximum $250,000 “insurance” per account no longer applies.

The question is, if my scenario played out, would that have caused a crescendo of bank runs. I doubt it. All depositors under $250,000 would have been fine, which is probably 99.9% of all bank depositors (I don’t have the actual number). Anyone with over $250,000 would be looking long and hard at a bank’s Statement of Condition, which they should do anyway.

Even the $250,000 guarantee is moral hazard. It is a classic economic inefficiency, ultimately paid for by the government (tax-payers). I recall the first thing the government did when the Reserve Primary Fund broke the buck in 2008 was raise that limit from $100,000 to $250,000. The regulators were scared. It is a serious problem, and we have been skating by, barely.

“outside of 10 giant stocks”

Ay…but that may be the rub.

The “magnificent 7” (sounds a lot more macho than the equally doomed “Nifty Fifty” of 1970-72) have managed to keep the equity indices from taking the sort of fast, really dramatic hit that scares the crap out of equity owners and gets them to stop YOLO consumer spending.

The Fed can’t really undo its 2000-2022 phoney-baloney, ZIRP driven “wealth effect’ (“Spend, spend, spend!! My fools for the Fed!”) without, you know, actually taking a pretty big axe to the phoney-baloney “wealth” (actually nothing more than an artifact of how DCFs are naively calculated and Fed manipulation of the money supply).

The equity indices have fallen, but punters have (repeatedly) retreated to the Mag 7…truly globe-straddling companies sporting the PEs (30+) of small startups with true room to grow.

(In other words…Apple/Microsoft ain’t gonna be doubling sales to $600 billion unless another planet is discovered…but the punters want to keep equity exposure…and the Mag 7 are the marginally least absurd way to do so…).

If the market was overvalued 40% (pre-pandemic!) then an equity hit of 20% just ain’t enough.

(And that is ignoring the profoundly stupid pandemic spike…which maybe took overvaluation to 60% at its worst).

“and most stocks are way down from their peaks”

??

YTD

DIA —– +7.76%

SPY —— +19.85%

qqq —— 46.53%

All recovered and recaptured the loss this year from their peak

Those waiting for the BEAR lost or clobbered if they bet against BULL.

Financial conditions are still relatively loose!

sunny129,

Nasdaq composite: -12% from Nov 2021, TWO YEARS AGO exactly.

S&P 500: -5% from Jan 3, 2022, nearly two years ago.

Bitcoin: -45% from Nov 2021.

No one knows what CRE is worth anymore, but values of the few transactions that there were have plunged. The sector is now in total upheaval.

Sure, Nvidia is up a bunch, MSFT just passed it Nov 2021 high, Apple reached a new high in July but is now off that, etc. And those huge stocks cover up the pain in the stock market. Thousands of smaller stocks have gotten totally crushed (-70% to -100%)

Yes, but then the Fed needs to work harder to convince people that it will not pivot. Powell should come straight out and say “Those models projecting a rate cut in March? They’re not happening, so stop the BS.”

But he doesn’t. Why?

Einhal,

He said precisely that at the press conference, except he was a lot firmer with a longer horizon. And everyone said, Powell was dovish.

People REFUSE to listen to what he actually said and come up with fantasy stuff about what they want him to have said.

https://wolfstreet.com/2023/11/01/well-probably-still-be-left-with-ground-to-cover-to-get-back-to-full-price-stability-powell-at-the-fomc-press-conference/

“The Committee is not thinking about rate cuts right now at all. We are not talking about rate cuts,” Powell said.

“The question of rate cuts doesn’t come up, because it’s so important to get that first question as close to right as you can,” Powell said.

“We are still very focused on the first question, which is, have we achieved a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2% over time sustainably? That is the question we are focusing on,” he said.

“The next question will be for how long will we remain restrictive? We said we will keep policy restrictive until we are confident that inflation is on a sustainable path down to 2%. That will be the next question. But honestly right now, we are tightly focused on the first question.”

Correction:

Re-captured most of the loss from their peak

The ‘market’ now is more algos than people. Both were trained on the recency bias of ZIRP. Can you blame them?

The question is why did the Fed ‘rescue’ the hyper financialized bubble system in 08, and 12, and 18, etc? It’s because all of the last 40 years’ growth was monetary. The US consumption has exceeded production and the deficit has been monetized at the expense of the divided foreigners. There’s no peaceful end to this Empire of debt.

Thank you, Wolf for responding with data to purely emotional comments from poorly informed commenters. Many still do not understand the difference between shareholders, bondholders and depositors of the failed banks.

SPDR S&P Bank ETF (KBE) is down 11%

where as SPDR S&P Capital Markets ETF (KCE) is up 14%

Find out the holdings at Yahoo/Finance

Banks are getting 5.4% for their deposits at the Fed.

T Bill Mfunds like VUSXX (Vsnguard) get 5.2%

Who is complaining!?

Main point is the indexes recovered ‘most of their losses’ from the previous 2 years, this year b/c the financial conditions are relatively still loose.

” Looser Financial Conditions Pose Conundrum for Central Banks

Despite sharp monetary policy tightening, financial conditions have eased around much of the globe, posing a challenge for central banks

Tobias Adrian, Christopher Erceg, Fabio Natalucci

IMF Blog

Many of them also do not even bother to RTGDFA. Wolf does a good job of playing whack-a-mole with these obnoxious punters, but he shouldn’t have to if people would just bother to pay attention and stop spreading BS.

The “impulse” spike in March is for “Loans,” which went to ~$300 billion overnight (March 16 balance sheet release).

If you look at the latest balance sheet (Table 5, H.4.1), the loan value is still ~$150 billion. So the March liquidity injection has only been halfway unwound.

The total assets have declined as more than $300 billion in notes, bonds, and MBS rolled off in accordance with QT in that time.

But half the loans still on the books from the March injection are inflationary.

Here is the analysis, for each type of “loan” (they weren’t all loans), with a chart for each. Excerpt from my monthly article about the Fed’s assets:

https://wolfstreet.com/2023/11/02/fed-balance-sheet-qt-1-1-trillion-from-peak-to-7-87-trillion-lowest-since-may-2021/

Repos come in two flavors, both $0 now. Repos with “foreign official” counterparties – likely the Swiss National Bank in its efforts to backstop the take-under of Credit Suisse by UBS – were paid off in April. At the peak in March 2023, they reached $60 billion.

The normal repos with US counterparties faded out in July 2020, when the Fed made the terms less attractive. The Fed currently charges 5.5% on repos, as part of its policy rates, which it left unchanged yesterday, and there are no takers at these rates. But there were lots of takers during the crisis in March through June 2020, and when the repo market blew out in late 2019. That’s the big bulge in the chart below.

The little bulge in early 2023 were the repos with foreign official counterparties.

Discount Window: roughly unchanged in October, at the near-nothing level of $2.9 billion, compared to $153 billion in bank-panic March (red line in the chart below).

Discount Window lending to banks is as old as the Fed. The Fed currently charges banks 5.5% to borrow at the discount window, and banks have to post collateral under strict conditions and at “fair market value.” Banks pay off these expensive Discount Window loans as soon as they can.

Bank Term Funding Program (BTFP): ticked up by $1.4 billion in October to $109 billion (green line in the chart below).

The BTFP, created during the bank panic, is less punitive and more flexible than the Discount Window. Banks can borrow for up to one year, at a fixed rate, pegged to the one-year overnight index swap rate plus 10 basis points. The collateral is valued at purchase price rather than at the lower market price.

This facility is small compared to the $22.8 trillion in commercial bank assets held by the 4,100 commercial banks in the US.

Loans to FDIC: -$16 billion in October, to $47 billion.

The FDIC has been selling the assets it took on with the takedowns of Silicon Valley Bank, Signature Bank, and First Republic. After the asset sales close, the FDIC sends the proceeds from the sales to the Fed to pay down the loan balance. The FDIC also issued a $50 billion loan to JPMorgan to fund part of the First Republic liabilities that JPMorgan took on.

Who has a policy of not letting anyone fail?

You do realize that lots of banks failed and their shareholders lost everything right?

There is a difference between bank shareholders and bank depositors.

Depositors should have taken a haircut.

1. Only depositors with account balances over $250,000 maybe should have taken a haircut.

2. Even those accounts were likely going to be made pretty much whole after all of the failing banks assets were sold off and depositors were reimbursed.

3. That would have taken months, or years even. Meanwhile, many of those accounts over $250,000 were things like payroll accounts and such that would have put the companies behind those accounts out of business because they couldn’t wait months or years to get their money.

4. That would have hurt lots of regular working people who did nothing wrong.

I was initially against the bailout of big depositors until I realized that they were going to pretty much be made whole anyway in the long wrong. The bailout just saved a lot of delay that could have hurts lots of people.

The central banks should stop worrying about the opinions of the markets they gave trillions and do the needful. Instead of telegraphing that things may be higher for longer make them higher and the markets will adjust accordingly and make the job easier possibly negating the longer. Waiting for them to stop partying with the free cash is a fools errand.

And there is still a gargantuan stockpile of free cash. That’s the problem, and also the reason that so many commenters here say QT should be more aggressive, or that the Fed should hike another quarter point. Then, on top of the gargantuan cash stockpile still sloshing around, we have a Congress that shows no signs whatsoever of fiscal constraint. Congress wants to spend trllions more each year, and they only disagree among themselves about what to spend it on. The Fed is at least on the right path, but staying on their current path will result in a fix to current problems after several years, vs a faster time frame, say six months from now. I believe that all the bitching comes from the Fed’s time horizon, not the progress it is making.

If the Fed tightens in response to this loosening of financial conditions, the market will immediately then price in cuts just a bit further out. “OK, NOW the Fed really IS done.” Guaranteed. If they tighten, I’m going long duration.

The markets all think the Fed will cut eventually. Today’s inflation expectations came in high. Initial jobless claims today were 209,000, well below the forecast of 225,000 and last week’s 233,000. Fed’s 2 percent inflation target seems like a pipedream.

The average Fed Funds Rate 1971 to 2022 was 4.86%, median 4.97%. Taking out ZIRP years, the average 1971 to 2008 was 6.43%, median 5.62%. Pretty much where we are now. I don’t want to shock anybody, but 5.5% is pretty much normal. Don’t expect it to slow down the economy much. It would be amusing if the Fed kept it at around 5.5% pretty much forever. However, historically it would not seem like a particularly high rate.

True, but companies across the globe and all financial markets have tasted 0% rates.

Once they realize it’s gone they may change the way they do business (actually producing stuff instead of taking out cheap debt to buy back their own stock).

However it will probably take some time as they are used to reserve banks flooding the markets with money whenever skies turn cloudy.

Junkies will always want free junk, and will whine and moan like you wouldn’t believe when they can’t get it. The markets need their junk, and Powell, the dealer who got them addicted to it in the first place, is not giving it to them. For now.

Yes. This is why all this talk of “look how fast they raised rates” is both true but also not really relevant to slowing the economy, rates should probably be 6 or 7% to really reset inflation, ZIRP is a historical anomaly and is not a new normal.

Perhaps it might help if the Federal Reserve released explicit numeric criteria for what it would take to cut rates. For example, “PCE +0.2% or less for 4 months in a row.” Or “unemployment rate above 4.25%.” This will get markets on the same page instead of just being left guessing.

Strangely, despite having a staff filled with quantitatively-oriented PhD economists, the FOMC voting members themselves (which include non-academics) prefer to be deliberately ambiguous & not bound to any numeric targets in their public communications.

It’s less surprising when you consider that Keynesians and neoclassical economists still don’t agree on whether saving is due to fear or willingness to delay gratification.

The more I’ve learned about economics (granted, not very much) the more shocked I am by how much disagreement there is over really basic facts. And the tribalism!

That’s because economics, especially the neoclassical orthodoxy, more closely resembles religion than science.

I agree. Religions and economics are based on stories. They aren’t based on the laws of physics. But people want stories. That’s why we’re reading “Wolf Street”. Wolf does his best to parse out the stories and the physics. We’re all trying to get a glimpse of reality through the fog.

Agreed — economics seems to resemble social sciences and some humanities (history for example) where researchers FIRST establish their team membership, or their religion to use your metaphor — THEN do research.

All economics problems can be solved either by a) a return to the gold standard, or b) government deficit spending — depending on your tribe.

The Fed has been clear that they won’t cut as long as inflation is above their 2% target.

And now that they’ve said that they have to stick to it.

If they cut with inflation still >2%, it could actually cause long rates to go up, as the mkt interprets it as the Fed abandoning their inflation target.

The Fed has shown it ultimately cares most about the stock market. It’s bigger than the economy, after all. If the stock market were to crash, they’ll panic and ease just like they always do, regardless of what inflation is doing.

This argument sorta makes sense if we consider that a whole lot of banks, which are traded on the stock market, are mostly only solvent these days based on their share price.

Maybe when the Fed is really only worried about the banking sector specifically? (Never mind, I just remembered GM and Chrysler — but those were Congressional decisions, right?)

Wait, that doesn’t make sense. Solvent means that your assets exceed your liabilities. What does a bank’s share price have to do with that?

The logic in this comment is more Kramer than George

Huh?

What does a bank’s solvency have to do with their share price?

Also, do you realize that all modern banks by literal definition are insolvent? Their liabilities (deposits they hold for others) exceed their cash on hand? It is called fractional banking.

Yes.

But don’t forget there is suspension of ‘Mkt to Mkt’ accounting standard since ’09. How do one price the liabilities? Beside Banks get 5.4% for their funds deposited at the Fed.

Stability of Banking system is of paramount importance to the Fed, than anything. They will ‘bailout ‘ the banks again if need to.

‘Fractional banking’ clearly and briefly summed up.

Define or describe how ‘non-fractional’ banking would work? If this NFB holds all deposits on hand, how could it make a loan, let alone a profit?

Of course, it’s not just ‘modern banks’ that don’t have all deposits on hand, it’s all commercial banks going back further than Julius Caesar. The bank takes deposits and makes loans, with the difference in the interest rates being its profit which makes the bank’s existence possible.

A fundamental problem for banks is that depositors want to lend ‘short’ while borrowers want to borrow ‘long’. This is why even a bank with solid loans can fail if a mass of depositors want their money NOW. It’s also why all developed economies have a central bank.

Jimmy Stewart, manager of a bank experiencing a run, does a pretty good job of explaining this in ‘It’s a Wonderful Life’. In the movie he succeeds in calming depositors. Which is good, because in the Depression the Fed was useless.

Yeah, maybe I conflated correlation and causation here… Loss of depositor confidence leads to withdrawals leads to share price decline.

I call BS.

What evidence do you have that the FED ultimately cares most about the stock market?

Remember, the stock market is down off of its highs and the FED hasn’t cut, not stopped QT.

Just less than 10% from their peak since 2021. Most of the losses got re-covered this year, favoring those who were buying dollar averaging

YTD

DIA —– +7.76%

SPY —— +19.85%

qqq —— +46.53%

B/c financial conditions are still relatively loose and the liquidity is NOT yet restricted. Effect of prolonged ZRP over a decade and 4 Trillion dump in the March of 2020.

You realize that supports my point right?

It has been over two years since the stock market hit its high. During that time the market has been even lower and the FED still didn’t backtrack on rates, nor QT.

Tell you what. Come back next time the market drops 40% and we’ll talk.

Amen!

Happy Thanksgiving!

Cheers,

B

When people say interest rates will be higher for longer, they are really saying inflation will be higher for longer, because higher interest rates are a response to high inflation.

In that sense, “higher for longer” is just another dovish excuse to prolong the inflation fight, allowing inflation to remain elevated and permanently embed.

Central banks can’t fight inflation if they allow Wall Street to tie their hands.

Agree

That is not what people are saying. But if you continue to assume that you are going to be deceived.

The comments on this site are a microcosm of how stock market investors feel in this country. Its like when a hurricane hits the Gulf of Mexico. Rumors start that there is going to be a gas shortage in Texas where I live. There is no basis for a gas shortage but everybody gases up and hoards gas anyway which causes a temporary shortage so the rumor becomes reality. Everyone is preconditioned now for the Fed to save the market no matter what. It might not be true but we may hit an all time high in the markets anyway even with higher rates and QT. Nobody wants to miss out on the Santa rally even though there is no basis for one. It will be interesting to see if the market can beat this drum long enough that even when the recession finally hits they are able to say we told you so even though they were fundamentally wrong the entire time and kept the market higher than it should have been the whole time.

“The market can stay irrational a lot longer than you can stay solvent!” Trite, but true.

https://www.marketwatch.com/story/central-banks-are-cutting-interest-rates-at-fastest-clip-in-years-when-will-the-fed-join-them-d77bb91a

I can’t read this article because it’s paywall, but I’m assuming it’s nonsense….

Correct, nonsense. I already addressed this right at t the top, so I’ll just repeat it again:

This is typical MarketWatch context-less headline BS.

For example, the central bank of Brazil has cut three times, but it cut from 13.75%, to 12.25% now.

This 12.25% is way restrictive still!! Inflation in Brazil is now 4.8%!!! It has come down from 12%.

Brazil started hiking a year before the Fed, and it hiked in huge mega leaps of 2 percentage points at a time, and got way high to (successfully) protect its currency ahead of Fed rate hikes.

Mexico’s inflation is now down to 4.3%, from about 8.5%. It hasn’t cut yet, and the rate is still at 11.25%!!! So it will cut eventually.

Unlike the euro and the yen, Brazil’s and Mexico’s currencies did well against the USD due to the huge and early rate hikes. And both of their rates are still in the double digits with inflation not much worse than in the US.

So when you talk about rate cuts in the headline, you need to say where from and to where and in which country!!! Obviously the morons or algos that write those articles don’t have a clue. So careful dragging this context-less BS into here.

“Nobody wants to miss out on the Santa rally even though there is no basis for one”

I have been in the mkt since 1982 and invested under the good ole, our genuine Free Market Capitalism. Then in the March, of ’09 the ‘free cap mkt’ ceased to exist thanks to Fed.

Ever since there has been fight between the PERCEPTION supported by Fed’s speak. FOMC members dovish remarks vs the REALITY..

Front running the Feds’ policies made the investing a casino game. Fundamentals mean nothing. The Fed’s balance sheet was less than 1 Trillion in 2008 but now over 8 Trillions. Where do you think all that money went – goosing the mkt. Rest is history

I think the market needs a true moment of “Fxxk around and find out” higher and longer is good, savers finally get rewarded for once..

Wall Street won’t get the hint until they are hit over the head.

“If the markets don’t infer from this that it’ll be high for longer, we’ll have to use our rate instruments and hike to get where we want to go.”

Fantastic. Knock em down to size.

Hi Wolf…when you wrote:

How are you going to get inflation to go down if the markets refuse to tighten financial conditions, and instead loosen the financial conditions?

What markets are you referring to? The DOW, NASDAQ??? If so, how do they tighten financial conditions?

Thank you.

This is mostly the credit markets: yields including junk bonds and leveraged loans, spreads, risk premiums, the kind of stuff that determines the cost of borrowing for consumers and businesses.

What about dropping interest rates to keep the same “real rate”(let say 1,5% real rate) and keep QT going strong? That should make everyone happy?

Balance sheet comes down slowly and interest on debt doesn’t skyrocket !

“That should make everyone happy?”

LOL, Wall Street hates QT more than anything.

LOL, Wolf has crazy eyes about now! I think he might need a ‘comment colonic’!

Not clear the value of the markets having a sudden and steep decline is considered good by so many. It isn’t like I sold all my equities and have slightly rebalanced my limited portfolio. Reality is there would be pain for most people whether it be through job losses or portfolios and retirement. Not clear why so many want “the market” to get its due, like it is some kind of living entity. If I had my way I would deconstruct most of it but given that is not in the realm of possibility, so I try to work within a system that works for the few. Unfortunately, sudden changes hurt the few less and a lot of people with less much more.

You don’t know why people want the market to get it’s due? Think harder. It’s quite obvious why. And it is within the realm of possibility to rein it in. These articles spell out all you need to know. You say you try to work within the system? You are exactly who they play to, and you are part if the problem. Wall Street destroys the people who can least afford it. Think harder.

Thinking harder doesn’t produce any positive result as long as the our good ole genuine ‘free capital market ‘system remains dead.

Interest rates should be determined by the free credit mkt and NOT the CBers but then of course I am dreaming.

This gang has already brought us TWO Boom-Bust cycles in this century by interfering with free mkt system and setting the price of CAPITAL very low (ZRP) for over a decade. This is an anomaly in the 200 yrs of US mkt history. So is the bull mkt since ’09.

No country in human history has prospered by spending debt on debt.

I can never help but laugh whenever someone talks about FREE MARKETS.

I would bet a lot of money that you couldn’t define FREE MARKETS in such a way that you would recognize all of the implications of what you are advocating.

I find that people who constantly complain about the lack of FREE MARKETS have absolutely no idea what they are talking about.

Honestly most of my beliefs would make me a Marxist/Leninist and have great respect for those such as Che and Fidel and Fred Hampton and such. Socialism, while understood only by a relatively small portion of our society was mostly defeated by the capitalists. Sadly with a country of our wealth it would be easily achievable. Playing in a different part of our system is still liberal economics or being a neoliberalist. I still believe in it but it won’t happen here in the US any time soon.

Most people are happy to fight for scraps at the table rather than take up a struggle and have been too persuaded that communism of one variety is trying to move to a classless society. Clearly the CIAs purchase and production of Animal Farm, Rambo movies and all else has replaced the history of labors struggles.

Glen – mebbe in part why I see so many young women aspiring to princesshood as opposed to that of the ‘rebel girl’ immortalized in old labor song…

may we all find a better day.

Glen-

Hard lessons are taught by painful markets, while chronically positive returns breed a dangerous complacency and, too often, euphoria.

“Tired mothers find that spanking takes less time than reasoning and penetrates to the seat of the memory.”

-Will Durant

Not wishing for that day, but expecting all the same.

I agree hard lessons can be learned but as my favorite show South Park demonstrates, it can also create a lot of people with victim mentality!

“Unfortunately, sudden changes hurt the few less and a lot of people with less much more.”

Not necessarily. Bankruptcy wipes out investors, but companies with a lower debt burden can actually stay open and save jobs, *and* allow the company to operate more efficiently going forward. Bankruptcy is the right way to clear markets under Capitalism.

Having the Fed prop up “fake” companies indefinitely is Crony Capitalism that causes a misallocation of capital. Crony Capitalism can actually reward unhealthy companies and drive healthy companies out of existence. For example ZIRP allows unhealthy companies with no profits to undercut prices of healthy companies with a good business model. The healthy company then has a choice to either (1) lose market share, or to (2) copy the “business model” of the unhealthy company. Artificially low interest rates set by the Fed are a feature of Crony Capitalism, not of a well functioning Capitalism model.

Don’t disagree. My point is many small investors, especially bundled in with the market with 401Ks and such get hit harder as if you are worth 10 million and suddenly are worth 5 million you likely are still okay.

I am generally against capitalism although China’s state capitalism would work as you have to adjust to the real world. They might for example own 1% of tencent video which is essentially their Netflix but they have Golden shares which provide more voting rights. I would argue most capitalism is corny capitalism but I get your point. It is the dominant system for now but just as slavery or feudalism went away there is possibility for a system that works for the benefit of all, although that is a tall order. I try to walk a fine line with Wolf as I agree politics has no place here but at the same time political and economic systems are linked closely despite many thinking they are not.

It’s the upper half of income workers that have a significant amount of wealth locked up in assets outside their home. The “people with less” would likely bounce back just fine from their relatively tiny investment losses vs their income, since the bulk of their wealth, in aggregate, is in their home.

JD – but, as long as we deal with unlimited speculation in housing, does that render those. investments on the lesser side into low-hanging fruit for certain segments?

may we all find a better day.

Re: the quote from the ECB…like, obviously. In the same way, there is a feed- back loop between markets and the Fed. The Fed is trying to tamp down excess, it paused to assess the results of its last hike: ‘Oh wow! Market has huge rally.

The market reacted to the pause in rates as though it was a cut in rates. So… Fed has to keep tightening. A theory is tested by its ability to predict: I predict next Fed move is a hike.

I know we are supposed to avoid politics but no one can deny politics play a role: I think the Fed would REALLY like to avoid having its future boss be its previous boss. It is not supposed to have a boss, as per the Inaugural Oath…but promises, promises. So in this theory, the Fed is trying to dish out the nasty medicine now, to get it over with, and hand out good news in mid 24.

We need a hot CPI number in December in order for the rate hike to happen. Then we will get the much-needed 20% market correction. Poetic justice for the greed of Wall Street.

PS: on a personal level, apart from the impact on the institution of the Fed, it would not be surprising if Powell does not want to work with someone who called him: “worse than Xi” when the Fed tried some ‘baby step’ hikes.

1) Japan : all rates are lower than a month ago. The front end is still negative. Y/Y all rates are higher than a year ago. The 2Y = 0.04. The 10Y = 0.73. The 40Y is 1.76. Not much above zero.

2) China : from 3Y all rates are down M/M. From 5Y all rates are down Y/Y. The 2Y = 2.4. The 10Y = 2.7. The 30Y = 2.98.

3) Germany : all rates are lower M/M, but above a year ago. The 3M = 3.7.

The 2Y = 3.0. The 10Y = 2,56. The 30Y = 2.74.

4) SPX and the Dow [1M] flipped lower in Oct 2023. The trend is down

until cancelled. If the US & Europe entered a recession zero rates are not too far below.

5) Wall street sent the stock market up to take profit, to dump at higher prices. Warren Buffett B&H might be stuck with a rotten AAPL.

Not sure if this was intended to be a comparison but Japan sets a maximum yield not unlike the US did back in WW2. Japan used to be capped at .5 but then raised to 1 and are now considering going higher. This is being done since US is up and to avoid having the BOJ from buying too many of their bonds to keep yields super low. Hopefully the US doesn’t do yield control as would like to see them go up.

Glen, in Oct 2008 the Fed raided bank accounts to save the large banks. Before that day the Fed controlled only the front end. Since

Oct 2008 the Fed had enough power to control the long duration and mortgage rates.

In aggregate mkt participants will keep slowly losing money by fighting the FED and the pain of losing will teach them but it will be a very long and drawn out process. The biggest problem may be housing and that may take years to straighten out.

For me, as a stock mkt participant, it is a matter of figuring out when to cover the Santa Claus rally and whether to short into the new year. This really isn’t a bad time to be a trader/investor but it takes a lot of effort.

The Swedish Riksbank (the oldest central bank in the world, founded in 1668) left its interest rate unchanged at 4% today. Most experts were expecting a hike by 25 basis points.

I think the reason markets are betting on rate cuts is because the debt is so high that Fed will have to pivot soon to ease the interest burden on government budget. I’d like to know what Wolf thinks about debt sustainability at current rates. Meanwhile the government keeps selling treasuries increasing its debt, what’s the endgame for ballooning debt?

The US Federal government doesn’t face a solvency constraint in $USD. it can make any interest payments regardless of the rate or the debt level. This is not to say that there are levels which might be politically untenable.

There is no “end game” where US Federal debt is concerned unless you are imagining some apocalyptic scenario of national collapse — the state is effectively immortal in human terms absent catastrophic civil war or conquest.

eg-

The State may (or may not) be immortal, but the currency is not, at least if history offers any lessons.

Not predicting that the currency is going to hell directly, but purchasing power will most likely trend downward as debt grows. And the “fiscal dominance” scenario that Calomiris described in an accessible Fed St. Louis article last month seems damned probable.

Bottom line: little “solvency” risk, but considerable currency/purchasing power risk.

I agree — the constraint is real resources (including labour) available for purchase in $USD; commonly understood as an inflation constraint. My point is simply that to approach it as a solvency constraint is a category error, and one that leads to all manner of analytical errors.

Of course, the state only has to worry about an inflation constraint to the extent that it’s accountable to its citizenry — hence my point about what may or may not be politically possible.

No one can go broke in their own currency, but other countries stop wanting it. It’s a bit odd when people say there can’t be a US currency crisis because there has already been one. Here is bit from the NYT.

BONN, Oct. 4 — United States efforts to explore the possibility of a new international aid package for the dollar have met with only measured West German support, a reception that bankers and money‐market analysts consider certain to limit the extent of any such plan.

In talks today, high Government officials stressed that while West Germany was willing to support the dollar on currency markets, economic developments since its participation in dollar‐rescue programs in January, March and November of last year had narrowed the scope of its possible contribution.

This is from Oct 4, nineteen seventy nine.

A few other symptoms of the crisis: tourists around the world were asked to please pay in local currency. One young couple delighted their Italian hotel manager by agreeing to pay in lira even though the price of their expensive stay had been priced in US$.

Other symptom: the Hunt brothers with Saudi help drive silver to 50 an oz and Americans begin fleeing the US $ for gold, silver, Swiss francs and W. German DM. It may have been the brothers’ announcement of a silver- backed bond that drove Volker to force the Chicago exchange to cease taking orders for silver delivery.

The US had to issue bonds denominated in Swiss francs.

It wasn’t just inflation that drove Volcker to take drastic action. A currency crisis really gets the attention of govts who can tolerate inflation: See Russia and Turkey.

These charts that show interest payments shooting shooting straight up are context-less BS.

Debt sustainability is determined the interest payments as a percent of tax receipts (tax receipts minus receipts for Social Security, etc.). I cover this quarterly, when the “tax receipts minus SS contributions” are released with the GDP revision, next one coming up in a few days. Here is the latest:

https://wolfstreet.com/2023/08/30/curse-of-easy-money-us-government-interest-payments-v-tax-receipts-average-interest-on-treasury-debt-debt-to-gdp-in-q2/

Wolf, that last year is shooting straight up, and would be twice as high if Joe Manchin didn’t exist.

I thought you said that nothing goes up in a straight line. Chuckle.

It won’t be straight. Next, there will be a zig, and then there will be a zag.

I think that eventually it will come down to supply and demand (like everything else).

The FED’S influence decreases the longer a bond/note goes out. So the FED has a ton of influence on short term rates. It has only a little influence on the long term rates. Those rates are set by supply and demand for those bonds.

Right now, lots of market participants think that long term rates are going to drop (after short term rates drop). They are pouring all of their resources into this bet by buying up long term bonds and driving down rates.

Eventually those participants who hold this view will run out of resources. The FED has made it clear that they are going to keep short term rates higher for longer. The U.S. treasury will continue to dump long term bonds onto the market as the U.S. continues to run high deficits. There is no indication that either of these things will change in the future.

Eventually participants will run out of resources to continue to buy up long term bonds yet the Treasury will continue to dump them on the market.

Something will give and long term rates will rise simply because there will be fewer buyers for those bonds.

The FED keeps saying higher for longer and the federal deficit keeps going. I don’t understand why people would bet against either of those things continuing. Eventually something will give. I have a feeling it is going to be very painful for a lot of people.

I stay with 3 month T Bills with yields around 5.2% for my cash account, with a few puts on TLT. Rest is short term trading but long term investing with div paying ETFs excluding RE, Green metals. ESG investing is a loser.

Until the World decides to limit ‘consumption’ to NEED and NOT WANT, the demand for fossil fuel will keep increasing.

Oil/gas is needed to produce for over 6000 day to day products, as of now.

Green energy is a distant ‘dream’

I’m starting to like this game of markets and central banks.

I smell more interest rate hikes after the new year!

“If the markets don’t infer from this that it’ll be high for longer, we’ll have to use our rate instruments and hike to get where we want to go.”

Not if the “hikes” continue in the 1/4 to 1/2 percent range. They need to be hiking ONE to TWO percentage points at a time.

I said something similar many months ago.

The market thinks the Fed can’t control inflation. Like a rubber band thats been stretched so far its gone loose, they can’t get it back.

I found a good inflation measurement the other day, not quite the Big Mac index, but printed books. Paperback books which conveniently have the printing date on them and also the price, and are also fairly inelastic in construction, you have to print onto paper and bind etc

You can find them in any second-hand shop check the date and see what the inflation rate is over a range.

“If the markets don’t infer from this that it’ll be high for longer, we’ll have to use our rate instruments and hike to get where we want to go.”

Not if the “hikes” continue in the 1/4 to 1/2 percent range. They need to be hiking ONE to TWO percentage points at a time.