The clueless WSJ reporter needs to be taken to the woodshed. That kind of BS article doesn’t belong in the WSJ.

By Wolf Richter for WOLF STREET.

The Wall Street Journal managed to publish another stupid article this morning with a clickbait headline and subtitle about hotels in San Francisco, concocted by a young clueless reporter who lives on the other side of the country and got her notions about San Francisco from reading what exactly?

WSJ: “Hotel Owners Start to Write Off San Francisco as Business Nosedives. City’s lodging business has been squeezed by crime and other quality-of-life issues.”

As her core example, she regurgitated a clickbait story engineered via press release by Park Hotels & Resorts, a publicly traded REIT that owns a bunch of decades-old overleveraged hotel properties. It doesn’t operate the hotels, other companies do that. It just owns the land and buildings.

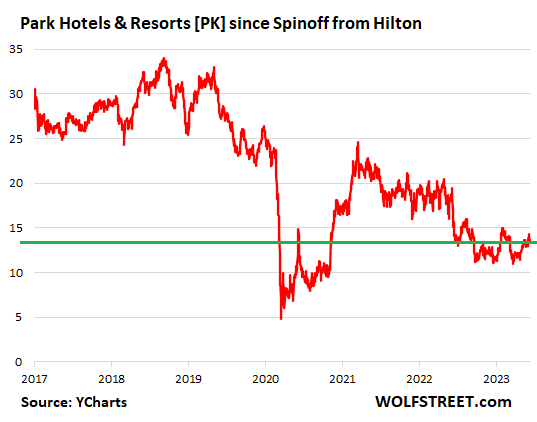

Its shares have collapsed by 59% from the high, and by 54% from the IPO in 2017, after it slashed its dividends multiple times and lost $1.9 billion in 2020 and 2021, far more than it had ever made as a public company.

And after ripping off its shareholders, Park Hotels is now ripping off bond mutual funds and pension funds that bought the commercial mortgage-backed securities (CMBS) backed by the mortgage that it defaulted on, and after ripping off all its investors to the tune of billions of dollars, it blamed in a ridiculous press release on June 5 the “street conditions” and high vacancy rates in San Francisco?

Park Hotels failed to pay off a $725 million interest-only non-recourse mortgage that matured last November. The mortgage was secured by two run-down mega-hotels in San Francisco, the 1,921-room Hilton San Francisco Union Square and the 1,024-room Parc 55 San Francisco. Their towers were built in the 1960s through 1980s and need an estimated $200 million in upgrades and renovations.

Park Hotels refinanced the properties in 2016, during the era of free money, with a high-risk interest-only non-recourse 4.1% mortgage of $725 million, backed by fantasy valuations of these decades-old run-down properties of $1.02 billion and $540 million respectively.

Banks hang on to their low-risk high-quality loans. But no bank would ever want that kind of toxic mortgage on its books, that interest-only, non-recourse commercial mortgage, backed by fantasy valuations of some old towers.

So, JPMorgan sliced and diced the mortgage and securitized it into CMBS, to where the top-rated slices were well into investment grade. The slices were sold to bond mutual funds, pension funds, etc., that manage other people’s money.

These other people whose money this was are now getting screwed, and they likely don’t even know about it.

So in November 2022, Park Hotels was supposed to pay off the $725 million mortgage but obviously didn’t have the cash. The mortgage had an interest rate of 4.1%. But by the time it matured, interest rates on these types of high-risk commercial mortgages were already over 7%. And getting a new 7% mortgage to pay off the old 4.1% mortgage wouldn’t work out at all. That’s why interest-only mortgages rolled into CMBS are toxic.

So forget it. Let other people’s money take the hit.

Park Hotels only owns the properties. The hotels themselves are operated by other companies, and when Park Hotel defaults on a mortgage and walks away from the property, it means ownership of the property will change. That’s all it means for the hotel. The operating company remains the same.

This default has no impact on San Francisco. But Park Hotels is screwing your bond mutual fund and pension fund.

Park Hotels was spun off from Hilton Hotels. In 2007, Hilton was taken private in a huge leveraged buyout (LBO) by PE firm Blackstone. In 2013, Blackstone began to unload its Hilton stake via IPO, ultimately at a huge profit. In late 2016, Hilton spun off its hotel properties into a REIT, Park Hotels and Resorts [PK], which began trading in January 2017.

Park Hotels has been a catastrophic nightmare for retail investors. The misdeeds that sank Park Hotels’ shares didn’t happen on the streets of San Francisco – as the company ridiculously alleged – but in the C-suite of Park Hotels and on Wall Street. And its investors and now the holders of the CMBS are getting ripped off.

The shares have collapsed by 54% since the IPO in January 2017, and by 59.5% from the peak in September 2018:

Park Hotels cut its quarterly dividends in big increments starting in 2020 to where it eventually paid just 1 cent for three quarters in a row. Last December, it raised its dividend to 25 cents, compared to a range of 43 cents to $1.00 in 2017 through 2019. Then in Q1 2023, it cut its dividend again to 15 cents, and for Q2, it also declared a dividend of 15 cents. People invest in REITs to get the juicy dividends, and to have a somewhat stable share price, and they got screwed on both fronts by this company.

Park Hotel lists “46 premium-branded hotels and resorts with over 29,000 rooms primarily located in prime city center and resort locations” on its site today, still including the properties that it is walking away from in San Francisco.

Alas, at the time of the IPO, the REIT had, according to the hype-and-hoopla press release, “67 premium-branded hotels and resorts with more than 35,000 rooms located in prime U.S. locations and international markets with high barriers to entry.” Such is the hype and hoopla, and investors fell for it, and paid a huge price.

First, they screwed the investors that bought the shares hoping for rich dividends and a roughly stable share price. Now, by refusing to pay off the mortgage, they’re screwing whoever indirectly holds the CMBS, such as retail investors in bond funds and pension fund beneficiaries. And the company blames the “street conditions” in San Francisco to distract from this rip-off?

It always makes great clickbait headlines if you can stick “crime” and “San Francisco” into it, and the blogosphere and the media, in their braindead manner jumped, all over it last week. Put “crime” and “Tulsa” into a headline, and no one reads it. That’s why clickbait exists: it creates clicks.

So now, the Wall Street Journal published another article with a clickbait headline and “crime” and “quality-of-life-issues” in the subtitle about hotels in San Francisco, specifically the two defaulted Park Hotels properties. Did the author, who lives on the other side of the continent, get her info about “crime” and “quality-of-life-issues” from the vast collection of fantasy porn about San Francisco?

In terms of hotel data, she wrote that revenue per available room was “nearly 23% lower in April compared with the same month in 2019.” I mean, DUH, hotels have to compete with a gazillion vacation rentals in San Francisco, and that’s hard. And so room rates have to come down.

In addition, the largest group of leisure tourists before the pandemic, leisure tourists from China, have yet to come back in large numbers, though they have started to trickle back. But that’s the case everywhere in the US where Chinese leisure tourists like to go.

And the Hilton is a convention hotel, catering to expense-account travelers that attend conventions and trade shows at the Hilton and other venues. During the pandemic, most conventions and trade shows were shut down across the US, which taught a lot of business executives that not every convention or trade show is necessary. But even that business is coming back, believe it or not.

San Francisco is teeming with tourists, they’re just not all staying in expense-account hotels. Many of them are staying in a gazillion vacation rentals and are very hard to track. Condos throughout the city are listed on the vacation rental market. This is a huge thing. And hotels have to compete with them.

Then get this: To cement her fantasy about “crime and other quality-of-life issues” or whatever in San Francisco, she throws in references about some retail stores that closed in San Francisco. Jeeesus. Doesn’t she know anything?

In a phenomenon triggered by ecommerce that I’ve called “brick-and-mortar meltdown” since 2017, and that I have reported on since 2017, retailers closed tens of thousands of stores. There are zombie malls everywhere. An endless number of retailers, from Sears Holdings and Toys ‘R’ Us on down to Bed, Bath & Beyond filed for bankruptcy and most of them vanished. All regional and nearly all national department store chains filed for bankruptcy and vanished. There are just a few left. J.C. Penney, which finally filed for bankruptcy in 2020, was bought out of bankruptcy by the largest mall landlords in the US, Simon Property Group (SPG) and Brookfield, because they didn’t want shuttered anchor stores doom their malls. Macy’s, one of the few surviving department stores, has closed hundreds of stores over the years and continues to close stores. SPG defaulted on and walked away from overindebted malls across the US, no problem, including the 170-store 1.2-million-square-foot Town Center at Cobb in Georgia, the 1.1-million-square-foot Montgomery Mall in North Wales, Pennsylvania, and in 2019, the 1-million-square-foot Independence Center in a suburb of Kansas City, Missouri, which generated what was then the largest loss ever by a retail CMBS loan. Three mall REITs have filed for bankruptcy since November 2020, SPG’s spinoff, Washington Prime Group, CBL & Associates Properties, and Pennsylvania Real Estate Investment Trust.

But when a few stores close in San Francisco, a clueless reporter thinks it’s a sign of “crime and other quality-of-life issues” instead of six years of brick-and-mortar meltdown due to the way Americans now shop, namely online, with San Francisco being the epicenter of ecommerce?

That kind of bullshit article doesn’t belong in the WSJ, and the reporter needs to be taken to the woodshed.

Someone is going to buy those hotel properties for a song from the ripped-off CMBS holders (represented by the special servicer Wells Fargo). The new owners of the buildings can then perform the necessary upgrades and renovations and end up with a decent business in San Francisco.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Where did the proceeds of the 2016 refi go? Didn’t any of the money get reinvested in updating the buildings? If it was a take the money and run refi, the buildings were doomed unless the boom kept expanding.

Nope. That company was the product of an LBO and had lots of debt. LBOs — “leveraged” buyouts — are that way, they’re loaded up with debt.

Park Hotels then further piled on debt. In 2018, it had $2.95 billion in debt. By the end of 2022, it had $4.8 billion in debt.

It lists $8.3 billion in assets, but that’s the hotels that it is now walking away from with big losses. So no telling what those hotel assets are really worth.

Stockholder equity (assets minus liabilities) is $4 billion. But if the $8 billion in hotels are worth nothing as it walks away, that’s a tough one, LOL

Large coastal cities all have nasty, and mostly corrupt, hot potato rent contracts. This isn’t new. BUT the rate of crime DOES change in these cities every couple decades. It goes up, it goes down, based on policy…but the crazy contracts do not. They just go up.

I will let everyone in on a secret. During a pandemic luxury hotels have plenty of fixed expenses and zero income. Park Hotels breaks out occupancy and revenue for each location. Many locations are fully recovered. With current labor and material inflation the replacement costs for their assets would be prohibitive. They are currently focusing on adding room keys to 2 beach front Hawaiian properties.

Well done!! LBO’s have been the underlying issue with major retailers for years.

No doubt that right wing Murdoch controlled WSJ is constantly twisting the news to push their agenda of blaming progressives for any and all problems in the world.

Republicans controlled 90% of the FED’s FOMC positions over the last 50 years.

= Money printing and lack of financial regulation are Republican policies that have caused 90% of the financial problems in the U.S.A.

= It is highly hypocritical when the WSJ tries to blame progressive controlled localities and policies for the problems that they are suffering from.

Didn’t Walgreens already use that crime excuse when they got in financial trouble due to being stupid in SF? There was an article here about it, maybe 2.

Our local one (in NICE area) is still trying to recover…shelves emptier…..service stinks…heavy turnover…confusion….the phone menu lies…..etc, etc.

Yes. So I’ll just repeat it here from my comment under the Westfield article:

Walgreens pulled the same crap. They’re all doing it. Walgreens had already closed 595 stores in the US in the two fiscal years through August 31, 2021, including some of the 200 Walgreens-branded stores that it had announced in 2019 it would close. This company is a store-closing machine. And no one cared, and it didn’t become global clickbait.

But then in Oct 2021, Walgreens announced that it would close some of its huge number of stores in San Francisco. Even after these closures, there were 53 stores in SF, some of them only a few blocks from each other. Walgreens blamed San Francisco, same BS. And it triggered a global wave of clickbait.

I ripped Walgreens apart, showing that it was a troubled retailer that was losing its pharmacy business in SF and elsewhere, and that’s why it closed the stores around the US and in SF.

Walgreens recently admitted that much, which was published in local media, but no one paid attention, and it didn’t become global clickbait. People don’t want to see reality.

Here is where I ripped Walgreens apart over its BS announcement:

https://wolfstreet.com/2021/10/23/why-walgreens-is-in-trouble-in-san-francisco-and-is-closing-some-stores-its-not-shoplifting-thats-a-purposeful-distraction-from-the-real-reasons/

I’m not going to let them get away with this crap anymore.

Keep investing in your bond funds and pension funds. We are looking for bag holders for our CMBS crap.

The rich hold their hedge funds accountable. So the passive investments like bond funds and pension funds is where we take a dump!

God bless the foolish retail investors so that we can take their money!

#Sarcasm

#Sarcasm

JD – dollars and cents, John, where is Wolf wrong? (Unless, perhaps, you are popping smoke as having an interest in the various perps biz?). Wherever population density increases (esp. cities) so do the myriad self-generated problems of humanity, well-represented here in the comments by those who are always throwing rocks at the West Coast but react with wonder and dismay at the associated issues linked to those moving to their presumably-perfect slices of heaven (hm, just like those who dealt with the millions who moved to the West in decades past). And if you do live out here, John, fer gawdssakes vote with your feet, or, (wherever you land), get involved with your fellow citizens and vote in the the good ol’ and grinding US PITA tradition of your local politics (to which you must pay attention to limit the awakening to outraged surprise at the morning’s news…), and DO share YOUR community’s problems and it’s efforts to effectively mitigate them (preferably other than by privatizing most profit and socializing most risk…).

may we all find a better day.

Dear John,

Throwing spit balls is not the answer. Blaming someone else is easy. I’m going reach here and think you are somewhere south of 50.

As far as I’m concerned, most in that age group doesn’t know what REAL WORK is.

The city website (sfgov) itself shows the metric for hotel occupancy and average room rates (both below 2019 level, even before adjusting to inflation).

For outsiders SFO does seem to be getting closer to Portland where businesses ARE leaving than to southern cities like Miami.

Your city, you know it better.

Latest month available: Hotel occupancy in March 2023 was 64.5%. In March 2019, it was 79.9%. But March 2023 had horrible weather/storms that tore up a lot of stuff and flooded things, and it was hell for tourists because what are you going to do? These storms started in December and went into April. You can see that in the chart below: tourists cancelled or left.

September 2023, occupancy was 76.6% compared to 87.4% in Sep 2019. So about 10 percentage points shy.

You also have to figure in the gazillion of vacation rentals that are not part of the hotel occupancy data. This is a huge business. They’re everywhere.

If it wasn’t for the reckless Fed we could have squeezed all these terribly run companies out of the economy in 2014-2015 at a much lower cost.

Instead the Fed used a free money bonanza that allowed every fool with the right connections mismanage their fiefdom of the economy for a decade.

Finally interest rates are bringing the smallest sense of sanity back to an economy gone mad.

I think this says more about the Wall Street Journal’s standards than anything else.

Decades ago the WSJ was a great paper. Great reporting, great editorials, smart insights. Then it was bought by the Murdochs and it went from being a great bastion of financial journalism to being a mouthpiece for the agenda the Murdochs wanted to drive.

It is unfortunate, but there is money to be made by playing up the fears of the ignorant. It has always been like this. In caveman days there was someone telling the ignorant that if they didn’t do what he wanted, the volcano gods would smite them.

Preachers!…the first hustlers!……or….first entrepreneurs?

It also highlights just how important the work that Wolf does. People are reading nonsense on supposedly reputable sites like the Wall Street Journal and making investment decisions which have real life consequences. Keep up the good work Wolf!

The WSJ hasn’t been reputable for years. Maybe not as bad as other Murdoch owned media, but still not reputable.

Wait till “The Closing Belle” shows up!

PE standard operating procedure during the quest for yield and ZIRP.

Blackstone a public company and many of the private PE pull the same. Oil and Gas MLP very similar any business with cash flow and stuff that banks could loan on fell into this game. I was a victim of the MLP game called MEMP mlp created by NGP partners out of Dallas . WSJ should be ashamed and the large banks that helped peddle the stuff to the public. Buyer beware and not sure who to trust myself .

R&T: he Window Is Closing for EV Startups

Even the most established and best-positioned EV startups — Lucid and Rivian — have lost billions upon billions in valuation as optimism dries up for the next generation of would-be-Teslas. For the rest of the little guys, the window of opportunity looks pretty slim.

Wolf, your articles are always a great source of unbiased information- but in this case I think you are letting emotions and your love of SF cloud your judgment. I lived in SF prior to covid and returned recently for the first time in 2 years on a business trip – the city has changed a great deal – and the cold hard numbers around public transport usage, foot traffic etc confirm it.

Much of downtown SF is a ghost town compared to what it once was – and this is unique to SF. Very few other cities across the US have experienced similar declines in the last 3 years.

So to claim that this is nothing special is disingenuous.

Have been to Tulsa Downtown??? DEPRESSING. There are lots of cities like that. Downtown SF is fine, there just aren’t as many people as there used to be. I go through it a lot, there are more people than than there were a year ago. But working from home rules in SF, everyone figures this out, and I have written extensively about the office tower situation in SF. WHICH HAS NOTHING TO DO WITH TOURISTS that stay in hotels that aren’t even downtown.

Yeah I am sure that SF is heaven on Earth and the best city in the USA and the world…………………………If you happen to be a biased person living in the city!!!!

I will take Tokyo or Yokohama or even Nagoya over SF any day.

(How long does the Shikansen stop in Nagoya? 2 Minutes and that is too long. First prize in a lottery is a week in Tokyo. Second prize is two days in Oasaka. Third prize is two weeks in Nagoya.)

SF is a cesspool compared to any of those cities.

My wife, who is from Tokyo, loves it in SF, 🧡🤣

I agree with your counterpoint here, Wolf. San Francisco is making a slow but sure recovery and I think it’s a fabulous place to be right now, offering virtually everything it’s been known for but without the crazy crowds. There are so many SF haters out there but rather than hate on SF, now’s the time to visit and spend time there. So much to see and do yet benefit from a feel the city last had in the early 90s before the two tech booms. Just avoid these two Park properties – they are awful. I am a Diamond Hilton patron and I’d never stay at either of these outdated convention hotels.

Tulsa has been featured on the show First 48 in over a dozen episodes. It’s a grisly show about solving homicides. I’m a regular viewer of the show. After watching a few episodes, I don’t think I’d ever want to live there. I’ll take the Swamp or even SFO with all of its problems any day.

Wolf You need to take a weekend trip to Warsaw The downtown is crazy busy I’ve been visiting since 1980 and this past January it was packed Tourists and Ukrainians added to the crowd like I’ve never imagined possible

We will know it’s bad in SF when Doc Savage expatriates

Warsaw is the second SF.

With uncontrolled immigration it became 3rd world city.

Dirty, overcrowded, expensive, smelly and with increasing crime.

I live in the touristy part of San Francisco (Russian Hill/North Beach). It’s crazy busy. Lots of people out and about. The tourists that have not come back in large numbers yet are Chinese tourists. Before the pandemic, they were the dominant group. During their zero-covid, it was hard for them to get out; now they can, and they’re starting to show up.

Downtown in SF is NOT the touristy part – that’s the business district. There is essentially no activity on weekends.

The Union Square area is more touristy. And there are lots of people there.

Park Hotels reported that their SF properties had a 48 percent occupancy rate during the last quarter. This is not sustainable. New York came in at 69 percent.

I must admit that a non- recourse loan secured by the 2 hotels is coming due at a bad time for the lenders. When the loan was originated SF was Park Hotels leading market.

Park Hotels made a decision to re-direct resources to Hawaii and Key West. Hawaii had 88.1 percent of their rooms filled. Key West is averaging $575 per/night with 79.1 occupancy.

Carl,

1. Blaming the city for their Park Hotels’ 48% occupancy rate is more effing corporate BS. The overall hotel occupancy rate in SF in Q1 was 57%. So their SF properties lagged far behind the overall market. And that’s THEIR fault, not the City’s, that they’re not competitive.

2. Q1 was horrible, super-storms one after the other, flooding, wind damage, all kinds of weather-related mayhem. Tourists left and cancelled because what are you going to do in weather events like this? This started in December and went into April. You can see the drop in the chart below. In March occupancy rate was 66%.

3. September 2022, occupancy was 77% compared to 87% in Sep 2019. So about 10 percentage points shy of pre-covid.

4. You also have to figure in the gazillion of vacation rentals that are not part of the hotel occupancy data. This is a huge business. They’re everywhere. Hotels have to learn how to compete with them or they’re going face the fate of Park Hotels.

5. These storms started in December and went into April. You can see that in the chart below: tourists cancelled or left:

Just look at the hotel OR stats of SF vs pre-covid and compare to NYC. Even with NYC’s own relative problems it has rebounded far more than SF.

SF has major problems. Likely just the beginning of a long decline.

The long decline is a nearly sure thing but I’d venture to say it will be nationwide SF , Baltimore, St Louis etc are just starting early

Everywhere in the US is going to take RE hits but SF/NYC/DC were ZIRP-City USA…it was in their…nature.

Aren’t you the ex-pat who chose to retire to Turkey (and has a rental house in downtown Warsaw)?

I’ll tough it out in here in the Bay Area, I like the challenge…..even if it is a lot tougher to get an AK-47……..:)

Do not trust anyone else with your money. Fund managers have taken billions of dollars in commissions off people offering financial products such as those involving these buildings, buying them with other people’s money, and alsobeing paid a commission to mismanage this money.

The only way out is to look after your own funds, investing in stuff you can see and check yourself.

I’ll never forget when my old boss’s high net worth financial advisor from JP Morgan tried to pitch me on managing my money. He showed me their long term returns which slightly outperformed the S&P which was underwhelming. Then I asked him what their fees were… which put their net returns below the S&P. Any high net worth individual would know this… but yet somehow their business survives???

Truth is most people don’t know the basics about how money works so although that sounds like good advice, most people simply don’t know how to do it on their own.

I interned for a high net worth advisor in Philly for a small boutique bank and it was the same thing. Always underperforming the sp500 and charging exorbitant fees. We were heavy in Chinese stocks in 2020 when I was there. Man he’s had a rough couple years. I’ll never forget the Covid crash and how I walked in on him sweating with his shirt off. He had no clue what to do, and his clients were calling non stop.

Even some PE shops are doing the same thing. Underperforming benchmark indices for the pension funds and keep making sh*tty investments because of the fees they get to charge the investors AND the portfolio companies for managing the businesses. They just pray one day they sell for 20x because they bought proforma synergized BS EBITDA at 16x with free money. I’ve been in PE for close to a decade and it’s all a facade. I’ll continue to ride the wave until it crashes.

“I’ve been in PE for close to a decade and it’s all a facade.”

It really does seem to be a lot more about surfing/gaming interest rate cycles than the hoary “operational business improvements”.

The PE industry has tried to push out its PR too many times in too compressed a period, against a background of too little success for the public to swallow it again so soon.

This isn’t to say there actually aren’t a ton of incumbent firms run like crap, already the personal fiefdoms of a handful of insiders.

But PE in practice may simply be about rearranging the self-dealing despots.

Yup. A lot of M&A add-ons I’ve seen in my PE experience is not to create a bigger better business, but it’s to prevent the platform from going bankrupt or facing a massive write down so they combine/proforma the performance and it doesn’t look so bad. Or to trigger a refi with a “new” set of bogus numbers so they don’t breech covenants… which are reported to investors.

I have worked in the mid market space so not the Blackstone, KKRs, Apollos and the like, but I assume everyone is up to the same tricks.

Convention “business is coming back, believe it or not”. –> While I have no data to dispute this, I can say for sure that several big tech conferences such as Oracle World (and it’s sister conference JavaOne) and VMWare’s Explore have permanently moved from SF to Las Vegas. I was at JavaOne a few years back and it was actually hosted at the Hilton and the Parc 55 (they are across the street from each other).

Lately there have also been a ton of articles about tech companies moving out of SF (mostly to Texas but also Las Vegas, Colorado, Florida, etc.). Many of these companies also blame crime but I think we all know it is about paying less taxes and less regulation. Would be great to get an article on this as well!

Elmo moved Tesla’s engineering headquarters from Texas to the old HP headquarters in Palo Alto.

I guess he was willing to put up with the taxes and regulations after all.

Tech companies left because it was too expensive in SF, office and residential, and because they hoped to escape CA income tax (only to be eaten up by TX property taxes). Good riddance. Some companies moved out of SF, but the startups among them are now running out of money, like lots of start-ups. Like I said, good riddance. You have no idea how congested this area is. About 80,000 people have left SF due to working from home, and moved to cheaper places. And yet, it’s still way too congested here, and too expensive.

And now there’s news that some of them are coming back, which should be illegal, LOL

In terms of events coming back, for example, at the Moscone Center:

Data + AI summit” June 26-30

Design Automation Conference July 9- 13

Semicon West July 11-13

Lift San Francisco August 2-4

Dash: August 2-4

ACS Fall: August 13-17

Google Cloud Next: Aug 29-31.

You can look this stuff up.

It’s a beautiful, timeless city — the fact that it’s rougher than it was 15 years ago is just readily perceptible. But I suspect it’s just going through an inevitable trough in the the ceaseless sine of evolution. We shall see.

Downtown Tulsa, meanwhile, was never not a little depressing, in my opinion…but I like Tulsa.

“the ceaseless sine of evolution. We shall see”

Yeah, but it might be a 1970’s NYC sine…

I liked Times Square when it was good and sleazy….all yuppie now…no character.

Wolf your references to Park Hotels stock prices dropping are accurate. There was a pandemic capital raise that diluted existing stock holders. There was a high interest rate relvolving line of credit which raised borrowing costs.

These costly moves were related to having 30,000 rooms in various stages of empty. Please fact check the following. Park Hotels paid all of their property related taxes to the city of SF. Management indicated that employees were retained and paid. I can not find where any vendors or utilities bills were deficient in SF.

I totally believe your point that the two hotels need remodeling. This could by why they have poor occupancy. You indicated that the city had a 59 percent occupancy rate. That rate of occupancy will not cover the costs of operating a hotel let alone remodel.

You could be right that hotel management is poor. This could be a win-win. SF will get new owners that have very deep pockets, or the city could repurpose the hotel.

Las Vegas is a true hellhole, full of porn stars, gamblers and other degenerates.

The conventions moved so that business travelers can cheat on their spouses, visit whorehouses legally, and go to Vegas strip clubs.

Truer words have never been spoken

I went to Fran’s Star Ranch 5 man scrambles for 4 days in1977. (mixed speed stars) !st place team got free 24 hr boogie at Fran’s.

MANY protests, but an absolute blast for all. Adrian crashed Yolo Beech on take off (hangover drunk). It is still there and sort of a monument now.

Truer words have never been spoken. Google it.

Beatty, NV.

And this is different from SF how?

SF got its start as a sailor’s paradise (ahem) and never really, really moved terribly far aware from that pretty randy, fairly seedy origin.

(“the Barbary Coast”)

That, in point of fact, was the seed of SF’s self-proclaimed “tolerance” and “progressiveness”.

The historically inclined progressives point this out rather proudly.

cas – I’m sure there were sailors during the ‘California Banknote’ (tallow and hides) days, but thought SF’s REAL sailor ‘start’ came with the original ‘gold bugs’…

may we all find a better day.

You bet Cas! SF WAS a very STRONG union town!

And this will be difficult for you to grasp, but as long as a worker bee has a livable wage package and a steward to go to if the boss had a bad day and wants to kick (or worse, put at bodily risk) worker butt, he doesn’t give a damn if the skim goes to the mob or the country club.

In fact he probably prefers the former.

No. Conventions are moving to Vegas because of their plethora of hotel rooms. Other than CES, there isn’t a convention around that could even come close to filling up the hotel rooms in the city.

A few years ago, Jacksonville hosted a Super Bowl. They brought in a bunch of cruise ships to dock for the week to expand the number of rooms available in the city. In a couple of years Vegas is going to host a Super Bowl. The city won’t even blink. There will be plenty of hotel rooms available. There will still be other stuff (conventions) going on that weekend.

The Super Bowl overwhelms most cities where it is held. In Vegas it is just one of many big events that are held throughout the year. It likely won’t even be among the top 3 biggest draws to the city (CES is bigger, F1 will be bigger, NYE is bigger).

One of the biggest areas of growth in Vegas the past decade has been hosting sporting events. From cheerleading, to soccer, to baseball/softball, Vegas hosts many national competitions. Many of these are at the high school level.

High school competitions are not coming to Vegas for gambling, drinking, drugs, or sex. They are coming because there are lots of hotel rooms and cheap flights. Besides, parents are more likely to attend their kids national competition if it is held in Vegas rather than a place like Nashville.

Don’t get me wrong, Vegas doesn’t hide its Darkseid, it flaunts it. There is no city in the world where it is easier to find trouble, whether it is financial trouble, addiction trouble, or whatever other trouble there is, but there is another side to Vegas as well.

Great food (biggest collection of great restaurants anywhere), a larger selection of shows than anywhere else, etc.

Yes, there is gambling, prostitution, and drugs but there is more than that.

“Nobody ever grew despondent looking for trouble”

-Kin Hubbard

After reading this article several times, I am confident that it was written by Wolf and not by some AI Wolf-bot. The style is unmistakable. Thanks for writing the old-fashioned way (by that, I mean human fingers typing on a computer).

One week ago, on Monday, 5 June 2023, from Tysons, Virginia, the good folks at Park Hotels & Resorts Inc. issued a press release.

“This past week we made the very difficult, but necessary decision to stop debt service payments on our San Francisco CMBS loan,” commented Thomas J. Baltimore, Jr., Chairman and Chief Executive Officer at Park.

“For further information, please review Park’s most recent investor deck on our website, which includes the illustrative impact on certain operating metrics when both hotels are removed from its portfolio. Also included in the deck is Park’s full-year guidance that was originally provided by the Company on May 1, 2023. That guidance does not take into account financial impacts, if any, from cessation of payment toward the San Francisco CMBS Loan as any such impacts are uncertain at this time.”

Today, Wolf Richter, CEO of WOLFSTREET Corp., Media Empire, cut through the bullshit and explained the real story as to what has transpired.

“Park Hotels has been a catastrophic nightmare for retail investors,” Mr. Richter reported. He further added, “The shares have collapsed by 54% since the IPO in January 2017, and by 59.5% from the peak in September 2018 …”

This Wolf Street reader’s favorite part of the real story is where Park paid out a quarterly dividend of one whole penny for three quarters in a row starting in 2020. Nice job there, Junior.

As always, thank you Wolf.

The criminal activity in our streets is a byproduct of the criminal activities in boardrooms.

Outside observer? You seem to have a political ax to grind yourself. The problems of homelessness and drug and alcohol abuse are the hallmarks of American society. There is probably no state which embraces your brand of politics as much as West Virginia and believe me, it is a bigger disaster than SF could ever hope to be!

There’s a crime alright, but the WSJ is as usual clueless on the identity of the actual perpetrators. Here’s a clue: 101 Market Street, San Francisco CA 94105.

Thank you for the article. These world of Finance is fascinating and fun; the sciences have nothing on the joy of business school.

Following this twists and turns of money is like watching a 3 (three) dimensional version of the three shell game, guessing under what shell the money is. Only in this game they took the money years ago.

I am going to reread this several times, maybe even draw a flowchart of the finance.

Seriously, is there a professional textbook, or reference work, of smaller Real Estate techniques. Serious about that, it can’t all be OJT (on the job training).

There aren’t any “techniques”. There is math. Research material, equipment and labor costs for delayed maintenance. Research what maintenance is and it’s costs. Account for skilled and unskilled worker shortages in expensive areas.

That is the deep secret that all gurus leave out the details on. Don’t be afraid to “loose out” on any particularly horrible investment.

And fraud. Don’t forget that part. Lots and lots of fraud. Indeed, that’s what the bosses specialize in and earns them the big bucks. The math is outsourced to mid-level Asian math majors (cf The Big Short)

Maybe this is fraud, maybe it isn’t, but my biggest issue with Wall Street is the “heads I win, tails you lose” culture.

So many Wall Street people are willing to take huge risks with other people’s money (or with knowledge that they would get bailed out if they end up wrong). So if they get lucky and are right, they get obscenely rich. If they are wrong, they either get bailed out, or they close up shop and go somewhere else where they can make another risky bet.

Don’t get me wrong, I am a capitalist through and through. I want to see someone who is willing to put their money on the line be rewarded when they are right (I have done it myself).

I just hate the concept of someone getting obscenely rich by gambling with when they are not really gambling.

I was talking about walking into a house and looking at it. Not algorithmic buying. That seems to have slowed down, probably because they are losing real money on it.

Oh my. You’re gonna get keelhauled.

Thanks Wolf! SF is a grand city, maybe a bit tatty at the edges right now, but if she can survive 1906, she’ll survive this too.

Hi Wolf and readers,Can these older office towers be converted to condos? Is there not an opportunity here?

No, and no.

Hi Joe,

SoCalBeachDude thinks he’s being funny, and he’s coming off as a jerk. The reason he said that is because this has come up a lot. Unfortunately, it is very expensive to convert office buildings to condos. Wolf has stated that it is often easier to tear down the building and rebuild a condo from ground up.

I would think the main things are plumbing and running more electrical. Plus the fact that any large company is going to pay through the nose to get anything done.

In contrast, an owner/contractor could probably get it done and make a good profit as long as the structure has been maintained and is in good shape.

San Fran, or Frisco as many of us call it in beautiful Los Angeles, has always been a tatty ratty little town going back to the gold rush days when it was loaded with hooligans and thugs and the typical never-ending foggy that reminds one of the worst of London. My parents took one look at it when they came to California in the late 1940s and said, “who in their right mind would even considering living there? By the 1960s, Frisco has gotten even rattier and had districts like Height-Ashbury and the Tenderloin and then it declined even further into the filthy swamp it is today. Much of it is built on the wreckage of old ships and garbage tossed into the bay which is why buildings are leaning over worse than the tower of Pisa with the most notable being the aptly named Millennial Building which is now closer than ever to falling west into the bay all on its own.

Frisco, TX?

Out of the blue one day my Mother asked me if I’d ever call her a whore. “Absolutely not, Mom!,” I immediately replied. She quickly responded, “Then don’t call it Frisco.” Day’m, and I was born in the old Children’s Hospital and already knew that.

I think this abortive joke was fashioned by an AI.

And yours?

hahaha! Nice

Should I tell LA-man that everyone up here has been relieving themselves (both ends) in that that canal since they built it?

Well, your parents, and by extension – you, would have done quite well, if they had settled into one or three Height-Ashbury Victorians back in the 1940s. You would have been a multi millionaire today. Think about all you could have done with that money!

But some will say that things like credibility are much more important in life than money. Yours went right out the window when you implied London has better weather than San Francisco. Enjoy the air in the basin!

Only bad script writers call it Frisco

…or call the Haight the ‘Height’…

may we all find a better day.

And only Bogart can say it right, anyway.

Wolf, maybe you should recuse yourself on criticisms of your home town, just like you do on politics and religion.

There’s an awful lot of anecdotal evidence that big city crime is changing the landscape. Are CEOs and journalists exaggerating it to suit their own agendas? Of course. That doesn’t mean we can dismiss it all as “BS”.

Harrold,

You’re promoting effing clickbait. You have no effing clue. Go read ZH and get your lies about SF there.

Wolf, is your angry mode shtick, or real?

Only a fool makes generalizations out of anecdotal evidence. Especially when real statistics show that crime is not all that bad compared to historical norms.

I think you need to get better sources of information. The ones you currently use are taking advantage of you.

Harrold,

PLEASE explain why ANY human being should recuse themselves on ANY discussion of Religion?

Do we not all exist in the SAME mysterious universe and at the SAME time?

Wolf 1. Wall Street Journal 0. In the modern age, it seems to be all about the headline. Speaking for myself, I enjoy your analysis. Especially the not-so-veiled sarcasm that AI has yet to mimic.

The nearby Westin St. Francis Hotel is seeking a 90% reduction in its assessed valuation. Also, we learned later in the day that Westfield is walking away from its mortgage on the San Francisco Centre.

Two things can be true at once: (1) commercial real estate is struggling nationwide, and (2) downtown SF is underperforming.

Westfield walked away from two malls in Tampa Bay in Florida in late 2020, it walked away from other malls, it finally walked away from the mall in SF. It announced in 2021 that it would dump ALL its Westfield malls in the US. I told you that in an email.

Article coming. I’m tired of this BS about San Francisco.

The journal ceased to be trustworthy when Murdoch purchased it. I cancelled my subscription shortly thereafter and have not resubscribed since.

Methinks thou dost protest too much. I sometimes wonder what Herb Caen would say about “Don’t call it Frisco” today.

1) SF Park hotel is hell, but the FAANG approach Nov 2021 top.

2) This week QQQ might close Apr 5/6 2022 gap, retracing about 75% of the move from Nov 2021 peak to Oct 2022 bottom. Thereafter QQQ might drop to the 290/300 area, lifting the VIX, before rising a new all time high for funfunfun.

3) The 2024 “corrections” might take QQQ down. US gov will use all it’s dry powder to lift QQQ and AI back up.

4) Comatose China might slowly wake up in late 2024/2025. US and China might lift the global economy in a more conservative pace, using less debt.

“Get rid of your opium and your missionaries, and you will be welcome here.”

-Chinese diplomatic message during the “Boxer Wars”

Taken from Mark Twain’s, “For those living in darkness” (IIRC)

I used to live in the Bay Area too, and have nothing but the best memories of the place. So with that disclaimer, I can understand where a lot of the sentiments are coming from.

In 2016 my company (in Shanghai) consulted on a large property buy for a China State-Owned Enterprise. The SOE had basically a blank check, credit lines totaling over a billion dollars. They were looking to invest it all in CME, and had guaranteed subleases (at the time) to WeWork, of all people.

My group had to do a deep dive on WeW, which was almost completely unfamiliar to us at the time, and also comps on other projects around the country. The key question was, if anything happened to the WeWork- or the Regus-style companies, what would happen to their underlying investments?

And SF and LA came in at the bottom, of what their investments would be worth if WeW walked away. We wrote a solid report, highlighting instead the far better options of Denver, Miami, Orlando, Atlanta, Charlotte, and Houston. The purchase price was simply too high, then the maintenance costs and taxes and insurance, to ever get the money back. We had no clue how WeW could pull it off, either.

They bought anyway, two stand-alone buildings in each city, and then We imploded, and now are being shopped to investor companies, also here in China.

None of the analysis had anything to do with crime, or the loss of convention business, or the political currents of the city, and also was pre-pandemic. The problem was the buy-in prices, which were ridiculous, along with the expectations that you could charge people above-market rents for smaller “shared” offices but with free coffee and granola. And I would agree that while this was a symptom of the free-money problems caused at the Fed, it’s also the culture of the Bay Area, where investors are just expected to keep ponying up more and more cash for “young talent”, quotation marks mine.

Yours Truly spent four years in a Tucson coworking space. While it wasn’t part of the WeWork empire, it sure did try to emulate it.

Place went out of business in June 2019.

In addition to the above-market rents for shoe box fishbowl-style offices and flimsy Ikea desks in open space that were supposed to foster collaboration, the coworking business model is a difficult one to make money in.

That free coffee and beer cost money, as does the marketing to keep putting posteriors into those flimsy Ikea seats. This marketing is an ongoing thing, because the owners of those posteriors are quite adept at finding better deals elsewhere.

So, in the face of constant turnover, you really have to keep your foot on the marketing gas pedal. The place I was in stopped doing that in 2018, and the high turnover problem turned into a vacancy problem that was never solved.

Too bad we couldn’t have met earlier. Your at-the-scene reporting would have saved our clients 200 mil. Cheers brother.

My goodness. Hit the pause button on the San Francisco bashing. Either that or go slug it out in the Dodger Stadium parking lot.

I’d imagine the reporter who got stuck writing this hit piece has an overloaded inbox with lovely compliments. She does have an editor, and the editor a…? However the hierarchy goes. So it might not be fair to put 100% of the soul crushing on her. Who knows?

Ultimately, the WSJ put their brand on it so who are they serving here? Ok, News Corp.

Regarding buyers – Vanguard, Blackrock, and State Street already own everything. So….maybe Goldman? Are Goldman and News Corp mixing it up?

Hmmm. What’s the focus here?

If it’s bad business practices or poor decision-making by Park Hotels that’s one thing.

If its Tulsa vice San Francisco – who cares? Not the only options. Don’t care whether WSJ cherry-picks or not.

If its WFH impacts – ok.

If its crime data, it gets interesting. FBI changed its data collection and reporting practices in 2021. Several major state’s city police departments, including many in CA and NY, are now refusing to submit data or only submit partial data. Sound like a familiar pattern? Crime, of course, is a genus-like term that has many “species”. Crimes of violence? Or property crimes? Gangs increasing or decreasing? Car theft up or down? What do crime surveys of local citizenry reveal? Is crime city-wide or localized?

If it’s population patterns – two things are certain: birth rates in CA have been falling and the state has one of the largest net population declines of any state in the last several years. Internally, there has also been net positive migration from coastal cities to more easterly CA counties.

Are there multiple factors in play influencing commercial and private occupancy rates in San Francisco? What are the dominant trends? Should Covid-related impacts be discounted?

Secondary thought: I have lived in San Francisco area, Tokyo burbs, San Diego and Paris (FR).

Comparing these cities is apples and blueberries.

“Park Hotel defaults on a mortgage and walks away from the property, it means ownership of the property will change. That’s all it means for the hotel.”

—————————————-

Doesn’t a foreclosure, and a new owner void the lease? Isn’t the hotel off the hook and able to renegotiate or walk? By the same token, can’t the new owner evict?

Please consider an article on San Francisco and actual crime and homelessness, and its impact. Nordstrom claims it left because of crime. So does Walgreen’s.

i visit San Francisco, Los Angeles and Orange County,CA, The homelessness seems worse in LA and just as bad in parts Orange County.

Retail is in trouble, REITs are in trouble and CMBS is in trouble. They could bring banks and pension funds down with them.

Listen to Wolf! He is warning us that vulnerabilities everywhere, not just San Francisco.

The Journal has fallen apart in integrity since the Murdoch kids took over and pivoted left. Now a wolf in sheep’s clothing they bleat about every left fantasy like ukraine victory and global warming starting 400 coinciding forest fires daily.

…live in fire country, do we?

may we all find a better day.

It’s real neat whenever things fit perfectly into that high-contrast manichean framework making our hatreds easier to hold in our hearts

WSJ still doesn’t have “Babe of the Day” (or whatever she is called in London)….I thought that was a Murdoch trademark?

“So, JPMorgan sliced and diced the mortgage and securitized it into CMBS, to where the top-rated slices were well into investment grade. The slices were sold to bond mutual funds, pension funds, etc., that manage other people’s money.”

Sounds exactly like what happened in the home mortgage market in 2008. Back then they took tranches of mortgages, securitized them into investment grade products and sold them to unsuspecting investors.

Satisfying peek at the gutter that runs all along Wall Street. Everyone who’s anyone knows about it but none of them want to see it kept swept clean. They all need it from time to time.

Be good to see more of this from time to time, if you can manage it without getting sucked into the gutter yourself. This is the kind of warning that wakes up the average investor, adds needed color to all the stats about bankruptcies starting to arrive.

We are getting more news about SFO here in Swampland than local news. This has become an obsession. I can’t understand this. SFO is 3,000 miles away. Why is this going on? Maybe it is because some of the things that happen there seem to arrive here with a delay of 6 to 12 months like clockwork?

Swamp – kinda like ‘…oh! Look over there, squirrel!…’.

may we all find a better day.

Oh man, that is some really OLD playground stuff!

But seriously, I watched the exact same smash and grab at Walgreens on at least 5 different days on Fox News 2 SF, and Swamp even saw it in DC and mentioned it here back then. Maybe several times…..?

Well Mr. Wolf, don’t let it bother you. This stuff is like having relatives / inlaws. Let them think what they want, nothing will change their minds or attitudes. I took great comfort watching heads explode over decisions the wife and I made. We could not be happier with our choices. Will keep clicking here looking for your updates……..

So I really want to know who owns the CMBS that is the equivalent of a flaming bag of doo-doo.

Could some of it have been sprinkled in PIMCO and Vanguard bond funds, kind of like sprinkling a little bit of cat shit in thousands of boxes of cornflakes?

Maybe some “safe” bond funds start to break the buck.

This time I recommend using South Park’s “headless chicken” method, which seems much more fair than last time’s “method”.

While trashing SF has become all too easy of late, can we really rule out the fall in travel to SF as the reason for this specific default? From what I can tell, SF is still about 16% below 2019 in terms of visitors, despite the recent recovery.

From my limited experience on the management side of the hotel industry (I sat as the proxy for my family’s interests on the board of a NYC hotel which used to own the fee on the land and building but leased it to a hotel operator–if you’re Sherlock, you can guess which hotel), hotel building leases have a fixed component and a variable component. The variable component is based on gross revenue.

In our particular case, the variable “percentage rent” component was usually greater than the fixed component, except for a few years during the global financial crisis, when it was zero. As I recall, the formula was zero below a given threshold, and 3% above that. The threshold increased every year, thus constantly raising the bar.

If the SF hotel has a similar rent contract, Park Hotels may be cash flow negative with little hope of catching up, as both occupancy and rates would need to skyrocket to get back on track to consistently exceed the ever-increasing percentage rent threshold.

A non-recourse clause in a mortgage is akin to a put option, which Park Hotels was within their rights to exercise.

Ahhhh…..Wolf! You have hit an Amerikaner nerve! Don’t you know, “blue” territories of the empire are not allowed to have pride, not allowed to have a loyal identity….because in Amerikaner thinking……no one really “comes from” the blue cities. “They’re all from somewhere else” it appears.

Could you imagine WSJ talking this way about “Cancer Alley in Texas” or other crappy parts of red states? THere would be a kinetic “reaction”.

Could you imagine Switzerland cheering the destruction of Zurich? Germany trashing Berlin?

Murica sure is a funny place. Knighthood for Rupert Murdoch! All hail!

Kiers – I like the way you observe!

may we all find a better day.

I’m german, born in 1969 and yes; I can imagine Germany trashing Berlin und we do so.

After WWII Berlin lost all of its industries and Bavaria(Munich) convinced them to come there.

So there was West-Berlin totally dependent of subsidies from (West)Germany and it was ok to show the East that (West)Berlin was rich and colourful.

Eastern Germany did the same with East Berlin. Shwoing the West that Eastern Germany was fine.

After Reunification there was a big city with low production and several generations of entitlements. Definitely an interesting city at that time.

On top of that there as no conscription in West-Berlin so it attracted people who valued that a lot.

Mainly the german South (Bavaria, Hessen, Baden Württemberg) is still asking from time to time for Berlin to give less ‘information’ and ‘teaching’ to the rest of the world. And they ask for when will Berlin finally be able not to rely on subsidies anymore because ‘Länderfinanzausgleich’ means that well-doing federal states have to give a share of their riches to the poorer states.

So you have different opinions on Berlin inside of Germany ranging from Life-is-so-easy-let’s-invite-everybody-and-demand-more-free-stuff to how-easy-my-life-could-be-if-just-someone-would-build-a-wall-around-all-of-Berlin

Wolf-

I feel your pain.

Signed,

A Chicago resident (former, but still love the city)

Fact is, at any given time, the MSM and right wing media (one and the same) have it out for a specific city, and will nonstop bash it regardless of truth. Chicago took it for about 10 years due to the crime of being Obama’s hometown.

Since Biden doesn’t have a big hometown to speak of, Gavin Newsom will have to do since he’s been the most prominent Democrat sticking a finger in the eye of precious Trump and DeSantis and other right wing darlings. So you folks will just have to do your time in the penalty box…

The Chicago bashing has nothing to do with Obama continues unabated because the city is in obvious trouble to anyone who travels there and is not afraid of facts. Crime is way up and people are moving out, the Mag Mile has more empty store fronts than ever before, and they elected a moron for mayor who doesn’t think staffing the police department is a priority. I love Chicago, it’s one of my favorite cities, but it is in real trouble, and the media if anything are understating the financial crisis the city is facing.

“Westfield said in its state-ment that the 35% drop in total sales at San Francisco Centre—from $455 million in 2019 to $298 million in 2022—is counter to sales increases across the rest of its U.S. portfolio.”

“ Foot traffic over that time fell 43% at the San Francisco mall, amid a recovery to near 2019 numbers at its U.S. properties overall.”

So much for the argument that this is happening everywhere.

Ridiculous BS. Westfield walked away or sold a dozen of malls before SF.

Westfield started by walking away from two malls in right-winger Florida in early 2021 (Tampa Bay). It was in the title even. Their sales in right-winger Tampa Bay malls are down 100% LOL. And now blame SF? Does your brain not work at all?

Westfield announced in 2021 that it is WALKING AWAY FROM OR SELLING ALL OF THEIR MALLS. First paragraph:

“Back in February 2021, we reported that Unibail-Rodamco-Westfield (URW), the largest property REIT in Europe, had announced that it would dump all its 27 Westfield malls in the US, of which 16 were in California, including the Westfield San Francisco Center.”

WHY IS IS SO HARD TO GET?