Debacle on the Inflation Front: The Fed’s victory lap about having licked rent inflation was premature.

By Wolf Richter for WOLF STREET.

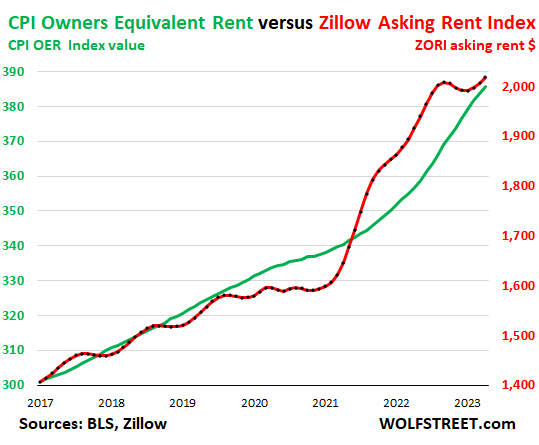

The Zillow Observed Rent Index (ZORI), which is based on asking rents, meaning advertised rents that landlords hope to get when a tenant signs the lease, jumped month-to-month by 0.6% in April, the steepest increase since August, after having already jumped 0.5% in March, and 0.3% in February, to a new record of $2,018. Annualized, the increase in April translates into a jump of +7.4%.

This is really bad news on the inflation front. But it’s not a surprise. It confirms what the biggest landlords in the US told us in their earnings calls, that they got 6% to 8% rent increases both on lease renewals and on new lease signings in April; and it confirms what the rent factors in CPI for April told us, that actual rents paid by all tenants jumped by 0.5% in April from March, and by over 8% year-over-year.

You can see how the ZORI (red, right axis, $) undershot actual rents during the pandemic as depicted by the largest rent factor in CPI (OER, green, index value, left axis), and how it overshot actual rents in 2022, and how it then dipped at the end of 2022 and early 2023, and how it has reaccelerated over the past three months:

Rent accounts for one-third of the Consumer Price Index, split across two rent factors. The CPI for Owners Equivalent of Rent (OER, the larger of the two, accounting for 25.4% of total CPI) jumped by 0.5% in April and by 8.1% year-over-year.

All these measures – asking rents as per ZORI; earnings calls from the biggest landlords in the country; and actual rents for all tenants as tracked by the CPI rent factors – are now showing that rent inflation in April was not slowing down at all, but re-accelerated.

The ZORI was much cited as proof that rent inflation was slowing down and would soon vanish based on the ZORI last year when it actually fell.

For the Fed, for Powell during the press conferences, and for many others, the dropping asking rents last year was the gospel that they had been waiting for, that inflation in actual rents, as experienced by current tenants, would soon abate as the asking rents would become actual rents and lower those actual rents, but that it just hasn’t done so yet because, you know, the CPI rent factors are lagging, etc. etc.

But that didn’t happen.

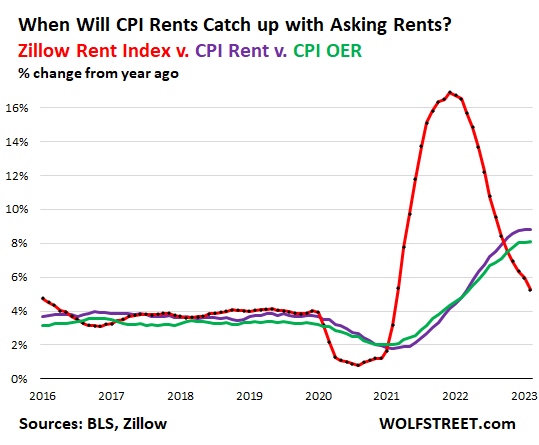

The year-over-year percentage-change mind-bender.

What may have also misled the good folks about rent inflation were the year-over-year changes. As you can see in the chart above, the ZORI undershot actual rent increases in 2020 and early 2021, and then off that low base, showed a massive year-over-year percentage gain in 2022, that caused it to overshoot in 2022.

But that huge percentage gain never made it into actual rents because it was off the undershoot, it just averaged out the undershoot on top of the regular rent inflation of 8%. And now the asking rents per ZORI are back in line on a month-to-month basis with the CPI measures.

This is the type of year-over-year percentage change chart that caused a lot of brains to short-circuit about rent inflation, showing the undershoot in 2020 and early 2021, and off that low base the massive overshoot in late 2021 and nearly all of 2022. This chart also shows the CPI rent factors as year-over-year percentage change.

The Fed’s victory lap.

The Fed divided the core inflation index (without the volatile food and energy products) into three groups: core goods, housing inflation, and core services without housing.

Inflation in core goods has come down a lot from the pandemic highs. Housing inflation measures (such as the CPI rent factors) would also certainly come down because this was already baked in, they said, based on asking rents dropping, and because the CPI rent factors are lagging, they said months ago. So the rent-part of inflation, they said, was already licked. And the only part left where inflation was super-sticky was core services inflation without housing.

So now it turns out, inflation remains nastily sticky in two of the three parts, and the Fed’s victory lap on having licked rent inflation appears to have been premature.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Fed needs to do a .5 hike in June and another in july if theyre going to walk the walk.

At my local market this weekend egg prices seem to have come down as well as romaine lettuce but heaven help you if you want cauliflower. Might have to do one of those buy now pay later deals, lol.

Fed thinks inflation is dying and already declared victory surreptitiously .

Fed already paused and there won’t be any more, forget about 50bpps hike.s

Fed doesn’t care about 99%.

What’s so baffling about recent Fed policy is their incredible meekness and timidity about aggressive QT, in general and compared to other central banks even the Bank of Canada. Of all the anti-inflationary moves, this is the easiest call and most effective with least downside, best focus on the crypto and asset bubble speculator class with less damage to the 99%. Interest rate rises constantly cause all this hand wringing about side effects on the majority of Americans, and while Powell is no Paul Volcker, he has raised interest rates more aggressively than the useless Bernanke or Greenspan (leave alone Arthur Burns) ever did. But quantitative tightening would be an even easier and more effective tool to choke off this inflation, esp by going big and selling off more MBS’s. Much cleaner, much more targeted attack on these inflationary pressures to reverse the COVID over-stimulus effects, and even once otherwise timid central banks elsewhere are going hard on QT, even Canada which has basically gutted the rest of it’s economy in favor of running a permanent housing bubble. So why has JPow been so feckless here?

This is where I wonder if you and Depth Charge may be right about this as far as the Fed having forgotten who they truly serve, it just makes absolutely no sense why’d they fail so hard on QT. The only beneficiaries of the pathetic QT policy are a few thousand big speculators including the corps like Blackstone and Blackrock buying up US housing wherever they can and over-charging rents. If so, this is a historically catastrophic mistake by the JPow Fed, because it’s no longer just their call or even just the American people, who are already being squeezed and crushed by this ongoing inflation esp with rents–a lot of the recent crime and unrest in the United States is no doubt connected to the stress of inflation, and the writers strike in LA is also a direct result of it.

But now on top, the rest of the world is ditching the dollar at unexpected speed, even Bloomberg just had a shocked article about how fast de-dollarization is happening as of May 2023 esp in Asia (even the Philippines now refusing the dollar and demanding payments in their own currency) and it’s no mystery as to why–a “reserve currency” isn’t worth the name if it 1) doesn’t store value effectively and 2) the institutions in charge of it make only half-hearted efforts to squash it’s devaluation from inflation. It’s not some grand geo-political chessboard or weaponization of the currency or anything like that–other countries are fast losing patience with the US dollar when it’s clear US officials are too timid to defend its value, and they can’t reliably store value in it anymore, not to mention USD inflation gets exported to other countries that use it, pouring oil on their own inflationary fires which threatens social unrest and their own stability. So they’re dropping the dollar like a stone as an acceptable medium of transaction. Not rocket science here, another confirmation of Volcker’s rule that sound money is one of the pillar’s of a country’s strength, something the Fed has dangerously ignored since Greenspan.

Jerome Powell doesn’t have a long window or much wiggle room to stop the bleeding from dollar-dumping here, talking here about months and not years. This thing feeds on itself once it gets going, on top of the fact that Americans are getting angrier and social unrest gets worse when rents, healthcare and other basic services get more and more unaffordable. He really has a binary choice here with QT, he can either keep up this timid QT policy and help his insider billionaire speculator buddies at places like Blackstone make even more money off the backs of the already suffering American masses, or he can ramp up QT to save the US dollar and preserve some measure of American geopolitical power. He cannot do both. Like our prof constantly repeated, failure to control inflation has brought down far more great powers and major empires than any war ever has, and right now JPow is at a crossroads of history here. The rest of the world is not going to tolerate a depreciating dollar with meek policy response much longer, and if Powell fails to ramp up QT a lot more aggressively than he has, he’ll go down in history forever as the official who finally broke the dollar and delivered a permanent blow to the place of the US in the world. Volcker would have risen to the occasion, we’ll see what his successor does.

Sorry, Miller.

TL;DR.

Way, way, way, way too long.

“fed already paused”

Lol, no.

The FED has zero credibility. Never in a million years would they raise by half a point in June. They are desperate to pause. Everybody knows it. They want to make this inflation stick. It’s intentional. These evil, disgusting pigmen have taken over the economy and destroyed pricing to benefit themselves and their rich buddies.

You speak of the grocery store. Two trips ago I saw a young woman quietly crying as she was shopping. She was trying to hide her face. She was not on the phone. She had a hand basket with very little in it as she was browsing. I believe it’s the prices. This is what the FED has done.

MW: Fed’s Bullard backs two more interest-rate hikes

The FED can do whatever they like… 25% or .5% or 1.0%.

Until they get aggressive enough to push the entire economy into a deep recession (not likely) or until we have some unforeseen event that crashes the economy (more likely), rents and real estate prices are NOT going down and inflation isn’t going down either. There’s simply too much money chasing a reduced amount of goods and services.

How many extra trillions are out there sloshing around? Who knows. Think 10 years of IPO’s, SPAC’s, Cryptos, Overpaid Social Media Influencers, Overinflated Stocks, Bonds and Real Estate.

I’ll tell you who knows – anyone selling goods and services knows. They figured out the meaning of price inelasticity, so they’re charging way more than pre Covid for everything … and getting it. They’re making higher profits on lower sales and making up for not having raised prices from 2008 – 2019.

#CCCB

There is some possible troublesome outcomes of a deep recession or economic crash that may negate any deflation that follow.

The purchasing poweer may follow the prices down or even go down faster. Nothing get more affordable that way.

Another possibility is that after bankruptcies and following fire sales production capacity have been cut too. Afterwards prices may be lower as few have the purchasing power to afford much. And those that can afford have little to choose from as supply have diminished.

QE, low interest rates and so on we where told was to pull demand forward. Anything pushing demand into the future is then a problem in an economy based growing consumption.

Everyday I realize my money is buying less and less. It’s pretty disturbing, and I make decent money. There are a lot of people making less, feeling worse. But, maybe they have a house with a low mortgage payment. Maybe they aren’t effed in perpetual rent increase hell.

People who own are also seeing their monthly costs go up. Not including repairs or maintenance.

The FED raised rates 5 full percent in 14 months. Did you predict that at the time? Have you ever taken this new fact into account?

What did the 5% rate hike achieve? NOTHING!

1. Inflation remains intolerably high.

2. Debt is all time high.

3. Bitcoin crap rallied >50% showing the level of speculation and liquidity.

4. Banks were Baile ld out with taxpayer money and JPM was awarded the prize and made a hero.

……

The list of idiocracy is just too long

Leo

Yes, but inflation fell from about 10 to about 6 percent, property deals collapsed, and prices plummeted from their peak.

Better than if the Fed rates stayed at 0.25, right?

N. B

Bitcoin was 60k USD, now 27k

You hound have offered to help her pay for groceries,if you have the ability to do so . Might have hungry kids at home. We need to become compassionate people again

Or she found a great way to fish for handouts to support her drug or alcohol addiction lifestyle? Not that I have a major problem with that.

I considered it, Flea, but it would have been a very awkward intrusion. I regret not saying “are you ok, can I help you with something?” I mind my own business.

I agree with Flea on this one. I used to wonder how money I hand out is used, but now I just think if it makes today a little easier for the person, that’s enough. Life’s too short to worry about everything being a scam when it’s clear so many people need help. I certainly don’t fault Depth Charge not intervening here, because she wasn’t asking for help so it’s impossible to know what was really upsetting her.

I don’t blame you DC, it’s very awkward.. I’d encourage people to buy things occasionally and bring them to the local food banks. Ask them what they need first.. Better to give quality food than money sometimes..

From what I’ve seen people bring home from the food banks this past year, some of that stuff is barely edible. My neighbors (who just lost their place) were cooking the worst of it up and feeding their dog. And yes, I have shared my food with them occasionally.

For a while a few friends and I were getting construction bags of old bread from the factory and handing it out. We had to say it was for goats or pigs as it was past date (but still good). That is no longer available as it’s gone within an hour or so and we all live pretty far away from it. Hopefully some humans still get some of it. Even out of date most of it was still better than what people are getting at the food bank right now.

…somewhere the ghost of Mike Royko is nodding…

may we all find a better day.

DC, if you are going to play with narratives, ya gotta practice story structure, just end it with helping her and get more approval….I would guess…But I’m no writer like you are.

Flea….maCa?…are you are treading on socialist thin ice by mistake? Like 1950’s tax schedules and financial/union laws?

I think the blame goes further back and into wall st who has an outsized influence on the fed. Plus even those in govt with big portfolios get big donations. The fed is just the most noticeable and we need a person to blame. At the same time, as long as most keep paying up, vendors will seek the highest price they can get. Just look at HD. They had monster profits as they gouged us during the pandemic. And now they are starting to send out the 10% coupons once again. But they already put through a lot of 50% price increases that appear to have stuck. The populace needs to boycott all non-essentials to turn the tide. Mend our clothes, don’t waste food, drink less beer (Whaa?) and make moonshine ha. Sounds like the great depression.

“The populace needs to boycott all non-essentials to turn the tide.”

Totally agree, we have been seeing some encouraging signs of this the past few months. Even among many notorious Big Spenders we’ve known in Texas which has one of the worst, “sure we’re broke but just put it on the credit card!” wasteful spendthrift cultures in the country, that’s truly pushing a lot of this inflation. People are backing off from throwing money out the window paying for “the brand” and getting cheaper store brands, they’re buying cheaper things at discount at Aldi and the Latino shops where things go for half-price, they’re no longer so blase about throwing away food and holding onto leftovers. More people even growing food in their own gardens, using half a paper towel instead of wasting 2 or 3. Our own kids and nieces and nephews drove us up the wall with the stupid tendency to fad-purchase every new and outrageously expensive iPhone upgrade (often for lowering quality and faster obsolescence), now they’re getting cheaper phones that actually work better and don’t force you into another useless overpriced purchase the next year, either going Droid or pre-paid. And there’s even a lot more fix-it-yourself going on with everything from clothes to home repairs to cars now, and a lot less wasteful spending on ex. way over-priced Disneyworld tickets. This attitude absolutely needs to spread and get worked deeper into the culture.

I went to my favorite car wash the other day. Used to be $20 for a basic car wash. It’s now over $30. That’s a 50% inflation rate I think Wolf’s service inflation data which he gets from the government needs some updating.

Everybody knows the BLS is torturing the statistics to present a rosier picture than what is really transpiring. I have yet to find any product or service that has experienced inflation as low as the reported CPI.

I used to have a monthly subscription to a local car wash; recently cancelled that after it went up 50% and now I wash my own car.

The whole world has inflation. The world is bigger than just this country and this Fed.

Just choosing to post here, DC!

As I’ve been saying for more than a year, illegal immigration is going to wreak havoc on rent, food, education healthcare prices and all sorts of other things. JD Vance just spoke in front of a committee highlighting the need to look at this issue through an economic lens just as much as social, cultural, law enforcement, etc.

This is kind of like WR’s point about EVs starting to make a dent in gas sales. This is the exact same thing, except no one is going to talk about this political hot potato.

Get used to it, people.

IF you think illegal immigration is why rents are skyrocketing, I hope someone cuts your food for you. And Vance is a charlatan and a clown.

People from Appalachia like to blame their circumstances on someone other than themselves.

There isn’t much real difference in immigration between one party and the other, they each just put a different spin on it. They all like cheap labor and manufacturing a slave class.

While I partly agree with you, I think the whole south border immigration issue is pumped up to distract us from EB-5 and other more wealthy immigrants who fly in and buy up all of the US’s assets, basic necessities and resources on the open market. The wealthy immigrants do more damage to this country than all the others combined. That profit does not stay here, it gets sucked up into offshore accounts.

I always find it interesting to see the hammers people carry around looking for nails.

There are many problems in this country with illegal immigration, rent inflation is not one of them.

Consider using a screwdriver on occasion when it is more suitable.

“I always find it interesting to see the hammers people carry around looking for nails.”

Frankly, when it comes to this particular hammer, a lot of them aren’t even bothering to seek out the nail. Just swinging the hammer around more or less at random.

A huge nursing home closed in my community due to lack of staff. Most Americans do not want to do this type of work. Immigrants often fill the gaps. Or they used to.

She prob had just seen Top Gun Maverick. ;)

Yeah, I recently was behind an elderly woman in the grocery line. The clerk was taking items out of her order and setting them aside because she didn’t have enough to cover their cost. These were not luxury items, rather basic food items.

I asked (trying to be discrete) if my impression was correct. When told it was, I asked the clerk to add the items to my pile, and paid for them for her. I am also elderly and it hurts to see someone have to manage their lives in that way.

Thumbs up!

See, DC? Instant affirmation.

Lately I have seen people crying quietly in grocery stores too.

Have also seen more people unable to afford rent and being evicted.

Many states increased the allowance on food stamps during the pandemic and extended it until sometime this spring because of inflation surges. That’s gone now but the surges are still happening..

I don’t know where you live, but I flew from Phoenix Int’l. on Saturday to attend to some family business.

There was not ONE empty seat on that plane. The airport parking lot (I reserved a space and paid for it in advance) was absolutely full. The main airport garage had only 4 hour spaces available. The “economy” lot where I park – per their space counter – had a grand total of 42 spaces in the “A” garage. The “B” garage had cones in front of the entrance with a “full” sign blocking passage.

The young man next to me had two cocktails during the flight. Plus paid $8 for the internet access… $24 spent. Plus airfare. Plus parking. X’s 2.

The van service from the airport was at full capacity. 8 people returning from a cruise.

I was a doubter that there was that kind of spending going on, but no more. And it was all generations, not just geezers or youngsters.

On another note, my “grandson” called today asking if I could send money to him as he was in trouble. The only problem for him was….. I don’t have a grandson. Do people actually fall for that crap?

I’m not sure what your point is. The people crying in grocery stores are not the same population of people buying plane tickets.

My grocer will not let me put cauliflower on lay-away.

Did she get her cauliflower?

Do you now hate the Fed worse?

Will your insults therefore get better?

Pigmen? Gonna trademark that?

Powel is the most incompetent Fed chair ever! He said inflation is “transitory” 2 years ago while he was and still is printing $ and pumping money via keeping the interest rates near zero and via backdoor to prop up the stock market for his “Rich friends” of Wallstreet. He doesn’t care about Mainstreet. He and Janet Yellen should be fired rightway. They r still advocating low interest rate to help their Rich friends who borrow at zero interest rate and buy up all the Real Estates and Stocks!!!!!!!!!!!!!!!

Powell might be the most incompetent FED chair only if someone doesn’t know Alan Greenspan exists.

Nice screen name.

But to those who are convinced he is their Savior, they will just blame government for stopping him and continue to call for it all to be totally burnt down…..as it is the evil “swamp”.

It’s a “leap of faith” thing, and with all leaps of faith it’s for the “better”……how or why, nobody REALLY knows or cares.

Maybe it’s just leaping that’s fun? I can testify to that, but it’s hard to learn how….for real. But you do have total trust in the gear or you wouldn’t do it. What you worry about is your own behavior under stress.

TL;DR.

Corn, Wheat, soybeans, oats are down 50% from a year ago. But prices have not dropped. Commodity indexes. Bloomberg commodities index is back to November 2021 price.

I read food wholesalers are paying 40% to 50% less on some items than a year ago but the wholesalers have only lowered their prices by 10% .

It did not mention who the wholesalers are but i am guessing they will see nice profits this year

Don’t forget labor costs. They jumped. That’s the majority of the costs for most companies. Then there’s rent, vehicles, equipment, supplies, etc. all of which went up in price. That’s why food prices don’t move in proportion with commodities prices.

The interesting thing about rent is that you can’t charge more rent than someone willing to pay.

So for some reason people out there are willing and able to pay more for rent.

How and why I don’t know.

Libertarian,

Housing is one of the more price inelastic goods…people have to sleep *someplace* and they really, really don’t want to double up and living outdoors is almost inconceivable to most Americans.

So, if NYC/SF/etc landlords decide to play Russian roulette with rates (double digit increases for multiple years) renters will endure a *lot* of economic misery before dumping such metros.

(The unusual thing about the unusual rent spike of the last two years, is just how continent-wide it is…NYC/SF have always been rental madhouses, but this go-around has seen 80%+ of mkts soar simultaneously, which is very unusual. It may just be badly overlevered landlords desperately trying to claw back/exploit pandemic rent losses).

Hopefully the multi-decade high in apt units under construction will gut this rental madness.

EL – thats true of chemotherapy and heart medication too! Wonder why prices keep going up….

Rent a room.

Please…a couch will do.

Gotta hide the dog and it’s ___.

Can share the shed,

Cause it’s sublet subterfuge.

Merci beaucoup…Mr. Fed!

“The interesting thing about rent is that you can’t charge more rent than someone willing to pay”

What’s the alternative to paying rent if you need somewhere to live and can’t afford to buy?

“Then there’s rent, vehicles, equipment, supplies, etc. all of which went up in price…”

New vehicle prices are increasing $300+ per month. That’s a $3,600 increase in the new price over the course of a year. So, a person has the be able to pay an extra $300 every month forever just to keep up with the price of a new vehicle. On some of my equipment, the new models are increasing $600 per month. That’s what runaway inflation does.

The FED is a complete and total failure. They need to be eliminated. There is no redemption for the damage they have wrought over the past 3+ years. What should be happening is CONgress should be working on a new model to replace the FED, and Jerome Powell should be in handcuffs.

True. Their inputs prices are down but their operation costs are up a lot.

As you well know, it’s called sticky inflation for a reason. You can try to explain it away, but all sorts of price increases are now permanently higher.

Agree with DC,

Except for the 3 years part; to any rational observer, it should be crystal clear that HUGE damage to the 90% if not the 99% has been done for the entire 110 years or so of the existence of the banksters puppets known as the Federal Reserve Bank of USA.

Old Andrew Jackson had it exactly correct…

Probably waaaayyyy too late to fix this without some very very serious ”social” type actions.

Sometimes I am happy to be close to the end of this lifetime, SO sorry for the young and younger folks who will have to deal with the inevitable carnage of every kind SO clearly coming.

VintageVNvet,

Not too late to fix. Roll back any tax law that makes Single Family Residences attractive to investors. This would cause home prices to fall as investors unload the SFRs they are already hoarding, which would also push down rents, which would then push down the inelastic componet of the demand for wage increases. Pushing down rents in SFRs would implicitly push down rents in multifamily, which could keep all their tax breaks, because multifamily is commercial real estate. SFRs should have *never* been treated like commercial real estate in the tax code, which is the root of all current housing problems. PS As you phase out all the SFR tax breaks, tax revenue for government would increase, offsetting any potential loses from assessed value price drops, so this is tax revenue neutral, making it a no-brainer for government.

Good point. I’d wager that a lot of suppliers could reduce their prices right now and be fine, but inflation is sticking around because we are still willingly paying it. Home prices are still too high, food prices are still too high, and dealerships are still tacking on an extra $10k to that new Ford Bronco just for the inconveniences of unloading it on their lot.

Americans have always made stupid financial decisions in the name of having the best of the best, but I think it got much worse after covid. Social media flaunts it in our faces. Every other post I see is some guy reviewing the fanciest new thing and it really has accelerated our consumption of high end goods.

Companies have no reason to stop charging crazy money because Americans will go into $200k in debt to buy it. Thus inflation doesn’t stop. Of course its more complicated than this boiled down thing, but I feel it plays a huge role in the “mentality” of the market.

End rant.

Inflation increases had temporarily paused. But the underlying causes are active and evolving. China is slowly ramping up its economy. Once China accelerates back to trend there will be constant upward pressure on commodities, this will prevent progress on the inflation fight. A recession with substantial labor market loosening is needed to truly fight high inflation and stabilize at close to 2%.

Covid back in China ,how convenient

Blackstone will do well with its new rent-to-own tents.

Americans are going back to the land!

#VanLife

They will quickly make living in a van illegal if it isn’t already. Or, they will force people into van parks where you have to register and pay, so the right people get a cut off of all the people living in the vans. The US is a giant graft racket where the billionaires and hundred millionaires use bought-off politicians to steer the money right into their pockets. It’s not a free market.

I’ve been watching videos on you tube regarding RV lifestyle. A lot of those folks are saying it used to be you show up at a park and take an empty slot. Now it’s more a matter of having a reservation made a year in advance. Or even going to the extreme of buying your own slot.

I know you have to be careful of what you see on you tube. But it is interesting. And I wonder how much prices have gone up.

I believe the same thing is happening on the intercoastal waterway. It’s a federal project but local municipalities have taken all the good anchorages and charge up the kazoo.

I think what is going on is government has turned to graft and corruption not because the WANT to but because they HAVE to. They have run out of opm to spend.

Yep, like cas127 and DC and others saying here, the problem with shelter is that it’s basically inelastic, so it’s not like Americans are happy paying these extra rents, it’s being extorted out of them to a detriment of other sectors and leads to greater impoverishment of the big majority of the population. In practice what we’ve been seeing is that for non-discretionary things like this, Americans are still down-shifting, just in sad ways that lead to much lower quality of life, so the landlords raising rents to extortionate levels will go bankrupt anyway, just causing a lot more local misery along the way.

We’ve been seeing a lot of people in Texas and surrounding areas doing the Nomad-land, Van Life thing, a lot of others basically couch-surfing with friends and relatives (especially the poor souls who got drawn into divorce courts, even doctors, SWE’s and execs wind up in financial disaster from that). Been seeing more going off the grid, sometimes not dramatically but just getting stuck indefinitely in an old friend or acquaintance’s guest room, esp in the small towns and rural parts of Texas. A lot more moving in with family, or going homeless (always an “option”). A lot more quadrupling and quintupling up with messy roommates in a filthy 1 or 2-BR (doubling or tripling up is so pre-QE inflation). More bouncing around cheap motels, even more and more emigrating–a lot more expats out of the US in my friends circle in just the past 2 to 3 years than it seems like the whole past decade combined, Bloomberg even had an article on all the Americans getting cheaper housing in Europe. So these ultra-greedy landlords over-charging for housing (including Blackstone and Blackrock) really aren’t getting their rents paid, they’re just forcing more and more Americans into poverty and reducing the quality of life throughout the country. The US already has the worst life expectancy levels anywhere in the developed world, this can’t be helping.

The WSJ had a strong story today about the (very short) history behind the recent largish apartment complex foreclosure in Houston.

Basically, what appears to be a pretty inexperienced/naive/foolish RE syndicator (apparent acolyte of late night, “easy money” RE borderline scamster for chrissakes) somehow managed to Cobble together sufficient millions in equity (pandemic funds burning holes in pockets) to get a big floating rate loan (stupid/corrupt bank? CLO 2.0?) to buy multiple complexes.

With long, long, long overdue hike in Fed-destroyed interest rates, the floater destroyed newbie syndicator’s model within like 18 months.

No amount of tenant rent squeezing could make this financial abortion pencil out – result? Foreclosure within maybe 24-36 months of syndication.

A related story is also emerging that maybe $90 billion in rent backed CLOs (remember them) are starting to implode…essentially for the same reason – ZIRP era lending provided the rocket fuel for stupidity/corruption among people who had little-to-no idea about rational finance.

As these fools started to drown, they dragged their tenants down trying to save themselves – thus, 20%+ metro rent hikes in under 2 years.

If the CLO/bank floater stories are accurate it,

1) Explains a lot about the rent hike insanity of last 2 years and

2) It is, unbelievably, just a riff on the identical idiocy of 2008 Bubble 1.0…this time focused upon apt complex “owners” instead of “homeowners”.

BTW, I covered this syndicator’s end via foreclosure auction in early April, when it happened:

https://wolfstreet.com/2023/04/11/trouble-in-multifamily-cre-two-big-messes-and-investors-are-on-the-hook-not-banks/

…the favelas are where you find them (…old term: ‘Hoovervilles’, last time around…).

may we all find a better day.

I’m in Seattle. My rent just increased by 10%.

Where exactly? From what to what?

Well I discovered what I already knew: I am not the best at doing math in my head. The increase is actually 8% from $2164 to $2335. Still a lot. Capital Hill.

We’re in Seattle and ours is going up too.

Every time these morons pass a feel good tax levy to help the poor homeless drug addicts, we pay for it. I can’t support any more drug addicts.

Tough love is needed for the addicts dying on our streets. If it was someones child that slipped into distress and addiction most parents would employ tough love to prevent the self destructive behavior. Then build them back up and allow confidence to reestablish itself and guide them to take the right path.

To go off on a little bit of a tangent: I moved to Seattle a few years ago to work with homeless mentally ill drug addicts in downtown Seattle. Had done similar work in Atlanta. Much much more successful in Atlanta. The difference: much much higher housing prices in Seattle, causing homelessness. Not just my personal observation; that is what the research shows. Homelessness is a housing problem, not primarily a drug problem. Seattle’s resistance to sufficiently increase the housing supply while the city has had a large increase in population over the last 8-10 years is the cause of Seattle having one of the highest proportion of homeless people in the country. Politicians have found it easier to futilely spend money on homeless services rather than allow and encourage sufficient housing growth.

I thought california is also trying to combat homelessness by building more accommodations. And they run into so many NIMBYers and costs, that they cannot ever get much built.

No one wants homeless people living near them. That’s the catch 22.

“Put them in a home! Just not near me!”

The Sackler family (and their Florida order filling counterparts) could and should pay for it, especially in the rust belt. But it will never happen…they all used the “laws of the land”…and very “smartly”….as another great US citizen once said.

How long before you leave?

Friend here in NoVA just got hit with a 12.5% increase. He is young and freaking out a bit. He has had some salary increases but it’s all eaten up by inflation.

Mine went up 9% or so last month. HYSA on part of my house down payment savings is covering my increase but still it sucks. Starting to look at new jobs for salary increase. Next go around might try to live in commercial space, would be more fun.

Let’s start with everyone ,not paying their rent huge problem for owners. I owned rentals but never overcharged,most stayed 10 years

Don’t you “nice” landlords hate the “bad” landlords that give you all scum status?

What’s wrong with having someone else buy your large money pile (and end up with nothing for themselves) for you, if you are “nice” about doing it?

Actually the Fed’s rapid rise in interest rates contributes to rent increases by (1) lowering the construction of new housing units for rental as well as for home ownership and (2) by raising mortgage rates to landlords as they refinance. Given there is demographically a strong demand for additional housing units, the Fed’s actions to restrict the supply naturally raises rents. Basic supply and demand economics.

So then by your logic…the last 10 years of zero interest rates and cheap and easy money should have had us with super duper affordable rents and housing.

But yet, it was exactly the opposite.

I agree with this: Basic supply and demand economics.==> The more the money printing, more the prices are. The cheaper the money is: more the inflation is.

Hence, we need more hikes and more aggressive QT.

There is no slowdown in multifamily construction, but a huge boom. The slowdown is in single-family construction:

https://wolfstreet.com/2023/05/17/slowdown-in-residential-construction-centers-on-single-family-houses-multifamily-flattens-at-highest-level-since-1986/

And landlords charge the maximum rents that the market will bear, like everyone, not based on what mortgage rates are. Rents don’t go up and down with mortgage rates. They don’t go up with house prices either. They move based on other factors related to demand and supply, but also market psychology, income gains, etc.

Here is my infamous juxtaposition of the Case-Shiller Home Price Index, and the CPI for OER:

I’ve been assuming the big surge in multi-family was due to pricing the Millenials out of first time home buying, among others.

In my little corner of flyover country, tourism is really big, Multifamily units going up all over the place. The last data I saw (couple of months ago), said only 30% of the new housing units are lived in year around.

Here it seems to be people cashing in on renting out by the day or week, etc. But then we also have snow birds fleeing places like Floriduh and Texas.

OK, I was talking about construction (supply), not demand. You’re talking about demand, which is a different story. One story was that retirees would downsize from single-family into higher-end multifamily, which can be very convenient, with elevators, and all kinds of services, such as your packages being safely deposited in the lobby. And another story is that younger people would want to live close to work and be surrounded by the buzz and convenience of living in an urban center.

Both of those stories — lifestyle choices — have a lot of reality to them. No one is building low-end apartments or condos in urban centers that people who cannot afford a house in the suburbs could afford. The costs of living in a higher-end high-rise or a suburban house in the same metro are similar, and if you go further out, the house will be a lot cheaper, but the life styles are not similar. So in terms of new construction — that’s what we’re talking about — it comes down to a lifestyle choice, not a financial choice.

For Wolf:

HUGE surge in GUV MINT subsidized new construction of ”affordable” apts, AKA worker housing in the pine ellas area these days.

County and cities have recently voted to support housing intended for those making as low as 30% of local median incomes up to 80% ditto.

Seems like it might work to keep actual wages down if this succeeds.

Makes sense as usual Wolf. Thanks for the clarification!

They also get big tax breaks in many cities. In my area if they kick in a few below market rate units they pay reduced or no property taxes for ten years. 84 units going in with reduced low cost financing arranged by the government. No off street parking provided either.

Why does the purple line not fall as fast as it rose in the first place? (Rise between 2021-22 versus late 22-23 fall)

Hey Owen,

Residential construction is dictated so some degree by interest rate but much more by local zoning codes and parking requirements. In places where the regulations have been loosened, more supply comes online quicker, thus checking rent growth due to competition

Mortgage interest rates have NOTHING TO DO with the Federal Funds Rate set by the Federal Reserve which is merely an advisory rate for overnight lending for liquidity purposes for interbank loans. All mortgage rates are keyed off the YIELD FOR 10-YEAR US TREASURIES plus around 3%.

Are rates that FOMC sets related to treasury yields?

And yet, employment in construction is at an all-time high

What “rapid” rise? The rise is nothing more than a slow drip but you are i’m sure too young to understand that

5% in 14 months isn’t rapid? That hasn’t happened since the early 80s.

Wasn’t “rapid” enough … not even close. It should have been 7% within 6 months. That would have brought enormous pain no doubt but it would have done the trick. If we’ve learned anything it’s this ….. inflation once it rears its ugly head needs a swift kick in the arse .. not a pat on the back.

The thing you’re not looking at is back in the early 80’s (and for a decade after that) the prime rate was in double digits. A 5% raise in the rate when it’s already 12% is a lot different than a 5% increase from 0.

KGC

But one should not forget about the indebtedness in the 80s and now.

Multifamily starts are actually really high right now.

Got my new property tax evaluation for metro Denver $2,000 increase. $5k to 7$. Rental increases expected along with every other cost associated with housing or rental properties, maint expense and insurance. Inflation has America in a world of shit, it keeps overflowing and running down hill. I bought steaks at Sam’s club for $8.00 off a 3 pack of 16oz ribeyes, $45 and $51 before discount $37 and $43. Egglands Best 18 count eggs dropped $4.48 vs $6.50. I’m happy to take advantage of lowers prices. I hope interest rates keep rising and 6 month treasury gets to 10.0. The cards are stacked against the W-2 wage earner, the rat race will only get harder to sustain.

Could cut ribeyes in half,and probably healthier for u as well

Well your taxes will go down if your property values fall again. If the bubble ever pops.

It may just be a waiting game until inflation devalues everything enough so that property HAS to be worth the insane prices they are zillowed at.

Remember you can deduct those prop taxes on your income taxes! Woo

Bottom line is the economy is too complex and Fed (or anyone else for that matter) doesn’t really have a good clue. But that doesn’t stop a bunch of economic PhD’s from micro steering the economy.

Wonder if Fed independence would be threatened because of their track record? Wolf is that an area of interest to you to write about?

I’d agree. The world’s problems have become too complex to manage. Oddly or predictabley, the wealthy among us are doing just fine in this economy. They don’t rent from what I can see.

The FED’s balance sheet is a grotesque abomination, made even more repulsive by the SVB bailout. They need to ramp QT up to $200 billion per month, and take the balance sheet back down under $4 trillion. Alas, they won’t. They are not serious about fixing this inflation, they are stoking it. They want it.

Of course they want it. The U.S. has inflated its way out of pretty much every major conflict and catastrophe in our history. Inflation was some part of how we paid for WWII and it was basically how we paid for Vietnam in its entirety. When my Grandfather (who fought in WWII) was born in 1924, a single dollar held the purchasing power of about $17.50 in today’s dollars, at least according to the BLS. His father experienced inflation, he experienced it, his son lived through inflation, and now his grandson and great grandson are living through it. The Fed will not tolerate deflation, so anybody who is waiting for meaningful deflation or even any action to properly stop inflation is living in a dream world. We run insane budget deficits each year and we were always going to print our way out of them. The post-WWII national debt of around $285 billion was a serious problem in the 40s. Nowadays, our government farts out $285B on any average Wednesday, no big deal. THAT is why we are going to live with hot inflation for a long time to come. It’s sickening, but since we the people absolutely refuse to vote for some balance between spending cuts and tax increases, we will be taxed by inflation.

Global debt just went past 305 trillion. It is up over 40 trillion pre covid.

Debt keeps increasing. This is inflationary while it increases. In 2010, the CBO predicted that the US Government debt would rise from 10 trillion to 19 trillion in 2020. It hit 24 trillion. The CBO was off by 40%.

US Government debt in 1980 was about 1 trillion. In 1990 it was 2.5 trillion. In 2000 it was 5 trillion. 10 trillion in 2010. 24 trillion in 2020. current predictions is 41 trillion by 2030( it will probably hit 45 trillion or more). Anyone else noticing the government debt doubled each 10 years since 1980. crazy.

Look at debt charts. People wonder why houses are expensive? Maybe one outcome of out of control debt will be housing price drops as local governments will have to tax houses like crazy to pay for all their rising debt payments. Thus reducing demand. i know. just a pipe dream. But i remember sales tax used to be 3.5% when i was a kid and now it is 10% in my city. i could see sales tax hitting 12 to 13% in another 15 years. Every time my city wants to upgrade or build a new school, fire station, jail, court house, they sell a bond that is paid by a sales tax increase. Then 10 years later when the fire station bond is paid off they ask to keep the sales tax for the bond otherwise they have to lay off the fireman. Replace fireman with police or teachers as this story repeats. They never say they will have to fire city officials if the sales tax is not continued, only police or fireman for some reason. lol

Exactly. We are receiving the inflation we voted for.

Honestly I think the 2017 tax cuts put us into this position.

They saved big business like 2.5 trillion.

There’s no way that was good for the Us economy.

It’s like if you were in debt 90% of your income and the you gave someone a 30% check (of your income), for no real reason but to reward loyalty.

Ridiculous

You’re looking at everything through too narrow of a time frame, as if they have found some sort of magic money tree and what they are doing works long term. It doesn’t. There is no free lunch, and you can’t just print money. It breaks shit. And shit has broken huge this time. And the new normal ain’t gonna be pretty. The ultimate end is always hyperinflation.

The math of interest rates on money is exponential growth in the amount of money. In other words, exponential monetary inflation. Then if the money is circulated prices go up if not the amount of goods and services increases equally fast. The last do not work out in a finite world.

I am not sure that hyperinflation historically always have been the end of interest carrying monetary systems. Loss of confidence due to other reasons are possible.

The average age of empires is something like 250 years, and we’re right about there. They all pretty much follow a familiar pattern… Huge early economic growth and expansion of prosperity up to a peak, then higher standards of living plus military and conquest costs make the empire uncompetitive on an international stage. That’s where the debasement or printing of currency comes in. Sometimes it leads to hyperinflation, and sometimes a longer grinding inflation, but once the currency’s use as a reserve fades, the fat lady is finishing her song.

There’s still no clear (realistic) replacement for the dollar at the moment. There has also never been a time in human history when every nation debased their coinage, printed paper, or monetized debt simultaneously on this kind if scale. So maybe the show can go on longer than a reasonable person could imagine. But yes, eventually this will be our undoing. A lot can happen in 20-40 years, so I might even still be around to experience it.

DC

There is a substantial inflation lobby out there that wants more inflation. It makes all their debt less burdensome. They are mostly the rich. Inflation is passed on to those at the bottom of the economic ladder and the middle class. This lobby is very powerful. That’s why nothing is dome to bring inflation under control.

Will be such a shame when Bezos’ yacht ends up at the bottom of the ocean….

So the Fed thought rent inflation was “transitory”? (Don’t look at me like that, somebody had to say it).

Right. The FED got caught with their pants down again.

But it does not impact them

Jerome Powell and his friends already made 100s of millions front running their decisions as Fed.

Also they are not accountable for their actions

Worst case they walk away with their millions

It does impact them at the end. They flee like rats from a sinking ship. There’s a reason all of these people have been buying bugout shelters all over the globe. They have a plan to gtfo when it all starts to burn. The unfortunate thing for them is that there is nowhere to hide on earth anymore. Technology made sure of that.

Depth charge ,seems like a lot of them are going to New Zealand . Just don’t know why

With housing affordability at rock bottom, landlords know they have renters over a barrel. Renters open the wallet, and inflation rises.

If the Fed is fighting inflation (the jury is out), it will continue to increase interest rates and start selling its MBS portfolio, ASAP. It should have started that a year ago, or earlier.

Unless renters are receiving big raises, any increase in rent will result in less spending in other budget areas.

Sure, the renters will have less money and buy less, but the landlords and homeowners receive the rent and have more wealth to spend.

Unfortunately, the Fed believes it can grow the overall economy without participation of the bottom 50%. That’s why wealth concentration is at an all-time high and getting worse (or better, from the Fed’s perspective).

As long as low wage are plentiful, the Fed knows the bottom half has a basic existence.

“landlords and homeowners receive the rent and have more wealth to spend”

Or, they end up giving that extra $$ to their city gov’t from their increased property taxes, water bill, sewer bill etc.

MM,

Yes, inflation is just a series of price adjustments, leading to arbitrary wealth transfers from one economic player to another. It’s hard to plan in an inflationary environment, rife with unknowns, instabilities, inequities and bias, so I’m not sure why the Fed isn’t attacking inflation with more vigor.

Does the Fed think inflation is not a problem? Their actions indicate to indicate that view. We are plateaued at 5-6% inflation, and the Fed is talking about pausing the small rate hikes.

What we need is Volcker 2.0. Nothing short of SHOCK AND AWE.

What we get is pussyfooting, and denial. Powell, Yellen, Biden and congress(yep, both sides of the gutter) are screwing everyone who doesn’t have assets.

What a joke.

Not news. The FED & all their C suite boosters have had the working classes over a neat little barrel for years while they grope around in the dark for that mythical fourth orifice.

I count six for men and seven for women. Do the math, bulfinch.

I lend to real estate investors and every single investor that brings me a rental income property always says the first thing they will do is raise rents. They have to think that way because 99% of the sellers of multifamily properties are asking for the value/price today that they would have in the future if their buyers did raise rents. In other words, list prices based on future value. Even though the numbers don’t work in 90% of the scenarios, and it takes me 5 minutes to show them, these potential buyers are still asking me, “But will you still lend on it?” I hope the multifamily starts shown in Wolfs chart here in the comments will create more supply, and the higher rates will deter more buyers, and these sellers of multifamily properties will come back to earth on their price expectations and rents will plateau or go down. Everyone has gotten so used to the free money that has inflated asset values, real estate investors paying any price because it will always go up, right? Crazy times.

It took massive layoffs to break the last real estate bubble. It will take massive massive layoffs to break this hyper bubble. My business has already gone completely dead. Others likely to follow.

“It took massive layoffs to break the last real estate bubble.”

No, it didn’t. That’s ahistorical nonsense.

Where I was it broke because some people realized that they would be making mortgage payments on a house which would be underwater for ~ 10 years. They came to their senses after they realized they grossly overpaid because of lured by monthly payments. They either jingle-mailed or squatted (don’t pay until eviction) they’re way out of it. Don’t recall the job/income thing being much of a factor.

Steve feel sorry for u, but can u lower prices to survive

what terms are you using these days?

As soon as the FED postulated that the banking failures would act as a de facto rate hike – thereby giving them the excuse to do a little less, you knew this would lead to a longer inflation battle. It was the opposite; after the bank failures the markets acted like there had been a rate cut.

Mr Wolfs ” GREAT ” charts have a lot of timelines based on Years.

Once all this current FED, FEDeral Government insanity plays out, I

bet his timeline charts are based on decades. Old folks may never get to know how this will all end. Hey, being an old fool does have advantages….

If you aren’t dead yet, then you have a front row seat, and the ‘ride’ has already started. Enjoy!

I wonder how Powell will try and spin it this time. He seems set on never doing another rate hike beyond possibly one more time. I wish Biden would call on the FBI to investigate the Fed for its fake inflation fight. Depth Charge is correct, the Fed is corrupt.

What isn’t corrupt in the federal government this day and age?

Good god!!! The FED has raised interest rates for the fastest time in 40+ years and that is not enough for some.

FTR, before some of the crazies go there and put words in my mouth, I definitely agree that the FED has a lot more work to do to reign in inflation, however it isn’t like they have stopped yet and started to lower rates. The future is still unknown. They have signaled a pause but a lot of money has been lost reading FED signals. Let it play out before whining.

If the FED starts lowering rates or saying inflation is gone then you can start complaining.

Agree!

This is insane. It doesn’t help that the government let banks buy homes as investments after 2008.

All the banks, investors, zillow, redfin, and blackrock are doing is buying all the homes driving, up the prices, sending emails to home owners to fix rent prices, tell people hikes are worth more. They’re all monopolizing rent and home prices.

The government will never revert the mistake they made as it would impact delegation and donations.

“All the banks, investors, zillow, redfin, and blackrock are doing is buying all the homes…”

Jeez, Guy, give me a break. 1) BlackRock does not buy homes. You are thinking BlackSTONE. Giant difference. I wonder how many on this site and others see that ignorance and believe it. 2) The amount that banks, Zillow, Redfin have bought, come on, man. Tiny. Blame your fellow citizens who bid even crapshacks up to the max.

In addition, both Zillow and Redfin are out of the home-buying business. They SOLD all the homes they had and washed their hands off it, at a massive loss, which we discussed here at the time.

This reminds me of reading sometime ago that corporations (Bill Gates included?) and hedge funds are buying even trailer home parks. My immediate reaction was it is a big receipe for civil war.

Close. Investors are buying mobile home parks from mom & pops who want to cash out.

Where do these people work that they can afford such ridiculous rent prices?

Not everyone can work in the tech sector. Very few of the jobs reported in the tech sector offer much in the way of job security anyway. Basically, none of the reported numbers make any sense to me.

$1,000 car payments, $2,000 rent payments and you still need to feed and clothe yourself? The ability to make such payments are reported as common/expected. Ridiculous is all I can say.

1 + 1 not longer equal 2 or 4 or 10 and yet it is reported as such?

FOMO is greed, in a class all by itself.

I’m in the DC Area. Try $3000 rents.

Modalita

Yep, the house next door to me rents for that amount. The single mom that moved can’t afford the rent, so she sub letted the street to a trucker contractor who parks his gigantic $80,000 truck on the street in front of her house and pays her cash under the table for this[ priviledge. The dude lives in an HOA community that doesn’t allow trucks on the street.

You’ll see more of these similar scams as rents get out of control.

Why is that a scam?

DC is so classy tho.

How much is an Uber black running there nowadays? I remember feeling like a celebrity. Ha

Everyone I know has roommates. Theyre in their mid 30s. Wonder why no one has kids…

And the rest of those houses that they would normally rent/own and start a family in are now parked on Airbnb.

3 young guys (look to be late 20s, early 30s) just moved into a 3 bedroom in my apartment complex. It was listed at $2800 a month. I don’t think the complex haggles on prices, but I could be wrong. So they are each paying about $1000 a month for a room.

I’m in a 3 bedroom also, but I locked in at $1750 a month. My apartment is fine, but its not as “updated” as the more expensive ones. I’m curious to see if they will raise my rent much when my lease is up in December.

They will.

my rent in houston is 3,000$ and i cant afford any car payments. 20yr professional engineer in oil & gas. family of three, no house yet.

We’re paying $3,650 for a two bedroom condo in San Diego. And that’s a comparative bargain. You can’t rent a SFH for less than 4K and most listings for SFH are anywhere from 5-8K on up. It’s insanity.

Good god!!! The FED has raised interest rates for the fastest time in 40+ years and that is not enough for some.

FTR, before some of the crazies go there and put words in my mouth, I definitely agree that the FED has a lot more work to do to reign in inflation, however it isn’t like they have stopped yet and started to lower rates. The future is still unknown. They have signaled a pause but a lot of money has been lost reading FED signals. Let it play out before whining.

If the FED starts lowering rates or saying inflation is gone then you can start complaining.

The Fed reacts asymmetrically to threats to the economy versus threats to the currency. It cuts rates rapidly and boldly when it sees threats to economic growth and acts slowly and deliberately when conditions justify rate increases. It let inflation run hot under cover of an “inflation averaging” theory that accompanied its “transitory” analysis. It’s going sit on its hands after June because its institutional bias is pro-inflation. After all, if price stability requires 2% inflation, 5% inflation is really only 3% inflation in Fed terms. No big deal, right?

Until the USD FX rate starts crashing.

Then the economy, public and markets will be thrown under the bus to save the Empire.

Things that may not go down well with the inhabitants of the empire. And as the economy very much is the empire, the future may prove interesting.

The US Dollar is doing extremely well this year and has stayed well above 100 on the DXY. Didn’t you get the memo? It’s not the US Dollar that is of any concern whatsoever, but rather the amount of the US federal debt and deficit.

Rate should be about 15% now. It won’t have a serious effect until it reaches the proper level on both borrowing and saving.

Wow, a natural balance? What a wonderful concept!

I wonder about how these NATIONWIDE MEDIAN ASKING RENT numbers translate into specific locations as well as actual rents paid..

A lot of of the increase in median may be from people moving inland from expensive coastal areas, for example. That would increase the rents inland but the coastal rents may be flat to falling.

Anyone have numbers?

My rent is Boston went up 12%. I did not renew.

Rents are seeing astronomical increases in CT. Young people and lower classes are struggling.

I was just back in CT this month looking for a house or condo to buy/rent. CT was my home 40 years ago. I’m thinking of leaving Texas for personal reasons and thought CT might be a good place to move to since family is still stuck there. Boy was I surprised at what I saw.

When I left Southbury, CT in the 1980’s, CT had no state income tax and property tax was low. I looked at condo’s in Heritage Village that sold for $70 K maybe 5 years ago. These were built in the 1970’s but it’s a well run 55+ community. Absolute junk on the market these is ~$250 K and the HOA fee is $600/month. Plus now there is a state income tax.

So much for that exercise in maybe buying. Published rents for the same complex are $2+ $3 K for 1,000 sq.ft. condo and none were available at the time I was there.

Other rents in nearby cities are similar and you need to be armed in some locations. My sister is still stuck there in the house she and her husband have lived in for 45 years near downtown Waterbury. Crime is rampant in Waterbury and her property tax was just raised again to ~$4,000 annually for a $115,000 falling down 90 year old house.

Texas is looking OK for now, but I am looking in other states to relocate to.

Iowa rural is cheap

Well Waterbury is not really representative of the rest of the state. But yes the situation in the cities is rough in regard to property tax rates. The suburbs are much more livable, but property is expensive. The value of my house has gone up 50% in the last two years alone.

Come to NH. Lower cost of living, no sales or income tax etc.

1) In 2011 Fitch and S&P reduced US gov rating. Fitch boss was fired.

If US gov choose the civil war fourteen amendment US gov rating might drop to B. The CPI might reach between 10% and and 20%, on the way up. The dollar will enter the recycle bin.

2) In order to move up the weekly Dow should close above Dec 12 2022

high @34,712.28. If it can’t, after half a year, it might try again. Options :

3) Halfway, between Oct 2022 low and March low for a sling shot.

4) Below Oct 2022 low, the Jan/Feb 2016 analog.

Two years from March 2020 low to Jan 2022 high. Two years from Jan 2022 high to the next low.

5) Our money tsunami was an IOU. We spent our IOU money. Recycle the boomers for the sake of Gen Z.

The bond rating on US government debt (US Treasuries) should have been cut to somewhere between C- and F well over a decade ago.

What do you base this on?

The United States federal government has responsibility paid its debt for a really long time. Furthermore, as the taxing authority on one of the most dynamic economies in the world, it has ample power to continue to pay its debts.

Saying that the debt rating of the U.S. government should have been dropped to a C- or an F just displays an ignorance of economics and debt ratings.

Now to be fair, there is a certain ideological segment of the population that wants to cause economic destruction by making it so the U.S. does not pay its debts despite having the ability to do so. Unfortunately that segment has acquired an outsized amount of power, but still…….

Some would argue inflation is a soft default.

Adjustment : in 2011 S&P boss was fired.

In 2016 we HAD to leave South FL due to a $115 a month rent increase. We were already spending over 50% of our income on rent and there was no more stretch. Voting with our feet was a good move for us.

We are now in another southern state and in our second rental house which has increased 17% since 2021. We are at the no stretch point with this rental now. The landlord can ask whatever he wants, but he won’t get it from us.

We are a few years away from retirement and are seriously looking into leaving the US. Our retirement income won’t cover the rent in any good metro area in the US, but we can live well if we leave. The choice seems to have been made for us by the rent seekers. The money and the value are just not there.

These landlords are turning a blind eye to this trend at their peril. All kinds of groups in the US are moving out because it is just too hard and not worth it to stay.

Several old friends – old in both ways – have done that in last couple decades and have no intention of returning to USA ever, at least so far.

Our last rental, a charming old house NOT updated, was in hood going ghetto, and when owner across street died, heir sold to immigrant family who gradually moved in 12 adults and many children into 2 bedrooms 1 bath.

”And so it goes,” per Vonnegut, is as it shall be going forward.

Based on this report, it’s easy to see why folks are snapping up houses in our current ”working class” hood for rents around $1800, purchases at $225/SF for not rehabbed, $300-$400/SF for updated and new.

When we left FL in 2016, most people on our street were already doubled and tripled up. You had parents living with their married children and grandchildren. The number of cars parked in front of some homes was 4+.

Where we live now new construction down the road from us is going for $1.3M. The neighborhood is nice, but not that nice. The taxes alone would be close to $30K or more. Crazy.

I have a retired friend that moved to a small beach town in Thailand. He loves it there and lives very well on only his Social Security income.

I believe you have to leave country ,every 6-9 months. And return look it up. Also what happens when debt default cancels your s s check . And your stuck in Thailand with no money

Petunia,

What countries are you considering moving to?

Not one place particularly but several over time: Spain, Italy, Mexico, Argentina, and other places in South America.

@Petunia

You might be able to retire now if you leave the US. I moved from Colorado to a large, cosmopolitan Mexican city last year and my quality of life has gone up tremendously. I bought a place for cash, but renting a brand new, centrally located 2 BR apartment only costs about $1200 here. The climate is like SoCal (traffic too, unfortunately), the food scene is incredible, and making friends is easy as Americans, Canadians and Europeans seem to be moving here in droves. And unlike where I used to live, I don’t worry about random gun violence anymore.

Wolf, You make Excellent points on the likelihood that Inflation will stay high ( including prior comments on robust consumer spending).

How do you think this will play out for FOMC?

Presumably, their “victory lap pause” in June will have to face reality this summer , especially as the base affects allowing the year over year CPI dissipates?

Assuming you are correct on sticky demand and inflation, I would think at least by September, the Fed will have to start pushing rates up again. With plenty of talk about it in August.

This inflation will continue to dish up nasty surprises. There are a couple of things that will not be surprises; we already know they will happen: as you pointed out, the base effect will reverse starting this summer, which will push year-over-year CPI up; and the health-insurance adjustment will end in September, and the new adjustment might go the opposite way (as it often does), and that will push up services CPI, core CPI, and overall CPI.

The PCE Price index doesn’t use this health insurance adjustment and will be unaffected by it. But it will still be affected by the base effects.

So we’ve got this coming, and the Fed knows it too.

Then there are the known unknowns and the unknown unknowns. I just don’t see a rate cut at all this year, unless something big blows up. It is possible if we get a big second wave of inflation later this year or next year, that the Fed will push up rates further. In my mind, the most likely scenario is relatively high inflation that will just move up and down around the range of 4% to 6% core PCE, where the Fed is going to keep rates high and steady and wait.

It’s interesting what the Fed will do if inflation doesn’t fall to 2 percent by the end of 2024. Because everyone is betting on it. And as the Wolf says inflation will fluctuate between 4 and 6 percent for a long time. Then it will be interesting to see what the Fed’s explanation will be.

I think that the way the rest of the rest of the year will play out is that the FED will want to pause, but the numbers will not let it do so. So there will be pauses mixed with rate hikes.

Meanwhile the balance sheet will continue to gradually run off.

Eventually, in a year or two or three, the balance sheet will reach historical “normal” levels and only then will the FED rate really matter. In the meantime, the FED rate is going to go up, but only at a slow rate that gives the appearance of action without really being meaningful.

The balance sheet needs to be resolved before the rate hikes are anything more than marginal.

The first chart is somewhat misleading as it looks like CPI owners equivalent rents have almost caught up with asking rents. If both had been rebased to 100 at the start, one could see that asking rents are up by about 43% since 2017, but CPI owners equivalent rents are only up about 30%, so still a long way to catch up.

United Nations Secretary General said a couple days ago, in Hiroshima, that its time to reform the Security Council and Bretton Woods. Bretton Woods being the system of World Reserve Currency that encourages or enables the huge historic (and present) inflation by allowing the Federal Reserve to spread it like a tsunami worldwide; Americans are definitely not alone in their contempt of the Federal Reserve’s money printing.

Because of its failure to budget, the US will have deficits that are 6-8% of GDP, as far as the eye can see. So yeah, some big changes are in store for the USD absent major deficit reduction in the short term.

Didn’t you get the memo months ago that the Federal Reserve is in the process of SHRINKING THE MONEY SUPPLY and significantly reducing its $8 trillion or so balance sheet? Are you aware that the US economy is larger than $22 trillion with hundreds of trillions in assets?

Got married in 1980 and we moved into a higher end apartment complex in Charlotte, NC. Rent for one bedroom apartment was $210 on $860/ month take home pay. Hard to believe with all the I. T. progress the standard of living for young has went no where during my lifetime.

It’s destined to decline noticeably in the future.

Living standards have been inflated for decades by expanding debt and the loosest credit conditions in history.

Both will reverse in the future, with the interest rate cycle almost certainly turning in 2020.

Add a declining or crashing FX rate versus the countries that actually produce the things people have to buy and it = the majority of Americans becoming poorer or a lot poorer.

For those unfortunate enough to be at that critical inflection point in their lives where homeownership would be that next step forward in providing for their growing families (older Gen Z, Millennials, etc), you’re basically stuck deciding between rampant rent increases and near-peak housing prices. It’s easy to tell people to just wait it out and keep renting, but that narrative loses steam when rent prices continue to sharply increase. Alternatively, you can buy now and risk losing 10-20% of your home value over the next few years if the enigmatic recession finally comes to fruition.

When it comes to housing, many are stuck between a rock and a hard place. The only way I really see this playing out is the eventually Fed having to push rates higher which will finally lead to a recession via increased job loss and reduced consumer spending. Maybe the cost of rent and homeownership will finally level off or decline, but not without increased unemployment undermining the ability to take advantage of a cheaper market. Hate to see it.

Housing prices can come down quickly with tax policy and regulatory changes. The government may be forced to make those changes at some point, in spite of government officials real estate holdings being affected negatively. Unfortunately, it will take widespread Hoovervilles (in the tens of millions of families) to make this happen. Government is absolutely not there to help the people, until it is forced.

A decade of depressed new housing unit construction cant be undone with rate hikes. Theres too many people and too few housing units. Now that mortgage rates are through the roof the market will pivot to drive rents north, and rapidly. The alternative is living in your car.

Lol! Mortgage rates aren’t “through the roof”. Not even close. There’s also plenty of housing. Wolf has some articles on that.

Mortgage rates have gone through the roof relative to what they were. And all those “plenty of houses” are sitting at prices set during the 3% era, now with 7% rates. The real mortgage payment for them has increased well above $1000, hence why there are fewer people buying them. Prices are coming down but the prices have not lowered enough to make their payments as low as they were before. So no, theres not plenty of housing, which is why theres going to be increased competition for rental units which are at historically low vacancy rates.

No, many of those housing units are sitting empty. The stock market and bitcoins need to collapse.

Could it be that rents reflect the (extra) price people are willing to pay to wait out a real estate correction? I put myself in that category, having sold my house to relocate. I’ve maintained all along that real estate markets aren’t “clearing” as asking prices reflect the marginal price that was set under completely different situation (ie free money bidding frenzy). I think once aspirational pricing becomes market clearing pricing all heck breaks out and eventually rents will follow.

Relative to population and incomes, home volumes are smaller. There’s a building problem.

Bernanke, pg. 287, “Lower long-term rates also tend to raise asset prices, including house and stock prices, which, by making people feel wealthier, tends to stimulate consumer spending-the “wealth effect”.

Public policy has been a disaster.

There is one overriding error, that banks are intermediaries between savers and borrowers.

This dynamic is at least as old as Henry George. Same as it ever was …

RedFin did an analysis recently which showed that in the US it is now on average 25% cheaper to rent than to own (in reality, the percent is even higher because I do not believe RedFin includes maintenance in their homeownership costs as part of their calculation).

25% is a waaay bigger gap than historically normal so either houses need to get way cheaper or rents will continue rising just to catch up with house prices… even if the rest of the components of inflation (and house prices) stabilize.

I actually did some math at some point.

And take it with a grain of salt. But I figured out that renting in Raleigh with semi annual increases. over a certain time period you are paying the equivalent of a $800,000 mortgage, for a crappy apartment where they treat you like an unwelcome human.

Just write down all the increases you will probably get over the next 20-30 years IF you stay there. Then look at mortgages. For a direct comparison of quality, house versus apartment. You are way overpaying.

And did I mention they treat you like a subhuman?

You can’t just look at apartment complex prices. Generally speaking, it is usually much cheaper to rent in the local private market than in an apartment complex owned by one of the giant corporate landlords.

Also, no one says you have to rent for 20 years. Renting provides flexibility which you can take advantage of during time like these where in many places, when all expenses counted, it is 30 to 40% cheaper to rent than own.

How do you figure?

By sq. Ft comparison the rents in a major metro are quite a lot.

Here in Raleigh $2,000 for a 1,000 sq. Ft apartment is about the new standard.

How much is a 1,000 sq. Foot house?

So we measure in length of time correct? Say a dweller averages 5 years at an apartment. Well any length of time you can compare to other lengths of time. And extract a cost from it.

So anyway I did the math and literally renting an apartment came to being equal to an $800,000 mortgage.