High demand by renters of choice trying to outwait the housing turmoil pushes up actual rents in a range of 6% to 8%.

By Wolf Richter for WOLF STREET.

Landlords and tenants are throwing a bucket of cold water on hopes that rent inflation will back off – it just doesn’t seem to be happening.

These reports have been coming in from the largest landlords of single-family houses and from multifamily landlords. The largest landlords of single-family houses are publicly traded, and so they report operational details, such as actual rent increases for lease renewals for newly executed leases on a same-house basis. The apartment data is based on millions of actual transactions, renewals and new leases.

They’re actual rents that tenants pay. Changes in actual rents for specific rental units are also the base for the rent inflation measures in the Consumer Price Index and the PCE price index.

None of them include “asking rents,” which are the advertised rents that landlords want to get for their vacant apartments, whether or not they’re actually able to lease at those asking rents. Zillow, Zumper, Apartment List, and others report “asking rents.” The double-digit spikes last year occurred in asking rents, not in actual rents.

Rent increases reported by the largest single-family rental landlords.

Invitation Homes [INVH], in its earnings call for Q1 on May 2, said that rent growth in April showed “further acceleration” in newly executed leases:

- April new lease rent increase: +7.5%

- April renewal rent increase: +7.2%

- April blended rent increase: +7.3%.

In terms of Q1, it said, “We have also seen stronger demand return following the winter leasing season, with new lease rent growth accelerating sequentially each month during the first quarter”:

- Q1, new lease rent increase: +5.7%

- Q1, renewal rent increase: +8.0%

- Q1, blended rent increase: +7.3%.

American Homes 4 Rent [AMH], in its Q1 earnings call on May 5, said that “strong demand continues to fuel solid occupancy and rental rate growth,” in Q1 and continued in April.

- April new lease rent increase: +9.4%

- April renewal rent increase: +6.2%

- April blended rent increase: +7.1%

Which were “well above our seasonal pre-pandemic norms,” it said.

- Q1 new lease rent increase: +7.8%

- Q1 renewal rent increase: +6.8%

- Q1 blended rent increase: +7.1%

Which “drove same-home core revenue growth of 7.7% for the quarter,” it said.

John Burns Research & Consulting reported some “takeaways” from the National Rental Home Council Industry Leaders Conference, including this:

“Rent Increases Driven by a Substantial Shift to Renters by Choice.”

“The tenant profile in professionally managed build-to-rent and single-family rental communities is significantly shifting. There is a growing trend of even more tenants choosing to rent single-family homes rather than buy one. More prospective homeowners believe that prices and rates will come down and more resale buying opportunities will emerge, so they are delaying their home buying.

“This shift has led to a rise in the number of renters who are less rent-sensitive, creating demand for higher-quality rental properties.

“These renters, by choice, value superior interior finishes, better amenities, and overall design, which were not commonly available 15 years ago. As a result, property owners and managers can command a premium for such properties.”

Multifamily apartment rents continue to surge.

The National Multifamily Housing Council last week released its industry benchmark report for January (the delay is to comply with federal antitrust guidelines, it says). This data is based on executed transactions tracked by RealPage from over 13 million rental apartments in over 400 markets. “Asking rents” for vacant units are not included:

- New leases (per square foot): +8.9%

- Rent at renewal (effective rent on the same unit): +8.4%.

You get the idea.

Lots of demand for rentals, given the high cost of ownership. A lot of people are now asking the question why buy the house, when you can lease a similar house for a lot less and outwait the situation – falling home prices and high mortgage rates.

And this relatively high demand by people who are renters of choice, who got the biggest wage increases in 40 years, is pushing up rents. That dynamic has been in place for a couple of years. And it hasn’t vanished at all, but appears to accelerate, based on these reports from the industry.

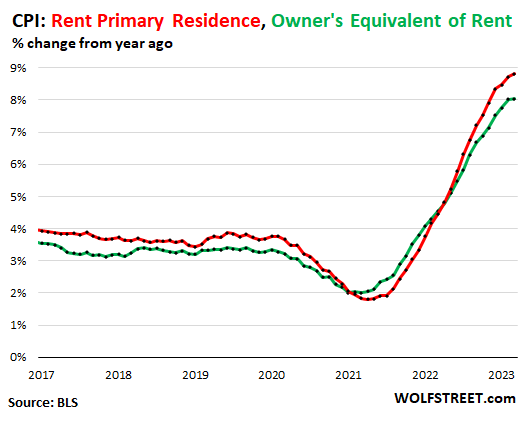

Rents are a big factor in CPI and PCE price index.

The Consumer Price Index for April will be released this week. About one-third of the CPI is “shelter,” based on two rent factors: Owner’s Equivalent of Rent and Rent of Primary Residence.

Both factors have shot up last year and this year. In March, OER was 8% and Rent hit 8.8%. The incremental increases slowed in March, and will likely slow further, and the year-over-year increases likely peaked, with annual rent inflation eventually dipping below that 8% level.

And those indices continue to be in line with what landlords are reporting.

We can see in the data reported by landlords that 6% to 8% increases in actual rents – renewals and newly executed leases, which is also how CPI measures rents – are currently playing out. So this is a little slower than the CPI rent increases in the range of 8% to 9%.

But the 6% to 8% range is a far cry from the hoped-for massive decline in rents – hopes that were espoused by big drops in “asking rents” off of the double-digit spike last year. But neither the spike nor the drop-off from that spike made it into actual increases that tenants are actually paying at renewal and when signing new leases.

So it seems unlikely that Fed chair Jerome Powell’s assumption will play out that rent inflation will be slowing sharply in a few months, and that actual rents are already going down, and that rent inflation will reach the point where it will no longer be an issue, and that the CPIs for rent are heading back to the 2% to 3% range, and that this decline is already baked in because the rent indices are lagging indicators, etc. etc.

It seems much more likely, based on these actual rent increases, that rent inflation will remain well in the hot range, above 6%, and that it will not help push down the services inflation measures and “core” inflation measures that the Fed is now so focused on.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Jerome Powell is peddling a fantasy. Every single word out of his mouth about inflation has been wrong. He’s a practiced liar who is destroying the financial lives of all but the most wealthy. And he and his cohort continue, unabated.

The longer this inflation goes on, the worse the long term damage for most. It benefits a very small sliver of mankind, but they’re the ones pulling all the strings. The future of the young was stolen – quickly – and it is currently parked in the bank accounts of the billionaires and hundred millionaires. This is the greatest financial swindling in US history.

Was there a swindling?

If the Fed gets his soft landing, there will be a new permanent price level for CPI and asset prices that is at least 20% higher than it was in 2019. The Fed will succeed in transferring 20% of wealth from young generations and renters to the wealthy. Before this occurred, we already had record wealth concentration.

Any central bank with public interest in mind would be looking to reverse the CPI inflation and asset inflation that was created by mistake. Powell isn’t doing that. He’s stated he wants to add to the inflation now and in future years.

Of course, in conducting monetary inflation in this manner, the Fed flip-flopped its intent. Back in 2019, the Fed said the intent was to average 2% inflation over time. Now that we’ve had 20% inflation in about three years, the situation calls for a period of deflation, but the Fed has apparently reneged on that promise.

Federal bodies should be transparent and consistent. When they tell the public one thing, then do another, and it transfers trillions of wealth from one group to another, I’d say that’s a swindling.

The Fed needs to sell the darn MBS, yesterday!!!

Without a big crash in Stock markets, a big crash in Real Estate, and Without a big number pf bankruptcies that will wipe out debt, NOTHING will get fixed. This is because:

1. There is too much liquidity and too much debt.

2. Productive work has lost value and Speculation has taken over. So inflation is now well entrenched to be moved by 0.25% rate hike.

“If the Fed gets his soft landing, there will be a new permanent price level for CPI and asset prices that is at least 20% higher than it was in 2019.”

I like effort & intent, but let’s be real. 20% is just a start. Housing in my area is up 60% in my area since the start of 2019. Cars are up at minimum 25. Most food items are up at least 25-40%. Oil will always fluctuate.

Again, great points, but let’s be more realistic with the actual floor. In general, it’s much higher than 20%, especially in housing which is the big ticket that hurts the most.

BENW,

” it’s much higher than 20%, especially in housing which is the big ticket that hurts the most.”

Hurts renters like myself.

Has been a bonanza for huge numbers of Americans who bought homes 2012 to 2020.

Not here but at other websites they gush over their great RE investment.

Something like this (made I p):

“Here in Boise. Bought 2013 185k.

Now sitting pretty at 550k.

Love real estate!”.

And I’m supposed to believe the 1% are the source of our problems per some folks.

That guy, gal in Boise isn’t worried about them one bit.

How much talk of inflation in DC by either party?

*Zero*.

The FED has been lying and manipulating and doing the bidding of their Masters for decades. It’s in their DNA.

Your comment seems pretty sensible.

But I believe the poor should not be concerned that the 1% have benefitted so much from 2011 to present.

Rather they should be upset that HUGE numbers of people in the 60% to 99% wealth segment have benefitted so much from housing, stock appreciation over this timeframe… while they have not.

But Sanders, Warren and many copy cats would have us idiots believe only the 1% benefitted. I’m almost of a mind that it is meant to be a great deception.

Sure, some folks other than the 1% have seen some benefits, but by and large, there’s been a whole lot more benefit to the few in the 1% than the many outside of it. After all, the top 1% still hold more wealth than the entire middle 60%. The bottom 50% have next to nothing while the top 10% hold roughly 3/4 of the total wealth.

Great article !!!!! More wealth transfer off the very bottom in the upward direction for sure.

Fits my personal experience even in zero frills tiny, low income hotel style 250 unit apt housing. (owned/run by BIG PE outfit, with housing all over hell, various types but mostly multi family, I think). Just tried to sell me renters insurance….for what? 2012 truck is outside uncovered. Nothing else worth risk of swiping, except maybe another resident who needs peanut butter or TP.

Anyway, rent up 20% from late 2019 to this May1.

BTW, Randy is a piss poor spinner of whatever obtuse shit he is trying to spin, just my opinion……maybe he’s a genius.

Scott,

I happen to think this should be viewed in relative terms not just absolute ones.

Suppose the following was true for 2 individuals:

X worth 5B. 1 percenter.

Y worth 2M. Upper middle class.

Last 10 years X net worth increased from 4B to 5B.

Same timeframe Y increased from

500k to 2M.

Absolute numbers X is 1B more wealthy. A 25% increase.

Doesn’t change his lifestyle, options hardly at all.

By comparison Y wealth increased a “paltry” 1.5k. Same timeframe Y wealth

increased 300%. This can significantly change Y’s lifestyle, options, and/or security.

Many politicians focus solely on X. Yet Y’s increase in wealth… though dwarfed in absolute tetms by X’s… is in very practical terms more significant.

If its so terrible that X’s wealth increased so much, its probably just as terrible that Y’s increased as it did.

At least viewed from the perspective of, say, a very poor person whose wealth may not have increased at all and whose lifestyle may have taken a step backwards during this timeframe.

My point is that while the very poor and poor generally benefitted little the last ten years, many in the middle class and especially the upper middle class benefitted considerably.

Yet many liberal politicians (and by the way I am in general liberal) only want to focus on how terrible it is the 1% got richer during this period while ignoring the benefits the middle and upper middle class accrued.

I dont like the great wealth disparities in our country but I’m not impressed with those who demonize the 1% in

blanket (overly general) terms.

If someone wants to change how people get compensated in our country then go ahead and discuss that. But dont just rant about somebody being extremely wealthy.

I take it you wouldn’t like my Constitutional Max Net Wealth notion…..with IRS as a FULL part of Military, enforcing economic cheating, like the Coast Guard (and the rest of the Military and supporting agencies) or local cops catch robbers, smugglers……. making money “illegally” simply becomes making and hiding TOO much money.

Still trying to decide between $10m and $15M as limits. Your vote? Sorry that’s the only two choices, but we are all used to that. Plenty “incentive” to work “hard” in either amount. Excess wealth goes to Comprehensive Green New Industry, run like any wartime “business”…..literal war for survival. Seed money from your 1% and less bunch. Includes big diet changes, too….healthier and cheaper.

It’s really much better than the huge mess of present laws, even those that are enforced. I’d also END tax-free status for religions FOR SURE…….and probably most “charitable” foundations. Single payer health care goes without saying, however the science behind it needs a COMPLETE overhaul….what a profitable wasteland of procedures, tests, devices, and pills, complimented by an also very profitable disease causing diet and lifestyle.

Buying congress critters would become more pointless and difficult….probably they’d just go back to the traditional bringing home district pork, which makes compromise much easier.

After a few years under this new paradigm, the politically dreaded ZPG can be seriously addressed.

I shouldn’t care, there is absolutely nothing special about our species other than WE think that there is.

The Earth has seen a lot of strange and different shit in 4.5+B years…..we are a multicellular evolutionary curiosity at best, like those weird critters in the nature films.

The single cell bunch still “win” EASILY in the max biomass sense, which fits our more, more, more, mentality/stupidity of deciding who is the “winner”.

We won’t even be the first to “self extinct”….I’m sure there have been many over virulent species who killed off all of what they lived on in the past.

The Universe doesn’t give a shit about us…deal with it.

20% inflation? I wish, my utilities has double food and gas up at least 40%. Insurance on both home and auto 50% and that’s after I changed carriers.

“…food and gas up at least 40%”

LOL. Have you even been to a gas station recently?

Lots of food prices have come down and now are below where they were a year ago, including meat.

Regular unleaded here in Phoenix is 5.03 on average today. Gas prices influence the price of many other goods and services. The government needs to focus on way to increase production and lower the cost at the pump.

C#Dev

I too am in Phoenix. I’ve been screaming about gas prices for a long time here on Wolf Street. I’m not seeing food going down here either. Prices may not be rising at the pace they were last year, but I’m not seeing prices go down.

Given that he was a partner at The Carlyle Group & his personal net worth is around $50 million, high inflation is an absolute benefit for he and his wealthy peers.

Jerome Powell knows exactly what he’s doing – it’s a feature, not a bug.

What good has the Fed done since it’s inception?

Landlords have to keep pushing rents. It’s their only lever left. Mortgages are rolling over and the new rates are crushing the mf space.

I was moved to tears, Brick Wall, thinking that landlords only have one lever left.

Dont forget property taxes. Assessments are going to the moon as well as insurance costs so owners/landlords are getting crushed and looking for somewhere to make up the difference

@HowNow,

Yes, the 40% asset price appreciation in the last two years weren’t “real gains”, so the landlords are now poorer in their minds.

My property taxes are up 36% in 3 years.

I don’t know if BW was advocating for LLs or simply pointing out that a lot of pretty stupid LLs vastly overpaid for properties during ZIRP and are now desperately trying to avoid foreclosure by squeezing tenants as much as they can (see rent yield optimizer lawsuits, etc.

Best guess…a lot of misery for both sides (thanks, sh*thead Fed) as rents will soar…but not enough to save the moron LLs (see recent large default of Houston multi-complex LL).

And some seem to think the Fed is not essentially the same as DC pols…if that were the case, where is the Dem focus on soaring rents (largest HH expenditure by far)?

Totally non-existent.

DC almost never addresses real issues…only irrelevant, obscure ones of its own creation/manipulation.

What has the Fed done? It’s obvious. The question I have is what is the connecting thread providing continuity of purpose and action over the 100 years? It is not the individual with a shorter lifespan. The officials turnover so not the multi-generational family. It’s not the charter and mission since they ignore it.

Some multi-generational entity is focusing the function on wealth redistribution. Or is it just individuals taking turns milking it?

50 million @5% = damn good living ,

With 6 million extra persons from south of the border to house, feed, educate & keep healthy, that’s a pretty big incremental increase to inflationary pressures going forward. With Title 42 about to end, it’s going to get worse. for political correctness sake, nobody in the MSM is willing to talk about this growing issue with regards to inflation.

Lololol

BENW are you being serious?

Apparently you’ve never been to migrant housing. They live in the fields in CA or cram like 25 people in shacks.

All so you can buy cheap strawberries

I like how you ignore the 6 million vacant vacation houses too.

I would argues illegal labor is DEFLATIONARY!

Imagine paying field workers a legal wage. You wouldn’t be getting cheap fruit/veggies. That’s for sure.

Same for roofing and every other crap job.

Wolf, maybe in the next rental article you can post a long term rent price chart. I went to Ipropertymanagement.com and pulled up 1940 to 2022. Rent prices averaged +8.85% increase per year since 1980 if they are accurate!!!

I also own rental property and can definitely confirm rent prices are not going down any time in the forseeable future. I have no clue where demand is coming from, but Ive never seen a market this strong.

If the fed is planning on lower rents to fix inflation, get ready for 7%+ fed funds soon

CCCB,

That 8.85% average increase since 1980 is mathematically a BS figure. EITHER They cannot do basic compounding match at Property Management, OR they’re blatant liars.

I looked at their numbers. They said the average rent in 1980 was $245. And in 2022, 42 years later, the average rent was $1,388.

Using a calculator, that’s an annual growth rate of 4.2%, not 8.85%

If the rent of $245 increases by 8.85% every year for 42 years, it would be $8,629 in 2022.

In fact, they themselves showed that this 8.85% number was pure BS in their table of annual rent increases. Look at it, just guessing, you see that the 4.2% is much closer with most years between -1.6% and 4.2%, and a few years with bigger increases.

Rent at $245 in1980

4% over 42 years : $588

9% over 42 years : $1,335

100 x natural logarithm of 2 = 70

70 ÷ annual % growth rate = doubling time

4% doubling time 17.5 years

9% doubling time 7.7 years

@Frick,

Are you, by chance, friends with Michael Engel?

Frick,

You’re not compounding the inflation percentages. You’ve simply divided the total period of 42 years by the doubling periods of 17.5 years 7.7 years and then multiplied that figure (2.4 in the case of 4% and 5.45 in the case of 9%) by the original rent of $245.

The easiest and most exact way to calculate the rent increase over 42 years if you have a calculator is:

1.04 to the 42 power multiplied by $245= $1,272

However, you can use your doubling periods as a way to quickly get very close to the exact answer without a calculator. I’ll use the 4% increase scenario:

Rent doubles twice in 35 years going from $245 to $490 to $980. The increases for the remaining 7 years will average a little over $40 (4% of $1,000) per year, or a little over $280 for 7 years. Adding $280 to to $980 is $1,260, which its very close to the exact answer.

I am so gwaddamn tired of hearing this old crap over and over. No one put a gun to their head, they decided to come over here. They drew the short straw in life and got to be born on the other side of the border. That does not mean every American should walk around feeling guilty. If they stop coming, or come via some legal route, the prices will adjust accordingly and so will the wages and people will buy the damn expensive strawberries. But enough of this guilt trip already!

Using Wolfs 4.2% you get a factor for 42 years of just over 5.6313.

Applying that to $245 yields $1380.

So yes, 4.2% is near spot on.

I lived in Lynnwood Wa during Seattle’s heyday (1996 to 2000), my rent went from $595 to $775 in 4 years, 4 increases.

This comes to a 7% annual increase in a very hot market. Pretty sure rents were going up much less so in the Midwest and other slow economy parts of the country.

That will further entrench and increase the economic disparity in this country and will end the middle class. You are basically advocating feudalism, on a basis to lower inflation.

The solution is much easier than that.

Maybe we should pay a decent wage to real Americans and care about our own citizens.

Inflation can be complicated. The MSM doesn’t do complicated.

People like you always think that immigrants are a drain and a cost to society. Most economists would disagree. Immigrants are workers who pay taxes for benefits many of them will never receive doing jobs that US citizens refuse to do at any reasonable wage.

Yes, but they also put their kids in public schools and someone has to pay for that.

Take an immigrant family with 3 kids in public school at a cost of 10k per child per year.

That is 30k per year.

What low income immigrants pay 30k a year in LOCAL taxes?

Even if everyone works.

The other local taxpayers have to make up the difference.

It’s just math.

Illegals use all the resources that were paid for by the American taxpayer. There is no other way to look at this. If the illegal is not here, then an American will do the job for 2X or 3X. And we will adjust. But sneaking over the border, breaking our laws, using our infrastructure, setting up a shadow economy, driving up the cost for every one via increase vehicle and medical insurance, tying up what used to be summer jobs for kids as a career, is not needed. I paid a guy $165 to fix a leaky tap. White guy, extremely knowledgeable, learnt quite a bit about plumbing from him. So don’t tell me Americans will not do the job. Once the job pays reasonable American will happily do it.

How about increasing legal immigration and make a real effort to stop illegal immigration? Our family and millions of others were proud immigrants who were law abiding. This would hurt the coyotes profits but that’s a good thing.

I was a social worker in a predominantly Hispanic school in a Hispanic neighborhood, with low income folks who were mostly undocumented. The majority chose not to learn or speak English for many years since being here, some did. Yes they are very hard workers! I’ve never seen people work so hard to take care of their families. But every single time we had to do an IEP the district had to pay for an interpreter which was 50. an hr, and some parents didn’t even show up or cancel. The interpreter gets paid anyway. Then there’s the cost of free lunches, ELA teachers, SNAP and Medicaid. If you are a migrant working on the strawberry fields and living in the fields, that’s not much of a cost to taxpayers. But having kids using the system does.

This is a very good question that has NOT been answered SO FAR by the ”growers” that want to have a bunch of ”illegals” as their serfs, as did the Gallo wine and other products since the early parts of the 20th century and continuing.

From what WE, in this case the WE protesting and marching and boycotting WE,,,

in and since the late ’60s have been able to find: Gallo and many others did the worker folks bad and worse, at least since the early days when gallo would hire them and work them for months with promises of pay, then call GUVMINT to get rid of them through various and sundry, apparently approved by GUVMINT.

FWIW, the movement started and continued in the name of Cesar Chavez was IMHO, one of the very great ones similar to revolutions of early USA…

I, for one, will continue to buy ONLY the produce, etc., that have a ”farmworkers UNION” label,,,

OR grow our own… At least to the extent possible.

And to be sure,,,, EVERONE everywhere has the potential to grow ALL the ”fresh” foods needed…

You seem to not be distinguishing between illegal immigrants and immigrants.

Immigrants are our strength as a nation, always have been. They come here with something to offer us and we have the environment for them to flourish. They are a complete boon to society. They pay taxes and assimilate to our country and expand it’s culture.

Let’s not act like we don’t have a legit process to become a citizen.

SOMETHING THAT WE ALLOW MORE OF THAN EVERY OTHER COUNTRY IN THE WORLD COMBINED PRESENTLY.

We allow more legal immigrants than the rest of the world combined.

Illegal immigrants on the other hand, come here with little to offer. Only seeking to gain for themselves, without the skills or ability to do so in a meaningful way. They drain taxpayers resources at a huge clip as they are not taxpayers on income. They typically do not assimilate and bring varying degrees of crime that degrades our country and culture. Physically and financially.

To bring in 10 million with no plan to assimilate them and turn them into Americans, it is the Cloward-Piven theory playing out in real time.

It’s a little complicated.

Immigrants who have skills, speak good English, are under 30 years old, etc. are an asset. Those who never attended High School, not so much.

Since most of the illegal immigrants from Third-World Countries are low-skill people, they are a net negative to the US economy. At this time, most immigrants are low-skill people.

That is to say, most “immigrants are a drain and a cost to society”.

Japan seems to have done pretty well with hardly any immigration.

Australia somehow managed to do well years ago when it limited immigration only to natives of the British Isles.

Would the US be a dump today if absolutely zero immigrants had been let in after 1800? I doubt it.

Escierto – economists work for the man.

Immigrants are one reason that blue collar wages failed to keep up with inflation for so long. I would put it at much higher than the loss of union power, as the effect is often in the areas where the job markets would be hottest otherwise.

Immigrants do pay a fair amount of taxes with a relatively low usage rate. A lot of small towns would be absolutely dead without the population influx. So there are positives.

Immigration, legal or not causes wage deflation. Wage deflation is what Powell wants. And there is a labor shortage.

Immigrants take the lowest skilled/paying jobs, allowing the hotel housekeepers to become wait staff or banquet set up staff. Wait staff moves to lower level hotel desk jobs … and on and on.

Also, all of those immigrants with jobs pay taxes and social security. Illegals pay in too, but they can’t collect at retirement.

Find some facts.

His still not wrong. You may be right that they are a net benefit but that does not take away from the fact that they take up a lot of housing.

I mentioned here before, that part of this inflation started from trump and Covid decreasing legal and illegal imagination.

That’s a little simplistic. Look at supply and demand. More people means more production and more demand. But the production is in low skilled jobs while the demand is in products from higher skill jobs – medical, housing, transportation, schools, smart phones.

Over multiple generations it would even out – allowing immigrants to enter the jobs that produce what they consume – if the US schools weren’t so crappy.

I’d be fine with random immigrants replacing bank CEOs.

I came across a woman in San Diego who was illegal at one time and then became legal

She would work only for cash and then use her zero or low income to get benefits from city county state and federal government.

She never paid anything for social security or Medicare

On paper she does not work and her family is very poor

She has 2 homes in San Diego and moves around in nice cars.

Just my anecdotes

@Jon – we all probably have stories.

A family member at 18 went to Verizon to get a cell phone and service. They told him you already have a line based on you SSN for the past 6 years. So Verizon refused to sign him up even though he had his drivers license and his SSN card.

During the confusion at Verizon, they told this person the actual address of the Mrs Lopez who already had service on his this SSN. He told the police about the identify theft and said he was going to go to Mrs Lopez house and tell her to stop the service. The police told him he could not go and confront Mrs. Lopez and tell her to stop.

We also decided to do a credit check to on his SSN. Come to find out he had a department store card for several years and a 10 year loan in Iowa for about $5k. LOL

No crimes were committed because they are illegal. Basically from what I read a few years ago that illegals do not know you cannot use someone else SSN so it is only a crime if you are a US citizen. If you are an illegal. No harm, no foul.

Your last paragraph is total BS. It’s a crime for everyone. And the police was right: don’t confront the perpetrator because if you do, you can get in trouble, including getting shot; turn them into the police and sue them. That’s all you can do.

Partly true… legal immigrants for the first few years take a lower paying job because they don’t know any better. Once they get a hang of the game, they command the right price. Illegals however know they are breaking the law, so they don’t have a choice, and put themselves in a situation that is quite exploitable. That is why along with proper border control, people caught hiring illegals intentionally need to face some stiff fines and jail time. The illegals are treated like cattle, its like some here in America did not really learn anything from the dark past.

Umm I mean the taxes part isn’t true tho.

A ton of people don’t pay taxes:

Hair stylist, drug dealers, many illegal immigrants, waiters, etc.

Anyone who can be paid in cash.

E g. Concrete contactor paid his illegal immigrants in cash daily.

Some of them DO pay taxes for sure, but not all.

“Also, all of those immigrants with jobs pay taxes and social security. Illegals pay in too, but they can’t collect at retirement.”

This might have been true decades ago, when I believe one on tourist visa could get SSN. I don’t know for sure how it was structured, but I have worked with an older guy, who actually had his own SSN, when he visited his aunt some time during 1990’s. He came back in 2000s and his number was still valid from years prior. He paid taxes, had a US DL, but because he was here illegally he could not collect Social Security benefits.

Immigrants do collect Social Security and Medicare.

In many places, they also collect AFDC and Medicaid.

Since most immigrants are low-skill/low-income people, they pay less into the system than they take out.

The REAL CRIMINALS are people hiring undocumented workers.

People complaining about the tax impact ignore the wineries, farmers, contractos ect. who benefit.

IF they legally paid workers, taxes would be collected for schools ect.

Arguing about tax load on rich vs. poor is a different argument.

Honestly, the poor’s are just exploited by the rich imo.

You really think Sundar Pichi and the like are worth a $1/4 BILLION per YEAR???

CEOs of bankrupt companies get “Retention Bonuses.” (E.g. Hertz shelled out $3 million)

Workers get fired when they fail, CEOs get bonuses.

Be angry at the guy in 105° getting paid $3 an hour though. He “stole” your job.

I have worked with many immigrants in construction,very hard working,but pay taxes . Don’t get benifits no unemployment,no ss no benefits. Only benefits company owners and uncle. That’s why they’re here

Maybe the law has changed but at the time the illegal who used my friends SSN about 5 years ago was not a crime for an illegal alien. Sure, the person stealing and selling his SSN is a criminal but not the illegal Alien who buys the SSN and uses it to work or take out a loan. (hard to believe they do not think it is stolen). The Supreme court ruled in such a case in 2009 and their ruling was the following:

—————————————————-

The Supreme Court has unanimously ruled that an illegal immigrant who used stolen documents to work is not guilty of identity theft because he didn’t know the information belonged to another person.

The ruling eliminates an important tool for prosecuting and deporting illegal aliens who victimize Americans by stealing their identities to get jobs in this country. In its 18-page decision the court says that the crime of identity theft is limited to those who actually know they stole someone else’s information.

It’s not to be politically correct. The media in this country has lost any semblance of integrity. They are in collusion with the government in service to the true masters. Multinational Corporations are running everything now.

Call it Corporatism or Neo-Fascism but whatever else you call it, it’s bad for us.

DC,

In the interests of complete accuracy, maybe you should have noted: “it is currently parked in the ‘insured’ bank accounts of the billionaires and hundred millionaires…”

Really? This is the biggest swindling in US history? US financial history is a story of one swindling after another.

As for the younger generations, they seem to be doing quite well making more money than any generation in history and spending it like there is no tomorrow. To be sure, there are people who are being hurt by persistent inflation but I doubt they are the majority.

Look at the charts of housing affordability. The problem is obvious.

Your view is tainted because you have some kids that are doing well.

If the society as a whole is not doing well then it creates a problem for other people who are doing well

But people usually don’t think this way as most are not able to percent the big picture

I am becoming suspicious that Powell is trying to keep the 5 year below 4.00, since the FVX is used by most community

Banks to market to market their investment portfolios. The AOCI

is applied against Equity.

Very good point that the Fed may be able to/motivated to differentially manipulate different parts of the yield curve.

I don’t think I’ve ever seen this possibility raised.

There has to be limit to the amount of rent increases people can absorb. Even if the Gen Z wünderkind in tech and healthcare world are getting wage increases of 8% to 9% each year to cover inflation, a lot of the rest of us are not.

There is already some mkt blowback…Phoenix vacancies have been rising since October…I’m sure other mkts have seen similiar results.

‘House prices have to come down so Americans can afford houses’ Jerome Powell 2023

There are many culprits, but for #1 see the baby steps Powell tried to take before 2010 but was publicly trashed by the then POTUS and so he caved. This btw was a violation of the incoming POTUS Inaugural Oath where he promises to ‘respect the independence of the Federal Reserve’.

And didn’t. POTUS wanted a negative Fed rate and envied the ECB for having them. Sure, assign some blame to JP but don’t forget Individual One.

The price of housing is never going to go down as long as there are more willing and able buyers than there are houses.

Now, more houses or fewer buyers would drive the price of housing lower.

You’re wrong it’s a supply issue if people quit buying ,every asset depreciates cars,housing food ,gold .But now it’s a merry go round of inflation . Whack a mole is not working

Then why the prices of houses are going down per wR previous articles?

My friend called me and complained that he tried to sell his house last year but he could not.

He told me he priced his home 100k more than the previous sale in his neighborhood but no one bite

Now he says to sell hed need need price it 150k less than his previous asking price

I told him… fire your realtor first and get a good one

“as long as there are more willing and able buyers than there are houses.”

Like I said.

Of course if there was a total buyer’s strike and every potential buyer and/or renter moved into a tent, home prices and rents would go down.

Temporarily.

Everyone has to live somewhere and there are lots of families willing to whatever it takes to buy a house rather than live in a tent.

They will drive the price of housing.

As long as there are more of them than homes for sale the price will go up.

Sure, well he broke about every law we have for a President so that one is an “of course he did”.

It’s really frustrating to me that no one every blames Trump for any of the inflation too. The economic situation is usually or mostly a result of what the last administration did…just like how he enjoyed a decent economy before covid hit despite the boneheaded things he was doing like bankrupting our farmers and adding tarriffs he said the Chinese were paying even though any halfway intelligent person knows this was really like a tax on Americans and the Chinese didn’t pay a cent.

T knew that low rates would juice the economy, that’s all Republicans ever do and sure, stocks go up for a while … until there is a mess from it and the deregulation. Now we are feeling that. Rates should have been raised during T’s presidency and it was obvious but of course T just did the stupid thing that was good for him and just like W left O a mess for the grown ups to clean up, now that’s happened again. R’s are not better for the economy and never have been in modern history, it’s just they are better at the propaganda and this idea has stuck just because they say it despite all evidence to the contrary.

It’s really frustrating that 95% of people can’t even discuss how these things really work never mind form a realistic opinion of the causes and who’s truly responnsible.

Give me s break. Warren, Sanders protégé ?

So middle class and upper middle class who bought homes (and stocks) in 2011 thru 2017 haven’t benefitted ? Some hugely ?

Maybe you should be a politician.

How wonderful it truly would be if our only problem was the actions of the upper 1%.

There are plenty of (is evil a permissible word in today’s unbelievably culturally correct country ? Probably not) bad people, well let me tone that down, sorry, not so good people, ah i feel better, in all classes of our society.

A bigger problem is devious groups.

Groups of all kinds I happen to believe.

Always have been. Nations to gangs and

everything in between.

“Jerome Powell is peddling a fantasy. Every single word out of his mouth about inflation has been wrong.”

What do you expect from simplistic garbage theory used to create garbage models fed with inadequate data points with those being fed manipulated for political reasons?

For a short video on how the Fed can’t possibly predict anything with any accuracy, see the two minute, 48 second video “Minsky Introduction Video” on the ProfSteveKeen YouTube channel.

This is a ‘market failure’ right? The markets mean the private sector is running (ruining) the show. I could be wrong but I’m spotting lots and lots of market failures recently. I can’t wait to see all the excuses from the ‘free market’ crowd blaming it all on government bureaucrats.

powell = lawyer = liar. simple equation.

Inflation is causing a widening of the gap between the rich and the poor. Around here Tesla cars are popping up everywhere. The monster homes are being snapped up by rich buyers. Meanwhile you see panhandlers on every intersection. Homeless tent cities cropping up everywhere. The middle class is getting clobbered. This is a direct result of the Fed policy and the excessive Federal spending. It started with Greenspan 2.0, in 1987, Bernanke made things a lot worse after the GFC, Yellen continued the bankrupt policies of Bernanke. Powell will not have a snowball’s change of correcting the problems even if he did the right things, which he has failed to do. We need another Paul Volcker to restore credibility again.

He’s a lawyer by trade= lyewerjust a different spelling

I’m afraid to ask this question

How many years is it going to take to turn this s**t show around economically speaking.

I have kids my oldest is expecting his first.

Is my grandson going to be in a oligarchical world monetarily.

It looks like that’s where it’s going .

The quality of most things are inferior but worst category goes to cinematic entertainment.

Vacuity shows up in the most prominent places

So much of the “pivot” logic is predicated on the home rental market cooling to 0%. If it re-accelerates instead, it’s going to destroy a lot of the best-laid-plans of “geniuses”. Absolutely ruin them.

Some people seem to think that if they tweet really confidently and point to an excel spreadsheet then inflation will obey them.

This suggests another interest rate hike in July.

Nah, they’re already working on their next lie which is “there is a lag between rate hikes and their effects. We want to be careful not to overdo it, so we believe a pause is the correct move.” Nevermind the fact that it’s already been more than 12 months since rate hikes began. And no, fraudulent bank blowups aren’t an indicator their policies are working.

In general, the effect of the increase is seen between 12 and 18 months, so there is still time.

If they justify themselves with this in the situation that inflation is growing, it will happen as in the beginning when they claimed that inflation is transitory. And then they will be forced to raise interest rates much more aggressively. No matter how cunning they are, they do not want hyperinflation, this should be known

Hyperinflation? Really?

Sorry, man, but hyperinflation isn’t around the corner. Even at 9% last summer, that wasn’t anything near hyperinflation.

In terms of the timing of the full effect, I think the truth lies somewhere between you and depth charge.

Remember, 12 to 18 months is average. There’s nothing average about this cycle. There $13T reasons why that’s the case.

At what % does regular inflation become hyperinflation?

I would agree he’s got much pressure from the ownership classes. But, he’s also cognizant of the dollar. It’s hard to argue against him selling the lag argument but doesn’t want to preside against the dollar

Are destruction.

What makes one cynical is his absolute refusal to sell MBS, he can’t really think he can reduce inflation without draining liquidity and expediting asset deflation. If only to reduce wealth effect consumption.

Blam35, exactly.

Setting a cap when you know you won’t reach it ($35 billion of MBS) is indicative of bad faith, unless you have a plan to sell them or allow more treasuries to roll off to balance it out.

The only reason is to prop up the housing market.

No rate hike coming as DC said.

The real inflation on ground is almost 60 percent plus in last 3 years

It means what costs 100 in 2020 now cost 160 in 2023.

The beauty is if it remains at 160 next year with no wage growth then inflation becomes zero and fed declare victory

The big losers are savers and middle class.

This is not normal inflation and you can call it anything you want

There is no official threshold for hyperinflation

Jon, exactly. Powell is a charlatan. The fact remains, the “2% target” is meaningless if every emergency will be result in mad printing, bringing it to 7-10% per year, unless there is a goal to have years of under 2% inflation (or even, deflation) to make up for it.

So in reality, the 2% target is really 2% during the “good times” and much higher during bad times, meaning it averages out to much higher.

These people are not even attempting to hide their bad faith.

I see comments here about the slow pace of selling MBS. Keep in mind that the Fed is trapped in the MBS market. They cant sell without very large capital losses. That is the whole reason the Fed has not sold off the balance sheet more aggressively and the whole reason they are in BIG trouble.

Imagine that inflation re-accelerates or just doesnt slow down. The unrealized losses on the balance sheet just get bigger and bigger. The Fed NEEDS to see inflation collapse and the economy collapse, so that interest rates can be driven down again.

But this is a catch-22 because part of the reason, which is almost never spoken out loud, that the inflation is raging is that people feel rich from a wealth effect of high asset prices, driven by that immense balance sheet.

China is trying to depose the dollar from its position of power. It might actually happen if the world loses confidence in the superpower of the world.

Time for Americans to wake up and realize that we have been sold lie after lie after lie by the billionaire class. The Fed is an agency that exhibits all the signs of regulatory capture by the industry (banking) that it is supposed to oversee. Powell is a puppet of guys like the chairman of Blackrock.

They better keep raising interest rates until they ring dry all the foolish casino players that we once called the stock market.

After all these are the people that got all the excess money anyway am I not right?

So the stock market had become Wall Street casino.

Dollar Rivers were flowing for a number years.

Not too much trickled down in those years either.

At least from where I sit

At this point I have to question if they want the young to be able to support the old in the US. Ex patriarion looks better and better every day.

With the coming debt ceiling debate they are already targeting the poor for more cuts on food stamps, social security, and increasing the retirement age. No talk of increasing the carried interest tax rate or the taxation of other rent seekers. Plenty of money to bailout stupid bankers too.

The caried interest “loophole” should be eliminated but that doesn’t change the complete unsustainability of government spending. There is no revenue problem in the federal budget. If revenue was 100% of national income, the government would still run a deficit.

Inflated government spending is a big driver of this inflation now by contributing to fake economic “growth”.

Always plenty of money to fight wars which are none of our business. Personally, I wouldn’t spend a dime on foreign aid of any kind. We can police the world but not our country.

2 trillion this year ,astronomical

Or you could revert taxes to what they were 40 years ago.

Hahahahaha.

Tax rates so low in US.

Compare to places like Europe where you’d pay 40% AND a WEALTH TAX.

I can only imagine the tears of the billionaires.

They act like a 1% wealth tax would break them.

1/2 of them are tax cheats anyways. My mom worked for some “upper middle class” (3 mil in property and an 8 figure business) people who hid their millions in the Bahamas.

I see articles all the time about avoiding inheritances taxes ($13 mil+). Oh ya and don’t forget you can gift $17,000 EVERY YEAR additionally. Oh ya and 529 plans. Don’t forget ROTHs.

US taxes so low. Cry me a river people.

Gutting Social Security is the 1%’ers dream.

For the rich to live in peace they need good social security for poor and other benefits for poor

Too many guns…

Don’t forget VA benefit cuts. Within the last year my copay per visit has gone from $5 to $50.

Now I’m reading they want to make drastic cuts to VA benefits as part of the debt ceiling “negotiations”. So much for the conservatives strong support of “our veterans”.

I think a copay of $50 seems reasonable. With no copay or de minimis copay, there is a segment of people who will run to the doctor for every little thing.

There needs to be a disincentive to doing that.

Einhal has never been to the VA.

Imagine going to the DMV. Huge waste of time. Grumpy workers etc.

VA is the worst. Also, they’ll just give you Motrin.

You’re thinking of NICE hospitals lol.

Waterdog – what VA hospital did you attend? Some are bad, some are good. (45 and his gang of 3 saw $ signs and did vets no favors, coming home to roost, now).

(broken record sidebar: if corporations have citizenship, why aren’t they registered for the draft? On the same trail, percentage of taxes paid by varying income groups, would the extremely wealthy man the divisions in proportion to their ownership of the economy?).

may we all find a better day.

Einhal – and what service may I thank YOU for?

may we all find a better day.

91B20 1stCav (AUS),

I think George H. W. Bush was the last time I saw an elite American put his body in harm’s way. I would be happy to hear any other examples. But everybody seems more into the fancy, tough talk now. I missed serving in ‘Nam by a couple years. But I am darn thankful for everybody who stands ready, and willing to pay my share in taxes.

As for me I made the money, that paid the taxes, that paid the armed forces bills. What is with that question? Why the capitalize YOU? It is almost like you expect some reward in addition to the compensation and status you get for volunteering for an armed force? And seek to shame those that did not make the completely voluntarily decision to make a commitment to an government entity and in return get compensation, education, medical care, and social benefits. My grandfather (WWII and Korea) and best friend (Iraq x2, Afghanistan x2, Congo x1, Balkans x1 and etc.) are 20 year men and both agree they got / are getting compensated for their service.

Venk – fellow citizen, you presume, and might need to acquire a bit more history (I can feel Wolf moderating this potential slagging match, couldn’t blame him if he does).

You speak of ‘volunteering’. The ‘AUS’ in my handle refers to ‘Army of the United States’, the component of those who were DRAFTED (as opposed to ‘RA’: Regular Army’, we all bled the same). The ’91B20′ was my MOS (military occupational specialty), at that time ‘ambulance attendant’, the ambulance a Huey or an M116 or the battalion aid station. ‘1stCav’ I think, with a bit of research, will let you work out the timeline and what the job entailed…

I helped some make it home, some I couldn’t, and too-many never saw twenty-five, to walk the streets of our nation to ‘make the money and pay the taxes’-their lives having been cashed out, or broken in our name. I was lucky, did my time, and whaddya know? Came home to eventually make a little money and pay taxes from the jump, just like you. So did thousands of others.

But to never, ever, forget those who wore the uniform, then and now, most of whom weren’t or will never be ’20-year men’ (or women) but ones who did their two, three, six, or more, who could always be assigned to the spearpoint with no guaranty of return alive or whole.

Ah, now for me, the ‘service’ comment, my failing, obviously. Over the years the subject rarely arose, but more recently, when it does, so many of the comments of: ‘thank you for your service’ became so palpably rote that my response became one (as I directed at Einhal) of hoping to hear a rejoinder of someone’s efforts for our common good or problem-solving, and NOT necessarily military. Am I shrill, here, no doubt, but I don’t need to quote my ancestral military cv (dating back to the Civil War) as evidence of my own service or an excuse for Congress to look the other way. Pray, sir, may I thank YOU for some form of service you have performed? Not saying I would expect it, though wonderful to hear, but don’t think for a moment that I’m trying to cheat you of something because I asked…(still making a little money and paying taxes, btw…).

May you always experience a peaceful life, and may we all find a better day.

Boy, the copium is sure flowing. There is no way around it. Housing is now one of the predominant drivers of CPI. You can correct commodities so far, but until housing is allowed to fall dramatically back to sanity, inflation continue to spiral out of control.

There are only two options to go from here here: A) crash the housing market, or B) prop up the housing market using some “unprecedented” Frankenstein financial meddling and let rent prices rip up to meet the bloated house values.

Option A will mute or even end inflation but will make Wall Street and the Real Estate parasites weep and gnash their teeth.

Option B will continue to harm poor and young people and will enable the asset collectors continue to live like fat cats.

Parasites, indeed.

Your comment is my opinion. The question is – what can we the normal people do to support option A. I am tired to sit and observe.

weld your wallet shut

You forgot option C, the one that the Fed is aiming for… Hit the brakes on QE, but keep interest rates manageable and let the now more numerous dollars find their new actual value over the next several years. Assets will find a higher price and so will labor, albeit at an increasingly disadvantaged ratio.

Disinflation is the best we can hope for and deflation is plainly not allowed. The ever-present specter of inflation marches on. Given enough time, we’ll all be millionaires when a loaf of bread costs a thousand bucks.

The big problem is that financing for the housing market is a rigged game. The bankers that originate these loans dont keep them on their own books, so they dont really care about market bubbles. Package them as MBS or sell them to Fannie/Freddie. Get rid of the risk and keep the fees.

This is a HUGE scam.

Solutions to the housing crisis.

– Cut regulations on building. 1/4 of the cost of a house is due to regulations. 98K per house.

– Eliminate the mortgage interest deduction over time. This gives an incentive that distorts prices.

– Privatize the mortgage market and force all originators to maintain the risk on their housing financing.

We want to see a vibrant building industry that replaces older homes with better living spaces and we want to see land prices plummet, since high land prices adds zero value to the economy.

Are local Governments housing illegal immigrants? There is supposed to be an influx of folks at our borders and they are busing them north. Would this folks be taking up rental units?

No.

It would seem on the surface that the illegal immigration that has occurred and is occuring is inflationary.

In northern cities those immigrants are generally housed in hotels at very high costs. Landlords generally will not house anyone without an income history.

Yes they are. There are several in my complex now. They get free rent and we pay for it in higher taxes, higher rents and higher crime. The cashiers in my grocery store say they have EBT cards with lots of money on them.

There is no way a cashier knows the balance on an EBT card. It doesn’t show.

Maybe the same person purchases lots and lots of stuff?

Nope. It’s available to them. I hear about it all the time.

There was section 8 during 44’s term. I recall several busloads were turned back in Temecula, Ca. Government will subsidize renters (as corporate landlords well know – most of the affordable housing built it not really affordable). There are empty internment camps built during 43 on the contingency of collapse and a large influx of refugees from Central America. They also proposed a trillion dollar wall. Remember Mexico has about 1/3 as many people as the US, so the immigration problem is really the other way.

Mexico is a retirement destination for those priced out of the American dream.

Not anymore. Many better places out there.

Mexico is going to be for the next 40 years what Columbia used to be back in the 1980’s. A narco state heading towards failure.

Full legalization in the US would eliminate that worry.

Section 8 housing assistance has been around for at least 40 years that I am aware of. I delt with it all of my working life as a property manager.

This is why renting is going up= uncle involved it’s a scam

A few folks in El Paso may have a different opinion.

The issue most everyone refuses to acknowledge is that the majority of the illegals coming over any boarder to the USA are not Mexicans. Now days the majority are not even from the America’s, period. They come from places like Somalia, Yemen, Pakistan, China, etc.

Illegal aliens (often called refugees) are economic warfare. They degrade the economy and standard of living in any country they migrate to. This is a fact. This is also why EVERY country has laws against illegal immigration.

If the USA enforced its immigration laws like Canada or Mexico does the entire world would be infuriated.

And employers would be infuriated as well. They would be very upset if they were forced to hire only legal immigrants.

I agree, punish those who employ them! If they didn’t employ them they wouldn’t be coming over.

Boss Tweed had this process all figured out.

When people have more money they can afford a bigger apartment. In ny there was a uptick in demand for one bed room apartments. Many of the same people one would have rented a studio could now afforded a one bed room so prices spiked.

I am sure this dynamic happens in all markets in one way or another. So one way for more inventory to come online is downsizing, which does not appear to be happening at this time.

Some of it is multi-generational living. Millennials still living at home and working is still a big thing, especially since these young people don’t seem to get married anymore. Big reason why David’s Bridal went bankrupt recently.

Just saying, rents in Phoenix are soft. And demand is soft too — so they aren’t up everywhere.

Forget “asking rents.” They’re meaningless. Actual rents at lease renewal and rents of newly signed leases matter. If you look at asking rent data — Zillow, Zumper, Apartment List, etc. — you will be misled.

Sample Size = 1

Rent went up 6.25% AND I have to move within the neighborhood.

(Owner of my unit wants to come vacation during the winter).

At least the double digit increases are out and things are slowing.

Fingers crossed for next year.

I’m not in PHX or AZ btw. Realized it was a bit misleading.

What evidence do you have that rents in PHX are falling? I just got back to PHX for a visit and that’s not the story I’ve been hearing from all my friends.

Demand here is through the roof in everything from what I’ve seen

My doctor emigrated from Arizona,to Nebraska 15 years ago,said it’s the best thing that ever happened to him

If moving to Nebraska was the best thing that ever happened to your doctor, he must have had a pretty sh!tty life.

Maybe he’s doctoring Uncle Buffy and Uncle Charlie.

Doctors make more COLA adjusted in the Midwest.

It’s geo-arbitrage. Kinda like the WFH people who left CA.

Tangent: Doctors are a bit of a scam tbh. They have too much pricing power. I blame the APA and the medical school structure. High barrier to entry = $$$

El Katz it was quality of life ,as explained by him

All the homeless people make a case for why rents will continue rising and never bend. I do find it funny the belief people have that rents will keep rising AND home prices will fall – fat chance, as the only way to escape the rent rat race is to own your land. (If you live in California this message does not apply, that place is fucked 😂).

“I do find it funny the belief people have that rents will keep rising AND home prices will fall…”

This seems logical to me… have you seen Wolf’s OER VS CS home price graph? Huge divergence in home vs rent prices, which can only be resolved by some combination of lower home prices and higher rents.

Another angle to consider: higher home prices must pull up rents, as the carrying costs increase proportionally (taxes & insurance) and there are now other ways to earn a similar yield (short-term treasuries).

Landlords need to make a profit, otherwise they won’t be landlords for much longer.

I’ve seen all the charts. Data is not one sided there are different interpretations.

Everybody talks about landlord losses, nobody talks about homeowners who I bet paint a much larger picture. Any new buyer can pay off their mortgage in as few as eight years by doubling their payment. I’ll be free of the rent wars or the mortgage wars by decade’s end. Anybody serious about their own wealth or even FIRE should too.

As far as overvaluation, I don’t buy it. The median salary is $69,000 in the US, while the median home price is $428,000. Those don’t sound like crazy numbers to me. A little bit of saving/compounding against your amortization can go a long way – I remain bullish in at least 49 states :)

Median US salary is $54K, so, yes ~8:1 mortgage:income is crazy high, and shows that US RE is way overvalued.

Better to look at median household income, it’s around $71K, which gives a 6:1 ratio, which is still way overvalued.

Appletrader:

Why would someone pay off or double-payment a sub 4% mortgage, when treasuries can net you more than that after taxes?

@Ltlftc

True, however both are currently yielding a negative real return.

These numbers in isolation are relatively meaningless. You have to look a realistic cash flow to determine whether something’s affordable or not.

Someone with a salary of 69k is probably bringing home 3500/mo in takehome pay, assuming an average state income tax and a small amount going into 401k. Plus benefit premiums.

A 428k house will carry a mortgage payment with current interest rates of about $2500. That leaves someone just $1000 a month for all other expenses. It’s basically an impossibility. With car prices through the roof, that homeowner won’t be able to eat.

Of course I don’t think it’s a fair premise to suggest that a median earner and a median homebuyer are the same person. A median homebuyer is probably someone in the ~65th percentile for earnings? Just guessing here. That’s an income of about 101k, and a monthly takehome of maybe 4500 after moderate retirement contributions. Leaves 2000 after mortgage payment. Not a lot of breathing room when car payments are through the roof, inflation is bonkers, etc. Definitely doesn’t leave much room for additional savings, vacations, pets, kids, etc.

I’d call that house-poor.

Appletrader:

I’ve never understood “real return” arguements. Real rate of return zero point is just an arbitrary number, unless you honestly think government inflation data is 100% accurate. Even then, still only useful as an arbitrary zero point on spreadsheets.

It’s all relative. Either it’s a better use of homeowners funds or it isn’t.

“Well you see officer, i was going 60 in a 25 but the earth is moving through space, so actually…”

That is one of the most ignorant comments I’ve ever read…you do understand debt inflates away and becomes more irrelevant? That buying power decreases every year, hence why gasoline used to cost $0.30 half a century ago? As a debt holder you do not want to be lending out under the rate that money holds its value. By the time you get your “4%” yield, the money can only buy you 95% of what it could a year ago. If you don’t believe me buy 30 year treasuries and see how useful that money is when it’s returned to you (not financial advice).

Btw if the government is underreporting inflation that makes the real results much, much worse. For everyone’s sake let’s hope treasuries are in fact giving a near breakeven return.

Appletrader:

“you do understand debt inflates away and becomes more irrelevant?”

I do, which is why I thought this remark was silly:

“Any new buyer can pay off their mortgage in as few as eight years by doubling their payment… Anybody serious about their own wealth or even FIRE should too.”

I’m not sure more back and forth will bear fruit, as we’re back to the original statement in question.

Any new buyer can pay off their mortgage in 8 years. Sure, ok

Appletrader,

“I do find it funny the belief people have that rents will keep rising AND home prices will fall…”

It happens, including last time and now:

Fair enough, but I’m skeptical. I think the lion’s share of that divergence will be met by the red line – we shall see

If rent prices didn’t go down after the Housing Bubble #1 low, they’ll never go down.

What WILL happen after Housing Bubble #2 blows – if it ever does – is real estate investors will go back to making 20%+ returns on their properties, like after the first bubble.

If this isnt an incentive to own your home (and rental property), nothing is.

Great point @CCCB. Oddly enough someone who bought in 2000 exclusively to landlord never took a hit on their rental income during the GFC. It just kept chugging along, year after year.

There’s simply no reason for rents to ever, ever drop – take the homeless as the demand side of the equation, they’d love to live under a roof but can’t afford it. Unfortunately for them someone else can, someone with even greater incentive to NOT live out on the street. It’s a mess and those who own nothing will get screwed hardest by inflation.

Appletrader and CCCB,

Not “Great point @CCCB.” You both make a huge error. You assume that you own rental property that is spread across the entire US – because you’re looking at national US rents. But your rental property is not spread on average across the entire US.

If you bought rental property in 1985 in Tulsa OK, you would have watched rents decline for 15 years. And by a whole lot.

In San Francisco, rents plunged about 25% during the dotcom bust and they didn’t get back to and above the dotcom bubble highs until 12 years later.

There are lots of cities like this. But since they all happen at different times, it tends to average out.

But a landlord doesn’t own property in the average US market. Landlords have to deal with their local market. In some local markets, rents rise while they fall in others, and the national average might go up.

So rents DO go down in local markets, for many years, and by a whole lot. And as landlord you have to deal with that.

If you cannot see this, you’re fooling yourself about real estate and rents.

The reason rents are surging is because interest rate rises have completely priced people out of buying and it’s created a demand spike. Mortgage availability has just dropped from (ballpark) 6 times household income to only 4 times and many people are renting because buying that property is no longer an option. Landlords will push the envelope as much as they can, but ultimately their tenants simply don’t have the income for rent to rise to match owners equivalent without house prices also coming down substantially.

It could create some interesting price effects. In my area, houses in the 1-1.5m range are selling like it’s still early 2022 (multiple offers and sold on the first weekend). There are plenty of 300k income households around here that can handle that. But houses in the 2.5m range that last year were also going in the blink of an eye are really struggling to shift. 500k income households are much rarer, and potential upsize buyers are balking at the huge additional mortgage costs they’d be facing. Meanwhile, investors would be getting a terrible yield and the likely prospect of equity loss to boot. Sellers trying to get over 3m are now screwed. As are the house builders in the area, who universally were targeting that 2.5m+ market.

So, it’s simple – just wait until the Case-Shiller reverts to touch the mean of CPI Owner’s equivalent – that should approximate the bottom of the house price index fall…..

It’s not that simple IMO or we’d all get rich beyond our dreams. For example if inflation resurges like many here believe it will, we can say goodbye to cheap homes forever.

I messed with a CPI calculator yesterday – 100 years ago you could buy a median home for $10,000 (equivalent buying power to around $350,000 today). If this trendline continues the average home will cost $10 million by the turn of the century.

Homes are an inflation HEDGE, do not forget that. The chart showing the divergence last time was during low inflation so perhaps homes were indeed overvalued relative to their rents. Such inferences should be made with caution today

Is it the home itself that’s the inflation hedge, or is it the mortgage (long term fixed rate debt in an environment of inflation & rising rates)?

Think about it.

@MM

Both. I’d even add a third hedge: avoiding rising rents, though for arguments sake (I’m aware of the divergence), let’s be safe and say these three benefits together take at least seven years to materialize.

USA Today had an article March 3.

Referenced a report from rent dot com.

Stated January median national rent was $1942. Prices peaked in August 2022 at $2053.

Prices peaked in August 2022 at $2,053.

Yes, short timeframe 6 months.

Many have pointed out apartments have been recently built at the fastest rate since the 1970s.

These are “ASKING RENTS.” read the g*d d**m f***ing article (RTGDFA) and what it says about “asking rents.”

You’re dragging BS into here.

What goes up must come down. Always. The Corona boom will be paid for with a Depression and a crisis. Probably both, given the pathetic financial state of the US. Because of corruption they will try to make it the poors’ problem first, which will cause social instability. There’s simply no way out.

My rent in CA had been increased aggressively in 2021/22. It was up to $2600/mo for a 1700sqft drywall & stucco box in a sort of OK part of the Inland Empire suburbs. When I told the landlord I was ditching CA and gone for good a few months ago, she was delighted! It was an opportunity for her to get a big jump in rental income. She barely cleaned it up (if at all) and put it right back up for $3,000/mo and she filled the vacancy within a couple weeks with a immediate long line of prospective tenants to choose from.

Good riddance. Why anybody would pay $3k each month to live in that traffic pit with fentanyl zombies roaming nearby is beyond me, but apparently lots of people are more than happy to sign up. What a bizarre situation… Wonder if it has anything to do those several trillion new dollars floating around?

Just for perspective, I moved in at $2000/mo in Oct 2019. By the end of Jan 2023, a new tenant was moving in at $3k with no improvements to the house. That’s a 50% increase in just a little over 3 years.

If I could sell my house for 2022 prices then I would have and rented a house in western burbs of Chicago but no rentals in my school district.

Just to give a different perspective, in SF East Bay, we moved out of a SFH rental in fall 2022, and the new tenants are paying less than we did. And renting is still way cheaper than buying.

I have heard of tenants making under the table deals with landlords if the tenant agrees to move out, in rent controlled areas. This can be a substantial sum.

Yes, it can be a substantial sum. But it’s not under the table. It’s standard open public legal practice. A landlord can offer a big cash payment to a tenant to get them to leave. Happens all the time in California. Nothing wrong with it. Tenants don’t have to accept; they can just stay. And then the landlord will have to jump through expensive legal hoops to try to get the tenant out. So it’s usually cheaper and a lot faster (which is a big cost savings too) to make a big cash offer.

I wonder how many long-time renters in rent-controlled areas:

1. Sublet to get money from roommates that more than pays the rent.

2. Leave the unit but keep the lease, and rent it to someone else at twice the rent.

3. Airbnb it.

I’m also near LA and a house a few blocks away was listed for 255k and sold quickly for 263k. It was then listed for rent at 2100 and was gone in an instant. The rentals in this area were like 950 to 1050 not that long ago. But you can be in Malibu in like 90 minutes so there’s that. Lots of Texans moving to this area believe it or not

Instead of allowing asset prices, specifically real estate to fall, they will offer subsidies. These subsidies will transfer wealth from the taxpayer to homeowners and to landlords. They will also encourage

immigration to create demand even though it results in higher prices.

Idiotic government housing policy makes housing unaffordable.

Same as with medical care and “education”. Wait until the government further subsidizes childcare.

What government housing policy? FhA loans?

Section8 look it up

Absurd. Theres absolutely no shortage of demand in any housing front.

They will encourage immigration though, to depress wages.

If there’s no shortage of demand, why have prices fallen from the peak? Why are active listings are growing? Why have days on market have gone up?

Demand is really now in current env. Sure peoples needs and wants are there but demand is low.

Demand for buying homes has decreased, demand for housing has not. Hence why rent is continuing to skyrocket. Increasing interest rates rapidly increased the cost of buying a home, rent is racing to meet it, and when it equalizes youll have the renters once again making the choice between renting and owning, just instead of housing costing 30% of their income it will be 40 or 50%.

Its why vacancy rates are at an all time low.

“why rent is continuing to skyrocket”

“why vacancy rates are at an all time low”

Man, you must live in an alternate universe.

Can confirm. Small landlord of SFHs. 3br, 2ba, 1100sqft homes that rented for $900/mo just three years ago now draw $1600/mo all day long. No let up in demand. Add another $50/mo for pet fee per pet…

Unbelievable really, but here we are and they have the money.

The only way prices go back to pre-pandemic levels will be if there is a really bad recession. Interest rates alone are not strong enough, the only thing that will kill the current inflation are the deflationary forces generated by a recession or worse. The Fed is completely responsible for the present hot mess due to its massive increase in the Fed balance sheet and monetary expansion.

Nope. Just look at the trend in the data. It won’t be long and we’ll be back to prepan levels and beyond. Interest rates are more than enough to do this. Don’t forget the 10 to 1 relationship between rate and loan amount, roughly speaking. That effect is huge and it is why we are seeing rapid declines now, and it’s also why people are choosing to rent.

Yup.

In my area, you can rent a ~$1.3M house for around $4.2k. $4.5k will get you something close to $1.5M of house.

To be fair, there are also landlords in the thick of delusions, asking for $5k for something smaller and less desirable in the same areas. They’ve been asking that for many months now.

Exactly.

RJ Talks (video) a few days ago referenced Redfin or realtor dot com. Home prices down in almost every city in the country. Most less than 10%, some less 5% but out west (Seattle, CA cities especially north, Denver, Boise, Austin, Las Vegas, etc ) often over 10% down from Spring 2022 peaks.

Amazing how so many in comments sections say their area is doing great.

Wacky movement in all kinds of prices, houses included, should be expected after the totally unprecedented money printing binge and economic upheaval that has taken place recently. That being said 5%-10% drops in the national median house price are really not abnormal.

On decadal time scales, the price trend is ever-upward with the devaluation of the dollar, which has never had a long meaningful bout of deflation. From ’70-’80, the median price tripled. From ’80-’90 it doubled again. ’90-’00 saw an increase of “only” around 50%. With the GFC in the middle of it, the median still went from $163k in ’00 to 220k even at the bottom of the housing collapse.