Housing inflation is peaking at 8%-plus.

By Wolf Richter for WOLF STREET.

The Consumer Price Index (CPI) for March, released today by the Bureau of Labor Statistics, was marked by plunging energy prices and surging services prices. Food inflation slowed, and month to month actually dipped for the first time in nearly three years. But durable goods inflation month-to-month suddenly rose again, after having been negative for six months, reminding us that inflation is a game of Whac A Mole:

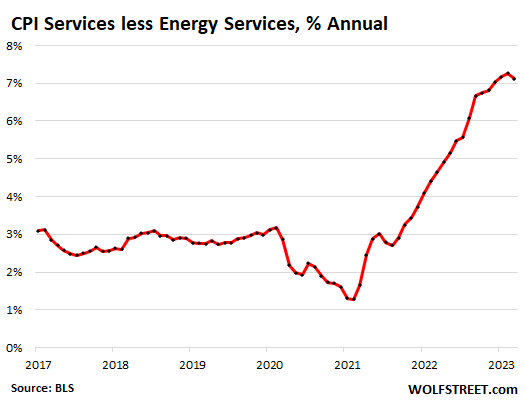

- Services without energy services: annual inflation jumped by 7.1% from a year ago, after the four-decade high of 7.3% in February, driven by housing, food services (food away from home), auto insurance, repair services, airline fares, pet services, and hotels.

- Food at home: inflation dipped in March from February (-0.3%), the first dip since November 2020. Year-over-year, prices increased at the slowest rate since January 2022 (+8.4%).

- Energy inflation plunged month to month (-3.5%), and year-over-year (-6.4%), driven by a plunge in prices of gasoline and natural gas.

- Durable goods prices rose month-to-month (+0.4%), the first rise since last August. Year-over-year, the index dipped at the slowest pace this year (-1.0%), on a smaller price decline in used vehicles and price increases in new vehicles and household furnishings and appliances.

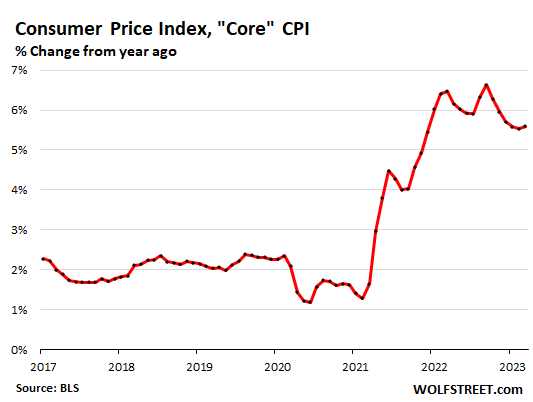

- Core CPI: rose 0.4% month-to-month, in the same range for the fourth month in a row. Year-over-year, core CPI accelerated again (+5.6%), after decelerating since September.

- Overall CPI (CPI-U): +0.1% month-to-month, +5.0% year-over-year.

“Core” CPI.

Core CPI – without the volatile food and energy products that consumer buy – jumped by 5.6% year-over-year, hotter than the 5.5% increase in the prior month, and the first year-over-year increase since September:

Month-over-month, core CPI jumped by 0.4%, driven by raging inflation in services, and now suddenly by a jump in durable goods inflation.

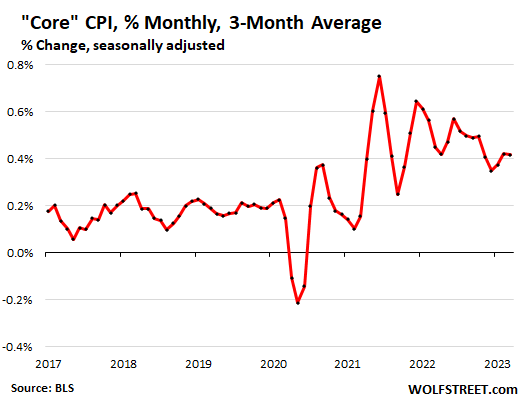

To see the trends amid these big monthly ups and downs, here is the three-month moving average of core CPI.

Core Services inflation (without energy services).

The CPI for services inflation without energy services jumped by 7.1% from a year ago, after the 7.3% jump in February. This was the fourth month in a row at 7%-plus, the highest range since 1982. Nearly two-thirds of consumer spending goes into services.

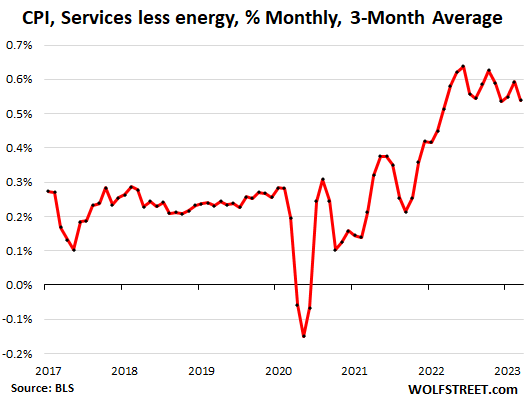

Month-to-month, services inflation without energy services jumped by 0.4% in March, down from the 0.6% jump in February. Month-to-month moves are volatile. The trends show up better in the three-month moving average of the month-to-month changes, and you can see that it has slowed in recent months just a tiny bit from last summer and remains at about double the rate before the pandemic:

| Major Services without Energy | Weight in CPI | MoM | YoY |

| Services without energy | 62.1% | 0.4% | 7.1% |

| Airline fares | 0.6% | 4.0% | 17.7% |

| Motor vehicle insurance | 2.6% | 1.2% | 15.0% |

| Motor vehicle maintenance & repair | 1.1% | 0.3% | 13.3% |

| Pet services, including veterinary | 0.5% | 0.5% | 8.6% |

| Food services (food away from home) | 4.8% | 0.6% | 8.8% |

| Rent of primary residence | 7.5% | 0.5% | 8.8% |

| Owner’s equivalent of rent | 25.4% | 0.5% | 8.0% |

| Postage & delivery services | 0.1% | 0.3% | 6.7% |

| Hotels, motels, etc. | 1.0% | 3.1% | 8.1% |

| Recreation services, admission to movies, concerts, sports events | 3.1% | 0.0% | 5.9% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.4% | 0.5% | 5.3% |

| Water, sewer, trash collection services | 1.1% | 0.3% | 5.4% |

| Video and audio services, cable | 1.0% | 0.9% | 5.8% |

| Medical care services & insurance | 6.5% | -0.5% | 1.0% |

| Education and communication services | 4.9% | 0.3% | 3.3% |

| Tenants’ & Household insurance | 0.4% | 0.0% | 0.9% |

| Car and truck rental | 0.1% | -3.8% | -8.9% |

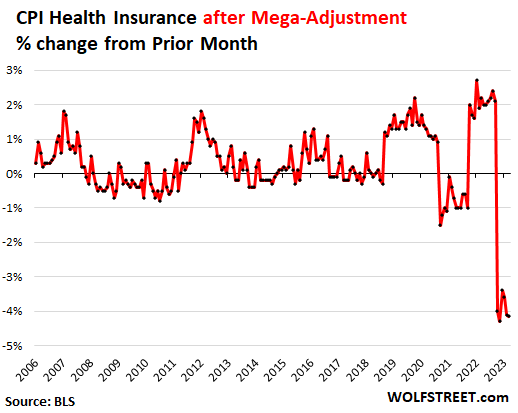

Reminder: Health insurance mega-adjustment understates CPI, core CPI, services CPI, and Medical Services CPI for another six months.

BLS undertakes annual adjustments in how it estimates the costs of health insurance and then spreads those adjustments over the following 12 months. For the 12 months through September 2022, CPI overestimated health insurance inflation (+28% yoy in September 2022). That over-estimation has been getting deducted every month, starting with the first mega-adjustment in October 2022 (more here),and this will continue through September 2023.

This mega-adjustment of the CPI for health insurance understates overall CPI, core CPI, services CPI, and Medical Services CPI.

So the CPI for health insurance plunged by 4.2% in March from February by 10.7% year-over-year.

The Fed’s favored inflation measure, the PCE price index, figures health insurance inflation differently and didn’t suffer these adjustments.

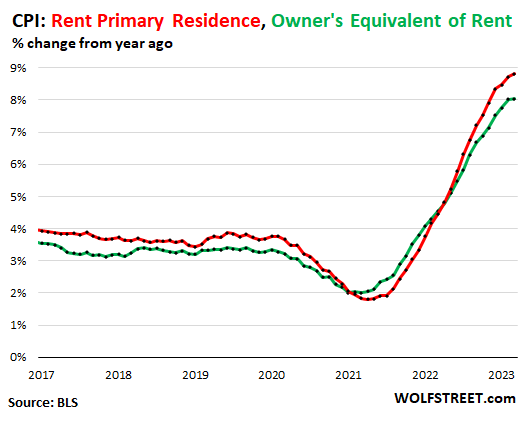

The CPI for housing as a service.

The CPI for housing as a service is based on rent factors, primarily “Rent of primary residence” (weight: 7.5% of total CPI) and “Owner’s equivalent rent of residences” (weight: 25.4% of total CPI).

“Rent of primary residence” tracks actual rents paid by tenants in houses and apartments, including rent-controlled units. The survey follows the same large group of housing units over time and tracks what tenants in them are actually paying in these units.

Not “asking rents.” Other rent indices, such as the Zillow rent index, track “asking rents,” which are advertised rents of vacant units on the market. The huge double-digit spike last year in asking rents never fully made it into the CPI indices because rentals don’t turn over that much, and proportionately not many people actually ended up paying those spiking asking rents. Now those asking rents have backed off from that spike, but this backing off won’t be fully reflected either since the spike wasn’t fully reflected to begin with.

“Owner’s equivalent rent of residences” tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for.

Both rent factors jumped:

- Rent of primary residence: +0.5% for the month, + 8.8% year-over-year, worst since 1982 (red)

- Owner’s equivalent +0.5% for the month, +8.0% year-over-year. Along with February (+8.0%), the worst in the data (green)

We can now see that the month-to-month increases are less hot than they were, and that year-over-year the two measures are now peaking.

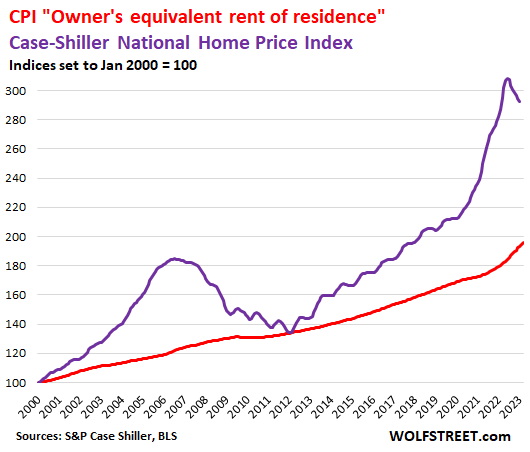

Compared to Home prices: The Case-Shiller Home Price Index peaked with the report called “June” then started to decline [by city: The Most Splendid Housing Bubbles in America]. The most recent data point is the three-month moving average of November, December, and January (purple in the chart below).

The red line represents “owner’s equivalent rent of residence.” Both lines are index values, not percent-changes of index values:

Food inflation.

The CPI for “food at home” – food bought at stores and markets – fell by 0.3% in March from February, the first month-to-month decline since November 2020.

Year-over-year, the CPI for food at home rose by 8.4%, the least-hot increase since January 2022, after 12 months in a row of double-digit increases. Most major categories booked month-to-month declines. Egg prices, which had spiked during the avian flu price distortions, are making their way back to earth.

| Food at home by category | MoM | YoY |

| Overall Food at home | -0.3% | 8.4% |

| Cereals and cereal products | 0.6% | 12.8% |

| Beef and veal | -0.3% | -1.9% |

| Pork | -1.1% | -0.6% |

| Poultry | -0.4% | 7.5% |

| Fish and seafood | -1.2% | 2.6% |

| Eggs | -10.9% | 36.0% |

| Dairy and related products | -0.1% | 10.7% |

| Fresh fruits | -1.7% | -1.5% |

| Fresh vegetables | -1.7% | 1.4% |

| Juices and nonalcoholic drinks | 0.3% | 11.7% |

| Coffee | -0.4% | 10.3% |

| Fats and oils | -0.6% | 15.9% |

| Baby food & formula | -0.4% | 7.6% |

| Alcoholic beverages at home | -0.2% | 3.9% |

Energy prices:

The biggest part here is the plunge in gasoline prices after the crazy two-year spike that is now getting unwound.

| CPI for Energy, by Category | MoM | YoY |

| Overall Energy CPI | -3.5% | -6.4% |

| Gasoline | -4.6% | -17.4% |

| Utility natural gas to home | -7.1% | 5.5% |

| Electricity service | -0.7% | 10.2% |

| Heating oil, propane, kerosene, firewood | -2.5% | 10.8% |

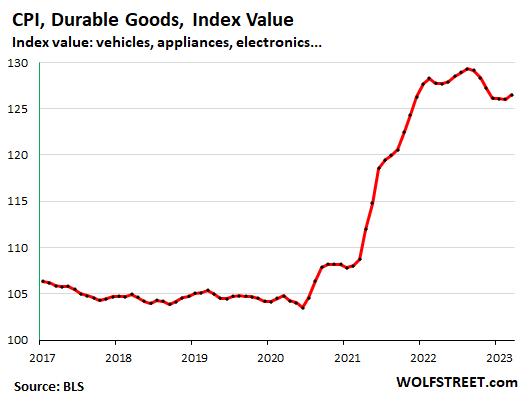

Durable goods prices: first increase in six months.

In a very unwelcome development, the CPI for durable goods rose month-to-month for the first time after six months of declines. This increase reduced the year-over-year decline to -1.0%. It may indicate that the decline of durable goods prices has already bottomed out.

Durable goods were a big force in pushing down core CPI, while services were pushing up core CPI. If durable goods prices are taking off again, it would be a very unwelcome development, but would be typical for entrenched inflation, which is like a game of Whac A Mole. By the time you hammer one down, another one pops up again.

The CPI for durable goods, expressed as index value (not as percent change) shows the spike in late 2020 through mid-2022. Prices started to drop last fall, driven by sharp declines in used vehicles and consumer electronics. But in March, prices rose again:

I want to point out that wholesale auction prices of used vehicles have been rising for four months. There is normally a lag of a couple of months before changes in wholesale prices show up in retail price measures, such as CPI. The wholesale-price increase hasn’t shown up yet in CPI. This may still play out over the next few months.

| Durable goods by category | MoM | YoY |

| Durable goods overall | 0.4% | -1.0% |

| Information technology (computers, smartphones, etc.) | -0.4% | -11.5% |

| Used vehicles | -0.9% | -11.2% |

| Sporting goods (bicycles, equipment, etc.) | -0.6% | 1.1% |

| New vehicles | 0.4% | 6.1% |

| Household furnishings (furniture, appliances, floor coverings, tools) | 0.4% | 5.8% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Gas upwards of $5 in Phoenix. Gasbuddy today says average is $4.73. Went up from $4.37 at Costco a couple days ago to $4.45 today. Rents increasing as well, 25% in some cases.

Yes, core cpi rising again. Oil rising after production cuts. Rents jumping really high. My bet is that inflation starts increasing again in April.

Some super-irresponsible statements made in mainstream media today:

1. Warren Buffet claiming that there is a government put on all bank failures irrespective of how irresponsible these banks become. It will encourage banks to make more irresponsible fed Pivot bets.

2. Mainstream media again claiming fed will stop hikes as of inflation is defeated.

So, how bad is fed at its job? Bitcoin is up 80% this year. That bad regarding speculation. Any pause in rate hikes now will push inflation straight into double digits.

Bitcoin still down significantly from peak… Over 50% Arkk down even more so it’s early innings here

Nasdaq is down 25% from peak, many good productive companies are dow 50% from peak. These companies are not crap.

Bitcoin is crap. It being down on 50% from peak and rallying 80% since start of year shows that “dollar denominated crap competes well with dollar denominated assets”.

That makes everything dollar denominated look bad and makes me worry about our future.

If Fed can’t let Bitcoin fail, speculation will win.

“down 50% from peak. These companies are not crap.”

A company may not be crap but still be hugely overvalued.

From at least 2015 on, the SP500 was at least 40% overvalued (PE of 25 vs. Long term avg of 15 – due to Fed ZIRP).

As unZIRP takes hold, even “good” companies are going to see share prices fall…because they were radically overvalued to begin with.

At today’s interest rates, the vast majority of SP500 companies with PEs well in excess of 15 are on borrowed time.

(There are plenty).

“Gold was the enemy to me because that was a speculative vehicle while I was trying to hold the system together.”

Paul Volcker

All of the gold ever mined in the history of the world is just a tiny grain of sand compared to global assets and amounts to less than 1% of assets even at current absurd gold valuation.

The lesson I take from history is when the current economic system is completely dead and gone, gold will still have value.

Leo,

BS on the Buffett comment.

“We’re not over bank failures, but depositors haven’t had a crisis,”

Equity and bondholders can be wiped out, a la SVB.

*Depositors*

He’s basically saying FDIC insurance is gonna cover all tho (which Yellen did do, but says maybe won’t happen in the future).

Your comment implies bond and equity will be made whole, which is NOT what Buffett said.

Yellen:

“I have not considered or discussed anything having to do with blanket insurance or guarantees of deposits,” she said.

“But when asked whether insuring all U.S. deposits required congressional approval, Yellen said she was not considering such a move and was reviewing banking risks on a case-by-case basis.”

So in the above comment, Buffett is pretty much calling BS on Yellen. He believes depositors will be made whole. Whether he believes it… idk. Buffett always tries to calm panic. He’s trying to prevent bank runs tbh.

(Yellen says not considering ‘blanket insurance’ for all U.S. bank deposits, Reuters, 3/22/2023)

Well, media changed the printed headlines by evening, good to see that feedback still works.

So let’s add something:

It said Buffet makes a $1 Million bet that government will not let a single depositor lose money till end of this year.

This is super-irresponsible. Who is Warren Buffet to define limits of bailouts by FDIC, when Fed and FDIC are using printed money to give cheap loans to bailout really bad banks.

If Warren Buffet starts thinking he can withdraw from taxpayers via debt anytime, what prevents him to force the government to do this to save the banks that he holds shares in. He can then encourage these banks to make bigger Pivot bets.

He disrespected FDIC $250,000 limit in his statement, hence its irresponsible.

“It said Buffet makes a $1 Million bet that government will not let a single depositor lose money till end of this year.

This is super-irresponsible.”

LMAO. You’re mad at *Buffet* for this? You think he’s the irresponsible one here?

Absolutely, in AZ the price of fuel has been going up for a while now, well over $4 in most areas. Is this unique to “this area” or is this going on everywhere and just not captured due to lagging effects of this data? Or, is Arizona officially becoming California?

$3.20 in deep blue CT

AZ just turned blue in the last couple years. 2x senate, plus the gov. I’m sure that is the factor that will drive those gas prices down.

Similar prices in ‘mixed’ NH. That said, the spread between regular & premium prices is ridiculous. Some stations charge >$1/gal more for 93 vs 89.

What difference does it make whatever price gasoline is at the pump on any given day?

It’s going to everywhere but way more in Arizona. Seems like California refiners are somewhat offline so supply issues I guess. Only $3.50 ish in New Mexico right now and Portland is around $4. Phoenix use to be cheap, hot, and ugly. Now it’s just hot and ugly lol

AZ is the land of bubbles, wild west in many ways (especially Real Estate). I love the state but to your point (hot and ugly) – there is no reason to ‘overpay’ to live in AZ. AZ has no oceans/beaches, no moderate coastal temperatures, mostly low wages, etc.

Grimp,

Most importantly…plenty of room to build (increasing housing supply = constraint on housing inflation, long term).

The only issue is how hard AZ makes new permitting due to ostensible water supply issues (I’ll buy lawn restrictions…but total new construction bans while legacy users go wholly unaffected…smacks of phonied up political supply strangling).

And in bizarro world…how crazy are things in CA? So crazy that the Gov (well known conservative, he…) is suing municipalities to stop stonewalling state laws calculated to *increase* housing supply. Pretty clear that a lot of CA munis insist upon artificially restricting housing supply in order to defend astronomical home prices…to such an absurd extent that the very liberal state gvt has to tell them to knock it off.

Phoenix is becoming LA. And, yes, Arizona is officially a California annex.

Phoenix has been L.A. East for many, many years.

I bought premium gas in Phoenix at over $5.20 a gallon. It’s definitely moving up again.

I looked it up at AAA

For whatever reason, AZ does appear to be joining the west coast high gas price club.

Here are the states with the highest gas prices in the USA

1. CA 4.885 /gal

2. HI 4.786

3. AZ 4.503

4. WA 4.418

5. NV 4.23

6. IL 4.036

I only counted 6 states with gas prices above $4.

AZ’s neighbor to the east, NM, has a gas price of 3.58/gal. And UT, to the north, is paying 3.66 on average. Grab your ankles, Phoenix!

Friend lives in Phoenix,went to visit stated groceries were 25% higher than Nebraska told me everything has to be trucked in and very little shipped out ,explained higher cost to me by the way he retired from teamsters.

Actually, AZ has a surprisingly sizeable ag industry.

Plenty of sun/heat for growing, if you can get the water.

Have a friend in Reno. Reno has always been higher, and not just a little, than Phoenix, Tucson, or Prescott. Now it’s flipped. Hmmmm! I’m a native Arizonan looking to get out. Have lived in other places though. Just need to figure out where to run.

$3.19 for gas in Panama City, Florida

2 bedroom, 2 bath “luxury” apartment rent for around $1450 (or $1600 in Panama City Beach)

entry level hourly wage is $15 at fast food restaurants in Panama City Beach

Roll Tide

I’ll bet a lot of Florida’s don’t like your post.

What ??? Somenpsrt of Florida is not out of this world expensive. Oh right Miami is on the other end of the state (and TB not too near either).

SoCal, Floridians especially but really just about anywhere (Montana, NC, Columbus, Ohio, Minneapolis, etc) there are these homeowners who just have to gush

(guuuussshhhh):

“Oh its just sooooo expensive here, prices just never coming down here”.

You never know if they are telling the truth…maybe. I wish I could vomit on them.

The movement of natural gas prices relative to what providers are charging is a JOKE! Here in GA, the providers / marketeers are acting like natural gas is lumber. The price per million BTU has dropped to almost $2 or where it was over two years ago when I got $0.38 per therm. But, the average cost to consumer is at least 2x that old price. And my current marketer shows that they want to lock me into 36 month rate while others are giving a decent rate but they only want to do 4, 5 or 6 billing cycles.

NATURAL GAS IS A FREAKING SCAM! I pay Atlanta Gas Light, the company who owns the pipelines, as much as $25 a month in the summer to send me 3 therms that even by today’s extortion prices only costs about $2.10.

It’s just a scam of unbelievable scale.

They have overhead costs,infrastructure,employees,and overpaid management .

Thanks, Wolf.

Looks like services inflation on cruise control.

This is asset value driven inflation. Unless Stonks/housing/Krypto collapse by at least 30%, the inflation will continue.

Real interest rates are still negative.

Real incomes are down 24 months in a row.

World growth continues to slow, and debt rise, basically everywhere.

While QT has proceeded in the past year, GSE’s

continue pumping out $, the Treasury has spent ~$650b from its general account, and various government agencies guarantee many types of bank lending – all far more than countering QT, creating a net QE.

In 2020, Powell said monetary policy alone couldn’t refloat the economy, and additional fiscal spending was also necessary. In a recent Q&A, when asked about the inflationary effects of deficit spending, Powell said it is not the Fed’s business to comment on fiscal policy. WHAT?

The first 6 months of the current fiscal year have produced a deficit of over $1T, and it is easy to model a 2.5T defecit for the year. The solution to this problem will be to spend even more.

The bank crisis is not over. Expect deposits to continue seeking better returns(pressuring the deposit base), and stress on HTM portfolios will likely intensify beyond duration over the next few years as the keys to CRE properties are given back to the lenders. (Commercial banks are hustling to get out of the way of that train wreck right now).

In this environment, Fed “tools” are some combination of ineffective, complexity intensifying, and a generator of negative unintended consequences.

And Fed modeling? Observing the Dot Plots chase reality is like watching fish in a bowl.

In sum, and unfortunately, our economic leaders are attempting to preserve an economic world that no longer exists.

So, going forward, expect more of the same.

Who knows? maybe the Treasury will stop paying interest on debt the Fed owns, and the Fed will buy underwater bank investments at par. All while continuing the current QE and simultaneously buying the coming tidal wave of upcoming Treasury issuance in a separate TreasuryAssistAccount.

Nirvana.

Yes, the majority of people are becoming poorer and in the process of becoming a lot poorer.

Fortunately, that sort of thing *never* leads to problems.

/tugs hard to remove tongue from cheet

FED can do the wildest thing possible as they create $$ out of thin air.

The Federal Reserve continues to substantially shrink the money supply in the US. Didn’t you get the memo. Go read the Federal Reserve balance sheet.

As you mentioned, the bank crisis is not over. It could get worse. People will panic. The FED will bail them out with new program (which will be probably the 30th since 2009). Then we are all good again. You just have to front run the FED and buy beaten up bank stocks before they bailout. We have seen this playbook.

In depression my grandmother got 80 acres in exchange for her $800 savings account. As told by her to me this seems like a fair trade .Should be implemented again

Unfortunately the American people love inflation so it will continue for the foreseeable future.

Fed needs to go back to 50bps hikes again. Get rates up to 7-8% or more and then you’ll need an electron microscope to find inflation. The fake economy will die off, those living off uber eats and door dash will have to learn to cook again but the good news is eggs will be under $3 a dozen then so they might lose some weight.

Problem in my humble opinion is Fed policy works with different lags on different things. Steve Hanke, a Milton Friedman follower, was only guy to predict inflation correctly that I know about. He is saying we will be at 2-5% by end of year based on trend of M2 which is accelerating negative. Time will tell. To get general inflation you got to have growth in money (with a lag).

Biggest problem is energy,food aren’t included in inflation data ,what a SCAM,brought to you by UNCLE

“…food aren’t included in inflation data…”

LOL. I mean, this place is getting hilarious 🤣👍❤😍😂😎

Read the headline of this article, and then read the section titled “Food inflation,” including the table by food category, and what the price changes were. Food accounts for 13.5% of total CPI, with “food at home” accounting for 8.7%, and “food away from home” accounting for 4.8%.

Credit market is freezing ,this is not good. Will slow economy down ,layoffs .Business have no working capital,this will do feds job without raising rates

Credit market is doing just fine. It’s not freezing. Someone spreading a whole bunch of BS.

I don’t understand, the idea of high interest rates is to stifle lending. How come with interest rates at this level and the prices of everything skyrocketing, credit is fine? If you say there is wage growth, it will say that hardly all wages are catching up and outpacing inflation. If you say that it is profitable to take credit because inflation is high, it will say that credit in these conditions reduces people’s purchasing power because of inflation. If you say that people are spending money saved during COVID, it will say that hardly people have saved enough to live long with this money or foreclose on properties.

“Credit market is doing just fine. It’s not freezing. Someone spreading a whole bunch of BS.”

“We believe the effect of the troubles in the subprime sector on the broader housing market will be limited and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system.”

Ben Bernanke

Juliab interest rates are BELOW the CPI and also BELOW the rate of monetary expansion (much more important than CPI). It is ridiculous to call these rates high.

The Fed continues to subsidize borrowers.

Raging Texan,

As I wrote ”If you say that it is profitable to take credit because inflation is high, I will say that credit in these conditions reduces people’s purchasing power because of inflation”

I’m talking about the mass of people, not the handful of billionaires. An average wage earner who has taken out a loan and whose salary barely keeps up with inflation will experience the full brunt of this inflation because the loan serves his life even more along with the already greatly increased prices

Wolf banks are cutting credit to car dealers it’s on the news

Flea,

Nah. You’re watching too much YouTube BS. The captives are ramping up lending and buying down interest rates — see the “0% financing” offers at auto dealers. Banks and credit unions are ramping up. New vehicle lending has loosened! Higher-end used vehicle lending has loosened. The thing that has tightened some is subprime used-vehicle lending, which was ultra-loose before and should not have been that loose.

Anecdotally, still plenty of 0% BNPL offers in the world of electronics e-commerce retail… and plenty of customers still expecting/asking about free financing.

Jeremy Siegel „has made the calculation”. Core inflation is wiped out. Everyone else is wrong. If you’ve been thinking wisdom comes with age you may need to reconsider.

Isn’t Siegel calling this inflation “phantom of inflation?”

The guy cracks me up.

This inflation is very simple; inflation will continue until all the monetary creation (currency debasement) is flushed through the system. Since inflation is a regressive tax, the loss to the 99% population will be the percentage inflation multiplied by time; simply the area under the curve.

It is obvious by now that the Federal Reserve has no intention to actually stop inflation, perhaps the damage is irreversible, the interest rises are simply to control the rate of inflation like a valve on a water faucet; a good steady flow where the population grumbles and not too fast where the population becomes politically active about regulation or God forbid an independent oversight group of real experts overseeing the opaque “work” of the Federal Reserve Corporation FOMC public relations officers.

The Fed is like the formation of the “nation” of Iraq: boundaries and job descriptions somewhat arbitrarily scrawled as a hybrid across multiple possibly contradictory bases. So its triangulations between employment, banking system stability and price stability can turn very weird and mushy and self-defeating. It seems to sprawl between these spongy bases rather erratically. Hopefully this time is the charm! Ha!

Or consolidation of banking into larger megabanks at the expense of regional/local banks persists; an orchestrated precondition for eventual CBDC implementation – and all the objectives associated with such a move.

Siegel has more flip flops than Copacabana. What a tired old hack.

His nose grows a little with every lie

Siegel also is calling for rate cuts before end of 2023. Zero credibility in my book.

I dont know about Siegal. There are quite a few Utubers who seem to think rate cuts will be coming. I dont know to what extent their narrative is driven by the desire to get more subscribers … I do believe it is in part so driven.

Usually the presentations are good although today one of the Utubers clearly misinterpreted a chart dealing with building material prices.

Here’s some of the more prominent people: Reventure Consulting, Sachs Realty, RJ Talks (usually like his presentations but today seemingly had the chart issue), Steven van Metre, Joe Blogs, Jason Walters. Others.

Guessing Wolf might not think much of their presentations or predictions though not sure. Sachs Realty has 30 years in the business just as an example. They usually are using data from Redfin, NAR, realtor.com, Freddie Mac, Case Shiller, Bloomburg, etc.

I’m still too new to this arena to trust anyone’s predictions. But again a lot of doom and gloom from half of these people… some see a big credit crunch, some expect many small & regional bank failures. Some wolfstreet commentators seem quite knowledgeable… any opinions on these individuals in particular ?

Thank you.

Siegel is spot-on. Just as he has been accurate across several cycles.

He understands the data – which is rare. Understanding how the data is constructed and how it relates to the real economy, along with associated lags between the readings and reality.

The Fed needs to stop tightening now. Policy is restrictive enough and we will see the demand crunch in the coming quarters as rate impacts converge with depleted savings. The aggregate data is masking the stresses already happening in large swaths of the market (and this is happening while job confidence remains strong). We’ll see the payroll numbers start to tick down rapidly and then stuff will hit the fan fast.

Doesn’t the fed usually overtighten and then have to back off? Wolf’s been saying a pause is coming to allow things to soak in.

The Federal Reserve needs to and will continue monetary tightening for the foreseeable future.

“The Fed needs to stop tightening now. Policy is restrictive enough”

Inflation continues to rampage across the economy, tech and crypto bubbles are reinflating, house prices are still in the stratosphere and heading back up–but yes, sure, policy is restrictive enough. Quick–stop tightening before anything becomes affordable again!

Crypto bubble reflating? Seems 90% of crypto is still 90% down. The mainstays are attracting the same speculative crowd that ran prices up 7 or 8 years ago… so long as they trade amongst themselves, who cares?

Tech bubble? Please explain how that has reflated since most garbage still trades like garbage. Tesla is still overvalued but, again, company specific realities will eventually resolve these value disconnects. Regardless of 3% or 5% short term rates.

…the casinos are where you find them…

may we all find a better day.

I always appreciate the OER vs CS home price index chart. Quite the divergence right now, which can only be resolved with some combination of higher rents & lower home prices.

Agreed! From the historical data on that chart it looks like home prices are going to need to drop quite a bit more to meet those rents

Waiting all day for the real news about todays CPI report. Thanks,,, Does the Wolfman predict the new I Bond rate for May 2023??? Asking for a friend.

The reason we have ibonds is so that we don’t ever have to think about them. We buy them every January, to the max, for all our accounts, no matter what, and then we forget about them. Been doing that for years. This is the bottom layer of our nest egg. If I want to think about something, there is plenty of other stuff out there, LOL

My friend says thanks, seems he can t not think about his I Bonds.

And it just piles up, untaxed until you take it out. Ibonds are great long term easy to do financial asset, if you have excess funds beyond food and shelter.

So long as you don’t need the money. Also 10K cap annually. Nice asset to own, no doubt about it. Not what drives a portfolio.

I bonds have other advantages like favorable tax treatment when you pay for your Kid’s college tuition. Plus they sit at Treasury Direct which is one place I hardly ever log on to. Time goes on and we wonder if we have savings there – and get a nice surprise.

New I bond rate starting May 1 is 3.38% without unknown fixed component yet. If you buy in April, you will still get the ~6.89% for the next six months.

Anthony A.,

BS

If you’re quoting Tips watch… read further down.

“The one unknown is: Will the Treasury raise the I Bond’s fixed rate on May 1? It’s definitely possible. I have been speculating that the fixed rate will end up in a range of 0.4% to 0.6% at the reset. No one knows. I will be writing more about this later this week.”

The fixed portion stays for 30 years, so it’s way more important if you’re keeping them long-term.

The Treasury pulls it out of their… nether regions.

There are no public formulas. Some people use the 10 years tips blah blah blah. None of them fit. It’s arbitrary. They should have a public formula imo.

The variable rate (inflation part) for new I bond purchases starting in May is now known, it’ll be 3.38% for the first 6 months. The only unknown is the fixed rate (permanent) which is added on top. It’s likely to stay about the same (0.4%), perhaps a slight increase so I’ll guess 0.5%. If correct, the first 6 months will yield 3.88%.

If you purchase before May you get 6 months of 6.88% plus 6 months of 3.78%.

I was thinking of diverting $5k from my tax return to paper ibonds. If I did that tomorrow or Monday, does anyone know how long the IRS takes to issue them? In other words, will it be before the end of the month and thus get the 6.89%?

UrsaTaurus,

I disagree.

A lot of people ARE saying that (.6% fixed).

Yet, TIPS are paying like 100 bps more. Historically, I bonds are *somewhat* similar to 10 year TIPS.

I still maintain there should be a public disclosure of the formula or meeting notes that determine I bond rates.

A bunch of old Treasury dudes just pick a number ヽ(。_°)ノ

Anecdotally not surprised by food at home going down. Seemed like starting last month things started going on sale from time to time. Not down in price much but some sale items I noticed.

Look out ahead for oil if it breaks out above $85 and to see goods inflation potentially on the rise again looks like we’re in a higher for longer scenario. Although markets won’t price that in for some time I’d imagine

I don’t see a decrease in any of my grocery bills. The only new thing is that I don’t throw anything out unless it is obviously bad. All left overs become some part of lunch.

Some things taste better the second time around. I keep telling myself this. It helps a little. At least I haven’t had to start growing my own food yet.

Recommend to EVERYONE ”grow what you can,,, wherever you are.”

Any one in any living situation, apt, condo, SFR, mansion, not to mention rural CAN and SHOULD grow everything they can,,, and if no experience, start now to learn…

WE, in this case the small family WE are currently growing as much ”tree foods” as we can: 20+ banana stems, had 5 big bunches last year from 10 or so stems; five mangoes, two bearing heavily this year, two (grafted, planted this year) three avocadoes, one bearing heavily this year; one lychee bearing heavily this year; a dozen or so papaya, some of which will produce dozens of fruits this year.

Get off your rear end and get to work planting as much and as many as your living situation allows…

Including balconies and windows if you don’t have dirt…

Good Luck, and may the Great Spirits Bless your every effort!!!

And BTW,,, if you can grow pot as so many of us did years ago,,, you can definitely grow tree foods and of course the ”truck garden” stuff SO similar to pot.

Give it time.

Yep I have been seeing some prove reductions in produce, frozen foods. I am thinking the food companies have discovered how far they can push prices and are pulling back a bit.

Absolutely. Since groceries are my job, I’ve been telling my wife the same thing for the past month and more. Some of the prices did go nominally down, while some items are constantly “on sale” for the past six weeks. I can buy bell peppers, cheese, and streak at 2015 “sale” prices. Even OJ and eggs are going down. (This is Canada so we didn’t have crazy egg price spike, just a typical dairy cartel pricing crawl.)

Even if the inflation goes down to zero, it basically means prices stay the same. It means a lot of working people have been proven a big loser with plateaued high price and wages which didn’t keep up with inflation.

Indeed, and yet deflation (our only hope) is considered a dirty word.

Jon wrote: “ Even if the inflation goes down to zero, it basically means prices stay the same. ”

This is what isn’t talked about in the mainstream news. High prices are very sticky

Agreed.

The (latest) MSM big lie is how wonderful everything is once inflation falls back to 2%.

Ignoring the previous 2 yrs of 15% annual spikes.

But God forbid prices fall by 1%…at which point the MSM rends its clothing and sets its hair on fire (like 2002) about how *any* deflation is the end of civilization.

Such disgusting tactics are precisely why people think of the MSM as state-run, Baghdad Bobs.

At least wage growth is moderating.

And yet the banking crisis gives Jerome an excuse to pivot (something he fervently desires).

The Fed is going to pause at some point because obviously rates cannot go up forever.

Wall Street believes that the Fed will stop no matter what after one more 25 basis point increase. That will bring the rate equal to the high under Bernanke, which didn’t last very long before it got cut to near zero. The Fed just avoided a bank run and a panic similar to 2008 by quickly rolling out the BTFP and defusing unrealized losses on bank balance sheets. There should be a few more dumpster fires facing the Fed as fifteen years of ZIRP financial assets meet the reality of 5.25% rates. Let’s see how nimble the Fed can be before it starts to cut rates again. Wall Street thinks it won’t be long no matter what the inflation rate is if the dumpster fire is big enough.

Ever consider that Jerome is defending the dollar as the reserve currency now, and perhaps he won’t pause? Looks like the Russians and Chinese are making their play, they voiced concerns in 08 and let us hang ourselves. If powell pauses or begins to reduce, i suspect OPEC+ will cut more production.

I agree, Powell/Fed will have to defend the USD value with high interest rates. Anything else would be suicidal.

But never underestimate the craziness of Washington. They may start WW3 to avoid the final reckoning.

Yeah this occurred to us too, there’s historic danger from letting US inflation continue to run hot like this and it’s why JPow cannot pivot, no matter what the dumb squawkers and media keep fantasizing on. It’s bad enough that Americans are getting angrier and social unrest looms as rents and food spike higher (and with 400 million firearms..) while their incomes lag, but banks and holders overseas are getting more reluctant to hold dollar-denominated assets whose value is evaporating from inflation. It’s not even a mainly a matter of major players making a move, it’s much more basic–the Saudis and other oil and commodities producers are getting furious that US inflation is basically being exported to their countries and threatening their stability. There’s nothing special about the USD, a reserve currency only gets that designation if it holds it’s value, and if overseas holders get even the hint that the Federal Reserve is taking their feet off the pedal and letting inflation run uncontrolled, they’re not going to hold increasingly worthless dollars and dollar-denominated securities, much less continue to buy them.

This is again another reason to ignore the pivot-mongers and other morons who keep talking about rate hike halts or even cuts. The very geopolitical viability of the US as a great power is at stake now, like our old prof said, inflation has brought down far more major empires and powers than any war ever has. Powell can’t afford to go soft now, even the once persistent dove Kashkari is now loudly hawkish. If anything they should be going full Volcker at this point, not just trifling 25 bp rises but more like 0.5 at next couple meetings. And going a lot more aggressive with QT, even more than rate hikes, strong quantitative tightening is most effective at the rich speculators and asset bubble pumpers who are responsible for this insane North American housing bubble and the Everything Bubble in general.

Miller:

”RIGHT ARM”,,, what we used to say instead of ”right on” back in the late 1960s/early ’70s.

Time and enough has gone to heck for WE,,, in this case WE the PEEDONs to DEMAND the FRB at least try, seriously TRY to tame inflation down to ZERO…

This whole nonsense about 2% inflation is just more bull pucky from the oligarchy/owners who want inflation to continue to screw each and all and every working folks…

Seriously appreciate your posts on Wolf’s Wonder…

Thank you.

Miller,

Good comments, understandable.

Steve van Metre, video, however was making (?) a strong case today (or yesterday) that the Fed must reduce rates to prevent too many banking problems. He sees too many depositors fleeing to money market funds with things as they are. But in general I didn’t follow his arguments that well, my shortcoming.

I encourage you to listen to his 15 minute or so presentation and poke holes in his arguments if possible.

The two of you are at odds as to what the Fed needs to do.

True, but Rates should at least be higher than at least the BS CPI if the FED is truly “fighting inflation”. Where is the big QT and MBS sales?….weak so far.

For those of us profiting on the short side, the pivot can’t come soon enough. History is clear: the big stock market drop comes after the pivot.

Inflation 5%, interest rate 5%, inflation is beat everything else is transitory. Time to pivot so no recession. Time to sign the multibillion dollar debt welfare package. Time to squeeze the middle class for taxes and inflation on everything and claim transitionary.

Softlanding acheived we want the nobel prize in economics for proving volkner wrong. Oh, since we timed it right and unemployment is up; everybody has to take a wage cut, non-recession and all you know, transitory.

Just got the price for a quarter of beef that we ordered. A bit more this time but that was because the butcher raised prices. The price from the producer is not much different. Overall the price per # was $4.25 for everything from burger to T-Bones, cut and packaged to desire for lean and grass fed.

There ARE ways to save money and have better source known food at the same time. And support producers outside of the commercial food chain that everyone complains about. The producer does better, the butcher and employees do better and the consumer wins.

Alternatives don’t have to be so hard unless you can’t break away from the way you’ve always done it.

I’m living well on about $10-15 per day for food, good quality. I’ve been able to hold the line there. Takes some focus to get there.

That’s exactly my daily food budget too.

Meanwhile I see coworkers spending $20+ on takeout for lunch multiple days a week.

Our food budget for a family of three (two adults + one teenager) is $800/month. Food is important to me and I am a good cook. About 18 months ago I completely overhauled our approach to food.

1. Bulk purchases. I shop at places like Restaurant Depot and Costco for items such as meat, poultry, eggs, seafood, flour, baking supplies. Perishable items are portioned out, vacuum sealed, and stored in a chest freezer.

2. Portion control. Meals are sized based on how much we will eat. No more cooking too much and throwing away food. Portions are generous but not wasteful.

3. Bake from scratch as much as possible. A 50-lb. bag of flour at the Restaurant Depot costs me $22. I can bake a lot of loaves of bread and prepare a lot of pizza crusts with that much flour. I haven’t bought a loaf of bread from the grocery store in years. We bake everything we can. Bread, bagels, English muffins, biscuits, hamburger buns. I can make it all.

4. Planted a garden. The growing season here is not very long, but for a few months in summer we have lots of fresh vegetables. We also trade/barter with acquaintances who grow their own food.

5. As much as possible I buy in bulk and prepare my own foods. I’ll buy a big slab of pork belly and make my own bacon. Or buy bulk ground pork and make up some big batches of meatballs or breakfast sausage. We prepare our own pasta sauce using bulk San Marzano tomatoes and herbs from the garden. My unit cost for an Italian meal is a few dollars, and better than any of the restaurants around here.

6. No more eating out at restaurants at all except on special occasions. My weekly Friday night pizza unit cost was $20 from the local Italian place. Now it’s $5 to prepare my own, and frankly it tastes better, and I know what ingredients are going into it.

7. I prepare a weekly menu. This helps with planning what foods to defrost or what needs to be baked or prepared ahead of time. No more running to the grocery store three or four times a week to purchase small amounts of food for one meal at a time.

With some planning and effort, our family is able to eat exactly what we want in the quantities we want for less money than our food budget was 18 months ago. That is my response to food inflation.

A good long term way to balance population with resources is if sex and marriage isn’t available to men. Unless they have built up enough of a career and income to support their wives and children.

How many meals? I am about $20/Day.

Just the basics, have to do a lot of prep work. Fruit, veg, nuts, proteins, a bit of carbs,good portions. No snacks. Juice watered down. No cola, 2+ meals at that price. All wholesale. Good quality is a matter of interpretation, fruit and vegs and animal protein could be drenched in hormones/?-cides

Phleep and others,

If any of you are tempted to go vegan or vegetarian you might give tempeh a try.

Fermented soybeans. I read Asians usually eat soybeans that have been fermented. Tofu isn’t.

Tempeh has much more texture than tofu and absorbs sauces well. Its still $2.29 for 8 oz. package at Trader Joes here in Spokane ($3 to $4 elsewhere).

I add BBQ sauce or olive oil, soy sauce, sage mixture.

JR. 50% increase in about 2 years. Looks like even more trending for next year.

Pow Pow just plain suck at wag a mole….

Btw, I think I briefly saw something from MSM about headline inflation down…looks like everyone is busy hyping the inflation is dying down fast narrative…market and dip buyers sure have been eating them up lately..

Does anyone have good info on what’s going on with used cars? 4 months in a row of rising wholesale prices but retail prices according to CPI keep falling! Is it a margin squeeze for the dealers, bad data, or a lag?

Inquiring minds want to know.

Article coming today/tomorrow. I’ve got some ideas about why this is.

Continues to easily look like rates should be raised. Lowering is silly and can always be done when actually needed.

I think Wolf said above that there’s a lag in that data.

A used car dealer on YouTube I follow, seems to think prices are moderating at auction and expects prices to head down some. He’s cutting prices on his lot to move cars now before he has to drop prices further (based on lower auction prices).

Of course, that’s just one empirical data point, but that guy is “on the ground”.

Cars are worst deprecating investment on earth ,but Covid turned brains to mush, dealers f*******g people over msrp and below wholesale on trade in ,banks are cutting there credit . Reeling them into reality. Just bought a new car ,worst experience of my life ,may they rot in hell

Maybe the way CPI calculates prices on used cars. I understand it’s a very limited sample size… Which is crazy if policy is being decided on by inaccurate numbers

BLS is buying private sector data from JD Power. This is fairly new and replaced the old way of doing it (sampling dealers). I covered the change of method when it took place. From the BLS, and I abbreviated it:

Used vehicles that are between 2 and 7 years of age.

Subcompact, compact or sporty, intermediate, full, and luxury cars, pickup trucks, vans, SUVs, and crossover SUVs

The CPI’s current used cars and trucks sample is calculated using data from the J. D. Power Information Network (JDPIN), a network of car dealers who report sales of used vehicles to the J. D. Power Company. A sample of 480 two to seven year old vehicles is selected from the JDPIN based on probability proportionate to sales.

The Washington CPI office collects prices on this sample on a monthly basis, using J.D. Power Valuation Services’ NADA values.

The sample is updated by one model year each September so that each vehicle in the sample maintains the same age over time. If a production model is discontinued, it is replaced by a comparable model. This process of refreshing the sample is called “model changeover”. Periodic resampling is scheduled as resources allow.

Off topic sort of. But I just came to end of term with my lease and after crunching the numbers there was zero reason not to just buy the car out. 2021 Honda civic, sub 20k miles on a two year lease.

The fact being prices for a new lease were out of control with big money down and more importantly, Honda seems to have some inventory issues as the few dealerships I went to all had waiting lists for new civics, at least in the northeast still.

In my situation, all in, I got a 2021 civic for 21-22k. I can’t imagine other people are not doing the same across the country and how this is affecting things in the car market.

I didn’t finance this either. Figure it was worth the investment with cash laying around in banks yielding not much.

1984 or 85 near Eatontown, New Jersey. Wanted to buy a new Toyota. Low inventory hard to get.

Dealerships gave me the run around while they made a bit of money off interest on my deposit (interest rates high then). Said they’d bring one in from Pennsylvania or CT but never happened.

Gave up bought very good used Datsun stick shift (clutch) from Canadian transplant.

Excellent car. Great gas mileage (low 30s city, low 40s Hwy).

Is this data for the whole month of March, or for a period of March that suits the government. A week or two could make a huge difference.

No one picks and choses the dates. There are 80,000 items in the index that get priced every month. The prices are collected throughout the entire calendar month.

So, it is to fit their narrative?

That is fed BS, and it is a terrible way to do financial policy.

Can you not read? You were given your answer and it was very clear.

Powell and company had better not wimp out. Then I will really feel back in that swampy, edgy sort of uncertainty, like back in the pandemic days. I prepared well for this situation, but would feel very bad if undermined from here.

I don’t think the Fed will entirely wimp out, but I do think they need to stop playing “catch up”. If you want to put out a fire, you dont do it one cup of water at a time. Although frankly I’m surprised they actually raised rates as much as they did and haven’t pivoted yet.

Fuel Prices to all the rest: “You haven’t seen the last of me, I’ll be back, baby!”

The currency markets reacted strangely to this inflation report. The DXY cratered when the report was released plunging from 102.20 to just above 101.50 and it stayed at that level all day. Do they think the pivot is coming? It made no sense to me.

While this was going on, Gold and Silver rocketed upwards to $2024 and $25.65 respectively. Of course then the bullion banks with their “paper gold” pushed the price back down. So the bullion banks succeeded in keeping the metals to a small gain. All they are doing is allowing China to buy gold cheap.

I think the dollar going down after a lower inflation reading makes sense as it points to weaker growth.

Yields and stocks were the “surprise” today based on pre market activity

Escierto……I’am no expert.

So good luck

Gold is being driven by many factors including:

1. Expectation of lower US interest rates caused by a reduction in M2 with a resulting serious recession. This is goosed when the market smells lower cause for the Fed to hike rates, like today, and goosed when the market smells inflation may be higher than expected causing higher rates. IMO this is a no lose position.

2. Weaponizing the dollar against Russia, Iran etc. Other nations want out unless they are in our direct orbit.

3. Our balance of payments deficit which in a world of marginal decline in international demand for dollars is a mess in the making.

4. Deglobalization which may goose inflation in the US and which will be driven to higher level by a lower dollar.

As for the banks defending a lower price…….the wealthy in the US WANT the US to lose central bank status over many years. They want China and friends to acquire gold so they can issue an alternate currency capable of threatening the dollar. IMO gold will stair step up slowly and then one day…you will be made good……all of a sudden when the new currency is introduced.

Why…….think about what happens if we lose status……only inflation is bad. The other results are mostly positive. Lower government spending, lower trade deficits, fewer foreign wars, more jobs in the US etc etc.

Kicking the lower classes in the …… has never been a problem for the higher class. So the higher inflation replaces shipping jobs overseas as the mechanism for keeping US workers in their place as the nation starts to rebuild its wealth as all those foreign dollars start to come home.

Will this happen in a few short months……hardly……unless I’am surprised…..and

In the end the US will remain a dominant international player……but instead of US soldiers in Iraq….those dudes will be Chinese. We will go back to prioritizing the Navy and Air Force and forget these scrub dollar burning wars.

Most of what is expressed above drives gold higher for many years…if not decades.

Dollar could bottom @94

Very interesting. Thanks Wolf.

Seems anybody that rents is getting worse and worse off – I’m not sure how they’re paying for these increases. My guess is it’s coming out of money that has been or would be saved toward purchasing since the prospect of that has flown out of the window for the foreseeable future.

Those doing the renting are instead seeing their paper wealth disappear. I suppose everybody getting poorer is one way to reduce the wealth disparity!

My relatives got married ,lived in an upstairs apartment. Has a hot plate to cook ,went to work everyday,bought a home ,saved money . But the is 92 now .

@Flea – Just in time to start a family and plant a tree!

Elevated home prices and higher interest rates are pulling up rents. Home prices need to come down a lot more to put a ceiling on rent increases.

In the not-too-distant future, I suspect we’ll see more folks taking on (add’l) roommates or shacking up (sooner) in response to higher rents.

I’m struggling to see how this doesn’t end with a massive affordability crisis for anybody who didn’t manage to hop on the gravy train when mortgages were cheap.

Housing is non optional. If buying is impossible (and it currently is for many), then landlords will just keep jacking the rent until it consumes every spare penny. Landlords will relax their affordability criteria quicker and further than mortgage lenders, who are also more constrained by regulation.

Yes, landlords might end up losing equity hand over fist in the short to medium term, but that doesn’t really matter all that much when your tenant is paying the entirety of your 3% mortgage plus quite a lot extra. And that extra balloons every year with inflation.

Are you a slumlord by chance?

Is your real name Mr. Elliot Carlin?

I am not sure all “landlords” can be put in the same category. Landlords I know value a good tenant and the last thing they want is to lose a good tenant in order to make a few more dollars by raising rent to whatever the market will bear. Rental costs are effected enough by rising property tax costs, utility costs, association fee costs, and so on. There is not much room remaining for unadulterated greed of the landlord. And there is a lot to be said about steady cash flow in the rental business.

“I’m struggling to see how this doesn’t end with a massive affordability crisis for anybody who didn’t manage to hop on the gravy train when mortgages were cheap”

END WITH an affordability crisis? Buddy, take a look around. It’s here. It’s been here. Millions have been priced out, for years now.

“I’m struggling to see how this doesn’t end with a massive affordability crisis…”

I think it will be tough for a lot of folks, but at the same time people generally manage to adapt and find a way. Case in point, my original example.

I see many coworkers at my office spending $20+ on takeout lunches almost every day. Perhaps they’ll start bringing a lunch.

Restaurants are still packed, and takeout joints are filled with doordash/uber eats etc drivers, lots still paying xtra $ for delivery/laziness.

I suspect a lot of folks have gotten used to a standard of living that was only made possible by ~40 years of declining interest rates.

I agree MM.

“I see many coworkers at my office spending $20+ on takeout lunches almost every day. Perhaps they’ll start bringing a lunch.”

Excellent idea. With the money they save, they’ll accumulate enough for a very modest down payment on a house some time around 2083. Why didn’t anybody think of this extremely original idea before?

Pea Sea,

“Saving for the future? That’s preposterous, spend it now!”

MM

Home prices are starting to go up here again in the Swamp and suburbs. There are no listings. Everything is snapped up within 2 weeks! Even the overpriced “LISTING FROM HELL” around the block from me sold the other day.

I visited Ms Swamp’s hairdresser who is working from home in a far out suburb, and there is little or any housing for sale or rent. This is NOT 2005/2006.

All of Powells effort to cool the inflation and slow the economy vis raising short term rates are a total failure. He ought to do everyone a favor, for the sake of the country, and hand in his resignation, not today but YESTERDAY.

Its common to hear the ” its not 2005/2006.” mantra.

As if that means the RE market (from a sellers perspective) will be smooth sailing so long as its distinctive from 2006. Simple sells well in America.

2005/2006 is not the only time the US RE took a hit. Regions take hits, nationwide stats mask it.

Texas 1980s. Neighbor sold for 77k three years after purchased new home at 101k. I sold 10 years after my new home purchase at 8% loss.

Why price drops ? S&L crisis, oil industry hits. Texas a non recourse state… many folks walked away from their underwater homes.

Apparently 4 other states took a RE hit (Colorado was one).

Separately Boston took a hit after large run up late 80s or early 90s.

Scott Burns had article in Dallas Morning News. Hard to sell homes. Condos he wrote could not be sold for half the original price… only in some cases obviously.

No. Real estate is not a sure thing.

Oh then there was this.

Forbes has a good article, 2018.

They mention:

In inflation adjusted prices Boston, NYC, and LA real estate peaked late 1980s, fell, and it then took 13, 15, and 13 years respectively to get back to their late 1980 prices.

Not the 2006 bust.

Not the Great Depression.

Not the bust that took down Texas and 4 other states.

I wonder how many other regional real estate correction/crashes most Americans aren’t aware of ?

What happen to most people,especially poor is they don’t understand money,or saving or investing.Igot out of high school without a dime ,worked saved ,invested . Rental property,stocks ,bonds,gold .We have too much of a welfare state ,and most corrupt tax system in the world . Billionaires really ,just stupid and they pay very little in taxes ask WARREN

“Seems anybody that rents is getting worse and worse off”

And anybody who doesn’t own assets and isn’t rich. Jerome Powell and his bankster scvm buddies stole the future of the young and gave it to the already obscenely wealthy. I hope he is ultimately chased down by an angry mob.

+ 1000 % to Depth Charge’s comment …..

DC

” stole the future of the young”

If the young knew the financial “environment” that was being made for them, they would turn their attention from climate change in a second. But they don’t….and won’t.

Longstreet – the climate and the economy are not

an ‘either/or’ situation. They, (and many other factors), are equally-existential.

(…I often wonder if the digital age has massively-accellerated the subconscious tendency of binary thinking among our species…).

may we all find a better day.

The idea of Jerome Powell facing consequences for selling out the United States genuinely made me smile. Despite the recent rumors of Alan Greenspan’s death, I was shocked to read he’s still kicking at 97 years “young”. Not to old for retribution, he needs to take a seat next to Reagan in the depths of hell.

Sorry Mr. Wolf if this seems somewhat extreme (I sincerely admire you and think you’re one of the few concurrently reasonable & successful people in this country that can see outside of the rampant misinformation we are fed on a daily basis) but I’m at a loss of words in relation to how bad things are getting in this country.

(Makes me wonder if repatriating back to Croatia is the only “Ace in the Hole” I have left. Too bad globalization saw capitalism entrench its claws irreversibly into all corners of the Earth.)

P.s This is my first comment on this site, despite reading your posts for 8 years now religiously. Thank you so much for sharing your wisdom with us, you really make a big difference in my life and most likely tons of other younger readers who spectate silently. Thank you to all the regular commentators, who share their perspectives, I value you all tremendously. In closing my comment was somewhat irrelevant so I’ll go back to strictly reading along again until I have a worthy contribution.

Jerome Powell is an abject failure and should have been fired years ago. He continues to fail, and fail badly, yet he still has a job. Inflation is raging out of control, and the speculators have run stocks, crypto and everything else back up due to Powell’s money-printing, yet all the talk now is that this fraudster is going to “pause” rate hikes. It’s dereliction of duty. This guy should be under arrest for crimes against humanity.

But what you really think, DC?

I share your frustration, but Powell didn’t cause this, it started way before him. There is a chance he might actually be trying to fix this mess – so we should cut him some slack for now.

If Yellen was still in charge of the FED, it would have been full on Weimar already, god knows she’s doing her worst from her new job.

Powell didnt need to do QE to the degree that he did.

Agreed, all this started with Nobel Prize winner Bernanke….the “temporary” QE.

Yellen was a disaster….”The theories we chose to follow were wrong.” It was not us making bad decisions….(ha)

In Dec 2018 Powell got rates in balance with inflation (both circa 2%) ….but then caved when the Dow shed 5K and Trump jawboned him.

We would all be better off if there was a formula driven monetary policy….FF = some moving average of inflation, and the Fed never again delves into the long end like they did since 2009. Inflation and employment, the dual mandate, deals with immediate concerns not anything to do with 10yr and out maturities.

I think Powell shares plenty of blame; especially the covid decisions and inflation.

Greenspan may have started it, but BernaQE probably the worst of all as he crossed the rubicon. Yellen just continued it and Powell added to the fire.

Horrible criminals all, tbh.

Stegelberg,

Not disagreeing with you.

I’ve already posted a lengthier version than this… no response:

Not all JP fault:

1. Supply chain disruptions (Trump comments partly to blame ?)

2. Pandemic money… some acknowledge this as an inflation contributor but many just ignore it ?

3. Business leaders raise prices. Their decision. JP, Biden, etc increased demand.

But businessmen raised prices. Not JP, nor Trump, nor Biden.

4. Some have pointed out…maybe JP needs other tools to deal with inflation.

Think about it. Different parts of the country can be undergoing very different degrees of inflation (in theory for sure and presumably in reality). Why is someone in DC setting interest rates supposed to address these various regions successfully when they have different circumstances ?

Occasionally someone alludes to this, i.e., the Fed has crude tools to work with.

Randy,

I don’t understand what your problem is. Short-term interest rates should always be at or above the rate of inflation. If they’re below the rate of inflation, you get all kinds of crazy distortions and then a deeply sick economy because of these distortions. Everyone knows that.

Wolf,

Perhaps you are not seeing what I wrote ? Your comment does not seem to make sense relative to what I wrote.

I made no mention of what short term interest rates should be.

I am concerned your view of my post has been hacked.

Please contact me via email. I would like to discuss this with you.

Thank you, Randy.

Yeah, sorry, that comment should have gone somewhere else, in reply to someone else. That’s easy to screw up in the commenting software I use, where all comments show up in chronological order, and are close together. Clicked on the wrong thing.

Obviously not, and all policy decisions at the Federal Reserve are made by consensus of the 12 member FOMC of which Mr. Powell is just one member and one voice.

Powell speaks in word salads which are incomprehensible. He’s worse than Greenspan 2.0 who used to do the same thing. Greenspan started this mess after 9/11, followed by Bernanke and Yellen. They are all responsible. Powell could have moved things back in the positive direction in 2018 but chickened out.

No. Jerome Powell couldn’t be more crystal clear. Listen.

powell is a symptom, an avatar of the system. You can replace Powell, imprison him and seize his assets. It won’t change anything. The entire system is defective. Not to worry, though. The system dies in about thirty years.

1) Rent y/y change stalled at 9%, lagging the CPI. It might drop to a lower high like the CPI, or drop faster. In the last 20 years, since 2000, rent index never had a dent – even during two recessions – and never had a negative year. Twenty years history aren’t good enough.

2) Price/Rent :

In 2022 : 310/180 = 1.7. // In 2006 : 190/120 = 1.6.

3) There is a systemic change in the rental market. A shift from spacious, with a target on their back, to smallness. The old, the useless, might be converted to smaller units for multi families, shared little boxes for the poor, at lower prices.

3) Vacant commercial buildings might become whore houses, pore houses, or drug fests for the homeless.

While “markets” are expecting a pivot, their actions ease money supply don’t they?

Thus the FRB won’t pivot.

This is why it always ends in a crash.

Confidence is lost and that tightens money supply, after exuberance let rates rise too far.

How often have FRB cut rates without a recession?

How often have FRB cut rates with inflation several times above mandated values?

At this point we’re flying by the seat of human natures pants.

Humans are predictable.

Humans will cause a confidence crash… this is the end game.

Rates rising, inflation hot, markets eager to BTFD.

2008/9 felt tame compared to what we’re seeing now with the added very high inflation factor, and moral hazard of 12 years of easy money.

Retired for 4 years with Hubby still working part time, I play Pickleball 4-5 times a week. Essentially free as there are plenty of free courts/ senior centers to play indoors /outdoors.

It’s summer and I am going to try to get financial markets out of my head. Stocks aren’t close to my buy price. I am sure I will hear about it if stocks fall a lot. Close to break even on cash vs. inflation is OK with me til something big happens.

1) In 2008 the Fed reduced interest rates to zero. At zero rates highly

elevated price should stay at high plateau. We produce bubbles after

bubbles that will never be pricked : stocks, bonds and real estate.

2) US GDP rose to $26T, financed by a $51T bond market.

3) China’s GDP rose vertically to $18T. The Eurodollar initially financed it’s infant industries, infra, RE and military. It was replaced by a $21T bond market that finance China and the rest of the world.

4) The unexpected higher rates might indicate :

prices will rise from their high plateau levels at lower pace, or deflate.

5) The Fed participants can grow the economy without the regional banks. They will fill gap with more liquidity while driving the economy intoxicated.

Im 63 and from (and still live) in the greater Northwest. I have been through a few of these economic turmoil but never like this one.

Washington State has always faired rather well as Boeing, construction industry and others keep things somewhat stable. I’m getting a real education this time around. Call it what you want this time things are so screwed up totally unimaginable.

I would like to hear your story. I think it would be a ‘real education’ for many of us. Looking forward to it.

Shandy

Seattle was a disaster in the early 70’s when I lived there briefly for 6 months. The happiest day I had there was the day I left.

The last one to leave Seattle please turn off the lights.

I remember it well

Jerome Powell’s “soft landing” narrative isn’t about dialing back inflation where prices of goods and services return to a level affordable for the masses, it’s all about making asset prices “stick” at or near their all-time highs – a repricing of everything at a level out of reach for all but the most wealthy, where everybody else struggles and lives hand to mouth.

We are living through the greatest financial crime ever perpetrated in the history of mankind. The already fantastically wealthy globalists used a health crisis to loot the treasuries of the world, in tandem, under the guise of saving the economy. In turn they destroyed it. It was orchestrated. They systematically siphoned off – carved out – a large portion of global wealth, the future of the children, and parked it in their bank accounts.

If that weren’t bad enough, the very people who were the victims of the heist are now footing the bill daily. They will be forced to shoulder the financial burden for their entire lifetimes. Shelter is now a luxury, as are new vehicles and all sorts of other durable goods and things. And all of the people who perpetrated this disgusting scam are still “in charge,” and they have all sorts of other nasty plans which promise to make life even more difficult and unpleasant going forward.

The conversation needs to turn to how the people are going to charge these perps with financial crimes, arrest and imprison them, and claw back all of that ill-gotten loot. There needs to be a great asset-stripping of these robber barons. It’s overdue. And that includes the corrupt politicians who have amassed fortunes of hundreds of millions over their lifetimes while only earning salaries of less than $200k. They were bought off. The entire system is shot through with corruption.

Unfortunately, sheeple will be sheeple. They will fall in line, no matter the absurdity.

Agreed. I received a letter from a local realtor here in St. Louis County the other day stating home prices are up 10% year over year, mainly due to low inventory. It’s difficult to have faith that things will get better when I read things like that.

Do not listen to any realtor. They live to lie.

DC

Very well said.

Marie Antoinette pops into my mind here.

Not sure why.

This ^^^^

Went thru some MSM spin on this. All are saying inflation is slowing down.

Stocks in general are up big time from October lows.

It’d take some shock to bring asset prices down.

This earning season would be interesting.

“It’d take some shock to bring asset prices down.”

It happened and we saw how they responded. Prepare yourself with endless amount of “It’s not QE, QE” nonsense.

I am looking at ERs. If people have money, they’d keep spending thus no impact to earnings as usa is consumer driven economy.

If people are suffering they won’t spend.. then there is a earning recession which should reflect in stock prices unless qe starts again.

special funding given to banks are at 5% rate, so not cheap.

Spending won’t slow until unemployment ticks up imo.

I still remember CA in 2010ish when everything was “horrible”…

Yet there was a 2 hour wait at BJ’s Pizza. We knew people who foreclosed and rented a bigger house.

People spend until they can’t.

I am not sure the corporations always tell the truth about the earnings. Enough room for them to obfuscate and at times lie. Nobody challenges them anyway.

I heard Warren Buffet just unloaded his entire position in one particular stock. I forgot the name. What was it?

Swamp,

“Buffett says geopolitics a factor in Berkshire sale of TSMC stake”

It’s chip maker TSMC. Taiwan-China tensions.

Expat

Your last class on Asian international relations may need a refresher. China invaded South Korea in 1950.

Warren Buffet may know something we don’t know yet?

Can you imagine the impact of a sudden naval blockade of Tiawan by China on the US economy?