The historic plunge in used vehicle retail prices from utterly absurd highs may have ended already.

By Wolf Richter for WOLF STREET.

Used vehicle prices, which spiked ridiculously in 2020 through 2021, were a big player in the surge of inflation during that time. Then, starting in early 2022, used vehicle prices began to drop, and the CPI for used vehicles plunged, and it helped push down overall CPI and “core” CPI.

But now, after these historic distortions, there has been a seemingly complete disconnect between used vehicle wholesale prices, which have been surging for months, and used-vehicle CPI, which has continued to fall, including yesterday’s seasonally adjusted CPI release for March. Or so it seems.

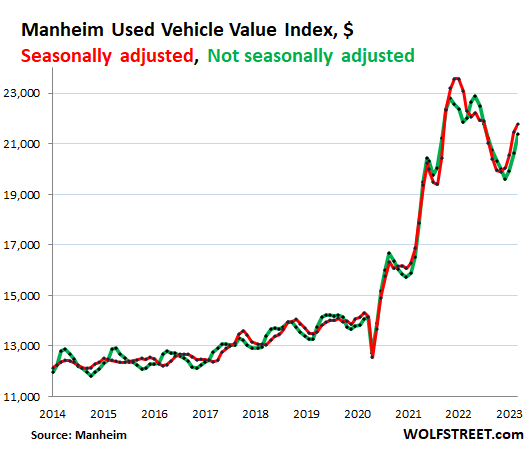

Used-vehicle wholesale prices, seasonally adjusted, jumped for the fourth month in a row, this time 1.5% in March from February, after the 4.3% spike in February, according to Manheim, the largest auto auction house in the US and a unit of Cox Automotive (red line in the chart below).

Not seasonally adjusted, wholesale prices jumped for the third month in a row, this time by 3.5% after the 3.7% jump in February, to $21,375 (green line). Wholesale prices have now regained in three months nearly half (+$1,760) of what they’d lost in the prior 13 months (-$3,199).

Both metrics of wholesale prices are adjusted for changes in the mix and mileage. These increases in auction prices show that dealers have to pay more to purchase vehicles to restock their inventory, and so their costs went up.

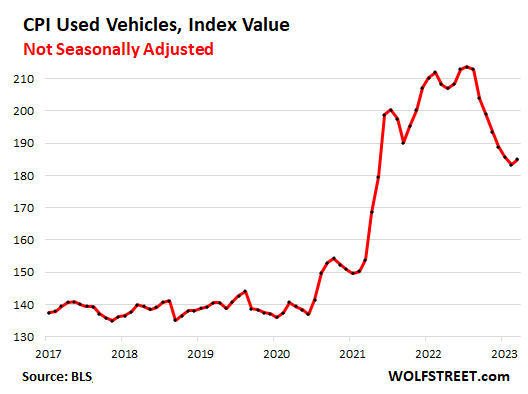

Used-vehicle CPI “not seasonally adjusted” rose in March.

The used-vehicle CPI jumped in March, but we didn’t look in the right place. The normally cited CPI for used vehicles is “seasonally adjusted.” But the “not-seasonally-adjusted” CPI used vehicles jumped by 1.0% in March from February, the first increase since July last year.

There is normally a lag of a couple of months between big changes in wholesale prices and when the CPI for used vehicles picks up those changes as they make their way into the retail prices at which dealers sold those vehicles for.

So this first rise of the not-seasonally-adjusted CPI for used vehicles is two months behind the not-seasonally adjusted wholesale index, which rose for the third month in a row, and the normal time lag of a couple of months is back on track.

This, along with an eye on the wholesale chart, kind of tells us that the drop in used-vehicle CPI is over, and that used vehicle prices may soon stop pushing down core CPI.

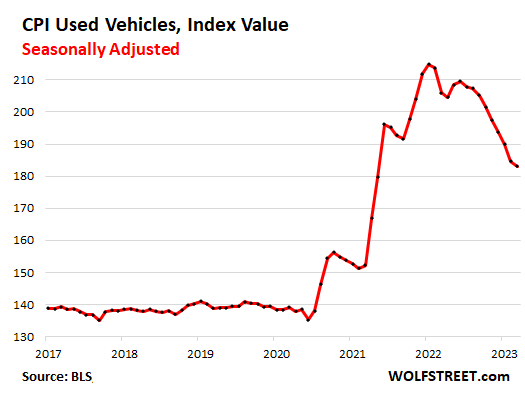

“Seasonally adjusted” CPI used vehicles continued to drop.

As if nothing had happened on the wholesale side of the business, the seasonally adjusted CPI for used vehicles continued to drop, including in March — though at a slower pace of 0.9% — bringing the cumulative drop from the December 2021 peak to 15%.

This is a huge unprecedented drop, after the huge unprecedented spike. And as the spike pushed up CPI and especially core CPI, the drop has pushed down CPI and especially core CPI. And this phase may be ending:

Seasonal adjustments…

Wholesale and retail prices normally rise in March. This is the beginning of the spring selling season, and it’s tax-refund season, and people, armed with tax refunds as down payments, are coming out of hibernation to buy used vehicles in March and April, and demand is driving up prices. Dealers are stocking up for it at auction and are driving up auction prices. That’s normal and predictable, and seasonal adjustments account for it.

The not seasonally adjusted CPI for used vehicles increased on average over the past 10 years by 1.24% in March from February. And so the increase in March 2023 of 1.0% was more than wiped out by the seasonal adjustments.

But this March was a little different in several ways:

Still high prices: Used vehicle retail prices have come down some from the absurd levels a year ago, but they’re still at near-absurd levels, and lots of people aren’t interested in paying those prices, and they’re just driving what they already have.

Smaller and fewer tax refunds: Even though the IRS processed more refunds through March 31 than it had in the same period last year, the average refund fell by 10% to $2,910, and about 1% fewer people received refunds. The IRS issued $183 billion in refunds (nearly all as direct deposits), down 10.4% from the same time last year ($204 billion), according to IRS data.

Dealers willing to give up slivers of their big-fat per-vehicle gross profits they’d feasted on during the pandemic. Dealers have lots of room to play with, given where they are with their per-vehicle grosses, and they can yield on price to get volume, and still make huge per-vehicle grosses, compared to pre-pandemic normal times. So they’re bidding up auction prices, even as they’re willing to make deals to get retail volume. This might look like a profit-margin squeeze, but it’s just a step back toward the normal-ish per-vehicle grosses before the pandemic, as this market is far from having normalized.

Finally…

So given the movements in wholesale prices, and the lag from wholesale prices to CPI for used vehicles, I expect the “not-seasonally adjusted” CPI for used vehicles to rise further in April, and the “seasonally adjusted” CPI to be either roughly flat or up in April, which would mark the end of the historic plunge in used vehicle CPI. This would indicate that consumers are getting more and more used to those still high prices, and that would be a bad sign for inflation.

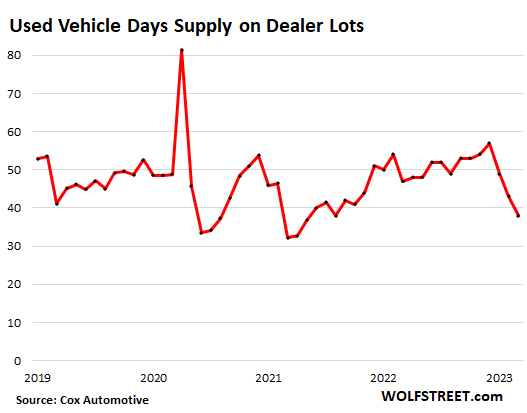

Suddenly tight inventories at dealers could fuel further price increases. At the beginning of March, used-vehicle supply was down to just 38 days (compared to 53 days at the beginning of March 2019), according to Cox Automotive data.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Still way too much free money at places like Carvana who will buy any car at pretty much any price.

Since prices are set at the margins and the point of corporate capitalism is to protect new higher price points, at all costs. Prices CANNOT go down.

these collusive forces will do anything to hide their bulging inventories and keep up that meme that there aren’t enough used cars out there, which is just not true. I can take you to places in the Seattle area where dealerships hide their excess used cars, literally in the woods, and in random fenced lots, that I would bet are not on their books.

Carvana is quoting sizable declines in their offer values. No surprise as the market is softening fast.

That declining trend line in used car prices will continue as credit availability is drying up in tandem with a rise in volume focus at the OEMs (now that they can provide volume and as they are exhausting the least price sensitive part of the market).

Deflationary for sure and we will see the continued decline in prices from here on.

yep and you’re going to see alot of businesses fold now, especially alot of used dealerships.

What you might be seeing is lease returns that belong to the lessor that the intaking dealer doesn’t want to buy at current price and is waiting for them to go onto the franchise online “auction” site in the hope they could score a deal. They also could be reposessions being held until the finance institution picks them up or resolves the loan. They could also be customer cars (think the Kia and Hyundai engine debacle) that have warranty issues that have yet to be repaired due to unavailable parts. Lots of reasons for cars to be sitting and not all are some deep dark plot to defraud the unsuspecting public.

On another note, it’s been reported that Nissan is back in the fleet business (which drove their sales increase in March). Overall fleet sales were up something like 46% over last year…. still not at pre-pandemonium levels, but still…..

“Nothing goes to heck in a straight line!”

Except a Nissan CVT transmission.

Except car or bread purchasing capability the US Dollar.

Car prices creeping back up, energy prices spiking, dollar falling, gold soaring, stocks soaring, crypto soaring, goods prices creeping back up, service prices soaring, consumer debt at all time high, houses stubbornly high while rent catches up.

All the while the Fed keeps hiking rates, with a yield curve inversion at 42-year high.

This is either a big fake out – the mother-of-all dead-cat bounces – or we’re on the verge of experiencing another explosive surge in inflation.

And this time it can’t be blamed on “supply chain issues.”

What you have seen are not rate hikes. These have been rate nudges.

Note the Fed is unnecessary, corrupt, benefits insiders, is illegal under the Constitution and blah blah blah, but I we woke up and they had set rates at least 20% with threat of increasing to 40-50-100% within two weeks if consumer inflation doesn’t reverse – I would call THAT a rate hike.

People have become naive dum dums about rates. People are choosing to be poor as they accept these rates. I often hear people excited they can get 4% short term rates or a hair higher long term rates right now which is the equivalent to begin excited about eating dry sand for dinner.

My proposed rates are reasonable, I know of people who are paying 40% on small biz loans, which means some people are getting that rate, which is reasonable considering m1/m2/m3 growth over the past several years. Actually I’d say lending below 40% is insane considering rate of expansion. Actually, better to say that lending in USD as long as the Fed exists is insane.

Volcker raised the FFR 900 basis points over a short 7 months back in the early 80’s. Totally agreed about nudges. But, the Fed has made so many mistakes in the last 3 years it’s mind boggling.

Mistakes or intentional malfeasance?

The Fed rescue of SVB (it should have been protected by Congress, not the Fed) had exactly the effect it wanted, which was to re-inflate the bubble, as the Fed showed it’ll print however much is necessary to prevent any real pain anywhere.

Inflation is just getting started, folks.

Except the Fed did no such thing.

The FDIC is not the Fed. Further they only intervened for two reasons:

1) to stop potential other bank runs and further instability/damage to the US banking system that would come from not intervening.

2) To keep as many start ups (any of which could become a large corporation paying taxes in the future) alive by insuring that they kept having access to the funds needed to survive.

Then there is that the bank itself had enough assets, that even at the prices the FDIC is selling (around 75% of the true value), to pay out of those sold assets the guaranteed $250 000 and 90%+ of everything over that.

It wasn’t a rescue since the FDIC is currently in the process of selling of SVB assets to get (most of) the funds back they used to make the depositors whole. It isn’t a bailout either since shareholders lost everything. The only ones made whole were the depositors (at an estimated cost of $20 billion more then the sell value of the assets) and that is a cost borne by every other FDIC insured bank in the US. Not the Fed, not the federal government, not the tax payer but the other banks in the US that have FDIC insurance.

Yes, but the Fed provided the liquidity by printing money. That’s the part I have an issue with.

No more money printing for any reason, whatsoever.

Again the Fed did no such thing.

Unless you complain that any insurance you have is financed by the Fed printing money when you pay your insurance fee.

I think I have figured out what you are confused about.

It is other banks that have been borrowing from the Fed to cover the liquidity crunch that resulted from the starting panic once the run on SVB started.

Most of, if not all, that money has been repaid already since the rent on this specific type of loan is ridiculously high from the perspective of the banks (that also means in the end it aided the Feds goal of QT by taking a bit of money from the economy instead of adding). Wolf will probably write about that next week or in three weeks when he discusses the Fed balance sheet again.

Sinhalese the fed can’t print money,banks bailed out svb bank .Maybe fdic is broke

@Who Cares,

re “The FDIC is not the Fed.”

they effectively are b/c Board of Governors of the Federal Reserve System “Federal Reserve” are the regulators/controllers of the FDIC.

I don’t know if it would be an explosive surge, but yes it does seem like a bounce is possible. All it would take is for cars and energy to creep upwards while services remain high. Then the headline numbers start trending up again. Can’t have everything hot all the time, though.

The core issue here is right under the nose of everyone and they are failing to see it. When the Fed gave banks loans at 100% of value of certain assets, they basically did the same thing as issuing a massive new round of QE, at least in terms of how it impacts markets. They essentially reversed 1/2 of the previous QT.

I explained this before, but when investors withdraw cash from a bank, normally that bank would sell their liquid assets (Treasuries). This would make them a seller and if the customer put their money in money markets, it would create a buyer on the other side and the markets are not impacted. But if the bank takes a loan from the Fed against their asset, it prevents a sale, while the cash that a depositor removed can and usually is reinvested and would be stimulus to a market. There are some differences between this and QE, but not enough to matter.

The Fed would probably argue that tightening of credit conditions somewhat offsets the impact of their program on the overall economy. But it had an immediate impact on prices of assets – propping them up again.

These loans to banks are intended to be very short term and for the balance to revert quickly, since they are being charged almost 5% interest, it is expensive money. But in this case, unless those banks can either decrease their loan balances, sell some securities that are not at a a loss or get more depositors money, they cant pay back the Fed quickly and these loans wont be paid back quickly.

Let’s see how rapidly those programs get paid back.

I just looked at the h.4.1 publication that came out this afternoon. The total Fed balance sheet was reduced only 12.7 billion in the past week. At this pace, they would only be reducing the balance sheet by a little over 50 billion per month.

AND those two bank facilities actually rose about 4 billion during the week. So far, they are not looking like a temporary injection of liquidity, they are looking like more semi-permanent QE.

Today is the 13th of the month. I believe the Fed gets their payments on their bonds on the 15th and 30th so it’s not that smooth of data looking at it week to week when you are a few days before they would get paid on those bonds and their total balance falls. Last week reflected end of March payments hence a big drop unlike the March 30th release.

I do agree the “temporary” BTFP and other facilities are behind the run up in asset prices. It is providing liquidity. Assets/markets go up when there is more liquidity and down when less. QE or BTFP etc…liquidity injected or not is what matters. Bank gets money from Fed for deposits. Customer then buys Tbonds/bills, MMF, stocks, cars, houses, gold, etc. Same result, different way it got there.

Interestingly, I have been keeping track of daily flows on SWVXX and SNAXX MMF through Schwab. Same fund, the latter requires $1mm minimum initial. The latter has had daily OUTflows for a month now except like 3 days. The former inflows now. So bigger money moving out of that MMF…

Side note on cars…I bought a car last month. I’m in the US, but bought the car in Japan. Being stored there until I can legally import it turns age 25. I think going forward I’ll just buy my cars from Japan used and import as the condition is amazing and they have cooler JDM-only cars that never came to the US. Plus I can avoid US stealerships and junk condition cars and their lectures on trying to get me to finance rather than pay cash like I do. Done with US car industry…

Just to clarify and not give false impressions – it makes sense for there to be weeks that are high or low in terms of assets rolling off the balance sheet, it just depends upon what is maturing that week.

But is significant is that we dont see the banks paying back those facilities – yet.

Don’t know if it is QE or not, but the bailout of the troubled banks certainly caused a massive rally in the stock market. Still hoping a black swan event would be able to stop this obscene asset price pumping.

gametv

Your first Fed comment is nonsense on several levels. And I explained it to you before, and I won’t waste my time here again. I’ll just address one:

You missed the QE party. It’s long over. It only last two weeks, LOL. And you’re still dreaming about it. What we now have is QT = balance sheet plunged.

The Fed’s balance sheet plunged by $119 billion in three weeks! Mega-QT Now!

QT happens mid-month and end of the month. Next week will have the mid-month Treasury roll off on it, and the balance sheet on May 4 will have the end of the month roll-off on it.

My headline on May 4 will say something like: “Fed Balance sheet plunges by $300 billion in 7 weeks.”

Both the Discount Window and the BTFP combined have now dropped by $25 billion from the peak on March 15, to only $139 billion. Each one of them dropped. This stuff didn’t go nearly as far people imagined (they salivated over a dream of $1 trillion, LOL), and it’s already unwinding a lot faster than anyone expected. This show is over.

right gametv wikipedia chimes in …..

“If it looks like a duck and it quacks like a duck, it’s a duck” stands at the heart of all scientific thought. We may imagine that it is not a duck;…

Wolf, but shouldn’t the level of drop be much higher, because it should encapsulate both the normal QT runoff and these new programs unwinding? If not, at best, isn’t the new money just countering the QT, and leaving it neutral?

Einhal,

Re-read my comment. You didn’t get anything. Read the whole entire comment, including the part about when the Treasury roll-off (QT) occurs.

Wolf, I read it. But then what explains why every asset class is melting up, along with rate hikes expectations dropping, and bonds being bid to the sky?

they’re not melting up. They’re all way down from their peaks. Markets move up and down. That’s what markets do.

Einhal,

In my *opinion* – not fact – it’s probably psychology; it “smells” like the Fed will pivot, and Powell’s famous 2018 pivot despite all his lamentation to the contrary gives added weight to the idea. Meaning, elements of the market (not the bond market, as I understand, but I’m no expert) are betting on Powell and the Fed to give back the punch bowl, and they are laying money on those bets. As in, buying equities, etc.

As Danielle Dimartino Booth might say, “They haven’t given up the notion of a pivot, nor bought into the idea that the Powell Put is serious.”

Just my two cents, which when adjusted for inflation is…well…

And Einhal, I assume you are referring to the fact that the markets seem to have been UP far more than DOWN these last few weeks, right?

Short-term thinking and ignoring the overall signs of recession, as well as not believing Powell is serious, I feel.

My confidence is now restored in the logic of economic value.

Yes, a depreciating, wasting asset like an ordinary used car should appreciate at 3x the rate of annual inflation.

If this continues, I will cash out my 401Ks, buy 50 5 year old KIA’s, quit my job then sit back and enjoy the windfall of contrarian economic functioning.

There were speculators buying brand new cars from one dealer then selling them to other dealers for a profit. This is what happens when the FED goes full money printing derangement.

Yeah, we bought a 2021 Honda Accord CRV. It is the low end model and pearl white.

$33,000 out the door includes extended warranty (100,000 miles / 7 years).

We took Honda’s offer for a car loan at 1.7% interest rate for 6 years.

We barely got to negotiate as they just gave me a $500 discount for being a military retiree. They also gave us free floor mats and cargo mat.

And we had to wait for a car salesperson as it was that busy.

.

Honda’s are great cars! I will always own a Honda. They last a really, really long time.

I bought a 2023 low end for same price

I’m looking at a 2020 Chrysler (Pacifica Hybrid) with 150k miles for $25k and calling it a good deal. If anyone had said this 5 years ago I would have died of laughter.

Biker,

Used and new cars are absurd. I have been around for a few decades now and the last couple of years is the only time I have ever seen car values go up as they are used. Truly baffling.

I just bought a used car and I had to be persistent and very patient to find a good deal. I bought off craigslist. The dealers I visited in the beginning were delusional with pricing and quality and I quickly realized the only chance I had at getting a decent price was buying from the owner.

I think this is a dead cat bounce with used car prices.

I drive by my local car lots on my way to work and the lots are stuffed with new and used cars.

Why can’t Chinese automobile companies come to the USA? The Japanese did so starting in the 1970s and some of our finest brands are Japanese. These bloated corporate margins are exactly what the “Big Three” Detroit automakers did in the 1970s stagflation event. 1970s stagflation apparently is the template for today’s economy that the Federal Reserve is using.

The Chinese make some good cars that are greatly expanding their offerings currently in Russia. Warren Buffet is invested in a Chinese car company, although reducing his shares.

From living through it, the huge amount of Japanese imports in the 1980s seems to have greatly helped inflation of that Era; just look at the history of Japanese car makers voluntarily limiting their exports.

With no real anti-trust enforcement and greater and greater consolidation, it appears that only are foreign friends can help.

The Japanese didn’t “voluntarily limit their exports”. There were import quotas imposed by the U.S. Government limiting what each manufacturer could import per year. Hence, the transplanted factories which then got whacked with content requirements. It got so goofy that some Japanese imports took station wagons and changed the back seat angle so the cargo area would qualify it as a “van/truck” – but it wasn’t a pickup (which had the “chicken tax” on it).

Chinese cars, for the most part, won’t pass Federal crash standards, emission, and equipment levels (like backup cameras for people too lazy to turn their head). The Buicks from China are built to be sold in the U.S.. Same reason the air cooled VW Beetle continued to be sold elsewhere after it ceased sales in the U.S..

And for the importer of JDM vehicles. Good luck getting parts for a discontinued car that was never sold where you live. Heck, our sacrificial airport hooptie (that’s 17 years old) has a ton of NLA parts and the repro stuff (mostly from China) is junk.

Hmmm….

Well, I bought a Chinese-made air compressor for my 18-year old daily driver Subaru 3-months ago cause the next one up was $500 more.

It lasted a grand total of…. 2.5 months. Just blew apart. Just in time for summer. China probably can make good stuff, but they don’t and they’re not going to. All of their products are crap. Absolute crap.

The Chinese are here already. It’s called Volvo – owned by Geely. Also their EV brand Polestar. We impose a 27.5 percent tariff on Chinese vehicles – but if they build factories here then there will be blood in the water for legacy automakers. The process is already beginning in Europe.

@Neel Kash & Kari,

re “Chinese vehicles – but if they build factories here then there will be blood in the water for legacy automakers”

how so? Their supply chain would still get it with tariffs, so they’ll have the same cost of labor, supplies, and materials as all other US makers.

Any truth to the rumor that cap one is pulling floorplan? Or that Santander is going the same route with mom and pop lots only?

Bloomberg:

“Capital One Financial Corp. is winding down a lending business that car dealerships use to buy inventory. The bank decided on March 29 to exit the business this year, a spokesperson said in an interview, citing the “more challenging economic environment.” The bank said the decision has “no impact” on its consumer auto-finance business, and that the so-called floor-plan lending operation was “a non-material component of our commercial banking business.”

Sounds like Capital One is a small-scale player in that very competitive field dominated by the captives. And with a lot less inventory on dealer lots, there is a lot less to finance. So maybe not worth it. Lots of companies are shuttering smaller unprofitable divisions that didn’t get much traction. Look at the mortgage refi business, 70% is gone, and lots of people got laid off.

TL;DR: Prices for new and used will remain elevated due to severe supply/demand distortions. Unless, and until consumers go on a buying strike….get used to this.

Related to tight supply: I don’t foresee supply of used vehicles improving at all for years, considering we are just now exiting 3 years of constrained production. Lots of people in 3 year leases electing to buy-out their lease and hold on to the car once they saw the payment for a new replacement vehicle jump by $200+/mo.

Related to demand: If finance rates for autos remain high, especially so for used vehicles, this will have an impact upon prices that consumers are able to pay.

Consumers got addicted to highly subvented and 0% rates since 2001 as “normal”. Payments jump quite a bit when you’re not paying .9% on a 72 month note….

A while ago Wolf wrote an article in which he pointed to.a pent up demand of “lost” sales during COVID, due to supply issues that reduced sales below their natural trend. It is my assertion that we are probably actually seeing some of this pent-up demand hitting the car markets now and for some period of time into the near future ( a matter of months or maybe a year to go).

But once this pent-up demand tapers off, sales of vehicles will go much lower, as they did in 2008. My premises are all built on an assumption that we will have a deep recession and prices of many assets will collapse, starting between April and July.

If you look back at how the stock market reacts to the level of Fed balance sheet, you can see that the market is no longer capable of sustaining a prolonged period of the Fed reducing its balance sheet.

I agree that there’s pent up demand – but the supply of vehicles to be purchased, new or used, is not rising to meet that demand.

Yes, at some point consumers accept the inflation and pull the trigger – but that becomes difficult if there’s nothing to buy. ;-)

My wife’s Grand Cherokee lease comes up in 12 months. We’ll likely buy it out if prices remain where they are now. I’m in a situation where I don’t *need* another car, but as a car guy, I’m the one sitting on the sidelines waiting for a deal – then i’ll move.

I should have said: supply is not rising *fast enough* to meet demand.

Grand Cherokee? Did Chrysler suddenly start making cars that last?

I wouldn’t be surprised if the housing market did the same thing.

Personally i believe housing prices along with inflation in general will reaccelerate upwards by the 3rd or 4th quarter. Pure conjecture…just a hunch

Thanks again Sir…..

Hopefully this is just a bounce on the way further down. But the hard push for electric vehicles by the Fed may be driving this consumer interest in used vehicles. Either way, it seems as though the auto market is going to continue behaving erratically for the foreseeable future. Always enjoy your posts, Wolf!

MOAR! MOAR! MOAR!

It may make more sense to buy a used vehicle at the present time. Electric vehicles are still expensive and the technology is not fully there yet. To buy a new ICE vehicle is to acquire a 15 year asset that may be an albatross in 6 or 7 years. So that leaves a used ICEV with a useful life of 7 or 8 years as an attractive option, which should push the value of such a vehicle up. Maybe that’s what us happening.

“To buy a new ICE vehicle is to acquire a 15 year asset that may be an albatross in 6 or 7 years.”

I don’t believe the plan is to stop selling gas in 7 years, so why would the ICE be an albatross?

Buying new ICE might be the best option right now. The transition to EVs is being mandated with no regard for cost, energy infrastructure, or availability of required minerals. I’m not confident that all the pieces are going to fall into place in the timeframe needed for a smooth transition. What happens when new ICE cars are banned and EV issues are unresolved? Gonna look like Havana

ICE will be around forever. Why? Because alcohol will be around forever. Modern cars (1995+) can easily be converted to run on EtOH without destroying the fuel tank and other systems. Congress already tried to outlaw alcohol once and that didn’t work. Won’t be commonplace, but will never go away even if oil/gasoline end up being impossible to find or produce for small areas. Easier than batteries in middle of nowhere. Biodiesel, too.

There’s also low carbon sustainable synthetic fuels with high energy density being developed. Toyota and ExxonMobil announced… (from a TMC presser):

“ExxonMobil is exploring innovative fuel blends with the potential to reduce greenhouse gas emissions from road transportation up to 75% compared to conventional fuels available today.*

Toyota has determined that these innovative formulas are compatible with older vehicles as well as its current model line-up.

These lower carbon fuels are also compatible with existing fueling infrastructure.”

Yes, synthetic fuels are getting more interest. Porsche has a facility in Chile for that and hope to expand. I think that will be the workaround the sports car makers in Europe like Ferrari will use to not have to do 100% EV since it will still be carbon zero (or close to it).

My favorite maker, Koenigsegg, has been running E85 in their 1,000+hp cars for a while. Just recently they started to use methanol created from CO2 emitted from volcanos. It’s called “volcanol” and a few articles are on it mainly on biofuel websites. Some YT videos he talks about it…very cool guy, too.

Alcohol is hygroscopic.

How do you get the ethanol? Heat required to distill costs energy. High boiling azeotrope needed in order to refine above 95 % pure, so you need benzene or similar. Kinda explosive if you are not equipped to refine at this purity, drinking version is ~ 40-50 % pure with a much lower vapor pressure.

Keep in mind lots of things besides cars run on gasoline: snowblowers, landscaping equipment, portable generators.

I have a 50cc scooter which gets >100mpg.

I wish cities were set up for scooters and motorcycles in a way where they didn’t have to mingle with cars and trucks. Drivers today, and the congestion, make it too dangerous to ride in my opinion.

Cars ( of all kinds) are only to get more and more expensive relative to the wages of the middle class. Think about how simple the supply chain was for an ICE motor like a ford v8 in the 1960’s. Ore came in on the lake from Ford’s mines in Minnesota, was unloaded and cast in to engine blocks a few miles from the dock in Cleveland. A bit of rubber, some gaskets, and springs and you had an engine, built and sourced in a small area. Now think of a modern ICE drivetrain, or EV drivetrain that has tons of intricate, complicated parts sourced and carried from all over the world. The golden age of motoring is over and we will soon be like Cuba, patching up old cars and riding around in crazy jitneys and such.

Absolutely!

Cars were initially available only to the Nobles and Aristocrats or the Military. Ford saw it and say a man should walk into the store and roll out a car today. Bill gates wanted a desktop computer in everyone desk. Steve Jobs gave a smartphone (Bri’sh intelligence will give it to 007 agents only), to common people. This is what “American” is. Being able to afford what only nobility could. Everything is now becoming an old world with a peasant class and master class. Financial engineering or not, now everything is now available only to the nobles from now on.

I agree that marvels ( like the auto) once available to the middle class in America will soon only be obtainable by the 1 percent who succeeded at strip-mining all the value out of the last 100 years of hard work, and innovation of the American project . But I don’t agree with your use of the term Noble. There is nothing noble about the current band of pirates atop the financialized economy. When I look at Zuckerberg or Bezos, or Kenny G, noble is the term farthest from my mind.

That’s all “nobles” are: the descendants of rapacious pirates. Any noble family, any single one you choose, was started or founded by some pirate, warlord, bandit, slaver, or gangster. “Nobility” is something invented by the children of said gangsters to justify their wealth and power.

That’s how history works, all the way back to the Lugals in Sumeria.

Just across the Mississippi River from my home, and a mile downstream, in 1925, Henry Ford set up the St Paul factory. He had hydro-electric power from the river, access to good quality hardwood from Minnesota’s and Wisconsin’s forests, railroad supply lines, and a skilled-labor supply.

It’s been a decade since the last Ranger pickup truck rolled off its assembly line. Now the factory is gone and the acreage has been redeveloped.

As I rode my Minnesota made OTSO gravel bike along the river today, a few vultures circled above me at the Ford Parkway Bridge. Maybe they know something I don’t. I prefer to see eagles instead of vultures when I ride. Just a little superstitious, eh?

Seems like everything got a boost of spending in last couple of months. Houses/condos etc in Chicagoland area all of the sudden are listed $80,000 – $100,000 above what comparable were listed on market few months back and go under contract in days.

Stock market got boosted out of thin air, bitcoin while down 50% from highs got nearly doubled since beginning of this year.

I truly believe that SVB was nothing but a trick from wall street to get FED to involuntarily pivot.

I have almost 32 Trillion reasons the world seems upside down. The 536+1 should have been stopped long ago. Stay out of debt and the future is gonna be fun to watch…..

The FED is fueling and coddling the biggest speculative bubble in the history of mankind. Their tiny little rate hikes are laughable and have done nothing to stop inflation. They know this, they just want to protect the bubbles at the expense of the majority to benefit the wealthy.

The billionaires and hundred millionaires their policies have created are a cancer upon society. These ungrateful, entitled scum said nothing when shelter became a luxury good reserved for the wealthy, where record numbers of homeless line the streets and the working poor live in their cars or modern day boarding houses, but cry publicly for a little more free cheese if their net worths take even the slightest ding.

Trickle down economics is a lie, and QE is a lie. All they do is harvest the wealth of the working class and poor, and give it to the rich. John F. Kennedy stated “everything is a rich man’s trick,” and he was right. This country has been hijacked by these scum, and it’s time to get rid of them.

Perfectly said. It is a hopelessly unjust world we live in. The question is when and if there will be any retribution for the perpetrators of this kind of extreme injustice. A resurgence in the CPI next month would be one way to punish the financial elites and the fed, who have repeatedly gotten away with their crimes against humanity.

Wolf’s “Not Seasonally Adjusted,” Says a lot related

DC : Your right ” little rate hikes are laughable ” > Thing is < Every Past Normal / Used Ore ever used in the water the economy brings only small

ripples then a slack tide leaving Inflation as the Driver

Inflation is the Drivers Seat Going Up and Going Down but Now Unstoppable in the near term

Used Cars Going Up LOL anything Cheaper is going to go up now .

Inflation Offsets Like 4.65 APY Liquid Bask Banks Latest Pump trying to

Draw Deposits . Banks are now like a discount window for the public

but the laugh is your not getting Interest but a discount on your losses

Incurred from Inflation . End the Fed ? and what ? replace it with what

some guy playing Bagpipes passing out Free food , Free Gasoline and Electric power as example. if you make a lot of stuff Fake then you become Fake Evan Inflation is Fake just a ruse for making Fake Money.

Its Easy to say " Its Working " when you see a small correction but is it really working ? / With Interest rates climbing along with Gold tells the true Story it seems to me watch out stock market looks like a house on stilts not a real foundation

DC… you said…

“This country has been hijacked by these scum, and it’s time to get rid of them.”

Absolutely… it’s only 110 years overdue!

The accepted meme that there is an inverse relationship between interest rates and growth is total bollacks and another component that TPTB use to perpetuate the pump-and-dump schemes that benefit the

obscenely wealthy oligarchs and impoverishes Mainstreet.

The truth is that there is a positive correlation and that economic growth happens first and interest rates follow along – higher growth leads to higher interest rates and lower growth leads to lower rates.

Low interest rates crushed the productive US economy and encouraged financialization. Central banks and more than 90% of economists always blather on about interest rates as their go-to strategy when it is simply a diversion and an alibi.

What drives growth is not interest rates at all – it is money creation – ie the quantity of credit creation and more than 90-97% of this is created by the banking sector.

If this money creation goes into consumption inflation will result. If

it goes into investment in existing assets it will be inflationary and this is exactly what is happening post the covid measures.

If this liquidity was only directed into the productive sector and was invested into healthy products and services then it is not inflationary and at the same time, interest rates can be raised to reasonable levels. This would then encourage a savings culture to develop again and would in turn provide begin the cycle of providing further liquidity for a healthy real economy.

The Fed is a monumental con, but so too is this tripe where the entire financial industry of the Western world misrepresents interest rates as an effective monetary tool in managing an economy for the good of the nation and society.

It completely ignores the demand side and has us believe that this control must come from the supply side. Was it JFK that said… “Everything is a rich man’s trick”?

Cheers

Col

I blame consumers. Americans were already poor consumers, in terms of tying their identities to what they drive or on just being consumers as an ethos. Nothing else explains the wholesale move to CUVs and SUVs and AWD for everyone (it may snow once!) versus sedans, coupes and wagons. Once the buying public showed their hand, manufacturers figured out that they could produce far less and still make the same profit. Anyone that can’t afford it or feels that $40,000+ for some bland crossover with technology that will be obsolete in 5 years is absurd is forced into the used market. With no reasonable new $20,000+ vehicles available used vehicles have naturally moved into this slot.

Severe inflation in new home and new car prices over the past three years has driven very large numbers of purchasers down market into used. This dramatic increase in interest in used cars and homes has jacked up their prices, affected transaction volumes and restructured the relevant markets. Look for the average age of vehicles on the road to keep increasing and high prices to stay high. The transition to EVs may run into a buyers’ strike and the used SFH market may turn into an auction based model.

Consumers with no self-control or discipline are surely part of the problem, but the fact remains, if you print $5 trillion and nearly all of it ends up in the hands of the already wealthy through inflated asset prices, they’ll spend that new “wealth.”

I’ve said it many times before. Current inflation (full restaurants, high car prices, high travel prices, etc.) is a function of the top 10% spending their asset gains. Someone who expected to have a $5 million portfolio in retirement who suddenly has a $15 million portfolio is going to spend with abandon.

The Fed has to knock asset prices down or inflation will stay at 5-8% indefinitely. There is no door #3. CPI inflation will not return to 2% while keeping stonks and bitcrap where they are.

I read somewhere that once inflation is around 5% it will no longer be much of a priority for the Fed and they will back off. I hope this isn’t true.

Lucca,

CNN has an article out called “US inflation just reached an inflection point”

“Some economists believe that this level — around 5% — is the point at which inflation is no longer considered an emergency issue. That means the Federal Reserve could feel less pressure to quickly stabilize prices through aggressive, economically painful interest rate hikes.

‘Once inflation gets down below 5%. It disappears from the headlines,” Johns Hopkins economist and central bank scholar Laurence Ball told Before the Bell last month. “People go back to worrying about budget deficits or climate change or other public issues there are.”‘

They go on to hype how returns were like 12% during other periods of 5% inflation blah blah blah. Buy more stonks. Stonks go up.

IMHO service inflation is still high. Housing costs are still redonkulous. People are still giving Elon Musk and Cathy Wood money. Crypto still exists…

Tighten J. Pow!!! Crush them all!!!

(ง •̀_•́)ง

If inflation is 5%, and the Fed says, ok, fine, this means higher interest rates for VERY LONG. If markets see that inflation will be 5% going forward, and that the Fed is happy with it, and won’t do anything about it, then the 10-year yield will spike to 7%. And mortgage rates will spike to 9%. And they will stay there. Can you live with that?

Right now, the entire market psychology is based on the hope that inflation will be back at 2% by the end of this year or early next year, LOL. So if the Fed says, 5% is fine, then yields will explode.

Then Powell would be doing an about-face. Because he’s always said his #1 priority was getting inflation under control, back to 2%.

The people with wealth you describe are not spending and are not the source of inflation. There aren’t that many people with 15 million dollars. When used car prices and basic restaurant meals double in price, it’s not the 0.1% driving that bus.

Slow down Happy1,

“There aren’t that many people with 15 million dollars.” is false.

There are depressingly many people with 15 million (not me!).

There are 22 million millionaires in the US. Almost 9% of the population (mostly Boomers). [I read it on the internet, so it must be true]

I would actually argue that they UNDERCOUNT the numbers!!!

People with huge pensions should also be counted. They should use annuity formulas to show the present value of said pensions.

My father-in-law thinks he’s a “poor retired blue collar worker” yet has a pension + healthcare worth millions. Not to mention social security, personal property etc.

First, the top 0.1% has far more wealth than $15 million. Second, I didn’t say it was the 0.1%. I said it was the top 10%. Their portfolios have gone from $500,000 to $1.5 million (just an example). Their $700k houses have gone to $1.4 million.

I agree. I googled how much wealth the top 10% have and according to Kiplinger, it’s a net worth of $854,000. I highly doubt the top 10% are the source of inflation.

All good news about used car prices.

We all need to relax. The 536 are ready for the debt ceiling problem very soon. Bet they fix it ( wink wink ) by making sure THEY never have to worry about a ceiling anymore.

Wolf, thanks for the excellent comment about the 5% inflation. It puts my mind at ease.

Wolfstreet comments section seems like a bunch of people who live honest working lives, saved their pennies, and played by the “rules.”

Naturally, this means they detest those evil speculators who took bigger risks than them, and got rewarded for it in the past few years.

So Wolfstreet commenters cling to the hope that Wolf’s reporting surely proves that the speculators and gamblers will finally pay the price!

Yes, any minute now, the savers will be hailed as the wise ones after all.

But due to widespread laziness and mediocrity, society no longer rewards those with prudence and discipline.

Instead, society stretches out like a used pair of stained sweat pants, to accommodate lazy, undisciplined, reckless people.

Sorry Savers. The retribution for risk-takers will never come. Idiocracy has arrived.

Naturally, this means they detest those evil speculators who took bigger risks than them, and got rewarded for it in the past few years.

Dont think so Pants Relief. Someone may be blocked in their thoughts?

You don’t have to look hard to find “I can’t wait for realtors to lose everything” or “My neighbor was a house speculator, can’t wait for them to lose all the gains they made in the pandemic.”

Plenty of similar comments on these articles, with agreeing replies and little to no pushback.

Must be my blocked mind causing me to read those.

It’s one thing to take risk and reap rewards – that’s being clever and i respect that greatly.

However, any idiot could and made money (one way or the other) during free money era. When FED stopped printing, they have no clue how to make money. Its the same group crying for pivot. Kind of like wild animals that were fed by tourists and no longer know how to survive without being fed by strangers… i think that is what most of commenters despise on this website.

Q2/20 or just another blip in downtrend starting Q1/22?

“Wholesale prices have now regained in three months nearly half (+$1,760) of what they’d lost in the prior 13 months (-$3,199).”

Awfk, rate of change walked in.

I’m sure I’ll get roasted for merely pointing out the economic impact, but some degree of the housing and used car market can be attributed to the millions of our new ‘neighbors’.

Since 2019, I’ve watched my suburban, fly-over town turn into Little Guatemala.

They’re stuffing 2 or 3 families in a 1,200sq ft 2 bedroom house and being gouged $2,200 a month. Next, they buy 5 used cars and slave away at low level jobs.