A REIT specializing in CRE loans foreclosed on 3,200 apartments in Houston. CMBS investors hit by default of 62 multifamily buildings in San Francisco.

By Wolf Richter for WOLF STREET.

Four Class B and Class C apartment complexes, built before 1981, with 3,200 apartments in the Houston area – the Reserve at Westwood, Heights at Post Oak, Redford Apartments, and Timber Ridge Apartments – were sold at a foreclosure auction on April 4 in Harris County by the lender, Arbor Realty Trust, a publicly traded real estate investment trust that specializes in commercial real estate lending. Arbor Realty’s shares [ABR] have fallen by about half since November 2021.

Investors took the loss, not banks, and are still on the hook. As often in CRE, it wasn’t a bank that took the losses on the debt, but investors. We just discussed banks’ exposure to CRE debt, that 55% of CRE debt was held by investors of all kinds, such as Arbor Realty Trust, and/or guaranteed by the government; and we discussed just prior the huge losses some office towers dished out, mostly to investors and not banks.

The debt on the properties amounted to $229 million. According to Bisnow Houston, which confirmed the deal with Arbor Realty, the four properties were sold for $196.5 million in total, that’s $32.5 million below loan value, to Fundamental Partners, a New York-based private-equity firm.

Arbor Realty took the $32.5 million loss on the loan so far, plus foreclosure expenses. According to Bisnow, it continues to be the lender for Fundamental Partners. So it’s still on the hook for what’s left of the loan.

Variable rate mortgages taken out just ahead of Fed’s rate hikes. The former owner that lost control of the properties, Applesway Investment Group calls itself “a privately held investment firm focused on acquiring stable, income producing multi-family properties in emerging U.S. markets,” and pitches “passive income from high-yielding multifamily investment opportunities” to retail investors.

It had gone on a multifamily buying spree focused on lower-income properties during the free-money era, and funded projects with variable-rate mortgages. According to the Wall Street Journal, Applesway took out most of the loans in the second half of 2021.

This was perfect timing for variable rate mortgages: on the eve of the steepest rate hikes by the Fed in decades. According to data by Trepp, cited by the WSJ, the interest on one of the mortgages had jumped from 3.4% at origination to 8%. The purchase of at least two of the properties was financed with about 80% debt. Applesway’s losses amount to the equity portion of these properties.

In addition, Applesway was facing a $1.6-million lawsuit for unpaid work at those properties, according to Bisnow.

The big multifamily default in San Francisco hit CMBS investors, not banks.

CMBS investors, not banks, were hit by Veritas’ default on a $448 million loan on 62 older apartment buildings in San Francisco. On the maturity date in November 2022, the joint venture between San Francisco-based Veritas Investments and affiliates of Boston-based Baupost Group refused to make the $448 million balloon payment. And they didn’t exercise their one-year extension option. They just defaulted on the loan. The loan has since then been in special servicing.

The floating-rate loan with a two-year term and a one-year extension was originated in late 2020, during the free-money era. The idea of much higher rates didn’t occur to investors, and they eagerly piled into it when the loan was securitized into two CMBS by Goldman Sachs: $344 million in GSMS 2021-RENT and $104 million in GSMS 2021-RNT2.

The loan is non-recourse; if investors eventually foreclose on the 62 apartment buildings, that’s all they would get, and the losses could be substantial. Given the condition of the San Francisco rental market, it would likely be the worst option for lenders. They really really don’t want to have to sell those buildings in a foreclosure auction, which would make a huge mess for other landlords too. Veritas has said that it is in talks with the special servicer. And according to Fitch, which rates one of the CMBS, it is looking for a partner to recapitalize the properties.

Floating-rate mortgages and new supply.

The special servicing rate of multifamily CMBS – an early indicator of trouble – has steadily increased since interest rates began to rise last year. In March, it rose to 3.0%, up from 1.7% in March last year, according to Trepp, which tracks CMBS.

Floating rate mortgages taken out during the free-money era are now causing all kinds of havoc beyond multifamily, including the defaulted Veritas loan, the foreclosure of the Houston apartment properties discussed above, and the default by PIMCO’s Columbia Property Trust on $1.7 billion in office loans, including two towers in San Francisco.

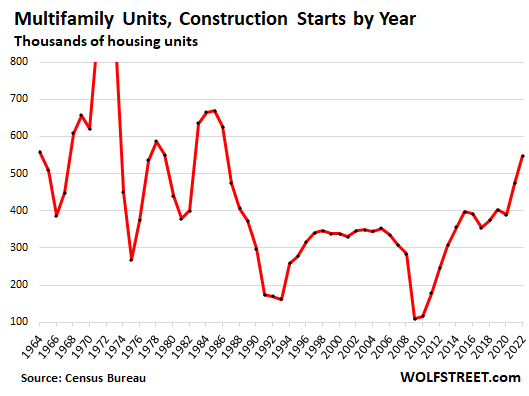

Boom of multifamily construction pressures older apartments. In 2022, construction started on 547,400 units in multifamily buildings of two units and larger, the highest since 1986, when the last multifamily boom ended. And it was up by 55% from the peak this millennium in 2005. And it followed the 473,800 units that were started in 2021, the most since 1987.

The construction boom has been driven by sharply rising or spiking asking rents and cheap money. But now, asking rents are no longer spiking and the cheap money is gone, and those units are coming on the market. These latest and greatest apartments with the modern amenities that people are looking for – much of it is higher end, because that’s where the money is – will find tenants if the rent is right, which triggers a flight to quality that pressures buildings down the line.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m wondering if the tax money raised by the Homeless Industrial Complex will buy any of these properties to house the homeless on the streets of SF and Houston.

Read the occupant reviews on the Timber Ridge Apartments website…..rats, roaches, no hot water, no maintenance, etc. Even the homeless wouldn’t want to live there.

so it’s perfect fit for them

you’d be surprised at some of the filth people live in.

No — I gathered what he was saying is that even the desperate & the dispossessed deserve more dignity than the typical KILZ-covered turdholes that work-shy slumlords offer up for lease.

Just my take, though.

Diddley is in no-empathy troll mode today….he’ll be back to taking his whole “crew” to lunch sooner or later.

and, yeah…just my take though, also.

Yep think about the ownership structure of these projects the owners are property managers that have sold the mortgages to another party that then sold the mortgages to the the retail investors. All packaged up and passed down the line . Unpaid work of 1.6 million contractors will refuse to work for the property management company not just on these properties but others they own. Quality drops and then the tenant quality drops and eviction difficulties mount. A private equity group (more of other peoples money) now own the properties but with lending from the previous lender. Flight to quality will drive this behavior and Houston has properties built like this all over the city from the population boom that occurred in the 1970s and early 80s. No short term fix if a fix at all. No idea how this will end but thinking about what people own through investments is not something they would touch if they knew. Cash flow marketing gimmicks that are invisible to the owners.

Each cycle brings out excesses. From the syndicators in the 1980s onward, the eventual retail buyer is sold a problem that is waiting to ripen.

With you mostly reply:::

Except for the implication this kind of ”stuff” AKA shieet has only been recent.

Fact is that JPM did exactly the same thing a century or more ago,,, as did Crockett and Stanford and the Hartford clan including Huntington Hartford,,, and all the other so called robber barons when they saw what was happening BECAUSE THEY had the best communications available at the time…

BIG changes because of the VAST improvement of communications to WE the PEEDONs…

Gonna have to change OUR name???

MAY BE SO, MAY BE NO???

So true;

The government collects tax money and some were given funds that could have been used for our government to keep taxes lower. Some wealthier or higher ranking individuals received funds, gifts and or invites for exchange and influence of power.

Imagine if those people would have renovated the properties. Imagine if they never took benefits, like Yellen did recently for the trust or buy out. Imagine, if they were able to use these funds to rehab the units and show the people more compassion. Just like Bernie Sanders did and does. Imagine if we were able to rehab the units as a true community.

There have been many studies where when placing lower income people with upper class individuals, the lower class individuals thrive and do much better. Many books have been published and are at our local libraries. See by reading past research, we can use this as an example to better each community where we live.

Imagine if the units were remodeled, provided and furnished with the best technology so the occupants can and could thrive. Imagine if we all reached out. Perception always has two sides. One side is to live strong and build communities that help all walks of life. Are we really better than some or do we perceive we are better.

Crime is everywhere, so are Rats. Even Rats have a place in our eco systems if we look at nature. Huston is an example of the worst. By reading many post, we are really doing the same as what we are blaming others for. Everyone puts skirts, pants on the same way. We all deserve a better life for the time we have here. Guess the question is, how may we improve, influence, and support others to have a better life.

We have a ton of crap roach motel apartment complexes here in Houston. Not a day goes by that you don’t see one on the news catching fire, being served papers fro compliance issues, or being a major crime scene.

That is exactly what they doing up here in Seattle/ King County and paying top dollar for the properties too.

So much so that I am very suspicious about kickbacks/campaign contributions.

EL,

It’s ghetto luxury, don’t be soooo suspicious.

Yep, just like Robinhood. We are over charging the poor to give to the wealthy. At least Robinhood took from the Rich and gave to the poor.

Unfortunately, campaigns are closely and deeply monitored. Every dollar is accounted for and reported. Many campaigns have CPAs, bankers and etc. monitoring every check and dollar collected. They even must post the treasurers name at the bottom of the signs.

They do get many invites to attend functions, but so do each of us. Yes Seattle/King County has had quite a bit of news about the high charges in Kings County. Japan showed us these kind of charges did not work for their economy and some banks that supported the rates collapsed.

I hope to not have following Deja Vu:

Why did the Federal Reserve purchase agency CMBS?

The spread of COVID-19 substantially disrupted economic activity and affected many different sectors of the financial system, including the agency CMBS market. The Federal Open Market Committee (FOMC) directed the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York to purchase agency CMBS as needed to support and sustain the smooth functioning of the agency CMBS market and the effective transmission of monetary policy. The Desk purchased agency CMBS secured primarily by multifamily home mortgages that are guaranteed fully as to principal and interest by Fannie Mae, Freddie Mac, and Ginnie Mae.

Why is the Fed in the long end of the yield curve at all (5 trillion?)

The heralded dual mandate concerns are both current and real time

(Paraphrasing here)

Janet Yellen:

“We are making sure that these essential operations of the monetary system are operating smoothly, and without intervention by the trading desk into these important areas, we cannot assist in financial stability for the average American.”

Literally means “we do what we want, you poors can go ask questions elsewhere”

Or something like that. This would be the answer from Janet, Jerome, or any other empty suit that you attempt to ask a same question to.

Fannie Mae, Freddie Mac and Ginnie Mae failed the economy once before. They even swooped up lands from many landlords and may be doing this as a publicity stunt to cover flaws in the real estate market place. They charged high interest rates.

The desk is not an open market place for others and New York, took most of the Feds money like thieves. Remember how many New York agencies fell back in our last housing bust. Ginnie Mae, Freddie Mac and Fannie Mae once fell even in the strong economy. Citizens rescued them but not for long. When they found the truth behind the lenders, people fled the marketplaces and worked with community banks.

Do you remember how much bail out money it took to clean up reputations and settle lawsuits against the lenders? Heck, even the innocent could see the real picture after the spread of COVID. There was never a smooth transition or function of the agency. If I recall many went down for under handed crimes. Some fled the US and retreated to other countries until the smoke lifted.

Something to ponder.

Lies are never the truth

And the truth is complicated by lies.

I like to try and estimate the occupancy of big new apartment complexes by looking at the lights at 9 pm on a Sunday evening, or counting the decks with anything on them ( everyone puts something on the deck). With few exceptions occupancy is lower than is being talked about. Unlike condo’s which can have absentee owners, an empty apartment is a money loser.

I agree with the balconies. So many empty balconies on these mixed use complexes that have gone up in the last 10 years around SoCal. Cities need to have some way of enforcing capacity requirements. For example if your building has been around for 3 years, it should be 70 percent full. This would help with the homeless situation and create a more realistic form of rent control.

Ridiculous.

It’s private property, it doesn’t belong to someone else.

Instead of advocating the theft of someone else’s property, you and those who agree with you can buy it and let the homeless live in it rent free.

“It’s private property, it doesn’t belong to someone else.”

That only works to a point – which we haven’t reached.

Social contracts become null once a certain degree of inequality and societal division occur. Then it ‘law of the jungle.’

I know, you’re talking about now. I’ve yet to be accused of using someone else’s post as a excuse to vent my mind! : )

Augustus Frost, you’re spot on. It’s amazing how quick people are to steal.

Never mind the fact that such policies will guarantee future rental shortages. Just as rental control ended new construction of multi-unit rental buildings in the 80s, the new generation of laws attacking landlords will do the same today.

So, then, per your values, a pirate equity company could buy up all apartments in a city and charge rents that result in 100% evictions.

Ayn Rand was a sociopath.

Reply to “two beers”… Ayn Rand (whose real name was “Alisa Zinov’yevna Rosenbaum”) was born in St Petersburg, Russia in 1901, came of age during the Russian Revolution and was educated in a communist government sponsored school of media. She then came to the United States, changed her name to Ayn Rand and began her divisive writing career. In some estimations, Ayn Rand was a Soviet plant.

I don’t think you’ve got a terribly sophisticated understanding of “property” there, Augustus, but that’s not uncommon.

Z2b,

“Always remember that the ones you disagree with might not be in the right, but that doesn’t mean that they do it with evil intent. They might have just confused ‘what is ‘for ‘what ought to be’.

*It’s easy to confuse ‘what is’ with ‘what ought to be’, especially when ‘what is’ has worked out in your favor.”*

–“Tyrion”, Game of Thrones(TV), 5×9

@NotDeadYet:

“In some estimations, Ayn Rand was a Soviet plant.”

That’s one of the dumbest estimations I’ve ever heard.

Not to mention that, like you’ve said before, most of this would be irrelevant if not for ZIRP and QE fueled speculation.

Housing shortages and empty units are a symptom of the problem, not the problem itself.

Property rights?

Samuel Adams had this to say:

“Among the natural rights of the colonists are these: first, a right to life, second, to liberty, and thirdly, to property; together with the right to defend them in the best manner they can.”

James Madison:

“The rights of persons, and the rights of property, are the objects, for the protection of which Government was instituted.”

The whole concept of “private property” is not, first off, inherently natural to homo sapiens anymore than it is with any creature. It is only the Laws as created and enforced by civilization which give it meaning, and even the basic idea that people SHOULD own property isn’t universal across our species’ history or cultures. It is a “western” concept of private property you are referring to, and as has been already pointed out that notion – in the modern day at least – is partnered with the notion of a social contract.

Put bluntly, once people become desperate enough, all social contracts and laws built upon them be damned, and people will just TAKE what they have the power to take. The fact anyone thinks the laws will protect them when this really gets going badly are cute, in a quaint way.

This is why social inequality needs always be kept in mind to some degree, even in a capitalist system. The goal is to balance free-market forces with some measure of social/economic safety nets, OR face the torch and pitchfork once enough of the masses feel the system doesn’t care for them anymore.

A whole lot of people advocating things like the destruction of unions forget what it was that gave them such teeth back in the 1800s, and why the “Titans of Industry” gradually realized that giving the working class some crumbs was far better than having them burn down your house and factory, and slicing your throat in the process. Only a fool thinks those days are in the past just because they aren’t happening right now.

Zari – never underestimate the destructive power of greed on societal memory (and, by extension, governance).

may we all find a better day.

“if it’s private property, it doesn’t belong to someone else”

So then when I see one of those signs, it’s just for decoration or something, and I can ignore it?

I always thought so.

You seem to be unaware that none of your tips are reflected in the data.

Let me try to disassemble your pronouncement that ” I like to try and estimate the occupancy of big new apartment complexes by looking at the lights at 9 pm on a Sunday evening, or counting the decks with anything on them” reads like a grand jury indictment.

FYI Here at the Senior Retirement Community, many people are in bed by 8 or 9pm. Others winter in warmer climates. So just counting the units with the lights on after 9pm may not be a good indicator of occupancy.

That’s an interesting hobby

What happened to the housing shortage and rising rents. Guess they can’t outrun interest rates

Maybe … household formations are reverting.

During COVID, the average number of people per household likely decreased. People sort shelter away from dodgy housemates. Increased demand; increased rents.

Post COVID, and with inflationary / interest rate pressure on purchasing power, there might be a trend back to shared accommodation, either with strangers or with relatives. Reduced demand; reduced rents.

Caveat: all real estate is local.

The Fed skewed traditional risk return relationships with their peculiar rate manipulations

Yield chasing

Over leveraging

For every action there is an equal and opposite reaction

Maybe the Fed should stick to a hard rail forumla

Fed Funds = 3 month moving average of a legitimate inflation metric

The idea of a market interest rate makes a lot of sense. In a real boom, activity bids up interest rates on real capital putting a damper on borrowing.

Fed has messed up twice in less than two years. Pumping up money supply in the last year of a housing bubble and now running money supply quickly negative just as the bubble is popping ensuring a crash landing. Two wrongs don’t make it correct policy.

You don’t get it. That sentiment was rejected in favor what we have now.

An out of control Fed that has taken upon itself the shiboleth of the imperial bank that makes decisions in favor of the rich, like the current supreme court.

The Fed is an aristocratic institution inimical to labour.

And as usual, the bag holder will be the small investor.

No, the bag holder will be large investors.

Nope. I own a bunch of ABR. I’m getting spanked too. Even the preferreds are getting slammed. Not a SWAN for quite awhile.

Wolf, thank you very much for the multifamily update.

Wolf Street us the best financial news site on the web.

The Wolfman types way over my head. Love the education from him about the FED………

One of Wolf’s most valuable uncovered data points is just how much “stacked” debt/equity has been pumped into these overvalued assets…multiple lenders holding multiple tranches, sitting on top of (multiple?) equity interests.

That’s how you get goofy overvaluations (well, along with ZIRP) – you get multiple disparate parties (with convoluted, intermingling rights) to all pump money into a deal.

You’ve really got to be a genius deal maker/residual equity holder to aggressively use floating rate financing at historically low rates and not have an escape plan…floating rate was what blew up the retail residential rubes in 2008…how do “pros” make the exact same mistake?

And, at least now we can guess at the cause of paradoxically exploding rents across the nation post Covid…landlords who leveraged up using floating rate debt, desperately trying to dump the consequences of their overpaying/poor financing decisions onto their tenants.

Wolf, any macro stats on which borrowing sectors are most exposed to floating rate debt? Aggregate totals of floating rate debt?

Floaters are an obvious but unthought of iceberg in the exact same way security portfolio impairments were pre-SVB/unZIRP.

Wherever floaters concentrated…that is where the bodies are going to start piling up.

Hey Beevis, he said ‘Floaters’… haha.

It also made me think of a local septic tank company.

And, floaters is probably a spot-on term for what’s coming, eventually.

I’d like Wolf to develop 10 one-hour videos explaining the fed, money supply, and all that, for the dummies (me).

A Wolf Richter Master Class. Not a bad idea. Janet, Joe, Jerome, Ron, Donny and every financially illiterate critter in Congress could learn a thing or two.

This cracks me up. I can’t even get people to listen for the entire 10 minutes all the way to the end of my podcasts, LOL

Can you imagine a whole hour of this?

I put this in a comment at the end of a long thread a few months ago that promptly go ignored but I’ll try one more time: one of the computer podcasts I listen to is called The Cloudcast about Cloud computing geared towards people in the industry. They’ve been doing it for 12 years. In 2020 they started a shorted podcast named The Cloudcast Basics for newer people in the industry. I would totally love to see Wolf create a set of “The Wolfstreet Basics” that go over basic topics like what are MBS and why is it a big deal that the Fed bought them, how is money created, how does the Fed work, etc. A lot of this content already exists embedded in some of the regular posts or in his comments so it would be more a job of curating the content than writing something new. I really believe that Wolf could become the authoritative reference on Finance and it would make his site more accessible to people (aka more traffic and ad revenue) that are less financially literate.

Do it do it do it. Dark background, gotta do the black turtleneck. Use sailing metaphors. It would be awesome. I have lots of friends who NEED to be educated. Heck use AI to make the whole thing haha.

Yes Wolf the video cracks me up as well I can’t listen to podcasts more than 2-3 minutes any more and that’s at 2x speed. Information overload. New content that covers the same subjects that probably require a few months of classroom and coursework . Just this one transaction took quite a bit of work to put together combined with knowledge of how and why the projects even existed to begin with. The good news is the banks are healthier and have less exposure to these issues.

Many decades ago while a student at University, I would take notes as the professor gave the class lesson. Then, in another notebook, I’d rewrite the notes in a legible manner (after scribbling them). This let me replay the lecture in my mind as I did so.

Before an exam, a read through of the revised notes was good prep.

If the subject matter is of interest, it’s easy to stay focused.

“Learn something new every day at Wolf Street.”

Actually for Wolf:

YES I can imagine 10 hours of your very very well thought out podcast.

ESPECIALLY IF,, ( and I know it’s a big IF ) you include in that 10 hours a couple of ”basic” rules of investing, in my case wanting ”basic” rules of investing into GUV MINT treasury products, especially the ”nuts and bolts” stuff for me to understand HOW,,, and WHEN to invest in GUV MINT bonds either directly or through ”brokers.”

Thanks again Wolf,,, another cheque going into the mail to you ASAP.

I agree Phil….I USED to watch a few eggheads who have daily 10 minute videos on various topics.

The problem is, 98% of them feel they have to say something EVERY DAY and as a result, often make fools of themselves by straining to find content EACH AND EVERY DAY. Thus 90% of the content is bombastic and 95% has zero influence on our lives.

I think Wolf would be great if he had a short 5 minute video (if possible) posted ONLY on days with information that truly is important and worth his time (and ours) to produce.

Less is more, time is valuable and I’d love to see a WOLF STREET video on occasion.

I crack up just imagining HALF the members of Congress even being able to understand the first two minutes of a Wolf Street Report, much less the whole thing. And Wolf breaks that sh*t down enough that most of my ex-high school students could grasp it.

Houston, we have a problem…

Wolf – perhaps an indicator that ADD leads to CH?

may we all find a better day.

Is it wrong that I am enjoying seeing these outfits getting taken to the cleaners? Is that wrong?

ask that touchy-feely kind of question to your AI chat bot. but here, in the land of wolves, it’s absolutely ok to enjoy watching what happens to sheep.

Wait 6 months ,layoffs companies downsize . Stock. Market correction perfect recipe for deflation and defaults.Residential will get wiped out . Our banking system expands 10 -$1.00 on loans it goes the other way in a depression.

10 cents-$1.00 sorry

I really think a deep recession is coming, but I still can’t figure out how to play it other than short duration treasuries, a little precious metals and no debt.

Policy is so extreme now, you don’t know what can be done. Bank lending is slowing, but we know banks will lend if government guarantees it.

“The loan has since then been in special servicing.” Not sure if this is the same thing as when I was in banking. In the mid 80s, our Special Assets Department handled nonperforming commercial loans. Another auditor and I were auditing the department. We had an appointment to speak to the department head. He was behind his desk piled so high with loan files that all we could see was cigar smoke coming up over the files. He was in a loud conversation with someone. He waved us in. We sat. The phone call finished. He looked over the loan files and said “Sorry guys, had to take the call, it was the Governor of Alaska.” Apparently, he was working out the bank’s nonperforming loan to a large logging mill that had political implications in the state. So Special Assets are serious business with important political implications beyond just financial outcomes. These guys are heavy hitters.

“According to Fitch it is looking for a partner to recapitalize the properties.” Translation: they are looking for someone dumb enough to put money into this dog.

Thanks for these latest series of articles! They’re much more informative than the mainstream press on the state of real estate liabilities. That said, I wonder if focusing on potential losses to banks is fighting the last war…

The last GFC in 2007/08 hit investment and commercial banks who had held onto large portions of the securitized loans they marketed to others. But now, as you’ve shown, banks have fairly small and probably manageable exposures. The real exposure is now with investors. So perhaps we should be paying attention to pension funds, insurance companies, etc?

It’s sort of like how the changes in the pound sterling markets led to gilt-based distress in pension funds, not banks. So if the next financial crisis were to occur, what are the actors most likely to fail? And more importantly for us as taxpayers, who will be considered too-big-to-fail and be bailed out?

I can easily see public pension systems being bailed out if they get caught. Next up would probably be large insurance companies; no politician wants to tell their constituents that grandpa’s life insurance policy, that he’s been paying into for decades, is no longer in effect just when he’s about to croak. Depending on how craven the politicians will be, it could then include purely financial players like REITs, private equity players, and hedge funds.

The biggest story of the last GFC was how distress would show up in seemingly unrelated markets. I remember how monolines, an obscure industry no one outside of bond traders studying for their license exams knew about, suddenly became a front-page issue and needed to be bailed out (they didn’t need to be, IMHO, but they were, nonetheless).

Since that time, regulations have forced risk to be dispersed away from systemically important banks. But that risk isn’t gone. It’s just pooled in other parts of the financial world. Parts that regulators, always fighting the last war, aren’t looking at. My concern is that some of those parts will be deemed too-big-to-fail, and bailouts will be undertaken once again.

FWIW, I do think the Bank of England and the Fed dealt with the pension and bank run issues, respectively, fairly well. The temporary market turmoil was resolved without taxpayer cost and without stopping QT. But if a big public pension fund blows up because they went chasing for yield in CRE that is now going down the toilet, political pressure will be immense to step up and make them whole in one way or another.

In CA the state pension fund obligations would be met by the state, which is already running a deficit. The banking crisis isn’t over and the Treasury has no policy for bailing out depositors, other than the one they abrogated. They set regional banks up to fail, which is the main source of lending for businesses. Without viable apartments the homeless problem gets worse, and very little affordable housing in this state was ever affordable, its simply subsidized expensive housing. If you can’t make it building apartments during the biggest housing squeeze in history, something is broken. Now I understand Blackrock is handling the sale of MBS for the FED, while Blackstone, which is seperate is deep into the homes for rent business. Then they cool off the labor market. I wonder how section 8 will work this time around?

“…if a big public pension fund blows up because they went chasing for yield in CRE that is now going down the toilet, political pressure will be immense to step up and make them whole in one way or another.”

That’s what the PBGC is for. Of course, when it gets swamped….uh oh.

Remember Mario Draghi? He had his hand on the printer and said he would do “whatever it takes” to defend the Euro, and the run on the Euro ended. The Fed will also do whatever it takes to stop any runs on banks, pension funds, insurers or other financial entities that it worries might start a wider panic. That’s why the stock market keeps holding up; they know the printer will start if an important player wobbles, and practically any financial entity can be deemed important. SVB is a good example.

That’s only possible as long as the DXY doesn’t crash.

There won’t be infinite “printing” at the risk of placing the Empire in jeopardy.

The Empire is already in jeopardy. Inflation of the currency is a late stage defense mechanism in the face of chronic trillion dollar deficits and negative real interest rates during peacetime and in the absence of a recession. Printing is what the US does now and there is no turning back.

Better have gold then.

And yet the Association of Realtors says we’re at/past bottom. 🤣🤭🤦♂️ Truth is, we’ve barely seen the tip of it.

Step 1: Draw down 2 decades of monopoly money equity from existing homeowners with the allure of new, severely overpriced homes.

Step 2: Make the up and comers (Millennials and Gen Z) think they have no choice but to chase and compete with said monopoly money equity, locking them into wage slavedom for a couple decades.

Step 3: Tank the stock market, draining the excesses in 401(k)s

Step 4: Crash real estate for the better part of a decade due to persistent stagflation.

Step 4: Buy back into real estate in the basement as Boomers exit the world stage left, leaving their heirs with capital losses on their homes purchased 2018-2023.

Gabe,

My fav Boomer quote is from Saturday Night Live:

Boomer – “I got 5 houses, good for me!”

-“Boomer Got The Vax” SNL

Powell and every politician want to keep older generations solvent as they continue to piss away their money. Forget the fact that they got fat pensions, full social security, houses for cheap, free or reduced college education…

You youngins are just lazy and eat too many avocados!

As an aside my my wife barely missed the pension cutoff for her last job (26 years at same company). IF she had gotten it… Wow. Just wow. Pensions are fat. Maxed out 401ks don’t even compare to pensions. Her dad also retired with 100% salary (El Cerrito near you Wolf). Potentially 40 years at 100% wage payout + Kaiser medical. Pretty rich.

You have to try to understand where the revenue for the pension is coming from. If it is an unreasonable pension then don’t own the stock or live in the locale that is being taxed to fund it. Vote with your feet is about all you can do.

The pension crisis is too big. Nobody will fully escape it, some will just be worse off than others. The private sector saw the insanity of defined benefit plans long ago. Governments continue to offer them. John Mauldin has done some great writing on this if you’re interested.

Had to work hard to mess this up. The complaints over the past year have been about rising rents, housing shortages, etc. Like Zillo losing money in a rising market. SBA bank failure. Too many MBAs…..

My son was living in Stuyvesant Town in NYC ( the largest apartment complex in the US) when it went broke. Blackstone and other partners took a haircut from 5Billion they paid to 3.2Billion. Thing was, the place was fully occupied and they still couldn’t cash flow it. The weird part is that they applied the security deposit and last months rent to current rent because it represented a liability for the new owners. I am sure it bummed the property managers to have no leverage over the renters when they left.

Whatever happened to HUD (Housing and Urban Development). The Secretary of HUD is a Presidential cabinet post that must be sitting around the conference table in the Oval Office, surely all the Presidents must recognize the person they nominated. Since they are confirmed by the Senate, maybe a couple of Senators would think of them from time to time. All of these housing issues for years and not a cricket out of that or any other societal cabinet post; i.e., education, etc.

All these cabinet positions are good for nothing for public.

These positions are good for these individual and their friends

Don’t expect anything good from these cabinet position holders

Google reviews of those complexes are enlightening. Seems like current mgmt is skimping on a lot of maintenance.

They’re being sued by contractors over nonpayment of $1.6 million in invoices.

it seems when they stopped making mortgage payments, they just collected rents but stopped paying for stuff, and stopped pretty much everything, and let the lender clean up the mess.

This stuff is really tough on tenants.

Good point.

The everyday people are caught up in this passion play, the collapse of at least four bubbles, simultaneously, leading to a bleak future or an opportunity for renewal.

Is the rescue of the ultra-rich still a national priority

In checking the location of the Houston apartments, they are in kinda crappy parts of town. Back in the late 70’s some were pretty good locations. But now, not so much. These look like a hard sell in 2023.

Thank you for your accurate presentation of the factual data, Which allows the rest of us to take liberties with the facts in the course of argument.

I would like to assert several hypothesis that are related to the referral of the CRE as a market.

1) It is a market that is not consistent, in the sense that the bad investments are a tragedy and should be rescued by the guys collecting their own dog’s poop.

Wolf said: “Arbor Realty took the $32.5 million loss on the loan so far, plus foreclosure expenses. According to Bisnow, it continues to be the lender for Fundamental Partners. So it’s still on the hook for what’s left of the loan.”

———————————————-

Trouble following this.

Arbor foreclosed and had to accept a $32.5 million dollar loss. Arbor should be out of the deal. They are done.

Fundamental bought the property. Typically at a foreclosure it is cash on the barrel-head.

There is no hook left. Arbor got filleted. No?

Fundamental bought the property from Arbor with money it borrowed from Arbor. They had a deal. Fundamental: “I’ll buy it from you if you’ll give me the money to buy it from you.”

Does it pass the smell test? No one cares these days… It makes stockholders happy — rather than having an even bigger loss. That’s all that matters.

Arbor may lose more money on it in the future when Fundamental defaults.

Heckonomics.

Debt funds have grown dramatically over the last 12 years and I think the approach Arbor took to provide seller financing makes sense given the current financing market, expect to see more of this. What the article doesn’t say is what percentage of the net received was cash versus the new loan. A 100% loan would be unusual. These debt funds, which are almost all floating rate debt, are where a lot of the early CRE stress is likely to take place. They have been very active in both “value add” and construction lending.

Huh. Tricky.

I believe that sort of this used to be called “Extend and Pretend”.

What fees will banks collect packaging up more dog crap and selling to investors who are/will be sitting on massive MTM losses?

No worries, “The Real Estate Roundtable” has already started crying wolf (no pun intended) to Bank Regulators and Senate for debt restructuring plan similar to Section 4013 of the CARES Act…

LOL

Commercial and multi family… How long before we see VRBO hit with similar issues? I’ve read articles that say demand is up but many owners aren’t getting their homes booked. How long do these VRBO owners hold on?

As long as they can pay their monthly but. They don’t need many rentals to do this, because the prices that they are charging are nuts.

Semi-true depending on the market. If you look at number of hotel rooms required to replace the rental and then add in 30-125 per meal for couples (let alone with kids) the prices don’t seem so absurd, hence the continued demand. The seemingly larger issue is that demand is falling in all areas (hotel and owner rentals). Again, not necessarily equally depending on the location and draw.

More examples of how, “the free money virus turned investor’s brains to mush,” lol. I know a few investors who bragged about getting involved with one of the groups here, saying their strategy was so smart. I mean, what could go wrong in a multifamily property, in a low interest rate, high priced environment?

On a small scale, I have found one cannot only focus cash requirements on acquiring a rental property, but there are ongoing cash requirements once the property is acquired. There are usually updates and repairs required before bringing the rental property online. There will be down time without rental income which needs to be considered and planned for and ongoing maintenance once the property is producing income. All of these things require a certain amount of cash reserve and planning. I imagine some of these same considerations should exist when large scale rental property is acquired. Sometimes it appears these considerations are not part of the plan.

MFs only make sense when bought right, in a downturn. Buying them at the peak with floating rates…OMG. It’s called an alligator, negative cash flow, it’ll eat you alive.

I didn’t understand the “considering the state of rentals in SF”. Down? by much? Consider me crazy but I always had the fantasy of renting an old, wood smelling apt on Nob Hill, a walk up maybe, with a view, unrenovated, for a few months, walking around the streets, shopping in the little Chinese grocery stores, how romantic. Young again.

Bob Lee , Hamid Moghadam a couple of billionaires mugged in SF. Curious is Wolf experiencing any increases of symptoms of society breakdown in SF. I have a genuine trust in the average person and tend to be very Leary of press and negative news in society when focused on crime. Events happen and there is an element of society that does not respect basic human interaction and with concentrated populations in big cities these events happen and become news. With the population of rich increasing especially in SF over the last decade the incident rate increases . So go rent your romantic inexpensive SF apartment and enjoy the summer. Rent may be cheap.

BS ini

Your braindead idiotic BS about SF is hilarious by now. An assault or homicide only makes it into the national headlines if it has “San Francisco” in it. Tulsa has 2-3 TIMES the homicide rate of San Francisco, and no one outside of Tulsa ever writes about it. It only goes viral if it has San Francisco in it. I mention Tulsa because it’s the other city where I lived for long time.

San Francisco by the numbers of homicides is one of the safest big cities in the US. But reality isn’t material for your right-winger fantasies. Pleasure yourself with them at home, not here.

The City of Tulsa had 68 homicides in 2022 and 78 in 2021. The city is HALF the size of San Francisco.

The City of San Francisco had 56 homicides in 2022 and also in 2021.

City of Tulsa homicide rate per 100,000 pop: in 2022 = 16.5 and in 2021 = 18.9.

City of San Francisco homicide rate per 100,000 pop: in 2022 = 6.8 and in 2021 = 6.8.

Data from the San Francisco Police Department and from the Tulsa Police Department. Here are the SFPD reports:

https://www.sanfranciscopolice.org/stay-safe/crime-data/crime-reports

In addition, most of the homicides occur in three relatively small pockets. If you don’t go into these small pockets, homicides are very rare.

No one ever sends links around about assaults in Tulsa, or murders in Tulsa though has three times the homicide rate of San Francisco, but it’s a right-winger city in a right-winger state, run by right-wingers.

It’s just when you can stick “San Francisco” into the headline that it goes viral among braindead idiots. This clickbait bullshit really gets old.

Tulsa has this high crime rate even though people rarely walk around on the street. I have no idea why Tulsa is so unsafe. It always baffled me. In San Francisco, there are lots of people out on the sidewalk and in parks. And we love it! We walk everywhere at night when we go out.

Your statement falls right into this moron fantasy category. Normally I delete this BS because I won’t allow a bunch of morons to abuse my site to spread this BS, but I just left it up to whack you over the head with data.

It’s like poor Durham, North Carolina around here. It is way down on the list of murders per capita in North Carolina: I see it listed at 12.6 per 100k. Which is something like #10 in the State. But it is surrounded by some of the safest urban areas on the East Coast, with one of them being the State Capital with the media apparatus that goes along with being the State Capital.

Thanks, Wolf for your diligence in limiting disinformation. I did not realize you were actively do this. This is the only site of its type I use because the articles are based in fact and help me (in my small world) to get a better perspective of the “big picture”. The comment section also serves to give me more and better perspective and some of the comments can be as illuminating as the associated article. I had foolishly assumed the lack of “non-facts” at this site were due to the members it attracted… (I suppose that’s wishful thinking, these days) Well, thanks, Wolf. Your efforts make a difference.

To support Wolf’s contention that Tulsa has a high crime rate, all you have to do is to turn on the show “First 48” on A & E. They has 10 eposodes from Tulsa showing what appears to be a war zone in Tulsa.

Beeing a stranger to the USA I do find your comments about society in the big US cities somewhat amusing. Traveling the world I did maybe not find USA to be the safest place, but there where rural areas more scetchy than the big cities.

As Wolf show, SF is not of the dangerous places when it comes to crime. Anyway, beeing run down by a drunk, or just distracted driver poses a far higher risk anyway.

cresus,

“I didn’t understand the “considering the state of rentals in SF”.”

SF lost about 60,000 people (8%) over the past few years [though it’s still amazingly crowded], even as something like 8,000 new housing units were completed and came on the market, and vacancy rates on rentals are big. Asking rents are down quite a bit from the peak of 2019. The older neighborhoods are apparently doing OK, the problem is the new apartment and condo towers that were largely vacated by tech people during working from home. A lot of these condos are on the rental market.

off topic

In March, hundreds of budding entrepreneurs descended on Noida, a suburb of India’s capital Delhi, to attend a three-day convention that had dubbed itself the “world’s biggest funding festival”.

Short promo videos featured popular influencers such as Ankur Warikoo, Prafull Billore, Raj Shamani and best-selling author Chetan Bhagat. The publicity material said that 1,500 venture capitalists, 9,000 angel investors and 75,000 start-ups were expected to participate. It was billed as a platform to meet potential customers, network and pitch directly to investors.

Mr Chauhan, co-founder of the bike servicing and repair app Apna Mechanic, spent 20,000 rupees ($244.4, £196.3) to buy tickets for himself and four colleagues.

They arrived with a presentation for potential investors. Their excitement, however, didn’t last long.

“Hours went by and we barely saw any investors,” he told the BBC.

Bherav Jain, founder of the start-up Reproc, had travelled thousands of kilometres from the southern Indian state of Tamil Nadu.

“The crowd was full of start-up founders,” Mr Jain said. “I don’t think there was a single person [there] who was an investor.”

By 1.30pm, a scheduled virtual address by Mr Gadkari had been cancelled and a rumble of discontent was spreading among participants.

Many began gathering around the stage, demanding an explanation.

“People started asking questions about where the investors were,” Mr Chauhan says. “And it [soon] became chaotic because the founders didn’t have answers.”

By the end of the day, a group of 19 entrepreneurs – including Mr Chauhan and Mr Jain – had filed a police complaint, accusing the organisers of cheating and breach of trust.

it was trust?

Cheap money is going away now gradually. Hence, this is normal as investors no more have to chase yield in start ups/ ipos.

I heard in 2021, people would present on table napkin their ideas and would immediately get few million dollar of funding.

As WR say, cheap money makes peoples brain go mushy

Why on Earth would reasonably competent adults go with Variable Rate mortgages when FIXED interest rates were the lowest that we will ever see in our lifetimes? It is not like the Fed didn’t telegraph what it wanted to do with the first round of QT before COVID.

Greed?

They were expecting negative interest I suppose.

I touched on the same thing in my comment below. I can’t recall if I’ve ever seen any commercial loan officer ever mention a 30 year fixed. It’s always a fixed period ARM. Seems to be the norm in the CRE scene.

Some mysteries are beyond our understanding.

Wolf

These CRE loans are typically, as you stated, variable with a fixed-period of usually 5 years but as low as 2.

They can also hit the interest rate adjustment cap on the first adjustment, as you also showed in the Appleway example. Well, you didn’t say it directly but it was pretty clear to see. Maybe commercial ARM’s don’t even have caps?

In addition, I think most of these loans have prepayment penalties as well that align with the loans fixed period. Like a 5-4-3-2-1 structure on a 5 year fixed period ARM.

If someone, like me, with limited knowledge on CRE knows this, then how are these “investors” being so short sighted? They have to be dialed into the markets, FED nonsense, etc and penciling this into their ROI and cash flow scenarios, right? Seems like the answer is wrong? What am I missing here?

Meanwhile, taking into consideration your data, Goldman maintaining a buy rating on CBRE, and the appearance of CBRE tapping support 5 times (on the daily) within the last 12 months is a little telling, to me.

With CBRE set to report on 4/27, all this info may be saying $55 is on its way with $40 to follow?

Thoughts anyone?

Sorry Wolf. You never stated that ARM are typically used to finance commercial property. I twisted my thoughts there

I live in Spain and the practice here is mostly adjustable rate mortgages. My British expat friends say it is even worse in the UK. Here the banks actually hide that they have fixed rate mortgages available and Liam officers do everything they can to discourage buyers from even asking anything about getting a fixed rate. Could the same type of thing have happened in CRE in the US?

In looking at the “Construction Starts” chart, though the recent increase is notable, we are in the average range of 40-50 years ago when the US population was 30% lower than today. Simple math would say we should be 30% higher ?

I am gathering from the rest of the article that those MF projects built 40-50 years ago are either getting bulldozed or foreclozed – the Houston “projects” being exemplars ?

If that is the case, this debt flushing is the needed enema. If a project started 40 years ago with a $100M note, and got foreclosed 40 years later with a $500M note, WTF were the owners doing to make the project “ROI positive” for 40 years beyond debt loading ?

“…when the US population was 30% lower than today.”

No, it’s not the population per se, but population GROWTH requires new housing units to be added. Population growth has slowed, compared to the 1980s. In 2020, growth was almost 0%.