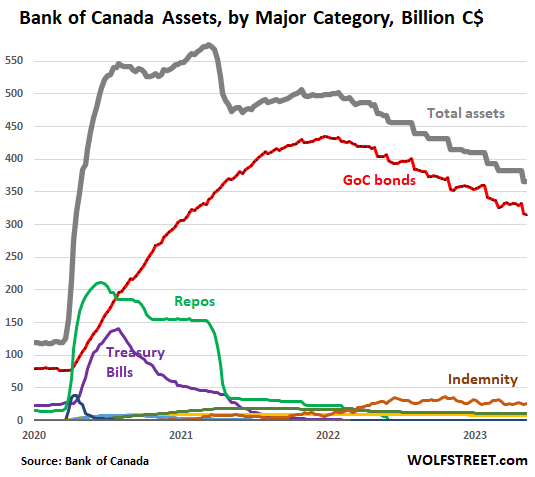

It unwound 46% of all assets it had added during the pandemic. Far more aggressive QT than the Fed’s.

By Wolf Richter for WOLF STREET.

The Bank of Canada, which has paused its rate hikes for the second meeting in a row at 4.5%, isn’t pausing at all its Quantitative Tightening. Au contraire. It seems to follow the policy of faster QT instead of rate hikes.

Total assets on the balance sheet today fell to C$365 billion, down by C$210 billion, or by 36%, from the peak in March 2021 (C$575 billion).

During its crazed QE starting in March 2020 through March 2021, it piled on an additional C$455 billion in assets. It has now shed 46% of these pandemic QE assets. Nearly half!

Largest holdings and percent change from peak:

- Government of Canada (GoC) bonds: C$315 billion; -27% (red)

- Repos, once its second largest holdings: zero; -100% (green)

- Short-term Treasury bills, once its third-largest holdings: zero; -100% (purple)

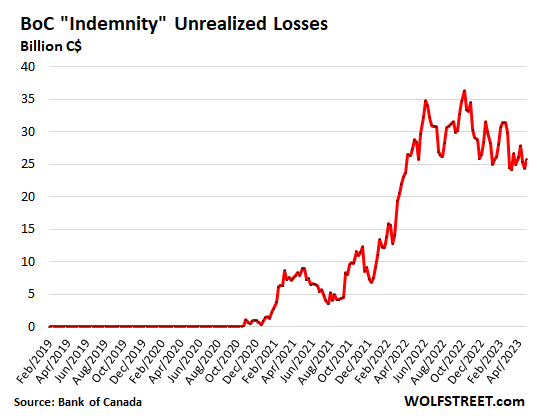

- “Indemnity”: unrealized losses on its bond holdings: C$26 billion; -29% (brown)

- Mortgage-backed securities: C$8 billion; -16% (yellow)

- Provincial bonds: C$11 billion; -40% (olive)

- Real return bonds (inflation protected government bonds): C$4 billion, -18%.

QT started unofficially in March 2021.

The BoC’s Quantitative Tightening (QT) unofficially started in March 2021, when its assets peaked at C$575, and began to decline, though the BoC denied at the time that it was QT.

That month, the BoC announced that it would unwind its “liquidity facilities” – Its repos and what remained of its Treasury bills – citing “moral hazard” as reason. So it started to exit its repos, which began reducing its overall assets. It was still buying GoC bonds, but at a slower pace than other stuff was rolling off, which is how the overall balance sheet began to decline.

Short-term Treasury bills had already been rolling off since the summer of 2020, and continued to roll off until they were gone.

The BoC never bought a lot of mortgage-backed securities to begin with, and ended the practice in November 2020 when it held C$10 billion. They’re now down to C$8 billion.

The BoC bought provincial bonds starting in May 2020. Its holdings peaked at C$19 billion in May 2021 and then started to decline. Today, they’re down to C$11 billion.

Unlimited roll-off of GoC bonds.

In October 2021, after its balance sheet had already dropped by 13% from the peak in March 2021, the BoC stopped increasing its holdings of GoC bonds, and a few months later started letting them roll off whenever they matured, without cap – meaning that it lets roll off whatever matures. So the roll-off varies widely from period to period.

The Fed was concerned that unlimited roll-off would spook the markets during months when a big pile of bonds would mature. But that doesn’t seem to be a problem in Canada; markets can deal with it just fine. And it allows those GoC bonds to roll off much faster (-27% from peak), compared to the Fed’s holdings of Treasury securities (-9.5% from peak).

“Indemnity”: unrealized losses.

Unrealized losses on the BoC’s securities holdings are tracked in the account, “Indemnity” (brown line in the chart above). This is the estimated value of the indemnity agreements between the federal government and the BoC and represents the unrealized losses on the bond holdings, if the BoC sold them today at market prices.

Those unrealized losses are a result of higher interest rates that have caused market prices of bonds to drop. Those losses will automatically reverse, no matter what interest rates do, as the bonds get closer to their maturity date because at maturity date the holder gets paid face value.

The BoC and the government have a deal that requires the government to reimburse (indemnify) the BoC for those losses on the GoC bonds, if the BoC actually sells those bonds and thereby realizes the losses. But if the BoC holds them to maturity, it will get paid face value, and those losses vanish.

The BoC’s unrealized losses on its GoC bond holdings began rising when the BoC started unwinding its balance sheet in 2021 and bond market yields started going up. “Indemnity” peaked in October 2022 and has since then dropped 29% to C$25.7 billion.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Fed never worries about “spooking the markets” when it’s slashing interest rates. Besides, the Wall Street types are paid the big bucks to be spooked from time to time. In any event, if the Fed doesn’t step up the pace of QT, most Americans are going to be suffering from inflation for a long time.

Indeed and same people calling FED to pivot and “stop” killing economy, never once questioned the QE madness and inflation that it would create.

Really? Actually, often the opposite. Jeremy Siegel flagged the inflationary risk before most and was very vocal. He dismissed the notion of transitory and called for a more hawkish stance well before the Fed acknowledged any issues.

It was obvious to the same group that there was a massive, speculative bubble. But as facts change, intelligent people also adjust their positions.

If Siegel thought the Fed made a mistake by stoking inflation, why isn’t he calling for a period of deflation to reverse that inflation?

According to Perma bulls like Siegel, apparently it’s OK for inflation to run above target, not OK to meet the target.

Siegel is the biggest crybaby of them all, a shameless pumper talking his book. Yes, he cares nothing about inflation.

Fed is not doing QT to save the 99% from inflation. It wants to protect the wealth of 1% at the expense of 99%, and that requires inflating away the debt of 1%, or bluntly transferring it to taxpayers through bailouts via “Special Purpose Vehicles” aka “not QE”.

Everything owned by 1% is “too big to fail”, and so without any bankruptcies, where debt is written off, only method is to inflate away the debt. We should get ready for years of high inflation!

The worst to suffer will be the older people. Their assets and savings will lose value and they cannot work to get inflated salaries.

Leo

To your point…

the big boys got hurt with FTX….and the politicians lined their pockets with “donations”.

Keep a close on this …(if you can find out anything)….and see how this plays out.

Leo,

Last time I checked the system works thus…….

1) Unencumbered socialism for the wealthy (any time they are at risk of losing anything they are made whole with OUR tax dollars)

2) Rugged individual capitalism for the masses (bunch of losers should have known better, suck it up buttercup and pay your damn debts or we will ruin you)

+1

Currently old people are golden:

1) being the primary holders of inflated assets which they can liquidate at historical overvaluations

2) getting inflation COLA adjustments to their SS income

3) still getting full SS income / Medicare benefits even though the system is broken with mathematical certainty and kick the can is the current political solution to it.

Since the system is entirely destined to fail within the next 20 years. compare that with a 40 year old:

1) if lucky they bought a home but likely at a hugely inflated price level and likely to liquidate in their 60s at a depressed level.

2) got to beg their employer for inflation adjustment of their salary

3) their retirement income is going to be 0-50% of the current if adjusted for inflation

Social security is so broken we will see the introduction of something like means testing or just achieve the same through adjustments of the tax code. So most screwed will be middle class retiring in 20 years who did everything right: Sizeable 401k/IRA to prepare for the bad times. They very likely will see their social security income cut to 0%.

I would be careful here. I agree with you 100% that Medicare is broken and unfixable as it is currently structured. On the other hand, Social Security is fixable with minor tweaks, still providing a lifetime cash flow in retirement until the day you die. In some sense, the current Boomer population is just a pig in the python that will roll off soon enough when the Boomers start dying off in mass. I agree that the Boomers create a stressful blip, but it is just a blip.

I hope Wolf keeps the link below, so you can run the numbers and see for yourself, a 1.6% payroll tax increase (0.8% employee portion) would solve the vast majority of the problem, costing someone making $30K/yr in salary only $240/yr in additional taxes to fix ($20/month):

https://www.crfb.org/socialsecurityreformer/

The amount that came into SS in 2022 was just a tiny bit smaller than the amount that was paid out. The gap was much less than expected, likely because of the excess mortality of SS recipients during covid. I will do my 2023 fiscal year update in October, and I kind of expect a small surplus:

And here is the trust fund level:

https://wolfstreet.com/2022/11/08/status-of-the-social-security-trust-fund-income-and-outgo-fiscal-2022/

Thanks Wolf, for keeping the link. FYI, here are the tweaks other than the 1.6% payroll tax increase needed to fund SS in perpetuity:

* Calculate benefits based on highest 38 work years

* Tighten SSDI eligibility criteria

* Raise full retirement age from 67 to 68

* Index COLA to chained CPI

* Slow benefit growth for top 20% of earners (no means test)

JeffD,

I can go along with some of the proposals But…

“Index COLA to chained CPI”– is an insidious way to impoverish the oldest people. Every year they will lose a little bit of purchasing power, but its cumulative, and after 20 years, when they’re in their 80s, they starve. I rail against it every time anyone brings it up. It’s a nasty shitty deceptive thing, and anyone that proposes it needs to go to jail for attempted elder abuse.

Medicare definitely has issues, but that has more to do with the U.S. broken healthcare system than it does anything else.

As for Social Security, many years ago I pushed a solution that would have saved SS for decades: removing the cap on income that pays into SS.

Unfortunately it was never implemented and SS finances have deteriorated since then so this fix will no longer save SS. However, removing the income cap would still go a long way to shoring up SS. More is still needed, but that would be a great start and no serious proposal should be without it.

Unfortunately it is hard to have a serious discussion about SS because of two reasons, for one any suggested modifications to SS are demonized and are an automatic no go (3rd rail of politics). For two, there is the other extreme, so many people demonize SS as a ponzi scheme and literally seem like they want it to fail. They have been predicting its failure for decades. It is impossible to have any rational discussion when these extreme voices drown it out.

The opposite is true the people on persons will prosper more than anyone. My income more than doubled when interest rates rose. Workers may see a 5 or 6 percent wage increase but I saw over a 100 percent increase in my yearly income.

Why does the M2 money supply go up still in Canada?

M2 doesn’t tell you anything. Waste of time to look at it. Nowadays, it’s a fashionable thing to throw into the conversation, oh look M2! And it gets tossed around everywhere, it’s falling the US, it’s doing this over there, and it’s doing that under here… Just forget it. It doesn’t tell you anything.

Care to explain why M2 doesn’t matter anymore?

Why should it matter? It’s a weird incomplete measurement, it doesn’t predict anything, it doesn’t explain anything that we don’t already know.

Wolf…

Question:

In your opinion, Which money supply metric does matter?

The only part of money supply that I’m worried about is central-bank-created money, and you can see that on central bank balance sheets as a result of QE, and that money-creation indicator is now declining due to QT.

That’s why I spend so much time here looking at central bank balance sheets because they DO matter and they DO tell us what’s going on.

The secondary effects of that decline due to QT are now pulling down M2 in the US just a tiny bit, just like M2 was hugely inflated during QE.

In Canada, the other effects that are picked up by M2 are bigger and M2 ticked up. But so what?

It’s a good thing these central-bank balance sheets are coming down — not a bad thing. The time to worry was when they were going UP. Now that they’re coming down, that problem is more or less slowly getting whittled down.

I read a whole article about this.

It said “Monetarists” we’re discredited in the 1970s and it is out of favor.

I believe “Goodhart’s Law” in 1975 was one of the reasons.

Monetarism may or may not make a comeback as it correctly predicted the most recent bout of inflation.

Ask a real economist for a better answer.

WaterDog,

What correctly predicted the current bout of inflation were the gigantic increases in central-bank balance sheets, repression of interest rates, and huge government deficit spending directly into the economy, starting in March 2020. This was everywhere. And 8-10 months later, inflation took off.

We tracked this stuff right here from day one, started screaming about inflation in late 2020 and early 2021.

Wolf I wasn’t trying to bag on you. I obviously greatly enjoy your articles.

I was trying to point out that Monetarism was greatly discredited in the mid 1970s.

Some articles are again featuring Monetarists due to inflation.

The fact that they correctly predicted inflation doesn’t mean they are correct. If an Astrologer predicted inflation does that mean they are correct? or just lucky?

However, for right or wrong Monetarism is popping up. I saw a M2 article in my Business News feed just today ;O

You and Powell agree that M2 is not a good indicator.

You look at the balance sheet, and its growth during 2020 and 2021 and see the burgeoning numbers indicating money supply growth.

Yet Powell who dismisses M2 also dismissed what we all saw in that balance sheet….massive monetary expansion. He apparently didnt regard either as a forward indicator.

Was Powell ignorant of the ramifications of an expanding monetary base and no increase in goods and services?

So why were the central bankers surprised at the inflation?

There are a lot of things a Fed head can NEVER admit. That’s just how it is.

Thank you for that comment. I just looked at m2. I have no idea why it started accelerating again in the last couple months. This seems really weird to me considering interest rates. Who’s taking out all these high interest loans, generating the M2? I do see house sales way up again the last month or two.

The QE program has no direct impact on the real economy, but it does generate a wealth effect that creates artificial wealth and influences people to spend what they don’t really have. Thus, it’s a temporary shot in the arm, which comes at the expense of future growth.

If QE is not completely reversed, however, it permanently increases the wealth of current asset holders at the expense of future generations. A legitimate central bank will not attempt to transfer wealth from one generation to another. Kudos to the Bank of Canada for reversing out its QE before more long-term damage is done to future generations, as well as societal trust.

QE accomplishes no legitimate purpose and should never should have been done in the first place by any central bank.

Its a morphine for governments, so they don’t have to worry about underlying cause of pain and actually treat it.

I partially agree: QE (and ultra-low interest rates and thereby, ultra low interest rates or rates of return to investors caused by the “Fed,” which occurred through money creation, enabled overuse of leverage, bankrupted pensions by reducing their earnings for years (which will ultimately need bailouts), bankrupted local, US governments (e.g., in part due to their pension debts), etc. It did have a real effect on the economy and created the inflation that the ultrarich have so loved for years: it is reducing their banks’ and companies’ US dollar liabilities in real terms by over a TRILLION dollars, PER YEAR OF their WUNDERBAR INFLATION. That is just considering merely the liabilities owed to depositors by the ultrarich’s US banks.

It is the height of irony that a certain country’s repeat of their prior, great mistake (HUGE, MANY mistakes, actually), will cause a worldwide recession soon that will tame most inflation. I predict that.

Unfortunately its not working as 5 year mortgage rates continue to fall and bidding wars are back everywhere in the housing market. The cost of living in Canada will mean most immigrants emigrating there will leave pronto but they tell you inflation is virtually non-existent in Canada. Quantitative tightening is supposed to drive long term interest rates higher but the opposite seems to be happening in Canada. The minimum wage in Canada will have to double or all the working poor will leave the country for better opportunities elsewhere.

Bobber

“QE accomplishes no legitimate purpose and should never should have been done in the first place by any central bank.”

Agree.

Some people actually save their money to “enter” into asset classes….but the Fed kept that door shut by a constant feed of new money. Just over a year ago they were pumping $120 Billion a month into the markets)

Central bankers do not allow normal business cycles to occur….cycles that FLUSH the poorly leveraged and the inefficient. This is healthy for economies and markets.

But QE was Bernanke’s baby and it won him the Nobel for Economics. Maybe there should be a “Kick the Can” Nobel prize….for we are currently feeling the ill effects of his policies .

I could actually see a purpose in temporary QE during the period when COVID hit. But there should be a firm commitment that the balances will be eliminated at the end of any crisis and not remain a permanent part of a central bank balance sheet.

Once Treasury starts to issue bonds again to bring the Treasury balance back up we are going to see the real impact of reductions in the balance sheet. And we will see that financial markets can not maintain their current levels if the Fed balances were sold off.

This balance is structural, unless they are willing to see all asset prices fall dramatically.

This may be off topic but with MBS being non-existent and rates ‘high’ relatively speaking, any commentary on why housing prices are still heading to the moon? Seems counter intuitive in theory but I guess Canadians can stomach 5% mortgages? I’m a canuck btw.

To the moon? LOL

For example:

Wolf sorry for the stupid question but can you tell what you call in US MBS to what extent is on the ECB balance sheet. I also mean the ECB, is it in favor of buying such huge amounts as the Fed or is it close to the BOC soon?

Is the ECB getting rid of these MBS?

This linked article goes into the ECB’s balance sheet. I posted it over two months ago, so the balance sheet has dropped a lot more since then. But it shows the two biggest categories separately: loans and bonds. The bonds are mostly government bonds and corporate bonds. But there are also relatively small portions of “covered bonds” which are mortgage bonds, some asset backed securities (ABS), and other stuff in small quantities:

https://wolfstreet.com/2023/03/07/ecbs-balance-sheet-drops-by-e1-trillion-from-peak-qt-milestone/

Thanks Wolf!

So wages have halved in each of those graphs in ten years.

And tax brackets haven’t moved anywhere near enough.

My labor is worth next to nothing in Canada versus ten years ago. I’m paid more but can own far less.

Adrian,

I can answer that one. Canada’s banks of which only the big six matter (there is no competition between banks in Canada) decided to extend amortization periods for mortgage loans instead of letting any default. The number of mortgages with amortizations beyond 35 years was zero last year and now is over 25 percent of all Canadian mortgages. This has fully avoided any forced sales glut on the markets and prevented any real correction of Canada’s housing bubble. Blame OSFI for allowing this and FCAC for encouraging banks to do this.

Blame the banks for taking advantage of desperate people with negative amortizations. But the banks will not care. Better to target the regulators.

Correct. Price discovery is illegal in Canada.

I assume that this applies only to those who have already received a loan and not to those who wish to receive one. Despite this measure, sales in Canada collapsed and prices fell

Ah that’s interesting to hear. As I’ve mentioned before, real rates are still negative and the effect of high nominal rates + high inflation is that it front loads the mortgage payments. But you can compensate for this with a longer term. Sounds like the banks are now actively pushing this. A 35 year term vs a 25 year might be ok if we have lots more inflation, as those extra 10 years of payments could be tiny vs wages (obv depends on how the exact numbers work out).

I guess we’re in new territory as to whether inflation can come down without having to push real rates positive. It seems that the more people figure out this ‘hack’ the more markets could pick up again. What a mess.

The other policy that Canada uses to pump up the housing bubble is immigration policies. Bring in enough people who need housing and you prop up the bubble.

I dont understand why Canadian youth are not more pissed off.

From personal experience I will say that

1. 90 percent of immigrants to Canada are poor people. The rich 10 percent go directly to Toronto and Vancouver

2. 50 percent of immigrants leave Canada within the first 5 years

3. Most immigrants are families, that is, the number of housing they need is not proportional to the number of people.(1 family =1 house)

4. in order to withdraw a loan for the first installment, they must have a permanent job and prove income. Most of these people work minimum wage or hourly.

So it’s not immigrants that are inflating the property bubble, it’s BoC money printing that’s already history

Yes indeed (I’m Canadian); projections of population growth that way exceed the capacity to build housing – growing demand raising prices.

Roughly 25% of all current mortgages (VRMs) had the ammoritizations extended just in the last 8 to 10 months – foreclosures and forced sales avoided and listings are way down.

Obviously, excessive and inane speculative bidding by buyers.

Where I live in Markham, Ontario rents will soon overtake Toronto as the city with the highest rents. As long as home prices go higher so do rents and in Markham no one asks questions about the price they just pay whatever the builder asks even if it starts at several million dollars for a starter townhouse with no basement and no backyard.

Do you think part of these rate pauses through language, slowing hikes, or stopping hikes, are because federal reserves want to sell their balance sheets at favorable levels before causing asset price depreciation through hikes?

Central banks don’t care about profits and losses. They create money, and they destroy money, every day routinely, and so profit and loss and capital don’t matter to them.

WOLF

If central banks do not care about profit and loss, then why is GOC (aka taxpayers) “indemnifying” BOC for losses on future bond sales? BOC is Canada’s central bank…right ?

The government is not paying the BoC for those unrealized losses unless it ever actually sells any of the bonds and takes actual losses. If it doesn’t sell but holds to maturity, nothing happens. It has no intention of ever selling those bonds. They’re rolling off just fine without selling them.

The Fed is set up in a similar way, via its remittances to the Treasury Dept. that it stopped making when it lost money.

These are largely accounting issues. How do you account for this stuff? Central banks don’t have a cash account (instead they create and destroy money every time they pay for something or get paid for something). Central-bank accounting is in a class of its own because they create their own money.

I was talking to a colleague today, who lives in Canada (west coast metro), he/she mentioned that last year his/her neighbor house was getting bids of 200k over asking but that is all gone now, no bidding wars, no over asking offers.

But lot of young people are getting hired right of college and are demanding and still getting paid salaries that was not imaginable 2 years ago. And in 6 months these new hires are asking 50k increases or they will leave for other employers who are offering that much more.

I was told the reason why (private sector) employers are paying this much is because the public sector is loaded with lot of money and they are spending (on systems upgrade, new systems etc) like no tomorrow.

anecdotal…

Interesting link between public/buying, private/selling supporting tech prices. The govt gave a lot of covid $$ to itself.

Owning a bank is good, owning a central bank best.

If that’s true their fed and fed government is more intelligent than US by a factor of 10

Nah, income levels in Canada are still pretty stagnant overall and besides nowhere close to supporting RE prices.

A recession is brewing there too and will hit later this year, particularly as the US decline will hit Canada squarely. This will be the catalyst to dislodge house price expectations. Hard to change the trend there with three factors a) speculator psychology that is entrenched culturally and supported by 20 years of unabated gains and b) sky high immigration and c) rampant money laundering.

> 50k more

That’s not far off the median wage in Quebec.

Reality: it’s a Ponzi scheme.

Real wages aren’t propping this up.

For starters if you’re on a decent wage in Canada, which you’d have to be to get a 50k wage, you’d see a little over half of that increase after taxes.

Here’s how you get rich in Canada.

1 start by earning your capital outside our high tax zone

2 move your capital in and leverage up on housing located near services Canadians paid high taxes for

3 enjoy not paying capital gains on your primary residence

4 leverage up even more as immigration rates are up

5 switch your primary residence

6 enjoy more tax free capital gains

7. Leave Canada if you can.

Thank-you for doing Canadian content Wolf. It is appreciated by your readers Up North.

So if QT is souking up extra liquidity, how does it translate to less lending and higher interest rate on mortgages? So far, there has been little sign cooling appetite for mortgages and prices.

“little sign cooling appetite for mortgages and prices.”

Sales volume has dropped sharply. And in terms of prices, they’re all down year-over-year and down sharply from the peak, see above charts for Toronto, Vancouver, and Vitoria.

Because Trudeau is letting in way more immigrants to put even more pressure on housing.

That’s how Canada prints.

Can confirm that endless waves of immigrants are still bidding up the price of houses and apartments in Vancouver. Thanks to Trudeau.

Probably backed by shady housing lenders that come with the lot. I have seen mortgage rate 0.05 point above BoC rates. Going down the drain in a blink of an eye.

The banks are taking a bit of a hit and lowering mortgage rates to drive home prices skyward. So far this has worked as mortgage rate have come down almost 3/4 of a percent for 5 year mortgages. The banks have lowered GIC rates but long term corporate bond yields are almost at an all time high for the last 15 years. The feeble public doesn’t know the correlation between long term bonds and 5 year mortgages they just see mortgage rates falling so now its bidding wars everywhere in Canada.

Powell sucks at his job lol

All policy decisions including the only 3 interest rate they set at the Federal Reserve are made by the FOMC (Federal Open Market Committee) by CONSENSUS of its 12 members and not by the single person Jerome Powell who is merely the Chairman of the FOMC.

The Fed sets 5 policy rates. Wolf details each of them after each Fed meeting.

Yes, thank you for pointing that out. Here they are. At the last meeting, the FOMC hiked:

1 – Federal funds rate target to a range between 5.0% and 5.25%.

2 – Interest it pays the banks on reserves to 5.15%.

3 – Interest it charges on overnight Repos to 5.25%.

4 – Interest it pays on overnight Reverse Repos (RRPs) to 5.05%.

5 – Primary credit rate to 5.25% (what banks pay to borrow at the “Discount Window”).

https://wolfstreet.com/2023/05/03/fed-hikes-by-25-basis-points-to-5-25-top-of-range-says-the-extent-to-which-additional-policy-firming-may-be-appropriate-instead-of-pause-qt-continues/

The Federal Reserve only explicitly sets 3 rates, one of which is merely advisory and in a rate range, namely the Federal Funds Rate:

1) Federal Funds Rate which is merely advisory and applies to interbank borrowing and is set in a 0.25% rate range.

2) Federal Discount Rate which applies to banks borrowing directly from the Federal Reserve at a rate .050% above the Federal Funds Rate and which carries a negative stigma.

3) IOER (Interest On Excess Reserves) which is the interest the Federal Reserve pays on Excess Reserves on deposit inside the Federal Reserve to banks with funds in those accounts which is presently more than $3 trillion.

Nope, read my comment above.

Of the five rates, if “sets” four rates in absolute terms, and it sets a target range for one rate (federal funds rate).

Wow, it’s fun to see such a large balance sheet drop not leading to a real recession.

Would it be fair to say that QT is not going to reduce the velocity of money as much as interest rates? But only make the wealthy less wealthy?

Lol read the headlines.

Canada is in a “Technical Recession.”

Real one on the way???

WaterDog,

Canada is NOT in a “technical recession” or any recession. A technical recession would be two quarters in a row of declines. So far, there hasn’t even been a single quarter of declines. Q3 GDP: +0.6%; Q4 GDP: 0%; Q1 has not been released yet. Even if Q1 is negative, it would only be one quarter that is negative, and you’d need the next quarter (Q2) to be negative as well to get a technical recession.

What the headlines are saying is that Canada MAY ENTER a technical recession in the future, based on estimates by economists. They have been saying that since last fall, and it hasn’t happened yet.

While we may not be in a technical recession yet. We seem to have entered a recession per capita. The last two quarters of 2022 showed a per capita gdp falling by -0.2% in Q3 and -0.9% in Q4. However, this recession is still hard to see on day to day basis because of the very high number of new comers.

Wolf and tooshort are right. I was wrong.

They were projecting Q1 as negative and listed “The last two quarters of 2022 showed a per capita gdp falling by -0.2% in Q3 and -0.9% in Q4.” like tooshort said.

Good day Wolf. It’s been noted that Canada is in a “gdp per capita” recession.

Q3 2022: -0.2%

Q4 2022: -0.9%

With another contraction expected for Q1 2023. (Source: better dwelling). With higher immigration/ population growth and public spending February’s gdp report I believe was +0.1% but negative on a per capita basis.

According to GDP per capita, Japan has long had one of the best performing economies among developed nations. Canada added lots of immigrants, which increases the population, but it doesn’t slow the economy.

It is remarkable that BoC Actually is doing something right for a change. Might other countries learn from Canada?

The ECB leads for now with its QT of minus €1.12 trillion, although it lags behind on interest rates

Come live here and see the reality on the ground. Working doesn’t work.

We still need to see fear increase in the real estate market. There is so much money on the sidelines that stocks and housing have a long way to go before investors are worried. They’re too well capitalized at the moment.

On a side note, I know over ten millionaires under 27 due to the real estate bubble. They’re all full of themselves and think they’re geniuses. Until these people start feeling pain we are not near taming inflation.

paper millionaires? paper wealth is not real until it is realized. There were countless of these empire of houses holders in 2007 from investors to everyday joes. When the market turned and renters vanished from job losses, most ran out of money trying to pay their mortgages and went bankrupt.

Nothing is worth anything until you sell it and bank the proceeds. Unrealized gains are vapor. Anyone who feels *rich* because they have equity in their housing is a dope if they tap it. No one in their right mind should put their shelter in jeopardy. Most people overestimate the value of their house (they forget things like seller’s fees, required repairs, things like termite tenting required in CA, etc.,) that all eat away at that “wealth” they think they have when they go to dispose of it. Think 10% of the gross value that could potentially go away before you walk away with a penny of the net equity remaining.

We bought a home from such a person in 2010. The knucklehead took a HELOC to give his wife her dream kitchen, redo bathrooms (which both required extensive plumbing and electrical work for code updates), did hardscaping in the yard with gardens far exceeding that appropriate for the neighborhood, and we can’t forget the hardwood floors throughout and the updated high end windows and hardwood custom millwork. Then he bought a boat and a motorhome to tow it with. And it all flushed right down the toilet when his job evaporated. I bought it for half of what he had in it. The motorhome was re-popped as was the boat and one car. He left with whatever would fit in the one remaining midsize beater with a “turtle top” along with his wife, daughter, and mutt – which means, not much.

So much for his “wealth” effect.

Your “over 10 millionaires under 27” are too young to remember the last downturn or to have been stung by it as they were still watching cartoons at the time. I remember my peers, who were purportedly 401K geniuses, that got chopped in half and have yet to recover from it because they were universally monkey hammered on all fronts (credit card debt, loss of home equity, collapse in equities, and some ended up splitting what little they had left in divorce and child support).

Old sayings, such as “don’t count your chickens before they hatch”, are still relevant in today’s connected world.

I agree with everything you say, but without being scalded, one cannot learn to protect oneself. Everything in its time, one learns while living

A lot of them have been flipping houses so they’re in and out. A lot of them are agents who have been doing absurd numbers over the last couple years. Most of the flippers have been doing 100-200k profit per house here in my Midwest city.

Ultimately, this real estate market has minted countless millionaires who have been smart enough to sell and sit on the sidelines.

I agree that paper millionaires will soon lose their short lived status.

Dave Ramsey has an interesting story of how he was a millionaire on paper in his 20s, all due to real estate. He went bankrupt soon after that. Guess he learned his lesson.

He learned don’t buy real estate at a peak. Buy low sell high. The Fed is teaching a new lesson to fools who listen – buy unprecedented high, sell higher. The correct name of the lesson – “greed, fomo, momentum and discernment, how to

fail at being wise”.

*Much more aggressive QT than Fed’s.*

It makes sense because the real estate bubble in Canada is much bigger than the one in the US. Also, the Canadian bubble has been inflating since 2005 without correcting while the US bubble underwent a major correction in the period 2007 – 2013

Earlier it was said that M2 (which I don’t understand much about) is meaningless.

Insofar as Canada’s central bank does NOT do MBS (or so little that it is trivial), is it fair to say the Fed’s gorging and super slow bleed off of MBS has little to do with elevated housing prices ??

If MBS was such a big factor, one would presume the US housing bubble would outsize Canada’s. It is in fact the opposite.

Is central bank hoarding of MBS a red herring in these real estate bubbles and in fact it’s mostly interest rate repression and good old-fashioned FOMO?

What Is M2?

M2 is the U.S. Federal Reserve’s estimate of the total money supply including all of the cash people have on hand plus all of the money deposited in checking accounts, savings accounts, and other short-term saving vehicles such as certificates of deposit (CDs). Retirement account balances and time deposits above $100,000 are omitted from M2.

The Federal Reserve tracks a separate money supply number, called M1, that includes currency that is in people’s pockets or in their checking accounts and savings accounts. The money that is deposited in time deposits and money market funds is not counted in M1. For the Fed’s purposes, this is “near money.” That is, the funds cannot be used as a medium of exchange and they are not instantly convertible to cash.

Makes sense in terms of reversion to normal economics. 5% rate is historically normal, and no free counterfeit is historically normal. Higher rates can help to stop inflation, but the real source of the current inflation is the endless counterfeit, not ZIRP.

“The BoC never bought a lot of mortgage-backed securities to begin with, and ended the practice in November 2020 when it held C$10 billion. They’re now down to C$8 billion.”

In stark contrast to the Fed.

Now, why would one central bank delve head over heals into MBSs, while another central bank decides not to? Why was the Fed pushed into buying MBSs? A very costly move.

Housing costs are out of control in Canada. This article makes it sound like the Fed are doing a worse job than the BoC.

Most Canadian kids are screwed.

Trudeau has taken one action post pandr: to further increase immigration above the known build rate.

Would you rather have some lines on a chart lower or actual reality where your kids will never own a home? If it’s the latter then send them on up for some 50% marginal rates, no doctors and very expensive supermarkets.

For decades the Fed stayed out of long paper…

now they own around $5 Trillion in MBSs and govt issue ten years and out.

They push their “dual mandate”, but both elements are current and real time…so why the departure from past avoidance of long paper…a HUGE departure and policy move that is reaping dire consequences?

The Fed currently holds about $2.6 trillion of MBS as part of its roughly $8 trillion securities portfolio.

So Cal…

“The Fed currently holds about $2.6 trillion of MBS ”

and?

They own about $2.5 Trillion in Treasuries with maturities 10yrs or longer….which is what I said.

“they own around $5 Trillion in MBSs and govt issue ten years and out.”

1) Canadian banks no longer borrow at 3M @4.5% and lend at 10Y @2.9%. Their short duration shifted to the right, towards the middle. Demand for the 2Y and the 3Y is high. The 10Y is flat for one year at about 3%.

The middle is caving in.

2) The Canadian financial sector is the leading sector, larger than energy. The top five Canadian banks are hanging on. They are not falling apart like their counterpart in US, despite the housing and commercial RE problems.

3) In 2022 inflation was 6.8%.

4) We don’t know if BoC raided “other” people banks accounts, without their knowledge or permission, to support the gov in 2020/21, to create the RE bubble.

I didn’t understand your point #4 in terms of raiding.

> The BoC and the government have a deal that requires the government to reimburse (indemnify) the BoC for those losses on the GoC bonds, if the BoC actually sells those bonds and thereby realizes the losses. But if the BoC holds them to maturity, it will get paid face value, and those losses vanish.

Do you think any of this actually adds up, Wolf?

My savings and wages are worth far, far less now than five years ago. I paid for the losses, along with other working Canadians. Our wealth was transferred to people in debt and to those who own housing.

Canada is a nightmare. Taxes are very high. Food inflation is lied about.

The BoC steal from regular Canadians daily.

Let’s not lose sight of reality because the BoC and the Canadian government agreed to lie about some entries in a table on a sheet of paper.

Do not think that this inflation is only in Canada and that it is worst there. On the contrary, inflation is everywhere in the world and for each person it is the worst in his country. As seen in the graphs above, Canadian home prices are falling and deals have collapsed. This will continue for a long time.

Inflation in Canada is worse across the board.

Housing inflation is in particular far, far worse than the USA.

Here in Eastern Europe, inflation is 14 to 20 percent officially, unofficially 30 percent. For housing, they ask for as much in the USA and Canada, even more, given that our standard of living is twice as low as yours.

And you know one thing that makes for better countries, unlike Eastern Europe?

I’m not going to accept our high inflation as reasonable just because some guy in eastern Europe tells me it’s worse there.

Canada can do far better and until it does I will continue to call it out, whether you tell me we can’t or not.

*I will continue to call it out*

georgist

You know, we have a common problem. It is that we are both calling for the same thing, but there is a wisdom that says that the dog barks and the caravan moves. What I am trying to tell you is that you should not take it personally and think that you are the only sufferer in the world. The big problem is that, unfortunately, nothing depends on you and me.

Sooner or later the coin will turn, and it’s not because of the central bank or the government or because of you and me, it’s just because life always does. Nothing lasts forever. It requires patience. And whether Canada could do better than the Czech Republic, for example, is a matter of another conversation. I say this because I have lived in both places and have a basis for comparison.

Zero wisdom in that reply.

The BoC did create this problem, along with our government.

It’s not magic.

1) Consumers spending is down. First they bought a 1M/5M

house, painted it, fixed the roof, built a fence, bought a dishwasher,

a new fridge, new washing machine, a dryer…

2) The 60K car is a step down, only 5% of a house.

3) Dentist, outpatient surgeries are a must.

4) Flying instead of hiking.

5) The de-accelerating cont. From the millions –> to the hundreds of thousands –> through the thousands –> to the crumbs.

Mr Engel your wisdom that you posses from your decades of experience is a welcomed comment and I appreciate your remarks. Thanks for contributing and best regards.

One of the interesting points is that many people do buy a new car shortly after the purchase of a house. We used to use the real estate closing data to direct market to those folks. You’d think that, after plunking down a bazillion dollars to buy a house, the last thing they’d do would be to buy a car. But, nope. The didn’t like how the old clunker looked in the garage of their new manse.

Interesting you say that. The new subdivision I stay at for work is full of new vehicles. Mostly trucks. I thought it seemed odd.

The Bank of Canada balance sheet would almost be a rounding error for the Fed’s. Of course their economy is much smaller than the US, but to their credit (no pun intended), BOC never went into the stratosphere like the US on their balance sheet.

Still, the rapid drop by the BOC of their balance sheet is quite revealing.

Most of the countries that matter in the world are getting their fiscal house in order in preparation/anticipation of the drop in US dollar hegemony. Countries are once again going to have to show fiscal prudence if they want to play ball. Simply being pals with the US isn’t going to cut it.

Britain know this all too well which is why they are almost rabid in their views and actions against Russia. The US unfortunately, is also in for a very big surprise in the coming years as much of our “wealth” is going to slowly (at first) and then suddenly evaporate.

House Prices in many markets in the USA are actually now moving back UP! In my market, existing inventory remains incredibly low, and avail houses sell very fast. I am surprised. When the FED started slowing their rate hikes, the 30 year fixed dropped out of the 7s and down into the high 5s and 6 percent range. People starting snapping up the homes again. The QT in the US has been anemic and where are those MBS sales? LOL! The FED as well as federal and state governments wit their 40 year loan mods, forbearance, on and on will not allow meaningful price (and property tax) deflation. What a joke.

People confuse the seasonal spring selling season when prices always go up with change in direction of the market. In the US, that also happened during Housing Bust 1. It was very confusing.

Home prices were back to peak levels 10 years after housing bust one. Do you suspect that will happen again?

Wolf – I understand the “seasonal” spring bump up in prices. However, we just went from 3% 30 yr rates, to now in the 6% range and homes in my area have been getting snapped up fast. Home buyers are still buying with and sellers are not selling. Inventory is extremely low and I do not see this changing anytime soon. This is more than a “seasonal” tick up. I really thought we would see the price decline continue, but it is definitely not happening here.

I can no longer handle things like “snapped up fast” when sales have plunged 25% to 40% year-over-year. I’m so tired of this stuff.

Days on the market have shot up — they DOUBLED in California. Active listings are 30% to 70% HIGER than a year ago. Other metrics have shown the same trend.

I’ll just stick to the data. You seem to be in Sacramento, so here is the seasonally adjusted median price. It’s down 6.5% from the peak last July. And year-over-year, it’s down 5.6% (not seasonally adjusted):

Thanks WOLF! – I totally agree sales transactions are way down. But I think part of this is because there are barely any homes for sale, and of course higher rates, etc. And yes, active listings are higher, but new listings have crashed much lower well below 2022 levels. Also saying active listings are higher is still a joke here as we are coming off record lows. So we are still way down, just not record way down? Prices went up in this market 35-50% in the last few years. So yes I agree they are down in price say in the 5-6% range or whatever, but this is pathetic and amazing given the run up in prices, current rates, etc. Recently prices here have bumped back higher!…seasonal they say?…we will see. As a buyer we are truly shocked at how people are paying these huge prices for houses still as of now. The resiliency in this market is breathtaking and shocking. The FED clearly is not serious about bringing inflation, house, prices, etc., down meaningfully. The CPI is a joke. Real life inflation is probably 10%, and the FED hems & haws with rates at 5% and likely a pause around the corner, no mbs, sales, bailing out banks…oy vey. Not to mention federal and state governments are bolstering house prices and property taxes with free $, mortgage forbearance, giving people with lower credit better rates/lower fees, 0% CA down payment program, 40-year fha loan mods/refis, LOL… whats next?

Typical Powell…..

I’am going to issue one gazillion dollars…..per week.

oh……time to tighten…..OK…..I’ll take back two million a month…..oh wait……should it be one…….oh……..well…..maybe we’ll just keep doing two and be tough. Inflation appears to be out of control…..oh well……those 3.7% 30 year rates don’t seem to be doing it…….let’s give it a decade or two to see if it all slows down.

In the meantime…..let them eat cake.

Extend the loans into over 35 years and allow negative amortization are two very risky moves. Beyond raising the duration of the assets at a time when the cost of deposits is rising, it risks lowering the quality of the bank’s books, thus lowering its liquidity and raising any discouts or haircuts in case a sale of such assets is needed.

This is denial. If the inflation entrenches, rates go highter or stay highter for longer, people start to demand better rates for their money or the housing markets get another leg lower and people start to default, staregically or not, Canada will get a hell of a banking crisis…

Fed screwed up by encouraging whole world to leverage up from about 1X to about 4X GDP. It was all great til inflation broke out and rates had to rise. Any one or any institution that had a model based on Zirp is going to implode from most leveraged to least leveraged until enough damage is done.

Will be interesting the choices democracies make whether to recognize bad debt or play games and extend and pretend. We have grown debt faster than GDP for so long that theoretical r* rate is basically 0% real rate. If we don’t stop expanding debt faster than GDP then r* will be a negative real number.

Argentina is a good example of one end game where official inflation rate is much lower than what is really going on (100% annual rate). People are now saving in dollars and transacting in black markets instead of using local national currency because savings rate in local currency is highly negative.

I don’t think Argentina takes its cues from the Fed.

In Canada and the US, the results of central bank monetary intervention have been devastating to younger generations. Home prices have risen beyond what a young person can ever hope to pay. Returns on retirement savings will be pitiful, based on the constant efforts of central banks to prevent popping of the stock market bubble. People buying into these markets will be lucky to squeeze out a 1% real return. Medical and education costs are skyrocketing due to rampant inflation. It’s to bad, many younger folk have lost hope of being able to support children and a family.

It’s debatable whether this is attributable to hubris combined with incompetence or a willful attempt to concentrate wealth. In any case, the results are clear. Wealth concentration and moral hazards are at record levels. Trust in government and institutions is lost.

Equally surprising is how younger generations have folded in the face of this repression. The propaganda machines have successfully channeled emotions to FOMO and lottery behavior, which prevents any organized thinking and political resistance. If minority constituents don’t make their voices heard, they take what they get.

good points. Its coming to upheaval. I submit even now, whoever wins the next election, half the country will not accept it to the point of new higher levels of civil unrest.