“Once crisis tools have served their purpose, central banks should scale them back.”

By Wolf Richter for WOLF STREET.

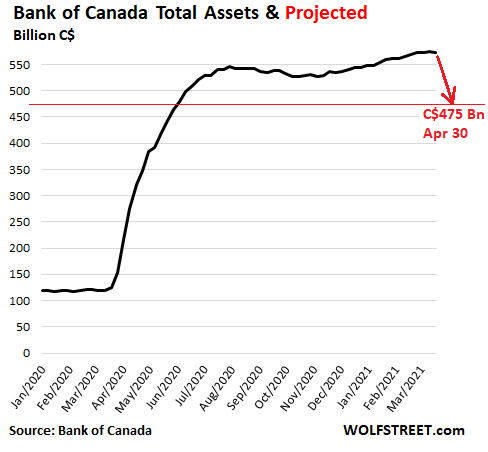

The Bank of Canada will unwind its crisis liquidity facilities, will further reduce its purchases of Government of Canada bonds, which it already started tapering in October, will let short-term assets “roll off” the balance sheet when they mature, and will as a result reduce its total assets from C$575 billion now to $C475 billion by the end of April, announced Bank of Canada Deputy Governor Toni Gravelle in a speech today.

Most of the speech was focused on the reasons for the QE and liquidity programs that the Bank of Canada unleashed starting in mid-March last year, in a two-fold role: In its role as “lender of last resort,” to deal with the “extreme stress” in the markets, as liquidity dried up and markets weren’t functioning or had “seized completely” as everyone was trying to sell everything in a mad “dash for cash.” And in its role as provider of stimulus as the economy that was spiraling down.

But these actions ballooned the balance sheet fourfold, to C$575 billion, and it created the possibility of “moral hazard.”

“Moral hazard emerges whenever market participants or other economic actors feel that they can engage in risky behavior without bearing consequences if things go wrong,” Gravelle said, a year after moral hazard became forever the guiding principle of the markets.

But moral hazard can be limited “by ensuring that such actions have a predetermined expiry date or are unwound when they’re no longer needed,” he said.

“Once crisis tools have served their purpose, central banks should scale them back to show that they are emergency measures and don’t reflect business as usual,” he said.

“When central banks provide liquidity, we have to do so in ways that don’t encourage market participants to take undue risks in normal times. Our actions must be targeted at specific issues and scaled back as those are resolved,” he said.

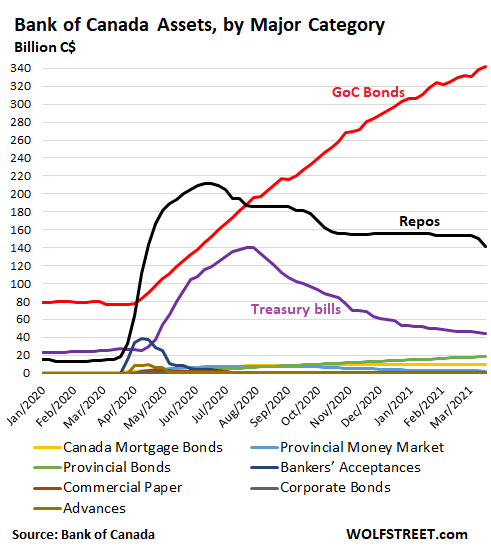

Since last fall, the Bank of Canada already ended it program for bankers’ acceptances, tightened the conditions for its repo program, stopped adding to its mortgage-backed securities, and slowed adding to its Government securities (but also shifted from short-term to longer-term maturities to provide the same stimulus for less money).

This chart shows the major liquidity and QE programs, and how they have fared. Several of them are already at zero or near zero. Two major ones, repos and Treasury bills, have been in decline for months. The biggie is still growing, the GoC bond program (red):

Ending and unwinding the liquidity programs.

“In the coming weeks, the Bank will suspend or discontinue our remaining market liquidity-focused crisis programs,” Gravelle said.

And the Bank of Canada announced today that it will let these programs expire on their originally announced expiration dates, but it “currently” doesn’t plan on selling the securities:

- Commercial Paper Purchase Program, on April 2

- Provincial Bond Purchase Program, on May 7

- Corporate Bond Purchase Program, on May 26

In addition:

- Term Repo operations (currently bi-weekly) will be suspended indefinitely on May 10

- Contingent Term Repo Facility will be deactivated on April 6.

As these programs end, short-term securities will mature and roll off the balance sheet (as the Bank of Canada gets it money back).

About C$120 billion in securities are expected to mature and roll off the balance sheet without replacement between mid-March and the end of April. Given the other movements on the balance sheet, the net effect is that total assets on the balance sheet would drop by C$100 billion, or by 17%, from C$575 billion currently, to about $475 billion by the end of April, which would be the lowest since May 2020:

Further tapering the purchases of Government securities.

Last October, the Bank of Canada reduced the purchases of GoC bonds to C$4 billion a week, but shifted to longer maturities to provide the same overall stimulus with fewer purchases.

Now the BoC is opening the door to further tapering of the purchases: It will continue to increases its holdings but at a slower pace going forward. “We would be easing our foot off the accelerator, not hitting the brakes,” Gravelle said.

Without naming dates, he said the BoC would be “gradually dialing back” the purchases of GoC bonds down to where the purchases merely replace maturing securities, and the balance of GoC bonds remains “largely stable.” At that point, the proceeds from maturing securities would be reinvested in new securities to maintain the balance at that level. This would be the end of QE.

“The process for getting there will be gradual and in measured steps,” he said.

And rate hikes? When the economy and inflation are on target, as outlined in its forward guidance, “we will need to start raising our policy rate,” he said.

And he added, “we will be mindful of the possibility that our stimulative monetary policy – while essential to achieving our inflation objective – could increase financial vulnerabilities.”

Which is ironic, this sudden mindfulness, because it’s obviously way too late because the policies have already created the biggest housing bubble and mortgage bubble Canada has ever seen, and it has seen bigger housing bubbles and mortgage bubbles than most countries. But hey, even in Canada, these bubbles might not last forever.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If anyone thinks JPOW will follow suit, think again. NY times just published an opinion piece praising Jerome Powell for his bailouts. The title? “The Years of Work Behind Washington’s Best-Liked Man.”

I know Depth Charge will love it :)

JPOW has already shut down, put on ice, or unwound all crisis “tools,” except MBS and Treasuries.

True;short-term assets “roll off” will shrink CB balance sheet , but the corresponding liquidity already created in the banking circle will remain hence “Moral Hazard” too.

“except MBS and Treasuries”

___________________________________________________

Is that not sufficient distortion for you?

Powell continues the FED practices of creating funny money, favoring wealthy asset owners at the expense of the working class, and suppressing interest rates.

Exactly

I agree “Powell continue creating funny money”. While W is technically correct, Powell is till in Eternal ZIRP mode, and is increasing QE by hundreds of billions/month (might have changed a bit).

That’s full steam ahead. And because both employment and inflation figures are nonsense, he’s got lots of wiggle room forever.

On a side note, Bank of Canada’s words don’t look un-similar to the Fed’s Hawkish Gradualism. Different words, same idea.

We all know how that worked out.

Powell has plenty of wiggle room to suppress interest rates, inflate the money supply, and practice theft from the working class and common savers.

He has no wiggle room to practice decency and support stable prices, sound money and honesty towards Americans AT LARGE. The FED, along with the FED tools of Greenspan, Bernanke, Yellen and Powell gave up that pursuit long ago, if it was ever there at all.

cb,

“Is that not sufficient distortion for you?”

For me??? I wasn’t talking about me. I was replying to a question, and pointing at the Fed’s recent putting on ice or shutting down entirely a whole range of much ballyhooed bailout and prop-up programs, such as buying corporate bonds and CMBS and letting the SLR exclusion expire. Nothing to do with me.

@ Wolf –

Sorry.

Let us never lose sight that the FED are a bunch of larcenous, market distorters that work against the AT LARGE good of the American people. I know that your vision is good.

You forgot the most important and market distorting “tool” – near zero interest rates. Shut that one down and the world comes crashing down with it.

Michael McKee had a couple of great questions for JPOW a week ago, which Powell basically danced around. He asked if a Japan situation of low rates and low inflation was possible in the US…and he followed up with calling Powell out on previously saying rates were too low to now saying they will be low until these moving targets are met. The response from Powell was along the line of we don’t see any bubbles in debt or housing so this policy is appropriate until maximum employment.

So, the message from the Fed is we will do what we want as long as we want to do it. And we will pick and choose the metrics and research that fit our policy decisions and we will only share those metrics after the decisions have been made. So, in a way, it’s party on boys.

“we don’t see any bubbles in debt or housing”

__________________________________

Liars “see” what they want to see …..

The driving bubble is in dollar creation. That drives all the other bubbles. Inflation is a monetary phenomenon. Prices are a symptom.

We all know that inflation is all ready at least 2% so the Fed is lying that they need to print to hit 2%.

We all know that for someone to work they must need money. Why are we paying people not to work through September when I see so many help wanted signs?

Tom S.

Isnt it remarkable that an unelected official can unilaterally decide to expand M2 by 27% in less that a year? (digital minting)

Isnt it remarkable that an unelected official can impose a tax (inflation) ?

The Constitution reserves both those powers to Congress. Article I, sect 8…..mining and taxation.

Sadly the politicians enjoy the condition, the borrowing to fund their vote gathering initiatives.

Feds real tool is forward guidance. The unemployment benchmark (Fed history as tragedy – Bernanke – then as farce – Powell) was walked back by Yellen yesterday who said (SUDDENLY) the economy is growing faster than we thought, and we might meet those (elusive) full employment goals sooner. Full employment for Wall St (JP) and for prudent govt policy are two different things, and phonecalls were made.

The FED’s real tool is creating money from nothing.

We had 3.5% unemployment which is below what was once considered FULL employment.

Did the Fed back off their QE? Nope.

Now the Fed is fighting the markets…fighting reality.

Question for Powell:

How can you expect people to buy 5 yr notes with a .57 yield when you promote an inflation rate 2% higher than that yield?

Wolf – With all due respect, your comment was like saying “Jeffrey Dahmer has been mostly shut down because he’s not eating people anymore, except he’s still killing and dismembering them.”

Of course the establishment media, and Washington politicians and lobbyists like Powell. They are all in the same pocket.

I hate to sound like a recording but remember that Forbes Magazine reported that 15 billionaires own most US media, so they control what is covered. If you count social media, it might be a slightly higher number of billionaires who have the power to censor. See “The New Censorship” in US news and world report.

I know some relatives of friends in the news business and they have told me that some things are not to be covered or said in their stories. This is just like what the CCP does in Chinese state media but instead of being sent to a concentration camp or prison, the reporter would just get fired or demoted or laid off and never hired again.

That is just the tacit or softly spoken censorship. See “It’s not just Trump: US media freedom fraying at the edges” in indexoncensorship as to other methods of censoring reporters and even photographers. I support higher taxes on the wealthy not just because of the US’s financial troubles but because we have to end the gigantic fortunes (and thereby oligarchy of the ultra rich), which amount to trillions of dollars more than all ordinary Americans are worth if their measly wealth were put together. See “The Spider’s Web: Britain’s Second Empire.”

You are right.

The biggest threat to freedom and free markets, is concentrated wealth and power.

This is not “New” censorship. The media have always been owned and directed by the people with money. 100 years ago “yellow journalism” was the term used, and William Randolph Hearst was directing government policy, ruining careers, and basically doing whatever he liked. And this hasn’t changed, and it won’t change as long as the politicians are bought and sold.

The problem is that with the changes in media it’s even harder for “the people” to force change. You can’t burn a printing press and stop the paper any more.

We have problems:

a debt problem – The corruption of debt that has diminished housing security and turned many to debt slaves, to the benefit of the counterfeiters at the FED and banks

a concentrated wealth and power problem – caused by financialization and money creation/counterfeiting along with corporatism/big government which has led to a rentier society and an asset distribution problem (no assets for you, you wageslave/debtslave/life long renter!)

an incentive to work problem – the above and the accompanying bailouts, misplaced stimulus, misplaced welfare (including government and corporate “workfare”), and pending MMT are putting a damper on a willingness to exchange honest labor, physical of mental, for compensation

@cb: Remember that “your” debt is “their” wealth (credit).

To avoid being owned by the rich, stay out of debt.

Step 2: Every time you buy products or services from the monopolists, you feed them profits. Don’t feed the monopolists!

Editorializing via omission. An old game.

There are those who completely believe that if it is not on CNN, MSNBC or NYT it didnt happen….and COULD NOT HAVE HAPPENED!

Yeah, I liken Powell to the parent who gives his bratty teenage kids everything they want and lets them do whatever they want.

You might be considered the “cool” parent at the time, but your kids will grow up to be completely useless.

I liken him to the booster parent who pushes his kid to the front of the line by bribing coaches, prestigious school admission councilors, lawyers and judges when his kid is in trouble, calling in favors for job appointments, etc. ,,,,,,,,,,,,,,,, then brags to the world about how exceptional his kid is.

(Hmm. why are thoughts of Romney, Bush Jr, and other “winners” floating through my mind)

cb, you forgot to mention the Kennedy family members….LOL

Oh, yeah, love it, Zain. Thanks. :)

Hahah hahah, BoC is worried about moral hazard.

The biggest purveyors of moral hazard are central banks keeping interest rates below inflation rates for decades now, punishing unsuspecting savers by diluting their savings to help asset holders and debt-beats no matter what. Those guys have zero credibility, what a joke.

“BoC is worried about moral hazard”

This is an oxymoron.

More of a non-sequitur.

Canada’s CB holdings are approx $500B? That’s approx 7% the size of the US (not accounting for currency valuation differences). Is the US economy REALLY 14X the size of Canada’s ?

Relatedly, it is encouraging to see Canada’s CB announce true taper intentions. I guess we will see if they can pull it off.

No, only 11x larger.

Hmmm…that actually tracks pretty closely to where our off the rails train is at since Canada is approx 10% of the US population. Looks like their “debt per person” is about the same.

Most of Canada’s population lives close to the US border. Some Canadians own vacation property in Florida or Arizona.

The Canada debt per capita is approx 50% of the US ratio. This is according to Statista.

The debt to GDP is 136% for US and 89.7% for Canada. This stat taken from World Population Review site of which Canada did not even make the top 10 list.

The US is 8.7 X as large per population.

Headline for Victoria BC news report just yesterday:

‘It’s a cut-throat market’: Greater Victoria single-family homes selling for way over asking. Victoria is very very expensive. Single family homes are at least 2X higher than anywhere else on the Island.

I don’t think sales are as robust in Vancouver or Toronto these days, but on Vancouver Island RE is scary. From what I can see people are bailing and moving to the Island for climate and lifestyle. The other day I mentioned that a friend’s property just went up for sale about 2 weeks ago. I see the listing disappeared so I assume a cash buyer magically appeared. (I haven’t snooped yet). We live in a rural valley off Johnstone Strait, 1 hour drive west of Campbell River for those still map minded. :-)

I was at our community vaccination clinic just yesterday (Pfizer) and was approached to do some building for a new buyer while lined up. This was at a community mass vaccination site. The only construction I have done here is for myself as I retired 10 years ago and worked away before that. That’s how busy it is these days, and down Island it is even busier. Everyone knows the rates are going up. My sister in law is doing a quick refi before the rates climb, crunching the numbers and paying the penalty.

regards

The Bank of Canada bought C$450 billion in 2020. The Fed bought $3 trillion. In that respect, the BoC was a lot more aggressive than the Fed.

Unlike the Fed, the BoC came into this crisis with a relatively small book as any QE they did in the 2007-2009 period rolled off a long time ago. The BoC has not been doing much QE between crises. As you can see, they can let the current aggressiveness roll off over the next few years without the kind of taper tantrums that the Fed would incur. Helps to be smaller and less followed.

Last I looked Canada’s household debt was about 50% worse per capita than US probably because of mortgage debt. I think a lot of countries are running at 300% plus if you combine household, corporate and government but in different mixes.

If you don’t borrow, big government is going to borrow on your behalf to kick the can a little further.

It looks like the Bank of Canada will be “a lot more aggressive” in exiting the QE than the FED as well. 20% in two months??? It took our Fed two YEARS to reduce its balance sheet by 20% the last time they tried.

Yes, but the BoC is unwinding its liquidity programs in two months. That’s where the drop comes from.

The QE program is being “tapered,” but not reversed yet. What the Fed did in late 2017 through mid-2019 was reverse its QE program. That’s a lot trickier.

They sound like Powell did when he started to raise rates. Of course, he was shoved back into the corner pretty quickly by Wall Street.

Central bankers have no conviction, no spine. They claim to be financial surgeons, yet they faint at the first sign of blood.

yup. well said.

no reason to expect anything different going forward but the same trend of spend, print, crisis &c.. &c.. whatever tightening they do is a just a blip on the overall wazoo chart.

The problem is they are trying to create demand, but so much of it is going into asset bubbles. I wondered in 2009 how the Fed would ever gracefully land the plane without destroying the golden goose. Doesn’t look like they can. Print fly or don’t print crash. Keep it in the air as long as you can.

Pretty immoral to give stimulus checks to people in prison, homeless drug addicts and illegal aliens, but not to engineers, doctors and plumbers.

They expect people to buy ten year notes at 1.6% while they promote an inflation rate (2-2.5%) that rips 22 to 28% off the dollar in ten years.

1.6% for ten years, compounded, would give you a 17% return.

It just doesnt make sense. What the Fed has created and tries to sell us doesnt make sense. It is a fake world.

In retrospect, Fed Hawkish Gradualism was always Hawkish Hypocrisy

#EndtheFed now.

I want a comfy front row seat and a big carton of buttered hot popcorn when this charade blows up in Fed head’s face.

Hubris and arrogance have another name: Jerome Powell.

The FED and central banks around the world can’t fathom allowing asset prices to find their market clearing price. A hint of house price deflation and they come in with the printing press. Heaven forbid those sitting pretty on their couches have to concern themselves with the “value” of their stucco sh!tbox. But the millions of people living on the asphalt in tents at best, with not a penny or asset to their name, you ask? “F**k ’em if they can’t take a joke,” says Powell.

I’m surprised that the BofC is doing this and wouldn’t be surprised if it doesn’t follow through or change course on their schedule. Likely a big BofC show given the state of our economy. We are way behind the rest of the world in vaccines (we are actually worse than Europe if you can belief that) and thus way behind opening up. Our economy is not healthy, totally dependent on handouts, and our private sector got whacked big time. Our support payments were generous to workers, many of whom earn more at home than working-so good luck getting them back to work-might be riots if they turn that spigot off. Of course, there were no government sector layoffs through all this, if they couldn’t go to work or work from home, and many couldn’t or wouldn’t, then they stayed at home (most are still at home) and did nothing on full salaries. The provincial bond buying (a Province is the equivalent of a State) program was essentially enacted to keep a couple of Provinces from going bankrupt-now that would have spooked International Markets. Our government spending is out of control at all levels, local, provincial and federal, and honestly I can’t see how they ever rein it in…assuming they even want to (the MMT-Guaranteed Annual Income idea is popular up here….especially when the real economy is so weak, with no real sign of opening. Our only real ray of hope is the US opening up, since we sell so many goods into the US. Oh yeah, the there is our main support: debt and money printing….as long as everyone thinks the Canuck Buck is Good…..So, good speech, great plan….but as as Mike Tyson says, “Everyone has a plan until they get punched in the face”, and I think we are for a pummelling up here…we are just making look good before we go in the ring

Augusto, where do you get this stuff? It is illegal for all local Govt to operate in deficit in Canada. This includes cities, municipalities, and regional districts.

My taxes are going up 1.7% this year. (Strathcona Regional District). Campbell River is going up 1.9%.

Long term local and city debt has to be financed, with payments being counted as operations expenses. An example of this might be a transit line, like Skytrain in YVR. Airports and airport operations are upgraded and operated with user fees and a ticket surcharge as they are privatised.

A common financing approach with large capital projects is the 1/3rd share. Fed money 1/3, province 1/3, etc.

Our economy in BC is actually doing quite well, except for the Covid hospitality nightmare. However, we will be vaccinated well before summer. The vaccine rollout was affected by Pfizer stopping their contracted deliveries for 1 month while they upgraded their factories. Meanwhile, the rollouts have been adjusted forward. I was just vaccinated yesterday and I am 65. In our community/area of 1200 people it was for all ages 18 and above. In the city south of here they are working with folks in the latter 70s this week, with all care homes and health workers long done. Teachers, grocery store workers, fire and police etc are slated for April, Province wide.

The structure of BC economy is very weak. It is mainly supported by flow of legal and illegal Asian money into real estate. Add related sectors (i.e. residential construction, mortgage finance) and it ends up being a huge chunk of the province economy. Very accommodative BoC Policy allowed Canadian to over-leverage themselves to compete against foreign buyers.

Except from real estate, Vancouver and Victoria are public sector towns with some relatively low pay tech jobs. The rest of the province is dependent on a declining lumber industry ( that however got a COVID boost) and tourism. Mining might be the only promising sector for BC interior.

sounds like failed government and manipulative banker

Failed governance combined with bankers is a sure road to the ruin of a people.

Funny money debt is evil. Cast out the counterfeiters.

“The structure of BC economy is very weak. It is mainly supported by flow of legal and illegal Asian money into real estate.”

That is true for most major cities in Canada.

A public affairs program sent some investigative journalists disguised, with hidden camera, as home buyers with deep pockets. During the meeting with the RE agent, the journalist tells the agent with no uncertain terms that the money comes from illegal drug business and asks if that would pose a problem. The agent didn’t flinch; quite the opposite in fact, he answered back that he doesn’t care where the money was from and that he’s heard this before and knows exactly what to do (or not do). Similar scenarios occurred with many agents the journalists met.

That program also showed people caught on security camera entering casinos with duffelbags full of cash (presumedly dirty money to be laundered). The laundered money would then find its way to the RE market.

Reply to intosh:

True to some extent, but Vancouver is by far the worst case.

Toronto (auto industry) and Montreal (aerospace) still have some manufacturing and are home to some large national headquarters.

Calgary and Edmonton have what remain of the oil and plastic industry + agro-food businesses.

Ottawa is a government town with some tech.

Vancouver…almost nothing significant. Even Winnipeg has more productive businesses.

Crazy to thing it is more expensive to live in Vancouver than Seattle when you look at the main city employers

Seattle: Amazon, Microsoft, Costco, Boeing

Vancouver: Telus (former crown corp.), Jim Pattison group (grocery), Lululemon.

Paulo said:

“It is illegal for all local Govt to operate in deficit in Canada”

“Long term local and city debt has to be financed”

__________________________________________________

If it’s illegal to operate in deficit why would any financing be required?

cb,

US states operate on the same principle, including your home state. So why do they have to borrow? The fig leaf is “capital expenditures” and other one-time expenditures. Their operating budget is supposed to balance. But for these one-time projects, they can borrow to fund them, in theory. Obviously, there are massive games being played with this everywhere.

Yes Wolf, It’s the camels nose under the tent.

Not true, municipalities just run deficits in other areas under other ways. The most common municipal trick is to short the employee pension plan (unfunded liabilities), essentially deferring payment obligations to spend on other things. You still recognize the obligation, but thats all it is an obligation, it doesn’t have to be “financed”, until required for payment. Essentially you go from long term funding program to a form of “pay as you go”, and since actual cash shortfalls in pension payments are years away, well that’s someone else’s problem. I understand this is a big problem in the US as well….in fact I think its worse….

@ Augusto –

That’s what a lack of jail time for financial and government criminals gets you.

Paulo, I get this “stuff” by looking, especially at how others are doing, not by basing everything on, if I’m alright Jack, then everything is great. First of all most municipal governments haven’t released their financials yet, so not sure how you know it is all great. Second, yes you are correct they cannot run long term deficits but government fund accounting, “stuff”, which I have dealt with ( a lot) is not as simple as you make out. There are lots of ways around running deficits, including 1)turning current account deficits into short term deficits (they get sign offs from the province, but will make a big show of demanding provincial governments bail them out and then when they don’t, blame them for the increase in taxes) 2) having their various subs such as transit systems, education boards run deficits, then transfer the money (its called Fund Accounting for a reason, lots of little slush funds to draw on) 3) simply re-designating certain current account expense amounts into capital and then raising money via debt financing(province has to go along, but it they don’t more blame) 4) shorting on cash contributions to employee pension “funds” (obligations) increasing accrued pension obligations (popular one in Canada), 5)borrowing from/charging off to various municipal reserve “funds” or accounts (some real, some fictional, more accruals). As an accountant, I’ve seen all these tricks and a few more, so don’t know where you get your ideas about how things “really” work, but I live in a City not a town of 1200….Yes, the feds currently have a 1/3 large capital project program, but they are also trying to drive the Oil and Gas business into the ground, the second largest in Canada after making gas guzzling cars, which can’t be too far off being staked either. As to BC I’m glad all the old people are getting shots, they are here in Alberta too…in 3 months, the best provinces in Canada have done one shot for 10 percent of the population….at this rate we will have everyone fully vaccinated by well you choose the date….I know some people in BC in the film industry…not much going on there, but like I said they are at home collecting a cheque because their real business (working in stores, casino, restaurant) is shut down….whether they open again is another question and a lot won’t . There are lots of businesses that have gone bust, or jobs that no longer exist. But maybe you are right, that’s why Trudeau keeps extending benefits for some 2 Million ex-workers, I know not really needed, booming economy, I feel good. Yeah, everything is coming up roses.

@Paulo: It’s hard to gauge the status of vaccinations due to supply constraints.

As an example, we (wife and I) got both our vaccinations in January. Everyone I know here in this area of Texas over 65 has been vaccinated already (both shots – Moderna). We have 650,000 people in this county.

I’m not saying the rest of the U.S. is like here, but we are vaccinating all age groups and the three hospitals in my area are using a school sports football field to handle the line of people on a daily basis. This has been a well coordinated and successful effort.

Oh no, Canada is coming out with a Budget, quick start pretending.

“Once crisis tools have served their purpose, central banks should scale them back.”

They cant. As soon as the plates stop spinning, they fall.

Let’s go back to the beginning…

Bernanke starts QE, and in a WSJ article of July 2009, explains how it will all be unwrapped, rolled off when things get back to normal. The Dow was circa 10K then and unemployment was circa 8%.

Later, Bernanke said unemployment below 6.5% would be a trigger for the beginning of end of QE and a return to normalcy.

Normal, for those who remember the 20th Century and the time prior to 2008, was Fed Funds equal to or in excess of inflation.

QE never stopped when unemployment dropped as low as 3.5%. Dow over 30K.

In fact, QE increased sharply.

Fed Funds have been below inflation for 12 years with the exception of a few months in 2018.

Central bankers can not, will not retire or retrieve that which they put in motion. For the stimulus of their actions become crutches….and we know what happens when crutches are removed.

They are trapped by their own devices….and seem to enjoy the condition, the power.

“…our inflation objective..”

I still bristle at any central banker who promotes the decline in the value of the currency of his nation. By what authority, from what thought process do you promote such a thing on the people of your country?

Only the blind and morally bankrupt can see past such irresponsible behavior.

As you know historicus, The FED is only promoting the decline in the value of the currency to the detriment the people that don’t matter, workers and common savers. The people that do matter, wealthy asset holders and those on their briberoll, benefit from the FED’s practices.

as to your question “by what authority”? No legitimate authority.

If I was Jpowell what should I do? 1) Infinite QE and zero interest rates to increase the assets of the rich. Considering that the power is given by the width of the gap between rich and poor, the game of QE cannot work forever because in this way even the poor people would begin to understand the game and become rich and the money would have no value. 2) The rich begin to sell some of their overvalued financial assets and buy land and other hard assets. 3) Central banks unexpectedly say the economy has improved a lot and raise interest rates and block QE 4) Financial assets implode and all the mass that had gone into debt to buy financial assets must cover their positions (Margin calls) 4) A lot of people lose money and the government and some monopoly companies come back to the “help” of the mass by offering them poorly paid jobs to pay their debts and, perhaps, with a microchip on their heads the new slaves will not even realize anymore to be and the rich will be even richer because they will own the slaves and all the hard assets. The Bit Reset. You’ll own nothing and you’ll be happy.

You will own nothing and be happy Really means you will be dead and own nothing and happiness comes from being in heaven! :-)

1) IWM ==> a spring < Jan 25(H) @217.91.

2) IWM crossed dma50, penetrated the cloud and landed on a support

line coming from Oct 30(L) to Mar 5 (L), on high volume.

3) Option #1 : IWM might bounce up, give the cloud a headbutt, make a round trip, and penetrate the cloud again, between Apr 13/15 for the Ramadan.

4) Penetrations and headbutts are illegal in Japanese comic books.

5) This round trip will create a new open space for a new dot, probably

a swing point.

6) Option #2 : IWM will osc wildly, make a doji, or two, plunge for Fri.

Hard to believe the BofC (or any Fed Reserve bank for that matter) has real concern for “moral hazard” when as an entity you are proven by your past actions and behavior to already be morally bankrupt.

“you are proven by your past actions and behavior to already be morally bankrupt”

Spot on, Lawefa.

I live in Montreal and what’s going on in the housing market is complete lunacy. People are buying everything they see, massive bidding wars almost doubling housing prices, no inspection of houses, etc. On the island, prices have gone up 20% this year and around the island, it’s 30%. This government has given so many handouts (much more than the US). This, coupled with low-interest rates, will certainly cause a massive collapse.

What could possibly go wrong?

Free dental care means brushing your teeth is optional!

“…the Bank of Canada reduced the purchases of GoC bonds to C$4 billion a week, but shifted to longer maturities….”

I read that as saying the BoC will compete for long Canadas against Canadian life insurance companies (like Manulife, Sun Life, and Great-West Life) and pension plans, and let bank investment dealers (speculators) get more for their government debentures than they would otherwise receive. So much for abandoning moral hazard!

(Embedded in my comment above is my futile attempt to address a pet peeve, of saying that a “bond” is something other than its historical definition of debt secured by a physical asset. Other debt securities are properly referred to as “debentures”.)

All this talk is easy and meaningless with markets at all time highs. Nobody expects them to follow through when housing or stocks drop a few percent.

The Fed did in 2018, and stocks ended up dropping 20% in late 2018, and the housing market was running aground with mortgage rates at 5%.

Yes, but they FED did not follow through. They turned and ran like scalded dogs, to save their hides.

They started normalising but they chickened out real quick. 20% is really not much of a drop after such a run up and such high valuations.

Of course I do hope that they will stick to their guns next time, and their hand may get forced this time by the bond market if inflation starts running too hot.

How can they possibly stick to their guns now, when fair value for the stock market is a 70% haircut?

This is Powell’s last year and they seem to be prepping Brainerd. She wants to lead the Fed on climate change policy. Epilogue on the political scrum L4Y: progressives have continuity, Obama’s VP in WH, Clintons Fed choice LB. Yellen gets kicked upstairs. She wanted “broader authority” for the Fed to buy stocks, and if they want to taper they better have some new tools. Sell bonds and buy stocks? To bring it full circle none of these central banks is going rogue. Not even Canada. The IMF wants to establish a 1/2T SDR fund for developing nations, which needs Congressional approval. One REP Sen raised his voice, but that kind of restraint, is all in the past. The brave new world of central banking takes a step forward.

Is this a signal to move to Canada? Perhaps those of us south of the border will have to think about how to get across, and starting lives there.

After all, with global warming/climate crisis/whatever new term we will start using in the next decade, there is a good chance that Canada will become the next California… weather wise.

So, like Lex Luther in Superman, May be now is the time to buy up “property in AZ” the next beach front.

This move by BoC looks like a trial balloon for similar moves by the other CBs in the future.

A curious tone to this article. It seems to me that the Bank of Canada understands the frenzy they have caused and intend to clamp down on it.

Hard to fault them for that… I just have my doubts they can do everything they say in under two months. Then again they may have taken “jawboning” lessons from the FED’s Powell.

Have I got into a bad habit, over the years, of thinking that US Fed sets the narrative for compliant nations everywhere and W house occupants keep rates low before an election only to see them rise again after the election so that there is somewhere to go before the next election? No, you’re right, it’s just a coincidence, I’m just being dumb.

Our Fed is an arcanum. They are not even properly a central bank, while they have Congressional restraints. Global central banks have greater authority, and little or no accountability. In the US the line between government and private industry is blurry, for global CBs it’s a super highway. Global corporations pay far more in taxes and have greater regulation. US Fed is a serial bubble blower, being accountable to Congress, they ask nothing in return of Wall Street. In the US outsized stock market returns are considered an entitlement, a third rail, not be touched. In order to get Global CB status the Fed needs more than a blank check from taxpayers, who we acknowledge are derelict. US Fed needs to get the labor market “squared away”, an outside the box assignment. The benchmark is oblique reference. The constant hammering on fiscal policy makers is a cheap shot. Corporations want Congress to throw them a few trillion in infrastructure jobs, labor benefits for 3 months, construction wages, and corp XYZ earns a steady stream of revenue from the project. These corporations may or may not hire workers at a living wage, or provide benefits. The Fed encourages them to subsidize this on the fiscal side. US is an exploitive business enterprise, (and offshoring was a blessing, better you than me) whose workers are independent contractors, able to exploit foreign workers at the merchantile level (the game moved from hispanic service workers to factory workers in Asia). China is becoming the labor broker for the world, which explains their regional ambitions. Am business person makes a few million and parks it in the Cayman islands. The Fed only creates the money business uses, they have little responsibiiity with how it is used. This is why the onerous moral implications of Crypto, are a moral relativism.

I don’t believe they are reducing, tapering, cutting bond purchases or printing less money for stimulus. They are trying to influence markets by talking directly to them and purchasing more than $4 billion a week.

Thank you for the reporting.

The Canadian government spending is wildly out of control, as your readers point out, and the worst part is, it’s undemocratic. Why are we bailing out these Albertan tar sands projects, or buying American fighter jets? No one voted for these, and yet they dearly cost every taxpayer. Canadians are the last ones to know anything about where their money is going.

“Once crisis tools have served their purpose, central banks should scale them back.”

_________________________________

“Crisis tools” seem to be no more than special privilege for the well connected and undeserving. Why have them at all?