Unicorn startups are even more unprofitable than those that did not achieve Unicorn status.

By Jeffrey Funk, an independent technology consultant (linkedin), for WOLF STREET:

About 90% of America’s Unicorn startups, ones privately valued at $1 Billion or more, were losing money in 2019 or 2020. According to my recent article in American Affairs, only 6 of 73 were profitable in 2019 and 7 of 69 in the first two or three quarters of 2020 despite most being founded more than 10 years ago.

The six profitable start-ups in 2019 included three fintech (GreenSky, Oportun, and Square) and one startup each in e-commerce (Etsy), video communications (Zoom), and solar energy installation (Sunrun). For the first few quarters of 2020, three of these firms became unprofitable (Oportun, Square, and Sunrun), and four others became profitable: three e-commerce companies (Peloton, Purple Innovation, and Wayfair) and one cloud storage service (Dropbox).

Unicorn startups are even more unprofitable than those that did not achieve Unicorn status. According to Jay Ritter, about 20% of startups at IPO time were profitable over last four years, much more than the 10% of Unicorn startups in 2019 and 2020. Thus, not only has profitability dramatically dropped over the last 40 years among those startup doing IPOs that went public, down from 80% to 90% in early 1980s, today’s most valuable startups—those valued at $1 billion or more before their IPOs—are in fact less profitable than startups that did not achieve $1 Billion in their IPO valuations.

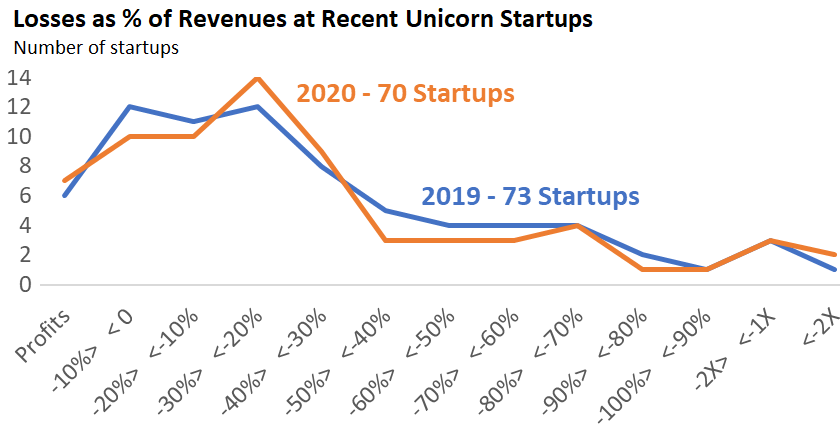

Even worse, a remarkably large fraction of start-unicorns have high levels of unprofitability, as shown in the chart below.

- In 2019, 21 of 73 had losses greater than 50% of revenues, and another 13 (including Uber, Lyft, Pinterest, and Snapchat) had losses greater than 30% of revenues (not counting liquidations).

- In 2020, 19 of 70 had losses greater than 50% of revenues, and another 11 eleven had losses greater than 30% of revenues.

Source: Jeffrey Funk, The Crisis of Venture Capital: Fixing America’s Broken Start-up System, American Affairs,

These high annual losses have also translated into large cumulative losses for some startups, much larger than Amazon’s peak of $3 billion twenty years ago. Uber has more than $30 billion in cumulative losses; and Lyft, Snap, and Palantir have more than $5 billion each in cumulative losses.

How many of these startups might become profitable in the near future?

One way to address this question is by looking at the changes in profitability during 2020, a year in which some Unicorn startups benefited from the lockdown and the higher revenues and willingness to pay that these lockdowns brought. Cloud computing services, food delivery, e-commerce, and Internet entertainment benefited from the lockdown enabling people to work, shop and amuse themselves while stuck in their homes.

Consider the 59 Unicorn startups for which full 2020 income results are now available. Twenty-six had higher ratios of income to revenues, 29 had lower, and four about the same, despite most achieving more than a 30% increase in revenues and some more than 100% in 2020 than in 2019. This simple counting suggests that overall, we shouldn’t expect a vast change in profitability in the near future.

Looking in more detail, consider those startups that went from unprofitable in 2019 to profitable in 2020 or that achieved an increase of at least 0.20 in their ratios of income to revenues between the two years. These startups are listed in the table below, along with their quarterly income since the fourth quarter of 2019.

If a startup is making progress towards profitability, we would expect them to show continuous increases in their ratios of income to revenues, and not just a one or two quarter improvement during the most severe months of the lockdown, when people were willing to pay almost anything for food, cloud computing, mattresses, exercise bikes, and other products and services.

The table below shows that most startups achieved one or two quarters in increases (figures highlighted in red), and not a series of increases that would suggest strong trends toward profitability.

Lemonade, Sumo Logic, Cloudera, Door Dash, Dropbox, and Fiverr are the most conspicuous with big reductions in losses for the second and/or third quarters of 2020, but then increases in the fourth quarter. Somewhat better, Peloton and Wafair show a bigger trend towards profitability but still declining results in the last one or two quarters of 2020.

A lack of continuous improvement in profitability throughout 2020 suggests that the ratio of losses to revenues for these startups may not improve once the lockdowns are over and ratios for some startups may even worsen.

Table: Recent Profitability for Selected Unicorn Startups (Improvements in Red)

| Ratio of Income to Revenues | |||||

| Startup | 4Q 2020 | 3Q 2020 | 2Q 2020 | 1Q 2020 | 4Q 2019 |

| Zoom | 0.29 | 0.25 | 0.28 | 0.08 | 0.08 |

| Peloton | 0.06 | 0.09 | 0.15 | -0.10 | -0.12 |

| Wayfair | 0.01 | 0.05 | 0.06 | -0.12 | -0.13 |

| Purple Innovation | -0.01 | -0.01 | -0.01 | 0.07 | -0.03 |

| Snap | -0.12 | -0.35 | -0.62 | -0.66 | -0.43 |

| Fiverr | -0.14 | -0.01 | 0.00 | -0.18 | -0.25 |

| Social sprout | -0.16 | -0.21 | -0.23 | -0.33 | -0.93 |

| Cloudera | -0.24 | -0.06 | -0.12 | -0.28 | -0.30 |

| Door dash | -0.32 | -0.05 | 0.03 | -0.36 | -0.45 |

| Slack | -0.33 | -0.29 | -0.35 | -0.37 | -0.46 |

| Sumo logic | -0.39 | -0.46 | -0.26 | -0.51 | -0.80 |

| Dropbox | -0.68 | 0.07 | 0.04 | 0.09 | -0.02 |

| Lemonade | -1.62 | -1.72 | -0.70 | -1.42 | -1.38 |

The best results, showing continuous improvements in ratios of income to revenues, can be seen for Zoom, Purple Innovation, Snap, Fiverr, and Social Sprout. Zoom is clearly far ahead of the others with rising profits while Purple Innovation’s improvements in profitability are much more modest. The others experienced improvements in profitability, but they still have losses greater than 10% of revenues.

Overall, these data suggest that most Unicorn startups will struggle to achieve profitability in the future and thus the small percentage of Unicorn startups currently profitable (about 10%) presented at the beginning of the article, will probably not change much in the near future. The percent profitable may rise to 15% or 20%, but not much higher without dramatic changes in technology or scale.

The startups that were profitable in 2019 but went unprofitable in 2020 (Oportun, Square, and Sunrun) may return to profitability, but some of those who became profitable in the first two or three quarters of 2020 (Peloton, Purple Innovation, Wayfair, Dropbox) may become unprofitable after the lockdowns end. Those experiencing continuous reductions in ratios of losses to revenues such as Snap and Social Sprout may also achieve profitability in the near future.

By Jeffrey Funk, an independent technology consultant, and a professor for most of his life, most recently at the National University of Singapore. You can follow him on linkedin. A much longer version was just published in American Affairs.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“About 90% of America’s Unicorn startups, ones privately valued at $1 Billion or more, were losing money in 2019 or 2020. ”

And how well were the startups doing in the year 2000 for comparison?

Robert

Do you understand where the data came from for this article?

Please do the 2000 v 2020 research & get back to us…

Jay Ritter found that percent profitable at IPO time fell from 80% in early 1980s to 20% over last few years but the low of 20% was also achieved in 2000. But the time to IPO was about 1/3 the current time. While many startups during the dotcom boom did IPOs within a few years of founding, most of today’s Unicorn startups are older than 10 years, so they have had ample time to become profitable.

In 2017 I worked for a silicon valley “pie in the sky” startup. It was a joke, bad tech, scamming investors with shady, hide the peanut tactics. I left after 6 or 7 months. Kept up with a couple of the founders, and later learned that they were snapped up eventually by one of the big tech firms. This happened while the company was basically broke, and couldn’t get another round of funding.

Half of the founders with “preferred shares” in the company made several million dollars each. So basically all you have to do is come up with a ludicrous idea, raise some money, mis-manage that money, get bought for pennies, and you can make a few million bucks. The best part of the whole deal was that at their height, this company had a “valuation” of around 700 million dollars. They had only raised about 80 million in operating capital. Insanity, absolute insanity.

No, just deregulated capitalism.

Grimm,

Call us back when bad VC has a 100%+ debt to GDP ratio like DC.

Bad private sector ventures generally self correct (go broke, get acquired for pennies on dollar, etc).

Bad public sector ventures self perpetuate (how many *decades* in Afghanistan, Iraq? How many decades of ten million plus illegals? How many deacdes of high medical inflation due to blind gvt subsidies? Ditto “education”).

And on and on and on.

“Bad private sector ventures generally self correct (go broke, get acquired for pennies on dollar, etc).”

__________________________________

What’s private sector anymore? Corporations with public contracts and/or that buy politicians? The FED and banks with their ability to create money from nothing?

It’s all convoluted with capitalism for those with no assets and without the right license or job, and socialism/fascism for those with assets and properly positioned.

That’s a joke. It’s the regulation of the system that has allowed capital to be allocated so poorly!

The problem is that even “blinded by stupid” investors are starting to catch up after so many dead unicorns.

Yes. The grand business ponzi model of “fake until you can shake it” and then run with your millions. So many beautiful unicorns to choose from….

Ponzi model is OK if you’re early enough

So, we have a slow growing economy that needs low interest rates or the CB’s say everything is going to implode. This financial repression is intended to ease the cost of financing as well get people to spend more and save less. The people say hell no and proceed to buy stocks mindlessly because “where else am I gonna put muh money?”

A bunch of other people realize this is a wonderful opportunity to cook a crock of shat. The shat gets eaten because “where else am I gonna put muh money?” Also, “wow! This is the future!” This is wealth extraction at its finest, when people willingly just give it to you by being easily duped. They used to do it via conquest and coercion or viable business.

Was the “snap up” a real acquisition or an acqui-hire?

Only 7 of 69 were profitable in the first two or three quarters of 2020 despite most being founded more than 10 years ago. Seems like there was something going during that timeframe. Can’t quite recall but didn’t it have a bit of a negative impact on pretty much every company? Can anyone help me out here?

Could there be a limit of say 5 years (someone would need to come up with a proper analysis of what this number should be) during which a start-up can be loosing money. A true innovative start-up /idea after all obviously does need some investment upfront. If it is a startup in an established line of business, such as selling used cars, selling furniture, operating taxis and so on, that limit should be shorter, or there is an additional limit on sales volume. But after that if they keep on loosing money, they get hit by anti-trust dumping regulations and fines. It can’t be that one is allowed to just burn investor cache to acquire market share and then see later on how to monetize ones monopoly!

lol nice onee

Are the nomination of Lisa Khan and Timothy Wu by the Biden administration (supposedly both more stringent antitrust enforcers) going to make any difference?

Chuck Ponzi

Graph included in the “American Affairs” link is difficult to read, but plainly shows high &age unprofitably is not a recent (ie: Covid only) phenomena.

The graph shows a dramatic & sustained increase in % unprofitable over what looks to be about the last 10 years (graph scale is hard to read; interpolating form the 2000 dot-com bust, gives an estimate of about 10 years).

actually the opposite is true. Most Unicorn startups benefitted from the lockdown and the increased demand and greater willingness to pay for software as a service, other cloud services, Internet entertainment along with delivered food, mattresses, exercise bikes and other things. Almost all the Unicorn startups had higher revenues in 2020 than in 2019.

As Jim Grant has noted in numerous interviews, all the CB money printing has eliminated “true” price discovery for most assets. It seems like the more these unicorns lose, the higher the retail investors give them.

I’m an old geezer & pre-Covid, traveled a lot, so I use Uber a lot.

I am perfectly happy to have millionaires, billionaires and millennials subsidizing my Uber rides. I think the subsidy is at least 33%, and I hope this goes on as long as I do.

The problem is, Javert, that the real Taxi companies have to compete with these people with their 33% subsidies. And they have been able to. Their business models are enabling them to survive while waiting for Uber’s business model to send it broke. Uber was relying on being able to send them broke, get rid of their drivers (whatever happened to the next best thing since sliced bread, driverless cars. Since killing those people, Uber seems to have written off the billions they spent on that scheme.) and crank up their prices to pay everyone back their investment money. You would have been better off getting a real taxi, Javert, and not taken part in Uber’s scam.

Sit23

You are, of course, correct in everything you say EXCEPT “you would have been better off getting a real taxi…”.

The problem with taxis in most large cities is the “taxi medallion” scam. Local politicians use this to artificially restrict taxi capacity and, thus, increase political campaign contributions.

Uber got around the “artificially restrict supply”problem, and did a pretty good job exposing (but not quite killing) the taxi medallion scam. Undoubtedly, Uber will eventually fall into the same swamp of campaign contributions.

As a “ride” customer, I (personally) benefit because I can now get a ride any time I want (no more taxi blackout at shift change). The poor guys who drive Uber or taxis pay the real price.

In reality, I have no love for Uber. It is a failed scheme to grow so fast as to monopolize the taxi/ride market, and blow away taxis. Any time the success of your business plan depends on creating a monopoly, you’re on borrowed time. I have no doubt a major reason Uber still exists is…wait for it…CAMPAIGN CONTRIBUTIONS!

@Javert

Your use of Uber (and prior to Uber, libertarian far right) talking points is so far off the mark as to be ridiculous.

Yes, the price of medallions was outrageous in major cities.

But the reason medallions exist was precisely to balance the number of drivers vs. demand.

Taxis became ubiquitous in the late 1920s and early 1930s. By the early 1930s, there were so many taxis on the road that “taxi driver” became synonymous with rapist, thief, scammer etc.

New York City had 12000 taxis at the time Fiorello LaGuardia created the medallion system. 30% of all medallions were reserved for 1 person operators permanently.

The issuance of new medallions is a public process, as are taxi rates. The Taxi Commission hearings are open to all.

Contrast this with the Uber/Lyft model: they’ll sign up everyone they can because the drivers have all the capital/time opportunity cost risk.

Uber/Lyft control pricing (as people are now finding out the hard way, both consumers and drivers).

The problem isn’t taxis and medallions per se – it is that taxi medallions are operated as 24/7/365 rental operations for taxi drivers now. Owning a medallion lets the owner have taxi drivers working for him with no risk: the taxi driver pays fees up front that cover insurance, capital cost etc and keeps whatever he makes – kind of like strippers.

But ultimately, the open system is still better than having techies/monopolists controlling everything.

It is also the drivers subsidizing you.

Remember the good old days when startups used to bootstrap everything? Nowadays they’ve gotta hire 1,000% more employees than necessary and spend a fortune on luxuries, as if they’ve been established for half a century. I don’t think profitability needs to take **decades**.

What was that one, Gumroad? Founder had something near 100 employees when the investors bolted and he started running everything on his own to stay afloat. And he could actually do it! Perhaps there was too much overhead on the payroll there, methinks.

And Paddle, it scared me that they practically had as many employees as customers. I was wondering if I should get involved if they’re burning money like that. Looked like a great way to tank. And still, their customer service was junk.

Whatever.

Imagine how shocked I was to be working on a project financed by a certain Japanese co. (often discussed here) and my employer’s “legal rights” to do the project were “unclear”.

I was told “What we’re doing isn’t legal, but it isn’t clear it’s illegal. It’s a gray area”. This seems to describe a lot of what happening.

It was a sh*t-show from top to bottom. I thought I was going to work for a “google” type co. and instead a friend described it like this: “It sounds like you’re involved in a Ponzi scheme.”

As long as people are willing to work for crooks, they will keep being crooked. It also makes them crooks as well. This explains a lot about the US corporate system.

Nothing makes sense anymore.

O_o

It’s just a game of hot potato. As the potato gets tossed around, the value goes up, but whoever holds it when it pops, loses. You can join or quit the game at any time (if you are not currently holding), but unlike regular hot potato, someone has to voluntary hold their hands up to catch it, when you are ready to toss. Do you dare to catch, in the hopes that at least one person will catch after you?

The hot potato despite its great value and appealing exterior, is worthless and will eventually explode in someone’s face.

The way I understand it, these Venture capital guys (yes mostly guys) big purposes is to support a business they are pretty sure can have a monopoly (a moat as Buffet says) and so conduct predatory pricing, supplier gouges, roll ups of other type businesses and as this proceeds over the years their payday comes once all of the competition has been destroyed and eliminated or bought up and they make their killing. Why Amazon could go 20 years without making a profit, same tactics. Bezos learned this when he was an investment banker in the early nineties. He thought, wow they’ll let me do this? in the name of “free markets” wow gravy train time.

Earl

If you’re trying to sound like you know what you’re talking about, the least you could do is spend 3 minutes researching the financials before you go off on a rant with made-up facts.

“…Why Amazon could go 20 years without making a profit…”

At least for Amazon, your naive analysis couldn’t be more mis-informed.

Amazon has been public 24 full reporting years since 1997, and never went 20 years without a GAAP profit.

o During years 1-6, Amazon GAAP net profits were negative and totaled -$3.037B

o During years 7-24, Amazon GAAP net profits were positive and totaled $43.870B

During Amazon’s start-up phase, free cash flow was probably more important than GAAP net profits:

o During years 1-5, Amazon free cash flow was negative 4 of those 5 years

During years 6-24, Amazon has always had strongly positive free cash flows

All the rest of your accusations are every bit as credible as your grossly inaccurate financial numbers

Amazon has often been described as not making a “meaningful” profit for more than 10 years. I would agree with that.

They really only started being very profitable (I thought they might go under in ~2008), in the past 5 years.

Technically, yes, they made some profit in ~2004 on, but their profit chart hugged the zero line (and continued to go negative sometimes) until web services business kicked in about 2015.

If people are suspicious of a business like Amazon’s, I think they might have some good reasons. AWS basically saved Amazon from being something like eBay or Travelocity.

wkevinw

As a retired CFO, I get your point about low (GAAP) AMZN profitability. To the untrained eye, GAAP financial statements can be misleading (especially for a growth company like AMZN). Until recently, AMZN essentially invested almost every cent it earned back into its business, showing up as massive growth in property, plant & equipment, which allows AMZN to expand even more.

o Over the last 10 years, WalMart (WMT) has out-earned Amazon (AMZN) 2.76% GAAP profit to 1.92%

o Over the last 16 years (as far back as I can analyze), WMT has out-earned AMZN 3.06% to 2.43%

I read financial statements differently than you do, and over the last 16 years, AMZN VASTLY outperforms WMT:

o GAAP profits are meaningful, but so is free cash flow

– WMT has been cashflow negative 6 of the last 10 years

– AMZN has been cashflow positive for the last 10 years -AMZN cash flow is 5-10 times larger than WMT cash flow, even on significantly lower revenue

Over the last 15 years:

o AMZN revenue grew from $8.5B$ to 386B (WMT $284B to $559B); AMZN;s annual compound annual growth beats WMT: 29% to 5%

o AMZN Prop/Plant/Equip compound annual growth beats WMT: 47% to 2%

You expressed concern “…they might go under ~2008…”; AMZN has NEVER EVEN BEEN CLOSE TO “going under”, including in 2008.

@ Javertchip –

I very much appreciate your CFO perspective.

I thought that GAAP earnings were typically lower than cash flow. I am used to seeing companies using cashflow before deductions for depreciation and amortization, etc. because that number looked better than GAAP earnings. I think EBITDA does this, and I’ve always thought that the use of EBITDA was a misleading salesman’s trick.

You stated that Walmart has out-earned Amazon over the last 10 years yet only had positive cash flow for 4 of those years. Amazon has been cashflow positive all 10 years.

I believe it’s possible possible to have negative cash flow and positive earnings, but to do that for four out of 10 years and still have overall positive cash flow for the 10 year period shows very bumpy earnings. I’ll have to think this through.

What am I missing here?

Thanks.

cb

The attached links is to the WMT cash flow summary page. What you’ll see for the last 10 years is WMT will go cash flow negative for $250-500M for a couple years, hen it’ll go $1,250 cash flow positive for a year. Lumpy is a good way to describe it.

https://www.macrotrends.net/stocks/charts/WMT/walmart/cash-flow-statement

Think of GAAP income statement as the “regulatory” book for the corporation; think of the Cash Flow statement as the corporation’s checkbook.

GAAP profits & earnings will frequently be wildly out of sync for a year or two, but a 5-yr moving cumulative total should bring the two into fairly close agreement. If it doesn’t, it does not necessarily mean there’s, it just requires further research to figure out what’s driving the distortion.

@ Javert Chip –

Thank you!

Profitability is not the only goal and is time-based taking into account market maturity, operational mandate and many other things. The game of disruption seems to have long tail repercussions that are winner take all substantial which require ongoing heavy investment to get over that hump. At least thats the ongoing stuff I keep hearing from ole Kathy at Arc among others.

Fraud never makes sense to those not profiting from the activity.

Kinda miss the days when people ran con men out of town on a rail.

@michael

“Fraud never makes sense to those not profiting from the activity.”

The story I heard was that, during the WorldCon period, AT&T was going crazy because they kept losing deals. WorldCom was pricing telecom service way below AT&Ts cost, and the CEO kept demanding that the tech guys figure out how to match the competitor’s prices.

Very stressful, especially if you are the guy saying “There’s no way that they are really able to deliver for that price.”

Of course, eventually we found out how it all works: WorldCon was selling below cost, using the investors’ money to make up the difference, and committing fraud in its accounting. A Ponzi Scheme.

The moral of this story is:

“Sometimes, things don’t make sense because they don’t make sense.”

Gab, headquartered in Pennsylvania, has about two dozen employees on a shoe string budget.

Gab is a highly competent competitor to Twitter and will eventually crush it if you extrapolate current trends.

So how much off all this is hype plus cheap and was money…

*wheezing laughter*

So what does Gab produce?

Same thing as Twitter…

Well, except for the $1.14 billion in net loss Twitter reported for 2020 alone.

Thanks.

You could probably buy a fully-functional Twitter clone for a few thousand bucks. What’s Twitter got? People use it, for some gawdawful reason, and for another gawdawful reason society and journalists at large treat it as if it’s a respectable source of knowledge. So they can burn money all they want, because they’re anointed. And if Gab presents a challenge someday, well, then we’ll just have to disappear them like Parlor, won’t we?

A change in perception might tell you that these startups are not training the next generation of IT engineers, they are training the next generation of financial engineers.

I saw an interview with some big shot from Silicon Valley a few weeks ago. He said that companies deliberately don’t want to make profit because then they will be measured against others using P/E ratios and other common sense valuations. But as long as you are a money burning unicorn, you keep the dream alive because nobody really know what it’s worth. Then cash your shares at crazy high valuations.

Never bothered Tesla…

As far as I’m aware, Tesla never made a profit from manufacturing cars. They only made a tiny profit because of carbon credits.

Tesla has a PE ratio of 984 as of today.

GM? 13.

“Common sense valuations”

Yes, perhaps Tesla made a mistake banking profits on the carbon credits. Perhaps this is the reason their stock has been falling recently ;)

And everyone thought oil companies drilling into shale plays were bad guys. And they even made a product that was a beneficial need.

Everything is backwards in this bastardized country.

Because of NDA’s, they are the good guys…

they are bad guys, their deceit involves poisoning the land and water for profit, creating cancer clusters for years to come, the others sell vaporware and other worthless stuff.

So where would *you* be today without oil and plastics? Certainly not typing that response on a computer. And the “vaporware and other worthless stuff” would not have been in existence.

a class of synthetic chemicals known as per- and polyfluoroalkyl substances — PFAS for short. Members of this class, often referred to as “forever chemicals” because they are highly persistent in the environment, are known to cause adverse health impacts in humans. This can include a range of symptoms, including damage to the immune system, low infant birth weights and cancer … its has been used in fracking fluids

Heck, it’s best to be pre revenue. The HBO show “Silicon Valley” covered this beautifully in a little over a minute.

Just go to youtube and search “Silicon Valley No Revenue”.

It’s a pure play.

The VC’s are long gone by the time reality sets in. The game for the early investor is to seemingly increase value enough, either through actual progress by the company, or just getting in early on a rising trend, or adding big names, and then to bring in other investors, who hopefully can cash out in an IPO where the dreck is dumped into 401k’s, pensions, widow’s and orphan funds, or where the company can be acquired.

The early stage investor is part slim-flam man, part carnival barker, part peep show tout, part trend spotter, but also clever packager and salesman and indeed, risk taker. They realize the company is nothing more than a product that needs dressing up, proper presentation, and marvelous hype, in order for their early $0.001/share stock to be worth $20/share.

What about a privately held company in information tech that is about 10 years old and has a proven record of profit. If this company wanted to go ‘unicorn,’ would its track record of growth and profitability not make it attractive to investors?

Basically, aren’t VC investors looking for value, or is a dice roll more exciting? Serious question.

Serious answer:

At various phases in the start-up-to-public life cycle, VC’s do indeed roll the dice. They search for value with a proprietary selection of a stable of investments in various phases of start-up.

There are numerous times in the start-up life-cycle for VCs to profit & exit the investment.

VC’s owning big chunks of unicorns are dudes in search of greater fools, which usually shows up in the form of fund managers in search of yield. VCs may have bought stock at $1/shr, but sell to follow-on investors at much higher multiples (3-1, 5-1, 10-1…whatever you can get & much higher than IPO 1st day pops).

(You may have noticed that stocks are being sold, albeit under restricted circumstances, even before going public).

VCs tend to negotiate special rights allowing them to exit early (including investment refund) as other, non-VC investors come onboard.

My experience is comically outdated, but In the primitive old days, if 1-in-10 of your prospects was successful, you made money. Today’s definition of success is infinitely more complex, and I’m wildly out of date, but you get the drift.

This definitely is not a gentle game of bean-bag.

Thanks JC.

Isn’t this all good though because it’s “the smartest guys in the room” “doing god’s work” again?

Well over the last 35 plus years I’ve worked for quite a few VC financed tech companies. Some became very successful public companies with high 9 digit $ revenue. And healthy profits. So I have seen up close how VC actually works in its last three iterations.

Before 1997 the VC’s were basically loan sharks in expensive suits but almost all the startup companies were legit. Trying to make products that made a profit. Most stood a good chance of IPO at some stage. And even a profitable future.

Then in 1997 the initial investor cash out rule was changed by the SEC and very quickly all the new VC financed companies were little more than pump and dump operations. The initial investors could cash out at IPO time, rather than the previous 12 / 18 months later. Which meanthat before 1997 the company had to be somewhat financially solvent at IPO time. To survive the 12 to 18 month to cash out time. After 1997 it was boiler room city. This was the first Dot Com Bubble.

The 2000 crash killed the IPO market and it never recovered so the VC’s no longer could count on any potential upside from an IPO. Which is where they made their real money in the past.

So they quickly moved to the hedge fund model, the 2/20. Before 2000 VC’s never charged management fees. Since 2000 all income for around 97% of hedge funds most years is purely the 2. The management fees. Its the other 3% of VC’s (the old timers) who make any of the 20 on the upside. Usually from a financially engineered acquisition rather than a traditional IPO or acquisition.

So now VC, especially in San Francisco, is purely a fraud. A VC raises a fund of a few hundred million and needs to stick it somewhere for 5 years to collect its management fees. Most of the companies they invest in last around 5 years before they are made disappear though “acquisition” or equivalent. The “valuation” of these companies is based on just how much money they raise, not on any future profit or ROI they might make or any realistic potential future revenues. I have run dev teams, I have prepared budgets, I know how much it costs to run a large dev team to create major products. The amounts raised in the last 10 to 15 years bears no relationship to actual business costs but purely to inflate “valuations”. So you see a product that might need maybe $5M to bring to market and grow raise $150M. Or a company whose future net income on revenue might be a reasonable low 8 figure, if everything goes right, raise $500M. Or if you apply traditional valuation metrics to a Unicorn the $20B company quickly becomes a $400M company. On a good day.

There will never be a positive ROI for about 95% of the VC financed companies I have seen in the last 15 years. None. They are purely financial engineering operations. To harvest VC management fees.

Think of the current VC model as little more than a sophisticated Ponzi scheme and you would not go to far wrong. It is so bad that it makes most of the “mixed strategy” hedgies almost look legit.

tfourier, well said. Pretty much lines up with what I saw over the same time period. The dance has evolved and is more sophisticated with multiple funding rounds.

Still the same dance, different beat.

Worth a read: footnote 25: Charles Duhigg, “How Venture Capitalists Are Deforming Capitalism,” New Yorker, November 23, 2020.

V.C.s seem like these quiet, boring guys who are good at math, encourage you to dream big, and have private planes. You know who else is quiet, good at math, and has private planes? Drug cartels.

“I see. Those are all broker’s yachts. Where are the customer’s yachts?”

Kind of makes you sick that Yellen and now Powell has stolen Grandma’s interest payment and given it to shysters to launch startups and Spacs. What did they think was going to happen?

Listened to some of Senate committee patting Yellen and Powell on the back for making it possible for the Senators to save the US with magic money. Sounds like IMF getting one trillion as well. Why not? It’s for the children.

Is Dropbox’s large 2020Q4 loss due to a one-time write-off of office space leases that don’t make sense any more? That might also be the case for some of the others showing one bad quarter.

1) SPX weekly dropped on top of Feb 1st(C).

2) SPX daily is training for Jared Borgetti deflections headers on dma50 and the cloud head bump, for nest week soccer game.

3) The 1970’s inflation was caused by Gamal Abdul Nasser after he closed the Suez canal between June 5 1967 and June 5 1975.

4) Onassis became a multi millionaire and married a famous girl.

5) Egypt switched from the Soviet side to the US side and Egypt kicked

the Soviet fleet from Port Said.

15 ships were stranded for eight years in the Canal after its closure. Hopefully the one blocking it now won’t be there that long.

1) Submarines could inflate M1 if Russians and gold.

2) Egyptians spend hours sifting sand, and digging out the canal might work.

4) Grace Kelly went to Monaco, and you still need a tie to enter the casino.

5) Cloud storage for NFTs works with certified valuation.

We have reached the limit of human time available to interact with any more device based crap that spews from that brain killer called the smart phone. What we need is a personal robot to be our surrogate consumer. While we sleep the robot will be busy doing shit on the phone or net to keep these venture capitalists productive doing more brain dead shit we don’t need done. My fishing pole is f#*king perfect. Has never required an up-grade.

The airlines might actually survive these monkeys. I can see DoorDash getting a bailout because Congress Critters probably use them to order food and other things. Fiverr as well, because hei Slavery at Scale As A Service (SSAAS) is definitely the future of this country. The other names?

ROFL.

Breaking News: China’s Didi (their version of Uber) is considering a $100 billion dollars US listing.

Given the climate, I consider it unlikely they will get a green light.

Let’s see, we give a Chinese firm located in Beijing $100 Billion and they give us imaginary pieces of paper and never drive their taxi on U.S. soil. Boy, that sounds appealing!

Is this going to be another Shaq SPAC deal?

No different from BABA.

‘Chipmaker Sky Water Technology announces IPO’

That’s the headline on this morning’s Minneapolis Star Tribune business page.

“The company which has its roots in the Minnesota high-tech pioneer Control Data Corp., has flourished in recent years as a maker of chips designed by other firms that don’t need the huge output and latest chip-making technology offered by the largest fabricators.”

“Amid a sharp fluctuation in the broader chip industry because of the pandemic and recession, Sky Water’s revenue rose by about 3% last year to $140.4 million, the (IPO) listing notice said.”

But here’s the kicker for a company aiming to raise $75 million with an IPO: “It posted a net loss (last year) of $19.7 million, widening from a loss of $16.4 million in 2019.”

So we have Minnesota’s largest chipmaker which has been around for decades, “.. has had investments and contracts with the US Department of Defense, and is working with university researchers on nanotube technologies and other ideas to move past silicone as the foundation technology for semiconductors.”, ready to launch a public offering.

OK, that sounds nice and rosy, but what we really have is a company searching for cash because it pulled in $140 million & lost $20 million – making semiconductor chips under contract last year. And doing so in a factory built in the mid-eighties, and presumably paid for long ago.

I reckon this needs to filed under WTF?

Check in on SKYT on NASDAQ in a few months to see how things shake out – or place your bets now if you want to roll the dice, eh.

1) What start up : it’s almost over.

2) Option : SPX weekly. // Next week SPX will make a round trip. A bull trap week. From a new all time high, a UTAD, — after touching a support line coming from Nov 2(L) to Mar 1st close, — to close inside Mar 8 close, x3 weeks in a raw..

3) The following week, Apr 5, Mon morning after Easter Sun, might be a big Kakki week.

4) If correct, Apr 5(L) will take every SL < Mar 1(C).

Wolf – your unicorn analysis of venture capital in the US just scratches the surface of this longstanding scam. Any VC fund < $500MM is up against a mathematical impossibility to return the 30X pie-in-the-sky returns to CIO guppies at the insurance companies and family offices. It is also a fact that a few outlier mega-winners have an outsize impact on total industry returns. Out of a model portfolio of ten companies on average, seven out of ten portfolio companies will not return the money invested in those startups and the majority will need to be written off. This requires heavy lifting from the remaining three. Of the three, two are expected to return enough to cover all the losses; the third to provide the 20 to 30 percent internal rate of return (IRR) investors anticipate. The math is simple: If a VC has less than $500MM to invest they cannot make enough table bets to improve the odds.

Lego Capitalist

Note the beautiful symmetry between Cubs baseball fans and human greed: the future is ALWAYS rosey and bright, except when it isn’t, but then hope springs eternal and we’re off to the races again!

How many times are you gonna buy Argentina government bonds? Even worse (better?) you know beyond an absolute certainty that Argentina won’t stay solvent for more than, say, 10-15 years…so you go out and buy a 100 year Argentina government bond.

That model died more than twenty years ago. That was the mid 1950’s to mid 1990’s VC model. You will only find it in textbooks, not in the real world.

If you think of current VC’s as having exactly the same business model as hedge funds you wont go to far wrong. Just like with hedge funds most VC’s only make money from the management fees. At least the principals do. The investors dont make money. In any given year less than 10% of funds have any kind of positive return and most of that is concentrated in a very few player. Of the 5K odd hedge funds maybe 100/200 make any reasonable return on the money invested. Same kind of ratio with VC’s.

As for which VC’s makes any real money among the Sand Hill crew. Companies or principals who were around pre mid-1990’s make almost all of the real ROI. Almost every post mid-1990’s VC operation is purely a management fee harvesting operation. They will never make any money for investors. By design.

Last time I looked a big chunk of the money to fiance this particular VC scam (sorry financial engineering product) came indirectly from large institutional investors like retirement funds and insurance funds etc in a desperate search for yield. When their traditional investment instruments like bonds no longer turned the historical 6% / 8% needed to support their business model there was a desperate scramble for anything that promised a much higher yield.

So think of the current situation as a much much bigger version of the German institutional investment in US real estate related products pre 2008 through offshore subsidiaries. To try get the yields they could not get from the traditional investment markets. Which almost bankrupted Deutsche Bank (saved by the offload to Depfa/Hypo) and left a $300B plus bad bank in Germany.

The same sort of people are currently financing the VC’s for the same kind of reasons. A desperate search for yield.

The only current VC investments that can return a profit on the huge amounts of money invested are those in companies that establish a defacto monopoly. With monopoly pricing they can make money. No other way. And I can count those on the fingers of one hand. When you add up all money invested over the years there are almost no positive ROI’s since the late 1990’s.

Because thats how financial engineering works. The only people who generally make any money are those selling the products. Any upside for the purchaser is purely incidental. And accidental.

Valuably insightful.

Thanks for sharing the view from the inside.

As near as I can tell the US unicorn start up business model isn’t broken.

In fact, it is working all too well!

It has never been easier to raise money!

There are more fools around today, than in all of human history!

The bigger your losses, the more money you can get!

“Investing” in Unicorns is akin to “investing” in a crack addict.

Returns are wholly dependent upon the greater fool.

Personally, I just can’t wait to invest heavily in, and replace Softbank in the WeWork IPO. Softbank has had WeWork to themselves way too long.

These businesses depend on ‘investors’ with more money than sense.

Thanks to the policies of central banks around the world, there is an increasing supply of these people.

I can’t help thinking we haven’t learned much since the Financial Crisis of 2007 – 2008. During this last financial crisis, massive losses were created when investors poured imprudent and highly leveraged sums into mortgage backed securities that were filled with questionable consumer loans. These consumer loans were called ‘subprime’, and many were questionable because underwriting deteriorated to the degree that many borrowers had No Income, No Job, No Assets (colloquially called “NINJA” loans).

It seems we now have a situation where imprudent sums have been poured into questionable ‘unicorn’ investments via venture capital, IPO’s, SPAC’s, equities, leveraged loans, and high yield bonds. Many of these investments are questionable because the corporations backing them have Negative Income with no path to profitability, No Governance, and (almost) no Physical Assets to liquidate in bankruptcy (what you could colloquially call “NINGPA” investments). This is essentially the same greater fools game that was played with housing prices before the 2007 crash.

So similar playbook to 2007 – 2008 Financial crisis, except what backs these investments has switched from consumer to corporate obligations.

This might seem like I’m stating the obvious but any company that constantly generates massive losses, and has virtually no assets will not be able to pay back its investors.

Sagittarius:

Sometimes the “obvious” is very “opaque” to most.

No bubble according to Ray Dalio. We are only halfway to 1929 or 2000.

Amazing stuff are happening!!!

You pompous celibates! We’ve off-shored jobs making actual things, and so many people look to being employed at companies making frivolous apps, or that are based upon a story. Unicorns create jobs.