Everything is on ice. But when forbearance ends, forced sellers or lenders will put millions of these homes on the market.

By Wolf Richter for WOLF STREET.

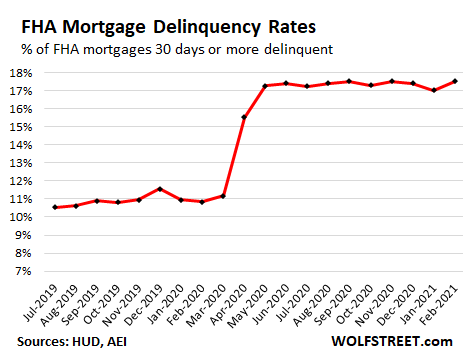

On the other side of the red-hot housing market, a historic delinquency problem has been fermenting since last spring, largely put on ice and on hold by forbearance programs, waiting to be dealt with. The Federal Housing Administration (FHA) which insures nearly 8 million high-risk mortgages, reported that the delinquency rate of its mortgages rose to 17.5% in February, up from 17.0% in January, matching the all-time records of September and November last year, according to the AEI’s Housing Center.

“Low down payments, low closing costs, and easy credit qualifying,” the FHA promises. So FHA mortgages always have high delinquency rates, even during the Good Times, when they were already rising. But during the Pandemic, delinquencies ballooned, and they’re not improving in any way despite the improving economy:

The delinquency rate for the largest 169 Metropolitan Statistical Areas (MSAs), rather than the US overall, accounting for about 6 million of FHA mortgages, rose to 17.9%.

“Seriously delinquent” mortgages – 90 days or more delinquent – in February rose to a record 12.0% for the US overall and to 12.4% for the largest 169 MSAs.

The delinquency rate exceeded 20% in 30 of the 169 largest MSAs, topping out in the metro of Nassau County-Suffolk Country, NY, at 24.8%. Among those 30 metros with 20%+ delinquency rates were 4 metros in Texas, 4 metros in Louisiana, 3 metros in New York, 3 metros in New Jersey, and 2 metros in Pennsylvania.

And when forbearance ends?

Rumors of perma-forbearance are now floating around, given the multiple extensions of the forbearance programs that no one has any political appetite to let expire. But those are just rumors. Eventually, those programs will end, and then the delinquent mortgages will have to be dealt with.

Borrowers who can do so will resume making payments, either with the missed principal and interest added to the end of the mortgage, or with the lender agreeing to modify the mortgage. This would cure the delinquency and bring the mortgage current.

Borrowers who cannot or don’t want to make mortgage payments can sell the home and use the proceeds to pay off the mortgage, including the missed interest payments. If the borrower fails to sell the home and pay off the mortgage, the lender can foreclose and sell the home. In either case, those homes are going to show up on the market.

Given the massive surge in home prices, a sale would be a logical solution for these borrowers who cannot make the payments. They might even walk away with a little extra cash.

But in markets with a large concentration of delinquent FHA mortgages, this would unleash a flood of homes coming on the market – and it would instantly cure, and more than cure, the inventory shortage now being lamented, and when large enough, the sudden supply of homes for sale would send bigger ripple effects through the market.

That’s why no one is eager to let the forbearance programs expire, and why it’s so hard to get out of this extend-and-pretend phase.

The AEI Housing Center identified 10 metros that are most at risk of this sudden supply of homes, with delinquent FHA mortgages showing up on the market. These are metros with both: a high share of FHA loans, and a high delinquency rate of those FHA loans. Note the large number of delinquent FHA loans in the second column, waiting for a resolution.

For example, in the Houston metro (#2), 48,483 FHA mortgages are delinquent, or 22.5% of all FHA mortgages in the market. Of them, 32,224 mortgages are “seriously delinquent.” This creates the potential that tens of thousands of homes flood the market over a relatively short period of time.

And those delinquent mortgages are just FHA-insured mortgages and do not include other delinquent mortgages.

| 10 Metros Most Threatened by FHA Delinquency Rates | ||||

| MSA | # delinquent FHA loans | % delinquent | % seriously delinquent | FHA Share by count |

| Atlanta-Sandy Springs-Alpharetta, GA | 50,499 | 20.4% | 14.5% | 21.0% |

| Houston-The Woodlands-Sugar Land, TX | 48,483 | 22.5% | 15.9% | 19.3% |

| Chicago-Naperville-Evanston, IL | 38,344 | 21.8% | 14.9% | 14.2% |

| Dallas-Plano-Irving, TX | 27,517 | 19.2% | 12.9% | 14.8% |

| Washington-Arlington-Alexandria, DC-VA-MD-WV | 27,243 | 21.1% | 15.7% | 13.7% |

| Riverside-San Bernardino-Ontario, CA | 21,770 | 17.1% | 11.9% | 20.6% |

| Baltimore-Columbia-Towson, MD | 20,899 | 19.9% | 14.1% | 19.4% |

| San Antonio-New Braunfels, TX | 17,881 | 19.6% | 13.0% | 19.3% |

| Orlando-Kissimmee-Sanford, FL | 15,593 | 18.7% | 13.8% | 21.6% |

| Tampa-St. Petersburg-Clearwater, FL | 15,459 | 16.5% | 11.9% | 19.6% |

With FHA loans, it’s not the lenders or investors that carry the risk. The FHA insures these mortgages; and the FHA being a government agency, it’s the taxpayers that carry the risk.

Inflated home prices theoretically reduce the costs of resolving these delinquent mortgages. But if a bunch of these homes suddenly show up on the market, as the floodgates of forbearance open and trigger forced selling, they will put downward pressure across the market, thereby increasing the costs of resolving those mortgages.

The table below shows the 169 MSAs and their FHA loans, in order of the overall delinquency rate of those FHA loans (3rd column). You can use the browser’s search function to find an MSA (if your smartphone clips the 5th column, hold your device in landscape position).

| MSA | # delinquent FHA loans | % delinquent | % seriously delinquent | FHA Share by count |

| NASSAU COUNTY-SUFFOLK COUNTY, NY | 13,660 | 24.8% | 19.3% | 15.4% |

| POUGHKEEPSIE-NEWBURGH-MIDDLETOWN, NY | 3,419 | 24.2% | 17.9% | 15.6% |

| NEW YORK-JERSEY CITY-WHITE PLAINS, NY-NJ | 21,074 | 24.2% | 19.1% | 9.7% |

| NEWARK, NJ-PA | 12,280 | 23.5% | 17.9% | 18.2% |

| LAFAYETTE, LA | 2,493 | 23.4% | 16.2% | 16.8% |

| NEW ORLEANS-METAIRIE, LA | 8,650 | 23.3% | 16.2% | 17.1% |

| FORT LAUDERDALE-POMPANO BEACH-SUNRISE, FL | 11,005 | 22.7% | 17.0% | 19.5% |

| HOUSTON-THE WOODLANDS-SUGAR LAND, TX | 48,483 | 22.5% | 15.9% | 19.3% |

| BATON ROUGE, LA | 6,219 | 22.1% | 14.3% | 19.8% |

| CHICAGO-NAPERVILLE-EVANSTON, IL | 38,344 | 21.8% | 14.9% | 14.2% |

| BRIDGEPORT-STAMFORD-NORWALK, CT | 3,437 | 21.8% | 16.5% | 12.0% |

| CORPUS CHRISTI, TX | 2,941 | 21.3% | 14.1% | 23.1% |

| SHREVEPORT-BOSSIER CITY, LA | 3,243 | 21.1% | 13.7% | 23.2% |

| WASHINGTON-ARLINGTON-ALEXANDRIA, DC-VA-MD-WV | 27,243 | 21.1% | 15.7% | 13.7% |

| MCALLEN-EDINBURG-MISSION, TX | 4,256 | 21.0% | 15.0% | 35.2% |

| CAMDEN, NJ | 12,118 | 20.9% | 14.9% | 26.1% |

| BEAUMONT-PORT ARTHUR, TX | 2,135 | 20.8% | 13.8% | 22.9% |

| GARY, IN | 6,462 | 20.7% | 14.2% | 22.3% |

| ATLANTA-SANDY SPRINGS-ALPHARETTA, GA | 50,499 | 20.4% | 14.5% | 21.0% |

| PHILADELPHIA, PA | 14,602 | 20.2% | 13.2% | 17.6% |

| BARNSTABLE TOWN, MA | 562 | 20.2% | 14.2% | 7.4% |

| BALTIMORE-COLUMBIA-TOWSON, MD | 20,899 | 19.9% | 14.1% | 19.4% |

| BOSTON, MA | 4,169 | 19.8% | 13.8% | 8.3% |

| MIAMI-MIAMI BEACH-KENDALL, FL | 10,765 | 19.7% | 14.8% | 20.0% |

| SAN ANTONIO-NEW BRAUNFELS, TX | 17,881 | 19.6% | 13.0% | 19.3% |

| WEST PALM BEACH-BOCA RATON-BOYNTON BEACH, FL | 6,544 | 19.6% | 14.5% | 17.4% |

| NEW HAVEN-MILFORD, CT | 5,498 | 19.6% | 13.8% | 20.7% |

| WILMINGTON, DE-MD-NJ | 5,773 | 19.5% | 13.4% | 23.5% |

| MOBILE, AL | 3,280 | 19.5% | 12.5% | 24.3% |

| CHARLESTON-NORTH CHARLESTON, SC | 4,130 | 19.3% | 13.5% | 13.7% |

| LAS VEGAS-HENDERSON-PARADISE, NV | 13,423 | 19.3% | 14.7% | 16.9% |

| COLUMBIA, SC | 5,809 | 19.2% | 12.9% | 18.8% |

| DALLAS-PLANO-IRVING, TX | 27,517 | 19.2% | 12.9% | 14.8% |

| BIRMINGHAM-HOOVER, AL | 7,353 | 19.0% | 12.3% | 18.2% |

| FORT WORTH-ARLINGTON-GRAPEVINE, TX | 15,879 | 19.0% | 12.8% | 18.3% |

| GREELEY, CO | 2,178 | 18.8% | 13.6% | 20.7% |

| EL PASO, TX | 6,887 | 18.7% | 13.0% | 26.9% |

| WORCESTER, MA-CT | 3,748 | 18.7% | 12.8% | 15.1% |

| ORLANDO-KISSIMMEE-SANFORD, FL | 15,593 | 18.7% | 13.8% | 21.6% |

| FREDERICK-GAITHERSBURG-ROCKVILLE, MD | 5,040 | 18.6% | 14.0% | 12.7% |

| ELGIN, IL | 4,594 | 18.5% | 12.5% | 19.9% |

| SAN RAFAEL, CA | 36 | 18.5% | 14.9% | 1.6% |

| SPRINGFIELD, MA | 2,916 | 18.4% | 12.2% | 17.4% |

| LITTLE ROCK-NORTH LITTLE ROCK-CONWAY, AR | 4,989 | 18.3% | 12.8% | 16.6% |

| MEMPHIS, TN-MS-AR | 10,392 | 18.2% | 11.7% | 21.6% |

| VALLEJO, CA | 1,645 | 18.2% | 13.0% | 16.4% |

| OAKLAND-BERKELEY-LIVERMORE, CA | 3,470 | 18.1% | 13.4% | 6.1% |

| SAVANNAH, GA | 2,264 | 18.1% | 12.1% | 16.1% |

| LAKELAND-WINTER HAVEN, FL | 6,090 | 18.1% | 12.8% | 34.0% |

| OXNARD-THOUSAND OAKS-VENTURA, CA | 1,249 | 18.1% | 13.0% | 8.7% |

| URBAN HONOLULU, HI | 808 | 18.0% | 14.1% | 4.0% |

| CAMBRIDGE-NEWTON-FRAMINGHAM, MA | 3,990 | 17.9% | 12.9% | 7.5% |

| HARTFORD-EAST HARTFORD-MIDDLETOWN, CT | 7,566 | 17.9% | 12.6% | 19.5% |

| LOS ANGELES-LONG BEACH-GLENDALE, CA | 15,170 | 17.8% | 12.9% | 9.7% |

| LAKE COUNTY-KENOSHA COUNTY, IL-WI | 3,860 | 17.7% | 12.0% | 12.8% |

| CHARLOTTE-CONCORD-GASTONIA, NC-SC | 13,095 | 17.7% | 12.0% | 13.7% |

| SAN DIEGO-CHULA VISTA-CARLSBAD, CA | 4,054 | 17.5% | 13.3% | 7.0% |

| PORT ST. LUCIE, FL | 3,097 | 17.4% | 12.3% | 24.9% |

| JACKSONVILLE, FL | 8,508 | 17.4% | 12.2% | 16.1% |

| NAPLES-MARCO ISLAND, FL | 1,361 | 17.4% | 12.7% | 14.0% |

| AUGUSTA-RICHMOND COUNTY, GA-SC | 3,628 | 17.3% | 11.1% | 17.8% |

| ALBANY-SCHENECTADY-TROY, NY | 4,189 | 17.3% | 12.0% | 15.0% |

| ALLENTOWN-BETHLEHEM-EASTON, PA-NJ | 5,073 | 17.2% | 11.7% | 22.2% |

| RIVERSIDE-SAN BERNARDINO-ONTARIO, CA | 21,770 | 17.1% | 11.9% | 20.6% |

| DURHAM-CHAPEL HILL, NC | 1,809 | 17.1% | 11.3% | 8.0% |

| CLEVELAND-ELYRIA, OH | 11,560 | 17.0% | 12.0% | 17.7% |

| DETROIT-DEARBORN-LIVONIA, MI | 7,762 | 17.0% | 11.2% | 19.1% |

| AUSTIN-ROUND ROCK-GEORGETOWN, TX | 8,836 | 16.9% | 11.4% | 10.6% |

| LUBBOCK, TX | 1,968 | 16.9% | 10.9% | 19.2% |

| TACOMA-LAKEWOOD, WA | 3,939 | 16.9% | 12.1% | 16.4% |

| RALEIGH-CARY, NC | 4,969 | 16.9% | 11.5% | 8.8% |

| PROVIDENCE-WARWICK, RI-MA | 7,518 | 16.8% | 11.4% | 19.0% |

| OKLAHOMA CITY, OK | 8,812 | 16.8% | 11.5% | 18.6% |

| WICHITA, KS | 3,558 | 16.8% | 11.2% | 16.1% |

| TULSA, OK | 5,734 | 16.8% | 11.5% | 20.4% |

| MONTGOMERY COUNTY-BUCKS COUNTY-CHESTER COUNTY, PA | 6,639 | 16.7% | 11.7% | 11.7% |

| DENVER-AURORA-LAKEWOOD, CO | 11,313 | 16.7% | 11.9% | 13.9% |

| SAN JOSE-SUNNYVALE-SANTA CLARA, CA | 670 | 16.6% | 13.1% | 2.3% |

| ANAHEIM-SANTA ANA-IRVINE, CA | 2,198 | 16.6% | 13.1% | 5.3% |

| STOCKTON, CA | 2,969 | 16.6% | 11.6% | 18.0% |

| VIRGINIA BEACH-NORFOLK-NEWPORT NEWS, VA-NC | 10,195 | 16.6% | 11.2% | 14.4% |

| RICHMOND, VA | 8,310 | 16.5% | 10.9% | 17.7% |

| ST. LOUIS, MO-IL | 15,649 | 16.5% | 10.9% | 15.2% |

| GREENSBORO-HIGH POINT, NC | 3,846 | 16.5% | 10.9% | 15.3% |

| TAMPA-ST. PETERSBURG-CLEARWATER, FL | 15,459 | 16.5% | 11.9% | 19.6% |

| INDIANAPOLIS-CARMEL-ANDERSON, IN | 13,459 | 16.4% | 10.9% | 18.0% |

| GREENVILLE-ANDERSON, SC | 4,161 | 16.3% | 10.8% | 17.5% |

| WINSTON-SALEM, NC | 3,184 | 16.2% | 10.5% | 15.3% |

| CAPE CORAL-FORT MYERS, FL | 4,345 | 16.2% | 11.7% | 21.6% |

| SACRAMENTO-ROSEVILLE-FOLSOM, CA | 6,470 | 16.2% | 11.9% | 13.2% |

| CLARKSVILLE, TN-KY | 1,398 | 16.2% | 10.4% | 14.5% |

| DES MOINES-WEST DES MOINES, IA | 2,874 | 16.1% | 10.5% | 10.8% |

| SALISBURY, MD-DE | 1,603 | 16.1% | 10.5% | 10.9% |

| TOLEDO, OH | 2,654 | 16.1% | 10.9% | 14.1% |

| COLUMBUS, OH | 10,082 | 16.1% | 11.0% | 13.6% |

| DAPHNE-FAIRHOPE-FOLEY, AL | 936 | 16.1% | 11.0% | 12.1% |

| MINNEAPOLIS-ST. PAUL-BLOOMINGTON, MN-WI | 13,747 | 16.1% | 11.5% | 11.2% |

| WARREN-TROY-FARMINGTON HILLS, MI | 9,975 | 16.1% | 10.7% | 11.7% |

| SCRANTON–WILKES-BARRE, PA | 2,344 | 16.0% | 10.7% | 21.5% |

| MILWAUKEE-WAUKESHA, WI | 3,969 | 15.9% | 11.2% | 8.1% |

| SYRACUSE, NY | 3,366 | 15.8% | 10.6% | 16.4% |

| READING, PA | 2,340 | 15.8% | 10.4% | 23.7% |

| FLINT, MI | 2,075 | 15.7% | 10.2% | 21.3% |

| SEATTLE-BELLEVUE-KENT, WA | 5,129 | 15.7% | 11.7% | 7.5% |

| FORT WAYNE, IN | 2,360 | 15.7% | 10.1% | 15.6% |

| OGDEN-CLEARFIELD, UT | 3,104 | 15.6% | 10.1% | 15.6% |

| NASHVILLE-DAVIDSON–MURFREESBORO–FRANKLIN, TN | 9,956 | 15.6% | 10.0% | 16.7% |

| SANTA ROSA-PETALUMA, CA | 474 | 15.6% | 11.4% | 6.6% |

| CHATTANOOGA, TN-GA | 2,842 | 15.6% | 10.1% | 18.5% |

| FORT COLLINS, CO | 688 | 15.6% | 11.0% | 8.8% |

| CINCINNATI, OH-KY-IN | 11,007 | 15.5% | 10.4% | 15.5% |

| KILLEEN-TEMPLE, TX | 1,822 | 15.5% | 10.1% | 12.8% |

| DELTONA-DAYTONA BEACH-ORMOND BEACH, FL | 3,551 | 15.5% | 10.3% | 22.4% |

| PALM BAY-MELBOURNE-TITUSVILLE, FL | 2,719 | 15.5% | 10.7% | 17.7% |

| KANSAS CITY, MO-KS | 10,405 | 15.4% | 10.1% | 15.3% |

| HUNTSVILLE, AL | 2,332 | 15.4% | 9.6% | 12.3% |

| BOULDER, CO | 398 | 15.4% | 11.3% | 4.5% |

| LOUISVILLE/JEFFERSON COUNTY, KY-IN | 6,866 | 15.4% | 10.2% | 16.2% |

| BAKERSFIELD, CA | 5,080 | 15.4% | 10.4% | 26.5% |

| SAN FRANCISCO-SAN MATEO-REDWOOD CITY, CA | 117 | 15.2% | 11.7% | 0.8% |

| ALBUQUERQUE, NM | 5,701 | 15.2% | 10.0% | 21.1% |

| MYRTLE BEACH-CONWAY-NORTH MYRTLE BEACH, SC-NC | 1,656 | 15.2% | 10.1% | 10.1% |

| SALT LAKE CITY, UT | 5,012 | 15.1% | 10.0% | 15.2% |

| PHOENIX-MESA-CHANDLER, AZ | 19,302 | 15.1% | 10.3% | 15.6% |

| NORTH PORT-SARASOTA-BRADENTON, FL | 2,802 | 15.1% | 10.8% | 14.3% |

| TALLAHASSEE, FL | 1,498 | 15.1% | 10.6% | 15.2% |

| PUNTA GORDA, FL | 775 | 15.0% | 10.5% | 16.4% |

| ROCHESTER, NY | 4,917 | 15.0% | 10.1% | 14.3% |

| ASHEVILLE, NC | 778 | 15.0% | 10.0% | 8.1% |

| COLORADO SPRINGS, CO | 2,560 | 14.9% | 10.3% | 10.7% |

| PENSACOLA-FERRY PASS-BRENT, FL | 1,950 | 14.9% | 10.0% | 13.3% |

| GRAND RAPIDS-KENTWOOD, MI | 3,407 | 14.8% | 9.4% | 10.5% |

| AKRON, OH | 3,375 | 14.7% | 10.2% | 16.4% |

| ANCHORAGE, AK | 1,685 | 14.7% | 10.6% | 13.9% |

| OMAHA-COUNCIL BLUFFS, NE-IA | 4,085 | 14.7% | 9.5% | 11.5% |

| PITTSBURGH, PA | 9,793 | 14.7% | 9.6% | 14.9% |

| MODESTO, CA | 2,072 | 14.7% | 10.0% | 21.6% |

| PORTLAND-VANCOUVER-HILLSBORO, OR-WA | 5,196 | 14.7% | 10.8% | 10.6% |

| MADISON, WI | 667 | 14.7% | 9.8% | 3.8% |

| TUCSON, AZ | 4,464 | 14.6% | 9.6% | 16.5% |

| WILMINGTON, NC | 854 | 14.6% | 9.7% | 9.3% |

| YORK-HANOVER, PA | 2,563 | 14.5% | 9.6% | 20.7% |

| OCALA, FL | 1,462 | 14.5% | 9.7% | 21.5% |

| PROVO-OREM, UT | 1,950 | 14.5% | 9.6% | 13.4% |

| YOUNGSTOWN-WARREN-BOARDMAN, OH-PA | 2,271 | 14.5% | 9.8% | 20.7% |

| DAYTON-KETTERING, OH | 4,021 | 14.4% | 9.2% | 16.2% |

| KNOXVILLE, TN | 3,441 | 14.3% | 9.1% | 15.9% |

| BUFFALO-CHEEKTOWAGA, NY | 4,873 | 14.2% | 9.5% | 14.0% |

| MANCHESTER-NASHUA, NH | 1,338 | 14.2% | 9.6% | 13.8% |

| FRESNO, CA | 3,547 | 13.9% | 9.2% | 19.7% |

| CANTON-MASSILLON, OH | 2,001 | 13.9% | 8.9% | 19.7% |

| BOISE CITY, ID | 2,639 | 13.8% | 9.0% | 11.9% |

| LANSING-EAST LANSING, MI | 1,945 | 13.7% | 8.7% | 14.6% |

| HARRISBURG-CARLISLE, PA | 2,341 | 13.7% | 8.8% | 15.4% |

| LANCASTER, PA | 1,785 | 13.7% | 9.1% | 13.5% |

| BEND, OR | 367 | 13.4% | 9.9% | 9.3% |

| CRESTVIEW-FORT WALTON BEACH-DESTIN, FL | 681 | 13.3% | 8.7% | 8.0% |

| VISALIA, CA | 2,191 | 13.0% | 8.3% | 29.4% |

| KALAMAZOO-PORTAGE, MI | 815 | 12.9% | 8.5% | 13.5% |

| LEXINGTON-FAYETTE, KY | 1,702 | 12.8% | 8.3% | 13.0% |

| SPOKANE-SPOKANE VALLEY, WA | 1,724 | 12.6% | 8.6% | 11.9% |

| EUGENE-SPRINGFIELD, OR | 777 | 12.6% | 9.0% | 12.3% |

| SALEM, OR | 1,176 | 12.5% | 8.8% | 15.7% |

| PANAMA CITY, FL | 572 | 12.5% | 7.9% | 15.4% |

| SPRINGFIELD, MO | 1,587 | 12.4% | 7.7% | 14.7% |

| PRESCOTT VALLEY-PRESCOTT, AZ | 493 | 12.0% | 8.0% | 12.9% |

| RENO, NV | 1,083 | 11.9% | 7.8% | 12.8% |

| FAYETTEVILLE-SPRINGDALE-ROGERS, AR | 1,850 | 11.6% | 7.2% | 13.5% |

| LAKE HAVASU CITY-KINGMAN, AZ | 461 | 11.1% | 7.3% | 13.5% |

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Staggering numbers. What say ye about that, housing shills?

“It is difficult to get a man to understand something when his salary depends upon his not understanding it.”

NAR (National Association of Realtors) said in its 2007 publication.

“While prices have softened a bit, this has never been a better time to buy a home”

I get this magazine quarterly. It is without a doubt the most sordid piece of garbage propaganda that has ever made it into the print media.

You mean Lawrence Yun is not looking out in my interest when he’s been telling me since 2006 inventory is low and the market is not build upon a bubble?

The fact that his bio on the realtor site describes him as “Dr. Yun” says all I need to know about him.

In my experience, every single non-medical doctor/dentist/vet/etc. who refers to himself as “Dr.” is a huge tool.

Lawrence Yun is a jackass

I think I still have a few bumper stickers saying “It has never been a better time to buy a home”. From 1986.

Amen. This was to be expected and is in accord with anecdotal evidence. Other types of mortgages are likely in similar states, albeit this type of federally guaranteed mortgages are likely to include more persons with lower incomes who are more likely to be in default due to limited resources.

That means that (aside from mortgages that are guaranteed by the government) the other mortgages (even if they have lower rates of defaults) have made the banks legally insolvent if they were not legally insolvent already in 2019 as indicated by their $2 TRILLION in MBS purchases by the “Fed”: their net capital after liabilities, has now been wiped out by their losses on these mortgages.

Since they were circumventing the US rules for a long time by gambling on derivatives through foreign subsidiaries, I wonder just how much in the negative the major US banks have gotten now? See “Regulatory arbitrage and the G20’s global derivatives market reform” in voxeu and reports by Wall Street on parade that their exposures are in the hundreds of TRILLIONS, so they really cannot be bailed out anymore.

The derivatives numbers listed in this website are so large that I do not know if they could be true: I suspect that banks’ total derivatives exposures are their little secrets, because they have been making a mockery of the post 2008 “reforms” which made deposits reachable by banks if the banks failed and did not really provide any protection from bank failures.

The rules now say that the rest of the credit unions and even smaller, legitimate banks will lose all of their funds to help bail out the larger ones if one of those gigantic banks goes under. I will say nothing about the other “protections.”

The US Office of the Comptroller of the Currency (OCC) reports quarterly on the banks’ derivative trading and holding. And yes, the notional amounts are huge. Here is the last one for Q4 2020:

https://www.occ.gov/publications-and-resources/publications/quarterly-report-on-bank-trading-and-derivatives-activities/files/q4-2020-derivatives-quarterly.html

So, should I pull my money out of my credit union? I have been thinking about doing that, but am uncertain where to park it while I wait for home prices to come down or foreclosures to tick up.

Somehow, I don’t think it is really safe anywhere aside from hard assets, perhaps.

How to have affordable housing.

Get government completely out of the mortgage business.

Interest rates at 6%.

20% down.

Banks eat their bad loans.

actually during depression – no bankster loans were available

and people paid cash for home

price was cheap

and NO GOVT PROPERTY TAXES – meaning you actually owned home

Income and property taxes are theft.

And what do you call the highways, health care system, military protection, education, environmental protect services, policing, court admin, etc etc etc….Charity?

I have never minded paying my fair share of taxes and have done so my entire life…sometimes 40%. But then again, I have never had a medical bill, either.

Everyone wants something for nothing, just because.

You’re not even in my country. Next….

I am in “your” country…..

And what do you call the highways, health care system, military protection, education, environmental protect services, policing, court admin, etc etc etc….Charity? Are you going to get your healthcare in Libertarian Paradise Yemen?

I thought Somalia was the libertarian paradise and home to unfettered capitalism.

We need to shrink government by 1/2, minimum. We are suffering from bureaucratic strangulation and over regulation. I believe in a consumption tax, and that’s all.

Agree, like totally dudes and dudettes, with Paulo on this one!!

Richest guy I ever knew well told me more than once that I should be happy and proud to pay taxes, as that was supporting the ”system(s)” that made it possible for folks from the middle and lower classes, definitely including him and me at that point, per G&S’s ”bow bow you lower middle classes, bow bow you tradesmen, bow you masses… ” be able to become rich as he had.

Works for many and many of folks who are willing, able, and ready to work hard for some period of their life IMHO, as I watch youngsters I know doing it right now, starting with literally nothing at all from family, etc.

If you want to read about how a world with no taxes would be, suggest you check out, ”Islandia” by Austin Tappen Wright IIRC.

Or just read about old times in various European and UK countries where the vast majority paid no taxes,,, etc…

Propaganda on all sides exists now, with out regard to reality!

Anyone who thinks they are getting their monies worth for the taxes they pay has simply not actually studied the return the taxpayer gets on their dollar.

There is also the issue of voluntary taxes such as fuel taxes, which by the way are what pay for the roads, which are moral because the taxpayer has the choice to buy the products or not, and forced taxes such as income taxes and property taxes which are immoral because they basically are theft by force.

In 1946 the Chairman of the Federal Reserve Bank of New York Beardsley Ruml in a speech to the American Bar Association stated that the need for taxes to support the Federal Government ended when the government ceased to exchange dollars for gold. The Federal Government has no need of taxes to fund itself. He went on to state that the purpose of taxes in our modern system was primarily to control “wealth distribution” and to control inflation and deflation.

“If you want to read about how a world with no taxes would be…”

I don’t recall anybody talking about “a world with no taxes.” It’s always knee jerk hyperbole when I mention anything other than the status quo. I was simply talking about real estate and income tax. I favor a consumption tax and a massive shrinking of this bloated cesspool we call government.

We could cut the entire federal government by 50% or more and you wouldn’t notice a thing. That’s one reason T lost. He didn’t drain the Swamp. He didn’t even try.

Prices were super cheap in the 70s and 80s too.

Prime rate at 20%, no federal guarantees to mortgages and banks ate their bad loans.

Not sure where you are getting your information but it is wrong.

The 70’s and 80’s were a time of mass inflation in many places which priced many people out of the housing market.

In San Diego average house prices went from about $19K in 1969, to $40K in 1975, to $100K in 1980.

Most “late boomers” I knew were never able to afford a home until their late 30’s early 40’s.

my first mortgage was at 17%, look up a mortgage calculator and see what it does to your payments

Mortgage rates got up to 18% back then, 1982. I would like to see those rates once again. Savers were compensated for inflation and devaluation. Now savers are fleeced to subsidize all the Wall Street shills and the crooked Banking Industry.

” NO GOVT PROPERTY TAXES” is not true. Taxes on real estate predate the American Revolution.

There have always been taxes, from the time of Kings. Actually from the time of warlords. Those that manage control of violence set the taxes.

You wrote the Fed can’t raise rates because it could be afforded.

Now you write 6% interest.

How it that possible you say 6% interest when you you previously wrote 3% was Unpossible?

How to have affordable housing.

Get Wall Street and other speculators and gamblers completely out of the housing business.

These days, who’s buying a home to actually live in it?

“K-shape recovery” is a sign of predatory behavior; and that’s an indication of economic collapse, not of a recovery.

I’m tired of so many urban planners not figuring in land speculation in housing costs. All I hear is “supply supply supply!”.

I mean I hear so much from Wolf about crazy amounts of money in the markets right now…that same money & drive for profits also impacts housing prices. There’s just no way that relying on markets to fix housing affordability is gonna happen. If we want housing for poor & working class people, we need to decommodify housing.

Housing market is certainly a complicated market where there are local, state and fed officials with fingers in the pie plus brokers, lawyers and bankers. Makes it very difficult for consumer to meet the most basic needs of a safe refuge. It’s a transaction we do so rarely, most are not good with it. Plus if local situation is bad you have to leave friends and family behind to get out of it.

Saying that, educating ourself about the market, how to do accurate rent vs buy comparisons and being willing to vote with our feet are tools we can use to not be a price taker.

Repurpose empty offices,stripmalls,warehouses,churches,whatever.

Agreed

Most homes are now bought for speculation not as place to live. The only way to stop this is to stop the government from subsidizing mortgages and let the rates achieve free market levels. Privatize the entire mortgage financing industry. Abolish the FHA, FNMA completely. Give Vets a voucher to buy their starter home and get rid of the entire VA home financing infrastructure. Required 20% down payment. Stop allowing mortgage interest deductibility for second homes. Restore SALT and full deductibility of Mortgage interest and taxes for owner occupied homes. Encourage home ownership but discourage home speculation.

“Most homes are bought for speculation” the spanner in the works sadly.

We have homeless persons sleeping in cars outside houses, flats & units that are empty & not for sale to the public.

Hooray for negative gearing.

I was 10ish & lived in Carlton Nth, Victoria, full of hard working & saving Italians, the government opened up Fawkner, Campbellfield & further for housing development & the upwardly mobile Italians purchased land & built. The abundant Jewish population moved to Caulfield.

This is when housing took on cost, before that a house in Nth Carlton, or anywhere for that matter was as cheap as chips .. this was the 60’s – 70’s & here we are today.

Most housing was owned by government .. derelict rentals .. not much home ownership.

How is a struggling homeowner wannabe affording %6 rather than 2 or 3?

Amazing. Looks like 2008. 2 heading the world’s way.

BTW: here are the Canadian rates for 2020 Q3

Delinquency rates are steady across Canada at 0.3%. Montreal continues to trend under the national average. Toronto and Vancouver maintain a flat rate, much lower than national average, at 0.12% and 0.16%, respectively.

So although the market sure looks frothy I guess the Crash won’t start here. Do all those US folks not have much equity to protect?

nick kelly,

You need to look at the weakest segment of the market. That’s where the problem arises, the bottom 10% or 20%. Overall delinquency rates in the US are low too, but 80% of the homeowners will never get in trouble anyway. Subprime is the bottom of the credit scale. That’s where you have to look. That’s where things began to fall apart last time.

Aren’t many of the locations listed vacation areas?

LongtimeListener,

Atlanta, Houston, Dallas, Chicago, Baltimore… Have a look at the table of the 10 most at risk metros. I don’t see any particular “vacation areas” among them.

Barnstable, Bend, Miami…

LongtimeListener,

They’re not in the top 10 most threatened metros (see first table). You picked them out of the biggest 169 metros. And in Bend, the FHA share is only 9.3% and the delinquency rate is only 13.4%. It’s toward the bottom of the list… meaning, one of the least threatened metros!

And Barnstable is minuscule little place with just a tiny number of FHA mortgages.

Bend, OR is not a “vacation destination” per se, but it IS SPECULATION CENTRAL. CA equity locusts love to run up there in their Lexus eggs and run up the prices. Ditto Ashland, OR.

I went for a vacation in Baltimore. It was a riot.

Well, you know I always agree with you but I REALLY agree with this. I’m seeing this first hand. The people who are at the lowest fringe of the market, who are coming into it with $20,000 they have worked to save over the last 15 years, they are the ones in the neighborhoods where no one wanted to live a year ago. And the prices now are 20-25% higher than they were pre-covid.

The working class and minorities are again going to get swept away in this. It’s so hard to watch. I’ve asked several clients to take a break from their search.

I mentioned that my mom’s cul-de-sac was a foreclosure wasteland last bubble. It inflated to almost 10x median household income. It’s much worse this time.

When I went to visit her last bubble, I noticed that the quality of the neighbors and their vehicles had actually gone DOWN while the prices had gone up. It was strange. The math seemed a little funny. Turns out it was. They were all sent packing by the bank.

Good advice

So there wasn’t much tightening after the GFC?

I can see US probs being 5 times Canada’s, but it looks like 40 to 60 times.

That’s because those at the top of the scale get bailed out.

The government owns the upcoming housing foreclosure crisis. I know many people struggle to make payments on their home directly because of the GOVERNMENT. And I live in an upper middle class community. I’m talking about attorneys too, some with student loans. Never missed payments ever!

It is sad and outrageous that these people were kept away from earning their keep. We are looking down the barrel of a very serious problem. And it’s not their fault, not even a bit.

“It is sad and outrageous that these people were kept away from earning their keep.”

yes, it is. and it’s just the tip of the iceberg. and as for a lot of those in the subsurface part of the iceberg,” it’s not their fault, not even a bit” either.

welcome to the precariat. the water’s great.

A hidden but valuable statistic could be the number of people in unnecessary forbearance despite having the cash. The number could be higher than we think, as alluded in your recent article about revolving credit being historically low.

I wonder if the G crossed checked gvt program delinquencies/defaults against recipients of past year’s grants and netted out the grants for arrears.

I doubt it, but it would have been easily achievable.

I don’t buy it. Nobody who can afford their house starts playing chicken with the bank.

Sure they do. I saw it first hand with several people I worked with. I mean what’s the bank going to do? As the saying goes, if you owe the bank $10,000 you’ve got a problem, if you owe the bank a million the bank has a problem.

I have always wondered if I was a homeowner and early into a 30 year, could I tell the bank I needed a year forbearance even though I have a job? The bank tacks it onto the end of the loan and I take all the would-be mortgage cash and dump it into the principal 2 months after I start paying again. That would easily wipe out the year of interest off the back of the loan? The only way I can see this wouldn’t work is if the bank made you pay off the forbearance interest before any extra principal payments.

That’s how it works. You pay the bank’s interest first and then you pay the principal at the end.

The forebearance gets added as a balloon payment to the end of your loan. Not a big deal for millennials with 30 year mortgages but boomers with 1-2 years left on their mortgage could get hit with a 12 month balloon payment all at once.. next month.

That’s the worst case scenario and worst case scenarios never happen in housing, right?

Jacklyn, what you describe is only one of multiple possible outcomes.

Have you never read Michael Hudson’s “THE BEST WAY TO STREAL FROM A BANK IS TO OWN IT”

I think you meant “The Best Way To Rob A Bank Is To Own One” by William K. Black. He is an ex regulator.

Hmm, you mean like a cheap bridge loan to buy their next house?

I hope no one purchases the plywood 500 sq ft shack with no clear access rights to public roads for $200k in my town. Maybe it comes with deeded right to construct a lane entitled “GameStop” that connects to the city street.

Take a video of it and sell it as an NFT.

Does the data you show take into consideration of all COVID forbearance? Because all Government-backed loans had specific instructions on how to handle the delinquencies for borrowers who requested for forberance.

Yes, loans there were delinquent when they entered forbearance are included here as “delinquent.” Loans that were not delinquent when they entered forbearance are not included.

Wolf,

So does that mean a huge number of houses may have become essentially delinquent but not counted as such during the past yr’s C19 forbearance/moratorium?

So the above stats may be seriously undercounting the number of homes likely to end up delinquent/defaulted?

No, the above stats are accurately counting delinquent mortgages. Every FHA mortgage that was delinquent when it entered into forbearance is included as delinquent.

You are asking if there is an accounting problem with delinquent numbers being under reported? Yes. Delinquent is an accounting definition that means you cannot pay your loan. Just because the government is trying to hide your loan behind a curtain doesn’t mean it escapes accounting definitions.

Doesn’t that indicate that the problem is infinitely worse? Or am I misunderstanding?

Wolf,

Any data on the delinquency rate for conventional and VA loans for the 4th quarter, 2020? Many homes in the Swamp are purchased via conventional loans because the prices are so high they exceed the FHA limits.

I know this isn’t what you’re asking, you want to know about existing VA loan statuses, but, I can’t get a VA loan accepted right now on offers to save my darn life. No one will take them.

I sold a house to a guy with a VA loan once. After inspection they tried to tell me that the wrought iron railing was not acceptable and that it would need to be replaced. I told them to pound sand and that I’d go with an even higher offer waiting in the wings. Suddenly the wrought iron railing was fine. Weird. Circa 2006, btw.

They aren’t that bad now. It’s an easier process. But, not being able to waive the appraisal or financing piece is the killer for those buyers.

Interesting comment that alludes to more high weirdness in this feeding frenzy housing bubble, to wit:

–sellers now hold all the cards and with multiple offers on their property they can snub buyer offers that include conventional contingencies like a traditional home inspection, and allowances for remedying defects found in seller’s house.

It is reported that buyers are even purchasing houses without ever stepping foot on property. I smell a lot of future buyer’s remorse wafting in the wind … ‘Buyer Beware’ is so old school now.

Madness of crowds …

Nothing has changed in 40 years. When I bought my first home they wouldn’t take a VA contract even though I was entitled to it. The realtor didn’t even try. Went conventional. I had to drain my entire savings to make the 20k down payment. The people in the Swamp have no respect for the military nor Vets. And neither do most Realtors. Sorry to break the news to you, but its true.

The problem probably wasn’t a lack of respect for veterens, but the problem of getting an older home through a VA or FHA inspection. Most first homes are older homes which always need some work done to them and will not pass the strict inspection.

I’ve been trying in San Diego with a VA loan and zero luck. I took a break finally after 6 months

Why would they sell if they can live in it for free until the Gov decided to man up & stop the scamming, I bet their train of thought is live free in the home & dare the Gov pull the rug.

I think a lot of people did this in 2008, if I remember correctly a couple said they stayed in their home many many years without paying anything because no one knew who owned the mortgage, I think they they stayed 5 years, the scams were so enormous that they didn’t even know about the home, the scams are even worse now, I bet the holders of these guaranteed mortgages are drowning in so many mortgages they do not even know what they own & were it is.

This is another reason why people have so much extra to spend, what’s to stop many more people joining them and choosing not to pay & just spend or save the cash for a new home, this is what happens when Gov stick their noses in markets & refuse to deal with reality, until reality deals with them that is.

While few people acknowledge it today, moral hazard is a very real thing. If you create an environment in which it becomes profitable to ignore ethics and morals, then a certain percentage of the population will do just that.

The result will be that you change culture, and the behavior of people within that culture.

If you tell people they do not have to pay their debts, or you pay them more to stay unemployed than to work, that will influence their ethics and their behavior.

“I’m talkin’ about friendship. I’m talkin’ about character. I’m talkin’ about – hell. Leo, I ain’t embarrassed to use the word – I’m talkin’ about ethics.”

—Johnny Caspar

Is the dole in the US higher than wages ??

In Australia you get to struggle & develop depression on the dole payment.

1 in 5 kids has gone hungry in Australia in the last 12 months.

We have approx: 60,000 charities in Australia.

Charities are not any kind of efficient, effective solution to poverty & other social problems .. but money wasting .. dysfunctional parasites feeding off the Australian people.

Reality & not romantic notions need to be put in place.

So kill me for saying what is true.

“Is the dole in the US higher than wages ??”

MUCH higher right now, so people will not apply for jobs and the “NOW HIRING” signs are everywhere. It’s disgusting, and it’s creating a class of freeloaders.

What is different this time is 96% of all mortgages that have originated since 2010 are guaranteed by the GSEs. So they are probably a pretty good investment even the house is in forbearance?

My questions, is most of the banks are just servicing loans. So who is the lender to make decisions on if the loan can be modified or if the home owner has to make up payments? Is it Freddie and Fannie?

They were scheduled to end FHA mortgage forbearance before, then extended again until June if I am not mistaken. There was also an idea about restructuring mortgages to make the payments smaller and payback period longer. Not sure what Congress will do.

The pandemic is disrupting supply chains at home and abroad. Builders sold homes that have not been built yet. Housing inventory is low. Illegal immigrants are flooding across the border. The Federal government is putting some of them in hotels. English speaking homeless Americans are not allowed to pitch a tent on the mall in DC. What will a wave of foreclosures and evictions bring?

That’s a lot of different subject you explore in a few paragraphs, as far as immigrants are concerned I do not know exactly where you got the idea they are put in hotels, last I heard the are in put in terrible conditions & separated, be careful what you believe, when it comes to immigrants people love to get people into a frenzy, painting a picture of how they cross the border & get treated like VIP’s, it’s never true, just the opposite.

As far as dents on the mall in DC, the problem isn’t were they can pitch a tent, the problem is having to live in a tent in the first place, link that to ya forbearance comment, so those who default get to live free in a home & those who are homeless stay homeless in a tent, congress needs to practice what they preach, deal with the reality instead of scamming & hiding problems.

Jack,

There is a thing called a “search engine” to bring you up to speed of using taxpayer money to put llegal immigrants in hotels

Biden Admin. Spending $86.9M to House Illegal Alien Families in Hotels

Who do you think paid for all those T-shirts with Biden’s name on them? Obviously something made these people think that something drastic had changed in US illegal immigration policy.

Whatever,

You say there is a thing called a “search engine” but fail to realise how a search engine works, a search engine will find WHATEVER you want it to, have a think about that, if you want anti immigration content you will find it, if ya want positive immigration content you’ll find that to, all I said is be careful what you believe, You said nothing about the homelessness I talked about.

People in the US should take note that they are all immigrants or children of immigrants, the US itself is responsible for most of South America’s ill & drug gangs, Biden spending $86.9M hey, are you kidding, the US just spent $7 trillion for 1.9 GDP growth, spending 7 trillion to gain 300 billion in GDP should be on ya mind & not a tiny $90 million, the US Gov probably spend that amount on paper clips every year.

Where do you think they go when they are released? Straight to the Social Services Dept. for their tax payer funded “entitlements”.

You might to go check the stats. There’s a surge at the border every year at the same time and the # of people in 2000 were over twice what they are now.

Whether or not the border situation is a “crisis” depends on if Fox “news” can drudge up anything real to complain about or not. Tucker Carlson and the other professional liars deciding it’s a “crisis” doesn’t make it one.

As with almost everything else, look at the historical data on your own and you’ll find out it’s much ado about nothing.

Is it a problem? Sure. But it’s way down the list below the pandemic deaths, unemployment, failing healthcare/educations systems, 1% robbing everybody else, etc, etc, etc.

A poverty stricken person from Central America who doesn’t speak English, fleeing gang violence and starvation isn’t your biggest problem.

Well said. Thank you.

i second this.

Do you have an acceptable number of illegal immigrants in mind? 1 million? 5 million? 100 million? Open borders means OPEN.

The borders arent “open”. People have a legal right to apply for asylum.

Biden said he wouldnt let a child starve to death outside our border. Thats a moral and humane stance that I support.

If u want to know why somebody would walk 1,000 miles to an uncertain future, risking violence and death, take a look at what US policies have done to Central and S. America.

Stop letting Tucker and Sean Hannity tell you what your biggest problems are.

If you read this site, you know Wall St-Bankers-DC-Big Pharma-MID-1%ers have ruined the USA more than some poverty stricken starving Central America refugees could in a 1,000 years.

600 million people want to come to the USA. Get real.

“The borders arent “open”. People have a legal right to apply for asylum.”

Yes, they most certainly ARE, which is why the previous admin was working to build a wall.

Her name is Kamala. You’re being disrespectful and you being a person of color, I would expect more from you.

TCK,

I am a Latina, but not a person of color. As a Hispanic, I don’t officially have a race in America. And I meant what I said.

“I am a Latina, but not a person of color. As a Hispanic, I don’t officially have a race in America.”

But you are an equal opportunity racist. Dependably so. You never disappoint.

NDRL:

Do a search on “Gila Bend Arizona state of emergency”. It is a “crisis” for a town of 2,000.

Maybe Border Patrol should bus them to Wilmington, Delaware….

Bus them to the Hamptons, Palm Beach or Aspen.. there’s plenty of empty bedrooms and big hearted folk.

Carlie, you should start a go fund me.

So according to you, if illegal immigration (migration) is not really a priority problem in overall context, the logical next step is to have true open borders to all comers (seems to be current admin’s plan), as long as they are fed and housed properly at taxpayer expense?

Just who do you think would take care of these indigent 3rd world denizens?

I’m guessing that the concerned social justice warriors are going to take them into their homes and put them up in the guest room until the paperwork comes through.

Who would Jesus turn away?

In the past 10 years, visa overstays in the United States have outnumbered border crossings by a ratio of about 2 to 1, according to the Center for Migration Studies.

These people are not “indigent third world denizens”, but I apologise for disrupting your feverish fantasies. Pegging an “illegal” immigrant by country of origin and race is convenient, but not accurate. I personally know a couple of Irish and one Russian person who is illegal because they have overstayed their visas.

Idaho potato,

People overstaying their visas doesn’t negate the unfolding crisis on our southern border with literally thousands of unaccompanied minors flooding north from central America. What is your solution? This is a humanitarian crisis and Biden encouraged it.

“So according to you, if illegal immigration (migration) is not really a priority problem in overall context, the logical next step is to have true open borders to all comers (seems to be current admin’s plan), as long as they are fed and housed properly at taxpayer expense?”

sick logical fallacy bro. you’re a real genius

Yo, C Kid – just refer to it as President-in-Waiting Harris.

The crisis in Central America was Made In USA. Has everyone forgotten about Major General Smedley Butler, USMC?

“I helped make Mexico, especially Tampico, safe for American oil interests in 1914. I helped make Haiti and Cuba a decent place for the National City Bank boys to collect revenues in. I helped in the raping of half a dozen Central American republics for the benefits of Wall Street.

The record of racketeering is long. I helped purify Nicaragua for the international banking house of Brown Brothers in 1909-1912 (where have I heard that name before?). I brought light to the Dominican Republic for American sugar interests in 1916. In China I helped to see to it that Standard Oil went its way unmolested.”

— War Is A Racket, 1935

The actual stats for February are 36,687 for 2020, and 100,441 for 2021. Hate to disagree with you, but those numbers obviously indicate the problem is much worse. In addition, the majority of illegal entries in 2020 were returned, where as the vast majority of illegal crossings in 2021 will be allowed to stay…. That is why they are coming. If you reward people for doing the wrong thing, that is what they will do.

Anyone who thinks that the Federal Government putting the interests of people in Central America ahead of the interests of the American Citizens is moral or ethical, really does not understand the relationship between the government and the people.

There is no surge: ” CBP has recorded a 28 percent increase in migrants apprehended from January to February 2021, from 78,442 to 100,441. News outlets, pundits and politicians have been calling this a “surge” and a “crisis.” … the CBP’s numbers reveal that undocumented immigration is seasonal, shifting upward this time of year. During fiscal year 2019, under the Trump administration, total apprehensions increased 31 percent during the same period, a bigger jump than we’re seeing now. We’re comparing fiscal year 2021 to 2019 because the pandemic changed the pattern in 2020. In 2018, the increase is about 25 percent from February to March — somewhat smaller but still pronounced.”

I read that there has been 482k apprehension of people trying to illegally enter the country the end of February for of this year. Yearly averages for the prior 3 years was about 700k.

I think the January and February usually has a lot because the temperatures are not as high in the summer. But unaccompanied children for YTD end of February is up 94% from last year and single adults is up 188%.

https://www.cbp.gov/newsroom/stats/southwest-land-border-encounters/usbp-sw-border-apprehensions

Biden said, in a flattering tone, “they are coming because they know he is a nice guy”. ;)

Incorrect. These numbers are widely reported and 2021 is worse than they last 5 years by a large margin. There is a humanitarian crisis at the border that isn’t about politics, it’s about thousands of unaccompanied minors flooding north because they perceive the border to be open. You can say what you want about the prior administration, but they did certainly address this problem rather than encourage people to rush the border. What is your solution?

here’s an idea: sponsor an immigrant and waive the fee for renouncing citizenship. add in some sort of bonus, like paying the fee to relocate vanuatu or some other such palm greasing endeavor, and i would happily take advantage of the program.

open borders are good, so long as everyone plays by the same rules. it amazes me that people still want to come here in the first place. i would be beating a path out the door if it was feasible for someone of my means.

Revolution? :-)

One other thing is why are Americans behaving like this virus has gone? It seems to me everyone is celebrating & lowering their guard like it’s over, it’s pretty amazing to see, especially with the fact the US is the worse in the world for cases & deaths, this is a grave error, cases are marching higher & the B117 as well as other variants are spreading fast, these variants will cause untold misery, take the B117, it’s lightning fast & deadly efficient.

The cases are already rising fast, the US is testing little, the numbers are back to 70k & rising, people catching flights, partying, opening everything up, not taking precautions, the B117 makes the original look like a wimp, why are people so cocky, it’s gonna be devastating, it will make 2020 look mild, the vaccine will have zero effect in my opinion, not with so many powerful variants.

So whether it’s the hyper stock bubble, hyper property bubble, or all the other bubbles, the pin is on it’s way, to go from believing it’s over to thinking it will never end will be a mental hammer to the head blow, or is it me?? Lokk at what the Uk went through with B117, look at Europe now who were to casual a few months ago. Brazil is another example to, hell I can list 50 countries as examples.

Maybe the Deagle 2025 population estimate isn’t BS? I was skeptical but now I’m having doubts….

the dead will be replaced. until they aren’t.

Because instead of bald eagle as our national symbol, we really should change it to cart before a horse. We are a champ at that which answers your question on why we are partying now as if the virus happened back in Spanish flu period..

This is a concern but you have to factor in the reality that the FHFA has given explicit guidance that unpaid principle balances and interest will be recapitalized and the amortization terms extended once forbearance is over. In effect millions of this forbearance homes that are delinquent will be begin making their regular payments again and be cured. I have close friends in the servicing industry and while much of the details about how that will happen remain to be hammered out, servicers are preparing for this now. The flood of instant supply won’t be as catastrophic as this article lays out.

Yep,,that’s why the Fed has been pumping prices for the last year. Creating equity for these troubled owners to use as collateral for a bigger mortgage. And the ones that do end in foreclosure,,the Fed will buy the mortgages, then sell in bulk to Blackstone or whoever.

Wolf,

Thanks for getting the metro list posted so quickly.

Do you think Fannie and Freddie loans are in comparable bad shape (so the “hidden potential inventory” might by 3 to 4x as bad?)

No, Fannie and Freddie have much tighter underwriting requirement. Their delinquency rates are far lower.

Why is Fannie Mae stock worth two bucks now with the new & improved housing bubble, when it was worth 30x as much in 2007?

Fannie Mae is in US government receivership. The US government bailed it out and essentially controls it and takes its cash flow in return for the bailout. The outfit has essentially no capital and cannot stand on its own.

I mean, sure, maybe a SPAC could buy it and drive up its “value” to $1 trillion or something.

I heard fannie is changing policy on April 1 with regard to investment properties. According to what I heard in an interview, their funding will go from 10% of all underwritten mortgages to 7%. Some commented that this may be because they want more money going to individual owners, instead of investors. Others speculated, fannie may be seeing problems in the investment properties portfolios.

As a potential buyer in the future, I like what I am seeing here in this article. However, maybe this is coming in the future, so far SoCal exist in a completely different reality disconnect from this and maybe will so in the future. Lose count of how many listings I saw from Zillow and Redfin, either pending sales with prices bumped up or people asking $1M for a crapshack…talk about a money grab…maybe this will have momentum in SoCal even when the forbearance is over.

No worries, it seems the hyper local numbers are missing. Chicago metro? That’s about 20+ million people, spread out over miles and miles. In my old neighborhood in SE Wisconsin, the housing prices have not at all gone up substantially. Foreclosures left and right, and you can still afford a single family home working a middle-income job ($75K houses been for sale for several years on my block).

The government will do what the bankers tell them to.

List houses very slowly to keep housing prices up.

What kind of disgustingly perverted government tries to make shelter as unaffordable as possible for its people?

A government owned by the rich!

Seriously? If you are looking for morality, the government is the last place you should look…..

assuming you live in the US, the government you currently have. and the one before it. and the one before that, etc.

During the last RE crash, in my old neighborhood an hour south of Tampa, FL, you would see homes the banks owned that sat for years (one sat there for 5 years) before they would go on the market.

You could tell: nobody lived there, home deteriorating, grass uncut, boarded up…. go check the property appraiser’s website: bank owned. They definitely sell ’em off slowly to keep prices from tanking too hard.

Sounds like a rampant mold problem (full disclosure: I own a couple townhomes in FL, BTDT).

I did some calculations right before the housing bubble popped. From my research, about 4 to 5 million excess home unites (homes/condos) were built the prior 4 to 5 years than what growth would support. That really meant it would take at least 4 to 5 years of population growth before we got to a good balance. That was about right 2012 through 2015 was somewhat the bottom depending upon where you lived and the excess.

This time there is no excess. When forbearance ends, there will be a bump in homes on the market but I am guessing the government will try to push workouts first. These people will have to live somewhere, so what will happen. I guess some people who have been saving up and outbid on properties may finally get a very short window but I bet most will be outbid by wall street landloards. We still seem to have a shortage of housing because even though people will be foreclosed on they have to live somewhere.

In the housing bubble people would let their house be foreclosed on and just walk across the street and buy the same type of house for 30% less. They will not be able to do that now. They will have to go find a homeless shelter I guess?

We actually don’t know if there is an excess now. Many units, especially condos in cities and houses in rural areas are just empty and rotting. They were bought as “investments” and stay empty.

And that saying “people need somewhere to live”, while very very true, could end up being a tent.

Really?Homeless shelters are few and far between.Most arent designed for families or petowners,many disallow couples.Men in one area,women in the other.Many people choose their vehicles or tents due to pet ownership,safety,privacy,unusual schedules-shelters have curfews.Many choose these options because of luce and bedbug issues.This country needs more clean,family/pet friendly shelters or minicabins as had opened in Ohio recently.Several very small,but clean units are on leased land with certain amenities.Do not know if there are curfews or other restrictions.People squash together with friends,coworkers,exes,whatever.They sleep in vehicles and migrate to tentcities.They buy an r.v. And pray it doesnt break down or leak.Some squash into residential motels.This isnt difficult to solve if people Want to solve the problem.Rehab unused spaces.You,reading this,prepay for some residential motelrooms maybe specifying that they be allocated to older petowners or families.This can be done in liason with a socialworker-city,county,state,or charity-based. Volunteer with Habitatforhumanity.

They are doing that now. Several houses foreclosed upon in my area. Called bank- not for sale.

OTOH, vandals seem to be moving into some. Fine by me. I don’t mind fixing holes and torn wiring if that’s what it will take to be able to buy one.

Problem is- when some of them are left for 5 years without roof repair or heat, they just fall apart and can’t be fixed. Complete piggish waste.

I suspect you are right.

I have seen properties in various stages of foreclosure (this was before pandemic and imposed forebearance) in my region listed on Zillow for hundreds and hundreds of days. No movement on them (and they did not look like crap shacks).

If banks were serious about cleaning out their pile of REO properties then this zombie property logjam wouldn’t exist IMO.

Some may very well have contested or unclear legal claims.Oldies move into l.t. Care home.Guardianships contested.No will or contested wills=lengthy legal processing especially since covd court closures have backlogged all cases.

Great to see our government and the FED are in lock step to ensure another bubble will never pop as they should and stop any natural cycle from happening. Wouldn’t be surprise if their next step is to ensure elites and powerful will never die too, can kicking and putting cart before the horse seems to be America’s greatest asset.

“Rumors of perma-forbearance are now floating around, given the multiple extensions of the forbearance programs that no one has any political appetite to let expire. But those are just rumors. Eventually, those programs will end, and then the delinquent mortgages will have to be dealt with.”

“Wouldn’t be surprise if their next step is to ensure elites and powerful will never die too…”

Adrenochrome ftw. JK. I’m not a conspiracy type.

I decided to try the baby’s brains….a little mushy but not too bad w/a lot Sriracha!!

Proven! :-) Google chrome server named adeno!

Government destroying then nationalizing all industries. Housing prices are up because Fed is buying all of the mortgage backed securities to suppress borrowing rates. Yes, and FNMA buys most of the loans issued by the banks. Therefore, residential housing is completely subsidized by the government. Not a free market. Will implode when the government decides or fails.

Nationalizing my butt. Those assets will be sold to the lowest corporate bidder the banks own stock in. Like Blackstone.

During the 2008/2009 market collapse, didn’t the GSEs and their USG protectors turn a blind eye to lenders holding millions of homes off the market, and only gradually offering them for sale/resolution?

It’s gonna be much worse than 2008. The corporate defaults added will create a Tsunami of chaos. I am debt free with cash ready to deploy.

same here. still pretty sure i will, as usual, end up holding the wrong end of the stick. but hope springs eternal, and so on. apparently i didn’t have the good sense to but the boots with the good straps.

maybe this time i’ll get it right.

This week mortgage companies selling no $ down FHA loans. Looks like the banks will call Wall Street if they want to unload homes& yes turn into rental. Wall Street needs to get out of rental business . Hopefully, individuals can snap up these homes if in ok shape& good school areas.

These numbers are concerning to a degree, but further extrapolation is necessary here. For instance, the Atlanta metro area makes it sound like it’s one very similar area but it’s not. Unless things have changed radically since I went to college, there is a staggering wealth gap between south Atlanta and the more affluent areas up north like Buckhead, Druid Hills, Sandy Springs, etc. that being said, how much of an impact would delinquent mortgages have on smaller properties in the more impoverished areas of south Fulton County have on the mega mansions in Buckhead? Will the uptick in delinquencies in a poorer area really have that large of an impact on the gated mansion and McMansion communities? I highly doubt your average buyer of those homes are using FHAs.

Also, does anyone really think in 2021 that politicians are not going to use the fed to financially engineer some bailout to kick this can down the road for another decade or so? They want/need the votes and will have little problem with destroying the dollar to maintain/acquire them. Social justice trumps fiscal responsibility in 2021 and will continue to do so for quite awhile. At some point the reckoning will come, banks will foreclose on homes, and these properties will be hoovered up by private equity to become permanent rental properties in some large portfolio. Renting will become the new norm and homeownership will become a luxury only available to the upper 10% of Americans.

Home ownership will become a multi-generational thing as it has been in Europe and South America for quite some time. In the US too when you consider the “family compounds.” Not just the top 10%.

FHA seems to be poster child for most irresponsible government housing agency.

Their mission appears to be to enable the riskiest housing loans to most vulnerable buyers in order to fulfill a goal to get as many people as possible into housing debt.

Wouldn’t be surprised if FHA executives get extremely nice bonuses based on numbers of clueless suckers they can seduce into this market. They appear also to have no shame or remorse for what they are doing, though.

Perhaps FHA has an understanding with .gov that this reckless behaviour is condoned and .gov will be there to bail them out and make them whole when it all goes south.

They just want the houses. The suckers pay the fees and payments for a while.

Fed: Don’t worry. It’s contained.

It ain’t over till John Paulson sings.

He made 30 billion last time, so maybe he’ll make another 30 billion this time.

The big prize of course is the “bankruptcy” of the United States.

Someone, somewhere is working on the Trade of the Millennium. 30 trillion dollars.

Doesn’t that indicate that the problem is infinitely worse? Or am I misunderstanding?

Wolf,

I guess the real question here is will mortgage forbearance (like rental moratorium) ever end. For everyone who says it must, it hasn’t yet. And given the rounds of stimulus, and all the other goodies, the government has created a set of moral hazard that might be as bad as the Fed helicoptering money. After all, our politicians want to keep their jobs.

Yes, there are days when I have my doubts too. Including about the never-ending eviction ban, buttered with billions of dollars in aid for landlords and tenants. No one has any political will to end any of this. Trump didn’t. Biden doesn’t. No one in Congress does.

I think it may all start with the markets, as all markets are based on confidence. Once the markets finally realise, that if they do push forbearance down the line,(again) that everything may fall apart if they don’t. Only then may the markets become super scared (like they sometimes do).. Then, we may see major corrections but don’t count on it because we all now live in La La land and it’s only cartoon brainiacs who can tell us the future……or not. Strange world…

The problem is – if you get scared, where do you run to?

“No one has any political will to end any of this.”

An existential crisis. No adults in the room. Gotta spare people pain, poor things!

It was great while it lasted.

I like Warren Buffet’s saying that if you use phony accounting to deceive your shareholders you will end up deceiving yourself. I think this sums up state of USA economy especially since pandemic. Our economy is too leveraged and the Fed too involved in setting asset prices and we will reach Minsky moment.

I think you can see with gold plus crypto increasing to somewhere around $3 Trillion it’s a vote of no confidence in the Fed.

Maybe they will continue kicking the can down road, maybe not.

Given current observable levels of insane behavior exhibited by people in charge of .gov and economy– anything is possible.

Except this– it is unsustainable and a day of reckoning will come when this lunacy must end (not by their choice but by brute outside force).

What happens in Washington, is a reflection of the morals of the majority of the population. The government only does what it believes it will get away with. If there was sufficient public outrage over forbearance and moratoriums, the government would have to stop it, but there is not.

In the end, the people get the government they deserve.

Everyone complains about government being unethical and immoral, but it is only that way because the public actually supports that.

So long as they are getting bread and circuses in the form of free money do not expect the citizens to demand ethical government.

I guess the pandemic threw a wrench into the plans for the boom/crash. It was supposed to play out slower maybe. But with all the forbearances it sped up time — like in that Star Trek episode where everyone aged fast. So the Fed took advantage of everyone’s fragile emotional state during the pandemic and created a land rush. How many times are they gonna play that Rocket Mortgage commercial during the NCAA tournament? Was Tracy Morgan ever funny? I can’t remember…

Remember the Dietek commercials in 2006/2007? Rocket Mortgage has replaced them, using the same bull S$it propaganda. Ricky Fowler, pro golfer, is even narrating these commercials. After watching that commercial the lemmings are picking up the phone and making deals with crooks.

It doesn’t mean there are not good deals. It means there are very, very, very few good deals- land, you can find good deals in raw land and manufactured homes on rural land; it is interesting, especially over 700,000. There are a lot of arrogant realtors who think a 1million dollar deal means nothing.

I knew a guy who went delinquent on his mortgage in 08. He stayed for 5 years without a payment. The paperwork was a complete mess. Eventually, the bank offered him $10k to vacate. He came back at $25k. They accepted. Banking at it’s finest!

And you forgot to add, his credit was ruined for the next 7 years.

LOL….you would think so but the government came out with a program that if you went to a special program and met with credit fixing / teaching people, and did not have any credit delinquencies for about a year, you could again qualify for an FHA loan with only 3.5% down.

They were trying to give the housing bubble as a free pass…..oops not your fault kind of a thing.

Did the house stay empty for 5 years after that or did someone buy it and move in?

1) The housing market collapse start at the top, plunging in millions of $ per unit. // The next level is in the thousands of $ per unit.

2) Houston : 50K FHA delinquencies // 19% participation rate : many houses are marked for demolition, or damaged beyond repair, because of the floods.

3) Atlanta : 50K delinquencies // 21% participation rate : small payout for loyal voters. They don’t care. The federal gov must pay. They aren’t going to throw them under the bus.

4) McAllen TX 4K // 35%, Lakeland FL 6K // 34% : crumbs.

5) The last 10 dots don’t move. They jumped within 2 months from 11% to 17.5%, because there is no penalty for not paying.

6) The last 3 dots look like a V shape.

7) It might be the lull before the next rise, – slanting up, not a jumping – to the next level, probably to 23% — 25%.

8) The top MSA list is about 300K delinquencies. The bottom, probably another 200K, for a total of about 500K delinquencies. Most units are between $75K to $200K.

9) it make sense to absorb them, otherwise they might protest or join BLM,

or even rise on congress.

10 ) The national guard and DC wall

forced sellers or lenders will put millions of these homes on the market.

Or not,

as because simply there are not millions of sellers being forced to sell.

So the only reason to put a home on the market is for profit.

dUH,

Did anyone jump a board here?

Perhaps the Federal Reserve Bank isn’t wanting to buy the bonds but are doing so in part of their two card switch a roo swindle?

Could it be hard assets like other central bank holdings, real properties, world supply chains, big stuff that these crime families are after?

Me thinks it’s getting very apparent.

Anyone see that new home sales print? -18.2%

That’s gonna be a lot of missing “Recovery” and “Inflation” to look forward to… on top of all this “Extend and Pretend”

Don’t worry folks, there will be a mortgage bailout. None of this ends until Covid is under control. There’s just too many sticking points.

The precedent has been set where we just print money, I mean how much really went to Covid. Total clown world.

That is a significant amount of “low end” inventory which could hit the market. Unlike 2008 where all strata of homes saw price drops, this will be mostly below median-priced homes.

This will be another rung on the ladder of separation between the top 10% and bottom 90%. Median and above homes will hold while the retched refuse gets recycled into rentals….again….but at higher rental rates.

The smart defaulters will sell early and profit. The ones who live wholly in the moment will destroy their asset while saving just enough for 1st month + security deposit on a rental.

Pure, unfettered fantasy. Absolutely zero regard for reality. Just a Kool-Aid tinged rant driven by wishful thinking at best. The properties taking the worst beating right now are the ultra-high end. It’s moving its way down the chain.

Bear,

I’m going to have to agree with DepthCharge on this one. My best indicator to date of the real estate market is what coops in NYC are doing. When they allow sales at lower prices, you know it is really bad out there. And not only have I heard they have allowed sales at lower prices, but they approved sales within a couple of months. This is radical economics in Manhattan. A clear sign of desperation, locking in a sale of the shares before prices drop even more, and the value is reflected in the share price.

Miami is also over, in my opinion, not cool anymore.

I was in Miami a month ago. Maybe prices have dropped there, I don’t really have a frame of reference. It seemed like the bottom end on everything was in the median range.

The urban flight and WFH effects on the price declines in huge urban areas is a different real estate microcosm. My predictions pertain to the inventory Wolf outlines in this article.

Green New Deal requires the majority to be moved into Federal eco-housing and looks like these forbearance programs will greatly help in achieving the goal.

Oh you mean the legislation that doesnt exist?! Right!!!

Boogie boogie boogie!!! Immigrants and green new deal are coming to get you!!!!

lol federal eco-housing doesn’t sound bad to me

Wolf,

From someone working in D.C. ,” they’ll just tack all missed payments on the back end”. Living in D.C. I believe they all think a like. IMO.

1) All those empty mall & shopping centers, empty office buildings & apartments lead to the growth of section 8 apartments.

2) People like Micheal Dell can absorb $20M realized loss.

3) The gov can absorb RE delinquency. The perpetual high level of FHA delinquencies rate is > 10%..

4) Section 8 subsidized apartments and section 8 subsidized private homes.

5) The the wide spectrum of snap and section 8 sacked Trump.

6) Under the slogan : “no fault of their own” ==> the more power the gov have.

7) More power the gov have the more they can flex and “rejuvenate” the antebellum constitution.

8) With their perpetual power, the gov can purge opponents and unruly friendly entities like the teacher union.

9) The risk is growing. Those who oppose the “fake constitution” might collide with the unruly ME proxies : Antifa and BLM.

So now the poorest of Americans are on the hook for unpayable bailouts, stimuli and endless (mostly fraudulent) government spending.

While mostly the rich benefit from the free money.

While getting foreclosed from the banks that they bailed out.

Wasn’t that the whole plan?

The destruction of lower and middle classes.

“So now the poorest of Americans are on the hook for unpayable bailouts, stimuli and endless (mostly fraudulent) government spending.”

And these are the same folks fighting ‘our’ wars in Afghanistan and Syria, among other places…

What could be more threatening than somebody silently kneeling and then saying “My life matters.”

The horror….oh God, the horror!!!

I guess we all know who the real snowflakes are!

You?

or at least a drama queen …….

you reported that credit card balances were being paid off at a high rate

Are [people paying down/off their 20% loans and then going to the 3% home loan “next year”

Wolf, thank you for your reports I am a very small investor but you and your followers seem to be ahead of the crowd

Bob

I would expect these forbearance and other handout programs to continue long enough for the powers to be to advance their Great Reset agenda forward since people on the dole will always readily accept whatever the govt asks of them in terms of giving up liberties.

If forbearance never ends (hypothetically) then what happens to real estate as an investment? (hypothetically)

Loaded question, is RE an investment?

Assets are valued on streams of income in the present or the future. If real estate cannot produce a return now or in the future, it is generally worthless. The real estate becomes a consumable product.

After I understood the unavoidable RE tax scam I always considered my home a consumable. There are much better forms of “wealth.”

Creeping up utility prices, city taxes contractor cost, sometimes insurance cost can blindside you, squatters, renter protection in some province make it impossible to make profit and interest rates not going anywhere would eat any returns.

I hate to sound conspiratorial, but if history is any indicator, the corporate world will use this to monopolize the rental real estate market in the same way they used the Great Depression to monopolize family farms.

The current environment since the beginning of COVID, has basically benefited the corporate world in many ways while driving small business people out of business in droves. While many small restaurants went bankrupt, the large chains, that are embracing to go orders and automation are set to gain massive market share. Access to low interest corporate loans give them the advantage to ride this out, and take advantage of the opportunities that are not available to individuals.

Small landlords who cannot afford a non paying tenants, will eventually have to sell, and corporations are in a position to take advantage of that.

In short, you are seeing a continuation of the wealth transfer, from the working class to the wealthy.

same as it ever was ………………….

isn’t that the whole function of financialization ,,,,,, banks, the FED, Wall Street?

Anyone care about RE in 2021?

Sourgrapes; The houses are bigger, cheaper, uglier than they ever been.