A hugely important concept: “There is no trade-off between price stability and financial stability.”

By Wolf Richter for WOLF STREET.

The ECB hiked its policy rates by 50 basis points today, defying predictions and fervent hopes out there that it would end its rate hikes. Yesterday, traders saw just a 20% chance of a 50-basis-point hike. They’d all been hoping that the ECB’s rate hikes would be shut down by the banking turmoil.

Since the rate-hike cycle started in July 2022, the ECB has hiked by 350 basis points, raising the deposit rate from -0.5% to +3.0%, the biggest rate-hike cycle in its history, to fight the worst inflation in four decades. With this 50-basis-point hike, the ECB stuck to the rate-hike indications it gave at its last meeting.

“Inflation is projected to remain too high for too long,” is how the ECB started out its press release today to point out where its emphasis was.

“We are not waning on our commitment to fight inflation, and we are determined to return inflation back to 2% in the medium term – that should not be doubted. The determination is intact. The pace that we take will be entirely data-dependent,” ECB president Christine Lagarde said at the press conference.

“There is no trade-off between price stability and financial stability. And I think that if anything, with this decision [hiking by 50 basis points when markets were expecting no hike], we are demonstrating this,” she said.

ECB staff “have demonstrated in the past that they can also exercise creativity in very short order in case it is needed to respond to what would be a liquidity crisis if there was such a thing. But this is not what we are seeing,” she said.

Calming a financial panic while tightening to fight inflation.

The Bank of England showed the way. It had been hiking rates when soaring long-term yields of gilts caused UK pension funds to get into trouble last fall. They faced margin calls from the investment banks that had sold them the infamous LDI (liability-driven investment) funds. When pension funds were forced to unload their gilt holdings to deal with the margin calls, yields spiked further and prices dropped further, forcing the pension funds to sell even more gilts, which pushed their prices down further, thereby setting the gilts market up for a “death spiral.”

The BOE stepped in with big rhetoric about massive buying of gilts, but in fact bought only small amounts. It calmed down the gilts market and gave pension funds time to clean up. In November, it started selling those bonds it had bought in September and October. And by January, it had sold all of them. With the panic settled down, the BOE’s rate hikes and QT continued.

Today, the ECB – while “monitoring” the banking turmoil – said that it had different tools in its “policy tool kit”: One set of tools to fight inflation (rate hikes and QT) and another set of tools to deal with financial panics (liquidity support for banks), and that it was not one or the other, but that both could be used, and there was no “tradeoff” between them.

The ECB “stands ready to respond as necessary to preserve price stability and financial stability in the euro area,” it said.

“Our policy toolkit is fully equipped to provide liquidity support to the euro area financial system if needed and to preserve the smooth transmission of monetary policy,” Lagarde said – so it could provide emergency liquidity to a teetering bank, while continuing the inflation fight via monetary policy.

She said if underlying inflation persists, more tightening would be needed. But the ECB refrained from giving specific forward guidance.

The Eurozone banking sector is “resilient, with strong capital and liquidity positions,” the ECB said (Credit Suisse is not a Eurozone bank).

This is an incredibly important concept, that central banks acknowledge they can deal with a bank liquidity problem without backing off their inflation fight. There have been some papers by Fed researchers to the same effect.

Inflation fight isn’t over, ECB says.

Energy prices in the euro area have been declining, but inflation has shifted to services, with the Eurozone CPI without energy spiking 7.7%, core CPI without food and energy spiking 5.6%, and services CPI spiking 4.8%, all of them records.

Lagarde said that “underlying price pressures remain strong” and that “wage pressures have strengthened on the back of robust labour markets and employees aiming to recoup some of the purchasing power lost owing to high inflation.” As a result, the ECB raised its projection for “core CPI” (without food and energy) to an average of 4.6% in 2023.

The ECB also raised its projections for economic growth in 2023 to an average of 1.0% “as a result of both the decline in energy prices and the economy’s greater resilience to the challenging international environment.” It projected growth to pick up some in 2024 and 2025, “underpinned by a robust labour market, improving confidence and a recovery in real incomes.”

The financial turmoil added greater uncertainty to the baseline projections, and risks to economic projections are “tilted to the downside,” Lagarde said.

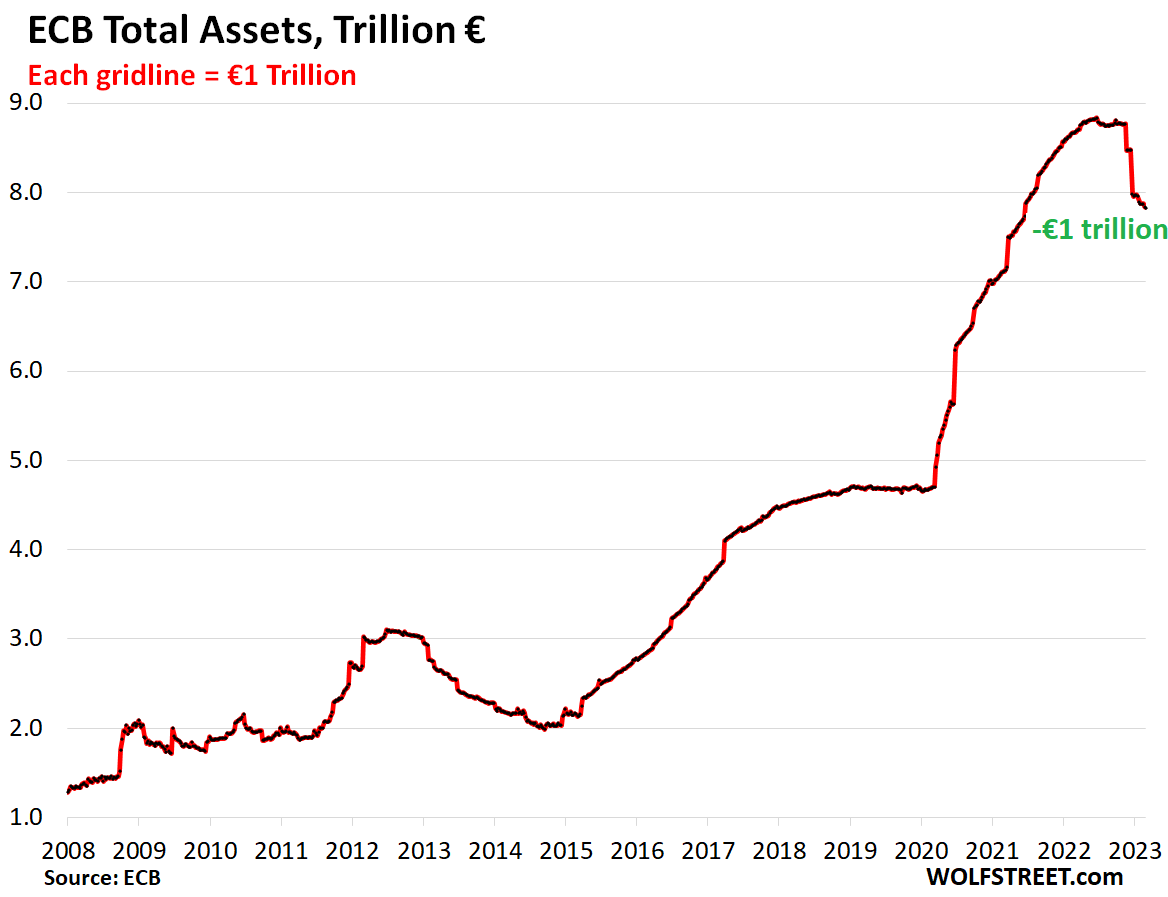

QT Continues.

The ECB had performed QE in two ways: initially, highly incentivized loans (without collateral) to banks for them to spread the money around in the markets; and later bond purchases.

As part of its QT kick-off last fall, the ECB changed the terms of the loans and made them less attractive, and opened more windows for banks to repay those loans. And they did – massively. In addition, the unwinding of the bond portfolio has started and will continue at the current rate (€15 billion per month) through June, the ECB confirmed today, at which point the new pace will be set.

As a result of this two-part QT, the ECB’s assets on its balance sheet have plunged by over €1 trillion from the peak:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hi Wolf do you think QT is having any real impact on Inflation yet ?

…also how does the QT reduction balance with the liquidity coming into the Market with these Bank Support Plans ? Sorry if this is a simpleton question !

Answered below, Thanks

haha although late to the party….good ol’ Christine is showing Pow Pow she has balls too….

If Pow Pow next week don’t hike at least .25 and keep the hawkish tone…then we all know who got the franks and beans between them two..If he really wants to be mini-Volcker then .50 is the way to go

Trump and Banksters stopped Powell before. This time should be different. We shall see.

That’s the way to go if you want to deliberately crash the markets. The Fed will do what’s best for the economy, and right now the economy is shrieking “no more rate hikes!” in a Fran Drescher-esque tone.

Have you seen the cute video where Cramer was touting SVIB a month before it went tits up? I wonder if he had anything to say about that recently.

I keep reading if you do the opposite of what Cramer says you’ll do quite well.

The rich have figured out how to game Jim Cramer,just let followers get in his recommendations,Wait 30 days short it ,or sell stock .Price drops they make boatloads of money

I agree the Fed will do what’s best for the economy: keep hiking. High inflation isn’t what’s best for the economy. The economy needs stable prices. Some people who don’t care about the economy might be shrieking “no more rate hikes!” You’re making a fundamental error by equating the markets to the economy, much like the real Jim Cramer.

Most likely the ECB raised 50 basis points in order to not panic the stock markets. Central banks will chose wealth stability of rich people over inflation for the bottom 99%, so beware as the inflation fight is only good as long as markets remain stable for the top 1%.

Not wise yet “this is the way”.

no, the economy is pleading for more rate hikes, it is Wall Street that wants to continue this loose money era.

Like a drunk at the bar at closing time and the bartender is saying he’s cutting the guy off and go home.

The puppet will do what his handlers ,tell him to do .

Hardly a mini Volcker with Fed Funds STILL below inflation (and since 2009)

There are the infamous “long and variable lags” between changes in monetary policy and inflation.

QT is already having a big impact on asset prices and it’s rattling the banking sectors.

Right now, ECB interest rates are still simulating inflation because they’re well below core CPI. For core CPI to calm down, higher rates are needed, and everyone knows this, even the ECB.

Serious question; isn’t the Fed’s new bank “bailouts” just some more QE to balance out the ongoing QT for that soft landing in never never land?

That’s wishful delusional thinking. It’s a loan at about 4.75% against collateral.

The banks cannot buy securities with the amount they borrow from the Fed. It just helps them fund their deposit outflow.

And where does the Fed get the money to loan to illiquid banks, other than conjuring it out of thin air?

Wolf, if the Fed continues to raise, will that 4.75% rate also increase, or does it stay at that rate for the term of the loan?

All be it overvalued collateral. And by what means is use of these borrowings limited?

actually, rates are pulling down inflation, even if they are bellow it. The correlation isn’t linear. This is why they aren’t targeting 7-8% but rather 4-5%. The lag plus this makes it more complicated. Even they don’t know what the peak will be.

Hardly a mini Volcker with Fed Funds STILL below inflation (and since 2009)

There also is a lag in costs being plugged into prices

Agreed, rates act as a drag, even if below the rate of inflation. Volcker used it as such back in the day, but it can backfire on you if you ease up too early

No one is mentioning this thought I have.

Raising rates is for the purpose of reducing credit, which in turn slows money supply, which reduces inflation.

If banks are scared, short on deposits and short on liquidity, then further rate hikes make no sense. The bank failures did what the hikes weren’t yet high enough to do. I would expect generating more loans is the opposite of what most banks are trying to do right now (at least in usa).

The EU is in a different position than the usa. They have higher inflation, lower rates, and their banks didn’t fail. Jpow should be PAUSING rates for a while.

Opposite. The problem is that banks overall have had TOO MUCH IN DEPOSITS — $17 trillion. Now some banks have a run on the bank as people are yanking their money out, and other banks are flooded with deposits, which is where some of this money ends up. There’s way too much money out there, it’s the foundation of the problem after all this money-printing.

Right. You’re describing the problem up until last week. Too much money. Then you also describe what happened after they pulled the money out(bank runs), leaving them short on deposits/liquidity, which is the problem now. They can’t loan if they are short on either.

I’m saying that within a week conditions have flipped because depositors ran to bigger banks and smaller banks that kept deposits would want to focus on defense, not expansion. The rate hikes are to depress credit, but sentiment and defensive tactics by many banks should be taking care of that right as we speak (unless the central banks reliquify the banks again).

Ugh. Per CNN’s main page headline: “Mortgage Rates Fall in Wake of Bank Failures”

party party party

Fall to what, LOL? To 6.71% from 6.79%.

Getting economic info from reading headlines and then posting comments based on it always makes people look very silly.

I’m my share of silly, to be sure — but not for this; maybe if I were promoting it, but I’m not; makes me wince & gnash. I’m showcasing the headline as an example of sensationalism. I don’t get what stake these outlets have in pumping housing like that. But silly or not, news troughs like CNN are where Joe Q Public line up to get their amen fodder.

I doubt that you’re silly Bulfinch (especially if you are descended from Thomas).

Starting your comment with “ugh” was the clue that you share a similar disdain for MSM as many of us do.

We’ve all had a clip around the ears from Wolf, sometimes deserved and sometimes collateral damage as he fights the good fight.

Wear it as a badge of honor.

Wear it like a badge of honour if you like, but I’d say, next time be more explicit about what you mean and don’t use code/slang like ugh.

Some readers may interpret the clue properly, but this site also has many non-native English speakers and it would be a shame if they interpreted you entirely the wrong way.

Anything to stir up some good ol FOMO….since there are plenty of zombies out there, it really doesn’t take much to get them going again. Can they buy though, that’s a better question.

To Wolf’s point though, 6.79 to 6.71 or even 6.50 and people are acting like it’s back to 2% all over again…yeah that’s how stupid some of these catch the knife buyers are

4 week bill is at 3.98%. Riddle me that.

New Issue brokered CD’s are yielding around 4.8% with 4 to 5 week maturities. It would seem that buying insured CDs in regional banks provides the best risk reward profile for managing cash that one might need soon (but not today)…

Again, I apologize if I am pedantic or redundant but Monetary Policy can only do so much when in the case of the US, team B is still pumping money into the economy. Heck, there are still hundreds of millions of COVID money waiting to be spent. Look at M2, it is still at a historically high point.

Inflation is here to stay unless Monetary and Fiscal policy align. In Europe, the Total ECB asset graph looks like ours FED assets, M2 …

Yes, correct. Inflation isn’t just going away because some people are hoping it will go away. It will stick around and it will serve up nasty surprises as this type of inflation tends to do.

Friends in Western Europe explain that each month they have a cap on how much they can use w/ their credit cards. Once the citizen goes beyond that amount, the bank sends out a warning: another eu put on the credit card and the bank closes that account.

We sense that the ECB was formed using the German model of finance: Restraints.

It may be there are “other tools” the ECB uses towards Credit Suezze (sp) to keep its behaviors from spreading to other banks.

The German love of financial restraint has been strained by ECB bailouts of the PIGS. On paper the ECB owes the Bundesbank a huge amount of euros: can’t remember if its one T or 2.

That would seem to discourage both responsible and irresponsible use of credit cards. There were (a very few) times I recall (before I had savings) when making a major purchase at a steep discount was worth paying credit card interest. Buying at 50% off can justify a 20% interest rate…

It’s good the ECB didn’t cave. This isn’t even a European banking crisis (HSBC took over SVB UK, and the Swiss government is bailing out Credit Suisse.)

Hopefully FOMC voting members will have spines next week.

I was just told today on Good Morning America that I want the Fed to lower rates at the next meeting and that every time they raise rates it is hurting everyday Americans. Then they said something about credit cards. I have never once heard the new media say that when the fed raises rates, CD rates, money market, and even now savings account rates also go up. I never bought into idea that the news being controlled by outside forces but that is starting to change.

“I never bought into idea that the news being controlled by outside forces but that is starting to change.”

Wolf’s site is a prime example of finding out and debating “truth”.

“News” is all rancid pablum, only viewed by lazy zealots.

boikin – the news media is just a shill for the interests of the super-rich.

dont believe a word they say. it is all a big con job. the american public ha been gaslit for decades.

the worst thing for everyday Americans is inflation, eating into their income.

the Fed will serve up a half-point interest rate increase at the next meeting. the sooner they kill off inflation, the lower interest rates can go in the long term. if they dont kill off inflation before it gets even more entrenched, they have a real problem.

It’s an oldie but a goodie:

“News is what somebody somewhere wants to suppress; all the rest is advertising.”

Lord Northcliffe (1865-1922)

The A to Z of too-big-to-fail US banks (JPM, Goldman, WF, B of A et al) are bailing out First Republic Bank with billions of dollars today.

I wonder if the Biden administration compelled them to do so behind-the-scenes due to backlash over the SVB depositor bailout.

Indeed looks like that they were told “Make sure FRB stays afloat, or all of you will be in trouble”. There is a reason, they said Bailout is considering only two banks. Even Feds know, the word “bailout” is a salt on a wound for taxpayers.

Also, many of them got the deposit inflow that was flowing out of svb and first republic. So they’re basically recycling that hot money back to first republic.

If/when the market calms down and FRC’s customers come back to it, they will pay off those loans with deposits that the customers withdrew from those big banks.

It’s basically circular but a way to provide liquidity where it’s needed and mop it up from places where it’s not needed.

“The ECB raised interest rates by 50 basis points today, defying forecasts and fervent hopes that it would end rate hikes.”

Now those hopes have shifted to future meetings based on the fact that the ECB did not set its future policy at this meeting. But they do not take into account that Legarde has repeatedly said that they will act according to the received data on inflation before each next meeting. A lot of people still want the pivot and they see it everywhere, even in their dreams

Banks are having trouble and the bad loans haven’t even started hitting yet. When will the office buildings get marked to market price?

When will the office buildings get marked to market price?

I have no idea, but I will bet there are some folks hoping it is a long way off! There will be ripples if and when they are marked to market.

Re: Pivot Mongers: I saw some calling for a freaking rate cute this time.

Been wondering this myself.

We know that WFH took a big chunk out of building occupancy. And we know that downtowns are built on a mountain of debt. What happens when those two factors collide? This stuff moves so slowly…

Toronto home prices increased by $7,000 last month and every realtor and homer are rejoicing.

Let’s hope that the Fed hikes rates next week and stop pandering to speculators and real estate millionaires.

The important thing is to look at the number of transactions that have collapsed and the prices in this case are irrelevant

And year-over-year, prices had the biggest plunge on record because prices always increase a lot in Feb (spring selling season), but this time, they barely increased.

Regardless of sales and a minuscule percentage increase during the start of spring season, the realtors and speculators are popping bottles in the club like a blizzard and celebrating. Reddit and TikTok are replete with cringe.

A measly $7,000 increase on a $700,000 property.

7K at GTA valuations is basically noise, if you have the source I’d love to read it though.

1) In the last month the German 3M gap lower the most. The long duration

the least.

2) In France the 6M gap lower the most.

3) In Switzerland the 1Y gap lower the least, but the 2Y plunged the most, splitting the yield curve.

4) In Japan the front end is glued together. The 10Y dropped the most.

5) U cannot fight inflation during a banking crisis. In US, Japan and Europe

within a month all rates gap lower. The bond market knew what we didn’t know. The global central banks raised rates, but the yield curve didn’t care.

6) US gov try to deflate debt in real terms ==> debt might deflate by itself.

EU inflation at 11% for 2 years and the EU CB raise rates to 3.5% wit a 50 basis point hike! That’s hilarious! Maybe they know IF they were really going to fight inflation there would be a deep deep depression!!!

I wonder if the FED would follow the same path and hike by 50bps to tame inflation ?

Last they discussed it, they said 25, and they haven’t said anything seriously to change that.

25 seems like the only choice. Zero would encourage the pivot-mongers and 50 would put a bulls eye on the Fed if there is any further bank turmoil. Steady as she goes on rates and let QT work in the background…

In addition, the Fed is 1.5 percent ahead of the ECB. If he wants not to break something, the increase will be from 25, maybe several times until the ECB, I doubt if it will even reach 4 pr. The Italians will pierce our ears

QQQ rock, dbl the size bar on slightly higher vol, but DIA didn’t get it up and closed < Mar 14 high.

QQQ breached Sept 2020 high and May 12/17 Anti BB, but not Feb highs.

Irrespective as to whether you are correct or not the BIAS in your articles towards no pivot is fat too apparent…

Try driving a car with one for on the brake and the other on the accelerator…this is Lagarde …

Fed has already taken onefoot off the brake

1. Pivot mongers have been out there for an ENTIRE year, and every step along the way, they were wrong. I’m just telling you what central banks are actually doing and saying, and they’re NOT pivot mongering!

2. One foot on the brake, and one arm on the baby to keep her from hitting the dash board.

Better to NOT NEED to have an arm on the baby in the first place Wolf, as that would mean, as in this case, that you have not secured the baby in a proper car care device as common sense dictates…

Howzaboot one arm on the pup??

That too going to become a felony soon in some places?

Certainly ‘hope’ fed continues with steady rate rises and INCREASES QT faster…

IMO that would help with the inflation reduction mo betta than massive interest rate rises.

Wolf, I thought the FDIC, without legislative approval, threw the baby out with the bath water by guaranteeing the deposits over the legislated maximum of $250,000. The expression of throwing the poor baby out with the bath water came from the practice in resource short American households ( late 1800’s/ early 1900’s ) of giving the poor toddler the last bath using the same repurposed water, and since it was so opaque at that point, you had to make sure you saw the baby to save it!!!

Anyway, in one fell swoop, the FDIC threw out a major component of deposit insurance that was instituted after the 1929-1932 Great Depression to limit the amount the American taxpayer was on the hook for in bank depositor bail-outs. The funding of the FDIC insurance fund is from the U.S. Treasury when shortages arise, which they just have, and Janet Yellen gets her spending power, primarily when Powell is not involved as Buyer of First Resort, from American taxpayer and business tax revenues.

Think this precedent is going to come back and bite us in the butt because I see more debt defaults and bank insolvencies just over the horizon in the most leveraged America and nation that has ever been on this planet. Expanding national debt ad infinitum has proven to be highly inflationary at this point. Stay tuned, folks. It’s going to be a very bumpy ride.

More and more Americans have gotten the message that there are many relatively safe non-bank alternatives than to only getting 0.5% on a regional or money-center bank account.

Have let Schwab use my money for almost two decades interest free while I was waiting to invest sale proceeds, and today became enlightened with 4.4% interest in a Schwab Treasury Money Market. The schizoid nature of the financial markets right now, wow the bond market is on amphetamines, prompts me to keep a good portion of proceeds in Treasury MMkts. There was little incentive until March of 2022 to do your own cash sweeps to a fund that actually bought you a burger every so often.

Me again, I think the next corpse to float to the surface in American banking is commercial real estate loans. Crapto- currency failures are not done yet, but for variety we can look forward or backward at this area for the next act.

Wolf wrote:

One foot on the brake, and one arm on the baby to keep her from hitting the dash board.

Another superb remark! How stunningly visual!

By the way … did you grow up in the 1960’s like I did? Both Dad & Mom drove like that when I was sitting in the front.

I didn’t grow up with a silver spoon in my mouth, LOL. We didn’t have a car. But yes, parents were routinely and automatically doing that.

One foot on the brake

That’s how I brake, TBH

So now the mantra is that the wobble in these regional banks is “doing the Fed’s work for them”, drastically tightening financial conditions.

But – is there any real evidence of that? I mean, so far the only people getting wiped out are investors. Everyone else is getting a signal that the government / Fed will save you in a pinch. Is this really going cause funding to dry up to anyone other than Tech start ups enough to cause the Fed to stop with CPI at 6%???

I’m not sure this really has that much downstream effect on John Q Citizen who doesn’t watch Bloomberg all day and is still spending like an inebriated mariner (trying to be a little more PC here lol)

March 16 2023. “Washington, DC — The following statement was released by Secretary of the Treasury Janet L. Yellen, Federal Reserve Board Chair Jerome H. Powell, FDIC Chairman Martin J. Gruenberg, and Acting Comptroller of the Currency Michael J. Hsu:

Today, 11 banks announced $30 billion in deposits into First Republic Bank. This show of support by a group of large banks is most welcome, and demonstrates the resilience of the banking system.” – FDIC

Well, well, well, the big fraternity boys are covering for one of their little brothers because of his indiscretions. Collusion? Desperation? Fear? Do we now have a cartel?

That’s how it is supposed to work. Banks supporting each other. That’s the opposite of contagion.

I am more of the mind that when you have frostbite you cut off the appendage to save the rest of the body.

To me, this is all part of the core cancer eating away at our economy. We keep incrementally spreading around risk and it just makes the core weaker.

Should Ford bail out GM if it starts to fail? Was ExxonMobil supposed to bail out Enron? Were Amazon and Walmart supposed to get together to prop up Sears and Kmart? Some companies are supposed to go belly-up in a capitalist system. Sorry, Wolf, companies are not supposed to “support each other”. Companies are supposed to compete against each other.

Before you know it, we are going to be bailing out communist China. Breaking news, Yellen just said that all depositors affiliated with communist China at SVB will get all their money back. The regulators also said “Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks.” So who is going to pay for this special assessment? Anyone who has a bank account in the United States, in the form of increased fees and lower rates on savings and CDs. So if you have a bank account, you get to participate in the bail out of depositors affiliated with communist China.

BTW, when I say “bail out SVB”, I do not necessarily mean bailing out the corporate officers. I mainly mean bailing out everyone whose deposits exceeded the $250,000 FDIC insurance level. In this new event with First Republic, banks have gotten together to bail out both the corporate officers and the depositors. I can only imagine the deals made behind the scenes. Probably more than mocha lattes for life.

“Should Ford bail out GM if it starts to fail? Was ExxonMobil supposed to bail out Enron?”

It happens all the time. It’s not called a bailout though. That would be too dirty a word. It’s called an “acquisition,” or “taking a stake in,” etc.

America will be borrowing 8% of GDP this year, around 2 trillion$$$ at 4 to 5%. With existing debt of 31 trillion $$$ at 2% interest rate, but will be heading higher as debt is rolled over, fed gvt interest payments will soon be over a trillion $$$! As the economy slows or comes to a jarring halt fed gvt borrowing will spike to over 3 trillion$$$. As far as inflation goes you ain’t seen anything yet!

Tax revenues already SPIKED. It’s really dumb to jabber about interest expense without discussing the spiking tax revenues:

But arent tax revenues going to plunge this year? I know in Cali a huge surplus is going to turn into a huge deficit.

Most of us on this board believe there is alot of downside in housing prices and the overall economy. So tax revenues are headed much lower in the coming year(s) unless they raise tax rates.

This spike in taxes is at least partially transitory, but debt doesnt go away.

I still think we are living in denial about the huge ramifications of too much easy monetary policy combined with an economy that consumes more than it produces. Combine that with some form of war between us and China (cold, hot) and you have a formula for major economic tragedy, IMHO. But I tend to focus on the negatives.

The FED just released new data and the balance sheet grew by 300B, ouch!

The various existing liquidity programs like the discount window (150B), and the new BTFP (so far 15B) found some good pickup in the recent chaos.

Will be interesting to see if/how they plan to sterilize this.

It will sterilize itself. The Fed is charging ~4.75% on that BTFP lending facility. The banks will want to pay that back as soon as possible.

That may be true for the discount window, I don’t think for BTFP though. I’d be surprised if the program’s size doesn’t increase over the coming months unless long term yields fall further. The conditions with partial collateral are just too good to be ignored by a bank that holds deeply underwater assets while needing liquidity.

The sterilzation is likely going to be that the money just moves into reverse repo back with the FED by it ending up either as a deposit at a big bank, or in a money market fund. At which point most of the interest that the FED receives from borrower bank A is paid back into the system to lender B.

So net effect is more of a flow thing, but at the same time increasing M2/reserves, thus decreasing risk / leverage. Good for the stock market? Unless it allows the FED to hike more freely now.

The Fed lent money to the banks at about 4.75% against collateral, and the banks cannot buy anything with it, no securities, nada, and these loans have therefore no QE effect. All banks can do with it is pay depositors their money back so that the banks don’t collapse.

And QT continued too with the Treasury roll-off.

Right, but isn’t it still putting more total money into circulation? If people withdraw their cash from those regional banks that were struggling (with the bank using the money borrowed from the Fed at 4.75%), and then deposit that cash into other banks, couldn’t those OTHER banks then use the money to buy assets, having a QE effect?

Yes I agree. This is indirect QE.

The banks can’t do anything the money as Wolf said except pay depositors if and when needed. Understood.

But instead of borrowing that money from somewhere else within the existing money supply, they’re borrowing from the Fed. Poof, money created, right?

If it looks and smells like QE…

” isn’t it still putting more total money into circulation?”

No it’s not because it takes the collateral out of circulation.

Fed balance sheet released today. The “Loans” category increased by $303 Billion from last week. Yikes.

“There is no trade-off between price stability and financial stability.”

I generally agree but we don’t have price stability. There is no way to bring this inflation down in a smooth and orderly manner and return to price stability without first enduring historic turmoil.

All the Fed had to do on Sunday to win the inflation fight was precisely nothing.

A de facto 100% guarantee on uninsured bank deposits is the latest salvo against deflation.

But you should remember for whom the Fed/Treas/Gov work for and hence they called an emergency meeting on Sunday to save their friends.

Wolf, thanks for providing a calm, reasoned, and highly informed perspective, while most others are running around with their hair on fire screaming. I’ve seen no one else even mention these facts and point out their implications.

Wolf, QT was fun while it lasted… The numbers are in. The Fed’s balance sheet increased by nearly $300 billion last week. LOL!!! Are you changing your opinion on this “hawkish” FED? Thx

Quit reading stupid headlines and look at reality.

The Fed lent money to the banks at about 4.75% against collateral, and the banks cannot buy anything with it, no securities, nada, and these loans have therefore no QE effect. All banks can do with it is pay depositors their money back so that the banks don’t collapse.

And QT continued too with the Treasury roll-off.

Braking with one foot and putting an arm around the baby to keep her from falling off the seat (like they used to before child seats).

Just curious, is there any rule/law/regulation from the fed that the banks can only use this loaned money to pay depositor?

The law of economics. These banks are OUT OF CASH and THEY’RE ABOUT TO COLLAPSE because DEPOSITORS WANT THEIR CASH BACK and banks NO LONGER HAVE CASH TO PAY THE DEPOSITORS.

Why is this so hard to understand?

Banks don’t borrow at 4.75% to buy securities that yield 4%!!!

Wolf, I feel you’re missing something here. Please see my comment above. Struggling to comprehend how this isn’t indirect QE.

Yea, I am totally confused how this is not the same as QE. The FEDs balance sheet increased by $300 billion (this is directly from FRED site, not a headline). Depositors are getting their money back but where did this money come from since the entire reason they couldn’t get their money back is that the bank has bad collateral. The Banks are getting the original value of their collateral instead of market value, right? Last time it was MBS, this time its treasuries.

Is the only difference that they are calling it a loan?

Because the loans are against assets-

THEY DIDN’T GIVE THEM THE MONEY.

THEY HAD BONDS, THE FED TOOK THEM AND GAVE THEM THE FACE VALUE.

There is a small subsidy based on the current value, but this is essentially cashing them out at par to get ready cash not bonds.

QE is the Fed creating money to BUY bonds increasing the amount of money in circulation.

Citizen AllenM,

I don’t agree. Loaning newly created money against collateral is exactly the same as purchasing the collateral with newly created money.

It’s QE while the loan is outstanding, and then the minute the loan is repaid, the repaid amount is QT. The only difference between a purchase is its duration.

It’s QS – Quantitative Special.

I hear you. You’re not wrong. But it’s not quite so straightforward either. “Therefore no QE effect” overstates things, at least a little.

That money is going to depositors, let’s say some medium-ish sized company, whose CFO is going to finally getting around to buying treasuries instead of holding liquid cash they don’t need (because they’re laying off half their staff anyway). Or maybe he’s going to move the company’s cash out of Bumf&ck Community Bank and over to JPM, who is in turn going to go buy treasuries or bargain MBS or whatever.

That’s conjured money indirectly buying securities.

The Fed continues to roll assets off its books, true that, and the sensational headlines from zerohedge and his ilk are BS. But to say “*no* QE effect” is not quite right either.

It is short term though, so any cherry picked scenario you come up with gets washed out in less than a year anyway. It definitely is not the same as normal qe and shouldn’t be considered in the same basket.

inflation is going to accelerate -consultants are pushing a strategy known as – POV -price over volume- reduce volumes and close higher cost facilities and raise prices 5- 10 percent more than inputs- pepsico – was one of the first to utilize it when they were forced out of russia- they found it dramatically increased profits – no push back from consumers – it is the hottest concept being sold by consultants –

Many speak of the “lag” in the effects of interest rate increases.

But MOST ignore the “lag” in plugging in higher costs….to your point

depends if there’s substitutes … unless your brand is soooo good, people will shift to alternatives. look at subscriptions … there’s no loyalty … subscribe today / unsubscribe next week. PoV is a short term tactic … not a strategy.

There is something to this but I dunno if it’s quite THAT strategic.

We are finding that everyone, ourselves included, are just not any mood to tolerate low-margin business right now. It feels great to have a little supplier power for once. I’m not clogging up my finite capacity to break even building an order for captain penny pincher when there are five other customers behind him that’ll take the build slot at a price that actually rings the cash register.

There has been a shift in mentality and it’s all because of excess demand. We’ve long been told to fire low-margin customers to maximize profitability, but we’ve only recently had the stones to try it.

This episode shows a flaw in current system. A demand deposit is something that you can get at anytime and for any legal reason. You can’t use past history or statistics to predict when people will panic. Central bankers rely on talking a good game that the system is strong. Its all backed by ability to print like Argentina and Turkey.

The big boys supported the Dow in 1929 to stop the plunge. XLF look like 1931.

In 1934, to restore confidence in commercial banks, the US government instituted the Federal Deposit Insurance Corporation (FDIC) deposit insurance in the amount of $2,500 per depositor per bank, eventually raising coverage to today’s $250,000.(Now whatever needed in the name of financial stability In Europe, €100,000 is the amount guaranteed by the state.

European regulators called the Fed’s decision a “total and utter incompetence.”

European authorities have slammed US regulators for their handling of the Silicon Valley Bank collapse, according to the Financial Times.

In particular, they pointed to US guarantees on all SVB deposits, even those exceeding the typical $250,000 limit.

One European official was surprised at US regulators’ “total and utter incompetence,” adding that it came after a decade of “long and boring meetings” where the US pushed to end bank bailouts in global bank policy standards.

A former UK policymaker who played a role in creating the standards called the US response to SVB a “disaster.” Another European regulator called it a “joke,” blasting President Biden’s claim that the handling of SVB’s collapse would pose no cost on the taxpayer.

“At the end of the day, this is a bailout paid by the ordinary people, and it’s a bailout of the rich venture capitalists, which is really wrong,” the regulator told the FT.

This is for the ECB. I think pretty soon we’ll see that the Fed’s balance sheet has increased again to accommodate the latest party.

Punch bowl got re-filled again. Happy days are NOT yet completely gone.

Following this 2nd moral hazard, Fed has no stand to resist next or the next moral hazard. Risk-on will be back very slowly.

(My apology. I intended the 2nd paragraph to be in above comment but it was too long)

Central banks are a linchpin of today’s world financial system. By purchasing government debt, banks can allow the state—for a while—to finance its activities without taxation. On the surface, this appears to be a “free lunch.” But it’s actually quite pernicious and is the engine of currency debasement.

In 1934, to restore confidence in commercial banks, the US government instituted the Federal Deposit Insurance Corporation (FDIC) deposit insurance in the amount of $2,500 per depositor per bank, eventually raising coverage to today’s $250,000.(Now, whatever needed in the name of financial stability)

In Europe, €100,000 is the amount guaranteed by the state.

FDIC insurance covers about $9.8 trillion of deposits, but the institution has assets of only $126 billion. That’s about one cent on the dollar. I’ll be surprised if the FDIC doesn’t go bust and need to be recapitalized by the government. That money—many billions—will likely be created out of thin air by selling Treasury debt to the Fed.

I hope this day never comes but happening incrementally in the name of ‘financial’ stability irrespective of price/cost. Whatever one call it, it is QE 5 (extra lite?) is operational. A 2nd moral hazard has been committed AGAIN. No one learned from 2008

Its a Good thing ECB Making 0.50 a Viable choice in the US rather then driving blind with foot on the Brake / they can cut it in 3 Months perhaps .

I think some Dramatic thinking is the way to go Like Cut Property Tax’s 20% Nation Wide stimulating the R.E. Market & fighting Inflation at the same time. Ya throw Money at it but with better aim Look at Property Tax today ? Going up ? Not down with the flow of things at all

The Fed started all this now to put on a mask and Hide is impossible

Just because something has never been done does not mean it can’t

The real Aim is to be Re Elected and keep hands clean

As some one said’ Never under estimate the stupidity of Bureaucrats”. They tend ‘double’ on their original mistake, thinking this time it will be ‘fixed’ just like our FOMC FDIC, SEC++

It’s not really stupidity, tbh. It’s just that there are no good options left without a lot of pain.

butters

Pain for the public NOT for the Banks!

I view the rate hike from the perspective that the Fed has been telegraphing and jawboning for a full year, consistently laying out their plans and following the dot plot, while inflation has continued to embed itself in the global economy.

Inflation is found in the data trends and it’s clearly evident in the grocery stores and throughout the global economies.

The fact that Wall Street and hedge funds and poorly run businesses want a break from hikes, is highly unimportant.

I hope the Fed doesn’t back down and I do hope we find more exposed naked zombies, and I’m hopeful a long strong of domino’s connected to pandemic era excess get their bubbles popped.

It should come as no shock to anyone if the Fed hikes. If they back down, we’ll get exactly what happened in January, as Powell backed away from chastising the market, that is, we’ll get an explosive move higher in stocks and speculation everywhere, including bank failures.

Hopefully the Fed won’t continue supporting zombies or fall under the spell of a bank like Credit Suisse, which has had literally years to adjust their balance sheet. Apparently the Swiss central bank felt pity watching that pile of garbage stay on life support, but it was suddenly systemically important after nonstop failure.

I hope Jerome isn’t going to be that idiotic or blind!

Amen

Hmmm…my totally random ass guess is that Fed definitely doing 25 basis (and near certainty GS probably had some shady trades to cover; those dudes opinions are as reliable as Zillow.)

Wouldn’t be shocked at 50 basis, although I’d bet Yellen would lose her shit in private. I still think 25 basis more likely and the Germans carried the day in the EU, pointing out that no EU banks started floating upside down.

I think it will be a pause and ‘hokish’ message. Meaning we will pause for few months, but we will hike again in six months.

OR

25bps increase and ‘dovish’ message that we are coming to an end of the hiking cycle + we will do whatever to support the ‘system’ and economy.

YIPPEEEE ! Pump those rates UP and UP ! 10%, 12%, 16%. Up and UP. And Faster. 1/2 percent increments are petty. Lets see some action. 2 points per quarter. The sooner we get them up there, the sooner we can stabilize.

But I suppose we don’t want to shock the markets right now. Steady playing it out. I get it. respect that they’re doing it.

Sure sounds like another/ECB version of “it’s transitory.”

I’m suddenly doubting rate hike, I’d still be highly supportive of beating the tar out of everyone involved in speculative excess, but I’m afraid we’ve reached a new area of hesitancy in Fed policy.

At this stage, the game of chicken between the Fed and 0dte whipsaw stupidity is quickly becoming a balance between systemic economic disaster.

I think the odds of allowing gaming forces to continue betting on the upside is now seriously changing, as bank contagion rapidly unfolds

If speculators want to bet on stocks going to the moon, the burden is shifted entirely to them in being able to manage downside risks.

The Fed can pause and clearly make that point , that further rate hikes may result in unanticipated consequences.

If market animal spirts are unleashed, into an environment of excessive downwards implosion, the Fed will look smart in capping terminal rate — as speculators get destroyed by a huge correction.

I don’t think there’s any room for mistakes, due to the deterioration of liquidity. Even the dumbest of beginner traders will start reassessing their hourly losses as capitulation becomes a severely dominant theme.

The main reason I’m tilting away from a prior post above, suggesting the Feds new magic bank failure facility is like an updated insurance policy — is like saying an insurance agency policy rider, doesn’t have a relationship to modifying valuation.

The Fed hoped to calm markets with a policy tweak, but instead, it’s calling attention to heightened risk and imminent implications.

I don’t think the new facility reduced risk, it increased risk.

The bond market is assessing that and clearly, extreme volatility is in the air.

“There is no trade-off between price stability and financial stability.”

That doesn’t seem right.

If a central bank has lost credibility and lenders and borrowers have fully embraced the inflationary mindset and agreed to loans that can only be repaid if an inflationary boom continues indefinitely, aren’t those loans guaranteed to become non-performing if the central bank takes action to halt the inflationary boom to achieve price stability. And doesn’t a sudden explosion in non-performing loans threaten financial stability. Seems like a trade-off, no?

I read that, scratched head and decided it was an awkward way to say they want to equally manage a balance of both price and financial stability, but, seems like that was written by a chatgptbot. It doesn’t make sense within the context of economic stability.

Maybe this type of confusing language is at the heart of the Fed being unable to articulate an effective means to perform its duties.

It’s an example of high priest gurus expanding on abstract theoretical dogma, then having their garble mis-translated into a message that’s open to interpretation by people that never get it.

Meanwhile, last March 2022:

March 1 (Reuters) – U.S. banks saw their profits jump nearly 90% in 2021 as firms shrank how much money they were setting aside to protect against credit losses, the Federal Deposit Insurance Corporation said on Tuesday.

I have to agree with that hedge fund the other day, who said we’re witnessing the destruction of capitalism … or something like that.

Duh, in terms of banks that are crashing in this bank run environment, one only needs to screen for exponentially stupid profit growth to see who’s exposed. SVB is a classical case of mismanagement, with unquestionable profit growth distortion.

Amen

Example of suspicious unsustainable profit growth

East West achieved record earnings of $1.1 billion or $7.92 per share for the full-year of 2022, an increase of 30% year-over-year. Our 2022 total revenue of $2.3 billion was our highest ever and grew 29% year-over-year.

Yippee

Turns out, lots of hysterical post pandemic distortions are easily found in looking at print margins