At around 4.75%, plus collateral, these are expensive loans for banks.

By Wolf Richter for WOLF STREET.

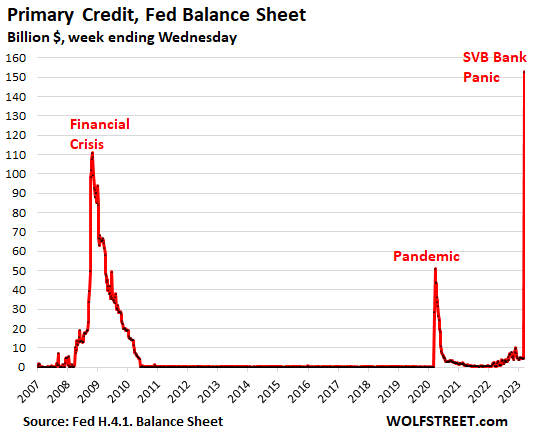

The Fed’s balance sheet through Wednesday, released today, shows to what extent the Fed has provided emergency loans at around 4.75% interest and against collateral to US banks; and how much it loaned to the FDIC which is tasked with bailing out all depositors at Silicon Valley Bank and at Signature Bank, which collapsed last Friday and over the weekend.

At the same time, it shows that the QT-related roll-off of Treasury securities and MBS continued

“Keeping an eye on potential warning signs.”

My monthly updates on the Fed’s balance sheet have had for months a section, titled, “Keeping an eye on potential warning signs,” in anticipation of what would happen. And it happened.

The section discussed two accounts on the balance sheet that are unrelated to QT or QE, but are all about whether or not the banks are in trouble: “Primary Credit” (“Discount Window”) for banks in the US, and Central Bank Liquidity Swaps for banks in other countries for dollar liquidity.

On today’s balance sheet, there are two new accounts, the Bank Term Funding Program (BTFP) and “Other credit extensions” that were announced last Sunday as part of the liquidity support for banks and the depositor bailout with the FDIC.

Discount Window: $153 billion. This Primary Credit, as it’s called, allows banks to borrow at 4.75% currently, against collateral. It spiked by $148 billion, from $5 billion a week ago to $153 billion today, the biggest jump in the data.

This is expensive money for banks, and it requires collateral, and so banks won’t borrow long at this rate if they can avoid it, and they tend to pay back those loans quickly, as you can see from the chart below.

They borrowed this way because they needed to have the funds like “right now” when depositors were yanking their money out late last week and this week, as SVB Financial collapsed and panic spread.

But in relationship to the amount of overall deposits, the $153 billion is much smaller than during the financial crisis ($111 billion). In 2008, total deposits amounted to $6.7 trillion; at the beginning of March, total deposits were $17.6 trillion, over 2.6 times the level in 2008.

Bank Term Funding Program (BTFP): $12 billion. The new thingy that the Fed announced on Sunday. Under this program, the banks can borrow for up to one year, at a fixed rate for the term, pegged to the one-year overnight index swap rate plus 10 basis points, currently around 4.6%. Banks have to post collateral, which is valued at par.

But no, banks cannot play cute games with this: To be eligible per term sheet, the collateral has to be “owned by the borrower as of March 12, 2023.” So banks cannot buy securities at market price and post them as collateral at par.

The $148 billion increase in loans at the Discount Window and the $12 billion in BTFP funding amount to $160 billion in new loans that the banks have obtained from the Fed over the past seven days.

“Other credit extensions”: $142 billion. Loans to the new FDIC-owned banks that the FDIC set up to cover all depositors of collapsed Signature Bank and Silicon Valley Bank. The FDIC transferred all assets and deposits of the failed banks into these new banks. And it’s these FDIC-owned banks that borrow at the Fed, and they have to post collateral, while the “FDIC provides repayment guarantees.”

This amount is set to decline as the FDIC sells the assets and with the proceeds from the asset sales pays down the loans.

Central Bank Liquidity Swaps: $0.47 billion, no change. With this facility, central banks can swap local currency for USD to support their own banks if they need dollar liquidity.

Total loans to the banks and to the FDIC amount to $302 billion.

QT-related roll-off continued. Treasuries roll off twice a month, when they mature mid-month and at the end of the month. Today’s balance sheet captured the mid-month roll-off of $7.1 billion in three-year notes, which was the only security on the Fed’s balance sheet that matured. A big roll-off is coming at the end of the month.

MBS come off via pass-through principal payments, most of it near the end of the month, and some smaller movements during the month. The last big pass-through of principal payments occurred at the end of February and was booked in the week ended March 1. No large payment is expected until the end of March. A small amount, as is often the case in between the large payments, came off today ($1.3 billion).

Total assets on the Fed’s balance sheet increased by $297 billion.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

4.75% may be expensive – to you – but much cheaper than the CDs the banks would otherwise have to issue. The collateral continues to earn, and therefore the net cost is significantly less than CDs.

LOL. Banks have $17 trillion in deposits. Much of it is commercial checking accounts that pay 0%.

And the national average for savings accounts (Feb) is 0.35%.

A small number of banks of the 5,000 banks offer savings accounts with 3-4%.

All the big banks — they hold the majority of deposits — are close to 0% with their savings account interest.

Banks offer some brokered CDs to raise some cash at 5% but that’s a minuscule portion of their deposits.

As the panic settles down, you will see bank borrowing at the Fed plunge because this is A BAD DEAL FOR BANKS. It keeps them alive, and that’s why they’re borrowing, but as soon as they can, they pay back those loans. Looks at the chart, how it plunged the last two times!!!

It seems that anyone who wants to put money in a bank CD should open a brokerage account instead…and then use it to buy a bank CD…

Yes, that’s the way to buy CDs

Why is it better to have a broker own a CD in your name, instead of you buying it directly?

Today I purchased 1-year brokered CDs at 5.35% that were issued by Charles Schwab.

I expect inflation to continue for years because the “Fed” created so many dollars starting in early 2020 and interest rates are still below the real inflation rate, which is being undercounted. Thus, buying a CD for various years would be the same error that SVB reportedly made: more inflation would reduce its market value aside from the reduction of its value in real dollar terms from its effectively negative return. Only a big recession or war might finally reduce inflation enough to make the interest rates I have seen on CDs palatable.

Why?

The “why” on this:

https://tickertape.tdameritrade.com/investing/brokered-cd-vs-bank-17225

Even better-Roth IRA if you over 59 1/2 years. May as well get it tax free.

Good points, but the banks most in need of help are not the giants. The relatively smaller ones are the ones who have to issue the high interest CDs. All one has to do is look at the list of banks offering CDs on a broker’s site to see this – no Citi, Bank of America, Wells Fargo on that list.

I have Wells Fargo CDs that I bought through TD Ameritrade account.

You are looking at the wrong list. I bought J.P. Morgan and Wells Fargo CDs at Schwab this week and both were in the 5% range with no call scheduled.

Thank you, Wolf. One of the few understanding that this is NOT new QE. Qe created the everything bubble. QT will bring down the beast.

Maybe this isn’t QT. But it is an increase in the Fed’s balance sheet. And the increase or decrease in the Fed’s balance sheet depends on other “unexpected” future events.

The reality is all Western Economies are full of dead weight because of the drug user addiction created by the Financialization of everything.

p.s. the Fed lending at par means marked to market bonds are getting subsidized directly

It is good to know that there was no regulatory failures (sarcasm), per NYT:

‘Jerome H. Powell, the chair of the Federal Reserve, blocked efforts to include a phrase mentioning regulatory failures in the joint statement released early Sunday evening by the Fed, the Treasury Department and the Federal Deposit Insurance Corporation.’

Maybe the regulator who was monitoring the interest hedging risk warning reported by the underlings will get a fat promotion to Fed Chair someday?

Per Bloomberg:

In a twist, the San Francisco Fed’s deputy point person in charge of monitoring the bank (SVB) until late 2021 received a new assignment afterward, becoming the regulator’s point person on Silvergate Capital Corp., according to people with knowledge of the situation. Silvergate also shut this month because of similar flaws in its deposit base and the positioning of its balance sheet.

A representative for the Fed declined to comment.

Quick question Wolf – in the 6 months or more that it takes the banks to pay this back, what impacts if any can be expected in the markets?

it looks like the SnP remained down the last two times this happened, is this time any different?

In terms of the $142 billion: The FDIC is going to pay a big chunk back as soon as it sells the assets. Auction #2 going on now. Auction #1 failed. If the FDIC cannot auction off the whole package, it will sell the assets piecemeal, which takes longer.

In terms of the $160 billion in loans to the banks: last time (March 2020), the peak occurred in the second week, and then the balance fell. Six weeks later, the balance had dropped by 50%. 12 weeks after the peak, balances had dropped by 85%. Back then, the interest rate at the Discount Window was 0.25%. Now it’s 4.75%.

I’m not going to attempt to guess how long it will take for the DW balance to drop 50% and 85% this time. I expect it to be pretty quick.

What impacts markets are the ebbing and flowing fears of a wider banking crisis — and not these two facilities, as you can tell from today’s market reaction (S&P now -1.2%).

I saw the Yellen testimony. So, big systemic risk banks get to be made whole, but small regional banks won’t be made whole. And the little buys have to pay a special assessment to make all those Chinese investors whole but not their own depositors.

Unless America’s rich & affluent are asleep at the wheel, it’s a pretty good bet that this action by the Fed / Treasury / Biden is going to accelerate the death banks that don’t meet the systemic risk thresh hold.

Perhaps that is exactly what the “regulators/too-big-to-fail banks” cabal want to happen. Nice, huh.

What are the rules for, if the rich and their regulatory lackeys are not following them? Why do I have to be careful about following the rules and not deposit more than $250k with any one bank, but the incompetent CFOs and the VCs get bailed out, again? If the bailout comes at no cost, then why wasn’t JPM keen to touch this dumpster fire and the government has to step in? Let the banks fail hard, like any other business, and hard lessons will be learned. Otherwise, systemic risks are only building up.

How is possible for Dems to survive politically, if they say we will bail out SV billionaires with deposits in excess of $250K, but not oil drillers if a Midland bank fails or Wyoming ranchers if a rural ag bank goes belly up? FDIC limits existed, so in the event of large failures, everyone got something. It seems, without really understanding the implications, and without a peep from Congress, Yellen just de facto agreed to backstop every US banked dollar. Since it would not be possible for the FDIC to charge premiums that large, Yellen, in actually, removed the stability FDIC limits provided in the event of huge, multi bank failures. Doesn’t that worry anyone?

How is possible for Dems to survive politically, if they say we will bail out SV billionaires with deposits in excess of $250K, but not oil drillers if a Midland bank fails or Wyoming ranchers if a rural ag bank goes belly up? FDIC limits existed, so in the event of large failures, everyone got something. Did Yellen just agree to de facto back stop every US banked dollar, without really understanding the implications, and without a peep from Congress? Since I assume it would not be possible for the FDIC to charge premiums that large, did Yellen, in actually, removed the stability FDIC limits provided in the event of huge, multi bank failures. Doesn’t that worry anyone?

“I believe that banking institutions are more dangerous to our liberties than standing armies; if the American people ever allow private banks to control the issuance of their currency, first by inflation and then by deflation, the banks and corporations that will grow up around them will deprive the people of all their property until their children will wake up homeless on the continent their fathers conquered.”

Thomas Jefferson

Too much happening now. I’d rather watch the NCAA tournament. Bank brokered CDs are finally yielding more than Treasury Bills. Got two today: Morgan Stanley noncallable 1 year at 5.25%, and Chas. Schwab Bank noncallable 1 year at 5.35%. The big banks must be worried and want to shore up their deposits.

That’s how you halt a run on the deposits: you offer reasonably attractive rates.

It’s about time — after screwing their customers for 15 years with near 0% deposit rates. I’m going to go shopping too.

But those rates are still below the rate of CPI inflation!

That’s the sad truth. We savers are finally getting a decent return but it seems like a hollow victory compared to inflation. My brick and mortar bank in town still pays next to nothing on savings.

Didn’t that flash $300 billion flash printing by Fed to banks and FDIC nullified 4 months of QT?

Already 10 year has plunged below 3.5% due to this printing. Wouldn’t this new printing increase inflation to hyperinflation.

Leo,

In a few weeks when the headline of my article reads, “Balance sheet plunges by $210 billion in four weeks as QT Continues, Bank Liquidity Measures Unwind,” are you then going to call the unwind of the liquidity measures “QT?” That’s be a hoot. Headline might then read, “Fed Triples Pace of QT” or something.

How do I know? Just look at the chart. Everyone knows this except you? LOL

Also it looks like the sudden neutralization of 4 months of QT has triggered huge market spikes.

The wallstreet should be able to spin up another 10% rally in name of “partial fed Pivot”.

So am expecting inflation is going higher.

“…triggered huge market spikes.”

One-day wonder? Check your charts, LOL

Wells Fargo pays .000000000001% interest on your savings. That’s why I only keep enough in there to avoid bank fees. I accidently went below the 20K minimum last month and they charged $25 penalty.

“My brick and mortar bank in town still pays next to nothing on savings.”

My mostly online bank was paying .8% on a “Money Market” account. Looking at their new account offerings(same bank) I found one at 3.48% !

A quick anecdote – I am a SVB customer (through their acquisition of Boston Private Bank – formerly Borel Bank with about 5 offices in the Bay Area). Prior to the SVB takeover in July 2021, Boston offered excellent CD rates (relatively speaking – not great but above comparable treasury rates). Had one year investments that came due in July 2022.

SVB automatically rolled over the CD’s for another year; at the rollover date the 1 year Treasury was around 3%. SVB’s offered rate was 1.2%. Needless to say, the CD’s didn’t stay at SVB.

Multiply this by thousands of customers and it’s possible that SVB was undergoing a slow rolling run.

Yes, that kind of persistent effort to screw depositors even as short-term rates have risen is why lots of deposits are now finally fleeing.

Interesting anecdote, thanks!

Yeah, you have to be careful. The fine print in bank CDs says they automatically roll over into a new one. Same term, but what ever they decide to pay you. Sometimes you can cancel the auto renewal online, sometimes you have to call.

There is a period of time you can cancel if it auto renews and you didn’t want that.

What I don’t understand is why banks would offer CDs above the 4.75% if they can just go to the Fed and borrow the money. Why would Schwab pay RickV 5.35% on a CD when they could pay the Fed 4.75%?

@Icebox

Because, as per the term sheet that 4.75% rate from the Fed requires an equal amount of collateral at par, already owned as per Mar 12th. If they don’t have that collateral, and need suddenly need money NOW… they offer CDs with very attractive rates.

So, now that you know this, what does it tell you about the strength of the balance sheet at Schwab, if they are willing to offer a 1-yr CD at 5.35%? Doesn’t tell me good things, that’s for sure.

Wolf, correct me if I’m wrong, but I believe the difference is the purpose of the money. The money being borrowed from the Fed isn’t intended to be lent out, it’s to survive should there be more bank runs. Strikes me as disinflationary to say the least.

One year treasuries were 5.25% just a few days ago. What rickv found may just be the shift in time you see in brokered CDs.

@Harrod

Doesn’t look like that to me:

Maturity Ranges Rates up to

1-3 Month CDs 5.15% APY

4-6 Month CDs 5.32% APY

7-9 Month CDs 5.28% APY

10-18 Month CDs 5.35% APY

At all durations, Schwab is offering CD rates today that are much higher than the rates offered by the US Treasury.

In fact, treasury.gov is showing highest rate was 5.25% for a 6-mo T-bill back on Mar 8th. Right now, that same 6-mo T-bill is at 4.94%

@yield

Schwab is TBTF. They have 7.1 Trillion of assets under management.

I just got an email telling me my assets at TD Ameritrade are now at Schwab so that 7.1 Trillion will grow even more the next week.

A couple of other reasons banks issue brokered CDs.

1. To establish the channel, including creating their internal department, and developing broker and customer relationships, for when they need funds in the future.

2. To avoid the negative publicity of using the discount window.

“Total assets on the Fed’s balance sheet increased by $297 billion.”

Wolf, shouldn’t this be the first sentence in the article?

It’s in the headline, except for you Andy who cannot make a simple addition 160+142=302 LOL

QE has started again but Wolf is claiming that QT is still going on in the headline. A right headline would be QE started with a bang, half of QT undone in one day of money printing.

Fed literally just undid half of the QT already in one shot of QE. I can assure you more bailouts are coming. QE infinity. I really thought this Fed is different but they are all the same. US govt continues to spend like a drunken sailor. Fed continues to bail out the wealthy. US consumers keep spending beyond their means. Where will all this money come from in the end. Whatever and however you try to explain this away and try to sound smart, in the end it is all money printing. Printing press going at full speed.

Kunal,

Make sure you come back in a few weeks when the headline reads, “Balance sheet plunges by $210 billion in four weeks as QT Continues, Bank Liquidity Measures Unwind.” I’ve got this article ready to go, all I need to do it fill in the final numbers. How do I know? Just look at the chart, LOL

Everyone knows this except you?

The articles write themselves? XD

I can appreciate Wolf’s tenacity regarding the fed not pivoting, but ultimately he will be proved wrong, probably in short order. They could have held the line with the bank problem last weekend and didn’t. They decided to push print, which is what they always do.

But it is not about being right or wrong about a pivot, ultimately it is about the destruction of the people of the united states. This continues unabated.

Per John Hussman: “Discount lending is not “quantitative easing” because the Fed doesn’t actually buy the securities. It just provides short-term liquidity, backed by collateral. That’s notable because many observers have misinterpreted a recent spike in the Federal Reserve’s balance sheet as “QE,” when it is actually discount lending under a new – though legally questionable – program called the Bank Term Funding Program (BTFP).“

On top of the loss of purchasing power due to the inflation rate being higher than the bank interest rate, don’t forget income taxes we have to pay on the interest.

To rub it in, the interest on your CD is taxed, while you are purchasing food, TVs, appliances, with after-tax dollars.

I bonds are still the best deal in town!!!

Too bad you can only do $10k per person per year.

WaterDog said,

“I bonds are still the best deal in town!!!” AGREED!

WaterDog said,

“Too bad you can only do $10k per person per year.”

There is a way to buy more than $10k per person of I Series Treasury Bonds. That way requires a bit of pre-planning. If you jack up withholding as much as you can (e.g. A person making $80k a year gross pay adjusts their W4 to have $50k withheld by the Federal Government), you can use all the Federal Income Tax Refund money (BEFORE it is refunded) the next year to purchase I Series Treasury Bonds, in addition to the $10k per person per year. In a few years, you would have over $100k in I series Treasury Bonds. If you believe that the inflation beast is not going to be tamed for several years, this may be a prudent course of action.

Of course, if you consume most of your net income right now, you cannot increase withholding unless you have at least as much in savings now to fund your living expenses as you plan to have withheld.

AGelbert,

The issue with this strategy is you haveto give the gov’t an interest free loan, in the form of extra taxes.

Personally I have as little as possible withheld, and ladder T-bills with the extra $ in my paycheck – but I’m not sure if its a better strategy.

NB: I also bought the max amount of I-bonds last year.

Right on Wolf! And remember CD rates are not only below inflation but they are also taxed which makes the return even less.

The difference is narrowing. Between now & June, I have about 6 brokered CDs that are maturing. I’m going to do my best to get them locked in at least 5% for 3 years, if the Fed keeps raising the FFR.

Next week should bring a 25-point rise with April off. I for one expect core CPE to not fall materially over the next few months. If so, then the terminal FFR may well approach 6%. What’s going to be interesting is if additional financial stresses pop up and it’s determined that someone should have caught them.

There’s no way the bean counters at SVB weren’t raising alarm bells last fall when the Fed was doing three 75 basis points increases. By January 1 of this year, it had to of been a three-alarm fire, but people looked the other way most likely.

And yet again, this proves the maleficence of the irresponsible Fed lowering rates so much and so long and especially manipulating the long end of the yield curve.

IMHO, I don’t think the Fed should be allowed to buy treasuries dated longer than 7 years. They’ve done extraordinary damage to the economy by creating this massive housing bubble.

It’s utterly scary to think that the Fed may get away with a short-term soft landing that doesn’t drastically reduce home prices across all the country. The back side of that is really scary in terms of affordability over the next 3-5 years.

5% inflation over 5 years is almost 30%, a reasonable housing correction. Of course, cash holders are doubly screwed due to existing 30 yr fixed at 3%. Mortgage will be paid with cheaper inflated $$.

And yet where was the media coverage of banks (read Fed) screwing savers to the wall for 15 years (I’d argue closer to 20). For all intents and purposes…non-existent.

(Contemplate the endless ocean of garbage, societally irrelevant news hysterias that received thousands of hours of coverage during those 20 yrs)

Even the blow-dried mannequins of the MSM are not that ignorant (if nothing else…they have bank accounts themselves).

It really is impossible to view these facts and not believe DC has *substantial* influence over what is allowed to be “news”…DC didn’t want to stir up savers into a revolt (by allowing a focal point of discussion in the MSM) or a broader, more DC dangerous discussion of why savers *had to be* strangled (death of American competitiveness, papered over by tiny rates that allowed zombie companies to survive).

The country we think we live in, really isn’t the country we live in.

Thanks for the tip – been laddering only T-bills lately, because they were consistently yielding 25-50bps more than equivalent-duration brokered CDs.

About time banks started offering competative yields.

A lot of stressed banks and entities like chuck Schwab are desperate for cash, so these types of CD rates are often a way to extract higher rates, as they try to get their trains back on track.

Distressed situations can also be risky. I almost was ready to buy Schwab shares Monday, but it struck me as a cheap deal that’s not worth ever owning.

That’s the big issue going forward, all the stocks are super overvalued with crappy balance sheets. Wall Street might have people believe p/e ratios are near fair value, but that preposterous, if you examine the three years of distorted earnings and obviously the prices.

Apparently it’s normal to think something like Costco is worth $500 a share — do your dad and don’t rely on looking at inflated, distorted pandemic valuation metrics

Good luck on the CD

The wall street tale is costco is recession proof. That might have been true decades ago, when there were good deals to be had. Now they just sell expensive gourmet foods in large lots. If consumers cut back, I think costco will lose sales.

That’s been my vibe too. I recently went to Sam’s Club and Costco recently and was disappointed in the value and experience at Costco, comparing prices on items. Very similar when you looked at it from weight, but Sam’s Club made you buy a bit less for the deal.

Costco overcrowded and understaffed, particularly the cafe. Sam’s Club less crowded and shorter lines.

I loved Costco. Lot of pleasant memories enjoying their $5 chicken or their huge pizzas. But Costco is coasting and Sam’s Club had a better deal on their membership.

Hope Costco gets better management. Would love to give them another shot.

Moody’s , S&P ratings agencies are the street dealers for the FedsMeds Kingpin, keeping America drugged up!

Submission Statement: posted by SomethingStinks via WolfStreet : ” The ratings agency are a joke; it’s like asking the pimp if his product is “germ free”. ”

Schwab says it is having problems with “cost sorting”, where people move money out of a low paying settlement account (.4% at Schwab) to a higher paying money market mutual fund (SWVXX yield is 4.58%). Schwab makes a lot money off of dummies who leave a lot of their money in their settlement account. Seems all of a sudden some of the dummies got smart. I started doing this when I first signed up with Schwab, many years ago, leaving only a dollar or so in my settlement account.

Schwab’s settlement account is actually a Schwab bank account. So Schwab bank may be losing deposits. However note that Schwab bank is FDIC insured. I would guess their brokerage side is safe. None of this recent Schwab stuff bothers me.

Explain noncallable exactly

A noncallable CD means the bank can’t redeem the CD during the full term of the CD. Many CDs are “callable” by the issuing bank before the end of the CD’s term according to a schedule issued by the bank. Basically, if interest rates go down, the bank will “call” the CD before the end of its term in order to issue CDs at the new lower rates. With a callable CD, the investor takes the risk that if interest rates go up they’re stuck in a lower rate CD, but if interest rates go down the bank will redeem it and the investor has their money back in a lower rate environment. An investor avoids the risk of having the CD redeemed if it’s noncallable.

I won’t go out 1 yr, last time I jumped in too early at 2%, thankfully it matures in May, laddered 2-6 months, got Fifth Third 6-mo CD 5.15% today, bought the stock too paying 5%, @$25, 60% of their deposits are FDIC, ex-div (announced) end of month.(.33) Only 100sh. Director bought 47,500sh at $26.40, on open market. Not a rec.

1-yr CDs could be 6-7%, who knows? I like 3-mo best now

I would appreciate it if you can post the amount that is covered by SVB’s assets, or conversely how much the government has to cover. Nobody else even mentions that SVB has any assets.

No one mentioned it because everyone knows it? A few days ago, everyone was talking about SVB’s assets and what they might be worth.

SVB Financial had $211 billion in total assets at book value as of Dec 31. This includes:

$9 billion in cash

$74 billion in loans to its customers

$17 billion in Treasury securities

$91 billion in government-backed MBS

plus some other assets.

The question is: how much will the FDIC get when it sells those assets. Maybe $150-$160 billion?

The rest of the deposits that asset sales cannot cover will be charged to the banks in a special assessment.

Where will the banks get the “special assessment” funds from?

From their profits.

There are 5,000 banks in the US, and each pays a little over time.

And it will squeeze their profit margins because now they have to pay more to attract deposits because now, they’re not only competing with each other but with Treasury bills.

In other words, it will come out of their profit margins.

They will just increase fees to us “customers”!

I never have accounts that charge me fees for regular activities. They require a minimum balance, but I need that balance anyway for basic liquidity and pay for stuff as it comes up. I collect 1.5% and 2% of spending on my credit cards FROM the banks. So if I suddenly get nickeled and dimed to death by my banks, I take my business somewhere else. That’s competition.

Ok. But, this whole thing still looks, smells and walks like a duck.

You would be right to be suspicious that the bank’s customers would be looked at to make up any hits that they will take, but I also think Wolf makes a good point that competition is taking on more than a role, and that those same bank customers need to be responsible for insuring they are getting a good deal and not being taken advantage of.

Until you achieve a certain level of systemic gravity with your finances, don’t expect the government to rush in and save you if you don’t manage your finances properly and aren’t reactive to a changing environment.

I disagree with the margin compression theory.

Big bank customers rarely switch.

As an anecdote:

My mom has been getting screwed by Wells Fargo for years. She’s only a WFC customer due to a buyout.

All their products are bad (low savings rates, money market rates, etc)

Even after the various scandals, she has refused to switch banks.

This is called “high switching costs.” It’s a know fact about banks and part of the reason big bank products are worse than their (somewhat smaller) counterparts.

Therefore, my guess is they screw their customers.

Remember when WFC got caught force placing auto insurance? You had to keep faxing them proof of insurance and then they would force place it anyways. Or all their more recent scandals opening accounts?

Or when BAC was charging $35 per insufficient funds (and the debit card would try to run 3 times). I got charged $105 by BAC in the early 2000s because they hadn’t cleared my check after 9 days.

Big banks have gotten better (after numerous lawsuits), but I still wouldn’t trust their altruism.

High concentrations in a few assets. That’s gambling.

I’m shocked, shocked, to find that gambling is going on in here.

thanks Wolf for being the voice of reason and clarity in all this bullshit being peddled oh so arrogantly by ZH and Fintwit.

ZH is bad because 1) there is an ocean of unjustified/unexplained hysteria there and 1) the user layout/interface is modern-era Amazon-shitty.

But…but…but..,if you have patience to weed through the 90% dross and translate finance-speak shorthand…you can occasionally find posts that are insightful and ahead of the curve…I wouldn’t be surprised if a unrealized-loss post showed up on ZH months ago (surrounded by crapola).

Basically, some insider pros go to ZH when their industry disgusts them too much and they want to drop a dime anonymously (same as WolfStreet).

Now, if only Wolf could pull that 1%-10% of ZH posters *here* where he could review, analyze, process, and curate their confessions, the world would be a better place.

Thanks Wolf, can count on you to provide some true context to what’s going on…

If you strictly just rely on MSM or plenty of so called financial expert YouTube, you would think the world is coming to an end and the FED just bailed everyone out aka 08 TARP style…

Well, Phoenix, the American world (USD) is coming to an end, just more slowly.

DC/Fed has grossly distorted savings/asset valuation for 20 years in order to obscure a horrible decline in America’s productive competitiveness. The hidden cancer was never treated and painkillers/hallucinogens eventually stop working (unZIRP).

I have a question

“The FDIC transferred all assets and deposits of the failed banks into these new banks. And it’s these FDIC-owned banks that borrow at the Fed, and they have to post collateral, while the “FDIC provides repayment guarantees.”

I am missing why these banks who now have the assets and deposits transferred to them must then borrow from the Fed?

thank you

The two banks also have the deposits, meaning the money that these banks owe the depositors, and the banks must have the cash to pay the depositors their money when they come to withdraw it, as many have done and are still doing.

And the banks have other liabilities and expenses that much be paid, such as interest expense, salaries, other operating expenses, etc.

I’m not buying the “sky is falling” bullshit from the billionaires and hundred millionaires who got caught with their pants down with massive deposits over the FDIC limit, where if they weren’t made whole the entire system would see bank runs and collapse. It’s just more fear-peddling to get what they want, and they did.

I also don’t believe the entire system would have collapsed in 2008. Only the ones who caused the mess and should have paid the price would have folded, as it should have been.

These latest bailouts reek to high f***ing heaven. Just because it’s not as reeky as the last bailout, doesn’t mean it’s not reeky. You can’t collapse a bubble without allowing a bubble to collapse. This shit is unreal. Let’s just let things play out in the system we already have, then pick up the pieces. I’m tired of the FED and politicians changing the rules mid-game.

“These latest bailouts reek to high f***ing heaven. Just because it’s not as reeky as the last bailout, doesn’t mean it’s not reeky.”

Yes. I knew deep down that Depth Charge would come through, LOL.

“…deep down…” Pun or not, you got to the bottom of it Wolf. LOLOL

Yes, and he’s right on point.

Depth Charge is always good for a laugh.

Wolf,

It does reek (again). If nothing else, the uninsured depositors could pay a haircut for their laziness and stupidity…but the “regulators” won’t do it for fear of starting a run (again). So the system is pretty *systemically* broken (lack of accountability, rich-stupid depositor division).

There will be some, temporally/specific bank attenuated accountability due to increased future FDIC assessments…but most of the wealthiest bad/dumb actors (depositor division) will be held 99.9% harmless (to f-up again another day).

There is a achievable world conceptually better than this…but DC has ceased even trying (being the central participant in the grossest monetary fraud in human history).

When I read your comments, I feel no one can write my thoughts in a better way than you :-).

Reading your comments is like someone reading my mind and writing it down in a way much better than I could write !

I am sure this sentiment would be shared by most of the common joe out there who could understand what’s really happening out.

AMEN!

“You can’t collapse a bubble without allowing a bubble to collapse”

IMHO Federal Reserve is seeking to deflate the bubble gradually over time, not to collapse it quickly. We shall see if they will manage to do this. So far they did manage to raise interest rate quite a bit, and to contain the fallout from this SVB debacle, so lets wait and see how things unfold.

Which is just another way of saying they want to let their Billionaire buddies get out while leaving the rest of us holding the bag.

Depth Charge

+100%

1000%

Not the entire system collapsing

just their system

Saw G Sax earned $100 million in this last emergency

Curious if true

I thought the bank runs were more a symptom of the banks not managing duration and interest rate risk? Could it be possible that this crisis is simply due to incompetence? I mean, these people should be well aware of the relationship of price and yield of treasuries right? USAA, for example, is also sitting on billions of losses in their securities portfolio, and they’re a conservative bank that mostly caters to the military world.

@Lauren,

“I mean, these people should be well aware of the relationship of price and yield of treasuries right?”

That’s exactly what I have been saying to myself!!!

Incompetence was a huge factor in this incident, for sure. Both in the bank management, ratings agencies, and in the screaming by the VCs creating a self-fulfilling prophecy.

Bailing out incompetence will just create more incompetence. Idiocracy is becoming a documentary.

We’re fish who were flooded with money at high tide. Now the tide is being sucked out by the moon (The Fed). Some of us fish are going to be caught wriggling and dying by the quick tide change.

I read somewhere that SVBs insured deposits were only 3% of the total. That tells me that we bailed out the wealthy and the politically connected corps. Yes, it stinks.

Let’s see what they do when a bank for *regular* people fails.

Yellen already told the politician from Oklahoma that they probably wouldn’t bail out regular guy banks.

My goodness, how could I have ever survived if AIG and GS had been flushed down the toilet together in a death grip in 2008?!!!

Wolf. The banks that are illiquid(SVB & Republic) are to be sold to banks that have liquidity. It would be impossible to accurately value their current loan book(s) over a weekend. A savage discount would be applied with no doubt some form of guarantee limiting losses. Why are the big five( JPMorgan etc) restricted in purchasing these banks? The system wants the stability that they provide

This mess with the banks is happening thanks to QT and rising interest rates, don’t you get that?!

If the Fed’s intentions were to keep inflating the bubble it would just cut rates and eliminate QT and tail off. None of this happens. What he is doing is building confidence in the banks to continue with his anti-inflation agenda. This inflation will persist unless there is a severe recession, but this recession also has many risks and unknowns. Better to go slowly than to go back to total QE and zero interest rates. I’m not saying this mess wasn’t created by the central banks, I’m saying the mess needs to be resolved, not made worse.

Financial Times – As Sheila Bair said: “It should replace the shock and awe of major interest rate hikes with new targets based on money supply, and aggressively shrink its portfolio, selling securities at a loss to do so, if necessary.”

JULY 22, 2022, The writer is a former chair of the US Federal Deposit Insurance Corporation and a senior fellow at the Center for Financial Stability

Waller, Williams, and Logan seem to agree. They “believe the Fed can keep unloading bonds even when officials cut interest rates at some future date.”

link Daniel L. Thornton, Vice President and Economic Adviser: Research Division, Federal Reserve Bank of St. Louis, Working Paper Series

“Monetary Policy: Why Money Matters and Interest Rates Don’t”

It’s Calvinball DC. Always has been. But as horrible as the medicine tastes, we don’t know how much worse it would have been if we ripped the band-aid off like you’re suggesting. Who else are you willing to see hurt just so the ones you do want hurt get theirs?

There is acid on my tongue when I say this, but we’ve got a system where bailing out one Too-Important-To-Fail bank is far easier than bailing out America’s economy. I’d rather we had a Too-Incompetent-To-Save system so we can allow these rich, reckless fucks to go TITS up, but that assumes the consequences are constrained.

Where my anger lives is with the attitudes and lack of forethought leading up to these events, as greed once again took the wheel, and supposed geniuses proved to be pretty incompetent on some basic matters.

DC

Janet Yellon on CNBC just said the banking system is sound. Now you know the banking system is NOT sound.

Do you really think she would say anything but that on nationwide TV? LOL

…mebbe she’s cribbing the ‘sound’ portion of the Bard’s “…full of sound and fury, signifying nothing…”, or (I would defer to DanRo on this) ‘sound’ as simply a ‘color’ of noise…

may we all find a better day.

The banks need the money because the dealers clogged the repo market.

They fail to return collateral, keep them deep in their pockets, because somebody there is in troubles. They pay fine for being late, but they don’t care.

Bailout! Didn’t even take that long.

Went directly to the stock market.

Yep. If these new programs resulted in $300 billion in four days, I only shudder to think how much new money will be created in the coming weeks.

andy,

This is the kind of BS that causes me to want to shut down the comments forever. Commenters don’t read anything and abuse my site to spread BS. It is really disheartening. Go do that crap on Twitter.

Einhal,

No, this will go backwards after the initial panic. READ THE ARTICLE.

I read it. I’m not convinced that the number won’t increase as more banks fail. I suppose if these actions stop banks from failing in the first place, then they won’t.

Wolf I voraciously read your insights. Huge fan. I still think you’re missing something here.

First, the math. +$300B is +$300B. Period. That is the opposite of QT.

Second, I feel the part not being mentioned is, again, where is this money coming from? Not existing money supply. New. That’s a form of QE.

Third, I totally get that the banks can’t use this other than for deposit liabilities. But if the rates are so punitive as you say, why are banks borrowing? Must be a genuine need. So they borrow from the Fed (new money) vs the general market (existing money).

That’s QE to me. That’s $300B that those banks would need somewhere and they got it from new money supply.

If I’m missing something please correct me.

Believe whatever you want.

Wolf, oh no. We will behave. The comments are the second best reason why people come here (after the articles). And you’re our hero. How about an IPA or two :-]

“This is the kind of BS that causes me to want to shut down the comments forever.”

So long as you then take over and write as many comments, ok, go for it! Maybe go with an array of handles, ranging from

“Wolf Charge” to “NorCalWolf”…..

“This is the kind of BS that causes me to want to shut down the comments forever.” Ha ha …..

If Powell stops raising after one left jab to the nose, or resumes counterfeiting immediately ….. you might have to shut down the comments. Because I (and others) would immediately request the biggest “mea culpa” from Wolf that he will likely ever give in his career. (I don’t claim to know what Powell will do).

I’ve been pretty aghast at Wolf ridiculing commenters as stupid because they don’t agree with Wolf that the Fed is “not trapped”.

I think this is the best site on the internet ….. but nobody is perfect. As Mike Tyson said – “Everybody has a plan until they get punched in the face”. Let’s see how Powell reacts to a light left jab to the nose, not even a knockdown .

PS Volcker’s Fed Funds rate was 16% in 1982.

I don’t think “belief” is relevant here. Isn’t this a pure (1) arithmetic and (2) new vs existing money supply concept?

I’m not trying to “believe” anything. I’m trying to understand facts and interpret them appropriately. My read of factors 1 and 2 = QE pop. Honestly would appreciate logical correction if I’m missing something here.

I think the idea is it will go similar to how the BoE handled the Glit crisis.

Liquidity now to support the market, which you could maybe kinda sorta argue is QE, but sucking that liquidity back out as soon as the crisis is over & otherwise resuming tightening.

I’d still put my money on +25bps later this month. Job market is still hot as hell.

Guys, the point is that it’s not ZIRP and it’s getting paid back in short order. Whole different ballgame than QE.

This is how the fed should behave and why they exist. They should not be in charge of stimulating the economy through experimental means.

Tom S,

Agree – and I’d go even further and say the Fed should not be buying bonds or manipulating the yield curve outside of an actual crisis.

Half the fun is reading the comments!

Wolf is one hell of an economist. Twitter is filled with wannabe economists. Go join the new QE party there.

Wolf always struck me as a finance guy not a straight economist (I guess he could be a corp. economist). He doesn’t use the words marginal, utility, or disequilibrium nearly enough for an academic economist.

The Bank Term Lending Program (BTLP) does allow a bit, or more, of game playing:

The securities used as collateral must have been owned on March 12, but did not necessarily need to have been purchased at par. A large portion probably will not have been. So it’s possible to borrow more than the market or purchase price of the securities posted. Nice deal. Most lenders will not lend at 100% of par, or even 100% of market value of collateral, and will require additional collateral if the value declines. Not for the BTLP.

The term sheet does not say who gets the interest on the collateral during the loan term. If the bank borrower does, the deal is even sweeter. Interest paid on the BTLP would be offset in part by interest paid on the collateral.

Also, it’s a wry comment to say QT continues. Roll off under QT of about 8.3 BB, but net expansion of balance sheet through discount window, BTLP and FDIC loans of $297 BB. Does that look like a dose of QE?

The Fed does much good, but in doing so also serves the interests of the financial aristocracy.

Always enjoy your writing including links to stuff not easily available elsewhere such as the BTLP term sheet.

Here is reality. Here is what banks are actually doing as soon as they can. Because for banks, these loans are a BAD DEAL. Banks are PAYING OFF THE LOANS AS SOONS AS POSSIBLE. You saw that during the financial crisis and during the pandemic — and back then interest rates at the Discount Window were 0.25%. Now it’s 4.75%

You cannot explain it to laymen having no clue about monetary policy or its mechanics. Their gumption tells them it’s QE so it must be QE -)

Here is what I don’t understand. There are banks that are “too big to fail” meaning that if they get in trouble they threaten the entire financial system and would need to be bailed out. Why do we let this situation persist? Why can’t these TBTF banks be whittled down in size until they are no longer threats to the financial system? It’s like these banks are financial time bombs – let’s defuse them so they are no longer a threat. Why hasn’t this been done?

It’s not the TBTF banks that got into trouble, it’s the regional banks with very concentrated depositors that failed because regulations were loosened up on those banks in 2018, and because regulators fell asleep, and the TBTF banks are bailing out First Republic.

any comment on the SVB CEO on San Fran Fed Board?

One might think he could have had an inside track on Fed policy which might have prompted proper hedging.

I don’t think it’s any one factor, but a “concentration” of them. SVB was without a risk officer when interest rates started to rise for 8 months. The bank also made an incredibly stupid bet on ZIRP.

The whole idea of concentration risk was something introduced to me by these events, but also VCs screaming like little girls and instituting a panic. Hell, I hate Musk, but at least he didn’t RHEEEEE on Twitter after getting caught in a $44 billion bad deal of his own making.

The CEO, Parker, of SVB sold all of his shares two weeks before they went under. He must have known something. He just went on a vacation at his 3.6 million luxury home in Maui, Hawaii. There may be some claw-back of the money that he got based on inside information he had when he sold the shares.

It’s like there were good reasons for regs and not a socialist plot to turn your dollars gay.

I just shake my head at how some bitcoin investors thought a lack of government involvement/central bank was a good thing and bet it all. Whatever you think about fiat vs. gold vs. whatever, the reason why central banks are universal was because of a good reason. Trusting some guy with a bad haircut to hold your money is insanity. The guy has your money and still cannot afford good grooming!

Bankers can be some of the most reckless dudes around. After all, the entire idea of “deposits” is a complete fantasy. At best, you’re buying resold insurance–a bit sketch by the way–because it’s fiat money, so the government can theoretically just pay more.

If I am JPMorgan, Bank of America, Wells Fargo, and the other major banks that deposited $30 billion into First Republic, does that mean if First Republic gets taken over by the FDIC then my $30 billion is fully insured? Since the $250K is no longer the FDIC insurance limit, why not deposit money into First Republic. This is the safest investment in the world fully backed by the U.S. government.

Seems like these bailouts are bs ,FEDS gave the money to make system look good.Banks only loan money to people who don’t need it ,personal or corporate.Crony Capitalism

What regulations were loosened up on those banks in 2018?

https://www.congress.gov/bill/115th-congress/senate-bill/2155

Excerpt of summary from FactCheck:

The Republican-controlled Congress passed the 2018 legislation with some Democratic support. It passed the House 258-159, with 33 Democratic votes. And it passed the Senate 67-31, with 16 Democrats joining Republicans.

Among other things, the 2018 law reduced the number of banks that were subject to stronger federal oversight. Under Dodd-Frank, banks with assets of more than $50 billion were subject to stress tests, higher capital requirements and other “enhanced prudential standards” designed to reduce risk.

Specifically, section 401 of the law largely eliminated enhanced regulation for banks with assets between $50 billion and $100 billion, and gave the Fed discretion to apply the enhanced standards on financial institutions with assets between $100 billion and $250 billion, including how frequently to conduct required supervisory stress tests.

At the time, the nonpartisan Congressional Budget Office wrote that the 2018 legislation “would result in fewer assets being subject to enhanced prudential regulation and would thus increase the likelihood that a large financial firm with assets of between $100 billion and $250 billion would fail.”

There is something, IMHO, very fishy about public blame on this “concentrated deposits” fad. Very fishy. SVB was ~$200Bn market cap! Not a small toy. It was highly rated. And now sudden multiple downgrades? Chris Whalen has gone on youtube (realvision) to state SVB “did nothing wrong” in their asset liability. REALLY?

What if:

–another euphemism for “concentrated deposits” is “circular banking”: the debtors are the depositors.

VB was a circular “bank”:

that’s why no buyers.

that’s why FDIC didn’t even attempt a bridge bank;

that’s why the Fed raising FDIC limits to every depositor in SVB doesn’t mean anything;

that’s why SVB management had both extremely high HTM portfolio of assets, and high proportion of uninsured deposits.

it wasn’t a real business.

The US media routinely lies, and it doesn’t cost them anything: I strongly suspect SVB uninsured deposits were not “payroll” as blurted out.

it merely made loans to VCs, and they turned around and parked that money back as SVB deposits. This was a $200bn market cap company on the US market.

Perhaps the loans were made so that borrowers (VCs) could show the liability while hiding the deposit from accountants, or vice versa, they could show the deposits while hiding the liability

SVB was leveraged 185 to 1. That’s why there were no buyers.

Can anyone tell me why bonds are reacting like they are the past 2 days?

Thank you.

Because with the Fed’s new lending facility, banks will never have to sell them for below par. That means that the prices set when they were issued in the past 13 years (the ZIRP era), are now the floors.

Danno,

Yields SPIKED this afternoon. Look at them! The 10-year yield spiked by 17 basis points in a couple of hours at the end of the day. There was a massive selloff in bonds at the end of the day.

Einhal,

This is a thoughtless statement. Read the article, use your brain, or at least look at the picture.

Banks are PAYING 4.75% in interest. So they borrow at 4.75% to not have to sell a bond that might yield 2%? Are you effing kidding me? How stupid do you think banks are??

Look at the chart: Banks pay these loans off AS SOON AS POSSIBLE because they’re bad BAD DEALS for the banks.

Selling the 2% bond now would force them to take the loss now. Until this crisis it may have been more convenient to pretend assets were not under water and borrow even at higher rates for a short time. Now that the question is less of how big a profit can be shown but more a question of survival the incentives of bank managers shift. The SVB event signaled a secular shift in interest rates and illustrated the real consequences of pretending it is not happening.

Wolf,

Sometimes I do not feel as altruistic.

Bad deal for banks Bad deal for bankers.

It is not the individual bankers’ money if they lose.

One could imagine a scenario of avoiding M2M rules by not selling their 2% paper that took a 15-20% haircut last year through JPow’s rate hikes?

If trying to preserve a bonus pool or RSU is the goal, extend and pretend could be the game. Borrowing at 4.75% does not to spare the recognition of a loss seems less expensive then?

Assuming on my part of course. Who knows for sure, lots of moving parts.

But feeling that a banker acts in the bank’s interest over their own self interest seems naive. Grifters gotta grift ya know.

Thanks again for the info, and have a great weekend Wolf!

Reminiscing the past

“We’ve got strong financial institutions…Our markets are the envy of the world. They’re resilient, they’re…innovative, they’re flexible. I think we move very quickly to address situations in this country, and, as I said, our financial institutions are strong.”

– Henry Paulson – 3/16/08

“I have full confidence in banking regulators to take appropriate actions in response and noted that the banking system remains resilient and regulators have effective tools to address this type of event. Let me be clear that during the financial crisis, there were investors and owners of systemic large banks that were bailed out . . . and the reforms that have been put in place means we are not going to do that again.”

– Janet Yellen – 3/12/23

Regulators blurt out just like a seasoned speak politician, irrespective of their promises to sheeple truly filled or not.

No accounting demanded

we are getting shafted again. The ‘buck’ due always lands as DEBIT in taxpayer’s account. Guaranteed.

Sunny, every time they march out the Treasury Sect to say everything is fine, I know it’s definitely not fine.

“How stupid do you think banks are??”

great question

LOL, touché

Wolf you may say the comments are the bane of your existence but to me they give additional insight not covered in your articles because you’re not stupid enough to think of the questions an average American would think of.

So when you reply to a stupid question you’re fighting misinformation, even if it comes at a terrible cost to your mental health it quells any stupid thoughts from fomenting in my head.

Looking at the balance sheet today I had similar concerns. Reading your articles and replies gave me a clearer understanding.

I learn just as much from Wolf’s answers as I do from his article.

Maybe Wolf can save a ton of personal effort over time with only writing out the day’s pertinent headline and never write an actual article body again, only respond to comments LOL! (no more RTGDFA, though)

“Wolf you may say the comments are the bane of your existence but to me they give additional insight not covered in your articles because you’re not stupid enough to think of the questions an average American would think of.”

Damn it, this may be the best description of the comments section of this blog I have ever read.

C’mon FOLKs,,, get real!!!

Wolf is absolutely the very best ”reporter” on the subjects he follows,,, far damn shore…

What he recognizes and helps with, are the wide varieties of our experiences in those venues…

Commentariat just widens Wolf’s reporting, a fact that I am convinced he not only knows but appreciates as his comments on his articles indicates IMHO.

Thanks to all commenters in good faith on Wolfstreet.com,,, and many more thanks to Wolf, demonstrated by $$$ support twice a year, so far…

(Probably already save US, the family US, at least a ton, maybe even more.)

I agree. The comments and replies really hammer the points home. Just today I was a bit confused about the mini bounce in SPY and crapto so I peeked at the “relevant news” and saw a lot of “Pivot” and “QE” rhetoric by “respected” analysts and investors and I mean A LOT of it, some of that filters in here and Wolf replies with clarifications backed by data which just clears things up very nicely for those of us without the qualifications.

I hope Wolf deletes some of the rhetoric though and saves his energy for the great articles, it’s enough to reply to the same nonsense once and just get rid of repeating BS.

I’ll trust the lower Treasury Direct rates over the commercial banks right now. Especially because I don’t have to keep so much locked up for a full year.

Very helpful article as always.

What struck me was the meteoric rise of bank deposits between 2008 ($6.7T) and now ($17.6T). Looks like “wealth”, at least nominally, exploded by 2.6x over the last 14 years. I feel left behind…

Don’t forget the concomitant rise in bank loans over those past 14 years which offset much, if not most, of those deposits if it make you feel any better. I’d be interested in knowing how much that side of the equation exploded, as well.

Heard Shelia Blair say the vast majority of depositors at Calif bank were not poor and 250,000$ limit was enough, meaning I guess if you have that much money you should know the risk and that’s how the kookie crumbles. Seemed like she was always a smart woman , yea too many bailouts except for the poor sucker washing the floors and paying rent to the “man”

There is nothing more powerful in this country than 50 billionaires with big megaphones.

The way Congress should pay for this depositor bailout is by putting a 50% wealth tax on everyone who advocated for this bailout.

Yep. HALF. Thanks for playin’.

Yes!

“The way Congress should pay for this depositor bailout …”

Havent heard a word of “clawbacks”…..the bonuses and high salaries of the officers of this bank.

Shouldnt there be a “if bailed out, then x,y and z happens?

There must be a price for bad decision making.

Agreed.

They’ll likely still make millions.

If Bill Ackman and David Sacks wanted a law passed in this country, all they would have to do is tweet and it would be passed in a week.

AMEN! (to both the above & below Wolf posts)

Yup, “_________ (insert billionaire) hit the phones when this crisis hit”

They prob yawned and ordered lunch. Lol

Wolf, are you saying America isn’t actually a democracy? *me taking cover*

“But in relationship to the amount of overall deposits, the $153 billion is much smaller than during the financial crisis ($111 billion). “

The comparison doesn’t seems right … or am I misreading this?

You cut off the second part. This is the whole thing:

“But in relationship to the amount of overall deposits, the $153 billion is much smaller than during the financial crisis ($111 billion). In 2008, total deposits amounted to $6.7 trillion; at the beginning of March, total deposits were $17.6 trillion, over 2.6 times the level in 2008.”

Never waste a good crisis. Covid 2 Crypto, PPP loans 2 Bank Liquidity Crisis. The Shock and Awe campaign never ends. Inflation is everywhere. FTX CEO on house arrest, Banks collapse and no one goes to jail, just give them more money. It all makes sense now, since Colorado legalized mushrooms. I will focus on the positive, wife got her new Samsung microwave $249 from Lowe’s installed today. My new 7/11 as the best damn gourmet cinnamon rolls money can buy if I get there early.

“New 7/11”

They’re never new. They come pre slurpee spilled, throw up stained, blood splattered, grimey, dingy, gas reeking, toilet overflowed, beer glass broken concrete palaces of commerce. Lol

I agree that the commentary, argument and opinion expressed here in this section are almost as interesting and valuable as the article itself. Of course, I will concede that I wouldn’t put up with dimwitted scribble myself, if I had my own website, but I’m glad Mr. Wolf does.

It’s actually amusing which is a refreshing change from the 99% of bla, bla, bla on other comment sections. In a way and for some unknown reason even the extraneous commentary here turns out to be of some benefit when it needles Mr. Wolf into a howl or two.

The fact that Wolf responds to comments at all makes him unique to most financial websites. The frustration he feels dealing with the public-at-large is that while he presents facts and charts al the time, we all bring our own biases, beliefs and conspiracies to those facts. The sad thing is that since it has been proven over and over again that rules can be changed at every panic, it is impossible to really predict a logical, rules-based future on these facts and charts.

The moderator being the most toxic guy on here is quite the inversion!

Back under the bridge, back I say, sunlight kills your kind.

Wolf continues to be awesome! His posts are awesome and his moderation skills with patiently replying to the new and uninformed (thank you!) as well as the lying self-serving idiots, is perfect.

Most blog owner/writers don’t even bother.

Thank you, Wolf!

Real News,

It makes one wonder just how bottomless the comments are that Wolf filters out. We just see the patient frustration that leaks through.

During the financial crisis in 2008, did the balance drop because the banks repaid the money with funds from the government (i.e. TARP)?

Sorry if dumb question.

“Discount Window: $153 billion. This Primary Credit, as it’s called, allows banks to borrow at 4.75% currently, against collateral. It spiked by $148 billion, from $5 billion a week ago to $153 billion today, the biggest jump in the data.”

Bet if they had been paying depositors 4.75% they might not have had so much trouble hanging onto deposits in the first place.

Just a tempting speculation…

Hello Wolf

Where did you find “Bank Term Funding Program (BTFP): $12 billion” in balance sheet?

Thank you

I found it

Thank you

On the balance sheet, under “Loans”

This moment reminds me about Arthur Cashins “buy buy buy” under the Cuba missile crisis.

If QE and pivot is on, society as we knot it will unravel, and we will not have to pay the creditors for being wrong.

Sell, sell, sell.

if this portal would have critical thinking, it would ask questions like this. But seriously there is a pronounced pro-Fed bias. We need people who can connect a few dots instead of just reporting current ‘facts’

“…pronounced pro-Fed bias”

LOL. But there’s something you should understand:

I railed against the Fed during QE and ZIRP for years. That’s how this site’s predecessor site (Testosterone Pit) started out, and it continued with Wolf Street.

When the Fed’s QT took off in 2018, I supported it because it was undoing the damage of QE.

When the Fed bailed out the repo market in 2019, I railed against the Fed.

When the Fed went hog wild in 2020, I shredded the Fed.

When the Fed ignored the surge in inflation in early 2021, still doing QT and ZIRP, I called it “the most reckless Fed ever.” Google the phrase, LOL. And I did for months until the Fed got serious about tightening.

When the Fed started hiking rates and then started QT, I supported it.

Get the drift? I hate money printing and interest rate repression. I you want a propaganda hype-and-hoopla rag for money printing and interest rate repression, this is not the place. You need to go somewhere else.

I understand that there are bloggers out there that railed against QE. And when the Fed switched to QT, they first denied it, and then railed against the Fed for doing QT, and they railed against the Fed no matter what the Fed does. To me, that’s just clickbait idiocy.

“the most reckless Fed ever.” Nice # 1 and #2 spots

I tend to find myself coming to this site when the fed starts QT. Unfortunately, just like back in 2018/2019 the party is now over. It was a good run, but not nearly high enough or long enough.

Best of luck to everyone.

Tyler,

So when the liquidity measures unwind and the balance sheet drops by $210 billion over a one-month period (i.e. $90 billion QT, $120 billion liquidity unwind), can I call it “Turbo QT” and “Powell nearly TRIPLED Pace of QT”? You’re making me do it, LOL

And thank you for doing that. There is so much shallow commentary out there by so called analysts whose memories last no further than the current news cycle. They will never connect the dots from the Fed’s 2020-2021 money-palooza to its inevitable denouement. Your filling in the gaps is a great public service.

…have always found Wolf-sama the best counter to the bane of solely next-quarter thinking…

may we all find a better day.

Wolf…

Has the Fed issued their 2022 report yet?

Federal Reserve Banks Combined Financial Statement for 2022?

They issued the one for 2021 on March 10 of 2022. Is it late ? I cant seem to find it.

Here you go:

https://wolfstreet.com/2023/01/13/despite-losses-since-september-the-fed-still-made-a-profit-for-the-whole-year-2022-remitted-76-billion-to-us-treasury-dept/

thnx

Thanks …. but what I have found was this

https://www.federalreserve.gov/aboutthefed/audited-annual-financial-statements.htm

that’s for 2021 and issued March 10 of 2022.

What I cant find is the same report for the year 2022 which should be out by now. Have you seen it, and if so, and if it is no trouble, could you kindly provide the link. Thank you.

The 2022 audited statement will come out shortly. I covered the preliminary statement for 2022 (the link I gave you) that the Fed released in early January. That’s how it goes every year: in early January, the Fed releases the unaudited preliminary statement and I cover it; sometime in March it releases the full audited version, which I don’t cover because by then it’s old hat.

This one’s wired a bit differently, but couldn’t US govt relax on Corporations to remit foreign money home eg Apple Microsoft etc virtually self bank, and have lots of dish sitting outside the US that could have plugged this hole.

Headline:

“Kevin O’Leary offers ‘tough love’: We don’t need regional banks in the ‘internet age'”

Right…

Rather than regulating banks properly by better determining which ones are ACTUALLY systemically dangerous by considering the characteristics of their depositors as well as what percentage are over the FDIC limit instead of just a dollar amount, somehow dealing with incompetent and fraudulent ratings agencies and, best of all, bringing back Glass-Steagall’s separation of FDIC insured commercial and investment banks, he apparently wants more too-big-to-fail banks which should be TOO BIG TO ALLOW TO EXIST. As an added benefit, it makes CBDC easier, at which point somewhere down the slippery slope your money WILL be controlled by the State.

What an absolute maroon…

Also:

“In August 2021, it was announced O’Leary would take an ownership stake in the parent companies of FTX.com and FTX.US as part of his compensation for becoming a “spokesperson and ambassador” for FTX.”

“Kevin O’Leary grilled on why he kept money at SVB if management were ‘idiots’”

“Saving” an insolvent bank by giving them a loan on highly overvalued (“at par”) collateral at 4,75% interest is an interesting concept.

The assumption is that the bank is illiquid but not insolvent. Those are two very different concepts.

Silicon Valley Bank was deemed insolvent.

I am pessimistic with 12 years ZIRP Fed can extricate us from it. Fed could stop here and the lag affects on just the residential and commercial real estate market should kill the economy by end of the year. Government is already saying they need $1.5T – $2T deficits for next 10 years to keep it afloat. When you see four bank roaches there are more roaches around.

longstreet wrote: “Haven’t heard a word of “clawbacks”…..the bonuses and high salaries of the officers of this bank..”

Clawbacks are only for poor people. If your mother lands in a nursing home, and has to eventually go on Medicaid, the gov’t will look back 5 years to see if she gave any of her money away. But the $84 million in bonuses & stock that the SVB executives got in the last 2 years…..pft. Forgetabout it. Just look away (that is what the gov’t does).

right you are.

SVB was doling out money to groups with political and ideological missions.

“The three top officers of Silicon Valley Bank earn a combined $18 million in salary and bonus while sitting on a powder keg” according to an article in the WSJ 3/17/2023

Yet, there seems no consequence for either of these profligate activities. And someone walks away with a lot of money, laughing up their sleeve.

SVB officers were milking it for as much as they could, probably knowing it was probably going to go belly-up, after which they would get nothing. I think clawbacks are appropriate, especially if gross mis-management has occurred. It has occurred.

Yellon just said that they will protect banks that could cause systemic risk to the financial system. Note, she didn’t say anything about banks, such as regional, and community banks that don’t cause the same risks.

The big banks will get rescued, and smaller ones’ will be on their own. Same with the depositors of those smaller banks. They could lose their funds if they are over 250K.

Swamp.

I don’t see how the FDIC can not, going forward, legally not cover all deposits.

I am not a Constitutional lawyer, but “equal protection” leaps to mind.

The move they did on last Sunday has a magnitude of which Janet Yellen has no idea….among other things.

I even think there is an outside chance the FTX “victims” might be made whole as well.

longstreet

Please don’t peddle this BS to me. Find someone else.

They replayed her statements on the media. She said exactly what I said she said. END OF STORY.

FDIC is allowed to cover all deposits if, by not doing so, there is a “systemic risk” to the banking industry. This is of course a judgement call. Frankly, I do not see where wealthy depositors losing billions is a threat to the banking industry. Elon Musk loses $40 billion or so of his net worth every once in a while. He does not clamor for a bail out, nor would he get one.

Wolf, since these loans are required to be backed by assets do you see the USA drifting into a situation like many of the European banks have, where they hold assets (like real estate) but can’t (or won’t) sell it because they can’t realize the value of the loan it’s held against without taking losses they can’t afford?

The great thing about fiat currency is the Central Bank can print it to infinity thus can never run out of the stuff, i.e. can never go bust. Just ask any Argentinian or Zimbabwean.

P.S. I see Credit Suisse is on the wobble again. Oh yes, and bitcoin’s just gone over £20k. Interesting times?

medial…

Credit Suisse can dig into that Swiss National Bank stock portfolio money…….the money the SNB accumulated with privileged central banking info.

Yep. I don’t think this whole $hit is ending until at least 10 to 12 trillion new money is printed.

It’s over for Inflation fighting.

Since someone brought up bitcoin.

I was shocked when I walked past one of the coin star machines on Friday and saw a sign on it advertising : “Convert your money to Bitcoin here”.

“At the same time, it shows that the QT-related roll-off of Treasury securities and MBS continued”

I’m not sure about that.

And how is the Fed buying devalued treasuries from banks at par different from QE?

I know you are going to say that is all just bank loans. So that’s different from loans to the government?

1. “I’m not sure about that.”

As I said, $7.1 billion in 3-year bond matured on Mar 15 and rolled off without replacement. And the Fed’s Treasury holdings fell by $7.1 billion. That’s QT. Nothing else matured on the 15th, so that was it. The next Treasury maturity date is Mar 31, and a whole bunch of stuff matures. You can just look this stuff up in the SOMA holdings at the NY Fed and compare it to the balance sheet entry to Treasury securities. It’s not rocket science.

Here is the SOMA page:

https://www.newyorkfed.org/markets/soma-holdings

Scroll to the bottom to the “SOMA Historical Data Export Builder” and download the data to see what matured and rolled off.

2. “And how is the Fed buying devalued treasuries from banks at par different from QE?”

Nonsense, as you suspected. The Fed is NOT BUYTING ANYTHING. These are LOANS at 4.75% against collateral. This is very expensive for banks. Bank can borrow from depositors and unsecured bondholders WITHOUT collateral.

Wolf. Correct me if I wrong, but aren’t the Fed’s purchases of treasuries from the government actually loans too since the government retires them at maturity by repaying the loan?

So what’s the difference?

You’re twisting everything ad absurdum.

Wolf – well that explains everything.

LOL, yes. Once the discussion has entered the absurd, it’s beyond me and I leave the chatroom.

A question for Mr. Wolf R.

Very good explanation of the financial backstory and current situation with the banks, The FED, and the FDIC.

However, I do not see the political variable being discussed here and it must be.

How did the fact that SVB and their depositors are financial and ideological supporters of the current administration factor into the administration’s decision to bailout SVB and Signature?

As long as you are throwing political lobs, wasn’t it the ardent and outspoken Republican Peter Thiel who initiated the bank run with his tweets? Did he orchestrate this debacle as a political strategy, then intentionally suffer a small loss in SVB to mask his larger effort?

Guessing about political motivations gets us nowhere. The RepDem uni-party is a self-serving wealthy bunch that is slowly pilfering and destroying the country, or what’s left of it. The Reps and Dems take their turns grabbing your cash. Leave it at that.

Yep. Time to drag Ross Perot out of the grave. My brother-in-law (a tough cookie himself) worked for him and thought very highly of him.

But now no sane rational candidate could survive the woke hurricane.

“There’s even moral hazard for employees who don’t get bonuses. Federal DEPOSIT insurance allows employees of closed banks to continue working for 45 days, and then DEPOSIT insurance pays them an additional 1.5 years of salary.”

Would this have happened if the Fed hadnt depressed long rates as they did?

If the yield curve had been POSITIVE?

It is the fake LONG rates that put SVB and others in a trick box.

And it is the Fed that sopped up 2.7 Trillion (at the highs) in MBSs and Trillions in long maturity Treasuries to pound long rates.

It is this situation the Fed itself in that kept the Fed prior to 2009 OUT of the long end.

SVB bank dragged IWM. The death of the best of the best is

good for smallness.

RRP rates plunged. It help the flyover crumb banks.

I’m not seeing any kind of “plunge” in the overnight RRP rate. And it would surprise me because the Fed bracket the repo market with its RRP offering rate (4.55%) and the repo bid rate (4.75%). And the SOFR has been stable too.

I see a big drop in the Treasury bill yields though — a sigh of HUGE demand.

All my money is at TreasuryDirect and brokerages, where access to my funds is walled off and accessible only by me.