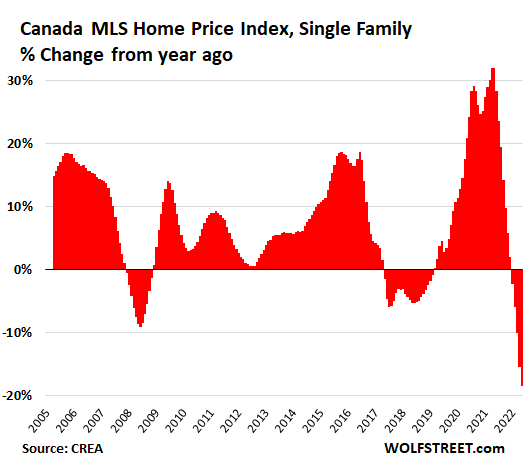

Year-over-year, home prices plunged by the most on record as the seasonal uptick in prices was far smaller than a year ago.

By Wolf Richter for WOLF STREET.

This is the beginning of spring selling season. So let’s see. Home sales in Canada rose by 2.3% in February from January, but that was less of an uptick than it should have been, and on a year-over-year basis, sales plunged 40%, compared to the 37% plunge in January.

Prices of single-family houses in February rose 1.2%. But that was puny compared to the year-ago month-to-month jump of 4.8%.

So year-over-year, prices plunged by 18.5%, the largest drop in the data, according to the Canada Home Price Benchmark Index for single family houses by the Canadian Real Estate Association (CREA). Since the peak last March, the index has plunged 19.1%.

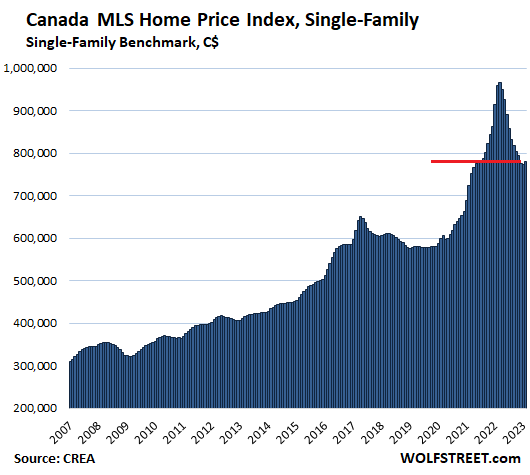

In terms of Canadian dollars, the Single-Family Home Price Index for Canada ticked up by C$8,900 in February from January, but that was puny compared to the C$44,000 increase a year ago, and so year-over-year the benchmark price plunged by a record 18.5%, to C$781,300, rolling the price back to July 2021.

Hangover after the free-money binge. This most ridiculous home price bubble was triggered by the most ridiculous money-printing binge and interest-rate repression globally and in Canada. But now consumer price inflation is tearing up this strategy, as it ultimately always does. And the Bank of Canada has now raised its main policy rate by 425 basis points to 4.5%. And its Quantitative Tightening is in full swing. Consequently, mortgage rates have risen across the board from the levels a year ago.

Canada’s housing market didn’t even have much of a reset during the Financial Crisis – unlike the US housing market – and a splendid housing bubble ballooned out that.

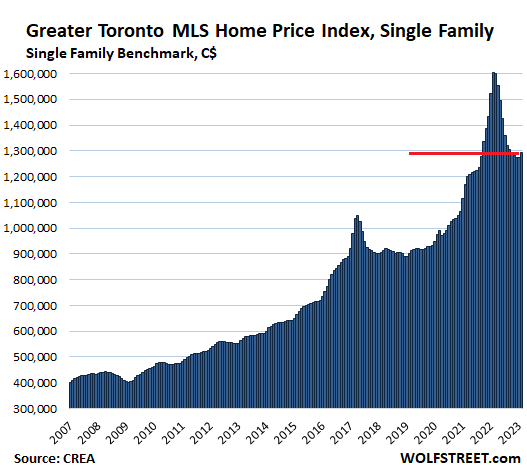

Greater Toronto Area: The MLS Home Price Index for single-family houses rose by 1.6%, or by C$21,000 in February from March, to C$1.294 million. But this was only about a quarter of the C$80,000 month-to-month jump a year ago. So year-over-year, the index plunged by 19.3%, or by $306,800, both the biggest year-over-year plunges on record:

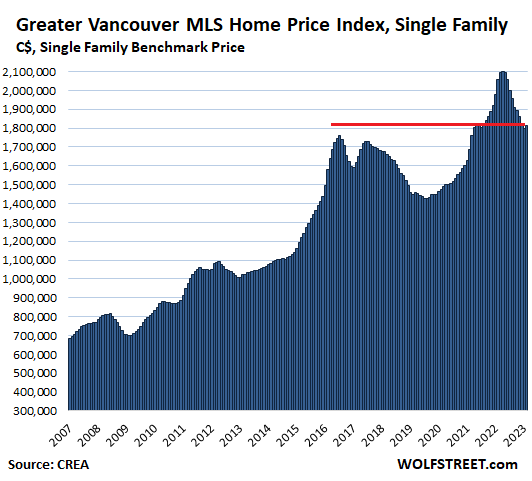

Greater Vancouver: The MLS Home Price Benchmark Price for single-family houses ticked up by 0.7%, or by C$12,000 in February from January, to C$1.812 million. But the month-to-month jump pales against the C$80,000 jump in February 2022. And so year-over-year, the index plunged by 12.0%:

- From peak in April 2022: -13.7%

- Year-over-year: -12.0%

- Drop in 10 months from peak in April 2022: -C$288,000

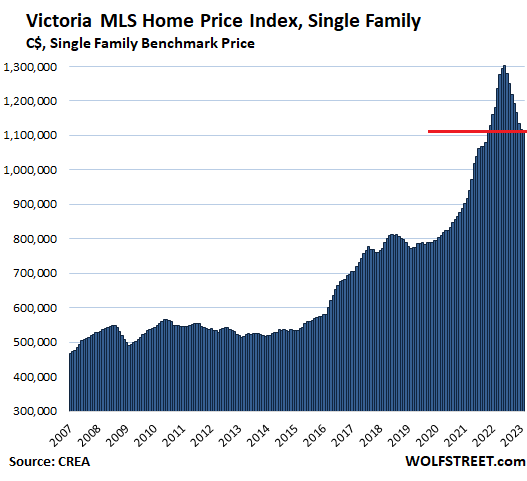

Victoria: The single-family benchmark price dropped by 0.4% for the month, despite the spring selling season, to C$1.113 million:

- From peak in June 2022: -14.5%

- Year-over-year: -5.7%

- Drop in 8 months from peak in June 2022: -C$162,200

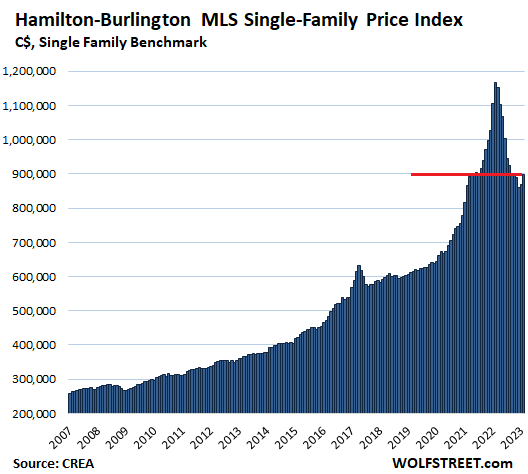

Hamilton-Burlington metro: The single-family benchmark price jumped by 3.1% for the month, to C$898,000. But the month-to-month jump was less than the 5.3% jump a year ago, and so the year-over-year plunge increased to 23%.

- From peak in February 2022: -23%

- Year-over-year: -23%

- Drop in 12 months from peak in February 2022: -C$268,300.

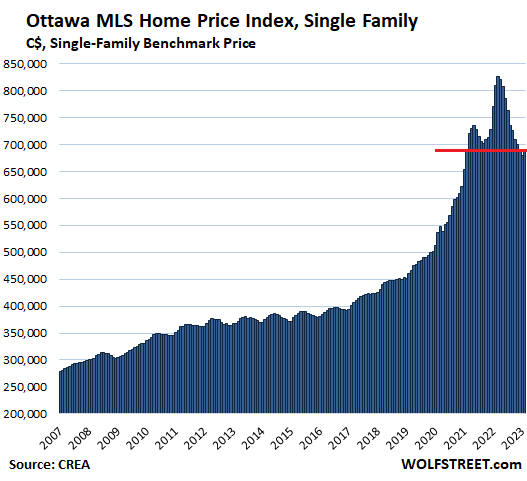

Ottawa: The benchmark price of single-family houses rose 1.3%% for the month to C$688,500. But last year in February, prices jumped by 5.0%, and so the year-over-year drop worsened to 15.0%:

- From peak in March 2022: -16.7%

- Year-over-year: -15.0%

- Drop in 11 months from peak in March 2022: -C$137,700:

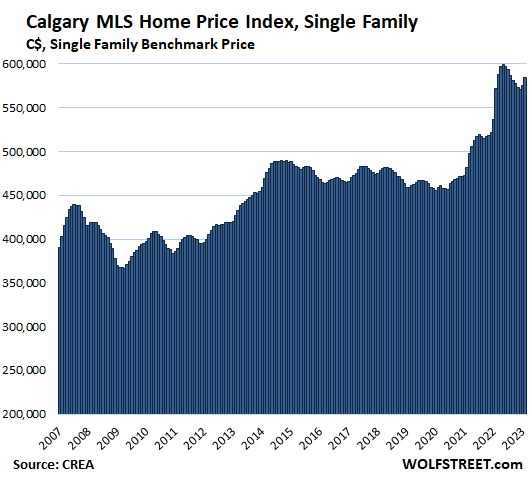

Calgary: The single-family benchmark price jumped 1.7% for the month, to C$584,700. But that was a lot lot less than the 6.6% month-to-month jump in February last year, and so the year-over-year increase got slashed to just 2.2% (from 7.1% in January):

- From peak in May 2022: -2.4%

- Year-over-year: +2.2%

- Drop in 9 months from peak in May 2022: -C$14,100.

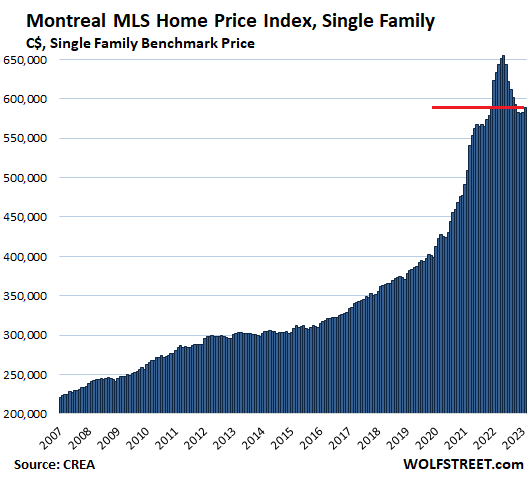

Montreal: The single-family benchmark price rose 1.1% for the month to C$589,500:

- From peak in May 2022: -9.9%

- Year-over-year: -6.9%

- Drop in 9 months from peak in May 2022: -C$65,000

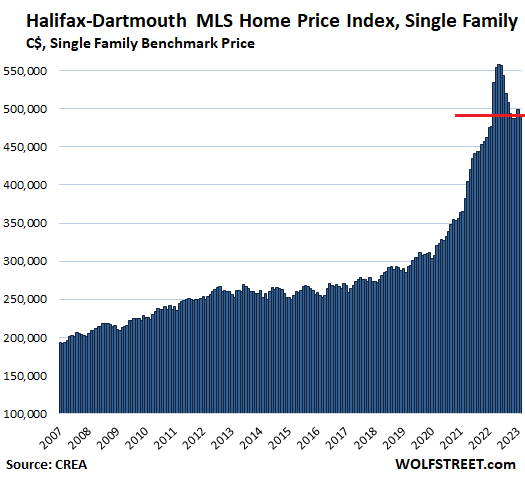

Halifax-Dartmouth: The single-family benchmark price fell by 1.6% for the month, undoing most of the increase in January, to C$491,400:

- From peak in May: -12.0%

- Year-over-year: +3.1%

- Drop in 9 months since peak in May: -C$67,100

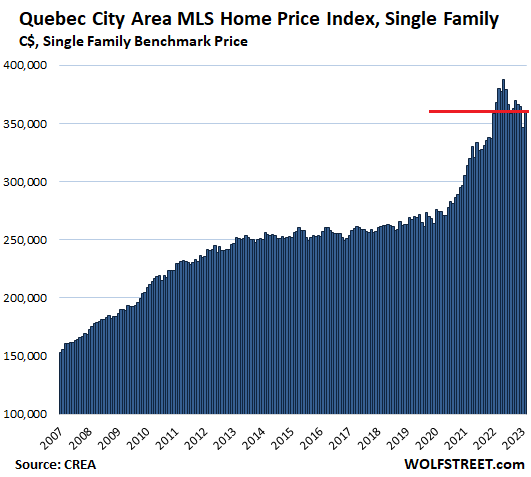

Quebec City Area: The single-family benchmark price jumped 4.2%, to C$361,500, undoing almost but not quite the plunge in January:

- From peak in May: -6.7%

- Year-over-year: -1.8%

- Drop in 8 months since peak in May: -C$26,000.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“This most ridiculous home price bubble was triggered by the most ridiculous money-printing binge and interest-rate repression globally and in Canada. ”

Amen

The NAR has the $s to get Govern ment to do its bidding. Pretty sure cash could be used to purchase property without any dollar limit.

You’re kidding, right? Some people are actually still droning on about “the Chinese” and/or “money-laundering? Or, both? Get real.

Still prices way higher than pandemic and expected to fall steeply. What can a smart buyer do today?

1. Make offer at 2019 prices to prevent steeply losses.

2. Postpone buying by 1 year.

3. Look for motivated sellers and foreclosures?

Any other option?

I like what you said above.

More things:

– Expect to make ~60 offers in order to find 1 good deal.

– Focus on for sale by owner/distressed/vacant looking houses that are off market. (Truepeoplesearch or whitepages.com + county assessor for ownership info).

– See if the owner is willing to finance at a reasonable price & terms.

– Don’t expect to find a good deal on the same real estate app every lazy buyer scrolls through on their couch for 6 hours a night.

– This is not financial or home buying advice, don’t listen to me, always obey local laws.

Thanks, good list with one exception.

“– See if the owner is willing to finance at a reasonable price & terms.”

This never happens, this is a scam, one year of good rate on expectation of future Pivot will not work.

Fed can’t Pivot anymore as despite so much QT fed has failed to control speculation. Bitcoin is at $27,000 now. That’s what happens when you bailout misbehaving banks and investors.

No, RE prices in Canada are not expected to fall more steeply. There is a housing shortage; prices will remain robust.

Lol, another NAR spam for housing shortage and Fed Pivot.

To the latter: Fed balance sheet chart for last 1 year looks really bad, as it looks like, half of all QT over last 1 year was reversed last week. However, it looks like Fed will have to eat it soon as when crap like bitcoin jumps by 10%, think what will happen to food prices (basic needs).

Canada urban has a housing shortage caused by 500,000 immigrants a year coming to the country of 38 million. That is almost 15,000 people a day that need new housing. That puts quite a floor under pricing (not that prices won’t fall somewhat, but there is no down elevator). Only if/when we start to see unemployment will prices adjust more.

In our area there is still no supply and houses are still going for over asking – quickly.

James,

These 15000 illegal immigrants or third world immigrants that come from countries whose currencies are atleast to a 100 to 1 against Canada and whose average per capita income is 1/20 that of Canada in same currency.

How will they suddenly buy a house when most Canadians native mellenials are strugglingto do this?

Also, don’t sell BS about housing being same as shelter. The immigrants need shelter and they can share cheap rented apartments for that rather than buy into Canadian dream house.

Most software MNCs no longer hiring in Canada

this for JW:

your math is wrong: 500K/365 = 1370

FYI, ”net” migration into FL is 800-1,000 per day on average

certainly suggest same situation, or similar

immigrants both places likely have some money/credit, etc., and no doubt about double ups

everywhere

”

james wordsworth

Mar 18, 2023 at 8:18 am

…

In our area there is still no supply and houses are still going for over asking – quickly.”

Which area?

Leo, you may wish to investigate the Canadian immigration system before commenting. The income and wealth distributions across their population doesn’t remotely conform to your characterization.

Eg, I looked at it. It’s actually worst.

Suddenly, all realtors have become immigration experts to support their supply narrative!

Immigration narrative for Canada is not better than US. If it doesn’t support housing in US, it can’t support in Canada.

Apologies on the math. Yes it should be about 1300 a day.

Look at KW- Cambridge for still hot market.

As for immigrants buying houses … in an area in Oakville I know … pretty much every new sale is a house being bought by Chinese … at $2 million+ a pop.

They sell a small apartment n Beijing and can buy a nice house in Canada. There is now a mass exodus of middle class Chinese from China.

Walls Street is probably working on a derivative product so when you buy a house you can hedge out risk of price going down. House price is another speculative instrument now.

Why do the hardworking to create an instrument based on complex derivative od stuff backed by speculative house prices.

They can simply sell print guids and sell instruments backed by nothing (aka bitcoin) for $27000 per piece.

Now, that really beats all wallstreet Fugazis.

There is this assumption by Canuckers..

That “Immigrants coming in”

Will be able to afford houses at the current costs..

Not so fast…

Buying now is the classic

Catching the Falling Knife…

Its a start…

You betcha, ya hey

Tell this to the guy who lost 150,000 dollqrs on average house after fomo buy during pandemic.

For him it would look like “gone too far”.

Paper losses. The “value” lost isn’t real until it’s sold. In addition, the seller may or may not lose money since it’s all about the purchase price.

Above and beyond that, I would hope anyone who bought at the peak realizes that home values go up and down. So strap in and go for a ride. Just don’t get off the ride at the bottom.

Not always so easy to hang on for the ride. Come refiance time when the LTV doesn’t match up to the mortgage, you have to come up with the shortfall or hit the bid

When the shortfall is 200 or 300k not so easy to come up with.

Bigc,

“come refinance time….” If someone is buying a house and is relying on a refinance later down the line to lower their payments or get cash out or whatever reason, and they cannot get their refinance approved or cannot come up with the difference then so be it. Hopefully that person took a calculated risk and didn’t just blindly bet on rates dropping and house values going up after they bought. If it wasn’t a calculated risk and just a “hunch” then WELCOME TO LIFE. Take the hits, move on, learn from the mistakes.

Personal responsibility keeps disappearing. If someone buys a home after a wild ride to the top, they need to understand that they need to have the stomach AND the financial stability to weather a possible ride down. If they don’t have the stomach for it, or cannot analyze what essentially is a call option, then they will suffer the consequences. They were clearly out of their league. They should stain their lane.

Compare the median wage in toronto to the median house price and it boggles the mind that houses are selling at all.

I’m thinking current homeowners are trading up or down but how many new homeowners are in this market?

This is the key metric. Because of the lack of true fixed rate mortgages (most “fixed” are fixed for only up to 5 years) Canadians rack up debt. Families use helocs to fund other RE purchases… predating the pandemic.

The ratio of home price to income is laughable. The rest of the economy looks similar. Everything is based on buy-now, pay-later in a way that makes the US credit binge in 05-08 look tame by comparison.

“This is the key metric….The ratio of home price to income is laughable.”

It is laughable, agreed. But it is not the key metric. There are lots and lots of entry level workers that keep the median income down. Think min wage and young workers. Well, now think about the housing stock. For the two medians to match up, then a whole lot of homes would have to be attainable by entry level workers.

Then consider that older, modestly paid people may have lots of equity for their downpayment from their 30+ years of ownership. You’d see them with $50k of income and think “how are they affording a $900k house????”

I don’t know if there is a key metric.

this is what happens when you put crazy liberals in charge of the government.

This is what happens when you put bankers, mega corps and government in bed with each other.

Not very many, there are some higher paying jobs in tech and finance plus smaller business owners but majority of hourly wage earners won’t qualify for a mortgage at these rates and prices still. Ofcourse in the GTA as in Metro Van you get some of the buyers who are using the entire family to qualify, you have the investors who make up about 1/5th the market and people with equity as you mentioned but if they’re trading then they have to put their own place up so the net change to total inventory is still 0 if they succeed. Out of those groups many are holding off and a lot of units are just sitting there.

RE agents are hyping up the spring, citing low inventory and one was actually on the central bank “pivot” train when I spoke with him, he’s buying precon units expected for 2027, he isn’t considering what would actually happen if a spring season price jump occurs, everyone who is not even trying to sell because of depressed prices now is going to put their property up in that scenario and supply will jump in summer yet transactions will stay low, probably send sale prices on another leg down. But I think Spring will be a major disappointment for them, not sure what BOC will actually do, they said they will pause but if FED raises again then maybe that will change, higher interest than now will exclude even more buyers.. so either way I don’t see how these prices can stay so high, construction would have to come to a near halt to strangle supply which I don’t think will happen, should be headed down again soon.

Wages have never mattered since 2015 when the rich Chinese emigrated to Canada. The Chinese leverage real estate to the hilt meaning if interest rates fall they can buy even more. Recessions and job losses don’t affect them so the only thing that matters is mortgage rates.

No way could any rational person believe that an average single family house is worth $1 million. Even newly constructed buildings are low-tech structures (100 year old techniques) built out of low quality commodity materials (soft pine, asphalt, glue, gypsum, nails).

The whole argument of “land is scarce” only applies to coastal vistas and perhaps extremely constrained areas such as mountain towns like Aspen, CO. But when an entire metro area (tens of square miles) has an average SFH price pushed into 7 figure range when natural demand cannot explain, and not even CPI inflation can explain such a phenomenon, you know that something is seriously F’ed.

Only a fraction of real estate is a place to live at this point in time. It’s mostly a Ponzi scheme at this point, a dumping ground for printed money.

Govern ment loves to create bubbles. Real Estate is a favorite of theirs in my opinion.

‘Cause they can tax it!

But a two-edge sword…

don’t knock real estate….it’s a “safe asset”!

Are you delusional,

Grandma told me as a child ,always pay your house off first. You can usually survive even if it takes a whole family to live in 1 house. Hispanic have been doing this for years struggle on the bottom ,then build up your wealt

We are about 5 years away from retirement and renting. I don’t want to own anything in the US anymore. I don’t see the value in the 500K suburban house even though I live in a rented one. The tax bill on this “beauty” is 11K a year, a total ripoff. We see ourselves living out of the US in retirement.

You make a lot of sense. I am curious about where you have in mind, in general.

Italy, Spain, and Mexico, maybe all three for awhile.

Its a good idea and even I am thinking about it when time comes for me.

Lol, so where are you going to live? Ukraine? Pls don’t tell me europe…..good luck finding something affordable there if you think 500k is too much

I wouldn’t live in a major city and I wouldn’t buy either.

Europe is not just London, Paris and Geneva. Once you leave the cities and the commuter bands of major cities, prices plummet. if you are truly adventurous, you can buy a house in a semi-abandoned Italian village for €1. You can buy castles on dozens of acres for a few hundred grand…even less if you are able and willing to rebuild a wall or two!

Just returned from a 3 week stent in Aktobe Kazakhstan. Very poor people but government rich from Oil . A local told me they call the issue the curse of oil . Incomes I’m sure are in the 1000 a month range. Because of old Soviet style infrastructure many utilities are shared such as town central heat cheap natural gas cheap domestic gasoline prices. I had a dental issue went to a pristine modern dental clinic. X-ray and exam was 5 usd . I had a crown installed in Jan and it has too many gaps need replacement. Had I had time 120 usd for a new one . Mine will be 1500 in USA. I’m sure medical similar. Far east Thailand Vietnam also offers low cost living . Egypt Spain Italy Portugal South America . Clear that USA is abundantly inflated and inflation is now sticky . Higher interest rates are needed and the bank and asset repricing just starting. We broke the party up when inflation hit. Keep the pedal down for rate increases .

Most of Europe is now much cheaper than the USA largely due to the strength of the US dollar. While house prices in Europe are very high, rents are generally lower than US and tenants have better protections.

Yep, just bring a dollar, go to Europe buy a castle, fix a few walls and while you at it build a target and a hospital close by. You won’t need a car shop either since you just fix it yourself.

Pls document your journey.

You’re paying taxes,insurance upkeep,principal and interest. Plus a profit..U could be broke in 5 years

Actually based on the local rents this house should be worth ~200K. The valuations are totally out of proportion to the local rents.

The crazies are in charge of the asylum. Leaving the country might be the best option. Not sure if I want to keep citizenship either.

So 11K tax on a 500K house is very high – only a few states like NJ, NH, IL, TX have property taxes that high. Instead of leaving US you could move to a state with much lower property taxes – 5K is probably about average and some are as low as 2-3K.

You forgot Nebraska taxes so high farmers are selling moving to other states

I have a neighbor who cashed in everything tangible (at the height of the bubble, the lucky &%$#!), gave or threw away anything that could not fit in a couple of suitcases, and then moved to Belize. Renting everything, house, car, furniture, pots, pans, … everything (furnished house), both seem happy and their son loves to go visit.

I am retired and single and have really lightened up. Right now I rent a small furnished house for $250 a week when I need it. The owner is living somewhere else.

Most of the time I am staying at my parents who are in their 90’s or dog sitting for a friend who likes to travel. I leave a scooter at my parents and my friend’s house so I can have something to do when I get bored.

You get used to living a stripped down life with all you need in a couple of backpacks. Once in a while I get a little stressed when I am not sure where I will land, but it always seems to work out.

I will modify what I do once my parents are gone, but I am 67 and I could still go first.

Listen to REDACTED with Clayton and Natalie Morris who moved to Portugal. They have a terrific YouTube channel. Loving the life as Expat and working independently too. I really like that plan

Even coveted areas inflated out of control. IMO: there’s room to build in Aspen. I live in Telluride, smaller, almost as expensive and not nearly as developed.

Geography is less of a constraint to building than regulation and NIMBYs. China, BlackRock et al factor into the metro areas.

Sadly for luxury markets, besides the rare foreclosure, a bubble like this acts as a ratchet. Big money doesn’t need to sell and can pay the bills without rental income. Prices hold for a while, then resume upwards.

We will own nothing, and be happy.

I am in San Diego and during HB1, even the most expensive coastal areas saw haircut of 40% or more.

There is a myth going on that good areas/neighborhoods/expensive areas can’t go down.

Well, how long did they stay down?

I was traveling through Telluride about 2018, and saw a Sheryl Crow concert, with some string cheese something. Nice little town, a ski haven between ski havens.

“…you know that something is seriously F’ed.”

Was it by chance that, when abbreviating an F-Bomb to express your outrage and bewilderment at our new present reality, you just happened to end up with the perfect term to both describe the true culprit who’s responsible for this mess, as well as describe what we got from them because of it: (The) “F’ED”? If so, how serendipitous!

I’d agree 100%. It’s the FED that FED this frenzy! Now, we are ALL F’ed!

Sorry for this silliness, Richter Sensei.

;-)

I think the psychological factor coming out of 2 years+ of COVID/lockdowns, etc. drove many people to bid way more than they intended on a fairly limited supply of houses. It was almost a desperation type event for some as they looked at it as “now or never” in their purchases. This was the case for 2 instances of which I know the circumstances. Both regret it now. I realize 2 cases is a small sample, but I believe they represent at least some of this mania.

Low interest rates helped with this bid up due to lower mortgage rates. The instances I know of, the folks didn’t need the “free” money handed out during COVID to make these buys and the house prices were quite high (700K+). They had plenty of assets; although admittedly, they “stretched to make the buy.

My observations. Anyone else know of similar?

Several people in my neighborhood could not afford, or would refuse, to purchase their homes at today’s prices and interest rates. These same people are watching their RE drop each month, to the tune of $20k to $40k per month. I imagine this is quite disturbing to them, as a huge portion of their total wealth is tied up the house. Will THEY sell? Time will tell. All we know is that others will.

Let the FED crushing of the Euro-Trash continue. Take it to 7%, hell 9%. LIBOR commie rate riggers can go suck eggs. SOFR measures the true cost of money and will guarantee a US FED instead of a global Fed. Listen to Tom Luango.

You sound unhappy.

There are many I know in North Dallas (Frisco and Prosper) area. People are absolutely going nuts and still willing to pay 850k+ for cardboard houses with 6% mortgage. I don’t get the logic.

@yubeie,

It’s baffling but true. The same thing in So. Cal. A house around the corner from went up for sale. There were pricing the house at early 2022 price levels. I told my wife with such confidence that they would not get what they were asking… but they did!!!

Whoever bought the house will be sorry I think.

Although slow but prices are dropping in San Diego .

Here I am begging my SO to play it carefully… Although we make 300K together and have pretty significant chunk of money on the sidelines.. I’m just not convinced about these prices.. The sad part is we waited 8 years pooling up and for other personal reasons.. and now I hate to burn that capital down knowingly… :(

Yubeie,

The logic is: Buy Assets!

ALSO:

Everything is an asset! If a digital cartoon (err NFT) is worth millions, a cardboard box (however large) must also be!

Americans are intrepid lemmings and there’s NO ECONOMIC DOWNTURN! (SMH) Look at the labor market tightness, GDP growth etc.

Today, the economy is “good.” A few small/ regional banks is isolated mismanagement (2nd and 3rd largest in history), some other companies struggling, and this is the “pain” J-Pow was talking about… right?

Now that that’s outta the way, it’s a new bull market in everything and rates will head back to 0%!

I’ll just get a HELOC to buy groceries in the meantime (probably buy BTC with it actually and buy groceries with the profits). I Already transferred my CC balances at 0% (yes, still happening) so I am good for the year!

“Buy Assets”…

That just sit there without creating any economic productivity whatsoever.

Because *things* always go up in value faster than the US Dollar is devalued, right?

On my return from Kazakhstan this week through Doha Qatar first overseas flight since 2016 I noticed something very interesting. The flight was to Dallas Tx . Date March 16 2023. Business class and coach were 100 percent full. I tried to go to rest room and navigate through airport and this airport was jam packed and men’s restroom had a line to the outside (most modern airport in the world).

Back to my point the demographics had changed on the flight . There used to be Middle East and Americans on the flight . This time 75 percent Indian . I have zero tolerance and the utmost respect for all races by the way. I asked one of the Indian fathers on the trip my observations and what the reason why was. He said Dallas was booking tech housing crazy Frisco and North Dallas. He said streaming video content . Universal and Disney planned big new campuses. His house had tripled in value. Thrilled for them but explained the situation. A whole new business that i as a 65 year old don’t experience or understand. So some of the increase is new technology and a shift of money from traditional TV and advertisers to streaming . He said in the spring India weddings and that’s the reason for the full flights of India nationals .

Concrete extruder built will last longer.

Family member in Florida purchased townhouse in late 2019 just before covid. They paid $360K, which I though was a high price, but seller had paid $500K before the GFC. Townhouse is now worth $720K.

Haha Petunia, must have been my old neighborhood.

Damp, rotting 1970s condos going for $550k.

It’s insanity.

I receive house price updates from Zillo and watch our value drop 10-15% monthly. In a way this makes me happy because if the decreases continue younger folks might once again be able to buy a home.

Too much greed is this world.

Real estate agent we know was making a killing and buying up homes to rent. She is way up right now. But maybe going to be upside down in the future.

Will home values keep dropping for years, like 2005-2011, even if medium to high inflation persists year after year? It seems counter intuitive. Is there a precedent?

If interest rates stay high to match inflation, how can housing maintain its value?

Because people don’t sell. Why sell my house with 2.7% locked in rate, to replace with a 7% interest rate? Hell no!

This is irrelevant in terms of inventory. It only matters to Realtors because they get paid commissions on each sale.

Why does it not matter for inventory? Because:

When a homeowner sells the house they live in, they then have to move into something else, and end up buying something else. So: 1 house comes on the market and 1 house is taken off the market and the net effect on inventory is zero (+1-1=0).

The events that actually increase inventory are these:

1. vacant homes that are now held off the market are put on the market (this can be hundreds of thousands of homes that show up suddenly).

2. Homeowner dies or moves to nursing home or moves to a rental or moves to another country to retire more cheaply, or moves in with kids/parents, etc. and the home is put on the market, and no home is taken off the market.

3. New homes are being built.

Wolf , why you just focus on sales? Sorry but this subject is repetitive. It feels like that this sales plunge news is more of a distraction. How about prices ? We are waiting and trying to get info about housing prices to have a clue about what will happen next year or couple years . We want to have more discussion about what can be next with this situation , for example lets have some scenarios what will happen next by considering Feds rate projections.

“How about prices ?”

LOL. The entire article except one sentence is about prices.

What my comment clarified has to do with inventory.

I get that , my frustration is for the Los Angeles not for Canada. and I see nothing affordable and nothing that can change the prices, yea it is 50k down for a 1,000,000 home, but my mortgage will be 1500 higher. This is not a market for first time home buyers but it is a heaven for cash investors. No competition , no bidding wars and even better, a 5% discount for them to but.

Where? In the US?

No, there isn’t. There was no real estate bubble in the 70’s.

My first house purchased in 1976 for $22.5K was a small 3B 1B waterfront on an eight acre. I sold it in 1985 for an unheard of $73K. Since that time it has been updated considerably (footprint is the same) and sold last year for $850K.

So there was house inflation in the 70s, although not as glaring as today.

Incidentally, property taxes are north of $12K, whereas they were $600 back in the day.

Eighth acre, not eight acre

I think so, unless the Fed lets wage inflation run or even looser lending than preceding GFR develops with a ton of government backstop for losses and really dumb people.

The hair cut is coming. Just unclear if it will be shave-the-head bald or frequent trims.

SDken,

If you go back to the 1920’s – 1930’s, the educated middle class left the US to live cheaply in Europe. It wasn’t inflation causing this, instead it was about relative value. The “intelligentsia” saw they could live better elsewhere, so they voted with their feet. Now you see retirees doing this because they are priced out of the US and the relative value is better elsewhere. This is why I think the macro for housing in the US is down in the long run.

Maybe this is the plan.

Import highly productive workers from around the world and export unproductive retirees in exchange.

This grows the US economy while reducing the dependency ratio.

When you retire and leave the US, you take your SS and retirement money with you.

WAY too simple P, and NOT generally true from first person accounts from my grandparents who were central in the times you mention.

Some of the elite ”intelligentsia” certainly went to EU, especially France, but mostly to do their thing without regard to the harsh censorship, etc., in USA at those times…

Others went to EU only for ”the season”, ”for the culture” ,,, etc.

Remembering the late 1940s-50s era in SW FL, there were plenty of folks who were similar to today’s ”alternate life styles” and were generally accepted as long as they did not get ”out of line” ,,,, EXACTLY the SAME as for almost everyone else…

…also begging the question, longer-term, if emigrating, of which international ,’police force’ will you be relying on, and why?…

may we all find a better day.

What people believe is long term is pretty short term. We have been conditioned to believe that inflation is normal and good so house prices must go up. Very long term data is hard to come by but it appears that house prices are at very high levels historically to begin with, at least versus incomes. There have been long term markets with declining or flat prices for decades in the US market over the past 150 years. If you broaden the time line and geography, you will find long term stagnation following a drop in many world markets.

Ah, but “today is different.” “They are not making new land.” “I won’t keep my house for ten years.” And so on

Real house prices will likely see a sustained drop but the trajectory of nominal house prices is much more uncertain – these may be mostly flat with a few dips and may even rise steadily at a slower pace than general inflation.

Get ready for the National Association of Gaslighters to log in as they must counter every housing bubble headline with NAR/NAG propaganda.

Was a licensed RE Broker and was ashamed of myself for being a member for 20 years. Worse than the most corrupt union in my opinion.

Mike R, same observances with several of my friends, desperately buying at the top. No one listened to the real estate major, just the real estate and mortgage agents.

Canada’s QT is not in full swing, in fact Tiff Macklem has suggested pausing any further rate hikes.

QT refers to assets on the BoC’s balance sheet. Total assets are down by 33.6% from the peak. That’s a big drop! And it continues.

Rates are a different thing. They’re another part of monetary policy.

Have a look for yourself. Here is the BOC’s balance sheet:

I don’t understand why has bank of Canada paused rate hikes. Our core CPI coming in lower or what? How is it significantly different from USA? Now everyone is waiting with baited breath for rate cuts, seems imminent here. Asking prices for RE way up this month.

They paused the rate hikes because they’re looking at my charts. Canadian mortgages are variable rate or fixed rate for short terms, such as five years. Higher mortgage rates also impact current homeowners. So it’s much more sensitive to rate hikes and has reacted faster than the US housing market. And Canada’s economy is uniquely depended on housing. The BoC doesn’t want to blow it up all at once, it seems.

billy,

The higher the rate the less people “qualify” to refinance their own homes. Maybe this is why they paused.

Thanks for the Reply Wolf. It seems to me then that this is a bail out of lenders / mortgage holders at the expense of renters via inflation. I’ve moved all my money to USD since USD has paid higher than our money market funds, 9% (USD) vs a measly 4.5% (MM). Then I put my USD accounts into STIP an SHY seems to be my only choice.

“I don’t understand why has bank of Canada paused rate hikes.”

Because it’s all part of their once-in-a-lifetime financial extinction event, where they slow-boil you and everybody else to death through inflation until you are absolutely destitute. That’s why. It’s not about inflation, it’s about rich people destroying lives for personal greed.

They could stomp out inflation in a hurry – but they won’t. They prefer to extend the pain for as long as possible, to shake out the weakest hands. This is a real-life game of Monopoly, only you don’t get to put the board away, go to sleep and wake up happy in the am. They are about to destroy your quality of life in ways you never could have dreamed of.

To save Brampton, Ontario as many of the homes there were bought with mortgages obtained by falsifying income.

That’s one hell of a gully

Wonder if they have a Canadian version of Lawrence Yun just to spin this as some transitory trend and the market is still strong, going up and up later..etc

In many ways, Canadian FOMO might even be worse than US, especially hopefully most of these people understand that there’s no locked in 30 years fixed like the excuse used here in the states why price won’t decline…so it’s either pure hubris or stupidity to think interest rate will forever be ZIRP…years of QE definitely rotted lots of people’s brain..

Hard to spin that tale when your mortgage payments went through the roof and that’s your biggest spend.

The uptick in February was heavily covered in the news up here.

It’s thought that it was a temporary thing. Likely due to people’s perception that they can get a short-term mortgage now (with lower house prices), suck up the higher monthly costs for a year or so, and then obtain a new mortgage at a much lower rate.

We’ll see how well that works.

Industry people I spoke to up here all are shaking their heads (quietly).

Canada’s economy is so dependant on housing bubble, that BoC has no option but pause, inflation be damned. Pure kaputalism if you understand my Germanics.

The benchmark price charts all seem to be hitting a short plateau, could it be they will stabilize somewhere near where they are now?

I wonder about how long those adjustable rate loans with fixed payments will eat away at equity before the lenders start sending out warning letters that their equity is becoming “inadequate” to support the on going loan.

There must be clauses in those types of loan contracts so the lender can call the loan if the underlying real estate equity fails to meet some minimum threshold. Would not raise its ugly head during an ever increasing real estate value situation, but could in dropping values, plus the potential for a reverse mortgage effect if payments don’t cover monthly interest.

Ugh, maybe I just don’t get those fixed payment/adjustable rate loans.

Grandma told me as a child ,always pay your house off first. You can usually survive even if it takes a whole family to live in 1 house. Hispanic have been doing this for years struggle on the bottom ,then build up your wealth.

Most Americans aren’t going to volunteer to do that. An implied belief in a birthright to minimum living standards (even if at someone else’s expense) which includes their own housing unit.

Welfare ,rent subsidies.It’s all fraud

The banks just extended the term of the mortgage to 30 to 40 years with no money going to the principle for the current mortgage holders that hit their trigger rate.

Canada now has an “Underused Housing Tax” which is 1% of the value of the property annually for all non-Canadian owners and some Canadian owners as well. There is a $10,000 penalty for any owner who fails to file.

Search Underused Housing Tax Canada for details.

Quick glance suggests it’s a joke.

First, this is a major problem. Make it 5%, not 1% (but be generous with the exemption reasons), and use the funds raised strictly to increase public housing stock.

Second and most important, seems Canadian residents are exempt as long as it’s held in their name directly.

The US should also reciprocate with Canada on restricting Canadian citizens from buying US residential properties.

It’s no joke its right on the 2022 tax year income tax form for Ontario and British Columbia and if you don’t fill it out you get hit with the empty home tax.

Who is going to check? I know Canada is a Soviet wannabe, but the logistics on this one seem challenging.

“Soviet wannabe”? Really? Is that because Canada provides health coverage to all citizens? Or I am ignorant of the dreaded Canadian Mounted Secret Police which has been disappearing American tourists into their ski-resort gulags for decades?

Health coverage yes, but no healthcare, unless you wait…wait…wait… and die doing so. The worst with England NHS. And yes on par with the USSR. Very low quality. When you know, you know.

Do you or have you lived in Canada or the UK? I have not lived in Canada but I lived in the UK for ten years and can tell you that far fewer people die from waiting and lack of treatment there than in the US. The NHS treatment I received (not elective) was fast, efficient and effective. Granted, this was in the 90’s. It is much worse now.

If Canada is facing the kinds of problems the UK is facing (long waits mainly) it is a willful policy. Thatcher and subsequent conservative governments (including Blair) gutted the NHS and then blamed the NHS for the gutting! Is the Canadian system being undermined the same way?

What the waiting time may be, all other countries have lower healthcare costs than the US. All developed countries have better health outcomes than the US. So, this meme about people dying while waiting is false.

Revenue Canada when they get your 2022 income tax you file. Part of the income tax form is whether or not your principle residence is empty if you live in Ontario or British Columbia.

Notice that Canada insists that the country needs 500,000 newcomers a year during a housing bubble and homeless crisis.

They’re also bringing in the FHSA (first home saving account) this year to drive prices even higher. Renters will either have to leave Canada or go on permanent welfare as rents in many places are much higher than what people earn on minimum wage jobs.

1) Canada MLS price look like the US dollar. It rose from the ashes of 2007/2008, stayed in plateau from 2015/2016 for 6Y and peaked in 2022. It deflated like the US dollar.

2) Next week exogenous causes might bring peace to the world.

3) Canada might benefit from European recovery

4) WCS might rise > WTIC for the first time, because the dollar might deflate.

Canada is also linked to energy/resource prices. Oil is down at the moment.

Am I looking at the same picture as the pessimist whom views the impressive decline in the price of single family homes as a tragedy.

I must be an optimist because I view a rapid collapse of the housing bubble would harm the speculators rather than the salts of the earth that will be substantially harmed if it drags on to long.

Selling bad debt to the salts is a particular specialty of the people that matter.

maybe I’m not such a cockeyed optimist after all.

Your graph of the MLS price of a single family home in Canada, is a portrait of your description of the era preceding this one as a mass ” consensual hallucination”.

I tend too agree. Money was flowing like and with a lot of vino. And now, we must receive our proper punishment which is the next morning, coming to too reality.

The loans may have to be made to the sort of people who carry a crumpled wad of a couple of bucks for emergencies. Who work their butts off and deserve value for their hard earned money. And the current price is still hoovering in nosebleed territory waiting for the next buyer in a macabre Dutch auction in which the reserve price is higher than bidders are willing to pay.

While I have the floor I feel compelled to talk about an event that occurred in the American financial markets this week that, statistically, is on the scale of finding life on Mars and the explosion of the Yellowstone super volcano.

The nearly instantaneous decline in interest rates has been reported as a 12 sigma event in the annals of recorded economic history. Which, of course, is the very data base from which the reported distribution was drawn. Logically, twelve standard deviations from the mean is impossible, because it means one of at least two things, either one of which may be consistent with the current reality.

The first scenario is that what occurred in the bond market last week was actually a plus or minus 12 sigma event which I judge would require at least mass hysteria comparable too the parting of the Red Sea according to one rendition.

The second scenario, which to me is most likely, is the problem that plagues the normal distribution which is insufficient sample size in which I am referring to the data base.

Obviously, the avalanche decline in the interest rate structure is a serious dislocation in expectations and, at the least, is extremely bearish.

Hi Wolf,

Please include Edmonton AB.

Not the same as Calgary, we are our own market of 1.5 M metro.

What’s is sensational about our chart is the contrast to the cazyiness elsewhere. We kept our sanity and averaged inflation.

Thank you

I used to include it and everyone asked why I included it, the topic being housing bubbles, LOL

Here’s one chart and dataset; Edmonton’s down almost 30% in a year.

https://www.zolo.ca/edmonton-real-estate/trends

Generally you can type the city of interest in the URL; some locales restrict access due to local RE association access rules.

Resale apartments and resale townhouses in Edmonton today are still down about fifty percent from their 2007 highs. They actually lost about 3/4 of their value inflation adjusted the last 16 years. I’ve seen places like Country Club Estate sell at 1990 level prices today noting the last sale December 13th 2022 at 107 7835 159 Street. I owned 2 places in the same building.

“This most ridiculous home price bubble was triggered by the most ridiculous money-printing binge and interest-rate repression globally”

And prices were already in a massive bubble in 2019, prior to the central banks’ money-printing orgy. The FED has engineered a super-bubble on top of a super-bubble.

The FED and all central banks are a cancer upon society at this point. They aborted their longstanding mandates to financially scalp the masses for the benefit of their rich buddies.

This wasn’t overnight, of course. It started with Greenspan and has gotten progressively worse until this past week they left nothing to the imagination and just openly wilted to the whims of of billionaire pigmen, running to the rescue of these reckless greedheads who are clearly their masters.

I think it’s time to end the FED and arrest Jerome Powell. He should be facing charges of domestic terrorism, along with Old Yellern and most of Congress. Their latest bastardization of their own roles, and of the current rules and regulations, is evidence of the depth of their corruption and the misery they are inflicting upon mankind. But the entire Justice Dept. and SCOTUS are shot through with corruption as well. They’re all on the take.

31 trillion lashes to the 536 + 1. Then death for high treason. I would feel better but will do nothing to stop what is coming for US.

Fantastic post DC I agree 100 %

Unfortunately as we currently don’t have any Law enforcement for such crimes these days I don’t hold their breath anymore for the Law.

(some Join them since it certainly seems legal with no one going to Jail)

So ? its all legal now as I see it simply because ? well no one been arrested or seem to seriously be on Trial unless I missed some ?

Some are now retiring ( with all their booty ) some continue and try to switch over what they have done to secure some false Family Legacy as soon they well die or old age and Medical perhaps also

Perhaps we shall see a Crime Bubble Chart upcoming showing all the gathered Wealth ? perhaps a Crime pays chart ?

I agree that ” Unfortunately as we currently don’t have any Law enforcement for such crimes these days I don’t hold their breath anymore for the Law.”

One can knock over a silicon valley bank, under the guise of legitimate transactions and walk away with several billion dollars of profit with no worry that law enforcement will be diverted from their primary purpose of keeping the little people down.

Unfortunately as we currently don’t have any Law enforcement for such crimes these days…. I agree .

Law enforcement is much to busy breaking the law themselves.

Crime is defined by the government. Government is the ultimate criminal organization. It’s just that its activities are usually legalized, through statute, regulatory fiat, or court decision.

Capturing government or any part of it is the ultimate protection and extortion racket. Far more lucrative and safer than doing it from the outside.

As the song says ,every cop is a criminal. Who knows which band sang this verse

…the mirror, crack’d…

may we all find a better day.

Flea – you know perfectly well. (Don McLean was of the opinion that the Jagger/Richards were no different…).

may we all find a better day.

Depth Charge for President!

As I am trying to understand the import of the data that you have presented, which I believe is an accurate measurement of the current status of the Canadian residential real estate landscape.

The data are current and don’t accurately reflect even the mid term ramifications of what is likely to happen to the asking price of single family homes when the Canadian adjustable rate market reflects the end of QE.

I feel your pain brother which in my case is a complaint that the luxury is not sumptuous enough. Is that what’s bothering you buncky ?

While I also feel that the Central Banks have been directed to be incompetent since man became aware.

In the long run, you may be right. In the short run there is only triage.

I sense that the immediate future will contain some of the drama you predict. I fear it may be much more mundane that people will become social media zombie’s unable to respond to the deconstruction of the society they have been accustomed to.

Depth Charge, don’t sugarcoat it.

Sorry I disagree with Depth Charge. Others beside the Fed are also responsible for housing

related concerns.

Miillions of Americans got very low interest mortgages… not me but too bad for me.

They constantly brag about this ! So how is the Fed only a bad actor ?

The Fed is the constant punching bag here.

Perhaps y’all are right in that he ultimately created too much demand. But you can’t just ignore all those low rate mortgages so many now have. Does the Fed not get credit for that ?

OK, maybe those rates were too generous.

I won’t argue on that.

What of all the politicians who allowed investors to buy up so much housing stock. In some instances this prevented an individual (or couple) from buying a home. This was very significant in certain regions. Politicians to be blamed for not being proactive. At all levels of government.

As home prices appreciated greatly rents skyrocketed in many urban areas, especially Western ones. Again, politicians generally speaking, provided no relief until the pandemic arrived. (Oregon an exception. They passed a limited version of rent control). Then the politicians went overboard not allowing renters to be evicted. Brilliant.

So in 2019 a renter could be evicted (economically) because they couldn’t swing a rent increase of 40%, but in 2021 some other renter could attempt to break into his neighbors apartment and not be able to be evicted (renter eviction moratorium). The latter i was told occurred in my apartment complex.

The narrative here is too simple: the Fed and only the Fed is to blame. As stated, huge numbers of Americans got 2.5 to 4% mortgages yet the Fed gets no credit for that. Why not ?

Conversely, government officials do next to nothing to prevent investors from creating great wealth inequality in the US and that gets no mention.

Doesn’t make sense to me. They also should have passed some regulation (oh dear is that socialism or just common sense) to lessen economic evictions of renters.

Finally: again politicians or better yet the building industry themselves should have created incentives (and penalties ?) so builders would have built smaller homes (700 to 1300 ft²)

in addition to the 2500 to 5000 ft² ones that became the norm. There are undoubtedly plenty of single people and childless couples who don’t desire a 3000 ft² home. They would prefer a 1200 ft² instead (especially at, say, 65 to 80% the cost of the McMansion).

Technical aside:

As of 2019 home prices had not increased drastically in the Midwest or South… just in the West (especially cities). Fortune magazine (Lance Lambert ) had 2 US maps: one early 2020 or so, the other early 2022. It clearly illustrated the drastic difference those two years made on housing affordability, the lack thereof.

Comparing everything to “a year ago” is the problem here. The past couple of years has been the anomaly that shouldn’t be compared to.

I gave you charts so you can compare it to any time.

Market is mostly frozen at the moment.

Still a big chunk of people holding on to a low fixed rate mortgage, and those folks would be crazy to move.

House prices are crazy high, but so are rents, so it’s not like people have a great alternative.

Immigration is running at all time highs, more then double the US rate (per capita).

Housing construction was already falling well behind the need for houses, and with the market slowdown, construction rates will fall even further.

A housing price fall would be extremely painful for an economy that is as dependent on the housing market as Canada is (extremely so), but the alternative, prices just stagnating at this extremely high level, would probably be much worse in the long run. High housing prices are destroying the country.

Inflation would actually help, by allowing the bubble to deflate (on a relative basis) without crashing the economy too hard, but inflation seems (at the moment at least, it could certainly turn around), to have mostly reverted back to the usual 2% level in Canada, with the painful exception of food.

The addict is always looking for the softer, easier way which keeps them addicted.

I believe that the bubbles should be collapsed quickly so as to stick the speculators with the losses rather than the salt of the earth people whom are enticed to overpay as a result of government agency doing the bidding of an industry.

This response is essentially saying that bubbles are acceptable as long as we don’t pop them. Let the poor and priced-out middle class suffer as long as my 3000 squre foot McMansion doesn’t drop in price!

That wasn’t my intention at all. Was expressing a fear that despite the spike in interest rates, housing prices still might not fall back to a saner level. I’d always believed that interest rate increases driven by inflation would be the pin to prick the bubble and bring back pricing sanity, but now starting to worry that even that won’t do it, in which case we may be truly doomed to stagnate forever.

As an aside, 3000 sq ft McMansion? Not sure where you live, but around here (major Canadian city) 3000 sq ft is the laneway house for the McMansion… :)

I live in Europe where 300 square meters is a massive home. That is another sign of a bubble; the belief that a “normal” house is one and a half to four times bigger than the typical family house in 1980.

According to most sources, the average house in the US is 2800 ft2 and 2000 ft2 in Canada. I agree with you that 3000 is small but it is the accepted low-end for a McMansion. Doesn’t that make the conversation all the more absurd? A family of five living in 4-5000 ft2??? We are four in 1700 ft2 and there is too much space.

Saint Patrick was a saint, unlike me and probably you. His humanity is really what’s being celebrated here. The morality for which he lived for is what is at the core of the heart of most people.

With a clear eye about the failures of character that all men posses, including his own, he went about his business, driving the snakes out of Ireland.

majorly opinion recently read: There were no snakes in the emerald island, ever…

faith and begorrah

VVNV – with apologies to actual snakes everywhere, myth or not, methinks ol’ Pat missed the common venomous two-legged type…

may we all find a better day.

I attribute it to DT’s. He had a pint of Guinness to cure the withdrawal and assured the population that he had seen thousands of horrid snakes but his prayers had driven them away.

What are peoples guesses on what the first chart in the article will look like a year from now?

It should have the year 2023 added to it, but nothing else is certain. What, if anything has changed from the aftermath of 2008? I’m not convinced.

There is no USA housing shortage. There is a qualified buyer shortage as buying at US prices looks like an invitation to find out what BK is like.

Big week for comments. 579 on March 12 is the most I’ve ever seen, plus several way over 300. Amazing for a “one man show” writing about the dismal science.

Wolfman ? Listened to the wolfman as a youngster and reading this wolfmans articles has me hooked today. FED insight especially. Be careful though, the wolfman will jack your jaw when needed.

Didn’t see you mention in the article, Canada has paused rate increases which is causing a swell of pivot hopefuls climbing out of the woodwork. Need to buy now or be priced out forever!

You first !

billygoat,

LOL, nope, sales volume down 40% from a year ago.

What about their banks?

The Canadian banking system is much more restrained than the US. Canada’s regulations much more strict which helped Canada avoid most of the pain of 2008.

Zero percent reserve ratio, and the US Fed helped bail out the Canadian banks in 2008-2009. Thanks for that, and they did pay back the loans.

The Eiger Sanction

It’s interesting, Here in Australia real estate ticked up in Sydney and Melbourne as well from January to February as well. Similar circumstances with low inventory. I wonder what is behind this. Is it enough buyers seeing 10-15 down and thinking its an entry point? RE in Australia has been a one way bet for a while so maybe not surprising….

It’s seasonal.

Summer in Sydney/Melb is the peak selling season. Watch for the mortgage renewal cliff.

Canada, a reverse elbow room country. Very low fertility rates in keeping with geographic constraints of a northern existance, yet…. still they come, inseminated and birthed in the torid zones.

Spread your tiny wings and fly away

To the snow pack country, where the cousin texted you on that day

The one I love forever is untrue

And if I could you know that I would fly away with to Fool

yes, if i could you know that I would fly eye eye, eye, eye… fly away to Fool

If one might recall, this all started in Vancouver …. and much was blamed, rightly or wrongly, on Chinese money laundering.

Lawyers were used to create legal buffers between the buyers and the sellers to hide the activity. Homes in Vancouver were quickly bid out of the affordable range for the working residents of the area.

London, Singapore, and Dubai all have real estate markets propped up by money laundering. It’s not just the Chinese, though they play a major role in Vancouver and Singapore. It’s Americans, Russians, French, Germans…and probably, gasp, even Canadians hiding their wealth and then deploying their personal politicians and bankers to prop up the market.

That said, the most expensive part of any criminal enterprise is money-laundering (I wonder if Bitcoin has changed that very much?). If you are laundering or hiding $10 million and lose 30% on your purchase price, it’s still pretty cheap…much cheaper than using other cleaning channels. The notion that these markets are “investments” is wrong for a significant proportion of holdings.

Back in 2004, I interviewed for a Singapore assignment at my company. I didn’t get it but did investigate condo prices at the time. My recollection is that it was reasonably affordable, for the size prevailing there, not here.

I moved to Singapore in 2001 when it hit bottom. 2004 was not bad but then the market exploded. Expat condos in central locations went from a few grand a month to nearer ten grand by end 2008. This was accompanied by buyouts of existing condo structures with spacious apartments (150-300 m2) which were knocked down and rebuilt with four times the number of tiny apartments. The financial crisis dampened things briefly but Singapore let in chinese buyers en masse, billionaires, and anyone who wanted to hide money or escape higher-tax regimes.

Anecdotal but representative: my flat of about 225 m2 went from S$2k a month rent to over S$18k a month from 2004 to now.

U got it exactly key rect on the % clear Ex…

Back in early 1960s, someone somewhere sold produce for cash in the field to the tune of several millions cash.

Season over, he called LV on the landline- the only phone system then: LV sent a private jet,,, he ”WON” a couple hundred thousand, declared and taxed…

Then he was flown home with all the blessings of everyone involved, including the IRS…

Win Win Win Wind,,, What’s the problem???

Exactly. How can Canadians compete on 50% marginal rate when buyers are coming in from other countries with lower tax rates?

The value of the home is in the location. Canadian homes have value because they are near schools and hospitals that *we* pay for via income tax.

Speculators coming in grab a slice of the value we create and live off our backs.

Meanwhile the government does absolutely nothing to protect us, instead they tacitly signal that they won’t do *anything*.

It actually originated in Agincourt, Ontario Canada in the mid 1970’s.

Wolf et al., Could attaching minimum wage to regional housing / rent costs be a self regulator? eg., In Aspen, maybe minimum wage is 25$/hr due to high rent etc? If businesses go broke then, no one rents, if no one rents landlords go broke. So, a equilibrium would be found over time and be stable? Just a thought…

Do (near) minimum wage workers even live in Aspen? Never been there but don’t see how they can afford it.

What you describer doesn’t seem to apply in small markets like that with outside money coming in, at least as long as the artificial economy and asset mania lasts.

From 1996-2000, I lived in SLC. Park City was already somewhat expensive at the time. I can only imagine what’s happened to prices since I left.

Passed through Raleigh, NC yesterday. Obviously everything is booming. First time that I saw homeless tents in wooded areas off of busy interchange here. Frost warning last night. That has got to be a tough life.

NC State in Raleigh has had 10 students die this year. Mostly males. Some suicide and some drug overdose. Last one was Fentanyl overdose. Very sad. I guess some things caused by Pandemic and who knows what.

Wolf,

A little surprised you haven’t released an article on the great ammoritization extension by the big banks. Q4 2022 results for the 5 big banks (BMO, SB, TD, RBC, and CIBC) all showed that the banks are sitting around 25%-30% of their mortgage portfolio at 30+ year ammoritization. A year ago they all pretty much sat at 0% for 30+ year ammoritization. Now it looks to be 20% to 25% of all outstanding mortgages were extended. 5.1 million mortgages – looking at least 1 million extensions. Worth checking out Mr. Richter.

Anyways, thanks for the great insight on you blog Wolf – much appreciated.

I looked at it when CIBC first disclosed it in the quarterly statement a couple of weeks ago. So this is an effort to keep payments fixed with a variable rate mortgage, and you end up with a negative amortization as rates rise. That’s a big problem when house prices go down; it’s not a problem when house prices go up.

On the other hand, Canadian lenders are less exposed than US lenders to interest rate risk due to the prevalence of mortgages with rates that are either variable or are adjusted at the end of a relatively short term. For lenders, the riskiest mortgage is the 30-year fixed rate mortgage that we have in the US, where everything actually stays fixed for 30 years. When interest rates rise, this is a treacherous beast for lenders and holders of the MBS because their prices drop – which is the problem here for banks now. That’s not happening in Canada to that extent because you don’t have US-style 30-year fixed rate mortgages.

I’d have to do a whole section on the complexities of Canadian mortgages and how they’re being dealt with by the banks. We down here don’t understand the Canadian mortgage market. We don’t even agree on the language: A “fixed rate” mortgage is something entirely different in the US than in Canada. So I don’t really feel like laying all this out for US readers – It gives me a headache and it’s boring to Canadian readers who grow up with this system. But without all the details, it would just turn into a clickbait bank-scaremongering article.

A few notes for anyone interested.

Canadian mortgages will typically be one of the following:

Most common: 5 year fixed rate mortgage. Like it says, the rate is fixed for 5 years and then you have to renew, at which point the interest rate is reset. If you stay with the same bank, and are up to date on your payments, you won’t have to get re-approved at renewal, they will just roll into whatever new term you agree to. If you want to change your interest rate terms (fixed vs variable, or length of term) before the 5 years is up, you have to pay a fairly hefty penalty, sometimes worth it, sometimes not.

There is also a fair percentage of the market in one, two three or four year fixed rate mortgages as well as these often have a better rate than a 5 year fixed (the fixed rates are linked to the bond yield curve, so depending on the shape of the curve, anything from one to five years might be the best deal in the eyes of a borrower at any given time), but these are not as common. Anything fixed longer than 5 years is very rare and very expensive (high rate).

Next most common mortgage is a 5 year variable rate mortgage. The interest rate paid is linked to the Bank of Canada (BoC) rate / bank prime rate and goes up or down as the BoC raises and lowers rates.

The variable rate mortgage comes in two types, some of them adjust the payment amount as rates go up or down in order to maintain a steady rate of principal repayment (keep amortization period the same) but for most of them, as rates go up or down the bank adjusts the principal repayment so that the overall payment amount stays the same. This means that when rates go up, as they have recently, the amortization period stretches out. If rates go up a lot, like recently, borrowers will hit their ‘trigger rate’, meaning they aren’t paying any principal at all any more, and are in negative amortization.

In these cases, most banks have been extending the amortization period, rather than increasing the required payments, and that is why you see the amortization periods blowing out as banks delay the hit to the borrower (and their delinquency statistics) from the rising rates. Falling principal repayment has offset the rising interest repayment so that overall borrower payments haven’t risen as much.

This delays the impact, but borrowers will still get hit with the full payment shock when they renew their mortgage (i.e. when their 5 year term ends), and in the meantime, very little principal is getting repaid so debt levels remain high.

Depending on the yield curve in the bond market, the gap between a variable and fixed rate varies. In the year or so before rates started to climb, short term (BoC) rates were very low and fixed rates were quite a bit higher, so there was a huge gap in rates, with variable rate much cheaper, and borrowers piled into variable rate mortgages (at the all time record high prices shown on Wolf’s graphs above). That meant when rates started to go up a lot of people were hit immediately.

It is possible to get a mortgage that is ‘open’ instead of ‘closed’ meaning that the borrower pays no penalty to change the terms, but this comes with a very high rate, and is typically offerred for a short term (e.g. 6 months). This is used mostly if the borrower is stalling for time and hasn’t been able to settle on what rate to choose when their mortgage expires or is temporarily stuck between selling one property and buying another (bridge financing) or something like that.

The amortization period is distinct from the term. Historically, most Canadian mortgages were 25 year amortization, more recently 30 years has become more common. As described above, many variable rate mortgages are now effectively on a much longer amortization period until their 5 year term is up at which point the amortization will need to be reduced to at most 30 years – in theory at least, unless banks and/or OSFI (Canadian banking regulator) allow longer than 30 year amortization at time of renewal as a borrower relief measure (I judge this is as unlikely, but who knows).

So, in general, the Canadian market is hit much faster and harder by rate increases than the US one, especially, in this case, because such a high percentage of the market was in variable rate mortgages when the rate increases started.

But at the same time, banks have been allowing amortizations to (temporarily?) extend past traditional norms in order to delay the full impact of the rate increase.

Historically, rate increases cause two waves of increases in delinquency/defaults for banks. The first wave is caused by people unable to pay the higher rate and this wave is typically smaller and limited to the more sub-prime parts of the market. Prime borrowers usually have enough slack in their finances to be able to ‘suck it up’ and pay the higher rates.

The second, bigger, wave comes as a second order impact, as the rate increases slow the economy, that leads to layoffs, and then your prime borrowers start to default when they lose their job. But this process takes years, it is still too early to tell if inflation will continue to rage because rates didn’t go up enough, or if we’ll just get a mild slowdown ‘soft landing’ because central banks got it exactly right, or (most likely – for Canada at least, in my opinion) we get a hard landing like the U.S. saw in 2008-2009 as the combination of rate increases and insane debt levels breaks things in the economy.

The other factor to watch is the percentage of borrowers that are underwater. Although Canada (outside of Alberta, and Saskatchewan to some extent) has recourse, meaning a borrower can’t simply send ‘jingle mail’ and walk away from the house, borrowers can still declare bankruptcy in other provinces to get out from under an underwater property. And they are still prevented from solving cash flow problems by simply selling their property if they are underwater. If won’t just be that the volume of properties to be sold by banks will increase, it will also take much longer to sell them, so the inventory will accumulate.

Because the recent post-Covid spike in prices was so sharp, the recent decline hasn’t put that many people underwater (it is just, ‘easy come, easy go’, for most people). So if prices level out around where they are now, this might not be a big factor. But if prices start to get down to those 2018/2019 levels, then we will really start to see things hit the fan. This is where inflation can help the banks, keeping nominal prices high enough to avoid this scenario while allowing wages (and rents) to catch up to prices.

In the meantime, Canadians are rooting for more bank failures in the US, as they are bringing down the 5 year bond yield that drives the 5 year fixed rate, and reducing the payment cliff that people are facing as their mortgage terms come to an end.

Heard one person joking the other day that they were going on to various US forums and starting rumours wherever they could :)

But for all that, sadly, sometimes I don’t think the war to bring down Canadian housing prices is someday, or ever, going to end.

Since I dumped a bunch of stuff above, why not cover one more topic on the Canadian housing market, mortgage insurance.

In Canada, the law requires that if a borrower makes a down payment of less than 20%, then the borrower (not the bank) has to pay a premium to buy insurance for the bank.

The way it works is that the insurance premium gets rolled into the borrowers mortgage payments so that they pay off the premium over the course of the amortization of the mortgage.

In case of a default by the borrower, the bank can get the insurer to cover any shortfall (with certain limitations, e.g. around the maximum legal fee that can be covered, etc.). The bank can either sell the property first and go to the insurer for the leftover balance, or in some cases, give the property to the insurer to sell, and take a full repayment up front.

The insurance is provided either by the Canada Mortgage and Housing Corporation (CMHC) which is 100% backed by the AAA rated Federal Government of Canada, or by a private insurer, either Sagen (formerly owned by GE and known as Genworth, now owned by Brookfield) or Canada Guaranty (backed by the Ontario Teachers Pension Fund).

Even where the insurance is through one of the two private players, the government still backstops almost the entire loan, with the exception of a deductible (equal to 10% of the initial insured amount at time of origination) which could be lost by the bank if the private insurer was to go bankrupt. Although it should be noted that the last time there was a severe downturn in the Canadian housing market (early 1990’s) the private insurer at that time (Mortgage Insurance Company of Canada – MICC) went bust, and the government arranged a bailout with GE picking up the pieces.

Anyway, the point is, the bank’s are not on the hook for highest loan to value ratio (LTV) mortgages most likely to be underwater in a downturn, the federal government is.

In addition to the insurance purchased by the borrower at time of origination for low down payment (high LTV) mortgages the bank’s themselves can also take portions of their loan book and purchase insurance themselves from CMHC. Typically they do this so that they can securitize their mortgage book (i.e. sell it to 3rd party investors). Because of the CMHC insurance, the mortgages can be sold for a better price as the credit risk is minimized for the purchaser with the loans being backed the Federal Government.

During the 2008-2009 downturn, as a low key banking bailout, the government allowed banks to purchase insurance for huge chunks of their mortgage book, but the government get a little nervous about the size of their exposure and limited somewhat the volume of this kind of ‘bulk’ or ‘portfolio’ insurance purchases from CMHC but there is still a lot of it outstanding, with the credit risk sitting with the government rather than the banks.

One final note on the Canadian housing market, is that the HELOC (Home Equity Line of Credit) product is extremely common and many banks have them set up as combined loans, so that as the borrower pays down their term mortgage over time, the limit on the HELOC increases so that the loan to value ratio on the mortgage doesn’t decline. Because of this added risk, HELOCs are limited to 65% loan to value ratio, and aren’t eligible for insurance, but there are still a lot of them out there and in a severe price decline they would add to the volume of underwater properties, especially in cases where people are using a HELOC as down payment on another property, or using the HELOC to make payments on their term mortgage and so on. HELOC’s are always variable rate, almost always interest only (no principal repayment required) and do not have a term or amortization, they just get reviewed internally by the bank every now and then.

What happened to

local bank

down payment

lock in a rate

It was so simple back then.

Great stuff. Thanks.

Thank you. I am a close watcher of the Canadian housing market and you have explained things clearly and perfectly.

The 5 year bond yield may come down due to the US bank failures but the Canadian banks are not immune to international credit markets and you will still see credit tightening conditions. This is likely to add additional pressure on the prices and push it down further.

Great stuff, Some Guy, and you’ve saved our host a lot of trouble with your primer on the Canadian mortgage scene.

Some Guy,

Thank you. I’m going to keep these two posts around for reference on a page that can be found more easily, and that can be referred to easily.

I have been watching real estate prices in Montreal for a long time. I notice that a few months ago there were about 8k listings for greater Montreal. Now there are about 11k. Low price range to 200k now from 200k to 300k. There are about 300 ads there for 3 months. Apparently the increase in inventory comes in the 300k+ price range. That is, in my opinion, there are very few transactions, and apparently at prices above 300k. 300k is obviously a lot of money for buyers. For this market to get going again in my opinion the low end needs to be in the 180k to 275k range. In other words, still a highly overvalued market

Prices in Montreal relative to the net median wage are *insane*.

Taxes are very high in Montreal. Wages are not high.

Food prices are high.

Most things you buy are overprices relative to the USA even after converting to CAD.

The Canadian bubble is so extreme I am expecting the BoC to let CAD slide.

This will hit most hard as food inflation will continue.

Canada really is in huge trouble. Trudeau will try to counteract the fall with immigration, he’s already announced higher targets.

Sorry forgot to add a couple of anecdotes.

Women at my work, two young kids. Her mortgage has *increased* by $1500 a month.

Guy I work with, bought a couple of years back on variable. His mortgage is up $2400 a month.

Guy at my kid’s soccer this morning. His mortgage is up $400 a month. He said he’s going to eat out less. This is obviously less of an impact on him but a great example of how Canadian businesses are going to be impacted.

Why would high wage immigrants keep opting for this? They will not.

What you say is what I said.

On immigration, I myself am a naturalized Canadian. I lived in Montreal for 8 years from 2003. Don’t rely on immigration. In the first 5 years, half of these people return to where they came from. In addition, a part of 500k immigrants are families, that is, the necessary housing for them is not 500k. People who go to Canada are 80 percent poor. 20 percent – wealthy immigrants go to Toronto and Vancouver. The rest cannot buy a property without taking out a loan. And in order to download it, they must have a down payment. And the work they find in most cases is part-time or low-paid. What I want to say is that immigration will not save the property market.