“Nothing goes to heck in a straight line.” That’s how functional markets adjust to a new reality: Higher inflation, higher rates.

By Wolf Richter for WOLF STREET.

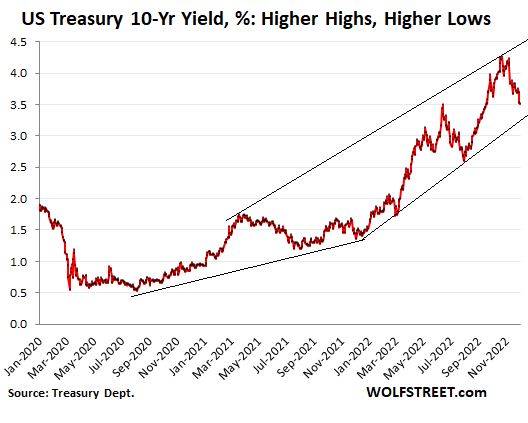

There has been a lot of discussion and handwringing and Fed-pivot fantasizing about the drop of the 10-year Treasury yield from 4.25% at the end of October to 3.51% at the close on Friday. That’s a 74-basis-point drop. In percentage terms, the yield dropped by 17%. A drop in yield means a rise in prices of these securities. So this drop in yields represents a rally in prices.

But here is the thing: During the summer bear-market rally, the 10-year yield dropped by 25%, from 3.49% to 2.60%. Before then, there were a few smaller bear-market rallies. But the biggest bear-market rally during this bond bear market was from April 2021 to August 2021, when the yield dropped by 30%, from 1.70% to 1.19%.

The 10-year yield closed at 0.52% on August 4, 2020, which marked the end of the 39-year bond bull market. Since then, the 10-year yield has risen sharply, with big surges followed by smaller retracements, followed by big surges, followed by smaller retracements, etc., adhering to the Wolf Street dictum that “Nothing Goes to Heck in a Straight Line.” The 10-year yield, as it went up, marked higher highs and higher lows each time. And the current bear-market rally fits in nicely, and the yield could drop further, and it would still fit in nicely:

Back in August 2020, the 10-year yield hit the low of 0.52% – after months of widespread propaganda by bond- and hedge-fund kings, queens, and gurus in the social media, on CNBC, and Bloomberg that the Fed would push interest rates into the negative, just like central banks had done in Europe and Japan.

This was an effort to manipulate people into buying a 10-year security with nearly no yield, thereby driving yields down further, and prices up further, to make said kings, queens, and gurus a lot of money.

Whoever ended up buying 10-year maturities at the time got a really bad deal because that marked the bottom of the 39-year bond bull market, during which the 10-year yield had descended from 15.8% in September 1981 to 0.52% in August 2020 – and not in a straight line – on declining inflation and declining interest rates, with some big wobbles in between, and since 2008, fueled by money-printing and interest rate repression.

But now we have the fastest Fed rate hikes in 40 years, and the Fed’s fastest QT ever, having unwound $381 billion in six months.

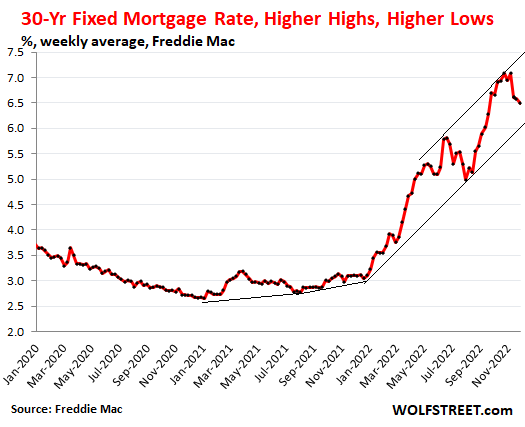

Mortgage rates followed a similar pattern. The 30-year fixed mortgage rate began the rise in early 2021, from a low of 2.65%. But also not in a straight line. By April 2021, it had reached 3.18%, and then it retraced to 2.78% by June 2021. By the end of December 2021, it was back at 3.11%.

And then as the Fed ended QE, and then raised rates, and then embarked on QT, mortgage rates surged – interrupted by big bear-market rallies, most notably the summer bear-market rally when the average 30-year fixed mortgage rate dropped by 14%, from 5.8% to 4.99%, only to surge again to 7.08% at the end of October. As of Freddie Mac’s index released on December 1, the rate has retraced some of that surge, dropping to 6.49%. This represents an 8.3% drop in the average mortgage rates.

Since early 2021, we still have an unbroken uptrend of the 30-year fixed mortgage rate, marked by higher highs and higher lows, and a further drop would still fit in nicely into the overall uptrend:

The trend is your friend. There has been a huge amount of Fed-pivot mongering and rate-cut mongering and the-Fed-will-restart-QE-soon mongering, etc. All this is part of the normal game of how markets are adjusting to new realities, with each side pushing in its own direction, thereby pushing markets up and down in a volatile manner. But this is how functional markets adjust to new realities. Adjustments don’t happen all at once. And if they do, it’s a truly spooky affair. And they don’t adjust in predictable straight lines either. They go about it over time in their rough and tumble way, but ultimately, they get there.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My money market/reverse repo pays me 3.8%, so I wouldn’t buy a 10 year for less than 5%, guaranteed bond loss with rates continuing to rise for the next decade.

Labor shortages and costs are actually accelerating. No one can afford to work for slave wages anymore.

Like to see an article on the CREIT implosion and fund redemption gating if you get a chance.

Real estate mutual funds and non-traded REITs are gated all the time. We covered a bunch of them in the UK a couple of years ago. It’s in the nature of funds that invest in illiquid assets (it may take months to sell an apartment tower) but allow investors to withdraw funds on a daily basis. This is the infamous liquidity mismatch. Smart fund operators write those gating rules into the fund documents, so everyone knows upfront.

Gating rules protect investors in the fund from what would happen to their NAV if the fund were forced to sell office towers and apartment towers and rental houses in a massive fire sale in order to meet the withdrawals.

But what this shows is that investors in real estate funds are getting cold feet.

Lots of press about Blackstone gating their fund. Makes sense, because it’s not a fkn mutual fund, and their clients are big boys.

Who was the biggest buyer in apartment market at 3.5% cap

Rates in 2021 and 2022. Blackstone. Starwood was 3rd. Almost all of the deals they bought are underwater.

Yes, they were deploying other people’s money (OPM) and collecting fees. It really doesn’t matter to Blackstone whether the fund makes or loses money — Blackstone gets the fees.

It is interesting to point out that fund managers collect a percentage of the total amount in the fund whether it goes up or down.

It is a wealth tax and there is less incentive to grow the fund when they are collecting fees based on the worth of the fund and not the gains or losses. Capitalism is dead.

There would be a revolt if the US government collect taxes based on net worth instead of income. The exception is property tax on houses. That is a wealth tax.

Whoa there, Wolf. They do get fees no matter what, but 1) they get way more if the fund makes money, 2) the partners have real money in the fund, too. REAL money, as in hundreds of millions. It most DEFINITELY matters to them whether the fund makes money, and that’s not even taking into account the reputational element of performance.

Gattopardo,

This is not a hedge fund with “2 and 20.” This is a non-traded REIT that passes on a measure of cash profits from rental revenues to the holders. For the holders, it’s a cash-flow instrument (distribution rate was something like 9%, I seem to remember), and not a wager on big price gains.

This is a great article.

Another great article. Thank you Wolf.

Agreed. The vaunted $17 / hour help wanted signs of today = $3.25 / hour in 1976, the year of my first W-2 job. Except more taxes at that level now.

My first W2 job also paid $3.0/hr ($3.75/hr. after three mos.) and had full=paid medical. That was in Cali.

Speaking of each side pushing its direction: anyone seeing an abundance of inflation is over articles?

Just today I’ve seen: shipping rates are plummeting, Chinese manufacturing orders are very low, chicken wings and gas are way down in price, we’re in a new era of moderating inflation and that the real question is just how fast the inflation will go away and that rent prices finally stopped growing.

On the other side I’ve only seen this article.

Inflation is now raging in services, not in goods. I’ve discussed this for a year.

Services is where people spend 62% of their money. That’s the biggie, and that’s where inflation is now raging.

Everything you mentioned translates into goods inflation. And inflation in goods has peaked. I have been saying that for months.

People should check their insurance rates, healthcare expenses, deductibles (did they go down, LOL?), the rent when the lease renews, the costs of services such as repairs, cleaning, etc. They’re massively increasing. That’s where inflation is now, not in goods.

https://wolfstreet.com/2022/12/01/core-services-inflation-gets-worse-core-goods-inflation-backs-off-yardstick-for-feds-inflation-target-core-pce-nails-what-powell-said-yesterday/

Just recently our semi-annual car insurance premiums have jumped $88 representing a 19% increase over last year.

The services is where I see inflation worse than products. As a landlord, I occasionally have to use a plumber. These guys are charging outrageous amounts to install a water heater. I had to hunt around for someone to do the job for little more than half of what two other guys charged. Same goes for A/C & Heating work.

Regarding insurance, I’ve been paying for my own health care since self employed for over 20 years. Crazy what they charge now that I’m in my later 50’s and increasing deductibles. Same goes for rental insurance on homes. I had to raise the rent twice over last 3-4 years because things aren’t slowing down.

I think Wolf does a great job distinguishing between “types” of inflation. Somehow, I see a lot of people thinking just house and security prices. There’s a lot of types of inflation.

I don’t see how the Fed increases will affect the services. Plumbers will plumb, auto mechanics will mechanic, health care will continue healing, etc. but prices charged will stick.

Not looking good.

JK,

“I don’t see how the Fed increases will affect the services.”

Powell addressed this issue in his speech last week specifically. It’s a tricky issue — and that’s why the Fed is looking at the labor market, because the costs of those services (costs for the service providers) that you mention are largely in wages, and those wages have been soaring. These are called “core services,” and Powell even included a chart that split them out from housing-related services.

https://wolfstreet.com/2022/11/30/these-crazy-rallies-on-hawkish-fed-plans-are-good-because-crashing-stocks-seizing-credit-markets-would-cause-the-fed-to-wobble-in-its-inflation-crackdown/

Health insurance at corporations is increasing as well. $5k deductibles are the norm now it seems.

Yesterday, I got a notice that our HOA fee for 2023 is increasing 25%. That increase wipes out mine and my wife’s SS increases (in cash terms) for 2023. Well, it was fun while it lasted.

And that’s only one item in your budget. When you add up the inflation in everything else, see how insidious it is? Meanwhile, Jerome Powell has his microscope out, and he’s starting to see signs inflation is waning, so he’s got to dial back those rate hikes immediately.

I forgot to add that part of that total cancellation of the SS increase was the large increase in homeowner’s insurance, not just all the HOA fee increase.

But agreed DC, all other ongoing costs are blowing out.

I can’t wait until the property tax bill shows up! /s

This is really the first time in our retirement life (8+ years) that I am starting to worry about the next decade of costs, if we live that long. Only a “two legged stool” here, just SS and savings (no pensions).

My wife and I went to an open house for a townhouse near us yesterday. The realtor said the HOA was $355, but was going up 20% to $427 in January. We’ve seen large HOA increases in other places we’re considering, though 25% is higher than anything we’ve seen so far.

There is always the option to live in another country. It will require buying local medical insurance.

AnthonyA:

You are bringing back fond memories. In my last few years in the Reserves I would give a lecture on retirement planning that I had developed. I used the changing of a light bulb in the center of a room as a proxy for “reaching your retirement goals.”

-Social Security was not enough… you can’t change the light while standing on the ground

-SS and your military retirement OR a private retirement/401K was not enough.. it created a ladder that leaned against a wall

-SS and your military retirement AND a private retirement/401K would just barely be enough to change the lightbulb… but on an obviously unstable three-legged stool

-All of these plus one other thing would create a safe 4-legged ladder that you could move around to where you needed to in order to change the lights… I gave the Reservists the idea to have their house paid off by the time they retired as the “fourth leg” of a stable retirement

I actually found little cartoon graphics of all of these approaches… including one of a eight-legged ladder to talk about the concept of Overdiversification. From there we moved into how to claim your military Reserve retirement.

Good Times!

SpencerG, our house is paid off and we have no long term debt. I guess you could call that one leg of the stool. Thanks for the post! It makes good sense.

Anthony A –

Have you considered…. could create a 4th leg to the stool by splitting the savings in half and using one half to “buy yourself a pension”. You’d still invest/maintain the other half of your savings – good for emergencies and upside potential. But then use the one half to buy an annuity. Requires careful shopping and a bit of market-timing on the pricing of the annuity, but gives you a steadier base income and more certainty about not outliving your money. I have older family members for whom this approach was a great source of peace-of-mind. (That and watching the insurance company’s stock like a hawk…)

P.S. It looks like annuity pricing has improved considerably over the past 2-3 years.

Anthony A.

Good Job! There is your third leg of your retirement stool.

As you said in your first post… it feels unstable… because it is. Believe me I know. At the current time I only have two completed… and just ten years to get the other two.

Wish me Luck!

Hmm, three legged stools are actually quite stable, and orchard ladders have a third leg that balances the back side. You also don’t have to worry about wobbling when one of the four legs is shorter than the other, or the floor isn’t even…

Got notice Tesla insurance premium is going up 12% for the first time ever

My USAA homeowners ins went from

$1281 2019/2020

$1372 2020/2021

$1422 2021/2022

$1481 2022/2023

Back in 2010 the premium was $675

I asked them what was causing the rise in price of the insurance. We have no hurricanes, floods, or tornados here in Montgomery County Maryland. Their answer: Inflation.

Swamp Creature – USAA is no longer the benefit it used to be. Might be a good idea to shop out your insurance unless you are getting a big annual kick-back.

Back in the day, other companies would call and ask who my carrier was. When I said USAA they told me they couldn’t touch their rates. Now others are routinely lower, much lower in some cases.

Distribute increase in cost to rebuild for those that do have hurricanes, floods & tornados. Insurance isn’t local and re-building costs dictate what the inflation in insurance looks like.

My property taxes & insurance went up this year, so I’m seeing what Wolf says. Fortunately I don’t have HOA costs, I beautify my own lawn!

How much has the value of your house increased during that time period?

We just switched everything to farm bureau after 24 years with usaa. Saved about 25%.

I just cancelled my USAA insurance because of the high cost, poor service, and lack of coverage. They no longer support the military or the Vets like they used to. They just use them for their advertising and to make them look patriotic, and for virtue signaling. In reality they have turned into another junkyard dog insurance company like the rest of them. Even their Board of directors are no longer required to be military vets. They are hiring Wall Street crooks with no military background.

Harrold

My house DID NOT go up that much during that time period. It went up about same amount as the dollar depreciated. Say 30%. So, they (USAA) are way out of line on their rates. I had no claims and had a lot of discounts applied ($750 worth). Without the discounts the homeowners ins would have been $2,600 for one year!! Then they lied to me and said it was due to Maryland Ins commission writing their policy and every other policy in every state. What BS, What Maryland did was write an endorsement, which allowed coverage for my claim. These people are not only incompetent but dishonest as well. Good riddance!

Swamp – recall back in the day that USAA was only offered to officers and warrants, expanding later to nco’s?

Agree that their advertising now is disingenuous at best, their coverage not being available to EM’s at many of the times they illustrate in their ads. Simply fishing for more market given the the total RIF since we left Saigon…

may we all find a better day.

They have to pay Gronk for those commercials.

“Since early 2021, we still have an unbroken uptrend of the 30-year fixed mortgage rate, marked by higher highs and higher lows, and a further drop would still fit in nicely into the overall uptrend.”

And that’s the thing. Every trend has an end. Now, I don’t think this dip means the end to the uptrend is done. However, I do think the steepness changes over the next six months. And I think there’s only one more rally in yields. As such, I don’t think the 10Y breaches 4% again unless the FFR finds legs above 5.5%.

The more likely scenario is the yield curve start to invert even more. I would suspect the Treasury will significantly slow down any 10Y+ auctions. They don’t want to lock in fairly large interest expenses over the next 10, 20, & 30 years. They may have already started this.

We all know how this ends. It’s just a matter of when.

If we all know where it ends then why don’t you tell us where it ends?

Spoiler: the sun goes supernova and earth is destroyed. Heck finally arrives. All bets are off.

All bets except the financial media. Even that scenario wouldn’t stop CNBC. I can see Jim Cramer now. “The recent Supernova means it is time to buy this sunglass company’s shares. Their new “Luminous Explosion” shades are very hip. Also, buy Caterpillar stock as they have announced their new “Earth Destruction” equipment line. This reconstruction will take years and Caterpillar is well positioned to capitalize on it…..”

End of World Sale!

Easy credit.

“sun goes supernova and earth is destroyed”

That’d be peak solar energy.

How do you know it hasn’t already happened, and the information just hasn’t reached earth yet?

Apparently quite a few mortgage insiders are now selling the narrative that rates will be at 4% by q1 2023. You gotta admire the never ending hopium train these people are on or the effort to rope in every last dope left..

These peaks / valleys are reassuring. If the trend continues, us peons can “sorta” time bond purchases sometime in the future. Said timing will not match inflation though. :-(

> timing will not match inflation though. :-(

If it was easy, everyone would do it. Meaning any possible edge would go away. It would become impossible to make money, because the buy-in price would adjust to everyone buying in. The future is uncertain, and information has costs.

If everyone had the formula to get rich, no one would get rich. It would cease to be the formula. Straight from Eugene Fama. That’s why the guy with the Lambo might just be high on luck.

phleep – even back moto-racing in the ’80’s, the saying was “…if you had to choose between an edge in talent, or an edge in luck, choose luck…”.

(…the rejoinder coming from the first 500cc MotoGP champ from the U.S., Kenny Roberts: “…I’ve been lucky, but y’know, the more I practice, the luckier I seem to get…”).

may we all find a better day.

Reminds me of there legged stool discussion above…..

Wolf has 10/yr. Ts as of Sept. 1981 at the peak rate of 15.8%. I distinctly remember that period of time. Those rates weren’t particularly attractive because no one was confident that it would actually stop the inflationary spiral. So, getting 15.8% seemed too great a risk, still. People were imagining hyperinflation.

Today, the sentiment is nearly the opposite. People are highly confident that the Fed will get this fixed, that we’re approaching a peak in inflation, that the Fed may overshoot, that rate hikes do work… etc. Totally different now. Too bad we can’t dial back to those feelings in ’81.

How would an investor feel if they bought a 10-year yielding 10% and watched the rate increase to 15.8% in about a 3-week interval? Volcker was raising the rates very quickly toward the peak.

If it were me, I’d feel OK.

If I purchased a 10 year treasury in 1979 paying 10% for 10 years when inflation was less than 6% from 1982-1989, I’d feel like I won the lottery.

I hope to repeat this now. If 10 year rates go to 10%, I am going almost all in.

It is a gamble, since in 1979 nobody anticipated rates to go to 16%. It is hard to pick the top or bottom.

I have no idea if rates will go to 50% with hyperinflation this time. I’d bet against that since it would hurt the banks and the wealthy at that level.

The big difference between now and 1979 is that rates were close to peaking, two years later.

Now, we are only two years from what is almost certainly the end of a multi decade cycle low with multiple decades of rising rates ahead. (The last rising cycle started in the 40’s.)

To avoid losing your shirt on the trade you propose, you will need to time the entry point effectively.

The other difference with today is that we’re at the beginning of a rising cycle, yet the fundamentals actually totally suck. This isn’t widely acknowledged (yet) but don’t worry. it will be later.

The USG’s actual credit quality is the worst since at least WW2 and probably the Civil War. Interest rates don’t reflect it but that’s because the end of the mania is not evident.

Yes, you will probably get repaid, but there isn’t much difference with an actual default when the value of what you get back is much less than what you put in. (Default does not automatically = 100% loss.)

The value of this debt (also included in household wealth) is destined to decline drastically because it’s not possible to service except at negative real rates, especially when it only increases. There isn’t enough real production to do it without crashing the economy.

Ultimately, rates are destined to “blow out” far past the 1981 peak. The fundamentals which are already mediocre to terrible now will match perception later.

phleep & HowNow

It appears this time around an investor / citizen is better off with a guess at bond peak yields while concurrently implementing a “reduce my financial footprint” program (aka cutting costs). It will be the only way to keep up AND it trains us to battle hyperinflation.

Recently discussed in the comments section of another article, but I think it’s also meaningful enough to mention again here that the 6 month treasury bill is yielding about 4.66% and the 10 year note is yielding 3.53% (open market quotes are as of the time that I write this). That’s currently an inversion of about 113 basis points. That’s not small potatoes and I personally find it to be noteworthy.

Hussman is not keen on long Treasuries presently. Requires 2% over T-bills or nominal GDP growth to deem them attractive.

In other words, don’t buy long term treasuries during an inverted yield curve. It will likely fix itself to your benefit.

I believe this variance, percentage wise and not yield differential, is the worst ever. If it isn’t, it’s close.

“They go about it over time in their rough and tumble way, but ultimately, they get there.” Get where?

Where they’re supposed to be.

Get to where an actual ”free” market would have them bee in the first place, without all the GUVMINT interference Brian.

That’s the reason this old boy – actually now elderly, etc., has been OUT of the stocks markets since 1980s — along with the now very clearly known ”pump and dump” schemes that were then and still are going on, as Wolf so clearly illustrates with his wonderful and unique focus on reality. And THAT is why only he gets my $$$ support.

As commented above, it’s really quite amazing how much hopium continues to be spread constantly by MSM, etc.

”Outta be a law” heh heh heh,,, maybe should be outta be some enforcement of law(s)…

If you have been out of the market for the past 40 years, you have missed out on some amazing returns.

True Harrold,,,,

But let’s be clear that I have also ”missed” being totally wiped out to ZERO a time or two or three…

Put it all together, and for me at least RE has been a much better investment, including commercial and residential.

NONE of my RE has ever gone to zero in the last 50 years,,, NONE!

Real estate has been my best investment in the past 10 years.

I don’t see bond yields going much higher (or mortgage rates), b/c if they do they will break things. And breaking things will cause economic slow downs and lower inflation, leading to lower yields. So higher yields are self-correcting. Tnly go so high with all the debt we have in the world and how high asset prices are. I think 4.25% was the high in the 10 yr bond. Won’t get above that again probably for a long time. I think better chance bond yields fall a lot by 2nd half 2023.

I believe the Fed is looking to break things. They want inflation at 2%. They said they want cooling labor market, cooling real estate market, and a cooling demand in supply.

Inflation broke everything. You’re looking at things cross-eyed.

The Fed is on record saying their target Fed Funds rate is 5-7%. And then stay there for longer than even they were expecting in September. You seriously expect 10 year bonds to stay permanently lower than the overnight rate?

BackRoad

The charts make a compelling case for 4.25% on the 10-year to be exceeded, aided by further rate hikes, services inflation and QT.

On the flip side, with 0.75% FFR increases off the table, goods inflation not raging like it used to, MBS shedding behind target and the stock market climbing on icy steps, your view has merit. It may not be such a straightforward return path to 4.25%.

Totally and completely wrong.

If your belief were true, there would never be a financial crisis, ever.

What’s eventually going to happen is the absurdly lax credit conditions are going away where governments, corporations, and households won’t be able to borrow as occurred in the last 30+ years.

That’s what enabled US households to maintain recent living standards. Once the easy credit ends, it’s over.

The majority of Americans are destined to become poorer or a lot poorer.

The working poor and middle will get wealthier with higher wages.

The elderly (not relying on stocks) will stay the same with SS COLA.

The upper middle and rich will get poorer due to lower stock and home prices. They did enjoy a huge increase in wealth the last 2-3 years but will lose most of it.

The rich won’t care and the upper middle will postpone retirement but won’t starve.

Without ultra-loose credit conditions (very low rates and multi-decade sub-basement credit standards), American living standards revert to something like the 70’s – or lower.

End of fake economy and fake wealth = most Americans becoming poorer or a lot poorer.

The labor shortage is artificial from the fake economy and fake wealth. The country isn’t actually that much wealthier where so many could retire (partly or fully) without loose lending standards and a fiscal debt binge.

Economic performance since the pandemic is also entirely fake. Prior to the pandemic, economic performance since the GFC had been mediocre to pathetic, and even that was only due to ZIRP and incremental deficit spending. “Growth” since 2009 almost entirely correlated to increased deficits versus pre-2008.

You don’t start with a mediocre economy (the one we actually had as opposed to the supposedly “greatest ever”), shut it down, and then come out on the other side into an organic boom.

Any such belief is ridiculous.

@Augustus Frost

People believe a lot of crazy stuff these days ;)

You and Powell both believe that. The NY Fed president has more sense, since he sees an inflation problem until at least 2025.

Unfortunately, what Powell believes is all that matters, since he alone controls the rate environment. Wolf has accused me of being against the Fed, because I believe *Powell* is a dove.

Things happen in the financial world that you think are impossible.

My view is the money drop was way too big and it inflated stocks and the economy. When the excess money runs out and the Fed funds rate bites enough we are going back to very low real growth and therefore very low 10 year treasuries if Fed really anchors inflation at 2%. But I am not really sure they will do that if real trend growth is only 1.5%. I think they want nominal growth of about 5% so they probably will be OK with 3.5% and a 10 year close to that when dust settles in a few years.

Economy was damaged by Pandemic and will be carrying more debt and worse demographics. Slow trend growth ahead.

Other important correlation is earnings yield on stocks trend about 4% higher than t-bills. If t-bills get to 5% and stay there for a while as Powell says then earnings yield on stocks should be around 9 or a PE of 11. That’s roughly 2000 on SP500, maybe less if earnings drop in a recession.

Good luck to all of Wolf readers. It’s a challenging time to invest. So much depends on if Powell really, really wants to kill inflation quickly with a recession or if he is going to take his time about it.

Yep I agree with the SPX in the 12 range and we don’t know what earnings future hold. Demographics playing a part of slower growth as well. I failed again to get an interview for an engineering position because of age (65).

Rapid drop in 10 year. I believe we need to be higher for 2 percent inflation and the consumer needs to see a SPX below 300

“Things happen in the financial world that you think are impossible.” – OS.

Who would have imagined that central banks would have negative yields?

The author who gave us “black swans” also gave us “Anti-fragile”. Do things need to break to get stronger? I don’t think anyone in the Federal Reserve is strong enough to let things break.

No

The bond mania and the 39YR cycle is over.

The idea that UST rates can stay low forever while debt increases “out the wazoo” is a complete myth.

The fundamental reason for it will be evident later, as usual.

The US isn’t exempt from math.

Possible, but consider Japan and Europe. Too much debt and poor demographics equals yield curve control. If society can’t service the debt or default on it the interest rate has to be forced down to where you can service it or you have to change the monetary system as FDR did or as Nixon did.

It’s not demographics and there is no specific level of debt that corresponds to a crisis.

I’ve been reading comparisons to Japan since the end of the dot.com bubble.

Societies that are broke or in economic decline with aging demographics = population has to work longer. That’s it. It doesn’t mean the central bank gains the magical ability to lower interest rates to an arbitrary level or creditors will permanently agree to get cheated forever so that spendthrifts and deadbeats can live beyond their means at someone else’s expense.

I attribute Japan’s experience primarily to creditor confidence but even if this is wrong, they were a large-scale creditor and still have a cohesive culture.

The US is the biggest debtor in history with a Tower of Babel Balkanized culture.

Europe is somewhere in between.

Japan can only do what it does because we support them as a vassal of the empire. Old school, i don’t think you’re considering the US losing reserve currency status. Like Hemmingway said “slowly and then all at once”, and i think we’re much closer to the all at once stage then most think.

The instantaneous $10 trillion money drop works out to $5.5 billion of additional spending *per day* over a five year period. Dumping in all on the market at once gives it that monopoly money feeling, so people spend this “extra” money without *any* regard for price consideration. Why noy pay $200,000 over asking to get just the house you want if you just had $1 million dumped on you? Heck, you have $800,000 left over to blow!

Gasoline in my area is down to $2.80. It peaked around June 11, 2022 at about $4.5. That does not mean cost of things will go down or my expenses besides gas will drop but it should put more income into the pockets of the Uber drivers, Door Dash Drivers, Amazon Prime drivers, FedEx, landscape people, truck drivers, etc.

USA built on cheap energy and if anything will drive higher services costs .

Yes, fuel prices have dropped where I live too. But I’ve since trained myself to not drive unless necessary, as the nearest store is 15 miles away (that’s 30 miles for a tank of gas). A new lifestyle! My car hasn’t moved from its parking place in a week.

Who says an old dog can’t learn new tricks? Inflation is a cruel master.

How dangerous were non-traded REITs, LP’s and private placements 15-20 years ago? It’s hard to think of any of the 20+ ones that series 7 brokers were selling that I was exposed to that didn’t go belly up or find themselves in a position where the investors had lost it all or were hanging on by their fingernails for a “pennies on the dollar” payback someday. No investor benefited from that. It all went to heck. Wolf, I’m glad you see things clearly. I’m with you, let’s not be surprised by what happens next.

The 10 and 30 year yields are driven by long term inflation expectations. If markets are confident that fed will get inflation back under 2% in an year or so, the yields will drop to around 2% very soon. Powell made a statement that he believes that dropping long term yields indicate market confidence in the fed. He seemed to like it.

Also a lot of the rally is now driven by recession fears. In recession bonds do good, stocks don’t. If fed breaks something and causes a recession, even if there is no QE, people buy treasuries just as a parking lot that pays some coupon rate and is safe if held to maturity. So as the economy weakens, inflation number comes down and layoffs start to pick up, I do expect the treasuries to do better and long term yields to come down.

Also just plain old reversion to mean. Stocks and houses are well above the mean. Long term bonds are beaten down so much that even a reversion to mean means like 20 to 30% appreciation in value. This might also be driving some rally.

Heard of “stagflation”? In contrast to the ’70s, we currently have massive deficits and general debt. Will this revert to the “typical” post-recessionary mean?

That is an understatement. “Massive Debt” versus GDP keeps going up. Crazy. I remember in the 80s when the Government Debt crossed 1 trillion. There were a lot of doomsday articles. Then again, you could by a new car for $7k and nice starter home for $70k. All of those items are now 400% higher. So I am sure that 1 Trillion has been deflated away by 70% with inflation. I am not sure why the FED wants 2% inflation when the government has so much debt. LOL We all know that the average YOY inflation was not really 2.6% from 2010 through 2019 like the CPI indicates. It was higher. I am being a bit nostalgic sarcastic here.

Amazing that debt keeps going higher and so far all is good? I think the CBO projection is $45 trillion by 2030.

The 2022 FY deficit supposedly approximately $1T.

Meanwhile, outstanding federal debt increased by more than $2T.

It’s in the public record.

“Reversion to mean” suggests that if inflation returns to 2%, bond yields should go to 5-6%, minimum.

It’s only in the past decade and a half that we’ve conditioned investors to expect a zero percent real yield by lending to spendthrift governments. I’m looking forward to having 5% yields on savings deposits, and another 3% to lend at 20+years.

TL,DR if there is a earth shattering recession soon and hell is breaking loose, how does one expect long term treasuries to do? Work as a safe parking lot and rise, or sell off along with everything else?

It’s nice, though, to think of a parking lot where you get paid rather than paying to stay there.

Depends on what inflation is doing. Powell has made it clear inflation is his #1 priority. If hell breaks lose but inflation stays high (aka stagflation), then rates will probably stay high. But if hell breaking loose finally also breaks inflation, then maybe Powell will start lowering again.

These graphs are familiar in engineering and neurology. This is how a mechanism with negative feedback responds to a sudden perturbation. A thermostat, or a muscle with a spinal reflex arc, wiggles back and forth on the way to the goal point, and then asymptotes into a somewhat more steady state after getting close to the goal.

keeping rates too low for too long reminds of control system input saturation. Then inflation is the lack of anti windup.

1) The German inflation rate is 12%. The ECB deposit rate is 2%. If the

Fed raise it’d EFFR to 12% to fight inflation, gravity with Germany will

drag it down quickly.

2) The Fed is no longer a stand alone mountain as it used to be fifty,

sixty years ago.

3) In the sixties the Fedrate was 2%-3% above the inflation rates. In the mid seventies the spread narrowed, hugging inflation in the late 70’s.

Paul Volcker threw a hail mary. It worked thanks to oil glut in the 80’s. These days there is no more oil & NG glut.

4) Regular inflation : between 0% and 10%. Moderate inflation : between

10% and 20%. High inflation : between 20% and 80%. Hyperinflation :

80% and above. In the 60’s and the 70’s inflation was moderate. It never

exceeded 20%.

5) In the 60’s and the 70’s gov debt was below GDP. Today it’s above.

6) Inflation tax the poor, the middle class and reduce gov entitlements.

Inflation for RE is frog cooking. Small landlords know that something is

wrong, but they don’t jump.

7) Inflation is gov preferred tool to reduce debt in real terms.

A long time ago, in a different life, I used to drink off hangovers. But sooner or later, the hangover cannot be staved off, and it is a doozy. Heck arrives. It can feel like being a bug covered with neurotoxin, for many endless hours.

Ya simply must learn to ”taper off” any binge of ”stuff” that the body can and does habituate too phleep…

This from one who learned to binge on booze very early from parents who apparently never did learn the detox skills definitely needed to survive booze, drugs of all kinds, (including many prescription pharmaceuticals) etc., etc…

Surely just another skill taking practice,,, but what fun in the practicing, eh??? LOL

Back at my worst I was a Fri/Sat night type (except for parts of 80’s recession, those were REALLY bad times). But I remember a probation officer saying, “you guys cause more trouble than the full timers”.

Never did understand how that could be true….but he did see a lot of people.

re: Paul Volcker threw a hail mary

That’s a myth. Volcker targeted nonborrowed reserves – when over 200 percent of legal reserves were nonborrowed.

Wolf,

Thanks, There is lower lows an lower highs in stocks which I’ve been paying more attention to. A bear market in bonds I have not been thinking about. Thank you for your constant guidance around all the noise. With repo, QT and rate hikes, holy moly, wtf, an what the heck! Cash is not trash now, and rates are still not real rates.

Yes, for the past 12 months, the charts of the S&P 500 and the 10-year yield look similar.

This may not be helpful but we have a tremendous ‘bear trap’ of way too much debt and compound interest overhead. The most successful bank ever in America was the public Reconstruction Finance Corporation (RFC). It funded the New Deal and WWII when it became the world’s largest bank. Interest rates were strictly regulated and relatively low compared to today. The RFC made direct self liquidating loans to large and small businesses, including farmers. Anyway, Congress killed it in 1957 (it made lots of money). Why? Because private banks couldn’t compete with what was a socialist bank.

Wouldn’t care to be in the mortgage lending business these days, or in the days to come.

Borrow on the short end of the curve, lend to the long end, with a home bought at the peak of the market as collateral on the loan?

In a falling interest rate environment with rising home prices, it’s almost impossible to lose money. Flip either of those around, let alone both, and . . . good luck.

“This was an effort to manipulate people into buying a 10-year security with nearly no yield, thereby driving yields down further, and prices up further, to make said kings, queens, and gurus a lot of money.”

Was it really manipulation? I always thought they really believed it.

“Never attribute to malice what can be put down to incompetence.”

Or ignorance!

…the ‘banality of moral hazard’, perhaps?

may we all find a better day.

“Alas, the time of the most despicable man is coming. The man who can no longer despise himself.”

-Nietzsche

SPX is lower, highs lower lows. Where the next lower low go. How many

lower highs and lower lows are needed to stop the inflation.

2800 Sox lower low target PE 12

Wolf has uncanny intuition.

Yep, pretty amazing!

Here is the market that is built on a narrative that half measures will produce half results. The idea that half the rate hikes will produce half the recession is comforting but simply disprovable.

Half the anti-biotic won’t cure the infection.

It’s interesting that Corporate High Yield (Junk) Bonds haven’t followed this trend (yet). I’m waiting for those to join the party!

The pendulum is swinging back this morning. The DXY is up strongly suggesting that people believe interest rates are headed higher. In turn the stock markets are down along with precious metals.

Interesting. Grain commodities are rolling over. Oil stocks are rolling over which may be an indication Oil may have some more downside. Nat gas has crashed hard.

Interest rates hikes have hit the commodities hard the past 4 or 5 months. At least the Fed work in this area is going well.

Been doing a little reading on the last major inflationary period and there is two factors missing from the modern day inflation recovery narrative. Fiscal policy, some people suggest that the higher carrying cost of the national debt eventually provoked congress to cut budgets and deficit spending aiding (causing?) the recession in the early 80s. I do not know how this plays out in 2022 where both parties are running serious deficits with very little fiscal discipline. Maybe 2024 it is a platform center piece, who knows, but I find it less likely now then when Reagan was president. Next, do we have a Saudi Arabia replacement? Can we reduce the price of energy by 66% in less than a year like 1985? I guess something like this could happen if we reverse our energy policy and Iran and Russia openly come back to the world market but the chances are slim to none. Cold fusion or city sized fission could also be an answer, but neither would come anytime soon even if we discover energy positive fusion tomorrow and released navy nuclear technologies to the market.

Good points V,,,

and I have read recently that Rolls Royce has already begun implementing, at least at the ”beta” stage, small local nukes for local power generation.

Been saying for a while that ”THE GRID” is an anachronism that really needs to be replaced by small and very local sources for the back up for the renewables, though continuing advances of battery technology and engineering could obviate a lot of that…

Certainly lots and lots of places in world and USA that could be totally independent of GRID sooner than later,,, just as was the case about 50-70 years ago before massive profits were the main reason for the GRID as it is today…

Oil could very easily fall again to NEGATIVE $33 PER BARREL where it was in Spring 2020 with all of the vast excess global supply and demand dropping globally.

It wasn’t so much that Reagan cut spending in the early 80s… with a divided Congress he really couldn’t do that. But everyone knew that (aside from Defense spending which because it is spent inside the U.S. is actually a boon to our economy) we finally had a President who was only going to be dragged kicking and screaming into more domestic spending. His battles with Speaker Tip O’Neill were EPIC!

As you say… name a single politician today who you think has the credibility to convince people that he will spend less of the taxpayers’ money. NONE of them care… Republican or Democrat.

Plus, the Saudis didn’t just switch the spigots to ON in late 1985… that followed four years of wooing by the Reagan Administration. Our current policy towards Saudi Arabia is “haphazard” to say the least.

Look at the DXY. It’s at 105, down from 114 a few months ago but up from 91 earlier this year and 71 in 2008.

As long as the DXY doesn’t crash (whatever that specific level may be), probably no change in fiscal policy.

If it does, watch the public, economy, and markets get “thrown under the bus” to preserve the Empire. If there is a choice to make, the Empire will not be sacrificed to finance modern day “bread and circus” for the public.

Wolf,

Apologies in advance if this is something you have explained to dummies like myself already but I have read several headlines this morning regarding growing fears about a $65-$80 trillion dollar debt relating to foreign exchange issues. I don’t really understand what it is and doubt the financial news media is accurately conveying the concept correctly and whether we should be nervous. Thoughts?

Ha, those clickbait headlines. Sooner or later, they show up here. A BIS report on stuff from a survey earlier this year.

$80 billion in swaps globally by non-US entities just isn’t much in the overall scheme of things.

Apple makes more net income than that in a year. The Fed destroys more money than that in EACH MONTH of QT. Crypto can do $80 billion in damage overnight, LOL

It might have included the pension fund investment strategies in the UK that blew up. So it might be a lot less now because they were forced to deleverage.

So there eventually, there may be some hedge funds or pension funds or whatever that get in trouble. But it’s just not a big thing in the overall scheme of things.

QT and higher rates will blow up a lot of crazy things that came about during QE and interest rate repression (the free-money era). We’re already seeing some of it, including crypto.

Wolf, Bloomberg is reporting it as in trillions and not billions. I still am not sure how big of an issue it is as it’s not like it’s all due at the same time as there is always more debt outstanding than M2 circulating in general…just how much leverage is the thing and if they can get the money when they need it (liquidity).

80 Trillion dollars stacked up would reach to the moon and back, 11 times. Just how much leverage is that?

OK, that would fit in with other derivatives in terms of magnitude.

Read the BIS December Quarterly Review, pages 16-17, and 67-71. Per page 16 “A key source of vulnerability is the dollar borrowing embedded in foreign exchange markets. Unlike most other types of derivatives, FX swaps, forwards and currency swaps involve the exchange of principal, and thus give rise to payment obligations equal to the full amount of the contract. Globally, dollar obligations

amounted to over $80 trillion in mid-2022. Importantly, since these obligations are reported off-balance sheet, standard debt statistics fail to capture them. Such dollar debt is, in this sense, “missing”.

I just cannot get excited about currency swaps. I lend you $1,000 so you can bet on some USD-asset, and you give me €990 as collateral. If your bet blows up and you cannot repay me the $1,000, I will keep your €990. The collateral is a liquid currency. It’s not like the collateral is a crypto whose value collapses or real estate that cannot be sold quickly except at 50 cents on the dollar.

Now if the swap is USD/ARS, with the ARS collapsing, it’s a different deal. But anyone engaging in that sort of thing knows they’re gambling.

That’s why in some jurisdictions, currency swaps can be done without listing them on the balance sheet as a liability.

Swimmer reports that BIS says – “involve the exchange of principal, and thus give rise to payment obligations equal to the full amount of the contract. Globally, dollar obligations

amounted to over $80 trillion in mid-2022”

============================

$80 Trillion is more than the dollar money supply. With principal exchanged, how is this possible?

All this derivative stuff is counted in “notional value.” It’s just nonsense to be spreading it around like this.

@ Wolf –

The reported BIS quote talks “exchanging principal” …. …. “payment obligations” …… “dollar obligations” ….. “over $80 trillion” ….

——————————————

The writing has me confused.

My reading has me thinking that BIS is saying exchanged principal amounts to $80 trillion dollars.

Thanks for your clarification.

In reading the article, it’s a guess at the size of the unregulated overseas derivatives market. One example I can think of might be Chinese shadow banking. Something relatively small blows up, then a chain reaction ensues and credit tightens up as liquidity is drained to cover bad collateral. But we have a lot of regulation and cash reserves so our banks in the US should be more protected than unregulated overseas stuff. This is why the fed likes to telegraph its moves well in advance to the whole world because so many people hold dollar denominated debt as collateral.

Dow skids over 550 points as strong data adds to worry Fed will need to be more aggressive, but how would that fix anything?

We expected the bottom of the first corrective wave to be in the low 90s on TLT, and its now rallied from there up to 107. While we believe we are in a much longer term decline in bond prices, there is now a decent probability we go up to nearly 150 again before bonds drop below the low set in October. I’m not claiming there’s a logical reason why this would happen, the market doesn’t need one. The move will not be in a straight line, as Wolf has said, but probabilities are that this is what will happen.

Once we reach that point, the decline down from there will be what everyone talks about for years to come. The decline since 2020 we’ve just witnessed will essentially be the footnote. Interest rates will undoubtedly reach double-digits. It will not be a good time for anyone.

I keep reading how people think we are going to “bottom” in 2023 and that 2023 will not be a good year, but 2024 is looking stellar. In my opinion, 2023 will surprise people and will be the “good” year – at least for the initial portion if not most of it.

2024 will likely be a year most of us will want to forget.

Yes. 2023 might wipe out the short sellers, perhaps both in stocks and bonds. Then the bottom falls out after. Nothing is as straightforward as people think it is.

1) SPX lower highs and lower lows. By year end SPX might rise above Aug high.

2) The Fed inflation target is between : 0% and 13%. The Fed like inflation and negative rate, in real terms.

3) The Fed real target is to cut US gov $30T debt by 50% within 5-7 years. Recession will slow it down.

4) The Fed might raise rate by 0.75% to feed old econ 101 prof who

dominate the cable networks with their extreme rage.

Who holds the massive $80T in FX Swaps debt? Since 70% is very short term (a week or less), what is keeping the financial system from melting down? Since most of this is off balance sheet, why the F should we believe any of what is reported?

I wonder why the govt bond prices spiked higher on 11/21? Looks like a lot of volume. Of course, the stocks rallied on it. But I can’t help but wonder if it was the Fed doing all the buying. If it was the Fed then the stock rally is only based on manipulation and not investor brilliance. Any thoughts on how we can see what the Fed bought on 11/21?

“But I can’t help but wonder if it was the Fed doing all the buying.”

Hahahaha, what ignorant braindead ridiculous BS!!! Have you been sitting in our freezer for six months and missed all about QT???? The Fed unloaded $60 billion in Treasury securities in November.

https://wolfstreet.com/2022/12/01/feds-balance-sheet-drops-by-381-billion-from-peak-december-update-on-qt/

In 2020 as the lows were being set in treasuries….a tranch of about $5 billion for the 30 year treasury went through at 0.5%

Setting the lowest bid. The highest bid was 1.3%

So if the buyer wanted to sell the next day he would have taken a 15% loss.

Hire me as bond trader. I would like to get paid millions of dollars to lose money for my company….how do I get this deal?

Is it investor brilliance to fall into a bear trap?

Hope is a powerful feeling. Any small change brings out hope.

Wolf’s charts show trends. I’d believe trends over hope at this point.

The real question is how low will it go.

10 years from now I believe we will all be happy campers, but for now, the bears are lurking in the bushes.

Long term yields look like they’re falling off a cliff and on life support. Look what happened with the last “soft” CPI report. Another soft report next week and that will be the final nail in the coffin. Looks like the system is now built on sentiment rather than factual data which makes me less confident about long term yields moving up. Powell and his doves will capitulate.

Sam s

Make sure you come around here in February next year when the federal funds rate is 5%. You can just copy and paste the same comment into the comments, and so we can play the “Powell capitulate” game some more. Maybe at 5.5%?

18 months ago, I thought they would stop at 4%. We’re now at 4%, and they’re still going.

I have my own selfish reasons for wanting 5/10 year yields to rise again – I’m a fixed income investor that depends on CD’s. Long term cd rates have crashed with these yields falling, despite history telling us that CD rates follow the FFR. I have been patiently waiting but now wondering if my greed caused me to miss the peak.

I am in general agreement with you and history tells us that a 5% FFR will result in plenty of 5% long term CD’s, but it feels like the bond market has become fixated on a fed pivot / recession / inflation dropping this taking CD yields down with it despite the FFR rising. How can yields continue to rise if that is the case ?