Margin debt issued warnings starting in early 2021 that the Big S would hit the fan. Folks blew it off.

By Wolf Richter for WOLF STREET.

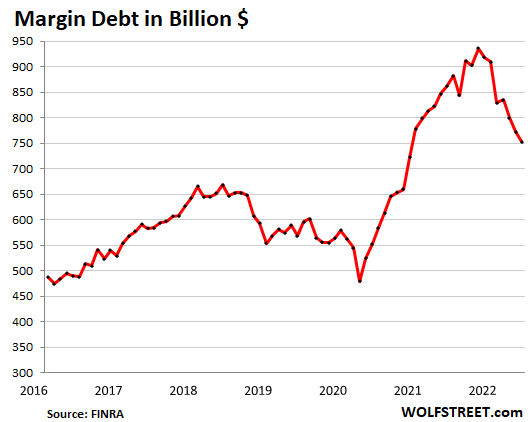

Margin debt – the visible tip of the iceberg of the direction of overall stock-market leverage – dropped by $20 billion in May from April, to $753 billion, according to Finra, based on reports from its member brokers. Margin debt had peaked in October 2021 at $936 billion, and began to decline in November 2021.

The Nasdaq peaked in mid-November as margin debt began to unwind and has since plunged 33%. The S&P 500 peaked on the first trading day in January, as margin debt was beginning to plunge. And the S&P 500 has since then dropped 22%.

In the seven months since the peak in October, margin debt has dropped by $183 billion, or by 20%, from the gigantic levels last year, an indicator of the turmoil in the market, but also an indicator that leverage is still extremely high and has a long way to go:

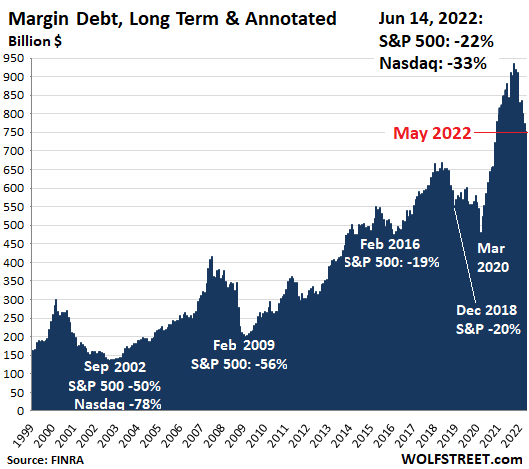

Sharp increases in margin debt are associated with increases in stock prices because leverage creates buying pressure with borrowed money; but then the tables turn, and in a vicious mechanism that includes margin calls, major stock market events are associated with sharp declines in leverage. Margin debt can serve as an effective warning about issues in the stock market.

The absolute amount of leverage in the stock market, across all forms of leverage, is unknown and no one tracks it. Margin debt reported by brokers is the only form of stock market leverage that is tracked and reported on a monthly basis.

Another form of stock market leverage, Securities Based Lending (SBL), is sporadically and partially reported by banks on their annual reports or their quarterly reports. Some banks give amounts, other banks lump it in with other forms of lending. There is no total metric for the amounts of SBL across all banks.

Other forms of stock market leverage include hedge funds and family offices that are leveraged at the institutional level. This is not tracked either. They do get margin calls, and every now and then, one of them collapses. It’s only then, when creditors pick through the debris, that the world discovers how much leverage there was.

Other forms of leverage include stock-based derivative products, such as those that felled the family office Archegos in March 2021, wiping out billions of dollars in capital at the prime brokers that had provided the leverage. No one tracked this leverage. Apparently not even banks and brokers that funded it knew at the time how much total leverage their client had from all brokers combined.

Margin debt and hype-and-hoopla stocks.

Brutal collapses of hype-and-hoopla stocks that get chopped down 80% or 90% in a matter of months trigger forced selling amid the margined crowd that was planning to get rich quick on those stocks and that therefore had concentrated holdings of these stocks. Hundreds of stocks have collapsed, starting in February 2021, and I’ve documented some of them in my Imploded Stocks.

Here are some well-known names whose share prices have collapsed. There are many more lesser-known names out there, including the EV SPAC, Electric Last Mile, that already announced that its stock will go to zero and die as it will file for Chapter 7 bankruptcy liquidation one year after going public.

Now imagine the margin calls these collapses triggered (percentages from their highs through June 14 mid-day):

- Carvana: -94.5%

- Vroom: -99%

- Rivian: -84%

- Nikola: -93%

- Lordstown: -98%

- Zillow: -85%

- Redfin: -92%

- Compass: -80%

- Opendoor: -87%

- Peloton: -94%

- DocuSign: -81%

- Snap: -86%

- Pinterest: -81%

- Buzzfeed: -88%

- Coinbase: -88%

- MicroStrategy: -88%

- Robinhood: -91%

- PayPal: -77%

- Block (former Square): -79%

- SoFi Tech: -79%

- Affirm Holdings: -90%

- Metromile: -96%

- Wayfair: -87%

- Chewy: -77%

- Shopify: -83%

- Rent the Runway: -87%

- Beyond Meat: -90%

- Teladoc: -90%

- Lyft: -84%

- Grab: -86%

- Zoom: -76%

- Virgin Galactic: -86%

- Palantir: -83%

- AMC: -84%

- Moderna: -76%

- DoorDash: -77%

- Chegg: -85%

- Roku: -85%

These stocks plunged from ridiculous highs that many folks had assumed would lead to even more ridiculous highs, which was why they bought them in the first place. As the shares collapsed, leveraged investors had to reduce their margin debt because collateral values vanished, and they became forced sellers.

Leveraged investors with a concentration in these stocks could get completely wiped out, with their brokerage account balance reduced to near nothing, if they didn’t dump these instruments in time.

Even some of the biggest stocks plunged far enough to have triggered forced selling among margined investors (percentages from their highs through June 14 mid-day):

- Netflix: -76%

- Amazon: -45%

- Tesla: -46%

- Meta: -57%

- Nvidia: -54%

- Salesforce: -47%

- Intel: -44%

Margin debt and stock market “events.”

I started warning about the spike in margin debt in January 2021, on the eve of the collapse of many of the above stocks that began in February 2021. And the warning was blown off.

What matters are the steep increases in margin debt before the selloffs, and the steep declines during the sell-offs. The absolute dollar amounts over the decades don’t matter. The chart below shows the relationship between margin debt and “events” in the S&P 500 index, including the current “event.”

But there were, and there will always be, people in our illustrious Wolf Street comments who said and will say that the chart should be adjusted in some way — in order to better, I don’t know what, hide the warning? These are the three most common adjustments they say should be used:

- The chart below should be put on a log scale

- The chart should be adjusted for inflation

- The chart should be adjusted by the S&P 500 Index level.

People just didn’t want to see, and still don’t want to see the warning signs. They’d rather adjust them away in some ingenious statistical way, such as a log scale. And then everything looks suddenly hunky-dory.

The Fed warned about hidden leverage in the stock market, citing the collapse of Archegos, in May 2021, and folks blew it off. And the Fed specifically warned about margin debt among “younger retail investors” in November 2021, and folks blew it off even as the stock market had already started to come unglued months earlier. So, OK.

Note the incomparable beauty of the near-vertical spike in dollars and in percentages of margin debt from March 2020 through October 2021, during the Fed’s $4.7 trillion money-printing binge and interest rate repression mania that is now coming apart:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s not real money…

Until it is…

It’s not real money…

Until it’s gone?

Playing with the houses’ money only leads to you losing yours! Gamblers can never stop!

There is a GA association! Everyone on WS and many in the US economy need to join Gamblers Anonymous.

Hey So Cal. Maybe we could get together play some cards.

I haven’t lost a single penny. Been in cash in my IRA since late February.

6.28% 30YFRM WooHoo! Go JPowell!!!

Hoping for 75 basis point raise to FFR tomorrow, then another nice wipe out.

I’ll start paying attention when the DOW gets below 23K.

Don’t it always seem to go

That you don’t know what you’ve got

Till it’s gone

They paved paradise

And put up a parking lot

Until they come for your home.

Amen. Jeremy Grantham, who has the nasty habit of telling the truth, has pointed out how financiers are parasitic and predicted what is coming, probably soon. He just made another presentation for Reppond investments available online as to the future.

The bankster owners of the “Fed” probably really would like for no one to see it as they try to keep the musical chairs dance going. LOL

It is real money when it’s yours…

Is this anti-inflationary (in all ignorant seriousness)?

It is anti-inflationary, to an extent (leveraged gains can be used to employ *more* leverage – the famous pyramiding of debt for instance in the real estate space. Declining collateral value (be it stocks, RE, whatever) reverses that dynamic).

The problem is that essentially 20 yrs of ZIRP from DC created a damn-near-everything-bubble, so there is inflation-feeding super-leverage entwined in almost every sector.

Until the collateral “values” (largely fictional) implode (almost certainly taking the real economy down with them), the inflationary toxin won’t really be drawn out.

Decades of ZIRP were the mother of ruin.

But, hey, it got plenty of sleazy used-car dealer Congresspeople an extra couple of 2 yr terms.

And what is the life of a nation measured against that?…

Collateral values are the basis of all loans. You are right on the money. Crazy valuations lead to crazy borrowing and crazy sorrow. Leveraged investments have outsized returns and losses, like Marvin.

Deflation in asset prices at the magnitude we are seeing will lead to debt destruction. That will incinerate lots of fake “wealth” and the collapse of the idea of the wealth effect, which is a fiction like rational expectations hypothesis.

The wealth effect goes both ways.

My hypothesis is that asset price destruction is another, albeit unstated, tool of central bank manipulation to mitigate and adsorb the effects of the CB inflationary profligacy.

Banks have moral hazard, especially since the 1999 legislation. Their mistakes get bailed out, supposedly to “protect” your bank account and mine. Heads they win, tails they don’t lose. By then their compensation structures have cleared them a pile of cash individually. So the incentives are rotten.

Having systems with juiced-in players who can’t lose, by definition, must be a road to ruin. Same goes for those who an issue edicts without suffering if they screw up. That was why we abolished royal families in the USA.

To the above post, collateral values used to be the basis of all loans. That’s what makes the financial system since the 1980’s so unsound.

Increasingly ridiculous valuations, artificially low rates, the lowest credit standards ever topped by moral hazard, mostly created by government but some also by financial intermediation.

Cas 127 said: “Until the collateral “values” (largely fictional) implode (almost certainly taking the real economy down with them)”

———————————-

What would that look like?

What is the real economy?

Services would still be with us. Existing infrastructure would still be with us. All existing facilities would still be with us. Housing would still be with us.

Collateralized debt would be erased. Ownership might/would change. The finance system might get wiped. Derivative packagers might have to get real jobs.

Marvin begs to differ.

Credit creates money with a keystroke. Debt default destroys money the same way. So does asset devaluation.

Credit isn’t money.

It’s true credit can be created with a keystroke, and default can destroy it as well. But that means credit is not a store of value – and that’s why it’s not money.

People worldwide have been fooled for 50 years by people who didn’t want us to remember the historical difference between credit and money. So many terms in the vocabulary of econ and finance have been bastardized, it’s no wonder this “social science” field gets almost everything wrong…

Credit isn’t “money”.

Credit isn’t “capital” either.

Interest rates are not a “cost of capital”.

Houses are not investments EXCEPT during falling interest rates.

Heck, most stocks at IPO aren’t investments either… In fact, most things people think of as “investments” … aren’t. (Investment: “Based on thorough analysis, an action which offers security of principal and a reasonable rate of return.”

Bitcoins aren’t coins, aren’t money and aren’t investments.

Bitcoins aren’t mined, they’re computed.

“Adjusted earnings” aren’t earned.

“One-time items” occur frequently… just maybe not every quarter.

The list of econ-linguistic delusions goes on and on…

Some might argue that credit is money.

Credit got me a house. That’s a permanent store of value. At any point the value would be affected by leverage, i.e., the amount of credit.

Stocks aren’t “investments” but a piece of paper with a common set of attributes. You don’t actually own a “piece of a business”, as your vote matters as much as it does in practically any public election, if not less. Exception is someone like Warren Buffet who can actually influence strategy. To everyone else, it’s just another speculation.

Defining an investment by whether it gains value is arbitrary. What practically everyone calls “investment” is speculation and the evidence for it is that the profit is based upon price changes with no value created.

With common stocks, trading it in the secondary market creates zero value. Buying into an IPO provides actual capital but it’s still a passive activity.

Does the definition matter?

Well, if most people admitted to themselves that they were actually speculating instead of supposedly “investing”, their behavior might differ at least on occasion.

It’s a lot easier to rationalize a financial decision when you convince yourself that it’s an “investment”. Same concept with buying a home to occupy it.

@ Wisdom –

Provocative post.

Credit should not be money. Used to be, if Seller had a good, Buyer either had to have money or Seller could extend credit in the hope Buyer would eventually pay. This kept competition for goods in line and self-policed inflation. Entities with excess actual money could loan the money to Buyer, at the risk of never seeing it again.

Then, freeloading parasites, Bankers, figured out a way to loan that which wasn’t. They created “money/credit” from nothing, backed by the law and authority of the government. Shysters by nature, Wall Streeters, joined in and we have our current situation.

They call it “capital formation.” They have written many books to justify the great service they provide. Many ,,,,,,,,,,, Romney, Blankfein, etc. are certain they are heroes.

Credit is a loan of money for a time period and a string of repayments.

J.P. Morgan said something to the effect:

“Gold is Money. Everything else is credit”

Thinking out loud …………….

Debt default does not destroy money. It just means the creditor doesn’t get their money back. The money stays in the system.

@ Wolf –

why do you allow myths to persist on your site?

Myth 1: Debt default destroys money. ( It does not.)

Myth 2: Three times, a usually highly commenter on this site has said that we have had deflation the last 40 years. Completely absurd, yet no challenge other then me.

https://wolfstreet.com/2022/06/15/fed-stops-dillydallying-so-ok-maybe-no-softish-landing-markets-on-their-own/#comment-442871

@ wolf –

Thank you.

Another great article, and something we don’t see in the mainstream media. In fact, a quick look at the local rag and there is an article about why house prices in my area won’t decline. Considering the global situation and the fact that I am in possibility the most over priced country in the world normal media is totally crap.

Keep up the great work

Sounds like you live in Australia if you are referring to real estate.

Close but no, with the exception of Sydney and Melbourne Australia is reasonably priced compared to NZ….NZ is not going to be the escape hatch that many people think it is

In both the 2000-2002 and 2007-2009 episodes, the margin debt dropped 50%, right along with the markets.

I expect margin debt in 2023 to drop down to about half of the 2021 peak, about $450B, with the S&P500 also down about 50%.

The one question I have is whether that’s enough of a decline to restore balance in the economy, or whether we get a second 50% drop (and if so, how soon… there could be a pause in between.)

BTW, a more complex chart that would also show the desired plunges would be a “drawdown” type chart. Excel can make these and it would eliminate the issues about adjusting for “inflation” or “S&P level”, or using “log scale”. Drawdown is always a percentage of the prior max high and ranges from 0 to -100%. Graphing the margin level drawdown in comparison with the S&P drawdown might show how the one often leads the other, which is perhaps the most valuable information this article is trying to convey?

I don’t know how far the sp500 will fall. I punched 6.4% hurdle rate (10 treasury plus 3% risk premium) into a dividend discount calculator, put in current dividends and played with all kind of growth rates and you are in the 1100 – 1500 range up to 10%. That’s pretty close to reversion to long term P/S ratio in the 1400 area.

Stock market just isn’t worth 3000 – 4500 unless you got nearly Zirp rates. Fed has made a mess.

The numbers you are using don’t account for future dividend cuts, which should be persistent and numerous unless inflation is so bad in which case, you’ll need to increase the discount rate used, noticeably.

Lowering the dividend noticeably will reduce supposed “fair value” noticeably.

Valuations overshot to the upside to a historical extreme.

No reason it can’t and shouldn’t to the downside either.

The answer to your question is no way, not even close.

A lousy 50% drop from the peak returns the S&P to just above the March 2020 low. US stocks weren’t even close to cheap then.

Even if the excesses aren’t anywhere near as bad as I think, at minimum, valuations should return to the 1982 lows and stocks should perform as least as poorly as 1966-1982 when the Dow lost 23% of its nominal value and 75% adjusted for price changes.

At the 1982 low, prices were barely twice the 1929 high in nominal dollars and much lower adjusted for price changes. That’s almost 49 years. Better with dividends but nothing close to the supposedly “historical” average.

Are the fundamentals better or worse now than in February 1966 at the beginning of that bear market?

I think we know the answer.

It’ll be about an 83 to 86% drop from market peak to market trough, before the crash will be over. Nothing goes to heck in a straight line, so expect plenty of massively steep bear market rallies.

As the old saying goes, those who sell first, sell best. Doesn’t matter if it is equities, credit, real estate, etc., those parties that have adjusted their portfolios over the past 12+ months, taking chips off the table and building a defensive position have, I’m sure, done just fine.

But the game now is not so much in stating the obvious related to inflation, bear markets, the direction of interest rates, margin debt, etc. but rather who can look ahead and begin to identify the bottom range of the correction to be properly positioned.

From my perspective, I don’t believe we’ve even come close to seeing the markets truly capitulate yet. This event is still coming. But what you are starting to see is that with dogs**t stocks now being almost worthless, higher quality assets, stocks, credit, etc. are being sold for any number of reasons (margin calls, desire to be liquid, need to raise cash, limit downside losses, etc.). Might be some interesting opportunities becoming available with higher quality assets that are being liquidated due to debt/leverage pressure.

I suspect the second half of 2022 is gong to be a wild ride as the Fed has no choice now but to raise rates and implement QT. The impact of rising interest rates should be evident by now but if QT is really undertaken (still to be seen over the long-term as I’m not sure if I believe the Fed will hold the line), the availability of USD’s around the world will contract which will make servicing USD denominated debt even that much more challenging. Imagine if you are a foreign country/entity, with large amounts of USD denominated debt, that is tied to variable rates (ouch), combined with a USD increasing in value. Talk about an impossible situation to manage as the cost of servicing the debt explodes higher.

For those of you that haven’t experienced the markets imploding, I would suggest you go back and take a look at the energy market meltdown in the late 1980’s, commercial real estate/S&L’s/RTC in the first half of the 90’s, the dot.com crash in early 2000’s and then the Great Recession from 2007 – 2009 to get a taste of what is yet to come. Boy, have we been spoiled with an abundance of cheap money for a dozen years. Now its back to reality where real returns have to be generated on real capital by real companies. Long-term, this is necessary and will be beneficial to the economy but short-term, it is going to be extremely painful for those unprepared.

No one here seems to mention one of the most brutal corrections to come: oil. Citi even said it’s 50 dollars overvalue. That’ll get clubbed by tighter USD supply.

Oil dropping $50 would do wonders for dropping the inflation rate.

This would happen overnight with a peace deal with Russia.

Natural gas is down 15% today.

“ Oil dropping $50 would do wonders for dropping the inflation rate.”

Not only no..

But, hell no…

At least wait until October…

PS… I’m a COLA baby… :)

Natural gas down 15% in the USA, up 20% in EU. Something with a LNG export terminal.

LNG export terminal that had an explosion will be out for at least another three months. So fewer exports from the US, meaning more supply for the US, meaning briefly lower prices in the US; but less supply in Europe, and higher prices in Europe. That’s the bet here. It was just a traders’ reaction to an announcement. NG is super volatile and can bounce back any time, no matter what blows up where.

2banana

‘with a peace deal with Russia’

LOL!

Dream on!

The US bent upon resurrecting their global hegemony, won’t allow it happen!

@2banana: incorrect. Oil prices were already high before Russia started the war. Indeed your formulation gets it backward. Crushing oil prices would bring about peace by bankrupting Russia.

Cytotoxic

‘ Crushing oil prices would bring about peace by bankrupting Russia”

NOT TRUE

The revenue for oil/gas went up more than 50%, prior to Ukraine war. They are transporting to ‘friendly’ countries via massive storage tankers. Ships from those load up with 30% discount in the silent of night, with their GPS turned off! The Rubel best currency now, than before, regained all the previous loss and went up!

Eu is hypocrite in admonishing other countries, while Hungary got a exception to get gas via pipeline from Russia!

This hypocrisy is NOT lost on other countries. The West especially USA is the cause for shortage oil/gas, food and what NOT b/c they want to regain their previous global hegemony status! Self inflicted injury and misery and the rest of the World is suffering!

The only thing that will cause oil to drop is increased production or decreased demand. With Biden in the WH increased production is off the table, and that leaves decreasing demand.

People still need to get to work… at least as long as they have jobs, which will probably be a declining number going forward, so as that happens, oil demand will decrease, and prices will drop.

World oil production is short roughly 2 million barrels per day due to primarily OPEC+ countries not being able to meet their agreed upon quotas. U.S. is producing 11.9 barrels per day of crude oil which is less than before the pandemic.

Oil prices won’t drop until worldwide production exceeds demand which is not happening anytime soon.

It’s complicated and time is a big factor.

Edit: 11.9 million BPD…..

You would do well to not watch Fox news. Recall when oil futures traded to zero. That was at a time when US declared energy independence. And so the Saudi’s (new Aramco) needed to tamp US oil down or lose market share. No one knows but I read they can pump oil at less than $10 a barrell. Then some in oil sector went out of business, the rest curtailed production. If you actually believe the WH is responsible for oil prices – well I don’t know what to say. Good luck.

@Cytotoxic –

Oil demand is inelastic, so it takes a lot of USD supply constriction rein in oil. I think we will be waiting a while…

Looking at some charts: Last time around, back in 2008, US & Brent crude reached $140 (higher even than today!). But oil prices didn’t peak until June or July. That was 9 months after the S&P had peaked (so maybe we have about 3 months to wait?). It was also 7 or 8 months into the Great Recession (so we might have longer to wait).

Importantly, the 2008 Oil Crash was just a couple of months before the big Lehman credit-crash in fall 2008. I don’t think there’s any hope the Fed can tighten USD supply “just enough” to bring down oil prices (inflation) without causing not just a recession but a major credit crisis. There’s not enough room in the eye of that needle…

On the plus side, today’s US economy really should be able to afford higher oil prices ($100-120/barrel was the norm from 2011-2014). At these oil prices gas should still be in the $3-4/gallon range. There’s more going on than just high crude prices.

When the US Fed Reserve last tip-toed into tightening-if even that-by simply ending QE in 2014, it caused the price of gold and all commodities including oil to nosedive. Fracking was there and contributed but the main driver was monetary. It was simply a matter of stable money making oil and other commodities lame investments.

“Oil demand is inelastic” =

We built our society on insanity

@TK

“If you actually believe the WH is responsible for oil prices – well I don’t know what to say. Good luck.”

US govt took Iran & Venezuela off the global markets quite some time ago, not to mention the Ruskies recently. I’d say that’s a heck of a lot of responsibility.

The poly in political economics also reaches further than just credit, labor, and supermarkets. It affects the natures of reality and sanity, and reflects the motivation, perception and means of market activities as well.

I’m not sure about that. I suspect that the producers of oil (the big ones anyway) have figured out that they are selling a dwindling resource that the world must have and that selling it cheap, now or tomorrow, is stupid.

I could be wrong, but if I were in their shoes, I would never let the price get below $75 or so again, ever.

The pandemic resulted in shutdowns, empty streets, empty malls, empty restaurants. WFH, Zoom, etc. Gasoline was $2.00 a gallon. Oil companies were bankrupted.

Then government worried about global warming. They wanted to phase out coal due to its carbon content. Oil became a dirty word. They halted some drilling and pipeline construction.

The price of gasoline is $5.00 and the government complains the greedy oil companies are not producing enough gasoline and diesel. Exxon has too much money. The White House wants them to pay a windfall profit tax, instead of funding more oil production.

I finally sold my XOM today, after owning it for over 40 years, for many reasons, including government interference. I admit I was pushed along reading Wolf’s articles. I feel I’ve never spent money more wisely than contributing to Wolf Street.

Colorado 1980’s. Mantra: Last one out of town, turn out the lights.

tagetracy

‘As the old saying goes, those who sell first, sell best’

Same as ‘ If PANIC comes, the first one to panic and act, is ahead others, who follow him/her!

Now the S&P is in BEAR zone officially, there is an amazing positive spin narrative at MktWatch: To lure investors back!

“Those who buy stocks the day after the S&P 500 enters a bear market have made an average of 22.7% in 12 months” by Mark Hulbert

I have lost respect for these kind of analysts serving the vested interest of the Wall St!

NONE of the time period he quotes, didn’t have prior conditions like QEs, suspension of Mkt to Mkt accounting standard, prolonged ZRP for nearly 13 yrs. Multiple stimuli – in essence Fed’s PUT.

Without Fed there wouldn’t this bull scoring over 300% since ’09. No fundamentals or true productive economy. Pure financialization with Buy -back shares gimmick!

Mr. Hulbert forgets all this and beckons poorly informed, to get into the mkt!

OMG!

I absolutely agree. Mark Hulbert, when he was tracking fund managers performances was a mainstay of my research. Lately, he seems like a shill for the forever bull market.

I also agree. 100% of my chips are off the table until there’s nothing but bloody guts and blood all over the bloody streets and the bloody countryside.

“This is ACME Carpet Cleaning calling to tell you about our special this week…”

OMG. I’m so glad you called. How soon can you get here? There’s blood everywhere!!!

@ Tagetracy –

“Boy, have we been spoiled with an abundance of cheap money for a dozen years.”

—————————————————–

To say we have been ruined might be more appropriate.

Adjust it away – that is great Wolf. Why bother with reality when the chart can be adjusted to emphasize the scenario that benefits me personally, and supports my “this is just a temporary situation” perception?

I doubt the corner grocer will be accepting adjustments for a pound of hamburger any time soon.

Now pardon me while I ask my broker to adjust the way the value of my leveraged stock investments is displayed in my account. Don’t need the wife to see the actual current value. I’ll have it list potential future valuations instead. Have to look to the long run, you see. Just like my realtor says.

Any ‘adjustments’ to any numbers are just plain stupid and bogus. Use the actual numbers always. I simply disregard anything that is adjusted as being laughably inane and beyond utterly bogus.

I agree. I want to see the seasonal fluctuations. They tell a more accurate story. Any 22 year olld redditor can plot the trend through the seasonal zizags. It’s not hard. Smoothing out the bumps just makes every month innacurate.

Margin debt and savings rates can be good indicators of when to buy stocks. People tend to operate on too little savings and too much debt and then panic into dumping margin loans and increasing savings at trough of the market cycle. At the top people tend to be leveraged up and not saving as the good economy has people too confident that the good life is going to continue.

Clearly central banks machinations have much greater effect on stocks than savings rates. If we learned anything this last decade..

After a wild party like the Fed has hosted, when it takes the punch bowl away, the partiers end up with severe hangovers. Some will opt for “the hair of the dog that bit them”, but they won’t be in any kind of shape to drink like they did the night before. And many others will swear they’ll never drink again. So even if the Fed brings the punch bowl back, they won’t be able to get the same kind of party going again, at least for quite a while.

This showed in today’s attempted rallies, which could hardly get back a little above the far-down opening before falling back.

The party’s over. It’ll be years before we see another of the like.

Well, beside stocks and cryptos falling , commodities seem to be rolling over too.

Nat Gas was down big today. It looks like oil is rolling over too.

Lumber is back down to almost pre-covid

Corn, wheat and other grains seem to be rolling over.

The last few weeks meat price have also rolled over.

That is good as we will not have the food shortages Biden talking about. Smoke and mirrors.

Maybe we have seen peak inflation.

Even the 2 millennial couples I know that have been outbid on over 25 homes are seeing the light at the end of the tunnel. One just won a bid this week and is doing the inspection now while the other just put in a good bid this Sunday.

1. Oil and natural gas have a big impact on CPI.

2. Other commodities little impact, or no impact on CPI (such as lumber) because most are used as raw materials in products where the vast majority of the value (price) comes from other sources, such as labor, transportation, other ingredients, profits, etc. The cost of wheat at the commodity price level in a box of serial is minuscule. Nearly all of the $4.99 for a box of cereal are for things other than wheat.

3. That’s why you didn’t see CPI spike when commodities other than oil and gas spiked.

4. CPI is now spiking in services:

And just wait for June’s numbers!

Wolf

I read there is an outage of LNG (export) terminal ( explosion!?) in Texas resulting in paradoxically increased supply domestically. The Price of natural gas went down but up in Europe!

That terminal ( deals 17% of natural gas supply, nationally) won’t be operational until about 3-4 months. Good for the consumers at least for a while. Oil still around 119-120,

“box of serial” ®

Lots of humans live in a serial box.

Wheaties from General Mills uses Klassic hard white spring wheat. Dad bred and released this variety forty years ago under Northrup King Seeds.

It’s grown under contract in southern Idaho. General Mills does hand-selections of its production fields, for seed grown to then be produced a year later by the farmers, and this keeps an ancient variety going.

One of the tricks that cereal companies, like General Mills, have is making a box of Wheaties taste the same year after year.

General Mills has a very rigid control structure in place to provide the wheat for their products. Two years ago, they bought a large tract of land in South Dakota for this very reason.

Limagrain Cereal Seeds bought the family wheat seed company out twelve years ago; note the “Cereal,” eh?

Pure wisdom dispensed daily. The worst is yet to come. Humans in the United States do not remember when the punch bowl was taken away in the 1980’s. It was too long ago. They are still spending like drunken sailors. That scares me.

Jeremy Grantham, who eloquently predicted the severe collapse of the US stock market a year ago, continues to note we have not hit bottom, but he is far more focused on soil loss, climate change and saving the earth and considers the stock market “a hobby”. Wolf’s excellent documentation of the decimation of numerous bubble stocks scares me; we might be due for a doozy of another dead cat bounce. David Hunter, ridiculously wrong in calling for new highs in the stock market averages on the the way down, before the really big colapse… is still adamant that there will be a giant rally before this 40 year bull rolls over and dies. That scares me.

If you are short right now, you have more courage then I do. I only short the rallies.

> They are still spending like drunken sailors. That scares me.

If it goes far enough, they will go from drunken sailors overnight to drunken unemployed heck-raisers. I imagine the Fed has one variable dedicated to that facet of this mess? It is hard to loosen again when the ghost of inflation (plus much else) is chasing you down he street full-clip.

Harry,

If one loses short position in a bear market, one may never be able to get back in. And oportunty cost is enourmous (may not see another for 20 years, or ever). But you already know this.

When I feel rally is coming, I roll expirations further in time at lower strikes (it will get there eventualy) And raise cash, so I welcome the rally. All set for the incoming face-ripping advance.

#4 is extremely worrying. Part of this is the wage spiral starting off. It’s self-enforcing, even if energy prices fall back.

Vertical charts will correct. The question is when and how much?

Lumber is back down to where it was in the beginning of 2018 after almost doubling in 2017. I was buying truckloads of lumber in 2017 and the 100% increase was a budget buster on my construction project. Futures went from 315 to about 625 in nine months. Then the increases of the last two years made that seem like a deal.

That lumber chart is really spectacular.

Only criminal repression of interest rates and money/credit creation made boring commodities like lumber soar.

Too much money sloshing around.

Born from nothing and going to die as nothing.

You are forgetting US tariffs on lumber as a contributor.

Cryptotoxic:

Trump put an {up to} 24% tariff on canadian lumber in April 2017, according to a simple search, that was partilly reversed over time. The futures price doubled in 2017 and only just came down to 2018 levels. The move in prices made sense in 2017 with the threat of a new tariff. Not so much in 2022

From the internet:

“In an email on Tuesday, February 1st {2022}, the U.S. Department of Commerce announced a review of reducing countervailing and antidumping duties on Canadian softwood lumber to 11.64%. This news follows after the U.S. raised rates on Canadian softwood lumber imports to 17.9% in November 2021, nearly double what it was previously”

I wonder what is economically on offer for the coming elections, from the GOP side, other than tax cuts (for those with wealth of course), trickle-down economics, cultural conservatism and environmental laxity? Especially tariffs-wise. That whole globalization thing sure is costly to unwind (and to maintain, too). We don’t even need a hot war if we are back to trade wars! But then another hot war may follow that. It seems like all kinds of piled-up problems are moving to the front burner. Always a bad time to be coming off a fed policy disaster.

Natural gas rolling over as we hit summer

Corn, wheat and other grains seem to be rolling over as the 400% increase in fertiliser hits and average crops only at 70% planted.

Even the 2 millennial couples I know that have been outbid on over 25 homes are seeing the light at the end of the tunnel as fixed rate mortgages hit 6.18%.

Maybe we have seen peak inflation.

Very funny, Good job I love sarcasm

You’d think those millenials have sense to wait after being outbid 25 times.

Blowing Bubbles and inflating something is not easy, not easy at all…

“A couple of years later, while researching a book on sailing, I blew up a rubber dinghy by mouth in ten minutes. I almost passed out.”

(Tour de France participant, from the book “Faster: The Obsession, Science and Luck Behind the World’s Fastest Cyclists”)

Imagine doing this non-stop for the past 14 years. 😀

The problem with all bubbles is that they pop suddenly.

No, no – this particular Fed Bubble is puncture proof.

Because the Future of Mankind depends on tomorrow’s Feds rate hike.World economy (which is no more than supporting branch of mighty US economy) can be compared to nuclear reactor and Mr Powell is carefully raising/lowering control rods, avoiding shutdowns & meltdowns.

I never had a flat tire in the past 7 years courtesy of Kevlar strips & Slime tire sealant. And I am just a regular person, unlike teams of genial PhD’s working for the Almighty Fed.

More face-ripping hysterical stock market rallies on the horizon !!!

Brent

‘More face-ripping hysterical stock market rallies on the horizon !!!

They are called BEAR traps for a reason. Investors front run on any ‘good/bad news in the short term to be ahead of the crowd.

See the chart of S&P and the beginnings of each QE ( 1,2.3 4) since ’09. Investors always front loaded on the news!

I have gone thru more than one bear since being in the mkt since ’82. It is said that Mr. Mkt wants more’ suckers’ to climb into band wagon, before plunging again.

The coming BEAR will be unlike, any before b/c utter disaster conditions the Fed created with insane credit creation since ’08!

DEBTs are in record territory unlike any time in human history!

Fed’s balance sheet went from less than1 T to 9 Trilions

Global debt(CBers) from 5.1 Trillions to 31.5 Trillions . Over a SIX fold in a decade! Just crazy. Now add inflation popping up real strong after 40 yrs of deflation! Fed is way behind the curve with too little and too late!

GFC was just a trial run!

Many are under the illusion, ‘some how’ thingswill go back slowly to ‘Happier days’ again with a year or two. Tough Luck!

Sunny129

Jokes aside, I concur with the opinion of Old Gent wearing bow tie who manages >$100B and who saw it all:

“We are in what I think of as the vampire phase of the bull market, where you throw everything you have at it: you stab it with Covid, you shoot it with the end of QE and the promise of higher rates, and you poison it with unexpected inflation – which has always killed P/E ratios before, but quite uniquely, not this time yet – and still the creature flies.

Just as it staggered through the second half of 2007 as its mortgage and other financial wounds increased one by one.

Until, just as you’re beginning to think the thing is completely immortal, it finally, and perhaps a little anticlimactically, keels over and dies. The sooner the better for everyone.”

@ Sunny129- “Now add inflation popping up real strong after 40 yrs of deflation!”

——————————————-

somewhere I missed all that deflation

I like the way you write. You must be an author or otherwise read alot.

The benchmark 10 year US Treasuries yield hit nearly 3.50% (3.481%) today in one of the most stunning moves in the history of interest rates and is heading rapidly towards a normal 5.25% from which interest rates should have never deviated back in 1985.

If it does go to 5.25, a lot of ‘important’ folks will have gotten it wrong. I think it could, as you say. Plenty of the educated economists out there were calling 3.5 a maximum for the year, not that long ago. I suspect they are ‘stunned’, and also on the wrong side of some large bets.

Great article on margin. thanks.

I would like to recommend Pearls before Swine comic today for a good laugh on the current market.

Economists always get it wrong. And if they work for the government or a glorified bucket shop it is their job to get it wrong.

doug

Many experts are of the opinion, that rate have to go 5% or 6% before inflation cools down! Inflation popping up this strong, after 40 yrs of deflation is NOTthat easy to control.

In 80s, I know that I was getting 14% on 10 y bond while inflation galloping 15% and above. Mr. Volcker had to increase the rates continuously to 20% before the inflation cooled down. He didn’t have dot chart or give advance warning or pussy footing like Mr. Powell does!

Our Fed slept on ‘transient’ mantra for over a year. Mr. Powell kept on buying 50B/m MBSs last year, even though the housing mkt was already sizzling. These are called Fed’s policy errors more than one!

@ sunny 129 – “Inflation popping up this strong, after 40 yrs of deflation”

——————————————

I pay attention to what you say. Typically very insightful. But what 40 years of deflation are you talking about?

thank you. I was there for the times you mentioned. and the 10 yr is going to rip much higher than a lot of folks have ever seen. interesting times.

S C B D,

If you look at the 3 Year from the beginning of the year on 3 January 2022, it was at 1.04%.

Today it closed at 3.60%.

Congress gets voted in or out on Tuesday, 8 November. Where will the 3 Year close on the evening of the election? So far this year, it has climbed 2.56%.

When will TSLA join the imploded stock list with a 90+% collapse? When that happens Tesla might also be looking at Chapter 7.

Even though it is a long shot, I do wish for it everyday and along with never hearing about Musk ever in any form of media

I fondly remember the day back in the 1970s when Stan Sporkin and I had a long afternoon talk about ‘Widows and Orphans’ stocks. I guess these stocks listed above just don’t fit into that rather quaint category!

Great article!

Anyone know why the crypto pushers are so quiet lately? Very strange …

Hard to speak while licking your wounds.

BTC is predictive programming for CBDCs.

“Satoshi” is as real as scooby doo.

We already have a 95% digital currency. CBDCs are a way to track every transaction with every monetary unit of measurement having an identifier that can be traced, through the glorious and exalted blockchain, all the way back to its origin.

Imagine how law enforcement will love having a ledger of everywhere a dollar went and where it was last. Kinda makes “following the money” a lot easier. I’ve been shaking my head for years that people were promoting BTC as anonymous. It’s the opposite of that.

The telling and surprising thing is that it was never shut down by central authorities.

It can’t be shut down by central authorities, and BTC has various ‘coin washing’ devices of varying effectivity, and there are various anonymous coins of varying quality as an alternative to BTC.

Make no mistake, crypto is going to change it all, and the cleaning it’s currently undergoing will help immensely to that end.

What is a partially effective “coin washing device?”

To realize any space coin gains one eventually has to exit the space coin and enter the financial system to buy anying big.

I know the government and IRS is after the taxes due on BTC gains. Do they care about the losses?

So the guy from the pizza shop shows up at the front door…

You say “ I got a bitcoin”…

I say, “I got a twenty”…

Guess whose ass is going hungry…

Jus’ sayin’ …

I don’t think you’re saying anything except that you are desperate to be perceived as sharper than you are.

damn, burn.

HODL!

Make no mistake, crypto is ….

…. crawling ignominiously in deep sh!t, much of it due not simply to careless “get rich” folly, but to its own deep structural problems that have been apparent for a long time.

I don’t own any, but these crypto’s were started when money was cheap. It seems like the real test and final exam is approaching rapidly. I probably would have played with it in my younger days, just like Penny stocks.

TSLA = POOP

Gee…….TBT and SDS are doing just great.

It always pays to play as if the guys running the big funds are educated morons……because they are……

Wolf…yet another great piece. Thanks and very nicely done! I forward your e-mails to my sister in Seattle…who was a music major in college…yet LOVES reading your real estate and financial material. LOL!

My younger crypto friends have been VERY quiet lately. I’ve always told them to think of crypto as they did Bernie Madoff…except in IMMENSE PROPORTIONS…with crypto very likely being the biggest pyramid scheme ever perpetrated. I believe much as with your list above of the HI-MULTIPLE stocks that have crashed…crypto is not going to end well either. YMMV.

Talking about margin calls: some massive ones getting triggered from defi schemes if BTC falls further. It’s such a textbook bubble!

Wonderful to see for a historical point of view (though I feel for the poor souls who bought the hype). This will still be talked about 1000 years from now!

That said, blockchain technology itself has some good uses. I have been using allocated vaulted gold on blockchain for payments (use as sound money outside the banking system). International payments, settled in 2-3 seconds. Pretty awesome!

1) JP will raise rates. The bond market is in a growing mess. USD weekly might close > May 9 2022 high, above 105, on the way up.

2) RRP is up to $2.2T, sucking liquidity and provide good collateral in the o/n market.

3) $SOFR is up to 0.73%, doing nothing for 7 weeks, not preempting 0.75%-1% higher rates, possibly on the way up to close Mar 9/16 2020 open gap.

4) US Treasury saving account in the FED is up from $78B in Oct 2021 to $723B. US gov is doing something right, at least for themselves.

5) Today low might send SPX higher to close June 10/13 and June 9/10

open gaps by Fri.

6) SPX weekly might become a green bar closing > May 16 low.

7) If so, in order to plunge, on day, there must be a close under May 16 low. Breaching it isn’t good enough.

8)

Speaking of margin…oh so close today, Saynor almost got that $21K margin call today. Since he didn’t have to pay up yet, guess the next best thing to do is to go on Twitter to advocate buying more at the dip and #HODL

“This is not tracked either.”

Ignorance is bliss, except when it’s ignorance of a ticking time bomb.

The FIC generated trillions in toxic waste last time around in the indulgent pursuit of its pleonexia, which The Fed cleaned up with NIRP/ZIRP and QE. Sort of. It had to, to keep the financial system from detonating, because those debts were unserviceable. And it still has those trillions in toxic waste on its books.

This time around, with NIRP/ZIRP, the FIC is expected to have generated at least as much toxic waste. But The Fed has gone to QT, reversing QE, and interest rates are rising.

So how is The Fed going to paper over trillions in toxic waste this time? Can the general population be squeezed hard enough and in time to prevent the FIC from going ballistic?

Tick tick tick . . .

Why is it that we have so many “experts” giving their opinions on everything to do with money and their favorite words are, could be, perhaps, never been down this exact road before, is a distinct possibility etc. while specializing in fence straddling. If I had a show focused on finance I would have three simple requirements to be on as a guest. First you would not be allowed to use such phrases as above and would have to give a definitive opinion. Second it would be shown a track record of your prior tea leaf reading results. Third you would have to disclose your investments and results over the past five years.

When you place a bet in Vegas don’t you think you should listen to those who have a track record of picking winners and are paid for their expertise? Why then do we constantly listen to all these talking heads with nothing but empty words rattling around in their heads?

I haven’t been to Vegas in 20 years, but I knew I was gambling when I was there. “listen to those who have a track record of picking winners” You mean the house?

No one consistently picks winners when facing an absolutely certain negative mathematical expectation. If you know someone that maintains otherwise, get away from them.

“When you place a bet in Vegas don’t you think you should listen to those who have a track record of picking winners and are paid for their expertise?”

You’re operating under a misconception of what constitutes a ‘rigged casino’. They’re cash machines. YOUR cash.

“If I had a show focused on finance I would have three simple requirements to be on as a guest.”

Let me know when you have a finance show so I can short your sponsors’ stock.

The future is uncertain. Anyone who doesn’t hedge his view of the future is making a super-concentrated bet. Most everything in finance is about avoiding that “Vegas” mentality. That’s why risk management has 3 classic pillars: reserves, diversification, and insurance: all based on what might happen, or not. The expectation that any sage could call it consistently (or would, on some show) is, I think, absurd. The person who can do that is out making money as we speak, not throwing pearls too cheaply before the masses. Good information is costly.

good point leap:

reminds me of the answer when someone asked why lamb boring ghini cars were not ”advertised on tv”

”because folks who can buy a Lamborghini do NOT watch TV” was the answer at that time

really appreciate anyone replying to that ”concept”

thanks

They do what you describe on the Wealthtrack. Show the guests their earlier predictions and how they went. Good show.

I’m not interested in predictions, nor am I interested in peoples trade records.

What I’m interested in is people posting original analysis and cogent arguments for their views, because I can learn from that and make my own judgement.

Being “right” in the end doesn’t prove anything. I can flip a coin and be right.

This is why many people lose big. They confuse luck with skill, then bet the house and discover to their peril that they didn’t know a thing. I see this all the time.

I often think it is a blessing to lose big early in your investment life, when the damage can still easily be repaired. The humbling experience will make you a better investor.

really GOOD comment YS,,, perhaps one of, if not THE best…

Many thanks for your presence on ”WOLF’s Wonder.”

YS-recalls moto racer Kenny Roberts’ observation (i paraphrase): “…of course i’ve been lucky. But the more i practice and prepare, the luckier i seem to get…” (couple that with immense talent and wind up winning the 500GP World Championship 3X…).

may we all find a better day.

Jamie Dimon the CEO of JPMorgan said “Brace yourselves for an “economic hurricane” – caused by the war in Ukraine, rising inflation pressures and interest rate hikes from the Federal Reserve.

“We just don’t know if it’s a minor one or Superstorm Sandy. You better brace yourself,” Dimon said, adding that JPMorgan Chase (JPM) is preparing for a “non-benign environment” and “bad outcomes.”

Dimon said that the economy is “distorted” by inflation. He’s also worried that the Fed is starting to unwind its bond portfolio, a process known as quantitative tightening, at the same time it is raising interest rates.

“That’s something that the market is not prepared for, Dimon said, adding that people will be “writing about [this] in history books for 50 years,”

I will add with the Fed meeting tomorrow they will raise it at least .50% – some say .75%, and on MarketWatch they forecast a 1.0% increase!

This IMO, – will drive the markets down starting tomorrow and for months till a recession hits, – maybe this is their cure for the “fire” of high inflation, commodities, crazy speculations, cryptotrash, and demand, by trashing the markets to lower levels, and the “fire” is “extinguished”

This is pure speculation on my part, and I could be very wrong.

Martok

IMHO, tackling to contain an inflation which popped and going at 8.8. coming after 4 DECADES of deflation, won’t be that easy! Mr. Powell is NO Paul Volcker.

There is NO ONE after him at the Fed matching his independence, integrity, intellectual honesty and in taking firm action!

He didn’t mess around dot charts or future guidance. He got the job done irrespective what the Prez Reagon demanded!

Now a days CBers are more obsessed with Mkts, wealth effect, than the real productive segment of the economy, producing living wage jobs. Unfortunately, NONE of the FOMC has/had never held a job in private sector or the experience of running a pay roll! We are being lead by a GANG which is unable to shoot straight!

That brings up a nasty scenario: this whole ball game really can be fumbled out of the technocrats’ control. There was that feeling in September 2008: like looking into a chasm, and being unsure whether anybody on deck had a hand on a working tiller.

The possibility of that, is what keeps me from any notion yet of calling a bottom.

sunny129,

I don’t think you read or comprehended what I said – LOL

Martok,

What did you say? Repeat of CNBC article from two weeks you just read?

sunny 129 said: “after 4 DECADES of deflation”

—————————————–

again???? we have had ongoing and continuous money expansion (inflation 1) and rising prices (inflation 2) for decades.

Martok

Markets have priced in 75 basis points. Also it is tremendously oversold. All indices are at major support. Watch for a face ripping short squeeze!

I sold ALL that day, go ahead and buy – LOL!!

I think that Dimon was trying to frighten Powell and the Fed. Playing his book.

Dimon talks his book and his interest. That is all.

“Hundreds of stocks have collapsed, starting in February 2021”

Hundreds of stocks can be expected to collapse during a recession, but the US isn’t yet in a recession, unless your metric is the collapse of hundreds of stocks, which would be a pretty crappy metric.

They’ve collapsed because Wall St., in its infinite greed, simply couldn’t find enough Greater Fools to sucker into buying stock in crap companies that should never have been chartered as corporations in the first place.

Wall St. cares nothing about crap companies. They care about making money, any way they can. They would gladly sell you nothing and charge you top dollar for it if they could.

They can’t, but doing it this way is the next best thing.

Wall St. (to quote): “Cha-𝘤𝘩𝘪𝘯𝘨!”

unamused

The beginning of recession is only obvious in retrospect. By the BLS announces that date, we all be coming out of that recession. Some think we are already in recession. Europe is already in one!

With continued interference from Fed since ’09, Mkts and the real Economy remain disconnected. Earnings have been manipulated by Buy-back shares gimmick, not excluding creative accounting. Even the GDP and inflation rate are constantly being manipulated, like putting lip stick on a pig! It is grotesque mess!

“The beginning of recession is only obvious in retrospect. By the BLS announces that date, we all be coming out of that recession.”

Beginning and ending dates of recessions are formally determined by the National Bureau of Economic Research, a quasi-independent concern, and not by the Bureau of Labor Statistics. You have to get these things right or readers will simply roll their eyes and move on to the next comment.

“Some think we are already in recession.”

Many Americans are always in a recession, a plunder-centric economy being what it is, so while your assertion is true it doesn’t actually carry any meaningful insight.

I like finance and economics jokes if you have any.

I believe it was Al Capone who said “You can get much further with a kind word and a gun than with just a kind word alone.”

Gomp

Don’t knock my fellow Italian “Al” once removed. If he were president right now the country would be better run.

You ain’t seen nothin yet

Bbbbbaby you ain’t seen nothin yet

These are early days, strap in, weeeeeeeee!!!!

1) Inflation is rampant in the ME. People are angry. Gov are volatile.

2) NatGas weekly failed to close > May 23 high and turned down sharply, closing under May 23 low.

3) Amos Hochstein might fix the problems, sending NatGas weekly

further down, with some help from USD.

‘Wall St. cares nothing about crap companies. They care about making money, any way they can. They would gladly sell you nothing and charge you top dollar for it if they could’

Only, if one is willing to buy from them, blindly without doing due diligence!

Stocks got bid up, mindlessly since ’09, b/c of Fed’s PUT guaranteed, that there will be no loss! It is NOT just the WALL ST but Fed ( + SEC, FTFC) is clearly complicit in this scandal. So are the regulators and our Congress!

“It is NOT just the WALL ST but Fed ( + SEC, FTFC) is clearly complicit in this scandal.”

I use FIC as a handy abbreviation for the Financial Industrial Complex.

“So are the regulators and our Congress!”

So talk to the USSC about reversing their decision to make bribery of elected officials legal, focusing on those appointed by presidents with an “R” after their name.

There are still several with a “D” after their name who are trying to keep you from having to live under an odious despotism next year, one that will have the morals of a famished barracuda, knowing that you could be very uncomfortable with the resulting squalor.

Sooner AND later una,,, u and WE will absolutely have to deal with the concept that ”fascism” is the aberrant of the left AND the right extremes…

Both SO clearly obvious in the ”run up” to WW2, if one cares to read the ”official reports” AND the very extensive other reports, journals of participants,,,, novels from those who were involved., whatever.

Time and enough for all of WE the PEONs to grasp the concept that aberrations leading to EXTREMES from any side are NOT helpful for the long trek to actual equality/democracy.

As an optimist, I can only hope that the clear challenges, IMHO propagated by the oligarchs who really are confusing their battles, SO similar to the generals of all kinds, with the last crash, will be resolved with at least ”neutrality” to those rich folks, while absolutely ”empowering” all,,, repeat ALL of WE the PEONs to get to work and enjoy the benefits of OUR HARD WORK…

Otherwise,,, ”IT” is really going to go down,,, and much farther DOWN than any of the oligarchy can comprehend based on past performance.

‘”fascism” is the aberrant of the left AND the right extremes…’

Faux News has pickled your cognitive functions.

Don’t under estimate the small real estate pyramiders …the 3, 4,5 unit owners and their new predicament

And dont underestimate the hit the pseudo intellects took in cryptos….forcing them to sell the “good” to pay for the “bad”

Thanks god I got out of Affirm early. Still lost but could have been much worse. This is a rough market to be green at investing.

It looks like you practically could have called the top of the market by looking at when margin debt started to first trend down significantly. I wonder if bubbles often behave like this graph.

Peachy, rather than trying to find the indicator that can tell when the market will turn (“timing the market”) you might find that a book on fundamental analysis or one on value investing may keep you from losing your shirt or blouse while learning to ride in the rodeo. B. Graham’s “Security Analysis” or his “Intelligent investor”, or maybe a Cliff Notes version, may serve as a good start.

Peachy, that is correct. Good observation. Now that you know this part, try calling the bottom.

Big S = Standard and Poor?

Big S hits the fan: The S is the first letter of a four letter word that cannot be mentioned in polite company.

PPI came in HOT again, so expect another high CPI number in next month’s report.

The YOY will begin to be measured against last year’s start of the inflation run up…..so the YOY might not be as dramatic going forward.

And CPIs that “read” as if inflation is being tempered (ex food and energy) will be heralded as some type of progress or victory…BUT,

and increases will be stacked upon the 8% of the last 12 months. Cheerleaders will ignore this fact.

Someone should ask the Fed

“Why is there still a 2% target when 4 x’s that was just packed into one year? Doesnt that change your goals? Should not the ‘new” target be rolling back those punishing price increases? (negative) Would the Fed welcome such?”

That’s true, but no matter what inflation is 8.x%. A big relative change matters coming from a low base, but if the base is HIGH, even a 0% change will hurt people’s wallets.

The cliffs seem to be steeper for the dive. Congrats FED!!! #CliffDiving #CashIsKingNow

Jim Cramer was on CNBC this morning complaining about all the hate mail he is getting on Twitter. He said Lucifer has a higher poll rating than he does right now. He added that the Fed should initiate “Shock & Awe” and go for a 100 basis point rate hike today.

The U.S. consumer is not really in great shape financially, and I am not just talking about the multiple decades of decline in inflation-adjusted or real incomes. The surge in Credit Card Balances in last month’s report, and in a tanking Consumer Confidence environment to boot, is just one more indication that many consumers are living paycheck to paycheck, and with surging monthly costs to live, many Americans are falling further and further behind the Eight Ball.

This obsession with debt as a solution to inadequate income flows or accumulated cash is most readily apparent in the U.S. financial markets as the charts above display. Investing with leverage is great on the upside in a bull market, but is proving across the asset spectrum to be deadly on the downside in the current Stock and Bond Bear markets we are firmly within. Ain’t going to get better anytime soon, except for those thrilling Bear Market counter-trend rallies where the Buy The Dips crowd dust off their buy buttons. Never try to catch a falling knife.

Still betting we are already in recession. The Fed is going to show real conviction at today’s lovefest and do probably a 75 basis points increase in the short end of the curve. If one studies their minutes and press conferences one can plainly see that they always leave themselves the OUT to do other than projected or expected monetary moves based on economic and/or financial market conditions. Recession not declared at this point, not their fault. Bond yields, where the rubber meets the road in actual trading, have already priced in an average of 4% Fed Funds by year’s end, and I think that is on the conservative side.

PPI came in with a 10% Year Over Year increase, so the peak in inflation via the CPI has a long way to go in percent terms before anyone can breath easy. And how about that oil price??!! Ain’t hit a top yet either.

Cash ain’t trash, and tangibles that hold their values vis a vis purchasing power over hundreds of years are the places to be. Aside from some stock and bond short positions …. of course. Layer in on a cost averaging basis. Back to retirement.

An uninformed person, like me, could get the impression that many of the newer companies in the US weren’t started with the actual goal of making a product or service. But for the purpose of making money on the stock issued by the company before it hits the inevitable skids.

I really thought margin debt would have dropped further given the losses in the market so far. And why haven’t these people covered their margins with their stock market gains to date??? The market is giving them every opportunity to cash out and live well by dropping slowly.

welcome to great depression 2.0