Margin debt is just the visible tip of the iceberg of leverage, and it reached the zoo-has-gone-nuts level.

By Wolf Richter for WOLF STREET.

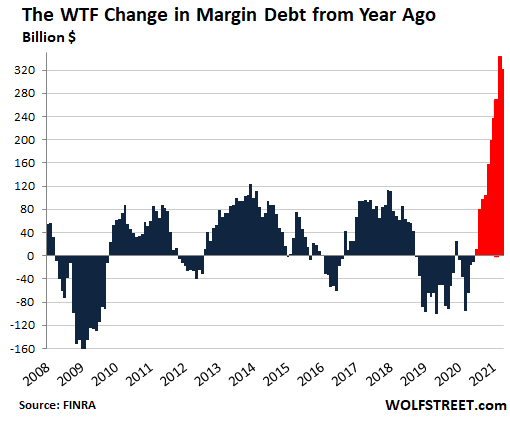

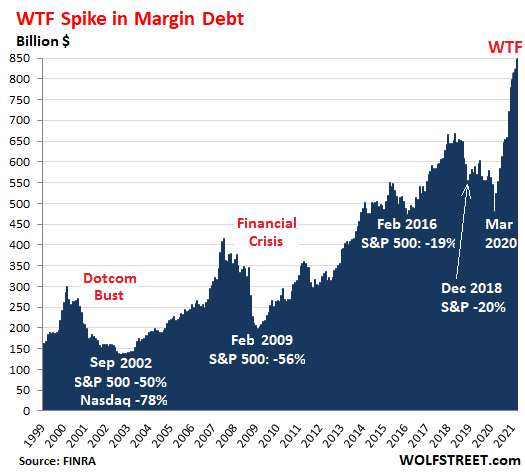

Stock market margin debt jumped by another $25 billion in April, to a historic high of $847 billion, according to FINRA data. It has exploded by $188 billion in six months, and by 61% year-over-year, and by 55% from February 2020:

Excess leverage is the precise and predictable result of the policies the Fed is promoting out of one side of its mouth with its interest rate repression and asset purchases.

Out of the other side of its mouth, the Fed – via its blissfully ignored Financial Stability Report – is warning about leverage, stock market leverage, and particularly the vast and unknown parts of leverage among hedge funds and insurance companies.

It named names: The family office Archegos, a private hedge fund that has to disclose very little, and that then blew up because none of the brokers providing it with leverage knew about the other brokers also providing leverage, and no one knew how much total leverage the outfit had. The amount of leverage didn’t come out until it blew up.

And this form of hidden leverage is not included in the known stock market margin debt reported monthly by FINRA, based on reports by its member brokerage firms.

This known stock market leverage is an indicator of the trend in leverage, the tip of the iceberg. History shows that a big surge in margin balances preceded and perhaps was a precondition for the biggest stock market declines.

In April, it exploded to a new WTF high of $847 billion, up by $188 billion in six months, having ascended to the zoo-has-gone-nuts level:

In this type of chart that covers two decades during which the purchasing power of the dollar has dropped, long-term increases in absolute dollar amounts are not the focal point; but the steep increases in margin debt before the selloffs are.

Leverage creates buying pressure and drives up prices. As prices rise, the collateral can be leveraged up further, and leverage builds with rising asset prices. And then when prices decline, the leveraged bets are sold to pay down the debt, and the selling triggers more price declines, and forced selling sets in. This is when Archegos blew up.

And so the Fed says in its Financial Stability Report that “measures of hedge fund leverage are somewhat above their historical averages, but the data available may not capture important risks from hedge funds or other leveraged funds.” And it recounts the Archegos fiasco, in terms of how this hidden leverage works:

“In a separate episode in late March, a few banks took large losses when a highly leveraged family office, Archegos Capital Management, was unable to meet margin calls related to total return swap agreements and other positions financed by prime brokers. Price declines in the concentrated stock positions held by Archegos triggered the margin calls, prompting sales of the stock positions, which led to further declines in the prices of affected stocks and, ultimately, substantial losses for some banks.”

“The episode highlights the potential for material distress at NBFIs [Nonbank Financial Institutions such as hedge funds] to affect the broader financial system,” the Fed’s report said.

It’s ironic that the Fed, out of the other side of its mouth, is warning about the results of its policies, including the ballooning leverage that isn’t known until it blows up.

Ha, and then says the Fed, still speaking out of the other side of its mouth, if that risk appetite declines “from elevated levels,” and outfits want to get out from this leverage, or are forced to get out from under this leverage, “a broad range of asset prices could be vulnerable to large and sudden declines, which can lead to broader stress to the financial system.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Funny how everyone says the Great Depression was caused in large part by an excessively leveraged investment market – and people then invent new ways to create a new way to generate excessively leveraged investment markets.

But, of course, the real problem is any regulations passed to prevent excessive leverage in the markets.

Fed doesn’t even need regs to let air out of this idiot bubble.

The tiniest taper (or even mere head fake) would shear 20% off this doubly or triply overvalued mkt…but that is the problem.

Everybody knows the insane overvaluation of equities only makes remote sense in the context of the systemically diluted dollar…and that the political lives of DC would end tomorrow if such dilution were stopped.

Thus the “problem” – the long term health/viability of the American economy or the private interests of a bunch of DC careerist sh*ts.

Guess which side has won for at least 50 years and whether reform could ever conceivably occur from the inside.

Interesting how the “DC careerist shits” find no problem privatizing the financial profits and socializing the financial risks: but for vaccinations find the needs of the many outweigh the risks to a few.

The Great Depression was not caused by market crash. Very few Americans were invested in the stock market.

However hundreds of banks collapsing wiped out millions of people’s savings.

About ten thousand US banks went under.

Moving on to today’s evaporation of wealth or wealth effect, as of today, Wed 19 AM, Bitcoin is down 25 % and XRP down 40 % overnite. Most exchanges are stalled by volume dumping. Significantly, CNBC is linking a mild tech sell- off to this coin thing.

A trillion dollars has been wiped off the coin space. Could the Fed be tempted to buy just a tad of BC, a lousy billion lying under a desk, to stabilize it? Just the announcement would do wonders. Sounds crazy, but does it matter how the ‘wealth effect’ is created?

When the term ‘nocoiner’ was born, that was the time to sell bitcoin (whatever that is).

Banks are major holders of investments. It affects liquidity if they have massive losses. 1929 was comparable to a tech crash effect on tech sector with the latter experiencing a 75% decline for 15% of the economy.

Excessive real estate lending and farming ill-suited prairie land due to Homestead Act were other reasons.

My mom said almost everyday one read a about a small town banker shooting himself, having failed at his duty to his depositors.

In the GFC the only suicide I know about was a European Noble feeding friends to Madoff, unknowingly.

Today’s financial bunch is a different breed of cat, no honor, no responsibility taken for their actions, and definitely NO EMPATHY.

So what has happened since then?

I guarantee you, any author that is able to write a concise, comprehensive, and accurate book containing the cause(s) has a best seller….and blockbuster movie royalties.

Hard to believe in 1920 the Shiller PE was 4.78 and today over 36. PE of 36 is earnings yield of 2.8% or roughly Fed’s intermediate term inflation rate goal.

A lot of finance is an asset gathering business. It’s free money for them when asset values go from low to high. Same with Real Estate. 6% of $1,000,000 is better than 6% of $200,000.

According to Avi Giburt over at Seeking Alpha, when this thing finally blows, we’re likely to be pretty close to those P/E levels again, and probably with equally destructive economic effects. His Elliot Wave analysis suggests a 70 to 80% sell off over a decade or more. Given his seeming ability to read the tea leaves, he might not be too far off the mark.

Is not just the leverage used to buy stocks outright, but the incredible exposure that Hedge Funds and others have created by shorting stocks in many different ways. In theory there is collateral in place to match a funds exposure to shorts going the wrong way, but from what I can see that has gone out the window also with naked shorts, fakes shares, and who knows what else.

It would be nice to see margin as a percentage of market cap.

Market participants believe a sudden unwind is highly unlikely, therefore the leverage.

And the passengers on the Titanic were sure that it had enough lifeboats…not that they could ever possibly be needed.

The Titanic was so unsafe no amount of boats would have helped. The thing literally burned for weeks before it’s maiden voyage.

I recall an abandon ship drill, standing on the deck of the aircraft carrier. The chief sent the supply PO to get the lifejackets. He came back, and said, “there are only enough for about 1/3 of the people in the division..” The chief said “Don’t worry, if this was the real thing that would be enough..”

FWIW – When the abandon the Bismarck, I don’t think one third of the crew was still alive.

Good story AB, but that’s a combat (and like any military support vessel, still at high risk, even at peacetime).

After the Forrestal (right?…the carrier McCain was on), fire disaster, the Navy changed it’s basic training so that EVERY sailor was a fire fighter, no matter his later official MOS and job. Just like in the Army or Marines EVERYONE is trained as an infantryman, and probably for similar long ago reasons….forts overrun, or whatever

From the top of my head it’s about 1.3%.

andy,

and before 2019?

The British picked up 10 German sailors, turned around due to

“submarines threats”, ==> the rest were eaten by the fish.

Margin Debt is not peak stupidity right now. Janet Yellen made a speech today that basically said she wants higher taxes and fewer US jobs. Brilliant. Stock markets responded accordingly, down.

Wall street is going to do what Wall Street does, margin debt or no margin debt – whatever works given the situation. Meanwhile you have a Jackass surrounded by morons running the country. For the first time in a long time I am trimming my stock investments. Long time readers here know how bullish I am, so this says a lot. Anyone who lived through the Carter administration remembers how much that sucked, and we are going through the same suckage again only worse. The fed is not our problem now, we got a bigger problem.

I want higher taxes too, guess I also suck.

Ditto.

Duane and Degobah Smith, the U.S. Treasury accepts volunteer contributions. You don’t have to wait for higher taxes to be mandated. You can write a check to the treasury today.

Anybody demanding higher taxes should start doing this.

Duane & Degobah Smith

Please go right ahead & pay more taxes now; don’t just post here about hoping you can do it “some day”.

A lot of people who say they want higher taxes really mean they want higher taxes for other people; 50% of Federal taxpayers already pay no net Federal income tax (different than FICA & Medicare “premiums”).

About 20-30 years ago, Massachusetts citizens also claimed to want to pay higher state income taxes. Massachusetts actually published “voluntary higher tax rate ” tax forms…turn out, VERY VERY VERY FEW actually paid the higher tax. Turns out, a few but vocal minority are very much in favor of other people paying more taxes.

Correct. Higher taxes on the rich are needed.

From 1916 – 1982 the top ferderal income tax rate was above 70%

From 1940 – 1964 it was 90%

The golden years of the USA. The super rich got control of the government again in the 90’s and taxes have been continuously lowered since then. Why anyone thinks that todays low tax rates are “normal” andoptimal is entirely beyond me.

Higher taxes are not needed.

What’s needed is that über-rich people and all of the very large international corporations START to pay taxes. It’s the same problem with the same solution all over this globe.

Artem why do you believe that tax increases on the rich would be passed on to you? That’s your false belief that keeps people like you groveling and worshipping at the alter of plutocracy. A bunch of people with a dishonest agenda started repeating that lie over and over and now you all believe it. The same people lied to you and sent all of your jobs overseas and didn’t give a damn when the middle class got hollowed out. They see you as prey and yet you act like they are your benefactors.

Rhodium,

I never made a statement anything about taxing the rich. My comment was entirely about taxing amazon. Taxing amazon gets passed on to the consumer and to the shareholders, like your 401K. It may also cost jobs.

In return, the government may find better use for the tax money collected.

I could care less about the rich. By definition, there will always be rich people and if you make them the enemy, you just shift power around and encourage corruption, zero sum game.

How about we all get a bill each year from the Gov for taxes needed to balance the yearly budget according to our % of income?? If you want to vote for the current politicians and Fed members blowing the heck out of money, you can pay for it directly.

Due April 15. Your tax bill comes to 82% of your income, just like everyone else of course, for your tax dollar used wisely.

CRV

Your comment: “…What’s needed is that über-rich people and all of the very large international corporations START to pay taxes…”

IRS figures show for top 1% (who you say are not paying income tax):

o Top 1% earned 21% of total US income

o Top 1% paid 38.5% of total US income tax

Always interesting to see how much people know about what they write about. My research took about 30 seconds…

LINK: https://taxfoundation.org/summary-of-the-latest-federal-income-tax-data-2020-update/

Taxes are already quite high in America.

When one factors in the numerous “bilkings”, “fees”, and “insurances”, which are not taxes as such, but, also still things that society demands must be paid for a somewhat tolerable life, then the average American is taxed (and worked) a lot harder than the average Scandinavian is!

Billionaires shouldn’t exist in a democracy. As wolf shows, the only way someone gets that rich is because the government gave them the money, they didn’t earn it.

Tax the heck out of them. 100% tax rate in wealth over $500 million.

100%? You are mad. Mad at yourself for not having the brains to be a billionaire.

I agree they should be taxed more than a middle class schmuck like myself, but to take 100%? Sorry Lenin, I’m not with you.

I’d rather see monopolies like Google, Amazon, Facebook, etc broken up. This would affect the “rich” much more and be better for all of us.

Income taxes are by their nature tyrannical and in 100% opposition to the principals the United States was founded on.

You cannot be a free citizen and have an income tax.

The United States was founded on the principal that every citizen owns themselves and their own lives, and productivity. Your productivity comes from you, and is your sole property. For the government to lay claim to it, they are in fact claiming ownership of your person, negating your individual sovereignty, and creating a slave base system.

If you support income taxes, then you are opposed to freedom and support feudalism.

Don’t wory, you can’t have this many billionaires and democracy, we either end the phenomena that makes them possible, or our we will complete our shift to a more repressive form of government.

How about cutting Government spending? Abolish 1/2 of the government agencies.

Where do people get these ideas from?

People are motivated by self interest, typically that helps to generate some degree of economy activity that then impact others.

When you artificially remove those… well you get predictable results.

Jdog,

You have NO IDEA IN HELL what “claiming ownership of your person” is until you get a draft notice and don’t have the money to pay for a phoney diagnosis or to buy your way into the Reserves……making you pay fair share tax rates are NOTHING…..more akin to “making” you have to wear some kind of clothing in public. TRY going outside nekked, and see what happens to your “free citizen sacred personage”.

And JK, do I detect a bit of that musty old desert god saying, “thou shalt not envy..(“brains”)……” in your mental make-up?

I’m with A, in fact I’d put that 100% bracket at $10-15M, using a Constitutional Maximum Net Wealth.

Curious, what do you want higher taxes for?

If you really want that, there are ways to achieve it besides voluntarily giving money to the IRS.

You could just move to a high tax state.

But if it’s a case of you want other people to pay more, but not yourself… well, that’s rather silly.

YOU actually sound “rather silly”, at least to me, but perhaps I just can’t grasp your way of thinking?

Duane, from the almost “defensive” sounding comments that follow your post, it seems that everyone has totally forgotten Eisenhower and even Kennedy IRS tax rate schedules. Were they and their administrations and the people then just BS’d?

BUT, oddly enough, both presided over the great American middle class times…..or the “maga” times, recently so sought after, but never delivered.

Go figure…something is fishy here.

Juts cut the government a check any time you don’t thing YOU pay enough in taxes.

That’s a classic deep into the second six-pack comment. Ward will sleep well tonite.

Funny you single out Democrat presidents. How about your Trump selling China deal story just about 1000 times, the stimulus story about 500 times, and big V-Recovery another 500 times to goose up the stock market?

I’ve been in the market throughout Trump era. Every single night some mysterious force will push the markets so unbelievably high; we are talking about pumping the likes of which I had never seen. Every single Friday, you were sure that the market will go up at least 1% in the afternoon.

Without Trump, Dow, S&P, and Nasdaq would be half of what they are now. So, don’t single out Democrat presidents.

keepcalmeverythingisfine

“…Wall street is going to do what Wall Street does, margin debt or no margin debt – whatever works given the situation…”

Most of your post made sense, but the above statement is not even close to being correct. A theoretical market correction with $850B of margin debt will much more destructive than one with $0 margin debt.

“The fed is not our problem now, ..”

Disagree. The entity that has run amok, turned lender slave to borrower since 2009.

IMO, the Fed has been rogue since its “rescue” brought the Dow back to the pre 2008 high of 14K.

Everything beyond that was “hey, this is fun…lets keep doing it.”

The Fed became central planners, digital minters (as opposed to short term liquidity provider), and now for the INFLATION TAX they desire…to lay on the citizenry, that will crush and pound working families and put pitchforks and torches in their hands.

Yes, taxes are the problem at historic levels of inequality. Incredible.

It’s not panicking if you run for the door first.

More sophisticated investors like GMO will see this for what it is and in time a straw will break this camel’s back.

By example apparently historical analysis of of the triggers of the 1929 bust are still as vague as to say it was precipitated by “out of town sellers”. Whoever they are.

That red spike is like one big giant erection and FED is the Viagra. This Viagra is not going to let that go limp in 4 hours though, it will pump QE infinity and continue security purchase and low interest rate until it kill the host, who would’ve though Weimar Powell is such a good dealer to the gambling addicts out there.

Lol I chuckled at this one.

Doesn’t seem like Powell and Co. can stop the sell in May and go away that seems to be starting to take hold on the Street.

Oh man……I laughed so hard. Bit I need to bleach my brain now.

“It’s ironic that the Fed, out of the other side of its mouth, is warning about the results of its policies, including the ballooning leverage that isn’t known until it blows up.”

Reminds me of a drug dealer that pretends to care about the junkies..duh aren’t you guys the one pumping them full of money and give in every time when the market throws a hissy fit? Not sure what their play is here, maybe they want to look slightly less guilty when things do end up blowing up and aftermath go on 60 Mins to tell people hey we tried to warn you guys..

“give in every time when the market throws a hissy fit?”

3.2% 10 yr T bond in Fall 2018 = 20% mkt fall.

Fed then bent over faster than a $2 lobbyist.

The US used to have an economy that could survive/thrive with 8% 10 yr Treasury bonds in the 90’s…without going into cardiac arrest.

Maybe the solution to adult onset diabetes is to never allow a sugar crash by eating sugar constantly.

The FED told me so.

I actually had hoped for a while I could get at least a half-ass return on my savings, maybe more….but…

“Someone” bent over fast for “someone”….and really fast. All seems like a short vague pleasant daydream, now…..

While a well over 4000 S&P is nothing short of Aliens in saucers running around….and this margin debt is like reports they are picking some people up and shoving strange instruments up their rear ends.

Phoneix..

Irony? How about the cheap cost of borrowing, provided by the Fed to “promote max employment, tapped into relentlessly by the federal govt to pay people to STAY HOME.

Then the Fed sees the bad employment numbers and keeps the spigots wide open. Cul du sac of Idiocy.

I was looking at the charts for Margin Debt from Yardeni. He has a series where he compares margin debt as a percentage of S&P 500 market cap. It is now the lowest it has been since roughly 2007 (and it has been much higher for most of those 14 yrs).

I hope I’m wrong saying this: this time really is different.

Yes, margin debt drives up stock prices, so spiking margin debt CAUSES stock prices to surge. This happens every time before a sell-off. This is exactly what then drives the selloff and causes so much damage when margin debt unwinds.

So if margin debt depends on collateral and collateral is spiking, 2018 peak of 3% market cap is still long a way to go (either up or down).

There is nowhere I know that discusses this sort of thing in so minute and logical detail. 99% of everybody I have ever known has no idea that these issues even exist, it takes half an hour of explanation to even start a discussion, so thanks for that Wolf.

The thing about debt in general, and most of your charts, is that the absolute level of debt at any time is neutral to demand. It is the second-order ie dd/dt ie change of debt with respect to time that causes changes in demand, and hence price level. If margin debt stayed absolutely static from now on, any change in stock prices would have to come from some other source, eg people spending stimmies on Robinhood.

Your chart of change from a year ago alludes to this over a relatively long time base. Chicken and egg, I think you will find all positives for growth in debt will match spells of rising stock prices and vice versa. Where it could get really interesting, is at the third-order level, ie d2d/dt ie rate of change of change of debt ie is it accelerating(getting worse) or is it slowing(getting better)?

Measuring the slope changes of your charts.

Magic, keep up the good work.

Yes, Steve Keen did chart the 2nd derivative effects in bank money around 2006 as house prices soared. One of the few ahead of his time. Too bad no one listened then. No one is listening now.

You are taking the percentage of independent/dependent variable to take conclusion from that? Are you trying to convince yourself or us?

This only means that the multiplier effect of the margin debt is high; and that is easily explainable because hedge fund and retailers have been driving prices higher through options. So, each dollar put in option has sometimes 10x or even higher effect on the price. This actually makes the bubble far more dangerous.

Hi Dan – Can you explain why and option drives the price of a stock higher. I would think only buying a stock and offering above the bid would drive the price higher.

Just trying to figure this one out.

If Amazon is $3000 and you buy Amazon at that price, then your margin debt goes up by $3000. But if you are driving the price higher through options, then you only have put in for example $50. So with $50 extra margin debt, you have driven a $3000 stock price higher.

If you buy a call option on a stock, the seller needs to hedge his short call position. When the stock price moves further towards the strike, the seller needs to buy more and more stock to hedge this. So this is a positive feedback loop (i.e. self enforcing).

“So, each dollar put in option has sometimes 10x or even higher effect on the price.”

Not really.

Options purchased out of the money, at strike prices above the current level, actually have less dollar impact on the stock.

The delta hedge for the seller of those options is less than one to one.

Not until the stock goes through the strike and is in the money does the leveraging kick in the other way.

I’m pretty sure “options” (calls and puts, the first “derivatives”) were invented in the 70’s by mathematical MIT types. Since they all had a “use by date” or they expired worthless if not exercised, that was one mathematical LIMIT, so to speak, and the other LIMIT was simply somebody’s mathematical version of Wolf’s famous, “nothing goes to heck in a straight line” assumption. They were written and sold based on a formula….plug and play.

That is all there was to them….way back THEN!

Folks who used them invented all the fancy lingo associated with playing around with them. BUT, AND MOST IMPORTANTLY! option (derivative) WRITING, and the RELATIONSHIP of their treatment as a PART our financial “system” has been modified many times over the years BY LAW to suit those who could pay for the new laws, and always working towards their own end benefit, immediate or calculated long term.

Liz Warren’s famous Senate floor shit-fit was all about passage of another newer derivative law written entirely by Citibank lobbyists.

From a simple plug and play math geek formula to something so complex that I am almost certain there is a legal specialty called “Derivative Law” in 40-50 years of twisting and turning lobbying and law writing.

Soros wasn’t kidding when he said, “They can come up with financial engineering faster than you can ever hope to regulate it”…(from memory at his “dog and pony show” hearing after he won big shorting housing (somehow) during the GFC “post mortem”).

I find a Rockefeller friends comment to Bucky Fuller more of the ethos of it all…..as he told Bucky;

“Why make business simple when you can make it complicated.”

The reasoning is obvious, make it hard to ever know quite what to do financially, or who to blame when things get personally worse…and peons are sure too busy with day to day survival to have time to figure anything out, while the very rich stay that way by paying full time attention to it all.

I am kind of thinking about the emotional part. The pain from 2009 bottom has been forgotten. I can still remember how most felt as we got near bottom in 2009.

Wasn’t many people throwing money away then. Buffet had to do an op Ed in Wall Street journal saying he thought it was a good time to buy stocks. Seems like most have forgotten how it feels to lose half their money and to not be sure you are not going to lose it all.

D

Tell me if I’m wrong but, I thought an ‘option’ only gave a right to buy or sell a share at a ‘set’ price up to a certain date and expired thereafter. It was therefor an insurance against a price drop bigger than you could stomach if you owned the shares, or a chance to buy them cheaper if you thought the price was going up but didn’t want to lay out the full purchase price on spec.

I know there are all sorts of ‘magic’ tricks played by speculators nowadays but I thought it was illegal to influence a share price by anything other than actually buying or selling an actual share in the regulated market. Maybe I’m dumb?

@Margin – Thanks for bring up the percentage. The percentage is sometimes overlooked for many analysis. It puts a number into a different perspective.

Many times we look at charts on a specific debt and it keeps hitting record highs. But then again the U.S. add 1 to 3 million people per year. So if they all take on average debt, then the overall debt numbers will hit record highs and freak everyone out but the average debt in theory could stay the same per each person so it is really not growing.

Just an example to put things into perspective.

Spot on Ru.

Population is the missing ingredient in all those indices. If Gdp grows 2% and population grows 3% you are getting poorer as Gdp per capita. Ditto what you say about debt.

The fed reminds me of that Pokémon Card trading millionaire in LA who gave his 17 year old kid a Maserati and then said “who me” when the kid killed an innocent motorist as he was racing through the hills in his dads “present”.

If it had been a Toyota Yaris instead, would that have been a better outcome?

One can’t show off ones racing skillz quite the same in a Toyota Yaris!

it was a Lamborghini Urus.

Had no idea the dad was a Pokemon trader

He was a distributor of trading cards, which included Pokémon cards. The son he gave the Lambo too didn’t even have a license.

And on the other end of the spectrum there’s this Belgian & Dutch kid who was too young to have a driver’s license when he won the 2015 Australian Formula One Grand Prix.

Dad didn’t give him the car, but he also drove in F1.

Those that leverage up to play the stock market are gamblers. Some people seem to need to get their gambling addiction fed (no pun intended) with non-stop action.

Unfortunately there is no license requirement for purchasing most stocks, options for futures for personal consumption. Except, of course, for the “qualified investor” bullshite. Fortunately you can go to Nevada and almost immediately lose all you want.

An excellent example of nurture far outweighing nature (in our old argument), although daddy did some racing, too. But I seriously doubt the existence of “F-1 Genes”…(too complex) Which reminds me, since I went to cheaper TV pkg, I sadly no longer have F-1. Have to use the site, kinda like the “Kangaroo” I used at Spa in ’07, sans pics. My one time only trip to Europe, 6am practice day to 6pm race day eve. Worth it.

What could go wrong?

Biden should tell Jerome to make the stocks go higher with NIRP and increased QE, and to create a Fed backed SPV just for stock margin debts with Fed buying up securitized margin debts that way the merry-go-round will never stop. That will encourage more stock market investing. And no more stimy checks to people but only the real people who built and run America – corporations, so instead Biden should make the Fed give that to corporations because they are already paying too much offshore taxes like in Ireland at what 6%? And the Fed could set up another SPV to buy corporate stock buybacks directly but at extra higher prices to encourage investment and job creations and make the stocks go up some more, too.

Then we could balance the budget by getting rid of SS & Medicare and cuts corporate taxes some more.

Indeed. And then the federal government can issue “Inflation Compensation Checks” to everyone to offset the ill effects of inflation.

That should work, right? /s

Well… In the name of “making money” they could also just make us all slaves and donate 100% of the theoretical value of the paychecks to the company stock. Since we’d all be paid in scrip or whatever for bare bones necessities the company at that point would just use dollar transactions between other corps. They could collude to buy each other’s stocks only ever at a higher price, and always on time (with a CB as the sole government entity to print dollars whenever they’re feeling a bit sad). Then they could glory in this concept of wealth while eating the fruits of our labor. It’s the perfect win-lose situation.

T

‘Masters of the Universe’ can do anything they want unless little humble voters stop them. It’s called democracy.

Wolf, do you think ratio of margin debt/total market cap is more accurate?

The only thing that matters about margin debt is that before each crash, margin debt soared, and as stocks were coming down, margin debt unwound and added lots of power to the selling process. That’s the only thing that matters about margin debt. It’s the great accelerator on the way up, and on the way down.

Add to margin calls the fact that very few are shorting this market, so less short covering (which slows a market crash) IF/WHEN the Fed can’t juggle any more monetary plates ad infinitum. Perhaps the Fed will drop a few monetary plates on purpose soon though, as dropping the MBS housing panic buying mania plate might be the best idea to stop spiking long term inflation as a lot of this “free money” is coming out of the home equity ATMs…so perhaps the Fed is a “Psycho Genius”, let us hope…

But don’t worry, I’m sur Psycho-Fed can drop all the monetary plates at once and then immediately launch an USD based central bank digital currency to buy up all the crashing stock ETFs, homes, Apple’s bonds, and all other top 1% financial assets both real and imaginary. ALthough watching the dollar fall 9.68% over the last 12 months, perhaps the Fed should label it “shitcoin”, as who will invest??? Worry not though, as I’m sure the Supreme Leader at Tesla will buy $1.5 billion, just like with $BTC…and then rage tweet crash it 50% for fun, as what does one do for fun when money is no object???

Fed has all the means and ammunition to pop up the market as he sees fit. There seems no evidence to suggest home owner treat home equity as ATM the same way as last time.

Yort,

Might be a surprise if inflation really is here and Fed is backed into corner about raising rates to kill inflation. Market expects Fed to save it, but if inflation is here and Fed can not injector more heroin, market might have to survive on it’s own

It looks more like a top every day.

We’ve been topping for the last 10 years.

We can do another 10 easy.

I am wondering – when it has eventually crashed, what the discussions here will be like about whether we are finally at the bottom or not yet :)

Why does it have to crash? Maybe the Global CB have it dialed in. It might be different this time. Nothing this time is lining up like all the previous times. This bubble is made of the good stuff that doesn’t pop. Much like when SpaceX went up against the big boys and won after sticking the landing literally. I never thought they had a chance but this time it was different. The world has changed. $20T stimulus here we come

Yep, these guys dice up that margin 1000x

the bernanke Put in 09 started it all….

the market is juiced like no other time but it looks controlled now….

Market Schmarket. Let’s look at the reality of the overall economic situation. You have massively inflated market bull runs on overly valued securities. . .yet the ACTUAL market produces less and less. Look at futures markets, how can futures contracts continue to value higher and higher when the fundamentals of the underlying asset/commodity are regressing? Answer: they can’t. Its all fake pump and dump. There are no magic tricks here people, this all comes down to basic economics-eventually. Now I can’t say when, but it WILL have to correct.

I think these people are forgetting that in this bubble prices are being driven up through options. In the past bubbles, options were not playing such a huge role.

The big moves come from the sellers of options trying to hedge their positions.

Sellers of volatility, sellers of the VIX count on nothing happening , net, over a certain period. They collect each day on time erosion.

BUT, when the window breaks, either up or down, the magnification of the move accelerates. This is where the big moves come from.

So, Archegos is the new LehmanBros ‘hot potato’ writ Larger .. which blowed up in the Feds rattletrap over-cooked appliance, possibly leaving quite the mess, with potentially other *SPUDs (Special•Purposefully•United•Disasters) to make any uhh, ‘oven cleaning’ impossible!

What are you waiting for, Jerome? Get on top of it, before the Eccles kitchen is ruined beyond repair!

*SPUD bits make for a fine home fry meal .. seasoned with saltpeter … and smothered of course, with plenty of formerly buttered pork!

Yummm …

Where there is a cockroach, there will be a lot more. You can bet there are at least a few dozens Archegos style hedge funds/family offices of various sizes who are leveraged 10 times their size.

When Long Term Capital was saved…

when AIG was saved, Goldman allowed to change banking jerseys in the middle of the game…when Lehman was allowed to go under, Bear Stearns, while others were saved….

those events were revealing about the “big game”.

Its like OJ Simpson being caught escaping with the victims blood in his car…..and then being let go….kinda

Would Archegos be the Westernised Version of Chinese Shadow Banking?

Not only is there more than one roach in the kitchen, but, we are being directed to look at kitchens, when there is a “roach universe” sitting right down the road, at the “meat factory” – the unregulated derivatives markets, about 60x “the market value” (assumning such a thing can exists for things that do not trade in a market as such) of the regulated exchanges, and, being “unregulated” that “market” doesn’t have to track boring and rude things like lending, leverage and collateral!

I think the regular stock market dropping 60% is well contained. The OTC-market …. nobody knows what that thing is doing, why it is doing it, and what will happen when somebody stubs their toe one fine morning and sells in anger!

After the smoke clears from the 2021 Implosion in 2026, we need to be able to audit the May, 2021 positions in the financial markets of the current Fed members via their not-so-blind trusts; kind of like wearing a blindfold with one eye uncovered. It will be stomach wrenching. These clowns, bozo’s, and charlatans (feel free to fill in your own derogatory labels for Fed members, we should start a contest!) know that the wheels are about to come off of the Post-2008 Hindenburg Bubble, and most of their double-speak is merely to cover their not-tiny asses so that they will still have a shot at the $200k per gig speaking tour scam a la Greenspam, BerKnuckleHead, Billy Boy, and Hillary Dillary Docs.

By 2026, many a pitchfork will be lodged in the facade of the Eccles Building in Washington, and the Fed Heads will be quivering underground to avoid public exposure. It will be about this time that the Abolish the Fed movement will be cresting like a primary tsunami wave.

David…

Yes. There should at least be a “delayed” audit into the details of the Fed’s operations. 6 months ?

There is a delay as to who is using the Discount window, and I guess there is some wisdom to that…

But some transparency is warranted….demanded.

The Fed has accrued too much power….to expand the money supply by 27% in less than a year? My God…what power..and by an unelected body, and likely the decision of one unelected person.

And to lay an inflation TAX on the citizenry when the Fed is instructed per their mandate of stable prices to FIGHT INFLATION…..and no outrage.

I guess the attitude is the “If it is wrong, but helps me, I will not object.”

So Congress and the fully invested have no issue with the affront to the mandate violations of the Fed.

Historicus, this Bubble is of record magnitude and the damage it will do to the 90% that have not ridden the Financial Market Rocketship to the moon will cause, IMO, the Sheeple to be very Woke to what body of people put them into the carnage that is just ahead. Hate to be so pessimistic, but this financial system, Government, and lopsided economy are so out of control, it is sickening to watch for a guy who grew up in the 1950’s and 1960’s when sanity and prudence were actually valued traits.

In the last 2-3 months, I’ve seen numerous times that whenever the stock market is under pressure, just at right time, the FED comes in and starts buying 10Y and 30Y treasuries to force the yield down real hard. Once the yields are down, money moves from bonds into stock market and voila stocks go up.

This happens specially right before the markets open; they force the yields down just before the market to force the stock prices higher.

And these criminals banksters talk about asset prices and leverage being high? The only reason they are doing it so that if the crash happens, they can tell us “We told you so.” Otherwise, they want and will continue on this path till something breaks.

The last time inflation was in this neighborhood, 1999 and 2006, 30yr mortgages were 6%. Now 2.95%. And the Fed keeps buying MBSs!

Everything the Fed touches, it skews.

Why would the Fed, who is pushing for higher inflation, lend money 30yrs out at the inflation rate….or lower?

An article on Zero Hedge mentioned the last time inflation ran this hot, interest rates were 18%. Not sure this is correct, but the point is made.

“And these criminals banksters talk about asset prices and leverage being high? The only reason they are doing it so that if the crash happens, they can tell us “We told you so.” Otherwise, they want and will continue on this path till something breaks.”

I find it funny that most of you only focus on the bankers. Think of the people at the top of all other industries, they all went to school together, live in the same gated communities together, country clubs and so on. You honestly think they are just as bad?

You honestly think they aren’t just as bad?

You people can all relax. This is all going exactly according to my PLAN.

Muhahahahahababaha!!!!!!!!!!

…an article I read. You buy the apple for $1 because you think it will be a good investment. The next guy buys one for $2 because he thinks it is a good bet to make some money. The charlatan buys it for $10 because he knows FOMO will drive it to $15/apple. Soon the apple is going for $300 because you don’t want the actual apple you want to sell it for $400 tomorrow. Nobody eats the apple just the thought of what they can sell it for

Jerome Powell headed for a “Bridge Over the River Kwai” moment…ala Alec Guiness

https://a.ltrbxd.com/resized/sm/upload/4t/5e/sn/dq/the-bridge-on-river-kwai-120-1200-1200-675-675-crop-000000.jpg?k=4d39fe5a0e

J POW is a pawn in a dangerous game men in black tell him what to do sad really I think the true outcome or reset will be terrible deflation or civil unrest not a good outcome either way say bye to 401k house savings

Or more likely what not to do…

“And this form of hidden leverage is not included in the known stock market margin debt reported monthly by FINRA, based on reports by its member brokerage firms.”

The Unknown

As we know,

There are known knowns.

There are things we know we know.

We also know

There are known unknowns.

That is to say

We know there are some things

We do not know.

But there are also unknown unknowns,

The ones we don’t know

We don’t know.

By Donald Rumsfeld—Feb. 12, 2002, Department of Defense news briefing

Yes, it is usually the unknown unknowns that will really do you in. “The pot you are watching may boil, but it won’t explode”

It’s not what you don’t know that kills you. It’s what you know that ain’t so.

The RUT should be first index to break down….a break below 2190 might not be helpful for bulls…

Why does arcane crap like this control half of my retirement money? Can’t we just invest in companies that employ people that make the company money which then pays a dividend and or creates more stock value? Why is it legit to break things into little pieces and then value those pieces more than the original value. I know I’m sounding naive. I am. All this derivative investment stuff and margin investing belongs far away from the money I’ve saved religiously since I was 14. Casinos and banks have different rules. I think someone ought to start separating out the casinos from the banks and get some stability in the stock market.

I’m with you. The whole financial system is needlessly complicated. Seems it got this way by some combination of accident, and by purposeful design to siphon off slivers of real earned wealth one transaction at a time.

I understand there might be a good use for options in agricultural products…but do we really even need stock options? Do we really need derivatives? Do we really even need leveraged positions? It all just seems like it adds unnecessary volatility to me.

One creative legislator looking for a tax loop-hole actually created the 401(k), which was a cost savings for businesses having to spend extra money to manage and guarantee pensions for retires, and instead make each and every worker responsible for their own self-funded retirement.

401(k) basically means each and every person has to either be their own financial guru, or hire a guru and still have to know enough to make sure they are not just taking your money via fees and poor returns. Corporation managed pensions to self-managed 401(k)s…what’s next, self-managed healthcare via Youtube DIY???

The irony of the 401(k) tax loop-hole is the number “401” comes from the “section 401” of tax rules in which it was found, and it was specifically subsection (k)….and thus 401(k) was born. I wonder if it would have been as popular if it would have been located under “Section 666”, subsection (D)…yet perhaps in was in a parallel universe…HA

I am so very with you. It’s very frustrating, and as a prudent investor, you look at the market and see a casino? WTH is this strange world we live in with zombie companies, spacs, crypto currency, etc. That crap all used to have a place, the pink sheets, and over the counter marlets. If you wanted to dable in high risk, shady valuations, and undiscernable balance sheets, you could. The rest of us had a market to place hard earned dollars and see a modest gain year over year, by investing in sound companies and securities. Not dogecoin, or buttcoin, or whatever it is.

Bitcoin at $39,500 right now, down about 40% from its high a few weeks ago.

ETH at $2,950 right now, down 32% from the high 6 days ago.

This market has changed.

Save us obi elon kenobi, you’re our only hope…

Seems fitting as “The Darkside” $90 billion $BTC haul just headlined tonight in order to crush the rebel scum on reddit…forcing Princess Yellen to use “the force” soon on Supreme Leader $BTC.

woops…$90 million, not $90 billion…I’m thinking like a Psycho-FED now…basically always supersize at all costs…HA

“Today’s billion is yesterday’s million”…Psycho-Fed 2021

The crypto crash just goes to show that SNL needs to think about their guest hosts. If they announce Jerome Powell will be on SNL run for your lives.

What a sham this whole crypto “market” is. It’s pathetic watching grown men try to justify their reckless gambling and lure others in by assigning utility to different “coins” when they’re nothing but Ponzi schemes. The kind of people who believed the crypto hype are the same kind who followed Jim Jones to South America and drank the Flavor-Aid.

It is funny how the narrative around Bitcoin has changed. In the beginning is was hailed as the currency that was going to take over the world. It would therefore be very valuable, because there is a limited amount of it and so the value of each coin has to increase a lot to be able to serve as a monetary base. It was also supposedly trustless.

Of course BTC is useless as a currency because it doesn’t scale very well. It can only do a few transactions per second and for that we need the electricity consumption of a small country. As a result, you need to aggregate transactions, so you now need (again) a trusted party. It’s expensive and painfully slow too.

Now the funny thing is that the BTC community seems to have finally accepted that BTC is useless as a currency, so now they hail it as a “store of value”. But the whole value thing was derived from its use as currency, which is clearly not going to happen!

However, blockchain technology itself is finding good uses now for settlement of transactions. Most crypto coins (including BTC) will die a slow and painful death. But some of the technologies that have emerge are transforming the way transactions are settled.

Cryptocurrencies have a lot in common with the 401K retirement plans, they are captured pools of money. These captured pools can easily be controlled by their creators. Maybe having all these ringed off pools of money was the plan all along.

Petunia,

I don’t understand the 401K analogy. You an sell your coin at any time, whereas 401K can’t be touched in many circumstances, and investment choices are limited.

Artem,

The 401K is a trapped pool of liquidity with a high exit premium. The exit premium is both monetary and political, it costs money to exit and the govt can limit the exit and controls the exit premium.

Crypto is the same trapped pool of liquidity controlled by its creator. The creator controls the exit premium and the exit thru its mining operation and software. Without the creator’s structure, mining and software, there is no liquidity.

Petunia,

Fair enough. Yes, that is a similar situation. I would add that it’s a bit more democratic than just the creator controlling everything. I would say it’s demand [for transactions] and the supply [of mining] that controls coin.

The whole point is software is law, and there is no centralized control. This falls in line with the secular trend of anti-central bank and anti-fiat movement.

Artem,

Don’t make the mistake of thinking of software as law or a semi permanent operating structure. Software can be changed continuously by the creator, without any warning, to change any attribute.

Petunia,

That’s the thing. Software can’t be changed once the network is in the wild. That’s the whole point, it’s distributed over many nodes, and virtually unhackable due to encryption. Unless all the coin is owned by one person who controls all the nodes, there’s no way to pull the carpet from under it.

Artem,

This is not the place for a lesson in hacking live software. It can be done and done across networks. You are living in fantasyland if you think otherwise.

I accept the author’s observation that rapidly peaking margin debt has pumped up asset prices which has led, through a positive feedback, to greater leverage of debt. From general control system theory, positive feedback creates ever larger perturbations until some limit, either by design or through failure, is breached. It is not clear to me where this limit is, or how it may be determined.

Therefore, I’m interested in estimating how much is at risk once the breach occurs. I acknowledge that this is just the iceberg tip, but let’s start somewhere.

I see that the FINRA dataset has 3 columns – “Debit Balances in Customers’ Securities Margin Accounts”, which the author cites, and two credit balances – “Free Credit Balances in Customers’ Cash Accounts” & “Free Credit Balances in Customers’ Securities Margin Accounts”.

I read the net difference between the sum of the two credits and the debit as “net customer cash”.

The FINRA dataset runs from 1997 and, from 2001 to 2012, shows +ve “net customer cash” between +$16B and +$50B with a +ve peak of +$200B in 2008. There were short lived -ve dips of around -$60B in 2007 and 2011. Over the 2001 to 2012 period, margin debt increased ~2x from $175B to $400B but the “net customer cash” was still +ve and manageable. Thus, I conclude that should the unthinkable happen and all the underlying assets go to zero, the brokerages are still solvent. I’m ignoring the bailouts for the sake of simplicity.

Now, from 2012 to 2021, the margin debt as increased by ~2x again from $400MM to $875MM. However, this time the “net customer cash” has gone massively -ve: -$320B in $2018, to -$396B for April 2021. This time, if assets go to zero, the brokerages will be insolvent to the tune of ~$400B.

I don’t think all assets will go to zero, but I don’t know the current value of customer assets held by brokerages. Will a 50% drop still ensure solvency?

In lieu of more concrete data, a “back of the envelope” worst case of $400B seems “systemically risky”, and would likely require yet another bailout. Or, perhaps I’ve got completely the wrong end of the stick and everything’s just tickety-boo…

BB, your premise/initial postulate is incorrect:

” From general control system theory, positive feedback creates ever larger perturbations until some limit, either by design or through failure, is breached. It is not clear to me where this limit is, or how it may be determined.”

Should bee: ”uncontrolled positive feedback”,,, which I would not suggest is not happening these days.

Have fun with it!!

OTOH, I cringe every time I read on here or other where that ” the LAWs of physics and economics” are XXX (fill in the blanks of your own choices.)

C’mon folks, just in case you have not been following the latest ”muon” conversations: There are NO laws of physics OR economics.

There are only very well considered, tested, and agreed THEORIES of physics,,, and even less well considered, tested theories of economics and all other social sciences.

Try to get over any prejudices of any absolutes,,, it will help you progress in your human lifetime,,, and maybe, just maybe, help you onto your next experience, if any, after your current lifetime…

Maybe, just maybe,,, if you are really and truly lucky/blessed,,, your next time will be as a dog, and you will have humans picking up your poop…

VVN:

“if you are really and truly lucky/blessed,,, your next time will be as a dog, and you will have humans picking up your poop…”

I’m heading in that direction and my dog knows who’s carrying the bag.

VV

I dispute the tested and agreed theory that letting go of this brick above your head will lead to a big headache.

What do you think?

Having a substantial amount of cash could be an excellent bet at this stage. Many people don’t appreciate the option value that it represents: you may be able to buy the S&P500 with 70-80% discount a few years down the line.

Don’t think it can’t happen. While it may seem outrageous, we have seen 50%+ declines TWICE in the past 20 years. And the situation right now is arguable much more precarious than it was in those instances. With interest rates already zero, Fed balance sheet and budget deficits off the scale and inflation running out of control, don’t count on the Fed to be able to backstop it.

With Shiller P/E ratio (CAPE) at about 37 right now and 10 being a reasonable value during a crisis bottom (it reached 5.6 in 1932 and 6.7 in 1982) there is some potential downside here, to put it mildly.

Not a prediction, just stating some facts :)

So holding cash is really a put option of sorts. The premium you are paying is inflation (or more accurately: negative real rates). And you benefit from other people’s leverage (other people’s margin debt, re-mortgaged houses to buy stocks and bitcoin, etc) when this house of cards collapses.

Yea, we’re at 50% cash; how many more months oh wise sage?

It’s an interesting analogy but there are no tangible terms. The “premium” is price inflation, which nobody seems to be able to quantify and which is also a moving target (eg, lumber). The premium is not a set price but a-pay-as-you-go.

There’s no strike price and no expiration date.

The only thing I see in common with a put is that you’re paying a premium in exchange for the opportunity to profit from devaluation of an asset.

Or instead of holding cash buy puts. Maybe even long out of the money puts since you don’t have a good handle on the timing. But if you think there will be a severe correction OTM puts are the cheapest option.

Two words: Counterparty risk.

Also, liquidity. You’re assuming someone will be able and willing to buy those puts if they increase in value.

I can define price inflation. It’s a higher price than the last time you checked for the exact same item. It’s easy to see if you are buying a static product, socks cost more today than yesterday.

It’s also not that hard to measure price inflation in stocks. If no new research or products are in the pipeline for the company, it is static. Static companies price higher as the “commodity shares” are bid up, price inflation. Growth companies are those whose price increases can be attributed to research or new products, leading to higher future earnings.

You’re welcome.

@Pete Koziar

Two words: Nassim Taleb.

His barbell strategy using a small amount of deep OTM options for fat tail risk has reliably put Universa over the moon during market meltdowns.

And Universa works like insurance. Over time your money bleeds away slowly on those options just like insurance premiums but when it’s time to collect on the insurance after a rare but colossal hit like your house burning down, it’s over the top.

Other than physical PMs I have a hard time thinking of insurance that has no counterparty risk.

@Petunia

Thanks. Here’s your Nobel Prize in Economics for solving the problem of calculating CPI.

MG,

The most important thing I learned as a math major was “Don’t ever underestimate an algorithm that counts something. CPI is wrong because they fail to count all the inputs. If you count all the inputs, you get an accurate CPI #.

The Nobel Committee can reach me via WS.

IF not for the seriously out of control Fed folks N2, it would be starting right now,,,

BUT, as several of the old timers on here have commented recently, ”this time IS different” (until it isn’t )

Certainly, the VAST increase in communications of information due to the www and internet THIS time WILL make it ”somewhat” different.

Who is to say when,,, no one,,, who is to say IF,,, getting pretty close to everyone from what is out there on the net the last few days.

Challenge is, Who is to say what the powelle person might do??

NOT ANY reasonable person, so far, and

”the devil take the hindmost” for sure!!!

“Having a substantial amount of cash could be an excellent bet at this stage. Many people don’t appreciate the option value that it represents: you may be able to buy the S&P500 with 70-80% discount a few years down the line.”

Which is why the simplistic garbage economic theory used to centrally plan the price of money worldwide and proven to be so wrong so many times in increasingly large bubble/bust cycles is never fixed, besides being an impossible task in the first place with far too many variables and with far too few data inputs involved, some of the data even being manipulated garbage like the CPI:

Those in position to change it benefit greatly from it and therefore don’t want to change it.

I can still remember being taught cash was deployable capital, savings.

Yep in the past you didn’t really miss much if you got out and set in cash for a few years when market got expensive. I think it is the same this time. You can never be sure, because they can print the nominal market higher like in Venezuela. Fed is going to bluff that they will do whatever is needed. Does that mean QE 40 Trillion. Don’t know.

The old fox guarding the hen house problem. I hear you.

As for sitting in cash, awaiting a buying opportunity, that could be expensive if inflation really gets out of hand especially if the coming bear market drags on for a decade or more and is accompanied by continued high inflation. In such a case that cash (along with the national debt) would get whittled away pretty quick.

However, if this market comes completely unglued, I cannot image inflation staying high for too long as I would expect the subsequent economic upheaval to eventually become a deflationary event. So in the end Powell may be proved right (at least that part about the inflation rate of change being rather temporary).

1) First ever : wall street whales beg the Fed to curtail, because their distribution is over.

2) Warren Buffett sold most of his WFC position, Suncor…. buying UST.

3) If there is such inflation why foreign central banks, US gov entities, banks, institutions and individuals are buying UST. Who is the patsy here.

4) $Lumber : up in two months, from 855 on Mar 2 to 1733 on May 10, down to 1250 in 7 trading days, or : 500 : 878 = (-) 57%, before SPX correction started. $Lumber probably will not exceed 1733.

5) Brokers : 8% x $850B = $68B, plus transactions slippage.

Todays morning meeting

“Archegos and Pearl Harbor”

Using the flip chart, list the common elements. Relax, take your time, get a coffee and cinnamon roll. Break at 10 for a stroll around the grounds. During the late morning session, abstract the tangents. I want to see sweat on your foreheads before lunch.

Oh boy……

Gonna be a busy day here on WolfStreet. ;)

Tic-tic-tic-tic…

Mark Baum: “It’s time to call bull****.”

Vinnie Daniel: “Bull**** on what?”

Mark Baum: “Every f****** thing.”

– “The Big Short” (2015)

Second favorite quote from that GREAT film by Mark Baum: “Boom!”

Correction:

Second favorite quote by Mark Baum from that GREAT film: “Boom!”

Wish there was an edit function here…

For the first time in my memory, the little guys could absorb an interest rate increase. Not so

for the fed or the large leveraged funds.That

is why they are fighting so hard to keep rates low.

It’s their feet in the fire for a change.

I hope they f#cking blister down to the bone! ….. and not just their toes, either.

G

If we can prove they colluded to keep interest rates ‘artificially low’. How about a class action by small savers against the Fed for 12years of 2.5% lost interest on provable cash balances.

I hear your Chicago lawyers are great. Try it on a no win no fee basis.

Just had breakfast and see that Bitcoin is down 23% and Etherium 31% today, at the moment. Hmmm…

23K gap will fill eventually….but it will be a long journey from here to 23K with plenty of volatility….

Yeah, so if you bought Bitcoin on May 8, a mere 11 days ago at $59,000, you’re now down 40%. Some “store of value!”

I’m just curious, does it matter if there is a crash?

Will the fed raise interest rates? Will they decrease money supply?

Will they stop gimmi to everyone making under 150,000 in taxable income? Will forbearance programs and moratoriums truly end? Will there be a child tax credit?

I’m not sure if it matters anymore.

I don’t care if the stock market crashes or interest rates go up. But the stimmies were really nice.

Eighteen states have ended the extra unemployment benefits. They have given their 30 days notice. We will see if the economy is really that great. I don’t think the economy is terrible, but not great either.

Seems like politicians couldn’t have done much worse with public policy than they have in last 50 years. Now we seem to be so divided and heading toward fiat printed socialism that I don’t see how there can be productivity gains to grow real income. If you believe Stockman US has been stuck at about 70 million good paying jobs for 20 years.

Robots have taken all the good paying jobs. Seriously, the rollout of automation hasn’t touched the lower rungs of the labor market. That’s because those people are expendable.

All the cash give without consideration is awful.

It hollowed out middle class savers and those on fixed income. Giving wealth to those on the lower in to transfer to the rich in goods and services.

It made me more poor in the end of the day. It took my 3% savings to .5% savings with bonkers inflation on top.

I don’t know if it was intentional but it seems the political class gave money to the poor to produce votes and transferred it to the rich to earn their political support and cash. Hollowing out the middle class and discarding the older generation preps for future graft as we all become more poor.

All for harvesting political power. Intentional? I don’t know.

I do know good/bad economy they will give out more money to the rich and the marginally poor in the form of direct cash, business loans, and special housing programs. I do believe they will not raise interest rates.

I consider myself middle income and don’t resent the stimulus money I received. We consider the money a refund of our taxes, which were not zeroed out by the stimulus money we received.

Those of you always promoting lower taxes should be glad the govt is lowering taxes for working people like us. I don’t see how you lost 2.5% of your savings by virtue of the stimulus money being refunded to us.

We spent all of our stimulus money because that was the intended purpose of the money and spending it improved our situation more than saving it.

H

Proper interest rates will change the current World beyond recognition. Reality of the true difficulty of making a living on planet Earth without a free pass will bite. Hard work and common sense will regain the premium they should always have had.

“It’s not what you don’t know that will get you in real trouble. It’s what you know for sure that just ain’t so.”

Where have I heard that quote before? Oh, about 5 hours earlier, right here. ;-)

I’ve never been able to pin down the original source.

A lot of HODLRs definitely got killed earlier this morning.

Soon they will need a bailout or two.

That would be unfair to gamblers in Vegas.

What happens in Vegas stays at Vegas.

Seems like an inside pump and dump job. The prices on crypto completely recovered within a few hours. I’d bet, if the information was available, you’d find some sort of sleazy billionaire fraud job going on.

Elon Musk the ultimate Crypto insider.

I wonder what his morning has been like.

MB

Musk, the battery man, maybe doesn’t like it that bitcoin could be a better way to get value from surplus renewable energy than storing it in his very wasteful, dirty and expensive batteries. That’s before any serious work has been done on using computer cooling to generate high pressure steam energy. It’s a beauty, does he know it? Just askin’

I think I would ride out my (dinky) crypto portfolio before I would ride stocks right now.

All I can say is, the premiums over melt silver coins are selling for is amazing. Hard money, baby.

Margin debt per se is not an issue, and the various third party contracts are not a real concern either. Greenspan said “derivatives make the financial markets more secure..” the interdependent web of contracts will never unwind. Even if you wanted to unwind them the cross border transactions shift the pressure away from the securities and onto the currencies, the various carry trades. Oh good news? Not exactly all that money or capital stays in the system, although central banks can backout debt written on phantom collateral. There is more than enough capital generated off those agreements that will never be unwound either. Hard cash. The problem then would be too much money according to economic demand, same problem as always, and that is deflationary. So why are they selling bitcoin? To capture lost capital in the upcoming credit slowdown.

Let see what might happen with the market–

Bond yields dropping

JNK stable

Vix term structure not inverted

Dollar dropping

Rotation out of worthless crypto – gee, who would have though a worthless currency was worthless?

My guess is that the Feds will be announcing some new regulations.

Magic 8 ball says buy the dip. As everyone has been trained for 10 yrs to buy it, I’m not sure why now should be any different. Only anomaly here is, as Wolf says the extreme leverage. Could be we have a flash crash but odds favor another melt up. Some kind of major crypto unwind is likely bleeding over into stocks.

P.S- I’m not buying but I’m not shorting either.

It’s been centuries of BTFD, if you think about it. Monetary inflation is how this country conducts business, certainly post-WWII. We’ve borrowed at a CAGR of 8% every year since 1952 – it’s on the St. Louis Fed site. We’ve always been debasing the currency, except when the markets would not allow it. Always will.

That Treasury does not ban cryptos is proof, for me, that the wealthy want an exit. We even offer futures contracts on them! Talk about capital flight.

So Bitcoin dropped to $33,000 overnight (losing 40% in a little over a week) and now is back to over $40,000, up 20% from the low.

It’s amazing to me that people pay for this crap.

Gambling has a certain allure.

In my opinion, ALL crypto are worthless. The fluctuation of bitcoin price shows an example of price manipulation. I only trust real money like gold and silver.

I can’t wait to watch Bitcoin price falling back to 4 digits. Get your popcorn ready!

Buy the Dip baby!!! This entire market, from Crypto, stocks, housing is all nothing but buy the dip, between that and the FED to the rescue, one even as negative as myself has to wonder how anything that ever go through a major correction unless the majority change their mindset to the other end of the spectrum overnight.

I mentioned right above – I think the hedge funds and family offices have been getting long for years. Cryptos are an almost perfect capital flight mechanism that reflects all our inflation. Our leaders are either ill-informed or corrupt as heck.

“I consider myself middle income and don’t resent the stimulus money I received. We consider the money a refund of our taxes, which were not zeroed out by the stimulus money we received.”

“We” consider . . .? Whose spokesperson are you? The National Association of Middle Income People Who Aren’t Starving and Living in Tents”?

Who resents getting free money, other than the people whose pockets are being picked? And why did you deserve a “tax refund” but not me? The stimulus checks were not intended as a tax refund. You just use the term to rationalize your free handout.

Those of us who didn’t get stimulus checks due to our own hard-earned prosperity might resent your “refund” as well as the money “refunded” to the half of potential federal taxpayers who never had to pay any federal taxes.

As we say in Texas, don’t piss on my boots and tell me it’s raining.

Hear hear

They are only going to give more money and keep interest rates low. There is no escape now.

Our elected officials, yours and mine, decided to send out the dough, as they have the constitutional right to do. So stop whining.

The BS about people who don’t pay taxes is getting old. I helped a low income person do their taxes. Single guy made $28K last year, wages and UI. He paid $1K on income of $18K, not counting SS & Medicare taxes. It’s pocket money to you, but $1K is a lot of money to him, and notice it’s not zero.

Nice, well help them pay for the $10 lb bacon and you did your job well.

Yes, such is the flaw of one man one vote. People vote themselves other people’s money.

The other issue is, it wasn’t at all targeted to people who had lost income. It was given to people to buy crap from Amazon.

We’ve really fallen as a society when the government thinks it’s appropriate to steal money from people to give it to others to go shopping.

I would trade the few thousand dollars we got for an income that disqualified me for the benefit. I would definitely trade $5600 for an income over $150K and the right to bitch and moan about the injustice of it all.

I hope you reach your goal, Petunia. But that wouldn’t make it right for someone to take from you and give you your neighbor who has no real need and will just blow it on a TV.

If stimulus were really stimulus, it would’ve been spread out evenly. If it were to help those in need then there would’ve been some qualification. Neither was the case.

To those privileged enough not to qualify for the stimulus checks and resentful of those who did qualify. Your greed and sense of entitlement shouldn’t surprise me but it does. The moral decay of America is not at the bottom, it’s at the top.

LOL, always amusing to hear people accuse others of greed when they are voicing displeasure with the fact that their money was stolen from them at government riflepoint.

Petunia, I’m just another middle class person with opinions, like you.

I don’t resent employed middle class people who received checks from the government. I just don’t think it makes sense.

I do resent being called greedy. You don’t know what kind of life I live or what I do with my money.

Hear, hear. And those of us in the upper middle class who didn’t qualify for stimulus can buy crap on Amazon just as well as anybody. Therefore, it wasn’t actually stimulus, was it? It was effectively a transfer of wealth from one group to another and that other group was largely not in need. The “stimulus” was either to appease the masses or just another wasteful government experiment. Not sure why I should effectively pay for my neighbors’ Amazon crap while I’m saving for a new roof.

There, I said it. Thank you.

PS. Kudos to those who donated their stimulus to charities that serve people who have an actual need. I know some have done this..

Well said, Turtle. The “stimulus” was a vote buying scheme. Period, end of story. That’s why Biden went out to Georgia to say “Vote for Warnock and Ossoff and we’ll give you $2,000.” The most blatant vote buying scheme we’ve ever seen.

Trump started it. He did two stimulus waves before the election. Biden did one after the election. They’re all doing it.

Yes, but I don’t remember him campaigning on it, as blatantly as Biden did. In any case, it’s a sick system, when people vote themselves other people’s money.

My first thought when Trump started it was that he was trying to win the favor of voters. But too many people already hated him too much. Their minds weren’t going to be changed so late in the game.

You got it all wrong. These people were being cheated out of their rightful share for decades, like say some indigineous folks, and now they get a little reparation check. Shameful to need to make these comparisons, but look at the faces in the crowd, (Jan 6th, even potus said, “they look so poor…”) his base as it were. Don’t worry the liberal rescue plan is to give them enough crumbs to keep them away from the levers of power. The conservative plan is to get out of town with the goods. Naturally you want to be on that bus, crazy or not.

Wolf, what’s your opinion about the current buffett indicator reading? Many say it’s out of date.

1) In the last 6 trading days SPX is bending dma50.

2) A bearish options : SPX is on the way to the small congestion between Mar 26 and Mar 30, to close few gaps.

3) Next stop : SPX might reach Mar 25 fractal, or the Mar 4/5 fractals zone.

4) Thereafter, a sharp rally. The first 9%-12% correction is just the jump start of the next downtrend. The economy is strong, the economy is strong bs is over : JP…please help !

5) A bullish option : the 9%-12% correction is good enough.

6) The round trip to Mar 25 or Mar 4/5 is a small correction relative to

the uptrend from Oct 30 low, or Mar 23 2020 low. The uptrend is strong.

7) SPX on the way to a new all time high.

8) Add 80% of the pole to the next low.

9) Another option : a trading range.

10) Day traders don’t care about the margin of debt.

All they care is about another lunch money in the next few minutes.

When they get it, they click and the margin of debt go zero.

11) The 90Y+ Warren Buffett started using $10B x (1.015^52), because his time frame is shorter.

12) QQQ daily : take a downtrend dividing line from Jan 26 close to

May 11 open for triangles above/ and below. Adjust if wrong.

A lot of crypto margin got wiped out this morning. oof.

Tesla will show a gigantic profit from crypto trading this quarter!!!

That should be enough to offset the problems he seems to be having at his Fremont factory. Supposedly there are 20K cars on “Factory Hold” right now with no known fix yet.

That “factory” although high tech seeming and cool from an outsider’s perspective is basically what E-dog always does. That is, take a giant warehouse and fill it full of the lowest earning, least skilled, wage earners in the area, pay them nothing, and work them to death. Fremont, Reno. . . they’re one and the same. It looks flashy to investors, but have a chat with someone who’s worked there, it’s a different story. I have multiple members on my current team of engineers and technicians that were suckered into the flash and name, only to find out that it’s a grind-you-up sweatshop. Rant over. Not a big Elon fan.

Tesla has a lot of great intellectual property, but Musk is a dangerous combination of a malignant narcissist and a sociopath. The best thing for the world would be for Tesla to go down so that other companies could buy up its valuable IP and actually do something productive.

JG

Switching to electric cars is exactly the kind of thinking that years of 2% cost of capital gives rise to. See how they all fare at 5 or 6%. Bargain basement clear out.

Still trying to internalize this. Putting aside cause/effect of rising margin / rising market cap, does including margin totals add anything that you wouldn’t see by looking at the chart of market cap alone? Seeming to me like the argument boils down to saying that the market has risen too quickly leading to intuitive sensing of a blow-off top forming (and given use of margin, likely leading to unruly unraveling).