Something has to give. And it’s going to be price.

By Wolf Richter for WOLF STREET.

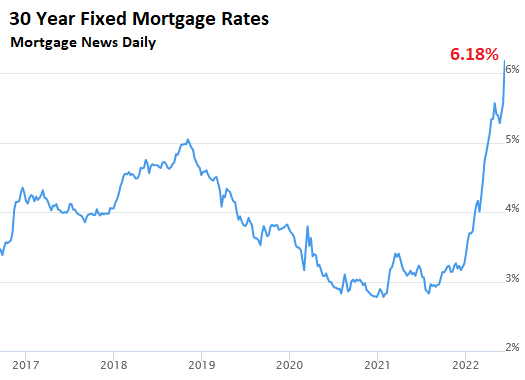

The average 30-year fixed mortgage rate today spiked to 6.18%, from 5.85% on Friday, according to the daily index by Mortgage News Daily. Aside from the sheer magnitude of the spike, this was also the highest mortgage rate since collection of the daily data began in April 2009. This was lightning fast, with mortgage rates nearly doubling since the beginning of the year (chart via Mortgage News Daily):

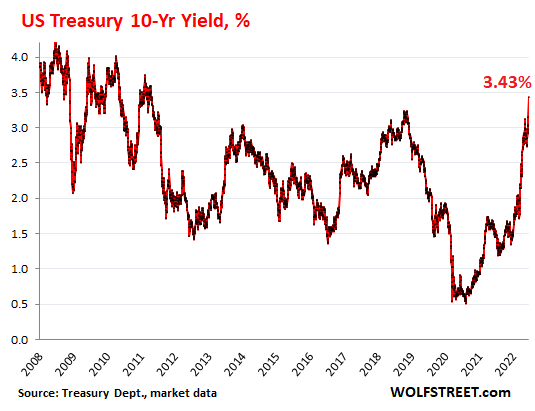

Mortgage rates follow the 10-year Treasury yield, but there is a spread between them, and the spread varies. The 10-year Treasury yield spiked by 28 basis points today, to 3.43% at the close, a huge move, and the highest since April 2011:

But wait…

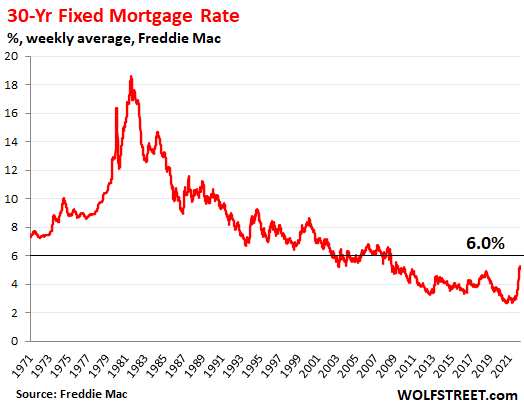

Back in the day, before QE and interest rate repression, 6% mortgages were considered low, I mean super-low, and I thought I got a great deal with my 15-year mortgage in 1989 at 8%! There are folks here that remember 15% mortgage rates. We didn’t even see 6% 30-year mortgages until 2002.

Freddie Mac’s data goes back to the early 1970s (though the June 9 release lags today’s daily measure by about a week). It shows just how fast mortgage rates have bounced off from record low levels, and how comparatively low they still are:

So let’s see. The Greenspan Fed ginned up the idea to cut interest rates following the dotcom bust to create a housing bubble in order to take over from the imploded stock market bubble. This worked, and we got a housing bubble, to which the Fed responded by raising interest rates again to over 5%, which worked and caused the housing bubble to implode, which triggered the mortgage crisis, which performed a rug-pull under the over-leveraged banks, upon which the Fed rolled out its new dual-weapon QE and 0% interest-rate policy, which worked, and it inflated all asset prices, bailed out the bondholders and stockholders of the banks, and soon it triggered the next housing bubble, but much more magnificent than anything before, etc. etc.

You know the drill. But this time, we got a new thingy: Raging consumer price inflation, like we haven’t seen in 40 years, and all bets are off. Raging inflation does a lot of long-term damage to the economy, to the currency, to businesses, and to the people, and it’s time to crack down.

Well, not really cracking down, just slowly raising short term policy rates from near 0% to still very low levels, and ending QE finally, and slowly starting QT.

So that’s not really a crackdown, but seeing how massively markets have reacted to this little bitty policy action shows just how overinflated all assets have become, thanks to 12 years of QE and interest rate repression – 12 years of Fed policy errors – and how hard it will be to unwind all this craziness back to some normalcy. But inflation is now raging, and all bets of a Fed put are off.

After 12 years of money printing and interest rate repression, home prices have ballooned to the point where higher mortgage rates have a very different impact than they had back in the day.

Each time mortgage rates rise just a little at current prices, they take a new layer of potential buyers out of the market. And transaction volume sags, and homes begin to sit on the market, and inventory is piling up. So it cannot happen here, they say, but it’s already happening, even in May before the current spike in mortgage rates, as inventories jumped in amid price reductions and sagging sales, because there is one way for sellers to nail down a deal: Cut the price enough to where the next buyers can afford the mortgage.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

House price destruction is well underway in Seattle area. Prices on average are down 20% from peak in March/April. Inventory inching towards pre pandemic level. Slowing sales. Amazon stock getting hammered sending even more buyers out of the market. Pre approvals down more than 50% in May compared to 2021. For buyers, popcorn sounds to be a great investment. It is not everyday they broadcast a housing crash live.

The FED blew the most massive housing bubble possible. It was beyond reckless and irresponsible – it was criminal. They have been putting people out on the street, literally. The explosion in homelessness is due entirely to the policies of the FED and .gov. Turning shelter into a speculative orgy is not only against the best interests of society as a whole, it’s totally immoral. The people at the FED are blinded by greed, and evil.

Amen

very well-said. Now we all have to face the painful consequences of fed policy error.

“Errors” happen, yet there is never accountability in our system for them. It’s the same as when Obama said we must look forward, rather than hold Bush responsible for the carnage in Iraq and Afghanistan.

And when it get big enough they will socialize the loss to the taxpayer.

Something going to break with all this debt destruction happening everywhere.

Buy insurance before you need it. I was early but I got a good rate.

I will still lose but that is the insurance game

Calling it an error is too charitable. They knew what they were doing. It doesn’t take a PhD and these people have them.

It is a good thing Canadas Government is so much better and very nice to their Slav…ups i mean Taxpayers.

Up in Canada we had policy error and the Chinese so our housing market took a double whammy and the Chinese provided a synergistic affect to the policy error taking our housing market to double that of America’s.

1/4 of Canadian mortgages are a variable rate.

Hold onto your hats.

The FED was founded by and for bankers. Bankers do not have the interests of society as a whole. It seems many people enjoyed the orgy of residential real estate speculation along with the bankers. Now we pay for that orgy.

It must be nice to be licensed to create money and direct it to whomever one wants. But if banks don’t do it, who will? Idiot uninformed/misinformed micro-consumers (thus no capital formation) or (other) oligarchs? Some manipulable AI bot?

It is like the court system: who decides? We face the loss of trust and with in, fragmentation that is very costly in its own way.

Obviously, the Federal Reserve is a CENTRAL BANK and it is most definitely not some sort of welfare agency or charity for the so-called ‘middle class’ and it enforces banking regulation and sound banking principles in the US.

EdH: bankers are simply humans and they will pursue their best interests. Just like the rest of us. So, rhetorically speaking, expecting bankers to have the best interests of society in mind is wishful thinking. The the root of the problems we face today is a function of a currency system that is NOT in the best interests of the general public. Fiat currency favors government and bankers. A gold standard favors the general public.

The Fed serves the the skimmers, not the producers.

If any country ever is going to get to where their Politically controlled Central Bank becomes the referee and not the player with the hardest elbows, then interest rates must be determined entirely by supply and demand not by edict.

Everyone on Wolf’s site knows this day was coming, but like Rome, this is not going to be over in a few days, weeks, or months. Price (and true value) will be determined and there will be blood.

So true. How about prosecuting these Fed guys for the massive counterfeiting they’ve done ?

They are criminals. They should be treated as such.

That you used “shelter” instead of the usual terms made your point unforgettable. I won’t think about real-estate matters from now on without remembering that, in the end, we all need shelter.

It’s not just the Fed. The implicit guarantees of housing GSEs, along with FHFA setting ever larger conforming loan limits, along with a plethoro of tax incentives for owning a home, including $500K capital gains exclusion, mortgage interest deduction, depreciation, etc. have pushed home prices to the moon. Take all those incentives away, and homes would become affordable to everyone in short order.

We need to ban HFs from buying real estate or make it prohibitively expensive for them to do so. Why is it ok for black rock to buy 1000 brand new homes in Houston directly from DR Horton thus bleeding what little supply we have?

“Sooner or later, everyone sits down to a banquet of consequences.”

—Robert Louis Stevenson.

Yup and as a reward for a job “well done”, Powell gets to keep his job for another 4 years! What a country!

There is no evidence of 20% price declines at this time. Please don’t post inaccurate info.

There is – according to my realtor. And you know that it is right when realtors give these type of numbers. Just to be clear – the comparison is between maximum sale price and current list price for similar houses (same community, floor plan etc). There are many redfin links that can support it.

An example. Both houses are pending. Exact same model in same community. May be some small differences. But a $420k reduction in less than a month. Newer houses are dropping faster than existing. Makes sense because builders have more inventory coming. And there are plenty more redfin links to support. Hope this provides some credibility to what I said.

1.68M

https://www.redfin.com/WA/Bothell/14-181st-St-SE-98012/unit-006/home/178744038?600390594=copy_variant&231528114=control&1778901559=variant&utm_source=ios_share&utm_medium=share&utm_nooverride=1&utm_content=link&utm_campaign=share_sheet

1.26M

https://www.redfin.com/WA/Bothell/2-180th-Pl-SE-98012/unit-36/home/178744039?600390594=copy_variant&231528114=control&1778901559=variant&utm_source=ios_share&utm_medium=share&utm_nooverride=1&utm_content=link&utm_campaign=share_sheet

Thanks for the link. The house with the $1.68M asking price might not have sold for that amount. It might have been the builder’s aspirational price, and the house could have sold for much less. It’s hard to say until the sale price is published.

In any case, it is evidence that builders might be reducing advertised asking prices to clear inventory.

Builders can move their prices quickly when they see a price crash coming. In Fall of 2007, I toured a house from a builder that was listed for $850k. After a week, he heard I was looking at other homes in a nearby neighborhood, and he voluntarily reduced the asking price to $600k. In a hot market, builders ask for moon. When they sense things are turning, they panic.

They need to keep inventory moving, or they can’t make payroll and the business falls apart.

The majority of the home price reductions should occur in the first year of the crash, even though housing may take several years to bottom, just like 2007/2008.

Hi Bobber,

True – what you said makes sense. However for me the key differences between 2008 and now are rates and inflation. During the bubble built up then, rates mostly remained steady at higher end 5%. And fed was easing during the crash and inflation wasn’t an issue. Today, rates have dramatically increased, fed is actively tightening with jumbo hikes and inflation is sky high. My estimate is that as tech stops drop and rates go up, the decline will be much faster compared to 2008. At any rate, if the economy does go to neutral, wherever house prices land can safely be regarded as fair values. I would rather wait 9 months and buy at fair value than today, whatever that is.

Ya, I’m seeing 15-20% reductions across the board on Zillow and Redfin in just a few months.

All the money came into Seattle from Vancouver when the Canadian government brought in 21 ways to kill housing back on April 20th 2017 budget day. Many were aimed at the Chinese so money moved into Seattle from Vancouver. The Chinese buy all the new homes. The price is irrelevant to them. Real estate is basically the only investment the Chinese make. They don’t put money into stocks so falling stock markets in America have no affect on the Chinese who buy into Seattle.

That is so funny. We live right next to this development. We were curious to find out how sales were going as DR Horton has 6-7 projects under construction in the immediate area. They just closed one of the 1.2 a

million asking price homes for 1.1million. they had 12 (!) Homes to sell me in just this one project. Back in 2017 when we bought our new build house nearby the same developer only sold 2 at a time and had a take it or leave it attitude with buyers. Many developments appear to have stopped construction. New home builders have flooded the market by adding dozens of projects during the crazy run up that take 18-24 months to come on line. Now they’re ready just in time for the busy!

I’ve been eyeing several markets sround the country for the last six months. I am still seeing no change or slight increases in every market I am looking at on realtor.com every community I am looking at is rural, but I would expect bigger drops there, since there is no local economic activity to speak of that could push up prices. Most are college towns, and since enrollment has drpped 15%+ in many of these communities, prices should be plummeting, but are not.

Wow, these house look like the Poorly built house they build in Florida but for 4 times the price, I feel bad forever has to settle for either of these houses. You would think they would have spent few thousand extra to make look fancier.

BTW, Redfin just announced they’re laying off 20% of their workforce.

These homes are ridiculously overpriced in any market but tech employee buyer heavy markets. But as tech stocks tumble, and the spigot on the stock options money prining machine is turned off, look out!

@JeffD — Enrollment may be dropping, but faculty(staff) numbers and salaries are at least stable and probably growing. That’s what has made some college towns we were looking at unaffordable.

Great examples — Cookeville, TN. $21K median income, but median home prices over $375K. Auburn Al, median income $22K, but median home prices over $440K. Just nuts.

Even if there were evidence of a 20% price decline from prior month, prices would still be up year-over-year :-]

True. I am not denying that prices are still way out of control. Even with this 20% decline,most houses in this area continue to be 50% or more overpriced compared to “normal” pre pandemic fair sale values. I just wanted to establish that downward trajectory has begun. This, by all means, continues to be one of the strongest seller’s market of all times.

Yes, but the fact that the drops have come so quickly are stunning.

DJReef,

The reason why the rate increases/price and volume declines are happening so fast, is because *many* mkt players know just how *phony* the prior economic environment was – an illusion created by DC at horrific cost.

Vast DC money printing was required to push interest rates down to historic lows, despite the US being an international trade cripple, with horrific accumulated debts – the very definition of a dangerous deadbeat posing horrible default risks (the kind of entity normally forced to pay huge interest rate *premiums*).

So the idiot buyers pushing home prices to historic highs (despite the nightmare economic fundamentals of the country) were speculating…and knew they were speculating (in the face of financial ruin).

They *always* had one hand on the ejection button, moronically confident of their ability to exit the deranged roller coaster before all the other dumb, arrogant thrill junkies.

That beginning process of hysteria among the financially “hopped up” is what you are witnessing now.

Here’s an anecdote for you. I know a guy that is a welder full time for big commercial builds in Boston area. He was working overtime for the past 18 months (mandatory) and they had a ton of “travel welders” hired at higher pay temporarily also to fill the demand needs. 2 weeks ago, they stopped all the travel contracts and his overtime is all gone. That is a very big business that has seen a very quick downturn in demand in a large urban area.

Maybe his buddies were into crypto and are now back to work, who knows. I doubt that is the main reason they now have adequate staffing.

SeattleTechie…have another cocktail and dream on…

Two links posted above. And 1.68M isn’t even the peak. These type of new houses have sold for 1.8M or more in surrounding area. Nothing astonishing really. Just plain economics at work.

Seattle Techie

I have to agree with you [a little]. It seems the market here has changed in the last couple of months. But a 20% drop for the whole local market might be a little pessimistic. The Eastside seems have leveled off, but that is a far cry from from a 20% drop. Right now there is still a double digit jump year over year, May 2021 – May 2022.

That will probably change by the end of the year. It has to, at the very least, level off as interest rates go up. Still a lot of people moving into the area and a lot of open jobs.

The homes beside and across the street from all the elementary schools must have soared in price far above anything else anywhere in Seattle. That’s a predominate trend in Canada with Chinese money. I told everyone back in 2017 what would happen to Seattle on ZeroHedge and to buy beside and across the street from all the elementary schools especially corner lots with the number 8 (the more 8’s the better in the address) and ever 4’s in the address.

OutWest, have 17 more cool aides and keep being in denial! Coeur d’Alene, ID median income $32k and median home price over $600k. Prior to us leaving due to this disgusting RE market, 80% of buyers were from the west coast paying quadruple for what homes cost 6-7 years prior.

Popcorn…you say popcorn? Your dead on! IT use to be under a buck, now a bag is 3-4 usd..up 400 %! The commodity everyone overlooked was telling you the real deal a long time ago!

I think I’ll go pop some..will only cost me around 20 cents .

It’s only the beginning, IMHO.

Keep it coming! The Fed created this entire mess, and supposedly they own 60% of all government backed mortgages.

So, let’s assume everyone is wrong, and we get another 2008 style housing crash and unemployment spikes to at least 9%.

What happens to the value of $2.7B in Fed MBS as a crap ton of houses go through foreclosure?

Like really? Can someone like Wolf speculate on what that looks like?

Oh, crap, I forgot! We’ll just have another round of rent & mortgage forbearance. Gotcha! Don’t worry, everyone, it’s all going to be fine.

When markets become unhinged, what we think of as the normal, Bell-curve shaped price/probability distribution flattens, implying “long tails,” which means much greater volatility, nearly any price is possible.

Hoping to see bitcoin price fall thru the floor into negative (like oil or nat gas). CNBC mentioned Musk invested $1.5 Billion of Tesla funds into bitcoin (think price was $55K or higher). El Salvador Presidente was averaging down with public funds.

Tesla bought somewhere in the $36k neighborhood. That means they are deeply in the red right now, though they did already sell some for a profit.

After reading my comment again, I must clarify. The trillionaire families exist and are responsible for avariciously sucking out the financial wealth of ALL Americans; that is the key point.

Even the Royal family of England owns part of the Bank of England and it and the City of London should be diligently investigated. See “The City of London Is Hiding the World’s Stolen Money” in the NY Times. ALL Americans and foreign holders of US dollars (of every ethnic, religious, and racial group) are being ripped off through the banksters’ ownership of the misleadingly named “Federal” Reserve. Some Americans are just stupid and enable them even as those parasitic banksters continually rip them off: e.g., through the creation of inflation by the parasitic banksters’ “Fed.”

Recognizing this is necessary to stop them, just as it is necessary to recognize that the Chinese Triads, Chinese CCP, Mexican Zetas, Japanese Yakuza, Italian Mafia, and other criminal groups are parasites that destroy the lives of others, even those they do not murder. Recognizing that the “Federal” Reserve’s ultrarich, parasitic, bankster owners, like the Chinese Triads or their CCP cronies or the Mexican Zetas, etc., are engaged in frauds or misconduct is not unfair prejudice or discrimination: see “U.S. banks handled trillions of dollars in “suspicious” transactions, report says” in cbsnews.

Who do you think launders the more than a hundred billion dollars earned just by sales of illegal drugs, not counting other organized crimes, Santa Claus? Who has the ability to launder over $150 billion dollars? See “Spending on illicit drugs in US nears $150 billion annually” in science daily.

I cannot ever disclose confidential information. Otherwise, I have my theories but no proof, which is probably why I am still alive. See “JPMorgan and Deutsche Bank Named in Money Laundering Report” in thestreet. See “Wells Fargo to Pay $7 Million Over Alleged Anti-Money-Laundering Glitches” in the WSJ. See “New UNODC campaign highlights transnational organized crime as a US$870 billion a year business” by UN office of drugs and crime.

SeattleTechie …I Absolutely Agree….My conversations with Amazon employees….They are very depressed as their income included their stock options.

The rental loans we did barely penciled out at 3% — Now 6.5% for a DSCR loan means NONE of them made sense, Either the Rate goes back to 3% or prices drop 30%. Seattle rentals never did cash flow, but at 6-7% – Game Over!. You can decide which comes next…

Seattle Guy

Given that Seattle is landlord hell and that it lost 3,000 rental properties and 10,000 rental units in the last couple of years -if my memory of the Seattle Times article is correct – I am not surprised that the rental market in Seattle is dropping. I wouldn’t buy a rental in Seattle even if the price dropped 75%.

I also never considered rental property in King County which is in a class rivaled by Florida mobile home courts in terms of onerous landlord responsibilities. But your comment drives me to follow this market through the upcoming bottom. I might be interested at a 75% discount from a contrarian point of view. Especially houses that will not finance, looking to sell them on mortgages after rectification. How exciting: crisis brings opportunity!

If Seattle RE dropped 75% I would guess that the surrounding areas would also drop, although not 75%.

So I would still look somewhere else.

If Amazon employees are depressed now, just wait until later. Stock still priced at nose bleed levels.

No, it’s cool, all you gotta do to cash flow in Seattle is put down 80% or more. No biggie

It’s interesting to see that even my CU which typically is just a tad lower on rates is today at 6.125% for 30yrs, on sat when I checked it was at 5.88%. Good job, keep these rates going up, if it helps with crashing the RE market by at least 40+% I am all for it.

What’s interesting to see is that Jumbo for 30 was quoted at 4.75%, I had to do a double take, usually Jumbo is about the same as regular 30, what’s more interesting is that this is even better than ARM which is at 4.85%. 30 yrs ARM, man you have to either be super desperate, brain damaged or totally believe in FED doing a super sharp U turn in rates in the next year or two to go for one especially with still sky high RE prices.

Same. My local CU is usually quite a bit lower than mortgagenewsdaily but it just crossed 6% today. Crazy fast increase.

What are your thoughts on Friday’s “no bid” on MBS? Will the Fed’s QT cause mortgage rates to hit double digits?

The ask was too high. Once the ask dropped enough, bids emerged. Makes perfect sense, at 8.6% inflation. Prices have to go down, and yields have to rise, and sellers don’t like that, so the asks are in the wrong place.

Need to study up on buying foreclosures.

Anyone knows a good source?

Top 1 percent selling stock ,shorting market ,stockpiles of cash then buy up housing 50 cents or less on the dollar .

That is distressing.

That’s capitalism. Concentration of wealth into fewer and fewer hands, market crashes, survivors buy up the remains. Rinse & Repeat.

Just get off the down escalator and get onto the up escalator.

I have close friends watching their portfolios get demolished because of the fear of generating a taxable gain. This is the first rule of stock market investing. Trade without regard to taxable consequences. Both President Obama and Senator Romney taught me (through the release of their tax returns) that if you do not have a IRS 501(c)(3) or equivalent, you are not taking advantage of the best method of tax avoidance which was created in 1913 (simultaneously with the Treasury Act of 1913:

The Revenue Act of 1913 imposed a one percent tax on incomes above $3,000, with a top tax rate of six percent on those earning more than $500,000 per year. Approximately three percent of the population was subject to the income tax.)

Of course, the oligarchs ( there were just over 6,000 millionaires in the US at the time) set their lawyers and lobbyists to work.

It only makes sense to save up and build a strong balance sheet while others are dancing carefree in the sunshine. That’s why the rich are rich, and vice versa. It is simply thinking over a different time horizon, discounting the future differently. (The ultimate discounting of the future, abandonment of the future, is deep drug addiction, or some flashy dangerous act.) A student of mine just weeks ago was praising “experiences” versus (what he saw as his elders’ foolish fixation on) “assets.” I said, sleeping on a sidewalk and eating dogfood is an “experience” too, and not all that improbable for many.

In a lot of markets, 50c on the dollar will hardly be cheap. That’s how inflated housing is now. Try (a lot) more.

At 50% off, a lot of those properties won’t be able to charge high enough rents to be cash flow positive either, because the economy and the labor market will be in the tank. That’s how inflated rents are now also.

Small Banks, they hate holding them because of maintenance and security risk. They only want to clear the paper. Go talk to your bank manager and cut him a deal for referrals.

Do banks even hold the paper anymore…

I thought they just originated, then sold…

In most all cases with conforming loans, that is correct but they often continue to service them for MBS holders.

“ Need to study up on buying foreclosures.

Anyone knows a good source?”

Back in the early teens, Fannie, Freddie, etc, had websites devoted to them…

Not sure about today… haven’t bothered looking…

“Anybody know a good source”

I hear Amazon sells books. (Go pull a few titles and we’ll give you feedback).

And there’s this thing called Google…

Not to be rude, but the world is *awash* in at least semi-useful info sources. Almost any book on foreclosures (except those with “Make a Million in a Day!”) is going to give you a basic grounding in the fundamental dynamics.

And reading a second or (gasp!) third book will give you more to think about, reflect upon, and question.

Ditto web pages/sites.

It is a process of continual self-education and there is no magical quick-fix shortcut.

That is the mentality of the losers who keep creating these financial disasters – destroying themselves and harming others in the process.

Keep your Eye on Wells Fargo and use a Broker who is very friendly with them

Meaning?

Yeah, I second that question. So, please do explain what you mean about problems (?) with Wells Fargo stock.

Wells Fargo has an internal REO (Real Estate Owned) that handles their foreclosures. But Wells Fargo also outsources many of their foreclosed properties to a third party contractor. We purchased a Wells Fargo foreclosure through a third party (we traced the loan back to Wells Fargo) in 2017. This house and 5 acre property was originally financed without careful review of the land survey and the legal driveway went right through the middle of a 1 acre stock pond. Our adjoining property with alternate driveway gave us significant advantage in the negotiations. I think Wells Fargo inherited this foreclosure from another finance company as part of the fiasco in 2008.

So I think what M C is saying is watch the Wells Fargo REO’s (they are listed on the internet) and have a good real estate broker who is friendly with Wells Fargo.

“I mean super-low, and I thought I got a great deal with my 15-year mortgage in 1989 at 8%! There are folks here that remember 15% mortgage rates. We didn’t even see 6% 30-year mortgages until 2002.”

Ditto but then again back then, you are not paying for a crapshack in Vernon for over $800K or in some cases in SF burned down house over $1.5M. Even adjusted back to nominal value at that time, the price is nowhere near as insane with interest rate back then at 8% or 15%

Right. Our first house same time and rate as Wolf: 1989, 8 1/8%, but the house only cost $120k. On Zillow today it’s $700k….for now.

similarly dogy:

first house actually bought in THE bay area was $40K with ”teen” mortgage with 20%+ down…

sold a couple years later for $105K, but we had done a fairly thorough ”rehab”…

same house now worth over $900K according to several sites claiming to represent such concepts…

while here in the ”saintly” part of the TPA bay area,,, some houses have gone up to well over triple just a couple years ago…

while IMHO, ALL RE mkts will go down,,,

”some” may bee many will just revert to long term ”mean” ,,,this time,,, LOCAL LOCAL LOCAL,,, eh?? LOL

while many will go below, maybe way below

RE IS and will always BEE LOCAL,,,

Plan accordingly IF you want to buy OR sell into this very very crazy situation for ALL mkts

The reason the burned out crap shack *reached* $1.5 million in the first place, is because DC insisted on driving mortgage rates to 2.6% earlier, creating a casino for momentum-only morons and dragging us all into their predictable nightmare.

My move to California in 1981 with the young family in tow resulted in a 18+% mortgage for a 2,000 sq ft. bungalow. Refied back to 10% in a couple of years and though I won the lottery.

There goes the Summer selling season.

and, much more importantly for SOME folks,,,

”there goes the summer SAILING season….

May all the various Great Spirits bless each and every one willing, able, and ready to go sailing,,,

People who OVERPAID for their NEW (or used) house can spend the summer sitting inside the unfurnished rooms with the A/C on and make believe they are at the park. A few PB&J sandwiches will add to the experience.

With temperatures over 100 in many parts of the US, parks are not the place to be.

In a normal market it is the sellers that are under pressure and the buyers have the advantage. Perhaps we will return to that sort of arrangement.

The price increases in everything are already exerting pressure on household budgets. People have to think about how much to budget for food, clothing and insurance going forward.

I would think that we are one or two rate increases from panic setting in.

Also with so much ever mounting stress over work, finances, kids in school, kids with mental illnesses…. Currently stress is at an all time high. Health problems can take you out of the home buying game as well due to medical costs or inability to work :( I sense people are feeling what I’m feeling, a bigger house is not worth health problems due to stress. Quality of life is more important.

After getting married and buying a house in a year, I sensed some kind of invisible line for my lifetime expansiveness in the 1990s (I was in my 30s). I started scaling back a little bit, getting everything I needed (stores, family, recreation, more digitized work-from-home) physically close. This triangulation paid off very nicely. It is important to “know thyself.” Some are more energetic and driven. I hit my wall with that.

Now everything is close and affordable.

IMHO, we will see the greatest demand destruction in several lifetimes.

As Wolf noted, it was a long time in the making. So the unwinding will be interesting. But somebody from Blackrock in a note Monday was already anticipating when the Fed, eventually, will capitulate. Or rather, substantially soften the rhetoric and guidance, which may signal a bottom. But that may take quite a while. The whirlwind has been unleashed. There will be very real wreckage.

What you describe may be the rationalization for a bear market rally lasting six months to a year.

If the interest rate cycle turned in 2020, rates will ultimately blow past the 1981 peak. The long-term fundamentals are absolutely awful.

The choice (if one is even available) will be that or crashing the USD and voluntarily ending the Empire.

My prediction remains that the public, economy, and markets will be thrown under the bus to preserve the Empire.

Suppose the Impossible happens, Uncle Jerome develops lung disease and stops blowing RE Bubble #2.

How quick do you think State Gov Sacred Cows will re-assess properties and REDUCE (Oh, the f… horror !!!) property taxes ?

Well, if the History is any guide –

“Taxpayers in Revolt – Tax Resistance during the Great Depression”

Scan of this book is in public domain at mises dot org

TOC:

1.Introduction

2.Tax Resistance: Origins and Development

3.Chicago: Portrait of a “Tax Racket,”

4.Taxpayers on Strike in Chicago

5.Breaking the Chicago Tax Strike

6.Selling the State: The National Pay Your Taxes Campaign

6.Selling the State through Radio: “You and Your Government,”

7.The Doldrums Set In: The Decline of the Tax Revolt

First step for workers:

File exemption from withholding.

IRS Form W-4

You can’t claim exempt on your W-4 if you can be claimed as a dependent by another taxpayer, you have more than $300 of UNearned income and your total “expected” income for the year exceeds $950.

This way, you get the use of your money for a year, instead of loaning to the government, tax free, you give them what you think you owe them and there’s no delays in getting your money.

To comply with the tax code, someone doing what you suggest will still have to file quarterly estimated income tax returns.

Don’t do that and if you owe above the cut-off permitted, you will get hit with and interest which won’t be at low rates anymore.

State governments know that people will leave if taxation is unreasonable. Why is there historic migration right now going on all over the US? It’s not merely people moving for political reasons. It is also to avoid taxation, which is why small government / red states are gaining in net migration right now.

Any state with high taxation regardless of political leaning will lose people.

EXACTLY CORRECT PG:

and some been doing same for many years as the ”net tax burden” has increased in SO many places in USA…

some on here have a very simplistic view/misunderstanding of their ”OVERALL” taxes in various locations, and continue to pay and pay and pay

others, clearly,,, have come to a clear understanding of their tax burdens and have moved ASAP,,,

time and enough for ALL jurisdictions to make ”RULE OF LAW” to ensure old and elderly have NO tax Increases at all from local jurisdictions so those old folks can continue to contribute to very much needed ”social stability”…

Lacking that, those areas without such ”tax stability” for elders will continue to experience folks,,, all who can IMO, leaving,,, and social stability continuing to be challenging…

Nebraska can’t get people to move here= ridiculous property,sales and vehicle taxes .stay away when real estate market corrects I’m done .My retirement won’t finance police and fire departments any longer .People talk about there dangerous jobs,worked in public works and utilities = way more dangerous

I didn’t realize it was bad in NE.

I’m surprised nobody from IL is moaning about their situation on this thread lol

IL is total taxation hell

A lot of people especially with similar political leanings to my own just cynically assume Powell & Co will pussy out on tightening. I understand why they think that and cautiously but increasingly disagree. Even in the years before the pandemic, I got the impression that there was an intellectual paradigm shift at the fed, they were getting real sheepish over QE and were happy to start selling it off.

Powell to his credit has acknowledged that he was wrong about inflation and must take responsibility for it. Axios contrasted this with the sniveling discourse from Arthur Burns who basically inflation on the whole world being against him. Should also note that Yellen has more or less admitted she was wrong about inflation. Point is, I think the people with the power are perceiving (correctly) that their credibility is on the line and their backs are against the wall. I think they are going to crank it.

Did Yellen submit her letter of resignation along with this admission?

“It is absurd to place important decision making into the hands of those who pay no price for being wrong.” T Sowell

Dishonest- would that resignation be tendered to Jill or Nantucket?

If the FED chickens out, inflation will eat everything, EVERYTHING!

They know that, but painted into a corner with the house on fire is not where anyone wants to be.

Two choices only and both are insanely bad.

Von Mises comes to mind

Don’t tell Dave Ramsey. He says this is the best time ever to buy a house prices will only continue to go up.

Cathie Woods is in the cheerleader line too. I am reminded of Voltaire’s satirical novel Candide, in which the character Pangloss, the eternal sunny optimist, keeps showing up and cheerleading even as disasters engulf him in increasingly ghastly ways. It is wickedly funny in a way befitting the moment. Might as well laugh.

“Wood”

Yes, Wood, not Woods, especially with equity price going down, and chop-chop.

It’s pretty stunning to see this all unfolding right before our eyes. When you think about how things have changed since just the beginning of 2022. Makes me wonder what will be at the beginning of 2023.

Further inflation, job losses then riots.

Bingo.

#1 & #2 correct.

#3 Never in America.

Dishonest, why, because we’re only capable of “mostly peaceful protests”, right? I think there’s a first time for everything.

Just for the fun it’s no doubt worth opening the jewelry box once a month for the next few years to bring out and dust off Janet’s little gem about no financial crisis in our lifetimes.

Was looking at Zillow today, and seeing some pretty substantial price reductions. It is about time for the RE brokers to get off their “sellers market” BS propaganda, and start telling sellers that their pool of buyers is shrinking by the day, and with every rate hike.

The problem is, many sellers are mortgaged to the hilt, and can’t lower their price much without going belly up. All adds up to some money making opportunity down the road about 3 or 4 years… At least for those who ignored the cash is trash nonsense….

As of this week, I’m seeing a lot of flips bought a few months ago just now being resold and priced well above comps (as much as 20%-30% higher). A flipper bought, then sat on the house longer than expected and paid more than expected for the remodel. Now they have to sell the house for their purchase price + overblown remodel price + taxes and other carrying costs just to break even. They won’t be able to unload at their asking price because even if they find a sucker to bite, a mortgage won’t be underwritten with an appraisal 20%+ below the sale price. Worse yet, they’re hitting the market as mortgage rates suddenly choke off middle class buyers. I’m even starting to see a few houses that are half-finished remodels. Some flippers are getting uncomfortable enough to bail mid-flip like rats on a sinking ship. From institutional operations on down to little independent RE speculators, the flippers are screwed and they know it. Now we get to watch them squirm.

We’ve read this book and seen the movie already. History actually repeats a lot more often than it rhymes.

I’m even starting to see a few houses that are half-finished remodels.

Some of these may be due to supply-chain problems with building materials. I know someone who waited a year for windows to be delivered – fortunately these were replacements for existing glass. But imagine months-long delays for a dozen different materials that need to be coordinated with each other timewise, putting you way behind schedule for resale as you watch mortgage rates shoot up for your potential buyers.

Great post!

Agree with price reductions and sellers mortgaged to the extreme. My realtor is one of the few who is actively discouraging buying now. And I know he is losing some significant business behind it. There are still plenty of realtors who are still preaching the “buy it if you can afford it” BS.

My buyer’s agent has been discouraging buying for a few months as well. At $5-6/gallon, probably not worth the gas for them to keep driving around looking at overpriced, rotting crap shacks they know we will inevitably pass on.

Which is why loan-to-value for refinancing/HELOC should be no higher than 75%.

75% isn’t a currently conservative loan given the extent of the mania, not in any market that has participated to any meaningful extent.

I’ve heard (don’t subscribe) that a Wall Street Journal article about the Fed possibly hiking rates at 0.75% this Wednesday is spooking Wall Street already. What would this do to already elevating real-estate rates? Shock and Awe?

Here’s Goldman’s Chief Economist after the report: “Revising Our Fed Forecast to Include 75bp Hikes in June and July Following a Hint in the Wall Street Journal”.

And here’s Evercore’s ISI Strategist (and former NY Fed Exec VP) Krishna Guhu: Client note headline: “WSJ Report Puts Us On Alert for Fed 75BP Hike This Week; We Think Mistake and Bad for Risk”.

Bad for Risk? Lookout below!

I know one thing: if they hike by only 50 basis points on Wed, without adding a huge threat of 75 or 100 bp for July, we’re going to get a huge rally because everyone is expecting/fearing some hugely hawkish twist.

Wolf, you have shown that interest on the debt as a percentage of GDP is historically low, but could you examine what that percentage might be if we have sub 2% GDP for 6-18 months, increasing rates, and increased borrowing by the govt to make up for declining tax receipts? I would think that might be a likely scenario going forward.

I would like for the interest burden to get so large due to higher interest rates that Congress will actually discuss how to deal with it, namely by tamping down on deficit spending and making the tax code fairer to where corporations, wealthy people (such as Buffett), etc. pay their share.

High interest expense (due to higher interest rates) enforces a borrowing discipline that has been lacking all across the economy (businesses, households, governments) due to interest-rate repression.

I think long term, taxpayers, the economy overall, and governance would benefit from the enforcement mechanism of much higher interest rates. Something like “tough love.” In a capitalist system, you need that form of enforced discipline. Or else it goes haywire.

One last hurrah!!! Or not.

IMO ….I think the markets would welcome some backbone from the Fed…ie .75.

Well I totally agree about the rally, but the question (on the Russell 2000) is it going to be off of 1700 or 1500? I am a tiny bit long URTY in the premarket Tuesday 6-14-2022. The rest in cash.

Happy Harry Houndstooth

RU2000 remains ridiculously overpriced. Dividend yield is a sub-basement 1.44% even with almost a 30% decline. I don’t know what the meaningless P/E ratio is now.

All of this was inevitable.

There’s no greater pleasure in life than seeing delusional people getting wiped out.

The sound of all the geniuses and HODLers getting flushed down the toilet is super sweet!!!

Go long Fentanyl !!! Demand will skyrocket!!!

It’s funny to me how Fentanyl is being discussed as Heroin used to be. When Fent was new, it seemed like a more extreme heroin, what people turned to when the Heroin wasn’t enough. Now it seems Fent is the bread and butter, and composite drugs are the new normal?

Vice News usually has a lot of interesting stories on the subject and the drug culture that exists in different hot spots around the world.

Maybe I’m wrong, but isn’t heroin derived from poppies, whereas fentanyl is strictly synthetic? Seems like the logistics of making fentanyl would be simpler, and thereby cheaper.

I can’t believe I’m discussing this.

U.S. Drug Overdose Deaths Top 100,000 for the First Time:

“The CDC said there were an estimated 107,622 drug overdose deaths in 2021, a 15% increase over the previous record of 93,655 set in 2020. Drug overdose deaths rose 30% from 2019 to 2020.”

Add to that “…42,915 people died on U.S. roadways in 2021, a 10.5% increase from 2020. The number of fatalities represents the most since 2005…”

That’s 150,537 deaths every year from drugs and cars. About a million less people every 7 years.

It doesn’t say much for the quality of life in the United States, but silver lining: the trend might help the Social Security and Medicare systems in the long run.

Agreed! But, it’s mostly young people (potential taxpayers) that are dying. That won’t help social security.

And who is gonna buy that house later? A generation’s wealth effect is relying on future buyers.

Whereas I think it not improbable that many USA youths will live in mass subsidized housing, eating mass subsidized soylent green.

Most of us old people know how to use drugs without OD’ing. Lots of practice over the years! And we are good drivers, too!

Hi Wolf, it seems that you do not think we will see QE again, at least for many years. Is that accurate of your beliefs ?

Yes, I think that there is a real possibility that CBs (not just the Fed) finally learned that you cannot print money without triggering all kinds of mayhem. You can do it for a little while maybe, and get away with it, but then suddenly something breaks that may take many years and lots of pain to fix. I think that there is a chance that this is now sinking in.

I have the same impression.

The odd one out is still the BOJ, who keeps capping their 10-yr at 0.25%, but this is crashing the yen and these guys need to import stuff too… It’s very interesting to watch.

The ECB has (at least in rhetoric) started to unwind, but spreads between core and periphery are starting to blow out again. Lagarde tried to do a Draghi-like “whatever it takes” statement, but it is not credible in the light of rampant inflation. Also, she doesn’t have the gravitas that Draghi had.

We may see the beginning of the end of the euro. Italy has massive and growing debts and hasn’t seen GDP growth for the best part of two decades. Demographics is terrible.

I would bet on the Italian government starting to pay with IOUs some time within the next few years, effectively creating a parallel currency (without calling it one). That would be the end of the euro as we know it, though it would survive as a unit of accounting.

People arguing that central banks won’t raise rates much because governments won’t be able to afford the interest rates got it wrong, imo. Rampant inflation causes economic carnage and that will eventually also end in default. So there really isn’t much of a choice.

You cannot “inflate away” debt with high inflation and high deficits. The reason that Japan has got away with such massive debt for so long is, imo, because they had very LOW inflation. That may be coming apart now.

YuShan, brilliant summation. This is a good platform from which to think of other sequelae (medical term for “sh!t that follows”).

Interestingly, the BOJ’s Kuroda has come under heavy fire at home, especially his remarks that even higher inflation in Japan (it’s soaring in some of the most important items people buy) would be a good thing. It was a completely tone-deaf thing to say, and it riled people up, and people might not have known who he was or paid attention, but now they do. He is becoming the most hated man in Japan. And his term ends next April. Seems, he cannot now suddenly back off his philosophy, he has to save face, but the new person in charge next year may chart a different strategy.

1) Rampant inflation in Turkey, not in US and Japan.

2) In real terms, US gov debt deflated since 2008. US gov cut payroll, Capex, unemployment benefit, food stamps…

3) Us gov collect more taxes.

4) This moderate inflation benefit gov, not people, especially poor people, or poor countries gov.

5) Unaffordable diesel crush the farmers

“(it’s soaring in some of the most important items people buy)”

Is that right?

Define “soaring”

And please give some real examples, we’d all like to know.

JapanMan,

https://wolfstreet.com/2022/05/20/inflation-comes-to-japan-amid-plunging-yen-and-inflation-subsidies-bank-of-japan-blows-it-off-as-transitory-throws-yen-under-bus/

So, in 2 months, when the share market has halved, and real estate is catering, you don’t see QE?

I’d put everything I have on it. The panic will be unbelievable. Governments freeaking, jobs evaporating, media whipping up a storm… they will print (to late).

Raise rates and print together.

MMT all the way.

They will print till a debt jubilee is the only answer.

We cannot go back to the old ways, because infinite growth is physically impossible. The entire fractional reserve banking is based on infinite growth. Antiquated capitalist ideas and institutions will have to go, to make way for a sustainable future. It won’t be pretty but there’s light at the end.

Would like to hear from Wolf on this too.

Personally I think it’s hard to imagine there won’t be at least some subset of policymakers getting cold feet about overly-generous ZIRP & QE the next time around. But there are a few things:

1) There are some central bankers who believe Congress was primarily responsible for igniting this fire, pointing to the previous decade of QE that didn’t lead to runaway inflation.

2) FOMC membership is constantly changing, with most spinning through the revolving door, after a few years of “public service,” to be greeted with multimillion dollar paydays doing “consulting” for Wall Street. It’ll depend on who’s in charge by then.

Jackson Y-

Regarding your Point 1) Who could view Congress as NOT responsible for the fire, when the Federal Reserve System was created and mandated BY CONGRESS and overseen BY CONGRESS? (For further similar evidence of unintended consequences of central banking policies one could examine the 1920’s, 1960’s and the housing binge earlier this century.)

Your Point 2) is astute, and important. It’s a potent argument for smaller government across the board.

The “public servants” and “consultants” are already in a panic. When the U.S. domestic economy no longer generates enough surplus to fund the state then the parasitic elite will have to scramble for bread crumbs and the infighting will begin.

Nice to have an article for a change where none of the graphs had WTF on them.

A house in our town bought in 2015 for 500k listed last month for 900k. No offers, and they pulled it off the market last week.

Another one was flipped and they’re asking 800, pd 500. No offers after 3 hours, so then they held a splashy open house. A few days later they are desperate, time to actually put a for sale sign up. Still nothing.

It’s too late, sorry. The tide has gone out. Start cutting your prices kids. Only question is how low will you have to go. Panic starts shortly.

Went from WTF to FTW (For The Win) for us looking forward to this and didn’t buy into this mania.

You know what is interesting. The new home buyer sort of ends paying the same monthly amount when interest rates rise and house prices drop. As interest rates rise and the price of the house drops, the mortgage payment may actually stay the same. This combination really does not help with affordability. I am thinking rental prices may also stay high?

Example. Take out a $500k loan at 3% and the house payment is $2100ish a month

Interest rates go up to 6.18%. Now a $2100 monthly payment will only afford a $375k house. If the house only drops to $420, the new home buyer comes out a loser? If the house drops to $375k, the new buyer pays the same monthly payment as when the house was listed for $500k.

I guess property tax and insurance will be a little cheaper so mauby we could bump of the equivalent home value to $390k.

Summary: new home may benefit from a drop in home prices if the mortgage rates are skiing. Cash buyers will though.

Thus, if home prices drop….It will be good to be a cash buyer.

So in theory if the above scenario happens where mortgage rates are at 6% or higher, house prices will drop, monthly loan payments will stay same, but equivalent rents should stay the same.

So this could actually be a better environment for the wall street investors as they can need less cash for a home but bet to keep the same rent?

Just thinking out loud but does this scenario make sense?

If you’re a buyer , you would be better off buying higher interest and lower home price. It is only a matter of time before you will refi. You can’t change your purchase price when you buy high.

No. For the same monthly payments a higher mortgage rate is much better. Firstly, when rates are above historic averages they have more chance of going down than up. Right now we have the opposite and sure enough they are now going up. Second, for every dollar of principle you pay down you get compounded returns at your mortgage’s interest rate.

Try a compounding calculator at 7% and in 20 years you’re doing well. Repeat at 1% and you’ll have to live to 100 before you get past the knee of the exponential curve.

There are a couple problems with this scenario. First, lower rates means that properties, as investments, are more attractive to investors, even when you take price into account. So you have more people competing for the same houses.

Second, to the extent that mortgage interest is deductible, a homeowner is better off having a higher percentage of the mortgage payment be interest (even if the total payment is the same).

Third, if a person with a mortgage decides he wants to pay it off early with higher income, savings, or what not, it’s better to have paid a lower purchase price.

Fourth, you get a free $250k in capital gains ($500k if you’re married). So you’re less likely to exceed that cap and owe money when you sell if prices are more reasonable to begin with. In other words, at the same percentage, if you buy for $500 and sell for $750, you don’t owe taxes. If you buy for $900 and sell for $1.35, you do.

There are probably other things I’m missing.

Higher prices and lower interest rates are better if you plan to rent it out and can get close to covering the nut…

Due to IRS basis for depreciation…

Property tax. It’s lower when the price is lower.

Higher interest rates and lower prices are a much better scenario.

$500K at 3% and $350K at 6% have roughly the same payment. But if you have a down payment of $100K on both your payment on the $500/3% goes from $2100 to $1690. If you have a $100K down payment on $350/6% your payment goes from $2100 to $1500.

Higher interest rates and lower prices reward savers. Higher interest rates and lower prices also encourage pre-paying your mortgage to get out of debt. You may have to save more and put off your purchase, but if you do then you will save money.

Higher interest rates reward saving and delayed gratification. Higher interest rates lengthen your time horizon by putting more value on future money.

Rents should not stay high, near current levels.

The economy and employment are entirely dependent upon artificially low rates. The fundamentals suck.

Where do you expect anywhere near as many renters to have the money to pay anywhere near current rents?

It is absolutely amazing how fast the real estate market evaporates after the top of a bubble.

I paid for my education learning this fact.

Bargains ahead, but have the patience to allow the knife to fall, hit the ground and vibrate.

It is all about what you put your faith in. Some people choose to believe that trends and easy money can continue forever. That this time is different.

Some people put their faith in the laws of economics and physics which dictate for every action there is a equal an opposite reaction.

Reality does not care what you believe, it is going to follow the same laws it has always followed, and the cycles will play out the same way they always have. This cycle has been extreme in one direction for many years, you can expect the correction to be equally extreme.

A house in my hood that sold for 130k in 2010 then sold for 1.3 million in 2017, is now for sale at 3.25 million. Where can I buy now that I will be able to sell for 10 times the price in 7 years?

@Joe, lol what??? Where is this? So Cal? Bay Area? Even in this stupid market this is the dumbest thing I’ve ever heard

Mortgages below 3%: Oh my god, we’ve never seen such short supply. This is the greatest housing shortage in history. Buy now of forever be priced out!

Mortgages above 6%: We won’t be able to walk 5 feet without tripping over a “For Sale” sign. Magically, a glut of houses will appear. Biggest housing oversupply since 2008/2009.

Funny how that works.

So true!!!

In Canada, fixed rate mortgages have to be refinanced after no more than 5 years at prevailing interest rates. There will be a lot of economic pain north of the US border.

Probably around half the Canadian market is in a 5 year fixed term, then around 30-35% in variable rate (rate changes every time bank of canada rate changes), and the remainder in fixed terms of less than 5 years (1-3 years mostly).

So, like you said, but worse.

Meanwhile realtor.com has a fresh email in my spam folder about how nobody could have seen this curveball that flipped the housing paradigm.

As above, so below.

I’m sure Zillow will come out in a week or two saying only 10% price growth. Down from 15% which is down from 20% which was down from 30%.

Never trust info from a conflict of interest. The only thing that remains to be seen is if wall street and corporate America take over private housing in this bust once a bottom is met.

This all day and all night! I don’t understand why news continue to quote Zillow, etc as of they’re trusted sources. They’re the definition of conflict of interest.

The math for corporate America will be completely different when prices are falling, rates are rising, and rental vacancies are much higher.

At some point, I expect a lot of corporate selling. Corporations have no attachment like homeowners and will bail as soon as they conclude ROI targets can’t be met.

All over again, but this time we are in a much worse situation all around.

Bubbles are bigger.

This downturn in stocks an cryptos has been pretty fast. Not much of any bear market bounces.

I have to wonder how much leveraging was done in the crypto space. There are a lot of defi companies out there that allowed the BTC hodls to hold and borrow against their cryptos. Some were up to 80% LTV.

Can you imagine having 500k in crypto and borrowing 80% against it to buy a $400k home with cash. Now that crypto dropped 50% and it is only worth $250k. The defi company calls you up and says the new LTV is $200k. So they want you to pay back $200k of the loan to get to 80% LTV

In BTC crazy blast off the past 2 years, I read that only 10% of the float was ever traded. That mean most BTC are hodls and probably borrowed against their BTC to buy other cryptos or assets.

In theory a smart move because you would not have to pay capital gains when you sold the crypto.

In the example above to come up with $400k, the crypto owner would have had to sell the entire $500k and probably pay 100k in capital gains. By borrowing $400k against the $500k, he still had all $500k that could appreciate.

So how many rich crypto owners borrowed against their crypto assets?

Just google all the companies that would allow you to borrow against your crypto for even business or personal loans. I guess they never thought the mainstream BTC and ETH crytpos would crash 50% to 60%?

I didn’t know you could borrow real cash( that has to be paid back) off fake digital cash, I guess they were too greedy to take profits. I wonder how much of the economy is actually borrowed against rising assets.(assets, of course, that will never fall) I’m sure Mr Wolf has done a chart on it but there goes my memory….

There’s more money in ruining people than helping them.

Mark Moss, a bitcoin guru with a podcast borrowed against his crypto to buy a ranch in Texas without seeing it in person first. There’s a video on YouTube from him about it.

Crypto exposure and leverage in all these obscure structures may turn out to be one of these previously overlooked/ underestimated things that later turn out to be significant contributors to a downturn.

Total crypto market cap was $3T at the peak in November and is now $1T. It may not be relevant (this “wealth” came out of nothing and then disappeared), but when people start borrowing money to buy it, or using it as collateral for loans, these $2T that suddenly disappeared may matter in the end.

It is an unregulated space, so who knows what hidden risks to the larger financial system suddenly materialize?

Indeed, For the “high rollers” who got caught in their Crypto mania……sometimes you must sell the “good stuff” to pay for the “bad ideas”.

You have to hope that this isn’t true….Can you imagine the mess for all economies if BTC went to say $5000

Who cares? With all those broke gazillionaires the current shelf price of “fava beans and a nice Chianti” might drop overnight. Got barbeque sauce?

Paraphrasing Andrew Mellon (as said to President Hoover in the early 30s):

Deplatform the influencers, deplatform the exchanges, deplatform the sh!tcoins ….

Who cares…you are part of the economy

How would that it in way be a ‘mess’ when it is worthless and that was known all along by anyone with a fraction of a brain?

Ask Jim Cramer invested in etherium ,Sold his position,bought a farm ,then brags about it on tv

quite possible the opposite could happen and could just witness an RE super-cycle as people throw anything and everything at real storages of value.

“…real storages of value.”

When prices begin to decline, that theory goes out the window even as a theory.

A theory is supported by evidence, and accounts for the facts. Real estate as a ‘store of value’ is a marketing deception. But it has never been more than an element in theories of valuation, and fails as a theory itself because it disregards the fact that the value of assets can be variously inflated, impaired, or zeroed out – something that actual theories of valuation account for.

So it was never really a theory. In the American vernacular, “theory” often means “imperfect fact”—part of a hierarchy of confidence running downhill from fact to theory to hypothesis to guess, but that is the kind of muddy thinking that deceptive marketing likes to encourage.

Speaking of theory and facts:

“If the facts don’t fit the theory, change the facts”.

– Albert Einstein

Yes, but at the end of the day, there is an asset one can shelter in, or farm, etc. All these intangibles, on the other hand, evaporate into nothing when a liquidity crunch hits. How about an uber ride down the block for $50? Versus my home loan monthly locked in at at $373?

Worldwide I am seeing all players grasp their tangibles tightly and warily look for prices. Putin takes it furthest with a grab for land and grain. With enough liquidity, one can hold out for value in trade.

The problem with real estate is that it is not a productive asset (unless you look at it in terms of the rental cash flow value). Unlike a company, it simply does not make anything.

Since the year 2000, real estate has appreciated at least 5% a year on average. Real estate may not be a produtive asset, but it is historically one of the best investments a person can make.

Rental real estate is a more viable business than a noticeable proportion of publicly traded stocks. It’s the price, carrying costs, and income stream that determine the outcome.

It’s an actual investment, as opposed to the home anyone lives in which is a combination of consumption and speculation.

History is bunk

This time it is different

Stock markets only go up

House prices can’t fall due demand from all the new immigrants

We will never have food shortages

Recession. What recession?

Electricity is always reliable

i deserve to go on holiday six weeks a year

Peter Schiff is a stopped clock

could go on forever but forgot to include

We Germans are proud to rely on Russia for our energy…(ha ha ha)

and, the Eurozone is the answer to our 20th century problems. And in connection with that, we call all vote ourselves “free” benefits, and it will create a virtual cycle, a perpetual motion machine, that will lift all boats, levitate us all. And, the recipients of those benefits will not be greedy. They will contribute value commensurate to what they receive.

Which is to say, the laws of gravity and entropy can be suspended.

Russia has always remained an absolutely reliable supplier.

We will always have unlimited gasoline

I was wondering if foreign buyers would help soften the landing of an ongoing real estate bubble pop. Or, one might say, the camel’s back sagging down slowly after the last straw causes a stress fracture in its spine, and perhaps finally snapping.

But the total property sales to foreign buyers peaked at 153 billion U.S. dollars in 2017. And by 2021, it had decreased to 54.4 billion (lowest in the last 12 years).

The Chinese buyers have been slacking off:

“Historically, Chinese nationals bought between 20,000 and 40,000 residential properties annually…Since 2011, Chinese buyers were responsible for up to 16 percent of all sales to foreigners, but in 2021, the share of Chinese property buyers was as low as six percent.”

In 2021, Canadian and Mexican buyers bought the most U.S. residential property, although Chinese buyers still accounted for the largest share when looking at the value of transactions. So it’s somewhat comforting to me that many of those high-end Chinese buyers of U.S. residential properties will end up holding the greatly diminished investment bag.

Mainland Chinese people aren’t allowed to go anywhere outside China unless they can provide a VERY GOOD REASON to do so.

Since that’s the case, there’s no reason to buy properties outside China. The people still buying are probably people carrying dirty money in which case it serves them right to lose all that money. But then again they probably don’t care since it wasn’t their money in the first place.

It has happened before, big waves of hot foreigner money into US real estate ends in bust – although if they hung on long term they’d have done OK.

Iranians and Saudis bought up chunks of Beverly Hills in the 70s as oil caused their economies to boom, then it slumped for years. Japanese piled into Hawaiian residential in the late 80s as their economy soared, to watch it deflate in the 90s.

Many of those high end Chinese buyers, especially in Canada, were engaged in money laundering.

Perhaps the shutdowns and the downturn in the Chinese economy tempered the need to, and the ability to move money.

1) When the dollar fell to 71 in 2008 foreign investors could acquire a lot of dollars and buy RE bargains in SF, Vancouver, NYC…

2) Today the dollar is expensive, up 50%.

3) It’s hard to buy dollars and CA, BC, TX expensive properties.

4) Most of the global RE market is booming. Houses are beyond reach for young couples. Rent is high, but in dollar terms the global RE deflated : 33% – 50%.

5) What matter is the rising dollar. RE is global, not local.

6) The first boom was created by foreign buyers, the next thrust was

caused by the virus.

Foreign buyers are no different than domestic buyers, they are not eager to catch a falling knife. In addition, you are going to see lenders tightening their standards considerably.

The last time I did any speculative purchasing was 2012. The loan officer at the bank was telling me that they were having real problems writing loans at that time because of the strict standards. It reduced the pool of people who qualified.

This economic collapse is going to be world wide, not just in the US. China already has a huge RE problem.

No, it’s a global mania and so will the bust.

“So it’s somewhat comforting to me that many of those high-end Chinese buyers of U.S. residential properties will end up holding the greatly diminished investment bag.”

From what our teams seeing unfortunately this is highly unlikely (even though agree it’d be richly deserved at least in some cases, a lot of that Chinese cash has been from money laundering esp up in Seattle and Vancouver). Instead the Chinese have been if anything like the big-name investors like Nadella, getting advance notice of a valuation fall and bailing out early to leave Americans–whatever the real estate equivalent of a retail investor is–holding the bag. There was apparently start of a massive exit of Chinese investors from US, Canadian and Australian housing kicking off around mid 2020, accelerating by spring 2021 (maybe behind a lot of what you saw) and then surging by February 2022.

Ironically the rough treatment of the Russian property owners overseas after Putin started his epic blunder in Ukraine likely helped the Chinese here, they saw the way the oligarchs had their property and wealth seized so aggressively and worried there might be pretext to go after them next. So they accelerated their asset repatriation and in essence based on hindsight, sold off their properties at their peak and brought the proceeds back to China. Untold billions of dollars. The timing of those events was perfect for them and prompted them to bail out early. And now with all kinds of capital controls in China on top of the looming asset bubble pop, they’re not going back in.

If there is a silver-lining, it looks like at least some of the biggest RE bag-holders won’t be small fry, but big corps like BlackRock and Blackstone that were buying up single-family homes to rent to Americans at inflated prices. They apparently purchased a lot of the homes esp on West Coast the Chinese were selling off. IMHO they’re even worse than the Chinese money-launderer buyers because of the way some of them have been swooping in and pricing out local homebuyers, only to drain away their savings with way too high rent like a financial vampire. It’ll be nice to see them getting crushed with the upcoming RE correction.

We saw the pullback from asian money in SoCal apartment and hospitality building in 2017.

Several very nice projects suddenly canceled just before contract signing, and were told it was because of some situation happening in China.

Seems to be quite a bit of schadenfreude on here today…..

Well earned. Only matching the very loud arrogance and hubris of the boosters in hot times.

Darn right. These people contributed to the obscene excesses we’ve seen in the past few years. I love watching them get their comeuppance.

Anthony,

What do you expect? Prudent investors and savers here got ridiculed for years, on top of getting financially crushed and screwed by interest rate repression. Now the tables have turned, they’re making a little bit of money, finally, and the people that ridiculed them are giving up some of their gains and maybe learning a lesson about ridiculing people for making different decisions about risks.

There are people here who’ve been priced out of everything due to the Fed’s asset price inflation. And now that it has ended, they’re maybe seeing a little bit of hope for less inequality.

Thank You

Thank you for saying this Wolf, this is exactly how we’ve been feeling. We’ve been doing all the right things based on sound financial planning, patience and prudence over centuries of experience and economic common sense. Being frugal, patient and avoiding asset bubbles. And we’ve paid a terrible price for our prudence, as the Fed’s arrogant and short-sighted policy, and manipulation of the free market rewarded the profligate, the greedy, the ignorant and just plain stupid while our savings shriveled due to inflation. Now the chickens are coming home to roost.

@Miller, I’m with you 100%. Nothing less than blood in the streets will suffice. I was disgusted at how soon people forgot about the last RE crash and went back to their old ways… on steroids.

As one of the prudent investors you reference , I’m impatiently waiting for CD interest rates to increase. What’s with that?

“…impatiently waiting.” Sheesh. Shop around. Banks are now marketing CDs through brokers (“Brokered CDs”) and those rates have JUMPED.

10-18 months brokered CDs now offer close to 3%.

Your own bank is going to rip you off and pay you nothing because it knows you’re just “…impatiently waiting.” Yank some of your money out and put it into a brokered CD that pays you something.

If you can’t sell it, rent it out and move on. The extra income will help you qualify for another home right? At the very least, property tax will go down. Currently my tax bill is more than my mortgage. Also, some neighborhoods will get it worse than others. I’m thinking now is the time to pick up a 2nd job at a fancy restaurant that wont run out of food or tipping customers.

The tax bill on my modest ocean front camp on the eastern shore of Nova Scotia is less than the phone bill…

@scared millennial, Sorry to break it to you but restaurants will get hit SO hard as it is as discretionary an expense as it gets (yes even the fancy ones) that’ll be one of the first things even the well-to-do will cut. Also bro, how in the F is your tax bill more than your MTG?

I retired long ago, back in 2009, I have been successful retiring just buying 3% to 3.75% GICs in Canada here. I lived off my severance and EI, unemployment benefits for 4 years, came in average $25,000 a year. I then started receiving by applying for my early CPP at 60, $650 a month then and just using 40% of my net interest income which is $20,000 then but $24,000 a year now. The bottom line is I am saving $37,000 a year from total income, CPP, OAS, interest income and I am debt free since I retired back in 2009 and I am still debt free. The only real estate I care about and own is my modest house and for me it is an asset I can sell later but is not an investment to become rich from. It is a place to live.

For grins and giggles I’ve got one of those “Comprehensive Mortgage Payment Tables”. It doesn’t even start unit 7%, goes to 18%. I show it to the kiddies who are only now just starting to “see”. Still have a ways to go I’d venture.

Let me guess. You also have a finance textbook which explains the inverse price-return relationship of bonds by positing a typical coupon of 8 or 10 percent.

I have one which explains compound interest with an example suggesting that the interest rate on a savings account is greater than the rate of inflation.

The world has changed in ways which did not require my prior approval.

“ The world has changed in ways which did not require my prior approval.”

Damn…

Are you still mad about that…

I thought you’d be over it by now… :)

The ghosts of past financial debacles haunt my restless sleep.

Just kidding. Don’t worry about me. When the ground falls out and Mister Market has to reach up to touch bottom, I’ll be just fine, really.

“So let’s see. The Greenspan Fed ginned up the idea to cut interest rates . . . (several salient points) . . . and soon it triggered the next housing bubble, but much more magnificent than anything before, etc. etc.”

An excellent Brief History of Recent Fed Malfeasance, which would be even finer parsed out into a timeline, with additional details, or extended into a longer timeline.

Observers since Jefferson have noted that Big Finance, aka the Financial Industrial Complex, has engineered and exploited booms and busts throughout US history to generate profits for its membership. The modern Fed has continued that tradition, but it was industrialized in the 19th century.

There are dozens of such observations, and they never go out of style:

“When you realize that the entire system is very easily controlled, one way or another, by a few powerful men at the top, you will not have to be told how periods of inflation and depression originate.”

– James A. Garfield

“This is well known among our principle men now engaged in forming an imperialism of capitalism to govern the world.”

– J. P. Morgan

“The powers of financial capitalism had another far-reaching aim, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole.”

– Carroll Quigley

Binge-watching “American Greed” on CNBC gets to be a bit much some times, but they never really mention the Financial Industrial Complex, probably because they don’t want to piss off TPTB.