In short, the party ran out of bamboozle.

By Wolf Richter for WOLF STREET.

Here’s the problem with companies whose hype-and hoopla stocks have collapsed by 80% or 90%: They’re facing an existential crisis. They cannot raise more money. But their operations were never designed to make money in the first place. Their business model relied on burning cash, and the whole thing was designed from get-go to use home-made growth metrics to bamboozle investors into buying the stock and pump up the shares. Then the companies, based on their high share price, could issue more shares and raise more money, and feed their cash-burn machine. The plan was to fake it until they could make it.

But with their shares down 80% or 90%, they cannot fake it any longer, and they cannot sell more shares because no one wants them, and they’re going to run out of cash and won’t be able to cover their expenses, and then they cease to exist, and their shares will go to zero, unless they can get the cash-outflows under control, which means cost-cutting. And the fastest and most significant places to cut cost is staff and advertising.

If they cannot cut their costs enough, and cannot get their expenses to be less than their revenues, they’ll eventually run out of money. And then that’s it.

But if they can cut costs enough, and cut their staff and advertising and other things enough, so that costs come in line, their revenues may sag, or sag even more, and then they may be reporting declining revenues, or more rapidly declining revenues, and continued losses because revenues are now declining faster than expenses, and the whole thing turns into a classic mess.

There are hundreds of companies in this position that went public during the hype-and-hoopla era of money printing and interest rate repression, and they’re all fundamentally facing the same existential crisis, though each company has unique challenges, and in addition, all have to face their industry challenges.

Just to stay within one industry: Today two companies in “real estate tech” with collapsed hype-and-hoopla stocks announced job cuts: Compass and Redfin. Two others had massive layoffs earlier. Zillow, which is also in real estate tech, has been laying off people since last year, when it exited its home-flipping fiasco, with layoffs occurring through at least April this year. Unrepentant home flipper Opendoor went through a bunch of layoffs in 2020, but has not recently announced any new layoffs.

They all have one thing in common: They lost lots of money every year of their existence as a publicly traded company.

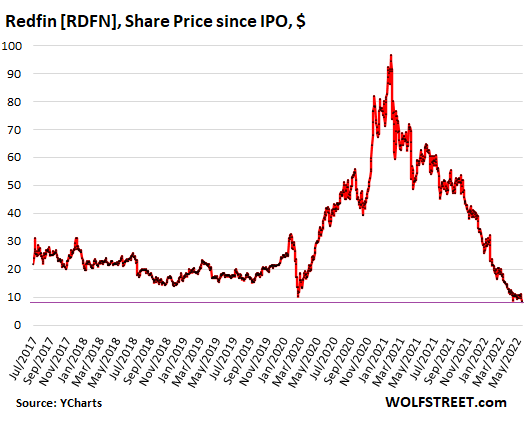

Redfin, the “Amazon of real estate,” as CEO Glenn Kelman called it as part of the bamboozle before the IPO in 2017, announced today that it would lay off 8% of its staff “today” because “It’s time to make money.”

“We’re losing many good people today, but in order for the rest to want to stay, we have to increase Redfin’s value. And to increase our value, we have to make money,” it said.

Apparently, there had been some kind of come-to-Jesus meeting at the top, with “May demand 17% below expectations,” and “not enough work for our agents and support staff,” and the decline in revenues means “less money for headquarters projects.” Yup, the holy-moly mortgage rates that just went over 6%.

Redfin has been a publicly traded company since July 2017, and has existed for 13 years before then as a startup, and it’s just now time to think about how to make money?

Good grief. I mean, Oopsiespalooza. I mean, WTF. This is the definition of what’s wrong with the entire hype-and-hoopla startup scene.

On the news, shares of Redfin [RDFN] fell to a new closing low of $8.13. Back when it was still the Amazon of Real Estate, in 2017, it went public at the IPO price of $15. Shares briefly spiked to $30 then got stuck at around $20 for years.

But during the pandemic, the stock encountered the miracles of the stock jockeys that plowed their stimmies into whatever, the meme-stock chasers, and the hedge funds that followed them, and they all had a hoot and catapulted the shares to $98.44 in February 2021, yes, that infamous February 2021, after which the bamboozle ran out, and everyone began ever so slowly to sober up, and everything came unglued. Since then, Redin’s shares have collapsed 92%:

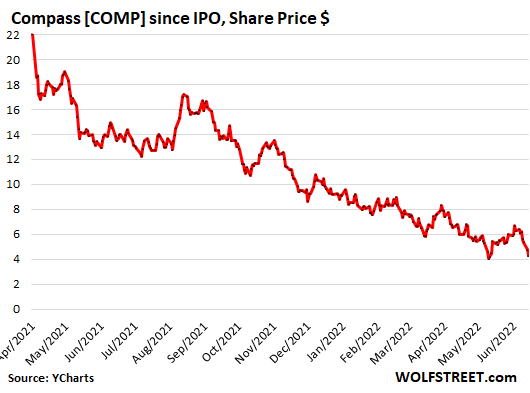

Compass announced today – after they too apparently had a come-to-Jesus meeting at the top – the “elimination” of 10% of its staff, about 450 folks. It said it would shut down its title and escrow software company, Modus Technologies, which it had bought in 2020, get out of some office leases, and halt further acquisitions, “to drive toward profitability and positive free cash flow.”

The real estate brokerage was backed by SoftBank and had raised $1.5 billion before the IPO, which it then spent, plus the money it raised in the IPO, on buying up real estate brokerages and on hiring brokers away from other brokerages.

So, now it wants to cost-cut its way to positive cash-flow and profitability after it couldn’t make money in what was for years the hottest housing market ever, where people paid no matter what to buy no matter what, sight-unseen, inspections-waived, no-questions-asked?

It is facing an existential crisis because its stock crashed, and it cannot raise new money to burn, and the real estate market has turned south, with demand withering amid holy-moly mortgage rates over 6%, and home sales are going to be far fewer and far harder to get.

Upon the news that Compass is now trying to figure out how to cost-cut its way to a positive cash flow as revenues are going to take a hit, and as its fake growth model fell apart, the shares kathoomphed 10.5%, to $4.26 a share, down 81% from the high, which occurred on the day of the IPO. Just about every investor that got bamboozled into touching this got shookalacked:

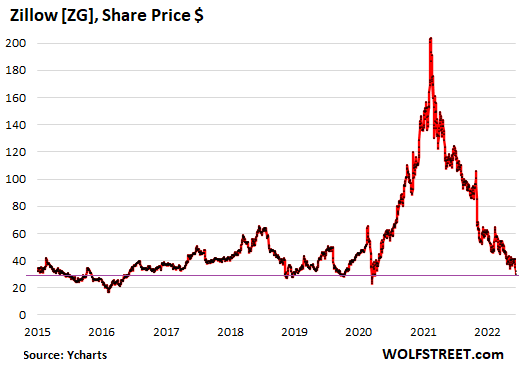

Zillow didn’t make any additional layoff announcements today, but given the conditions that the housing market is now facing, and the plight of Redfin and Compass, its shares dropped 6.2% today, to $30.22, down 86% from its meme-stock-stimmie-miracle high of February 2021, and back where it had first been in 2013. It probably saw something coming in its vast housing market data when it decided to get out of the house-flipping business last year:

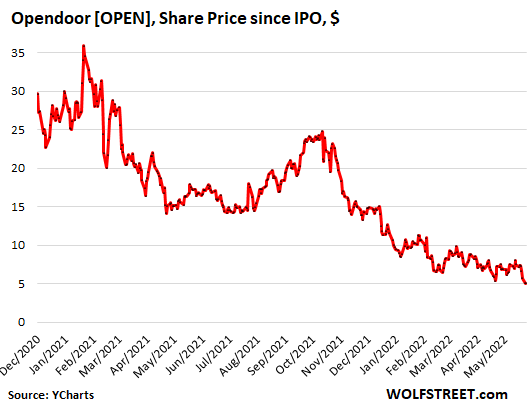

Opendoor Technologies, the home flipper that decided to stay in the home-flipping business – because what else is it going to do? – didn’t announce any layoffs today either. Its shares inched up 2 cents from its all-time low yesterday, to $5.04, down 87% from its high which occurred, you guessed it, in February 2021.

The company now faces the inconvenient challenge of selling thousands of houses that it had bought in the hottest housing market ever, but now there are these new holy-moly mortgage rates, and price drops are spreading, inventories rising, and volume is dropping, and everything is going to get a lot tougher than before.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Learn to code?

I am a software developer who talked to a recruiter trying to pitch me a job at Compass shortly after the IPO. I didn’t get the business strategy and passed. Luckily I also passed on a bunch of crypto companies like Coinbase. Luckily I am not one of those people who see the grass as being greener on the other side…

I got an offer from compass a few years back that I declined to work in a much more boring company. I’ve gone back to my offer package a couple of times to see what the stock options would have been worth. Needless to say, I was smart to have stuck with the slow boring company that pays it’s employees in 100% cash.

Wolf wrote: “They all have one thing in common: They lost lots of money every year of their existence as a publicly traded company.”

And now we know why Wall Street refers to these speculations as “investment vehicles”. They were planning to drive off with your money all along.

How long, I wonder, before cryptocrap goes to it’s intrinsic value of ZERO.

Never, because crypto has tons of potential value particularly in micro-payments and making a unit of account that’s actually stable. This rout is going to bring us closer to unlocking that value by killing the hype-mongers.

Is there a crypto coin that is anywhere near the credit card guys’ per transaction cost?

Tether is zero AFAIK.

Crypto is literally nothing. Other than a “stablecoin”, it’s also too volatile to ever achieve scale as a payment method.

Micropayments don’t change the equation at any scale either.

Moreover, use as micropayment has nothing to do with the price. It can be used for micropayments, regardless if it is valued at 1c or $1MM.

Just another rationalization

Some developers were nipped even in this first round of Redfin layoffs. From their news release:

“Because for every project we start, we have to think about another we’ll stop. We’ve already built tools for teams to work together on a transaction, so we need fewer engineers to add to those tools.”

I am a software developer for one of the companies above

The real estate market in the Bay Area is turning faster than I thought possible. My neighbor told me last month he was planning to list his house for $2.4M. It went on the market today for $2M. I’m also seeing 6 figure price cuts everywhere. Has this ever happened before?

Still hot over here in So Cal. As I said before, people will pay ANYTHING to live near SocalJim. SocalJim is synonymous with Real Estate that Never Depreciates.

Come down here and join the Utopia.

Echo that, there’s certain level of stupidity in SoCal especially in South OC unseen anywhere else.

As time goes though, the domino will eventually fall even in this perceived invincible market.

Socal… I’ll be happy to redirect all the NY, NJ, Illinois and everyone else heading to Florida your way. As long as you don’t ask me to chip in for gas.

Agreed, Space Coast is slowly turning into Miami.

Lots of early retirees heading here + jobs. No sign of a collapse in prices, Goldman Sachs just bought an entire neighborhood of 87 houses in Palm Bay. Pretty hard for the average Joe to compete.

We got lucky, sold the overvalued stocks for an overpriced house 6 months ago.

I am seeing some softening in SoCal. My old condo complex that I keep a eye on for sentimental reasons is having price cuts for units on the market, and it is apparent prices peaked in the development about March, and now coming down there and the area nearby. My current SFH neighborhood had houses easily sell in one weekend during 2021 and up through 1Q22, now have houses sitting over a month, one pulled from the market. This is not to mean there will be fire sales, but I think the most aggressive sellers are realizing things have changed.

In my San Diego neighborhood a townhome took down the “Just Listed” sign today that had been sitting atop the For Sale sign for the past six weeks. 2 bd, 2.5 br still on the market and started at 1.15M, now down to 839K.

Near the coast, yes. Expect that will be last to fall like last time.

Volume plunged!

I’m also looking in the Bay Area and the number of $300-$400k price drops is incredible. They are starting to list way below Zestimate but still above 2020 prices so we still have a long way to go. My realtor told me that half his buyers stopped looking stating they will reevaluate in 2 years! That’s just one data point but it’s crazy.

You have to be stupid to buy in a Bay Area market like this. Nothing the Fed did today is going to have an affect on inflation. We could be seeing upwards of $150 a gallon this fall. Housing prices are dropping in Dublin/Pleasanton, Benicia and Outer Richmond SF. Tech companies are saying, you either come into the office or no job. YES, waiting 2 years, let this all ring out.

Prices are being slashed all over the country. Hell, just do a search on any of the named sites. Houses are being reduced by $10,000-$35,000 pretty much across the board. I just had a couple dozen hit my inbox, and was astonished at how fast the prices are coming down. It’s not time to buy yet, but at this rate it should be come Next year.

It won’t be time to buy until literally nobody talks about housing as more than a place to live and nobody talks about a bottom. When ti’s dead and gone and everybody hates it (including you and me) then and only then is a bottom reached.

We’re a long long long way from a bottom

That will happen when Wolf’s excellent chart showing housing appreciation intersects with CPI inflation. It happened in 2012 and when it happens again, I will urge my son to buy a house at this time.

Like 2012, it will be a dark, scary time when renters are crowing about how smart they are over how much they could have lost if they had purchased during the peak. They will be correct but like 2012, many will miss the bottom again and lament a few years later about how they cannot afford to purchase a house.

The wheel keeps turning. We have seen it all before.

I saw a graph yesterday, about 1% of the work force are realtors right now. I was flabbergasted. That’s slightly higher than the last peak during the housing bubble of 2006. Even normal is 0.5% which seems way too high. I don’t wanna know what % lawyers represent.

Its fairly easy to be a real estate agent in most states. At todays valuations, it may be an easy way to save $10k when you buy or sell your own house.

In my area a potter and a doula became real estate agents, just to cite two of many.

In south Orange County I still see a ton of prices that are really high. People need to understand that real estate declines take 2-3 years. The last one continued long after the Fed had cut interest rates. This time the Fed has to raise rates.

I feel sorry for people who will get hurt by this, but would love to see the investors who were trying to get rich quick lose everything. They were investing in housing that priced many people out of the market.

The only smart sales agents left are those pricing far below comps and baiting the final few FOMO buyers to bid $100k over on the “bargain” priced home, carrying it close to what it would have fetched a few months ago with 3% lower rates.

It is delicious here in Greater Boston to see for the past month, sellers greedily reach for the moon with $700-800k listings only to have them languish on the market and slowly price drop.

Interest rates on 30Y mortgages have never risen this much, this quickly other than in the spring of 1980, however 3% to 6% hits much differently than 13% to 16%.

There were huge price cuts during the Great Financial Crisis. I read a recent article about single digit home price cuts in several cities, some of these were in the rust belt.

Housing prices went up faster than incomes. New home completions are low. Inflation is 8.6%, rising faster than incomes. Retirement accounts have taken a hit from falling equity and bond prices.

The sanctions against Russia have caused a spike in energy prices. Russian military actions caused food prices to rise.

Retirement accounts have taken a hit from falling equity and bond prices…

from prices that were never real and existed for about a year.

Crazy come, crazy go.

I wonder if this means the end of that glossy real estate magazine printed on oversized paper and filled with multi-million $ San Francisco – East Bay area home listings? I suppose a lot of real estate brokers will be looking for new jobs soon.

It’s interesting that the Innovative Disrupters always base their future expectations on a completely NON-innovative and NON-disrupted ambient environment. I am the only variable in the world.

QE will continue forever. Prices will continue to rise forever. I don’t need a real business or real profits or real savings, because the free money will continue forever.

In fairness the free money thing has been going on for a very long time.

As in welfare good idea ,but abused .Labor shortage make time limit on benefits then go to work ,some will be able to do daycare . Seems to me it is a good idea

I think these companies were sort of designed as investor hit-and-run machines. They’re meant to sell a story, have an IPO where VCs and execs cash in big, and then fold once investor cash dries up.

If anything, most of the founders are probably amazed that the Fed stepped in with such aggressive QE for so long allowing their cash burner business to stay open many years beyond its originally planned lifespan.

There was a time when being an elite vulture capitalist or former CEO of a totally failed business was such a huge badge of shame that one would be shunned socially, family all but ruined, kids unemployable by any reputable companies, etc…

I remember when having a bankruptcy on your record was a kiss of death business wise – also socially – even if you weren’t a CEO and were just a ‘normal’ person.

A couple of less well known ones.

– Side Inc, this month laid off 10% of its workforce. The way I understand it, the company provides “tech” to a select number of elite brokers.

– Digital mortgage lender, Tomo also laid off 1/3 of its workforce, around 44 people.

It’s over people.

Another one:

– Blend Labs. They partner with Wells Fargo and a couple of other banks for mortgage origination. Their stock is off 80% from the high and they too laid off 10% of their workforce back in April.

I googled Glenn Kelman. It turns out that Redfin has made bucketloads of money…………..for him. He has sold over 32,000,000 Redfin shares which he got cheap as part of his employment package. He has averaged sales of over 60000 shares every 70 days for the last few years. Don’t try to tell me Redfin isn’t a moneymaker. It is doing exactly what it was designed to do. To make money for the top directors and executives. It will go bust in the near future, but you won’t catch Glenn and his mates putting any money back in to it. I do wonder what they do put it into. Is it blue chip low yield real estate? I suspect so.

Homes in the Hamptons, big boats, vacation homes in far away places, divorce settlements, kids sucking off the money tree….lots of places to put Big Dollars.

Company officers saw an opportunity when the Fed lowered rates to zero and started purchasing MBS’s to drive mortgages to historic lows to start a risky business based on a gamble with the Fed and were helped with the Pandemic.

They started the companies like Redfin and Zillow when they saw the demand. I don’t think they were emotionally attached to a cause other than making money and jumping ship with the money before it collapsed. True entrepreneurs.

I feel sorry for the employees but most could see the party would end at some point. The good ones who have sales skills will move on to selling the next big thing. Then at some point, it will crash also.

I still feel sorry for all of the buggy carriage workers and the vacuum tube engineers but that is progress.

My main problem is that I do get emotionally attached to my work. So far, it has worked out OK, but I suspect my end will happen at some point also.

I am proud of the work I do around the house.

I build things to last hopefully 100 years.

However, all good things must pass.

Bob,

Two engineers, Jason Stoddard and Mike Moffat of Schiit Audio, make a sweet vacuum tube preamp in the USA. And quite a few other high-end products with vacuum tubes.

I have their preamp, a Freya +, in the living room. Of course, it runs with two other pieces of Schiit: a Modius DAC and a Vidar stereo amp — made in the USA.

I bought ’em a couple months ago.

On the other hand, nope, I do not have a buggy carriage.

A company like Redfin wont go bankrupt, they will simply downsize until the market solidifies. The website traffic to Redfin is still valuable. Same thing for Zillow.

But the executives will stop wasting money on stupid stuff and dreams and focus on cost cutting, which will cut jobs, salaries and also cut on plenty of over-hyped technology companies.

The transition from the old real estate model to an online digital transaction still makes a ton of sense. The company that is willing to execute this plan on low overhead is the one that wins/thrives.

i like Craig Newmark, the guy who founded craigslist.com and only charges for listings for job openings. eBay invested money in his company and wanted to take it over and make it charge for all listings, but Newmark wouldnt let that happen. So I can list stuff for sale locally and not pay a dime.

We need more online businesses that focus on delivering great value to the consumer, using digital platforms to reduce prices, not increase them.

I like Craigslist too, and have used it for many years for buying and selling misc junk, and to advertise rentals.

I admire Craig Newmark and Jim Buckmaster for their longtime commitment to a website that maintains a simple interface free of advertising, that supports barter and trade in local communities, genuinely benefits the users and not just the C-suite, and is largely free! You don’t even have to set up an account to use Craigslist.

CL does charge a modest fee in certain categories, including help wanted, auto dealers, and several real estate markets. From what I understand that is primarily to control fraud and spam in those categories. For the first time ever I recently had to pay $5 to list an apartment for rent in the Boston area.

Ebay used to own a 25% stake in CL, but Ebay divested it back in 2015.

(SK ===> SK01)

“We have to protect our phoney baloney jobs here, gentlemen! We must do something about this immediately! Immediately! Immediately! Harrumph! Harrumph! Harrumph!” Mel Brooks in Blazing Saddles.

Mongo only pawn in game of life.

-sigh-

pffffft…

I didn’t get a harrumph out of that guy!

Harrumph!

I love the smell of BBQ’d phony companies. The sooner these shams cease to exist, the better.

If the gang-banging could stop for a few minutes… Zillow (and Redfin?) are great public utilities. I hope they survive. I don’t know much about the others since we’ve never used them. But I’d hate to see either of these disappear.

If the very impressionable, modern-day investors get bamboozled, tough tittles. You can’t characterize this whole thing as fraud just because the story was irresistible to the gullible: Hey diddle diddle, the cat and the fiddle, the cow jumped over the moon.

“Marry in haste, repent at leisure.”

I like Redfin’s layout and I hope their site at least sticks around. Zillow’s UI is disgusting, I’m not sure how that site got so popular when they make it hard to see the actual information on the home. Well, I know how, because the average dummy just focuses on the “pretty pictures” and doesn’t even read the background info about the home.

The worst one of all of them is realtor.com, the “official” site of realtors. spam central stupid popups and impossible to quickly find info. typical of the real estate grift.

Funny, LGC — I was just going to say that I’ve found realtor . com to be a lot easier to use than Zillow and Redfin. Different strokes, I guess.

Zillow earned its traffic by providing a “zestimate” of home value, but those zestimates are now completely inflated.

They used to have more info on the homes including what was left on the mortgage when it was about to foreclose. They stripped a lot of info out when they were preparing to buy the homes themselves.

Their algorithms have always been off though. IDK, maybe they believed in themselves too much.

I have been looking at Redfin and Zillow for years at the incredible history of sales that they record. I also look at Zestimates with an open mind.

All for FREE!!

Maybe that’s the problem.

Zillow’s “Zestimates” are phony garbage, which is part of the reason they lost money flipping houses in the biggest real estate bubble in history. The whole company needs to cease to exist.

Don’t know about everywhere, but seem to remember that the six states we have owned RE in the past 40-50 years have had all or almost all the information available to the public as it is recorded and made part of the public records.

Used to take a visit to the county courthouse to access, but thinking it is all on line these days.

Certainly is currently in pine ella’s FL, and although not the most easily navigated website(s), that appears to be a function of each county.

The funniest thing is watching the spam emails from Zillow showing their algorithms 12 month Zestimate prediction all still being at +15% in most markets. Are you kidding me?!?

Algorithm built on lagging indicators not leading.

If Zillow, Redfin or Opendoor end up being another Grocery.com and forever cease to exist, the only tears I have for them is tear of joy.

My disdain is especially strong for Zillow since they are about as terrible as Lawrence Yun when it comes to housing will forever go up or stay up gospel. You would think after $400M+ disaster of getting it so wrong, they learn to STFU in predicting the market but nope their “economist” still yapping on about growth for 2022 and 2023..

Oopsiespalooza! OpenDoor definitely deserves a ‘holy-moly mortgage rates’ hyperlink. Bamboozle time is over!

Done!

I’d never invest in Zillow but their Zestimate is a particularly convenient reference. And it’s free. Redfin has always been geared toward the RE crowd.

Well, the Zestimate isn’t useful if it is wrong/misleading.

If it simply listed transacted historical comps in a clear, detailed fashion that would be one thing.

But they pitch Zestimates as having some extra “magic” and they are wholly silent on the underlying factors that drive valuations (ahem, interest rates).

And then they try to specifically value every residential property.

All very misleading, biased upwards, and really, ultimately, a black box.

Just charge a fee for straight transactional data easily accessible and be done with it.

But that approach won’t generate the dreams of billions in revenues necessary to drive an IPO.

So you end up with a clown car of a company with a bunch of “revenue drivers” tacked on that aren’t sustainable.

Not unique to Zillow, but wayyyy too many people treated Zestimates as gospel. Probably beloved by Fed as driver of phoney baloney “wealth effect” (the real “transitory” number…)

“ Not unique to Zillow, but wayyyy too many people treated Zestimates as gospel”

You know it…

Then they meet reality with hard appraisals or FHA Automated Valuation Model (AVM)…

And then they get mad, really mad…

We’ve been in our house for 4 decades+. So no actual number … just nearby comps.

The Zillow and Redfin estimates are fun to see but the appraiser gave us a somewhat … uh … different number.

Our HELOC – unused – was due to end this September after 7 years so we decided to get a renewal. With any luck we’ll only pay the $75 yearly fee … but KNOWING we can tap it to cover a really large unusual expense is comforting.

We do plan to ‘downsize’ after the kiddies … finally … get all the stuff they want to save out of their freebie storage lockers. :-)

For what its worth … in our case Redfin was closer to the appraiser’s valuation.

I’ve looked at Sales history that Zillow provides more that Zestimates.

I’m sure Sales history is a factor in Zestimates, but historical data has more weight.

If a house goes on the market for $1M, and the previous sale in 2018, is 500K, Run!!! Unless they scraped the house and built a mansion.

If a house goes goes on the market for 500K and it previously sold for 100K in 1990, I look at the neighborhood houses for comps that sold more recently.

Zillow is so awesome for that free feature.

How Redfin and Zillow estimate work:

1. If a house is off-market, the estimate is based on recently sold comps in the area.

2. When a home is listed, this is where the lies begin. The algorithm takes that as the “starting price” and adjusts their estimate to within a couple percent of the list price. You can verify this by seeing an off-market home the algorithm claims is worth $425k, then say it is listed for $500k, the estimate will change to like $497-503k. Fat fingered entries, for example adding an extra zero, the algorithm would claim the house is worth $5M, that is how bad these algorithms are.

3. Upward adjustment is mainly done based on engagement with the listing on the site, for example views and favorites are weighted in adjusting the price upward. The home with the most favorites in a town, will have the highest percentage increase in the estimate.

Honestly their methodologies are very poor, and could be replicated by a novice coder with an Excel spreadsheet and VBA.

Flounder,

Very informative, thank you.

People don’t realize that now that almost all transactions/interactions are computerized, they could very well be dueling with automated yield optimizer software when it comes to price for many/most goods (including housing).

Given the truly insane levels of rent inflation over the past year (20-25% nationally, 40% for places in FL) there is clearly *something* new/wacky going on that never went on before.

Automated price optimization software might be part of that.

And, as Flounder points out, the software need not be limited to consummated transactions, mere queries/engagement might be used to automatically hike prices.

It will even out in the long run, as the software adapts to true supply/demand, but in the interim huge dislocations may occur as bid/ask price spreads grow enormous.

Zillow Zestimates for UNLISTED properties are actually quite a good start when pricing a property. The algorithm is mostly based on the ratios of recently sold similar properties to their tax assessments in that area with a correction for tax appraisal time lag. This factor is then applied to all unlisted properties in that taxing district. Simple, practical, and reasonably accurate. The zestimates for LISTED properties are essentially the asking price as a sop to realtors, their main source of income.

Prices cannot rise forever, not even for real estate. However, they will not fall a lot and might rise for a little more time than I expected since the banksters are using their access to ultra low-interest “loans” from their “Fed” and from their gullible depositors (many needing to keep significant operating cash in accounts often paying no interest or in CDs to avoid risk) to buy huge amounts of real estate.

In happier news, “Saudi Arabia plans to spend $1 billion a year discovering treatments to slow aging” per MIT Tech. Review. Hence, all of our corrupt oligarchs and the world’s corrupt oligarchs are engaging in research that unintentionally may coincidentally extend all of our lives. Talk about trickle down. LOL

Well, who is going to pay Google a quarter Trillion dollars per year, every year? Perhaps oil companies will start advertising their oil.

Google is probably better protected than most techs – for all its flaws, internet advertising is a helluva lot more potentially accountable than what was pumped out by TV (especially in the bad old oligopoly days…which didn’t end as much as people think it did.)

And then there came Brave browser.

Try it sometimes, you are going to love it. Using it on my phone and laptop.

Plus, they don’t track you.

So, what’s THEIR angle?

When an app is free, a profit needs to come from somewhere.

If it isn’t ads or my data as they claim, what is it?

I have been using brave browser everywhere for quite some time.

Along with different search engine who does not collect and sell my data.

They key word being “potentially”.

Internet advertising has been cooking their books for decades.

“internet advertising is a helluva lot more potentially accountable”

Sure and I’ve got a million or so bots to sell you.

“Redfin has been a publicly traded company since July 2017, and has existed for 13 years before then as a startup, and it’s just now time to think about how to make money?”

IRL is sometimes even crazier and funnier than parody as Mike Judge said about Silicon Valley and the general mentality of tech valley VC in general. As the character Russ Hanneman said on the show or something to the effect of “F making money…VC loves it when you forever lose money but can sell that dream..”

Wolf: Its time you included “WARNING. Distressing Content” at the start of articles like these.

The tide is out and its a veritable willie-fest of those who were swimming naked. People may choose not to look.

They drove out all kind of small businesses, drove wages and employment conditions to new lows and now they will tank the economy into recession while the SOBs at the top laugh all the way to the bank!

Wolf, “They all have one thing in common: The lost lots of money” should be “they lost” is missing the “y”. I know you enjoy your crowd sourced editing so not meaning to nitpick. I assume you delete these comments after making the fix.

Thanks!

Yes, by all means, point out the typos. I rely on my slave-labor line editors. They’re the best in the world!

That is so disruptive….maybe an IPO? or a SPAC at least?

I wasn’t going to say anything, but always dreamed of being a line editor. In the third paragraph under “Compass” it should be “Inspections-waived” with an “i.” It’s harder to pick up typos when the misspelling is another word. Please don’t hesitate to delete this comment.

I use auto-correct and a spell checker, and I have my computer read the text back to me. So normally, I catch typos that sound different, such as transportation which, if I get something wrong, my auto-correct turns into transpiration. But I hear the difference. Waved and waived slip through all my safeguards :-]

Ha! I just pictured someone wildly waving their arms yelling “No Inspection!”

I suspect the bad financial news is going to be coming fast and furious for several months and that this correction will be ongoing for years. We all saw it coming because we pay attention. What’s shocking is that even though we knew it was coming there seems to be a common thread here that none of us thought it would be this fast. This is going to be bad.

Not going fast IMHO bowo:

Just a couple of dips in the road to heck SO FAR…

We are still waiting for the FFR to go to at least 5 while the ”official” inflation is at least 8, maybe double both as it was in late ’70s/early 80s.

Zestimates certainly appear to be a joke when they show our modest house now worth FOUR times what it was this at this month 2015.

OTOH, our appraisal by the county is supposed to be at 100% of market value, so I suppose Zillow could just pick that public record up in addition to the method described above.

In any case, with rises like that, it would not surprise me at all to see RE go down by a lot more than 50% eventually in this cycle.

So another SoftBank company is having issues. Perhaps Compass should change its name to WeBust.

If I see Warren Buffett’s name, I think if I keep reading/watching I will get good advice to follow. Now, when I see SoftBank mentioned, I think I will find out what I should avoid.

Buffet’s BRK is starting to get to reasonable price. Somewhere between current price and around $200 is probably the bottom for it. Price to book around 1.2 now. Usually a long term winner if you can get around 1.0. Long term average price to book around 1.35.

Yep. BRK.B is getting within range. I have to wonder whether a new CEO would feel the same commitment to some of the laggards that Buffet has, like Kraft/Heinz, Restoration Hardware, and a few others.

Some of those holdings may be for the associated political or other connections, rather than cash generation…

To some extent I believe it is on redfin themselves. Their estimates are so bloated up that the buyers just resign and not even try looking. May be if they made sure their estimates were more in line with current market, probably they would have some more business? And I don’t know, may be use mortgage rates in the algorithm for estimates?

ARKK domino. RE domino. Within few months the energy domino might inflame another energy region.

In Orange county CA, residential real estate has gone from $400/sqft to $600/sqft since 2020, as reported by movato market trends. 50% increase in two years from an already expensive starting point. To be honest, I’m not sure prices will come down much until/unless mass layoffs begin when the recession hits (mid next year?). Even then, people will be coming out way ahead. It is just pure insanity that the Fed did this.

I watch Holden Beach property in NC and prices have basically doubled to get on the island to about $550/ SQ ft. A lot of new $1.5 – $2.5 million new construction properties being listed. A million used to be top end there.

Seeing some price cuts in the last three weeks. One did two 3% cuts and then last Friday did 10% price drop to around $380/ft. Still way above pre pandemic price.

You may want to hoist the house up and slide under a few pontoons to keep that investment from slip-sliding away.

Wolf…

Excuse off topic

Who made the money in the Bitcoin crash? (if this is a zero sum game)

For sure the people who got in early and sold at the top and took their fiat and went home, they’re the ones who won this game. Same as in just about anything. There are also some derivative ways to bet against bitcoin, and those people won too. There may be other ways to make money on this crash.

Hey Wolf how about a article on farmland,prices soared on land ,fuel,fertilizer,but now Wall Street is pushing it ,Watch out below

I will claim myself to be in this category as a computer nerd who knew about buttcoins in 2011, mined for a while on my lowly, lowly ATI 5770, and sold my buttcoins for a whopping 30 dollars when the price hit 11 dollars a coin and all of us shut in weirdos were having collective aneurysms.

I’ve seen so many crashes and moonshots in cryptocurrency it’s not even funny. Just wished I’d have kept my 3, decade old bitcoins and sold them at the peak. Oh well.

I really wished I would have stayed in computer science instead of becoming a trucker… That was the real screw up lol.

I think the makers of video cards used for mining profited the most. Sorta like how during the gold rushes, they guys selling shovels made lots of money.

NVDA had a good run, and the electric power providers made “money” (dollar-credits) too.

Shovel-sellers back in the actual gold rush actually earned money (precious metal coins).

P.S. I’ve found that terminology matters for understanding things and avoiding scams – I try not to give in to the hype, not to adopt the sellers’ framing of a transaction. If I use the right words when thinking things through for myself, I stay out of trouble. Blockchain tokens are computed numbers, not “mined coins”. And today’s digital credits aren’t exactly money in the traditional sense.

Put your seatbelts on,its going to be a rough ride on the “correction” machine…

California must be floating on a sea of cash to have these prices for homes that has been around for decades. At least since the 1970s and 1980s

In 1983 I was offered a move to Ca from Ok and the home prices then in Ventura CA were triple the price in OKC and Tulsa.

Now from the 400 to 600 sq ft pricing I’m seeing they are still 3 to 4 times the prices in Houston and other parts of Texas that are not Austin and Dallas.

Tech has easily replaced oil for generating the greatest wealth transfer in generations vs the railroads steel banking and oil of the 1800s. Tech reigns supreme for asset prices salaries and stock grants and return on capital and the ability to raise capital!

Very similar to my industry energy. Sell the hype.

Real Estate leverage in 2005-8 created one of the worst recessions ever with the banking crisis.

The cure for that was QE and zero fed funds rate for another 13 years until now.

Decades to create and now decades to unwind.

Looking like ECB QE may be coming back already Wolf ?

I bet they have a plan to buy equities.

Notice with each emergency, central bankers accrue more powers.

You misread their statement.

App Crap Snap!

Maybe we’re missing the point here… one of the objectives is for the Fed to try to maintain full employment. If you print lots of money it allows companies who make no money to raise lots of cash from Wackstreet. This then allows them to hire lots of technically competent people and get them some real world training. I get it!

3.6% unemployment with 11 million open jobs…..can be considered FULL employment.

It used to be that 5% was considered full employment….decades ago.

To your point, inflation makes businesses trim payrolls and head to the bank for loans.

Check out the employment-to-population ratios – they tell a very different historical story from the politically engineered unemployment rate.

The E2P rates are getting closer to late 90’s highs…but that took 20 *years*.

“unretirement” is the latest job trend.

What you fail to understand about Opendoor is that they are selling these homes to large Corporate buyers. Before they have even complete the purchase of a home, there is already a contract with a Corporate buyer in place. Conrex, Progress Residential, Tricon and First Key are buying hundreds of properties per day and many of those are Opendoor acquired properties.

Jewels,

What you fail to understand is that Zillow unloaded thousands of houses to corporate buyers last year and this year because it couldn’t sell them fast enough one-by-one to retail buyers. That’s how Zillow got out of the house-flipping business. But you cannot make any money doing that. Zillow lost a ton on those deals.

Sorry for your loss on OPEN. My thoughts and prayers are with you.

I don’t think you have a clue. OPENDOOR is printing money by just being an exchange. They aren’t struggling with inventory. They turned a profit last quarter and the economies of scale that they continue to grow are only going to improve their bottom line.

OPEN doesn’t really fall into the same boat as everyone else. Their business is sustainable and will actually excel in a down market. If you know their buying strategy they don’t buy top-condition homes, they buy the ugly house in a nice neighborhood, sell it to investors with no holding time, or fix it up and make a profit. They have the closest thing to the Amazon Book Store model of this group.

As an OPEN stockholder, let the prices drop, I bought at 5.30 two weeks ago, bought more yesterday, and will continue to buy. This is a long game stock, one that has a business model I’m sold on.

Jewel, you must understand that Opendoor lost $662 million last year even as their industry approached peak mania. They lost $253 million the year before. They lost $341 million the year before that.

You fail to understand that a business strategy and clientele are meaningless to investors if a business can’t translate their story into profits. Much worse if the best they can do is burn hundreds of millions per year in net losses. Opendoor will run out of investor cash and will have to become Closeddoor.

Yet their cash flow is growing each quarter. Also, you didn’t mention they turned a profit last quarter. This is 5 years earlier than they planned. They are also almost 10 years ahead of their growth plan because of this market.

I guess what you don’t understand is, are they a growth-focused company that is building a network or a short-term profit center that has no potential to scale?

OPEN is a 20 Billion dollar company, with about 3k in employees, with overhead that as they scale will not have to grow. This is the type of company that as they grow, will make billions and billions of dollars.

This site is full of selective data analytics that truly doesn’t know up from down. OPEN grew its cash available but didn’t significantly change its inventory levels, this is a sign of a company that is starting to hit strides and make money, lots of money.

Jewels,

This isn’t entirely true for sure because I have seen many Opendoor properties sit on the market for many weeks even during the hottest time of the market in the last year or so in the one of the hottest metros in the US.

I never had much bamboozle myself. I think I used up what little bamboozle I had just getting Holly to go with me to the senior prom.

Instead, I’ve had to rely on my other talents, which is probably why I’m stuck at my desk all day, every day, and only go outside to freshen up my sunburn and aggravate my allergies.

It’s tough, trying to break into established markets. It’s pretty crowded out there. Creating new markets is even worse. It’s no wonder nearly all new companies fail. Look at what happened to Sears Roebuck and Co. For a while there it looked like they were going to make it. At least they got enough altitude so they could crash and burn. You’re lucky if you can even get off the runway.

It’s a dog eat dog world out there, and let’s face it, I’m probably pretty tasty.

It’s a total disgrace

Because they set the pace

It’s always a race

And the best I can do is

Walk.

Hilariously unamused!

Poetry! Paul Simon has a good tune about the allergies. Also that one that goes “what you gonna do when your looks are gone?” That’s also the one about being stuck at the desk wondering how am I gonna get out of here. Lucky music guy. He knows how it is and what we think, even when we isn’t him. And he can just rest until the end now if he wants.

Ah yes, everyday I enjoy what Sears, Roebuck and Co. was.

For I live in a modest, but very nice 2 br, 1 bath, build it from a kit, Sears Craftsman bungalow. Nine foot tall ceilings, beautiful woodwork inside and going on its second century of life.

“Life is good in Minneapolis.”

Dan,

Across California, the Sears kit homes from I think the 1920’s-30’s are prized and cherished. Lath-and- plaster walls, outstanding wood accents, gorgeous true-divided light wood windows and solid core wood doors/French doors, high ceilings with pizazz, oak floors with dovetailed corners, charachter, charm, integrity, and classic design. So glad to hear it. Well done.

It’s an endlessly programmed world of 1950’s television. Every day starts with Bozo the Clown pumping new cereal for the kiddies and winds up with Groucho’s duck revealing the secret word is “Ennui”. Ozzie always comes to his senses in the end and laughs off the latest predicament.

My Craftsman lawn mower, chainsaw, battery charger, socket set, wrench set, screwdrivers, sander……. haven’t died in nearly 20 years.

Sears didn’t have obsolesence as part of their business strategy so they maintained customers but could never grow sales. That is death on Wall Street.

Maybe bad management also had something to do with it.

Way I heard it when working in their stores, and kmart’s too, was some smart guys who had learned a lot working at wally’s world got enough financial backing to buy them, Sears and Kmart, and then basically ”value engineered” them out of existence.

Dividing out and closing and selling some stores, rather than updating, maximizing cash out values of RE, stiffing or beating up vendors, leading to reduction of quality and quantity of goods,,,, fighting contractors, etc., etc.

Sears was essentially cashed out by its CEO, Eddie Lampert. There are perfectly legal ways to rob and execute major corporations for fun and profit, and they’re not called vulture capitalists because it sounds cute. It’s less common than it was because potential victims have wised up to the financial engineering techniques and have set up defenses.

Whack

They’re coming to take me away Ha haa, hee hee to the happy home

How about mortgage broker companies? Remember Countrywide? This should be another epic round of destruction.

In the little SE Utah town I’m currently in (pop. 6000), 14% of the houses on the market have been reduced in the last two weeks. It seems like just yesterday there were only a half-dozen on the market, all selling literally overnight, and now there’s 71, nothing selling that I can tell. And several of those houses are gutted and obviously belong to flippers who panicked or can’t get supplies to finish them. Prices range from 100k to 450k. A slowly dying coal mining town.

Like others have said, it’s happening very fast. The resort town in Colorado that I’m from has seen about 20% of listed properties reduced in the last month. Prices range from around 750k to upwards of many millions, and there appear to still be some sales, though much slower. The town has a population of around 8k, but is a popular resort town and sees many tourists. All very impressionistic stats, I know, but data points to add to the mix.

The few people I know who have recently bought are all of the mindset that whew, I got in just before the rates increased, when they should be thinking, oh man, I screwed up and bought at the top.

Ha…true

Why don’t you name both towns? It’s not exactly classified info. Creepy and dorky that you think it needs to be anonymous.

what do you think is happening or trending in the south Denver metro area?

Take a good look around you. It is all fake. There are plenty of companies that seem real and are ‘making money’ but are just as fake. For four years right before the pandemic and before I turned to the dark side and got on the government payroll, I was working for a general contractor. During that time the only thing keeping us going was constructing and remodeling government buildings. Nobody in the private sector could afford upgrading to an ‘ADA bathroom’ for 40 grand. So even indirectly, how many ‘profitable’ companies are only so because of the same government handout as these stimmie infused IPO gold diggers?

It was a money laundering gig!

1) 3.75% rent on a $1,000,000 house = 37,500/year.

2) 3.75% on $1,000,000 10Y gov note = $37,500/ year. No evictions,

plumbers, roofers, dishwashers, lawyers, RE agent, taxes…risk free, clean.

3) When gov rates were zero and the dollar was zero, – when the whole world was spitting and laughing at the plunging dollar, – foreigners buying cheap dollars flood US RE markets.

4) During 2020 panic demand was booming.

5) In mid 2020 the RE markets might start to decay, in real terms. RE have competition from the gov and the 6% mortgage rates is slowing down transactions.

6) 3.75% rent in smurf country get smurf landlords deflated rent, in dollars terms. Smurf countries are subjected to different risks.

7) RE is not local, it’s global.

“3.75% rent on a $1,000,000 house = 37,500/year.”

For AirBnB rentals locally, the local house cleaners are charging $500/clean. The equals 2K/month which is 24K/year just for cleaning.

Just like the suppliers for gold miners, the locals know how to make money in a boom.

Just for cleaning. Nevermind heating/cooling/taxes/fees/repairs.etc…..

Money will flow with the demand.

FYI, the only way at this point that I would own an AirBnb is if I was willing to roll up my sleeves and clean between renting, repair anything necessary, and actively market and manage the property.

The dollars for rentals are huge with AirBnB but IMHO, it is not profitable for the landlords who want to generate truly passive income. Too many expenses with this boom.

And demand goes away without money. The thing about money is it can only be spent once. Money spent on increased housing costs, $5.50 gasoline, $10 lb. meat, and higher taxes and utilities cannot be spent elsewhere.

Jdog,

Demand for vacations, post-pandemic, seem high.

How long will that last as budgets now go to food and rent and less for vacations?

Hotels have cleaning/repair/front desk crews hired at minimum wage for many more units.

So far, AirBnB is cheaper for travelers, but with increased cleaning/repair/management costs, does this make financial sense? Not to mention mortgage/taxes/local fees. It probably makes sense long term with taking losses on taxes against gains short term and waiting for things to stabilize.

If you diverted your hard-earned money into an STR in 2020 or 2021 in the hopes of a huge gain, be prepared for some tough times. Both in increased costs or a sale at a loss. I’d hold with the the loss and hope for better times in the near future.

I don’t know what will happen with hotels and Bed and Breakfasts. The post-pandemic travel boom will likely continue as a high priority since people have been homebound and saving for the last 2 years. They think they can afford it and deserve it. At least a few times.

Was talking to an Air&B owner yesterday here in this little SE Utah town (about two hours from Moab). She said the entire region is flooded with AirB&B’s. She has had only three weekends booked for the last month. I checked some of the others and they have tons of openings all summer. Probably from the price of gas.

I’m going to the west side of the Tetons soon and everything up there is booked solid and expensive, but not like the east side. If you want a cheap stay this summer, go to Livingston and Gardiner in Montana – most of their business is from Yellowstone and you won’t be able to get there from there for months because the road’s washed out. These towns are already looking for federal bailout money according to one of the county commishes.

Fascinating article on Bloomberg about people getting rich on AirBnB/Vrbo rentals, bought with loans made assuming continued income far in excess of what could be gotten from conventional rentals:

Am now thinking about a vacation in South America. When I log on to the AirBnB site, I’m greeted by ads for luxury vacation homes priced at more than a thousand dollars a day. (My previous AirBnB stays have all been at rates around $100/day, so I’m not in their database as a high-roller. )

A friend’s daughter works as the pricing manager for a set of several luxury hotels in Florida (esp. Miami Beach). She’s amazed at the prices she’s able to get for the rooms — just keeps on raising them, but the customers keep on coming. There’s clearly a lot of people out there who have (or think they have) a _lot_ of money to spend on vacations.

What’s sad for me is I really enjoy some of these disruptors and will miss them. Redfin and Zillow upended the realtor monopoly and gave buyers vast amounts of housing information; Uber and Lyft upended the taxi monopoly and provided me a far superior experience.

I’d hated these industries forever and saw these disruptors as godsends. But like everything else in capitalism, you just can’t leave a good idea alone; instead all the sharks soon appear in the form of financialization and hollow out all of the meat, leaving it and society in ruins. Greed rules all.

Greed is why we have these disruptors. The strong few will survive the current carnage and I have little doubt they will upend the market like Amazon and Uber did. Pretending otherwise is like pretending the internet is no big deal in 1998.

Investing in the internet when it was a crazed fad in 1998 would have cost you millions in 2001 during the DotCom bubble.

Selling in 1999 would have bought you a mansion in the Bay Area and generated millions today. Who knows about tomorrow?

Investing in the internet in 2004, and holding for 10 years would have brought great wealth.

Investing in Tech in 2019 and selling in mid 2021 would have brought great wealth.

Timing is everything.

I still lament loudly the loss of my crystal ball in the Northridge quake of 1994.

We are all flying blind but thanks to Wolf, my working Magic 8 Ball now says “The future is murky”.

Everything is cyclical. The trick is to figure out where you are in the cycle. There are short term and long term cycles which complicate things even more.

The 1930’s were the end of a long term cycle. Had you invested in the market in 1928, it would have taken you around 25 years to recoup your losses.

In boom times, everyone thinks they are smart. In bust times, most people get hurt… bad.

Uber and Lyft aren’t typically superior experiences anymore, at least in my dealings with them. I’ve gone back to taxis, even if they’re more expensive in some places. Too many dirty vehicles and too many close calls for my safety in rideshares.

I believe it was an Uber driver in Los Angeles who told me he’d just moved back from San Francisco where he’d been researching meth addicts for a script he was writing…

Was I looking to buy?

“What? A script?”

No. Meth.

“Uh, I’m good man.”

They are nothing but horribly bad and inane TAXI services.

I agree with you about Redfin. The core business provides great value to consumers and I think their website is fab. And I always read the emails they send me though I have no intention of selling my house.

The issue is that their core business is maybe a $200mm annual sales proposition. It’s not a unicorn, but a relatively non cyclical part of a key segment with with time a strong market position. And experience and stability will give them the opportunity to keep getting better at their core functions. But that’s not enough for SV in this environment. It has to be some massive growth play, trying to make Redfin something it isn’t.

The contrarian view is that real estate will generally keep up with inflation in the long run.

Let’s say you bought a $1M home with cash at the very top earlier this year. Compare that with someone keeping the $1M in cash. If we assume roughly 10% inflation for the next 5 years, the cash pile will be worth around 600k in terms of purchasing power. The house is likely going to do better.

My take is that there is really no place to hide when it comes to deep recessions but tangible assets will tend to keep up with inflation.

You mean DEPRESSION

That is not the contrarian view, it is the RE enthusiast view. The value of any asset is arbitrary. Some assets have a intrinsic value, but many others value is based on speculation. RE has been in the latter category for about 50 years. That does not mean it will continue forever. Shelter has an intrinsic value, but that value is no where near $400sq.ft.

“The contrarian view is that real estate will generally keep up with inflation in the long run. ”

I am a contrarian. I agree.

In the long term, RE will do better than inflation.

The keys are:

1) Hold RE for 10-15 years. Sell at a peak. Hold at a low. Always hold your primary home.

2) Have enough cash to pay your mortgage for 2-3 years even when underwater.

3) Don’t panic! Walking away an foreclosing on an underwater house is a bad long term decision.

Redo the numbers assuming the person holds cash for 2 years, buys a home in two years at 50% of current price, and the other 50% is invested at a stock market bottom.

The value of patience is skyrocketing.

Sounds good. Okay, so I just need to invest half my cash in two years, when home prices are at bottom, then buy equities with the rest of my cash when they’re at a bottom. Then sell when they’re at the top? Or should I just keep holding? This sounds pretty straightforward and very do-able. I don’t know why I buy at the top and sell at the bottom. I must not have understood.,,,

There another factor no one here is talking about: zoning laws and the YIMBY movement. Housing supply is wildly constrained across much of America because of zoning and the YIMBY movement is beginning to change that.

Japan’s zoning is set by *national* government, and as a result it is relatively open to building and prices have been stable for decades. Ultra-easy monetary policy but no increase in housing price, at least as percent income.

That’s not the contrarian view, except these comments. It’s the majority view.

It’s also the correct view, historically. But we saw an earlier price spike caused mostly by low mortgage rates (and some relaxing of standards). That resulted in a sharp correction in prices. We’ve recently seen another price spike caused mostly by lower mortgage rates (with tighter standards but artificial constraints on supply because of government intervention in foreclosures & evictions). Will history repeat with another price collapse? Maybe?

What we do know now is housing price volatility seems to be up, with homes behaving more like other assets. What goes up can go down.

Hardigatti,

That’s not contrarian. RE has outrun inflation by a HUGE margin over the past 20 years, and so it’s going down and overshoot on the way down, so that on average over time it will roughly stay level with inflation.

H:

The keeping up with inflation story we always heard BITD (‘back in the day’) in the flower state, was three ”real” assets would do it:

1. Waterfront property.

2. Fine Art.

3. Fine jewelry.

This I heard a bunch from older and mostly ”retired” folks who at least seemed to have been very successful, as they all had all of the above.

That was in the period after WW2 until 1980s.

Of course it’s different this time, eh?

Fleeced Investor (stonks,SPACs,craptos,crapshacks etc) from the roof:

I’m gonna jump !!!

Me:

Also do the Backward Flip and f…ck yourself in midflight on your way down.

Pardonne-moi ce schadenfreude d’enfant 😀

Here is my greatest error as an investor. During GFC a female friend told me she was going to ULTA. I said what’s ULTA? She said that’s where I get my beauty products. I went with her to scope it out as a possible investment. Store concept looked good, but I looked at finances and they had a lot of debt. It went on to be a 50 bagger.

Telling the story because the biggest opportunities in a decade could be coming up as stock prices crater.

Stock tip from a person who shines his own shoes:

Dutch Bros Coffee – BROS – I bought at 40 and it went down to 20 in the last few weeks.

They haven’t made any money but are spending on opening new locations. They are taking a hit due to this like all of Wolf’s profitless companies.

Every location I pass has a line going around the building even though they have been around for several years so I don’t think they are just a fad.

I saw a couple on the local news that were giddy with excitement that as first time buyers their $500k “as is” offer won the bidder war on a 1950’s era frame house that required a complete over-haul to being close to present standards. I am very familiar with the houses on that street. Down to the studs stripping of walls. Wiring, service entrance, main panel. Galvanized and black iron plumbing will be stripped. Orangeburg sewer service “tarpaper”pipe removal with PVC sewer service complete replacement to the street. Ditto potable water. HVAC and all its ducting and 220v branch wiring. Oil tank removal in ground and gas service install. The outside is original asbestos concrete sheet rock that is painted. They will find termite damage on the sunny side of the house. All those houses on that street have been visited by termites. The roofing shingles will have to re-done and some sub roofing because it needed new shingles 10years ago but the slum lord who owned it could not get enough money out of the crack-head renters. The crack-heads got downgraded to the interstate under-passes not long after the F$&King Fed cranked up the bubble blower. It’s a “mill workers” house that has little yard and no parking except on street. The buyers,God bless them,are hard working service industry workers that have been saving and dreaming. This F$&King house bubble mania shit need to die and die hard and die fast. The local tv anchor was presenting the buyers as if they had won the lottery. I hope some of the buyers friends or family does an intervention. This is real and it’s everywhere.

My wife and I recently did an intervention with my son who was trying to buy a house.

After presenting an offer 20% over asking on a beautiful superficial flipped house and conducting an inspection, the results were:

1) Leaking pipes behind the beautifully re-drywalled walls.

2) A carefully hidden and unconnected sump pump in the side of the house with the beautiful hardwood floors.

3) An electrical system that was noted to be a haphazard fire hazard with cloth wiring behind ALL beautifully painted walls.

4) Huge cracks carefully covered under the new carpet due to settling.

5) Signs of leaking in the 20 year old roof in the attic. All signs were painted over and repaired inside the living areas.

The home inspector actually said “Lipstick on a pig” and recommended ripping out all of the beauty to fix it correctly.

My son backed out and is waiting due to our intervention.

It sounds like your house everything was in the open. Hopefully it was priced accordingly for the critical repairs required.

Beauties..

Looked at a house over a year ago where I found that the owner fitted a thin, crumbling concrete and gravel false front to the outside walls of the post and pier foundation to make it look like a poured foundation.. Also, no one could find the septic, it was so overgrown with trees..

The best one was where the previous tenants seemed to have poured cement down the toilet and the septic was all dug up and all plumbing lines disconnected at all of the drains. With serious water damage from everything draining onto the floors. But they all said the septic system worked!

The ONLY way “real estate tech” is a real business is if it either replaces human brokers en masse, or, failing that, it continues to erode commission rates and gradually disintermediates the brokers. No reason it can’t be done. Chuck Schwab did it 50 years ago with stock trading. Somebody needs to do it now with houses.

Agreed. The legal part of buying and selling houses could all be done online.

However, in normal times, most people want to see, smell, and touch the biggest investment of their lives. Some in-person interaction is needed.

I don’t want to see, smell or touch any stock investment. Well, except for gold and cash. I can’t roll around in bitcoin so I don’t invest in it.

Given that, in a hot market, RE agents make up to 6% commission (Split between buying and selling agent).

On a 1M house, is the 60K commission worth it when people are overbidding and buying within a day without seeing or inspecting the house in-person?

RE agents hit the lottery jackpot in the last year if they could match a buyer with a seller.

Agreed, but I don’t think they’ve come up with a solution yet.

Buying/selling houses is a lot more difficult than buying/selling shares of stocks. They are some of the biggest transactions most Americans will experience, are tricky because you have to navigate different players such as title, lender, inspector, buyer, and seller, and deal with unique goods.

The latter is a big issue. Cars are arguably an easier lift to eliminate some of the middle men but so far continues to be dominated by dealers rather than private transactions with tech handling the backoffice stuff. Zillow and Opendoor tried to replicate being basically the “Dealers” for housing, and their efforts failed or look to be circling the drain. I doubt there is enough capital out there to pioneer Home Dealers, and the automobile market seems to suggest that private party transactions will continue to be niche because the of risks and complexity to do the deal.

I totally agree. Real estate transactions are tricky and onerous. But think about this: Does a real estate transaction for 1 million USD home trickier than that for a $100K home ? The players/processes involved are more or less same in both the cases.

And the moral of the story of Wall Street is the IPO and VC and originak shareholders all walk away with cash while the poor retail suckers get screwed.

When arw theses cheap stocks cheap? When they hit ZERO!

0.75% is fair.

It’s very interesting that the Fed couldn’t care less about the dire need for affordable housing for young households when creating a second housing bubble this century while as soon as elderly on fixed income start complaining… they finally act.

Super interesting!

If the guys selling the shovels are losing their shirts, it’s probably looking grim for the speculators digging for gold.

I have yet to see a good media report on the status of the “institutional” real estate buyers — the companies supposedly buying a lot of the SFRs to rent out and/or flip. Unclear whether these players are private or publicly traded companies, so maybe they don’t have stock prices or reports to track.

But they’re the ones I’m interested in as they might be a good indication of future prices and are likely more rational re prices than individuals who won’t be willing to book a loss unless they are forced to do so because of income volatility.

American Homes 4 Rent and Invitation Homes are two public companies (REITs) in the rental market.

INVH just hit a 52 week low. Not sure of the reasons behind it (aside from the whole market taking a beating), although I expect that if home values take a hit, the book value of the company at least will come down.

I can’t recall but what happened in Feb 2021 that turned those stocks negative?

I have a theory. And I’m going to write about it shortly.

I tremendously respect Dave Ramsey and his advice to people working on getting out of debt.

However, his new RE business is going to fail terribly with honest advice like he just sent out:

“You’re ready to buy if…

1. You’re debt-free and have an emergency fund of 3-6 months’ worth of expenses saved. – Great!!

2. You’ve decided on a home price you can actually afford. – The payment needs to be no more than 25% of your take-home pay on a 15-year, fixed-rate mortgage.

3. You’ve saved a down payment. – For first-time homebuyers, I’m okay with a smaller down payment like 5-10%, but remember… anything less than 20% of the home’s price will mean you’ve got to add private mortgage insurance to your monthly payment. So, be prepared to add about $75 a month per every $100,000 you’re borrowing. (After buying, pay that down as quickly as you can to get that PMI off your monthly payment.)”

His #2 advice limits your PITI to 25% of your take home pay with a 15% mortgage. This is GREAT advice!

The first response on his post was:

“Median annual salary in the U.S: 50,000 that’s around 3,200 take home pay. 25% of that is 800.

According to this, Dave is telling the majority of Americans to have a 800/m mortgage on a 15 year loan.

That means with 20% down you’re looking for a unicorn. A 120,000 dollar house in a 348,000 average house price market. Good luck folks.”

Not a good business plan if his new RE agents are honestly following his recommendations.

Yeah. If you can stomach to listen to that show long enough you’ll realize Dave is kind of a con man. A jovial con man, maybe. His reply would probably make the caller feel like a bum for only earning 50k and tell him to look for another job. Save a bigger down payment and deliver pizzas, or something.

Jovial?

is that how one describes a self righteous ass?

One thing I am seeing less of is the in your face recruitment pitches from eXp real estate agents wanting to bring you in under them. Previously they would all talk up their great stock program being able to earn eXp stock. With the price well off its highs seems they rethunk their position.

Good news, thank you!

Finally, the 2 rural counties where I am are showing more houses coming onto the market than sold in the past month. On the first page of zillow for one of the counties 30% of the homes’ prices have been reduced, and the new ones on the market seem like their asking prices are reduced as well. Still way too high to be reasonable, but it’s a start.

I’m seeing some come on the market that I recognize that were bought within the past 2 years..

Late to posting on this one, so haven’t read all prior posts.

These companies aren’t “tech” and never were “disruptors” either. Traditional brokerages have online websites for real estate listings too you know.

As for data analytics, BlackKnight has access to the most data as the largest mortgage servicing provider and sells it, probably to these supposed “tech disruptors” too. They also consistently make money and have a 70% or so market share.

Me: I would like to buy a house.

Real estate tech: House? You must be mistaken, we sell dwelling-ready, asset class investment quarters. Our high velocity purchase journey powered by AI and Machine learning is right for you. We are the leader in J2H co-creative dwelling transactions.

Me: I’ll be back in 2 years…

So much for the efficient market theory …

That theory was dead on arrival

Today I got a letter from Opendoor. Here is what it said:

“See what we’d pay for your home in Los Angeles

1.Tell us about your home online

2.Get a competitive cash offer in minutes

3.Choose your own close date.”

Their stock price is down 71% from a year ago. I wonder how long they last?