Spent $20 billion more at gas stations, compared to a year ago, due to spiking prices; came out of hide of other retailers. Inflation eats everyone’s lunch.

By Wolf Richter for WOLF STREET.

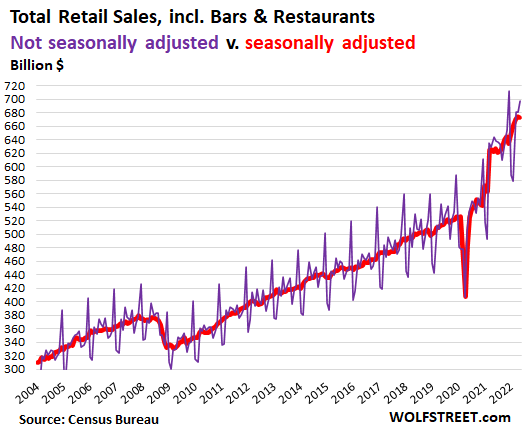

Retail sales in May, not seasonally adjusted, jumped to $698 billion, the second highest ever, behind only December’s shopping-season splurge, and up 8.2% from the stimulus-miracle bonanza a year ago.

On a seasonally adjusted basis, retail sales in May dipped by 0.3% from April, after having jumped in the prior four months by 07%, 1.2%, 1.7%, and 2.7% respectively, and were up 8.1% year-over-year, the Commerce Department reported today. The chart shows retail sales seasonally adjusted (red) and not seasonally adjusted (purple):

Retail covers only goods. Spending is shifting back to services.

These retail sales cover only sales of goods, not services. For months, consumers have been shifting their spending from goods back to services, particularly discretionary services, such as travels and elective medical treatments, where spending had collapsed during the pandemic. Spending on services is now surging. Services make up about 61% of total consumer spending.

Despite the shift back to services, consumers still spent a huge amount on goods, with year-over-year sales up 8.2% from the already sky-high levels last year.

But raging inflation is eating everyone’s lunch.

Price increases are inflating all sales numbers, but to varying degrees. Inflation in goods has been particularly bad, with prices having jumped by the double digits in many categories of goods. Each retailer struggles with their own cost increases, and they’re struggling to pass on those cost increases, as Walmart, Target, and other retailers have disclosed.

The price increases in goods vary to a large degree. The overall headline CPI inflation number of 8.6% simply does not apply. Here are the annual CPI inflation spikes for the biggest categories of goods, per the Bureau of Labor Statistics:

- Gasoline: +48.7%

- Food at home: +11.9%

- Food away from home: +7.4%

- New vehicles: 12.6%

- Used vehicles: 16.1%

- Auto parts & equipment: +15.3%

- Appliances: +6.4%

- Apparel: +5.0%

- Tools, hardware, outdoor equipment: +11.0%

- Furniture and bedding: +12.7%

- Housekeeping supplies: +9.2%

But CPI inflation declined for consumer electronics, which is an issue for Best Buy, other retailers that sell them, and ecommerce retailers:

- Consumer electronics and software: -7.1%

- Video and audio products, including TVs: -5.2%

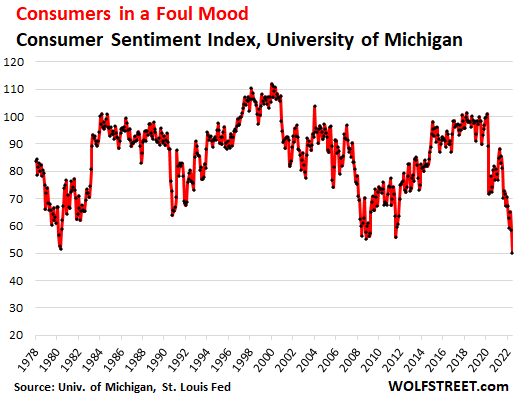

Consumers are in a Record Foul Mood.

While still spending hand-over-fist, consumers are hating the rampant price increases and are in the foulest mood ever, according to the University of Michigan Consumer Sentiment Survey (data via St. Louis Fed and University of Michigan Survey of Consumers):

Sales by category of retailer, not adjusted for raging inflation.

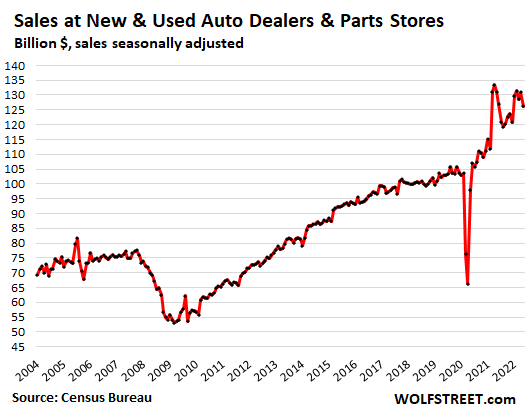

Sales at New and Used Vehicle and Parts Dealers, the largest category, fell by 3.5% in May from April, to $126 billion, seasonally adjusted, and were down 3.7% from a year ago, despite raging price increases, attesting to the volume challenges dealers face, with used vehicle deliveries down due to buyers’ resistance to sky-high prices, and new vehicle sales down due to vehicles shortages. The price increases can no longer cover up the decline in unit sales. Note the record stimulus-bonanza a year ago:

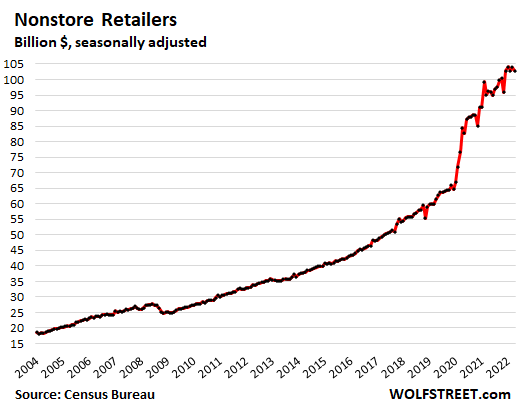

Sales at ecommerce and other “nonstore retailers,” the second largest category, fell 2.3% seasonally adjusted in May from April, to $103 billion, and were up 8.5% year-over-year. But a year ago was still the huge stimulus-bonanza. Compared to May 2019, ecommerce sales were up by 67%. This includes the ecommerce operations of classic brick-and-mortar retailers:

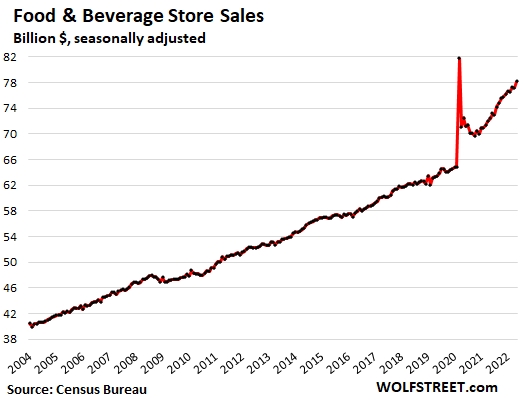

Food and Beverage Stores: Sales rose 1.2% for the month to $78 billion, seasonally adjusted, and were still up by 7.9% year-over-year, which is interesting given the double-digit jump in CPI inflation of “food at home,” which is what these retailers sell, and it shows that people are fighting back where they can, by switching to cheaper items or buying less:

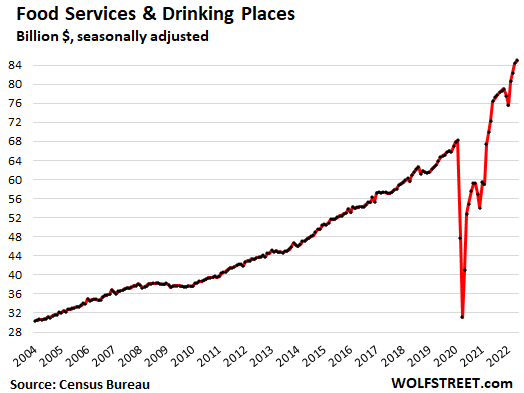

Food services and drinking places: Sales at bars, restaurants, cafes, cafeterias, etc. rose by 0.7% for the month seasonally adjusted, to a record $85 billion, up by 17.5% year-over-year. This year-over-year growth being over two times the annual CPI for “food away from home” (7.4%) suggests that people are going out and are having fun, despite their record foul mood:

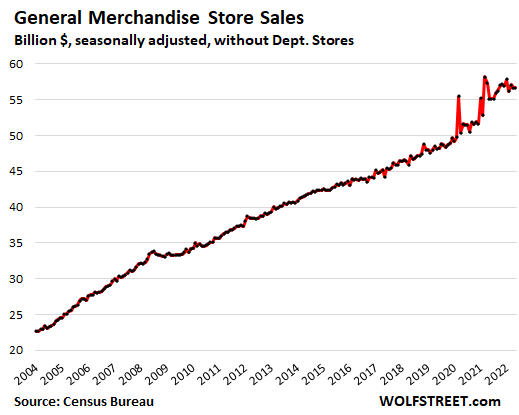

General merchandise stores: Sales were roughly flat for the third month in a row, at $57 billion, seasonally adjusted, and were up 2.8% from the stimulus-miracle bonanza last year. Walmart and Costco are in this category, but not department stores.

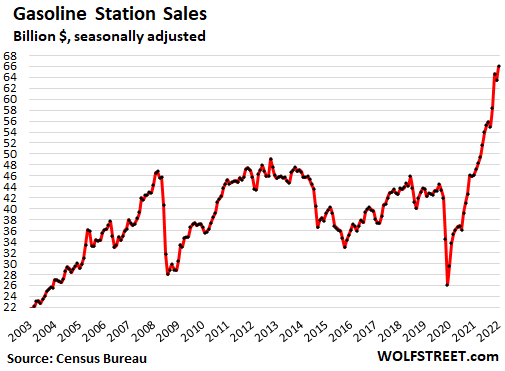

Gas stations: Sales jumped by 4.0% for the month, on spiking gasoline prices, to $66 billion, seasonally adjusted, and by 43% year-over-year. Consumers spent about $20 billion more at gas stations in May compared to May last year, and these $20 billion came out of the hide of other retailers.

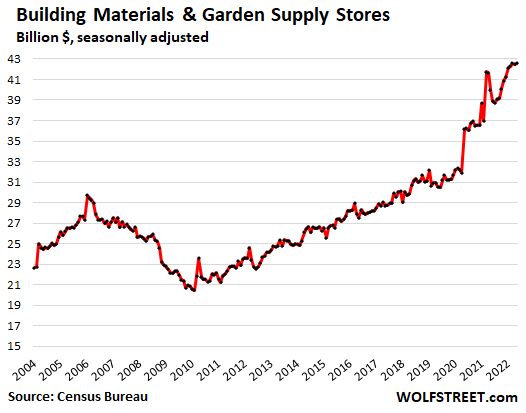

Building materials, garden supply and equipment stores: Sales inched up for the month and rose 6.4% from the stimulus bonanza last year, to $43 billion:

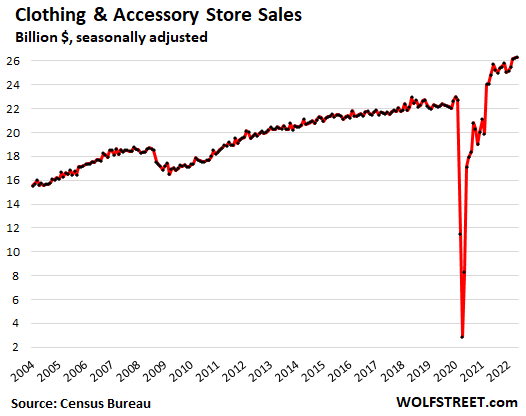

Clothing and accessory stores: Sales were roughly flat for the month and rose 6.1% year-over-year to $26 billion, seasonally adjusted:

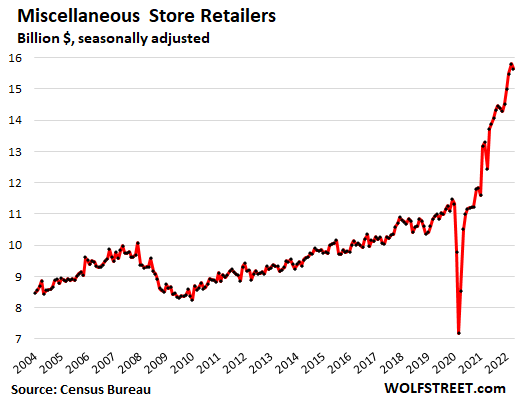

Miscellaneous store retailers (includes cannabis stores): Sales fell by 1.1% for the month to $15.6 billion, but were up 26% from a year ago. Compared to three years ago, sales were up 43%! This category tracks specialty stores, such as arts supplies stores, brewing supplies stores, and cannabis stores – now a hot category in brick-and-mortar retail:

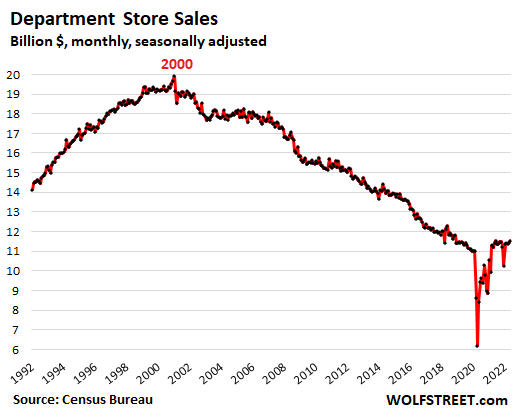

Department stores: sales rose 0.9% for the month, to $11.5 billion, but were up only 0.9% from a year ago. Compared to the peak in the year 2000, sales were down 42%, after thousands of stores closed, and numerous department store chains, from the smallest to the giant, were liquidated in bankruptcy courts. Macy’s too is still closing more stores in 2022.

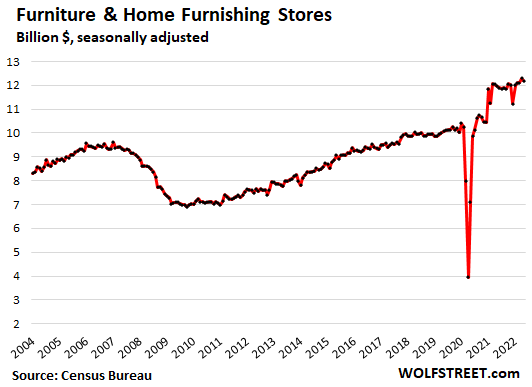

Furniture and home furnishing stores: Sales fell 0.9% for the month, to $12 billion, and were up only 1.9% year-over-year, despite rampant price increases:

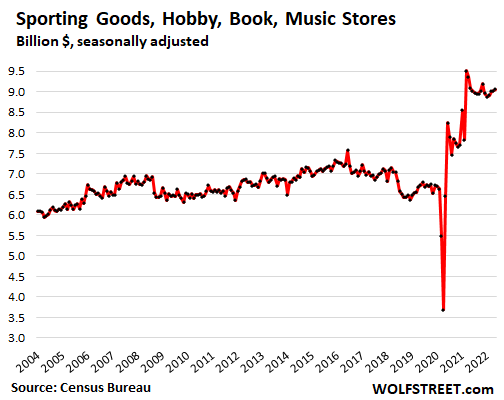

Sporting goods, hobby, book and music stores: Sales rose 0.4% for the month, to $9.1 billion, but were about flat year-over-year:

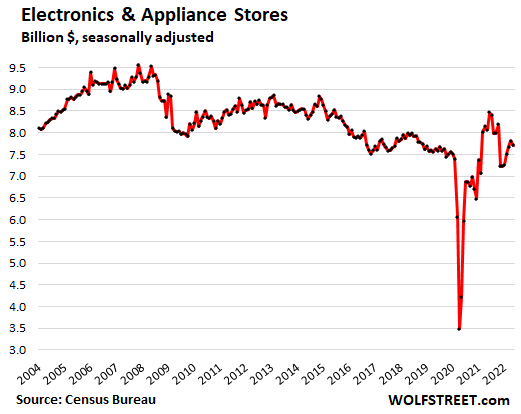

Electronics and appliance stores: Sales fell 1.3% for the month, to $7.7 billion, and were down 4.5% year-over-year. This segment covers only sales in specialty electronics and appliance stores, such as Best Buy or Apple stores, not the ecommerce sales, and not the sales at other retailers, such as Walmart and Home Depot, which are included above.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

American consumer will bop until they drop. Thats how the debt slaves roll.

there are lots of reasons behind this spending spree, but it is coming to an end. loss of home equity increases in the coming year will help to stop the spending. loss of job opportunities, declining bank balances. it will all come to a head over the coming years.

The convenience of electronic shopping increases consumption. Spending more time at home increases home purchases.

Things will get back down to normal in the not so distant future.

REAL INTEREST RATE = 1.75% – 8.6% = -6.85%.

* This is according to FED and BLS.

No wonder everyone is interested in borrowing as much possible to instantly replace their dollars with stuff that they really need!

Why blame only consumers, investors, big banks and big companies are doing the same. The Assets on their balance sheets will be highly questionable in a world with positive real rates.

Better yet producers can borrow cheaply and use the funds to hoard intermediate inputs to drive PPI higher. They can make substantial profits by simply buying and hoardng.

This is a solid reason why rates must go up much higher.

Where is the evidence that this increase is substantially or mostly for necessary stuff, whatever that is?

Given the behavior of so many Americans, there is definitely substantial unnecessary consumption in this data too.

The apparent retail sales spending spree has nothing to do with American consumers feeling more confident or wanting to buy more, it’s just a dumb artifact of the way consumer spending is calculated–based on total (dollar) sales and not on units sold–so if course the number will shoot way up with inflation, because Americans have to spend so much more to get bare essentials (such as gas and food), which Wolf’s charts demonstrate. If retail sales were calculated based on actual units sold, consumer spending would be way down. But of course more dollars are being spent because Americans have to pay so much more per gallon of gasoline and per gallon of milk. It’s another way inflation leads to sheer stupidity and confusion even in the basic economic measurements themselves, the media stupidly repeats “Americans are spending more! The economy must still be doing good!” when in reality, Americans are struggling and facing greater anxiety and desperation as their savings and real earnings dwindle faster, and they fall deeper into debt to get bare essentials. There really needs to be more effort to disconnect consumer spending from increased spending due to inflation costs, otherwise it’s just garbage in garbage out. The Fed at least is starting to ramp up anti-inflation moves, but its moves are still inadequate–it needs to go full Paul Volcker and bring interest rates way above inflation with moves between FOMC meetings, otherwise it’s the collapse of the USD, fall of confidence in US finances and literal blood in the streets, social unrest, rioting.

“…it’s just a dumb artifact of the way consumer spending is calculated–based on total (dollar) sales and not on units sold”

Unit sales are tracked for big-ticket items, such as houses, new vehicles, used vehicles, boats, RVs, motorcycles, etc. And I cover some of those, and if you ever paid attention, you would have seen them.

But unit sales make ZERO sense for tracking other retail sales, such as groceries, clothing, tools, etc. Thank God we have a “unit of account,” namely the dollar, that makes tracking sales at grocery stores, hardware stores, general merchandise stores, etc. possible.

“Unit of account” is one of the three fundamental roles of a currency. The other two are: “store of value” and “medium of exchange.”

Wolf,

You are right about using $ as unit of account, but you do have to be fair and admit it would be very, very useful to have easily accessible product unit sales volumes for a wide, wide array of physical products.

(Thank god nowadays we have quick volume stats for new home sales, used home sales, new autos and used autos – it wasn’t *that* long ago that only the pros had such key macro numbers and they cost a decent amount of money to get).

Without easily available volume unit sales for the rest of physical pdts, we all have to wander around in that rather large grayish area populated by CPI, PPI, inflators, deflators, etc.

I really don’t want the ethically conflicted (and competence impaired) G to be the primary/only source of inflation “adjustment factors”.

Miller,

I’ve had to spend a lot more this year to replace clothing. There are no bargains out there anymore and everything seems to have doubled in price. I have to spend more in order to replace items I need.

This is the year that everything had to be replaced, it just worked out that way. And yes, I do look nice.

Makes some sense to me. Much, if not most, of the current spike in these charts is due to inflation.

I analyze our company’s unit sales and dollar sales every month. Unit sales are running -25% below average, which we would normally consider a recession level, but dollars are on pace for a pretty solid year historically. The difference is all because the price of our products went up 30-40% in 18 months. By dollars, we are having the fourth-best year in the last since 2005 where my data set stops. By units, the fourth worst.

If retail sales are up by 8.2% and inflation is 8.6% then sales are actually down by 0.4% after adjusting for inflation. Imo the only metric that matters is inflation adjusted changes in retail sales. Everything else is smoke and mirrors.

That’s not how it works. Overall CPI (=8.6%) includes services. So if you look at sales at car dealers, with new and used vehicle CPI over 10%, you have to adjust their sales to their CPI. With car dealers, we track the number of vehicles delivered, and they plunged (prices too high for used, and no inventory to sell or the wrong inventory for new).

Not to worry, guys. That spike there at the end is just my girlfriend got a hold of my credit card again.

No. Americans purchased all the things that they will need, because they anticipate hyperinflation to begin or at least, much more inflation. The wealth sucking through the parasitic “Fed” continues and will continue.

For example, as to wealth sucking, if the Teamsters’ pension or Sri Lanka held $10 billion in deposits in US dollars in US banks for ten years, if the “Federal” Reserve ran inflation up to 7% a year and those banks paid 2% a year on those deposits, then during those years (ignoring compounding) it would have taken at least 50% (5% per year for 10 years) of those $10,000,000,000 away from the Teamsters’ pension or Sri Lanka: i.e., over $5,000,000,000.00 just via inflation, which I opine secretly ran far higher than 5% for years as reported in the alternate inflation charts using measures of the 1980s and 1980s in online sites.

That is the great, enormous theft and largest fraudulent scam in history that we have all suffered due to the “Federal” Reserve. All of us, of every group. People in Sri Lanka may soon starve right now, because the US banksters skimmed billions off their dollar holdings through inflation!

The banksters are from diverse groups of ultrarich, some of whom may not be crooked, but it still profit from the wealth sucking via the “Federal” Reserve and other corruption.

Hail the mighty American consumers, this is what 20-30+ years of buy at all cost consumerism conditioning will do and they will continue to keep buying until it’s 100% tapped out. Buyer’s strike? Not a chance…

Market must have saw these data and rally up now to over 400+pts even with .75 rate hike and Papa Powell talking tough trying to get people to think he is the next Vocklner, market knows, the good time will still keep on going cause you can always count on consumers to take out more debt to keep up those spending..

The first hike was 0.25%.

The second hike was 0.5% after being advertised at 0.25%.

The third hike was 0.75% after being advertised as 0.25%, then 0.5%.

Any best on what the third hike will be?

On the one hand – it seems like they’re doing a good job of weaning the markets off of “tiny” rate hikes. The market is now prepared to accept a 1% hike.

On the other hand – at some point, something’s gonna break down, inflation will fade out, and then there won’t be a need for more hikes. But this retail report doesn’t show a breakdown yet.

In the meantime – we had raging inflation. Now we’re approaching stagflation (no growth beyond inflation). Wolf is showing how the next step is a sort of “bi-flation” – inflation in things you need and have to pay for; deflation in things you want but can no longer afford…

When I listen to the next FOMC minutes, I am going to play Little Lies by Fleetwood Mac in my head over and over again..

Great way to keep yourself straight, hear a good tune AND stick to the “It’s the 70’s all over again” market vibe!

Meanwhile the younger generation will be playing a different breakup song, something like (so much for my…) “Happy Ending” by Avril Lavigne. At least until they have to cancel Spotify in order to cover the grocery & gas bills…

Most relevant song ? “Suffer The Little Children”

“Down in the heart of town

The devil dresses up

He keeps his nails clean

Did you think he’d be a boogey man ?”

OK – I’m going to take the bait.

This is an arithmetic progression.

And the next 4 hikes are therefore going to be:

1, 1.25, 1.5 and 1.75 meaning that we end this year with FFR of 7+%

The current Fed forward guidance is based on PCE trending down to 5.2 at the end of the year. So long as inflation and labor market continue to run hot (upside surprises), Fed will keep lifting their year-end PCE estimate and Fed will continue to lift forward guidance.

Keep dreaming ,fed can’t pay interest on debt over 4% tops. Then printing press = digital money flying everywhere

If the “printing” press goes “whrrr” again at the scale you are implying, the USD will tank in the FX markets. There is some latitude with the DXY at 105 since the all-time low is 70 but that’s all.

Those with the most influence aren’t going to trade “hard power” for fake paper “wealth”, even though they don’t care much if at all about the public.

Doing that is idiotic and it’s not going to happen voluntarily.

Flea – US gov’t can pay interest up to 4% for quite a while. The debt takes time to roll over, so the interest payments don’t rise instantly when rates do.

This is actually a strong argument for raising rates faster, to kill the inflation cancer swiftly and allow rates to come back down again before the elevated rates trigger a fiscal crisis.

Rates have already risen substantially in anticipation of rate increases, psychological. I have not seen a comment (yet), but I can infer that many are surprised market rates fell today.

No surprise – that smells a lot like a short-covering rally, based on the widespread sell-the-rumor/buy-the-news trade enabled by Timiraos at WSJ giving a heads-up about the 75bp hike following the adverse news of the past few days.

There would also be a fair number of traders wanting to get flat after the Fed meeting while waiting for the next “narrative trade” to emerge.

Everyone still believes real estate is an investment. They can cash on it with Helocs and Refinancing and then use the money to buy more stuff.

Meanwhile this house keeps gathering more mold, it never grows even when it eats up heating, cooling, water, maintenance, insurance, HOA, electricity…..

The sad truth: When housing goes down, everything goes down with it. If it remains this high, we start hyperinflating as labor productivity collapses and US becomes in-competitive in every field (not only manufacturing). So WE ARE BETWEEN A ROCK AND A HARD PLACE.

Anyone holding real estate in the United States had better like roller coasters… A death grip screaming vertical downhill.

LOL In so much words, Powell just said look at how the things have dropped without us even acting much yet (raising rates and QT) just by everyone knowing our intentions.

Basically saying their jawboning had a big effect. Is he alluding that they may not need to raise as much or do a lot of QT if jawboning keeps working?

I guess he is trying to pull a Greenspan irrational exuberance?

Also, someone asked if the FED is going to try to avoid a recession. I think Powell said we are not going to try to prevent a recession, we are trying to get inflation down to 2%?

He did say they have not control of commodity prices that effect inflation. He said they can target things they can effect is things that experience excess demand. So I guess that means they can target assets that are frothy. (Stock margin, Stocks, Housing, cryptos, ) What else?

Basically anything bought ‘on time’

When Trump was president if the price of oil got too high he got on the phone in the morning and by afternoon the bottom would fall out of the price of oil the same day. So we know they can control prices to some extent.

If they killed silver and crypto’s it would kill any net worth the teenagers have and bring them back into the workforce. That would push down inflation somewhat.

I don’t believe many teenagers (or anyone else) proportionally own silver, “paper” or physical. Certainly not material amounts.

Only “metal bugs” and coin collectors care about the price of silver. To everyone else, it’s just another commodity or asset to speculate on price changes to make fiat $ profits.

Silver. Who owns silver. LOL It is about the only commodity that has gone nowhere during the last 13 years of money printing.

I was almost thinking it is the only asset that has some appreciation left in it. But not right now.

As a collector, I don’t really care about the price of silver. Traded out of junk silver when it got profitable into numismatics, which are doing a lot better now. A Morgan with eight tail feathers or a VF 1909-S-vdb Lincoln penny is much cooler than a handful of slick old mercuries. My coin guy is selling lots of silver rounds to young people, who probably don’t understand what a fickle mistress precious metals in general and silver in particular can be. And she’s a sweetheart compared to the love interest of cryptocurrency “investors”, most of whom probably believed that the West Wing and Penthouse Forum was real too.

Gasoline ,diesel make price so high no one can afford it

If that tool really wants to be the next mini-Volcker…then go fast and go harder after the housing/rental market. Reverse wealth effect is a really good way to bring down inflation since rent equivalent is a big part of CPI. All we’re asking for is bring housing down by 40% in some of these insane markets and that barely bring it closer to wage fundamentals, not even asking for a fire sale pricing here.

Most people and I see this a lot at my work, don’t care day to day or month to month what the market is doing, other than seeing their 401k drop when they log in once every 6 month but they are still spending, planning trips, going to Hawaii..etc. If their house all of a sudden drop 40% in value, I am going to bet they will be less willing to go on spending spree. Outside of this, the other method of taming inflation such as sharp increase in unemployment will do the job pretty well too.

JP actually answered a question about housing price and mortgage rates in the end, and said young people should wait for now till housing resettle & rates are low again, which indicates he sees lower prices, but what did not make sense is that he thinks lower prices could coexist with lower rates!

I think housing Prices and Rates WILL both be lower, here’s how:

1) Interest rates surge due to inflation, crushing prices and sales.

2) Crushed housing and stock markets trigger recession, bringing high unemployment.

3) High unemployment and weak financial markets mean both more distressed sellers AND reduced demand for housing, since no one has money to buy anymore.

4) With inflation crushed, Fed lowers rates to re-stimulate the economy.

5) Prices are low and rates are low. Best time to buy, but…

…the bad news is that, when both prices and rates are low, it’s because few people can afford to buy, even at those prices and rates! So it’s quite the feat to be one of those few.

With a falling birthrate and an aging society falling interest rates are helping virtually no one and hurting virtually everyone. No wonder they have to give stimulus money to retirees. If interest rates were higher they wouldn’t need any stimulus money.

If the interest rate cycle turned in 2020, rates are ultimately going to “blow out” right past the 1981 high. What the FRB wants to do is irrelevant because they won’t control the outcome.

Their supposed god like powers are coincidental with the mania. If the credit mania is over, so is the illusion.

The basis of any central bank’s power is the currency. The fundamentals supporting currency stability have deteriorated dramatically since 1981, not just in the US but also elsewhere.

The free lunch for the country in the form of high and rising asset prices, cheap borrowing costs, and sub-basement level credit standards supporting what is predominantly actually garbage level credit quality (most debt now) are either over or approaching it.

Specifically for housing, mortgage rates have also been low due to mortgage guarantees, despite what are actually very low credit standards regardless that it’s better than housing bubble 1.

Government mortgage guarantees don’t magically eliminate or even reduce the actual risk of lending at bubble level prices to weak

borrowers. It’s another off balance sheet liability, one of many waiting to be triggered in multiple by some supposed “black swan” event. An accident waiting to happen similar to the numerous security commitments from imperial overreach which many in leadership seemingly view as “free”.

Falling rents would get many of the homeless off the streets so they have a vested interest in bringing down home prices.

Yeah, fed heads prefer to use their mouth to make things go up.

“ Yeah, fed heads prefer to use their mouth to make things go up”

Here’s something you can’t make go up because they already are….

$50 fuel surcharge on my electric bill…

That’s $50 that will not get spent elsewhere in the economy any way, shape or form…

I don’t think the full effect of energy has affected the numbers yet…

Won’t be long and many retailers are going to be in trouble at the corner of Dismal and Sucks…

Macys was having a pretty good sale and I thought about ordering some new shirts because some of mine have shrunken mysteriously in the closet…

Because of my electric bill, I declined to participate…

My energy bill for last week is $4.31. Admittedly I live in a pretty nice (on the hot side) climate. I learned to just live, paleo style (have not used any climate control tech in 20 years), and not constantly grow more dependent, including, psychologically, on all this. I feel casual and just ducky right now. Blankets still keep me warm, and when hot, letting in night air before sunrise, keeps me cool.

… and I live 5 miles from aging Mom, so I can help her. I live 2 blocks from the food store. 5 blocks from health care. 1/2 block from forested park. Americans are such poor planners! They make hostages of themselves to such stupid things. They overextend their supply lines like Napoleon and H!tler and wonder why they are defeated.

I was always a minimalist but now I’m a tactical xonsumer.

My hobby is taking complete advantage of Amazon’s return policies. Instead of searching through reviews I just buy all of em. Every different one, try it out and return all except one. I only use Prime when they offer it for a free month.

The hubris of bezos the space cowboy thanking his customers for his Shatner rocket ride pushed me over the line. I hope every interaction I have with amazon costs them.

I don’t like Bezos either, but this is stupid. Amazon makes the manufacturers eat the cost of returns, so your scheme only hurts them, not Amazon.

Remember those good old days? Feels like decades ago but 2 short years later, the guy sure can pivot with the best of it. What’s the point of even saying anything or telegraph messages in FOMC if everything is so been consistently wrong…

“Powell says Fed ‘not even thinking about thinking’ about rate hikes”

Among the central bank’s first economic predictions this year, officials also said the core inflation index will fall l per cent this year and remain below the Fed’s 2 per cent target in 2022.

Completely off topic:

2000 6.5% FFR with 3.4% inflation

2006 5.25% FFR with 2.5% inflation

2022 1.75% FFR with at least 8.6% inflation

My goodness. The enormity of how far behind the Fed is just breathtaking.

Don Lemon interviewed Larry Summers yesterday with a general conversation about the FFR. But at no point did Lemon try to pin Larry down to how high her things the FFR will have to be moved to in order to tame inflation. This isn’t so much of a critique of Lemon but journalist, in general. Get people on record, so we know down the road how smart of clueless these people really are. Like an economist said yesterday, the Fed should shotgun the FFR to 3% today. And even that’s still way behind the curve for where we are in this cycle.

Oh, my bad! The national debt has grown by $25T, so we can’t afford short-term bond yields like the 3YT at or above 5% like it was before 2004. The Fed has to constantly suppress rates, so we can afford the interest expense on our national debt.

Depressing, but vital and true. A portrait of decadence, of something for nothing, which turns out to be for a LOT of something payable by all! appreciate it!

In the end times, people will be carrying on as normal….. eating, drinking, getting married and then…….phurwatt……they don’t

I liked the phurwatt.

I could just see a massive horizon of phurwatt sweeping all before it.

The American public trying really hard to keep the inflation going, I don’t see how inflation could abate while many tapping into their savings and just started to reuse their credit cards on discretionary services like traveling and dinning out like there is no tomorrow.

You will see inflation abate. There is real economic hardship coming, and that will create demand destruction. Look at the drop in mortgage apps. in the past 30 days and what theoretically that is going to do to the construction industry over the next 6 mos. Where I live, almost 40% of all new jobs over the past 5 years are construction related.

Well, it’s not coming fast enough. We have been experiencing this inflation for a year, any reasonable person would have changed plans and reduced spending by now. People complain but never act until forced to.

At least 80 years with some blips in between

The idea with inflation is to buy before prices go even higher. Forward demand isn’t easy to kill when the public has figured out what to do in inflationary times.

Jdog-

I suspect we will see once in a lifetime demand destruction rapidity and magnitude.

Extinction burst.

It will be interesting to see how related statistics are affected:

– Savings rate

– Household debt

– Loan delinquencies

– Foreclosures

– HELOCs

So on and so forth.

You’d think that with skyrocketing rents, house prices, vehicle prices, and everything else, people wouldn’t have that much extra cash to burn, but one must never underestimate the financial irresponsibility of the intrepid American shopaholic.

People might be spending like there’s no tomorrow because they expect that someday soon there won’t be a tomorrow, but it’s probably just the endorphins. Marketing guys know that Americans will spend too much on stuff they don’t need because it will make them feel good for sixty seconds, down from ninety before The Plague. This tends to explain why US second hand stores have designer stuff on the racks that still have the original price tags that were never removed.

Debt is certainly going to get more expensive but some important rates are too low anyway. The Fed’s .75 hike was higher than many anticipated but still within the range of expectations. This summer may not be as economically exciting as one might otherwise suppose.

How is everybody’s false sense of security holding up? Pretty good so far?

unamused,

I’m expecting to see HELOCs rise again, after plunging for over a decade, as people shy away from cash-out refis at these mortgage rates. It’s better to have 6.5% on a $50,000 HELOC plus maintain the 3.5% mortgage on $450K, than a 6% rate on the entire $500K mortgage after the cash-out refi.

If I’m right, we should see the first real uptick in over a decade in HELOCs when the Q2 data comes out in two months. I’ll report on it for sure as part of my big consumer credit report. Here was the one for Q1, including HELOCs:

https://wolfstreet.com/2022/05/10/consumers-can-handle-fed-tightening-update-on-consumer-credit-delinquencies-foreclosures-collections-and-bankruptcies/

The $64K question, if there’s a rise of HELOCs, will it help burst the housing bubble faster and harder? If it plays out like 08, maybe the sign is pointing to a yes?

Up in Canada where HELOC’s are maxed out with falling home prices the maximum amounts will fall as the banks will lend on the value of the home and when it falls so does the maximum amount of a HELOC. This is happening right now in Canada.

Mr Richter;

I think that your expectations regarding HELOC Renaissance will not come to fruition – UNLESS… ( see my suggestion at the end)

It is not for lack of demand that HELOC is plunging.Demand for Free Sh…t (handouts, stimuli, loans & mortgages which will never be repaid) is stronger than ever.

But…

Big banks may or may not be evil but they are definitely not stupid.

“Wells Fargo will no longer accept applications for home equity lines of credit”

CNBC, APR 30 2020

My BofA stopped HELOC BS too.

Also when I walked past one Citibank branch in Chicago (Kenwood area) I saw “No more HELOC for you a$$holes” notice.

Fed should step in ASAP & start taking toxic HELOC loans off the bank balances ! Just like toxic mortgages ! Because people are struggling ! And repaying HELOC loans & mortgages is bad for the economy – it cuts spending !

Brent,

Nooh. Wells Fargo got out of this line of business because the demand for HELOCs collapsed, as did other banks, and it wasn’t worth going after the shrinking little corner for a big company.

Wow Wolf. Mark Hansen the past two years has been talking about HELOCs being untapped too and when rates go up, he was suggesting the same strategy would happen. He thinks all the banks will start flooding home equity rich people with these type of offers to generate fees to make up for the loss of refinancing income.

Guess what. A relator friend of mine, told me he wanted to sell his McMansion a few months ago at this current peak, take the equity gains, then rent for awhile until housing drops told me the following.

His wife would not let him sell because she does not want to live in an apartment. So he said exactly what you said.

He refinanced his mortgage last year and has a 20 year loan at 2.18%. He told me he wants to take out a HELOC to tap into the equity to pay for their kids college tuition. He wants to lock in the HELOC as he was thinking rates are going higher. When he told me this a few weeks ago, he could still get a HELOC at 5.5%. Maybe not now.

I just went to the Bank of America site and they are offing 5.15% for HELOCs while a 30 year mortgage is about 6%.

When I read Marks blog post a year ago, He was saying untapped home equity was at $22 trillion, which is up for the $11 trillion peak of HB1.

But that was a year ago and I think HE is now close to $24 trillion. Of course, it will fall as house prices fall.

He might be too bullish on his HELOC withdraw theory because at the time, he said it would lead to consumer buying binge.

They are spending like it is yesterday and this can be seen in savings rates and credit card balances.

Demand destruction is occurring alongside this as a function of bringing so much demand forward with the Godzillion dollar forced health scare money blizard that failed to cure our dysfunctional medical services wealth extraction system cartel.

Note that Wolf wrote:

“On a seasonally adjusted basis, retail sales in May dipped by 0.3% from April,…”

Note also that as Wolf shows, the YoY increase is about at the rate of inflation, so people really aren’t buying more, they’re just paying more for about the same amount of goods and services.

As I pointed out in the article, the overall CPI inflation rate of 8.6% doesn’t apply to retail sales because it includes services and housing, which still run lower, but which are not sold by retailers. Retailers only sell goods.

I listed the CPI rates for the major goods categories that retailers sell, such as new vehicles CPI, used vehicles CPI, food at home CPI, tools CPI, etc. and you can match those up with the individual retailer categories that are depicted with numbers and charts.

Mr. Richter do you see any future demand destruction in gasoline? $20 billion gasoline sales increase year over year is significant.

We’re already seeing some of it, not much, but some. This is inevitable. I should post an update on it.

For the past few weeks, I have been wanting to say that you have the best vocabulary on the internet. Nothing takes the edge off pain like a good giggle. Thank you.

Wonder what percentage of the disgusted consumers have mortgages under 3 percent?

What little more they pay at the store they are likely getting back in less debt burden.

Also, how are GDP and employment ratios doing these days?

That is the other five halfs of the story …!

Regardless of the rate people may have, they still committed to pay a certain percentage of their income. So, perhaps, they got a larger house than they would have purchased with higher rates. They still have to pay the mortgage along with higher carrying costs of a larger home.

So, I’m not convinced that they truly have less debt burden. Nor do I believe they are only paying a “little more” at the grocery.

There is a delay effect, talked to a local farmer who told me he spent $600 in one day on his tractor, he’s still trying to get is head around a future where that is the norm, his big tractor will burn 3k a day, if is the new norm then it won’t look anything like this.

Yeah headline inflation isn’t going down anytime soon. It may hover around this level but that becomes more of a problem when it is staying the same on top of last year’s higher inflation (compounding). The inflation rate was already 5.4 % last year around this time right, so when you add 8.6 % to the gains from last year of 5.4 % these two years don’t look awesome. When you start adding 8.6% or the like to December 2021’s 7% inflation then things get even more interesting for the economy. Even going down slightly, the pain from inflation increases as we meet that rise from last year. And I don’t actually think it will go down with this dovish Fed for a long time.

So, 500 “+” home calls with 50 questions in the contiguous US with the 100 “reference” set at the results in 1966? About the start of when outsourcing and Japanese engineering beat the living shit out of everything our Corporations produced, except marketing/financing BS.

SO WHY are the advertising PROS going after max data on each and every individual who has a cable TV and at least a cell phone to get on the internet, plus all his other corporate connections like credit card, bank, online buying, stores, etc, etc, and are competing like crazy for even more in depth individual data? Im sure they could produce a much better “consumer survey”, based on whats DONE, not anyone who will stay on the line to answer 50 questions (who would do that?) Not me, I’m not that bored.

I don’t doubt major changes picked up from this survey, but it AT LEAST ought to be split along the lines of Wolfs Wealth Inequality charts.

Most of those toward the bottom lose their assets, those at the top will buy them. Rinse and repeat. (Still say 1980 was the biggest in all our lifetimes.)

Public stocks are probably not long for this world. (except maybe for scams noted here, and enough other shit to make an “index”) All my wealthy relatives are in PE run “means of production” like FOOD, the managers of which answer to no one and don’t worry about “liquidity” problems from withdrawals….there aren’t any allowed (except maybe after a “sit down”) even with a typical min $500K-M buy in or more.

And there is a whole ‘System” for the hiding of profits. Naturally most have Charitable Funds, with Missionary “work” being the most popular in the bunch I’m related to, or knew as a kid.

NBay,

Good lordie. What the heck are you talking about? What a crock. Retail sales are NOT based on a consumer survey. This is data from RETAIL BUSINESSES by retailer category. This is based on BUSINESS REVENUES. That’s why it’s called “retail SALES.” You know, SALES!!! What a business sells.

By the way, no (and I mean zero) government survey operates the way you imagine. You’re describing a silly internet survey. Government surveys are HUGE. If they go to businesses, like retail sales, they go to tens of thousands of business locations; if they go to consumers, they go to hundreds of thousands of households.

Wolf. I’m trying to buy “big like” on Amazon or eBay. I can’t find it anywhere. Is it still for sale if so where? I see the electronic version but I’d like the physical version. Any plans to put it to a script for the big screen? Sounds like fun

Ivan,

Thanks. It’s still there on Amazon, ebook and paperback:

https://www.amazon.com/gp/product/B00613TA56

FYI the Canadian employment survey monthly surveys 54,000 households (determines jobs added/lost and unemployment rate).

Statistics theory says that should be ok for a population of close to 40 million, but in reality the numbers bounce way too much month to month to be “real”.

Sheesh! All I was talking about was that Michigan Consumer Sentiment Survey which I have had a beef with for a long time. I don’t doubt the other data being the the best available. Why do you think I come to this website knowing nothing about economics at all? (Except what I learn here, and sure I like to see my 2 cents in print like anyone else who posts)

RTFComment;) On second thought, I just noticed I didn’t state what I was referring to at the very start. My bad, won’t be the first nor the last. Hope it makes some sense in that context.

3rd thought on “RTFComment”. It’s all too easy to forget the MASSIVE amount of shit you must have to sort through and the speed you have to be able to do it….my bad again…..sorry.

So basically people are paying a lot more and getting a lot less for their money. Hope you enjoyed your stimmy ck. You are now paying for it, and will continue to do so going forward. No such thing as free money.

Didn’t “enjoy” stimmy checks but it sure WAS at a good time. Dentist and endodontists got it all.

1) Total retail sales, a lower high. Eleven lines from 2020 low to Oct/ Nov

2020 high, whatever. Eleven line from Jan 2021 low to the top. The main target was reached.

2) The good news : Motor vehicles and online sales are down. F-150 in accumulation. Diesel crush the farmers.

3) JP : if Unemployment reach 4.0% – 4.2% it will normalized.

4) SPX might close June 10/13 gap by Fri and June 9/10 gap by next week, because JP released RRP liquidity to the market, while hiking by 0.75%.

5) RRP is a valve to regulate the economy. It also provide good collateral

for the o/n market. Fred : SOFER is 0774%, from 6/15 7AM. No panic.

6) The Fed fight inflation two ways : 1) by raising rates moderately. 2) by sucking a lot of liquidity from the market. Fo year and a half the Fed accumulated $2.2T RRP, sucking total $3.5T from the banks.

7) Consumers confidence is the lowest since 1974/75, since ARAMCO. After falling 33%from Nov 22 2021 top, NDX might turn around.

8) Madam ECB might imitate JP. Higher European rates might weaken the dollar for a while, until we enter recession.

Inflation, daily : down from 8.5% to 8.3%, that’s what the chart says.

The bottom line is if the real or true inflation rate is 12 percent and the average wage gain is 6 percent the average worker is losing 6 percent a year. At least back in the late 1970’s they told you the real inflation rate not some cockamamie conjured up rate.

It’s so interesting, and incredibly tragic, how a handful of private citizens (the Fed private banking cartel), created a few decades ago, completely call the shots on the US economy and the ~340M US citizens.

Lives are ruled; generations are ruled. The bleating is off the charts.

Be that as it may, the dog is wagging the tail now. The Fed is so in control. Can anyone quantify $4tn? No, no you can’t.

No one knows the consequences. We only know they are, and will be, wild! Good luck everyone.

> The Fed is so in control.

A whole different nightmare is if it slides out of their control. Not something to be wished for either. Then the remedies get really drastic, somebody going overboard, more somebodies, way more than now.

Now that we are talking trillions, one trillion is a million millions.

“To find how long it would take to count to a trillion dollars divide 1 trillion by 31,536,000. That is 1,000,000,000,000/31,536,000 = 31,709.79 years” ~the internet.

So if you had your chauffeur drive you continuously around the US in your EV and you threw a $100 dollar bill out the window every second it would take 317 years to throw a trillion out the window. Plus charging time.

For sake of comparison the amount of money sent to Ukraine recently worked out to $90K per homeless person in the USA by my calculations.

LOL. Interesting. That would be, what, $8,640,000 out the window each 24 hours, right? (My math is notoriously poor)

Well, if you weren’t stupid (and assuming you got that trillion for yourself somehow, you’re probably not), if you kept, say, $999 Billion in a 2 month t-bills earning 1.56% interest while you rode in style? Even after paying 33.3% max capital gains Fed/State taxes in California (where all Trillionaires live, don’t you know), you’d have more money every single day than you did at the start of your throwfest.

But the arms…they would get tired, no?

Along that line, saw Snoop Dogg paid a guy around $40K/year just to roll his dope, and even gave him an inflation raise. All publicity, but helped someone out. Like a lot of celebrities, he’s doing commercials now for extra money. South Park had fun with Matt Damon’s electronic coin commercial.

How come 0.75% increase today suddenly let the investors become bullish after the announcement? It has happened last time as well when the FED hiked the rates by 0.50%.

Cause the market is insane….trying to predict what the market will do under normal logic or rationalization is and has been an exercise of futility in the last 2 decades in the ever so easy monetary environment. Unfortunately even in a tightening environment, that programming is so entrenched it will take a while to reverse course..

Either that or PPT finally wok their A$$ up from a drunken slumber and did their job last min

Because the Fed didn’t lift forward guidance more.

They didn’t threaten 75bp next time or at next few meetings after that as market had feared.

So long as inflation and labor market continue to run hot, this will be a temporary reprieve only.

You are right but you kind of have to ask how stupid is the market if they still believe in what the FED is trying to telegraph, pretty much everything they telegraphed beforehand in the last 2 years have been wrong wrong and wrong or just straight up opposite.

Maybe the market should watch more Seinfeld and copy what Constanza did in that one episode, act complete opposite of what they said. So if Powell is now saying they are not considering 1% next time, expect 1%…in that case, it makes no sense to rally off this but stupid begets stupid…

Powell did threaten 75 basis points at next meeting.

Short squeeze. Market always tends to go up on the day of FOMC meetings.

And because the Federal Reserve always announces its decision in advance (this one was leaked to financial media early), there is a relief rally.

Market tanked the day after the May meeting.

Coming down from 1507 (IIRC) there were a lot of S&P (the main one I watch) 4% plus days..maybe 5%, too..still haven’t seen one, but getting closer to them.

CNBC folks were losing it and going off script….they looked very scared.

Also remember a very panicked Cramer “calculated” it CAN’T go under 500…..guess maybe that was based on corporate raider skills learned at the GS Financial/Political/Legal Pirate Finishing School.

Did see that Garmin guy stick his neck out and call the bottom within 3 days, though…..maybe just an insider thing, as everyone knows there is no such thing as a “free market”….any market will be dominated by the largest player(s)…..that’s without nasty “government interference”.

The Fed said last time they would not raise 75 bps, but they just did today. The lack of forward guidance is actually negative for the market, because next month it will be 100 bps.

Short term market gyrations are to be ignored.

Bull&Bear,

We had a MUCH bigger sucker rally after the May 4 Fed meeting. During the last 90 minutes of trading on May 4, stocks spiked by around 3% amid panic-buying by speculators trying to cover their short positions. It was a vicious sucker rally. The next day, the S&P 500 plunged 3.6%.

Some where in this mess is a black swan / overleveraged bank,hedge fund ,or bond market could blow up , this is a global problem might take everything down = RESET . Besides we’re probably going to global digital money ,you will be controlled

I am at least looking for some eye-catching financial scandals, when firms are exposed by anything-like-reasonable interest rates. New Madoffs, new Enrons.

JP : the short duration is negative : 1.74% minus 8.3%, but the long

duration almost normalized.

So the bond market shows some confidence this will work out, right? The lesson for me is, have enough acorns to survive to that day.

After failing for 5 weeks to close < May 9 low, Boeing F-15 is

taking off. BA is up 9.5% today, closing June 10/13 and June 9/10 gaps

in Mach 2.

It’s quite amazing to see how much Boeing has gotten beat up from their highs back in 2021, if you squirt a little, their decline down from the 2021 mania have you mistaken them for Zillow or Redfin..

In the first line million should be billion?

Yes, thanks.

Spent some quality time at Lowes this weekend shopping for home-related stuff. All the nearby retail stores were absolutely packed. Consumer discretionary spending still looking strong in my neck of the woods. Stock/bond massacre aside, it will probably take a major hit to the job market before a more precipitous drop-off in consumer spending takes place. Personally I will be laying off the lawn seed and fertilizer this year as prices are just disturbing right now…

I think Powell said sentiment was low because people are complaining about gas prices but the economy is still doing well as people are still spending.

Well, my rents just keep on rolling in every month and the buildings keep going up in value.

So I respectfully disagree.

I am going to keep repeating it.

Everyone has to live somewhere.

No one is making anymore real estate.

When you have raging inflation in interest rates, labor, and materials new construction grinds to a halt. That restricts supply. More people every year means more demand. The only real threat to RE [in the long run] is too much government control.

People make new real estate, defined as dwellings, every single day. WTFUTABW? Look into the amount of vacant homes in the US. 19 million, I did it for you.

If you are an old geezer WTFUTABW

Means what the F you talking about Willis?

Sorry, always ask the same.

What about health and private education?

Can middle class obtain the same level of education?

Can the middle class have a good level of health cover?

For me the two subjets are the main way for makd a country

MUPPETS signing their own death warrants.

100 bps increase coming next month.

You guys are celebrating way too early. When this Elliott Wave 4 down completes soon, and then the S&P takes off to 5000 by next year, you’ll climb back into your shells. There will be the big collapse, but it’s probably still a couple of years away. It’ll begin right after the headlines start to read “Coast is clear, inflation scare is mostly behind us, etc.”

Market tips end with maximum optimism. Not there yet.

“Market tops”, not tips

So you are 100% long….. even using margin, right? LOL

Today’s update to Atlanta Fed GDPNow forecast for Q2: 0% growth, as in zero. None. Maybe 1Q wasn’t just one-timey stuff after all. Uh oh.

We have 8.6% inflation and zero growth. What’s that called, class?

I would track container loads, reefer loads, and van loads truck and rail and also average cost to ship instead of unit sales.

We do that right here. But that doesn’t give you retail sales. It’s like tracking tonnage. It shows nothing about value. There is a huge difference to the economy and retailers between shipping a ton of iPhones and shipping a ton of coal.

Wolf, wonder if these charts were NOT based on highly inflated sales dollars, but on actual volumes of products sold.

2021 Widgets at $3.10 each at 10,000 volume = $31,000 “sales”.

2022 Widgets now at $5.19 each at 8,000 volume = $41,520 “sales”.

Volume? Not such good news. Widget plant to announce layoffs.

RTGDFA

Where did they think all those reckless Fed trillions and ZIRP and stimmies were going to come from? Manna from heaven? The government can only move wealth around, it can’t create it. Everything it spends gets paid for one way or another. With interest …