You can see why some retailer stocks are not liking the shift from goods back to services.

By Wolf Richter for WOLF STREET.

Americans outspent inflation by a good margin in April. “Real” spending on goods – what consumers buy at retailers, adjusted for inflation – rose for the month but was down from the stimulus-miracle peak last year. “Real” spending on services (such as healthcare, travel, entertainment, etc., adjusted for inflation) jumped, after having collapsed during the pandemic, as the shift in spending from goods back to services continues in a sign that the distorted stimulus-economy is normalizing. Services spending is the biggie, accounting for over 60% of total consumer spending.

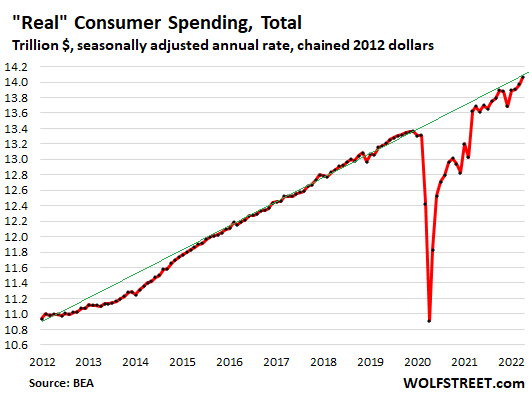

“Real” spending rose, approaching pre-pandemic trend.

Inflation adjusted spending on goods and services jumped 0.7% in April from March, to a new record, and was up 2.8% from stimulus-miracle April last year, according to the Bureau of Economic Analysis today. It is now approaching the pre-pandemic trend, as the consumer economy is normalizing at pre-pandemic growth rates, all adjusted for inflation:

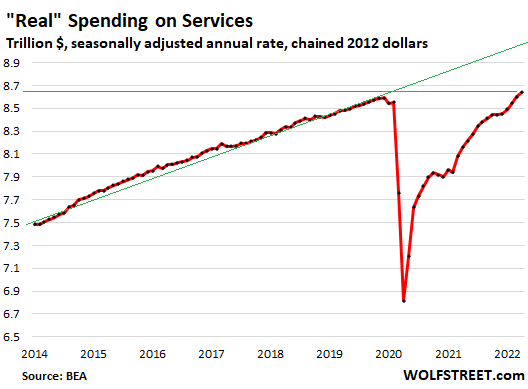

“Real” spending on services jumped, but long way to go.

Inflation-adjusted spending on services – healthcare, housing, education, air fares, lodging, rental cars, entertainment and sports events, haircuts, repairs, etc. – jumped by 0.5% in April from March, and by 5.9% year-over-year.

Real spending on services finally surpassed the levels from before the pandemic and set a new record, after the collapse of spending on discretionary services during the pandemic (such as airfares, discretionary healthcare services, such as dentists and elective surgery, haircuts, etc). It remains far below the pre-pandemic trend (green line), but is on the way to normalizing, as spending shifts from goods back to services.

This sharp increase in “real” spending on services in recent months (+5.9% year-over-year) is what has been driving consumer spending, even as spending on goods has fallen from the stimulus-fueled peaks a year ago.

Spending on services matters: In April, it accounted for 61.4% of total consumer spending, but is still down from the pre-pandemic average of over 64%. This is an indication that spending on services, as it normalizes, will continue to grow at a disproportionate pace (so watch out for services CPI inflation, which is starting to eat everyone’s lunch).

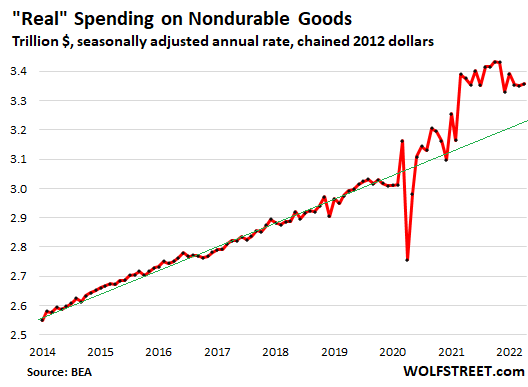

Real spending on nondurable goods slowly normalizing, at nosebleed levels.

Inflation-adjusted spending on nondurable goods – dominated by food, fuel, and household supplies – edged up by 0.2% for the month but was down 0.5% from the stimulus-miracle spike in April a year ago.

Even after the year-over-year decline, consumer spending on nondurable goods remains at nosebleed levels, up by 12% from April 2019, and well above the pre-pandemic trend (green line). But it is on track to gradually normalize and revert to pre-pandemic trend:

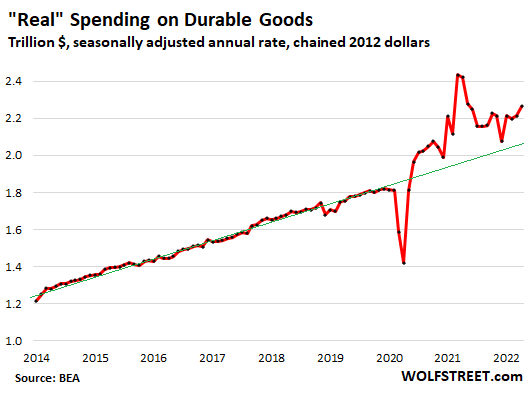

Real spending on durable goods suddenly jumps month-to-month.

So, just to dish up another surprise about the “tapped-out” or whatever American consumers, inflation-adjusted spending on durable goods jumped by 2.3% for the month, just when you thought that consumers had bought all they stuff they needed, and were going to back off.

Compared to the stimulus-miracle spike in April last year, real spending on durables was down 6.5%. Spending remains at nosebleed levels, up 29% from April 2019, and continues to contribute to the shortages and price spikes of some of these goods, and to the massive trade deficit as many of these goods are either made in other countries or contain components that are made in other countries.

But you can see the uneven normalization, the regression toward the pre-pandemic mean:

“Real” income below pre-pandemic trend.

Inflation-adjusted personal income from all sources fell 3.5% from April a year ago, when the stimulus money was still arriving, but ticked up a tad from March (purple). This includes income from wages and salaries, dividends, interest, rentals, farms, businesses, and government transfer payments (stimulus, Social Security, unemployment, welfare, etc.), but does not include capital gains. Late last year, as inflation was surging, real income fell below the pre-pandemic trend and has stayed there. It’s up just 6.0% from April 2019.

Inflation-adjusted income without transfer payments rose by 2.0% from a year ago, and by 0.3% in April from March (red line). It fell below pre-pandemic trend at the beginning of the pandemic. After a partial recovery, it lost more ground since late last year due to the surge in inflation and has remained essentially flat since November.

![]()

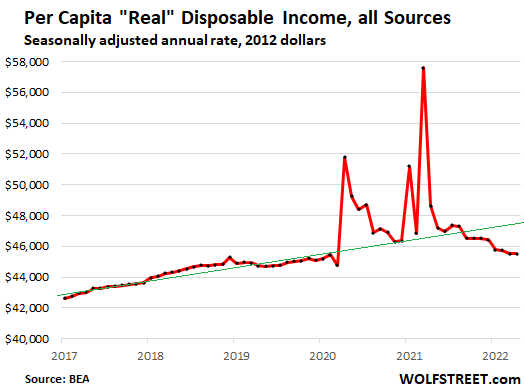

“Real” per-capita disposable income looks worse.

The above income data was for aggregate income, for all consumers combined, where income growth is also fueled by rising employment and population growth.

Here is the per-capita level of “real” disposable income – meaning per-person after-tax income from all sources, which was flat for the month and down 6.4% from a year ago, and up just a tiny minuscule 1.8% from April 2019. And it’s deeply below pre-pandemic trends:

The substantial increase in inflation-adjusted spending and the morose situation of inflation-adjusted income (which does not include capital gains) show that consumers – not all but enough to move the needle – are still flush with money from the gazillion stimulus programs and with money they can extract from the surge in the prices of real estate, stocks, and cryptos, where consumers made in aggregate trillions of dollars, some of which they already spent, and some of which have vanished in recent sell-offs, and some of which they still sit on and will continue to spend.

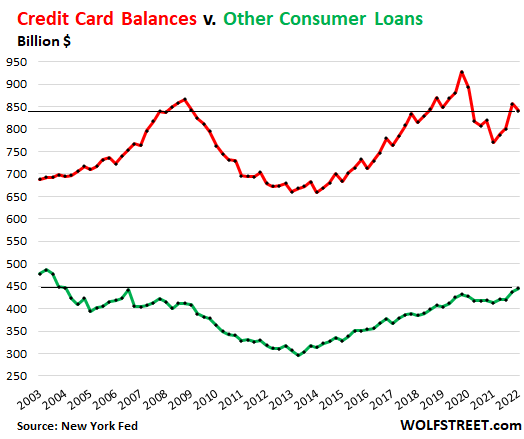

But consumer borrowing to spend, well… not so hot.

Not adjusted for inflation: Credit card balances, excluding other revolving loans such as personal loans, dipped to $840 billion in Q1, from Q4, still below Q1 2020 and Q1 2019, and back where they’d been in Q1 2008, despite 13 years of population growth and 37% CPI inflation (red line).

Other consumer loans, such as personal loans and payday loans, at $450 billion, were also below the highs before the Financial Crisis, despite 13 years of population growth and 37% CPI inflation (green line).

For my detailed discussion of consumer borrowing in all categories, delinquencies, foreclosures, third-party collections, and bankruptcies, read… Consumers Can Handle Fed Tightening: Their Debts, Delinquencies, Foreclosures, Collections, and Bankruptcies

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I guess that’s the end of the fake recession they tried to dream up. I still can’t believe they tried to put that one across on the public.

Recession was (and is) one of various quite real possibilities. I didn’t see anyone trying too hard to sell it. Shall we try to get all conspiratorial about it?

Whenever rates are supposed to be raised some baloney like a fake recession is always dreamt up to mitigate any interest rate increase. It’s been the same for more than a decade.

Too Early to make conclusion!

Many Economies:

If you have owned one or more properties – You have made a fortune over the last 10 20 or 30 years..

One example: Friends that have owned Principal Residence for 20 + years in a great neighborhood – Net gain on Home is at least 3-5 Million Dollars in a a Metro Area..

In Canada ( One example) they can sell at any time with ZERO Taxation.

They feel very secure (Funny that)

Now.. Young folk – Small savings in same Metro area..

1,5 to 2 Million to get into a Home..(First) Need 250,000.00 Family income to qualify for a Mortgage..

(Not feeling so secure) :(

Lots of different economies in one economy

Eh?

So, normalizing toward trends, after pandemic disruption. Debt is not at runaway levels. Domestic services economy is picking up.

This, considering the headwinds of various global disruptions.

These variables sure don’t look to me, to be headed for heck in a straight line.

Consumer spending is holding up. We saw that in the last GDP print, which was negative due to a “freak event” in net exports, that will reverse in Q2, while consumer spending was just fine

https://wolfstreet.com/2022/05/15/that-q1-gdp-drop-was-a-freak-event-that-will-get-unwound-in-q2/

Disagree. People spending just from being cooped up. But the Walmart and Target warnings portend the truth: the fed made fake stimmie economy is now running out and with inflation will come double fast reversion to the mean. My car business has never in 20 years been completely dead as it’s gotten. Recession started in Jan and 2nd quarter will confirm.

Just what the Fed needs to keep raising rates.

Consumer debt is a small part of total debt. Debt to GDP ratio is at a record.

How is total debt calculated for the debt to GDP ratio?

If I interpreted correctly, Wolf and comments here have pointed out that there is no complete measure of leveraged debt (because much of it is hidden).

Drifterprof

For a fascinating and useful discussion of systemic debt, you could reference McKinsey Global Institute’s:

— Debt and Deleveraging: The Global Credit Bubble and Its Economic Consequences (2010)

MGI did sequels in 2012 and 2015, but they are skewed by omitting info before 1990. And of course the info excludes the experiences of the last 7 years.

I disagree with their conclusions, but the framework and historical sweep are quite good.

Unfortunately, when you ask about “total debt” to GDP, you get into a quagmire of definitional nuance.

For example, are SS and Medicare trust funds NOT to be counted because we owe it to ourselves? Or, should a private pension guaranty be considered “debt?” Is a US dollar (says “Federal Reserve Note” right on the face) a debt? Are federal mortgage guarantees “debt?” …. And a hundred more.

The stacked charts showing systemic US debt (Gov’t; Household; Corporate; Financial) that go back before the 1990’s are especially interesting (p.59 in the full report version) in that they show a progressive increase in systemic debt that implicates the Fed, Wall Street Bankers, and Academia, IMHO.

No

The bear market is over and bulls are back in charge ;-)

It looked that way today. But was any of the last two days up a short covering exercise just before the holiday weekend?

Until Apple’s second quarter earnings come out. Make that until most of the second quarter earnings reports come out mainly Apple’s.

Classic bear market rally. Look at the 6-month chart of the S&P 500. Perfect pattern so far.

Dead Cat Bounce!

This is exactly the place where retail and likewise thinking short term trend following folks getting slaughtered.

Open monthly bar chart and see for yourself how wick/tail is being created at top/bottom of the bar. Especially, end of month is slaughterhouse, as there are many pressures, end/beginning of month/week/days wick/tail creation in process. Pull back creation, usually in quite rapid/volatile way. Unsuspected eye can see change of trend and is wiped out rather fast. That is where big players getting out and back into positions. Depending on long term trends.

This is happening ever end/beginning of month/week/day/hour/minute any common period. Just more concentrated in the end/beginning of a month.

Watch where the smart money goes, before they pull the rug out from under tou. There is really no direction in this market until FED starts pulling the purse strings. Then it gets political

Inflation will ultimately force the banksters’ “Fed” to act in the only way proven to decrease the rate of inflation: raising the interest rates charged to banksters, who then triple the rate increase, as they usually also charge Americans 25% per year in interest on credit cards for money they get from their “Fed” (or from foolish depositors or CD holders) for less than 2.5%. That increase in interest rates (or the increase in inflation if no increase in interest rates occurs) will ultimately make investors realize that their returns of 7% or less per year, while real inflation runs at 8% to 10% per year, are insufficient to avoid a real, negative rate of return.

THEN, independent, individual investors will jump out of the markets, and bonds, CDs, and other investments, unless those provide real, positive yields. It is just a matter of time, albeit that avoidance of negative, real interest rates might just result in some asset classes getting inflated values, like real estate has inflated values in many countries.

Only problem with this is that it doesn’t make any sense.

The difference between CPI vs. PCE is now at its widest since 1980, and the widest since the Federal Reserve switched from targeting the CPI to PCE around 2000.

For April 2022,

1) Headline CPI is a full 2% higher than headline PCE (8.3 vs. 6.3%)

2) Core CPI is 1.3% higher than core PCE (6.2% vs. 4.9%)

3) Though not directly comparable, headline CPI, the number most often reported in the news, is now 3.4% higher than core PCE, the actual benchmark being used to set policy.

We could well end up in a situation later this year where headline CPI remains well above 6% but core PCE is in the upper 2s, giving the most dovish FOMC in history an excuse to slow, delay or even reverse tightening.

Markets realize this and that’s why stocks rebounded sharply this week. Raphael Bostic is already talking about declaring victory against inflation and potentially pausing or stopping rate increases by the September meeting.

If Bostic is even mentioning words like victory he must be very naive. If the Fed stops too early inflation could easily ramp back up, even with their manipulated metrics. In any event, attempts by them to ignore inflation could really backfire since the people who are damaged the most are already mad as hell (about various things). I’m not sure they understand the potential fallout from failing to contain inflation.

Looking at the chart of Real income adjusted for inflation may show the the stimulus money may be all spent and now the credit cards are picking up some of the slack.

Also, a lot of refinancing mortgage the past two years involved some cash out.

Maybe inflation has peaked and the market is reacting. Most likely a bear market with more rate hikes and QT coming down the pipe.

It will be hard to take the market higher with liquidity being withdrawn. That is a pretty big headwind.

My mortgage broker friend here in Texas was just told to take the month if June off and call back to the office in July. Refi’s are dead and very few new mortgage applications pending.

Last year he was busier than a one armed paper hanger.

“…now the credit cards are picking up some of the slack.”

I don’t understand because the above article said that credit card balances are dipping:

“Credit card balances, excluding other revolving loans such as personal loans, dipped to $840 billion in Q1, from Q4, still below Q1 2020 and Q1 2019”

Fed needs to get to 2% sustained inflation to “declare victory” on inflation.

We are very far away from that.

Bostic’s primary constituency is the group most impacted by both higher inflation and weaker growth/recession. Whether he believes what he said or not, he wants it to be true.

Everyone knows the facade of falling inflation will end once the midterm elections are over. Plan on inflation spiking back upwards at the start of 2023 leading to hyperinflation in the following years. This is their game plan.

How many experts in how many fields do you think are toiling away, calculating the announcement date of Biden’s criminal, immoral and retarded “cancelling” of $10k/person of student loans that will generate the most democrat votes?

You got this wrong. The people who owe over $10,000 in student loans (median is $17k) and only get $10,000 forgiven, instead of the whole thing, are going to be pissed off, and they’re going to call Biden names. There is nothing more entitled than a bunch of people who borrowed a bunch of money and suddenly have hopes, fueled by the fawning media, of this being a free gift.

PCE is chain weighted and allows the substitution OUT of items that rise TOO MUCH in price.

A metric with low inflation bias.

Housing is also a much smaller factor in the PCE index.

Why is the 10yr treasury dropping? Fed has stopped buying and will start QT on June. Does the market think Fed will not tighten any more?

Yields go up, and yields go down, which is what markets to. The 10-year exploded this year, so now its backing off a little. On April 26, it was 2.73%. Today it’s at 2.74%. But at the beginning of the year, it was at 1.63%.

And the Fed has raised by only 75 basis points, and it hasn’t started QT yet (starts in June).

Right. The 10-year would be more affected by QT than the change to the short-term Fed Funds rate.

Do you have any sources or articles that try to estimate how the QT starting in June will impact the 10 year? So far it looks like nobody has any idea. JPMORGAN CEO said it is one of the unknowns facing the market. Also, with fed decreasing MBS purchase, is thete any estimate on how low the MBS prices can go?

Great info. Thanks, Wolf.

Any insights or commentary on the decline in personal savings?

Oops…Should have said “personal savings rate”

1. “Personal savings” is a misnomer. It has nothing to do with “savings.” It’s just annualized income from all sources minus annualized PCE spending. Meaning, it’s income that wasn’t spent on consumer goods and services.

2. But capital gains are not included in this income, nor are cash-out refis, and some other sources of funds that are linked to capital gains, rather than “income.” As I said in the article and in the title, the substantial increase in spending is supported by the huge (and now dwindling) increase in asset prices (stocks, homes, cryptos) that consumers have been drawing on. In addition, there is still a huge amount of money floating around the various stimulus programs, including PPP. The whole system is flush with money/assets from money printing by the Fed stimulus spending from the government.

Yes, truly great Info Wolf, thank you.

So far, the FED hasn’t done very much to tame inflation. I wonder how QT will fit in here together with some more rate hikes for the rest of the year. It that doesn’t shake up the whole fakonomy, I don’t know.

The Fed will rely on the YOY bringing the inflation headlines down.

But let’s realize that any subsequent gains in inflation even though by less amounts will be stacked upon the previous gains. There will be no rollbacks. 5% sounds good now …tack it on the 8% ….doesn’t sound so good.

“If you create this [FED] you will have created an engine of inflation.”

– Rep Elihu Root, 1913 Congressional debates on creating the FED.

The FED is still massively JUICING the economy, as inflation is running over 8%, yet fed’s fund rates are less than 1%. That’s 7% ‘juice’ still stimulating the economy. The FED WILL NEVER PUT any brakes on the economy, so don’t let these so called ‘rate hikes’ fool you. This is why we are about to witness a rather massive rally, back to new all time highs on the SNP 500.

Once we hit new stock market highs, then we can talk about a REAL market crash. A load of stocks have been taken out to the wood shed no doubt, but there is still a massive FED PROP under the stock market which are the still absurdly low interest rates.

These teeny tiny ‘rate hikes’ are meaningless, and are NOT fighting any inflation. The Fed does not fear inflation at all, and basically wants it badly. What they still very much fear is deflation. That’s why they are gonna let inflation run as hot as possible for as long as possible, as the gargantuan debt they have helped create gets paid back with every more worthless dollars.

Their public rhetoric, tiny hikes, and joke of a balance ‘reduction’, are merely eye candy to get the public to believe that they are actually doing something to help.

Whats actually going to cool off inflation is massive demand destruction, caused in part by inflation itself, but more caused by massive increase in costs of energy, especially oil, and the massive shortage of oil, that nobody is really talking about. The big oil companies are not investing in E&P, because all of the oil has been ‘found’, and the ROI is not there to invest one more stinking dime. So oil is going to keep going up and up, until it basically runs out, which we are witnessing now. Fracking is basically done, and now flat, and if we weren’t exporting the heck out of natural gas, the fracking could sustain us for decades on natural gas alone. Renewables (a total joke and mirage), and the governments blow hardish comments about it, ain’t never gonna happen here in the US beyond a very small lame percent of any other source. We are going to be forced to go back to coal, and then kicking and screaming into nuclear (but thats if we are very lucky). More likely our country will die off in population to less than half of what we have today, because the government will resist adding nuclear power. By the way, the entire automotive industry has entirely written off EV’s. What you see from Ford is only a red herring. An industry presentation on what happens to the grid, with a very specific and tragic demonstration of a line of super chargers stacked in a row. They all gulped, choked, and puked, when they realized that the US power grid, NOR any countries power grid, will ever handle anything more than maybe 10% of the current vehicle population converted to EV’s. The only plausible scenario, is plug in electric hybrids, which can run on about 10% of the fuel that cars use now, while maintaining our power grid, and not causing it to collapse. And they will stumble along with fuel efficiency standards rammed down their throats, to where the least efficient vehicle will get at least 50 MPG if it runs purely on gasoline. Hydrogen fuel cells, powering EV’s, will very slowly be added in. It will take decades, but battery powered ev’s will have died a rather painful death. Musk knows this, as he KNOWS Tesla’s days are literally numbered, which is why you have seen him pull so much money out of Tesla, and he is creating his next landing spot in the form of a new and re-incarnated Twitter. Just like he went to Tesla for a short stint after PayPal. Musk is the world’s greatest con man, and will be ultimately be remembered for creating the white elephants formerly known as tesla’s, which will all for the most part be ‘bricked’ by 2030. He’s duped a crap ton of people into believing battery operated EV’s are real, and that the power grid could support them. It will be gone due to the brick wall of inability to get much more than an insignificant amount of super-chargers in place, the grid crashing (blackouts everywhere and year round) and not able to support more than a minor handful charging stations that will mostly still be all too slow, and due to no parts, no batteries (lithium gone or all used up), and no corporate Tesla. Guys Musk has already planned his exit, and will be out before Tesla stock REALLY crashes and burns. So you ain’t seen nothing yet for Tesla stock crashing. But that will be after new ATH’s in the stock market, which will be the forever top, before the most wicked crash, and subsequent longest bear market on record. Lasting a generation or more. Where folks will FINALLY and truly shun stocks.

Hi Mike, thanks for your thoughts. I see we are in for a wild ride.

I will stick to my Diesel car, even though the propped up it’s price worse than anything else.

Cheers

That’s a crap-ton of predictions there. Maybe once a year give us an update on how each of those is going.

Savings rate dropped to lowest level since 2008. As long as there is stimulus change in the sofa, all is well with the ecomony!

Might be a continuation of the tendency of people in the last few years to put their money anywhere but the bank, so that they can get some actual positive returns (a strategy that works very well until it doesn’t).

I see Posts about Saving Rates like yours :

Bask Bank Saving rate @ 1.25 % APY

headquartered in Dallas, Texas

They have hi rate FDIC Insured savings ( 1.25 APY % currently )

or the have a American Airlines travel Miles account

Bask Bank is a Very Hi Rate online type Bank a part of ” Texas Capital Bank ”

Extremely easy to join I wired Funds and they showed the same day

but a part of ” Texas Capital Bank ”

NO Fees /No Checks/No Credit Cards/No Debit Card/Free ACH

They say as the Fed raises Rates they will increase the Saving rate

FDIC Insured to normal Max $250.000 X 2 to $500.000 with 2 POD

Beneficiaries are Not contingent but rather Equal at 50 % each .

I have Had no Bad Issues with this Bank and they have no Fees

with the exception to wire Transfer OUT is $35 that’s a top of the line fee

I have not see a Better rate anywhere

IMO revolving credit levels will begin to show the consumer is putting the incrementsl inflation price increases right on the credit card

How is credit card debt calculated?

Sum of monthly statements?

Sum of daily balances averaged?

If it is based on statements, it could be misleading?

Avraam Jack Dectis,

The same with the S&P 500 Index or the Case Shiller Home Price Index or any of the other big indicators: It doesn’t matter how it’s calculated. What matters is that it’s calculated the same way each time, and it is.

It shows you the movement, up or down, and how much up or down. That’s what matters in these aggregate figures.

But if you don’t like what you see, you can always say it’s misleading and question the index.

Oh, the engine isn’t running hot, it’s the temperature gauge that is misleading :-]

The band Boston has a song, “Cool The Engines.”

‘We keep getting hotter

Movin’ way too fast

If we don’t slow this fire down

We’re not gonna last

Cool the engines

Red line’s gettin’ near

Cool the engines

Better take it out of gear

Take me for a ride

Take me all the way

Take me where I’ve never been

Someplace I can stay’

Corporate debt is way too hot if interest rates climb higher and stay there. Zombies gonna get burned out — as they should, I reckon.

It seems to me that lumping all Americans into one income and spending profile is very misleading. Is there any income and spending data available that gives this data broken down by income and/or wealth categories? With the very broad income and wealth distribution in the US putting everyone in the same category seems inappropriate.

This is about the overall economy, not individuals. This is data that goes into GDP (Q2). And it gives you an indication of where GDP is going. That is the purpose of this data.

And so it would appear that tightening is destroying the source of future spending?

And restricting future borrowing.

This doesn’t bode well does it?

How can you soft landing a system that operates on a knife edge of greed and fear… tipped in a moment by what the Fed says, never mind what they do?

Rates up just so they can cut them later?

Kenny Logouts,

Raging inflation is the biggest economic enemy that people today have. It’s the biggest enemy that the overall economy today has. It needs to be crushed. It should have been crushed a year ago. To crush inflation, the Fed uses its tools to raise yields (and lower asset prices), which will slow demand in what is still the most grotesquely overstimulated economy. Right now, the Fed is just removing stimulus. It’s not actually “tightening” until after it gets to “neutral,” wherever that is.

If the Fed does enough of it, it will bring inflation back down. If the Fed doesn’t do enough of it, inflation will drag on, as will higher and higher interest rates and lower asset prices.

The ten year seems reluctant to find a home over 3%.

When is the QT starting again??

The Fed is limping along ….is it dereliction or is it planned procrastination?

I think the Fed is betting on the YOY inflation readings coming down significantly….but that doesnt cure the damage done.

All inflation rate increases will be stacked upon previous increases….(8%)

the Fed’s inflation target should now be 0% if not negative for the next few years……it wont be. Will anyone ask them of their want to average inflation now?

If I recall, QT never started and is planned to start in July? I could be mistaken on the month.

Starts in June.

“Will anyone ask them of their want to average inflation now?”

Sure, people who are well educated and concerned with macroeconomics will prod the Fed to continue “their want to average inflation.”

And if the average American working stiff actually starts to understand what the Fed is and what it does (unlikely), then there may be hell to pay on the streets and in politics.

However, if as the year wears on, people are convinced that inflation is being tamed, many will treat the last few months as water under the bridge and get on with their life. Most people now seem to understand that both major parties are full of too many dogs / rats working for special interests, instead of the general health and welfare of the culture. So no use in spending your energy trying to fix it.

Drifter

” people who are well educated and concerned with macroeconomics will prod the Fed to continue “their want to average inflation.”

The Fed had a 2-2.5% target for inflation.

Then there was an 8% jump.

The Fed still has a 2-2.5% target.

Why? It should be zero or negative for the next couple of years, if they still believe in averaging.

The Fed seems to accept the idea the price increases are imbedded.

They seem unnoticing of the cumulative nature of it all……conveniently ignorant.

Thanks Wolf, I understand why they’re raising rates.

The issue I pointed out is if people are spending non-cash gains in assets that are disappearing… then these return to pre-pandemic spending levels can’t continue to occur.

Combined with inflated prices consumption will remain low.

And the pandemic surge in spending was largely on inflated price non-durable goods.

So the asset prices are unwinding.

The spending is unwinding.

The Fed is removing via QT (tightening) in days from now.

March 2020 to now appears to be being reversed.

But we’re all expecting a soft landing back to March 2020?

Won’t the resulting lack of demand in the economy from the rates required, lack of spending power, loss of confidence (they wittered on about this one for years post 2008 in the UK), etc, cause asset deflation and ultimately CPI falls, unwinding much of the inflation we’ve seen?

Or do you believe businesses won’t cut costs to compete, and instead will just go bankrupt?

All this said, in the UK we’re now getting pseudo UBI for help with energy bills, while the BofE is increasing rates to fight inflation on the other side.

I can’t see this ending with a soft landing.

If it does then it’s ultimately terrifying.

It shows extreme competence!

Inflation at Walmart is now well north of ten percent. The last I just saw a 10 pack of small chocolate bars go from 2 dollars apiece to 3 for 10 dollars in one fell swoop. 2 dollars to $3.33 is like 66 percent inflation.

Could some of the spending be people attempting to front run inflation? Has the inflationary mindset already spread?

I was thinking the same thing. The big spike in housing prices in 1Q2022 certainly was a lot of people front running interest rates.

I bet some companies did the same thing regarding their finances?

Inflation and forward demand is causing the so called broken supply chain not the broken supply chain is causing inflation.

It doesn’t seem to me that the Fed’s strategy to decelerate the economy working fast enough to tame inflation to 2% any time soon. Right now it seems they are really aiming for like %4 inflation at this point and will declare victory whenever we reach there which could be this fall or winter. Stocks are not lower enough to leave meaningful dent in anyone’s wealth so far considering how much they have ascended in just couple of years & housing might take couple of years to correct.

Meanwhile lower middle class & poor are the only ones losing in this environment.

I’m not sure anybody could have even dreamed of such a massive money-printing/speculative orgy as what’s taken place. It’s just repulsive. And to think that they nominated Powell for another term. The guy has literally financially destroyed the middle class and the poor, and CONgress fawns all over him.

Now he has the audacity to act like he’s the second coming of Paul Volcker while he talks of “soft landings.” What he’s trying to do is actually not stop inflation but temper the rate of inflation, parking asset prices at a permanently high plateau – a Powell souffle. We are absolutely doomed with the people who are running things.

Powell’s confirmation wasn’t unanimous. Vote against those who approved him, support those who didn’t.

Inflation is hitting services, too. People can’t spend money they don’t have for very long.

Services will catch some the spending coming out of goods, but it won’t last long.

In print with summer AC coming.

Electrical rates in Texas have more than doubled since last time I signed a 2 year contract.

My previous contract was 0.08 cents/kWh and current internet postings lowers I saw was around 0.15 cents/kWh.

As mentioned by Wolf inflation for economy is repulsive. Natural gas has climbed to 9 usd/mcf vs a several year price under 3 usd/mcf.

Where does utilities cost sit in the spending realm ? Services?

I did not see this electric cost coming!

Big homes remodeled homes people flush with cash and spending continues for how long I don’t know.

The graphics and literary describe the data in an even handed way. I would judge the data as optimistic, the enemy of pessimistic.

Perhaps, the bear market rally this week, reminds me of a Knute Rockney scene about three yards and a cloud of hope.

Of course I was on the negative side of the man period.

I mean, who would pay 5 years of dividends to buy a stock that was on sale last Thursday, still at an exorbitant price.

Then I became aware that Chair Powell’s grimace was decidedly bullish for the stock market, a readily available table stakes banker who signaled that the Fed wasn’t serious about inflation.

As the stock salesman say, this market will break the multitude of historical financial records set last year. Gives me confidence that, next week, after the first of the month, this rally feels desperate. I’m not in the stock market at this time but will buy in when the market is not synthetic and the valuations reflect reality.

To me, your graphic, “Personal Income adjusted for inflation” is the central part of the story, the all important measurement that leads credence to all the other measurements.

Which supports my assertion, that the problem with America is the inequality. A few, capitalizing on their genius for gaining ownership, of other people’s creativity and hard work.

America’s ideal is a living wage income and family benefits which includes discretionary income.

“ America’s ideal is a living wage income and family benefits which includes discretionary income.”

Go give a poor person all your money and get back to me how that works out for you…

On my current trip, two Mickey Ds were advertising jobs at $10 and $11.25 per hour respectively…

“ Which supports my assertion, that the problem with America is the inequality. ”

Inequality, my happy a$$…

In the last 20 years, there has never been a greater opportunity for skills training and/or college at minimal or no cost to “underprivileged” people….

Even WalMart will pay for college, but you kinda have to show up and “work”…

While “inequality “ can be defined in many ways, being lazy does not fit the bill…

The problem with America is the inability to think and reason as individuals which makes you better, not handouts that make you weak…

1. “America’s ideal is a living wage income and family benefits which includes discretionary income.”

2. Go give a poor person all your money and get back to me how that works out for you…

How did you jump from #1 to #2, COWG?

“While ‘inequality’ can be defined in many ways, being lazy does not fit the bill…”

The “inequality” dang described was “a few capitalizing on their genius [I would describe it as predatory greedy intelligence] for gaining ownership…”

That statement is not related to your assertions about laziness in the culture, which for the most part I agree with. Wolf’s articles on the wealth effect affirm what dang was pointing out (hard to find the wealth effect articles, since there doesn’t seem to be a category for them).

IMO, asserting that laziness is the root cause of poverty is a slippery slope the tends to end up overly simplistic, unfairly blaming the disadvantaged which is untrue the majority of cases.

“How did you jump from #1 to #2, COWG?”

dp,

Easy, brother…

The fallacy of the inequality crowd starts with the premise that all are able and capable …

The simple fact is they’re not…

You and I are not equal… you are way smarter than me…

So I want you to send me some money to make up for that fact… :)

The minute you think “ hell, no… I’m not sending you any money,” you just lost any equality argument AND exposed yourself as a hypocrite…

And the reason? You think I don’t deserve it because I had the same opportunities as you but didn’t take advantage of them… i.e., lazy… so why should you have to send me money…

As a point in case, how many have we read in here bemoaning about buying a house, yet never got off their couch because they were too lazy to do anything except.look at Zillow…

As to the genius of the world, Wolfs imploded stock list makes a mockery of genius in the world today…

I’m of the belief that everything important has already been discovered… there may be an outlier or two… aliens, for example…

How many “new” cookwares have we seen.. 8,10…. How many dating sites have we endured… 15,20… one for the blacks, one for the farmers, one for the Christians, jeez…

How many have we seen lose a crapload of money because they were too lazy ( there’s that word again) to learn financial education and instead threw their money at BS because, well, I just can’t be bothered with that stuff…

Whaddaya mean I’ve lost all my money in stocks and I have to get a job… a job… how humiliating..

Yeah, I stick with lazy…

But then again, I don’t confuse inequality with appeasement… for another day…

I know we have a time difference, so have a good evening, my friend…

Actually for cowg:

WAAAY Too simplistic bro or sis… far below YOUR usual IMO…

Please do NOT rely on anything similar…

but serious thanks for commenting on Wolf’s Wonder,,,

I suspect, the current inflation is an artifact of excess speculation, funded by the Fed’s bloated monetary accommodation. QT can’t begin soon enough. It is high time the Fed sponsored larceny, stops.

I have too continually remind myself that the population has tripled since my memories were formed. I exclaim to myself;\\

How can it be the same as that which I remember, while at the same time, never was.

Well, I simply choose the option that paints me in the best light.

The official debt figures consist of bonds and bank loans, and for consumers, it includes all types of housing related loans and consumer loans. Those are known and tracked. It doesn’t include leverage in derivatives and stock market leverage of the various kinds.

I suggest that America is at the crossroad of an existential dilemma about the economy. As the American government adopts the harsh techniques of their competitor, the Chinese communist party, who control the American manufacturing function. As Adam Smith warned, never allow the merchants to decide.

“Wherever there is great property there is great inequality. For one very rich man there must be at least five hundred poor, and the affluence of the few supposes the indigence of the many. The affluence of the rich excites the indignation of the poor, who are often both driven by want, and prompted by envy, to invade his possessions.”

― Adam Smith, An Inquiry into the Nature and Causes of the Wealth of Nations

It is all well and good to quote how free markets would function but, I submit, there is no free market, by definition. QE suppresses the financial market. Pointing out the current structure of consumer loans seems as a straw man argument, small potatoes.

QE provides the speculators zero interest rate money to purchase assets.

Let’s look at what happened this week, the 10 year dropped 25 basis points in response to Powell’s public cave in his promise that inflation is the priority, by suggesting a pause in September. Risk on, the Fed put is alive and well.

There’s a huge imbalance between dividend yields and interest rates. One has to give either interest rates have to fall or stocks have tot fall to push dividend yields higher.

1) Since Apr 6 2022 revolving home equity loans are rising again.

2) Real disposable income have reached Nixon level in 2021, a year ago, but it’s down from $58K to $44K, minus 25%.

3) Nominal wages are higher, but part timers work less/ week.

4) Xboxes, dishwashers, stuck in Savanna and Long Beach before Xmas are clogging sold out warehouses, because nobody want them anymore. Real spending on durable goods are down.

5) We are spending more on dentists, heart surgeries and diagnostic, because we stayed away from them for too long.

6) We are spending on rent more than ever before.

7) Income minus transfer will turn down if we enter a recession. Transfer

payment will rise, but they are only fraction of a real income, unless JP

stimulate…after cannibalizing RRP.

8) Iran privateer two Greek oil tankers due to the high inflation. That’s a good start for a 3 days weekend.

Michael, just putting your #8 comment in context. Several days ago, the United States govt imposed additional economic sanctions on Iran. As a result, the United States govt requested that Greece confiscate an Iranian ship moored in its territory. So in response, the Iranian Rev Guards took control of those 2 Greek tankers in the Persian Gulf and then threatened – there are 17 more Greek ships in the Persian Gulf. Bigger question is if the Greeks will get help from our incompetent government now. Maybe our current administration wants higher oil prices for a long time?

“Here’s the situation. And when it comes to the gas prices, we’re going through an INCREDIBLE TRANSITION(!!) that is taking place that, God willing, when it’s over, we’ll be stronger, and the world will be stronger and less reliant on fossil fuels when this is over…” Biden said during a joint news conference with Japanese Prime Minister Fumio Kishida.

You have to understand…this is part of the plan. They’re screaming their future designs for us right into our faces, plain as day, for crying out loud.

Ship our Nat Gas to Europe, prices triple here.

Cut leases and drilling opportunities.

Drain the Strategic Petroleum Reserve.

Gasoline and Diesel prices continue sharply higher…

Businesses and people destroyed…

All by design and to the delight of the Green Power people..

ideology trumps all. The ends justify the means.

problem is the economy will be destroyed, and the technology is not there for Green Power to replace traditional fuels.

Idiocy, and destructive ideology, IMO.

Fake intellects with “good intentions” ….”Good intentions is an overrated virtue. ” (Milton Friedman)

Do gooders doing great damage.

Real spending up, real income down.

That helps explain the personal savings rate that’s the lowest since 2008. No free lunch. People are going into reserves to keep up. Can’t last forever.

1) Crude oil is stuck between two backbones.

2) Exogenous causes might send CL > Mar 7 fractal zone.

3) The Fed cannot control temp exogenous events, but if oil prices rise and the Dow plunge, JP wouldn’t mind.

4) NDX retraced 50% of covid low. NDX might retrace 62%, before recovering in a low slog up.

5) Can AAPL still do it, or it fell out of favor in BRK trading room.

1) Crude oil is stuck between two backbones.

2) Exogenous events might send it above Mar 7 fractal zone.

3) If oil rise and the Dow plunge, JP wouldn’t mind.

4) NDX might retrace 62%, before rising in a low slog up.

5) Can AAPL still do it, or it fell out of favor in some major trading rooms.

Michael Engel-

“3) If oil rise and Dow plunge, JP wouldn’t mind.”

You could add Mortgage Rates to your short list. Energy costs, falling stock prices, and higher mortgage rates will indeed have done much of the Fed’s job for it.

Might those economic retardants allow JP to justify a “transitory” pause from his ballyhooed rate increases.

Given all this heroic spending by consumers, why are companies reporting less revenue and lowering guidance? I understand that inflation should start making a dent at some point but that doesn’t appear to be the case yet.

Misconception here. Some companies that sell goods (retailers) lowered guidance. Note the shift to services spending — the core topic of this article. Retailers don’t sell services. They sell goods. But over 60% of consumer spending is on services. And they’re booming.

Other companies that lowered guidance were mostly tech companies that sell to businesses, and companies that sell ads, and they lowered guidance on growth, but still forecast growth. So instead of growing at 40%, they might forecast growth of 20%. That might kill the stock, but it’s still growth. Some services, such a streaming lost ground, while other services, such as airline ticket sales are booming.

Many companies lowered guidance on earnings, and not on revenues, due to higher costs. Revenues are holding up, but higher costs are eating their lunch.

Some pandemic darlings, like Peloton, were in a bubble during the lockdowns, and now the world is going back to normal, and exercise bikes are just not a hot product anymore.

Also, analyst have not lowered their S&P earnings for 2022. They expect ATH in earnings every Quarter in 2022.

That does not mean stocks would not fall….which they have. They were overbought.

Earnings will fall in the second quarter of 2022 versus the earnings in the first quarter of 2022. Rising inflation will hit earnings.

I still don’t understand where all the stimulus money went/is. I know some people got checks for $1400 ??? (a couple of times?).

If I went to SF and took Wolf out to dinner with a few friends that money is gone. One night. Poof!

Is it the criminal PPP money that’s still floating around? Who the heck got all this money? And how are they STILL spending it?

I didn’t even get a lump of coal.

I think you’re right about the individual stims ($1,400 etc.). But as the title of the article states:

Powered by (Formerly) Huge Gains from Real Estate, Stocks, Cryptos, as “Real” Incomes Lag? “Real” Consumer Spending Rises, Spending on Services Jumps

And Wolf states in the comment section:

“…there is still a huge amount of money floating around the various stimulus programs, including PPP. The whole system is flush with money/assets from money printing by the Fed stimulus spending from the government.”

In March, when I was in the United States, I had a conversation with the driver when taking an Uber cab. The young man described how many of his friends had become accustomed to living a party life (work having a very low priority) after enjoying flush benefits from windfall pandemic unemployment compensation and various other benefits.

Like you say, it seems like the free money allocations to individuals would have run out a while ago for most individuals. But maybe a lot of people have been cashing out of their ballooned asset investments too, and have tens or hundreds of thousands of dollars to indulge in whatever.

The $1400 probably pales when compared to the money that went business. I know several who did not need the money took it. Of course they were not sure at the time if they would need it or not.

Also, thousands or hundreds of thousands of people opened up LLCs just to get the PPP money. Were they supposed too….no. Time will tell if they can ever track it down or will they even try.

I remember reading how 100s of airline LLCs were started during Covid.

Business basically got tons of money free,free. Free, my brother got 300k then bought a much nicer house . Thanks FED .

There has been a Washington DC party and you are not on the guest list. In fact you do appear at the DC parties, as the menu.

Infidelity was not an issue breaking the sacred bond of trust

That may be the unrecognized blessing, that I’m ugly. Or my prudence, prescribed by the church during my 12 years of parochial education. Who knows or cares.

As I prepare for tomorrow, I salute America, and repudiate the times that I questioned being white.

Not just white, but pure white, genetically

Is the implication the US population has not yet realised en masse that wealth destruction is already here? i.e. the paper wealth is disappearing rapidly at this current time.

As it hard to understand why real spending would be maintained by people facing considerable losses to their savings.

Looks like the central bankers are trying to slamdunk Bitcoin and silver to bring the teenagers back to work.

1) RE loans are banks biggest assets. Ohmi is killing hundreds American daily. The latest subway shooter discourage NYC riders. WFH increased NYC office buildings vacancy.

2) Traffic to NYC is still down 50%. Spending on lunch is down. The cancer of dark vacant street level is spreading in NYC.

3) The banks are strong, but JPM dived into Feb 24/ Mar 2 2020 zone.

4) JPM latest bear market rally failed to close above Apr 20 close despite all the effort.

5) JPM was rising on falling spread and volume.

6) JPM weekly big white bar > ma200 closed between Feb 28 close, a setup bar and Mar 7 open that triggered the next wave down, but failed to close above Apr 18 high, – a shooting star – and Jan 13 2020 high, the highest point, before Mar 2020 plunge.

7) Jamie is a black pique Diamond.

If people are still gladly spending with 8.3 % inflation, then interest rates need to rise 0.5% each month for the next 12 months, giving a rate of roughly 7%. Add on to that QT and you might get inflation rates down to 6-7%………..

“The whole system is flush with money/assets from money printing by the Fed stimulus spending from the government.”

Which means the US economy should be going full steam ahead, and not just hanging in there with more than a couple of weak trends which are expected to turn lower, and lower again, with the coming rate hikes, QT, consumer overspending, and capital misallocation.

Doesn’t anybody else hear the air hissing out of the bubble?

The only things in the US economy which ARE going full steam ahead are inflation, corporate profiteering, political dementia, and resource depletion and degradation, none of which are conducive to economic stability.

The optimists here seriously need to go back and reread the tea leaves.

Air usually doesn’t hiss out of a bubble. It pops.

Maybe the wrong metaphor is being used. Hot air balloon might be more accurate. Or fat tire? Hopefully not Hindenberg dirigible?

You guys are way too hung up on metaphors.

Una-

If I suggest we will “muddle through”, would that:

a) Sound too optimistic?

b) Constitute a whiskey-old-fashioned metaphor?

“corporate profiteering,”

and thank goodness…

for if there were no profits there would be only government hand outs via printed money

No services, no products, no food. It is all profit motivated and IT WORKS!

Average profit margin is around 6%.

MUSK: BRING ON THE RECESSION TO BANKRUPT THE LOSERS!

More signs of softening housing market as summer begins…

Sellers slashing prices…

Bubble trouble?

Consumer sentiment falls further…

Savings Rate Lowest Since Financial Crisis…

Profession: Consumer.

Not “profession.” This is far broader: “Purpose in life.”

American Dream.

Most if not all of this increase in this consumer spending for services is just inflation. Just had to make a service call on my refrigerator after the temp inside the refrig went up to 50 deg and spoiled all of my food. The diagnostic fee just went from $75 last year to $99 this year. That’s 25% inflation for the same service. This increase has affected nearly all the critical services that you have to buy, I don’t believe any of the garbage the government puts out with regard to inflation in the price of services. I’ve got my own inflation index based on real data and it ain’t pretty.

SC:

It was more like a @32% increase ($24 into $75). So, it’s worse than you thought.

My son was visiting my sister. Her toilet valve was running. A plumber quoted $200 to repair. He did it for $14 (cost of the part at Home Despot) and a cold snack.

This is where having some skills can reap you benefits.

A friend who has a few Audi’s in his family’s stable told me today that the service fee (mechanic work) at his Audi dealer is now $180/hr (up from $125/hr last year). No wonder an oil change there is near $200!

Add, the quality of repair service is zero. NTB tried to do an oil change on my Subaru. When I got home all the oil was all over the driveway. They forgot to screw in the cap properly. I got all my money back and will never take my car there for anything.

Meanwhile in other news major companies are fast forwarding into automation which will eventually destroy many, many jobs. What do the rich know that we don’t? That an automated machine can run 24 hours a day 7 days a week and doesn’t ask for a raise, cost of living adjustments, workers comp etc.

I guess it’s good to be the person putting those systems in place but sucks to be on the other end of things.

What don’t the rich know? Energy is limited, which puts a limit on complexity of which automation is one part. So no, in the future, living standards will drop for everyone including the rich.

I’m scratching my head . Consumer spending up, yet savings down, real income down and yet people are spending more in real terms.

It tells me:

1. The stimulus from free Fed money and mortgage deferrals and rent deferrals put much more money into people’s pockets than is commonly acknowledged.

2. Students probably stopped paying back their student loans.

3. If people are buying new cars with loans rather than buying cheap clunkers for cash (do they still exists?) this frees up disposable income for other purchases.

4. Do crypto count as personal savings? Anyone with half a brain is selling their crypto and pocketing the cash and buying something else.

5. Optimism effect- people are finally getting raises and although they don’t compensate completely for inflation, this encourages them to anticipate future wage increases. So they go out and spend now.

All this suggests the market bounce in stocks will continue as the consumer is strong.

Real spending on services will never get back to the green trend line. To do that services would have to be consumed at a higher than normal pace. You don’t consume twice as many restaurant meals, airline tickets and insurance because you did without for two years. It’s a one time gap.

Spending on services include housing (such as rents), healthcare, education, travel (plane ticked, hotels, Ubers), insurance, financial services, entertainment and sports events, etc. They’re 70% of what consumers spend their money on. And yes, it will get back to trend just fine.