In details and charts.

By Wolf Richter for WOLF STREET.

There has been a lot of confusion about that 1.4% quarter-over-quarter drop in “real” GDP. So let me just go through what didn’t cause it, and then what caused it. What caused it was a freak event, and this freak event is likely to start unwinding in Q2. We’re already seeing some evidence of it.

What didn’t cause the drop in GDP:

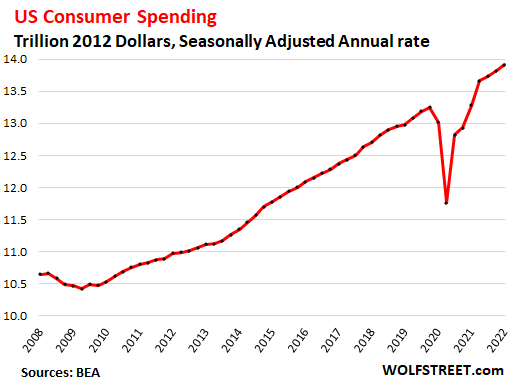

Consumer spending rose by 2.7% in Q1, annual rate, adjusted for raging inflation. It accounted for 70.5% of GDP. This growth was in the middle of the range prevalent after the Great Recession until the pandemic (from 0.4% in Q2 2011 to 4.5% in Q4 2014).

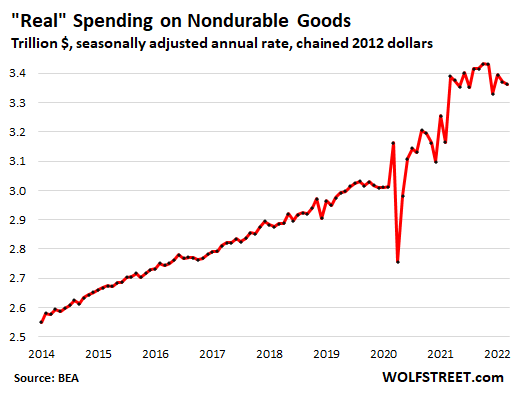

However, there has been a pronounced shift from spending on goods to spending on services, especially discretionary services, where spending had collapsed during the pandemic. These discretionary services include plane tickets, sports and entertainment venues, cruises, more or less discretionary healthcare services (such as dentists, elective surgeries, routine doctors’ visits, etc.) I discussed this shift in consumer spending from goods to services in detail here. This shift in spending from goods to services will be important in a moment. The chart shows total consumer spending in the GDP data in inflation-adjusted dollars:

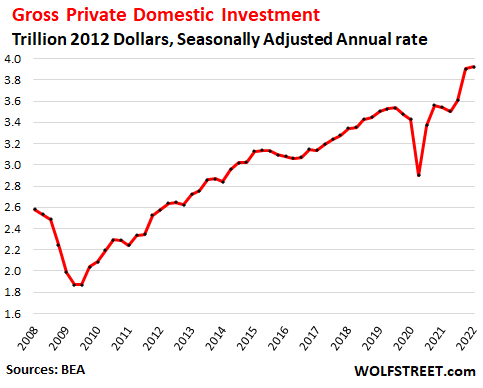

Gross private domestic investment rose by 2.3% annualized, following the spectacular spike in Q4. This measure includes investments in residential and nonresidential structures, equipment, intellectual property, etc., and it includes “change in private inventories” (more in a moment).

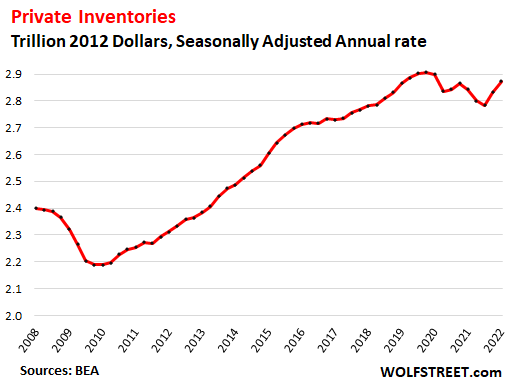

Private inventories rose by 5.7% in Q1, after the 7.1% jump in Q4, annualized and adjusted for raging inflation. There has been a boom in sales of goods, particularly durable goods in 2020 and 2021 that triggered all kinds of supply chain issues, and shortages, and US companies depleted their inventories in many goods categories. They have been scrambling to catch up, and some of the supply chain issues improved later last year and earlier this year.

In addition, consumers switched spending from goods, where spending has been dropping, to services, where spending has been surging. Goods require inventories. And the reduced demand for goods took some pressure off inventories. But inventories remain far below the levels needed for a smoothly running economy:

The Freak event that caused GDP to drop in Q1:

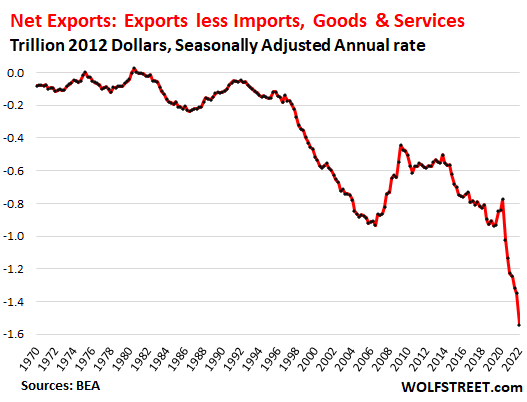

The Trade Deficit in goods & services exploded by $192 billion in Q1, annualized and adjusted for inflation, the second-worst ever drop in dollar terms, behind only Q3 2020.

Exports are added to GDP, imports are subtracted from GDP. With exports rising moderately but imports soaring, “Net Exports” (exports minus imports) have been a negative on GDP for decades. During the pandemic, stimulus-fuelled consumers spent huge record amounts on goods, many of them imported, and the trade deficit surged.

But what happened last quarter, the super-spike in the trade deficit, was extra-ordinary. As supply chains improved somewhat and as businesses were able to build inventories, imports of goods surged in a historic manner, causing the brutal worsening of the trade deficit in goods.

And this brutal worsening of the trade deficit reduced GDP by $192 billion annualized. But overall GDP fell by only $70 billion! A decline of half the size, which would have still been huge, would have produced a positive GDP reading:

Why this freak trade deficit figure will start unwinding in Q2

For the next quarter or two, the trade deficit will get smaller than the freak show in Q1, and it will be a smaller drag on GDP. Why? Because…

Consumer spending has been switching to services on a large scale, from goods (all adjusted for inflation).

Spending on nondurable goods fell again in March, seasonally and inflation adjusted. It has been falling since November last year, and was down 0.8% from a year ago. But it still remains very high, up by 13% from 2019, and will likely ease further in Q2. Nondurable goods are mostly food, fuel, and household supplies.

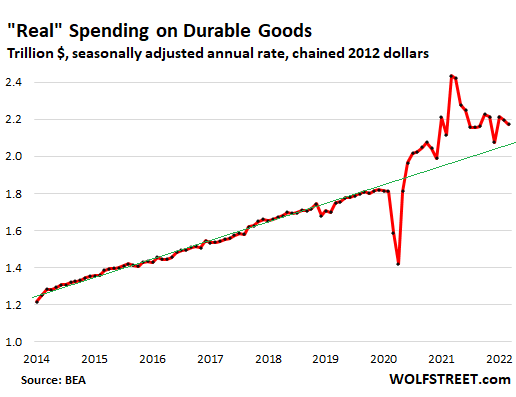

Spending on durable goods has fallen sharply since March 2021 (-10.7%, adjusted for inflation). But it remained very high, up 24% from March 2019, and will likely fall further, regressing toward the pre-pandemic mean, as consumers switch their spending back to services:

Many of these goods are imported, and a decrease in spending on goods will lower imports from the freak-show levels last year and in Q1 this year. This isn’t to say that magically, the trade deficit will disappear, but it will shift from abysmally horrible to just horrible, and the trade deficit will get smaller and be much less of a drag on GDP.

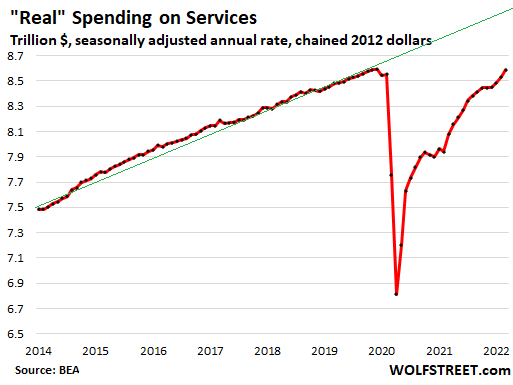

Meanwhile, spending on services is surging. Even when adjusted for inflation, it jumped by 0.6% in March, and by 6.3% year-over-year. But it remains below pre-pandemic trend and has a long way to go with higher-than-normal growth to get back to normalish levels, and we’ll see more of this normalization in Q2:

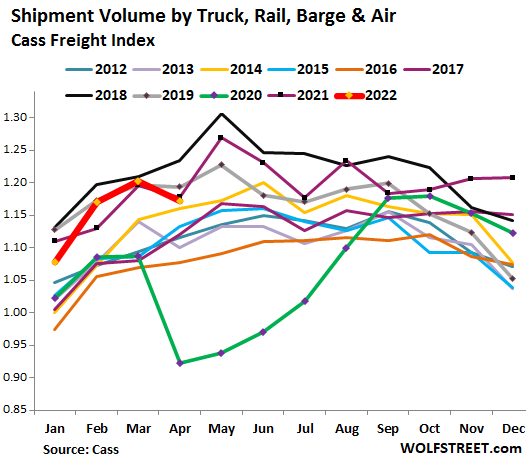

Sudden pullback in freight shows slower demand for goods in Q2.

We’re already seeing US transportation volume slowing down. And this is across the board. Shipment volume in the US by all modes of transportation, but excluding commodities, fell by 0.5% year-over-year in April and by 1.8% from April 2019, and by 5.0% from April 2018, according to the Cass Freight Index (my discussion: Signs of a Downshift in the Freight Cycle, Trucking, and Demand). See the bold red line:

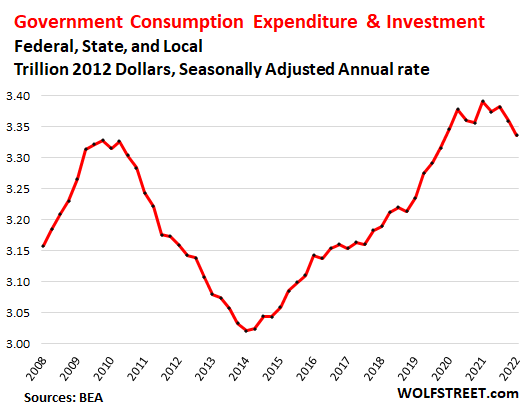

Government consumption also fell in Q1.

Spending by federal, state, local government agencies on equipment, supplies, fuel, etc. (not salaries and social spending) fell in Q1, which also dragged down GDP.

I’m not going to make predictions about government consumption, but governments at all levels are floating in a sea of cash after the money-printing binge and the high tax revenues for 2021. And these governments are going to spend this money sooner or later, which will then boost GDP.

The GDP Decline in Q1 likely gets unwound in Q2.

Less-catastrophic imports, thereby a less-catastrophic trade deficit, will reduce the drag on GDP. Consumers are holding up for now. And there is still an unspeakably huge amount of money floating around out there among consumers, businesses, and governments at the state and local levels, after the $11 trillion in stimulus in two years – $4.7 trillion from the Fed’s money-printer and about $6 trillion in government deficit spending. And some of this money will get spent over the next few quarters.

Yes, there will be a recession some day because sooner or later there always is, because recessions are part of the business cycle. But so far in the data, there is no recession being outlined. Consumer spending on durable goods has backed off from the crazy highs during the pandemic, as spending shifts to services, and overall spending growth is reverting from the spike during the pandemic to pre-pandemic normal. This normalization is happening, and that’s a good thing.

However, in terms of asset prices, there’s a rug-pull going on: The Fed has embarked on rate hikes and will soon embark on quantitative tightening, after interest-rate repression and QE have inflated nearly all asset prices to often ridiculous levels. So that’s where the action will continue to be.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wow I think this was a non pessimistic / non bearish article. 👍good news.

You should read my articles more carefully. I’ve been bullish on the economy for a long time (jobs, job openings, retail sales, consumer spending, etc.), and bearish on stocks, bonds, real estate, etc. Cryptos don’t belong in the list because they’re just gambling tokens.

People confuse the economy and asset prices. But they’re totally distinct. We can have decent economic growth and shitty asset markets.

I think the Fed will be lucky if they can ease out of the asset bubble. It’s just not normal for investors to take the losses without trying to get out the door before everyone else.

There might be some exceptions, but I don’t know of any asset bubbles that popped that didn’t cause the economy to go down with it.

I don’t know if decreasing asset prices will cause the overall economy to go down but I do think that asset prices influence consumption decisions. And the downturn in that consumption will influence the overall economy.

Consumption decisions are made not only by an assessment of where an individual perceives the state of their finances today but where they expect them to be tomorrow.

When the media begins trumpeting headlines about layoffs (like the 2500 people laid off from Carvana this past week), decreasing asset prices (particularly stocks) and other news of that sort it will affect the purchasing decisions of certain items. People who are experiencing job insecurity are less likely to consume.

No doubt that some consumption decisions in the past 2 – 3 years were made from the “irrational exuberance” that comes with high paper wealth. I think that particularly applies to financed items that require a long term monthly payment.

As my macroeconomics professor used to say “it is all about expectations.” So while I’d agree with Wolf that we can still have some economic growth while asset prices go down, the demand for some discretionary expense products/services during that downturn may decrease substantially.

Devaluation of fiat ,= inflation so fed can reduce all balance sheets. Don’t see any taxes being reduced,trying to drain billionaires assets ,they’ll just relocate

This isn’t an ordinary bubble. That’s what most imply who bother to acknowledge one even exists.

This is the greatest asset, credit, and debt mania in the history of human civilization. It’s not even close.

I get the rationale used in this article. I also know that “printing” and borrowing never lead to long-term prosperity. If it did, there would never be an economic contraction anywhere, ever.

The key is credit conditions, not specifically interest rates and not whether consumers need or want something. Without the loosest credit conditions ever, the economy weakens noticeably or dives into the dumpster.

If credit conditions remain at their 21st century sub-basement levels, the economy will continue to expand. But this isn’t just credit conditions in the US, it’s global especially in China and the EU.

Any actual financial market crash will send the economy into a steep recession because the fundamentals are far worse than the past, including pre-GFC. It won’t take much for the current demand to evaporate.

It’s not like a neutron bond where only financial values are destroyed while the economy is mostly or entirely unaffected.

Credit Bubble Bulletin is a good source to follow in real time. It’s bearish but not overly so.

“We can have decent economic growth and shitty asset markets.”

And yet, consistent asset inflation and consistently expansive wealth disparity suggest that asset markets have not been all that shitty. And they never seem that shitty for the big winners who always seem to win.

As for the US having “been in a deep depression every year since forever”, for 37 million Americans living in poverty it would seem to have been so. But that is not how a depression is defined.

Two-thirds of the population (70% of millenials) living paycheck to paycheck may also define economic conditions differently, but definitions, like history, are written by the winners.

John Williams just isn’t much of a fan of hedonic quality adjustments, or of a number of other statistical adjustments, but isn’t the best exponent of his positions, to put it at its sweetest. He’s surely not that well-adjusted, but then, so very few of us are.

Don’t mind me. I’m just being contrary. I’m an observer, not a participant.

I have been hearing this paycheck to paycheck doomsayers since 1990. At least there is paycheck. In most of the world there is not enough paychecks

It is very bearish. If we would avoid technical recession the FED has the green light to tighten the screws…

“I’m not going to make predictions about government consumption, but governments at all levels are floating in a sea of cash after the money-printing binge and the high tax revenues for 2021.”

I will, Wolf ; )

And this will have an significant impact (aka wild card) with keeping inflation high for the next 2-3 years. Our economy remains quite in terms of consumer spending, etc, with more delayed government spending to come. As such, this will make it harder for JPowell to tame raging inflation this year.

As we all know, he’s still moving WAY to slow!

I hope you’re right, but I’d bet that while, nationally, we may be OK (no recession), the areas with high concentration of money losing “tech” companies are going to take a big hit.

Wolf,

Who’s going to jump in a buy a big ticket item when they are looking at 30% loss in their stock or bond folio? These asset price drops can do wonders for consumer spending.

Ben Bernanke just said we are already in Stagflation. He should know. He had a lot to do with putting us there.

This is funny. Suddenly everyone thinks Bernanke is the new Jesus, after having himself screwed up so badly with QE?

The comments on Bernanke remind me of a former quarterback of the Washington Redskin football team, Heath Shuller, who threw more interceptions than completions and was cut after one year on the team. He later came back as an elder statesman commentator and was hailed as an expert on quarterbacking.

“We can have decent economic growth and shitty asset markets.”

So where are these dudes going to get the down payment for their homes, or money to buy a new car if their investments are off 20 to 30%. A negative wealth effect comes into play. A market crash could affect economic activity and I think it will in this case along with a lot of other factors such as an energy crisis and political instability.

The top 10% of the households own most of the stocks. But those are the wealthy, and we don’t need to worry about them. The bottom half of the income spectrum own almost no stocks. To bottom 80% hold very little. That’s why a stock market downturn, no matter how long, had only a minor impact on the overall economy. But 10% short-term interest rates would have a huge impact.

Hi Wolf thanks for the great articles. I would like to clarify a couple of things though.

1) The deficit spending, the money the fed printed, doesn’t that go into financing the government deficit(all of it is used to purchase bonds?) So the actual spending would be 6 trillion, but then again, the sale of bonds not purchased by the fed would need to take money out of someone else’s hands in the economy?

2) You say governments at all levels are sitting on huge cash reserves, but they seem to still be selling large numbers of bonds in the market. Where could I go to look at the actual balances.

3) IS the reverse repo market not a massive liquidity reserve that could be tapped by the economy at any time. for example as short term rates go up, a lot of those funds could exit the reverse repo market and get into government securities? Or is this a cushion that the fed is maintaining in order to prevent a meltdown of the repo market as happened in 2019.

The Fed’s stimulus went into the economy via the financial market (the “Wealth Effect”). The Government’s stimulus went into the economy via money given to consumers, businesses, and state and local governments. Both worked together.

Look at the huge budget surpluses in California and other big states.

Yes, the Fed’s RRPs represent liquidity that the Fed has pulled from the market temporarily by offering higher rates on that cash. So there’s $1.8 trillion that is part of the huge flood of cash that the economy is floating in. A lot of QT will eventually bring this to zero. But until then, it’s a sign that there remains a lot of — way too much — liquidity in the economy, and it’s hard to imagine a recession with the kind of liquidity floating around.

“But until then, it’s a sign that there remains a lot of — way too much — liquidity in the economy, and it’s hard to imagine a recession with the kind of liquidity floating around.”

But didn’t the vast majority of this “liquidity” get shoveled to the top of the food chain? So while the overall math supports the theory that a recession is a long shot, doesn’t the skew of this distribution portend badly for that position?

Reading reports that tech companies on the bottom of the chain (those other than FAANG) will be slashing staffs 20-40% . Which means job losses for those servicing these people. The flipping of the housing market and dramatic increases in construction costs (as well as the mortgage industry layoffs that you pointed out somewhere) will potentially challenge the entire “housing industry component” of GDP as contractors and worker bees encounter a dried up market for their services. I don’t think the economy can handle such a turn of events.

Not to mention the fallout to commercial real estate from pandemic related issue.

Billionaires will not come to the rescue of the working man or the economy with all this excess cash. They’ll be buying everything up.

Thank God government coffers are in great shape. But pension funds?

I’ve never found Wolf to be bearish or bullish—just accurate.

He’s pretty bearish. He publicly shorted into the middle of this last bull market. Not that I disagree now or then. But he did it.

Net exports… What a freak show!

Here is my take.

Airline fares. I booked a family 2022 vacation in Dec2021, and the price of that is up by 22%. As well the cruise we are on is up 21%

.

Lets not confuse inflation with real economic growth.

Good news I guess – the economy not likely to grind to a halt in the near future !!

I knew it was total lies just so they didn’t have to raise interest rates as much. In Canada everyone is broke but GDP has been expanding since last June.

If Q2 does the unwind, as Wolf suggests, we can’t technically claim the Recession (which started Nov 2021) exists. If GDP is the bellwether (not S&P or DJIA), then we remain “recession-less” for 15 years. Fed wins ??

Well, if you introduce enough new money, and spending goes up, then GDP goes up. But if you have increased inflation and increased deficits, is that a win?

is the “win” just making the case for MMT (modern monetary theory)?

GDP is an aggregate data point. It’s not an accurate reflection of increasing prosperity.

I’ve used this data multiple times here and I’ll use it again. Per FRED, “real” median household income and net worth have gone nowhere in the 21st century. This is even with fake “growth” from unprecedented deficit spending. QE, the biggest asset mania ever, and the lowest interest rates/loosest credit standards ever.

This statistical outcome is partly due to income and wealth distribution but not entirely. Not hardly at all IMO.

If both reflected a similar distribution to pre-1982 (about the start of the financialization era), inflation would have been much worse a lot earlier because it’s not possible to spend fake income and wealth on goods and services that don’t exist. The distribution doesn’t change the supply only demand. Less demand for financial assets and more demand for production without a corresponding increase in supply.

I’ve never seen it quantified but the likely reason aggregate consumer finances have stagnated in the 21st century is because the country isn’t actually wealthier. If it is, it isn’t even close to the increase in GDP.

Trade with China is snarling up again in Q2; wonder how much this will reduce imports?

Weapons exports to Eastern Europe seem to be up…

It’s an election year, and governments have money to spend, but in the absence of spare production capacity, that spending might simply overheat the inflation?

There’s a month and a half left in Q2 … a lot can change, and various credit markets are beginning to show some distress.

Jay Powell was re-confirmed on Friday and no longer has the risk of a Senate filibuster hanging over his job security. Will the Fed shift direction, and if so, which way?

“Jay Powell was re-confirmed on Friday and no longer has the risk of a Senate filibuster hanging over his job security. Will the Fed shift direction, and if so, which way?”

Why would they shift direction?

The Fed operates in the best interest of the Financial Industrial Complex, and has no need to ‘shift direction’. And for the present, congress votes in ways preferred by its campaign contributors, like the bankster owners of The Fed. Which is wrong, of course, but The Fed is never a campaign issue anyway, for reasons which should be obvious.

Trump pushed J Fowell around like a bully on the playground. Stand by your convictions,or your legacy is ruined .Might be too late

Foul

Yes, there’s going to be some of that too.

WWJD?

brilliant. more acronyms.

I know this acronym.

The answer is virtually nothing most contributors here or anyone else believes.

Go read what he actually said, not what so many claim he meant.

I don’t know who “he” is, and I have no idea what WWJD stands for.

Wolf should ban acronyms, except for FED. maybe WTF, though in poor taste.

AF-s’pose ‘J’ could refer to either the metaphysical presence or J-pow here and now…

may we all find a better day.

As food and fuel inflation keeps increasing, wouldn’t non-durable spending keep increasing?

Tremendously informative article, thanks.

My spending reflects this: I’m going back for discretionary medical services I missed.

Our CA governor is promoting a huge rebate to the public to spend down the state’s surplus (and supposedly compensate for inflation, especially gas prices). I guess this is inflationary again though: more stimmies. Maybe altogether this means too much cash circulating, still chasing goods and services, equals persistent inflation?

I wonder if some sloshes back into equities again.

Yes, Wolf’s articles are like cliff notes. They expain the real story. I like to call the Street Notes.

Why don’t he just lower the tax on gasoline?

They should save that surplus for a (lack of) rainy days, they’ll need it to buy water.

How is the aid (money+weapons) to Ukraine accounted for in GDP?

Money the government gives to other countries is not counted in GDP. The money the government spends to purchase arms from US arms manufacturers is counted. And given the gigantic defense budget (to include intelligence services, many of which are part of Homeland Security and other agencies, the nuclear weapons program which is in the Energy Dept., etc.), the aid to Ukraine is small.

I thought homeland security is mainly ICE and deportations? And that the ICE budget could thus be shrunk if there was some actual immigration reform?

Homeland security includes the Secret Service, the Office of Intelligence and Analysis, the Coast Guard, and other members of what is called the “Intelligence Community.” Homeland Security is huge, and came about after 9/11 to bring a lot of separate agencies under one hat.

Compared to the Huge 4 (Social Security, Medicare, Medicaid, and Defense), the rest of Federal spending tends to be smaller-ish (collectively) or tiny (individually).

Unless the Huge 4 are bought under control, little else really matter in terms of Federal spending.

They are the drivers of the endless fiscal nightmare.

CAS127, including Social Security in that group is totally ridiculous! It may need occasional fine tuning, but is the only good program that operates near its budget.

This is the problem of ‘bundling’ things together, of which the parties are experts.

Dawns,

The facts are the facts…SS accounts for a huge percent of Federal expenditures and there is no “magic lockbox” where previous decades’ surpluses got “saved” (those surpluses got spent as they came in – by earlier generations of degenerate politicians – the money is long, long gone…but the looming debts remain).

The SS system was *always* designed to work in this inherently corrupt fashion – so I’m not sure how you think it “functions well” on a societal level.

The only fix that talent-free DC has for the looming disaster of unfunded entitlements is the same ruinous one that it has made more and more use of, printing money (read horrible consumer inflation).

The facts are the facts, and the disasters to come are the predictable consequences of 60 years of absolutely shitty, shitty government (abetted by incest partner MSM, who worked every day to keep the public ignorant of how these programs actually operate).

It could have been fixed, but the American political leadershit felt it wasn’t in their interest.

It is far too late to fix now – until the system breaks down, printing/inflation will be used to “cover” the corrupt promises made over the last 60 years.

All the charts are in 2012 dollars except for the second chart, which is chained to 2021 dollars, and the shipment volume chart. Some of the charts go back to 2008.

I guess my question is what motivated the BEA back in year 2008 to use year 2012 as the base or reference to allow for adjusting for inflation?

The “2021” was a typo. Should have been 2012. Thanks.

The shipping chart is not in dollars, but it’s an index of volume.

The BEA will shift to “2022 dollars” pretty soon for its inflation adjustment.

Thank you.

Why is the BEA using dollars chained to 2012? Is there statistical significance or is it because it is 10 years back and hence, somewhat arbitrary? If arbitrarily chosen, why not use a stationary reference instead, like chaining dollars to the time of the Big Bang, for example?

Using dollars of a past year is how inflation adjustments to dollar figures are expressed. If you go back too far, the dollar figures become too small to be meaningful.

For example:

Q1 “Nominal” GDP, which is not inflation adjusted ran at an annual rate of $24.4 trillion in “current dollars.”

Q1 “real” GDP (adjusted for inflation) ran at an annual rate of $19.7 trillion “2012 dollars.”

If you use “1950 dollars,” Q1 “real GDP” might be only $280 billion. This number is meaningless. That’s why a more recent year is used, and why the year gets moved up at regular intervals.

FAR from ”meaningless” Wolf,,,

using older ”basis” for GDP shows all too clearly the terrible degradation of the USD since the Federal RESERVE Board took over our ”money” supply in 1913.

That IMHO would be the real reason ”they” keep bringing forward the basis for comparisons.

Even with the so called hedonistic adjustments, the officially admitted by the BLS inflation calculator value of the March 1913 dollar compared to March 2022 is $29.34

Absurd isn’t in it!

This analysis is fine work, Wolf.

“Consumer spending has been switching to services on a large scale, from goods (all adjusted for inflation).”

Wolf,

I wonder how much the increased spending on services is a reflection of price increases and not actual demand since the phony inflation figures cannot possibly adjust for it?

So if airfare from here to Europe increased 30% due to fuel costs, and hotels charge 25% more now, that spike does not seem indicative of real demand. I see the same issue with paying for babysitters, healthcare, auto repair, restaurants, etc. They costs for services have exploded to the point where I am not sure if the inflation figures adjust for it.

Example: A recent quote for replacing brakes on 4 wheels plus rotors for $1,200 on a VW. Something like this would have cost $600 before the pandemic.

Thanks

John Apostolatos,

If you believe the Shadowstats BS, you cannot do math. According to Shadowstats, the US has been in a deep depression every year since forever. This is just a willful malicious lie. The guy is totally nuts and pollutes the minds of people who refuse to or cannot do math.

Inflation is personal. Everyone feels it differently, but this is the most grotesquely overstimulated economy ever, and excess demand is a big part of the problem, and if you don’t get this, you completely misread this entire website.

Judging inflation by anecdotal stuff is BS. Some things I pay for have gotten cheaper, including my broadband connection when I switched from coax to fiber a few months ago (plus I got 15x the speed), and my wireless service. No one ever talks about stuff that gets cheaper AND better.

Whenever I hear about Shadowstats, it’s in the context of how the government computed inflation differently during the 1970s-1980s. Have you considered showing what current inflation would be if it were computed under the old criteria? Thanks.

Just do the math on Shadowstats. That will tell you that it’s total BS. That guy has been debunked, including by me, a billion times.

The trouble is, it is impossible to compute CPI today as they did fifty years ago! Then I will cotradict and say the way CPI is computed it is done the same way all the time.

The culprit is the metodology behind the CPI. It measure the price increase on an over time variable selection of consumer goods. Where the weight each item is given change with time.

And to measure the CPI the selection of goods must change as consumers buy other things today compared to fifty years ago!

In essence, someone is selling rubber bands by the feet.😉

All too true. Get enough people like that together and the country would be doomed.

I’ll defer reiteration of one of my primary theses at this point. It does get boring after a while.

“Have you considered showing what current inflation would be if it were computed under the old criteria?”

It’s been done, but not by John Williams. He just plugs in a fudge factor, and it’s dishonest.

The adjustments made to how inflation is calculated are valid, and disliking them because they make things more difficult to afford isn’t a valid approach to discrediting them. That New and Improved products are in fact better than the old ones is objectively factual, and better necessarily costs more than worse. That cheaper obsoleted products often become unavailable, even though they’re serviceable, is a separate issue.

Introducing irrelevant information and avoiding relevant information doesn’t help either. Then there are the emotional appeals, apriorism, and straw men; weak analysis, where there is any, makes it too thin to hazard the more sophisticated fallacies. Shadowstats might look good, and getting your buttons pushed might feel good, and it does get some things right, but in sum it’s too misleading. Good economics can be hard enough to come by under the best of circumstances. The sooner you sour on shadowstats the better off you’ll be.

unamused,

Well said. Thank you!!

“better necessarily costs more than worse”

Tell it to the electronics industry.

Or commodity producers.

In fact, the increase in technology and the increase in the dissemination of knowledge tends to *lower* costs for the same or better products.

Unless snake government tries to steal the resultant wealth through engineered stealth inflation (just enough G money printing to offset tech cost improvements) and lecturing about the evils of “deflation” (known as affordability to the non political lizard humanity)

Okay, but if you go on an annual road trip, and gas costs 25% more, motels 30% more, and food 20% more, over an identical trip taken last year, GDP is increased solely as a reflection of increased prices.

Also the wear on your car is more expensive and to be reflected when you get new oil change, tires, brakes, etc.

same demand, more money ……………… increased GDP

NOPE, ALL GDP data that I used here is adjusted for price increases, and I said this a million times in the article.

“Nominal” GDP, which I didn’t discussed here, is not adjusted for inflation, but it spiked 10.5% year-over-year.

Nice! I wish Com-circum-cast had those deals.

Would love to see you invite the ShadowStats nut job onto one of your podcasts. Fireworks, baby!

While he may or may not be a crackpot, I whole heartedly agree with this statement from the ShadowStats website:

“With the misused cover of academic theory, politicians forced significant underreporting of official inflation, so as to cut annual cost-of-living adjustments to Social Security, etc.”

When CPI was 2.5% on average between 2012 and 2019, he said it was 10%+. That’s total BS. It would have made “real” GDP growth negative by 5-6% every year, year-after-year, and by 2019 there wouldn’t have been any kind economy left. This is just idiotic and doesn’t deserve any kind of discussion. You cannot have a discussion with a moron that spreads that kind of braindead crap. If he had said real inflation was 3% or 3.5%, when CPI was 2.5%, there would have been a lot to talk about and a lot of common ground.

“When CPI was 2.5% on average between 2012 and 2019, he said it was 10%+. That’s total BS. It would have made “real” GDP growth negative by 5-6% every year, year-after-year, and by 2019 there wouldn’t have been any kind economy left.”

I’ve never looked at his website until today. However, I do believe wholeheartedly that BLS underreports inflation for the stated purpose. However, I don’t agree with 10%. 1-1.5% common ground, but today it’s more likely at least 3%, possibly as high as 4-5% if housing costs were expanded beyond rent. But, that’s what happens when we have the “most grotesquely overstimulated economy ever . . .”

Thanks, Wolf!

Wolf,

As you have pointed out before, housing costs make up a big proportion of the services GDP (the biggest by a lot, right?) and you have also pointed out the absurd spikes in home prices/apt rents.

These facts alone make it more than reasonable to look at inflation as being a dominant driver of GDP “growth” – without having to get into the weeds on every item in the CPI basket.

If you save $20/month on internet services (and I’d really like to know your provider and if they are nationally available…) but your rent has gone up $300 per month, we really don’t have to argue over the price of beef and orange juice (btw…).

“These facts alone make it more than reasonable to look at inflation as being a dominant driver of GDP “growth” ”

That’s just BS. ALL GDP data that I used here is adjusted for inflation, and I said this a million times in the article.

“Nominal” GDP, which I didn’t discuss here, is not adjusted for inflation, but it spiked 10.5% year-over-year.

“If you save $20/month on internet services (and I’d really like to know your provider and if they are nationally available…) but your rent has gone up $300 per month….

65% of Americans own their own homes. Their housing costs didn’t change at all!! People, don’t ignore that biggest facts right in front of your face!!

“65% of Americans own their own homes. Their housing costs didn’t change at all!! People, don’t ignore that biggest facts right in front of your face!!”

Maybe I’m missing the point you’re making, but I know my property taxes and hazard insurance have gone up notably in the last 2-3 years. Certainly, they’ve risen faster than normal. Some people’s HOA and utilities have gone up. Not sure if those get captured in rent or OER as calculated by BLS.

But, those 65% of owners have seen their costs rise.

The point was the anecdotal increases in some prices as experienced by someone somewhere, such as a $300 rent increase cited by cas127, cannot be extrapolated to a national inflation rate. Doing so just creates BS.

Wolf, your Shadowstats comments has saved me from ever sending money. It is probably one of many that brought me here in the first place.

Keep up the good work as I can afford it.

Ridin scots ain’t all fun and games! Its sometimes work with what’s on the road.

VVNvet may want to look at Depression wages versus todays.

Order parts online – watch u tube video pretty easy job ,if you have any tools . Was brought up ,taught how to fix my own vechile now only oil ,filter changes and brakes . Your being raped

Yep, thank god for youtube/the internet.

And, in broader terms, 20 years of the G treating deflation as evil incarnate (and, by implication, inflation as some sort of idiot elixir) is a strange, strange world to live in – treating inflationary rape as some sort of magic.

It was the perverted result of the G being a massive debtor who controlled the printing press.

Flea-plenty are more than willing to leave the technical, hands-dirty jobs to others and complain about the expense, youtube or not, especially those in their advancing years…(hat off to you! have wrenched my own stuff ever since i figured out in the early ’70’s that it would be the only way to continue to afford/enjoy motorcycling at the level i wanted. Have lost count of the number of folks who approach me thinking i’d be happy to repair their vehicles for little or free just because they saw me doing a renovation/restoration. The shocked look at what i say i would do it for (well above local shop levels), if i did (and i don’t, except for VERY close friends who swap their own specialized knowledge/expertise with me, and family youngsters willing to learn how on the way to doing their own work), is priceless.

may we all find a better day.

I guess, as always, a country is split into parts. There are parts where people earn a good living, maybe work from home, have a fixed rate mortgage and little debt, this world is not yet in a recession.

Another part is where you earn a lower basic wage (or have a fixed income), maybe have to drive to work, pay rent, have some debt and live paycheck to paycheck (40-70% or so of the USA, so some say???)…I guess this part clearly is in a recession and would explain why the foodbanks are running dry.

Recessions always start with the poorest, it’s when it reaches the better off that the screaming starts…..

Don’t forget, for US figures, companies like Apple, Amazon, Netflix, Microsoft are international companies and make huge parts of their profits and turnover from a rich UK and Europe, (pop 460 million) whose people are now cutting spending like you have never seen….and those companies bring parts of their profits and turnover back to the USA…..

They also appear (like many other US companies) to have lost the Russian, Belarus, Ukraine market for awhile….(population approx 200 million)

I did forget to mention one of the biggest businesses of the USA is war, so huge amounts of dosh will be heading to the USA to buy weapons… I think that could outstrip anything else…. who knows??

“ Recessions always start with the poorest, it’s when it reaches the better off that the screaming starts…..

When you are poor, everything is expensive…

Even the cheap stuff…

and as prices rise for the cheap stuff, more people become poor

At the margin, much of if not most of discretionary GDP is contingent upon the top 5% or maybe 10% of spenders. It’s these people from the income and wealth distribution to keep the economy expanding or afloat. The bottom 80% don’t have much discretionary purchasing power.

Their affluence is also contingent upon the asset mania. Without it, their mostly inflated fake wealth takes a huge hit Their income is a lot more contingent upon the asset mania than most believe too. A noticeable percentage are dependent upon fake economic “growth” to provide the income for their spending habits.

Parts of China are closed for most of Q2, less shipping to US, so most likely overall import will be less and trade deficit figure better

Official inflation number is 7-8%, if same methods used in US as in Europe, then real like inflation, the true one is 14-16%

Keeping this in mind, real economy is and will be in recession, no matter what official numbers will try to paint

Once the excess liquidity is out, this will be clear. But this won’t help much with getting inflation lower, as there still will be too much liquidity left for shrinking economy.

For some inflation may be 14% but for others it is less. If you pay rent, drive, buy food as a large part of your income then maybe but I don’t rent, have no mortgage and don’t drive that much…

Saying that, my heating gas and electricity just jumped 54% and food is up, so my inflation will be just below 10%…..

Dude, forget Q2, try mid-2023.

China just cancelled a massive pan-Asian soccer championship they had agreed to host in June of 2023.

June of 2023.

Sh!t is breaking loose over there. When North Corea implodes and refugees start swimming across the Yalu river all hell will break loose.

Gird your loins, ladies.

The virus hit N.Korea. It spread during the last military parade. Kim J

and his generals were muzzled with a face mask. When the pandemic spread three ballistic missiles took off from their underground pads.

King Kim rejected Moderna, Indian or Chinese vaccine. Twenty seven

million N. Korean are locked down.

Dictators are locking down 27 million people, because inflation

is raging in N. Korea.

Argentina hyperinflation sent protesters to the streets.

N. Korea is always in lock down for the past 50 years. LOL

Our U S biggest problem is that we only export 10% of GDP ,corporations Apple ,Microsoft Gm all made trillions on cheap labor. Mexico,China ,S Korea . Now everyone is bringing manufacturing home ,seems global just in time doesn’t work well

OM, one just has to look at the dismal level of Consumer Confidence of late to get a non-stats view of the U.S. economy going forward. You don’t spend freely when inflation is eating your lunch (and dinner), you have a sick feeling when watching the evening news about our dysfunctional Government, your 401(k), if you are lucky enough to have one, looks like the poker table at Vegas (house wins, you lose), and you are noticing more and more empty shelves at the grocery store.

A sudden and severe drop in Consumer Confidence is all you need to look at for a recession forecast in May of 2022, forget about studying the entrails of the chicken. New York Fed GDP print just came in at a negative reading vs. very positive estimate; watch for more of these regional GDP air pockets. Just takes a handful of economic regions with the highest GDP per population to go South to begin to drag the rest of the U.S. economy with it.

Just think we are more into the Recessionary Quagmire than current government statistics would imply.

@ David W Young and Wolf –

not to mention people needing baby formula that can’t get it at any price ……………

starting to feel like a third world country …………….. thank you FED

If you are dog-paddling across the Rio (I almost said “swimming”, but I haven’t seen an Australian Crawl stroke yet!!), I just bet you can get all of the baby formula your whipper-snapper could need in a year on the America side of the Free Zone. Hey, everything is free in the Untied States, and the streets are lined with Gold. Ooops, it actually is gold-tinted tinsel!!

Of Course WE,,, in this case WE the PEONS, are in recession,,, and it absolutely does NOT need any of us to hear it from some talking head of the GUV MINT who are always doing their best to support the current executive branch administration to know this.

WE know this because WE are suffering directly each and every day from the incredibly incompetent decisions of the so called Federal Reserve and SO many other unelected ”boffins” making decisions without any ”legal” basis.

That has certifiably been going on in many western EU nations for centuries; that the same process has been going on in USA for the last several decades should be IMHO the very top of the ”agenda” of every concerned person in USA…

Not going to end well with this crash that will very likely be much worse than the last crash, and might very well be the worse crash, world wide, in the ”modern” era…

Hope for the best,,, but far shore prepare for the worst!!

It was the Empire State (New York) Fed manufacturing survey that printed a negative 11.6 reading yesterday when estimates were for a positive 15 reading. Another outlier?? Me thinks not, just another shrill and squawking canary in the coal mine.

OM< Your statement the economy "is" in a recession that the "real" rate of inflation for all of the US is "14-16%" is unadulterated homemade BS and doesn't belong on this site.

It’s my idea, in case same methodology is used in US, as in EU

In EU, official CPI is around 7.5%

And I wish, it was only 7.5% :)

Doing complete home renovation now. Was lucky to negotiate and prepay most of materials and labour in last year August. Some unexpected stuff poped up later on during the winter, like the need to replace the roof and completely rebuild the terrace. While doing all necessary paperworks for this, over last 2 months metal parts +50%, wood +100%, labour costs up, some small items up 200% or more. So, overall, roof +40% compared to initial estimate, terrace +80%. That’s a lot of price increases in just 2 months time.

Home heating bill up 2 times compared to last winter

From some other small stuff, like the groceries bill, is +20% compared to this winter.

And just few hours ago got bill for steam sauna we are doing. Equipment price is fine, payment deadline is 10 days, and a note that prices will be up 10-30% from 1st June depending on a model.

All this just does not make me believe in official numbers.

Yeah, you only add the stuff that went up. Now add all the stuff that didn’t go up (0% inflation) and all the stuff that went down (deflation). For example, my broadband subscription plunged 40%, and the speed increased 15x, and my cellphone service got cheaper a bunch. My new laptop got cheaper….

This is why extrapolating from the anecdotal stuff to the US average overall is just cherry-picked silliness.

@ Wolf –

Okay, electronics, and communications in your specific location got cheaper.

What else?

cb,

You don’t get it, do you? Using anecdotal prices that you experience to come up with a national average is BS. I only have to come up with one single counter-anecdote to prove your anecdote wrong. You can say, “my costs went up x%,” and that’s perfectly good, but you cannot say that “therefore the national inflation rate = x%.” That’s what this whole thing is about.

@ Wolf –

Yes, but do you understand that the CPI with their hedonics and selective substitution is complete BS.

The real issue is that they digitize more dollars from nothing (inflation 1), driving up prices (inflation 2). They do this while suppressing interest rates, which exaggerates both inflation 1 and inflation 2. The net effect is to make the dollar worth – less, steal from savers who hold the dollar as fruits of their past labor, and reward borrowing and debt based financial engineering.

The FED/Bankster/Wall Street/GovernmentComplex does this while inside trading, misleading and lying about what they are doing. Food, rents, education, healthcare, etc. all up. Dollar purchasing power down. Concentrated wealth up. Working class security down.

I think i get it.

cb,

“Yes, but do you understand that the CPI with their hedonics and selective substitution is complete BS.”

Nope. This is just nonsense. The hedonic quality adjustments make fundamental sense, and I agree that they’re needed.

A Mustang today cannot be compared to the 1968 POS deathtrap that I used to drive in the 1970s. These new vehicles are a gazillion times better than those from prior years, in a gazillion ways, and so you’re not buying the same product. You’re buying a much-improved product. And the costs of the improvements are not due to the loss of the purchasing power of the dollar but due to the improvement of the vehicle.

Consumer electronics have gotten a million times better and a lot cheaper at the same time. I paid $4,000 for my first computer in 1985, and it came with two floppies, no hard drive, and had 640 kilobytes of memory (which is near-zero by today’s standards). Now you can buy a laptop with a 1 terabyte hard drive, 256 gigabytes of SS drive, and processing power that a supercomputer in 1985 couldn’t match, all for $1,000. You need to understand the importance of this in terms of CPI and hedonic quality adjustments.

Inflation means the loss of purchasing power of the dollar, not paying more for much much better products.

You’re not buying the same products for the same amount of money.

I might quibble a little with the amounts used for the hedonic quality adjustments. But I don’t have hard data to show where exactly I would disagree. But my gut says that the hedonic quality adjustments are a little (not a lot) aggressive.

BTW, hedonic quality adjustments are applied only to certain durable goods, such as cars, and therefore in the overall CPI play only a small role. People who blame the hedonic quality adjustments for a huge gap in where CPI is and where it “should” be don’t understand how the CPI is structured.

@ Wolf –

Fair enough. Well written.

Consumers have benefitted by economies of scale and innovation which has pushed down prices. Good engineering, production and management practices have been beneficial.

The FED/Bankster/Wall Street/Government created debt society, on the other hand, has been a disaster for consumers. Anything financeable ………….. shelter, health care, education …… has had inordinate inflation.

Inflation varies depending on your lifestyle. I tend to agree with OM that it is closer to 14% to 16% for most people. Even David Stockman agrees. For me and my family its closer to 3 to 4%. This is based on actual data and monthly expenditures which I track.

“Government deficits add net financial assets and surpluses remove net financial assets.

This is a massive fiscal tightening. Buckle up.” ?

https://twitter.com/cullenroche/status/1523790681705132032?s=20&t=eZHWxx7_Q6ENtuK-YnQZog

1) The dollar is strong, because we no longer visit London, Paris and Rome.

2) Turkey will be on the back of list for F-35 to smooth their resistance

to Finland.

3) ASEAN nations,fearing China will keep our defense industry busy for years. Trade with ASEAN nations will rise at China expense.

4) Real Spendin on Service is shooting to the moon. GDP components will gradually change in the next few years : mfg will rise at the expense of service and import.

5) Infrastructure, mfg jobs and moderate inflation will boost real wages

and productivity.

6) Innovations will reduce housing prices.

7) Losing the House will be a gift to the US economy.

How will innovations reduce housing prices? Housing prices are a function of supply, demand, loose money and government/bankster supported lending programs ,,,,,,,,,,,,,,,,, and a good amount of hype induced FOMO (fear of missing out and being perpetually poor) and FED induced rent increases.

you are forgetting the RED TAPE component of housing — and all construction including petroleum refineries, etc — cb

Older friends in coastal CA just spent 5 years and $300,000.00 JUST GETTING THE PERMIT to build a new totally wheelchair friendly single family home on land that had been owned by their family for couple of generations.

Others on here have mentioned the decades it takes to build a new refinery.

@ VintageVNvet –

absolutely correct! the fees and red tape are ridiculous.

(you and I have spent time in some of the same areas – Florida, Bezerkeley …………… and similar businesses, so I relate to many of your stories)

Won’t the ongoing rate hikes combined with a reduction in fiscal support lead to a recession?

If inflation doesn’t come down, a recession is the only thing that will bring it down. And ultimately, that’s what we might get, and it’s part of the normal business cycle. It’s just not in the data now. This is still the most overstimulated economy ever, and trillions of dollars from that stimulus are still sitting around at all levels to get spent. Government consumption is not going down quarter after quarter. Governments are swimming in cash. They’re going to spend it. Don’t worry about that part.

Yup.

https://fred.stlouisfed.org/series/NA000333Q

1) AAPL is doing well in N. Korea : 27 million people are locked down

spending money on Korean restaurants.

2) Shanghai was locked down, people are playing video games on AAPL.

3) AAPL is doing well in Ukraine, watching Ukraine winning the Eurovision.

4) AAPL is doing well in Europe. People are watching the news all day.

5) ARAMCO is number #1. AAPL is behing only temporarily. If wrong : good

things will happen to the US economy : rotation from bs to real stuff.

The real economy and the asset economy have decoupled.

The asset economy can’t decouple entirely from the real economy. The parasite is still dependent on the host. But just try explaining that to the parasite.

Wealth disparity is taking care of that ……………

The wealthy claim they are the host, and all the people serving the wealthy, are living off the generosity of the wealthy

and a lot of broke hillbillies buy into that logic, and vote accordingly

All too true. Get enough people like that together and the country would be doomed.

I’ll defer reiteration of one of my primary theses at this point. It does get boring after a while.

We may be seeing a glut in SOME durables this year, then? If I’m reading right.

Some already there…

Checked appliances at the big box guys, free home delivery within 2-3 days now…

They are offering some discounts…

But the prices… oh my…

A Samsung front load washer/dryer set in I bought in 2018 was $1200… same set today… $2200…

Bought a microwave at Best Buy 270$ GE seems about right ,business are raping u ,but umust be willing

I believe the numbers will eventually show most threw the inflation costs onto their credit cards…..and once maxed out……key consumer numbers will drop. IMO. Gasoline purchases, food, etc…

Behavioral changes havent kicked in yet, IMO.

Restaurants (perhaps the ultimate discretional expenditure) will be first to be effected…IMO.

Nominal GDP grew. This growth is in dollars not adjusted for inflation.

S&P 500 earnings reports showed increased earnings per share for Q1 2022 compared to Q1 2021.

I remember there was an Arab oil embargo decades ago that was said to have caused a recession. People waited in lines to buy gas at gas stations.

Start of American downfall ,we got oil they got our money ,meanwhile stupid politicians did nothing to stop bleeding = renewables,

Does the Atlanta Fed GDP now model account for this import/export anomaly? I see in its current estimate of Q2 GDP it’s at 1.8%, which would still be very anemic when taken with the -1.4% for Q1.

Thanks

anecdotal evidence of big inflation coming in services numbers – our neighbor is vp of hr for a large regional accounting firm – she told us they can’t keep people -lots of turnover with people leaving for higher salaries or wfh opportunities – their costs are rocketing up – good news – no problem passing those costs on and then some! profits are strong and growing

I believe GDP doesn’t take into account inflation.

If true, then that would be a major offsetting factor on the plus GDP side of the equation: it contributes to “GDP” but is not actual growth.

“I believe GDP doesn’t take into account inflation.”

GDP figures are normally inflation-adjusted. That’s what “chained 2012 dollars” means.

GDP does not account for debt. Try working with that. What happens when debt increases faster than GDP?

c1ue,

RTGDFA

ALL data here is inflation-adjusted as I pointed out a million times in the article, including GDP, consumer spending, inventories, trade deficit, etc.

“Nominal GDP,” which I didn’t discuss here, is not adjusted for inflation. Nominal GDP spiked by 6.5% in Q1, and by 10.6% from a year ago.

Russia pacific fleet can beef up the seven fleet.

Thanks, Wolf;

I would be a bit cautious about treating ‘goods’ versus ‘services’ as a binary decision tree. Services include goods. As examples, an airline needs petrol and spare parts; a plumber requires pipe, solder, tools; a hotel relies on food – all substantial goods. If the cost of these goods components escalates sufficiently due to scarcity, that will have a non-trivial effect on the price of services. As pricing for these ‘discretionary’ services rise, the average consumer will either eliminate or reduce them in his/her budget.

“airline needs petrol and spare parts;”

That’s not consumer spending; that’s business spending, which is a separate category in GDP, but it’s small compared to consumer spending (consumer spending = 70.5% of GDP in Q1).

Just one comment- if the US decreases its imports from the rest of the world, it is also likely the rest of the world will decrease its imports from the US. The net number might not change that much going forward. Sure, the last quarter was a particularly bad decline in the net position, but that trendline down is 7 quarters in duration- how much recovery can we really expect? Additionally, the trend is still on that 30 year long line, too, or catching up to it again.

Yancey, the recent surge in the Battered Greenback due primarily to a domestic surge in U.S. interest rates, will guarantee that Exports going forward are going to be adversely affected. Add in a Europe for one where energy costs are going thru the roof, and don’t look to Europeans to buy American goods increasingly at a higher cost in domestic currency. Perfect economic storm for a Global Recession, not just a U.S. recession.

DXY up 16% from a year ago.

O, I wish I was in DXY, hurrah, hurrah.

LOL, thanks for the morning lift!

Don’t forget the later line:

Live and die in DXY

Wolf said: ” And there is still an unspeakably huge amount of money floating around out there among consumers, businesses, and governments at the state and local levels, after the $11 trillion in stimulus in two years – $4.7 trillion from the Fed’s money-printer and about $6 trillion in government deficit spending.”

—————————————————–

Is it true that only the $4,7 trillion from the Fed’s money printer is the only new money out there?

Is there a way to know if a portion of The $6 trillion in government deficit spending constitutes new money? i.e. If it was borrowed from private entities, it would not be new money. If it was borrowed from a bank, it might be new money.

@ Wolf –

By pointing out stimulus of $11 trillion, $4.7 from FED new printing and 6 trillion in government deficit spending, is that not double counting?

One went to the markets (to inflate asset prices), the other went to consumers, businesses, and state and local governments.

So 4.7 Trillion new FED created dollars went into asset markets, while $6 trillion Government deficit spending, financed by existing dollars (dollars already in the system) took place.

Incidentally, I would think that for the $6 Trillion to be considered Corona related stimulus, then that $6 Trillion should be additional to what deficit spending would have normally have taken place.

Your clarifications are always appreciated.

Government deficit spending (spending money that the government had to borrow) is stimulative, by definition. If the government only spends what it takes in from taxes and fees (a balanced budget), it’s neutral.

> Consumers are holding up for now.

How long can they hold up with:

(1) Inflation taking big chunks of incomes for several months now

(2) the reverse-wealth effect – interest rates have been going up for several weeks now and mortgage refinancings are a trickle of what they were in 2020 and 2021.

Yes, there is still a lot of money in bank accounts which I would guess is with the higher income/asset groups. Can we count on them to keep spending or resort to some belt-tightening? Will they spend enough to keep the economy afloat and the GDP positive?

Ethereum co-founder says every ‘average smallholder’ impacted by Terra’s stablecoin crash should be made whole, cites FDIC’s $250,000 as ‘precedent’

Wow. Cryptos are an asset and not someone’s cash savings. That would be like making everyone who buys a house that goes underwater should be made whole.

The Crypto crowd is really getting pretty bold.

Or what?!!!

I believe imports have a neutral impact on GDP. Importd are included in consumption and then reduced by the import amount. Thus a net wash and no impact on Gross Domestic Product. The formula creates confusion as people don’t realize that imports are included in two spots when GDP is calculated. Do the people I follow have it wrong, doesn’t seem like it. Thanks Wolf as always.

Nick,

No. You’re leaving out the import element. Think about what imports actually are: with imports, Americans spend their money overseas, which adds to the GDP in those countries, and subtracts from GDP in the US.

If Walmart imports a widget at a cost of $10 at the port, it’s an import and the $10 is subtracted from GDP. When Walmart sells it for $25 in the same quarter, the $25 is added to consumption, but since the $10 was imported and subtracted, the net effect on GDP in that quarter is +$15 ($25 – $10).

If that widget had been manufactured in the US, without any foreign materials, the net effect on GDP would have been +$25.

Bitcoin will not become an alternative form of money, or a store of value, says Bernanke

How a bitcoin market ‘in extreme fear’ compares with the past, and what to expect next

Crypto speculator Barry Silbert offers sympathy and advice to those who have lost fortunes this week

GDP drop equals supply chain disruptions. The process of repatriating US domestic production will take some time, and then we can have tariffs.

Tariffs make companies lazy.

That’s the wrong way to look at it. Tariffs resolve trade imbalances, which strengthen economies and societies.

Persistent trade imbalances are extremely harmful in the long run. Tariffs force companies need to invest in the jurisdictions they operate in, which is required for sustainable long-term growth.

Thought being if you don’t have companies to compete what is the point of trying to protect their business. Gorby the notion goes from Nietzsche to Darwin that competition degrades the product and the producer.

“Persistent trade imbalances are extremely harmful in the long run.”

Agreed. If nothing else, it makes obvious dependency and a lack of self sufficiency…..national security issues.

Even Adam Smith held that certain industry that is essential to the existence of the nation state must be protected.

Yet the left leaning academics (globalists) maintain that trade imbalances do not matter, for the dollars must return to the host nation. What they miss is the change in ownership and control that comes with that return. IMO

Thank you Wolf…….this site is the best. It definitely helps clarify the news we hear……and anticipate the future.

Counting on consumer spending consistently outpacing inflation, which in turn is outpacing wages, seems a tenuous hope for avoiding recession. If inflation doesn’t moderate soon, the only way consumer spending drives growth is via higher credit debt. Spending via HELOC is going to be minimal, and most of the population has very little savings (again).

Most of the spending increase since 2008 has been due to increasing government spending which then shows up as consumer income. That’s the primary “growth” driver. This is evident in the deficit as a percent of GDP prior and subsequent to 2008. If the deficit as a percent of GDP after 2008 had trended as it did even from 2001-2007, there would have been virtually no “growth” at all. It’s completely artificial.

The second primary factor is the loosest credit standards and lowest interest rates in history. The bond mania appears to be over. As one example, interest rates on BB and lower rated corporate (junk) debt have already “blown out” and the bear market is just getting started. It won’t be long before a noticeable percentage of public companies are “sucking wind”.

Wolf,

Another excellent analysis. It would be helpful for your readers if you could drill down and explain the gap in real spending on services since 2020. For example, is it cruises, air flights, concerts, etc. And how much will the reported surge in US COVID cases effect the recovery in real services (this is a tough one)? Also, keep an eye on the dollar.

Given the level of inflation be it in commodities supporting the production of goods and or the labor force, and one can debate the real level of inflation, are production and service numbers really comparable to the historic time series. A service that now cost 10% more whose indices increase 10% is not growth?

TYVM for this awesome insight Wolf.

MKts expect Mr Powell to turn around after a couple of rate hikes! Every times he opens his mouth, how he is control inflation, he wishy-washy and wobbly.U.S. stocks finished sharply higher Tuesday after Federal Reserve Chairman Jerome Powell said a “softish landing” for the economy still was possible. The Dow Jones Industrial Average DJIA, +1.34% advanced about 431 points, or 1.3%, ending near 32,655, up for a third straight day in a row. It also marked the biggest daily percentage jump for the blue-chip index since its 1.5% gain on Friday, according to FactSet. The S&P 500 index SPX, +2.02% rose 2%, while the Nasdaq Composite Index COMP, 2.76% closed 2.8% higher. Powell said there are a number of plausible paths to slowing inflation without sparking a recession, even if it causes Americans some pain, while speaking in an afternoon talk at The Wall Street Journal’s Future of Everything event…”

h/t marketwatch

Mkts beileve that he is DOVISH at heart and has NO guts like Mr. Volcker!

Only a rip roaring inflation will force Fed. Mkts reaction today proves that.

Wait n See

There was zero wishy-washy in what he said. Zero. The wishy-washy interpretation is just wishful thinking by the markets. The Fed has a plan. It announced the plan. And it’s sticking to the plan. It has stuck to the plan so far. There will be no surprises, one way or the other. Rate hikes and QT as planned.

JP will keep on JAW BONING his mantra ‘ Soft Landing is still possible’!

He doesn’t want to shock the mkt, right? Even Mr. Barnake has come out swinging against Mr, Powell. Says he is behind the curve. IMHO Mr Powell is a smooth talker but ingenious, insincere and dishonest

“Bernanke spoke with CNBC’s Andrew Ross Sorkin in an interview during Monday’s “Squawk Box” show. He told Sorkin, “The question is why did they delay that. … Why did they delay their response? I think in retrospect, yes, it was a mistake.”

Inflation has become one of the most severe threats to the economy. Bernanke said, “And I think they [Fed] agree it was a mistake.” He explains why the Fed missed the window of opportunity to tighten:

“One of the reasons was that they wanted not to shock the market.

“Jay Powell was on my board during the Taper Tantrum in 2013, which was a very unpleasant experience. He wanted to avoid that kind of thing by giving people as much warning as possible. And so that gradualism was one of several reasons why the Fed didn’t respond more quickly to the inflationary pressure in the middle of 2021,” he said.

h/t zh

sunny129 said – ” IMHO Mr Powell is a smooth talker but ingenious, insincere and dishonest”

————————————————

now, there is an understatement. And that applies to everyone of those FED bastard’s since and including Greenspan …………..

cb

You are correct.

But Mr Powell denied the role of Fed in makingthe income and wealth inequality worse, more than once, in his statements That’s outright intellectual dishonesty.Thinks we all are deaf and dumb!

His pontification emphasizes that SOFT LANDING is possible, repeatedly another gross lie. Mkts zoomed today after his speech (WSJ interactive) Wonder why? They don’t believe he has the guts to do what’s required just like 4th qtr of 2018.

Only a rip roaring inflation will uncover his hubris.

Here is an interesting stat:

Combined together4 largest CBers – of Fed, ECB, BOJ and PBOC, their combined balance sheet was during financial crisis was JUST 5 trillions.

Today that figure is 31.5 Trillions! Doesn’t this bother anyone else out there? Collective cognitive dissance is freightining!

sunny129 –

” Doesn’t this bother anyone else out there? Collective cognitive dissance is freightining!”

——————————————-

It bothers a lot of people. They know they are being gas lighted and lied to. Much of the country knows they are being played by vested interests.

The vested interests just make sure there is insufficient address to the concern. That has been taking place for 100’s and 1,000’s of years.

It doesn’t frighten anyone else whose balance sheet has increased at the same rate.

GDP CRASHES with simultaneously, unprecedented levels of INFLATION in basic needs across the board! food, housing, fuel, cars, healthcare…even ‘emergency’ induced INFLATION isn’t enough.

I feel bad for adding a question to the long list, but…

I don’t understand the numbers…

Inventories contributed negatively by an annualized rate of -0,84 % QoQ in Q1, but somehow also increased by 5,7 %… How is that possible?

Also net exports contributing negatively is in my view a mechanical interpretation. If consumption increases but is imported from abroad, then the positive contribution is canceled out by the negative impact of imports. This is so because GDP is the domestic production. So an increase of imports for consumption does actually not lower GDP (+100$ in consumption – 100 $ in imports = 0 Delta GDP). If net exports contributed negatively it would have to be because of lacking domestic production, perhaps in the service sector?

Best

Daniel

OK, I figured out why inventories contributed negatively.

I still dont understand why the net exports declined and why this would be a “One Off” event.

OK read my original article about this GDP data (which is linked in the article above). It has a lot more info on this:

https://wolfstreet.com/2022/04/28/gdp-sunk-by-trade-deficit-result-of-globalization-drop-in-government-spending-consumers-held-up-despite-raging-inflation/

I did, thanks a lot.

Your content and the fact that you take the time to answer dumb questions like mine is extremely impressive.

Daniel

Daniel,

“contributed negatively by an annualized rate of -0,84 % QoQ in Q1,”

Yes, it’s confusing. You need to forget this metric (“contributed to GPP growth,” negatively or positively). This is a rate of a rate. Rounded numbers here to make it easier:

If inventory increased 6% in Q4 and then increased further in Q1, but by 5%, and actual inventories now 5% higher than in Q4, then the rate of change (from +6% down to +5%) was negative, and then this is called “negatively contributed,” when in fact inventories jumped by 5%.

This metric is very confusing and should never be discussed in the media because no one (least of all the reporters) really understands what it means and don’t explain it the way I just did. They just throw it out there, and people end up with misinformed. This metric is for GDP nerds only.