Commercial Real Estate hit by construction boom, oil bust, pandemic, working from home, now hiring freezes and layoffs. Older office towers dish out huge losses.

By Wolf Richter for WOLF STREET.

The news for the office sector of commercial real estate just keeps getting worse. Some tech and social media companies have announced hiring freezes, including Facebook and Twitter. Others have made cutting costs suddenly a priority, promising very constrained hiring, such as Uber. Numerous startups are laying off people, included used-car online dealer Carvana, which fired 2,500 workers last week. Mortgage lenders from Wells Fargo on down have started laying off significant portions of their employees as mortgage lending is now in the dumps.

In addition, there is the shift working from home for office employees, and hybrid models where employees show up at the office only every now and then.

All this follows years of office construction booms. New office towers are being completed and put on the market with the latest and greatest amenities, and these trophy towers are competing with older office towers for shrinking office needs.

A widespread flight to quality has set in: When leases in older towers terminate, the tenants move to the trophy towers, and leave the older towers vacant. And landlords cannot lower the rents enough because they wouldn’t be able to meet their mortgage payments. So, the office sector of commercial real estate is facing an ugly reality.

Availability rates, which sounds a less bad than vacancy rates, have shot up during the pandemic, and in many cities have continued to rise through Q1 2022, and are now in the astronomical zone.

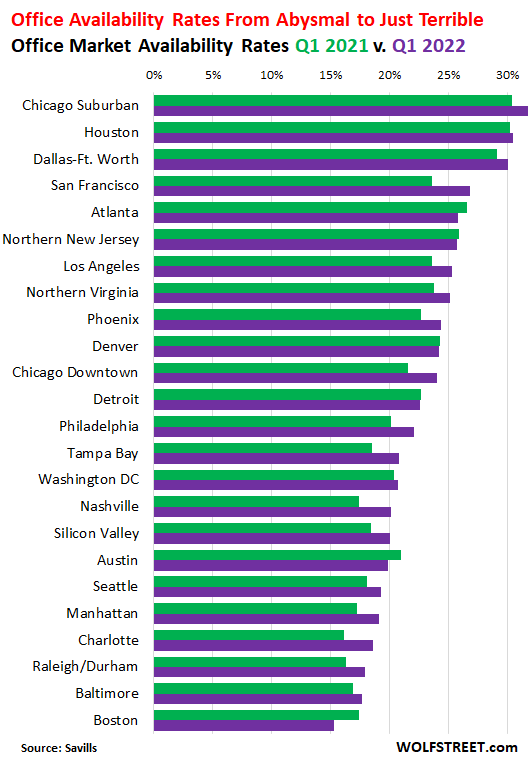

The worst four office markets in terms of availability rates are Chicago Suburban (31.7%), Houston (30.5%), Dallas-Fort Worth (30.9%), and San Francisco (26.8%), according to data from Savills.

In San Francisco, for example, the availability rate of 26.8% was a new record worst in the data, and was up from an availability rate of 7.3% in Q3 2019. In 2017 and 2018, San Francisco was the hottest tightest office market in the US. It was called “office shortage,” where companies were leasing or buying office space they didn’t need, and to hog this space, before anyone else could get it, so that they’d have space to eventually grow into.

Now there are 23.1 million square feet (msf) of available office space on the market in San Francisco, according to Savills, up from 6.1 msf in 2019. And new construction is still coming on the market.

Meta, for example, back in 2018, when it was still Facebook, leased an entire office tower in San Francisco, in addition to all the other office space it already had in the City, in Silicon Valley, and elsewhere. “This new space will support our growing workforce as we continue to attract talent,” Facebook said in a statement. It has since signed more leases in Silicon Valley. Then came the pandemic and working from home, and now the hiring freeze. So who needs all this office space?

This is how the market in San Francisco turned from an endlessly hyped office shortage to an endless office glut that no one knows what to do with.

But San Francisco isn’t the worst office market. That honor goes to the Chicago Suburban market, Houston, and Dallas-Fort Worth – all of them with availability rates above 30%, according to Savills.

Houston had for years the worst office market in the US, starting in 2015 when an office construction boom smacked into the oil bust, where a slew of Texas-based oil and gas companies filed for bankruptcy, and where the entire industry went through major bouts of cost cutting, layoffs, and footprint reduction. Houston’s availability rates soared. Then came the pandemic and working from home, and it got even worse.

It’s not the new office towers that get in trouble; They attract tenants by offering them the latest and greatest, and a flight to quality sets in that leaves older office towers vacant, and they default on their debts and dish out huge losses to the holders of this debt, usually investors in Commercial Mortgage Backed Securities (CMBS) that these mortgages were rolled into; or banks, insurance companies, and other investors that hold mortgages outright.

For example, in Houston, two office towers, built in the 1980s on the same campus, recently were sold in a foreclosure sale, first Three Westlake Park, and then Two Westlake Park. After fees and expenses, investors ate losses on the mortgages of 81.9% and 88.3% respectively, as the value of these older office towers has collapsed due to lack of demand.

And there is a flood of sublease space on the market where tenants that don’t need the space are putting it on the market in the hopes of finding a tenant that would help lower the carrying costs of the space until the lease expires. Companies that put their vacant space on the sublease market tend to undercut landlords because they don’t need to make a profit on the space; they just want to recoup some of their costs.

There were hopes in the second half last year that the sublease space had seen the peak, as companies were either finding tenants for the sublease space or taking it off the market. But in Q1, the sublease space grew again by 3.6% from Q4, to 159 million square feet, according to CBRE, cited by the Wall Street Journal.

Despite the astronomic availability rates, landlords have not broadly cut their asking rents, and in many markets have raised them. There are some exceptions, including San Francisco, where asking rents have fallen.

But whatever asking rents may be, landlords are negotiating and making deals, and are offering all kinds of incentives, from periods of free rent to large build-out allowances, in order to sign tenants for their empty space.

So here are 24 major office markets in the US (update: I just added Nashville to the original 23 after Savills released the data a few hours after this was published), and their availability rates in Q1 2021 (green) and Q1 2022 (purple), in order from abysmally worst to just terrible, with the least worst on this list, Boston, having an availability rate of 15.3%.

In six of the 24 markets, availability rates fell year-over-year, and the most in Boston (by 2.0 percentage points).

In 18 of the 24 markets, availability rates worsened year-over-year, and they worsened the fastest in San Francisco (by 3.2 percentage points), in Nashville (by 2.7 percentage points), in Charlotte (by 2.5 percentage points), in Chicago Downtown (by 2.4 percentage points), and in Tampa Bay (by 2.3 percentage points):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Is the headline backwards?

From the graph, it looks like things got worse Q1 2022 (purple) than Q1 2021 in most markets (green).

“From Abysmal to Just Terrible: My List of 23 Major US Office Markets”

2banana,

Oh gosh, no, that’s not at all what I meant. What I mean is that the list is sorted by vacancy rates, from “abysmal to just terrible,” and by making it shorter, it got confusing it seems. So I changed the headline to make this clearer. Thanks.

Well, good to see Chicago is doing better finally.

Huh? It’s getting worse.?.

When vacancy goes up, the city is doing worse. At least at these large vacancy rates. Chicago is not doing well in the office real estate market.

Anecdotally … I live in ‘Chicagoland’ as do all my children and grandchildren. (One daughter and her hubby are up in Rockford … but that’s less than a 60 minute drive from me.)

Those who aren’t either Teachers or Librarians (or full time mommies) are all some sort of ‘office dwellers’. Those all WFH at least 3 days a week.

When they do go into the office they tell me their offices spaces are, perhaps, 20% full.

There is a tremendous amount of open office space available in the Chicago area.

Jingle Mail, Jingle Mail, Jingle all the way…

On a serious note: High gasoline and vehicle prices are now another factor favoring work-from-home over commuting to an office, at least for workers without access to mass transit. Commuting is also a time expense for workers. To what extent are those with a choice of work-from-home jobs able to shun employers who need “on-site” workers – unless they offer extra pay to cover the time, hassle, and expense of commuting?

Add the higher vehicle cost, maintenance cost, insurance cost ,taxes, tolls and fees.

No joke

I get my motor/ transmission oils and filters from the same supplier, and I have been for years. They supply local stealerships and shops. Getting good oil is getting harder and harder to come by, and it comes at a premium

Parking. When I drive that’s the single largest expense.

Home prices also favour work from home.

If a company want me on site I ask for enough compensation to buy a reasonable house within a reasonable distance.

Most will not pay that much.

So the entire country has been afflicted by bad real estate ownership incentives.

You bet it has. And for maybe 100 years. Why?

1. Upon sale, commercial real estate per the tax code can avoid any capital gains tax if the real estate is replaced with like-kind. Imagine selling Apple stock for a gain and avoiding taxes if you re-invest usually in 90 days in Amazon. That’s real estate.

2. Real estate is highly leveraged, similar to buying a house for 10% down. Moreover all the mortgage interest for commercial real estate can be deducted from taxes.

3. But most of all, the commercial owner can depreciate the building, not the land, but all of the building. In the past 40 years, this means he depreciates an increasing asset. Maybe won’t work so well now with a decreasing asset.

Why so many breaks?

In 1890, maybe real estate needed tax breaks to settle the West and to develop the manufacturing base.

Not now, manufacturing has been off-shored to China, et al.

But the real estate interests are entrenched, so the code will not change. Imagine Trump Republicans changing the tax code to eliminate the real estate tax advantages.

1. Exchanges were part of the 1921 code, not 1890.

2. Approx 20% of commerical transactions utilize an exchange.

3. The Biden admin proposed to eliminate exchanges: they estimated 6 to 7 billion annually in increased revenue. Barely a rounding error in todays budget.

4. Interest is considered an expense for all businesses, not exclusive to real estate.

5. Yes you can leverage real estate to 90% and more, but most is not and certainly not with attractive interest rates. Same is true for every business.

6. Yes, depreciation and amortization expenses are at the root of what needs to be evaluated for any meaningful tax reform. This isn’t exclusive to real estate and if you look at why some very large companies have low tax bills, the d&a is a major part of the problem

You know what else favors work from home? Regular napping.

And a 6 pack of beer

I feel seen.

Where I live (Atlanta), it’s almost always still faster to drive even if within “reasonable” distance of a transit station.

I live close to one (about one mile) on the east MARTA rail line but unless I time it right, after driving and parking, waiting for the train to arrive, and changing lines, it’s still faster to drive. I also don’t like riding it.

I commute to work by bus and I agree it takes longer to do so. But I have a solid Toyota truck that I want to keep forever. The last thing I want is to get hit by some angry birds on the freeway and then have to buy some POS software with 4 wheels at the current mafia markup.

I would assume 10% vacancy is sufficient in a healthy market to give enough buffer for worker and office movements. At 30% vacancy rates, I would assume that the rents will plummet in a truly free market. Specially mom and pop and smaller landlords who own just a few properties. They cannot afford to keep properties empty for years, they will drop the rent or sell. Once the falling rents match the running cost of the building, they should stabilize.

Still a large fraction of the remaining 30% empty offices would need to be demolished. This smells like bankruptcies and foreclosures of highly leveraged landlords. I wonder why it has not started yet at large scale.

Wonder if this is a leading indicator for what’s coming in the housing markets for those specific cities…

It’s primarily artificially cheap funding costs preventing real price discovery.

Vacancy rates are already awful, yet the bond mania just barely ended and the economy is still “growing”.

When most think of stabilization, they are usually thinking in terms of the economy with the current fake “growth”.

I’ve never seen comparison data globally, but if it’s anything even close to retail, the bottom in any economy outside of the current artificial one is far lower than most think. The US is a complete outlier on retail SQ footage per capita versus other countries. Some of it is presumably due to geographic space constraints but not all of it.

…’extra pay to cover the time, hassle, and expense of commuting?’

Did these employees have their pay reduced for such expenses when they started working from home? This might result in an increased bargaining chip for the employer/employee.

Lots of people don’t have the WFH option. Nurses, auto mechanics, retail workers. Be interesting if Wolf has a handle on how these break down.

Its not all gas and commute hassle.

Anyone who had kids in the past decade without foolishly anticipating a crippling global pandemic first (/s) better have Boomer parents willing to provide unconditional babysitting, since childcare centers shuttered left and right in the last two years.

Our company was bought out by a much, much larger company who sprung a ‘hybrid model’ on us not 5 days after close. Our jobs were WFH pre-pandemic, so suffice to say its going over like a lead balloon. Our salaries were not negotiated based on near non-existent child/elder care and these gas prices, but as everyone finds the Exit the company can pat itself on the back for avoiding layoffs.

WFH may have additional costs ( eg internet, utilities, coffee, … )

When the pandemic WFH started two years ago, gasoline was around $2/gallon. With the capital cost of the car, repairs/maintenance and insurance thrown in, I was easily spending $10k/year to commute.

In the last two years, about half of that money was reallocated to plug other holes in my budget (food has skyrocketed). Car prices are massively higher, and now gasoline is over $5/gallon.

Yes, I saved money by not commuting, but the inflation of the last two years has consumed those savings and then some. To go back into the office would cost me about $20k/year right now. If I don’t get a raise, I don’t know where that money will come from.

And then there’s the office. The open bullpens were disease factories before COVID. My last bout with COVID knocked me down for two weeks and I’m still recovering from it three weeks later. You want me back in the office, I’ll want a private office with upgraded ventilation and an effectively unlimited sick-leave policy so that when I get the next variant, I don’t lose my job.

My commute is 40 miles. Thanks to WFH, I only go in occasionally and am purposefully avoiding as much fuel costs as possible. I’m really glad I have the option; I truly don’t know how my entry level staff is affording fuel based on what we pay (not even $15).

I know it’s been covered before, but I have to believe some enterprising companies / individuals can find a way to flip this commercial RE into residential and make a profit.

I was never accused of being an authoritative source in English, but abysmal seems a more severe adjective than terrible. In the spirit of a post a few weeks back, I would like to offer one of my favorite underutilized words for consideration: heinous.

I wonder how much could be switched from offices to light-industrial factory-type workplaces. Bringing back supply chains will require new infrastructure.

Well, if you were British, everything is “appalling”.

Things do seem dour in much of the industry of All Things Related to Office Space, and by extension in the office construction industry. And yet, we’re told in other reports that Opportunity Awaits, presumably elsewhere.

This from Deloitte:

2022 engineering and construction industry outlook

Preparing for another strong year

The engineering and construction industry has made a significant recovery from the 2020 recession, but it has also experienced multiple headwinds that are expected to persist. 2022 should be another rewarding—but challenging—year, and the industry looks to be poised to capture growth opportunities.

https://www2.deloitte.com/us/en/pages/energy-and-resources/articles/engineering-and-construction-industry-trends.html

Despite the qualifier, I think Deloitte may be a bit overly optimistic and perhaps unduly hopeful, but then, I have my own unrelated reasons for lacking confidence in Deloitte, so I may not be the best person to ask. Which you didn’t.

I am confused. I see the facts provided by Wolf and then I see articles like this: https://www.theguardian.com/commentisfree/2022/may/08/working-from-home-commercial-office-space-booming. Certainly my lived experience (working for a company that got office space on the cheap during Covid in SF) is more in line with Wolf but what gives? I am old enough to have been through 3 recessions and that experience tells me when the helium comes out of the balloon it will fall.

Read carefully what that linked Guardian piece is: it’s real estate hype and promo talking about higher asking rents despite the high vacancy rates. It seems like someone got paid by the CRE industry to post this. This is the kind of industry-sponsored garbage that gives the MSM a terrible name for the coverage of the economy.

One thing I like about the Guardian is they survive on voluntary donations for revenue rather than forcing paywalled subscriptions.

The price to pay for this is the occasional industry puff piece to help the Guardian cover its bills.

I still find this approach OK given that many other Guardian articles are nicely in-depth and unbiased on a variety of topics.

10-4 Wolf:

Read that huge per cent of ”articles” in news – papers and websites are actually ”press releases” from PR folks at companies and especially ”institutions” these days.

Another reason Wolf’s Wonder is currently the only news source to receive my financial support at least twice each year!!!

Many thanks for your efforts.

This is true of the business and sports press. The reporters and analysts are spread thin and tend to take what’s given without a critical eye.

Is it because the private organizations do not have to answer questions?

Zero access if you aren’t deferential.

Wolf,

An interesting (and crucial) aspect to all this is just how much vacancy real estate owners can endure while propping list “per square foot” prices that leave them with 15% to 30% empty buildings.

I continue to be semi-amazed by real estate owners’ willingness (apparently near universal) to list prices so far in excess of market clearing, that almost a third of their space goes unleased. Even at 15% vacancy, that is a lot of zero revenue space.

And yet, it must work for most of them (price elasticity and price discrimination math allowing for any combination of prices/lease volumes…in theory).

And the same bizarro world holds in pre-pandemic lodging…where a mere 65% yr round Ave occupancy seemed to be a norm (due to unnecessarily high ask prices).

Perhaps those with large scale real estate experience can explicate the math/logic/results of huge over-pricing with equally huge vacancies.

(All of this applied well before the pandemic).

Of course, this over-pricing provides the niche for the Pricelines/Hotwires of the world (selling enormously idled space at much lower than list prices) but it is a weird economic world that generates the ecology in the first place.

Any big lessors care to explain the logic?

A lot of landlords cannot cut asking rents below a certain level because they have to show the income potential of their property to their lender in order to make the mortgage payments. Once they start cutting asking rents below this level, it cuts the income potential of the entire property, and the lender (servicer) gets very nervous. Most likely, at that point, where rent payments don’t cover the mortgage payments, the landlord will stop making mortgage payments and let the lender have the building and walk away from it. Then someone else buys the building in a foreclosure sales for cents on the dollar, and with a much lower cost basis, can then spend some money on renovation, and offer much lower rents to fill the property. And this then puts downward pressure on other properties.

RealityDose

“If you don’t read the newspaper, you’re uninformed. If you do, you’re misinformed.” Mark Twain

How do you know when a politician is lying…they open their mouths……

You can trust what you see on the internet, especially the news talking about politics

It’s never been this dry/hot/wet/rainy/snowy/windy before…..

Congress Campaign contributions are used for campaign contributions (really funny lol)

the list goes on and on and on and on……

ps Here in Manchester…we still call it the Manchester Guardian, even after it moved to London(1959)….it moved to London coz that’s where the godless commies live and they needed staff……. ha ha

I read the article. Manhattan and Chicago are mentioned in the article as well as the data here. This is not a dig at Wolf, but you always have to consider both sides of the coin. Wolf lists the worst markets by availability. He doesn’t mention the best markets. I don’t believe he’s doing it to mislead anyone, however, it may come off that way.

There could be markets where over-building has not happened and vacancy rates are very low. The top offenders on this list are clearly places wher over-building went bananas. In the DFW area I hear people tell me every day that residential and commercial real estate is so healthy that anyone who thinks this market is running out of steam just doesn’t “get it”. The hype of companies “considering” a move to DFW is just hype. I believe we have reached the peak influx into the DFW area and should plateau. However, more commercial space is still being built and projects are getting approval and funding. Vacancy will get worse, before it gets better.

“Wolf lists the worst markets by availability.”

That is BS. I listed ALL the markets that Svalls released data on as of the time of publication. I didn’t leave out any. And I organized them in order of availability. Tampa Bay is on the list, and it’s pretty bad. Boston is the least bad of the markets that Savills released data on for Q1. Note that I did not quote industry promoters, which is largely all that the Guardian piece cited, instead of raw data.

There are other markets, not just these markets.

Nice article. I would love to see a followup for 2023.

In part, because I know Boston is going to get a lot worse. There are tens of millions of square feet of space currently being built. The skyline is full of cranes. MIT also started a major development of its East campus (Kendall Square) building millions of square feet that MIT itself does not have a use for. Many developers “piggy backed” onto this, building additional office space in the surrounding area.

I have no idea who is going to lease all of the space coming online in Boston next year. In addition to that, Boston doesn’t have the housing infrastructure and transportation infrastructure to support workers for the space even if companies wanted to lease. Everyone I’ve talked to in the city and suburbs is expending a major quality of life drop due to the new commercial development.

Boston is a little bit unique in that there is strong demand for “wet space” (bio labs) since we have major pharmaceutical companies head quartered here. But, many of the bio and tech companies built themselves new head quarters in the past five to seven years. So, I don’t see most large companies shifting from older to newer development. That has largely already happened in Boston. Perhaps, there is hidden demand for “wet space” that I don’t see?

In addition to “Boston proper”, our two ring highways (128 and 495) have had signs on office buildings along them advertising hundreds of thousands of square feet for over a decade. Things look much worse when you look a bit beyond the metro area.

Regarding “working from home”, I will say that at least for my office (about 340 people), there are about 11 of us here on the average work day… in about 120,000 square feet. In large parts of the office, the lights aren’t even on during the average workday. My company is stuck in the lease for another 9 years and many employees have said they would rather quit than return to the office.

Just as in NYC, all of this empty commercial space will have a huge knock on effect on the local economy.

So, in short, I would say be very careful investing in Boston CMBS paper.

Perhaps the Chinese concept of “Ghost Cities” can be applied to “Ghost Office Buildings”.

The idea of anybody living in them is NOT part of the event.

The idea is to create economic growth by spending on construction. Everybody makes money. From inception to completion, millions of dollars are made. Who cares if it is occupied.

Today we create wealth by creating paper notes and digital credits, right? Nobody cares that there is really nothing. So, why care about the use of the building? The paper notes served a purpose and the construction of these building served a purpose.

We don’t need to occupy them. We need to keep churning our more to keep the economy going. People sitting or living in these buildings has NO economic advantage.

Move on to the next project. Rinse. Repeat and watch the GNP increase every year. Stop thinking like it’s 1880 and value is in dividends, Gold Bonds, and occupied Real Estate. This ain’t the days of the Astor’s, or Vanderbilts, or other rip off artists, who created nothing as well…………………………………….It’s different today.

As for debt? Sell the Loan to the FED. They hold it. The building sits empty and everybody is happy.

Commuting times in Houston are terrible with traffic that is as bad as pre-pandemic. No evidence from traffic patterns that size-able numbers are working from home.

Small flyover towns have buildings that are vacant for 40 years, since

the malls moved in.

Now they have dark malls and a ghost downtown.

My hometown in Connecticut took an old brass mill (100+ years old) that was shut down, and leveled it. The state paid for the environmental cleanup, which Cost millions.

This property was just adjacent to downtown and a big mall was built on it 20 years ago. I just read in my hometown paper that the mall was sold to a developer and will probably be torn down due to declining sales. No word on what’s going to replace it.

I’m guess in low income apartments.

A lot of tenants are turning into squatters. They keep occupying the office space and retail space while not paying any rent. I know several in my area. I wonder if these statistics are reflected in the office vacancy data that is published above. The landlords let them do it just to keep the property occupied and look like it’s in demand.

The same, it seems, is happening at my SoCal community college campus too. I thought maybe students (and their parents) would leap at the students getting back into a world of people. The place is like a ghost town, but a ghost town with building still happening.

A lot of youths seem permanently acclimated to life in front of a screen. And I admit, there are advantages, as a teacher. But the idea of communities of humans (outside of one’s nuclear family) interacting in the non-digital world still retains some appeal for me.

In 2008, enrollments did spike up, so if recession is the outcome here, that may happen.

College going population is dropping and college costs are going up.

Kind of like new car production and prices.

Mesa?

Wolf, love to see how Nashville (unicorn market or just head in the sand?) is faring through this. It seems that nothing can stop the “it city”.

I just added Nashville to the original 23 after Savills released the data a few hours after this was published. Availability rates worsened by 2.7 percentage points, to 20.1%

Boston? Maybe it’s that biotech companies require more work in person? Or that the younger population is more okay heading back into the office?

I don’t think Boston got as over built as the other cities on this list.

One of the questions to ask about the Boston data: Is this just the formal city of Boston, MA or the greater metropolitan area? Traditionally, the tech corridor was along Route 128/I95 and there’s a LOT of office space out there. In the last ten years or so, the “hot” place has been the city of Boston and to a lesser extent Cambridge. This results in a relatively low office vacancy rate in “Boston”…

However, the metro extends from the Rhode Island border all the way up to the New Hampshire border and from the coast to roughly 50 miles inland. If you look at that whole area, no way it’s only 15%.

Digital Equipment Corporation vacated a massive amount of space.

The old Wang Towers in Lowell just lost their major tenant and replaced the sign on the top of the building as a result.

Bedford, MA is a ghost town. Bedford used to be filled by all the companies doing work for Hanscom Air Force Base, but Hanscom got scaled back pretty brutally after Teddy Kennedy died and all the companies left town for greener pastures.

These are just a few random examples that I’ve noticed, the whole area has a bumper crop of “For Lease” signs.

Boston is also smaller. Young people are not the ones coming back. We haven’t collapsed yet, as my thinking, leases haven’t all expired to renegotiate smaller foot print. Wolf is correct, flight to quality, the new State Street Bank building is now fully leased. Winthrop Sq. opens next year. (Worlds first class A passive house constructed bldg) currently signing leases, at the expense of older buildings. No one new moving in, just lateral moves. This may take years to see full effect of covid. It also remains to be seen how much of a hybrid work environment will exist. I’m inclined to think a 4 day work week will evolve in Sept.

If work is done on computers , why do workers need to be located in high rise towers . Leasing less space is a plus for companies and is a plus for workers.

It is a negative for commercial owners of buildings , for businesses dependent on office workers , for municipal taxes and for large cities as a whole .

It increases the probability of municipal defaults in the future

“If work is done on computers , why do workers need to be located in high rise towers .”

As opposed to letting them code in their underwear at home with a cell phone open to a social media site. You’re going to give Capers Jones fits, dude.

We get these kinds of questions from people who have never been technical leaders, or supervisors, or managers of successful IT teams, unfamiliar with well-established software development methodologies. We do get them from inexperienced, ambitious MBA types who are mostly interested in impressing their bosses with cost-cutting measures, with little consideration of the effects on motivational psychology, team dynamics, and so forth.

Let’s put it this way.

No man is an island, entire of itself; every man is a piece of the continent, a part of the main. Treat them like islands, absent an effective, team-oriented development methodology, you don’t get continental outcomes. You get a lot of cowboy coding that results in extremely expensive projects to fail.

Been there. Done that. Apologies.

I wonder how Wolf can be so successful without a manager?

But, he’s marred 😁

married

He’s married and obedient

… clearly I need to get up 10 minutes before Dawn

Married and I am sure it was voluntary.

didn’t you mean Donne that una?

apology accepted…

Correct. This is the earliest part of a major long-term change in work. In my field, about 1/3 of the work is now done from home, prepandemic it was close to nothing. Multiply by one million and the urban office market and housing market is in major trouble. There will always be some in office work but it will be substantially less long-term, probably by 25 to 50%, most knowledge work can be done anywhere.

If it can be done in your home, it can be done in Bangladesh.

Fossil fuel companies would prefer that people commute to work rather than work at home, but they won’t care if you still want to sit at your desk in your underwear.

Once these numbers come out of the dream world and reality reflects on valuation……the big banks are going to have one heck of a write off time……of course the little buggers are doing everything right now to pass the losses off to investors at what might appear to be attractive terms before the whole thing falls apart……the old joke about used car dealers should now be re written to use investment banker in the punch line.

Urban DK.

Wonder how far we are from informal occupations of vacant skyscrapers, like I used to see when I lived in Sao Paulo. “Couldn’t happen here”?

Let’s say everyone walks away and some of these places go vacant. The lost taxes would crush a lot of these cities financially. Many big cities would be running enormous deficits if not for the American rescue plan.

I think a multi year recession is in the cards. Things are beginning to crumble from the bottom up. Housing market is drying up. Car market has a big backlog but volumes are still way down from 2019, itll slow down further. The last leg to fall will be commodity prices. Inflationary bubbles don’t really end any other way, that’s why the fed insisted inflation wasn’t a problem and then that it was temporary. Many governments globally are beginning to impliment forms of austerity measures.

Taxes don’t go away. They get paid first when property sells.

One of the reasons, Boston Mayor Wu, has privately been contacting large firms to push people back to workplace.

Which governments?

I read this claim recurringly. Running a slightly lower (massive) deficit than previously isn’t remotely “austerity”. Any such claim is a farce.

Otherwise, generally agree with your sentiments.

Was San Diego not a large enough market? Was hoping to find my local data.

JD, I was wondering about St. Louis, too, but I’d imagine it’s smaller than even San Diego.

The $4 million sale of the downtown AT&T building last month when it was once worth $205 million back in 2006 had to earn St. Louis an ignominious crown somewhere.

Local data is available, but the sources are not immediately obvious. For example, Texas A&M University gathers/reports data for the commercial market in Texas. They also gather/report data for the residential market, although not every town/city is covered by them. Maybe others can point you in the right direction if they are in the commercial real estate business.

Don’t forget that many of these buildings are owned by large corporations, especially foreign companies, and are used by them in ways that financially may not make sense to any individual. For example, Samsung from Japan owns a major building in downtown Chicago, that is quite old. They are in a partnership with two other firms. There are also mutual funds that have ownership in buildings. Quite a few German and Chinese companies own buildings in Chicago as well. There are far worse places around the world one could own buildings and commercial property than here in major US cities. Imagine the steeply declining value of all the buildings in Russia, especially all the stores that McDonalds is getting out of permanently, and then all the other US firms that have left or are leaving, Russia is being economically gutted. Probably a worse situation than after the fall of the USSR.

After this next market crash, later this year, there are probably going to be a lot of Wallstreet financial firms and banks that will have tons of newly available office space for some other. Bag holder to then lease. Maybe we are talking 50 % vacancy post the market crash in places like Chicago Suburbs. Taxpayers are fleeing Illinois and particularly Chicago in droves. Especially the union retirees who are taking their pensions and running.

Samsung is Korean. Otherwise agree, Chicago and IL are in major long-term decline.

“… Russia is being economically gutted.”

That must explain why the ruble is near all-time highs.

Duke DeGuise,

“That must explain why the ruble is near all-time highs.”

That is hilarious. Not even Putin would say that kind of BS. Look at a long-term chart. The ruble rose in recent weeks back to where it had last been in Feb 2020. See that tiny little-bitty uptick at the end, that’s the recent surge. The ruble has done nothing but collapse. Over the past 25 years, it collapsed by 99.9% against the hated soon-to-be-worthless USD!

Excellent perspective/chart Wolf!

When was the last time the ruble was worth something? Before Russia got involved in WWI?

Rumors said Renault was paid one Rubel for all it’s Russian car manufacturing plants and other investments in Russia. Who got gutted?

With a bit of bad luck McDonalds will lose the right to use that name in Russia and someone localy allowed to…

With all the shortages, Renault may be using the parts that went to Russia and send them to their other factories and cutting their losses in Russia.

“Williams said MBS sales are not under consideration for the first stages of the plan unveiled this month to pare down the Fed’s $9 trillion balance sheet starting in June. Speaking to a Mortgage Bankers Association conference, Williams said “once our balance sheet reduction is well underway … that is an option that the Federal Open Market Committee (FOMC) could consider.”

Looks like QT has reduced by 35% by the Fed before it started. Was the Fed lying about the quantum of QT when it announced it? Cannot put it past the arsonists & firefighters.

KPL,

BS. If you don’t even understand the term “sales,” don’t make grand statements. Ask instead. And I’ll answer your question. You should have asked, “What does it mean when Williams says that sales…”

So I’ll help you.

MBS come off the balance sheet via passthrough principal payments when mortgages are paid off (such as when the home is sold or when the mortgage is refinanced) or are paid down (regular monthly payments). The principal portion of those payments is forwarded to (“passed through to”) MBS holders, such as the Fed, and the balance of the MBS shrinks. To keep the balance flat (as right now), the Fed buys new MBS to replace them. These pass-through principal payments amounted to about $80 billion a month before the increase in mortgage rates. Now they have slowed but are still very large.

So when the Fed stops buying MBS to replace the passthrough principal payments, the MBS balance on the Fed’s books will shrink rapidly, but the Fed said it will cap the shrinkage to $35 billion a month. So that’s QT. And it starts in June.

Over time, when a lot of the MBS are gone from the Fed’s balance sheet, these passthrough principal payments will slow down, and fall below the Fed’s cap of $35 billion a month. This is when the Fed will be considering outright “sales” of MBS to get rid of them.

What Williams said was that early on during QT, the Fed will rely on the passthrough principal payments to reduce the balance. This has been in the official policy statement two weeks ago, and there is nothing new here, because that’s how QT works:

https://wolfstreet.com/2022/05/04/powell-confident-in-softish-landing-for-the-economy-but-we-may-keep-inflation-markets-can-figure-out-their-own-landing/

Thanks for correcting me and the elucidation.

So in effect you are saying pass through payments are sufficient to do QT of $35 billion a month from Sept. And if insufficient then sales will happen.

KPL,

Yes, “pass through payments are sufficient to do QT of $35 billion a month from Sept,” roughly, during the early stages of QT. This is a function of interest rates. Lower interest rates trigger refis, which trigger a huge flood of passthrough principal payments. In 2020, there were months when the Fed got well over $100 billion a month in passthrough principal payments. Rising interest rates reduce refis and the flow gets smaller, but it’s still big. This is unpredictable, and it will fluctuate.

The cap of $35 billion will be frequently hit early on, and then eventually, as the balance of MBS shrinks, and mortgage rates continue to rise or stay high, those passthrough payments will be under the $35 billion cap. At that point, the Fed may begin selling some MBS outright to keep the pace roughly at $35 billion a month.

Wolf,

Not to incur your wrath for not RTGDFA, but could you expand on the assumptions behind pass through being adequate.

My assumption is that the $2.715T of MBS that are on the books today were aggregated new mortgages when purchased. If they were all 15 year mortgages, the principal payment would be not reach $15 billion until month 93. If they were all 30 year mortgages, the principal payment would be under $6 billion for the first 10 years. So for the first 5-10 years, the pass through from payments should be around $10 billion.

The additional amount should be refi’s and sales. Refi’s should be effectively zero with interest rates increasing That would leave the rest of the $25 billion to be due to sales. If all of these homes were bought or refi in the last 18 months, who is going to be selling? Are 1% of homes (which would give $27 billion extra) sold in the first two years, especially with the market tightening?

Again, I’m not questioning what you are saying. I am just trying to make the math work and wondering how much of the pass through is based on refi’s that won’t be happening any more.

MattF,

I’m not going to repeat my comment. You’ll have to re-read it. It answers some of your questions.

I’ll just add: The average 30-year mortgage gets paid off in 7 years (refi, house sold, etc.). All these payoffs become pass-through principal payments to MBS holders that reduce the principal balance of the MBS. A few years into the life of a 30-year MBS, the principal balance may be down by 30%; and maybe 7 years into it, it may be down by 50%. At some point, the balance gets too small and Fannie Mae (of other GSE) “call” the MBS, meaning, it buys them back from the holder to repackage the remaining mortgages into a new MBS, and at that point the entire remaining MBS comes off the Fed’s balance sheet, many years before maturity date.

Refis are down a lot but they’re not zero:

Maybe these huge office tower blocks would be ideal for conversion to Vertical farms as the food would then need to travel hardly any distance to get to market. Also maybe all the empty and soon to be empty Malls could find new life and be used for this to? Although the idea of the food they will be creating scares the life out of me and I for one won’t be eating any of it even if starving.

You say that on a full stomach!

You’ll Eat it and be Happy.

If they don’t keep the HVAC running, they’ll have vertical farms of mold and mildew. Executive carpet is a good sprouting medium. And 5% ethanol, like spilled beer and wine, results in increased germination rates.

These buildings for the most part weren’t good for anything except their original purpose at their original time. Many bullets will be bitten and they will be razed.

Truth is, we don’t know. A lot of lobbying went into assuring that people will not be able to read “GMO” on the label and avoid it.

In my opinion, the main point of genetically modifying produce is for “Big-Ag” to lock food production (and producers) inside of their “value chain”, leaving nothing on the table for the farmers. It’s retarded, but, like many things retarded that big-money wants, it just is what it is.

Guerilla growers getting into “vertical farming” do not care for that.

What I look forward to seeing is entire office floors occupied with grow-bags, energy efficient LED lighting, PLC’s to control humidity, water, lighting, CO2 levels, and rows and rows of cannabis plants :)

During the transition, there will be occasional frenetic shootouts and medieval sieges every time some law enforcement gets a bee in their bonnet and try to take over a “vertical farm” from the “Liberators of the Void-space”.

Once enough casualties have been racked up, a system will be worked out and normal life goes on again, with a different setting for “normal”.

To what extent is this a replay of the overbuilding of malls in the US? It’s my understanding that you have 40% more retail space per person than we do in Canada and that you hit “peak mall” in ‘06 or so.

Maybe past is prologue?

This is a really good question. I hadn’t thought of it this way.

A lot of the space where I’m at is being built with the expectation that start-ups will use it.

I’m pretty hooked into the start-up community. What I see from that community is that most new start-ups are either Fully Remote or Hybrid and don’t need much office space (if any). The hardest thing about a start-up is getting traction before you run out of “runway” (burn through all your funding). If you aren’t paying to lease a bunch of office space, your funding lasts much longer (and you’re books usually start looking better a lot quicker).

There was a split that happened around the early 1990’s between kids that were “Mall Rats” and kids that had never been to a mall. I wonder if there’s not a similar generational divide forming in the corporate world between the older “Office Rats” and the young companies that have never worked in an office tower.

I agree with the general sentiment on this site that the economy is rather healthy in the USA. But, certainly gas and diesel prices could push us into a recession if they keep rising or stay persistently high. If that happens and we start to see the large layoffs from established companies that are typical of a recession the trend away from demand to lease office space may accelerate quickly.

One postscript I will add is that because the office towers are largely empty where I’m at, many of the restaurants and shops that typically occupy the first floor of the towers have either gone out of business or remain long term closed. This is even true of the train/commuter rail stations and immediately surrounding areas. That represents a lot of missing lease revenue (and sales/meal/employment tax revenue for the local municipality and state).

Technology is getting really compact: The Surface Mount Device (SMD) plant that supplies all of Grundfoss built-in electronics fits comfortably inside of one 140 m^2 building.

The rest of the many thousands of square meters of factory is all for mechanical assembly.

If/When 3D printing improves by one, maybe two magnitudes, then there will be just another 140 m^2 building performing most of the mechanical production and assembly. The rest of the space will be a logistics centre.

My guess would be that the technology improvements will happen before the next 20 years are up. Which is scary and interesting.

What are typical vacancy rates? This doesn’t mean much without a reference. I do not believe 2021 data serves as a valid reference.

In San Francisco, it was below 9% in the years before 2020, and below 8% in 2019. In Seattle, it was 10%-15% in the years before 2020. Houston, as I pointed out, has been bad since 2015 due to the oil bust, with rates 20%-25%.

Commercial real estate must be massively leveraged if 30% vacancy rates lead to debt investors receiving 12 cents / dollar. Apples / oranges I guess.

When I was actively in SFH rental ownership (lower end), it was not uncommon to have 20% or more vacancy, but they were always cash purchases. I would not think leverage at such low interest rates would create such a dilemma in commercial RE….but….debt is in fact the devil I guess.

The good news is all these losses are owned by billionaires so I’m sure there will be a special government bailout to recoup their losses.

I mean, this isn’t like 2008 where the middle class got into trouble and needed to be punished by our overloards. These are the billionaires, so we obviously need to use tax money to ensure they feel no pain.

How is the vacancy rate calculated and how can it be manipulated? Do all of the property owners use the same method to compute a vacancy rate? Do the aggregators differentiate between the various ways of computing vacancy rates?

This is NOT survey based. Availability is based on the total office space that is advertised (listed) for rent and on the market to be rented, and is therefore available to rent. It’s either listed for rent or it isn’t. If it’s not listed for rent, it’s not for rent, and is not included in the availability. There are reasons why empty offices are not for rent, for example the Facebook tower in San Francisco may not have anyone in it, but Meta is making rent payments, and wants to keep it around for future use, so it’s not listed for rent, and no one else can rent it, and it is not included in the availability data.

The total square footage of commercial office space for each city is a known quantity, and is part of the data. The availability rate is total square footage listed as available for rent divided by total square footage of office space in this market.

And this is before the recession formally begins…

These rates will only move higher, as many companies are stuck with office space they are not using, so they will cut the space once the lease expires. This is going to be a problem for many years to come.

It needs to get worse, and the landlords need to be forced to cut rates or file for bankruptcy, so that rental rates start to reflect the true market.

Real estate is still way overpriced, both commercial and residential. We need to have a really big real estate purge, to reduce these absurd costs.

I think Chicago has close to 30 million square feet of unused office space. Conversation to residential would help residential rents.

I’m a Boston area delivery guy. My route is mainly a plush office park, mostly biotech and medical tech companies and includes a few well known companies’ headquarters.

Since The Epidemic, this complex has turned into ghost town. Parking lots are maybe 20%- 30% full now. I’m still busy feeding dry ice boxes and the like to labs on campus, but the offices are dead. Makes my job a little easier. I’ve noticed that a lot of the non-tech companies that have left this little suburban office paradise have either folded or fled into downtown Boston.

Like the lab rats I deliver to, I, unfortunately, cannot work from home.