But the first upticks in delinquencies from breath-taking record lows are cropping up.

By Wolf Richter for WOLF STREET.

Americans are exiting the weirdest economy ever, a two-year period where the Fed threw $4.7 trillion in printed money at the financial markets, thereby inflating further the greatest Everything Bubble ever, printing millionaires and billionaires on a daily basis; and where the federal government threw $6.6 trillion in borrowed money directly at consumers, businesses, and state governments, topped off by wide-reaching forbearance programs for mortgages and student loans, along with eviction bans.

But now, it’s over. It’s the next morning and bad breath: The worst CPI inflation in 40 years, spiking interest rates to deal with this inflation, and deflating asset bubbles. The hot air is already hissing out of stocks, bonds, and cryptos; and housing, which is very slow moving, is getting in line.

So here’s how consumers are exiting the free-money and credit paradise, based on today’s data from the New York Fed’s Household Debt and Credit Report for the first quarter.

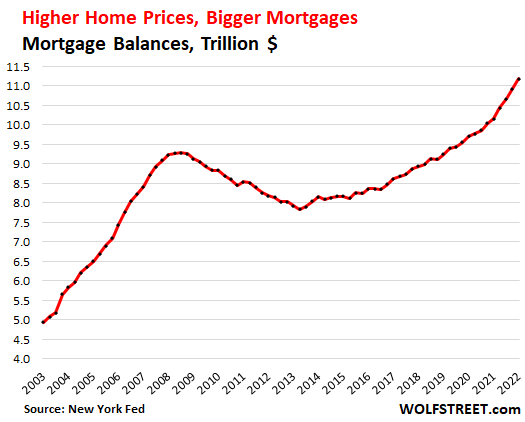

Mortgage balances, delinquencies, and foreclosures.

Mortgage balances jumped, as people bought fewer homes but with larger mortgages to fund the spike in home prices of 15% year-over-year according to the National Association of Realtors and of 20% according to the Case-Shiller Home Price Index.

Total mortgage balances jumped by 10% year-over-year in Q1, to $11.2 trillion, even as home sales declined 3.6%:

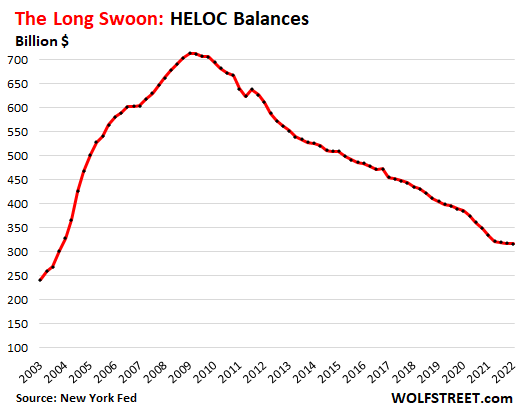

But HELOCs continued to fall out of favor. Since the Financial Crisis, the balance of Home Equity Lines of Credit has declined – replaced by cash-out refi – and in Q1 edged down to $317 billion, the lowest since October 2003:

Forbearance cured delinquencies, but now it’s over. Delinquent mortgages that were entered into a forbearance program were reclassified to “current,” though the homeowners stopped making mortgage payments. Then the process started to get homeowners out of these forbearance programs.

The surge in home prices over the past two years had the effect that homeowners could exit forbearance by selling the home, pay off the mortgage, and walk away with cash. This was one way of exiting forbearance.

But lenders, amid the surge in home prices and improving job market and rising wages, helped their customers exit forbearance by modifying mortgages or refinancing them.

The number of homeowners still in forbearance dropped to just 525,000 by mid-April, from 4.3 million at the peak in June 2020, according to the Mortgage Bankers Association. So that issue went away with the explosion in home prices.

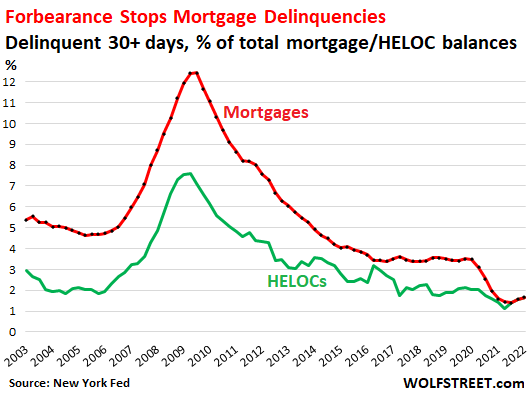

Now, with forbearance programs largely over, mortgage delinquencies have started to tick up from the record lows last year.

Mortgage balances that were 30 days or more delinquent rose to 1.66% of mortgage balances in Q1. While a change in trend, it’s still near the record low of 1.39% in Q3, 2021 (red line).

HELOC balances that were 30 days or more delinquent rose to 1.65% of HELOC balances in Q1 (green line):

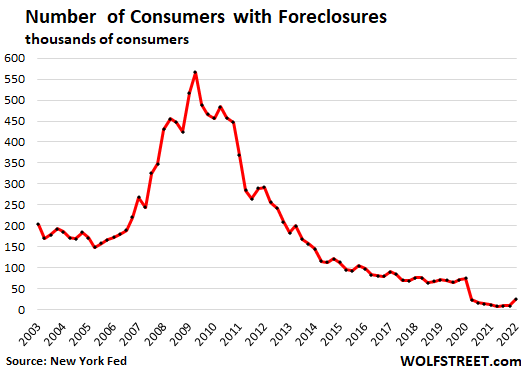

The number of consumers with foreclosures ticked up to 24,240, up from a record low of 8,100 consumers in Q2 last year, and the first real uptick during the pandemic. But it remains near record lows. By comparison, during much of the mortgage crisis, over 400,000 consumers per quarter had foreclosures:

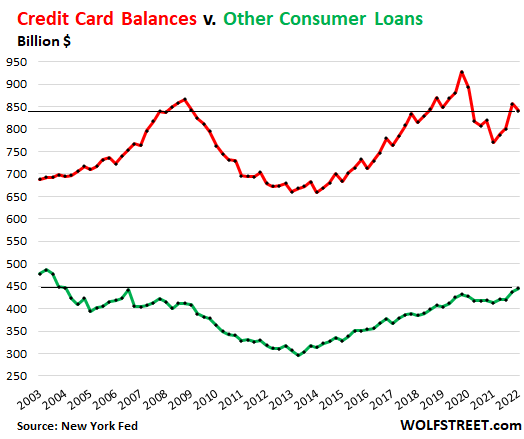

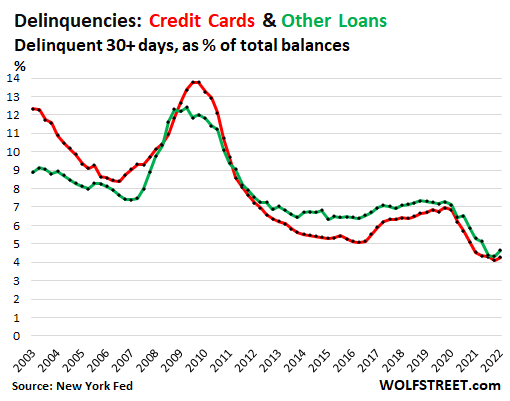

Credit card balances and delinquencies.

Credit card balances, excluding other revolving loans such as personal loans, dipped to $840 billion in Q1, from Q4, right back where they’d been in Q1 2008, and below Q1 2020 and Q1 2019, after 13 years of population growth, inflation, and raging inflation (red line).

This shows that consumers have reduced their reliance on credit cards, which makes sense given the usurious interest rates. But on an individual basis, some borrowers are overextended even during this miraculous stimulus era.

Other consumer loans, such as personal loans, edged up to $450 billion, but was below the highs before the Financial Crisis (green line):

Credit card delinquencies of 30 days or more ticked up a tiny wee bit from the record low in Q4, to 4.27% of total credit card balances, the first uptick during the pandemic (red line).

Delinquencies of other consumer loans, such as personal loans, also ticked up from the record low in Q4, to 4.65% of loan balances (green line):

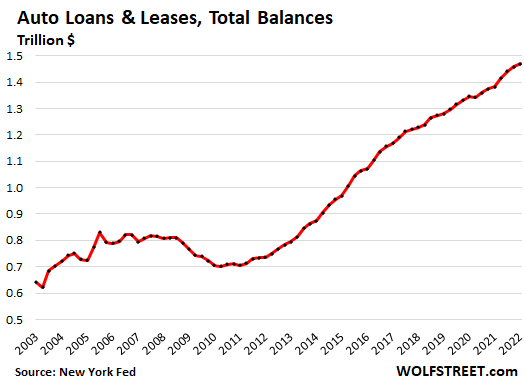

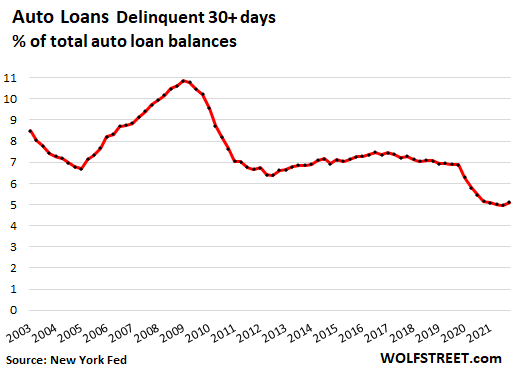

Auto loan balances and delinquencies.

Balances of auto loans rose 6.4% year-over-year to $1.47 trillion in Q1, on much higher vehicle prices and lower volume:

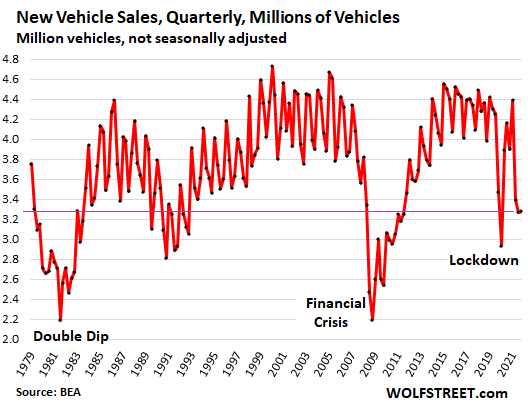

That auto loans rose at all shows just how much more the shrinking number of customers paid for their vehicles because:

- The number of used vehicles sold retail by dealers fell in Q1 fell, including by 15% year-over-year in March.

- The number of new vehicles sold in Q1 fell by 16% year-over-year, to 3.28 million vehicles, right back where they’d been in 1979, due to empty dealer lots.

Auto loan delinquencies of 30+ days ticked up to 5.1% of total auto loan balances in Q1, from the record low in Q4 2021. All that free money, and not having to make rent and mortgage payments helped a lot of folks catch up with their car payments. But now with those programs ended, we can see the first little bitty increase in delinquencies:

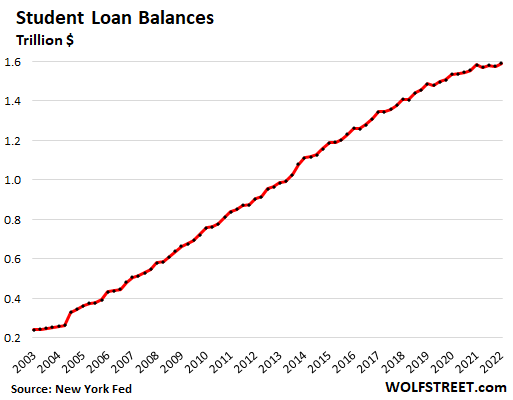

Student loans balances, forborne, and to be forgiven.

I’m at the moment not even sure how to write about student loans anymore. Are they still loans, when everyone expects at least some of them to be forgiven, and some expect all of them to be forgiven? A bunch of loans are already being forgiven even as I write this, and then they’re written off and disappear. It’s a taxpayer asset that just disappears.

Student loans are split into two groups, according to a separate report by the New York Fed:

- Federal student loans: 37 million borrowers, $1.3 trillion.

- Family Federal Education Loans (FFEL) owned by commercial banks, and private loans, combined 10 million borrowers, with $133 billion and $95 billion in loans respectively.

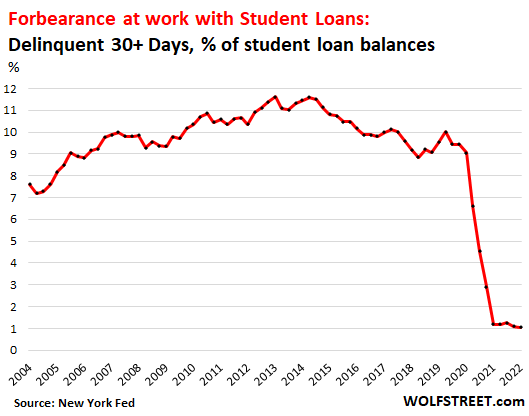

All federal student loans were automatically enrolled in forbearance in March 2020, and borrowers still don’t have to make payments.

Borrowers with FEEL or private loans were not enrolled in automatic forbearance, but were in shorter voluntary forbearance programs and then had to make payments again.

And new student loans are being added. But few pay-downs are being made, and the balances have been flat for a year because loans are being forgiven in big blocks and are written off, just like that, and taxpayers get to kiss their asset goodbye.

The unbearable burden of student loans? So now let’s destroy the ridiculous notion that these poor kids owe $100,000 or $200,000 each, and must therefore be forgiven their student debt because they’ll never be able to pay it off. Surely, some folks, especially those with long graduate programs, such as dentists and doctors, may owe that much, but they’re also much better able to pay for them.

Here is reality – the median loan balance by type of loan. Median means half owe more and half owe less:

- Federal: $18,773

- FEEL: $10,143

- Private: $14,087

All federal student loans were enrolled in forbearance in March 2020 and delinquent loans were classified as “current,” and the delinquency rate fell to something close to 0%.

The borrowers with delinquent FEEL or private loans are now classified as delinquent.

The delinquency rate here is the combined delinquency rate of all student loans, but nearly all delinquent loans are FEEL or private loans, as the federal loans are still in forbearance. And these forbearance programs caused loan balances that are 30+ days delinquent to plunge from a range of 9% to 11% of the total before the pandemic to about 1% in Q1:

Cleaning up credit scores with stimulus money.

Some of the gazillion dollars handed to consumers and businesses alike, and some of the money consumers didn’t have to pay for rents and mortgage payments, was used to catch up with debts that consumers had fallen behind on. Hence the record low delinquency rates in 2021.

This had the effect that credit scores have been rising, and many borrowers’ credit scores went from subprime to prime, and this played out across the scale, and it improved the “credit quality” across the board of consumer lending.

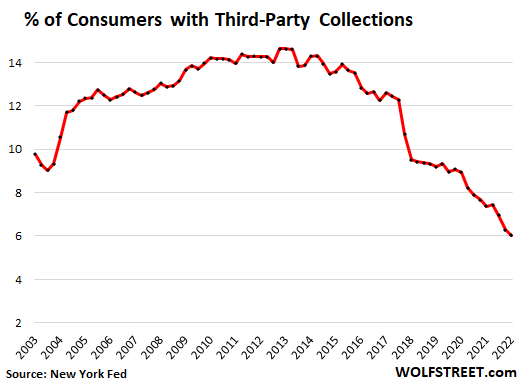

Third-Party Collections.

The percentage of consumers whose loans had been sent to third-party collections plunged throughout the pandemic on a trend that started in 2015, and in Q1 hit a record low of 6.0%. No uptick there yet:

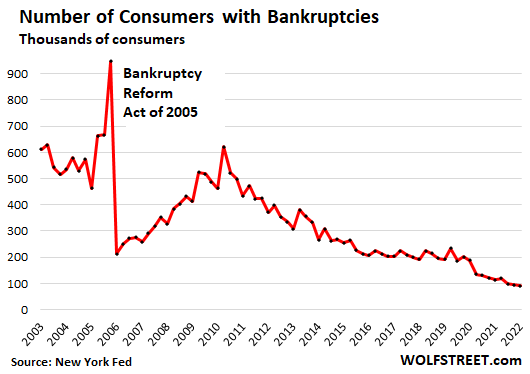

And bankruptcy filings.

The number of consumer bankruptcies in Q1 dropped to a record low of 90,880 consumers. The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 caused a spike in bankruptcy filings before the deadline. After the new law took effect, bankruptcy filings plunged. The Financial Crisis fueled another surge. Since then, filings have declined:

Higher interest rates are not going to knock over consumers yet.

Consumers might gripe about higher mortgage rates and higher rates for auto loans, and they’re going to buy fewer homes until prices come down far enough. And they might spend a little less on other stuff.

But in terms of their debts, and in terms of delinquencies, foreclosures, and bankruptcies, consumers are “solid” and in “great shape,” as Powell keeps pointing out. Credit scores have improved across the board. Delinquencies are near historic lows. Consumers payed down their credit cards, and they’re off the worry list. And the government is going to perform a miracle with the student loans.

This clean-up of consumer credit is why consumers can handle higher interest rates just fine, and Powell keeps pointing it out. And many consumers – particularly the belittled and denigrated savers – benefit from higher interest rates, and they’ll provide some positive oomph the spending when interest rate repression ends.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thank you Wolf – the stark numbers always tell a story and it is certainly better than the off the cuff remarks we typically hear – thank you!

closing on home today

just gonna pay cash for it – don’t want worthless stuff

remember in 2021 that with all stimmie $$ our fiat $dollar devalued 30%

just trying to keep REAL ASSETS in hand

good luck with all those stocks, cryptos

so when 10 year ‘yield’ went from 1.5% to 3% you only LOST 1/2 money

hahahahaha

Certainly looks like the average consumer is in markedly better shape than the lead up to the financial crisis in the late 2000’s. Unless interest rates continue to rise exponentially, a cooling of housing price appreciation or a soft correction seems more likely than a major housing bust (In most markets anyways). Strong employment is a major buffer as well. If layoffs become more prevalent in the near future, however, a lot of these credit and housing figures may turn more ugly. Time will tell!

I’m not sure what numbers you’re looking at, but everything I see points to the most massive real estate bubble in human history. Prices are almost double the last peak in many places, and have zero to do with economic fundamentals. Consider that a 40% price drop only brings them back to the past peak, then let your imagination take hold from there. COULD.GET.UGLY.

Strong employment, relatively “tight” lending standards, limited supply in most markets and a scarce quantity of forbearances suggest, in my mind, that despite ballooning housing prices, what we’re seeing now is diametrically opposed to what happened in the 2000’s. If supply and demand fundamentals drastically change and employment numbers suddenly shit the bed, then I would agree things could get ugly. Still too many buyers still out there drenched in cash scooping up properties.

You just told that lie again – “tight lending standards.” This is braindead vomit that I have shown to be false on this blog numerous times. It’s been subprime city the whole time. Where did you come up with the “tight lending standards?”

Here is a quote from a longer piece I have posted twice on Wolf’s blog. It is from a mortgage article back in 2018. You can find the longer quote most recently under the April 27th “Mortgage Volume Gets Crushed” thread, if you click on Wolf’s “Housing Bubble 2” link in the header.

“Many of Christian’s customers have no savings, poor credit, or low income—sometimes all three. Some are like Joseph Taylor, a corrections officer who saw Christian’s roadside billboard touting zero-down mortgages. Taylor had recently filed for bankruptcy because of his $25,000 in credit card debt. But he just bought his first home for $120,000 with a zero-down loan from Christian’s company. Monthly debt payments now eat up half his take-home pay. “If he can help me, he can help anyone,” Taylor says. “My credit history was just horrible.””

Does that sound like “tight lending standards” to you? Let’s be real once and for all. Stop the f***ing lies.

+1 for ‘drenched in cash’ reference. Lol

DC –

I’m interested in facts about real estate lending laws and standards. I did a few web searches on the article you posted with no results. The longer version of the article you posted on April 27 does not provide any additional general data. The article needs further context to be anything more than anecdotal.

For example, what is the federal government backed “most important affordable housing program” referred to in the article? What percent of the total real estate mortgage balance in the United States does that program represent?

American Financial Network Mortgage Broker, which the guy in your article works for, offers different kinds of mortgage programs: Conventional mortgages, FHA, USDA, VA

What percent of American Financial Network’s business is the type of mortgage described in the article’s anecdote?

My intuition is that the Fed printing 11 trillion or so, and the near ZIRP policy for the last decade or so, was a much bigger cause of real estate inflation than loose lending in a specific government program.

One place to look is the FHA, which insures subprime mortgages and allows for down-payments as low as 3%. There are bout 8 million FHA insured mortgages out there right now.

You can go to the FHA website and look at the criteria.

The VA has a similar program with 0% down-payments (I’m OK with giving Vets a little extra help). There are other federal programs like that too.

drifterprof-

I don’t even care what the percentage of this subprime garbage is, the point is that it’s readily available. Furthermore, you may want to remember that the last meltdown actually wasn’t even due to subprime – prime loanowners defaulted at a higher rate. Bernanke and his disgusting ilk just like to blame it on the poor.

But this subprime is an important factor in actually driving the prices to these levels. You can’t get to where we are without it, and the fraud that is involved. Make no mistake about it, there will be tremendous fraud uncovered once this whole thing blows. The high prices mask it, the crashing prices uncover it all.

And you know what’s going to cause it all to melt down? The declining prices themselves. Once everybody realizes they are in a negative equity position, subprime or prime, they bail. Nobody wants to pay for a house that isn’t worth the contract price. And it’s not just homebuyers, scvmbags like J.P. Morgan and Co. do it all the time with commercial real estate.

“But this subprime is an important factor in actually driving the prices to these levels. You can’t get to where we are without it..”

If Wolf presented some data and reasoning to support that statement, I’d be more convinced. But just one guy’s general opinion with no factual reference or analysis doesn’t cut it.

If you insult people like the OP, you should have solid factional information and analysis. Not a half-baked quote from an article cherry-picked and currently inaccessible.

“If you insult people like the OP, you should have solid factional information and analysis. Not a half-baked quote from an article cherry-picked and currently inaccessible.”

Wolf doesn’t allow links, or I’d post the direct link. And it wasn’t some “half-baked” quote or article, it was from Bloomberg. Heard of them before, smart guy?

Depth Charge,

Go ahead and post the link. Generally, if someone asks for documentation, I will allow the link.

“Depth Charge” appears out her depth here. Pray for her.

““Depth Charge” appears out her depth here. Pray for her.”

Oh, look, a misogynist with nothing to add but gender insults.

1 in 4 purchases are cash. The other 75% require a mortgage. You are free to gamble based on the minority if you wish, but I’m betting based on the majority, which are currently seeing their purchasing power vaporize. With every 1% rise in rates the amount that can be borrowed for a fixed payment level goes down by roughly 10%. That is an iceburg dead ahead of the market. Just read today that ARM use is rising because of this. Amazing. Those borrowers are tomorrow’s defaulters… last gasp of a dying dinosaur.

Depth Charge is a woman? I would have lost that coin flip bet 100 times out of 100.

Please just the post the whatever link. You were given permission.

Personally, I’d jump on the chance to post some.

A lot of money managers I respect believe the over indebted US economy can’t handle more than a 2% Fed funds rate and 3.2% 10 year. Not sure if they are correct, but we will find out within a few months. We tagged 3.2% on 10 year this week and fell back.

Sure, positive rates with negative real growth for 30 years and no government spending. GDP is gonna collapse like a turd.

The only caveat I have for that is that since you’ve never been here before and they’ve never been here before, your guess would carry as much weight with me as theirs…

Here’s the link, Wolf. Thank you.

https://www.bloomberg.com/news/features/2018-05-24/small-time-bankers-make-millions-peddling-mortgages-to-the-poor

This is but a single article. These articles have been a dime a dozen for years. Note that this is 2018, well before this blow-off top in house prices. Subprime has been going on during this entire bubble.

“Why is he confessing?”

“He’s not confessing, he’s bragging.”

– The Big Short, Paramount, 2015

Good run down on consumers under raising interest rates, but Wolf left out the government.

I handle the government in separate articles, with my infamous “Debt out the Wazoo” chart:

I’m not averse to some blocks of student loans being forgiven, such as borrowers who got public service jobs.

However, full cancellation of all student loans is a huge wedge issue that goes beyond the two major tweedledee and tweedledum electoral bases.

Admittedly, perhaps too much of my opinion is based on anecdotal experience, as well as having paid back my own student loans. Having taught at a two-year Colorado state college for a few years, I got the impression that many students were borrowing money to live a college-loan supported lifestyle, not striving for realistic career path.

Word was that a lot of farm-boys in the area took out loans to buy a pickup truck or similar young discretionary lifestyle toy. Some would sit in the back of the class totally ignoring lectures, flashing their new tats and snickering.

So full forgiving of all student loans is pretty much a wedge issue for me which will strongly affect my voting (or not voting) in the foreseeable future.

The forgiveness of student debt is to buy votes.

I don’t believe that forgiving student loans is all based on buying votes. There are various analyses of effects, and various rationalizations.

But to the extent that the goal is to buy votes, it’s a foolish strategy. Most irresponsible or entitled people, or people with poor judgement, are not going to get up off their asses and put in the time and effort to vote. If they feel entitled to not fulfill their responsibilities, chances are they are not in the habit of paying back a political favor that’s already been given to them.

So in this cases like this, the vote-buyer will lose more votes than he or she buys, sometimes lose very bigly. There are similar effects on other wedge issues like abortion.

Drifterprof

Not only that but if they’re not paying back their student loan then the taxpayers are. What’s the ratio of student loans to taxpayers? Sounds like you’re buying 1 vote but losing thousands.

A dude I know said they were promised by the government that the loans would be forgiven in return for 10 years of public service. After 10 years they changed the rules and the dude found out that it was all a lie. The loans would not be forgiven and had to be paid in full even in bankruptcy.

When you hear the words:

“I’m from the government and I’m here to help you” hold on to your wallet. Its the third greatest lie.

The other two are “The check is in the mail” and “I love you honey”

Bambam added a forth one: “If you like your Doctor you can keep him”

+1

Chuck

Absolutely..

What of all the people who COULD PAY, but don’t…waiting for forgiveness…mostly on their kids debt.

How many people with the new cars, two homes, fancy vacations…could pay but don’t? I am surrounded by them…and they all vote Democrat waiting for the forgiveness.

My neighbor just put 100K into his kitchen, and his kids have student loans. If the forgiveness happens, he just got a free kitchen.

And what of the new entries into college…..do they get instant forgiveness of tuition?

Universities must set up their own credit departments….like Ford Credit. They are, after all, businesses.

And the great unasked question…”Why is education so expensive?”

Static courses like math, most science, language, history, etc can be taught with canned lectures and grad student Teaching assistants.

What of all the people who COULD PAY, but don’t

AOC and Tlaib ?

So what was the $2 trillion TCJA then?

In some ways, this is almost laughable…except that we now are experiencing problems for which there likely are no real solutions. Even a casual look at what pakistan and bangladesh are baking in. I mean, relatively speaking, we are arguing over the color of the drapes, while the roof is on fire. Pragmatically, I would have little problem ‘forgiving’ student loans, or whatever we might want to call it, because we did the same things for banks that are, quite literally, felons, and businesses who are making record profits selling us insulin at a hefty markup. Among other things. And we ‘forgave’ them a HELL OF A LOT MORE than $1.7 trillion. Regardless, ours is an economy that requires folks to buy houses, cars, and baubles. And if they financially cannot, or feel they cannot…well, consequences. Buying votes? One of the real problems we currently have is that many, if not most politicians we have are little more than elected lobbyists. So someone worried about ‘buying votes’, now, is just a little bit naive.

> Some would sit in the back of the class totally ignoring lectures, flashing their new tats and snickering.

Sounds bad, but not as bad as students taking online (video link) classes and turning off their cameras, meaning they might not be there at all. The high number of such blank screens in the little “Hollywood Squares” video display is about as insulting as it gets.

So there is a petty form of moral hazard, but a form nonetheless. I would NEVER have been so discourteous to an instructor (or the subject), no matter how banal the person was.

Blame the student’s parents for the rudeness attitude.

Sorry over 18 = adult. Not a parent problem.

SteveO, it’s a direct reflection as to how the parents raised their children and to what moral standards they instilled (or didn’t) in them.

“Sounds bad, but not as bad as students taking online (video link) classes and turning off their cameras”

Is that really so bad?

I mean I’m 59 and attend several video meetings a week. I turn my camera off most of the time. For example yesterday I was in a meeting and my camera was off. At some point I wanted to show a circuit board, so I turned on the camera briefly and then turned it off again.

So IMO if a student is listening and answers questions when asked, I don’t have a problem with them turning off video if they are not comfortable with it on. However, if they are turning off the camera and not in attendance, then yes that is very rude.

The government should never have guaranteed any student loans at all.

The existence of loans and loan guarantees is the primary cause of soaring costs and lack of affordability. My six years at a state university cost about $10,000 total in the 80’s since I lived at home. One of my younger co-workers at my employer completed an “executive” MBA program at the same institution (sometime within the last ten years) at a cost of $45,000. That’s insane.

Harvard has endowment funds of something like $30B (or more) and should be subsidizing those they want to accept entirely at their own expense, not the taxpayers. Same for others. They purportedly already do a lot of it anyway.

The university “industry” is one of the few where providers can perpetually charge above their supposed customer’s ability to pay. Without loan guarantees, they would have to find a way to cut costs or close.

“The government should never have guaranteed any student loans at all”

The very first thing Obama went after when he was elected was the federalization of student loans.

historicus,

I’m so tired of this BS. I had a federally guaranteed student loan in the early 1980s under the FISL program, which was created in 1965. Most people that went to college after 1965 have had access to federally guaranteed student loans.

What Obama did was for the federal government to take on the student loans directly, which cut out private profiteering lenders that benefited from the government guarantees and got rich of risk-fee fees and interest.

FWIW, my student loan came with an interest rate of 8%, and the monthly payments were a pain in the butt, but instead of whining about it, I paid it off as quickly as I could to get rid of it and be done with it, which took a few years.

AF-

“The government should never have guaranteed any student loans at all.”

Agreed.

When the you subsidize bad behavior, what do you get?

Bad behavior.

In this case the bad behavior is loan abuse, university sprawl, rampant educational price hiking, abrogation of contracts (“debt forgiveness” and/or delinquency), and college entrance shenanigans.

Who pays? The taxpayer, the most serious and talented students, and employers who must hire from a diminished hiring pool.

Subsidies, in their infinite forms, have unexpected and socially destructive consequences.

The definition of colleges and universities have changed. Before the 80’s most universities lived by endowments and grants from successful patrons. Most instructors lived in housing provided by the university paid for by patrons. Student tuition was very low due to the nature of philanthropic giving. Employees were often scholars brought in under a stipend that covered medical and living. Now the university kept the royalties from inventions and did not give back to the inventor in major ways. This is why this practiced died. Children of brilliant teachers did not benefit from their parents patent. The school, or the benefactor, did. When the scholar was to old to contribute they often ended up living with adult children or given to charities. Most successful scholars went on to work for benefactors. If the benefactor was a fair person everyone excelled. Those that did not lived much like the hourly or salary individuals of today. The universities, or colleges, are now ran like a full business in which scholars expect a decent pay equivalent to that in the workplace. This include benefits. Benefactors do not give us much and cost of housing meets with todays cost. Student Loans thy name should be poor business practices.

During the era you refer to offspring of university employees attended university for free. Employees living on campus for free no. I was a plumber while attending university. I did many plumbing jobs at professor homes in 1970 s. In the 1970 s no student loans for white males.

Unless the field of study needs Lab instruction, the courses can, entirely, be on line.

In my field of work, I am required to take Continuing Education. Knowing that 95% is totally worthless to what I do, day to day, every single one of the classes-lecture can be done on line.

But we are required to physically show up, where most of us then sit in the back of the room, on our iPhones, ignoring the useless boring lecture.

Each weekend of this farce is at least a $1,000 expense I must endure. Money I could be using, instead, for $5 gas for my huge truck.

It is a huge money making racket. Just like Colleges are today.

Perhaps Professor Wolf could do a WTF article about College.

Gabby Car,

I love you but all and every part of this is nonsense:

“The definition of colleges and universities have changed. Before the 80’s most universities lived by endowments and grants from successful patrons. Most instructors lived in housing provided by the university paid for by patrons. Student tuition was very low due to the nature of philanthropic giving.”

Is that the kind of BS that gets circulated among young people to show how good boomers had it? Let me tell you, we went to the cheapest colleges because that’s all we could afford, and we paid tuition, and we lived in unspeakable roach-and-rat-infested dumps because that’s all we could afford, we worked while going to college (I worked 48 hours a week as a security guard at night Fri-Mon), we ate the cheapest worst food because we couldn’t afford anything, we never ate out, we had nothing, and worked hard to get through this, and somehow got through it. And then we spent years in shitty jobs that didn’t pay enough… Back then, our elders told us that it was part of “paying your dues.” And eventually, we got our shit together, and life was pretty good, but not until then.

My clearest memory of college back in ’74-’77 was being hungry all the time because I couldn’t afford to buy much food.

Everyone had money before the 1980 recession. Why would anyone need a student loan unless you were in dentistry? In Canada if you didn’t have the money you went to college instead of university. I don’t know anyone who had a student loan.

I don’t see the problem as being who offers/backs the student loans, how much colleges charge or how large the college endowments are. The problem is that we don’t teach basic business principles to high school students so that they can assess the cost / benefits of going to college as if they were a business considering a major capital investment. Would most people pay $60K, picking a number, for an empty cardboard box? No, of course not. We need for the students to see that paying the same amount for an empty degree (one that won’t produce a decent return) is equally problematic. Then, those that chose to go to college as a business investment won’t have as many problems paying the student loans back and we won’t care as much about who made or backs the loans.

Those hefty university endowments have to be getting fat haircuts in this market. Many along with pensions got out of energy before the run up to virtue signal and probably bought RE, crypto and other unicorns at the top. I had a pension with a large system in California and was able to roll it over time self directed ira last year. Sleeping pretty good right now!

All those politically correct/virtue-signalling endowments must have a chart lkike ARKK these days.

Forgiveness = giving money to lenders via the taxpayer, and rewarding debt junkies. BIG NOPE. I am firmly – vociferously – against any student loan forgiveness period. Go to work and pay off the debt. You chose it.

Yup! Or allow it to be shed in bankruptcy. Then the lenders will have to eat the loss.

Why should the tax-payers be left holding the bag at the whim of the politicians?

Can this (such write-off and the power to authorize the write-off) be taken to the courts?

Again moral hazard and making fools of sensible prudent guys.

A lot of stuff this administration is doing is actually illegal. They know it, but they do it anyway until the courts stop it, finally. I have never seen anything like this in my life. They just stomp all over contract law and do whatever they want. It’s incredible. Politicians have become emboldened dictators all of a sudden, and it’s not just the US. We are in dangerous times.

Student loan debt is not forgivable in BK.

Beardawg,

Correct, but why.

By the end of the 80s the news was filled with stories of doctors, lawyers and other professionals who loaded up on student loans and then walked through bankruptcy to discharge the debts. Once discharged, they could start a practice …

Also, there were no teeth in the collections of these debts as the same sorts would just refuse to pay … and never be penalized. Obviously, Banker Biden (Senator of Delaware) used the opportunity to support the banks and make these loans non-dischargeable. Given how angry the public was at the scofflaws, they cheered at the legislation.

While I don’t care for the current status, I wouldn’t want to return to the old practices.

exactly my sentiment. this ‘take out loans to live a lifestyle of not working while I go to school’ is a root cause of the labor shortage now that these same people are graduated and expect to not have to work and get their loans paid off.

work while in school – even if part time – and pay back the debt you took out.

Don’t ‘forgive’ the student loans. We all know the taxpayers will end up paying for the balance, while the educational institution will continue the scam.

Instead, make it possible for the student to declare bankruptcy on the loan, and if the student does, void all credits/degrees received under the loan. You can’t just void one side of the equation.

And yes, I paid off my VA student loan.

I put in 4 years in the military between 1964 – 1968 and got the G.I. Bill ($222/month at that time) to pay for college. With that stipend, and part time jobs, I got an engineering job and an MBA. NO LOANS TAKEN.

The military G.I. Bill now pays $50 K (last time I checked) for veterans who want to go to college.

The military is available for those who wish to go to college if they can’t fund it on their own.

Edit: engineering “degree” not “job” from college. Got the job later.

You were pretty lucky. They ended that program years ago.

This: “And eventually, we got our shit together, and life was pretty good, but not until then.” My life in a nutshell.

Dawns,

Much simpler solution. Allow the IRS to handle the debts. Make the debts payable over the working life of the debtor with payroll deductions similar to unemployment, SSL, and other deductions. No work? No pay…easy deal.

…And I’m talkin 4-5%…a doable figure.

In the UK students loan payments are collected only through payroll deductions, with the first £20K or so exempted, then written off after 30 years if not paid. The interest rate is pretty high though….government studies have already concluded that mist of the cumulative debt will be a write off…oh well, at least no being hounded to the grave…

Yes, the point is, to allow the the borrower to have some options in paying off the loan, but to make the borrower ultimately responsible. Even in BK, the terms are negotiable.

Student loans cannot be discharged via BK.

LOL, really? Seriously? Wow!?!

The whole premise of student loan forgiveness is beyond stupid and very regressive. Let’s forgive the debts of people with above average earnings potential because … ? Even people with “some college” earn more than people with no college. Just cut checks to everyone or to low income families if you want to buy votes or redistribute wealth.

Just allow student loans to be discharged in bankruptcy. That way the issue will fix itself.

Imo it’s very un-American / un-capitalistic to have a private debt that has special rights where it can’t be wiped in a bankruptcy.

You know, I wonder how much of a positive election issue forgiving student works across the entire voter spectrum?

My gut feeling is that it pisses off many more voters than it benefits.

So it might be a big plus for a narrow band of Democrat elites but an overall loser as a campaign issue.

Big plus for the Republicans in 2022?

Agree it’s a very bad idea for taxpayers to pay off ”most” student loan balances by GUV MINT.

Also agree it’s a very bad idea for GvMnt to provide student loans or for that matter ANY loans at all.

GvMnt subsidized or supported loans are truly the foundation of the crazy situation we are in and have been in for decades.

But it’s nothing new: when I finally paid off my private college loans 50 years ago, the lender told me I was the only one he had loaned to who had paid anything at all,,, then he opened a bottle of VSOP cognac — that cost then what he had loaned me — which we totally consumed that evening as he told me of his experiences as a spy in the OSS during WW2.

It was the first and only time he mentioned those experiences in a 40 year relationship; wouldn’t talk about it otherwise…

Great Guy!!! R.I.P.

Totally agree ,pissed is a great word,does not teach accountability.No wonder this country is SCREWED

Agreed that arranging some forgiveness for those that commit to public sector jobs for a specific period of time probably puts some semblance of fairness to managing down this large debt problem.

The key is to prevent this from continuing to be a problem. Schools and institutions that encourage students to go into debt should be made to share in the payment guarantee. So that in future, they will act as control and limit to this becoming a large problem again.

It affects my vote too. The majority of students are not intentional scammers, but there are enough that I would never vote for anyone touting loan forgiveness.

There are the practically unemployable who have figured out that they can live tolerably for four or more years in their middle age taking out loans and getting grants, including vocational rehabilitation scams. There will never be a payment in these cases as these people have no assets. They are a small number, on the margins of society, but sane enough to play the system.

The ones that affect my vote, however, are the car/wedding/luxury student housing big spenders. The ones I know have been government employees who make the minimum payment because they fully expect that public servants will have everything forgiven. They also max out other debt to maintain their lifestyles. One I knew had about $20K starting 20 years ago, still outstanding, and the other played the system for $80K at a public university.

I don’t see any fix coming for the broken higher education system. People have always gone to school for various reasons other than learning, but high living off loans is a newer one. Again, this is a minority of entitled cases among people I have known, but one too many is enough.

Simple fix ,make people claim single and zero dependents .Then keep there tax return until loans are paid in full .Then watch universities start to crumble

A better fix would be to remove all government loan guarantees, and allow all debtors to go through bankruptcy if needed. That would put the risk where it belongs, on the institutions making loans.

I know a fellow who made a decent living recruiting students for vocational/technical schools. His pitch was all about the Loan Loan Loan. He got a percentage of the loan. So that was his big selling point.

Before the internet made “online learning” possible, around here it was mostly learning “Truck Driving”. For a while around 2000 it was “movie making” and designing video/arcade/online games.

Then there were the farm boys who thought they were getting an engineering degree. They mostly wound up working as laborers setting up and pouring basements for suburban homes.

It’s a wedge issue for me as well. If they want to encourage education, they should enact incentive legislation prospectively, so everybody has equal opportunity to benefit from it. Bailouts for selected individuals after the fact and “equal opportunity” do not reconcile.

Further, what controls would they have in place to ensure only qualifying needy students WHO CANNOT GET A JOB are targeted. We’ve seen how government handles programs like this. Remember PPP?

I’m OK allowing students to work off the debt via temporary guaranteed government jobs. There’s lots of infrastructure to be done. If they can hold a $1300 iphone, they can hold a leveler or shovel.

I doubt all the unions getting all those government contracts would allow this. Every student working off their loan would be taking away a [high paying] union job. They would fight it tooth and nail. I can hear it now “Scabs” “Union Busting” Anti American”.

EL-you forgot to add: “…and the corporations who employ those union workers…”. (Unions don’t generally own contracting firms…)

may we all find a better day.

“But lenders, amid the surge in home prices and improving job market and rising wages, helped their customers exit forbearance by modifying mortgages or refinancing them.”

Indeed, the Fed and the government bought all the duct tape they could with those trillions and wrapped it around the economy. I have done this with tail lights and it works wonders with preventing things from falling apart. I kept doing this for years like the Fed. One day due to rain and speed the duct tape fell off my tail light, and then a cop pulled me over.

I use duck tape to keep the frunk on my Tesla from opening on a freeway.

Yeah, we call it, “Going NASCAR!”

The proper term is, “Helicopter tape.”

I use a thin strip of it on the top & inside of my right-side bicycles’ chain stay.

“The proper term is, “Helicopter tape.”

Dan,

In the military, the proper term is “100 mile an hour tape”.

Duct tape is also known as “poverty chrome”.

gaffa (gaffer) tape’s better than duct, if you can find it…

may we all find a better day.

Paying back a loan you voluntarily signed up for is now looked at as a foolish decision.

“And new student loans are being added. But few pay-downs are being made, and the balances have been flat for a year because loans are being forgiven in big blocks and are written off, just like that, and taxpayers get to kiss their asset goodbye.”

“…taxpayers get to kiss their asset goodbye.”

That is the crux of the problem. If those debtors are not going to pay, then the tax payer will pay one way (through inflation and money printing) or another (direct taxation).

Debt that is defaulted or forgiven does not extinguish in our current distorted capitalist system. It is paid through taxation, through inflation and money printing, or simply by taking it from those who were prudent and responsible. Debtors and irresponsible spenders are usually looked upon as essential to the consumer economy while savers are despised. Hence the responsible are Going Galt which is why you have such labor shortage.

Oh yes, I’m sure the reason for labor shortages is because the responsible are going galt. More like the boomers were given another handout via asset price manipulation via stimulus and artificially low fed rates and they could retire early and sit on their asses complaining how no one wants to work. The unlucky younger ones see no point participating in a rigged economy, have turned nihilistic, and are doing the bare minimum to survive

Yep!

The next credit crisis won’t come from US consumer debt. It will come from somewhere “unexpected” where most aren’t looking, like China, Japan, or EU or US corporate debt.

The other mistake many people make is looking at things linearly when that’s not what happens. Given the leverage in the (global) economy, it doesn’t take much of an “accident” to create a “black swan” (actually, something which should be totally expected) to trigger tightening financial conditions. Whatever the supposed “reason”, it will be psychological, as always.

Look at the US bond market recently. Rates have barely started rising from the all-time low (it’s barely noticeable on a long-term chart), yet market losses are big.

It won’t take much more before many US corporations with garbage balance sheets (which is most) start gasping for financial air as they are shut out of the credit markets.

Are the low interest rates that started around 2012, the reason for the ever increasing debt from credit cards and consumer loans?

I haven’t carried a balance since 2012, so don’t pay attention to rates on credit cards. I presume rates since 2012 have been lower than previously (don’t actually know) but I wouldn’t call it “low”, by current standards. I would call it “low” by the actual risk lenders are taking but which is papered over by fake “growth”.

So, IMO, not usually. The artificially low rates since 2008 (really since 9/11 before housing bubble 1) have been more of a factor in rising corporate and government debt.

Corporate for LBO and stock buybacks which are a quasi internal LBO in some cases. Governments because whatever fiscal discipline these entities had before the GFC (which hadn’t been much in a long time either) totally went out the window. The USG is among the worst.

Auto pay

Never paid interest on credit card ,and they pay me to use it .Greatest invention since sliced bread

Has the Fed mentioned anything about taking bank and corporate Bailouts off the table in the future? Of course not. The important ones (to them) can’t be allowed to fail.

This has been about banks, corporations, and the super-rich all along in case you haven’t noticed. Whatever goes down, it won’t be them.

Great ideas here today but expect more of the same, just look out for yourself and your family. The only way politicians are replaced nowadays it seems is when they die of old age sitting in Congress. After a while, someone will notice or they start smelling worse, then they get rolled out.

I’m very confident most of the 724 billionaires and their less affluent counterparts will also “lose their shirts” when this financial house of cards comes crashing down.

I’m confident because there is no basis to believe that those with the most influence (which doesn’t include most of the 724 billionaires) will choose to defend fake paper wealth over real world “hard power”.

As exhibit A, the public, economy and markets will be thrown under bus to preserve the Empire which requires the USD as global reserve currency.

The FRB has no motive and isn’t going to trash the USD to save billionaire fake paper wealth, especially since the USD IS the basis of the FRB’s power too.

AF, I’m watching the implosion of the cryptocurrencies as part of the next credit crisis.

If one accepts that cryptos have no intrinsic value, then they are all basically credit bubbles build atop the dollar. No different from bonds unbacked by either sustainable cash flows or adequate collateral.

Sellers make off with real dollars and bagholders eat losses.

Social peace bought with funny money is TRANSITORY. Powell can put that in his pipe and smoke it. This joyride will not be exited so easily.

Powell has about $85 million in “funny money”. He only had $50 million in his piggy bank when he started the job as National Counterfeiter.

He has plenty to put “in his pipe” , as does all of his family for decades into the future.

Sri Lanka is in riots over food and energy,coming to your neighborhood?

A few months ago someone from Sri Lanka sent me this:

Rice 1 kilo—-now–140-160 rupees. Former price—44-50 rupees

Sugar 1 kilo–now—135-150 rupees Former price—50 rupees.

Bread 1 –now—75-80 rupees Former price—50 rupees

Gas 1 cylinder now–2750 rupees Former price –1250 rupees

Cement 1 bag now–1900-2000 rupees Former price—850-900 rupees.

Dang, they can’t even afford to make cement boots for the corrupt government officials…

They have been rioting there since my sister-in-law went there 15 years ago as a member of the Non-Violent Peace Force. It’s a wonder she didn’t “take one” for the natives when she was facing down the Rebels.

Not a fun place to live….

America has been a textbook model of paying off or co-opting (brainwashing) the lower classes into submission. The only comparable precedent was European Feudalism.

Extend and pretend!

Overfeed the pigeons and then stop, and they’ll start eating each other. And anyone else in sight.

As Wolf makes note of frequently how this process of unwinding QE and Interest Rates will take time with the credit markets showing the slight tic upwards.

Balance sheets of the consumer is much stronger based on the data provided. A piece that may be missing is the interest much of this debt is issued at is at 3 percent or less in many cases vs the 2008 crisis with interest rates north of 5 percent.

So the picture for the consumer is even stronger than the data charts provided in my opinion.

Recession may be further out than I thought.

But how much are of variable rates? The small uptick in rates is already showing an uptick in delinquencies. The cheap money train has left the station.

Consumer solvency is primarily dependent upon employment. Have you seen the recent CNBC article claiming 64% of US househoids live paycheck-to-paycheck?

This is an extrapolation from a survey but indicates that household finances aren’t actually that great and it isn’t just low income households either. The likely disconnect between this survey and Wolf’s article is that first, the survey is subjective. But second, the debt statistics are an aggregate. It lumps the wealthiest (who often have a lot of debt but can easily service it) with the middle and lower economic class who individually owe a lot less but a disproportionate percentage at or near broke.

Given how terrible corporate balance sheets are now (the absolute worst ever), it won’t take long before a noticeable percentage of these entities run into liquidity problems and the pink slips start flying. When that happens (as it does in every recession), consumer solvency will be exposed for what it actually is, most Americans are actually close to or broke.

Many companies have extended maturities on their substantial debts but that doesn’t solve the problem of new financing which many need (regularly) in addition to rolling over existing debt.

Think of it this way, if perpetual prosperity was really a function of just “printing” and providing “free” handouts, there would never be a recession anywhere, ever.

One other thought. Just because the economy isn’t in a technical recession doesn’t mean living standards aren’t falling. That’s what’s happening now, except to the extent the gap is being plugged by debt which this data indicates is happening. Despite the fake “growth” last year, real median household income fell anyway.

> Just because the economy isn’t in a technical recession doesn’t mean living standards aren’t falling

Isn’t the standard of living of those working remotely and relocating to LCOL areas from HCOL areas increasing like crazy?

Augustus Frost,

“Have you seen the recent CNBC article claiming 64% of US households live paycheck-to-paycheck?”

These types of surveys ask – and have asked for decades – the same question about “savings” and if people don’t have “savings” they’re said to live paycheck to paycheck.

But this is BS because people no longer have “savings” because it doesn’t pay anything. They have investments, such as 401ks, and equity in their homes, and they use electronic means for cash-flow management, namely their credit cards, which most people pay off every month as the money comes in, as you can see in the chart above. No one needs “savings” anymore. And savers have been punished for 13 years through interest rate repression.

They need to change the question to fit modern cash management methods, but then it won’t generate the kind of clickbait-headline article about living from paycheck to paycheck, but rather some complex nuanced thing that people don’t read and won’t spread around.

I respectfully disagree. There are multiple surveys showing that about half of Americans, when asked, can’t afford an unexpected 1,000$ expense. This isn’t about savings accounts vs someone with brokerage account assets, it’s about half of Americans not having 1,000$ to pay for a broken furnace.

There wouldn’t be so many payday loan places if that were the case.

Harrold,

Hahahahaha…

My response was in response to this, in case you missed itt:

“Have you seen the recent CNBC article claiming 64% of US households live paycheck-to-paycheck?”

64%! That’s nearly two-thirds of the population. But payday loans are a MINUSCULE portion of consumer lending. Why? Because they’re a total ripoff and everyone knows it. In 2020, total payday loans outstanding were $32 billion with a B compared to, with a T:

$11.5 trillion in mortgages and HELOCs

$1.5 trillion in auto loans

$1.3 trillion in other consumer loans, such as credit cards, personal loans, etc.

Your comment gets a gold medal in today’s One-Liner Ridicul-Olympics.

According to FRED, median net worth was $121K in 2019 and somewhat higher now. So yes, 64% is exaggerated but most people are still actually close to broke since this number includes everything including the kitchen sink.

Many people have more home equity now because of the housing bubble. They can always borrow against it and increase debt further.

I am confident only a very low proportion have any meaningful liquid “savings” (of any kind) outside of retirement accounts like a 401K or IRA. Some of this is accessible and some of it is not.

It’s really hard to accumulate meaningful “savings” in a taxable account as spending money, unless you are really frugal for a long timer, make a bunch of money, inherited it, or made a windfall during the asset mania. The overwhelming majority haven’t done any of that.

The vast majority are also very exposed to the asset and credit mania. Everything looked great in late 2007 and less than a year later, the economy and with it the majority of the population was at risk of economically falling over a cliff.

@Augustus re: “…home equity now because of the housing bubble. They can always borrow against it and increase debt further…”

I’d just edit “always” to “currently” – we both know that both the equity and the affordability of the home-equity-lending are in jeopardy.

The coyote is over the edge of the cliff. The credit card was the first parachute. Home equity will be the second. But demand destruction is Fed-mandated to bring down inflation. There will be more pain and a lot of lowered expectations.

Is not solvency pretty much always depending on cash flow?

That people live pay check to pay check is a sign that expenses and income balance and there is no slack in the timing.

No problem with this as was with just in time supply chains. If there is a large disturbance on the other hand, there will be problems.

For now. When they participate in our morning-after economy for a while with 50% costlier mortgages and 15%+ costlier essentials and companies looking for “efficiency” over growth, this will all change.

It’s like when you’re still a bit drunk in the morning and don’t quite have a full hangover yet…but it’s coming.

Good analogy in my experience will:

”It’s like when you’re still a bit drunk in the morning and don’t quite have a full hangover yet…but it’s coming.”

Finally, WE the PEONs who are prudent and savers We can at least HOPE that we will see enough of a ”over hang” that TPTB will at least take this opportunity to sober up for a while instead of just doing what so many drunks do and they, the corrupt politicians, etc., have done so far:::

DRINK MORE and drink earlier and drink the next morning to avoid the overhang and go to work or drive drunk as has clearly been the case by GUV MINT for many decades.

It truly is clown world. Hard to imagine how and when it will end.

The sun will burn out, and the universe will expand to the point everything freezes.

Ohh, but if you mean this economic cycle, markets will drop 20-30%, the fed will say mission completed on fighting inflation and proceed to cut rates again.

If you have any other theories, take a look around, if you aren’t in a mansion eating cavier, then you know your theory is wrong.

I’m actually of the firm opinion that we aren’t even having inflation. The price rises are actually all the government military related subsidies (i.e invading and subjugating 3rd world countries) is losing impact on prices for oil, minerals and food stuff products.

Now we’re just paying the actual cost for stuff.

I agree, but I think we need to add the factor that essential resources are becoming more scarce, too. The low hanging fruit was picked a long time ago.

As an aside, the 70’s student loan situation was equally ridiculous. Students taking out huge loans at then very low rates and investing the loan proceeds at high Volker era rates 20% ish. Others

bought expensive guitars. Reminds me of Groucho who famously said the government is adept at causing a problem, misdiagnosing its cause, and applying a completely ineffective fix.

Where do I apply to get my paid-off student loans’ balances returned to me? I will even negotitate on the back-interest owed to me since paying them off about 30 years ago. Not sure how to calculate that part nor the opportunity costs on that money, though. Maybe a Wolfstreeter can work on that calculation. Anyone? Oh maybe I can: 1 part wishful thinking times 2 parts thackamuffles times zeeeero.

Exactly. The level of unfairness in this is incredible. Not only do those of us who paid for our own college get the shaft, but the people who chose not to go to college because they didn’t want to go into debt and couldn’t afford it are punished for their responsible, yet personally impactful decision.

There is tremendous, and I mean TREMENDOUS anger out there over this stuff. The politicians are really pushing the limits, not to mention doing their best to bankrupt this country for good.

Politicians are mostly hearing from those who still owe now, especially those with worthless degrees but large loans.

The student loan program should be abolished.

I’ve got over $100,000 in outstanding student loans (undergrad and grad school out of pocket), and I will absolutely lose my sh*t if blanket forgiveness happens. I entered a contract, and now I’m abiding by it and paying back the money (sure, it would be nice to not have that payment, but I’ve definitely come out ahead).

In any case, I refinanced my loans to private a bit before covid to get a lower rate, so I expected to get hosed in any forgiveness program on top of paying this whole time. At least I’m not my former coworker who used the money “saved” in forbearance to buy real estate in Seattle. I expect he’ll be regretting that in a few years.

That should be LOAN coyote

What a weirdo. You are playing by a rule that no one in power in this country actually plays by and you want, what? A fucking pat on the back for being a good little serf? Your coworker is smart. You’re an idiot. Especially, refinancing federal to private when there is the possibility of some sort of forgiveness. But the olds who spend all their time on this comment section will be by to drop you a comment saying that you’re doing the right thing lol. Maybe that means something to you

Harsh, Phoenix.

How old are “the olds?”

I suppose I’m one.

Think of the kids who joined the military rather than taking student loans. They must be thrilled to see that they could have had a free education without putting their lives in peril.

Depth Charge, I like your reference earlier about what precedent the Commander In Grief is setting by pushing carte blanche Student Loan Debt absolution. A student loan is a binding legal contract between the money provider and the money consumer, the student in the latter case. I had a National Student Loan when I attended Michigan in 1974 to get my very productive MBA in Finance that took me 10 years to pay off; and I don’t regret the necessity of same or the burden it placed upon me during the amortization period.

We have a nation of Whiners. We have a nation of entitled individuals that put their inherent freely-incurred responsibilities upon the tax paying public. College is a waste of time and money for many of today’s applicants, and technical training would be a far more useful pursuit as well as a much more cost to benefit positive one. Liberal arts are wonderful, but get your wrists ready to be flipping burgers when you graduate with a BA.

To say that American consumers are fine this nanosecond with raging inflation and ballooning interest rates combined with incomes not keeping pace with said inflation is to spike the football on the 5-yard line. I watch Metcalfe of Seattle run like the wind to the endzone about 2 years ago, then spike the ball on the 5 yard line. Weighing some 230 pounds he left everyone in the dust, it was wonderful to watch such a big man motor along until the final act of stupidity and mis-timed celebration.

“Great shape” and “solid” just doesn’t come to mind when one looks at the Real After-Tax Income charts of Americans over time and look at the metrics that determine true financial health such as Debt to Liquid Asset coverages. Powell and his merry bunch of self-enriching men don’t have a clue as to the real condition of the man or woman on the street!! They are more attuned to the Hamptons crowd and Wall Streeters, their own financial advancement, and have not personally shopped for groceries in the last 30 years.

I too am a Baby Boomer, Wolf, and am also proud of it for I had worked very hard for almost 5 decades to get to where I am; never a hand-out or debt-forgiveness or forbearance from anyone and only whining now in Old Age due to stiff joints. Americans would do better to blame the image in the morning mirror that to attempt, ad nauseum, at casting blame for the pit we are in onto everyone but themselves. We allow these charlatans to keep sticking it to us, so we possibly deserve what very dark place we are now in.

There is tremendous, and I mean TREMENDOUS anger out there…

Which, depending on your perspective of those currently ‘in charge’, is precisely why they would do it. More division, more diversion, etc.

Some good news and tomorrow maybe inflation will tick down just a bit. We’ve already rotated the balance in stocks to value, and bond buyers are locking in higher rates. Oh and the deficit is falling. Paying down the debt. Maybe the sky is falling.

It better tick down a bit. It’s been going straight up for months. That’s not how inflation normally works… it should go up and down in zigzags and waves, not just one brutal spike.

I doubt it will tick down. Didn’t PPE come in hot last month? That points to gangbuster CPI.

As you said Wolf, the inflation mindset seems to be ingrained within consumers.

There’s been NO paying down of the debt for decades…just the annual increase in debt slowed down a bit (as it should’ve, as we exited the pandemic)

Math comes out to $35k per borrower. That is a lot of money. I am not in favor of loan forgiveness. Had a friend who was $250k in the hole for two masters degree. Sadly, she is a project manager at a state facility and has verbally told everybody she never plans to pay them back. This flippant attitude sucks.

We all know the government will never be able to restart the payments. It would be to draining on the economy or some other malarkey. “It would be a catastrophe to add this on top of the pain of inflation” imagine Yellen stating. We just have to find the money to spend and pretend

“Math comes out to $35k per borrower.”

That’s the AVERAGE. Averages are skewed by outliers. That’s skewed by the 10% or so that have over $100k in debt, and maybe 3% over $200k in debt. But now they’re doctors, and they’re trying to buy $1 million homes, so they can pay off that debt.

I gave you the MEDIAN in the article. Median means half owe more and half owe less:

Federal: $18,773

FEEL: $10,143

Private: $14,087

This means that half of the Federal borrowers owe LESS than $18k, half of the FEEL borrowers owe less than $10k, and half of the private borrowers owe less than $14k.

Keep in mind many times those borrowers overlap. I had Federal and private loans for sure (maxed out the federal loans and had to supplement), and pretty certain I had FFEL as well.

On the plus side, college is the one time it pays to be poor. The need based grant from the school covered a majority of the cost and I ended up with “only” $50,0000 of loans.

I guess Nathan failed 4th grade math. Student loans versus more killing equipment for Ukraine and the world. I vote student loans.

False dilemma fallacy. The better answer is neither.

Ukraine by a mile. People can work during college. Ukraine is a line in the sand. If dictatorial countries can invade their neighbors willy nilly with no consequences, WW3 is at our doorstep. See 1937-1939 for details.

If everyone who now currently has a student loan refuses to pay, until the feds print up enough money to pay it all back for them [and maybe force the lenders to take a haircut on the deal], won’t that destroy the program for the next generation of borrowers? Who would ever make another student loan?

Full disclosure – I paid off all my student loans as soon as I got out of school.

The government guarantees most loans. That’s politics.

Whatever private lending remains only exists because of the credit mania. It’s part of the multi-decade trend where most lending is based upon cashflow instead of conservatively valued collateral. It’s worked to this point because total debt outstanding has only increased, except for a tiny decline during the GFC. It’s inherently unstable and destined to collapse because the overwhelming percentage of these debtors aren’t actually credit worthy except under artificial conditions.

Without a credit mania and government guarantees, there would either be no student lending at all, very selectively at much lower loan balances, or the institution would have to do the lending directly.

Why must money be made to pay back these loans?

Money today is fiat money. The government can if they so decide say that all students loan are void, nullified and that those money did never exist.

Ok, some bookkeeping rules may have to be modified to accomplish this or at least not end with funny looking checks and balances in the books.

Yes, based on your theory of this just being some bookkeeping entries, the government could hand everyone $1 million dollars for Christmas.

My wife graduated veterinary school with 220k in loans at an average interest rate of 6%. She’s on a 10 year repayment plan with a minimum monthly payment of $2400/mo. Long story short we’ve been paying close to 4k/mo for the past two years, and have just over a year left before it’s all paid off (final balance likely ends up closer to 300k). That’s the cost of higher education right now.

My wife graduated Veterinary school in 2017 with a student loan balance of 220k. She’s on a 10 year repayment plan with a minimum monthly payment of 2400/mo. Long story short we’ve been paying 4000/mo over the past two years and should have the whole balance paid off in another year or so. Without my additional income she would have been hosed paying those loans herself (veterinary income is good but not THAT good). Cost of higher education is brutal.

What school charges $220k for veterinary education?

Easy to get to that number with undergrad and very school, actually probably below median for very school grads.

Vet school…

That would be Iowa State.

Fortunately my wife didn’t have undergraduate loans as well; she has quite a few friends/former classmates who have over 400k in loans between undergrad and grad school. Much more common than you’d think.

I took out $20k in student loans for undergraduate education decades ago, which would likely be the equivalent of $80k at today’s tuition rates. I kept costs low by staying local, living with my parents, taking the bus, etc. When I landed a job, I lived for a few years out a fleabag apartment, specifically to pay down my student loans. I had them paid off within 4 years because I was saving so much. I still had a ton of fun though.

If you cut all expenses to the bone for a few years, you’d be amazed how fast student loans can be paid off.

Wow two masters, the first major had to be dumb as hell to put oneself through the ringer again

Some people like to see those abbreviations after their name…..makes them feel important.

I’d bet that doctors and lawyers owe the largest amounts. I don’t think its unusual for doctors to graduate with $300k in debt. Cost of medical school is approaching $100k/year.

Wolf, at what point ( if there’s such a possibility) will a saver see a meaningful interest rate on their savings?

“Meaningful” meaning more than inflation, so at least 10% or so. Personally I don’t see this kind of interest rates on savings before hell freezes over.

Remember, the whole purpose of that famous “2% stable inflation” is a psychological trick to sell continuous theft to the masses. In this scenario, if one doesn’t get a pay raise, one is perhaps disappointed but it feels completely different from an announced 2% cut in wages. If one gets a 1% raise, one is happy, not realizing being still 1% in the hole.

People will probably be happy seeing savings interest rates go up to 8% or so, while they continue being robbed of 2% per year, just like they were in the “2% stable inflation” times with 0% interest rates. “Plus ca change…” so forth.

Most people lack basic math skills and the powers that be know all too well how to capitalize on that.

If by “saving” you mean long-term (1 year plus) parking of $10K or less per person per year (or $15K if one uses the max allowed $5K of your tax return as well), then the “I” Series Savings Bonds at the US Treasury now offer a 9.62% return, indexed twice a year for inflation.

That’s about as good as one can get for “meaningful interest rates on their savings” these days, IMHO. Maybe there are other options, I don’t know…

Wow, from reading the comments about student loans above, you’d think we’d just revived Reagan’s Welfare Queen trope. I believe I’ve hit my limit of white men (most over 50, I suspect) complaining about everyone who isn’t as privileged as they are, lumping them into anecdotal bins where everyone who took out loans and now can’t pay them back was either partying or spending the funds on new cars and vacations. What’s next? Evoking the cliché underwater basketweaving invective to describe anyone who didn’t go into STEM or become a plumber instead?

The comment I find especially galling is the one suggesting that those who can’t afford to pay should be permitted to file for bankruptcy, but have their diploma ripped away. I happen to be one of those people, and let me tell you, I worked my ass off for that degree. I was paying back my loans ahead of schedule until something changed my life forever, something beyond my control. There are lots of people to whom sh*t happens and they can no longer pay. How magnanimous to suggest they can forfeit 4 years of hard work and end up even worse off than when they had the temerity to believe they could better their lives by attending university.

Wolf, thanks for the housing bubble info. Your charts are excellent and I’ve returned here to the site multiple times for those. Normally, I just ignore this stuff, live and let live, but I can’t take the Ayn Rand MAGA hat vibe in here any longer.

Like you said, ‘Shit happens’. No one said you ‘had’ to declare BK.

“There are lots of people to whom sh*t happens and they can no longer pay.”

Many of the tax-payers who are left holding the bag (just because they can be stiffed by the politicians) also are people to whom sh*t happens. That does not matter?

No KPL…..it DOESN’T matter.

Unless…..you also object to our massive military and constant wars.

See, those MIC industries are the REAL welfare queens.

Someone defaulting on a student loan is peanuts compared to our 1.5 trillion per year war making machine.

“Unless…..you also object to our massive military and constant wars.”

I do.

Very poor logic. What does education have to do with war funding? You are trying to link two issues that have zero connection.

Yours is a “tit for tat” argument where one party does a boondoggle (say, tax cuts for wealthy, or excessive defense spending, or PPP program), then another party tries to correct it with crazy random bailouts, under the “two wrongs make a right” theory.

Neither party has credibility in that world.

You should be arguing for balanced budgets and meaningful progressive tax rates on individuals and corporations. Every dollar spent have to come out of another person’s pocket. It would put a quick end to all boondoggles. No freebies for anyone, except those who truly need it. Make a reasonable argument like that, and people might listen from both parties.

Bobber

The logic is impeccable.

Student loan liability and MIC / military outlays are both taxpayer liabilities.

If you hate paying taxes you object to both liabilities.

If you hate one and not the other you don’t object to taxes.

If you don’t object to taxes, why are you complaining ?

OTB,

An apple is NOT the same as an screwdriver, just because both are purchased.

You can argue excessive defense spending is the wrong thing to do, but that doesn’t make a student loan bailout the right thing to do.

I think you know that, and you are trying to defend a bad argument for some reason.

Bobber

Your logic, yet again, is flawed.

Why do you dance around the subject?

If you hate paying taxes just admit it. Both the MIC and student funds fees come out of the same pocket, your pocket, all of our pockets.

Just admit you love the MIC and would give them your money freely.

Just admit you hate student loans out of disapproval of our sons and daughters education. Envy, eh ?

Haha!

You two just made DL’s point and don’t even know it.

My sentiments exactly DL, except I NEVER considered education hard work, or a means to a damn job.

I consider learning a privilege and love and continue it to this day, this site being my only Econ interest. Mostly I like sciences, especially Bio, but with some History and Anthro thrown in. The comments under this (and others) particular article I consider Soc, and draw much the same conclusion you did. Yeah, heavy Ayn Rand vibe…..survival of the richest.

“ I believe I’ve hit my limit of white men (most over 50, I suspect) complaining about everyone who isn’t as privileged as they are, lumping them into anecdotal bins”

Damn…

Did your student loans not pay for the classes in contradictions, hipocracy and bias…

BTW, I intentionally misspelled one word… can you find it…

May I humbly suggest, as I would like to hear your thoughts, that you drop the ‘tude…

And FYI, I never went to college… waste of time for me and I didn’t need to…

I would bet she got a degree in some type of woke studies.

I may be Privileged, but she is Entitled.

I doubt if Rand would agree with MAGA. Ayn would have coined:

“Make the Individual Great Again.”

MA

Confirmation bias much ?

There is a difference??!!??

I think not, Mr MA….Besides MIGA wouldn’t work politically, not when you are blaming “woke elites” to get votes.

BTW: I liked “snowflake elites” better as an insult, woke sorta implies “more aware”……you know….asleep/awake? I could be wrong as I am the insult target.

It shows.

COWG…I have LOTS of college and flunked your test, thereby proving your point…I guess…..although do I have a suspect word…..

And thanks again DL, for making things more interesting.

Agree the lucky are insufferable.

It’s a Calvinist thing…runs deep in this culture.

No doubt many black people and others have been conned by the educational industrial complex into taking out loans to blow on “education.”

The educational industrial complex (EIC) thrives on advertising such as “Be the first in your family to attend college.”

Mostly by PRIVATE colleges, yes?

Entrepreneurship (aka “American Innovation”) at it’s best.

You sound just like the type of person who has what it takes to pay off their loan.

Good. Don’t stop. Work at it, an pay it off.

MA

You sound like the type of person who says: I got mine. F**k you.

Thanks again DL, for pissing off all these…ahhh….folks.

DL, you said you worked very hard for your degree [I believe you].

I am just wondering what you got your degree in that you can’t/ won’t pay back your student loan? Would you dp it again?

Full disclosure-I got a degree in Philosophy but I never expected that someone else would pay for it. It was my choice and I paid for it in more than one way. Still h lad I did it.

And THIS guy is worth $20M (so he said), so obviously he’s glad….Philosophy eh?

Wow, just wow!