But wait… Haven’t seen anything yet. Impact of today’s holy-moly mortgage rates won’t show up in the sales data for a couple of months. Here’s why.

By Wolf Richter for WOLF STREET.

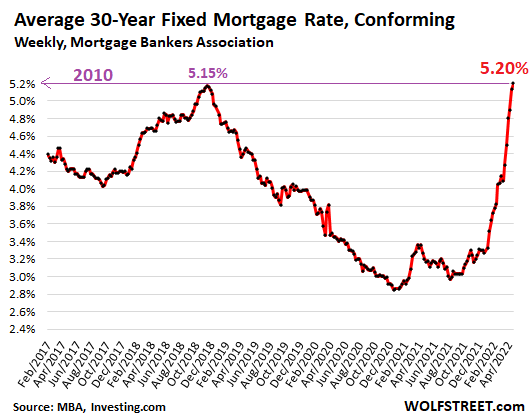

The spike in mortgage rates – a result of the Fed’s widely telegraphed future crackdown on inflation – would sooner or later have to impact the crazy housing bubble. We knew that. Now the average 30-year fixed mortgage rate has spiked to well above 5%.

For example, the Mortgage Bankers Association reported this morning that its weekly measure of the 30-year fixed rate jumped to 5.2%, the highest since April 2010, two full percentage points higher than two years ago, “causing a pullback or delay in home purchase demand,” the MBA said. “Home purchase activity has been volatile in recent weeks and has yet to see the typical pick up for this time of the year.”

Given the huge increase in house prices, to be financed with these much higher mortgage rates, well, we know how this goes: Sales will decline because there are fewer buyers that can still afford to buy, and inventories will rise because there are fewer sales and because fidgety owners of multiple homes who hung on to those homes to ride up the market all the way are starting to put them on the market.

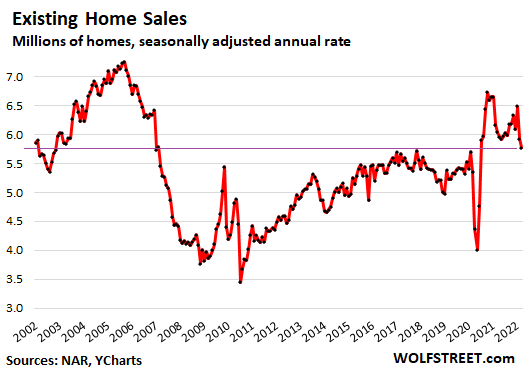

So today, the National Association of Realtors reported that sales of previously-owned homes – houses, condos, and townhouses – fell to the lowest since June 2020, down 4.5% from a year ago, the eighth month in a row of year-over-year declines, even as supply of homes listed for sale rose.

The NAR expects home sales “to contract 10%” this year, it said, and it blamed mortgage rates and inflation: “The housing market is starting to feel the impact of sharply rising mortgage rates and higher inflation taking a hit on purchasing power.”

But wait… We haven’t seen anything yet. It’ll be two months before the effects of today’s holy-moly mortgage rates show up in the data.

The sales figures today are based on sales that closed in March, meaning that many of the deals were made in February with mortgage rate locks from February or January or even prior, when mortgage rates were much lower. In February, the average 30-year fixed rate rose from 3.7% to 4.1%. In January, it was around 3.5%.

Many homebuyers today and in the coming weeks still have rate locks with lower rates from prior months. They’re still able to buy with those lower mortgage rates. But buyers now entering the market and who get a rate lock from today on are looking at mortgage rates above 5%.

In other words, we won’t see the bulk of the effects on home sales from today’s holy-moly mortgage rates until the sales data for May is released in June.

Sales of single-family houses dropped by 2.7% in March and 3.8% year-over-year, to a seasonally adjusted annual rate of 5.13 million houses, the lowest since June 2020.

Sales of condos dropped 3.0% in March and by 9.9% year-over-year to a seasonally adjusted annual rate of 640,000 condos, the lowest since August 2020.

By Region, the percent change of the seasonally adjusted annual rate of total home sales in March from February, and year-over-year (yoy):

- Northeast: -2.9% from February, -11.8% yoy.

- Midwest: -4.5% from February, -3.1% yoy.

- South: -3.0% from February, -3.0% yoy.

- West: no change in February, -4.7% yoy.

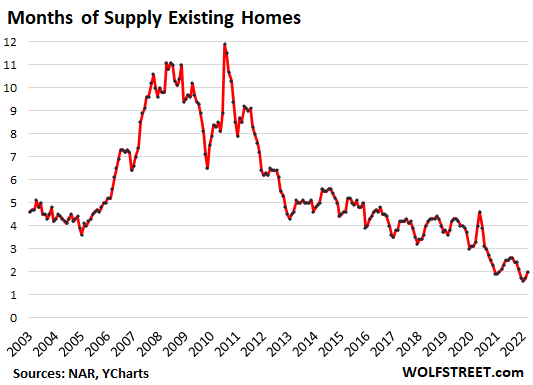

Supply of homes listed for sale rose to 2.0 months, the second month in a row of increases, from the record low in January (data via YCharts).

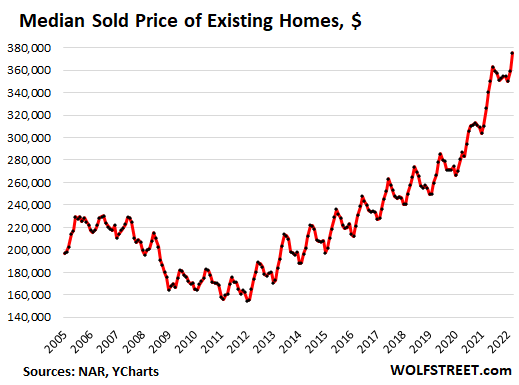

The median price rose 15% from a year ago, to $375,300. The year-over-year spikes had peaked last May and June 2021 at over 23% (data via YCharts):

Investor share of sales remained roughly in the same range. Individual investors or second-home buyers, who make up many cash sales, according to the NAR, accounted for 18% of the transactions in March, down from 19% in February and 22% in January, but up from March 2021 (15%).

“All-cash” sales rose to 28% of all transactions, compared to 25% in February and 23% in March 2021. As overall sales decline due to rising mortgage rates, and as sales to homebuyers who have to get a mortgage decline in particular because they cannot afford it anymore, the percentage share of all-cash sales increases automatically, even if those cash sales themselves don’t increase.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It seems much of Wolf’s predictions will depend on when and how fast the psychology reverses.

For example, in 2008 many were saying cities like San Diego (no more land to build) and Seattle (something special about Emerald City) would never experience a downturn. Two years later sellers were rushing for exits and prices were cut at least 30%.

Right now however many seem to think that they can stay where they are until the Fed again drops rates to negative territory and pay people to buy a house. The “Fed has your back” has spread to housing mania.

I believe the Fed will prove to be more impotent this time than omnipotent. They can’t depend on deflation due to globalization like they did in the last 20 years and keep on printing money, and now they have to worry about the end of the dollar as reserve currency.

Even at 5% rates the Fed is still paying speculators to Buy, pay a little interest, get a little rental income, then sell at a higher price. Easy money while it lasts!

So far in 2022, owning houses beats owning stocks or bonds. And until it becomes unprofitable, housing speculation will continue to drive up house prices and drive innocent young couples insane with frustration.

We know how speculative-frenzy stories have to end. But like a bad movie, the plot will take way too long to unfold…

The Federal Reserve doesn’t pay anyone interest except to Banks on IOER (Interest On Excess Reserves) and what it pays in the reverse repo markets for US Treasures.

My point was metaphorical not literal.

Because of below-inflation interest rates, it pays to be a speculator, buying houses and then selling them at a higher price.

That’s as good as if the Fed IS paying them.

The Fed must be held responsible for the effects of their policy.

True, but housing is not a liquid asset. Many such speculators got their assets handed to them in 2008. I believe the same will unfold soon. So far they don’t believe the Fed and are in denial phase. This normalcy bias will cost them dearly.

“Even at 5% rates the Fed is still paying speculators to Buy, pay a little interest, get a little rental income, then sell at a higher price. Easy money while it lasts!”

I am not sure what you are smoking, but it’s really good stuff. At current prices, there are almost no markets where rents allow a speculator to get positive cash flow. When I was last looking for a rental, I was offered a house on 5 acres for $1,000+ LESS than their mortgage, and they said “it’s negotiable.” I declined because the asking was still too high. And they purchased at probably 25% less than current pricing.

To play devil’s advocate, an investor doesn’t have to get a positive cash flow on a rental for it to be a good investment, ASSUMING the asset value appreciates. Heck, the investor doesn’t even have to rent it out– which is actually happening a lot and is absolutely horrible for the vast majority of Americans. I think the point of the post you’re responding to is that if real estate appreciates at 10-20%, a 5% mortgage still makes it profitable, and any rental income is just gravy.

Now when the mortgage rate exceeds asset appreciation, then these speculative investors will be in a bind. They’ll have to take a loss on rents since the overall market (led mostly by existing homes) sets that. Perhaps the madness will continue with all-cash buyers but it seems like this won’t be the best investment and we should (hopefully) get a correction.

I think Wolf’s point is that the real interest rate on that loan is -3.5% (5% mortgage – 8.5% inflation), so the Fed is indirectly paying you to buy a house using a mortgage. And that doesn’t even get into the likelihood that inflation’s actually worse than 8.5% given the way the Fed has modified the CPI over the years.

You don’t need positive cash flow to make a profit on a house as a speculative investment, if the sales price is sufficiently higher than the purchase price.

What I’m saying is that it’s not enough for rates to be high, they have to be high enough to stomp out the rising prices that are encouraging the speculative buyers.

Housing should be for living in, not for trading like stocks or bonds.

Yep.

The spread between the inflation rate (loss on cash) and the 30yr still prompts businesses to buy real estate. Note I said businesses in the business of buying real estate.

And there is a clear consolidation of ownership occurring.

Until there are many who have bought at higher levels, wanting out….this will continue, IMO.

For entertainment I listened to a real estate podcast. The discussions were all about continuing to cash out the new found equity and buy an additional property even if you dump your 3% loan and get a 5%. Crazy times. Leverage makes people go insane.

I vividly remember 2008/09 in San Diego where people used to think San Diego is different: No more land to create. Lots of rich people, Best Weather, everyone wants to live here, lots of golf courses. Hence prices in San Diego can never go down :-).

My friend bought a home in 2005 for 750K in San Diego. IN 2006, he put it out for 790K, had a offer for 760K he rejected. Finally the home got sold for 480K. This is a classic example of chasing down the market.

Hiking rates would not only impact housing but other consumer spendings as well e.g. autos.

My SD home lost about 40% then. But I was never underwater, having paid steadily since my ’94 purchase. All this points back to the unfashionable virtue of patience, and soundly paying off the mortgage. Sort of like holding good bonds to maturity?

Today, I owe less than $10k on it, and pay less than $400/mo on my loan. I would rather sleep in a house than on a blockcahin or in an NFT! The something-for-nothing mentality needs to be wrung out. That means subjective pain. And patience.

Oh and my home energy bill this month? $18. San Diego has that gorgeous Mediterranean climate.

“Oh and my home energy bill this month? $18. San Diego has that gorgeous Mediterranean climate.”

You and your house gloating are pretty played out, IMO. You have been virtue-signaling the shit out of your life ad nauseam.

If you have a home to live in then it does not really matter. The pain would be for investors, both small and big.

I own my home in SD with no mortgage.

I am looking for avenues to exit CA for better places. Just few more years. SD is becoming unlivable with more and more passing time.

Holy mackerel !

I agree with Depth Charge this one time !!!

I am in SD proper and my energy bill is $200/month. Water bill is $150/month. No solar though. Family of 4.

Run away before u run out of water ,nothing much exists in a desert inviroment

Just wondering how much you house went back up?

Seems like houses everywhere are worth far more than they were in 2008-2011.

If you bought in 2006 and rode it out you would very well off today.

DC, “virtue signalling?” No, just living it, straight up. I’m not lying. The facts are the facts. I’m living creatively and, as it is said, traveling light. If you and enough others had a whiff of this creativity, virtue and discipline, the world wouldn’t be deteriorating into a crowded dustbin of elbowing pigs, crying for more silly privileges and, like you, everyone else’s head. But I’ll let your own skyrocketing blood pressure settle our accounts. Zero cost to me.

“If you and enough others had a whiff of this creativity, virtue and discipline, the world wouldn’t be deteriorating into a crowded dustbin of elbowing pigs, crying for more silly privileges and, like you, everyone else’s head. But I’ll let your own skyrocketing blood pressure settle our accounts. Zero cost to me.”

Wow, talk about unrestrained arrogance. You bought a house in 1994 before any of this nonsense was going on, lucked out due to filthy, reckless central bankers with no moral code, then have the audacity to call yourself creative and virtuous while castigating those affected by skyrocketing shelter costs as you spin yarns about your perfect house and life? How gross.

He bought in 2005 and was selling in 2006. Can you say SPECULATOR? These are the idiots who need their clocks cleaned. Let’s get back to houses as shelter, not financial hot potatoes.

DC: He didn’t say why his friend was selling. If he sold for $480K, he wasn’t necessarily “speculating”. If he was, he sucks at it.

$18 energy bill? Mustn’t even wash his clothes or have hot water. Our monthly power company service charge (aka connecting fee) is $20 and we have inexpensive power.

Apologies, bough in 2004 and selling in 2006 and he wanted to move upto larger home.

He did move into larger home and bank ate the losses as it was short sale I guess.

Yes, it reminds me of the free-range chicken joyfully proclaiming how wonderful it is to breathe fresh air, eat fresh worms and live in peace…

The free range chicken was riding in an empty box car looking for somewhere he could earn a living….just like people were during the Depression….I never saw the humor in it, but then I hate corporations and their endless consumption marketing shit.

San Diego RE prices are absurd and will once again fall as we enter into an inevitable recession and bear market, along with continuing non-transitory inflation and rising interest rates. I have so many friends and family around the country and – GASP! – none of them want to live in San Diego! Blasphemy, I know.

If devaluation comes anywhere close to the last bubble event it’s going to be disasterous. Last time – minimal homeowner skin in the game. This time – lots of skin in the game.

Yes, they all want to live in Austin now. Now, let’s compare San Diego and Austin real estate prices.

San Diego may fall, but Austin will get crushed. The real FOMO is not in San Diego, it’s in places like Austin and Phoenix.

It will be the same as the GFC. Once house prices start to decline the Fed will drop interest rates – perhaps into negative territory.

You have interest rates at -2% or -5% you are crazy not to buy a house.

Absolute bargains will abound and house prices will shoot up again.

The best time to buy a house was yesterday, the next best time to buy a house is NOW.

I wouldn’t hesitate if I was in the market.

Buy now or forever regret not taking the plunge.

I’ve noticed that if you google “30yr mortgage rates” Google’s answer will typically be 1.5%-2% higher than actual average mortgage rates. Wonder if it’s too tin foil hat for Wolfstreet to wonder if they’re doing a gov’t a favor here. The inflationary mindset vs. google’s informational monopoly.

The mortgage rates we cite here top tier borrowers with conforming mortgages. So with a near-subprime FICO score, the mortgage rates will be higher. Lots of borrowers are near-subprime and below.

In general, I don’t know how to explain Google’s answers. Some of them are really way off. I call it Google Humor. If there is a link, go to the link and see that they say.

Mortgage rates are all keyed off the yield (interest rate) on 10 year US Treasuries and that is the reason that mortgage rates are rising right along with leading US Treasury interest rates soaring. The Federal Reserve will be entirely out of the MBS markets in the very near future.

I started looking again in the North Tampa FL area about 3 weeks ago with a realtor I had worked with back in early 2020, right after COVID… while showing us a unit, it slipped out of his mouth that he was already out of the market, had sold his home (without telling his wife apparently) and was renting waiting for the drop.

That makes zero sense, but good story….

It wouldn’t surprise me if over the next 1-2 years we see a dramatic rise in bankruptcies and foreclosure activity … time will tell.

Much of that could come from HELOCs. Many homeowners may have paid off their homes or locked in very low rates, but they binged on taking cash out of their house. Those rates are not fixed and spell trouble as rates rise.

If I understand correctly HELOC debt has been falling since 2008. Half as much debt now as then. Can’t really see them as a driving force in foreclosures or bankruptcies.

If HELOCS are declining I’d infer that lenders don’t think they’ll get enough money back after the house is under water.

Lots of homeowners did cash out refi’s. Then used the money for toys and vacations.

It wouldn’t surprise me at all if everything is 2x higher in a couple years. The fed is much faster on the gas than the brake.

I’m afraid that there is so much pent up demand and anxiety around housing, that prices will remain stubbornly high, even if rates go higher. Everyone around me thinks I’m insane when I mention the prospect that prices can in theory go lower.

The last housing bust took five years to play out. And longer if you consider the last year of the boom, when the edges were already coming apart. This is a slow-moving affair.

I believe lack of the Fed maneuvering room this time will accelerate the timeline for the crash. Balance sheet is too bloated, the Fed is way behind the curve, and inflation is raging. What took a 2-3 years to play out after 2008 should take place in a year or so. Jay stopped QE and is about to embark on QT. It is do or die time for the dollar.

Ooof. I bought my first place pre-pandemic and my second place very recently. I live in multiple cities/states, and that has been my norm since 2012 so nothing necessarily new.

I did the math 1,000 different ways (trusting no one else) and decided to buy a property that was affordable within the context of my liquid net worth. I also turned over every rock for about 9 months and only bid with laser precision twice on properties that I believe are minimally overvalued relative to the market. My greatest risk (IMHO) is losing roughly $187,000. And that assumes I sell not necessarily at the very bottom but somewhere within 10% of it.

I did a bunch of stress testing as well of various bearish scenarios that clearly show waiting and renting 5 years will cost me $143,000 ($330,000 total loss) more than a $187,000 loss. Of course, I’m never selling either property regardless of what happens to the price.

Add that on top of the money lost by living in subpar conditions. And the fact that we’re hoping to have a child in the next 12-18 months.

People forget housing is not an investment, it’s a place to live. That said, I’ll happily buy tons and tons of real estate in 5 years if you’re right, Wolf.

I find it funny that everyone and their mom largely believes housing will crash soon. I tend to think that’s a lower probability event than most, though not one I’m willing to bet the house on (literally). A 10-20% correction? Healthy. A 40% crash? Yeah, okay. Maybe in Austin, Phoenix, and generally very poor purchase decisions (of which there are plenty).

My memory is hazy, in 2008 was there an online MLS? I am wondering if tools like Zillow will accelerate price discovery so it plays out faster this time. I bought in 2011 and I remember my realtor gave me a special MLS login, and in 2008 I was looking at prices in the paper but maybe I was behind the times.

SilentC,

Funny that you bring that up. In California, there was a website that published MLS median price and volume data monthly by the major cities, no paywall, within about a few days after the end of the month. Sometime after the Financial Crisis, it was acquired by what became S&P CoreLogic, and the whole thing disappeared. That’s how it goes with real estate data. These people HATE competition.

Wait until the demographics kick in. We’ll see abandoned houses. Our population is only growing due to folks living longer. Immigration is not keeping up. Birthrate is way down. Not sure exactly when this kicks in, estimated over the new few decades.

The saving grace now is high employment. Recession eliminates jobs, forcing folks to move, which in turn forces them to sell their home, or just walk away. Likely a long slow deciline in prices.

Let the rates rise. Rise baby rise, I got a boat load of cash waiting for deals…

Quite FrankLY, you’re off the mark here about demographic trends at least in the next 20 years.

BTW – you and everyone else are waiting in cash for deals. Amazing and about as intelligent as investing in ARKK in September 2020.

With our business…we are the canary in the coal mine….spring rush….dead.

Housing will tip into recession by fall time. Inventory to work through…that which is not canceled…will get us through the year.

Alot of dead weight to be cut. Will be able to let go the ones who work when they want. Keep the good ones paid and give them extra time off. Hope it’s not as bad as 08, and we dont flush another generation out of the trades.

At least this time around we are debt free.

What part of the construction cycle are you in?

I’m theorizing but the guys who grade the lot might be the first to notice a pullback where as painters/window installers might be the last. I could be totally wrong though.

I was working clearing and grading lots when March 2020 hit. Suddenly we went from having 90 lots in queue to having 6. I went from working 6 days a week 10-12 hour days to working 2 12 hour days. Less than a month we were contracted for 400 lots, across 3 adjacent subdivisions. Boss got scared and said 7 days a week, sunup to sundown (illegal in trucking), flat rate pay on a 1099. No OT, no benefits, nothing all at 12.50/hr. Not even paid driving to the job site in the company truck from the bosses house. Clock started when you got on the job. (also illegal but everything we did broke laws and regulations)

I told him eat shit and got in another truck and started pulling groceries coast to coast instead of trees and stumps. Then I wisened up once more and got a union job where I don’t exist solely to work 70 hours a week. Maybe one day I’ll smarten up again and get a white collar job like professional grifter… But you know, in a suit with an American flag pin and not a tattered trench coat and boots where you can see my toes.

12.50/hr for a heavy equipment operator?

Wow have not heard of that in 20+ years.

The “boss” must have been able to hire & train illegals

for a good portion of crew.

Private, or union, I know what they are paid in my little slice of the world. I would have gave the boss the same answer.

Atlanta suburbs and north GA. This was with a cdl as well.

Most operators in the area made 15-16/hr with really old hands getting maybe 20. Tack on another couple bucks for a CDL.

I was on the low end but I’d just been laid off so it was the first position that offered something. I know where I’m at in the northwest anyone that can even tell you what a trimble system is are making 30/hr. It’s crazy.

I hear ya.

When I take trimble update

Classes I’m the only old guy in the room. If gps goes down

Nationwide alot of machinery

Including ag would come to a stop.

My company did the same and used the rush last spring to pay off most of our debts. I can say that we’re seeing a massive slowdown and I don’t think it’ll take until fall at this rate. By July the housing market will have gone from a raging river to a small creek. We run a moving company in one of the “bubbly” cities so I would assume we would be one of the first industries to feel the slow down. And we can feel it.

Wolf, I love reading all your articles, haven’t found anyone else that understand all this the way you do. Housing is in trouble, everyone in my area(small vacation town in northern MI) has been spending over asking price and covering the difference between the appraisal and the offer with cash. Never seen anything like this before.

But I would like to see what your take is on the Transportation industry. I work for a large freight broker and the last 4 weeks we have seen rates decline at a rapid pace. The amount of trucks to loads ratio is basically start to even out. If this continues at this pace we will start to see trucking companies fold due to the very expensive equipment they purchase the last 2 years with the combination of high diesel prices. Is it due to it being a election year? Or are the inventories back up? Or investment $ just dried up? Looking forward to what you find!

Jer08 – I think zerohedge had an article on this in the last week or two. Stimulus money drying up, more truckers coming back to work, as well as businesses slowing down restocking. My guess would be hesitancy as well, as people see gas, food, and housing prices jumping so much.

It’ll also be interesting to see effects of China throttling supply with all their lockdowns, which may hurt truckers short term and then help if there’s a later surge in goods coming from China.

I’m sure Wolf has more thoughts and ideas on this. I just figured on adding my two cents before the Genius steps in.

Freightwaves CEO just did a fairly bold prediction that trucking is headed for a bloodbath. He cites the load rejection rate as a solid indicator of market direction. Google it.

We manufacture truck equipment and are starting to see orders flatline after a crazy 2021. We ran OT for 16 straight months and came down off of it in March. Hovering around breakeven order/ship rate right now. Any slower and it’ll be pink slips for the newest folks.

I don’t run for dispatchers and load boards and that rat race, I service restaurants but I’ve noticed our product we deliver is getting smaller and smaller each week. When I leave the scale I’m lower and lower again. The only exception is loads going to really rich tourist towns like Jackson hole or Sandpoint etc. They’ve remained unmoved accounting for seasonality. Last year I was pulling loads over legal gross weight this time of year. Company paid the fines, we were making so much it didn’t matter. Run they said. Same time from a year ago I’m barely cracking 60k on the scale. It’s anecdotal and all but it raises an eyebrow.

I can see these are small steps towards the removal of crazy prices but at this point in time I see these as mere noise.

Also, Mortgage rates have to rise a lot I think to make any dent in pricing. Although some of my friends have been priced out because rates doubled.

IN last 2 years, home prices increased 30% or so.

No, rates don’t have to rise much at all. Look at the relationship between the amount that can be borrowed and interest rate for a fixed payment level. That’s what matters since most people can’t increase their payment level. In fact, with inflation out running wage growth, a lot of people would like to decrease their payment level. At any rate, the aforementioned relationship is dramatic. I think there is roughly a 10% decline in the amount that can be borrowed for a 1% rise in the rate if the payment level is held fixed. We could easily have a 30% decline in purchasing power soon, and we could go beyond that. This is a very predictable train wreck.

I agree. If payments rise $600, The qualifying ratio has to rise by 2.5 – 3 times. Incomes are not and cannot keep with that. Therefore price has to come down to accommodate.

jon-

I just posted last thread the difference between the monthly payment on a $500k house at 3% interest vs 5.35% (the latest rate Wolf cited). Based upon 5% down, it’s $700 more per month and an additional $240,000 over the life of the loan. That $500,000 house is now $740,000 due to the increase in rates. The idea that this is “mere noise” and won’t “make any dent in pricing” is delusional.

The collapse of the Japanese yen during the past few weeks has contributed to this mortgage rate rise, too. Japan is the largest foreign owner of 10-yr treasuries ($1.3T) and they will be buying less due to their own yield curve control struggles decimating the yen at the moment.

In Canada, realtors are threatening realtors who post listings which fell in value for the past few months. Canada wants to censor dissidents when it comes to the real estate bubble.

Okay, that’s funny right there. Realtors don’t control the price, the market does.

Now that’s funny!

I’ve been getting blown out by 6 figures for a year and a half now in Canada. Something interesting is starting to happen here in Ontario an hour outside GTA.

1. Seeing homes that sold 6 months ago get listed for 200k higher than the owner paid. Then they sit. And sit. Usually they delist them after a month.

2. I see homes list for prices that I consider to be high, but not insane. Made an offer on one, went 200k over asking. Was rejected. Next day house was relisted for 350k higher than original asking. 3 weeks later it’s still sitting there.

3. Many more houses on the market than this time last year. Sales not keeping pace.

The party is almost over, but these idiots don’t want to believe it. Bring the pain!

Fewer units sold means nothing without PRICES actually coming down.

In fact, fewer sales might lead to higher prices due to supply/demand imbalance.

Millennials will be priced out of homeownership for the rest of their lives.

Prices don’t come down until they have to. They’re the LAST item to come down. It’s when you cannot sell at the price you want, and you have to sell, that you will lower the price, not before. This is a slow process.

Declining volume along with rising supply are among the first indicators of a market softening.

Back in 2005 the first thing I noticed before the real crash hit was that it took longer to sell the houses on the market. Then all hell broke loose. This hasn’t happened yet, as of April 2022.

Has an entire generation of Americans ever been priced out of home ownership for their entire lives before? Or would this be another first, aka This Time It’s Different?

Well, think about it this way. At least multiple bids over asking have fallen off a cliff in the Portland Oregon area. That alone is having a substantial impact on curtailing the rise in prices.

Everyone knows real estate is a balancing beam ,interest rates on on one side ,home prices on the other side .It went way out of balance on interest rate side now will correct ,hope you didn’t over leaverage yourself

I’m trying to learn how the 25 bp effr hike correlates to the 10 year rising and which of those has had the greater impact on mortgage rates rising.

Here in Bend, home prices reached 2006 levels in 2014-2015. We moved here in 2015. Thinking we were at a peak, I didn’t buy. Prices have more than doubled since then. It’s been 7 YEARS of reading articles about how “continued low interest rates are fueling this red hot housing market”.

It’s all been so frustrating. I’m just glad that for some reason rates are going up, and I’m hoping for a major correction.

It is more than interest rates.

We are entering a “Crack Up” boom. The proliferation of Federal Reserve Notes will create an increase in housing prices simply due to the amount of “money”..

You are too late.

More and more paper will raise the prices simply because of the flood of paper notes. Imagine there is 5 Trillion in “Dollars”. Then, the FED creates 5 Trillion more in 2 years. This, regardless of inflation, recession, wars, depressions, will increase the price of the homes.

You lost out. You are too lae.

Have you considered Oklahoma? Easy flights to anywhere. Sensible legislature. Home prices make sense. It’s where the normal people live now…

True Dat!

I have a friend who buys raw land in OK on a regular basis. He grew up there and knows the market well. And Tulsa isn’t a bad place to live.

“Easy flights to ANYWHERE”? Will Rodgers “World” Airport must have REALLY grown since I was spending a lot of time back there in late 80’s-2002.

And what is a “Normal People”?

I could probably make a guess…….

Home prices have many influencing factors primary as u say price and interest rate

Then qualifying level (income) and as mentioned coverage for inflation

None of these appear to be positive for future price escalation.

Social impacts as well with a country of renters.

Housing drops will take years in my humble opinion

Last week I mentioned that a house, near me, in Northern California had been reduced from $599 to $559. It went pending within days. Will post here when the closing price is listed.

Wolf…

Your thoughts on the mantra that showed up in the markets today…

1. There are real returns in the interest rate market now.

2. Bank of America calls for a 2.25% ten year yield.

To point #1…..I can not understand the calculation. Are they looking at the Ten Year vs. the Fed Target for inflation? That is ridiculous IMO, if that is the case.

historicus,

What the media is referring to as “real yields” are the TIPS yields. TIPS holders get compensated for CPI inflation by having their principal increased based on CPI, and the principal value of the security rises with CPI inflation. Hence “Inflation Protected” (the IP in TIPS). During the pandemic, the 10-year TIPS yield turned negative because the principal value of the securities increased. But recently, this yield has turned positive for like one day. You can get the quote here:

https://www.cnbc.com/quotes/US10YTIP

thanks

Right and bonds rate are not set negative at issue, they can’t do that. Buyers bid up zero rate bonds, same as negative rate EU bonds. If you bought TIP bonds before 2020, you have a positive fixed rate probably, your bonds market value has gone up, and you are earning a coupon payment at CPI. The Fed engineered a perfect storm which benefits TIP bond owners.

Another thing that has been going on that isn’t being reported. We do work for lenders and have been having major problems collecting our fees from them after we do all the work. They are taking money from home buyers for the appraisal and inspection up front and putting it in their escrow accounts and using that money to bankroll other loans that they make at userous interest rates. This has been going on for a long time but now is out of control. Most of these are shadow banks that make these loans. They are crooks plane and simple and are completely unregulated. I hope they go bankrupt like they did in 2008, only this time I don’t want to see any of them bailed out. I’m going to publish a list of these SOBs

Swamp Creature,

I am sorry to hear that lenders are not keeping their books clean with those who do the appraisals. That is just plain wrong!

My job as a ticket broker was partly against the law in Minnesota until 2007. Not a lot of ‘status’ in it — which I couldn’t care less about. But I had four rules of business, and I liked to think of it as a code of honor. This was my true wealth — trust from clients.

1) Answer the phone (then texts & emails too)

2) Be on time (my clients ran companies — their time was valuable. The last thing to do is make someone wait while you are running late!)

3) Be honest (my accounting was tight as a drum)

4) Be polite

The thing is, this was so freaking easy to do. I was trained to do it by my parents growing up, and by my coaches in sports. It was instinctive to me to keep my word. But many of my competitors could not do these simple tasks reliably. It blew me away that a part time job like hustling tickets was too difficult for many others to do 24/7.

But what you are seeing is deeper than that. This is a deliberate choice being made to run a business unethically. For your sake, I hope it bites these expletives in the ass!

And one of the coolest parts about selling wheat seed in Fargo & Grand Forks region was that since I’d been on the streets of the Twin Cities so long, I was known by many a farmer and seedsman as their ticket guy long before the seed business took off. My reputation was spread by word of mouth and carried over into the wheat biz.

My only advice is to do what you’re planning to do with getting the word out to others. And continue running your business with integrity. In the long run it will pay off.

All the best to you S C.

One last thing: If you want repeat customers who’ll buy from you long term and you want season ticket holders who’ll give you tickets on consignment to sell year after year, treat them right and think of the future; make your business grow. A quick buck today ain’t worth as much as a hundred bucks down the road.

Are these lenders who’re stiffing you just in it for a quick buck today? Or do they want a hundred bucks next year?

Americans are awash in the highest amount of cash on hand in the history of the country and those amounts far exceed consumer credit that is outstanding.

The people with cash are NOT the same people with consumer credit outstanding. Two different sets of people.

Does the “cash on hand” include the digitally printed money on balance sheets of primary dealers, hedge funds, etc.”

If so, will that “cash on hand” trickle down to help people pay off their outstanding consumer credit?

Time for another of Wolf’s charts of WHO has the wealth and income in this country again? Even leave out the 1% and it’s still sad. Been playing trickle down (I mean “supply side”, excuse me) since the Reagan-bot and his “Nobel winner” Milty Friedman, and lot’s of folks still waiting.

Probably any day now?

I think gold holdings are near record low as a % of assets even though it’s at $1950 per ounce. Fed has suckered us into holding negatively yielding paper promises. Even regulated electric utilities are paying negative 5% real dividend with stock PE’s 25.

Utilities are a perfect mirror of our times. You feel rich because share price shows up as a big number on your brokerage statement, but 3.5% dividend buys less than it did a year ago. Fed has wrongly priced everything. Price used to be the foundation of economic theory.

Boston Media citing local realtors reporting significant slowdown in activity despite low inventory compered to last year and the year before, Although inventory started to rise slowly according to one report at least.

Here is my theory, we don’t have a house shortage, we have a single family houses not owned by investor shortage. There are about 15m single family rentals, largely owned by mom & pop’s. Homeownership rates in the US are near long-term averages and vacancy (which includes second/vacation homes) are only slightly below normal (11% vs. 13%). Middle income families want to buy homes but investors are blocking that path (due to the Fed). However, as we build at a rate of 1.2m single family homes (assuming they get finished, about 9% of the middle income families stuck in single family rentals can leave the rentals. Rents start going down, investors start selling, and that is how this bubble bursts (or at least one of those ways). Just my theory, I am wrong a lot.

Pretty common story is during a severe recession people lose jobs, people get divorced and end up being forced sellers of homes, especially vacation properties. Shattered dreams and shattered finances.

Don’t forget the increased number of SHATTERED PEOPLE below with those shattered dreams and finances.

According to the U.S. Census and St. Louis Fed the U.S. rental vacancy rate was 5.6% in 2021 Q4. This is lower than the long term average vacancy rate.

Rents have been rising. About 25 years ago I rented a trailer for $200 a month rent. I saved enough money to buy my own place.

Anecdotal:

Ca Central Valley town (about 30 miles east of Gilroy). Daughter and husband placed a rental for sale; “fixer-upper” in good neighborhood. Went into official listing this week Tuesday morning. Six bids within two hours. Tuesday afternoon sale was closed $60,000 over asking ($400,000 range) All cash. Crazy!

Isn’t it coincidence that they removed the crime statistics from RE search engines to make it easier for “the Investors” to overbid crackholes? Surprises are coming.

I live in a rural county of 24,000 where most people pay cash for their homes, most new homes are custom homes on the client’s dime, few homes built annually are spec homes, and the number of active homes on the MLS is “in the 50s” per a newspaper ad by one of the realtors this week.

If things don’t pop, my home will sell for the mid to high $800s this summer, and I paid $405K for it in 2015. Currently, there are 11 homes for sale between $750K and $900K, with four showing as pending.

Here, it’s a supply vs. demand thing. And good luck finding a rental here. There was a 3/2 rental in the paper yesterday for $2650/mo, and they will get it.

But home prices are still rising and there are no signs of weakness. No one will sell for lower price and lower locked mortgages.

Home prices will only go up this time with declining inventory. So the American dream of owning a home will keep vanishing.

The real question is Are Fed members going to jail for the greatest robbery from middle class Americans to enrich their wealthy masters?

Inventories are rising both in Canada and the US. RTGDFA

Lawrence Yun bot on full autopilot when it combs the web for article like this..

Anyone guessing where rates will top out?

Until something breaks, then like Vin Diesel hitting that NoS in F&F, turbo boost back to ZIRP and housing bubble continues, everything back to “normal”

Houses still flying off the shelves in my corner of Southern New England. Open houses are still packed and multiple bids over asking are common. I have family members in real estate and while they reference an increased urgency to buy as a result of higher rates, buyers en masse are not dropping out of the market… for now. As long as cash purchases remain high there will be at least some immunity to higher rates. New homes for sale are also few and far between since most land that can be developed already has been. Other areas of the country (Midwest, South, Interior West) where neighborhoods are going up by the dozen will probably be at a higher risk of future oversupply and price corrections.