But future bond buyers get the higher yields.

By Wolf Richter for WOLF STREET.

The interesting thing is that no one at the Fed is trying to talk down those spikes in Treasury yields and mortgage rates. It shows that those yields are going where the Fed wants them to go, and that the Treasury market is coming around to the Fed’s rate-hike plan, and that those yields have a long ways to go, given that CPI inflation is 8.5%, a gigantic mess that has unfolded over the past 15 months, finally, after 12 years of money-printing.

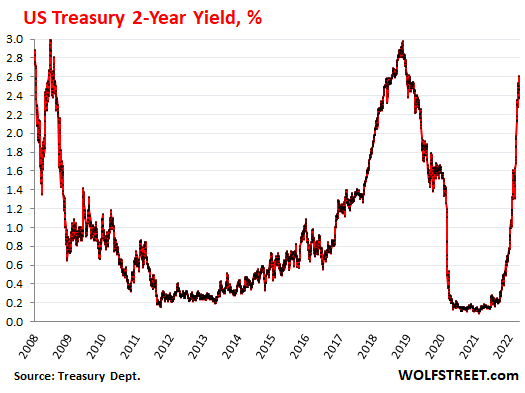

The two-year Treasury yield spiked by 15 basis points today to 2.61%, the highest since January 2019. This has been a huge move in just seven months. When the two-year yield goes over 2.83%, it will be in territory not seen since 2007, as the Treasury market begins to price in the Fed’s coming policy action to crack down on inflation:

Even the biggest doves at the Fed are now fully on board the rate-hike train, and it’s only a question of how fast and how long. Chicago Fed President Charles Evans, one of the biggest doves, is “comfortable” with 25-basis-point hikes at every meeting this year (there are seven more), and even he is “open” to 50-basis-point hikes: “we want to be humble and nimble, and get to neutral before too long – maybe 50 helps, I’m open to that,” he said.

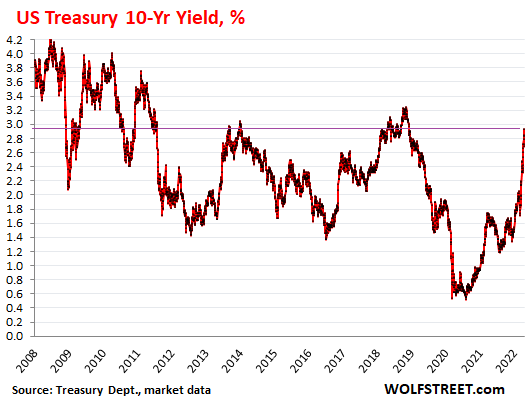

The 10-year Treasury yield rose by 8 basis points to 2.93% at the close today, the highest since December 2018. The magic number there is 3.24%, beyond which yields are back in 2011 territory:

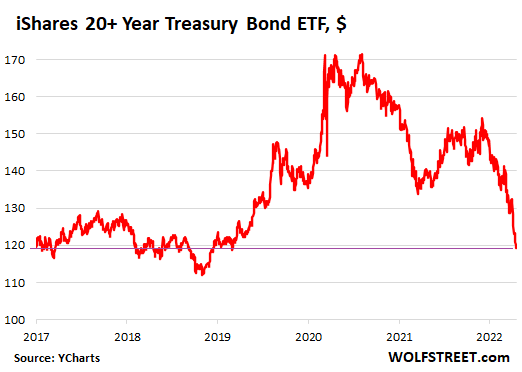

When yields rise, it means prices of those bonds fall, and prices fall the hardest of bonds with the longest remaining maturities.

And it’s a massacre for people who invested in what they thought was a very conservative and prudent instrument, namely a bond fund tracking long-term Treasury securities, when in fact it turned out to be a highly risky wager on long-term Treasury yields always going lower forevermore.

The iShares 20+ Year Treasury Bond ETF [TLT], which tracks an index of Treasury securities with at least 20 years of remaining maturities, dropped another 0.75% today, is down 19.5% year-to-date, and has plunged by 30.6% from the peak in August 2020, which was when long-term Treasury yields had hit historic lows, and which was – with hindsight – the moment the greatest bond-market bubble in US history began to implode:

But future buyers get the higher yields. Treasury yields across the spectrum are still way below the rate of inflation, but they’re a lot higher than they were, and they’re a lot higher than what banks are paying in interest, even so-called “high-yield” savings accounts, which still pay nearly nothing because banks are awash in deposits that they don’t know what to do with – thanks to the Fed’s ridiculous amount of money printing – and the last thing many banks want now is to attract even more deposits.

So folks looking for yield that blows past the interest that banks are paying, and that blows past the dividend yield of the S&P 500, they have some options now and better options coming their way with Treasury securities. As yields rise, future buyers get to enjoy them.

But note: If you buy Treasury securities, buy them outright at issuance and plan to hold them to maturity, at which point you will get paid face value no matter what happens in between, and stay away from longer-term bond funds unless you want to speculate on the direction of interest rate movements, that’s an iron rule of mine, exemplified by the TLT fiasco.

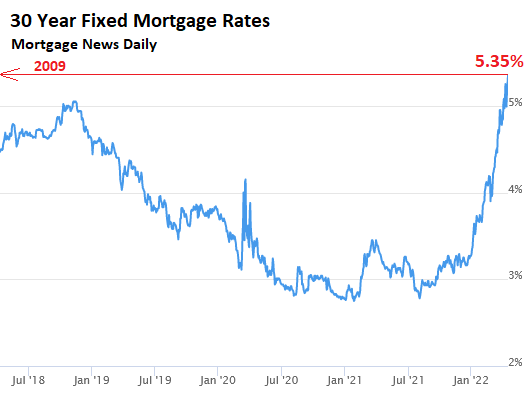

Holy moly Mortgage rates. The average 30-year fixed mortgage rate spiked to 5.35% today, the highest since 2009! This daily measure of mortgage rates by Mortgage News Daily had briefly hit 5.05% in November 2018, with inflation at or below the Fed’s target, and with markets tanking left and right, before the Fed made its infamous U-Turn, and mortgage rates dove. Now the Fed is just getting started, with inflation at 8.5%.

There is no one that can persuade me that this jump in mortgage rates isn’t going to have a serious impact on the housing market. It’s the Fed’s way of getting the housing bubble under control before it tears up the financial system again:

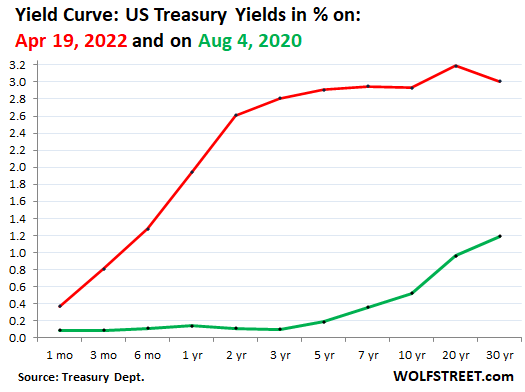

The yield curve is getting less weird. It reflects the Treasury yields across the spectrum, from the 1-month Treasury bill to the 30-year Treasury bond, and there were some weird things happening in March and early April, but these weird things have now started to reverse just a little.

Below is the yield curve today (red line), reflecting today’s yields across the Treasury spectrum; and the yield curve on August 4, 2020 (green), at the peak of the greatest bond bubble ever. The weird thing was when the three-year yield and then the two-year yield rose so much that they were higher than the 10-year yield – leaving the yield curve “inverted” in those parts. This has now un-inverted.

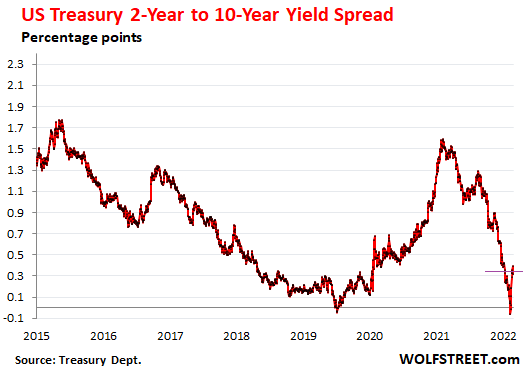

With the two-year yield shooting higher in March, and with the 10-year yield rising, but not as fast, the difference between them (the spread) narrowed and for two days in early April turned negative, with the two-year yield a tad higher than the 10-year yield. This had caused a lot of hand-wringing in the recession-watch community, because inversions of this kind have been associated with recessions.

But with the two-year yield now at 2.61% and the 10-year yield at 2.93%, the spread between them is 32 basis points:

The Fed locks down the short end of the Treasury yields via its policy rates, including its rates for overnight repos and overnight reverse repos, which box in the overnight yields in the gigantic repo market.

The longer end of the Treasury yields, from five-year maturities on up to the 30-year yield is still weighed down by the Fed’s obese balance sheet. QE was designed to push down long-term yields, and it did that. Now QE has ended, and the yields have come up some, but not nearly enough. But QT – the kick-off is sometime after the Fed’s meeting in May – will do the opposite of QE and will remove little by little that weight and will allow long-term yields to rise further, while the short-term yields will rise with the Fed’s rate hikes. And this should make for much higher long-term yields, higher mortgage rates, and a steeper yield curve as QT gets going.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Great article. yeah, I see a lot of investors foaming at the mouth already over these bond yields. Once they all pile in, it will push down rates again obviously. Rinse and repeat.

I sold a lot of my stocks and starting to buy ZTL (Canadian etf of TLT) . At this rate people think that it’s going to zero because interest rates are going to the moon.

I think ZTL is already pricing in as if it’s going to get to 3.1% rates. So far the US fed only raised 0.25%, and another.50 next month, and then another.50? How long until thinks start to break?

Shouldn’t you start buying when it’s blood in the street?

I also went out and buying Japanese yen for my next skip trip to Japan. Both charts are a straight line down.. Not normal at all..

You are a braver man than me Mike….

I’m not seeing blood on the streets. Just a few bruises. 3.5% might be the new normal in a few years. The blood letting may begin at 6%…

We have a long way to go before there is blood in the streets. How about 30 year US Treasuries at 16%? That’s what their yield was in early 1982. Later that year, you could have purchased Las Vegas Airport Revenue bonds yielding 15% Federally Tax Exempt with 15 years of call protection. The revenue source included profits from slot machines located throughout the airport.

It depends upon the time horizon and if you are willing to speculate on interest rate changes. You can’t hold to maturity on a bond fund.

As a long-term hold, this bond fund, others like it, and individual bonds are going to be huge losers. If the bond bull market from 1981 is over (as I believe), ultimately, yields are going to blow right past the 1981 high. The fundamentals are far worse even now, even ignoring that this is still a mania.

Look at the price of UST 30YR where the futures have gone from 191 on March 9 2020 to below 140 yesterday. Thats’ a huge loss when the yield was less than 1% at the time of purchase, like over 25 years of interest coupon payments.

I think you hit the nail on the head. These are not 20year buy and hold….

Nothing goes down in a straight line and no way 6% or 16% are even in the cards ATM.

These long term treasury ETFs have priced in 3% yields. As a reminder, the fed only raised .25 and rates are only at 0.5.

I will be extremely surprised if the fed manage to get to 2% before credit markets blow up. They are so far behind the curve, they’re a fat man running in the Olympics getting lapped for the tenth time.

Once the market realizes pricing 3% is out of the cards, I’ll take the capital gains when they price in back to 0.25 yields. LOL

Tony,

It already pushed down yields a few days ago. Then that group of investors bought all the bonds it wanted, and yields spiked further until the next group emerges… Rinse and repeat. This will keep going upward for quite a while, in waves. I will start nibbling shortly. And I will keep nibbling on the way up, like everyone else. The Fed will unload about $100 billion a month that will have to be absorbed too. Yields will start looking much better by the end of the year. A 2-year yield of 4% maybe? 10-year of 5%? We’ll see.

Wolf, they’ve *talked* about unloading ~$100 billion a month (eventually). This has been such a corrupt Fed since the Great Financial Crisis, that I have trouble actually believing it until the precise day it actually happens. That said, definitely look forward to it, especially if they keep it up for six+ months.

I agree. If everything plays out the way the FED is expect, we won’t even get to $95B until August. There might be two 50 point basis increases to the funds rate, putting it at a measly 1.5%.

Is anyone surprised at how slow the FED is moving on QT? Of course not. They don’t want he housing market to implode. I don’t see an implosion, but it certainly could take 12 months or more for the FED to find the top of treasury yields & mortgage rates.

I just don’t see it taking longer than that. From next August until next May is 9 months. By then, the FED will have rolled off $1T from its balance sheet. Despite their having made adjustments to the Sept. 2018 REPO freak out, I don’t have any confidence the bond market is going to be able to absorb all these treasuries & MBS without creating a significant melt-down in the markets.

Wolf,

When the economy gets to the point where the FED decides to reverse course, which part the yield curve will see the biggest gains in bond prices as yields fall?

The short end? 5 years

The last part of my post didn’t send correctly.

Short end less than 5 years or long end above 5 years?

Jay,

Last time we had this kind of inflation, and the Fed was finally able to knock it down, short-term yields reacted to the Fed’s rate cuts, but long-term bond yields remained very high for years, relative to inflation — hence the term “bond vigilantes.” I don’t think anything that has happened over the past 30 years can guide us here. We have to look at the 1970s and 1980s

I discussed this issue and a little bit of bond history here:

https://wolfstreet.com/2022/03/30/bond-massacre-inflation-prick-biggest-bond-bubble-in-history/

Isn’t your nibbling called “laddering”?

I just started grabbing. Its not laddering because I am virtually all in on the 1 yr-15 month treasury notes average 2.24%. It is a better decision than waiting till later to make a buy at a higher rate and not accrue interest income. These notes will mature quickly at a guaranteed profit.

NY Geezer, I’m doing the same thing. Starting to ladder the 1 – 15 month maturities. I’m buying a treasury bill/bond each start of the month and they will mature over next year.

Edit above 1 – 15 is really 12 month to 15 month maturity treasuries. Buying existing issues.

I’m not doing classic laddering, which goes across the maturity spectrum. I just want to earn interest on cash I keep for the short and median term. I’ll be looking at 1-month to 2-year securities, while I wait for this to play out. Some of my cash has to be very liquid in case there is suddenly a good place to put it to work. I won’t be buying anything longer than two-year maturities for a while, until yields are much much higher at the long end.

I don’t understand why “…the last thing many banks want to do is attract more deposits”. Seems like they always want that, yes?

As usual it’s probably a point of view or financial reason I don’t get or forgot, sorry.

Thanks for any help.

NBay,

Money printing by the Fed has generated a huge mountain of liquidity (cash) that no one knows what to do with. The Fed has removed temporarily via overnight reverse repos about $1.7 trillion of this cash that money market funds didn’t know what to do with, and the Fed is paying them interest for it. There are several trillion dollars of excess cash in the banking system, and the Fed is paying banks interest on those reserves that banks put on deposit at the Fed.

When you put cash in the bank, the bank gets the cash (an asset) that it can do something with, but it also has to set up a liability (the amount it owes you), called “deposit.” These liabilities increase leverage for the banks, and they have trouble dealing with it and staying within their leverage ratios.

Deposit-rich banks will be the last to raise their interest rates on deposits. Banks with not enough deposits will raise their interest rates first to attract deposits. This will be smaller banks and credit unions at first. We will see that happen pretty soon.

Thanks…I think…..The Double Entry Bookkeeping “learning website” on my cluttered desktop remains unread….for a couple years now….sorry.

An increase of 3% to 5.35% in mortgage rates on a $500k house with 5% down equates to an additional $700 in the monthly payment and an extra $240,000 over the life of the loan. And yet I see the mouthbreathers drinking the Kool-Aid saying house prices are only going to continue going up. We need to seriously start teaching math in schools again, because MAFF ain’t workin’ out.

*increase from 3% to 5.35%

I’m retired but built part of my portfolio years ago buying strip bonds and have held them to maturity. I gave up buying bonds a few years ago as they just gave such meager returns instead focusing on better quality dividend stocks and ETFs. Recently GIC rates have finally showed signs of life, 2 yr paying 3.6% and fives paying 3.8%. If this continues I may sell more dividend stocks and just add to GIC’s.

Meanwhile there are many articles showing up in cnbc and wsj claiming that housing markets remain strong based on low supply, high demand and due to house being perceived as inflation hedge.

Many of these articles are encouraging buyers to dive in irrespective of higher mortgages! Are these really snake oil salesmen trying to get out at the top? Shouldn’t we be seeing first price cuts now?

I was a real estate broker for 35 years. House prices go up a lot faster than they come down. Sellers are always looking at what someone got last year or what they think they should get and are very reluctant to take less. I don’t know how many times I heard a sellers say, I have this much into it and I need this much out..

Weakness will need to settle in and become a trend to change their attitude. It will take foreclosures and repossessions before most sellers will give up hoping for what they could have gotten. This is a process and takes years.

This everything bubble will have to pop and fear and loathing will have to enter the markets before there will be any real significant reduction overall. A real reduction in house prices will not be an event.

It has started but it has a very long way to go.

As for the snake oil sales; that is how they make their living. The system needs new money and it is created by loans so the entire Ponzi is based on higher loan values and expansion. None of those benefiting really care what you want or can actually afford.

Waiting for the Sword of Damocles to fall

What could be the reaction of China and its mountain of US bonds that is still devaluing, sell everything? And after ?

They are selling already. And probably not them only. That is why you see higher yields. The treasury yields are now higher than the yields on Chinese bonds in yuan.

I fancy I speak for the wolfstreet masses when I say we breahtlessly await Chairman Wolf’s proclamations on WTF is going on with China.

I don’t think China would sell all its US bonds. Not unless they really needed the money… which they might. Imagine they did sell all the bonds driving the price down to, let’s say, a dime on the dollar. Then the US would be able to retire $30 trillion in debt for $3 trillion. China isn’t going to willingly do the USA a favor like that.

The People’;s Republic of China only owns about $1 trillion in US Treasuries out of the around $30 trillion outstanding and it wouldn’t make a hoot of a bit of difference to yields (interest rates) if they sold them all. Japan also owns about the same amount. The US has to sell around $15 trillion a year in US Treasuries just to keep the existing debt financed and accommodate the new US deficits and that is the core issue as yields move up towards normal and then much higher yields (interest rates) in the US Treasuries markets.

Trade between the US and China is in dollars not yuan. They have to have dollars to facilitate the trade. They can not sell all their dollar holdings.

The right hand of the mortgage rate graph looks like one of the waves from Miller’s planet in Interstellar.

Is the 5.35% mortgage rate an average and are many Americans actually paying more? If you have a fantastic credit rating and boat loads of cash, for a deposit, then you should get the best rates but what about Mr Joe Average with a normal credit rating and with a smaller deposit. Does Joe have to pay more?

I ran the calculations many times putting in every value I could: different credit scores, different down payments, loan amounts etc… the quotes I got for rates weren’t as affected by credit scores as I would have thought. It was actually mostly determined by overall loan amount. For instance, a $500k loan with 5.1% vs $250k loan with the same credit score at 5.5% is what I got quoted.

Different credit score ranges only changed my quoted rates by a tenth of a percent or less, until I went all the way down into the sub 680 realm. For some reason or another it seems like the mortgage market finds smaller loans actually more risky, or so I would assume by their pricing. Maybe someone can explain that to me as it seems backward and counter intuitive.

Actually that sounds a great deal worse than I thought as it appears to be a way to smash people into more and more debt…. The other problem, would be the lack of people at the starter home base if they are paying a higher rate. Maybe you don’t have housing chains in the USA ???

The other question is how many buyers are in the the sub 680 realm….?

According to data from 2020, approximately 34% of the US population has a credit score of 670 or below. Just FYI.

Forbearance of student loan debt had a positive impact on credit scores because the loans were no longer “technically” late / delinquent. Once the forbearance ends, watch for the number of <680 scores multiply.

<680 is what we considered to be a "credit criminal" when we would offer subsidized financing. We used the PC term of "standard"….. we had another level lower for the real rats. They paid through the nose and we were very selective about those we approved.

As far as the rate differential between larger and smaller loans, that might have to do with the costs to administer the loan. The fixed costs are the same whether it be $1M or $100K.

Anthony- Credit ratings have been buoyed in some cases through forbearance edicts preventing eviction proceedings in the US, presumably credit utilization had better numbers as credit card balances were paid down with FedGeld. One of my cards with TransUnion credit monitoring, which I rarely use, dropped their interpretation of my creditworthiness by eleven points because I charged twelve hundred bucks on another cashback card, everything’s paid at the end of the month as usual. Two months earlier, it went up over forty points for no reason whatsoever. It’s not useful information. Not owing anybody a dime makes counterparties nervous. Now apparently medical bills in delinquent/default status won’t be used in computing scores, and some savvy uninsured patients will take advantage of it. As credit scores reflect less and less the borrower’s ability to repay debt, favoring regular spending patterns and continuity of indebtedness instead, they won’t be used by potential creditors in the same way as before, or as much. As mentioned in comments above, their significance in determining the mortgage rate and payment is waning. To me, this is saying that society doesn’t recognize the virtue in thrift and hard work anymore. Add the disproportionate returns on rentier activity, and it’s easy to conclude that the working person who saves is a fool. A draft animal, like Boxer(“I will work harder”) who gets knackered by the pigs. Boxer should have stomped some pigskin into the barnyard dust, cut a deal with the sheep, and started a Horse Nation. If Orwell had lived in an armed country his animals at the Farm might have wiped out the porkers in a bloody coup. Our current treatment at the hands of the “haves” is going to determine how comfortable the rich and their brats will be for the rest of their lives. We’re all stuck on the same ball of dirt, and we know where they live, since we built it for them.

“Down and out in Paris and London” is a better book than”Animal Farm, imho.

Look at what happened to “prime credit” risks during the GFC. Plenty of them reportedly defaulted and the reason they did is because they weren’t really prime but close to broke. They lost their job and had limited financial resources. Or they walked away.

What about a VA loan? No PMI.

Anthony,

Yesterday I heard a guy on Youtube talking about that exact same thing. He says the worse the credit rating of a buyer the higher interest rate they end up paying.

What about buying some I Bonds?

They’re great. But the limit is $10k per year per entity. So it’s hard to move a lot of money into them all of a sudden. This is something you do every year, come hell or high water. Some tax benefits too.

Note that they’re floating rate bonds, with the yield linked to CPI. If CPI goes to 0%, your bonds that now pay 7.5% will then pay 0%. Just make sure you understand the nature of that variable yield. It’s NOT 7.5% forever.

Wolf, sorry for my financial ignorance on this particular topic but how do we specifically go and buy I-bonds? I’m by no means a newbie on things debt securities related but we’re not exactly sophisticates in our household either, and somehow the neat (esp for these ridiculously inflationary times) vehicle of I-bonds eluded us, least until we started looking into them last year. But our financial advisor was evasive (or just in a big rush) when we asked, and I’ve found the Investopedia articles for some reason to just confuse us more without getting to particulars. Is there a user-friendly ELI-5 somewhere on their specifics, and how to actually buy them on a garden-variety brokerage account?

visit treasury direct dot com. learn all about treasury buying, i bond buying etc. Easy to do on your own.

Thanks, we’ve maybe been over-complicated it..

Treasury Direct is the only place you can buy them. You have to open an account there and then link a bank account to it and then make the purchase.

One other way is if you have a tax refund of $5,000 or more due to you, you can elect to have $5,000 (max) sent to you in paper I bonds. Once you have the paper I Bonds, you can mail them to the Treasury and have them converted to electronic in your existing account.

“Note that they’re floating rate bonds, with the yield linked to CPI. If CPI goes to 0%, your bonds that now pay 7.5% will then pay 0%. Just make sure you understand the nature of that variable yield. It’s NOT 7.5% forever.”

The hedonic adjusted bond. Hard pass.

Maybe we need some more clarification on the TIPS?

Way I read it on the GUVMINT site where ya buy them, the rate of return is a combination of a base rate of the FFR when you purchase AND the CPI adjustment every six months, with a bottom of zero if the CPI goes negative more than the base rate.

So, even if or when we do get a depression situation and the CPI goes to double digit down, you would still be able to get your original money back, perhaps when ”prices” were down by that CPI amount.

Anyone want to expound on this for folks thinking to buy these things when the FFR gets to 10%, eh?

A tax-time purchase option.

The option to use your tax refund to buy up to $5,000 in paper I Bonds raises your limit from $10,000 to $15.000 in that year–$10,000 in electronic form and $5,000 in paperform.

“There is no one that can persuade me that this jump in mortgage rates isn’t going to have a serious impact on the housing market.”

I wont be me…

But, the differential between the inflation rate and the mortgage rate is a consideration. It would be an interesting chart.

Inflation now running 3% above the 30yr mortgage…yet in 2018, as noted in article, the inflation rate was 3% BELOW the mortgage rate.

At this current point in time, nearly everyone who sold a home to date could have sold it higher, and every buyer seems to be at least even.

This likely to change soon. But getting out of cash seems still to be the chosen sport, especially for corporate real estate investing. The “take my money and buy something” game. IMO

Mortgage rates were high through the 1970’s and 1980’s. They were 18% in 1981. The nominal price of a home in America was higher in 1980 than in 1970 and higher in 1990 than in 1980.

Not if you paid all cash.

Unless “money” is based on gold, it is all a waste of time.

Does a “foot” change? A Kilometer change day to day? A Kilo change day to day?

Why does the value of a “dollar” change day to day?

Money should be fixed, as is an inch, a centimeter, a kilo, a mile, etc.

Don’t tell me it can’t be done. We do it to “ton”, “yard”, “square foot”…….

Find a way, maybe not perfect, that approaches the “limit” of standardization of a “dollar”. So far, the only thing that comes close is the “barbaric relic” called: Gold

No one wants the barbaric relic any more. It’s all about crypto garbage.

True, but totally irrelevant. The period of time you mention didn’t begin with albnormally high price levels, making it possible for RE to increase with inflation. Today we have abnormally high levels. In legitimate forms of analysis this is known as initial conditions. There is no comparison between the current situation and the previous period of inflation, and yes i was alive back then i remember it well. Totally different situation.

You used to be able to assume loans of the former owners at much lower rates too. Times have changed.

BOJ announces today they are digging in their heels to hold rates where they want them…creating their own reality, for a while longer…

the hubris of central bankers is boundless.

Util the Yen starts crashing. It’s already at a 20 YR low versus the USD.

Looks like I done got caught up in this spike in interest rates. Even my conservative short term muni fund has taken a bath.

Got my 3 month statement yesterday.

Strike 1. Yield still below 1%

Strike 2. Asset value dropped 4%

Strike 3. Inflation at 13.8% and climbing

Thats 3 strikes. In baseball as in investing 3 strikes and you’re out.

Looks like I done struck out on 3 pitches.

I go out on a limb with haiku:

The Fed’s endless ZIRP

Yielded gains that weren’t real;

But the winds shifted.

Let the bank dis-intermediation begin!

Question for J Powell…

If it was good policy to “average back” the inflation..ie, if inflation was under the Fed’s self authored 2% for a few years it is okay to let it run over the target for a while…..then the question must be asked..

“Is it then good policy to drive inflation down below the target levels if it has run well over the target for years? (Like now ) Does the “averaging game” work in that direction too?”

The “averaging” scheme and the “let’r run hot” idea will hang around Powell’s neck like an inverse ribbon of shame at the county fair, forevermore. It will be almost as famous as the Volcker rate hike. Only if a vaguely softened landing happens, will his rep be partly rehab’d.

He was honest with you.

He clearly stated that the 2% Inflation was temporary.

He was completely and honorably honest.

YOU, though, were not honest. YOU wanted something different and refused to elucidate. YOU defied reality. He didn’t. 2% was temporary.

*Weren’t should have been “were not” to be standard Haiku format…

Luckily the haiku police were busting another line, otherwise it could have been curtains for you.

Actually, there are more rules on making Haiku than just 17 syllables.

Read up on it.

They don’t call them “Haiku Masters” for nothing.

“The problem is one I have outlined several times in recent months.

The inflationary pressures are not coming from excessive growth in nominal spending. Yes, nominal spending is somewhat out of whack with available supply, particularly in the goods sector, but that is because supply is out of whack. Purging demand through interest rate rises (which will take very significant increases in rates and many insolvencies) doesn’t fix the out of whack supply.

It doesn’t get Russia to behave.

It doesn’t get OPEC to behave.

It just creates more gloom via rising unemployment – adding further woe.”

Austrian economist Bill Mitchell, co-founder of MMT.

Raising rates LOWERS DEMAND and it causes assets prices to go down, which further LOWERS DEMAND, and lower demand makes it harder for companies to raise prices. This includes energy commodities. And overall inflation recedes. Hiking rates works in bringing down inflation if applied sufficiently, supported by big QT.

Investments in new production may go down too. Now, if that will be the trend with commodities and energy the future supply may shrink. Depending on what the customers can afford, a new price level will be set. Still this could be at a lower supply as the price will be to low for investments in new production.

The end result may be like a famine where there is reasonable supply of food, but no purchasing power to buy the food.

Your a week and a couple percentage rates off Wolf! The 30 year mortgage is at almost 7 percent as of this morning! Never seen anything in the real estate market move this quickly.

Subprime?

They’re probably referring to this article from Money dot com from a few days ago:

“After briefly falling below 6% last Friday, the average rate for a 30-year fixed-rate mortgage jumped up to 6.875%, increasing by more than one percentage point. The rate is nearly two percentage points higher than the average rate just one month ago.

Money’s daily mortgage rates reflect what a borrower with a 20% down payment and a 700 credit score — roughly the national average score — might pay if he or she applied for a home loan right now. Each day’s rates are based on the average rate 8,000 lenders offered to applicants the previous business day. Freddie Mac’s weekly rates will generally be lower since they measure rates offered to borrowers with higher credit scores.”

What’s hysterical is I’m now seeing comments from sellers panicking about these rates since their house “isn’t quite ready” to sell, but they hope to get it on the market soon. Seller FOMO. LOVE IT.

That “article” is rewritten by a script every day with fresh numbers pulled from a source they don’t name. That source appears to be the same glitching, incorrect source that is causing some people to see unrealistically high rates when they use Google to look up mortgage rates.

Money.com has been reporting 6.4% to 7% rates lately for 30-year fixed, 20% down, 700+ credit score. I have no idea how they compile it and whether it is accurate. That could be on the edge of subprime.

No I just googled this and it says average 30 year is at 6.75%. This was the google provided rate so aggravated from various sources I’m sure. FHA at 5.67%, these are for 20% down 700-719 credit score.

Have rates ever moved this quickly before? This is interesting.

I’d like to get one of our mortgage brokers here to comment. They’re dealing with this all day.

The average rates cited by Mortgage Daily News and by The MBA are for top-tier borrowers with qualified mortgages.

Google calculators have been showing 6%-7% for a month now. Maybe anticipatory, assuming someone using their calculator is gonna get that rate by the time they complete an actual mortgage app? Or they’re just helping setting the goal post.

FHA is 3.5% down typically, and its appeal is mainlyfor low credit scores (down to 580 if memory serves me), or people who have a more recent bankruptcy (3 years, vs. 4 for some conventionals). Low down payments as well. The PMI is brutal though and most of our affordble, aging housing can’t meet FHA standards.

Wolf – I have two questions:

1) What will be the impact on the longer end of the yield curve when the Fed’s lower bond purchases start to hit bond auctions/offerings and the billions in inventory they have squirreled away start to mature?

2) Why are TIPS going down when CPI is a a generational high?

Traders’ nickname for TIPS: Terrible Illiquid Pieces of Sh!t

No, those are liquid. “Illiquid” is real estate.

TIPS are NOT for wealthy people (unless they trade them and are better than the pros) because the CPI they make is added to your income each year. Just like I-Bonds, they are for the “have some, but not so much” bunch. I have friends who like them, although when rates are raised they will probably wish they had the money to buy regular Bonds and Notes.

They are like me, hate corporations and still hold out hope for a democratic government.

Lego C.-

1. Premium prices leading to gap between current prices and par, on TIPS

2. Short Treasuries now offer a more completive return/risk/liquidity package vs. TIPS than they did a few months back.

See TIPS market activity in 1999 to 2001.

IMHO.

I’ve been leery of Tips to protect from inflation because they still go down with increases in real interest rates.

Just learned that lesson myself. Experience is a brutal teacher.

Time to party like it’s 1994. Lots of blow-ups happened in short order, amongst folks who in some way, as Wolf put it, discovered that in some way they “were in what they thought was a very conservative and prudent instrument, … when in fact it turned out to be a highly risky wager on long-term Treasury yields always going lower forevermore.” There are many of these, yet unrevealed.

Then again, I bought my home in ’94, and by now, I pay a ridiculously low monthly sum on a very appreciated asset (though this valuation will adjust too, but there is a lot of equity here).

Then too, this time, global politics/finance has some new wild cards. That party might turn out to look more like 1920s-1940s.

Your asset did not appreciate.

The paper notes, in which your asset is defined, has lost value, thus appearing to fool you into thinking your asset has appreciated.

Example: Sell you asset. Collect the “notes” and now go buy another home. Surprise. It will take all, if not more, of your notes.

The paper notes have lost value. Your asset went mostly nowhere. In reality, your home should cost LESS than when you bought it.

With the increase in productivity, home construction, economy of scale, mass production, etc., you asset should cost, in gold dollars, LESS than you paid for it.

This is how a FORD car went from $850 to $250 in Gold Dollars. Mass production, assembly line innovation, volume purchases of all parts, lower shipping costs due to Rail Road efficiency, cheaper Iron due to economy of scale of Iron Ore Mines and shipping expenses, etc.,

The $20 bill is the new 20-cent piece.

A $20 Gold coin is worth about $2,000 today.

What is you $20, 1913, (Will Pay On Demand Twenty Dollars) note worth today)?

$20.

Who is the idiot today.

But if you put the $20 in the stock market or real estate even in bonds or the bank, how much in income and capital gains would have made by today? That is the question you have to ask.

The Alton Route- per the Mega Red Book, 2017 fourth edition, the least valuable twenty cent piece is the 1875-s which goes for $100 in Good-4 condition, with a mintage of 1.155 million. At twenty bucks I’ll buy every one I find.

It seems to me that Fed has messed up big time by trying to achieve the wealth effect. By supporting assets for 13 years they have most US middle class households too leveraged up in housing and too exposed to equity markets.

While they have blown up assets the demographics and debt burden has gotten worse so the ability of real rates to be positive for more than a few quarters is not possible.

Last time Powell couldn’t get to 3% before breaking credit market. My bet is he will not make it to 1.75%.

Also been hearing the theory that inverted yield curve tells you there is going to be a recession in a few quarters but the warning signal that it’s close is when it goes from inverted back to normal. Let’s see if we get a recession in by summer. Of course recessions aren’t officially called til many months later after the data comes in.

A recession is impossible with the spread between inflation and the Fed funds rate this wide, In fact it tells you hyperinflation is in the cards not a recession.

Economic contraction can and does happen with hyperinflation. It’s happened many times in other countries.

The US isn’t close to hyperinflation, unless your inflation cut-off is very low.

The Real Tony,

Maybe, but trends get broken as in things feel best, look the hottest right before the top is in. A lot of examples such as Japan, Tech bubble and last housing bubble. I don’t think it is going to reciprocal action on tightening. Took many trillions to build bubble, but will not take as much to pop it.

High inflation will kill an economy just as fast as a deflationary spiral. High inflation will cause demand destruction just as fast as high interest rates. That is why the saying that the best solution to high prices are high prices is absolutely true. High inflation can only last a short while before it kills the goose laying the golden eggs. In Wiemar Germany it lasted less than 2 years and the currency totally collapsed.

High prices kill themselfs is true as long as there are no wage increases.

The Weimar situation was a completely different story and is in no way comparable to what we see now.

It is a good example that the gold standard causes a problem and not solves it. As quickly as the Reichsbank put other valuable assets into their balance sheet instead of AU the hyperinflation immediately was gone.

Neither are depressions until after GDP plummets by more than 10% in two consecutive quarters.

In my locale, Olympic peninsula, the housing market is still being pushed up by cash buyers. I recently saw a home sell for $850K with asking of $550K, sold for $216K in 2016. We actually looked at it in 2016 before buying our current home and decided it wasn’t worth the price given the style of construction (A-frame loft) and apparent code violations. While this is just one, albeit extreme, example, I can’t imagine that the rise in rates will have direct impact on the prices. Home prices are still much lower on average than Seattle, Portland, and CA where folks are cashing out and buying here. I assume that the cash pipeline will continue until the seller’s net in those places reflect the higher rates – which may take never. The inventory around here is so low that it just keeps getting crazier. “Affordable housing” for local working folks and first-time buyers is nonexistent @ $500K++ for a 2bd/1ba (without the bump from Seattle-area wages). There is no way we would’ve bought our home at these prices…insane. Lucked into buying before the market exploded.

Your observations are precisely why the market will collapse. Your logic is the very essence of the bubble mentality. It is truly amazing that so many people fall into this trap.

In my county, there is affordable housing all over the place. One can buy nice homes, with a yard, etc, close to schools and churches and shopping from $175,000 to $225,000. 3 bed-2 bath affordable homes. Families every where. Just drive around. Kids in the yards, on bikes, etc.

Marcus Aurelius: Are you kidding? Where do you live?

South Florida.

Homes all over the place that are affordable. The are great starter homes. Most built in 1960-70, but are close to down town, walking distance of schools, shopping, parks, and churches.

Most of them never come on the market and are occupied due to the demand for them. BUT, now and then one can see the listing. Seems that “connections” rule and families tell each other that such a home is on the market.

But they are there.

Yes, seriously, please give us a city name.

Oh, the “cash buyers” narrative again. Gag.

I just borrowed a million dollars. I’m a millionaire!

As interest rates rise, this will be very good for the earnings of banks in the US and US Treasuries will rise well about where they were in 2007. The markets will just have to start dealing with mathematical reality and adjust accordingly in a rather rapid manner.

Economists are proven idiots. If you destroy velocity, you destroy R-gDp. The 1966 Interest Rate Adjustment Act is the solution to a soft landing, an ample reserves regime notwithstanding. It was Volcker that said interest should be paid on IBDDs, “on rounds of equity”.

People just don’t get it. Powell eliminated legal reserves. The banksters are in charge, not the people. The only tool, credit control device, at the disposal of the monetary authority in a free capitalistic system through which the volume of money can be properly controlled is legal reserves.

In 1966, legal reserves were reduced tightening the money stock, while savings were driven out of the banks, activating savings.

Remarkable … the cable financial shows all talking about how yields have reached positive real levels………huh?

They apparently are using the Fed’s target rate as the benchmark…..with actual real inflation over 8%…..

and BofA calling for the ten year to go back to 2.25%?

The team effort here is remarkable.

Not to mention startlingly stupid and beyond utterly ignorantly laughable and mind boggling as it shows they can’t even add and know nothing about the concept of interest rates.

Interest is the price of credit. The price of money is the reciprocal of the price level. Neither the MMTers nor Powell understands this. The money stock can never be properly managed by any attempt to control the cost of credit.

The effect of the FED’s operations on interest rates (now largely via the remuneration rate), is indirect, varies widely over time, and in magnitude. What the net expansion of money will be, as a consequence of a given injection of additional reserves, nobody knows until long after the fact.

The consequence is a delayed, remote, and approximate control over the lending and money-creating capacity of the payment’s system. The consequence is FOMC schizophrenia: Do I stop because inflation is increasing? Or do I go because R-gDp is falling?.

Monetary policy should delimit all reserves to balances in their District Reserve bank (IBDDs, like the ECB), and have uniform reserve ratios, for all deposits, in all banks, irrespective of size (something Nobel Laureate Dr. Milton Friedman advocated, December 16, 1959).

SBHall-

“The consequence is a delayed, remote, and approximate control over the lending and money-creating capacity of the payment’s system. The consequence is FOMC schizophrenia: Do I stop because inflation is increasing? Or do I go because R-gDp is falling?”

Great statement! Is this the “loose joint” that Hayek had referred to?

I read somewhere that performing monetary triage on either problem — inflation, or GDP (i.e., employment) — is akin to doing a self-appendectomy using a mirror and in the dark. You feel your way along, it takes far longer than you thought, and you’re bound to get a result you don’t like.

I early cashed out a bank CD at 0.5% (higher than anything at the time) and put it into a secondary market 18 month t bill at 2.5% yesterday. Even the 3 month interest penalty on the CD made this a no brainer.

I have two more of the cds maturing over 4 months, figure those worth waiting for further t bill increases, so will wait for their regular maturity before moving to treasuries.

And been maxing out ibonds last two years.

Moved funds out of bond mutual funds years ago when I got hammered on sudden interest rate increases, so now buy bonds directly and hold to maturity – except this case now that made the CD cancellation very worthwhile.

No matter what history says about inverted yield curves and recessions the spread between the Fed funds rate and the inflation rate has never been this wide so a recession is virtually impossible. I still have a 28 year corporate bond bought in 2011 knowing the day I sell it the war in the Ukraine will end and rates will plummet.

Paul Volcker didn’t stop inflation by raising interest rates, he stopped inflation, the “time bomb”, the release of savings in the 1st qtr. of 1981, by imposing reserve requirements on NOW accounts in the 2nd qtr. But Powell eliminated reserve requirements.

We may have already passed the point where the problem of servicing the national debt can be solved without violating the principles of a free economy. That is to say for example, through a non-debilitating level of taxation rather than a confiscatory capital levee. Our economy will be forced into an increasingly totalitarian mold, and the freedoms which we are presumably arming to defend will be lost.

The First Law of Fiat-Dynamics: The Fed will overreact with raising rates to the same degree and duration that it lowered them.

No, that would be an under-reaction. The Fed needs to raise rates far more and for far longer to get this inflation under control. Raising short-term rates back to 2.5% won’t do anything, as CPI inflation is 8.5%.

True. But then the Fed may blink – if things go wrong in the asset market.

This is the “moral hazard” that the FED has created. Everybody now thinks “the FED’s got my back” after their pivot back in 2018, followed by their impossibly reckless money-printing.

Wolf-

A commenter above mentioned adjusting (re-instituting?) reserve ratios as a policy tool to slow down lending and inflation.

Any thoughts on that, or other “tools” beyond rate manipulations?

Thanks.

Adjusting reserve ratios would be useless today in the US because banks are loaded up with “reserves” (cash that banks have deposited at the Fed) and don’t even know what to do with them. They have no idea who to lend this much cash to. There isn’t nearly enough demand for loans, and there is way too much cash in the banking system right now. This is the result of money printing. The Fed discusses this issue from time to time (its “ample-reserves regime,” is it calls it).

QT will bring down those reserves. And when reserves are much diminished, then imposing minimum reserve ratios might limit lending. But not before then.

So the first step would be massive QT to bring down reserves, and the Fed will do some QT though not massive, and it said it will stick to its “ample-reserves regime.”

So as long as there are these ample reserves, imposing minimum reserve requirements isn’t going to change anything. But QT, if large enough, will change a lot.

“As announced on March 15, 2020, the Board reduced reserve requirement ratios to zero percent effective March 26, 2020.”

That’s all you need to know. Banks have been absolved of all responsibility. At this point, deposits are pure liabilities for the banks. The only reason banks continue to allow deposits is because the Fed can arbitrarily reinstate reserve requirements.

JeffD,

The minimum “reserve ratio” is irrelevant when banks are drowning in reserves, which they are today.

The critical huge factor is the minimum “CAPITAL ratio,” and they have not been lowered. People confuse those two easily.

Thank you both.

I will:

1. Read that 3/15/20 announcement and try to gleen Fed’s motive for reducing reserves to zero, when there were apparently excess reserves in the system already.

2. I will retain my question till the Fed follows through on its QT threat and when reserves have been drained. Seems to me like a QT panicked market might be a touchy time for the Fed to reinstate reserve requirements, though…

Interest on the federal debt of $28 trillion in 2021 was $413 billion. That works out to be 1.475%. Now imagine that rate was doubled to 2.95%. That would mean an extra loss of $413 billion in spending for Congress. I note the following as of this posting:

30 year yield 2.94%

10 year yield 2.87%

5 year yield 2.87%

Seems rates have already doubled! How long before Congress starts screaming bloody murder?

RedRaider,

That’s not how it works. Those 30-year bonds and those 10-year notes and those 5-year notes won’t be replaced with higher-interest debt until they mature, which is years from now. Until then, their coupon interest remains the same, and doesn’t change with rising rates. And the interest expense for the government won’t change until those bonds mature and are replaced by higher-interest bonds.

For example, the 30-year bonds that the government issued in February and had a coupon of about 2.25% won’t mature until 2052, and that amount borrowed with that bond issue will cost the government 2.25% a year for the next 30 years, even if the 30-year yield goes to 10% two years from now.

The higher interest rates will make short-term borrowing this year more expensive as those bills mature; and it will make long-germ borrowing more expensive only gradually over then next many years as the existing long-term debts mature and have to be replaced with more expensive debts, and as new debt is added to the pile.

So the increase in interest expense based on the rate hikes will be relatively small at first. However, the debt keeps growing by over $1 trillion a year in new debt, and that new debt will add more expense to the budget.

“That’s not how it works. Those 30-year bonds and those 10-year notes and those 5-year notes won’t be replaced with higher-interest debt until they mature, which is years from now.”

Wolf, George Gammon mentioned on his channel that most of the treasury debt is in short-term T-Bills. If so the outcome of what RedRaider said will happen (not in the way that he predicted as you corrected him).

John Apostolatos,

“George Gammon mentioned on his channel that most of the treasury debt is in short-term T-Bills.”

I love you, but quit citing George Gammon here. He doesn’t know what he is talking about.

Of the $30.4 trillion in Treasury securities, only $3.9 trillion (12.8%) are T-bills (1 month to 1 year).

This is published info that is updated monthly by the Treasury Dept. I have no idea why this idiot Gammon doesn’t just look it up. This guy is a clueless moron. He is just producing clickbait lies.

Sorry, could not edit this comment. Do you know how much of the treasury debt is in short-term T-Bills vs. long-term? Based on Gammon it is significant enough to cause huge problems for the government as rates rise.

That’ll teach me to not post before my morning coffee!

Imagine if Manchin had not stopped the spending that was going to happen. He took incredible heat for that. Where would we be on inflation then?

“There is no one that can persuade me that this jump in mortgage rates isn’t going to have a serious impact on the housing market. It’s the Fed’s way of getting the housing bubble under control before it tears up the financial system again.”

I scratch my head when I hear realtors and home owners say “but but there is a housing shortage, so prices will rise more slowly.”

We are clearly in the denial stage.

“but but there is a housing shortage, so prices will rise more slowly.”

Right. The housing stock is rising faster than population growth, so where did all those houses go?

Really, there is a “for sale” house shortage. There are plenty of houses, but not many for sale…….YET!

When the bell rings and there is a stampede to SELL EVERYTHING, there will not be a “housing shortage”.

Take a look at a 200 year historical interest rate chart. Rates bottomed in 1945 and peaked in 1981 in a parabolic 36 year up move. Rates then descended into the the 2020 bottom in a parabolic 39 year down move. We are now two years into a new 35 to 40 year parabolic up move in interest rates. Bet accordingly.

I hope you’re right but the worldwide birthrate is falling. Anyone with money is retired or going to retire very soon. Unfortunately both are negatives for rising interest rates longer term.

Everyone in the know knows the BLS changed the CPI calculation from 1983 to 1998 that now significantly underestimates real inflation as it relates to house prices, since the BLS focuses solely on rent. On MishTalk, he had a comment from a BLS CPI expert that says if the 1983 CPI were used today that current CPI would be 16%, so the FED has a LONG WAY to go to get inflation under control. Considering how slow they’re moving, and they’re still moving very slowly, there’s no telling how high yields & mortgage rates could go before the house of cards falls down.

I really wish we were able to lock in our mortgage interest rates for 30 year like in the USA. Here in Canada the max I believe is 10 years. Most people do 5 year variable rates.

I would feel a lot more comfortable with my mortgage then! Maybe one day the politicians will make that happen up here but not until rates are 10+%!

IMO, the US 30YR fixed rate mortgage will be a casualty of the new bond bear market.

There is a reason long-term mortgages do not exist hardly anywhere else. Outside of pension funds and insurance companies, there is no private buyer at any scale, except to speculate on interest rates. They won’t do it because long-term lending in a perpetually depreciating currency is a guaranteed economically losing proposition.

Governments have a political motivation to subsidize it, but with an exploding debt and future soaring interest rates, even the US is going to have to choose what it will and won’t subsidize. The choice will have to be made when global reserve currency status has to be defended.

The days of subsiding anything and everything are numbered.

So the US government is directly subsidizing these 30 year mortgages? How?

Through mortgage guarantees (such as FNMA and GNMA) and more recently, QE.

Current US mortgage rates do not remotely reflect the actual risk in mortgage lending.

First, the collateral value is grossly inflated which alone is enough to make the traditional conventional 80/20 a low quality asset.

Second, rates do not compensate for perpetual currency debasement, even with prior “low” inflation which wasn’t actually low compounded over time.

Third, the borrower’s job stability and therefore, ability to service the mortgage, is substantially contingent upon fake economic “growth”. That’s why supposed “prime” borrowers aren’t prime, as evidenced by the GFC.

Modern US mortgages are not actually low risk but garbage quality loans.

If US mortgage lending wasn’t distorted by government policy and reflected the actual risk of a free market, the proportion of prospective buyers who could afford anything close to current prices would be a low to minimal fraction of what it actually is now.

Forgot to mention, also with FDIC insurance for jumbo non-conforming loans.

“It’s the Fed’s way of getting the housing bubble under control before it tears up the financial system again”

I mean, good luck with that. The housing bubble is so grotesquely out of control and worse this time around that 2008 looks like a bargain by comparison.

Been trying to figure out the FRN auction. The consensus seems to be if the Fed hikes big they stop the economy, and there are no more rate hikes forthcoming. If they take a baby step now they could keep the economy moving and reach their goal of 3% in a year, which would be better. It mostly depends on what the institutions think. they can put that number anywhere they like. I would guess they are afraid of zero FFR and won’t bid it up. In that case honyocks like me can buy indirect and get a decent price. Also the REPO market is hot, and REPO fails, so collateral is scarce. Hate to go indirect and and then the Fed makes a big hike and or GDP pulls back, and poof. You get pulled into an overpriced auction just before the rug pull. Might be better to try direct but never done that.

Serious question…

So if home prices go down but mortgage rates go up in proportion, how is that supposed to help the housing situation and make it more affordable for first time buyers?

Down payment might be the big one. Another lack of future oriented thought process is environment for capital appreciation. If someone finances a home today with 20% down and it loses 20+%, there goes the cash you’ve worked hard for and may take years and years to get equity back, which would impact new homebuyers in todays market. Personally, I could care less about 30 years worth of interest savings, understanding the avg mortg. length is 10 years, closed out thru refi or sale. 30 years of interest “savings” in my mind wont beat any cap appreciation over the avg 10 year period.

When prices fall far enough their parents give them money to buy a house all cash.

The answer is that the Fed should have never repressed interest rates as it did, and it should have never done QE, to inflate asset prices, and particularly home prices. It created this mess. Now there is no good way out. The good way out was passed a long time ago.

My 2p. Based on what I can grasp of CB actions over the years.

Get rates up quick this spring and summer, ready for the correction/recession it’ll cause in late 22 early 23, and the space required for rate cuts/stimulus.

I can’t see rates being high for any length of time.

Net effect. Debts deflated a good chunk. Cost of future borrowing remains low for the future.

Privatise profits, check.

Socialise costs, check.

What could go wrong?

CB can use currency debasement to cheap the local population.

It doesn’t work as well or at all with anyone else.

The US by running large trade deficits isn’t going to be able to cheat foreign producers forever to current scale.

I love seeing mortgage rates alongside treasuries like this. Too many people think about housing as a commodity, but I like to view it as a fixed income instrument (like a bond) where the price moves inversely with the rate.

The impact on end-user demand for housing from rising rates is clear, but it also affects the investors currently in the market. Why would I take the risk of becoming a landlord only to beat the risk free rate of the 10-year by a few points (if at all).

I fear that the low mortgage rate so many buyers rushed to “lock in” will end up looking as useful as a cement life jacket on the Titanic.

Too many people still think US Treasuries are “risk free” — that is what college professors indoctrinate students into thinking. CAPM, Black Scholes options, etc etc. Its dogma.

A debt issued by an entity that runs massive spending deficits – decade after decade after decade – is not risk free.

An entity with on balance sheet debt 1.5x its GDP is not risk free.

An entity with $130 trillion in unfunded promises is not risk free; social security and medicare may not be “legal debts”, but registered voters think they are unbreakable promises. The US cannot keep these promises, therefor it won’t. It is far from risk free.

An entity run by ~80 year olds is not risk free. Pelosi and McConnel are over 80. Biden is nearly 80. Schumer is 75. Trump is the “youngster” at 74. Janet Yellen is issuing debt that will mature long after all the above persons have gone to the next world. The people issuing the debt are **NOT** going to repay it. They have no plans to balance spending (stop incurring more debt) – never mind talk of repaying.

There is no way US Treasuries are risk free, no matter the dogma preached in business schools. The US government does not even qualify as investment grade.

Printing currency is a stupid suggestion. First of all, that is a technical default. Second, printing currency has been tried countless times in history; it has never worked. And third, a global power is not supposed to behave like a 3rd world banana republic; 3rd world banana republics print currency to conceal debts.

The US government cannot afford to let interest rates go to “free market levels”. It is far from solvent even at artificially low rates.

Default via inflation or formal default – two technicalities for the same broken promises.

Most people are too stupid to understand inflation for what it is: a sleazy underhanded form of default.

Treasuries are a disaster for the next couple decades. Maybe someone without dementia will win in 2024 and be brave enough to admit default… HAHA!!! Far more likely, the government will default via inflation. LOTS more inflation to go, they haven’t even stopped the hemorrhaging — continued deficits are forecast for years to come.

Greg,

I have news for you: inflation in the US hits ALL dollar-denominated assets exactly the same way. But some have higher yields and others have lower yields to make up more or less for inflation, and some have no yield, and with others you have to rely on the market to pump up the prices to make up for inflation.

If asset prices decline, such as stocks, you get hit by a double-whammy: the decline in price, and the effects of inflation. So you might lose 30% due to a decline in the stock market, PLUS 8.5% due to inflation. You’re nearly 40% in the hole.

When and how will it all come to an end?

If I knew Alton, I promise I’d tell ya.

I’m holding TLT and seeing it produce some losses. Today it’s going up slightly. Is this a change in trend or should I cut my losses and sell my tlt?

lia,

TLT is down 30% since Aug 2020. Right now, it hit another multi-year low. It’s going down because long-term Treasury yields are going up. Do you think that long-term Treasury yields won’t go up any further? That’s your bet by holding TLT.

TLT, like many bond funds, has been mis-sold as a conservative investment when instead it is a speculative instrument to bet on always DECLINING long-term Treasury yields.

If you want to bet on declining long-term Treasury yields, you might want to hang on to TLT.

If you think long-term Treasury will be going higher from here on out, then why are you still holding TLT?

If you want to own Treasuries, buy them outright.