Something Has to Give.

By Wolf Richter for WOLF STREET.

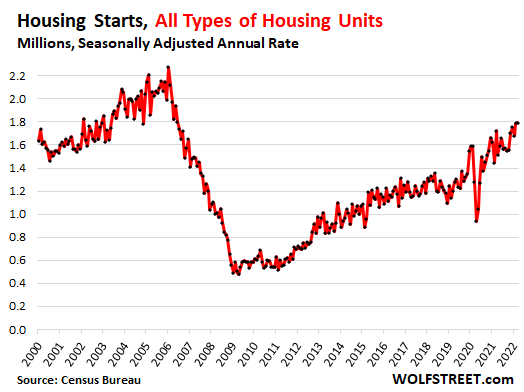

Builders started construction on 147,400 privately owned housing units of all types in March, the biggest March since 2006. Housing starts are very seasonal and peak in the summer. This included:

- 99,100 single-family houses, which was below March 2021 (102,800 houses), but both were the biggest March housing starts since 2007.

- 46,700 units in buildings with 5+ units, such as rental apartments and condos. This was the biggest month – any month, not just March – since 1986, as the boom in multifamily building construction continues, unperturbed by rumors of some kind of urban exodus.

In terms of the seasonally adjusted annual rate, builders started construction at a rate of 1.79 million housing units of all types in March, the highest of any month since June 2006.

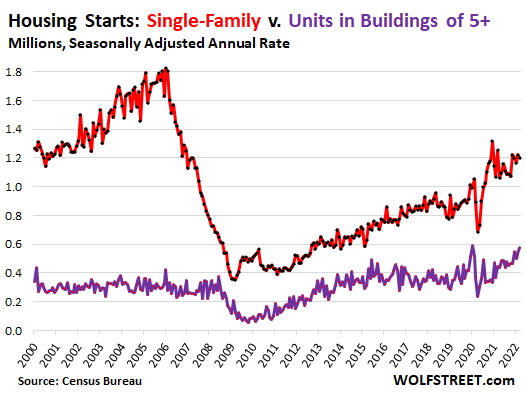

Single family houses v. units in multifamily buildings.

Construction starts of single-family houses, in terms of the seasonally adjusted annual rate, dipped from February to 1.20 million in March, in the same relatively high range that has prevailed since late 2020 and measures up there with 2007 (red line in the chart below).

Construction starts of units in buildings with five or more units, rose to a seasonally adjusted annual rate of 574,000 units. This and the spike in January 2020 were the biggest multifamily housing starts since 1986 (purple line):

Construction and the industries that it supports are important parts of the US economy. A downturn in the construction industry can substantially contribute to an overall economic recession.

Before the Great Recession, housing starts peaked in 2005, after years of overbuilding, and then went into a long downturn. The Great Recession didn’t start until December 2007, by which time housing starts had plunged. Housing starts bottomed out in early 2009 and stayed in the dumpster for two more years before beginning to recover.

Now, housing starts are booming, and there are no signs of a construction slowdown, beyond the issues foisted on the industry by shortages of materials and labor that cause construction projects to be delayed.

The “Housing Shortage?”

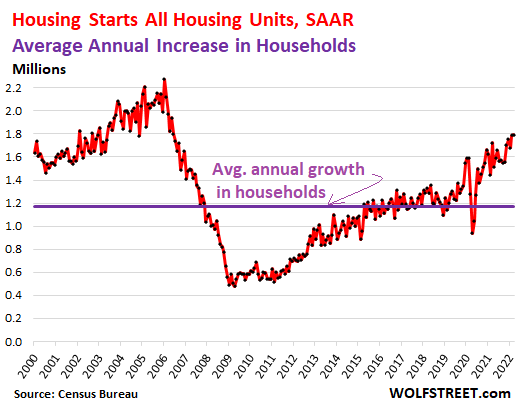

On a theoretical level, let’s compare the annual rate of housing starts to the annual rate of the increase in the number of households. This isn’t 100% on target because housing starts alone don’t include the (relatively small number of) housing units being torn down to make room for new housing units. But it serves as a rough indication of the trend over time.

In the chart below, the horizontal purple line marks the average annual increase in the number of households since 2000, according to the annual data from the Census Bureau through 2020, amounting to an average increase of 1.17 million households per year. Annual household growth varies from year to year. In 2020, household growth actually turned negative for the first time in the annual data going back to 1948.

A household is defined by people living in a housing unit (an address), whether a single person or a multi-generation family or a bunch of roommates. As long as they live in the same housing unit, it’s a “household.”

Where the red line – the seasonally adjusted annual rate (SAAR) of housing starts of all types – is above the purple line, housing units were built faster than households were being added on average.

As the chart shows, during the housing construction boom through 2005, there was significant overbuilding, which then contributed to the housing bust.

Even as the housing bust set in and the land was flooded with vacant and newly built housing units, housing starts continued to outrun household growth until 2007, when housing starts had plunged far enough to where for the next few years, there were fewer housing starts than average household growth, and those additional households started absorbing the housing units (buy or rent).

Between 2015 and 2019, housing starts and household growth were roughly in balance. But they’re not in balance now – with far more housing starts than average household growth, particularly in light of the negative household growth in 2020.

The picture of the much cited “housing shortage” is muddled by numerous factors, including the construction boom that is outrunning household growth. Many households have acquired more than one housing unit, where the other units are vacant much or all of the time. This may be a second home or a third home, or a vacation rental, or a home they haven’t sold yet after moving out in order to ride up the market all the way and then sell it (I know a few people who are doing precisely that).

However, when investors buy housing units to then put them on the rental market, there is no impact on the overall “housing shortage.” It’s when someone buys a second home or a vacation home that remains unoccupied most of the time, or is turned into a vacation rental, that a housing unit is removed as a housing unit.

What there is, though, is a shortage of housing units that are priced such that people can actually afford to live in them, rental or purchase, after the massive price increases in recent years, and the rent increases in many cities.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m old enough to remember when homes were for living in. You know before fictionalization.

Right? I can think of two seperate people/households that are essentially homeless because of this “great” work of fictions’ impact on the rental market. Combine that with the fact that relatives that could have helped them prior to inflation/ increased cost of everything no longer can, and you have a mass of unescessary suffering.

Hope the horders under the guise of “investment” like the societal “fruits of their labor” 10 years from now.

We all effect eachother in the grand scheme of things.

(Apologies, I’m fed up with the victim blaming that has become en vogue amongst those playing money games- people shouldn’t suffer for sitting at the craft station instead of a poker table).

Thanks for that apt metaphor. Craft vs poker table. I will remember this. The condemnation of anyone without interest, appetite or funds for crypto and housing speculation makes me indignant. “Have fun being poor” and similar memes. It’s gross how rampant this is. It’s nothing short of terrifying.

I’m all for fair rules that reward merit/discipline (with safety nets) and prudent budgeting/living with means, to be clear. But the current cynicism and misanthropy is off the charts for my 46 years.

Craft station vs. poker table. Thank you. A million times. I get so tired of the virtue of every activity in life and judgment about that activity being reduced to how much money it makes.

I think you mean securitization

Securitization + Mark-to-Model Accounting = Fictionalization.

Awesome

Or “mark-to-make-believe”

Lol. I meant financialization but whatev

It’s all fake no matter how you slice it

NONE of it could’ve happened without the Fed aiding and abetting via money creation. Take away the punch bowl (and KEEP it away!) and all the partiers end up on the clean-up crew with the rest of us.

I know you didn’t mean “fictionalization”, but what an accurate and realistic way to look at “financialization”! It is creating fake values using fake money and manipulated the market to no long reflect reality.

And the common people are the people who suffered the most from these fake fictionalization of our economy.

Pretty sure he meant “fictionalization”, which is a very succinct way of describing the zeitgeist of monetary (and fiscal) policy writ large since Bernanke & Co.

Hopefully rising interest rates will start driving up inventories and affordability. What this country needs is a building boom of single family homes with two bedrooms (one used as an office) in the 1100sqft range that the average single person or couple can occupy and maintain comfortably. But as with yachts, the real money is in larger models so smaller more efficient options are hardly built these days.

“What this country needs is a building boom of single family homes with two bedrooms (one used as an office) in the 1100sqft range…”

While I agree, that ain’t gonna happen. At least not where the land is worth anything. Land where most people want to live is too expensive/valuable to put a small house on it. Builders are much better off building as large of a home that aesthetically fits on a given lot. So….we get bigger houses. Out in the sticks, or places where demand to live is relatively low, different story.

The state of CA’s solution is to make smaller — as in tiny — pieces of land buildable. It’s a law called SB9. Any lot can be subdivided into as little as 1200 sq ft (not a typo). And then you can put a house AND an ADU on it (also not a typo). That’s CA’s best shot as a boom of 2-ish bedroom homes in good areas.

Is this the State’s (Ca) way of increasing population in order to collect more tax revenue?

AA-my fair state has never had to try to increase its population, and, in fact, has historically discouraged it over multiple occasions (Woody Guthrie’s ‘Do-Re-Mi’ an entertaining example). Y’all just kept coming, anyway, with the attendant costs of herding so many cats rising appropriately (as many other states now absorbing a current pop. increase will discover/are discovering to their oft-stated chagrin, here…).

may we all find a better day.

No one wants to live in a 2 bedroom/1bath house…and if you are the minority who *chooses* that instead of having it forced on you, that’s what the townhouses are for. Which is exactly what the builders are angling at these days. They’re building more 2-and 3-unit townhomes than I have seen since 1986. You can now purchase half a unit for what a single family house used to cost, just 3-4 years ago.

I am seeing townhouses built but they are they are rentals. Also, when I talk to people who are looking to buy a home, they want a single family home and not a Townhouse. They have been overbid so many times they may settle for a townhouse.

What the country needs is a change in laws to make it financially unattractive to own more than two homes. This is in the same spirit as a law needed to prohibit share buybacks via issuing debt. It’s all nonproductive investment, detrimental to the real economy but benefical to “financialization” that is running the world into the ground.

Not a single law needs to change. Simply stop the Fed from printing trillions of dollars and the whole game ends.

Bingo….alt way…balanced budget. Cut medicare, medicade 80%. Trim ss down to real needs. Cut defence 10% a year for 5 yrs….rest of govt programs

Cut 10% a yr for 5 yrs. Inflation goes to zero with NO deficit spending!

Lastly put congress on paid commision. Paid on what you dont spend!

No JeffD,

What the USA does not need are more restrictions on an individual’s rights and liberties to decide their own destiny.

Please, please do not think that your ideas of what is correct and proper for me to do, or not to do with my life’s choices to follow should be made into law – local, state and/or federal.

I already have this financial incentive that shapes my decision making. It is called “Property Tax.”

Thank you,

-DanBob

What this country needs is a “sustained period” of time where mortgages are at a level that supports housing affordability. If we’re lucky enough to see 6% mortgages this year, it most certainly we foster the falling price environment that’s needed.

The FED has totally skewed the housing market. And the FTC didn’t do their job by stepping in and investigating lumber price fixing, which along with ultra low rates created enormous upward pricing pressures over the last two years.

All of Wolf’s charts show that construction of new homes is 200 to 400K units below from what it was from 2005 – 2007. Don’t worry, all of this will get sorted out in the next 2-3 months. By July, we’ll see definitive proof that house prices are on the decline. The decline in housing prices will be governed by how high the FED lets mortgage rates go.

And with $9T is assets on the balance sheet to roll off, we could be looking at very large increase in the 10YT & subsequently mortgage rates.

I’m personally hoping for 7.25% 30YFRM by October which will most assuredly gut punch the housing market. Housing has to drop by at least 20% over the next 18 months to return some form of healthy long-term affordability to the market.

I keep hearing this, and I like what I hear, but keep in mind that this time there are other issues at play that didn’t exist in the last housing bubble. You simply can’t build a home for what it would cost you to buy one today. If you are building, good luck getting windows, doors, and utility-associated hardware. When you can get them the prices are severely inflated due to very tight supply (not just higher raw material costs). Forget inflated wood prices – at least you can still get it!

Ah the United States is finally catching up to the other anglosphere nations. You see houses aren’t for living in they are for making money in an endless Ponzi scheme. But this time the Ponzi scheme can never fail!

Sure you guys and the Irish tried it in 2008 but you really slipped up by letting it all crash.

Australia has been doing this for 25 years now and we are all super rich! (Except for those damn millennials who never bought a home for some reason.) Who needs to work when you home increases in value by more than you earn in a year! The typical home in Sydney is now $1.4mil so we are all millionaires.

Trust me nothing can go wrong ever. Especially if you have government policies that literally give you tens of thousands of dollars for building a house.

What about those who can’t afford rent? Well our Prime Minister recently had excellent advice for them, they should go buy a house!

A succinct description of the malady but no description of the cause.

Political, economic, or humanistic, or various combinations of all three categories. Opinions are like elbows which provides cover for the lies that we believe.

Australia is a foreign country of which I have never been and therefore have no associative snide comments to make about ‘stralia other than to say that the ones I met seemed like the same blokes I grew up with.

The holy grail is love.

I just recorded a video on this last night. I’ll be posting tomorrow. This is going to be interesting for sure.

Be sure to leave us a link eg. nnn dot com.

goomee – Her name is a hyperlink to her website.

Thanks, didn’t know slanty blue lettering is a hyperlink.

Are multi family buildings with 2-4 units really that small, or am I missing something? (Fewer than 2000, if my math is right)

And if yes, why?

I ask partly because my son has voiced an interest in buying a duplex and renting out half, as a possible way to enter the realm of home-ownership.

The numbers are very small: 1,600 in March not seasonally adjusted, for a seasonal adjusted annual rate of 19,000 (0.019 million) in March in the 1.79 million total. The issue is that the monthly number is so small that it doesn’t meet Census Bureau’s own sampling reliability requirements for publication. And so it releases the number for people to see, but it’s not designed for publication.

In the overall total of 1.79 million, the 0.019 million is included.

“Many households have acquired more than one housing unit, where the other units are vacant much or all of the time.”

Must be nice.

Bought my first house in1983 POS ,remodeled made some mistakes.But this is how we learn ,if your mindset is right everyone can own a home. Won’t be in best neighborhood,will probably need a lot of work ,but get off your ass and do something

I’m at so unbelievably tired of hearing this.

I’ve built furniture, custom motorcycles etc. I can fix up a complete pos in a year or two no problem. In fact I’d love to do that, however, anything at or below average values for my area sells in days maybe less, for cash, with no inspection.

Please flea, tell me as a millennial who’s earns well over the average wage for my age how I should scrounge up $400k?

You elderly folks are so so out of touch with reality right now it’s truly unbelievable.

Cem u must not live in flyover country ,plenty of houses here way cheaper

Getting your hands on $400K isn’t impossible but it requires creativity. You need a business partner.

One way to get $400K to make a “cash” offer is to borrow from parents (who might refi to get the cash).

I’d bet you can also find some bank-like loan-shark sort of company willing to make a “non-mortgage” loan that will be paid off quickly once you own the house and can take out a mortgage on it…

Back in 2005-2008 there were “down-payment assistance” programs that would let insane buyers skirt the mortgage lenders’ minimum-down-payment rules by lending them enough for the down payment.

Same principle applies now, except the “down payment assistance” is 100% of principal to get to an “all-cash” offer.

Yes, all of this is insane, and the foolishness of it will be exposed when interest rates rise high enough. At that point you’ll be able to buy fixer-uppers on your credit card.

Check out the Cleveland area. There are some nice-looking houses that are incredibly cheap. And they are on nice-looking blocks.

There may be a crime issue a half mile or mile away.

But I think the stronger factor is that Cleveland is 200,000 people smaller than it was in 1970. All over the Midwest there are astoundingly cheap houses to be found . . . as long as you don’t need a local job to go with it. The Upper Peninsula of Michigan has towns with populations that have been shrinking for years and years. Houses there are practically free and there is no crime problem.

Just no jobs.

flea is correct Cem:

Last time around this cycle, a bit later to be sure, a friend was working for a guy who was paying $3-5K per house on the courthouse steps in flyover area near us.

Friend was fixing em up in couple of weeks, (and could not help us during that time) as needed for safety, code compliance, etc., and usually new paint and rugs.

Guy was either selling outright or renting em out and then financing on basis of rent to buy the next one.

Some of those houses were in pretty good stable hoods, usually empty from an elder death.

Likely to be that way again as we continue the cycle been going on for eva!!

Cem:

The same way my kids did…. We bought my daughter’s house with cash (mine) and she repaid me by refinancing with a conventional mortgage. The reason we paid cash was so her offer was better than the competition. Quick close. Only contingency was an inspection. No appraisal problems. Nada. And this was in the Bay Area in 2010 when the Chinese money was flowing freely.

Ditto my son’s first house. He bought a POS in TX for $110K and breathed drywall dust for three years as he rebuilt it. In his current house, he and his wife have inhaled drywall dust for going on 5 years. Bought for $400k and now “worth” $1.2M in Austin, TX.

So us “old folks” aren’t out of touch with reality. My son’s house (the first one) was funded by money I inherited from my mother. He repaid me and I rolled that and a tad more to help my daughter. She made me whole and life moves on.

The first house my wife and I bought was beyond our ability to save the down stroke for. We borrowed from my sister and parents to make the offer. Ate ramen to pay them off.

So, the question remains: How important is owning a home to you? If it’s super important, you’ll figure it out. If you sit around whining, the world will pass you by.

As my father used to say: If you’re looking for sympathy, you’ll find it in the dictionary between sh*t and syphilis.

Lol to these boomer responses, “have your parents loan you the money, get a hard money loan @ 10% etc “

Cem, you are justified in your frustration. There are many clueless people of all ages bragging about their great investment genius of having been born at the right time or to the right parents. Cluelessness is being born on third base and thinking you hit a triple. I know elderly and young people like this. Don’t you have access to limitless funds from the bank of mommy and daddy to pay cash? Inheritances? What is your problem? $400K is indeed a lot, a two-income amount for most.

“The same way my kids did…. We bought my daughter’s house with cash (mine)…”

See, you can do it, too! Just borrow the money from your rich parents. Great advice! What’s the matter, are you too lazy to have been born into an already wealthy family??

P.S. If you weren’t born with parents who’ve got over $400K in home equity, so you need a business partner: Find a realtor and ask how others are handling that situation… since there’s demand, there will be a supply (at the right price).

Cem

Lots of observations here and most of those Boomers really do want to help. As a younger Boomer with a Millenial kid, I will also add that beyond housing, Millenials have grown up with unique challenges – but that’s a separate discussion on its own.

Your dilemma does come down to how important home ownership is to you vs where you work or what you do for work.

At 23, I moved FROM flyover country TO So Cal. Rented 2 years, partnered with my fiance to get into a low end condo, then a modest SFH a couple years later with a 26 mile commute. Boy my job / work was just soooo important – and my income was modest. (by CA standards).

After 10 years, realized the Hotel CA lyrics by the Eagles were true and escaped back to flyover country (jobs with less pay) and retired at 51.

If your job / status / current domicile / salary are important to you, it’s no sin. It was hard for me to leave So Cal weather and desirous social attractions to that area, but looking back, it was the right call for me.

There are thousands of decent homes under $100K in flyover USA. If your personal situation can accommodate that option and YOU determine the cost-benefit seems right, then you can choose that route. If not, it’s no sin to live and work in a cool place and enjoy your life !!

Just ask Mom and Dad. Just inherit and you’re golden. Just get a business partner. Ugh.

It’s not only Millennials hearing this type of advice ad nauseam. I’m a younger Boomer and have been supporting my mother for much of my adult life (she’s never been “robust” healthwise). My father is long dead and left everything to his second wife. The idea of me—a full-time, now low-income caregiver for a bedridden parent whose only income is social security—getting a business partner is ludicrous.

Make no mistake. I, in no way, feel sorry for myself. I’m happy to fulfill my responsibility. I’m only commenting to point out that one-size-fits-all advice rarely fits all.

And, yes, one day, I don’t know how, but I WILL figure out how to buy a house. Back home, somewhere in dreaded overpriced Northern California. I would even love for it to be one of those small SFR that HoneyCat16 says no one wants. 1 br and an office would be perfect once I’m on my own again. Why would I want to maintain anything bigger than that?

Here’s my take:

If you’re buying right now, you’re making a mistake. One that might lead to bankruptcy or getting stuck in a location for a long period of time. THAT is the crux of Wolf’s article.

Can the market remain elevated longer than you think? Yes. Will it mean revert, putting 2022 buyers under water: yes.

Buy low/sell high.

Not really “nice” under normal conditions because the carrying costs of a home are fairly large. It’s only nice if home prices jump 20% a year, which they won’t forever. And it’s not at all nice when home prices decline; it then turns into a big headache except for the truly rich.

Houses are money pits. Truly. Most people can ill afford a $15k HVAC replacement, a $20,000 roof, etc. I chuckle to myself at all these Johnny-come-lately types who drank the Kool-Aid and think of houses as some sort of magic money tree. Meanwhile, they’re rotting to the ground in real time.

A home is a consumer durable with a longer shelf life. It wears out without maintenance, just like anything else.

Buying at bubble prices, millions are going to find out later they cannot actually afford to consume the home they live in, even where they can (supposedly) afford the monthly payment or qualify for the loan.

Depth Charge, ALL housing rates as money pits. Where do you think the money for repairs on apartment houses comes from? (Hint – it’s from the tenants in the their rent). Condos can be an absolute nightmare for the residents. The board picks the contractors, and the owners get hit with an assessment. At least with a single family house, I have some control of the expenses.

It is when you can’t lose money… until you do.

But this time will these people be living in an economy where they can hodl post correction?

No, not unless the government imposes another mortgage moratorium.

The economy and financial system are in worse shape versus 2007. Fake “growth” will continue to some extent in the upcoming massive recession or depression (a lot more if the government can get away with it) but credit standards are going to tighten noticeably to go with higher rates.

“No, not unless the government imposes another mortgage moratorium.”

The illegal suspension of contract law is disgusting. What the FED and .gov have done is created an ecosystem of moral hazard which is almost inconceivable in its scope. It’s a giant “the FED and .gov have got my back” echo chamber among the debt junkies.

Not nice. Eliminate capital gains and I will sell to someone who needs a home. Don’t eliminate capital gains and I keep the property til I die so my kids can inherit it.

That is the smartest thing you can do.

Otherwise you killed with taxes on the inflated value of your house.

Two words: Zillow, Open Door – when these companies come in w all cash and buy up entire zip codes the middle class folks get let out the market

Shawn C

Two things:

1. Zillow already threw in the towel on the flipping business, after losing a ton of money. Opendoor is still doing it but losing a ton of money, and its shares have collapsed.

2. The flipping business doesn’t remove homes from the market and doesn’t contribute to the “housing shortage,” because flippers buy and sell. But it might contribute to price increases.

The post has an article that claims 15% of homes in 40 major markets were bought by investors. This has been climbing for years and is at a peak now.

That has an effect.

The NAR has been saying that about 20% of single-family houses and condos are bought by investors, roughly the same over the years. Investors are from mom-and-pop to large firms. They put them on the rental market, and so they remain on a housing unit. The problem arises when they turn it into a vacation rental or keep it as a second or third home that remains mostly unoccupied.

ALL of the multifamily apartment buildings are owned by investors, by definition.

Ed

Why are you and others quoting bull s$it from the Washington Post. Frankly, I’m not interested. The WP is not a newspaper. Its nothing but a rag which shills for its advertising sponsors. I’m surprised Wolf allows this crap to be posted on his site.

One can only hope that we find ourselves in that same environment in 2008, when flipping houses became a big risk. What helps prices go up and help them cascade down. I for one hope all of these big investment companies lose their shorts in the next 2-3 years.

Outstanding stuff, as usual, Wolf.

One quick thought (I’ll probably have more later) – by averaging out the annual household growth, you may be obscuring the signals that homebuilders actually use (n-1 yr household growth).

(Marginal note – I’m sure builders look at occupancy – particularly in apts – and rent levels too).

That flat 20 yr average line is useful in highlighting the volatility/oscillations that the ZIRP Era (error) hath wrought in the home *building* mkt but it obscures the impact that ZIRP’s failure has had on household *formation* growth (ie, hope) itself.

I’m almost certain that household formation rates have been deteriorating a long time (metric of economic despair) – but averaging things out tends to obscure that.

But the more important point is that you have really locked onto a major, major dynamic here.

1) ZIRP as a 2002 response to the US’ emerging (horrible) lack of intl competitiveness (translated into unemployment/lack of job growth) resulted in,

2) a horrific destabilization of the housing mkt…

3) whose inevitable consequence (2009 implosion) fed back into

4) the awful downward spiral (collapsing household formation due to hopelessness, despair, vastly overpriced assets…and *still* the lack of intl competitiveness).

For 20 yrs DC has been trying to fix horrible US economic fundamentals with paper solutions that have only been making the economic fundamentals worse.

cas127,

Using the year-to-year household growth data each year to make decisions for the next year is a fool’s errand. And using the annual data each year to compare to housing starts the same year is conceptually wrong. Here’s why:

Household growth data – the data, not the reality of people forming an actual household – is very erratic from year to year. But if you look at it in pairs of two years, already it’s not that erratic anymore, as a year of high growth is followed by a year of low growth, and vice versa. This is due to the way the data is collected and estimated.

Every ten years, we get the census, and with it the most accurate household data. But within the annual figures, from one year to the next, we’re looking at a lot of noise that gets canceled out the next year (see the annual figures below).

Builders don’t look at the national data. It’s irrelevant for their decisions. They look at a lot of local micro data where they intend to build. If they want to build in Plano, TX, it doesn’t matter what household growth is in California, or the US overall. What matters is what’s happening in the Dallas-Ft. Worth metro and in Plano.

Here’s the annual household growth in thousands of households per year (note the negative for 2020):

2000: 831

2001: 3504

2002: 1088

2003: 1981

2004: 722

2005: 1343

2006: 1041

2007: 1627

2008: 772

2009: 398

2010: 357

2011: 2389

2012: 1157

2013: 1375

2014: 770

2015: 1358

2016: 1232

2017: 405

2018: 1362

2019: 993

2020: -128

Wolf, I had a similar thought to cas127 – that the conclusions related to whether they are under or overbuilding are very much based on where you put that purple line. So I thought to myself, “maybe a 3 year rolling average with a 95% confidence interval will really change my mind”. Leaving out 2020 and using your data above, the moving average is actually declining… Wow. So where the heck does this narrative that household formation is driving low inventory and high prices come from? Completely made up?

Much of housing depends on illegal import,export of immmigrants

2020 was the last year of Trump, he clamped down on immigration somewhat to look good for the election. In the last 1.5 years, around 4 million immigrants were added to the US population – legal and illegal. I don’t think this is reflected in any government stats and they aren’t trustworthy anyway.

There are a lot of government (really taxpayers) subsidies for new construction, section 8, etc. Go to any metro rental complex and you will meet plenty of people who will greet you with “No hablo ingles”… fresh from the border. The taxpayers are being drained in order to bring real wages further down in the next leg of the race to the bottom.

Whatever the reason. It is quite amazing the amount of immigrants arriving in the U.S. This has to have an effect on housing? From the Center of immigration studies. Basically we need to add enough houses that would be in a city the size of Denver or Seattle. These are the people caught and released. Many more enter undetected.

——————————————

Border Patrol set an all-time record for apprehensions there in FY 2021, and since the beginning of February 2021 (Biden’s first full month in office), CBP has encountered nearly 2.5 million aliens who have entered illegally or without proper documents at the U.S.-Mexico line.

Of those nearly 2.5 million aliens, about 1.356 million have been expelled under Title 42. That still leaves more than 1.124 million who have been processed under the Immigration and Nationality Act (INA) since February 2021.

Which brings me to DHS’s migrant releases. Under section 235 of the INA, DHS is supposed to detain all illegal migrants and aliens seeking admission who are not clearly admissible, but through the end of March, the Biden administration has released 836,225 of them. The Biden administration’s lawful authority to release any of those aliens — as opposed to returning them to Mexico to await their asylum hearings — is at the heart of Texas.

As I have noted before, the number of illegal migrants the Biden administration has released into the United States is greater than the population of Seattle (787,995) or Denver (760,049).

ru82, we are all taking Spanish speaking classes here in Texas now. Come visit, enjoy a Taco. Get sick?.. no insurance required at the ER.

“…housing starts continued to outrun household growth until 2007…”

I remember how locally some builders at that time went bust, others moved to the oil fields in North Dakota.

Always a question of how much living space people can afford. In China about 1/10 of the US. I see a lot of new non-affordable affordable housing being built and I have to assume these are govt subsidized rents. The US housing market is distended, with older homeowners stuck in larger homes, working class people warehoused in smaller homes near their work. Work locations keep moving. Mobility is key to the US workforce, and WFH was an innovation on that design. Housing is a government policy, keeping the squirrels running inside their cage is economic policy. Nuff said.

Besides how much can one afford, but what size does one need. I grew up in a 3 bedroom 1200 sq ft home. I Live in a 2400 sq ft home. I do not need this big of a home. Most families do not either.

VERY astute r10:

when WE, in this case the family WE, relocated from our home built home in flyover, back to the saintly part of the tpa bay area to care for very elderly parents, WE, in this case my spouse, said WE did NOT need the 2500 SF WE had built,,,

So, WE have less than a K of SF, and other than the storage of all the ”stuff”,,, the SF is plenty…

Still plenty of ”challenges” to keep even that much clean and tidy and so on and so forth,,,

MANY challenges coming,,, keep powder dry and, especially, keep your mind as clear as you possibly can to recognize and understand the VAST changes coming quickly these days…

Thanks again Wolf, for the very very GREAT GRAPHICS

Most people I know have a second property

or regular access to one. Usually, a vacation home.

They are not super wealthy and Wolf may have hit

on a big reason there is a shortage of starter homes.

This may bode well for the future if the population #’s

stabilizes

True. My city has a hosing shortage but it certainly is not a vacation destination so the vacation home scenario will not apply in my situation.

Vacation homes will be regional at vacation areas? I guess like Florda, etc.

In Midwest cities, there are not any vacation homes or 2nd homes to help with the housing shortage.

I live in flyover country but we have a nice tourism draw with the bourbon trail that has exploded over the past 7 years. I know of many single family homes that are short term rentals on AirBnB. These same homes were occupied by long term tenants or owner occupiers ten years ago.

It would be interesting to find welt/annual supply data for number short term rental/AirBnB homes over the past 5 years?

I think the popularity of AirBnB has had a major impact on the housing shortage.

AGREE Marco, and thanks for putting your 2cents or howevermany into these comments.

Please continue reporting from YOUR locale, as this is one of,, just one of to be sure, the wonderful aspects of Wolf’s wonder,,,

Take a walk in the lumberyard and check on lumber prices. A sheet of OSB is $50, 2×4 studs are pushing $10, PVC plumbing is up, and that is before you try to hire anyone. It is common on construction sites for builders to use the overhead cranes to hoist their generators high in the air to keep them from being stolen. This weekend I saw a bundle (usually of 60 sheets) of OSB hoisted 40 feet in the air. Throw in high lumber prices, shortages of everything, no laborers, and interest rate hikes and you can get into trouble quick.

It won’t last. Look for lumber prices to revert to their 350MBF range. Windows, garage doors, pipe, cable to drop to less than production costs. Builders begging for work. Sub-contractors looking for other fields of endeavour.

It will hurt. it is certain.

Price oscillations are pretty typical in a lot of fairly liquidity mkts, as supply/demand both respond to earlier price movements. The variations feed on themselves to an extent.

But money-print inflation increases the amplitude of the oscillations – one reason why inflation has historically been hated – it increases the uncertainty in the system, making it harder to plan accurately.

I’m not sure where you’re located but here in the Twin Cities builders are begging for subcontractors because there’s more work than they can handle. Some of the local general contractors hire crews that commute from 60 miles away. We’re a crew of 3 and we’re booked out until September. I’m sure it will end eventually but I don’t see it happening this year.

Right after the housing release Bullard announced he is considering a 3/4 point increase.

IMO the fed is going to go 3/4 or more.

They are now being called near idiots….by their friends. Rates are going to sky rocket. Expect an immediate 100 billion per month of sales

I cant stop laughing at this comment. the FED is moving slowly to allow inflation to chew away at the deficit. It does surprise me that the housing market inflation doesn’t catch their “eye” as supreme bubble territory or there are just plain ignoring it. Remember “inflation is transitory”, “its a supply side problem” and of course we must move slowly a we dont want to spark a “recession”. ha ha ha. As many others have said we need a reasonable reset and restart with real manufacturing as our cornerstone ( not military of course) with upgrades in infrastructure and STEM education as well as a “rebirth” of the trades. Will it happen??? I hope every day for future generations it does. Of note in the midatlantic (PA/MD) the builders are pushing the 3000 sqft – 550K home that was 2500 sqft and 300K just a few years ago.

Will V,

Interesting comment about a ‘rebirth in trades.’ One of my sons is an electrical contractor (industrial and commercial, but will do residential at times). He’s had the hardest time finding an apprentice who is reliable, will work hard, etc. Finally he got a guy — a serious 37-year-old family man looking for an opportunity. Working out for both parties.

So much for the Millennials.

Millenials are 37…you mean Gen Y, short for “Why work”

MiTurn,

That 37-year-old is a Millennial.

…what

37 is a millenial.

Do Canada next! (Please? :) )

Re record number of buildings with 5+ units.

The U.S. will probably have to redo zoning standards at some point to allow more tiny homes, container homes, etc to deal with poverty/homelessness.

The trends go in the opposite direction, by making it a crime to be homeless so that poor people will be encouraged to go live somewhere else. That way they won’t be a burden on local taxpayers or compromise home values.

Problem solved. Next!

Besides, there are no poor people in the US, because compared to poor people in other countries they’re actually rich. You can tell because even poor people in the US have color teevee sets, even if they don’t have any place to plug them in.

Wealth is relative though. If everybody has $10 million the people with $5 million will riot, though more politely than those with nothing.

There are a lot of people in the U.S., about 30%, who do not have enough savings to cover two months of bad weather.

Zoning real estate to encourage ‘low budget housing’ solves a lot more problems than it might create.

Zoning *is* the problem.

If there were *no* zoning, supply and demand would be in balance. Zoning is *the* reason, long term, that you can’t build a house: because you don’t have a correctly zoned space to build on.

(I didn’t say what it would cost you, etc. That’s another supply-@demand thing. But you could build your own house.)

Actually for AD:

Right on!!!

and perhaps why we see some cities now either eliminating SFR ”zoning” or at least restricting it to the places in their cities where the really really rich folks live.

Eventually, we can at least hope that the vast majority of cities will eliminate, or at least modify zoning so that ADU, etc., will be not only allowed, but encouraged.

Efforts to criminalize homelessness persist in Georgia and other states. The increasing unaffordability of housing guarantees the US will soon be experiencing a major crime spree. Those who aren’t well off won’t have to do anything but fail in their legal obligation to be sufficiently profitable.

State officials will have no choice but to imprison such persons and rent them out as cheap labor to plantations – er, factory farms, so as to defray the cost of imprisoning them and maybe even turn a profit. Impoverished persons with extra kidneys could be encouraged to sell them so they won’t be such a burden to the prison system, which is expected to be extremely expensive.

Their kids will be taken care of by giving them jobs in manufacturing, but because of child labor laws it won’t be possible to pay them anything so they’ll wear tatters but no shoes. On the plus side it won’t cost taxpayers anything to educate them. They will grow up proud that they can make a positive contribution to society, despite their initial poor decision to choose lazy immoral parents.

People who think skyrocketing home prices are a problem just aren’t looking at the big picture.

Another modest proposal should be considered- faced with a possible global food shortage due to the war in Ukraine, fertilizer shortages, climate change etc, have we considered simply eating these excess homeless people?

Ahh the flippant uninhibited British humor of pre-PC era…

In my next life I will be a British Gentleman of Independent Means, living off 7% perpetuities aka consols…

Wearing top hat, spending time fox hunting and writing pamphlets.

“A Modest Proposal For preventing the Children of Poor People From being a Burthen to Their Parents or Country, and For making them Beneficial to the Publica commonly referred to as A Modest Proposal”

Jonathan Swift, 1729.

Conclusion:

“A young healthy child well nursed, is, at a year old, a most delicious nourishing and wholesome food, whether stewed, roasted, baked, or boiled; and I make no doubt that it will equally serve in a fricassee, or a ragout.”

600dpi scan of Mr. Swift pamphlet can be found on archive dot org 😁

Thank you, Google Books scan service !!!

Do all y’all think the bubble pops or deflates? What will be the catalyst?

The most important thing a British Gentleman ever learns is when to stop being one.

Wasn’t Swift executed for his modest proposal?

“…have we considered simply eating these excess…people?”

I fixed it for you. The homeless should not be on the menu, but instead the central bankers.

Granny Yellen is round and seriously plump, and should be grilled on kabobs served to the homeless near the dump.

Gangly Jay Powell looks to be tough to chew, therefore lending himself to hobo stew.

And so on and so forth…

Soylent Green is people…..

Dry, funny. :-)

Sooooooo, Unamused,

Did you just lay out the ground work that the South should have won the Civil War…

Sounds like it….

COWG, a sophisticate like yourself should be able to recognize sarcasm without the sarcasm (“/s”) switch, but that’s probably my fault because I try to be clever instead of making it obvious.

In point of fact the South did win the US Civil War. They didn’t win it militarily but they did win it culturally, socially, and politically. And they’re still winning it. Next year, once they’ve gotten rid of Social Security and worker rights and all that other commie crap, they can work on reversing certain unconstitutional amendments and get womenfolk back to being barefoot and pregnant like they’re supposed to.

See Richardson, Heather Cox. ‘How the South Won the Civil War: Oligarchy, Democracy, and the Continuing Fight for the Soul of America’. New York: Oxford University Press, 2020. Print.

Don’t forget banning all math books.

Those numbers can be scary and teach the youngins about slave… err I mean states rights.

and those would be the very reasons that gazillions of folks from up north continue to move to the flower state, eh una?

of course some of them cannot stand the incredible heat and humidity, not to mention the existing humanity on that long long peninsula, and end up being ”half backs” somewhere north of paradise, but still in what is called the south

truly wondering why SO many folks want to move SO far south,,, used to wish they wouldn’t, but gave that up about 1956, and here WE are at a similar point in the cycle once again for maybe the SIXTH time since then??? something like that

Cem,

The world is finding out…

Maff is complicated….

“truly wondering why SO many folks want to move SO far south”

Jobs have been in the confederate states in recent years because that’s where corporations have been going. And corps have been going there because that’s where the cheap labor, cheap land has been. Also non-enforcement of restrictive regulations, if any.

Unlike Union states, you can get away with just about anything in Confederate states. Well, maybe not you personally.

VintageVNet, New York, MA and CT are surprisingly (to some–mainly Southerners) Right-leaning states, save for the handful of their most heavily populated cities/counties whose votes dictate for the rest of the state.

Retiring to FL is standard practice in NY. Even for the Left-leaning, as the lure of not having the fillings in your teeth taxed (and later retaxed as inheritance upon your death) drives most of our older buzzards to migrate South.

You ARE the ORIGINAL una-, alright! And back up to speed, AND at the perfect time in the comments. Just when I was starting to get a headache. Thanks, I will continue doing sociology.

BTW, eating babies IS DEFINITELY a healthier meat diet….check out sialic acid, we are different from the other mammals.

re “Impoverished persons with extra kidneys could be encouraged to sell them so they won’t be such a burden to the prison system”

There are only so many kidneys a person can sell before medical costs outweigh payoffs.

The Chinese system of removing two kidneys is frowned upon by medical experts.

Great data as always. I follow the housing markets, both local(Naples, FL) and national on a daily basis. One of the smartest housing analyst is Ivy Zelman(Zelman & Assoc). Ivy believes the US has a bit of a housing shortage(1M homes or so). While the bulk of the housing analysts believe this figure is closer to 5M. Ivy called the bubble in the GFC well before it imploded. My money is Ivy and Wolf are closer to right than the bulk of the housing analysts.

There is no housing shortage. There is an excess of people who can’t afford housing because they’re morally deficient, but that number is easily reduced by encouraging them to live somewhere else.

Seriously, you need to start thinking outside the box. So to speak.

“Are there no prisons?” asked Scrooge.

“Plenty of prisons,” said the gentleman, laying down the pen again.

“And the Union workhouses?” demanded Scrooge. “Are they still in operation?”

“They are. Still,” returned the gentleman, “I wish I could say they were not.”

“The Treadmill and the Poor Law are in full vigour, then?” said Scrooge.

“Both very busy, sir.”

“ There is no housing shortage. There is an excess of people who can’t afford housing because they’re morally deficient, but that number is easily reduced by encouraging them to live somewhere else.”

Spot on…

The crash in the numbers of housing available after the GFC tells you one thing…

Housing Is a product, like every other widget any other manufacturer makes…

What the data doesn’t show is the number of builders who only built 3-4 houses a year but made $200k a year doing so…

A good gig…

The decline in the number of houses for sale is directly related to the available customers to buy that “ widget”…

After the GFC, the waitress who bought 3 houses, and the other fools were washed out …no more widget buyers…

The builders DIDNT CARE…

Their “widget” was sold and it wasn’t their responsibility any longer… on to the next widget…

So we quit building widgets ( housing) because there was no one to buy them…

The 30yr mortgage at that time was around 6%…

Housing is very, very local and very price sensitive based on the neighborhood *and* the availability of making money from it…

If you tell me different, you’re lying :)

Poor people are poor for a reason…

If they moved in next door to you, would you like a 30-40% reduction in your house value… I think not…

Right now, housing is hot because there are willing buyers to buy the widget….

And until the Fed changes the dynamics, it will remain that way…

Prove me wrong… give me an example where you gave up a $200k gain so you could sell your house to a poorer person so they could live at your level…

Look inward before you answer…

“give me an example where you gave up a $200k gain”

I’ve probably given up twice that much bailing out family members and old friends. Also ex-girlfriends, through church groups and lawyers, because they’d be devastated if they knew where it was really coming from.

If you’re a libertarian you’ll have to confess your sins to somebody else because I’m way over my limit here and don’t have that much time to give you.

OK…

You called me on that one…

Other than family, dammit….:)

Got burnt on that one myself…

The people living “somewhere else” have increasingly become meth addicts as there are are not enough manufacturing and resource extraction jobs there. The marginally employed in the cities and burbs are steadily being squeezed out by increasing business automation.

An excellent excerpt from the heartwarming tale of how rich people must be supernaturally terrified into sharing.

Sorry, just had to comment, I’ll go back to watching the show now.

Any supposed housing shortage can be resolved by the bursting of housing bubble 2, the one occurring now.

Let’s the 30 year mortgage rate reaches 8-10% and then we’d see there are no housing shortages but housing glut.

For a lot of people/investor, if the rates are high enough, they’d bail out on being a rentier and see yields somewhere safer/less hassle.

Just based on the charts posted, and judging by the early 2000’s overbuild (the chart only goes back to Y2K, but is in dramatic overshoot that entire time, moreso than now), this could go on for years and years. So something may have to give, but it might take a long time.

Usually real estate goes in 18 year cycles…..so if the last cycle building peaked in 2005-2006 then the next building cycle should peak in 2023-2024. Usually prices start to fall after….

I suggest we end all immigration until we have affordable housing.

1) Something have to give. For entertainment only. Competition and high oil prices sent Netfix 25% down in AH, dragging Disney and Roku down. Covid era superstars are bleeding in the cage : down from 700.99 in Nov 17 2021 to 258 in AH.

2) IBM Ginni Romantica upper cut sent Warren to the canvas.

3) IBM two years triangle is centered around the Anti BB :

129.99/ 120.69, from Feb 28/ Mar 3 2020. It’s 131 in AH > the Anti.

Those interested, there is a Zero Hedge article depicting BlackStone’s continued expansion of ownership in residential housing….now they are going after student housing.

And though the housing ownership is moving from one housing entity to another, the concentration is of note and, IMO, one designed to corner rent control in certain areas.

h,

There is a certain faction that will *always* rent…

You suggested one, student housing… wasn’t it a thing a while back to buy while the child was in school, then rent or sell afterwards…

Another rental market that companies are going after is the military… These folks are PCS or TDY for 6 mos to two years… doesn’t make sense to try to buy…however, companies will buy a SFH, refurb it to upgraded standards, and look to rent it in heavy military areas…

A mid grade enlisted with family will receive appx $2000 a month for housing allowance…

Service member gets a nice place to live, company gets ROI….

I don’t see that as a bad thing…

A mom and pop is not going to buy a SFH and put $60k refurbishment in it to rent it out…

Do you think?

Many companies also provide 24/7/365 service technicians for any problems…

I guess I’m long winded saying sometimes a rental from a company can be good…

Blackstone paid a HUGE premium over the all-time high of the share price to buy the shares of the student housing developer and manager. This was a take-private transaction of a publicly traded company with OPM (other people’s money). Student housing is one of the most troubled housing segments. Blackstone is making some really stupid moves overpaying ridiculous amounts to buy out other companies.

US imports a LOT of college students.

Blackstone will probably bundle the debt into a MBS or equivalent and sell it to some investor. The stupid move will be the investor that buys this stuff.

Blackstone will make a lot of money off fees. I agree this is a stupid move if you hold the debt but if you make money on the deal, transaction, and fees. Good for Blackstone?

Then again. The bigger you get, the better chance you can qualify for TBTF? Buy, Buy, Buy Mortimor.

I hope Blackstone goes bankrupt

One bubble (college tuition) feeding off of another one (housing).

The student tuition bubble isn’t sustainable either, whether there is mass loan forgiveness or not.

This should be obvious as no “industry” can perpetually price out a substantial proportion or majority of its “customers” forever, especially with decreasing ROI as the economic value of many or most diplomas decreases.

Everyone is citing Boise as the canary in the coal mine, and while that is true for the top 100 markets, I live in a market that is even more ahead of the curve. I live in Washington County, Utah. It has roughly 200,000 people, so not a huge county, but it is just big enough so you avoid most, not all, pitfalls to living in a small town. It’s in the far southwest corner of the state and it was the fastest growing place in the country between mid 2020-2021 — in other words, proportionally it was the top destination for people migrating due to the pandemic. There could be some smaller counties in Montana or something that grew faster, I don’t know. This place started taking off late spring 2020. The price increases were GREATER here than Boise, which is really saying something.

Looking at the inventory now is illuminating. If you adjust for population, we have 2x the inventory as Boise. Compared to Maricopa (Phoenix) and Clark (Las Vegas) counties, we’re close to 3x the inventory. Additionally when looking at overall inventory (not vacant lots, actual dwellings) and the ratio between all units and those that are NOT pending, less than 30% of the units are under contract. By contrast, 2/3 of the inventory in Maricopa County and Boise (Ada County) are pending. I’ve looked at suburban counties in Dallas, Oklahoma City, Indianpolis and in California and they’re all around 2/3 under contract.

The only county I found with similar stats as mine regarding the pending/not pending ratio is Pinal County, AZ which is an extreme exurb of Phoenix. These are the types of places that got hammered the most during the 2008-2012 housing bust, they’re also the places which first started showing declines. For those in SoCal, think Lancaster and Victorville.

During the last meltdown, inventory in the greater Phoenix area rose to staggering levels, and hardly anything was moving anymore. It was truly like the music just stopped and there were tens of thousands of houses on the mls with no buyers at all. It seized up. And it happens while people are still drinking the Kool-Aid, like right now.

I bought my first house, which I just sold last August, back in late 2008. We avoided 2/3 of the decline, but not the last 1/3. Luckily, we insisted that we buy a place that was big enough to handle more children, we only had one at the time. So, it wasn’t really a starter home, more like the second home you buy on the way to your forever home.

If I had waited just one more year, it would have set us up on an entirely different trajectory. The thing was, I was an early proponent of the idea of their being a housing bubble way back in early 2006 shortly before I got married. My wife and I held off. I still remember reading an article out of Florida around March 2006 regarding a house flipper lamenting that they didn’t get 50% appreciation over the course of six months of ownership. I knew housing was hot, but since I had never seriously inquired into buying, I didn’t realize the extremity and I soon found out that people were taking out unconventional ARMs. Then I realized the only reason for these crazy loans was because the affordability wasn’t there and they needed some way to meet speculative demand.

I saw many similarities here as what I saw 15–16 years ago, that’s why I sold and DID NOT buy. Instead of crazy loans, instead we had record low pandemic rates coupled with PPP loans and an insane amount of liquidity sloshing around the market.

The list prices here are totally unhinged. There’s been a flurry of building in the least desirable town in the area and the people living there must be suffering from group psychosis. Some of these idiots are listing their homes at $400 a square foot (i.e. 2,500 square foot homes for $1 million). Look at okay suburbs of LA, e.g. Santa Clarita. I see homes on view lots, with pools going for less than that a square foot. We don’t make LA money.

Over half the inventory in that town (Hurricane, UT) is over $800k. Of the roughly approximate 90 homes for sale in that range only 10 of them are under contract. 12% of the homes being under contract doesn’t indicate that housing is moving.

Needless to say, I’m seeing plenty of price drops.

I lived in Phoenix on two occasions between 2001-2011 for eight years.

I consider most of the metro area either mediocre or a dump.

Yeah I’m wondering if the truly loser no interest towns will get taken out back like last time. Denver sucks big time. Phoenix sucks big time. Vegas sucks to live in. All of them and more got flogged last time around. Meanwhile cities with true value and not trendy western cities faired the storm well enough. Say Seattle, Portland, Frisco, LA, Atlanta, NYC etc.

I look at my local market (Spokane) and realtor shows Pend O’Reille county, WA as like 50% yoy. Northern Idaho has had consistent 20-30% yoy gains for nearly 3 years now.

What is to the north of Spokane? The world biggest trailer park, a gas station casino, and deep snow for 6 months out of the year. Yeah a single wide is 300-500k there.

What of Idaho?

-Off the grid privacy

-Road maint. is non-existent so you don’t have to worry about those evil gov-mint folks monitoring you.

-Enough mining waste and superfund sites to give you super powers and a third nut.

-No internet access that way you won’t be corrupted

-Snow deep enough to make a fallout shelter from

-Some random Canadian guy to tell you that he isn’t your guy, buddy.

All for the low, low sum of 750k for a crappy starter home where every corner was cut. Buy now or be priced out!

I can’t help but think of all the cities I’ve been, it’s always the lamest ones peaking the housing bubble right now. Boise? SLC? Phoenix? They’re all so unbelievably terrible compared to real major cities. They have all the downsides of small towns and the downsides of living the city life. At an unaffordable price. What’s not to love?

If I had to live in a major city it would be one with actual opportunities, jobs, and uniqueness like Boston or SF. Not ABQ or Billings lol.

I live in ATL now. It’s my second time here totaling about 28 years starting in 1975.

Housing is still relatively affordable but no longer cheap and neither are rents. It’s got a lot of nice or really nice areas but more dumps too.

Like about the entire I-20 corridor, 2/3 of what used to be the perimeter (I-285), and most of the section south and west of downtown. Downtown isn’t very nice either which is a charitable description. It’s an arm pit like the other areas I just listed.

It’s a lot more congested now too (absolutely sucks), with about a 4X population increase since 1975 to about 6MM. The culture has changed noticeably too, which some may like and others not.

If you can tolerate the climate, Atlanta is okay. Wages are depressed but you can live in a major city and get a metropolitan lifestyle for a more affordable rate than pretty much any other part of the US, definitely the West. Rent in the CDA area in Idaho is on par with Atlanta but CDA is smaller and lamer than Conyers. It doesn’t even compare to Lawrenceville. Spokane is comparable in feel to Athens but the same or more expensive than Atlanta.

And yes, in the past 10 years Atlanta has changed a huge amount. On so many levels. Really the past 5 I noticed it. But then again, the US has also changed a lot in that time frame.

I hate the climate, the poverty outside of Atlanta, and the crowded nature of the East coast. I’d never go back to living in GA or the east coast in general but it may fit some people’s taste. But in general I like east cost cities a million times more than the west. NYC vs LA, I’d take NYC 8 days a week. Lower profile cities change it a bit but city life in general isn’t for me. If I was retired I’d live in Alaska, South Dakota, or Wyoming.

The north to NW corridor is the most affluent part of ATL, along with Midtown, Buckhead, and east up to Decatur and Druid Hills.

The other areas I specifically listed in the suburbs are poor to working class, especially south of town in Clayton County. Inside the city limits south and west is poor or really poor too.

I also hate the summers here. It’s too hot from about May to the end of October.

Trucker Guy:

Portland is a real city? Good lord. BTW, the crackerbox I lived in back in 2002 has now eclipsed $1.2M….. Dysfunctional coconut city government.

BTW, how do you define “real cities”? You claim PHX is not a “real city” but is the 5th largest metropolitan area in the U.S.. Jobs? Take a peek at what’s going on in Chandler, AZ.

I’d define a real city as having all the amenities of a unique metropolitan area, a competent mass transit system, decent or tolerable weather, diversity in everything, from things to do, see, shop, people, etc. Somewhat tolerable vehicle infrastructure, and have a prosperous job market.

Phoenix has endless congestion, an extreme affordability problem, one of the worst climates in the US, and is boring. The job market is about the only positive to the area.

Phoenix feels like it just was Albuquerque that got lucky and outgrew itself before it could scale to the growth. It’ll get there one day maybe but the last time I was there (2021) it was a miserable experience. It feels like a complete suffocating rat race. I couldn’t imagine living there.

It’s all opinion at the end of the day but I’d take Portland a thousand times before I lived in Phoenix. Or God forbid some place like Austin or Baltimore.

Phoenix was more like a large town when lived there. Doubt it has changed much.

The congestion was much better than ATL due to the better road layout, but I commuted in the NE part of the valley or from NE to NW most of the time, not from N to S or on I-10.

TG,

True about Denver. I lived there from 2004 – 2018 and watched a substantial negative change in the city over that period.

Denver was still a “net positive” (for me at least) until after the passage of Proposition 64 (marijuana legalization act) in 2012. It was all downhill from there.

That change brought a FLOOD of people into the state and the traffic situation went from bad to ridiculous. Not to mention the cost of living. I would not live there again. Visit yes, live no.

Trucker Guy

Read your comments with interest. I think it goes to show that beauty really is in the eye of the beholder – and perhaps beauty is what you are familiar with (prefer).

I grew up in / around arguably one of the most cosmopolitan and pretty areas in the US (MSP area). Went to college there and left as soon as college was finished and moved to So Cal and then AZ (East Valley) – now in the AZ mountains (Prescott). Every place I lived in the SW USA has also had culture / arts / fun.

LOVE the Midwest and especially MN, but if weather and open spaces are your triggers, the SW USA is the best. PHX has some of the best free hiking and the largest city park in the USA (South Mountain Park). It’s hot in the summer but everyone lives poolside June-Sept. I could obviously go on, but I have visited and/or know folks in many of the places you cite and none of them would be interesting to me as a place to live – because it’s COLD there. ;-)

Interesting observation, Trich. Thanks for posting.

I grew up in Utah and am quite familiar with both your area and Idaho. I’ve wondered what happens in Idaho when the people who moved there from where I live (SoCal) experience a winter – which, especially in eastern Idaho, is exceptionally harsh. Will they stay or bail after a couple of years?

Similar could be said about your area, only in the summer. Will they stay after a couple summers of 110 all the time?

Personally I think a majority will look to somewhere with a more manageable climate (Boise isn’t too bad, SLC isn’t too bad either except for the pollution in the winter).

Most of the California types that have flooded CDA and the surrounding area are very, very right wing retired military/police/fire fighters etc. The old timers tell me everyone thinks winter will run them off or hopes so but it doesn’t typically pan out.

Idaho hasn’t had a loss in population in 30+ years. The climate in the panhandle is very mild and if you state west of the MT state line winters aren’t harsh at all imo.

Most of the people going to Idaho, at least up north are going there for political reasons and to cash out of higher expense areas. I’ll say I’ve been coast to coast in the US during the 2020 election and Eastern Oregon and North Idaho have by far the most weird militant right wing political vibe. It didn’t have it as bad a few years ago. It’s like what I would hear about in the 90s during the neo Nazi ethnostate they were trying to make up here and the ruby ridge incident. The Nazis are still gone (to Eastern Oregon) but the right wing doomsday survivalist crowd is unlike anywhere I’ve ever seen.

So in short, I doubt some cold weather and snow will drive the current crowd away.

Harsh inland winter? They are probably boomer retirees getting a couple of govt checks so they will just load up the 6 mpg 35′ motorhome (foo foo doggie on the dash, blue hair in the passenger seat, toyota in tow) around October and head south to their second home or condo.

That actually sounds pretty good! The desert south west is beautiful from October thru May.

Or “mark-to-make-believe”

Sorry meant as reply to Wisdom seeker

I totally agree with your conclusion in the last paragraph, and I appreciate the way you used facts and graphic presentations to take the readers through your thinking.

Great job on the article.

It is my opinion that the 2017 tax law put “real estate developer tax cuts” into law that has incentivized large corporations to buy up property, rehab them and then ask outrageous prices for them.

Because of the tax law, they can let the properties sit vacant until they get their price. This is a revival of the “tax shelter laws” that were abolished years ago. The cost of maintaining the properties can be used as a tax deduction to shield other income from taxation. They may never get their price, but they don’t care.

Apparently, Trump liked the old tax shelter laws.

Anyway, the recession created a lot of opportunity for big corporations to scoop up a lot of properties at low prices. They were already doing this for a couple of years, but it accelerated recently.

The acceleration has been so profound that it has caused an affordable housing shortage, despite a building boom.

Maybe some bohemian playwright will write a play about homeless people living under a bridge at the end of a street full of sparkling, and vacant, housing.

I’m not a RE or housing expert; I’m a financial/operational auditor. I see real estate assets sitting around in blighted condition, with low occupancy, in good locations, and in communities that bewail the lack of low/middle income housing.

I live in Cottonwood AZ. Sedona, to the north won’t build housing for workers; Camp Verde to the south is too far away and offers only low income housing.

A typical Cottonwood block has 8 0.25ac lots on the corners and 2 1ac lots in the middle with an alley running lengthwise. Most of the 1ac lots are either bare or have a 75yo block house.

Subtract 10 years of age and provide a modest line of credit and various local problems can be solved.

To what degree have corporate buyers of residential real estate impacted the market and available inventory? I’ve read that in some markets corporate buyers are snapping up everything, and then sitting on them to drive market prices higher. Also, what about the impact of boomers moving on to assisted living and such, shouldn’t this be an offsetting factor as more and more boomers transition from their home into other accommodations as required by changing health and mental fitness?

National Public Radio did a documentary news story about this recently. My opinion is that the 2017 tax law, with it’s provisions for real estate developers, is the cause of this problem.

It can be fixed. Vote for Democrats.

Politicians are always the best solution. ;-)

One well-known internet financial site is saying the average 30-year fixed mortgage rate is 6.4%, based on 20% down and 700 credit score. Other venues are saying the 30-year mortgage rate is around 5%. Not sure why the differences result.

If the rate is closer to 6.4%, that’s going to severely restrict housing transactions on the coasts. In my area near Seattle, the average home price jumped up to $1.6M. The mortgage payment on that is well over $10,000/mo. If you household isn’t bringing in $350k or more, it isn’t going to work.

Even at a 5% mortgage rate, the payment looks bad. Many of these houses requiring $10,000/mo. mortgage payments can be rented for $3500/mo.

If you can afford a $10,000 per month mortgage, you shouldn’t need a mortgage at all. Things are really screwy.

It’s right near 5% which given the price run up over the last few years, is already enough to noticeably increase the monthly payment on a 30YR fixed.

Property taxes on the coasts are prohibitive. And if you have a HOA or Co-op, its suffocating. I don’t know how anyone affords to even heat and cool their giant houses, and the taxes skyrocketed again this year.

Friend of mine pays more than their mortgage premium just in taxes and co-op fees, for a small, no frills 2 BR, can’t even have a dog or put out holiday decorations. Neigbors breathing on their neck. Never could make sense of that math, throwing housing money to the breeze to live in a sardine can.

Is anything in your comment even remotely true, or are you mistaking this for a QAnon meeting?

Are you mistaking the comment you intended to reply to? Otherwise you’d be hard pressed confusing me for a Q but go on.

Contributing to the problem are zoning laws that only allow SFHs to be constructed. In my old neighborhood, they only allow $1M mini-mansions to be constructed. The mini-mansions are huge, yet occupied typically by only a family of 2-3. The only option for the builder is building a mini-mansion due to the value of the land. But why not a duplex ($500K ea.), or a quad for $250K each – same money in the end. Such a waste of highly desirable land that is close to employment centers & public transportation.

I doubt any owners of $1MM homes want to live next to a duplex. NIMBYism.

“But why not a duplex ($500K ea.), or a quad for $250K each”

Probably things like infrastructure (existing sewer system old and treatment plant under sized for additional dwelling units), increased consumption of government services (school capacity, police, fire companies, etc.), water mains (additional units lower water pressure), traffic on over taxed arteries, parks and recreation, etc…..

Many communities were developed multiple decades ago and the infrastructure underneath the streets is old, in poor repair, and undersized. That’s why green field developments are usually cheaper. Imagine the main traffic arteries in your community losing two lanes to construction for years as they upgrade water and sewage. I live in the sticks and our local water company has been expanding the pipes for new development for nearly three years. The funny part is that the expansion only required an extension of less than 2 miles.

If you do a search, you’ll find that metros like Boston leak millions of gallons of water per day because the cost to repair the mains exceeds the monetary value of the water. Chicago (per an article published in 2014) loses 22 billion gallons of treated water per year.

These “how comes” are often not well thought out. Nothing is ever as simple as people think it is. You can’t build a 4 plex on a residential lot for the same money. The 4 plex likely requires 4 water taps (onto the main) and four individual sewer taps. It’s why they limit the number of residents based on a bedroom / bathroom count. If you’ve ever owned a house on a septic system, you’d understand the concept. Once the limits of the systems are reached, the effluent has few places to escape… and often it’s into the dwelling or it floats up to the top in your yard (flooded leaching field). Now price the cost of the taps… city permits, street repairs, cost of city workers to complete the taps, fees…..yada yada yada. Or build one home and avoid all the nonsense.

We have a neighbor who is trying to develop 37 lots on a parcel adjacent to our community. He shrank the size of the development (it originally had condo buildings in addition to the homes) and the county is making him completely redo the impact study. He has to pay for the evaluation of the water supplies for the new development as well as measure the impact on existing developments. He has to bear the cost of that. The upshot is that he has to guarantee that there is a 100 year supply of water available to his new development or there’s no permit and the value of the land he bought becomes in peril.

In Orange Country I’ve recently begun to discover more and more people who own multiple homes. Just within the last few weeks I discovered 2 (that I know of) of my 5 neighbors in the cul-de-sac own 2 other homes and are renting them out.

When prices drop, I guarantee one will be a seller at the first sign of an actual downturn. The other will likely hold on for a bit, but will sell if prices are really dropping. Neither of these people are wealthy with high paying jobs. They just picked up homes when prices were lower.

I’d say there’s a good chance many people around us are in similar situations. If they begin to see their paper net worth dropping, homes will come out of the woodwork and hit the market.

Most people think that home prices just can’t drop, but also think the stock market is going to crash. I ask them “how many crashes have you experience when everyone is looking for a crash?”

To me this is just more evidence that the housing market is likely reaching a top while the stock market has a good amount higher to go.

Housing (of some sort) is a necessity, but the stock market is a much bigger mania than housing is in a bubble.

Housing bubbles are local. People can move if they can’t afford to live locally. Not every stock has mania (or even bubble) valuations but there is no precedent where the major averages crashed and “cheap” stocks didn’t fall noticeably. It’s not going to be any different next time.

There are very few who really believe a stock market crash is coming since blogs like this one are not representative of the population on this topic. It certainly isn’t those who own stocks now.