In a world where valuations are irrelevant.

By Wolf Richter for WOLF STREET.

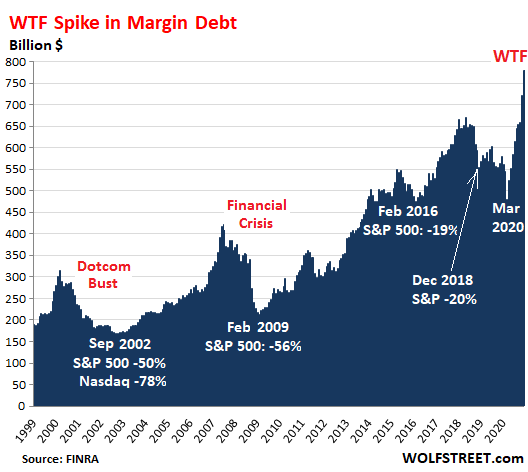

Margin debt – the amount of money that individuals and institutions borrow against their stock holdings – spiked by 56 billion in December, after having already spiked by 63 billion in November, by far the two largest month-to-month increases on record, to $778 billion, according to FINRA which regulates brokers and exchanges. Since March, this measure of margin debt surged by nearly $300 billion, or by 62%.

Margin debt as tracked by FINRA at its member firms isn’t the only form of stock market leverage, but it’s the only form that is disclosed monthly. There are many other forms of stock market leverage by institutions and individuals that are not disclosed, or are only disclosed voluntarily in SEC filings by the brokers and banks that lend to their clients against their portfolios, such as “securities-based loans” (SBLs). We don’t know how much total stock market leverage there is, but margin loans indicate the trends, and we had another WTF moment:

High margin balances tend to precede epic stock market sell-offs, as annotated in the chart above.

With these two-decade charts, the long-term changes in the dollar amounts are less relevant since the purchasing power of the dollar has dropped over the period. But on a short-term basis, the movements are very indicative about rising or falling leverage in the stock market.

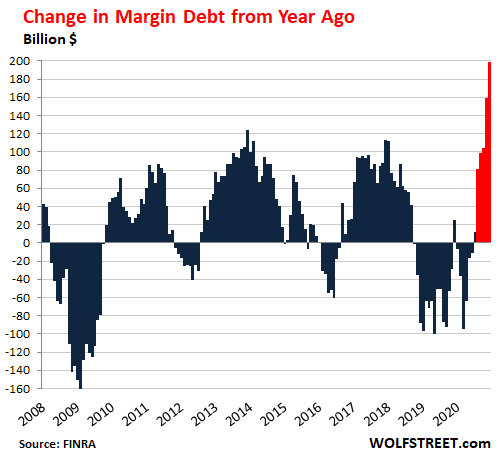

On a year-over-year basis, margin debt surged by nearly $200 billion in December, by far the most ever:

Stock market leverage is an accelerator. When stocks already rise, and investors feel confident, they borrow money to buy more stocks, and they can borrow more against their stocks because their value has risen. And this additional borrowed money is then chasing after stocks and thereby creating more buying pressure, and prices surge further.

And stock market leverage is an accelerator on the way down, when stock prices are already falling and brokers issue margin calls to their clients that then have to sell stocks to remain compliant, triggering a bout of forced selling, and many leveraged investors sell ahead of margin calls in order to avoid being forced into selling at the worst possible moment.

This spike in margin debt over the past few months is another sign that markets have gone nuts, and everyone is chasing everything, regardless of what it is, whether it’s a penny stock with a similar name to something Elon Musk mentioned in a tweet, or whether it’s Tesla’s stock itself, or any of the EV makers or presumed EV makers that might never mass-produce EVs, or a even legacy automaker that is now touting its EV investments, or whatever it is, including Bitcoin – which exploded higher, before plunging 28% in two weeks.

Everything is getting chased higher by speculators who are totally indifferent to valuations, who focus only on the fact that others are chasing these things higher, and valuations are irrelevant, and some of this chasing is happening with borrowed money, from regular margin debt all the way to borrowing against the home or credit cards. That’s what this surge in margin debt tells us. It has gotten crazy out there.

Lenders that funded apartment buildings are getting nervous amid dropping “physical occupancy” rates (tenants living in the apartment) and even lower “economic occupancy” rates (tenants actually paying rent). Read… Eviction Bans, Surging Apartment Vacancy Rates Trip up CMBS Backed by 43 Apartment Buildings

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Buy high sell low… or something.

It’s really a game of hot potato. As long as you aren’t holding it when it blows, you win big.

If however, you are an average worker who has someone else handling their money for them, well then, you are screwed; Some currently retired and soon to be retirees, could potentially still be in luck if there is one more big wave of stock highs. It cannot go on forever though.

I have a friend who stayed in the market until he reached 65. His plan was to retire as soon as he could get Medicare. He had arranged his mortgage to be paid off by retirement. However, he never recovered from the last stock market drop. He had taken on a lot of debt by cosigning for $150,000 in college loans. When 65 came, he did not have enough money to retire, so he had to keep working. He is in poor health, but still has to go to work every day. He is 70 now. Not exactly the retirement he dreamed of. If he had stayed out of the market during his later years, he would have his savings. Instead, he had put it all in the Wall Street Casino.

Terrible story, roddy.

I can fathom (never condone) the idea of borrowing money against firm assets for golden opportunities. (cough cough). I can see lenders issuing credit against firm collateral, say house equity up to a certain percentage of the current market. BUT lending money for stock purchases based on the value of other market holdings? Really?

I have a friend who stayed in the market until he was in his early 60s. Back when we were still talking he told me that he just lost 15K on a recent stock purchase, and an additional 35K the following week. He also went on the explain that he had chosen a new investment advisor, a golden wonder who only takes on clients with excess of one million in their portfolio. In my friend’s case they were going to make an exception and take him on as a client. My jaw dropped and I almost crushed the phone, but being a polite Canadian I simply suggested there might be a wee bit of grift going on. That’s one reason why we don’t talk anymore. The other was when I said he was not an epidemiologist despite what his Facebook friends all believed about the virus.

I’m wondering what contribution Social Media is making towards this market irrationality? We know what it has done for politics. We know what it does for the ‘dining experience’. We know what it does sharing misinformation about everything and everyone. It seems likely it has an additional influence upon low interest rates and vaunted returns..

re: “In my friend’s case they were going to make an exception and take him on as a client.”

Wasn’t that Bernie Madoff’s shtick?

Cosigning for college loans? Were they off the track colleges? The gov is on the hook for most defaulting ed loans.

And the collegecasino.Student should have worked two jobs,saved almost all while taking free classes,community college classes and other educational options.Then s/he can test out of some pre-reqs. And sail through other courses because the earlier free or cheap ones wouldve laid the foundation for credit courses.Moocs,Tedtalks,Gale ed. Courses,Coursers,you name it.I never wouldve expected or wsnted my parents to cosign for such a huge amount unless I was in Great heslth,was supersmart,and was going to br a surgeon or some other highpaying,in-demand mega earner.Sad!!

“It’s really a game of hot potato. As long as you aren’t holding it when it blows, you win big.”

And that’s all you need to know about the stock market.

But many who jumped in the market now hope that it will give them a ticket to early retirement. (A colleague at work just revealed to me that he is buying stocks now and that instead of the weekly poker games with his pals, they now have a stock discussions group on the Web.)

Right, at this point, it’s functioning like a pyramid scheme. The problem is, statistically, the bottom of the pyramid is always going to be the biggest, meaning that the vast majority will end up holding the bag when it blows.

I’ve written about this before. Any selling pressure would cause prices to drop, so everyone is only “rich” if they don’t try to actually cash out and do something with that wealth.

hernando,

If you sell high and buy low long enough you will run out of fiat fuel.

‘Apple and Tesla’s earnings key to next week’ CNBC

Jan 22

How weird to see those two lumped together. A cash generating machine and a cash burning machine.

At least CNBC didn’t say ‘profits key…’

If you know for sure that the Dow will be at 10k a year from now what’s the best way to profit from it?

Short the S&P 500 ETF…..but I would wait for a trend change.

exactly, wait for it…..yellen-powell will not be easy game to short

even volatility players tend to jump in too early with those stupid leverage instruments, the research I’ve done is you can get in after it starts and profit well, avoid geting trapped and let the leverage and front month futures price fix accelerate the move…..

but we are close to 10% correction at least…..Bitcoin is front running the move…

I’m not sure I agree. Powell is out of tools, and has been for a while. All he has now is jawboning. He’s already agreed to “unlimited” QE. What more can he do? Congress is not going to allow him to buy stock, and the only way to do more QE at this point is for Congress to spend more.

Shorts have been pounded (including myself). I am starting to believe this bull still has fuel. There will be volatility to trade, but I hate to say it – the market will continue to rise.

1) Rates can’t go much higher, but they can go lower

2) Equities are an inflation hedge

3) Fed backstop

4) Market consolidation

5) Buy backs might start making a comeback.

ers, once everyone capitulates is usually when we’re near a top.

To address your points:

1) Not with the amount of new spending being projected. The global markets are already signaling alarm with our levels of printing and spending.

2) For a small amount of inflation, maybe. But inflation ultimately decreases demand if there isn’t a corresponding increase in wages. That hits company profits.

3) There is no Fed backstop. There’s just the perception of one that causes investors to throw caution to the wind.

4) Can you elaborate?

5) Maybe, but many companies are already leveraged to the hilt. They have already borrowed up to the value of most of their assets in the first 10 years of ZIRP.

Three timeless tips from Warren Buffet:

1. Never risk being out of cash

2. Never short stocks

3. Never use margin to buy stocks

Those are simple rules to keep the average Joe out of trouble. Doesn’t mean you can’t take the risk and escape the lion’s mouth.

first advice is funny because he used margin to generate his returns, with the premiums from his insurance business. That’s not broker margin though

I think “The first billion is the hardest” was his ONLY honest statement. He is nothing but an disgusting old financial pirate, masquerading as everyone’s kindly old money wise grandpa.

Dow from 30k to 10K?

Open a soup kitchen. It will be the only way to profit from the misery.

You mistakenly confuse the DOW for the economy. It’s not.

It’s not on the way up. It is on the way down.

Auld Kodjer,

Or stake out a corner from where to sell apples from an apple cart.

“Can you spare a dime brother?”

Short Dow futures, buy OTM puts.

1) Bear call spreads (Sell at the money call & buy insurance Far out of the money call )

2) Bear Put spreads ( sell at the money put & buy a lower strike put)

3) Strangles/ Straddles (sell at the money call + sell at the money put ) (buy otm call & put as insurance)

4) Futures+ protection ( sell futures + buy out of the money call as insurance / Buy futures+buy out of the money put )

5) Buying naked puts hardly makes money (only sellers make money mostly)

7.If you want to bet trading SPY/DIA/Russel 2000 etfs. instead of short selling etf, sell options at the expected down strike. if the price falls to that level , you will be short at that strike level (premium earned is keeps as your cushion) for example say S&P is now 3800 , you sell monthly option 3600 (360)strike , you will be short at 360 if price falls to that level.

8) Help support the financial economy’s exchange and broker fees by trading a lot. Because they’re so hard working.

Where is Dow now?

Dead, but immortalized digitally amongst trading computers, along with Jones.

Memento mori,

You either buy in once it hits bottom. Or you can ride the waves, trying to buy and sell as the stock market goes up and down, this is very risky and difficult to predict though. Alternatively, you can buy things such as precious medals or other assets that jump up, as stock market goes down.

A person that can read the indicators well, would sell off most stocks once they are about to fall. Storing that money in precious metals and other assets that people will flee to as stock market actually falls. Then once stock market bottoms out, sell off precious metals and other assets and buy back into stock market.

Some stocks will do well as most free fall. Never buy paper gold. Small people have to buy the real thing at nearby locations and have to find a place to store it (possibly savings deposit box at a well performing local bank) or inside your walls (way easier than sounds).

In my country Silver future in recogonised commodity exchange (silinar to CME/LME)trades in 3 sizes : Silver Micro 1kg/ Silver Mini 5kg /Silver standard 20kg denomination

I buy 1kg physical silver daily or weekly in cash at wholesale market (brand /specification that can be delivered against short futures to the commodity exchange if neccessary)

If the price goes up too much in 24 hours , I short paper Silver Micro Futures (1kg Silver ) & lock in short term profit or sell weekly/monthly call options against my physical silver & eat the premium . Same way I buy 1kg silver futures if it is going down as a averaging ladder (instead of buying 5000 ounce Silver contract all at once) and doing some what ok. {watching &trading paper silver from 8.30am to 23.55pm at my exchange. physical buy/sell visit wholesale market only when the market is at extremes.}

Buying silver 1kg brick =can pay cash.

Gold the investment is high for a 100gram 999.9 purity exchange standard bar or 1 kg bullion uk/swiss /australia/Southafrica numbered bar. I never deal in collectibles.

If you get a massive stockmarket selloff, the price of gold is likely to fall too, because it will be used to fund the margin calls on stock portfolios. We saw that in 2008 and 2020. It recovered quickly afterwards, but it doesn’t protect you well on the way down.

You absolutely need gold as wealth insurance. But only buy what you could afford to take a hit on. And then hold for the price recovery that, in todays environment, will come. But we on this site know that.:-).

Or Thomas, you can go to the local Stop and Go and buy the new lotto ticket. But only do it when your lucky numbers are going to be drawn. That’s what my tenant does. He says he’s giving me half.

Paulo,

If you have money saved up, where you gonna put it?

Thomas, not in overpriced stocks, that’s for sure.

reply for Thomas comment as seen down below.

I do have money in the bank and plan to buy my neighbour’s place when they sell and move. He is 94 and she is 86ish. We have first dibs, supposedly. I consider RE in our area to be a solid investment.

Years ago we sold our house in town and had money left over. A sweat equity gain. We bought 16 acres across the road from us which coincidentally is zoned residential. We paid 200K for it. People laughed at me as they thought we overpaid, not realising it was zoned residential, and the last decent sized piece around.. Now, it’s “oh, I get it”. 1 acre lots around here are going for just over 100K. Pretty simple math, but my kids will be getting it as we have no reason or desire to subdivide. I built a rental on it and the rent pays all taxes and insurance, for our own house as well. The neighbour’s house is basically a shack, but it’s certainly modernized and rentable. It requires painting and some upgrades, all of which I do myself. (carpenter) We will offer a good deal for a quiet renter that fits in around here. There is a jerk who moved in down the street who plays drums. We can’t hear it but his widow neighbour has to wear earplugs when he starts drinking and pretends to be Ginger Baker. If that happened to us I would go nuts and likely worse. Regardless, the rent will be in the neighbourhood of $1,000/month. It’s a pension add on.

My son is doing the same thing at age 37. He cashed out stocks this December to buy a house, his second. He owes a lot but his renters mostly cover all expenses including mortgage and taxes. The renters move in next week. He came down $400/month because they are really really good tenants.

Paulo,

That might work for you, alot of people in my family own a lot of real estate in my city, so I’m very familiar with everything related to buying and managing real estate. Not everyone can deal with real estate though, there’s not enough to go around, they don’t know how to deal with it, they lack the time, they don’t have enough money to get into it, or their local real estate market is not investment worthy.

For the general population, there are only a limited types of ways to store money. Stocks, bonds, cash in the bank (savings or money market), precious medals, commodity futures, maybe real estate, or somethings less scrupulous. What would you recommend for a person not capable of putting it in real estate, at this exact time? Right now, I’m recommending, cash in the bank (Warren Buffet method) and precious metals.

Paulo once mentioned here that the hard core survivalists up his way prefer to “invest” mostly in .22 bricks.

A pretty obvious choice, to me, having grown up mostly mountainous rural.

ALL security experts measure security in TIME.

Momento mori

‘A person that can read the indicators well’

Those ‘indicators’ are INOPERATIVE since free mkt capitalism has ceased to exist since March of ’09!

Stocks have remained in over valued territory over the last 3 years, (thanks to 3 trillions bailout last March)

Mkt cap to GDP is over 180%!

DEBT to GDP is around 120%+

Last year’s S&P earnings was NEGATIVE 14%!

Now FED is the mkt and everything else is moot!

It doesn’t matter what kind of indicators they are. If a person who plays the stock market can figure out whatever signals the market has peaked, free market or not, it still works. As for the stock market itself, the real US economy adjusted for population is probably smaller than 20 years ago, and the stock market has been a joke ever since. Anybody involved with the stock market in any way, is playing a game of shenanigans.

Thomas-hopefully an autocorrect error, but buying too-many ‘precious medals’ will have the same effect in reducing to meaninglessness akin to debasing ‘precious metals’ to a point of ‘non-preciousness’ (ref: U.S. ‘Presidential Medal of Freedom’ recently, 3d Reich military awards expansion less-recently, coinage debasement, governmental AND non-governmental back to it’s inception…). Ah, but we DO seem to love our awards, even down to a ‘participation trophy’ level.

(Gold bugs should hope that the unlikelyhood of fusion power never comes to fruition, if it does-now there’s a REAL ‘Philosopher’s Stone’…).

Sorry to rant, and-

may we all find a better day.

I wouldn’t actively short it because you bleed to death quickly if you don’t get the timing exactly right.

Cash (or cash equivalents) are not a bad place to be right now. Yes, you are bleeding slowly because of inflation and ZIRP, but you can see that as a kind of option premium: you are buying the ability to buy shares at much lower prices IF indeed the wheels come off at some point in the future.

Get a job working for the City of Chicago. They never lay anyone off, even if they are at home doing nothing.

SDOW – 3X inverse ETF

As long as the Fed printing press is working all 3 shifts plus weekends and holidays the Market will hit 40,000.

Or you can show some gumption and stand in front of the tidal wave.

Why 40,000 and not 100,000. Or more. The same logic applies

Memento……if you are positive……SQQQ…..but if you are wrong the zoo animals will be released to eat you

Fred is right!

The zoo monsters ( if you would’ve invested in SQQQ ) in March 2020 would’ve dined on your flesh ( and the bones!!).

Your investment would’ve been worth 0.08

Of its value . It is a zoo after all :)

SQQQ or any other Negative leveraged ETFs should be matched with positive ETFs like TQQQ ( proportionately) control the damage by daily decay. Until DIP buyers disappear, shorting without hedge is a dangerous game.

Those negative ETFs did wonders for me during GFC, when there was still ‘Free mkt Capitalism’. NOT any more under the casinos run by CBers!

Sounds kinda like you miss the old rule that the casino can’t work on a slot that’s paying off till nobody is playing it.

Maybe you can file a complaint with the Gaming Commission?

Actually, no.

You haven’t lost until you sell.

Average/double down Mortimer.

Ask any banks to sell u a put leaps on dji

Dow at 10K? Possible. This year? LOL. There’s a reason they’ve brought in “We Need to Act Big” Yellen.

It’s not just the stock market. Even the yield on junk bonds is getting lower and lower setting a record low every single time.

MB

Yellen is planning a takeover of BITCOIN as well :)

First threaten the holders that

“ it might being used for illegal- criminal actuality “

as if blind Freddy didn’t know that!

then squash its value to a %10 of its current value ( if it has any),

then called it a NEW NAME-

Say( American Digital Currency) or something like that!! :)

Cause nothing will be allowed to threaten fiat and de facto government control. If you don’t like it…. too bad. It may not be the dollar in the long run, or the yuan, or Euro, but no matter the form, it will be government controlled.

That’s scary. Hopefully governments don’t start undermining their own fiat.

MCH:

You mean “crypto” is not “fiat?”

If not, Please explain for me the difference.

Ralph,

Officially: Fiat money is a currency (a medium of exchange) established as money, often by government regulation.

Right now, cryptos, specifically Bitcoin is not regulated, it is a medium of exchange. The primary factor of cryptos not being a fiat.(I think) is the lack of regulation and control from a centralized source.

And that’s at least how I think about fiat. Another of what I consider non-fiat medium that would be similar is gold.

Ralph, the supply of fiat is virtually unlimited, while the supply of Bitcoin is almost virtually unlimited.

Crypto is worthless.

Outlaw BTC in the US, if your are caught holding i

t, you go to jail. That should kill that industry dead.

And I thought BTC was already illegal in China.

Yes, it is practically illegal in China:

https://en.wikipedia.org/wiki/Legality_of_bitcoin_by_country_or_territory#East_Asia

“the BIG BAD PANDA is the biggest baddest mining player”

That is wrong and baseless. Some Chinese startups are indeed in the mining game, such as selling mining equipment, but not the Chinese Gov. Why would it want to mine bitcoin? In fact, it introduced its own official digital currency.

Bitcoin and Ethereum are good ways to make a few bucks at the moment. It’s easy to go back in forth and out into cash. I rode Bitcoin up to 40k, sold into cash, bought back Bitcoin about 30k as it climbed back to almost 40k again, sold into cash. Now have Bitcoin (32k) with a stop loss at 29k. It’s kinda fun.

Brant Lee,

Just make sure you understand that a stop loss is only good in a slow and orderly decline, with lots of bids all the way down. If the price plunges because there are no bids around your stop loss, it will not execute and you wake up and you still have all your bitcoin but the price is at $25,000.

This is a feature of stop losses. They don’t protect you during a price plunge. They only protect you in an orderly market.

But in an orderly decline, your stop loss might have executed overnight, and the next morning when you wake up, all your bitcoin were sold at $29,000, and now the price is back at $33,000.

Those are the risks of stop losses.

I would add: the market must offer trades at EXACTLY your stop loss price, and there must be a sufficient number of bids at that price to execute your order.

Fear not oh humble Peebles, for the good news is, if the Mr. Market declines 10% or more, Damit Janit will up the WooZoo QE from $8 trillion to….$16 trillion….$80 trillion….?

Go Big. Or go home. Be somewhere or not at all.

Here is one thing I can’t figure out. The big tech stocks are momentum trades. How does the smart money beat everyone else out the door?

Before our 401k self directed option was taken away in December 2020, I spent the last 6 months of 2020 playing day trader with my 401k. I learned some interesting things. Since previously I had only ever invested in the sucker’s game which is index funds, I was not aware that there is a settling period for stocks. Plenty of times I bought stocks and then wanted to sell them the next day. I was not allowed because there is a settlement period and you can’t sell before your buy has settled, which can take days. A few times I was able to sell anyway and Fidelity gave me some nasty warnings that I was treading on thin ice. They don’t like floating transactions on little guys’ behalf.

Anyway I made 40% on my 401k in 6 months (wish I’d started in March instead of July, would have done even better!), then had to cash it all back in and return to index funds when my company took away the self directed option. Maybe I just got lucky but it sure was nice to do so much better than I ever did using index funds. I expect that I reduced my retirement age by 2 – 3 years just in those 6 months.

But I’m off track. What I meant to get at is, I learned that the notion of buying and selling on the same day in order to somehow capitalize on those crazy day run-ups that sometimes happen (I recall some Canadian cannabis stock doubling one day then going up like 60% the next but eventually falling back down pretty quickly) is kind of an illusion. You can’t really do it due to settling period. Maybe big players can do it via special agreements with their brokers but peons like me can’t.

Zantetsu,

The settlement issue in your 401k that you described — having to wait for days before you can sell a stock that you had just bought — must be related to a rule of your 401k. These are not day-trading vehicles. Most 401k plan don’t even allow stock trading.

But if you use a regular brokerage account, even an IRA brokerage account, you can buy and sell the same stock dozens of times a day. Once the buy order is filled, you can sell the shares again. If your buy order is “at market,” the fill happen nearly instantly (at whatever price). If it’s a limit order, the trade won’t fill until someone buys your shares at the price you specified. If that price is high, your limit order may just sit there.

If you roll over your 401k into an IRA next time you change jobs, you can turn this IRA into a day-trader vehicle, no problem.

No Wolf my Ameritrade IRA does not allow that. I get warnings for “good faith violations”.

Mmmm! I have had no trouble selling the same day what I’d bought earlier that day. And I have done it many times. That said, I don’t do dozens of rapid-fire buy/sells of the same stock in a day. If I did that, maybe I would get a warning.

I did it once and got a warning.

@Idaho

I think the rollover has to do with settlement dates on the order. As long as you have sufficient balance in your account you’re fine. That was at least the reasoning with some of the brokerages.

So, if you had a $4k account, and you say traded a share of AMZN 20 times a day, you need a margin account to do that… I think

Wolf is, or at least was correct for several ”day trader” friends who were imitating the big boys a couple decades or so ago.

Would buy early each day, then call all their friends to say which stock to buy that day,,, then start to dump as soon as their buying made them a clear profit,,, then buy in again when their dump drove down the price.

When one of my friends told me about their procedure, I begged them to stop asap, and, sure enough, other folks doing the same thing went to jail very soon thereafter, ( several for 15 years IIRC,) for ”rigging” the market exactly as is done exactly similar every day by the big boys and frequently their criminal cohorts in the congress.

No wonder that many if not most of our elected federal ”public servants” end their public service as millionaires.

”Clean House, Senate Too.” should be the mantra of all folks/voters of USA until we have at least a federal guv mint who will actually represent WE the PEEDONS…

My Fidelity 401K account gives me “good faith violations” warning if I try to buy and sell the same stock same day I guess.

Jon,

I had two 401k in my life, and NONE of them would ever let me trade in stocks. I could only buy one of the available funds. And I could not trade them at all. Long settlement periods.

If you have day trading status at the brokerages (with Margin)-, you can trade at will. If not, a non-day trading margin acct can have no more than 3 roundtrip trades with the same stock within a 5 day period. If trading with cash you can trade at will in your IRA that has no margin availability.

One can do option trading ( Level I) both ways in the same day, in an IRA, at SChwab and also Etrade without any restriction.

I use it option trading on DIA, SPY and QQQ, both ways.

NOT recommended for the newbies.

(Been in the mkt since ’82)

Usually 3 day settlement, unless you get a margin account. Even then you can only make 4 round trip day trades (sell/buy or buy/sell same stock) in 5 trading days, unless you get “pattern day trader” status, by having some minimum total margin account value. Violations got ya locked out for 90 days. At least that’s how it was at TD Ameritrade in ’07, IIRC.

No longer F with any of it. Was stupid to just fool around and lost some money, but not as much as I did in funds. All out around S&P 1400. But it was kinda cool to watch blown up screen after hours trading on one stock…much less action then, so you could see the bid/ask lines move along and then “pop”, a trade. Also big bill from tax lady that year. Friend of my mom’s, so she could tell me I was a dumb sht.

A retirement account must be a cash account. Good Faith Violation in a cash account means that you have sold stock A and used the proceeds to buy stock B and then sold stock B before the sale of A has settled. The broker is granting you good faith on the sale of A prior to settlement. Settlement on stocks has been T+3 since, well a long time. In a margin account, you do not run into the same problems but you do run the risk of being classified as a pattern day trader.

Front-running, I would guess.

OTH, no need to overthink this “market”, one can just buy whatever the loons on WallStreetBets are hyping.

Thank you all for the info, very helpful. I am still learning what is and isn’t possible and what the best way to do things is. I didn’t even know you could roll your 401k into an IRA. Interesting concept ….

Actually, you should do that with any 401k that’s no longer with your current employer.

More options in an IRA and more control. The only down side is you can’t just let it sit there and forget it. Active management means actual work even if it just means keeping eye on market and holding ETFs.

The other benefit is that you could potentially do a back door Roth under the right conditions.

One other thing, I was using tax paid money from sale of off grid home. May make a diff. Me and Implicit seem to be roughly similar, and he’s probably still fooling around with it. I tend to push things to the limit and then get bored or wiser and quit and move on.

I don’t think there is a smart money. There is big money, and in my opinion, lucky money.

Lucky money is a guy who day trades all the time, and either knows the up and down of the markets well enough to eek out good gains and at least not lose his shirt.

The big money are the ones with access to dark pools, Bloomberg terminals, supercomputers with direct access to the exchanges, MIT math PhDs who make millions on bonuses each year, and so forth. They are the “smart money,” but only because they had so much money to begin with in order to access resources that your day trader could NEVER hope to afford. Hence, the appellation, big money. That and the fact that these people trade for a living and their bonus depends on how much money they make trading. So very quickly, any loser will get weeded out.

The old fashioned way. Insider trading. You surely aren’t naive enough to think those few people busted mean anything. That’s just a little show for outsiders.

Keep in eye on biotech, it usually leads down based on risk, there was pretty good down move today. PNF target for XBI on weekly is 170, we reached 156….sideways and then down or a last gap up to 170 on M and A news…

investors now should just ask themselves is the additional 5% worth it, or is a potential 20% loss worth the additional 5%

EOM March CDX roll coming up next… CDX NA HY BB spreads bottomed recently in early dec have have risin since, B spreads flat for about as long and a higher low than from sept and feb.

Time for dealers to get those +30 times UST collateral rehypothication levels down to 6, or die trying…

Gotta love these quarterly bottlenecks, nice chance to front run broke banks/funds trying to paint their books…

It’s been crazy time for a long time. Valuations & margin debt hasn’t meant anything to highly leveraged investors for over 10 years. The markets are in a state of extreme euphoria from all of the money printing & there are no signs that Central Banks are ever going to let up. Why? Because they can’t. The world would plunge into an instant Depression the likes of which humanity has never experienced.

Nothing matters except the promise to keep Everything propped through stimulus. Not only the markets & big business, but everything in between including the drowning consumer.

It’s not a matter of If but When but I’ve been saying that for a long time and here we are in 2021.

Double D, 2001

Now 2021

20 year cycles help revert to the mean….

this year was going to be ugly no matter the potus has always been my thinking.

confidence is the key of the equity market…..confidence is suspect right now…..

confidence is the key of the equity market…..confidence is suspect right now….

All that confidence depends EXCLUSIVELY upon FED’s policies, as usual since March of ’09!

FED is the mkt. NOTHING else matters!

Brinker guy used to say same thing 25 years ago. For the “get richer doing nothing” crowd, the FED IS GOD.

Speaking of crazy times and valuations meaning nothing, anyone here followed the GameStop stock craziness?

It’s about winning an argument on the Internet between fanboys vs haters. There is no more agreed-on reality; rather, it’s about generating enough mob followers to bend reality to fit one’s beliefs.

“Short-seller Citron Research predicted the price would drop, but members of the Reddit board r/wallstreetbets, who had been generating interest in the stock, criticized Citron on the Reddit message board and continued praising the stock on social media.

[…]

Citron said Friday it would no longer comment on the GameStop stock because of “the angry mob who owns this stock.”

”

https://www.theverge.com/2021/1/22/22244900/game-stop-stock-halted-trading-volatility

Yeah I bought $25,000 of GameStop about 4 or 5 weeks ago, about a week before its earnings announcement. I figured that all people are doing these days is staying at home playing video games. Then it dropped on bad earnings and I sold at a loss of a couple of grand figuring it would never recover. Then it like doubled. Doh.

Wow. Considering your request for trading info above, you are rolling some pretty big dice. I used to make $50-$150 every few days or so, and was actually pretty pleased with myself. But the stuff is addictive. AND I was also, like you, playing in a market that was going UP.

Be careful, you are up against some real monsters. And “unknown unknowns”.

I guess you should have bought back in after it bottomed. Next time, sell just before it drops. Should be no problem for you as you seem to be very shrewd.

A few trillion more in stimulus ought to keep the plates spinning for another 12 months or so. That said there is always the possibility of a small correction along the way.

I have noticed that the more plates that are spinning the faster the entertainer has to run around the stage.

A nice big infrastructure revitalization package would provide some healthy demand side stimulus. I’m sure at least a few of the restaurant workers can be retrained to drive dump trucks. The Austrian supply side folks may not like it much, but this time it really is different.

makruger,

“A nice big infrastructure revitalization package would provide some healthy demand side stimulu”

I absolutely agree with you here but with a caveat!

Who do you entrust this sorely needed infrastructure revitalization process ?

If it is the likes of TESLA, GOOGLE, and other FAKE COMPANIES, then I say No!

The US is indeed in need of a revolution in terms of turning around its REAL ECONOMY and starting to push Manufacturing, Production, and linking its hubs together with a 21st century infrastructure.

Enough of the VALUE SUCKING paper,self serving corporations that suck so much needed CAPITAL out of the real economy into a parallel imaginary LA LA LAND!

Imagine if a small percentage of the money poured into the F$&(()G. FAANGS was to find its way to companies that actually make Things ACTUAL products, Technology that enhance the live and livelihood of millions of this country’s citizens! wouldn’t that be incredible!

Alas these live and capital sucking pieces of the proverbial keeps all that from happening.

And you know [ who is to blame].

Cheers

Jack says: The US is indeed in need of a revolution in terms of turning around its REAL ECONOMY and starting to push Manufacturing, Production, and linking its hubs together with a 21st century infrastructure.

Excellent comment. Exactly right. An economy certainly requires some specialization, but not at the expense of reality and it absolutely applies when ‘sugar turns to sh$!.

‘turning around its REAL ECONOMY and starting to push Manufacturing, Production, and linking its hubs together with a 21st century infrastructure’

Sounds great!

But be aware of Global competition including labor wage arbritrage. Education remains disconnected from the skills needed. Healthcare expense is a major drag on the GDP, compared to industries in other OECD Countries.

Robotics. Let’s make robotic factories and then we won’t need Chinese manufacturers anymore. The only problem is that they will still be more willing to trash their environment than we are so they will always have that edge.

Like seriously, we are not going to be competitive in manufacturing. We’re too lazy. Just accept it.

Green New Industry (deal) Declare war on fossil fuel and climate change. WW2 scale. No other rational move, none, nada, zilch.

Won’t be fun at all, but then neither was WW2.

Now. May be too late but worth a shot.

first chart makes me naively speculate it needs to reach 1T before implosion

“First rule in government spending: why build one when you can have two at twice the price?” Of course the gov’t is not the one directly spending. But the chart won’t really fit the mold of Wolf Street unless it looks gawdy and rightful deserves to be titled “WTF”

I’m going to go out on a limb and say that the party stops at 31,400 +/- 100 for the Dow. Then, it reverses and you hold on to dear life.

I think you’re very close Wolf, just hang in there. You pulled the trigger too soon but the end is nigh.

If you save your f****d , no escape none, real negative rates of 1-3% a year, is it any wonder people invest in the stock market and hope to profit, it is the only place left to even stand a chance, currently, and for those who say wait things economically will get back to normal, yes I agree they will, but when? and in the meantime my wealth has been eroded down to f**k all, so I may as well take a gamble since I will definitely lose if I don’t.

If you take a look at failing economies you will often see that their stock markets do very well Zimbabwe or Venezuela, its escape money, as I pointed out above where else do you get anything other than a certain loss?.

18 trillion of negative yielding bonds, are bond holders mad, or are Tesla or bitcoin buyers?.

Buy a farm and bug out off grid isn’t easy for a lot of people, try going back to an agrarian economy at boomer age with aches and pains.

grit your teeth take the medicine and Jump on the ponzi scheme because if you don’t you are f***d, just hope you can jump off at the right station. The exception is of course if you are so wealthy you can afford to allow your money to erode, in which case well done, good luck.

Yup. I escaped to the boonies 40 years ago. I knew the sky would fall eventually, just no idea exactly when. Along the way I learned the skills necessary to survive here, but now, just when I need them the most, I am too sick and old.

How’s that for irony?

It’s still cheap living. If my back hadn’t gone out I would be living in comfy 800 sq ft container home, with million dollar view in two directions, paying local kids to cut fire wood, keep me fire safe (weeds, trees, etc) had propane delivered, and still able to do light weight maint on batteries, propane gen, and solar panels. And have a big shop to tinker in.

Also could pay kids to grow dope, clean it and split profits to help with bills, sell stumpage, etc,

High speed internet, and satellite for TV also available up there, and only 1/2-3/4 hr to town for groceries, etc.

Life wouldn’t be too much different, further from sister and bro, but closer to friends.

But I’m ok here, too.

Paul Krugman in 2002:

“To fight this recession the Fed needs…soaring household spending to offset moribund business investment. [So] Alan Greenspan needs to create a housing bubble to replace the Nasdaq bubble.”

Janet Yellen at Financial Crisis Inquiry Commission in 2010:

“We did not see and did not appreciate what the risks were with securitization, the credit-ratings agencies, the shadow banking system, the [structured investment vehicles]—I didn’t see any of that coming until it happened.”

So we are at it again. Blowing bubbles that at some point in time will be popped by something and people in charge didn’t see it coming.

The “funny” thing is that plenty of people see it coming, but they are just not in charge. The whole subprime mess was well known by many commentators in the blog sphere. Based on that, I actually withdrew most of my money out of my bank accounts in 2007 (more than a year before the Lehman collapse) because I feared the banks would collapse. I’m glad I didn’t short the market though, because I was about 1.5 years early. It would have ruined me.

YuShan

Thanks for the memory!

I so much remember that type of comment that Krugman and others were making at that time. I don’t remember whether he was saying it approvingly or disapprovingly–I suspect disapprovingly.

I remember thinking “here we go again!” And it DID go on for six years. I’m sure a few struck it rich.

And now in 2021, “here we go yet again.

The eternal question again: How much longer before I get out?

Will irrationality THIS time exceed solvency?

Krugman was dropping by Calculated Risk back in years 05-10 to comment every once in a while. There were other posters that were more knowledgeable on what the current state of US finance was.

Krugman is a tool.

one guy named MP, since passed I believe, called the bottom perfectly and named it the Bernanke put…..if you just bought everything when he mentioned it….you are mega rich now….

YuShan,

Marvelously stated FACT: “The “funny” thing is that plenty of people see it coming, but they are just not in charge. ”

Yellen’s appointment SAYS A LOT about the MOB in charge now, doesn’t it?

It really amounts to stomping on an average man’s head once he’s already down.

Total debt and money control the price of assets. A deleveraging of margin debt would cause a vicious correction, but that’s all. Because within two months the federal reserve would make sure that total debt was above and beyond what it was before the correction. Anyone who doesn’t understand that now just doesn’t want to admit the obvious truth.

All the analogs to the past, like 2000, 2008, are from a time when private bank leverage was the determinate of money supply, and thus asset prices.

That’s over. Now the total value of debt is determined by the federal reserve.

If one wants to look and analyze todays market against historical analogs, one must compare the present day market to countries in the past where their central bank when full lunatard, like ours is now.

And after doing these comparisons, it will create a 180 degree shift in who should be pointed at a laughed at for saying “it’s different this time”.

Iow, for those who still don’t understand, our market is going to go up and keep on going up, albiet with corrections for change of margin debt, until those lunatic bastards at the federal reserve have destroyed the fiat currency. And people who think 2000 or 2008 is right around the corner are the real perveyors of “it’s different this time” catchphrase.

‘Now the total value of debt is determined by the federal reserve’

May be Public debt but NOT debt in the private sector other than keeping the rate at ZRP, buying MBSs and supporting Corp Credit mkts. But how long?

When defaults in the commercial RE ( malls, high office towers/apts/condos++) held by Pension funds, MFunds and Hedge funds++, Will Fed bail them ALL?

‘“If you think you live in a world where output doesn’t matter and you can just create paper, sooner or later you’re going to do the impossible, and that is bring back inflation,” Grantham said. “Interest rates are paper. Credit is paper. Real life is factories and workers and output, and we are not looking at increased output.”

Geremy Grantham (GMO)

“Everything is getting better and better look at the stock market” the 1920’s believer in free markets

There was no way that anyone that experienced this would believe in the markets again.

Once that generation had moved on, the memories faded and a whole new generation of suckers were ready to learn the hard way.

Only they haven’t learned, anything. This article says as much, it’s been carry on as usual, margin debt at record levels. Implying, much like the Tesla share price, we’re still in the FOMO stage of things. Still plenty of money around needing a scam to be lost on.

I believe sometimes much clarity can be brought to discussions such as these if one is able to use different words and phrases. So here is my original thought for all of you:

Markets have reached a permanent high plateau.

You’re welcome.

Have commentators been talking about “Priced to Perfection” yet? I always loved that phrase ‘cuz at the top there is only one remaining direction.

We’ll know we are over the top once the talking heads start blabbing about “Soft Landing”. I guess the Warren Buffet crowd will get a soft landing because they are landing on the rest of us.

Yeah, still recall enjoying the panic in the eyes and speech of the usually confident CNBC crowd (they were really LOSING IT, so to speak) as it just went dow, down, down….down….

Did watch Gartman call the bottom within 3 days, (no idea who he gets to talk to, though), and watched it live……666 and change.

Thought the preacher crowd would make a big deal of that, but most of the important talking head preachers were terrified about their own portfolios. Maybe in some small churches, though.

‘Markets have reached a permanent high plateau’

AS long as Fed?CBers determined to support them, as they done it continuously since March of ’09. Yellen is on record saying that Fed should be allowed to buy stocks, as BOJ and SNB have done!

‘Yellen says the Fed doesn’t need to buy equities now, but Congress should reconsider allowing it’

CNBC April 6, 2020

We are entering a long term bond bear market. The last bond bear ran from 1940 to 1980-81. Then the bull ran until 2021. 40 years each. Rates have been moving higher with stimulus. They have stopped because stimmy talk has subsided. Soon the fed will find themselves trapped. We are an old, sclerotic country and demographics do not favor us , as they did in the 40’s. Higher rates will crush all those companies that have loaded up on debt to buy back their stock. Zombies of course, will disappear. Housing is DOA. We will see a 60 to 70% drop in stock prices. Hopefully, the 2001 and 2008 S+P high of about 1500 will act as support. Welcome to the decade of “Fear and Loathing”.

First of all great post Wolf. There are a few things I’d like to

weigh in on . The fear of banks calling in your loans right now

is small. They have so much money and so little imagination

that they only resort to stock buybacks to increase stock prices.

Growing the bus. and by extension the economy is risky for them .

Also I’ve come to believe the only way for punters to make money

is to wait for a major pullback and then jump in and hold. No need

to borrow money with this strategy. Computers which trace every

thing you do are are always front running you in normal times.

I don’t think they have yet figured out how to control panic so

hence my strategy.

What do you folks think about buying Dividend Aristocrat stocks with modest payout ratios, even at current high prices, as an alternative to buying bonds and planning to hold them through any big market corrections. I’m retired with 50 % cash and 50% indexed funds currently but looking for something to do with some of the cash that pays more than 50 bps.

Pay attention to payout ratios.

Don’t be blinded by the .5% yield on cash. If the yield is .5%, -.5%, or 3%, it really doesn’t matter. The real benefit of cash is its option value. If and when the market crashes, any cash can be invested in depressed assets to generate expected gains of 100% to 10,000%.

From that perspective, cash may have the highest expected yield of any asset in your portfolio, by a wide margin.

Holding a good share of cash in your portfolio is just plain smart. You never know for sure what is going to happen, or when something will happen, when it comes to the stock market.

Take a look at the March 2020 drawdown and decide if you have the stomach for it. Bubble markets will eviscerate “Dividend Aristocrats.” I owned a couple and watched them dive to 40-60% of their 2020 highs.

Advice needed

Explore div paying ETFs outside USA especially EM mkts ( DVYE, DVYA, EMDV, VPL- in various sectors.That’s where the demographics and the future growth is.checkout FENY -XLE. or Cannabis ETFs like MJ, TOKE & POTX) Please do your due diligence

Nothing is RISK free!. I look for ‘RISK adjusted RETURN”

Be aware Div can be cut if there are less earnings.

I agree, but I am experiencing great difficulty precisely quantifying RISK.

Big tech has to finish before it all goes. Msft fb googl amzn tsla all have unfilled gaps at higher prices. I am waiting for that and reports in the next two weeks. Plus the holy SPX to 4000. February monthly charts look ominous. This slight drop is bear bait. Shorts must be destroyed and bulls lined up on the cliff. The flooding of SPAQS in the markets, the vertical moon shots of small caps and now the pink sheet explosion. I have seen this movie before. It’s close. Watch the VVIX. The futures on the VIX. When that’s lined up. Toonces will be driving

Or I could be wrong and it all goes sooner than later. Advice. If long bookem Dano

If you want to buy puts. Buy at least a 50 delta three to four months out in time(at the money)

Just my WAG. ( wild a$$ guess)

And once again wallstreet will destroy mainstreet or rather the fed once again

Destroys it all. Took 20’years and a new generation of muppets

I just saw what I consider to be one of the biggest crooks on Wall St. complaining about SPACs. Even he thinks it’s a scam.

Toonces for Fed chair. Perfect!

Recently read some old time Technicians who are actually calling the increase in margin debt an “indicator” that this market has plenty of room to run along with the stimulus forthcoming. The Fed will play the game as long as the market allows…no one knows when the bubble will burst but it will be interesting to watch how the “circuit breakers” work when FIRE is yelled in a crowded theater…

I wouldn’t be so sure more stimulus is coming in any noticeable amount. The fact is, no one wants treasury bills at these rates, at least not $2 trillion worth. So the only way to issue them is for the Fed to “purchase” them, i.e., further devalue the dollar. The Fed knows its power derives from a strong dollar. Even Yellen has said as much. So I suspect we’re going to see a smaller stimulus bill that is more targeted along with tax increases. Remember, tax increases are anti-inflationary, as they remove dollars from circulation.

It’s just the printing, same as it has been for forty years. Eventually those printed dollars make their way to corporate financial statements and the game keeps going. I don’t want to sound too much like my namesake, but there’s trillions in cheap money sloshing around.

What do US creditors get in return for the debasement? How do those phone calls go?

You could avoid all of this by spending your money instead of hoarding it like misers?

Wealth concentration is the reason for the Fed’s interest rate repression policies and the speculation we are seeing in the markets today.

There are lots of folks out there with net worth of $10M or more that have nothing better to do with money than shove it into passive assets at sky high valuations. They have zero inclination to spend any of that money because they really don’t need anything. They’d gladly give it to the kids or to charity, but not until they croak. Many of them are two-earner families in their 40’s, 50’s and 60’s that add $100k or more to their savings each year, as they watch their investments and RE sky-rocket, courtesy Federal Reserve policy.

Earn a million or more over a period of years, save a lot of it, buy stocks and RE, and watch it grow 300% to 1000%. It has been way too easy. At some point, you can’t even spend the interest/dividend return on the passive investments, and your wealth keeps growing even when you are retired.

Who are they? Walk through the hallways of any large corporation, and you’ll see plenty of them. Steady paychecks of $150k-$500k or more per year, when combined with some patience and frugality, will create many millions of wealth over a couple decades.

Pretty accurate statement Bobber. Add in the trust fund kids that don’t spend all of their “allowance.” If you have “enough” the pile grows and grows, year after year.

Like his random $10M number pick , too? Told ya it was plenty money to live on.

This is nothing that the securitzation of margin loans cannot solve. :>))

In 17th century Holland people started collecting rare tulip bulbs. The price quickly spiked 20X, then imploded to normal. In WWII people were so hungry, they ate their tulip bulbs.

I heard a rare coin dealer on TV state a rare gold coin was worth $100 million. I did not believe him. Someone else went to buy shares in a gold mine and went broke as they spent their investors’ cash digging through hard rock.

I read the book, “The Everything Bubble.” Cash is not always the safest position either. The author offered some good arguments.

Wells Fargo, Citi, and BOA have all announced big stock buybacks. Why are they doing this when they are only giving the depositor 8 basis points on their savings and 1 basis point on their checking account???? And all this bad paper valued at full value when its really worth 10 cents on a dollar. I’m getting so ticked off I’m ready to close out another one of my accounts with them. On a $25K deposits (min checking bal needed to avoid bank fees) , that’s a whopping $2.50 in interest for the entire year, all reported to the IRS so my net is about $1.50 after Fed and state taxes. I can’t even get my usual morning cup of coffee and begal with the interest from 1 whole year!!!!!

Screw these banks!!

Banks will not tell that they have a better deal available. In my case, when the bank started raising fees and minimums, I looked carefully at their website, and found a low fee + minimum basic checking and savings. A deeper look at the fine print revealed that I was just old enough to get the accounts with no fees or minimums. Do some digging, and you can probably save some money without having to go through the hassle of changing banks.

After having a checking account with fees with Chase for 10 years, I found out through a friend that since I am a veteran, I can have a FREE Premium Checking Account with Chase. No fees, no min balances, just free.

There are whole online communities devoted to churning bank accounts for the sign-up bonuses. Having done it, I will say that a minimum of record-keeping and enough spare cash lying around, you can bring APY up closer to 5% on FDIC insured money. A lot of hoops and gotchas, but can be done.

@SC – Banks are buying back their own stock with the same consideration of their customers that they use to borrow at the overnight rate and lend to their credit card holders at 12%.

I forgot to add JPM/Chase also joined they fray in announcing massive stock buybacks. And with the new adminstraton looking the other way, they are bringing back the London Whale trading desk to boost their bottom line.

The Bond market will start to tank first. Then the stock market. The High yield junk Bond market will lead them all. I’m keeping a close eye on the inflows and outflows of that sector.

Since the melt up is global I’d though I’d mention Japan. Only now, in the face of relative US valuations is the Nikkei spiking. Everyone touting government stimulus as the reason for the rise in US markets should observe the Japanese market since 1990. No inflation in Japan despite years of intervention. My guess is that they’ll push the Nikkei 225 far above 30000 to create a new generation of bag-holders. Since I believe Biden is a fiscal hawk, I suspect there will not be as much stimulus as most people believe.

Japan does have an aging issue, and lack of natural resources. I guess they’re also still a vassal to the US. Plus summer olympics might get canceled.

I think if you drew a Venn diagram, the overlap between Blue/Red is way more than advertised. Biden is going to print, that’s why Yellen was hired, she is well versed in hiding or passing the costs on to the ROW.

I think that’s an good point, though I’d amend it to:

Overlap in Venn diagram between red/blue policy (as opposed to rhetoric) is way more than advertised. – Your point.

Overlap in values, principles and priorities between voters who identify as red/blue is way more than recognized.

Overlap between the interests of red/blue voters and their chosen party are way less than imagined.

Money churn to make fees/interest! Gotta do it until it doesn’t work anymore.

I mentioned not too long ago that there was a somewhat weird change in perception around 2016 when trump became president. The stage had been set to perceive risk in a new way, as-if to embrace risk .

The seeds were sown in late in mid 1990 and supercharged before the GFC and this “new behavior” is the outcome of moral hazard, from The Fed. The Fed, with the Greenspan put and the bailouts of GFC and the anything goes pandemic crisis.

It was late March, when it seemed highly likely that the Fed would do anything to save the stock market. The trump thinking that the Dow was his barometer of success, also played a role and maybe even the ghost-like plunge protection team played a role to add fuel to the latest bubble.

So here we are, with every metric broken and nothing making sense as we continue to watch the WTF pandemic bubble expand further, understanding that there is no risk and that more moral hazard will play a role in our recovery. Was there a better option in not saving the economy or the stock market? Would we all be better off if stocks collapsed along with substantially more unemployment, lower yields, less growth, but more fiscal restraint and austerity?

I think in some ways the moral hazard is not unlike strategic bankruptcy, where globally, countries, including the USA will restructure and in some way restructure in a way that allows for future growth, even if that means to pretend and extend. Is that the basis for a real recovery, probably not, but a lot of pieces will be picked up and put together to create a path forward.

Yesterday, I posted a link that shows the Fed SOMA, CMBS account playing with $10 trillion, which is just one program underway, among many. Thus, what’s the actual cost of this pandemic in the USA and globally? I remember way back around March, that the global stock market had lost $20 Trillion — all these trillions bouncing around for 10 months point to substantial systemic global problems that will be challenging for many years, maybe decades.

Maybe, the concept of Capitalism will become something new, but as of today, the stock market remains a zoo — and this issue of leverage, connected to stupidity will become the mechanism to take moral hazard too far. It’s hard to see how this ends well, if we continue to support moral hazard activities.

Not only are we supporting moral hazard, but we’re disincentivizing any actual productive activity. Why would you save to buy rental real estate if the government can just seize it with no compensation under the flimsiest of pretexts? Why would you start a small business if you can in no way compete with the big boys, who can raise unlimited money at 2% rates on the capital markets? That’s assuming that you don’t get shut down without compensation.

We’re very badly screwed.

Martha Careful,

“Yesterday, I posted a link that shows the Fed SOMA, CMBS account playing with $10 trillion, which is just one program underway, among many.”

The SOMA is the Fed’s trading account. It has been published for years. Everything that is in the SOMA also ends up on the Fed’s weekly balance sheet, which I have been reporting on for years. Your $10 trillion figure is ridiculous BS. The total all assets combined is $7.4 trillion but it includes some assets (such as gold) that are not in the SOMA. There is NOTHING in the SOMA that is not also on the weekly balance sheet.

There are not “$10 trillion” in “CMBS” in the entire world. The Fed holds about $10 billion with a B of CMBS.

I deleted that comment for numerous reasons.

Here is my latest discussion of the Fed’s balance sheet, which includes all of the SOMA items.

https://wolfstreet.com/2020/12/11/update-on-the-feds-qe/

Wolf,

First off, I’m suffering from cabin fever, so if you find mistakes or don’t like things I post, I apologize. It doesn’t matter if this is posted, but just want to respond. I always enjoy your blog!

With all due respect, did you look at the Fed SOMA CMBS tab on that link? The only reason I posted that Total Holdings figure was because of what I read at New York Fed .

Maybe that’s where I went wrong, with Total Holdings, which may be different from Total Assets? Maybe I’m looking at billions and not trillions?? I also suggested the SOMA value isn’t on a FRED site.

On that site, at the bottom of the Domestic Security Holdings as of January 20, 2021, under the CMBS tab (which I clicked on to see data) the total holdings reported is:

Total 9,843,460,886.1

In addition, that has all the current CUSIP, Security Description and Current Face Value.

It looked to me like $10 trillion — no big deal, I’m just inside killing time, while it’s 5 below zero.

I realize what SOMA is: On March 27, 2020 the New York Fed began purchases of agency commercial mortgage-backed securities (agency CMBS) for the SOMA.

I’m probably missing something obvious, because the Fed indicates that in “normal” times, CMBS comprise about $800 billion of the $3.4 trillion CRE debt market.

Oh well,

Have a nice day. I need a walk.

Martha Careful,

Yes, we all get cabin fever these days. I go swimming in the San Francisco Bay to keep my sanity. By all means, take that walk (put on LOTS of clothes, obviously, and don’t stay out too long at -5).

“With all due respect, did you look at the Fed SOMA CMBS tab on that link?”

Yes, I look at the SOMA holdings ALL the time. The dollar amounts are in “Thousands.” So this is what it shows on the front page, converted to billions and trillions:

— Agency Commercial Mortgage-Backed Securities: $9.8 billion with a B

— Total SOMA Holdings: $6.8 Trillion with T

But, but, but… Now you sent me to the bottom-line total of CMBS holdings on the details page where the individual CMBS are listed. I have never gone down that far and looked at the total because I don’t need to look at it because the total is on the front page.

But now you sent me to look at it. Turns out, you’ve discovered a formula error on the Fed’s spreadsheet… someone forgot to divide the total by 1,000! They divided all other figures above it by 1,000, but not the total.

I now know because I pasted the entire data on that page into a spreadsheet and added it up.

What it says at the Fed’s page at the bottom: 9,843,460,886.10 (actual $)

What all CMBS added up together on that page amount to: 9,843,461.40 (in thousand $)

So I give you HUGE credit for having discovered a formula error on the CMBS line-item details page.

I will reach out to the NY Fed and tell them about it and see if we cannot get that fixed. Take a screenshot of the bottom of that page that shows that total, and save it. And then when they fix it, take another screenshot of that part of the page with the fixed amount (divided by 1,000), and then you can take credit for having found it ?

If it’s worthwhile, I might post an update on it after they fix it, giving you credit for pointing at the issue, and including what the people at the NY Fed said about it, if they say anything.

I am sure at some point the market will crash but I am so jaded and so disillusioned at this point I think that will probably happen way after my time or when I am too old and fragile to do anything about it. The inmate has taken over for sure and established a new normal. One only has to look at Telsa and add some extra F at the end of WTF to that one

Just a tough time for someone like me that’s holding cash and getting almost zero return….it’s just hard to convince yourself to jump in the market now, it would require throwing out any sense of logic and analytical thinking out the door.

I hear you. As someone more knowledgeable than me in these matters said, “bubbles can go to insane heights…and then double”. No one truly knows when this ends and just when you think it can’t get any crazier, it “doubles”. Who would’ve thought TSLA would hit $6000 (pre-stock-split price) but a few more weeks of this madness and it’ll have a real shot at that.

Looking back at previous mega-bubbles though, this kind of madness lasts months, not years. I think we could have something on our hands sooner than you might think.

The big unknown for me and for anyone looking to deploy their “dry powder” is what the magnitude of this will be. Is it going to be 20-40% before the Fed’s efforts (and you can count on them for this) reverse the trend of is it going to be 70-80% which means pulling the trigger to early can hurt you mightily despite having waited all this while.

Isn’t diversifying still the best bet?

Rather than trying to game it, just aim to preserve what you have.

I wonder if there’s any correlation to the Robin Hood app?

Margin debt relative to money stock is probably not excessive. Margin borrowing costs are low. Regardless of your political ideology when you cut regulations and you boost stimulus, money supply (and repress interest rates) you are going to get results. The characteristic of modern leverage is that it cannot be unwound. Globally interdependent trades can only be resolved through forex, in the aggregate, and various hedges insure that a coordinated drop in currency values would go unnoticed. Assuming a sychronized loss of value in global currencies the dollar is the beneficiary. If the dollar starts higher then yields don’t need to follow, but if yields start up the dollar is certain to go up as well. The first case is probably better for the market that is why I don’t like Yellen.

I admit, I don’t fully understand how the Rydex Ratio for sentiment is calculated, further, any ratio or metric in this WTF pandemic period is obviously not going to make a huge amount of sense, or confirm to some prior historical norm.

I still maintain, this economic dynamic is like a large tsunami, where the Earth, in the bottom of an ocean rips apart, sucking vast amounts of liquidity down a huge hole at light speed, then, almost instantaneously, the two parts of the wall slam together in an explosion of energy that fuels the epi center of a tsunami wave. The ocean waves before the explosion are linear while the tsunami waves that dissipate are non-linear, as they head to the nearest shoreline, where the massive wave smooths out and subsides.

Economically, we’re still in the initial shockwave and this event has to play out and smooth-out over time and the damage has to be evaluated.

It makes sense, that in this smoothing out process of linear dynamics, the bubble isn’t sustainable and it isn’t going to grow, but decline and recede back to a more predictable normality. People who see water rushing away quickly from a beachfront, before a tsunami, sometimes put 2+2 together and run to higher land for safety, as they assume that there is imminent risk — while a select greedy few, run out to collect stranded fish flopping around, from the sudden massive loss of water … the people heading for the hills have a far greater chance of survival ….

As for the Rydex Ratio, does it foretell anything?

Rydex Series Trust – Nova Fund

Total Assets (M USD) (On 01/21/2021)358.424

Rydex Series – Inverse S&P 500 Strategy Fund

Total Assets (M USD) (On 01/21/2021)62.897

A big picture perspective will serve you well during times like these. We have two periods, Before QE (BQE) and After QE (AQE). During BQE we had decent price discovery and well traveled paths through the financial jungle. AQE we have little price discovery and in our lifetimes we’ve never traveled down this path before. Margin debt has been historically high during most of AQE, and it is very high right now. All financial metrics have shifted during AQE, and there are a number of them that look even worse than the margin debt charts. However, we are unlikely to get more than a 10% pull back for the foreseeable future. When will we get another 35%-50% bear market? It is probably going to be a while, like 10 years. There’s a chance that a bad virus mutation will throw us into a double dip, but for now BUY THE DIP!

Even stocks like Apple seem way overvalued to me.

It has a market cap of $2.3T.

Apple has two basic business segments.

One business segment has revenues of $300B and free cash flow of $80B that have grown at a 5-10% rate the past five years. Based on 5-10% growth (which translates to 3-8% real growth after inflation), the valuation of this business is $1.6T when provided a generous 20x multiple.

The other business segment has zero revenue, no contracts in place, no employees, and no intangible property. The business involves selling hopes and dreams to investors. It’s valuation is $700B. Arguably, investing in this $700B business would be more speculative than investing in Tesla or Bitcoin.

Apple like Tesla & the whole index is a hyper bubble, in 2018 they made 59 billion, now they make 57 billion, then the stock price was $36 compared to now at $138. This market is the biggest bubble in history, it is driven by psychology, maybe insanity & greed would be a better description, a fool & his money are soon parted, reality Apple is worth around $500 in this climate, that’s being generous, a PE ratio of 41 right now is devoid of sanity, Apple will only make less money in the future, share buybacks of 100 billion in 2020 twice their earning to prop it up so insiders can sell. This is the theme all over the market yet Powell can’t see it, like all the other FED leaders before didn’t see it, they can see it but if they admit it it will all collapse, they just let it rip until it collapses under it’s on weight, the markets will burn, soon, every man, women & their dog in a position of power will say it was the Robinhoodidiots, the options, they are already flooding the airwaves with that narrative ready. Markets like this always collapse, the time it takes to do so always seems an age, reality is looking back all the losers will see is how long they had a chance to escape but buy the dip worked for so long when the collapse came it was another dip, they didn’t escape, when ya brainwashed to buy the dip when do you leave, at minus 10%, 20%, 30%, 40%, I’ll tell you when they will leave, at the very bottom of the capitulation move lower, markets could drop 70% & still not be cheap. PE ratios of 5 is cheap, not PE’s of 10 or above, They’ll get crushed.

This is a question to Wolf.

Can you confirm?

Do we have 2 handle operating @jack?!!

Please check this above comment is Not mine!!

No offense to the other Jack! :)

Jack,

Yes, two different “Jacks” here. You are not the other Jack.

Dear other Jack: please use some kind of alphanumeric combo behind “Jack” to distinguish yourself from Jack here — who has been commenting for many years — and from any other Jacks on this site. This can get very confusing. Thank you.

I have absolutely no faith in the market as of now/or for the last few years but I have pretty good money for the last few years although with no convictions.

My mantra is: Don’t fight the FED and keep playing and at the same time don’t take too much risks.

Market can remain irrational longer than we can imagine.

I totally agree.

You may be determined to swim against the current but you might have to do it for a long time and waste a lot of energy without any fun, while others let themselves go and experiene a fun ride and a thrilling descent. (Some end up hitting their head on a rock at the bottom but…)

This chart is just U.S. market leverage, right?

I feel better holding things outside the U.S. right now, as markets don’t appear to be quite as nutty.

As a simple accountant I do not understand the purpose of opts and puts and derivatives and synthetic derivatives and ETFs etc.

Surely they create a situation where the shares of the company have no relationship to the value of the company.

I cannot see how these can help a company regarding day to day trading.

One group of people that it might help are directors being able to cash in their options on basically false share values.

The director’s salaries and bonuses also seem to have no relationship to the value if them as employees of the company. Surly their total remuneration should be limited to say a multiple of 20 times the average wage of the employees based on, say a 40 hour week.

I don’t get it anymore and suspect the majority of people playing it also don’t.

I am reading so much about crypto currency being a store of value etc. “The digital gold”.

I ask myself, what can Bitcoin actually be used for, except speculation because it is so volatile so how could you use it as a currency for running a business with a 10% gross margin when it fluctuates by 20% in a day?

I can only see the purpose of Bitcoin being a way in desperation of moving currency out of a country with Capital Control, e.g. China or Venezuela and as said speculation that it will go up.

Cash-that ‘group of people’ sound a lot like they’re hitting the lottery because they already possess the winning numbers (…might also be termed ‘front-running’ or ‘insider trading’ among polite and civilized company…).

may we find a better day.

Morgan Stanley thinks its a New Economic Cycle. Chase said “Lever up” a month ago. 2021 recovery expected to be Strong. GDP up to 6% on major banks forecast. Perhaps, that explains it…

So I’ve just finished a re-reading of John Kennth Galbraiths’ ‘The Great Crash of 1929′.

They say history doesn’t repeat, but it often rhymes.

Right down to a spike in margin debt just prior……

Next up is a re-reading of Charles MacKays’ ‘Extraordinary Popular Delusions and the Madness of Crowds’.

We never learn; we have to keep re-learning.

Some things are different this time though.

Principally the lack of an external gold standard to enforce central bank discipline – or perhaps that should be rationality. Thus the US FED will print and print and print and print. Provided all other fiat-controlling central banks follow suit in the currency value destruction game at broadly the same rate, the Forex exchange rates will remain broadly in line with current values – with a few normalish exceptions (like GBP now that Brexit has actually happened; we should perhaps expect some weakening action by the BoE should Cable rise too much).