So the Fed Gets Ready to Walk Away from the Bond Market, and All Kinds of Stuff Happens.

By Wolf Richter for WOLF STREET.

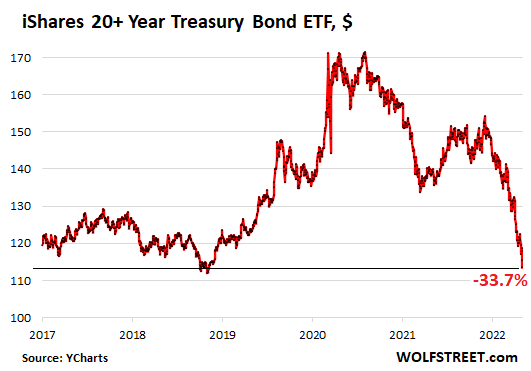

The price of the iShares 20+ Year Treasury Bond ETF [TLT], which tracks an index of Treasury securities with long maturities, dropped another 1.5% on Friday, after having dropped 2.7% on Thursday. It has plunged 21% year-to-date and 33.7% from the peak in August 2020. In return for this plunge in price, investors get a yield that has risen to 3.0%.

August 2020 marked the peak of the greatest bond-market bubble in US history. It was when the 10-year Treasury yield hit historic lows while our favorite hype mongers predicted that it would drop below zero and become negative. But this bond bubble is blowing up. And this is what the “bond massacre” looks like for investors who’d thought they’d invested in a conservative instrument, when in fact they’d bought a high-risk bet on the continuance of the bond bubble, a bet on long-term interest rates going negative. And WHOOSH went their money:

Holy-Moly Mortgage Rates.

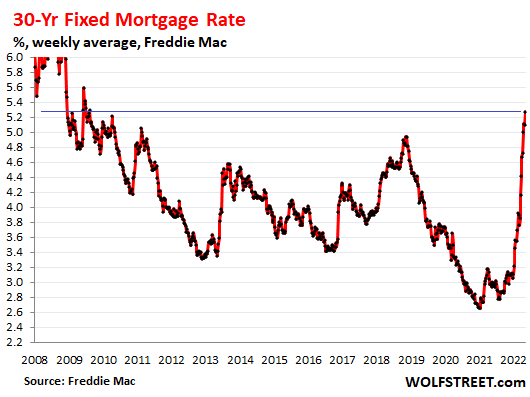

Mortgage rates are shooting higher relentlessly. The daily measure of the average 30-year fixed mortgage rate by Mortgage News Daily reached 5.64% on Friday, the highest in the data going back to 2009.

The weekly measure by Freddy Mac of the average weekly 30-year fixed mortgage rate, which lags behind a little, spiked to 5.27% the highest since June 2009.

Holy-Moly Mortgage Payments.

Home prices have spiked and mortgage rates have spiked on top of it by over two percentage points and more. How much difference does it make in terms of the monthly payment?

In 2021, a home bought at the national median price at the time of $326,300, with 10% down, and financed at the average 30-year-fixed mortgage rate at the time of 3.09%, came with a monthly payment of $1,251.

In 2022, a home bought at the median price of $375,300, with 10% down, and financed at 5.27% came with a monthly payment of $1,869.

In other words, the mortgage payment jumped by nearly 50%, and related expenses of property taxes and insurance also increased. This 50% jump in cost of homeownership at the current price is going to wipe out demand from big layers of potential buyers.

Most people, when they apply for a mortgage, get a rate that is guaranteed for a certain period of time, such as three months. Many current buyers still have rate locks that were obtained in prior months, and they’re not fully feeling the spike in mortgage rates. But people who get their mortgages today are feeling it.

The volume of purchase-mortgage applications has already dropped substantially as has the volume of home sales. And over the next few months, the new reality in the housing market will become more apparent.

Interest rate repression, including through QE, caused the biggest housing bubble ever. Interest rate increases, including through QT, are going to unwind it. It’s the Fed’s effort to get the housing bubble under control before it tears up the financial system again.

The Fed finally thinks about cracking down on inflation.

The Fed has ended QE, and this week it raised short-term policy rates a second time, this time by 50 basis points. It also confirmed what it had hinted at in the minutes from the prior meeting that it would reduce the assets on its balance sheet starting on June 1 by not replacing maturing securities.

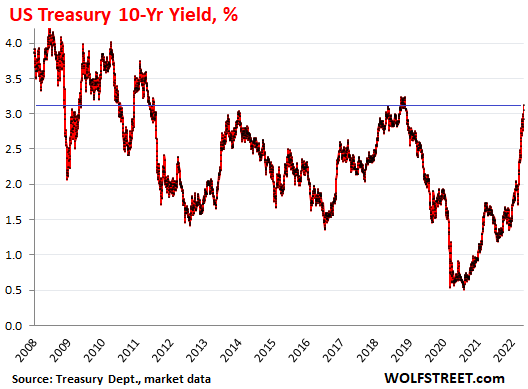

This Quantitative Tightening or QT has been discussed for months, and there were no surprises in the announcement of QT, and the bond market has been anticipating it and reacting to this anticipation. Yields have shot higher, which means that prices of bonds with long maturities have dropped – and not just a little, as demonstrated by the iShares 20+ Year Treasury Bond ETF.

The 10-year Treasury yield rose by 7 basis points on Friday to 3.12%, the second day in a row of closing above 3%. It’s now just a hair from the high in the prior tightening cycle when the yield peaked at 3.24% on November 8, 2018. When the 10-year yield moves beyond 3.24%, it will be the highest since 2011:

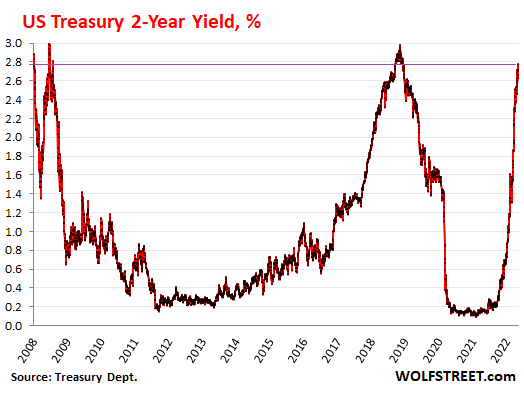

The two-year Treasury yield, which had spiked in the prior months in anticipation of many hikes in short-term policy rates, has over the past few trading days remained roughly in the same range, and on Friday closed at 2.72%, down a tad from the recent high last Tuesday of 2.78%, which had been the highest since January 2019.

For the two-year yield, it has been a huge move in just seven months. The magic number is 2.83%, beyond which you have to go back to 2007 to find higher yields.

Future bond buyers benefit from the higher yields.

Current holders of long-term bonds are having to sit through the bond massacre, after decades of having been coddled by the greatest bond bull market ever.

But future buyers get a much better deal, being able to buy bonds at lower prices with higher yields. These yields may still not be enough to compensate for inflation, but very little compensates for inflation as the Everything Bubble has begun to deflate, certainly not stocks and cryptos, which have already cratered, and real estate is shaping up to be next.

And those future buyers still face rising yields after they buy the bonds, meaning lower prices for their bonds after they bought them. But hey, that’s the bad breath of the Everything Bubble the next day.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hi Wolf,

How high do you think the US 10 Year could realistically get to ?

Marco

I think the 10 year could go to 6% because that will slam the brakes on all the stupid speculation and give them a shot at making inflation look like they are trying to slow it down.

Real rates will still be -10% but it is the perception that they are fighting inflation not the reality.

Still won’t be able to head off the MASSIVE deflationary crash coming.

Z

Deflation. I’m glad someone else sees this coming.

Reversion to the mean seems baked in when the inflation was driven by a transitory supply/demand shock event… unlike inflation as a result of economic growth.

And we know CBs can’t do soft landings.

Well, there was the 40% jump in the M2 money supply. The supply shortages aren’t going to go away at this point unless the economy slows.

Everything is transitory on this earth, including people.

so if INFLATION is the devaluation of fiat $dollar

then DEFLATION = ???

—

issue – is bond market decoupling from FED and moving on its own now??

if so wolf is right – good qx

Deflation is reduction of asset prices cars,homes,stocks,bonds if it gets bad enough than a depression

joedidlee

Inflation is alwaysoccurring contimuously even if it is 1% or 2%!

Purchasing power of US$ ( and other currencies) keeps going down, just a matter of fact how fast, corresponding to inflation rate. In purchasing power A US$ in 1913 is now worth 3 cents!

Once the demand destruction, accelerates (depending upon how fast and deep) there may be first dis-inflation and or STAGFLATION. If assets prices crash (deeply!?), watch deflation and in worse scenerio (?) D2

B/w

Despite a record high eurozone inflation rate of 7.5% in April, the ECB is sitting on -0.50% funds rates with a pledge from Christine Lagarde to move slowly. Wow! Europe is already heading, if not already in recession

We are in uncharted waters!

This is traders’ mkt not for investors. Cash may be trash and may lose 8% a year but Bonds and equities LOSE a lot more!

Yep to much debt = deflation. Unserviceable debt by definition is deflationary. The USA postponed deflation of the unserviceable debt via moratoriums on student loans and mortgages.

Marco,

Great question :-]

Its great to see wolf write about this. Most other websites are either not covering Inflation and Housing or are applying their own spin on it!

Totally Agree!

“Most other websites are either not covering Inflation and Housing or are applying their own spin on it!”

And trying to sell you some BS product.

Harvey, it seems like everyone to trying to sell everyone else something these days. It’s getting to be like a cruise ship stop at Cancun where the mobs are hawking everything from trinkets to their sister.

“And trying to sell you some BS product.”

Unlike the collectible Wolf Street beer mug which I’m waiting patiently for.

I believe this is the first leg down, followed by a second and third. Time to change your shorts !

I’ll answer with a question.

What time frame do you have in mind?

If you are looking out far enough, it will eventually blow past the 1981 high, by a large margin.

Specifically, concerning AF’s mention of the year 1981, the all-time high looks like it occurred in September of that year when the 10-year-yield peaked at… wait for it, it’s coming… 15.82%! Holy moly is right!! Heaven help those who bought a house with an adjustable rate mortgage these last few years!

Paul Volcker knew what had to be done, and he did it. Can today’s Fed replicate his actions today? I don’t think so, because back in those days, debt (personal/corporate) was much, much lower. Think today of those IDIOTIC GREEDY CEOs and board members of all the corporations that borrowed massive amounts of money to buy back shares in those share buyback programs. Yeah, they became wealthy, but what’s going to happen to their companies going forward. I think we know.

Don’t forget National debt being almost nothing! (Or at least well hidden…not sure).Reagan had only begun to deficit spend. Today’s FED could never do a Volcker, so he’s not exactly the FED hero he is often made out to be here…..usually in the Powell insults. Wolf does it well enough for me, thank you. I like guesses on how this will shake out, personal info, etc, but that’s just me…..everyone loves to just bitch now and then.

I don’t mind his (or anyone’s) excessive net wealth being insulted, though, have at it!

At some point, creditors will take control of interest rates or the USD will crash. It’s one or the other.

Contrary to practically everyone else, I’m placing my bets on the FRB throwing the markets, economy and public to support the USD and preserve the Empire. Trashing the USD would also trash the bond market. It makes a lot more sense to trash one only, the bond market.

Those with the most influence (which isn’t most of the 724 billionaires) would be nuts to trade geopolitical “hard power” for fake paper wealth.

The idea is completely nuts.

AF, the FED may throw the markets, economy and public to support the USD and preserve the Empire. My bet is that it will be in vain. The Empire will then fall apart as there then no longer will be an economy and public to support it.

Bonds should.

Beat inflation

Pay you for your risk.

At least 10% for Treasuries.

Junk high tech bonds should be at 25%

Meanwhile, it would be curious to see if we get to the 4.5% 10yr position in the next few months, say by September. Maybe a pause, retrenchment, then higher to where you suggest.

I wonder if enough pain occurs that ‘all bonds are junk’ fear begins to take hold.

Aye,

Rewards commensurate with risk. Fed put price discovery in solitary confinement for over a decade. Now about to be freed from its shackles. Watch the carnage unfold.

The bursting of the corporate bond bubble will wreak the most havoc. Look at SPX member balance sheets. Where do they park huge portions of their ‘cash’? In each other’s bonds. Balance sheets implode rapidly when the bubble pops.

As for the USD$, we’re just getting started on a massive secular bull market. Many, many years. An added kicker when Tether gets its margin call and all cryptos crumble. When that day arrives, the move higher in USD$ will be breathtaking.

Still don’t see how Japan survives. USDJPY headed to 150.

I think stuff is already starting to break. ZH just had a article that Used Car Prices Are Crashing Near Record Pace.

11:35 AM — Tyler Durden

Used Car Prices Are Crashing Near Record Pace

They also had another article about things starting to break in the long term treasury markets too.

May 5, 2022 7:03 PM — Tyler Durden

Bond Market Is Breaking: The Last Three Times 30Y Treasury Yields Jumped More, The Fed Intervened

I started to buy TLT when it priced in 3% yeilds, and will keep buying my other 4 tranches is prices keep falling.

IMO everyone is on the bearish side of the bond boat, which means it’s time to seriously look at long term treasuries.

I think a lot of the inflation figures are lagging indicators, things will break and we’ll go back to ZIRP.

Like your optimism. Things will break, and we will go to NIRP.

Zero Hedge has been publishing doom and gloom stuff for like 10 years, at some point in time they will be right :)

“at some point in time they will be right”

Same for Nouriel Roubini (Dr. Doom), Peter Schiff, etc. They are correct in saying that which fundamentally cannot continue indefinitely won’t, while being way off in their predictions, especially the timing of their predictions. I’m just surprised this farce has been able to be dragged on this long.

If, rather than managing a boiled frog descent to “fully cooked” we get a major depression, worse even than the GFC, there might be more public pressure for accountability… nah, strike that, they’ll be just as clueless and easily misled as last time.

NIRP means everyone will be poor all over again unless you can pick the top of the interest rate cycle and buy the longest term corporate bonds at that time. What if everyone is wrong and hyperinflation grips America starting in 2023? We know its what the Fed does not what they say.

Real Tony

Hyperinflation can not last long as it destroys the currency which not only destroys demand but destroys import / exports.

Hyperinflation is the end of the US as a major everything.. It destroyed Wiemar Germany, Zimbabwe, Argentina and Venezuela

“ I think stuff is already starting to break. ZH just had a article that Used Car Prices Are Crashing Near Record Pace.”

Dude, seriously…. Zero Hedge?

Jeez… oh, wait… seems I remember… oh, yeah, here it is… from a month ago…

https://wolfstreet.com/2022/04/08/despite-big-jump-in-tax-refunds-for-down-payments-used-car-retail-sales-and-auction-prices-drop-as-price-resistance-sets-in/

Canada conveniently put used car prices in the CPI right before they fell in price.

azani,

“ZH just had a article that Used Car Prices Are Crashing Near Record Pace.”

That was ZH headline clickbait BS. Used vehicle wholesale prices dipped 1% in April from March and were up 14% yoy. Not seasonally adjusted, the index was up 2.9% in April from March, and was up 16% yoy.

For ZH, a 1% dip seasonally adjusted is a collapse. But not here. Here, as I have covered it since last November, the ridiculous used vehicle prices are weakening from their ridiculous levels. There is no “collapse” though.

“According to a Bloomberg Interview, the ZeroHedge founders/authors were anonymous until 2016. The website is registered in Bulgaria under the name Georgi Georgiev, a business partner of Krassimir Ivandjiiski. According to Rationalwiki, the only writer conclusively identified is ‘Dan Ivandjiiski.'”

The providence of ZeroHedge is quite well documented on Wikipedia. Anyone who reads ZeroHedge without anything but the utmost skepticism needs to read the Wiki page about who is behind it.

Not to mention the comment section of ZH has become unreadable. Full of Russian and Chinese trolls and apologists.

“Anyone who reads ZeroHedge without anything but the utmost skepticism needs to read the Wiki page about who is behind it.”

Both ZH and Wikipedia are FOS. If you’re relying upon either for accurate info, then you are misinformed.

ZH is a Russian disinformation site masquerading as a Libertarian gathering place.

Try posting something that is anti-Putin and watch what happens.

See the Rand Corp analysis for details.

Wikipedia is not FOS. If you think it is, you don’t understand how it works.

Anything political in wikipedia is not to be trusted. Other subjects are sometimes more reliable.

Either short term rates go rapidly to 10% to counter inflation and show that the Fed respects the dollar or they don’t.

In the first cast 10y gets to 7%, in the second they go well beyond 10% until the Fed finally wakes up.

I hope you’re right but my luck has been shot since 1984. Still if I’m 100 percent liquid I should be able to pick the peak of the interest rate cycle. It might help if daily interest rates go up. Presently they’re paying next to nothing. In bible prophesy it says inflation will rage everywhere but I don’t know if we’re smack in the end times. It could be hundreds of years in the future.

The technique is called “laddering”. You buy a little at set increments, time or yield or both. Not sure you want the ETFs, they tend to follow the present, and the price is dependent on fear. Fear in the markets causes selling in the ETFs, while those actually holding the bonds at higher rates, enjoy the ride.

For the last 50 years I’ve been able to pick the top of the interest rate cycles almost to the day but in the past most times all my money was locked up The time its no different I’ve got a fortune that comes due January 4th 2024 so remember that date. Rates should plummet just before then. I’ll try to hedge before then unless I see interest rates actually going higher at the time.

You ain’t seen nothing yet.

Agree totally

“You ain’t seen nothin’ yet

B-b-b-baby, you just ain’t seen n-n-n-nothin’ yet

Here’s something that you’re never gonna forget

B-b-b-baby, you just ain’t seen n-n-n-nothin’ yet”

BTO – great song!

Fed is the market. There is no fundamentals anymore.

If Fed decides the rates should be 10%, that’s what it will be. If Fed decides rates should be 1% that’s what it’ll be.

All your a$$es are belong to the Fed.

Shut down that monster.

Here’s the raw truth. We began losing our Democracy with the Reagan administration in 1980. Ronnie told everyone that the government was a trouble maker and capitalists were our saviours. End of story, TINA. Now, 40 years and three full-on bailouts of our supposed saviours (fourth bailout now in the making) the nation is a dumpster fire and the Oligarchs are about to grab every libertarian windpipe within reach. With the most corrupt judiciary in our history. You think 5 outright liars on the Supreme Court is bad, consider that Trump appointed more than 200 justices into our federal judicial system! The judiciary is a swamp, folks. With a single party system now about to take hold (GOP version, i.e., those libertarians about to be strangled) i have no clue what the future holds. But I don’t think it’s going to be pleasant.

“”Finance, natural resources and industry are parts of an interconnected system much like astronomy-and to me, an aesthetic thing of beauty. But unlike astronomical cycles, the mathematics of compound interest leads economies inevitably into a debt crash, because the financial system expands faster than the underlying economy, overburdeneing it with debt so that crises grow increasingly severe. Economies are torn apart by breaks in the chain of payments.”

From ’Killing the Host’ a book by economics historian Michael Hudson.

A=P(1 + r/n)^nt

Yes, this leads economies inevitably into a debt crash. It creates overburdened, severe debt crises, expanding faster and faster until they become increasingly dangerous!

But an even more vile mathematics equation as the above compound interest is, to me anyway, “Addition.”

Why? Because when my bills add up, which they inevitably do, I have to pay them. Oh, the horror.

Yep.

Fed says easy money, Market rallies.

Fed says tight money, Market dumps.

There is no market.

It’s time to end the Fed.

Marco, from a charting perspective on TLT, we are close to a bounce, followed by a drop to roughly 100. This would be another 10% drop in TLT, though I don’t know how it would relate to the 10 year as TLT is made of both 10 year and 30 year bonds.

Once we strike the 100 region, we are likely looking at a year to multi-year rally that will take TLT back to 155 area (so a 50% drop).

Then we will again turn down and this time the drop will make what we’ve witnessed since 2020 feel tame, with TLT hitting the 70-80 area (which could mean rates of 10%+).

So from a sentiment charting perspective, the immediate calls for 10% rates are quite unlikely for a another few years. But they are coming….

Does that still work when the inflation is above 8.5%? It seems the methodology is “broken” unless you add the outsized inflation corrections to the technique.

3.72%

Whendo you think the best time to buy 30 year treasuries willbe

There was a comment awhile back that we wish we could have stockpiled 10 year and 30 year Treasuries back in the early 1980’s when they were paying 12%-18%. And held them for 10-30 years.

If they reach 8% again, I will start buying. That should carry me for the rest of my life.

Inflation must be driven down. Inflation was higher than 6% from 1973-1982 (peak at 13.5% in 1980) before it was beaten down to the 2%-5% range for the next 40 years.

I will be like my parents (they had a 6% mortgage and were earning 10+% in LT savings accounts.) and not pay off any remaining mortgage amount.

If government insured, safe 10 year treasuries are over 5%, when you have a 3% mortgage, why pay the mortgage off or down?

I’ll just have to hold onto my house during this wild ride and expect my house value will possibly drop 30%-50% until the next bubble starts inflating. Or, maybe housing prices will just flatten and 4 years of 8% inflation will painlessly remove 32% of real equity.

It’s probably already peaked out @ 3% since the US public and private debt levels probably cannot tolerate anything much higher. Might actually be a good time to buy long dated bond funds at this point since rates are probably downhill again from here.

makruger,

“…good time to buy long dated bond funds”

Are you trying to rob people with your advice???

This kind of stuff of rates going down is everywhere, and is bigly promoted on ZH, and it confirms to me that rates will be heading higher for a long time. ZH predicted assiduously in 2020 and 2021 that the 10-year would turned negative. Lot’s of people did. People don’t get it when the 40-year trend suddenly changes course, as all trends eventually do.

If I was to drive a car, drunk and recklessly at 80 miles an hour on the freeway, then I would be rightly arrested and sent away. The FED has done exactly the same reckless incompetence with monetary policy and peoples lives … I wonder what penalties will be taken for their failures or will it all be Putin’s fault ?!

Felony reckless driving plus massive felony counterfeiting= The Fed.

We need a national referendum to vote on criminal prosecution of the Fed members responsible for this. But I sure won’t hold my breath.

Even if there was a national referendum, 80 to 90 per cent of the people would vote in their favor. Very very few people know what the Fed is or understand how they are responsible for this mess. The average guy – he thinks Powell is looking for him. Americans are the most deluded people on earth!

The average guy doesn’t have the slightest idea who Powell is, what agency he leads, or what that agency does or is supposed to do.

Not going to be arrested in many areas of USA for driving erratically at 80 mph Marco:

More likely to be tailgated or even bumped aside if going that slow many places with many very different conditions.

Friends have been bumped on the circle around Atlanta, in spite of going 85,,, others, including my dear ones bumped on I-10 in the Permian Basin, some more than once…

And WE Wonder why the death toll on USA highways EVERY YEAR is near or more than the death toll from VN war???

Apologize for this comment not being ”directly” on article.

“Apologize for this comment not being ”directly” on article.”

It’s a good comment Vintage.

I hear you. I drive down my alley @ idle speed. I drive through my neighborhood and residential areas slowly & carefully.

My machines are very fast. But I don’t let them go very often and only when & where it is appropriate. Plus, only where I am not near another vehicle.

A couple smooth decreasing radius cloverleafs with good sight lines are fun, and I have my favorites, but unless you are on a race track, there’s no point to driving dangerously.

Keep an eye on the 6 and accelerate fast to get out of way is my style. No one messes with you that way.

Oh, they are gonna feel it.

When the house they just purchased drops in value by 50%

“Most people, when they apply for a mortgage, get a rate that is guaranteed for a certain period of time, such as three months. Many current buyers still have rate locks that were obtained in prior months, and they’re not fully feeling the spike in mortgage rates. But people who get their mortgages today are feeling it.”

Around here people are now getting variable rate mortgages starting at 5.65%. Since there still is shortage of affordable housing the low end first time buyers are still lining up for the slaughter. They have no other choice as the cost of renting is going up 20%. The higher end homes are sitting as they have become unaffordable.

Housing markets typically correct symmetrically to the rise just like a mirror image. This time, the rise has been too sharp. e.g. in Bay area, case shiller index went up 27% in 2 years. The mainstream media is still in denial that houses can correct at this speed.

They are still advertising that buying house is an inflation hedge as housing went up 20% over last year against a 9% inflation. Also many realtors are using FOMO to scare clients, into stretching themselves to buy unreasonably priced properties, with all their money, by telling them that they would otherwise miss out indefinitely.

Everyone has choices ,But because of fake money ,our kids have never seen hard times . There not prepared or understand the reprucussions or consequences of idiotic policies .GOOD LUCK

Wait a minute, AOC herself said that her generation has “never known prosperity.”

There is nothing in any way ‘fake’ about the US Dollar.

In Canada its 90 to 120 days but the people funding the mortgages though guaranteed interest certificates get about a two day guarantee on the interest rate sometimes zero days. The only real option in Canada is Manitoba credits unions for savers unless you’re broke. They give you a guaranteed zero days guaranteed interest rate.

I’m 20% TLT + 20% IAU (gold). Always figured that if T-bonds ever got whacked in an inflationary environment, then gold would boom as a store of value.

…at least I tried.

I guess we’ll see how wide the excesses of the “everything bubble” are. I always see liquidity as the ultimate calming influence for me. This works well when my fixed expenses have been gradually cut to the bone, and are relatively level. One’s balance sheet dictates “which economy” a person is living in.

As Wolf has noted, inflation’s hit to the dollar’s purchasing power does not (yet, anyway) equal these drawdowns in other assets. But nothing goes in a straight line ….

As Augustus Frost responded to a commenter above, it depends on your timeframe.

Over the last 4 years your gold hedge did it’s job, I think.

Where does one go to sell gold? Local pawn shop? Numismatic club?

I had that problem with a few little bars I bought in Abu Dhabi around 2014.

I’m not the type who waits for an apocalypse in order to trade the gold bars for armored Hummers fitted out with canons or something. And not having a secure residence, I didn’t like carrying costs of keeping them in a safe deposit box.

So a couple months ago I sold them to a relative who is set up enough that most likely he would not have any need to convert them. He is happy with the pretty shiny base relief art on them (PAMP Suisse).

JMBullion.com buys gold online. Choose the product that you want to sell from the products that JM sells, and if you’re looking at the page on a laptop it will also display the “buy it from you price”.

Lock in your sell price and mail it to them, they pay you after a non- destructive test to verify authenticity.

Too easy.

It’s all TMV now ……

Gold? No. The strength of the US dollar is destroying gold. Now slightly under 104 the DXY is headed for 120. Gold will be annihilated.

Yep. It may stay transitorily above its mean of $456 per ounce, however, for a short while.

lol! Patently absurd.

Gold is at all-time highs in JPY, and a number of other currencies. Not far off in Euros, and has held strong in the face of recent USD strength.

At $1878 and dropping like a rock, you must have a different definition of strength than I do. The dollar is kicking sand in gold’s face and mocking him for being a weakling. Only a true gold bug has any faith in their hero any longer. Gold is now down there with bitcoin!

Please – stop with the comedy. Gold is 10% off of its all-time high in USD, while Bitcoin is down ~50%, but in your view they are equivalent.

This is an honest question – why does the dollar going up cause gold to go down?

The stark dichotomy of the eastern and western US is in terms of the housing market. I was looking at various markers compared to my own. It’s shockingly close in price between buying a house on Staten island vs buying a house in Coeur d’Alene, Idaho.

Western cities and counties show no relent. Well not much of one anyways. Fascinating how Boston and NYC are down and already seeing price drops. Rocket homes market report shows how many homes sell over/under asking. West is blazing a trail with 80-90% over at times. Meanwhile a lot of eastern seaboard cities tread water in neutral territory.

Some southern cities like Atlanta are still going strong but boy, north east and the Midwest seem to be dipping.

Wonder if history is repeating itself. But even still, my skeptical mind wonders if we can collapse as far as we’ve run up. We went mighty far up the mountain, when we slip and fall at the top who knows if Sisyphus will have to start over at the bottom or if a tree will catch the ball on the way down.

If you can work from wherever you are, go West young man. The East can no longer chain their white collar workers to the corridor.

For years they have dreamed of moving somewhere they can breathe again. And not deal with the crush of humanity. And cost of survival.

I would do it if I was 50 years younger.

The work at home model gave America a taste of “working to live”.

As a “Puritan” society we have always taken the inverse position.

Most now have figured out that that is not healthy.

I do not think this paradigm shift will be brushed aside. Note the workers quitting over Return to Office.

Evolve with your workforce or die is being accepted by many companies. Thanks to Covid.

Things are only worth what someone is willing to pay.

As employees seek a life after work, property prices where they choose to relocate reflect that.

“go West young man”

Please don’t, at least not onto the eastern slopes of the Rocky Mountains.

> The stark dichotomy of the eastern and western US is in terms of the housing market.

When will markets in the west start pricing in lack of water?

California has been for decades the homeless capital of the world, but doesn’t seem to upset market participants one bit when it comes to pricing housing.

Quality of life-wise, it’s a disaster.

How would you know??? You’re in Tulsa, where I used to live for decades. And I just spent some time there again in November to see off an old friend. It’s cheap, that’s for sure. Downtown is full of homeless people, and super dreary. The rest is just dreary, no snow skiing, no ocean, no mountains, no business vibrancy. Not much of a restaurant scene except for chain restaurants. A few craft brew pubs though, but they close early (9 pm?). They pay people $10,000 to move there if they bring their job with them — a city having to pay people to move there! So if that’s “quality of life” for you, that’s awesome. But don’t judge the quality of life in California because you’re clueless.

I don’t know, I mean, I’ve always wanted to see a few twisters to liven things up. At least they’ve got that….

Depth Charge,

Yes, I saw a couple of them there. Spectacular. Used to live in a high rise with west views, which is how you see them.

The one that ransacked Wichita Falls in 1979 went by my dump just a few blocks away, and I saw it… it was a grayish-black wall with parts of houses in it. Killed over 60 people. I was working as a security guard at the time (while in college), and after the Tornado came through, I had to guard a bank building at night of which only the safe was still standing. That’s the force of nature. And I respect that a lot, and I respect people’s ability to deal with it afterwards. Same with earthquakes or firestorms in California. Or hurricanes along the Gulf Coast. People are tough.

“Yes, I saw a couple of them there. Spectacular.”

I bet. I’m a huge fan of mother nature. While it’s terribly sad when anybody loses their life, I’ve always wanted to witness a tornado in real life. If I could actually make a living as a storm chaser, I’d do it in a heartbeat. The risk does not bother me.

I can’t think of a better way to go, honestly. “He got sucked into the sky by a tornado” sure beats “he died on the couch watching tv.” (I don’t watch tv, just sayin’) We’re all going to die someday anyway, and I prefer it to happen while living an exciting life.

Not me. I live in New England and we occasionally get a coastal storm, remnants of a hurricane, or a bad ice storm, but we don’t get clobbered by hurricanes, tornadoes, earthquakes, or wildfires. I would have extreme anxiety worrying about having to evacuate or the house being demolished every year.

My town was incorporated nearly 400 years ago, and there is something reassuring about living in a place that has structures that are still standing after hundreds of years.

Besides, we have 4 seasons, the ocean and the mountains, plenty of water, the best summer weather in the country, and winters are getting milder. Another decade or 2, people will be reverse migrating back up here. Maybe.

Demographics, cultural cohesion, crime rates, high trust communities.

These are far more important quality of life metrics than whether you can get craft beer after 9pm or go skiing.

I hear from a lifelong resident of SD about how much it is going downhill. She said her family wants to leave. Years ago she used to brag about SD all the time.

The entire middle part of the country is going to empty out. We should give it back to the descendants of the original inhabitants and bring back the bison.

I expect the water issues to increase in the West over time and is an underappreciated long term risk there, especially with the increasing population. Maybe that’ll ease off some as the baby boom retirement wave passes.

Agriculture uses most of the water in the West (irrigation), not people living in cities. And that makes the water shortages in the West a national problem because much of the food produced in California and some other Western states gets sent to other states and countries.

Good point Wolf. The warming climate will exacerbate the agricultural supply issues too.

Gov figures for 2015 (the easy find on the net) was Power at 133 billion gallons a day, Irrigation at 118 bgd and Public Supply at 39 bgd. I assume most of the power is industrial but it serves the public too obviously.

That’s a lot of water!

https://www.usgs.gov/mission-areas/water-resources/science/total-water-use?

That billions must be a typo btw – the chart above says millions… Whew.

“Fascinating how Boston and NYC are down and already seeing price drops.”

Per the Case-Shiller indexes and regarding the last RE correction (bust for some metros,) Boston topped out in Sept. 2005, well in advance of the other metros and the national index. The national index topped out in July, 2006 and most metros topped out coincident with, or slightly later, than the national index. As explained by Wolf, the Case-Shiller data lag by 2-3 months.

– One part of the explaination is called “retirement”. A LOT OF people who retire in the Mid West & North East sell lock, stock and barrel and then move to southern parts of the (our) US, or then move to “cheaper” parts / warmer & sunnier parts of the US. Think e.g. Georgia, Florida, California, Nevada but also e.g. Idaho.

That’s part of the explanation of why prices in the South West & South East are so “strong”.

Willy2,

As a boomer retiree my anecdotal lived experience is 100% in agreement with your comment.

Most of my retiree friends have left the midwest – Chicagoland area – to live full time in warmer & sunnier climes.

A few have small condominiums in both locations to enjoy Summer heat up here and Winter ‘cold’ down there.

We are going to leave Texas and go back to New England. Property taxes and home insurance in Texas has skyrocketed so much that you are actually better off in Massachusetts. I did not believe it until I did the calculations myself. Texas is destroying itself as we watch.

Does Texas rely on property tax to fund what other states use their income tax to fund?

I have always thought the feds [all branches of government] will step in if things get too scary. Got to bailout those big banks one way or another.

It’s already happening but ever so slowly. As rates creep up, sellers fear the disappearance of buyers and settle for less. Here outside of Philadelphia area, over 100% offers are now 93-94% of asking and the sellers will take it. A few sellers around here specifically stated they didn’t want to get caught without a “buyer” as rates increase and price people out. 10 year T at 4% before end of year and 5% next spring. As Wolf has made clear the FED has telegraphed every move and though they are derelict in speed they will save the union and currency. Not a Michael Burry worshipper but this time he’s “right”, markets will sawtooth downwards as leverage decreases (margin, etc) and the corporate bond market disintegrates. Don’t get stuck on the tracks on this one. BTFD anyone? Not….

I hear you. But the Fed has taken a bite out of the forbidden fruit (QE) now multiple times. They will not be able to come clean. The next crisis, real or imagined, is just around the corner.

Just because houses aren’t selling at the inflated ask price doesn’t mean the market is going to bust right away, if at all. If the homeowners are free and clear, they will just wait longer to sell, and those who have income to cover the lower interest mortgages they locked up years earlier will just continue to hold and pay down those mortgages. The question is whether inventory will creep up or whether we wil be deluged by a glut of housing. My guess is we won’t actually see as much housing on the market as many of you think we will, as it was already tight before inflation began skyrocketing up.

I fear you’re spot on, as I want to buy in next few years. SF home price is _the_ market I’d like to see worthwhile analysis of. Hope Wolf keeps covering it.

So in 2022, all the Fed has done so far is to end QE and raise the Fed benchmark rate by 0.75%. We haven’t even started QT and the mortgage rates are up to 5.64%.

Wow!!

Yes, we’re in for a quite a ride.

The Great Margin Reset is going from A story to THE story of the market selloff. Not even Bitcoin is safe.

“Not even Bitcoin is safe.”

So, maybe people should shift to one of the other 13,424 electronic tulip bulb varieties that exist as of today?

And on bitcoin tracking equities, I wonder what the mechanism is. Whales enticing more suckers abandoning stocks into bitcoins? Whales selling bitcoins to buy the market dips? Maybe both because the latter also accomplishes the former.

MicroStrategy and a few of its friends manipulate the price of Bitcoin at the margin, just like the Fed manipulates the bond market.

BitCON is worthless nonsense of no value whatsoever and it has already plummeted 50% in price from its highs as it heads to its true intrinsic value of zero. Warren Buffet and Charlie Munger last week said they wouldn’t pay $25 for the entire amount of BitCON out there. I would suggest you follow their advice.

So…winning!!!!

I hear you loud and clear but we are not supposed to go there. What a dumb place in history we are.

They are going to back off by the end of the year. The Fed’s only mandate is the stock market. They signaled and proved that many times. It’s different this time.

Harvey Mushman

Once Mortgage rates get close to 7% the inflation of houses, townhomes, condos will be over. Then you will see houses sitting, as the shadow inventory comes on the market, and sellers refuse to lower their prices. Foreclosures will start accelerating. But, none of this has started yet. The movie will not be the same as 2006/2007, This time the foreclosed homes will be snapped up by investors and added to the rental inventory. There will be no banking/lender crisis like the last time. Blackrock and foreign investors are already salivating over the prospects which are backed in the cake.

We are actually back to long-term normal on bonds and mortgages, but the bonds haven’t yet caused any change in savings account interest. Remember the old 3-6-3 rule?

Stock market may find a way to blast higher anyway since the end of this aspect of the mania is not confirmed. If it does, it should be an even narrower advance and the last hurrah.

RIP, TINA. We loved you but it’s time to say goodbye. Yes, breaking up is hard to do.

So…what’s left?

Nothing, so far, even keeps up with inflation.

Sometimes I feel like this is Charlie brown with Lucy and the football.

We have to stay at ZIRP, and I think the markets are going to break before the fall.

At that point inflation will be out of the news cycle and it will be deflation againg/back to ZIRP.

“We have to stay at Zero Interest-Rate Policy?”

Is that sarcasm? I am not sure if it is or is not, Azani.

Not in the plan ,deflation time hold onto your ass ,things will get a lot worse . People are dumb ,

It’s a matter of minimizing losses, in this environment, I think. Anchoring around making good money is just not in the cards. Holding on is mostly about having moved in the right way awhile back, before this startling dinner check arrived. Lots of money will just be running around in circles. Some will be frozen, deer-in-the-headlights.

Inflation, like war, like financial panics, is something just — here. It is like the air we breathe, like a tidal force we are all caught up in. We are all in this situation, but some have a little better-configured floats than others.

Correct. When the mania is actually over, all major asset classes will be losers measured in buying power.

That’s why I sound like a broken record when stating, the majority of Americans are destined to become poorer or a lot poorer over the indefinite future.

Once the “can kicking” ends, there is no escape from falling living standards for most Americans. Same for much of the world.

I read a lot of bearish posts here, but the sentiments still seem to be mostly abstract. It’s, we’re going to enter a major bear market, the economy is going to be bad or awful, and the environment is going to suck. But somehow some way, living standards won’t differ noticeably from now.

That’s not going to happen. Most Americans are going to take a big if not drastic hit to their lifestyle.

That’s what happens when cheap credit and loose credit standards can’t paper over extended economic and social decay in a society that is actually mostly broke. Most Americans won’t have access to credit to live beyond their means. The type of credit we have now wasn’t common until the 90’s and it can disappear again because it’s another result of the mania. It was never “normal”.

It took decades for credit standards to fall to these basement levels, so it won’t happen “tomorrow” but it’s coming. It won’t be decades from now either.

Inflation eats, silently, everything, 24 hours a day

Saving, real returns on stocks, profit margins, effective wages and salaries and eventually it eats turnover of money.

It is not going to be stopped until the inflationary depression (yes the “D” word) sends it back into a deflationary Hell.

Well Done Central banks, you have killed us all

“ Well Done Central banks, you have killed us all”

Not yet… there are actually a lot of folks pretty well positioned to ride the wave…

I don’t think people realize how serious the Fed is taking this screwup of monumental proportions…

I think they have given the stock and bond trading markets a sporting chance to adjust to the reality that’s coming…

I also think that consideration for the markets will soon be over…

Especially, if you continue to get hot CPI numbers…

With the Fed looking at a16-20 % inflation in a 2year period, they will have respond aggressively, stock market be damned…

Eighty percent of bank loans are short term and for property purchases. As long as the ‘collateral’ seems real they will loan up to the point where they suck up 100% of the collateral’s value. Compound interest always suffocates economies. GDP growth simply cannot keep up with the cost of debt. They are called ‘creditors’ for a reason. Been around for more than 5,000 years.

Could say a highly inflationary period is an economic equalizer . . . for while those owning assets are having valuations squeezed, those owning nothing have nothing to lose.

All the Fed needs to do to promote equality is let markets crash 50% or more. Bottom 50% will be unaffected since they only own debt. Voila, mission accomplished JPow!

I’d disagree. Inflation really hurts the common man. Have you gone to a grocery store or filled up your truck lately? It is crazy out there. However, if you are worth $10B and your assets shrink 50%, you are still doing fine.

No. The poor have to buy food and they generally spend their entire income to survive. Inflation crushes the poor. Look at Venezuela for the extreme example.

Not great but many preferreds are selling way below par. ATT is safe.

TprC yields 6.36, call is 3/25.

Again, not great but not crazy either.

Preferreds are really just bond proxies.

I got out of AT&T Inc. 5.35% Global Notes (due 2066) when it was under 25. I took a small loss just before the mania pumped it to 27.62 at end of December 2020.

My chagrin has eased a little, watching it fall to it’s current 24.43 (about 12% drop from peak).

Excuse me when I grin if it drops to 23.5 like it did in March 2020.

Maybe it’s not all about ‘keeping up with inflation’. Maybe it’s just about keeping above ground!

been very clear for at least decades 2b:

Waterfront property, fine art, and fine jewelry.

Dad used to deal with ”old money” folks who bought and built on such property, and IIRC, they all also had the last two.

These days, as far as I can find, those folks are completely hidden,,, totally unlike the latest ”arrivestes” such as the latest group of international criminals, no matter their locations, GUV MINT situations, etc.

Racehorses sold at the yearling sales have more than hedged inflation. Prices were subdued due to Covid but like new and used cars prices explored upwards.

“RIP, TINA. We loved you but it’s time to say goodbye. Yes, breaking up is hard to do.”

Lots of folks have been piling into their 60-40 setups for a long time. Lots of pensions (and pensioners) must be nervously eyeing the numbers too. This is tens of millions of people. where else are they gonna go, investments-wise?

Many (I know) are having the deer in the headlights look, and reciting the mantra of buy and hold. When those folks bail out, locking in trillions in losses, there is the bottom. Spring of 2009, Spring of 2020. But this time supposedly the Fed is not there to backstop-and-prop it up. So it could go far.

Before the major bear market is over, there will be multiple March 2009 or March 2020 bottoms, all but the last one false.

Somebody has to own everything at all times, unless it goes bust.

To me it looks pretty likely we will revisit the pandemic lows in stocks and crypto. RE will go back to probably 2016 levels or worse. And that’s just a minimum – we had so much speculation that has to unwound.

Wait until the folks figure out the 40 part of that equation wasn’t really invested in bonds, but a fund that traded bonds….

If you hold a bond fund for the duration of its average holding, you will do fine. Just don’t sell at the bottom.

Plus there was the year 2000 when no one believed equities could ever go down. Remember Lucent Technologies ? Everyone should remember that bear markets can be cruel. Plus there is no shame in taking profits. Lord knows the gains never come easy. So folks should just all sell together – crowd sell and get it overwith. Then we can all buy again because the Fed has a mandate to help us. None of this jives with the theory of investing. But we don’t live in that world. Good comment. Thanks.

Also Level 3 classic pump and dump Scott and Buffett

When you add the price of homes in bubble terrritory with the price of financing these homes at these new mortgage rates, the cost to get in the door has just gone up 30% in just over a month. I wonder what the bull s$it CPI numbers will say when they come out next month. Anyone who believes these numbers well “I got a bridge over the East River in NYC I’ll sell ya”.

My next door neighbor pays 2 1/2 times to rent what I pay, all-in, to buy the same unit. I’m falling down thanking my lucky stars; she’s sweating every night. I wonder how much this is perceived inside the Beltway. The elections may be very interesting, with all the cross-currents. Fear of the gutter focuses the mind.

Dalio already said he believes 2024 elections are when civil unrest ,becomes the norm

“The elections may be very interesting”

And for absolutely no good reason because any fool who believes ANY politician’s promises probably also believes that the stripper likes him.

The only people you’ll be given the chance to vote for are the same type of people who got us here. And, BTW, where is The Fed on those ballots?

“The whole idea of government is this: If enough people get together and act in concert, they can take something and not pay for it.” – P.J. O’Rourke, Parliament of Whores: A Lone Humorist Attempts to Explain the Entire U.S. Government

Renters in Florida are demanding the state impose rent control in the special legislative session to start this month. I told you this was coming years ago.

The political cross currents are already huge and very much under the radar. People with money are spending it massively. The working class is living on the edge of disaster and they know it.

My prediction for the 10Y is it will approach double digits, pushing 30Y rate comfortably into double digits, before 2024 election.

Double digit 10 year and I will back up the truck and buy as much as I can.

Ahhw AA, you’re just copying Wolf,,, how some ever, WE, the family WE, are totally on board with that concept, but only for the I-bonds when the FFR hits at least 5%.

From what read, it appears that will be the bottom rate at least until and if we hit serious ”deflation.”

The current rate of 9.62% is good, far shore,,, but with the base rate SO much lower AND with the now clearly known massive manipulations by the FRB, et alia, that could go to ZERO much sooner than the 30 years of I-bonds.

I would appreciated any comments on the obviously wonderful I-bonds.

Thank you.

VVN, I am out of equities and loaded with cash waiting for the T bills to become buy-able. I am buying 13 week ones until the high rates appear in the longer ones. I have also loaded my allotment of I bonds for the year.

Fed successfully inflated stocks, bonds and housing to 99% percentile or to ATH values. Any body holding all three assets will probably not see their real net worth be back at that level for a few decades.

The Fed is behind the curve and will have to crash land the plane. Doubling the mortgage rates in housing in just a few months is a desperate admission they created a housing bubble.

” “I got a bridge over the East River in NYC I’ll sell ya”.”

Swampie,

Will you accept bitcoin?

I actually think that the FED will / could start to lower interest rates already next month or in July by e.g. 0.25%.

You’re dreaming. But enjoy it while you can.

My guess is 2 – 3 months of QT which would be July or August.

Once they get to the full run rate on QT they are going to have the equivalent effect of 1% plus combined tightening and who will be buying a house, a car or a vacation on credit when the wealth effect is gone and rates are 3% – 5% higher than today.

In hind sight we all should shorted Cathy Woods.

Not too late to short Tesla.

Actually I’ve been looking at AARK as a contrarian play. Maybe not just yey, but soon :-)

A lot of the “contrarian bets” during the dotcom bust went to zero when the companies shut down. If they have negative cash flows and cannot raise new money and cannot get another company to buy them out, they’re done.

Willy2

Hopium is eternal, conditioned by Fed turning around, whenever asset prices start coming down. This may NOT the case going forward! Wishful thinking always gives hope, right?

These mortgage rates are still extremely cheap, as cheap as AFTER the housing bubble ended. It just goes to show how ludicrous the FED has been to jump up an insane housing bubble for over a decade.

I don’t see how this ends without so many tears.

It will end in tears, but the question is who’s tears? My guess is that the fed will get the feds funds rate to 1.5% before all the wheels come off, “inflation” disappears overnight and the have to cut rates again.

The question is if it happens before or after the midterms..

Considering the actual quality of the mortgages being issued, rates are dirt cheap.

Concurrently, considering that the bond bear market has just started yet housing affordability (measured by payments to income) is within a whisker of the lowest ever, that should be a hint of what’s in store.

Granted that average individual will have a hard time buying.

But I wonder if corporate and large landlord buyers now form a larger part of the buyers pool than in the past, and what will it take to deter them?

“These mortgage rates are still extremely cheap”

But home prices are the highest on record.

Inflation will come down the same way as it went up as demand gets destroyed.

But if developers destroy supply at the same time, nothing changes.

Absolute demand has been cratering and continues to so since all stimulus was removed last summer. Main Street is in dire straits.

I agree with @Aazani “I think a lot of the inflation figures are lagging indicators, things will break and we’ll go back to ZIRP.”

Our government is a criminal syndicate engaged in global enterprise racketeering. A Mafia. Judgment time comes.

Have I explained to you the appearance of Bitcoin? It’s parentage is global criminal enterprises, from weapons to human trafficking to tax cheats. It’s the perfect financial currency for corruption, which is immensely profitable by the way. Hence its popularity amongst the criminal crowd, and also among libertarians who are true fantasists.

That comment is completely off base PP. People certainly have different views regarding the viability of bitcoin as a store of value, but this notion that it’s use case is criminal is tired BS. Its parentage is in the financial crisis and global recession, and an effort to create a form of money that is not subject to abuse by a central bank’s inability to give in to the temptation to print and thus deflate the value of the currency. Bitcoin is in fact a terrible vehicle for criminals, because the blockchain records every transaction. Fiat currency has always done just fine for criminals, and will continue to do so in the future.

Bitcoin is and was a gambling token from get-go, nothing more. So now it’s down 50% over the past 6 months. But no biggie. It’s just a gamble.

Warren Buffet said Bitcoin is heading for zero.

Good!

In Redmond WA, there continues to be high demand in Seattle in the $2M to $3M range. It’s amazing how fast prices rose these past two years. The median sold price went from $1.300M to $1.718M from April 2021 to April 2022 (just one year!).

It’s hard to understand why a median house should appreciate $418,000 in one year. A realtor in the know said the buyers are young with Chinese background. Why would this demand pop all of a sudden? Perhaps money is leaving the Chinese RE market and looking for quick RE investments in the US, given the growing RE problems in China.

Perhaps it’s a continued preference for RE investing, and high prices are feeding even higher prices. In any case, the rise in mortgage rates doesn’t appear to having an impact, at least given today’s low supply levels.

“ Perhaps money is leaving the Chinese RE market and looking for quick RE investments in the US, given the growing RE problems in China.”

I think you got it…

Desperation, to a degree…

Availability, I would think, is the name of the game on the oceanfront west coast versus price…

I don’t recall but didn’t Vancouver put the brakes on the Chinese…

Yes they did, to stop the prices from inflating

Easy way to take over a country,no weapons needed. Get elected it’s over

Bobber,

The run up in RE prices in the PNW started when Vancouver imposed restrictions on foreign buyers. They simply migrated down south along the Pacific Coast.

Petunia : Your so correct on that !

The run up in RE prices in the PNW started when Vancouver imposed restrictions on foreign buyers.

The PNW :

That’s exactly what the USA Need’s so badly to do Just Like New Zealand and Australia saving the Country for the actual Citizen’s

This is a Very Big deal and the Foreign Buyers driving prices Sky Hi.

Good Luck on any changes on that when big money is involved !

Greed takes the front seat and no Air Bag will stop Greed

Re Chinese real estate buyers, dollars we spent buying Chinese stuff are just coming back home pushing prices up.

I see that Boeing is leaving ChiTown for the Swamp after leaving Seattle years ago.

CEO David Calhoun go his Accounting Bachelors degree @ Virginia Tech & his customers are in the Pentagon, so it makes sense, eh?

All the money was pushed out of Vancouver, Canada on April 20th 2017 budget day when the Canadian government brought in 21 new rules to try to break the housing market in Canada to the downside. Consequently a lot of the Chinese money went from Vancouver down to Seattle.

Maybe AMZN and MSFT employees with stock incentives too.

So many big time fund managers like Paul Tudor Jones saying – “He can’t think of a worse financial environment for stocks or bonds right now” – that’s a huge statement.

Plus we inch towards WWIII with the Ukraine war spreading, and NATO’s big increases of supplying weapons, and even more sanctions tightening the noose around Putin’s throat, – this is a huge unknown that will rattle markets for years, with the oil, financial sanctions.

I believe “Crazy Ivan” will escalate and declare it’s a official war with Ukraine, and he views the US and NATO support a proxy war – and our Intel help sink his prized flagship “Moscow” battleship, and rumor has it his 770 million dollar yacht was seized in Italy, and family assets, and his many setbacks militarily, – that gives you have a enraged “caged animal” with a huge bruised ego with his finger on the nuclear button.

I haven’t even talked about the 2T of crypto Monopoly Money, throwing a “monkey wrench” into this chaos, something our Gov is just now is looking into regulating, – should have been squashed years ago.

The utter incompetence of the Fed, and how folks lost 33% on TLT?? – a real conservative fund for investors/savers is a absolute failure of immense proportions!

And yes this real estate bubble will come to a brutal end, maybe worse than 2008.

Tax reform breaks for the RE crowd have a lot to do with speculative use of debt. Toss in a lack of tax on wealth and you’ve got ‘it:’ An Oligarchy!

I enjoy reading the comments. There are rational people in the world and they read Wolfe Street. Collectively we point to causes but no one can predict the future. All we can do is watch the metrics. One that is murky would be the amount of money borrowed for stocks. We get the 2 week delayed number but the banks and the hedge funds and their ilk don’t have to report. Does anyone have any way to see the leverage, other than retail margin interest ? We need to see when that debt unwinds – somehow.

TK,

I think Wolf wrote an article on that very subject a few weeks back and explained what was visible and what wasn’t….

TK,

Correct, we don’t know what the overall leverage in the stock market is. We only know margin loans, and that’s only a fraction of the total. Some banks disclose in their 10-Q or 10-K reports the amount they have lent to their customers against their securities. This “Securities-Based Lending” is not tracked on a national basis, and no one knows the total. There are other forms stock-market leverage, like the one that blew up Archegos Capital and cost banks many billions of dollars. Not even the banks involved knew the total leverage of Archegos. So some funds are going to blow up, and then when people sort through the debris (see Archegos), they’ll discover the total leverage of whatever blew up.

The FED, with the blessing of CONgress, took over the economy 2008, with despicable results. The people who call this a “free market economy” are delusional. The FED has absolutely destroyed pricing in every corner of the free market. And CONgress has tinkered to exacerbate the problems. We need to return to a free market economy, where pricing is set by the market, not by the FED and .gov. QE should never be allowed again. END THE FED.

AGREE totally DC, especially the last part,,,

And because YOU agree with ME SO much, I have to think you are very intelligent, per many studies.

Please do not retort to ”nay-sayers” with invective, as such only lowers you to their level(s).

Thanks for taking the time and energy to add to the wonderful commentariat on Wolf’s Wonder…

If/as long bonds drop further, what industries or institutions are most likely to face an existential threat?

Perhaps:

Insurance companies?

Pension plans?

Hedge funds?

Broker/Dealers?

Others???

Nobody , and no values are impacted whatsoever as long as the holders of bonds simply hold them to maturity.

I have a 1922 German 50,000 Mark 10-year bond paying 4% interest beginning in 1923, 2% twice annually, with all the coupons unclipped. The last year, 1931 pays 5% as a bonus. Maturity was 1932; apparently someone just forgot about it. Should I redeem it?

Compounded at the 4% the bond would be worth 2,525,247.41 Dm, plus of course, the initial 50,000 Dm investment.

Purchasing power at the time of issue would have been about 800,000 USD in today’s money, so good investment.

One trillion old marks for one rentenmark. Then came the reichsmark. And then the DM after WWII. Don’t remember how the transition from rentenmark to reichsmark to Deutsche Mark worked out.

I keep wondering about pension plans and SS pegged to a soaring CPI. They have to pay.

I figure two options.

Print money like crazy or bugger the CPI to far less than real inflation.

Or both?

Up in Canada I shorted the third tier listed banks about two months ago. I haven’t shorted the private mortgage insurers but they would be next. If they break the Chinese stranglehold on housing in Canada the entire house of cards will implode. People more or less just tried to ride on the coattails of the Chinese and paid anything for a house since around 2016.

I have a little bit in TLT and I’m happy for it to go to zero.

I need to buy a home and every 10% off TLT means housing will fall by far, far more than I’m losing on TLT.

Mor importantly I’m happy my kids won’t have to grow up in the “rentier age”. Good riddance to that time!!

All just as expected and just as predicted. Things will start to settle down appropriately when the yield (interest rate) on 10 year US Treasuries gets into the 5% to 6% range.

If the Federal Reserve wishes to appear at least somewhat relevant it should increase the Federal Funds Rate to the 5% to 6% range in the next few weeks or months.

I’m not sure it matters what the fed does. Inflation is baked in due to the shutdown in China making so much of the products we use scarce along with the war in Ukraine and the refusal to get domestic energy production up to compensate. A lot of the parts shortage from china is killing business that use those parts to do higher level manufacturing and employers cant afford to keep workers idle. Lots of layoffs coming.

Fed can’t do squat about any of that. Its all on President potatoheads shoulders!

The Fed can and will reduce DEMAND, which will make those shortages disappear.

When that happens, when demand has been reduced, do you think that the fed will — or should — pause with either rate escalation and/or QT, Wolf?

No thanks.

Rollercoasters make me dizzy and I don’t like getting nosebleeds.

Besides, the risk/benefit thing makes it not worth it. I’d need about double. And they ain’t got it because they’re shysters. I’m better off tending my tomatoes.

Thanks for the charts, Wolf. I keep telling people on this site and others not to look at the the discount rate being 1% (even though it is ridiculously low). Stop QE and we have this situation. Raise discount another 1/2% and start QT and real fireworks will start.

Many people still seem to have their heads firmly buried in the sand and elsewhere. They keep denying reality and rely on anecdotal evidence. “I live in San Diego and home prices are hot here; my home went up 10% since January according to Zillow.” Well, car prices crashing (starting with used) is exactly what happened in 2008, followed by stocks and then housing and then credit freezing up.

The Fed cannot pull any more demand forward–this is an economic fact and the reality that we face after the greatest money printing orgy in history. If you think Powell can come to your rescue to protect your 410K and home prices:

I got some ocean front property in Arizona,

if you’ll buy that, I’ll throw the golden gate in free.

“Debt is self-liquidating when used to generate future income, from which interest is serviced and principal repaid. Used for any other purpose, it is non-self-liquidating and results in payment obligations with no countervailing source of income.

How does it end?

A debt-based monetary system has a lifespan-limiting Achilles heel: as debt is created through loan origination, an obligation above and beyond this sum is also created in the form of interest. As a result, there can never be enough money to repay principal and pay interest unless debt is continually expanded. Debt-based monetary systems do not work in reverse, nor can they stand still without a liquidity buffer in the form of savings or a current account surplus.

When debt grows faster than the economy, the burden of interest is bearable only so long as the rate of interest is falling. When the rate of interest reverses course, interest charges start rising faster than debt growth.”

Quite so. I’ve phrased it in terms more stark, but you get the idea.

“there can never be enough money to repay principal and pay interest unless debt is continually expanded.”

Which is why total debt – government, corporate, household – only goes up, doesn’t stabilize, and doesn’t get repaid. The alternative is to default, which blows down the whole house of cards. And since things which cannot go on forever will not go on forever, default is inevitable anyway and the system must eventually fail.

“When debt grows faster than the economy, the burden of interest is bearable only so long as the rate of interest is falling.”

And because debt grows faster than the economy, inflation is the inevitable result, which requires the rate of interest to rise. This is where we are now, watching the burden of interest as it becomes unbearable, so that default is again inevitable and the system must eventually fail.

GDP is a lame measure of national economic performance because it does not account for debt. It’s like corporate accounting reports that would list assets and cash flow and income – but not CGS or liabilities. That’s just nuts.

“The Fed cannot pull any more demand forward–this is an economic fact and the reality that we face after the greatest money printing orgy in history.”

So much as been stolen from the future to feed the past and the present that there really isn’t that much future left.

It’s why TPTB are grabbing like there’s no tomorrow – because they know that soon there will BE no tomorrow.

The effects are not limited to finance. You can see it in how planetary resources are being used up – and the resources that will be needed in the future simply won’t be there. Deforestation hits new records on a regular basis. Peak oil is behind us. Desertification continues to increase. Arable land decreases. Major ocean fisheries have disappeared. Half of coral reefs are gone. Shortages of raw materials crop up and then persist. Meanwhile externalities increase and degrade what’s left, externalities like carbon pollution which results in global heating, accelerating the process of degradation. It goes on for pages.

There has never been any proper accounting for environmental assets in national and global balance sheets. The assumption is that those assets are infinite, and they’re not. And they’re disappearing.

Resource wars are coming. We’ve already had hot wars over oil. Just wait until we also have them over food.

“How does it end?”

Data-driven projections made since at least 1972 show that civilization will collapse around 2040. The milestones are met every step of the way. The global population is projected to begin falling around 2030, and that can only happen with mass die-offs, and that’s only eight years away. A billion panicking people will be ugly.

Meanwhile, people speculate about whether The Fed will raise rates a quarter or half a point, and when they’ll be able to buy a new car, and where they’re going to send Johnny and Suzie to college, when they should be planting potatoes.

Don’t worry about me. I’ll be just fine. It’s the rest of you I worry about.

Love your ramblings, Una.

Are you possibly “imminentizing the eschaton.”

That didn’t work for the Millerites…

Nobody’s getting Raptured, John H. I’ve discussed this with the Adventists. They agree with everything I tell them, but it doesn’t change anything.

Jung believed that the human propensity to believe that which is not true would be the undoing of civilization, and yet, everybody has the right to be a perfect nutjob. It’s in the Constitution.

Religious cults are very popular. Political cults even more so. They’ll be taking over the management next year, and that, as they say, will be that.

The last time the religious right got their way with the country we had Prohibition. That didn’t work out so well. Nowadays they want to ban fornication and related activities, and that will be catastrophic.

“ The last time the religious right got their way with the country we had Prohibition. ”

Actually, Una, more recent that that…

The last time the religious right got their way, we got Reagan because they hated Carter so much…

That’s when all the hippies/boomers started going to church…

That hasn’t worked out so well either…

This is terrifying.

How so and why?

You forgot, “Soylent Green is people!”

Nope…

Only the corporation that makes the Soylent Green is people according to the Supreme Court…

LOL @ JeffD 🤣

When I was 17 – I protested during the “Occupy Wall Street” movement and the sign I held up said, “Greed is a weapon of mass destruction,”

With thousands of years of history as proof, mankind can’t seem to get it right.

Love your comment, unamused.

Look at farming ,there costs equipment,fuel,fertilizer. Are skyrocketing but we don’t hear much about it .when they fall over the cliff = we starve

My Libertarian friends tell me agriculture is only 5% of the US GDP, so if it is wiped out completely, the consequences will be trivial. The “Hidden Hand” of the market will provide.

LOL. LOL.

Can the hidden hand ,get you food at grocery store !

Good to see how closely Grantham’s latest commentary matches Wolf’s.

Legendary investor Jeremy Grantham has issued a warning about the US housing market as mortgage rates rise, saying a property crash would be much more dangerous for the economy than a drop in stocks.

“2000 showed you can just about skate through a stock market event,” Grantham said in an interview with Bloomberg columnist John Authers on Wednesday, published Friday. “But Japan and 2008 showed you can’t skate through a housing crisis.”

In the two years to February 2022, the S&P Case-Shiller US national home price index surged by more than one-third, aided by ultra-low interest rates on mortgages.

Grantham warned last year that there would eventually be a “day of reckoning” for housing markets around the world after huge price increases.

In Japan, property prices peaked in 1991 and crashed dramatically. They are still yet to recover, with the property market a key factor weighing on Japan’s economy over the last decade.

Grantham told Bloomberg on Wednesday that stocks are selling off sharply, as investors begin to realize that the world economy has changed dramatically and inflation is here to stay.

The S&P 500 tumbled 3.56% Thursday to take its losses to 13% this year.

“This was the biggest decline of the S&P in the first four months of trading since I was one year old, in 1939,” Grantham said. “The reality is that this is about as rapidly as any market comes down.”

I think Wolf said that the banks will be ok in a housing bust, since they’re not holding most mortgages, whereas they were in 2008.

If the government is holding those mortgages, then it seems to mean that the government will not be ok.

For sure, someone will not be ok.

So what will that mean for investing?

“For sure, someone will not be ok.”

In one word: The Taxpayer.

Government will not be okay = the current government will not be okay. I see a dramatic change in government. Biden et al seem to be offering nothing to the general populace which means someone else will fill the vacuum. Trump?

We can call Geithner back to “foam the runway” this next 2008.

Print oodles of dollars for the Blackstones and their ilk to “soak up the supply” and then calm the serfs with medications.

As a mortgage guy – We are seeing layoffs…the phones are really quiet – and I used to pull 30 credit reports a month in Feb…5 in March and 0 in April…Refi’s are down 80%…

My business feels like Kathy’s AaaaRRRRRKKKKK fund crashing…..and my 2 biggest lenders’ stocks ….Rocket (QUICKEN) and UWM wholesale (UWMC) are both down 70% from their IPO (2021)

Thank goodness I can short QQQ’s and SPY’s….else Dollar Tree cat food would be on the menu.

Remember – with Real Estate crashing goes appliances – new construction – lumber – all the title companies – real estate agents – appraisers and the supporting industries…and a lot of FB advertising …

Thank you Wolf for a reality check on the Real Estate Bubble 2.0 …I have mailed those charts and articles to a 100 clients

“… 30 credit reports a month in Feb…5 in March and 0 in April…”

I am waiting for the peak in CSI. Given the 3 month lag, this data may suggest we’ll see the top soon.

@Seattle Guy

Thanks for the info. I keep hearing conflicting stories about your neck of the woods. On the one hand, really really hot Seattle and East Side housing market making new highs (sounds fishy), and your story among others that prices drops are actually happening in the area and many buyers have disappeared.

But your point is well taken, and Powell knows it. With real estate so much will go down, so he cannot afford to let volume of sales crash in exchange for a few homes going up in price. Grantham makes the same point. As soon as layoffs start, look out below.

+1 to what the mortgage guy said. I am looking at a house right now that would have sold at 1.8m in February and struggled to sell for 1.2m last week. That is more than 30% drop in just 2 months. Now the reality is that the house is really worth 800k which is still selling for 1.2m. That is still way overpriced. But nowhere near the madness that was going on for last few months. Would be fun to see where prices land when fed is done.

John A.-

Bannister of Stifel is not so well known as Grantham but does convincing analysis. In a recent report, he opines that this year is probably safe from recession because gasoline prices, earnings slowdown in US, and China slowdown are “doing the Feds work for it,” leaving the Fed free to ease up on its fight against inflation. This resonates with me…